UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-04085

Fidelity Income Fund

(Exact name of registrant as specified in charter)

245 Summer St., Boston, MA 02210

(Address of principal executive offices) (Zip code)

Cynthia Lo Bessette, Secretary

245 Summer St.

Boston, Massachusetts 02210

(Name and address of agent for service)

Registrant's telephone number, including area code:

617-563-7000

Date of fiscal year end: | August 31 |

Date of reporting period: | February 29, 2020 |

Item 1.

Reports to Stockholders

Fidelity® Government Income Fund

Semi-Annual Report

February 29, 2020

Includes Fidelity and Fidelity Advisor share classes

See the inside front cover for important information about access to your fund’s shareholder reports.

Beginning on January 1, 2021, as permitted by regulations adopted by the Securities and Exchange Commission, paper copies of a fund’s shareholder reports will no longer be sent by mail, unless you specifically request paper copies of the reports from the fund or from your financial intermediary, such as a financial advisor, broker-dealer or bank. Instead, the reports will be made available on a website, and you will be notified by mail each time a report is posted and provided with a website link to access the report.

If you already elected to receive shareholder reports electronically, you will not be affected by this change and you need not take any action. You may elect to receive shareholder reports and other communications from a fund electronically, by contacting your financial intermediary. For Fidelity customers, visit Fidelity's web site or call Fidelity using the contact information listed below.

You may elect to receive all future reports in paper free of charge. If you wish to continue receiving paper copies of your shareholder reports, you may contact your financial intermediary or, if you are a Fidelity customer, visit Fidelity’s website, or call Fidelity at the applicable toll-free number listed below. Your election to receive reports in paper will apply to all funds held with the fund complex/your financial intermediary.

| Account Type | Website | Phone Number |

| Brokerage, Mutual Fund, or Annuity Contracts: | fidelity.com/mailpreferences | 1-800-343-3548 |

| Employer Provided Retirement Accounts: | netbenefits.fidelity.com/preferences (choose 'no' under Required Disclosures to continue to print) | 1-800-343-0860 |

| Advisor Sold Accounts Serviced Through Your Financial Intermediary: | Contact Your Financial Intermediary | Your Financial Intermediary's phone number |

| Advisor Sold Accounts Serviced by Fidelity: | institutional.fidelity.com | 1-877-208-0098 |

Contents

|

Board Approval of Investment Advisory Contracts and Management Fees | |

To view a fund's proxy voting guidelines and proxy voting record for the 12-month period ended June 30, visit http://www.fidelity.com/proxyvotingresults or visit the Securities and Exchange Commission's (SEC) web site at http://www.sec.gov.

You may also call 1-800-544-8544 if you’re an individual investing directly with Fidelity, call 1-800-835-5092 if you’re a plan sponsor or participant with Fidelity as your recordkeeper or call 1-877-208-0098 on institutional accounts or if you’re an advisor or invest through one to request a free copy of the proxy voting guidelines.

Standard & Poor's, S&P and S&P 500 are registered service marks of The McGraw-Hill Companies, Inc. and have been licensed for use by Fidelity Distributors Corporation.

Other third-party marks appearing herein are the property of their respective owners.

All other marks appearing herein are registered or unregistered trademarks or service marks of FMR LLC or an affiliated company. © 2020 FMR LLC. All rights reserved.

This report and the financial statements contained herein are submitted for the general information of the shareholders of the Fund. This report is not authorized for distribution to prospective investors in the Fund unless preceded or accompanied by an effective prospectus.

A fund files its complete schedule of portfolio holdings with the SEC for the first and third quarters of each fiscal year on Form N-PORT. Forms N-PORT are available on the SEC’s web site at http://www.sec.gov. A fund's Forms N-PORT may be reviewed and copied at the SEC’s Public Reference Room in Washington, DC. Information regarding the operation of the SEC's Public Reference Room may be obtained by calling 1-800-SEC-0330.

For a complete list of a fund's portfolio holdings, view the most recent holdings listing, semiannual report, or annual report on Fidelity's web site at http://www.fidelity.com, http://www.institutional.fidelity.com, or http://www.401k.com, as applicable.

NOT FDIC INSURED •MAY LOSE VALUE •NO BANK GUARANTEE

Neither the Fund nor Fidelity Distributors Corporation is a bank.

Note to Shareholders:

Early in 2020, the outbreak and spread of a new coronavirus emerged as a public health emergency that had a major influence on financial markets, primarily based on its impact on the global economy and corporate earnings. The virus causes a respiratory disease known as COVID-19. On March 11, the World Health Organization declared the COVID-19 outbreak a pandemic, citing sustained risk of further global spread.

In the weeks following the end of this reporting period, as the crisis worsened, we witnessed an escalating human tragedy with wide-scale social and economic consequences from coronavirus-containment measures. The outbreak of COVID-19 prompted a number of measures to limit the spread, including travel and border restrictions, quarantines, and restrictions on large gatherings. In turn, these resulted in lower consumer activity, diminished demand for a wide range of products and services, disruption in manufacturing and supply chains, and – given the wide variability in outcomes regarding the outbreak – significant market uncertainty and volatility. Amid the turmoil, the U.S. government took unprecedented action – in concert with the U.S. Federal Reserve and central banks around the world – to help support consumers, businesses, and the broader economy, and to limit disruption to the financial system.

The situation continues to unfold, and the extent and duration of its impact on financial markets and the economy remain highly uncertain. Extreme events such as the coronavirus crisis are “exogenous shocks” that can have significant adverse effects on mutual funds and their investments. Although multiple asset classes may be affected by market disruption, the duration and impact may not be the same for all types of assets.

Fidelity is committed to helping you stay informed amid news about COVID-19 and during increased market volatility, and we’re taking extra steps to be responsive to customer needs. We encourage you to visit our websites, where we offer ongoing updates, commentary, and analysis on the markets and our funds.

Investment Summary (Unaudited)

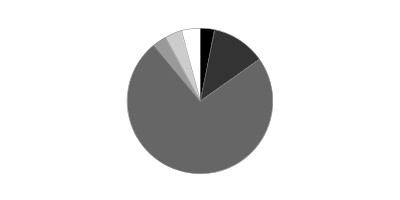

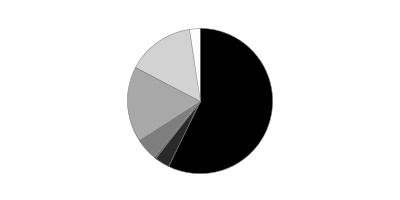

The information in the following tables is based on the combined investments of the Fund and its pro-rata share of the investments of Fidelity's Fixed-Income Central Funds.Coupon Distribution as of February 29, 2020

| % of fund's investments | |

| Zero coupon bonds | 0.0 |

| 1 - 1.99% | 18.8 |

| 2 - 2.99% | 30.7 |

| 3 - 3.99% | 21.2 |

| 4 - 4.99% | 12.9 |

| 5 - 5.99% | 2.6 |

| 6 - 6.99% | 0.2 |

| 7% and above | 0.0 |

Coupon distribution shows the range of stated interest rates on the fund's investments, excluding short-term investments.

