UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF

REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act File Number: 811-00696

| T. Rowe Price Small-Cap Stock Fund, Inc. |

|

|

| (Exact name of registrant as specified in charter) |

| 100 East Pratt Street, Baltimore, MD 21202 |

|

|

| (Address of principal executive offices) |

| David Oestreicher |

| 100 East Pratt Street, Baltimore, MD 21202 |

|

|

| (Name and address of agent for service) |

Registrant’s telephone number, including area

code: (410) 345-2000

Date of fiscal year end: December

31

Date of reporting period: June 30, 2016

Item 1. Report to Shareholders

|

|

Small-Cap

Stock Fund |

June 30,

2016 |

The views and opinions in this report were current as of June 30, 2016. They are not guarantees of performance or investment results and should not be taken as investment advice. Investment decisions reflect a variety of factors, and the managers reserve the right to change their views about individual stocks, sectors, and the markets at any time. As a result, the views expressed should not be relied upon as a forecast of the fund’s future investment intent. The report is certified under the Sarbanes-Oxley Act, which requires mutual funds and other public companies to affirm that, to the best of their knowledge, the information in their financial reports is fairly and accurately stated in all material respects.

REPORTS ON THE WEB

Sign up for our Email Program, and you can begin to receive updated fund reports and prospectuses online rather than through the mail. Log in to your account at troweprice.com for more information.

Manager’s Letter

Fellow Shareholders

The first half of 2016 was challenging for small-cap investors, as small-cap stocks corrected sharply through late February before rebounding. Defensive sectors, such as utilities and consumer staples, led the Russell 2000 Index returns as investors sought safety. The materials sector also bounced higher after a poor start to the year. Value shares significantly outperformed growth over the half year, and our portfolio’s durable “all weather” core blend of growth and value once again served us well. The end of the six-month period was particularly volatile as investors reacted to the unexpected UK “Brexit” vote. We were pleased, however, to end the period with modest outperformance. As we look to the second half of the year, we remain cautious on the small-cap space given what we believe to be its elevated valuation levels.

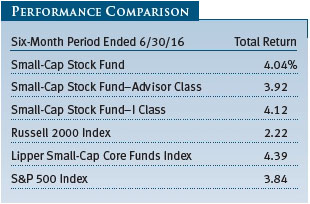

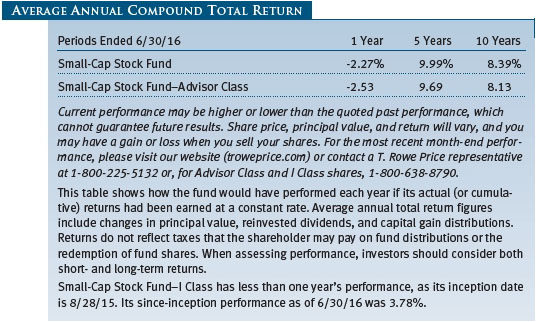

The Small-Cap Stock Fund returned 4.04% in the first half of 2016 versus 2.22% for the Russell 2000 Index and 4.39% for the Lipper Small-Cap Core Funds Index. (Results for the Advisor and I Class shares varied, reflecting their different fee structures, cash flows, and other factors.) Based on cumulative total return, Lipper ranked the Small-Cap Stock Fund in the top 14% of small-cap core funds for the five-year period ended June 30, 2016. Lipper ranked the Small-Cap Stock Fund 193 of 821, 142 of 697, 83 of 607, and 23 of 416 small-cap core funds for the 1-, 3-, 5-, and 10-year periods ended June 30, 2016, respectively. (Results will vary for other periods. Past performance cannot guarantee future results.)

PERFORMANCE REVIEW

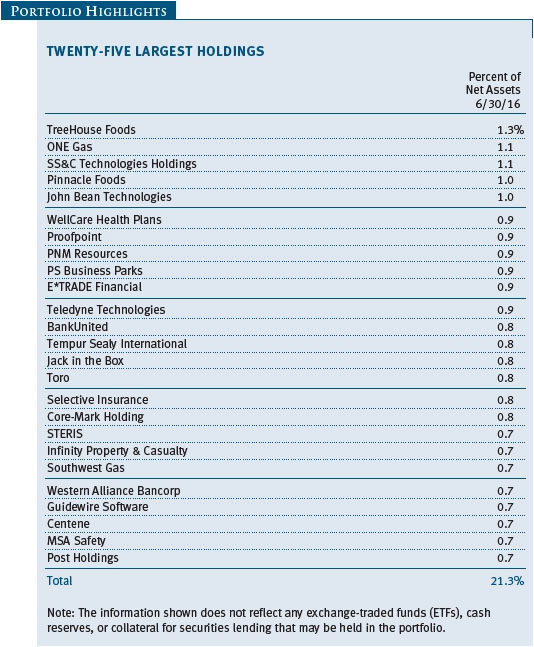

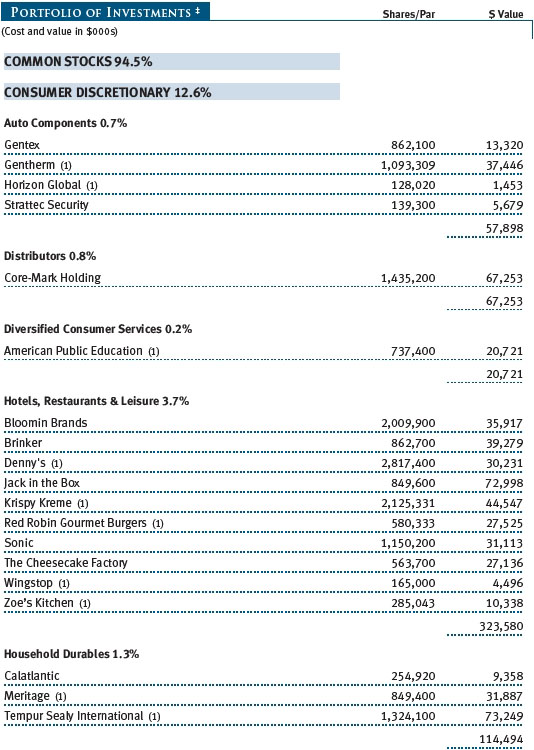

Over the period, we had our strongest results in the industrials, health care, and energy sectors. Our overweight position and solid stock selection in the industrials sector helped performance. Ritchie Bros. Auctioneers was a top contributor after the firm reported strong first-quarter results and amid investor expectations that the industrial auctioneer would benefit as commercial contractors downsized fleets during the later stage of the economic cycle. That move was expected to make more attractive equipment available for auction. Shares of John Bean Technologies also boosted returns, thanks to the company’s strong management team, which reduced costs and restructured while pursuing accretive mergers and further investing for renewed organic growth. The company’s earnings per share solidly beat expectations in the first quarter. Toro, a high-quality industrial that raised its forward guidance in May, rounded out the gains in this sector. (Please refer to the fund’s portfolio of investments for a complete list of holdings and the amount each represents in the portfolio.)

Our underweight to the health care sector also helped relative results, as did our position in health plan provider WellCare Health Plans, which reported strong first-quarter earnings and raised its 2016 earnings guidance.

Several of our energy holdings helped performance during the period as oil prices rose. Diamondback Energy outperformed in this environment and also benefited after it raised equity during the six-month reporting period to further bolster its balance sheet. In May, the firm (which operates in the Permian Basin) also increased production guidance for 2016. Parsley Energy, another well-financed player in the midland basin, also took advantage of the oil rally to raise incremental equity to bolster its capital in the wake of a $280 million deal to buy additional mineral rights in the Delaware Basin. Another exploration and production company, Rice Energy, benefited from the recovery in energy prices and reported higher production volume and lower expenses in the first quarter. The stock of SEACOR Holdings helped performance even after the company missed estimates as lower oil prices pressured its offshore support vessel business. The inland river barge operation also hurt results. Nevertheless, the rise in commodity prices and the company’s solid reputation kept the stock afloat. The diversity of its business lines, its shrewd management, and its strong financial position should enable Chief Executive Officer Charles Fabrikant to acquire value-added businesses at attractive prices. SEACOR remains an attractive value play in our eyes.

