Registration No. 2-93177

File No. 811-04108

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

FORM N-1A

REGISTRATION STATEMENT UNDER THE SECURITIES ACT OF 1933 [X]

Pre-Effective Amendment No. [ ]

Post-Effective Amendment No. 73 [X]

and/or

REGISTRATION STATEMENT UNDER THE INVESTMENT COMPANY ACT OF 1940 [X]

Amendment No. 68

Oppenheimer Variable Account Funds

(Exact Name of Registrant as Specified in Charter)

6803 South Tucson Way, Centennial, Colorado 80112-3924

(Address of Principal Executive Offices) (Zip Code)

Registrant’s Telephone Number, including Area Code: (303) 768-3200

Arthur S. Gabinet, Esq.

OFI Global Asset Management, Inc.

225 Liberty Street

New York, New York 10281-1008

(Name and Address of Agent for Service)

It is proposed that this filing will become effective (check appropriate box):

[ ] Immediately upon filing pursuant to paragraph (b)

[X] on April 30, 2014 pursuant to paragraph (b)

[ ] 60 days after filing pursuant to paragraph (a)(1)

[ ] on _____________ pursuant to paragraph (a)(1)

[ ] 75 days after filing pursuant to paragraph (a)(2)

[ ] on _____________ pursuant to paragraph (a)(2) of Rule 485.

If appropriate, check the following box:

[ ] this post-effective amendment designates a new effective date for a previously filed post-effective amendment.

OPPENHEIMER

Capital Appreciation Fund/VA

A series of Oppenheimer Variable Account Funds

<R>

Prospectus dated April 30, 2014

|

Share Classes: |

|

Non-Service Shares |

|

Service Shares |

As with all mutual funds, the Securities and Exchange Commission has not approved or disapproved the Fund's securities nor has it determined that this prospectus is accurate or complete. It is a criminal offense to represent otherwise.

Oppenheimer Capital Appreciation Fund/VA is a mutual fund that seeks capital appreciation. It invests primarily in common stocks of "growth" companies.

Shares of the Fund are sold only as an underlying investment for variable life insurance policies, variable annuity contracts and other insurance company separate accounts. A prospectus for the insurance product you have selected accompanies this prospectus and explains how to select shares of the Fund as an investment under that insurance product, and which share class or classes you are eligible to purchase.

This prospectus contains important information about the Fund's objective, investment policies, strategies and risks. Please read this prospectus (and your insurance product prospectus) carefully before you invest and keep them for future reference about your account.

Oppenheimer Capital Appreciation Fund/VA

<R>

| Table of contents | |

|

|

|

|

3 |

|

|

3 |

|

|

3 |

|

|

3 |

|

|

4 |

|

|

5 |

|

|

5 |

|

|

5 |

|

|

5 |

|

|

Payments to Broker-Dealers and Other Financial Intermediaries |

5 |

|

|

|

|

6 |

|

|

8 |

|

|

|

|

|

10 |

|

|

13 |

|

|

13 |

To Summary Prospectus

Investment Objective . The Fund seeks capital appreciation.

Fees and Expenses of the Fund. This table describes the fees and expenses that you may pay if you buy and hold or redeem shares of the Fund. The accompanying prospectus of the participating insurance company provides information on initial or contingent deferred sales charges, exchange fees or redemption fees for that variable life insurance policy, variable annuity or other investment product. The fees and expenses of those products are not charged by the Fund and are not reflected in this table. Expenses would be higher if those fees were included.

|

Shareholder Fees (fees paid directly from your investment) |

|

|

|

|

Non-Service |

Service |

|

Maximum Sales Charge (Load) imposed on purchases (as % of offering price) |

None |

None |

|

Maximum Deferred Sales Charge (Load) (as % of the lower of original offering price or redemption proceeds) |

None |

None |

<R>

|

Annual Fund Operating Expenses (expenses that you pay each year as a percentage of the value of your investment) |

||

|

|

Non-Service |

Service |

|

Management Fees |

0.69% |

0.69% |

|

Distribution and/or Service (12b-1) Fees |

None |

0.25% |

|

Other Expenses |

0.12% |

0.12% |

|

Total Annual Fund Operating Expenses |

0.81% |

1.06% |

|

Fee Waiver and/or Expense Reimbursement* |

(0.01%) |

(0.01%) |

|

Total Annual Fund Operating Expenses After Fee Waiver and/or Expense Reimbursement |

0.80% |

1.05% |

*After discussions with the Fund's Board, the Manager has contractually agreed to waive fees and/or reimburse the Fund for certain expenses in order to limit "Total Annual Fund Operating Expenses After Fee Waiver and/or Expense Reimbursement" (excluding any applicable dividend expense, taxes, interest and fees from borrowing, any subsidiary expenses, Acquired Fund Fees and Expenses, brokerage commissions, extraordinary expenses and certain other Fund expenses) to annual rates of 0.80% for Non-Service Shares and 1.05% for Service Shares as calculated on the daily net assets of the Fund. This fee waiver and/or expense reimbursement may not be amended or withdrawn for one year from the date of this prospectus, unless approved by the Board.

Example. The following Example is intended to help you compare the cost of investing in the Fund with the cost of investing in other mutual funds. The Example assumes that you invest $10,000 in a class of shares of the Fund for the time periods indicated. The Example also assumes that your investment has a 5% return each year and that the Fund's operating expenses remain the same. Although your actual costs may be higher or lower, based on these assumptions your expenses would be as follows, whether or not you redeemed your shares:

<R>

| 1 Year | 3 Years | 5 Years | 10 Years | |||||||||

| Non-Service | $ | 82 | $ | 259 | $ | 450 | $ | 1,005 | ||||

| Service | $ | 108 | $ | 338 | $ | 587 | $ | 1,300 | ||||

</R> <R>

Portfolio Turnover. The Fund pays transaction costs, such as commissions, when it buys and sells securities (or "turns over" its portfolio). A higher portfolio turnover rate may indicate higher transaction costs. These costs, which are not reflected in the annual fund operating expenses or in the example, affect the Fund's performance. During the most recent fiscal year, the Fund's portfolio turnover rate was 77% of the average value of its portfolio.

</R>Principal Investment Strategies. The Fund mainly invests in common stocks of "growth companies." Growth companies are companies whose earnings and stock prices are expected to increase at a faster rate than the overall market. These may be newer companies or established companies of any capitalization range that the portfolio managers believe may appreciate in value over the long term. Currently, the Fund primarily focuses on established companies that are similar in size to companies in the S&P 500 Index or the Russell 1000 Growth Index. The Fund primarily invests in securities of U.S. issuers but may also invest in foreign securities. The portfolio managers look for growth companies with stock prices that they believe are reasonable in relation to overall stock market valuations. In seeking broad diversification of the Fund's portfolio among industries and market sectors, the portfolio managers focus on a number of factors that may vary in particular cases and over time. Currently, the portfolio managers look for:

- companies in business areas that have above-average growth potential,

- companies with growth rates that the portfolio managers believe are sustainable over time,

- stocks with reasonable valuations relative to their growth potential.

The Fund may sell the stocks of companies that the portfolio managers believe no longer meet the above criteria, but is not required to do so.

Principal Risks. The price of the Fund's shares can go up and down substantially. The value of the Fund's investments may change because of broad changes in the markets in which the Fund invests or because of poor investment selection, which could cause the Fund to underperform other funds with similar investment objectives. There is no assurance that the Fund will achieve its investment objective. When you redeem your shares, they may be worth more or less than what you paid for them. These risks mean that you can lose money by investing in the Fund.