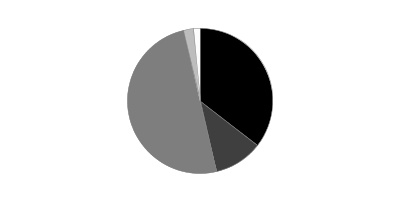

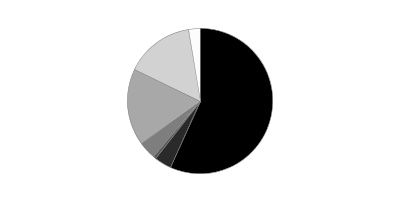

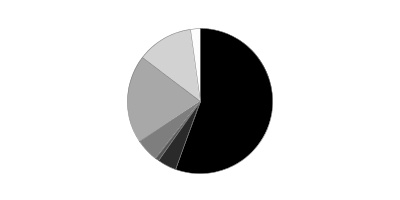

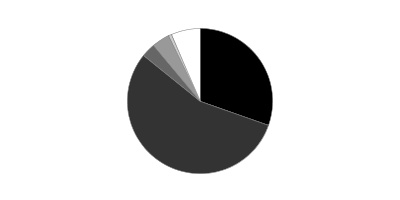

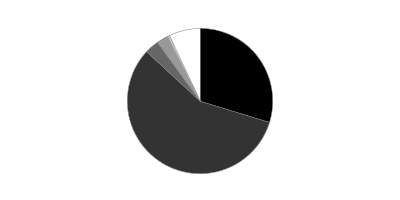

Asset Allocation (% of fund's net assets)

| As of February 29, 2020*,**,*** | ||

| Mortgage Securities | 37.1% | |

| CMOs and Other Mortgage Related Securities | 11.3% | |

| U.S. Treasury Obligations | 52.4% | |

| U.S. Government Agency Obligations† | 2.3% | |

| Foreign Government & Government Agency Obligations | 1.5% | |

| Short-Term Investments and Net Other Assets (Liabilities)†† | (4.6)% | |

* Foreign investments - 1.5%

** Futures and Swaps - 15.2%

*** Written options - (9.9)%

† Includes NCUA Guaranteed Notes

†† Short-Term Investments and Net Other Assets (Liabilities) are not included in the pie chart

An unaudited holdings listing for the Fund, which presents direct holdings as well as the pro-rata share of any securities and other investments held indirectly through its investment in underlying non-money market Fidelity Central Funds, is available at fidelity.com and/or institutional.fidelity.com, as applicable.

Percentages in the above tables are adjusted for the effect of TBA Sale Commitments.

Percentages shown as 0.0% may reflect amounts less than 0.05%.

Schedule of Investments February 29, 2020 (Unaudited)

Showing Percentage of Net Assets

| U.S. Government and Government Agency Obligations - 54.7% | |||

| Principal Amount (000s) | Value (000s) | ||

| U.S. Government Agency Obligations - 0.2% | |||

| Tennessee Valley Authority: | |||

| 5.25% 9/15/39 | $2,235 | $3,369 | |

| 5.375% 4/1/56 | 2,737 | 4,837 | |

| 8,206 | |||

| U.S. Treasury Obligations - 52.4% | |||

| U.S. Treasury Bonds: | |||

| 2.375% 11/15/49 | 50,321 | 58,740 | |

| 2.5% 2/15/45 (a)(b)(c) | 141,861 | 165,772 | |

| 2.875% 5/15/49 | 4,458 | 5,712 | |

| 3% 2/15/49 | 100,124 | 130,990 | |

| 4.75% 2/15/37 (a)(b) | 55,003 | 83,386 | |

| U.S. Treasury Notes: | |||

| 1.125% 2/28/27 | 9,286 | 9,335 | |

| 1.375% 1/31/22 (d) | 154,000 | 155,366 | |

| 1.5% 9/30/21 | 92,347 | 93,108 | |

| 1.5% 9/30/24 | 13,631 | 13,984 | |

| 1.5% 10/31/24 | 49,500 | 50,801 | |

| 1.5% 1/31/27 | 171,050 | 176,226 | |

| 1.5% 2/15/30 | 29,700 | 30,712 | |

| 1.625% 11/15/22 | 12,773 | 13,023 | |

| 1.625% 9/30/26 | 14,543 | 15,092 | |

| 1.75% 10/31/20 | 1,915 | 1,921 | |

| 1.75% 7/31/21 | 19,823 | 20,031 | |

| 1.75% 7/31/24 | 1,720 | 1,781 | |

| 1.75% 11/15/29 | 8,300 | 8,764 | |

| 1.875% 7/31/22 | 37,445 | 38,320 | |

| 2% 8/15/25 | 9,743 | 10,275 | |

| 2.125% 12/31/22 | 32,217 | 33,332 | |

| 2.125% 3/31/24 | 88,361 | 92,648 | |

| 2.125% 7/31/24 | 59,641 | 62,744 | |

| 2.125% 5/15/25 | 11,929 | 12,640 | |

| 2.25% 7/31/21 | 5,589 | 5,688 | |

| 2.25% 4/30/24 | 2,843 | 2,997 | |

| 2.25% 12/31/24 | 6,135 | 6,516 | |

| 2.25% 3/31/26 | 928 | 996 | |

| 2.375% 4/15/21 | 49,955 | 50,681 | |

| 2.5% 12/31/20 | 46,107 | 46,622 | |

| 2.5% 1/31/21 | 60,329 | 61,088 | |

| 2.5% 2/28/21 | 47,678 | 48,342 | |

| 2.5% 1/15/22 | 52,113 | 53,625 | |

| 2.5% 2/28/26 | 68,418 | 74,381 | |

| 2.625% 6/30/23 | 5,027 | 5,312 | |

| 2.625% 12/31/23 | 62,484 | 66,512 | |

| 2.625% 2/15/29 | 30,872 | 34,836 | |

| 2.875% 11/30/25 | 25,337 | 28,010 | |

| 3.125% 11/15/28 | 14,449 | 16,869 | |

| 1,787,178 | |||

| Other Government Related - 2.1% | |||

| National Credit Union Administration Guaranteed Notes Series 2010-A1 Class A, 1 month U.S. LIBOR + 0.350% 2.0196% 12/7/20 (NCUA Guaranteed) (e)(f) | 1,433 | 1,433 | |

| National Credit Union Administration Guaranteed Notes Master Trust 3.45% 6/12/21 (NCUA Guaranteed) | 58,911 | 60,695 | |