Our stock selection in the financials sector was the largest detractor to relative performance. Financials stocks came under pressure during the reporting period as a slowing global economy and the unexpected UK vote to leave the European Union increased expectations that interest rates would remain low for a prolonged period. E*TRADE Financial, whose business is levered to rising rates, suffered as a result. Even so, the brokerage firm continues to aggressively manage its capital structure by repurchasing shares. BankUnited also struggled as investors worried that its net interest margin (NIM) would be pressured by low interest rates. Indeed, the firm’s first-quarter revenues were slightly disappointing, and its NIM declined. Concern that BankUnited’s commercial real estate concentration is higher than many of its peers also weighed on the firm’s share price, as did weaker-than-expected loan growth. Broker-dealer Waddell & Reed Financial underperformed as its first-quarter earnings fell well short of expectations and as it continued to struggle with the loss of some of its senior fund managers. The performance of its flagship Asset Strategy Fund, which experienced elevated outflows during the period, also lagged. We believe the firm can fix its problems, and we are holding on to the shares.

Also detracting from relative performance was our underweight to and stock selection in the materials sector. Namely, investors punished the stock of Multi Packaging Solutions International, especially following the Brexit vote, because of the company’s high exposure to Europe (46% of revenues). The company remains highly levered after recently going public. Leverage is never popular with investors when market volatility rises.

PORTFOLIO STRATEGY

On the Buy Side

Our largest purchase in the first half was Tempur Sealy International,

the world’s largest bedding supplier. Longtime fund shareholders may recall that

we bought shares at the height of the last financial crisis, which eventually

led to a 300% plus return. While we don’t currently foresee this level of risk

and reward, we nonetheless found the shares reaching attractive levels earlier

in the year as investors feared a consumer slowdown could hurt the company.

Therefore, we bought the stock again, believing that the company has the

opportunity to improve profitability. Recent

sweeping changes in the management and the Board could prove to be the necessary

catalyst to drive improved returns.

We have been longtime owners of Jack in the Box, the parent of the Jack in the Box and Qdoba restaurant chains. Jack in the Box reported solid second-quarter results and further noted plans to increase its effort to refranchise company-owned stores. This increased focus on improving returns should escalate the firm’s return on invested capital profile and allow for expanded valuation.

We also made further changes to our technology holdings during the period. In the semiconductor space, we added Microsemi, a high-quality, security-focused company with a strong competitive advantage in long-cycle defense and aerospace markets. The company is capable of strong operating leverage as these markets improve in line with an improved outlook for defense outlays and integrated circuit design contacts, which should pick up in the aerospace industry. The company, which designs analog semiconductors, has a history of accretive acquisitions. The PMC-Sierra deal should prove accretive over time as Microsemi tends to run more disciplined operations. Microsemi’s shares seem to trade at an unwarranted discount to peers and look to be attractively valued. Similarly, in optical networking, we added Ciena, which provides optical networking equipment for transport, switching, and traffic management over optical networks. We believe the firm will be a beneficiary of the long-awaited metro fiber build out. Ciena is well positioned for the current 100G (100 gigabits) cycle. The firm has excellent Internet protocol, and the market sell-off allowed us to add the shares.

Cybersecurity remains an ongoing investment theme in today’s uncertain world. Neither governments nor corporations can afford to skimp on investments in cybersecurity. Therefore, we bought shares of Proofpoint and FireEye. Proofpoint is a security software company that provides a secure email gateway and archiving solutions. The firm sells add-on products, including an advanced persistent threat solution and several emerging products in social media and mobile threat containment. The firm has a strong management team; a high-quality, cloud-based software model; and a widening advantage over its competitors.

FireEye, a security software company that specializes in defending against advanced malware, has a virtualization technology that executes network traffic in a secure safe “sand box” environment to assess potential threats and identify malicious software for defense across its networks. The firm also has a very high-quality service business, Mandiant, which specializes in incident response following an attack. The stock had been weak following a leadership change and the company’s ongoing transition from a product-oriented business to a subscription/services model. The firm has promising new cloud products and a renewed focus on cost discipline.

Further in technology, we also initiated positions in Booz Allen Hamilton and EPAM Systems. Booz Allen Hamilton is a highly regarded management consulting, technology, and engineering services company to the U.S. government, serving defense, intelligence, and civil markets. The U.S. government’s spending on cybersecurity looks set to accelerate meaningfully, and Booz Allen is a best-in-class provider of differentiated services. The firm can deliver sector-leading growth, which, when combined with modest margin expansion, should allow it to stand out in a market increasingly searching for companies that are insulated from economic cycles. Department of Defense consulting firms are great late-cycle plays, and we have begun to establish a position. EPAM provides high-end software engineering and IT services to global clients out of low-cost locations, primarily in central and Eastern Europe. The firm is headquartered in the U.S. and employs over 15,000 IT professionals. We believe it is a high-quality earnings compounder capable of strong revenue and earnings growth over the next three years. Management has an excellent execution track record and exposure to structurally attractive end markets. Earlier in the first quarter, the shares sold off sharply after a competitor’s dramatic share price decline. Investors have, in our view, focused on the political risk of an employee base heavily located in Belarus, Ukraine, and Russia. Management, however, has solid contingency plans in place.

One trend that is unlikely to abate is the continuing need for clean water and the ongoing capital spending needed to upgrade our aging infrastructure. Most of us were shocked by the disaster that unfolded in Flint, Michigan, earlier this year. Flint’s woes were perhaps the catalyst that drove regulators to insist on upgraded water systems under their jurisdiction. California Water Service Group is a high-quality company with the makings of an attractive multiyear utility holding in small-cap portfolios due to significant rate base growth associated with aging infrastructure investment. Management is competent and disciplined. We believe this is a fine opportunity to invest for a multiyear play on the secular outlook for improved returns and potential further consolidation/privatization in the space.

In the financials sector, we established an investment in Webster Financial, a $3.4 billion solid core Connecticut bank with a unique health savings account (HSA) bank asset. Growing HSA deposits and earnings should drive a rerating of the stock over the next several years. The firm traded at less than 12 times to 18 times earnings, which, in our opinion, gave little valuation credit for its unique HSA growth profile. Webster is the largest provider of health savings account trustee and administrative services in the U.S., with a 15% market share of $4.3 billion over 1.7 million accounts.

On the Sell Side

One of our largest sales during the period was Cray, a leading supplier of

supercomputing technology to governments, research institutions, and industry.

For the past several years, Cray has prospered as its largest competitor stepped

back from the market, allowing Cray to increase share. We fully expect the

competitor to reengage and, undoubtedly, the next cycle may be more competitive

than expected.

After shares rose significantly, we reduced our holdings for position size management. Later in the quarter, the shares weakened as the firm reiterated the risk that component availability might delay the acceptance of third- and fourth-quarter shipments. Such delays, when they occur, have little bearing on the long-term value of the business; therefore, we will carefully watch the stock in the second half of the year.

A number of our technology holdings were subject to takeover activity in the half. Microsemi bought PMC-Sierra, and as previously noted, the potential accretion from this deal is a key reason we added Microsemi. Buyout firm Vista Equity Partners agreed to acquire both the event planning firm Cvent and software development firm Marketo in the first half. Finally, salesforce.com reached an agreement to buy Demandware for $75 per share. Demandware enables customers to optimize e-commerce channels through merchandising, content management, and shopping cart functionality.

We sold Interactive Intelligence in the first quarter after a series of operational missteps. The company is the only provider of a single integrated suite of contact center infrastructure software. While we like this niche, we lost confidence in management’s ability to exploit the space. Finally, in technology, we sold Imperva, a security software company that sells solutions for securing Web applications and corporate data files. We added this company following the arrival of a new management team who sought to leverage its best-in-class technology and strong market demand. After reporting a series of attractive quarters, the firm badly missed its first-quarter earnings target, shaking our confidence in this management team’s ability to deliver on opportunities.