Main Risks of Investing in Stock. The value of the Fund's portfolio may be affected by changes in the stock markets. Stock markets may experience significant short-term volatility and may fall sharply at times. Different stock markets may behave differently from each other and U.S. stock markets may move in the opposite direction from one or more foreign stock markets.

The prices of individual stocks generally do not all move in the same direction at the same time and a variety of factors can affect the price of a particular company's stock. These factors may include, but are not limited to: poor earnings reports, a loss of customers, litigation against the company, general unfavorable performance of the company's sector or industry, or changes in government regulations affecting the company or its industry.

<R>Industry and Sector Focus . At times the Fund may increase the relative emphasis of its investments in a particular industry or sector. The prices of stocks of issuers in a particular industry or sector may go up and down in response to changes in economic conditions, government regulations, availability of basic resources or supplies, or other events that affect that industry or sector more than others. To the extent that the Fund increases the relative emphasis of its investments in a particular industry or sector, its share values may fluctuate in response to events affecting that industry or sector. To some extent that risk may be limited by the Fund's policy of not concentrating its investments in any one industry.

</R>Main Risks of Growth Investing. If a growth company's earnings or stock price fails to increase as anticipated, or if its business plans do not produce the expected results, its securities may decline sharply. Growth companies may be newer or smaller companies that may experience greater stock price fluctuations and risks of loss than larger, more established companies. Newer growth companies tend to retain a large part of their earnings for research, development or investments in capital assets. Therefore, they may not pay any dividends for some time. Growth investing has gone in and out of favor during past market cycles and is likely to continue to do so. During periods when growth investing is out of favor or when markets are unstable, it may be more difficult to sell growth company securities at an acceptable price. Growth stocks may also be more volatile than other securities because of investor speculation.

<R>Who Is The Fund Designed For? The Fund's shares are available only as an investment option under certain variable annuity contracts, variable life insurance policies and investment plans offered through insurance company separate accounts of participating insurance companies, for investors seeking capital appreciation. Those investors should be willing to assume the risks of short-term share price fluctuations that are typical for a fund focusing on stocks. Because of its focus on long-term growth, the Fund may be more appropriate for investors with longer-term investment goals. The Fund is not designed for investors needing an assured level of current income. The Fund is not a complete investment program and may not be appropriate for all investors. You should carefully consider your own investment goals and risk tolerance before investing in the Fund.

</R>|

An investment in the Fund is not a deposit of any bank and is not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency. |

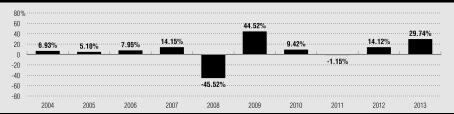

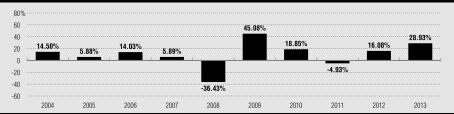

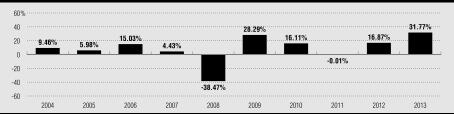

The Fund's Past Performance. The bar chart and table below provide some indication of the risks of investing in the Fund by showing changes in the Fund's Non-Service Shares performance from calendar year to calendar year and by showing how the Fund's average annual returns for the periods of time shown in the table compare with those of a broad measure of market performance. Charges imposed by the insurance accounts that invest in the Fund are not included and the returns would be lower if they were. The Fund's past investment performance is not necessarily an indication of how the Fund will perform in the future. More recent performance information is available by calling the toll-free number on the back of this prospectus and on the Fund's website at:

https://www.oppenheimerfunds.com/fund/CapitalAppreciationFundVA

|

|

During the period shown, the highest return before taxes for a calendar quarter was 19.10% (2nd Qtr 09) and the lowest return before taxes for a calendar quarter was -27.73% (4th Qtr 08).

The following table shows the average annual total returns before taxes for each class of the Fund's shares.

<R>

|

Average Annual Total Returns for the period ended December 31, 2013 |

||||||

|

|

1 Year |

5 Years |

10 Years |

|||

|

Non-Service Shares (inception 4/3/85) |

29.74% |

18.27% |

5.73% |

|||

|

Service Shares (inception 9/18/01) |

29.43% |

17.98% |

5.46% |

|||

|

S&P 500 Index |

32.39% |

17.94% |

7.41% |

|||

|

(reflects no deduction for fees, expenses or taxes) |

|

|

|

|||

|

Russell 1000 Growth Index |

33.48% |

20.39% |

7.83% |

|||

|

(reflects no deduction for fees, expenses or taxes) |

|

|

|

|||

Investment Adviser. OFI Global Asset Management, Inc. (the "Manager") is the Fund's investment adviser. OppenheimerFunds, Inc. (the "Sub-Adviser") is its sub-adviser.

<R>Portfolio Manager. Michael Kotlarz has been portfolio manager and Vice President of the Fund since June 2012.

</R>Purchase and Sale of Fund Shares. Shares of the Fund may be purchased only by separate investment accounts of participating insurance companies as an underlying investment for variable life insurance policies, variable annuity contracts or other investment products. Individual investors cannot buy shares of the Fund directly. You may only submit instructions for buying or selling shares of the Fund to your insurance company or its servicing agent, not directly to the Fund or its Transfer Agent. The accompanying prospectus of the participating insurance company provides information about how to select the Fund as an investment option.

Taxes. Because shares of the Fund may be purchased only through insurance company separate accounts for variable annuity contracts, variable life insurance policies or other investment products, any dividends and capital gains distributions will be taxable to the participating insurance company, if at all. However, those payments may affect the tax basis of certain types of distributions from those accounts. Special tax rules apply to life insurance companies, variable annuity contracts and variable life insurance contracts. For information on federal income taxation of a life insurance company with respect to its receipt of distributions from the Fund and federal income taxation of owners of variable annuity or variable life insurance contracts, see the accompanying prospectus for the applicable contract.

Payments to Broker-Dealers and Other Financial Intermediaries. The Fund, the Sub-Adviser, or their related companies may make payments to financial intermediaries, including to insurance companies that offer shares of the Fund as an investment option. These payments for the sale of Fund shares and related services may create a conflict of interest by influencing the intermediary and your salesperson to recommend the Fund over another investment. Ask your salesperson or visit your financial intermediary's website for more information.

The allocation of the Fund's portfolio among different types of investments will vary over time and the Fund's portfolio might not always include all of the different types of investments described below. The Statement of Additional Information contains additional information about the Fund's investment policies and risks.

The Fund's Principal Investment Strategies and Risks. The following strategies and types of investments are the ones that the Fund considers to be the most important in seeking to achieve its investment objective and the following risks are those the Fund expects its portfolio to be subject to as a whole.

Common Stock. Common stock represents an ownership interest in a company. It ranks below preferred stock and debt securities in claims for dividends and in claims for assets of the issuer in a liquidation or bankruptcy. Common stocks may be exchange-traded or over-the-counter securities. Over-the-counter securities may be less liquid than exchange-traded securities.

<R>Risks of Growth Investing. If a growth company's earnings or stock price fails to increase as anticipated, or if its business plans do not produce the expected results, its securities may decline sharply. Growth companies may be newer or smaller companies that may experience greater stock price fluctuations and risks of loss than larger, more established companies. Newer growth companies tend to retain a large part of their earnings for research, development or investments in capital assets. Therefore, they may not pay any dividends for some time. Growth investing has gone in and out of favor during past market cycles and is likely to continue to do so. During periods when growth investing is out of favor or when markets are unstable, it may be more difficult to sell growth company securities at an acceptable price. Growth stocks may also be more volatile than other securities because of investor speculation.