| Private Export Funding Corp. Secured 1.75% 11/15/24 | 8,660 | 8,901 | |

| 71,029 | |||

| TOTAL U.S. GOVERNMENT AND GOVERNMENT AGENCY OBLIGATIONS | |||

| (Cost $1,729,577) | 1,866,413 | ||

| U.S. Government Agency - Mortgage Securities - 11.3% | |||

| Fannie Mae - 1.0% | |||

| 12 month U.S. LIBOR + 1.480% 4.221% 7/1/34 (e)(f) | 40 | 42 | |

| 12 month U.S. LIBOR + 1.520% 3.798% 3/1/36 (e)(f) | 80 | 84 | |

| 12 month U.S. LIBOR + 1.550% 3.946% 2/1/44 (e)(f) | 65 | 68 | |

| 12 month U.S. LIBOR + 1.550% 4.345% 6/1/36 (e)(f) | 33 | 34 | |

| 12 month U.S. LIBOR + 1.550% 4.428% 5/1/44 (e)(f) | 140 | 144 | |

| 12 month U.S. LIBOR + 1.560% 4.69% 3/1/37 (e)(f) | 83 | 86 | |

| 12 month U.S. LIBOR + 1.570% 3.868% 2/1/44 (e)(f) | 83 | 86 | |

| 12 month U.S. LIBOR + 1.570% 4.445% 5/1/44 (e)(f) | 43 | 44 | |

| 12 month U.S. LIBOR + 1.580% 3.592% 1/1/44 (e)(f) | 79 | 82 | |

| 12 month U.S. LIBOR + 1.580% 4.705% 4/1/44 (e)(f) | 100 | 103 | |

| 12 month U.S. LIBOR + 1.590% 4.534% 4/1/44 (e)(f) | 283 | 293 | |

| 12 month U.S. LIBOR + 1.660% 4.184% 11/1/36 (e)(f) | 22 | 24 | |

| 12 month U.S. LIBOR + 1.710% 4.588% 6/1/42 (e)(f) | 56 | 58 | |

| 12 month U.S. LIBOR + 1.750% 3.941% 3/1/40 (e)(f) | 348 | 365 | |

| 12 month U.S. LIBOR + 1.750% 4.075% 7/1/35 (e)(f) | 50 | 52 | |

| 12 month U.S. LIBOR + 1.800% 3.813% 1/1/42 (e)(f) | 181 | 189 | |

| 12 month U.S. LIBOR + 1.800% 4.498% 7/1/41 (e)(f) | 87 | 91 | |

| 12 month U.S. LIBOR + 1.810% 4.068% 9/1/41 (e)(f) | 31 | 32 | |

| 12 month U.S. LIBOR + 1.810% 4.388% 2/1/42 (e)(f) | 173 | 181 | |

| 12 month U.S. LIBOR + 1.810% 4.537% 7/1/41 (e)(f) | 50 | 52 | |

| 12 month U.S. LIBOR + 1.830% 3.907% 10/1/41 (e)(f) | 27 | 28 | |

| 12 month U.S. LIBOR + 1.850% 4.567% 5/1/36 (e)(f) | 28 | 29 | |

| 6 month U.S. LIBOR + 1.470% 3.553% 10/1/33 (e)(f) | 28 | 29 | |

| 6 month U.S. LIBOR + 1.510% 3.449% 2/1/33 (e)(f) | 31 | 32 | |

| 6 month U.S. LIBOR + 1.530% 3.553% 3/1/35 (e)(f) | 38 | 40 | |

| 6 month U.S. LIBOR + 1.530% 3.687% 12/1/34 (e)(f) | 45 | 47 | |

| 6 month U.S. LIBOR + 1.550% 3.713% 10/1/33 (e)(f) | 16 | 16 | |

| 6 month U.S. LIBOR + 1.560% 3.44% 7/1/35 (e)(f) | 23 | 24 | |

| U.S. TREASURY 1 YEAR INDEX + 2.200% 4.833% 3/1/35 (e)(f) | 15 | 16 | |

| U.S. TREASURY 1 YEAR INDEX + 2.290% 4.263% 10/1/33 (e)(f) | 43 | 45 | |

| 3% 1/1/28 to 6/1/34 | 10,438 | 10,905 | |

| 3.5% 7/1/32 to 10/1/34 | 11,750 | 12,415 | |

| 4% 5/1/29 | 3,594 | 3,781 | |

| 4.5% 11/1/25 | 1,316 | 1,375 | |

| 6% to 6% 1/1/34 to 6/1/36 | 2,418 | 2,825 | |

| 6.5% 3/1/22 to 5/1/27 | 101 | 111 | |

| 33,828 | |||

| Freddie Mac - 0.8% | |||

| 12 month U.S. LIBOR + 1.750% 4.007% 9/1/41 (e)(f) | 433 | 452 | |

| 12 month U.S. LIBOR + 1.870% 4.376% 10/1/42 (e)(f) | 224 | 235 | |

| 12 month U.S. LIBOR + 1.870% 4.817% 4/1/41 (e)(f) | 22 | 23 | |

| 12 month U.S. LIBOR + 1.880% 3.838% 10/1/41 (e)(f) | 577 | 602 | |

| 12 month U.S. LIBOR + 1.880% 4.13% 9/1/41 (e)(f) | 35 | 36 | |

| 12 month U.S. LIBOR + 1.910% 4.66% 6/1/41 (e)(f) | 38 | 40 | |

| 12 month U.S. LIBOR + 1.910% 4.734% 6/1/41 (e)(f) | 75 | 79 | |

| 12 month U.S. LIBOR + 1.910% 4.785% 5/1/41 (e)(f) | 54 | 57 | |

| 12 month U.S. LIBOR + 1.910% 4.813% 5/1/41 (e)(f) | 66 | 69 | |

| 12 month U.S. LIBOR + 2.040% 4.784% 7/1/36 (e)(f) | 162 | 170 | |

| 12 month U.S. LIBOR + 2.060% 4.723% 3/1/33 (e)(f) | 4 | 4 | |

| 6 month U.S. LIBOR + 1.740% 3.83% 5/1/37 (e)(f) | 42 | 44 | |

| 6 month U.S. LIBOR + 2.680% 4.873% 10/1/35 (e)(f) | 22 | 24 | |

| U.S. TREASURY 1 YEAR INDEX + 2.310% 3.91% 2/1/36 (e)(f) | 3 | 3 | |

| U.S. TREASURY 1 YEAR INDEX + 2.540% 4.956% 7/1/35 (e)(f) | 353 | 371 | |

| 3% 4/1/33 to 11/1/33 | 22,352 | 23,382 | |

| 3.5% 7/1/32 | 2,189 | 2,311 | |

| 6% 1/1/24 | 265 | 279 | |

| 28,181 | |||

| Ginnie Mae - 6.6% | |||

| 6% 6/15/36 | 2,072 | 2,391 | |

| 3% 3/1/50 (g) | 40,000 | 41,329 | |

| 3% 3/20/50 | 24,750 | 25,631 | |

| 3% 4/1/50 (g) | 4,800 | 4,954 | |

| 3% 4/1/50 (g) | 2,500 | 2,580 | |

| 3% 4/1/50 (g) | 6,550 | 6,761 | |

| 3% 4/1/50 (g) | 10,900 | 11,251 | |

| 3.5% 3/1/50 (g) | 12,200 | 12,639 | |

| 3.5% 3/1/50 (g) | 9,900 | 10,256 | |