During the first quarter, we purchased or added to a number of industrial names around the unfounded fear that we were slipping into a near-term recession. We purchased Genesee & Wyoming after the market began unfairly discounting a moderate recession in its stock price. The shares had a very sharp recovery, leading us to take the profits after a quick 38% gain. Other industrial sales included Rexnord, Toro, Graco, and John Bean Technologies. Rexnord has high financial leverage coupled with challenged end markets and will surely be paying down debt, but other industrials with less leverage will be better positioned for opportunistic acquisitions or stock buybacks. Toro, which continues to be the equipment leader in the niche markets of golf and professional landscape, has been a successful investment for the fund. We reduced the position in the quarter based on a valuation that is about 30% above its average. While Toro’s business fundamentals are strong, we do not believe there will be a material acceleration to the growth rate of this mature business. We reduced our holding in Graco because of valuation concerns. We would expect the multiple to contract this late in the business cycle; however, this year, the opposite has occurred. The enterprise value to earnings before interest, taxes, depreciation, and amortization (EV/EBITDA) multiple is 20% above its longer-term average. The fund still holds Graco because this high-quality industrial stands out among peers with 4% to 5% sales growth, only slightly off its upper-single-digit long-term model. We slightly reduced our position in John Bean Technologies after the stock had a strong run. We believe this stock has gone through the initial phase of discovery and that it is fully valued at 13 times its estimated EBITDA. We continue to hold it as a top position because of its positive longer-term growth prospects.

One of our largest purchases in recent years was Incyte. The shares had performed admirably, tracking its success with its drug Jakafi and investors’ unbridled enthusiasm over the biotech sector. The market cap grew quite high. When it exceeded $20 billion, we substantially reduced the position size. The shares were subsequently hard hit in the biotech correction early in the year.

Knoll is a true design leader in office furniture, which is a cyclical business. We have thus begun reducing positions here as we look toward the end of the office furniture cycle. We expect Knoll’s results to hold up over the intermediate term, during which we would expect to see significant multiple compression as investors anticipate peak earnings. Therefore, we trimmed to redeploy proceeds elsewhere.

We continue to remain cautious on the energy space. RPC, which provides specialized oil field services and equipment to independent and major oil field companies, has a good balance sheet and a solid management team. However, we believe its shares will lag the market and that its pressure pumping business will remain depressed for longer than expected because of supply/demand constraints.

OUTLOOK

The past 12 months have certainly tested investors’ patience. From its July 16, 2015, peak to the February 11, 2016, trough, the Russell 2000 Index fell a sharp 25%, which would certainly qualify as a bear market. This was indeed a bit more than your typical midcycle correction. Stocks have since rebounded sharply, and many investors may be wondering if now may be the time to redouble their interests and investments in the small-cap space.

Currently small-caps look about fairly valued versus large-caps. We noted in our December outlook that small-cap valuations versus large-caps were below the median for the first time in seven years. At period-end, they remain in discount territory, yet they look cheap on a relative basis largely because of the expanded valuations in the large-cap sector.

Currently, the Russell 2000 Index, according to Steve DeSanctis’s work at Jefferies, stands at roughly 17.9 times forward earnings and very close to one standard deviation in valuation above its long-term average. This places valuation at levels where investors typically earn lackluster returns.

To be clear, while current valuation levels give us pause, we do not see an immediate need to get more defensive. In our opinion, unless some catalyst emerges and pushes the U.S. into a recession, small-caps are not poised for a sharp correction. We believe that small-caps will continue to lag large-caps and that multiples will further compress until small-caps reach a more significant discount versus large-caps.

This will be my last letter to shareholders of the Small-Cap Stock Fund. As we have recently informed you, I will be stepping down from active management of the portfolio on September 30. It has indeed been a pleasure to serve as your lead portfolio manager for the past 24 years. We have seen several small-cap cycles, two recessions, two secular bear markets, and numerous corrections over the period. Each has brought its own challenges and opportunities, and throughout this period, I have been aided by our very able team of T. Rowe Price analysts.

I have the greatest confidence that the succeeding team of my long-time partners, Frank Alonso and Curt Organt, will continue to steward our portfolio with investment skill and insight. Therefore, I am certain that our strategy will remain the same. Both are very solid risk-aware long-term investors. Both have many years of investment experience, and both are appropriately skeptical of investment fads. Frank and Curt were responsible for selecting many of our best names over the last few decades. Each has worked with me for many years. In fact Curt was hired as my associate analyst at the very beginning of our management of the OTC (Over-the-Counter) Fund—the Small-Cap Stock Fund predecessor. I am also certain that our group will continue to discover interesting names to build a durable blend of growth and value, which should continue to add value over the long term. Thanks again for all your support over the last 24 years.

Thank you for your confidence in our small-cap team.

Sincerely,

Greg A. McCrickard

President of the fund and chairman of its Investment Advisory

Committee

July 22, 2016

The committee chairman has day-to-day responsibility for managing the portfolio and works with committee members in developing and executing the fund’s investment program.

RISKS OF STOCK INVESTING

As with all stock and bond mutual funds, the fund’s share price can fall because of weakness in the stock or bond markets, a particular industry, or specific holdings. The financial markets can decline for many reasons, including adverse political or economic developments, changes in investor psychology, or heavy institutional selling. The prospects for an industry or company may deteriorate because of a variety of factors, including disappointing earnings or changes in the competitive environment. In addition, the investment manager’s assessment of companies held in a fund may prove incorrect, resulting in losses or poor performance even in rising markets. Investing in small companies involves greater risk than is customarily associated with larger companies. Stocks of small companies are subject to more abrupt or erratic price movements than larger-company stocks. Small companies often have limited product lines, markets, or financial resources and their managements may lack depth and experience. Such companies seldom pay significant dividends that could cushion returns in a falling market.

GLOSSARY

Basis point: One one-hundredth of one percentage point, or 0.01%.

Lipper indexes: Fund benchmarks that consist of a small number of the largest mutual funds in a particular category as tracked by Lipper Inc.

Market capitalization: The total value of a company’s publicly traded shares.

Price/book ratio: A valuation measure that compares a stock’s market price with its book value; i.e., the company’s net worth divided by the number of outstanding shares.

Price/earnings (P/E) ratio: A valuation measure calculated by dividing the price of a stock by its reported earnings per share. The ratio is a measure of how much investors are willing to pay for the company’s earnings.

Price/sales ratio: A valuation measure calculated by dividing the price of a stock by its current or projected (forward) sales (or revenues) per share.

Return on equity (ROE): Calculated by dividing a company’s net income by shareholders’ equity, ROE measures how much a company earns on each dollar that common stock investors have put into that company. ROE indicates how effectively and efficiently a company and its management are using stockholder investments.

Russell 2000 Growth Index: A market-weighted total return index that measures the performance of companies within the Russell 2000 Index having higher price/book value ratios and higher forecast growth rates.

Russell 2000 Index: An unmanaged index that tracks the stocks of 2,000 small U.S. companies.

Russell 2000 Value Index: An index that tracks the performance of small-cap stocks with higher price/book ratios and higher forecast growth values.

S&P 500 Index: An unmanaged index that tracks the stocks of 500 primarily large-cap U.S. companies.

Note: Russell Investment Group is the source and owner of the trademarks, service marks, and copyrights related to the Russell indexes. Russell® is a trademark of Russell Investment Group.

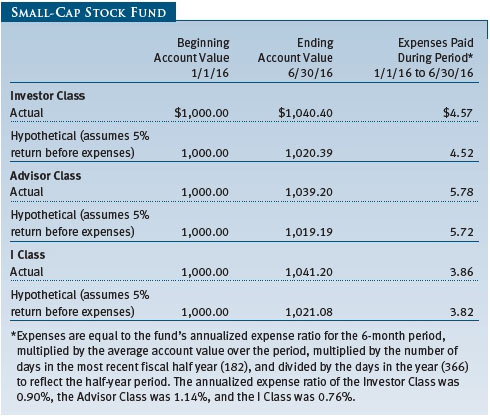

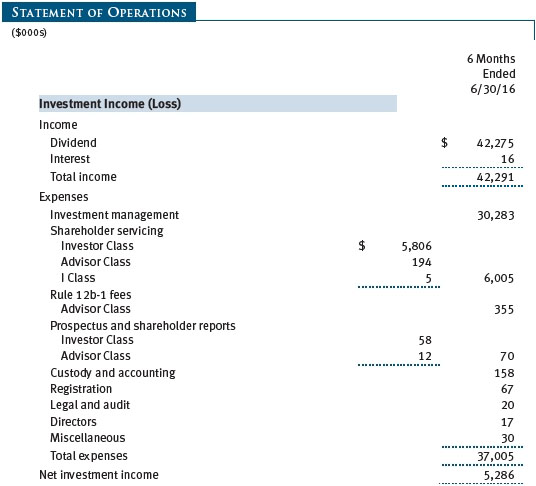

Performance and Expenses

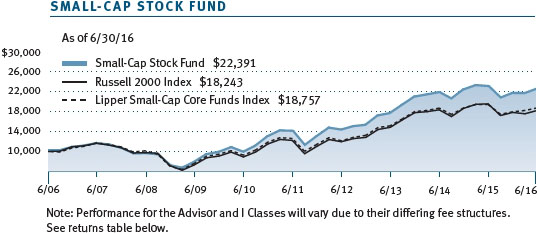

| Growth of $10,000 |

This chart shows the value of a hypothetical $10,000 investment in the fund over the past 10 fiscal year periods or since inception (for funds lacking 10-year records). The result is compared with benchmarks, which may include a broad-based market index and a peer group average or index. Market indexes do not include expenses, which are deducted from fund returns as well as mutual fund averages and indexes.