</R>Growth Investing. Growth companies are companies whose earnings and stock prices are expected to grow at a faster rate than the overall market. Growth companies can be new companies or established companies that may be entering a growth cycle in their business. Their anticipated growth may come from developing new products or services or from expanding into new or growing markets. Growth companies may be applying new technologies, new or improved distribution methods or new business models that could enable them to capture an important or dominant market position. They may have a special area of expertise or the ability to take advantage of changes in demographic or other factors in a more profitable way. Although newer growth companies may not pay any dividends for some time, their stocks may be valued because of their potential for price increases.

Other Investment Strategies and Risks. The Fund can also use the investment techniques and strategies described below. The Fund might not use all of these techniques or strategies or might only use them from time to time.

Diversification and Concentration. The Fund is a diversified fund. It attempts to reduce its exposure to the risks of individual securities by diversifying its investments across a broad number of different issuers. The Fund will not concentrate its investments in issuers in any one industry. At times, however, the Fund may emphasize investments in some industries or sectors more than others. The prices of securities of issuers in a particular industry or sector may go up and down in response to changes in economic conditions, government regulations, availability of basic resources or supplies, or other events that affect that industry or sector more than others. To the extent that the Fund increases the relative emphasis of its investments in a particular industry or sector, its share values may fluctuate in response to events affecting that industry or sector. The Securities and Exchange Commission has taken the position that investment of more than 25% of a fund's total assets in issuers in the same industry constitutes concentration in that industry. That limit does not apply to securities issued or guaranteed by the U.S. government or its agencies and instrumentalities or securities issued by investment companies; however, securities issued by any one foreign government are considered to be part of a single "industry."

Special Portfolio Diversification Requirements. To enable a variable annuity or variable life insurance contract based on an insurance company separate account to qualify for favorable tax treatment under the Internal Revenue Code, the underlying investments must follow special diversification requirements that limit the percentage of assets that can be invested in securities of particular issuers. The Fund's investment program is managed to meet those requirements, in addition to other diversification requirements under the Internal Revenue Code and the Investment Company Act of 1940 that apply to publicly-sold mutual funds.

Failure by the Fund to meet those special requirements could cause earnings on a contract owner's interest in an insurance company separate account to be taxable income. Those diversification requirements might also limit, to some degree, the Fund's investment decisions in a way that could reduce its performance.

Investing in Small- and Mid-Sized Companies. The Fund currently focuses on securities of issuers with large capitalizations. They may pay higher dividends than small-and mid-cap companies and their stock prices have tended to be less volatile than securities of smaller issuers. However, the Fund can buy stocks of issuers in all capitalization ranges. At times the Sub-Adviser might increase the relative emphasis of securities of issuers in a particular capitalization range if the Sub-Adviser believes they offer greater opportunities for total return.

Other Equity Securities. In addition to common stocks, the Fund can invest in other equity or "equity equivalents" securities such as preferred stocks or convertible securities. Preferred stocks generally pay a dividend and rank ahead of common stocks and behind debt securities in claims for dividends and for assets of the issuer in a liquidation or bankruptcy. The dividend rate of preferred stocks may cause their prices to behave more like those of debt securities. A convertible security is one that can be converted into or exchanged for common stock of an issuer within a particular period of time at a specified price, upon the occurrence of certain events or according to a price formula. Convertible securities offer the Fund the ability to participate in stock market movements while also seeking some current income. Convertible debt securities pay interest and convertible preferred stocks pay dividends until they mature or are converted, exchanged or redeemed. The Fund considers some convertible securities to be "equity equivalents" because they are convertible into common stock. The credit ratings of those convertible securities generally have less impact on the investment decision, although they are still subject to credit and interest rate risk.

<R>Risks of Foreign Investing. Foreign securities are subject to special risks. Foreign issuers are usually not subject to the same accounting and disclosure requirements that U.S. companies are subject to, which may make it difficult for the Fund to evaluate a foreign company's operations or financial condition. A change in the value of a foreign currency against the U.S. dollar will result in a change in the U.S. dollar value of securities denominated in that foreign currency and in the value of any income or distributions the Fund may receive on those securities. The value of foreign investments may be affected by exchange control regulations, foreign taxes, higher transaction and other costs, delays in settlement of transactions, changes in economic or monetary policy in the U.S. or abroad, expropriation or nationalization of a company's assets, or other political and economic factors. These risks may be greater for investments in developing or emerging market countries.

</R> <R>While foreign securities may offer special investment opportunities, they are also subject to special risks.

</R> <R>- Foreign Market Risk. If there are fewer investors in a particular foreign market, securities traded in that market may be less liquid and more volatile than U.S. securities. Foreign markets may also be subject to delays in the settlement of transactions and difficulties in pricing securities. If the Fund is delayed in settling a purchase or sale transaction, it may not receive any return on the invested assets or it may lose money if the value of the security declines. It may also be more expensive for the Fund to buy or sell securities in certain foreign markets than in the United States, which may increase the Fund's expense ratio. Foreign securities may trade on weekends or other days when the Fund does not price its shares. As a result, the value of the Fund's net assets may change on days when you will not be able to purchase or redeem the Fund's shares.

- Foreign Economy Risk. Foreign economies may be more vulnerable to political or economic changes than the U.S. economy. They may be more concentrated in particular industries or may rely on particular resources or trading partners to a greater extent. Certain foreign economies may be adversely affected by shortages of investment capital or by high rates of inflation. Changes in economic or monetary policy in the U.S. or abroad may also have a greater impact on the economies of certain foreign countries.

- Foreign Governmental and Regulatory Risks. Foreign companies may not be subject to the same accounting and disclosure requirements as U.S. companies. As a result there may be less accurate information available regarding a foreign company's operations and financial condition. Foreign companies may be subject to capital controls, nationalization, or confiscatory taxes. Some countries also have restrictions that limit foreign ownership and may impose penalties for increases in the value of the Fund's investment. The value of the Fund's foreign investments may be affected if it experiences difficulties in enforcing legal judgments in foreign courts.

-

Foreign Currency Risk. A change in the value of a foreign currency against the U.S. dollar will result in a change in the U.S. dollar value of securities denominated in that foreign currency. If the U.S. dollar rises in value against a foreign currency, a security denominated in that currency will be worth less in U.S. dollars and if the U.S. dollar decreases in value against a foreign currency, a security denominated in that currency will be worth more in U.S. dollars. The dollar value of foreign investments may also be affected by exchange controls.

The Fund can also invest in derivative instruments linked to foreign currencies. The change in value of a foreign currency against the U.S. dollar will result in a change in the U.S. dollar value of derivatives linked to that foreign currency.

- Foreign Custody Risk. There may be very limited regulatory oversight of certain foreign banks or securities depositories that hold foreign securities and foreign currency and the laws of certain countries may limit the ability to recover such assets if a foreign bank or depository or their agents goes bankrupt.

- Time Zone Arbitrage. If the Fund invests a significant amount of its assets in foreign securities, it may be exposed to "time-zone arbitrage" attempts by investors seeking to take advantage of differences in the values of foreign securities that might result from events that occur after the close of the foreign securities market on which a security is traded and before the close of the New York Stock Exchange that day, when the Fund's net asset value is calculated. If such time zone arbitrage were successful, it might dilute the interests of other shareholders. However, the Fund's use of "fair value pricing" under certain circumstances, to adjust the closing market prices of foreign securities to reflect what the Sub-Adviser and the Board believe to be their fair value, may help deter those activities.

Derivative Investments. The Fund can invest in "derivative" instruments. A derivative is an instrument whose value depends on (or is derived from) the value of an underlying security, asset, interest rate, index or currency. Derivatives may allow the Fund to increase or decrease its exposure to certain markets or risks.