| 3.5% 3/1/50 (g) | 5,300 | 5,491 | |

| 4% 3/20/47 to 11/20/48 | 34,923 | 36,827 | |

| 4.494% 2/20/62 (e)(h) | 175 | 176 | |

| 4.5% 6/20/48 | 61,655 | 65,370 | |

| 4.758% 2/20/62 (e)(h) | 12 | 12 | |

| 5.044% 1/20/62 (e)(h) | 183 | 184 | |

| 5.47% 8/20/59 (e)(h) | 5 | 5 | |

| 225,857 | |||

| Uniform Mortgage Backed Securities - 2.9% | |||

| 3% 3/1/50 (g) | 14,000 | 14,417 | |

| 3% 3/1/50 (g) | 73,600 | 75,792 | |

| 3% 3/1/50 (g) | 8,300 | 8,547 | |

| 98,756 | |||

| TOTAL U.S. GOVERNMENT AGENCY - MORTGAGE SECURITIES | |||

| (Cost $381,867) | 386,622 | ||

| Collateralized Mortgage Obligations - 9.5% | |||

| U.S. Government Agency - 9.5% | |||

| Fannie Mae: | |||

| floater: | |||

| Series 2001-38 Class QF, 1 month U.S. LIBOR + 0.980% 2.6068% 8/25/31 (e)(f) | 40 | 40 | |

| Series 2002-49 Class FB, 1 month U.S. LIBOR + 0.600% 2.2585% 11/18/31 (e)(f) | 39 | 39 | |

| Series 2002-60 Class FV, 1 month U.S. LIBOR + 1.000% 2.6268% 4/25/32 (e)(f) | 16 | 17 | |

| Series 2002-75 Class FA, 1 month U.S. LIBOR + 1.000% 2.6268% 11/25/32 (e)(f) | 34 | 34 | |

| Series 2010-15 Class FJ, 1 month U.S. LIBOR + 0.930% 2.5568% 6/25/36 (e)(f) | 2,629 | 2,671 | |

| planned amortization class: | |||

| Series 2005-19 Class PA, 5.5% 7/25/34 | 64 | 64 | |

| Series 2005-64 Class PX, 5.5% 6/25/35 | 502 | 538 | |

| Series 2005-68 Class CZ, 5.5% 8/25/35 | 2,239 | 2,581 | |

| Series 2006-45 Class OP 6/25/36 (i) | 355 | 329 | |

| Series 2010-118 Class PB, 4.5% 10/25/40 | 2,909 | 3,230 | |

| Series 2012-149: | |||

| Class DA, 1.75% 1/25/43 | 483 | 487 | |

| Class GA, 1.75% 6/25/42 | 508 | 511 | |

| sequential payer: | |||

| Series 2003-117 Class MD, 5% 12/25/23 | 255 | 265 | |

| Series 2004-91 Class Z, 5% 12/25/34 | 2,413 | 2,699 | |

| Series 2005-117 Class JN, 4.5% 1/25/36 | 150 | 164 | |

| Series 2005-14 Class ZB, 5% 3/25/35 | 767 | 858 | |

| Series 2006-72 Class CY, 6% 8/25/26 | 1,301 | 1,403 | |

| Series 2009-59 Class HB, 5% 8/25/39 | 1,034 | 1,157 | |

| Series 2010-139 Class NI, 4.5% 2/25/40 (j) | 1,177 | 84 | |

| Series 2010-39 Class FG, 1 month U.S. LIBOR + 0.920% 2.5468% 3/25/36 (e)(f) | 1,668 | 1,706 | |

| Series 2010-97 Class CI, 4.5% 8/25/25 (j) | 58 | 0 | |

| Series 2012-27 Class EZ, 4.25% 3/25/42 | 4,935 | 5,518 | |

| Series 2016-26 Class CG, 3% 5/25/46 | 10,585 | 11,167 | |

| Freddie Mac: | |||

| floater: | |||

| Series 2530 Class FE, 1 month U.S. LIBOR + 0.600% 2.2585% 2/15/32 (e)(f) | 23 | 24 | |

| Series 2682 Class FB, 1 month U.S. LIBOR + 0.900% 2.5585% 10/15/33 (e)(f) | 1,282 | 1,305 | |

| Series 2711 Class FC, 1 month U.S. LIBOR + 0.900% 2.5585% 2/15/33 (e)(f) | 716 | 728 | |

| planned amortization class: | |||

| Series 1141 Class G, 9% 9/15/21 | 5 | 5 | |

| Series 2682 Class LD, 4.5% 10/15/33 | 313 | 336 | |

| Series 3415 Class PC, 5% 12/15/37 | 220 | 245 | |

| Series 3857 Class ZP, 5% 5/15/41 | 2,697 | 3,383 | |

| Series 4135 Class AB, 1.75% 6/15/42 | 382 | 385 | |

| sequential payer: | |||

| Series 2004-2802 Class ZG, 5.5% 5/15/34 | 3,791 | 4,373 | |

| Series 2587 Class AD, 4.71% 3/15/33 | 1,400 | 1,493 | |

| Series 2877 Class ZD, 5% 10/15/34 | 3,006 | 3,363 | |

| Series 3007 Class EW, 5.5% 7/15/25 | 1,974 | 2,102 | |

| Series 3745 Class KV, 4.5% 12/15/26 | 3,864 | 4,118 | |

| Series 3871 Class KB, 5.5% 6/15/41 | 9,243 | 10,957 | |

| Series 3889 Class DZ, 4% 1/15/41 | 30,608 | 33,163 | |

| Series 3843 Class PZ, 5% 4/15/41 | 2,308 | 2,818 | |

| Freddie Mac Multi-family Structured pass-thru certificates sequential payer: | |||

| Series 4335 Class AL, 4.25% 3/15/40 | 2,256 | 2,348 | |

| Series 4341 Class ML, 3.5% 11/15/31 | 4,790 | 5,134 | |

| Ginnie Mae guaranteed REMIC pass-thru certificates: | |||

| floater: | |||

| Series 2008-2 Class FD, 1 month U.S. LIBOR + 0.480% 2.127% 1/20/38 (e)(f) | 124 | 124 | |

| Series 2008-73 Class FA, 1 month U.S. LIBOR + 0.860% 2.507% 8/20/38 (e)(f) | 959 | 971 | |

| Series 2008-83 Class FB, 1 month U.S. LIBOR + 0.900% 2.547% 9/20/38 (e)(f) | 755 | 774 | |

| Series 2009-108 Class CF, 1 month U.S. LIBOR + 0.600% 2.2585% 11/16/39 (e)(f) | 515 | 520 | |