| Fund Expense Example |

As a mutual fund shareholder, you may incur two types of costs: (1) transaction costs, such as redemption fees or sales loads, and (2) ongoing costs, including management fees, distribution and service (12b-1) fees, and other fund expenses. The following example is intended to help you understand your ongoing costs (in dollars) of investing in the fund and to compare these costs with the ongoing costs of investing in other mutual funds. The example is based on an investment of $1,000 invested at the beginning of the most recent six-month period and held for the entire period.

Please note that the fund has three share classes: The original share class (Investor Class) charges no distribution and service (12b-1) fee, the Advisor Class shares are offered only through unaffiliated brokers and other financial intermediaries and charge a 0.25% 12b-1 fee, and I Class shares are available to institutionally oriented clients and impose no 12b-1 or administrative fee payment. Each share class is presented separately in the table.

Actual Expenses

The first line of the following table (Actual) provides

information about actual account values and expenses based on the fund’s actual

returns. You may use the information on this line, together with your account

balance, to estimate the expenses that you paid over the period. Simply divide

your account value by $1,000 (for example, an $8,600 account value divided by

$1,000 = 8.6), then multiply the result by the number on the first line under

the heading “Expenses Paid During Period” to estimate the expenses you paid on

your account during this period.

Hypothetical Example for Comparison

Purposes

The information on the second

line of the table (Hypothetical) is based on hypothetical account values and

expenses derived from the fund’s actual expense ratio and an assumed 5% per year

rate of return before expenses (not the fund’s actual return). You may compare

the ongoing costs of investing in the fund with other funds by contrasting this

5% hypothetical example and the 5% hypothetical examples that appear in the

shareholder reports of the other funds. The hypothetical account values and

expenses may not be used to estimate the actual ending account balance or

expenses you paid for the period.

Note: T. Rowe Price charges an annual account service fee of $20, generally for accounts with less than $10,000. The fee is waived for any investor whose T. Rowe Price mutual fund accounts total $50,000 or more; accounts electing to receive electronic delivery of account statements, transaction confirmations, prospectuses, and shareholder reports; or accounts of an investor who is a T. Rowe Price Preferred Services, Personal Services, or Enhanced Personal Services client (enrollment in these programs generally requires T. Rowe Price assets of at least $100,000). This fee is not included in the accompanying table. If you are subject to the fee, keep it in mind when you are estimating the ongoing expenses of investing in the fund and when comparing the expenses of this fund with other funds.

You should also be aware that the expenses shown in the table highlight only your ongoing costs and do not reflect any transaction costs, such as redemption fees or sales loads. Therefore, the second line of the table is useful in comparing ongoing costs only and will not help you determine the relative total costs of owning different funds. To the extent a fund charges transaction costs, however, the total cost of owning that fund is higher.

Unaudited

The accompanying notes are an integral part of these financial statements.

Unaudited

The accompanying notes are an integral part of these financial statements.

Unaudited

The accompanying notes are an integral part of these financial statements.

Unaudited

The accompanying notes are an integral part of these financial statements.

Unaudited

The accompanying notes are an integral part of these financial statements.

Unaudited

The accompanying notes are an integral part of these financial statements.

Unaudited

The accompanying notes are an integral part of these financial statements.

Unaudited

| Notes to Financial Statements |

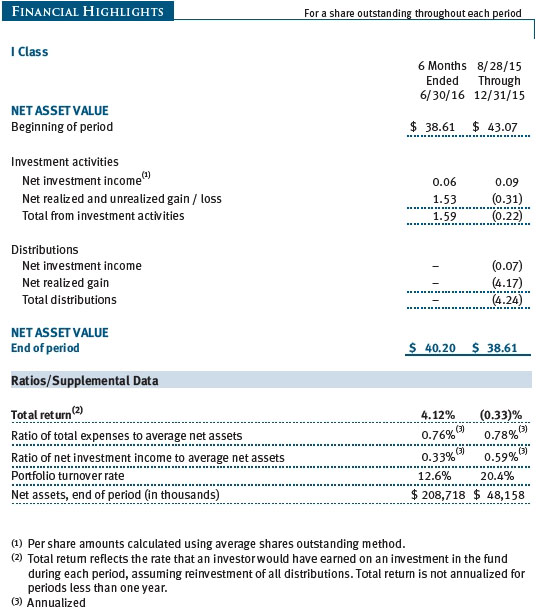

T. Rowe Price Small-Cap Stock Fund, Inc. (the fund), is registered under the Investment Company Act of 1940 (the 1940 Act) as a diversified, open-end management investment company. The fund seeks to provide long-term capital growth by investing primarily in stocks of small companies. The fund has three classes of shares: the Small-Cap Stock Fund original share class, referred to in this report as the Investor Class, incepted on June 1, 1956; the Small-Cap Stock Fund–Advisor Class (Advisor Class), incepted on March 31, 2000; and the Small-Cap Stock Fund–I Class (I Class), incepted on August 28, 2015. Advisor Class shares are sold only through unaffiliated brokers and other unaffiliated financial intermediaries. I Class shares generally are available only to investors meeting a $1,000,000 minimum investment or certain other criteria. The Advisor Class operates under a Board-approved Rule 12b-1 plan pursuant to which the class compensates financial intermediaries for distribution, shareholder servicing, and/or certain administrative services; the Investor and I Classes do not pay Rule 12b-1 fees. Each class has exclusive voting rights on matters related solely to that class; separate voting rights on matters that relate to all classes; and, in all other respects, the same rights and obligations as the other classes.

NOTE 1 - SIGNIFICANT ACCOUNTING POLICIES

Basis of Preparation The fund is an investment company and follows accounting and reporting guidance in the Financial Accounting Standards Board (FASB) Accounting Standards Codification Topic 946 (ASC 946). The accompanying financial statements were prepared in accordance with accounting principles generally accepted in the United States of America (GAAP), including, but not limited to, ASC 946. GAAP requires the use of estimates made by management. Management believes that estimates and valuations are appropriate; however, actual results may differ from those estimates, and the valuations reflected in the accompanying financial statements may differ from the value ultimately realized upon sale or maturity.

Investment Transactions, Investment Income, and Distributions Income and expenses are recorded on the accrual basis. Premiums and discounts on debt securities are amortized for financial reporting purposes. Dividends received from mutual fund investments are reflected as dividend income; capital gain distributions, if any, are reflected as realized gain/loss. Dividend income and capital gain distributions are recorded on the ex-dividend date. Income tax-related interest and penalties, if incurred, would be recorded as income tax expense. Investment transactions are accounted for on the trade date. Realized gains and losses are reported on the identified cost basis. Distributions from REITs are initially recorded as dividend income and, to the extent such represent a return of capital or capital gain for tax purposes, are reclassified when such information becomes available. Income distributions are declared and paid by each class annually. Distributions to shareholders are recorded on the ex-dividend date. Capital gain distributions, if any, are generally declared and paid by the fund annually.

Currency Translation Assets, including investments, and liabilities denominated in foreign currencies are translated into U.S. dollar values each day at the prevailing exchange rate, using the mean of the bid and asked prices of such currencies against U.S. dollars as quoted by a major bank. Purchases and sales of securities, income, and expenses are translated into U.S. dollars at the prevailing exchange rate on the date of the transaction. The effect of changes in foreign currency exchange rates on realized and unrealized security gains and losses is reflected as a component of security gains and losses.