The Fund may use derivatives to seek to increase its investment return or for hedging purposes. The Fund is not required to use derivatives in seeking its investment objective or for hedging and might not do so.

Options, futures, options on futures, and forward contracts are some of the derivatives that the Fund may use. The Fund may also use other types of derivatives that are consistent with its investment strategies or hedging purposes.

Hedging. Hedging transactions are intended to reduce the risks of securities in the Fund's portfolio. If the Fund uses a hedging instrument at the wrong time or judges market conditions incorrectly, however, the hedge might be unsuccessful or could reduce the Fund's return or create a loss.

<R>Risks of Derivative Investments. Derivatives may be volatile and may involve significant risks. The underlying security, obligor or other instrument on which a derivative is based, or the derivative itself, may not perform as expected. For some derivatives, it is possible to lose more than the amount invested in the derivative investment. In addition, some derivatives have the potential for unlimited loss, regardless of the size of the Fund's initial investment. Certain derivative investments held by the Fund may be illiquid, making it difficult to close out an unfavorable position. Derivative transactions may require the payment of premiums and may increase portfolio turnover. Derivatives are subject to credit risk, since the Fund may lose money on a derivative investment if the issuer or counterparty fails to pay the amount due. As a result of these risks, the Fund could realize little or no income or lose money from the investment, or the use of a derivative for hedging might be unsuccessful.

</R> <R>In addition, under financial reform legislation currently being implemented, certain over-the-counter derivatives, including certain interest rate swaps and certain credit default swaps, are (or soon will be) required to be executed on a regulated market and/or cleared through a clearinghouse, which may result in increased margin requirements and costs for the Fund. It is unclear how these regulatory changes will affect counterparty risk, and entering into a derivative transaction that is cleared may entail further risks and costs, including the counterparty risk of the clearinghouse and the futures commission merchant through which the Fund accesses the clearinghouse.

</R>Illiquid and Restricted Securities. Investments that do not have an active trading market, or that have legal or contractual limitations on their resale, are generally referred to as "illiquid" securities. Illiquid securities may be difficult to value or to sell promptly at an acceptable price or may require registration under applicable securities laws before they can be sold publicly. Securities that have limitations on their resale are referred to as "restricted securities." Certain restricted securities that are eligible for resale to qualified institutional purchasers may not be regarded as illiquid.

<R>The Fund will not invest more than 15% of its net assets in illiquid securities. The Fund's holdings of illiquid securities are monitored on an ongoing basis to determine whether to sell any of those securities to maintain adequate liquidity.

</R>Conflicts of Interest. The investment activities of the Manager, the Sub-Adviser and their affiliates in regard to other accounts they manage may present conflicts of interest that could disadvantage the Fund and its shareholders. The Manager, the Sub-Adviser or their affiliates may provide investment advisory services to other funds and accounts that have investment objectives or strategies that differ from, or are contrary to, those of the Fund. That may result in another fund or account holding investment positions that are adverse to the Fund's investment strategies or activities. Other funds or accounts advised by the Manager, the Sub-Adviser or their affiliates may have conflicting interests arising from investment objectives that are similar to those of the Fund. Those funds and accounts may engage in, and compete for, the same types of securities or other investments as the Fund or invest in securities of the same issuers that have different, and possibly conflicting, characteristics. The trading and other investment activities of those other funds or accounts may be carried out without regard to the investment activities of the Fund and, as a result, the value of securities held by the Fund or the Fund's investment strategies may be adversely affected. The Fund's investment performance will usually differ from the performance of other accounts advised by the Manager, the Sub-Adviser or their affiliates and the Fund may experience losses during periods in which other accounts they advise achieve gains. The Manager and the Sub-Adviser have adopted policies and procedures designed to address potential identified conflicts of interest, however, such policies and procedures may also limit the Fund's investment activities and affect its performance.

The Fund offers its shares to separate accounts of different insurance companies, as an investment for their variable annuity contracts, variable life insurance policies and other investment products. While the Fund does not foresee any disadvantages to contract owners from these arrangements, it is possible that the interests of owners of different contracts participating in the Fund through different separate accounts might conflict. For example, a conflict could arise because of differences in tax treatment.

Investments in Oppenheimer Institutional Money Market Fund. The Fund can invest its free cash balances in Class E shares of Oppenheimer Institutional Money Market Fund to provide liquidity or for defensive purposes. The Fund invests in Oppenheimer Institutional Money Market Fund, rather than purchasing individual short-term investments, to seek a higher yield than it could obtain on its own. Oppenheimer Institutional Money Market Fund is a registered open-end management investment company, regulated as a money market fund under the Investment Company Act of 1940, and is part of the Oppenheimer family of funds. It invests in a variety of short-term, high-quality, dollar-denominated money market instruments issued by the U.S. government, domestic and foreign corporations, other financial institutions, and other entities. Those investments may have a higher rate of return than the investments that would be available to the Fund directly. At the time of an investment, the Fund cannot always predict what the yield of the Oppenheimer Institutional Money Market Fund will be because of the wide variety of instruments that fund holds in its portfolio. The return on those investments may, in some cases, be lower than the return that would have been derived from other types of investments that would provide liquidity. As a shareholder, the Fund will be subject to its proportional share of the expenses of Oppenheimer Institutional Money Market Fund's Class E shares, including its advisory fee. However, the Manager will waive a portion of the Fund's advisory fee to the extent of the Fund's share of the advisory fee paid to the Manager by Oppenheimer Institutional Money Market Fund.

Temporary Defensive and Interim Investments. For temporary defensive purposes in times of adverse or unstable market, economic or political conditions, the Fund can invest up to 100% of its total assets in investments that may be inconsistent with the Fund's principal investment strategies. Generally, the Fund would invest in shares of Oppenheimer Institutional Money Market Fund or in the types of money market instruments in which Oppenheimer Institutional Money Market Fund invests or in other short-term U.S. government securities. The Fund might also hold these types of securities as interim investments pending the investment of proceeds from the sale of Fund shares or the sale of Fund portfolio securities or to meet anticipated redemptions of Fund shares. To the extent the Fund invests in these securities, it might not achieve its investment objective.

<R>Portfolio Turnover. A change in the securities held by the Fund is known as "portfolio turnover." The Fund may engage in active and frequent trading to try to achieve its investment objective and may have a portfolio turnover rate of over 100% annually. Increased portfolio turnover may result in higher brokerage fees or other transaction costs, which can reduce performance. The Financial Highlights table at the end of this prospectus shows the Fund's portfolio turnover rates during past fiscal years.

</R>Changes To The Fund's Investment Policies. The Fund's fundamental investment policies cannot be changed without the approval of a majority of the Fund's outstanding voting shares, however, the Fund's Board can change non-fundamental policies without a shareholder vote. Significant policy changes will be described in supplements to this prospectus. The Fund's investment objective is not a fundamental policy but will not be changed by the Board without advance notice to shareholders. Investment restrictions that are fundamental policies are listed in the Fund's Statement of Additional Information. An investment policy is not fundamental unless this prospectus or the Statement of Additional Information states that it is.

<R>Portfolio Holdings. The Fund's portfolio holdings are included in its semi-annual and annual reports that are distributed to its shareholders within 60 days after the close of the applicable reporting period. The Fund also discloses its portfolio holdings in its Schedule of Investments on Form N-Q, which are public filings that are required to be made with the Securities and Exchange Commission within 60 days after the end of the Fund's first and third fiscal quarters. Therefore, the Fund's portfolio holdings are made publicly available no later than 60 days after the end of each of its fiscal quarters. In addition, the Fund's portfolio holdings information, as of the end of each calendar month, may be posted and available on the Fund's website no sooner than 30 days after the end of each calendar month.