| Series 2011-H20 Class FA, 1 month U.S. LIBOR + 0.550% 2.2844% 9/20/61 (e)(f)(h) | 4,786 | 4,796 | |

| Series 2011-H21 Class FA, 1 month U.S. LIBOR + 0.600% 2.3344% 10/20/61 (e)(f)(h) | 3,008 | 3,018 | |

| Series 2012-H01 Class FA, 1 month U.S. LIBOR + 0.700% 2.4344% 11/20/61 (e)(f)(h) | 2,772 | 2,787 | |

| Series 2012-H03 Class FA, 1 month U.S. LIBOR + 0.700% 2.4344% 1/20/62(e)(f)(h) | 1,732 | 1,741 | |

| Series 2012-H06 Class FA, 1 month U.S. LIBOR + 0.630% 2.3644% 1/20/62 (e)(f)(h) | 2,580 | 2,590 | |

| Series 2012-H07 Class FA, 1 month U.S. LIBOR + 0.630% 2.3644% 3/20/62 (e)(f)(h) | 1,608 | 1,611 | |

| Series 2012-H21 Class DF, 1 month U.S. LIBOR + 0.650% 2.3844% 5/20/61 (e)(f)(h) | 86 | 86 | |

| Series 2013-H19: | |||

| Class FC, 1 month U.S. LIBOR + 0.600% 2.3344% 8/20/63 (e)(f)(h) | 758 | 759 | |

| Class FD, 1 month U.S. LIBOR + 0.600% 2.3344% 8/20/63 (e)(f)(h) | 1,861 | 1,865 | |

| Series 2014-H02 Class FB, 1 month U.S. LIBOR + 0.650% 2.3844% 12/20/63 (e)(f)(h) | 25,202 | 25,313 | |

| Series 2014-H03 Class FA, 1 month U.S. LIBOR + 0.600% 2.3344% 1/20/64 (e)(f)(h) | 7,709 | 7,730 | |

| Series 2015-H07 Class FA, 1 month U.S. LIBOR + 0.300% 2.0344% 3/20/65 (e)(f)(h) | 109 | 109 | |

| Series 2015-H13 Class FL, 1 month U.S. LIBOR + 0.280% 2.0144% 5/20/63 (e)(f)(h) | 275 | 274 | |

| Series 2015-H19 Class FA, 1 month U.S. LIBOR + 0.200% 1.9344% 4/20/63 (e)(f)(h) | 319 | 317 | |

| Series 2016-H20 Class FM, 1 month U.S. LIBOR + 0.400% 2.1344% 12/20/62 (e)(f)(h) | 238 | 238 | |

| Series 2017-161 Class DF, 1 month U.S. LIBOR + 0.250% 1.897% 10/20/47 (e)(f) | 3,209 | 3,190 | |

| Series 2018-65 Class DF, 1 month U.S. LIBOR + 0.300% 1.947% 5/20/48 (e)(f) | 3,946 | 3,929 | |

| Series 2018-77 Class FA, 1 month U.S. LIBOR + 0.300% 1.947% 6/20/48 (e)(f) | 4,557 | 4,538 | |

| Series 2019-115 Class FA, 1 month U.S. LIBOR + 0.450% 2.097% 9/20/49 (e)(f) | 6,724 | 6,735 | |

| Series 2019-98 Class FC, 1 month U.S. LIBOR + 0.450% 2.097% 8/20/49 (e)(f) | 24,178 | 24,201 | |

| planned amortization class: | |||

| Series 2010-31 Class BP, 5% 3/20/40 | 8,909 | 10,123 | |

| Series 2017-134 Class BA, 2.5% 11/20/46 | 489 | 504 | |

| sequential payer: | |||

| Series 2011-69 Class GX, 4.5% 5/16/40 | 8,124 | 8,750 | |

| Series 2013-H06 Class HA, 1.65% 1/20/63 (h) | 597 | 597 | |

| Series 2013-H26 Class HA, 3.5% 9/20/63 (h) | 11,248 | 11,374 | |

| Series 2014-H04 Class HA, 2.75% 2/20/64 (h) | 3,210 | 3,279 | |

| Series 2014-H12 Class KA, 2.75% 5/20/64 (h) | 3,205 | 3,249 | |

| Series 2016-H02 Class FM, 1 month U.S. LIBOR + 0.500% 2.2344% 9/20/62 (e)(f)(h) | 1,655 | 1,655 | |

| Series 2016-H04 Class FE, 1 month U.S. LIBOR + 0.650% 2.3844% 11/20/65 (e)(f)(h) | 232 | 232 | |

| Series 2017-139 Class BA, 3% 9/20/47 | 8,687 | 9,211 | |

| Series 2004-22 Class M1, 5.5% 4/20/34 | 534 | 722 | |

| Series 2010-169 Class Z, 4.5% 12/20/40 | 6,079 | 6,804 | |

| Series 2010-H15 Class TP, 5.15% 8/20/60 (h) | 73 | 75 | |

| Series 2010-H17 Class XP, 5.31% 7/20/60 (e)(h) | 143 | 144 | |

| Series 2010-H18 Class PL, 5.01% 9/20/60 (e)(h) | 39 | 43 | |

| Series 2012-64 Class KI, 3.5% 11/20/36 (j) | 354 | 10 | |

| Series 2013-124: | |||

| Class ES, 8.667% - 1 month U.S. LIBOR 6.4707% 4/20/39 (e)(k) | 792 | 818 | |

| Class ST, 8.800% - 1 month U.S. LIBOR 6.604% 8/20/39 (e)(k) | 2,868 | 2,974 | |

| Series 2013-H07 Class JA, 1.75% 3/20/63 (h) | 5,856 | 5,853 | |

| Series 2015-H17 Class HA, 2.5% 5/20/65 (h) | 1,680 | 1,682 | |

| Series 2015-H21: | |||

| Class HA, 2.5% 6/20/63 (h) | 1,167 | 1,167 | |

| Class JA, 2.5% 6/20/65 (h) | 470 | 471 | |

| Series 2015-H30 Class HA, 1.75% 9/20/62 (e)(h) | 2,965 | 2,968 | |

| Series 2016-H13 Class FB, U.S. TREASURY 1 YEAR INDEX + 0.500% 2.03% 5/20/66 (e)(f)(h) | 13,020 | 13,058 | |

| Series 2017-H06 Class FA, U.S. TREASURY 1 YEAR INDEX + 0.350% 1.88% 8/20/66 (e)(f)(h) | 11,817 | 11,821 | |

| Series 2090-118 Class XZ, 5% 12/20/39 | 12,709 | 14,647 | |

| 322,289 | |||

| TOTAL COLLATERALIZED MORTGAGE OBLIGATIONS | |||

| (Cost $318,604) | 322,289 | ||

| Foreign Government and Government Agency Obligations - 1.5% | |||

| Israeli State: | |||

| (guaranteed by U.S. Government through Agency for International Development) 5.5% 12/4/23 | 38 | 44 | |