Class Accounting Shareholder servicing, prospectus, and shareholder report expenses incurred by each class are charged directly to the class to which they relate. Expenses common to all classes, investment income, and realized and unrealized gains and losses are allocated to the classes based upon the relative daily net assets of each class. The Advisor Class pays Rule 12b-1 fees, in an amount not exceeding 0.25% of the class’s average daily net assets.

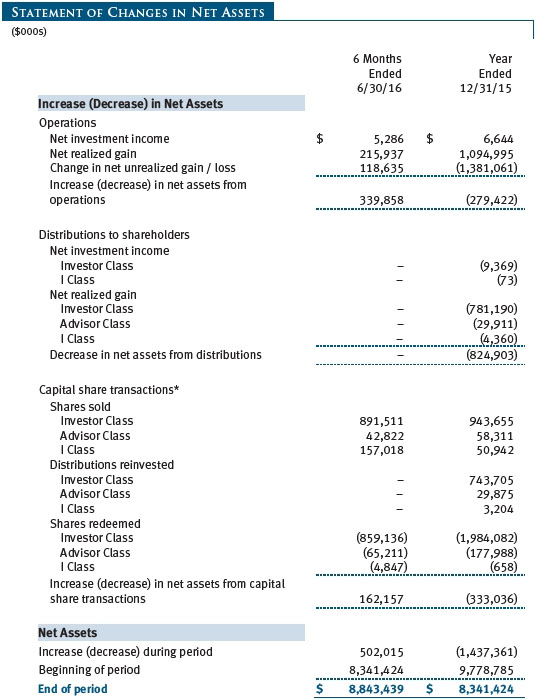

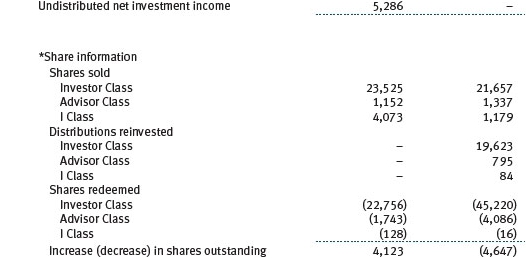

Rebates Subject to best execution, the fund may direct certain security trades to brokers who have agreed to rebate a portion of the related brokerage commission to the fund in cash. Commission rebates are reflected as realized gain on securities in the accompanying financial statements and totaled $109,000 for the six months ended June 30, 2016.

In-Kind Redemptions In accordance with guidelines described in the fund’s prospectus, and when considered to be in the best interest of all shareholders, the fund may distribute portfolio securities rather than cash as payment for a redemption of fund shares (in-kind redemption). Gains and losses realized on in-kind redemptions are not recognized for tax purposes and are reclassified from undistributed realized gain (loss) to paid-in capital. During the six months ended June 30, 2016, the fund realized $85,707,000 of net gain on $238,659,000 of in-kind redemptions.

NOTE 2 - VALUATION

The fund’s financial instruments are valued and each class’s net asset value (NAV) per share is computed at the close of the New York Stock Exchange (NYSE), normally 4 p.m. ET, each day the NYSE is open for business.

Fair Value The fund’s financial instruments are reported at fair value, which GAAP defines as the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date. The T. Rowe Price Valuation Committee (the Valuation Committee) has been established by the fund’s Board of Directors (the Board) to ensure that financial instruments are appropriately priced at fair value in accordance with GAAP and the 1940 Act. Subject to oversight by the Board, the Valuation Committee develops and oversees pricing-related policies and procedures and approves all fair value determinations. Specifically, the Valuation Committee establishes procedures to value securities; determines pricing techniques, sources, and persons eligible to effect fair value pricing actions; oversees the selection, services, and performance of pricing vendors; oversees valuation-related business continuity practices; and provides guidance on internal controls and valuation-related matters. The Valuation Committee reports to the Board and has representation from legal, portfolio management and trading, operations, risk management, and the fund’s treasurer.

Various valuation techniques and inputs are used to determine the fair value of financial instruments. GAAP establishes the following fair value hierarchy that categorizes the inputs used to measure fair value:

Level 1 – quoted prices (unadjusted) in active markets for identical financial instruments that the fund can access at the reporting date

Level 2 – inputs other than Level 1 quoted prices that are observable, either directly or indirectly (including, but not limited to, quoted prices for similar financial instruments in active markets, quoted prices for identical or similar financial instruments in inactive markets, interest rates and yield curves, implied volatilities, and credit spreads)

Level 3 – unobservable inputs

Observable inputs are developed using market data, such as publicly available information about actual events or transactions, and reflect the assumptions that market participants would use to price the financial instrument. Unobservable inputs are those for which market data are not available and are developed using the best information available about the assumptions that market participants would use to price the financial instrument. GAAP requires valuation techniques to maximize the use of relevant observable inputs and minimize the use of unobservable inputs. When multiple inputs are used to derive fair value, the financial instrument is assigned to the level within the fair value hierarchy based on the lowest-level input that is significant to the fair value of the financial instrument. Input levels are not necessarily an indication of the risk or liquidity associated with financial instruments at that level but rather the degree of judgment used in determining those values.

Valuation Techniques Equity securities listed or regularly traded on a securities exchange or in the over-the-counter (OTC) market are valued at the last quoted sale price or, for certain markets, the official closing price at the time the valuations are made. OTC Bulletin Board securities are valued at the mean of the closing bid and asked prices. A security that is listed or traded on more than one exchange is valued at the quotation on the exchange determined to be the primary market for such security. Listed securities not traded on a particular day are valued at the mean of the closing bid and asked prices for domestic securities and the last quoted sale or closing price for international securities.

For valuation purposes, the last quoted prices of non-U.S. equity securities may be adjusted to reflect the fair value of such securities at the close of the NYSE. If the fund determines that developments between the close of a foreign market and the close of the NYSE will, in its judgment, materially affect the value of some or all of its portfolio securities, the fund will adjust the previous quoted prices to reflect what it believes to be the fair value of the securities as of the close of the NYSE. In deciding whether it is necessary to adjust quoted prices to reflect fair value, the fund reviews a variety of factors, including developments in foreign markets, the performance of U.S. securities markets, and the performance of instruments trading in U.S. markets that represent foreign securities and baskets of foreign securities. The fund may also fair value securities in other situations, such as when a particular foreign market is closed but the fund is open. The fund uses outside pricing services to provide it with quoted prices and information to evaluate or adjust those prices. The fund cannot predict how often it will use quoted prices and how often it will determine it necessary to adjust those prices to reflect fair value. As a means of evaluating its security valuation process, the fund routinely compares quoted prices, the next day’s opening prices in the same markets, and adjusted prices.

Actively traded equity securities listed on a domestic exchange generally are categorized in Level 1 of the fair value hierarchy. Non-U.S. equity securities generally are categorized in Level 2 of the fair value hierarchy despite the availability of quoted prices because, as described above, the fund evaluates and determines whether those quoted prices reflect fair value at the close of the NYSE or require adjustment. OTC Bulletin Board securities, certain preferred securities, and equity securities traded in inactive markets generally are categorized in Level 2 of the fair value hierarchy.

Debt securities generally are traded in the OTC market. Debt securities with remaining maturities of less than one year at the time of acquisition generally use amortized cost in local currency to approximate fair value. However, if amortized cost is deemed not to reflect fair value or the fund holds a significant amount of such securities with remaining maturities of more than 60 days, the securities are valued at prices furnished by dealers who make markets in such securities or by an independent pricing service. Generally, debt securities are categorized in Level 2 of the fair value hierarchy.

Investments in mutual funds are valued at the mutual fund’s closing NAV per share on the day of valuation and are categorized in Level 1 of the fair value hierarchy. Financial futures contracts are valued at closing settlement prices and are categorized in Level 1 of the fair value hierarchy. Assets and liabilities other than financial instruments, including short-term receivables and payables, are carried at cost, or estimated realizable value, if less, which approximates fair value.

Thinly traded financial instruments and those for which the above valuation procedures are inappropriate or are deemed not to reflect fair value are stated at fair value as determined in good faith by the Valuation Committee. The objective of any fair value pricing determination is to arrive at a price that could reasonably be expected from a current sale. Financial instruments fair valued by the Valuation Committee are primarily private placements, restricted securities, warrants, rights, and other securities that are not publicly traded.