</R>A description of the Fund's policies and procedures with respect to the disclosure of its portfolio holdings is available in the Fund's Statement of Additional Information.

THE MANAGER AND THE SUB-ADVISER. OFI Global Asset Management, Inc., the Manager, is a wholly-owned subsidiary of OppenheimerFunds, Inc. The Manager oversees the Fund's investments and its business operations. OppenheimerFunds, Inc., the Sub-Adviser, chooses the Fund's investments and provides related advisory services. The Manager carries out its duties, subject to the policies established by the Fund's Board, under an investment advisory agreement with the Fund that states the Manager's responsibilities. The agreement sets the fees the Fund pays to the Manager and describes the expenses that the Fund is responsible to pay to conduct its business. The Sub-Adviser has a sub-advisory agreement with the Manager and is paid by the Manager.

<R>The Manager has been an investment adviser since 2012. The Sub-Adviser has been an investment adviser since 1960. The Manager and the Sub-Adviser are located at 225 Liberty Street, 11th Floor, New York, New York 10281-1008.

</R> <R>

Advisory Fees. Under the investment advisory agreement, the Fund pays the Manager an advisory fee at an annual rate that declines on additional assets as the Fund grows: 0.75% of the first $200 million of average annual net assets, 0.72% of the next $200 million, 0.69% of the next $200 million, 0.66% of the next $200 million, 0.60% of the next $200 million, and 0.58% of average annual net assets over $1 billion, calculated on the daily net assets of the Fund. Prior to November 1, 2013, under the investment advisory agreement, the Fund paid the Manager an advisory fee at an annual rate that declines on additional assets as the Fund grows: 0.75% of the first $200 million of average annual net assets, 0.72% of the next $200 million, 0.69% of the next $200 million, 0.66% of the next $200 million, and 0.60% of average annual net assets over $800 million, calculated on the daily net assets of the Fund. Under the sub-advisory agreement, the Manager pays the Sub-Adviser a percentage of the net investment advisory fee (after all applicable waivers) that it receives from the Fund as compensation for the provision of the investment advisory services. The Fund's advisory fee for the fiscal year ended December 31, 2013 was 0.69% of average annual net assets, before any applicable waivers.

After discussions with the Fund's Board, the Manager has contractually agreed to waive fees and/or reimburse the Fund for certain expenses in order to limit "Total Annual Fund Operating Expenses After Fee Waiver and/or Expense Reimbursement" (excluding (i) interest, taxes, dividends tied to short sales, brokerage commissions, and other expenditures which are capitalized in accordance with generally accepted accounting principles; (ii) expenses incurred directly or indirectly by the Fund as a result of investments in other investment companies, wholly-owned subsidiaries and pooled investment vehicles; (iii) certain other expenses attributable to, and incurred as a result of, a Fund's investments; and (iv) other extraordinary expenses (including litigation expenses) not incurred in the ordinary course of the Fund's business) to annual rates of 0.80% for Non-Service Shares and 1.05% for Service Shares as calculated on the daily net assets of the Fund. This fee waiver and/or expense reimbursement may not be amended or withdrawn for one year from the date of this prospectus, unless approved by the Board.

The Manager has also voluntarily agreed to waive fees and/or reimburse Fund expenses in an amount equal to the indirect management fees incurred through the Fund's investments in funds managed by the Manager or its affiliates. During the fiscal year ended December 31, 2013, those indirect expenses were less than 0.01% of average annual net assets and are therefore not shown in the Annual Fund Operating Expenses table earlier in this prospectus. The Fund's annual operating expenses may vary in future years.

A discussion regarding the basis for the Board of Trustees' approval of the Fund's investment advisory arrangements is available in the Fund's Annual Report to shareholders for the period ended December 31, 2013.

Porfolio Manager. The Fund's portfolio is managed by Michael Kotlarz, who is primarily responsible for the day-to-day management of the Fund's investments. Mr. Kotlarz has been a portfolio manager and Vice President of the Fund since June 2012.

</R> <R></R>

Mr. Kotlarz has been a Vice President and Senior Research Analyst of the Sub-Adviser since March 2008. Prior to joining the Sub-Adviser, he was a Managing Director of Equity Research at Ark Asset Management from March 2000 to March 2008. Mr. Kotlarz is a portfolio manager and officer of other portfolios in the OppenheimerFunds complex.

The Statement of Additional Information provides additional information about portfolio manager compensation, other accounts managed and ownership of Fund shares.

You may only submit instructions for buying or selling shares of the Fund to your insurance company or its servicing agent, not directly to the Fund or its Transfer Agent. Information about your investment in the Fund can only be obtained from your participating insurance company or its servicing agent. The Fund's Transfer Agent does not hold or have access to those records.

WHAT CLASSES OF SHARES DOES THE FUND OFFER? The Fund currently offers two different classes of shares. The different classes of shares represent investments in the same portfolio of securities, but the classes are subject to different expenses and will usually have different share prices. The Service Shares are subject to a distribution and service plan. The expenses of that plan are described below. The Non-Service Shares are not subject to a service and distribution plan.

THE PRICE OF FUND SHARES. Fund shares are sold to participating insurance companies, and are redeemed, at their net asset value per share. The net asset value that applies to a purchase order is the next one calculated after the insurance company (as the Fund's designated agent to receive purchase orders) receives the order from its contract owner, in proper form. Fund shares are redeemed at the next net asset value calculated after the insurance company (as the Fund's designated agent to receive purchase orders) receives the order from its contract owner, in proper form. The Fund's Transfer Agent generally must receive the purchase or redemption order from the insurance company by 9:30 a.m. Eastern Time on the next regular business day.

The Fund does not impose any sales charge on purchases of its shares. If there are any charges imposed under the variable annuity, variable life or other contract through which Fund shares are purchased, they are described in the accompanying prospectus of the participating insurance company. The participating insurance company's prospectus may also include information regarding the time you must submit your purchase and redemption orders.

The sale and redemption price for Fund shares will change from day to day because the value of the securities in its portfolio and its expenses fluctuate. The redemption price will normally differ for different classes of shares. The redemption price of your shares may be more or less than their original cost.

<R>Net Asset Value. The Fund calculates the net asset value of each class of shares as of the close of the New York Stock Exchange (NYSE), on each day the NYSE is open for trading (referred to in this prospectus as a "regular business day"). The NYSE normally closes at 4:00 p.m., Eastern Time, but may close earlier on some days.

</R>The Fund determines the net assets of each class of shares by subtracting the class-specific expenses and the amount of the Fund's liabilities attributable to the share class from the market value of the Fund's securities and other assets attributable to the share class. The Fund's "other assets" might include, for example, cash and interest or dividends from its portfolio securities that have been accrued but not yet collected. The Fund's securities are valued primarily on the basis of current market quotations.

<R>The net asset value per share for each share class is determined by dividing the net assets of the class by the number of outstanding shares of that class. The current net asset value per share of the Fund is available on our website at www.oppenheimerfunds.com.

</R>Fair Value Pricing. If market quotations are not readily available or (in the Sub-Adviser's judgment) do not accurately reflect the fair value of a security, or if after the close of the principal market on which a security held by the Fund is traded and before the time as of which the Fund's net asset value is calculated that day, an event occurs that the Sub-Adviser learns of and believes in the exercise of its judgment will cause a material change in the value of that security from the closing price of the security on the principal market on which it is traded, that security may be valued by another method that the Board believes would more accurately reflect the security's fair value.