| 5.5% 4/26/24 | 4,828 | 5,679 | |

| Jordanian Kingdom 3% 6/30/25 | 15,338 | 16,726 | |

| Ukraine Government 1.471% 9/29/21 | 27,711 | 27,907 | |

| TOTAL FOREIGN GOVERNMENT AND GOVERNMENT AGENCY OBLIGATIONS | |||

| (Cost $48,448) | 50,356 | ||

| Shares | Value (000s) | ||

| Fixed-Income Funds - 21.1% | |||

| Fidelity Mortgage Backed Securities Central Fund (l) | |||

| (Cost $680,173) | 6,464,481 | 719,109 | |

| Money Market Funds - 6.9% | |||

| Fidelity Cash Central Fund 1.60% (m) | |||

| (Cost $235,597) | 235,551,685 | 235,599 | |

| Maturity Amount (000s) | Value (000s) | ||

| Repurchase Agreements - 4.6% | |||

| Investments in repurchase agreements in a joint trading account at 1.59%, dated 2/28/20 due 3/2/20 (Collateralized by U.S. Government Obligations) # (n) | |||

| (Cost $158,558) | 158,579 | 158,558 |

| Purchased Swaptions - 0.9%(o) | ||||

| Expiration Date | Notional Amount (000s) | Value (000s) | ||

| Put Options - 0.1% | ||||

| Option on an interest rate swap with Bank of America N.A. to pay semi-annually a fixed rate of 1.67% and receive quarterly a floating rate based on 3-month LIBOR, expiring February 2030 | 2/7/25 | 3,100 | $60 | |

| Option on an interest rate swap with Bank of America N.A. to pay semi-annually a fixed rate of 1.7375% and receive quarterly a floating rate based on 3-month LIBOR, expiring September 2029 | 9/20/24 | 30,800 | 518 | |

| Option on an interest rate swap with Bank of America N.A. to pay semi-annually a fixed rate of 2.215% and receive quarterly a floating rate based on 3-month LIBOR, expiring July 2029 | 7/10/24 | 35,000 | 346 | |

| Option on an interest rate swap with Bank of America, N.A. to pay semi-annually a fixed rate of 2.605% and receive quarterly a floating rate based on 3-month LIBOR, expiring May 2029 | 4/29/22 | 18,500 | 49 | |

| Option on an interest rate swap with Citibank, N.A. to pay semi-annually a fixed rate of 2.54% and receive quarterly a floating rate based on 3-month LIBOR, expiring April 2029 | 4/5/22 | 39,000 | 107 | |

| Option on an interest rate swap with Citibank, N.A. to pay semi-annually a fixed rate of 2.651% and receive quarterly a floating rate based on 3-month LIBOR, expiring April 2029 | 4/14/22 | 8,900 | 21 | |

| Option on an interest rate swap with Goldman Sachs Bank U.S.A. to pay semi-annually a fixed rate of 1.4% and receive quarterly a floating rate based on 3-month LIBOR, expiring February 2030 | 2/26/25 | 16,700 | 412 | |

| Option on an interest rate swap with Goldman Sachs Bank U.S.A. to pay semi-annually a fixed rate of 1.4025% and receive quarterly a floating rate based on 3-month LIBOR, expiring February 2030 | 2/26/25 | 17,900 | 441 | |

| Option on an interest rate swap with Goldman Sachs Bank U.S.A. to pay semi-annually a fixed rate of 1.905% and receive quarterly a floating rate based on 3-month LIBOR, expiring October 2029 | 10/28/24 | 12,400 | 181 | |

| Option on an interest rate swap with Goldman Sachs Bank U.S.A. to pay semi-annually a fixed rate of 2.495% and receive quarterly a floating rate based on 3-month LIBOR, expiring October 2027 | 10/5/20 | 13,400 | 6 | |

| Option on an interest rate swap with Goldman Sachs Bank U.S.A. to pay semi-annually a fixed rate of 2.7875% and receive quarterly a floating rate based on 3-month LIBOR, expiring January 2028 | 1/25/21 | 27,300 | 13 | |

| Option on an interest rate swap with Goldman Sachs Bank U.S.A. to pay semi-annually a fixed rate of 2.815% and receive quarterly a floating rate based on 3-month LIBOR, expiring March 2029 | 3/7/22 | 22,000 | 36 | |

| Option on an interest rate swap with JPMorgan Chase Bank, N.A. to pay semi-annually a fixed rate of 3.0580% and receive quarterly a floating rate based on 3-month LIBOR, expiring April 2028 | 4/20/21 | 65,300 | 32 | |

| TOTAL PUT OPTIONS | 2,222 | |||

| Call Options - 0.8% | ||||

| Option on an interest rate swap with Bank of America N.A. to receive semi-annually a fixed rate of 1.67% and pay quarterly a floating rate based on 3-month LIBOR, expiring February 2030 | 2/7/25 | 3,100 | 122 | |

| Option on an interest rate swap with Bank of America N.A. to receive semi-annually a fixed rate of 1.7375% and pay quarterly a floating rate based on 3-month LIBOR, expiring September 2029 | 9/20/24 | 30,800 | 1,266 | |

| Option on an interest rate swap with Bank of America N.A. to receive semi-annually a fixed rate of 2.215% and pay quarterly a floating rate based on 3-month LIBOR, expiring July 2029 | 7/10/24 | 35,000 | 2,007 | |

| Option on an interest rate swap with Bank of America, N.A. to receive semi-annually a fixed rate of 2.605% and pay quarterly a floating rate based on 3-month LIBOR, expiring May 2029 | 4/29/22 | 18,500 | 1,878 | |

| Option on an interest rate swap with Citibank, N.A. to receive semi-annually a fixed rate of 2.54% and pay quarterly a floating rate based on 3-month LIBOR, expiring April 2029 | 4/5/22 | 39,000 | 3,813 | |

| Option on an interest rate swap with Citibank, N.A. to receive semi-annually a fixed rate of 2.651% and pay quarterly a floating rate based on 3-month LIBOR, expiring April 2029 | 4/14/22 | 8,900 | 930 | |

| Option on an interest rate swap with Goldman Sachs Bank U.S.A. to receive semi-annually a fixed rate of 1.4% and pay quarterly a floating rate based on 3-month LIBOR, expiring February 2030 | 2/26/25 | 16,700 | 532 | |

| Option on an interest rate swap with Goldman Sachs Bank U.S.A. to receive semi-annually a fixed rate of 1.4025% and pay quarterly a floating rate based on 3-month LIBOR, expiring February 2030 | 2/26/25 | 17,900 | 572 | |

| Option on an interest rate swap with Goldman Sachs Bank U.S.A. to receive semi-annually a fixed rate of 1.905% and pay quarterly a floating rate based on 3-month LIBOR, expiring October 2029 | 10/28/24 | 12,400 | 577 | |