Subject to oversight by the Board, the Valuation Committee regularly makes good faith judgments to establish and adjust the fair valuations of certain securities as events occur and circumstances warrant. For instance, in determining the fair value of an equity investment with limited market activity, such as a private placement or a thinly traded public company stock, the Valuation Committee considers a variety of factors, which may include, but are not limited to, the issuer’s business prospects, its financial standing and performance, recent investment transactions in the issuer, new rounds of financing, negotiated transactions of significant size between other investors in the company, relevant market valuations of peer companies, strategic events affecting the company, market liquidity for the issuer, and general economic conditions and events. In consultation with the investment and pricing teams, the Valuation Committee will determine an appropriate valuation technique based on available information, which may include both observable and unobservable inputs. The Valuation Committee typically will afford greatest weight to actual prices in arm’s length transactions, to the extent they represent orderly transactions between market participants, transaction information can be reliably obtained, and prices are deemed representative of fair value. However, the Valuation Committee may also consider other valuation methods such as market-based valuation multiples; a discount or premium from market value of a similar, freely traded security of the same issuer; or some combination. Fair value determinations are reviewed on a regular basis and updated as information becomes available, including actual purchase and sale transactions of the issue. Because any fair value determination involves a significant amount of judgment, there is a degree of subjectivity inherent in such pricing decisions, and fair value prices determined by the Valuation Committee could differ from those of other market participants. Depending on the relative significance of unobservable inputs, including the valuation technique(s) used, fair valued securities may be categorized in Level 2 or 3 of the fair value hierarchy.

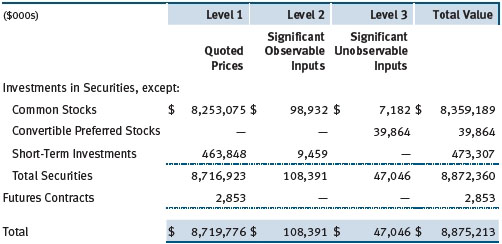

Valuation Inputs The following table summarizes the fund’s financial instruments, based on the inputs used to determine their fair values on June 30, 2016:

There were no material transfers between Levels 1 and 2 during the six months ended June 30, 2016.

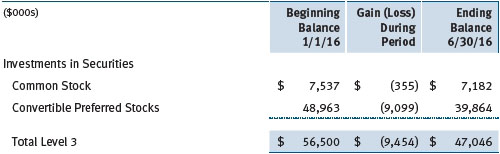

Following is a reconciliation of the fund’s Level 3 holdings for the six months ended June 30, 2016. Gain (loss) reflects both realized and change in unrealized gain/loss on Level 3 holdings during the period, if any, and is included on the accompanying Statement of Operations. The change in unrealized gain/loss on Level 3 instruments held at June 30, 2016, totaled $(9,454,000) for the six months ended June 30, 2016.

NOTE 3 - DERIVATIVE INSTRUMENTS

During the six months ended June 30, 2016, the fund invested in derivative instruments. As defined by GAAP, a derivative is a financial instrument whose value is derived from an underlying security price, foreign exchange rate, interest rate, index of prices or rates, or other variable; it requires little or no initial investment and permits or requires net settlement. The fund invests in derivatives only if the expected risks and rewards are consistent with its investment objectives, policies, and overall risk profile, as described in its prospectus and Statement of Additional Information. The fund may use derivatives for a variety of purposes, such as seeking to hedge against declines in principal value, increase yield, invest in an asset with greater efficiency and at a lower cost than is possible through direct investment, or to adjust credit exposure. The risks associated with the use of derivatives are different from, and potentially much greater than, the risks associated with investing directly in the instruments on which the derivatives are based. The fund at all times maintains sufficient cash reserves, liquid assets, or other SEC-permitted asset types to cover its settlement obligations under open derivative contracts.

The fund values its derivatives at fair value and recognizes changes in fair value currently in its results of operations. Accordingly, the fund does not follow hedge accounting, even for derivatives employed as economic hedges. Generally, the fund accounts for its derivatives on a gross basis. It does not offset the fair value of derivative liabilities against the fair value of derivative assets on its financial statements, nor does it offset the fair value of derivative instruments against the right to reclaim or obligation to return collateral.

As of June 30, 2016, the fund held equity futures with cumulative unrealized loss of $336,000; the value reflected on the accompanying Statement of Assets and Liabilities is the related unsettled variation margin.

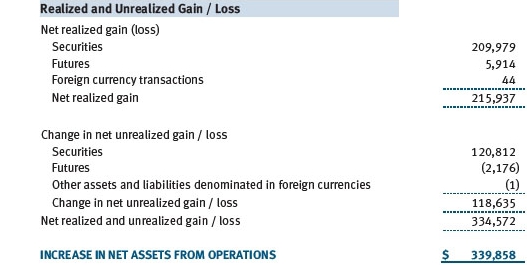

Additionally, during the six months ended June 30, 2016, the fund recognized $5,914,000 of realized gain on Futures and a $(2,176,000) change in unrealized gain/loss on Futures related to its investments in equity derivatives; such amounts are included on the accompanying Statement of Operations.

Counterparty Risk and Collateral The fund invests in exchange-traded or centrally cleared derivative contracts, such as futures, exchange-traded options, and centrally cleared swaps. Counterparty risk on such derivatives is minimal because the clearinghouse provides protection against counterparty defaults. For futures and centrally cleared swaps, the fund is required to deposit collateral in an amount equal to a certain percentage of the contract value (margin requirement), and the margin requirement must be maintained over the life of the contract. Each clearing broker, in its sole discretion, may adjust the margin requirements applicable to the fund.

Collateral may be in the form of cash or debt securities issued by the U.S. government or related agencies. Cash and currencies posted by the fund are reflected as cash deposits in the accompanying financial statements and generally are restricted from withdrawal by the fund; securities posted by the fund are so noted in the accompanying Portfolio of Investments; both remain in the fund’s assets. As of June 30, 2016, securities valued at $8,877,000 had been posted by the fund for exchange-traded and/or centrally cleared derivatives.

Futures Contracts The fund is subject to equity price risk in the normal course of pursuing its investment objectives and uses futures contracts to help manage such risk. The fund may enter into futures contracts to manage exposure to interest rates, security prices, foreign currencies, and credit quality; as an efficient means of adjusting exposure to all or part of a target market; to enhance income; as a cash management tool; or to adjust credit exposure. A futures contract provides for the future sale by one party and purchase by another of a specified amount of a specific underlying financial instrument at an agreed-upon price, date, time, and place. The fund currently invests only in exchange-traded futures, which generally are standardized as to maturity date, underlying financial instrument, and other contract terms. Payments are made or received by the fund each day to settle daily fluctuations in the value of the contract (variation margin), which reflect changes in the value of the underlying financial instrument. Variation margin is recorded as unrealized gain or loss until the contract is closed. The value of a futures contract included in net assets is the amount of unsettled variation margin; net variation margin receivable is reflected as an asset, and net variation margin payable is reflected as a liability on the accompanying Statement of Assets and Liabilities. Risks related to the use of futures contracts include possible illiquidity of the futures markets, contract prices that can be highly volatile and imperfectly correlated to movements in hedged security values, and potential losses in excess of the fund’s initial investment. During the six months ended June 30, 2016, the volume of the fund’s activity in futures, based on underlying notional amounts, was generally between 1% and 3% of net assets.

NOTE 4 - OTHER INVESTMENT TRANSACTIONS

Consistent with its investment objective, the fund engages in the following practices to manage exposure to certain risks and/or to enhance performance. The investment objective, policies, program, and risk factors of the fund are described more fully in the fund’s prospectus and Statement of Additional Information.

Restricted Securities The fund may invest in securities that are subject to legal or contractual restrictions on resale. Prompt sale of such securities at an acceptable price may be difficult and may involve substantial delays and additional costs.

Other Purchases and sales of portfolio securities other than short-term securities aggregated $1,307,678,000 and $988,716,000, respectively, for the six months ended June 30, 2016.