In determining whether current market prices are readily available and reliable, the Sub-Adviser monitors the information it receives in the ordinary course of its investment management responsibilities. It seeks to identify significant events that it believes, in good faith, will affect the market prices of the securities held by the Fund. Those may include events affecting specific issuers (for example, a halt in trading of the securities of an issuer on an exchange during the trading day) or events affecting securities markets (for example, a foreign securities market closes early because of a natural disaster).

The Board has adopted valuation procedures for the Fund and has delegated the day-to-day responsibility for fair value determinations to the Sub-Adviser's "Valuation Committee." Those determinations may include consideration of recent transactions in comparable securities, information relating to the specific security, developments in the markets and their performance, and current valuations of foreign or U.S. indices. Fair value determinations by the Sub-Adviser are subject to review, approval and ratification by the Board at its next scheduled meeting after the fair valuations are determined.

The Fund's use of fair value pricing procedures involves subjective judgments and it is possible that the fair value determined for a security may be materially different from the value that could be realized upon the sale of that security. Accordingly, there can be no assurance that the Fund could obtain the fair value assigned to a security if it were to sell the security at approximately the same time at which the Fund determines its net asset value per share.

Pricing Foreign Securities. The Fund may use fair value pricing more frequently for securities primarily traded on foreign exchanges. Because many foreign markets close hours before the Fund values its foreign portfolio holdings, significant events, including broad market movements, may occur during that time that could potentially affect the values of foreign securities held by the Fund.

The Sub-Adviser believes that foreign securities values may be affected by volatility that occurs in U.S. markets after the close of foreign securities markets. The Sub-Adviser's fair valuation procedures therefore include a procedure whereby foreign securities prices may be "fair valued" to take those factors into account.

Because some foreign securities trade in markets and on exchanges that operate on weekends and U.S. holidays, the values of some of the Fund's foreign investments may change on days when investors cannot buy or redeem Fund shares.

How Can You Buy Fund Shares? Shares of the Fund may be purchased only by separate investment accounts of participating insurance companies as an underlying investment for variable life insurance policies, variable annuity contracts or other investment products. Individual investors cannot buy shares of the Fund directly. Please refer to the accompanying prospectus of the participating insurance company for information on how to select the Fund as an investment option. That prospectus will indicate which share class you may be eligible to purchase.

Suspension of Share Offering. The offering of Fund shares may be suspended during any period in which the determination of net asset value is suspended, and may be suspended by the Board at any time the Board believes it is in the Fund's best interest to do so.

How Can You Redeem Fund Shares? Only the participating insurance companies that hold Fund shares in their separate accounts can place orders to redeem shares. Contract holders and policy holders should not directly contact the Fund or its transfer agent to request a redemption of Fund shares. The Fund normally sends payment by Federal Funds wire to the insurance company's account on the next business day after the Fund receives the order (and no later than seven days after the Fund's receipt of the order). Under unusual circumstances determined by the Securities and Exchange Commission, payment may be delayed or suspended. Contract owners should refer to the withdrawal or surrender instructions in the accompanying prospectus of the participating insurance company.

Redemptions "In-Kind." Shares may be "redeemed in-kind" under certain circumstances (such as redemptions of substantial amounts of shares by shareholders that have consented to such in kind redemptions). That means that the redemption proceeds will be paid to the participating insurance companies in securities from the Fund's portfolio. If the Fund redeems shares in-kind, the insurance company accounts may bear transaction costs and will bear market risks until such securities are converted into cash.

Redemption or transfer requests will not be honored until the Transfer Agent receives all required documents in proper form. From time to time, the Transfer Agent, in its discretion, may waive certain of the requirements for redemptions stated in this prospectus.

Frequent Purchase and Redemption Limitations

</R> <R>The Board has adopted a policy to discourage and seek to limit or eliminate frequent purchases or redemptions of shares of the Fund by shareholders or authorized broker-dealer representatives of shareholders, in order to prevent the negative impacts, if any, that this activity may impose on other shareholders of the Fund. Negative impacts may include, without limitation, interference with portfolio management, increased taxes on portfolio securities, diminishment of Fund performance due to the need to sell portfolio securities at less favorable prices, increases in portfolio and administrative transaction costs resulting from large volumes of frequent purchase or redemption activity, and the possible dilution of Fund yields as a result of such activity. In addition, a Fund that invests in non-U.S. securities is subject to the risk that an investor may seek to take advantage of a delay between the change in value of that Fund's portfolio securities and the determination of the Fund's net asset value as a result of different closing times of U.S. and non-U.S. markets by buying or selling Fund shares at a price that does not reflect their true value. A similar risk exists for Funds that invest in securities of small capitalization companies, securities of issuers located in emerging markets or high yield securities (junk bonds) that are thinly traded and therefore may have actual values that differ from their market prices. This short-term arbitrage activity can reduce the return received by long-term shareholders. The Fund will seek to eliminate these opportunities by using fair value pricing, as described in "Fair Value Pricing" above.

</R> <R>There is no guarantee that this policy, described below, will be sufficient to identify and prevent all frequent purchases or redemptions that may have negative impacts to a Fund. In addition, the implementation of the Funds' policy involves judgments that are inherently subjective and involve some selectivity in their application. The Fund, however, seeks to make judgments that are consistent with the interests of the Fund's shareholders. No matter how the Fund defines frequent purchases or redemptions, other purchases and sales of Fund shares may have adverse effects on the management of a Fund's portfolio and its performance. Additionally, due to the complexity and subjectivity involved in identifying certain frequent trading and the volume of Fund shareholder transactions, there can be no guarantee that the Fund will be able to identify violations of the policy or to reduce or eliminate all detrimental effects of frequent purchases or redemptions.

</R> <R>

The Fund may from time to time use other methods that it believes are appropriate to deter market timing or other trading activity that may be detrimental to a fund or long-term shareholders.

The Fund does not offer an exchange privilege.

Right to Refuse Any Purchase Orders. The Fund may refuse, or cancel as permitted by law, any purchase order in its discretion for any reason at any time, and is not obligated to provide notice before rejecting or canceling an order.

</R> <R>Right to Terminate or Suspend Account Privileges. The Fund may, in its discretion, limit or terminate trading activity by any person, group or account that it believes would be disruptive, even if the activity has not exceeded the policy described in this prospectus. As part of the Fund's policy to detect and deter frequent purchases and redemptions, the Fund may review and consider the history of frequent trading activity in all accounts in the Oppenheimer funds known to be under common ownership or control. The Fund may send a written warning to a shareholder that it believes may be engaging in disruptive or excessive trading activity; however, the Fund reserves the right to suspend or terminate the ability to purchase shares, with or without warning, for any account that the Fund determines, in the exercise of its discretion, has engaged in such trading activity.

</R> <R></R> <R>Monitoring the Policy. The Fund does not have the ability to directly monitor trading activity in the accounts of policy or contract owners ("contract owner accounts") within the participating insurance companies' accounts. Participating insurance companies will generally enter into written agreements which require the participating insurance company to provide underlying shareholder or account data at the Fund's reasonable request. The Fund's ability to monitor and deter excessive short-term trading in insurance company accounts ultimately depends on the capability and diligence of each participating insurance company, under its agreement with the Fund, in monitoring and controlling the trading activity of the policy or contract owners in the insurance company's accounts. Overall purchase and redemption activity in contract owner accounts will be monitored to identify patterns that may suggest frequent trading by the underlying owners. Participating insurance companies will be permitted to apply the Fund's policy or their own frequent trading policy if the latter is more restrictive. In cases where a participating insurance company's more restrictive policy is applied, the Fund will rely on the participating insurance company to monitor frequent trading activity in accordance with its policy. The Fund may request individual account or transaction information, and based on the information and data it receives, will apply its policy to review transactions that may constitute frequent purchase or exchange activity. The Fund may prohibit, in its sole discretion, purchases of Fund shares by a participating insurance company or by some or all of its clients.