| Option on an interest rate swap with Goldman Sachs Bank U.S.A. to receive semi-annually a fixed rate of 2.495% and pay quarterly a floating rate based on 3-month LIBOR, expiring October 2027 | 10/5/20 | 13,400 | 1,353 | |

| Option on an interest rate swap with Goldman Sachs Bank U.S.A. to receive semi-annually a fixed rate of 2.7875% and pay quarterly a floating rate based on 3-month LIBOR, expiring January 2028 | 1/25/21 | 27,300 | 3,260 | |

| Option on an interest rate swap with Goldman Sachs Bank U.S.A. to receive semi-annually a fixed rate of 2.815% and pay quarterly a floating rate based on 3-month LIBOR, expiring March 2029 | 3/7/22 | 22,000 | 2,541 | |

| Option on an interest rate swap with JPMorgan Chase Bank, N.A. to receive semi-annually a fixed rate of 3.058% and pay quarterly a floating rate based on 3-month LIBOR, expiring April 2028 | 4/20/21 | 65,300 | 8,912 | |

| TOTAL CALL OPTIONS | 27,763 | |||

| TOTAL PURCHASED SWAPTIONS | ||||

| (Cost $17,862) | 29,985 | |||

| TOTAL INVESTMENT IN SECURITIES - 110.5% | ||||

| (Cost $3,570,686) | 3,768,931 | |||

| NET OTHER ASSETS (LIABILITIES) - (10.5)% | (357,934) | |||

| NET ASSETS - 100% | $3,410,997 |

| TBA Sale Commitments | ||

| Principal Amount (000s) | Value (000s) | |

| Ginnie Mae | ||

| 3% 3/1/50 | $(4,800) | $(4,960) |

| 3% 3/1/50 | (2,500) | (2,583) |

| 3% 3/1/50 | (6,550) | (6,768) |

| 3% 3/1/50 | (6,950) | (7,181) |

| 3% 3/1/50 | (10,900) | (11,262) |

| 3% 3/1/50 | (8,300) | (8,576) |

| 3% 4/1/50 | (24,750) | (25,546) |

| 3.5% 3/1/50 | (7,400) | (7,666) |

| 3.5% 3/1/50 | (20,000) | (20,720) |

| TOTAL GINNIE MAE | (95,262) | |

| Uniform Mortgage Backed Securities | ||

| 3% 3/1/50 | (29,400) | (30,276) |

| 3% 3/1/50 | (37,500) | (38,617) |

| 3% 3/1/50 | (20,700) | (21,317) |

| 3% 3/1/50 | (5,000) | (5,149) |

| 3% 3/1/50 | (2,500) | (2,574) |

| 3% 3/1/50 | (800) | (824) |

| TOTAL UNIFORM MORTGAGE BACKED SECURITIES | (98,757) | |

| TOTAL TBA SALE COMMITMENTS | ||

| (Proceeds $192,571) | $(194,019) |

| Written Swaptions | |||

| Expiration Date | Notional Amount | Value (000s) | |

| Put Swaptions | |||

| Option on an interest rate swap with Bank of America N.A. to pay semi-annually a fixed rate of 1.395% and receive quarterly a floating rate based on 3-month LIBOR, expiring February 2030 | 2/24/25 | 33,200 | $(824) |

| Option on an interest rate swap with Bank of America N.A. to pay semi-annually a fixed rate of 1.45% and receive quarterly a floating rate based on 3-month LIBOR, expiring September 2029 | 9/4/24 | 11,700 | (256) |

| Option on an interest rate swap with Bank of America N.A. to pay semi-annually a fixed rate of 1.89% and receive quarterly a floating rate based on 3-month LIBOR, expiring December 2029 | 12/9/24 | 100 | (2) |

| Option on an interest rate swap with Bank of America N.A. to pay semi-annually a fixed rate of 1.92% and receive quarterly a floating rate based on 3-month LIBOR, expiring January 2030 | 1/8/25 | 27,000 | (408) |

| Option on an interest rate swap with Bank of America N.A. to pay semi-annually a fixed rate of 1.97% and receive quarterly a floating rate based on 3-month LIBOR, expiring August 2029 | 8/1/24 | 15,000 | (194) |

| Option on an interest rate swap with Bank of America, N.A. to pay semi-annually a fixed rate of 2.26% and receive quarterly a floating rate based on 3-month LIBOR, expiring June 2029 | 5/31/22 | 9,000 | (45) |

| Option on an interest rate swap with Goldman Sachs Bank U.S.A. to pay semi-annually a fixed rate of 1.487% and receive quarterly a floating rate based on 3-month LIBOR, expiring October 2030 | 10/2/20 | 21,900 | (185) |

| TOTAL PUT SWAPTIONS | (1,914) | ||

| Call Swaptions | |||

| Option on an interest rate swap with Bank of America N.A. to receive semi-annually a fixed rate of 1.395% and pay quarterly a floating rate based on 3-month LIBOR, expiring February 2030 | 2/24/25 | 33,200 | (1,056) |

| Option on an interest rate swap with Bank of America N.A. to receive semi-annually a fixed rate of 1.45% and pay quarterly a floating rate based on 3-month LIBOR, expiring September 2029 | 9/4/24 | 11,700 | (383) |

| Option on an interest rate swap with Bank of America N.A. to receive semi-annually a fixed rate of 1.89% and pay quarterly a floating rate based on 3-month LIBOR, expiring December 2029 | 12/9/24 | 100 | (5) |

| Option on an interest rate swap with Bank of America N.A. to receive semi-annually a fixed rate of 1.92% and pay quarterly a floating rate based on 3-month LIBOR, expiring January 2030 | 1/8/25 | 27,000 | (1,270) |

| Option on an interest rate swap with Bank of America N.A. to receive semi-annually a fixed rate of 1.97% and pay quarterly a floating rate based on 3-month LIBOR, expiring August 2029 | 8/1/24 | 15,000 | (730) |

| Option on an interest rate swap with Bank of America, N.A. to receive semi-annually a fixed rate of 2.26% and pay quarterly a floating rate based on 3-month LIBOR, expiring June 2029 | 5/31/22 | 9,000 | (724) |

| Option on an interest rate swap with Goldman Sachs Bank U.S.A. to receive semi-annually a fixed rate of 1.487% and pay quarterly a floating rate based on 3-month LIBOR, expiring October 2030 | 10/2/20 | 21,900 | (980) |

| TOTAL CALL SWAPTIONS | (5,148) | ||

| TOTAL WRITTEN SWAPTIONS | $(7,062) |

| Futures Contracts | |||||

| Number of contracts | Expiration Date | Notional Amount (000s) | Value (000s) | Unrealized Appreciation/(Depreciation) (000s) | |

| Purchased | |||||

| Treasury Contracts | |||||

| CBOT 10-Year U.S. Treasury Note Contracts (United States) | 709 | June 2020 | $95,539 | $2,168 | $2,168 |

| CBOT 2-Year U.S. Treasury Note Contracts (United States) | 865 | June 2020 | 188,854 | 1,762 | 1,762 |

| CBOT 5-Year U.S. Treasury Note Contracts (United States) | 83 | June 2020 | 10,188 | (6) | (6) |

| CBOT Long Term U.S. Treasury Bond Contracts (United States) | 404 | June 2020 | 68,781 | 903 | 903 |

| CBOT Ultra Long Term U.S. Treasury Bond Contracts (United States) | 133 | June 2020 | 27,598 | 560 | 560 |

| TOTAL FUTURES CONTRACTS | $5,387 |

The notional amount of futures purchased as a percentage of Net Assets is 11.5%

For the period, the average monthly notional amount at value for futures contracts in the aggregate was $405,606,000.