NOTE 5 - FEDERAL INCOME TAXES

No provision for federal income taxes is required since the fund intends to continue to qualify as a regulated investment company under Subchapter M of the Internal Revenue Code and distribute to shareholders all of its taxable income and gains. Distributions determined in accordance with federal income tax regulations may differ in amount or character from net investment income and realized gains for financial reporting purposes. Financial reporting records are adjusted for permanent book/tax differences to reflect tax character but are not adjusted for temporary differences. The amount and character of tax-basis distributions and composition of net assets are finalized at fiscal year-end; accordingly, tax-basis balances have not been determined as of the date of this report.

The fund intends to retain realized gains to the extent of available capital loss carryforwards. Net realized capital losses may be carried forward indefinitely to offset future realized capital gains. As of December 31, 2015, the fund had $21,000 of available capital loss carryforwards.

At June 30, 2016, the cost of investments for federal income tax purposes was $6,889,608,000. Net unrealized gain aggregated $1,982,416,000 at period-end, of which $2,512,432,000 related to appreciated investments and $530,016,000 related to depreciated investments.

NOTE 6 - RELATED PARTY TRANSACTIONS

The fund is managed by T. Rowe Price Associates, Inc. (Price Associates), a wholly owned subsidiary of T. Rowe Price Group, Inc. (Price Group). The investment management agreement between the fund and Price Associates provides for an annual investment management fee, which is computed daily and paid monthly. The fee consists of an individual fund fee, equal to 0.45% of the fund’s average daily net assets, and a group fee. The group fee rate is calculated based on the combined net assets of certain mutual funds sponsored by Price Associates (the group) applied to a graduated fee schedule, with rates ranging from 0.48% for the first $1 billion of assets to 0.270% for assets in excess of $500 billion. The fund’s group fee is determined by applying the group fee rate to the fund’s average daily net assets. At June 30, 2016, the effective annual group fee rate was 0.29%.

The I Class is subject to an operating expense limitation (I Class limit) pursuant to which Price Associates is contractually required to pay all operating expenses of the I Class, excluding management fees, interest, borrowing-related expenses, taxes, brokerage commissions, and extraordinary expenses, to the extent such operating expenses, on an annualized basis, exceed 0.05% of average net assets. This agreement will continue until April 30, 2018, and may be renewed, revised or revoked only with approval of the fund’s Board. The I Class is required to repay Price Associates for expenses previously paid to the extent the class’s net assets grow or expenses decline sufficiently to allow repayment without causing the class’s operating expenses to exceed the I Class limit. However, no repayment will be made more than three years after the date of a payment or waiver. For the six months ended June 30, 2016, the I Class operated below its expense limitation.

In addition, the fund has entered into service agreements with Price Associates and two wholly owned subsidiaries of Price Associates (collectively, Price). Price Associates provides certain accounting and administrative services to the fund. T. Rowe Price Services, Inc., provides shareholder and administrative services in its capacity as the fund’s transfer and dividend-disbursing agent. T. Rowe Price Retirement Plan Services, Inc., provides subaccounting and recordkeeping services for certain retirement accounts invested in the Investor Class and I Class. For the six months ended June 30, 2016, expenses incurred pursuant to these service agreements were $23,000 for Price Associates; $793,000 for T. Rowe Price Services, Inc.; and $733,000 for T. Rowe Price Retirement Plan Services, Inc. The total amount payable at period-end pursuant to these service agreements is reflected as Due to Affiliates in the accompanying financial statements, if any.

Additionally, the fund is one of several mutual funds in which certain college savings plans managed by Price Associates may invest. As approved by the fund’s Board of Directors, shareholder servicing costs associated with each college savings plan are borne by the fund in proportion to the average daily value of its shares owned by the college savings plan. For the six months ended June 30, 2016, the fund was charged $211,000 for shareholder servicing costs related to the college savings plans, of which $167,000 was for services provided by Price. The amount payable at period-end pursuant to this agreement is reflected as Due to Affiliates in the accompanying financial statements. At June 30, 2016, approximately 2% of the outstanding shares of the Investor Class were held by college savings plans.

The fund is also one of several mutual funds sponsored by Price Associates (underlying Price funds) in which the T. Rowe Price Retirement Funds (Retirement Funds) and T. Rowe Price Target Funds (Target Funds) may invest. Neither the Retirement Funds nor the Target Funds invest in the underlying Price funds for the purpose of exercising management or control. Pursuant to a special servicing agreement, expenses associated with the operation of the Retirement Funds are borne by each underlying Price fund to the extent of estimated savings to it and in proportion to the average daily value of its shares owned by the Retirement Funds. Prior to February 1, 2016, the Target Funds were subject to the same special servicing agreement; thus expenses associated with the operation of the Target Funds prior to that date were borne by the underlying Price Funds. Effective February 1, 2016, expenses associated with the operation of the Target Funds are borne by the Target Funds. Expenses allocated under the special servicing agreement are reflected as shareholder servicing expense in the accompanying financial statements. For the six months ended June 30, 2016, the fund was allocated $1,589,000 of Retirement Funds’ and Target Funds’ expenses, of which $651,000 related to services provided by Price. At period-end, the amount payable to Price pursuant to this agreement is reflected as Due to Affiliates in the accompanying financial statements. At June 30, 2016, approximately 27% of the outstanding shares of the Investor Class were held by the Retirement Funds and approximately 6% of the outstanding shares of the I Class were held by the Target Funds.

Mutual funds, trusts, and other accounts managed by Price Associates or its affiliates (collectively, Price funds and accounts) may invest in the fund; however, no Price fund or account may invest for the purpose of exercising management or control over the fund. At June 30, 2016, approximately 27% of the I Class’s outstanding shares were held by Price funds and accounts.

The fund may invest in the T. Rowe Price Reserve Investment Fund, the T. Rowe Price Government Reserve Investment Fund, or the T. Rowe Price Short-Term Reserve Fund (collectively, the Price Reserve Investment Funds), open-end management investment companies managed by Price Associates and considered affiliates of the fund. The Price Reserve Investment Funds are offered as short-term investment options to mutual funds, trusts, and other accounts managed by Price Associates or its affiliates and are not available for direct purchase by members of the public. The Price Reserve Investment Funds pay no investment management fees.

The fund may participate in securities purchase and sale transactions with other funds or accounts advised by Price Associates (cross trades), in accordance with procedures adopted by the fund’s Board and Securities and Exchange Commission rules, which require, among other things, that such purchase and sale cross trades be effected at the independent current market price of the security. During the six months ended June 30, 2016, the aggregate value of purchases and sales cross trades with other funds or accounts advised by Price Associates was less than 1% of the fund’s net assets as of June 30, 2016.

| Information on Proxy Voting Policies, Procedures, and Records |

A description of the policies and procedures used by T. Rowe Price funds and portfolios to determine how to vote proxies relating to portfolio securities is available in each fund’s Statement of Additional Information. You may request this document by calling 1-800-225-5132 or by accessing the SEC’s website, sec.gov.

The description of our proxy voting policies and procedures is also available on our corporate website. To access it, please visit the following Web page

https://www3.troweprice.com/usis/corporate/en/utility/policies.html

and scroll down to the section near the bottom of the page that says, “Proxy Voting Policies.” Click on the Proxy Voting Policies link in the shaded box.

Each fund’s most recent annual proxy voting record is available on our website and through the SEC’s website. To access it through T. Rowe Price, visit the website location shown above, and scroll down to the section near the bottom of the page that says, “Proxy Voting Records.” Click on the Proxy Voting Records link in the shaded box.

| How to Obtain Quarterly Portfolio Holdings |

The fund files a complete schedule of portfolio holdings with the Securities and Exchange Commission for the first and third quarters of each fiscal year on Form N-Q. The fund’s Form N-Q is available electronically on the SEC’s website (sec.gov); hard copies may be reviewed and copied at the SEC’s Public Reference Room, 100 F St. N.E., Washington, DC 20549. For more information on the Public Reference Room, call 1-800-SEC-0330.

| Approval of Investment Management Agreement |

On March 11, 2016, the fund’s Board of Directors (Board), including a majority of the fund’s independent directors, approved the continuation of the investment management agreement (Advisory Contract) between the fund and its investment advisor, T. Rowe Price Associates, Inc. (Advisor). In connection with its deliberations, the Board requested, and the Advisor provided, such information as the Board (with advice from independent legal counsel) deemed reasonably necessary. The Board considered a variety of factors in connection with its review of the Advisory Contract, also taking into account information provided by the Advisor during the course of the year, as discussed below:

Services Provided by the

Advisor

The Board considered the nature,

quality, and extent of the services provided to the fund by the Advisor. These

services included, but were not limited to, directing the fund’s investments in

accordance with its investment program and the overall management of the fund’s

portfolio, as well as a variety of related activities such as financial,

investment operations, and administrative services; compliance; maintaining the

fund’s records and registrations; and shareholder communications. The Board also

reviewed the background and experience of the Advisor’s senior management team

and investment personnel involved in the management of the fund, as well as the

Advisor’s compliance record. The Board concluded that it was satisfied with the

nature, quality, and extent of the services provided by the Advisor.