</R> <R>You should refer to the prospectus for your insurance company variable annuity contract for specific information about the insurance company's policies. Under certain circumstances, policy or contract owners may be required to transmit purchase or redemption orders only by first class U.S. mail.

</R> <R></R> <R></R>DISTRIBUTION AND SERVICE (12b-1) PLANS

<R>Distribution and Service Plan for Service Shares. The Fund has adopted a Distribution and Service Plan for Service Shares to pay the Distributor for distribution related services, personal services and account maintenance for those shares. Under the Plan, the Fund pays the Distributor quarterly at an annual rate of up to 0.25% of the daily net assets of the Fund's Service Shares. Because these fees are paid out of the Fund's assets on an on-going basis, over time they will increase the operating expenses of the Service Shares and may cost you more than other types of fees or sales charges. As a result, the Service Shares may have lower performance compared to the Fund's shares that are not subject to a service fee.

</R>Use of Plan Fees: The Distributor currently uses all of those fees to compensate sponsor(s) of the insurance product for providing personal services and account maintenance for variable contract owners that hold Service Shares.

Payments to Financial Intermediaries and Service Providers. The Sub-Adviser and the Distributor, in their discretion, may also make payments for distribution and/or shareholder servicing activities to brokers, dealers and other financial intermediaries, including the insurance companies that offer the Fund as an investment option, or to service providers. Those payments are made out of the Sub-Adviser's and/or the Distributor's own resources and/or assets, including from the revenues or profits derived from the advisory fees the Sub-Adviser receives from the Fund. Those cash payments, which may be substantial, are paid to many firms having business relationships with the Sub-Adviser and Distributor and are in addition to any distribution fees, servicing fees, or transfer agency fees paid directly or indirectly by the Fund to those entities. Payments by the Sub-Adviser or Distributor from their own resources are not reflected in the tables in the "Fees and Expenses of the Fund" section of this prospectus because they are not paid by the Fund.

<R>

The financial intermediaries that may receive those payments include firms that offer and sell Fund shares to their clients, or provide shareholder services to the Fund, or both, and receive compensation for those activities. The financial intermediaries that may receive payments include your securities broker, dealer or financial advisor, sponsors of fund "supermarkets," sponsors of fee-based advisory or wrap fee-based programs, sponsors of college and retirement savings programs, banks, trust companies and other intermediaries offering products that hold Fund shares, and insurance companies that offer variable annuity or variable life insurance products.

In general, these payments to financial intermediaries can be categorized as "distribution-related" or "servicing" payments. Payments for distribution-related expenses, such as marketing or promotional expenses, are often referred to as "revenue sharing." Revenue sharing payments may be made on the basis of the sales of shares attributable to that intermediary, the average net assets of the Fund and other Oppenheimer funds attributable to the accounts of that intermediary and its clients, negotiated lump sum payments for distribution services provided, or similar fees. In some circumstances, revenue sharing payments may create an incentive for a financial intermediary or its representatives to recommend or offer shares of the Fund or other Oppenheimer funds to its customers. These payments also may give an intermediary an incentive to cooperate with the Distributor's marketing efforts. A revenue sharing payment may, for example, qualify the Fund for preferred status with the intermediary receiving the payment or provide representatives of the Distributor with access to representatives of the intermediary's sales force, in some cases on a preferential basis over funds of competitors. Additionally, as firm support, the Sub-Adviser or Distributor may reimburse expenses related to educational seminars and "due diligence" or training meetings (to the extent permitted by applicable laws or the rules of the Financial Industry Regulatory Authority ("FINRA")) designed to increase sales representatives' awareness about Oppenheimer funds, including travel and lodging expenditures. However, the Sub-Adviser does not consider a financial intermediary's sale of shares of the Fund or other Oppenheimer funds when selecting brokers or dealers to effect portfolio transactions for the funds.

Various factors are used to determine whether to make revenue sharing payments. Possible considerations include, without limitation, the types of services provided by the intermediary, sales of Fund shares, the redemption rates on accounts of clients of the intermediary or overall asset levels of Oppenheimer funds held for or by clients of the intermediary, the willingness of the intermediary to allow the Distributor to provide educational and training support for the intermediary's sales personnel relating to the Oppenheimer funds, the availability of the Oppenheimer funds on the intermediary's sales system, as well as the overall quality of the services provided by the intermediary and the Sub-Adviser or Distributor's relationship with the intermediary. The Sub-Adviser and Distributor have adopted guidelines for assessing and implementing each prospective revenue sharing arrangement. To the extent that financial intermediaries receiving distribution-related payments from the Sub-Adviser or Distributor sell more shares of the Oppenheimer funds or retain more shares of the funds in their client accounts, the Sub-Adviser and Distributor benefit from the incremental management and other fees they receive with respect to those assets.

Payments may also be made by the Sub-Adviser, the Distributor or the Transfer Agent to financial intermediaries to compensate or reimburse them for administrative or other client services provided, such as sub-transfer agency services for shareholders or retirement plan participants, omnibus accounting or sub-accounting, participation in networking arrangements, account set-up, recordkeeping and other shareholder services. Payments may also be made for administrative services related to the distribution of Fund shares through the intermediary. Firms that may receive servicing fees include retirement plan administrators, qualified tuition program sponsors, banks and trust companies, and insurance companies that offer variable annuity or variable life insurance products, and others. These fees may be used by the service provider to offset or reduce fees that would otherwise be paid directly to them by certain account holders, such as retirement plans.

The Statement of Additional Information contains more information about revenue sharing and service payments made by the Sub-Adviser or the Distributor. Your broker, dealer or other financial intermediary may charge you fees or commissions in addition to those disclosed in this prospectus.

You should ask your financial intermediary for details about any such payments it receives from the Sub-Adviser or the Distributor and their affiliates, or any other fees or expenses it charges.

Dividends, Capital Gains and Taxes

DIVIDENDS AND DISTRIBUTIONS. The Fund intends to declare and pay dividends annually from any net investment income. The Fund may also realize capital gains on the sale of portfolio securities, in which case it may make distributions out of any net short-term or long-term capital gains annually. The Fund may also make supplemental distributions of dividends and capital gains following the end of its fiscal year. The Fund has no fixed dividend rate and cannot guarantee that it will pay any dividends or capital gains distributions in a particular year.

Dividends and distributions are paid separately for each share class. Because of the higher expenses on Service Shares, the dividends and capital gains distributions paid on those shares will generally be lower than for other Fund shares.

Receiving Dividends and Distributions. Any dividends and capital gains distributions will be automatically reinvested in additional Fund shares for the account of the participating insurance company, unless the insurance company elects to have dividends or distributions paid in cash.

TAXES. For a discussion of the tax status of a variable annuity contract, a variable life insurance policy or other investment product of a participating insurance company, please refer to the accompanying variable contract prospectus of your participating insurance company. Because shares of the Fund may be purchased only through insurance company separate accounts for variable annuity contracts, variable life insurance policies or other investment products, any dividends from net investment income and distributions of net realized short-term and long-term capital gains will be taxable, if at all, to the participating insurance company. However, those payments may affect the tax basis of certain types of distributions from those accounts.

The Fund has qualified and intends to qualify each year to be taxed as a regulated investment company under the Internal Revenue Code by satisfying certain income, asset diversification and income distribution requirements, but reserves the right not to so qualify. In each year that it qualifies as a regulated investment company, the Fund will not be subject to federal income taxes on its income that it distributes to shareholders.