Investment Performance of the

Fund

The Board reviewed the fund’s

three-month, one-year, and year-by-year returns, as well as the fund’s average

annualized total returns over the 3-, 5-, and 10-year periods, and compared

these returns with a wide variety of comparable performance measures and market

data, including those supplied by Lipper and Morningstar, which are independent

providers of mutual fund data.

On the basis of this evaluation and the Board’s ongoing review of investment results, and factoring in the relative market conditions during certain of the performance periods, the Board concluded that the fund’s performance was satisfactory.

Costs, Benefits, Profits, and Economies

of Scale

The Board reviewed detailed

information regarding the revenues received by the Advisor under the Advisory

Contract and other benefits that the Advisor (and its affiliates) may have

realized from its relationship with the fund, including any research received

under “soft dollar” agreements and commission-sharing arrangements with

broker-dealers. The Board considered that the Advisor may receive some benefit

from soft-dollar arrangements pursuant to which research is received from

broker-dealers that execute the applicable fund’s portfolio transactions. The

Board received information on the estimated costs incurred and profits realized

by the Advisor from managing T. Rowe Price mutual funds. The Board also reviewed

estimates of the profits realized from managing the fund in particular, and the

Board concluded that the Advisor’s profits were reasonable in light of the

services provided to the fund.

The Board also considered whether the fund benefits under the fee levels set forth in the Advisory Contract from any economies of scale realized by the Advisor. Under the Advisory Contract, the fund pays a fee to the Advisor for investment management services composed of two components—a group fee rate based on the combined average net assets of most of the T. Rowe Price mutual funds (including the fund) that declines at certain asset levels and an individual fund fee rate based on the fund’s average daily net assets—and the fund pays its own expenses of operations (subject to an expense limitation on operating expenses with respect to the I Class). The Board concluded that the advisory fee structure for the fund continued to provide for a reasonable sharing of benefits from any economies of scale with the fund’s investors.

Fees

The Board was provided with information regarding industry trends in

management fees and expenses, and the Board reviewed the fund’s management fee

rate, operating expenses, and total expense ratio (for the Investor Class,

Advisor Class, and I Class) in comparison with fees and expenses of other

comparable funds based on information and data supplied by Lipper. The

information provided to the Board indicated that the fund’s management fee rate

was above the median for certain groups of comparable funds and at or below the

median for other groups of comparable funds. The information also indicated that

the total expense ratio for the Investor Class was above the median for certain

groups of comparable funds and at or below the median for other groups of

comparable funds, and the total expense ratio for the Advisor Class and I Class

was at or below the median for comparable funds.

The Board also reviewed the fee schedules for institutional accounts (including subadvised mutual funds) and private accounts with similar mandates that are advised or subadvised by the Advisor and its affiliates. Management provided the Board with information about the Advisor’s responsibilities and services provided to subadvisory and other institutional account clients, including information about how the requirements and economics of the institutional business differ from those of the Advisor’s proprietary mutual fund business. The Board considered information showing that the Advisor’s proprietary mutual fund business is generally more complex from a business and compliance perspective than its institutional account business and considered various other relevant factors, including the broader scope of operations and oversight, more extensive shareholder communication infrastructure, greater asset flows, heightened business risks, and differences in applicable laws and regulations associated with the Advisor’s proprietary mutual fund business. In assessing the reasonableness of the fund’s management fee rate, the Board considered the differences in the nature of the services required for the Advisor to manage its proprietary mutual fund business versus managing a discrete pool of assets as a subadvisor to another institution’s mutual fund or for another institutional account and the degree to which the Advisor performs significant additional services and assumes greater risk in managing the fund and other T. Rowe Price mutual funds than it does for institutional account clients.

On the basis of the information provided and the factors considered, the Board concluded that the fees paid by the fund under the Advisory Contract are reasonable.

Approval of the Advisory

Contract

As noted, the Board approved the

continuation of the Advisory Contract. No single factor was considered in

isolation or to be determinative to the decision. Rather, the Board concluded,

in light of a weighting and balancing of all factors considered, that it was in

the best interests of the fund and its shareholders for the Board to approve the

continuation of the Advisory Contract (including the fees to be charged for

services thereunder). The independent directors were advised throughout the

process by independent legal counsel.

Item 2. Code of Ethics.

A code of ethics, as defined in Item 2 of Form N-CSR, applicable to its principal executive officer, principal financial officer, principal accounting officer or controller, or persons performing similar functions is filed as an exhibit to the registrant’s annual Form N-CSR. No substantive amendments were approved or waivers were granted to this code of ethics during the registrant’s most recent fiscal half-year.

Item 3. Audit Committee Financial Expert.

Disclosure required in registrant’s annual Form N-CSR.

Item 4. Principal Accountant Fees and Services.

Disclosure required in registrant’s annual Form N-CSR.

Item 5. Audit Committee of Listed Registrants.

Not applicable.

Item 6. Investments.

(a) Not applicable. The complete schedule of investments is included in Item 1 of this Form N-CSR.

(b) Not applicable.

Item 7. Disclosure of Proxy Voting Policies and Procedures for Closed-End Management Investment Companies.

Not applicable.

Item 8. Portfolio Managers of Closed-End Management Investment Companies.

Not applicable.

Item 9. Purchases of Equity Securities by Closed-End Management Investment Company and Affiliated Purchasers.

Not applicable.

Item 10. Submission of Matters to a Vote of Security Holders.

Not applicable.

Item 11. Controls and Procedures.

(a) The registrant’s principal executive officer and principal financial officer have evaluated the registrant’s disclosure controls and procedures within 90 days of this filing and have concluded that the registrant’s disclosure controls and procedures were effective, as of that date, in ensuring that information required to be disclosed by the registrant in this Form N-CSR was recorded, processed, summarized, and reported timely.

(b) The registrant’s principal executive officer and principal financial officer are aware of no change in the registrant’s internal control over financial reporting that occurred during the registrant’s second fiscal quarter covered by this report that has materially affected, or is reasonably likely to materially affect, the registrant’s internal control over financial reporting.

Item 12. Exhibits.

(a)(1) The registrant’s code of ethics pursuant to Item 2 of Form N-CSR is filed with the registrant’s annual Form N-CSR.

(2) Separate certifications by the registrant's principal executive officer and principal financial officer, pursuant to Section 302 of the Sarbanes-Oxley Act of 2002 and required by Rule 30a-2(a) under the Investment Company Act of 1940, are attached.

(3) Written solicitation to repurchase securities issued by closed-end companies: not applicable.

(b) A certification by the registrant's principal executive officer and principal financial officer, pursuant to Section 906 of the Sarbanes-Oxley Act of 2002 and required by Rule 30a-2(b) under the Investment Company Act of 1940, is attached.

SIGNATURES

Pursuant to the requirements of the Securities Exchange Act of 1934 and the Investment Company Act of 1940, the registrant has duly caused this report to be signed on its behalf by the undersigned, thereunto duly authorized.

T. Rowe Price Small-Cap Stock Fund, Inc.

| By | /s/ Edward C. Bernard | |

| Edward C. Bernard | ||

| Principal Executive Officer | ||

| Date August 17, 2016 | ||

Pursuant to the

requirements of the Securities Exchange Act of 1934 and the Investment Company

Act of 1940, this report has been signed below by the following persons on

behalf of the registrant and in the capacities and on the dates indicated.

| By | /s/ Edward C. Bernard | |

| Edward C. Bernard | ||

| Principal Executive Officer | ||

| Date August 17, 2016 | ||

| By | /s/ Catherine D. Mathews | |

| Catherine D. Mathews | ||

| Principal Financial Officer | ||

| Date August 17, 2016 | ||