This information is only a summary of certain Federal income tax information about your investment. You are encouraged to consult your tax adviser about the effect of an investment in the Fund on your particular tax situation and about any changes to the Internal Revenue Code that may occur from time to time. Additional information about the tax effects of investing in the Fund is contained in the Statement of Additional Information.

<R>The Financial Highlights Table is presented to help you understand the Fund's financial performance for the past five fiscal years. Certain information reflects financial results for a single Fund share. The total returns in the table represent the rate that an investor would have earned (or lost) on an investment in the Fund (assuming reinvestment of all dividends and distributions). This information has been audited by KPMG LLP, the Fund's independent registered public accounting firm. KPMG's report, along with the Fund's financial statements, are included in the annual report, which is available upon request.

</R>| FINANCIAL HIGHLIGHTS |

|

|

Year Ended |

Year Ended |

Year Ended |

Year Ended |

Year Ended |

|||||

|

|

December 31, |

December 31, |

December 30, |

December 31, |

December 31, |

|||||

|

Non-Service Shares |

2013 |

2012 |

20111 |

2010 |

2009 |

|||||

|

Per Share Operating Data |

|

|

|

|

|

|||||

|

Net asset value, beginning of period |

$45.06 |

$39.75 |

$40.35 |

$36.94 |

$25.67 |

|||||

|

Income (loss) from investment operations: |

|

|

|

|

|

|||||

|

Net investment income2 |

0.23 |

0.42 |

0.23 |

0.11 |

0.09 |

|||||

|

Net realized and unrealized gain (loss) |

13.09 |

5.18 |

(0.69) |

3.36 |

11.27 |

|||||

|

Total from investment operations |

13.32 |

5.60 |

(0.46) |

3.47 |

11.36 |

|||||

|

Dividends and/or distributions to shareholders: |

|

|

|

|

|

|||||

|

Dividends from net investment income |

(0.50) |

(0.29) |

(0.14) |

(0.06) |

(0.09) |

|||||

|

Net asset value, end of period |

$57.88 |

$45.06 |

$39.75 |

$40.35 |

$36.94 |

|||||

|

|

|

|

|

|

|

|||||

|

Total Return, at Net Asset Value3 |

29.74% |

14.12% |

(1.15)% |

9.42% |

44.52% |

|||||

|

|

|

|

|

|

|

|||||

|

Ratios/Supplemental Data |

|

|

|

|

|

|||||

|

Net assets, end of period (in thousands) |

$626,907 |

$573,684 |

$637,868 |

$771,086 |

$1,074,190 |

|||||

|

Average net assets (in thousands) |

$595,912 |

$600,121 |

$713,770 |

$976,242 |

$ 927,670 |

|||||

|

Ratios to average net assets:4 |

|

|

|

|

|

|||||

|

Net investment income |

0.44% |

0.95% |

0.57% |

0.31% |

0.29% |

|||||

|

Total expenses5 |

0.81% |

0.81% |

0.80% |

0.79% |

0.78% |

|||||

|

Expenses after payments, waivers and/or reimbursements and reduction to custodian expenses |

0.80% |

0.80% |

0.80% |

0.79% |

0.78% |

|||||

|

Portfolio turnover rate |

77% |

28% |

27% |

58% |

46% |

|

1. December 30, 2011 represents the last business day of the Fund's 2011 fiscal year. |

|

|

|

2. Per share amounts calculated based on the average shares outstanding during the period. |

|

|

|

3. Assumes an initial investment on the business day before the first day of the fiscal period, with all dividends and distributions reinvested in additional shares on the reinvestment date, and redemption at the net asset value calculated on the last business day of the fiscal period. Total returns are not annualized for periods less than one full year. Total return information does not reflect expenses that apply at the separate account level or to related insurance products. Inclusion of these charges would reduce the total return figures for all periods shown. Returns do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. |

|

|

|

4. Annualized for periods less than one full year. |

|

|

|

5. Total expenses including indirect expenses from affiliated fund were as follows: |

|

|

|

Year Ended December 31, 2013 |

0.81% |

|

|

Year Ended December 31, 2012 |

0.81% |

|

|

Year Ended December 30, 2011 |

0.80% |

|

|

Year Ended December 31, 2010 |

0.79% |

|

|

Year Ended December 31, 2009 |

0.78% |

|

<R>

|

|

Year Ended |

Year Ended |

Year Ended |

Year Ended |

Year Ended |

|||||

|

|

December 31, |

December 31, |

December 30, |

December 31, |

December 31, |

|||||

|

Service Shares |

2013 |

2012 |

20111 |

2010 |

2009 |

|||||

|

Per Share Operating Data |

|

|

|

|

|

|||||

|

Net asset value, beginning of period |

$44.66 |

$39.40 |

$39.99 |

$36.64 |

$25.42 |

|||||

|

Income (loss) from investment operations: |

|

|

|

|

|

|||||

|

Net investment income2 |

0.10 |

0.31 |

0.13 |

0.02 |

0.01 |

|||||

|

Net realized and unrealized gain (loss) |

12.98 |

5.12 |

(0.68) |

3.33 |

11.21 |

|||||

|

Total from investment operations |

13.08 |

5.43 |

(0.55) |

3.35 |

11.22 |

|||||

|

Dividends and/or distributions to shareholders: |

|

|

|

|

|

|||||

|

Dividends from net investment income |

(0.37) |

(0.17) |

(0.04) |

0.00 |

0.00 3 |

|||||

|

Net asset value, end of period |

$57.37 |

$44.66 |

$39.40 |

$39.99 |

$36.64 |

|||||

|

|

|

|

|

|

|

|||||

|

Total Return, at Net Asset Value4 |

29.43% |

13.81% |

(1.37)% |

9.15% |

44.15% |

|||||

|

|

|

|

|

|

|

|||||

|

Ratios/Supplemental Data |

|

|

|

|

|

|||||

|

Net assets, end of period (in thousands) |

$364,214 |

$366,664 |

$375,330 |

$423,989 |

$444,170 |

|||||

|

Average net assets (in thousands) |

$367,615 |

$382,196 |

$407,413 |

$427,640 |

$368,634 |

|||||

|

Ratios to average net assets:5 |

|

|

|

|

|

|||||

|

Net investment income |

0.20% |

0.71% |

0.32% |

0.06% |

0.03% |

|||||

|

Total expenses5 |

1.06% |

1.06% |

1.05% |

1.04% |

1.04% |

|||||

|

Expenses after payments, waivers and/or reimbursements and reduction to custodian expenses |

1.05% |

1.05% |

1.05% |

1.04% |

1.03% |

|||||

|

Portfolio turnover rate |

77% |

28% |

27% |

58% |

46% |

|

1. December 30, 2011 represents the last business day of the Fund's 2011 fiscal year. |

|

|

|

2. Per share amounts calculated based on the average shares outstanding during the period. |

|

|

|

3. Less than $0.005 per share. |

|

|

|

4. Assumes an initial investment on the business day before the first day of the fiscal period, with all dividends and distributions reinvested in additional shares on the reinvestment date, and redemption at the net asset value calculated on the last business day of the fiscal period. Total returns are not annualized for periods less than one full year. Total return information does not reflect expenses that apply at the separate account level or to related insurance products. Inclusion of these charges would reduce the total return figures for all periods shown. Returns do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. |

|

|

|

5. Annualized for periods less than one full year. |

|

|

|

6. Total expenses including indirect expenses from affiliated fund were as follows: |

|

|

|

Year Ended December 31, 2013 |

1.06% |

|

|

Year Ended December 31, 2012 |

1.06% |

|

|

Year Ended December 30, 2011 |

1.05% |

|

|

Year Ended December 31, 2010 |

1.04% |

|

|

Year Ended December 31, 2009 |

1.04% |

|

<R>