Swaps

| Payment Received | Payment Frequency | Payment Paid | Payment Frequency | Clearinghouse / Counterparty(1) | Maturity Date | Notional Amount (000s) | Value (000s) | Upfront Premium Received/(Paid) (000s)(2) | Unrealized Appreciation/(Depreciation) (000s) |

| Interest Rate Swaps | |||||||||

| 1.75% | Semi - annual | 3-month LIBOR(3) | Quarterly | LCH | Mar. 2022 | $153,768 | $2,018 | $0 | $2,018 |

| 3-month LIBOR(3) | Quarterly | 1.75% | Semi - annual | LCH | Mar. 2025 | 37,904 | (1,101) | 0 | (1,101) |

| 3-month LIBOR(3) | Quarterly | 2% | Semi - annual | LCH | Mar. 2027 | 9,990 | (453) | 0 | (453) |

| 3-month LIBOR(3) | Quarterly | 2% | Semi - annual | LCH | Mar. 2030 | 88,450 | (4,931) | 0 | (4,931) |

| TOTAL INTEREST RATE SWAPS | $(4,467) | $0 | $(4,467) | ||||||

(1) Swaps with LCH Clearnet Group (LCH) are centrally cleared over-the-counter (OTC) swaps.

(2) Any premiums for centrally cleared over-the-counter (OTC) swaps are recorded periodically throughout the term of the swap to variation margin and included in unrealized appreciation (depreciation).

(3) Represents floating rate.

Values shown as $0 in the Schedule of Investments may reflect amounts less than $500.

Legend

(a) Security or a portion of the security was pledged to cover margin requirements for futures contracts. At period end, the value of securities pledged amounted to $2,579,000.

(b) Security or a portion of the security was pledged to cover margin requirements for centrally cleared OTC swaps. At period end, the value of securities pledged amounted to $5,850,000.

(c) Security or a portion of the security has been segregated as collateral for mortgage-backed or asset-backed securities purchased on a delayed delivery or when-issued basis. At period end, the value of securities pledged amounted to $109,000.

(d) Security or a portion of the security is on loan at period end.

(e) Coupon rates for floating and adjustable rate securities reflect the rates in effect at period end.

(f) Coupon is indexed to a floating interest rate which may be multiplied by a specified factor and/or subject to caps or floors.

(g) Security or a portion of the security purchased on a delayed delivery or when-issued basis.

(h) Represents an investment in an underlying pool of reverse mortgages which typically do not require regular principal and interest payments as repayment is deferred until a maturity event.

(i) Principal Only Strips represent the right to receive the monthly principal payments on an underlying pool of mortgage loans.

(j) Security represents right to receive monthly interest payments on an underlying pool of mortgages or assets. Principal shown is the outstanding par amount of the pool as of the end of the period.

(k) Coupon is inversely indexed to a floating interest rate multiplied by a specified factor. The price may be considerably more volatile than the price of a comparable fixed rate security.

(l) Affiliated fund that is generally available only to investment companies and other accounts managed by Fidelity Investments. A complete unaudited schedule of portfolio holdings for each Fidelity Central Fund is filed with the SEC for the first and third quarters of each fiscal year on Form N-PORT and is available upon request or at the SEC's website at www.sec.gov. An unaudited holdings listing for the Fund, which presents direct holdings as well as the pro-rata share of securities and other investments held indirectly through its investment in underlying non-money market Fidelity Central Funds, is available at fidelity.com and/or institutional.fidelity.com, as applicable. In addition, each Fidelity Central Fund's financial statements are available on the SEC's website or upon request.

(m) Affiliated fund that is generally available only to investment companies and other accounts managed by Fidelity Investments. The rate quoted is the annualized seven-day yield of the fund at period end. A complete unaudited listing of the fund's holdings as of its most recent quarter end is available upon request. In addition, each Fidelity Central Fund's financial statements are available on the SEC's website or upon request.

(n) Includes investment made with cash collateral received from securities on loan.

(o) For the period, the average monthly notional amount for purchased swaptions was $586,200,000.

Affiliated Central Funds

Information regarding fiscal year to date income earned by the Fund from investments in Fidelity Central Funds is as follows:

| Fund | Income earned |

| (Amounts in thousands) | |

| Fidelity Cash Central Fund | $977 |

| Fidelity Mortgage Backed Securities Central Fund | 7,992 |

| Total | $8,969 |

Amounts in the income column in the above table include any capital gain distributions from underlying funds, which are presented in the corresponding line-item in the Statement of Operations, if applicable.

Fiscal year to date information regarding the Fund’s investments in non-Money Market Central Funds, including the ownership percentage, is presented below.

| Fund (Amounts in thousands) | Value, beginning of period | Purchases | Sales Proceeds | Realized Gain/Loss | Change in Unrealized appreciation (depreciation) | Value, end of period | % ownership, end of period |

| Fidelity Mortgage Backed Securities Central Fund | $730,709 | $130,992 | $150,000 | $8,398 | $(990) | $719,109 | 34.6% |

| Total | $730,709 | $130,992 | $150,000 | $8,398 | $(990) | $719,109 |

Investment Valuation

The following is a summary of the inputs used, as of February 29, 2020, involving the Fund's assets and liabilities carried at fair value. The inputs or methodology used for valuing securities may not be an indication of the risk associated with investing in those securities. For more information on valuation inputs, and their aggregation into the levels used below, please refer to the Investment Valuation section in the accompanying Notes to Financial Statements.

| Valuation Inputs at Reporting Date: | ||||

| Description | Total | Level 1 | Level 2 | Level 3 |

| (Amounts in thousands) | ||||

| Investments in Securities: | ||||

| U.S. Government and Government Agency Obligations | $1,866,413 | $-- | $1,866,413 | $-- |

| U.S. Government Agency - Mortgage Securities | 386,622 | -- | 386,622 | -- |

| Collateralized Mortgage Obligations | 322,289 | -- | 322,289 | -- |

| Foreign Government and Government Agency Obligations | 50,356 | -- | 50,356 | -- |

| Fixed-Income Funds | 719,109 | 719,109 | -- | -- |

| Money Market Funds | 235,599 | 235,599 | -- | -- |

| Repurchase Agreements | 158,558 | -- | 158,558 | -- |

| Purchased Swaptions | 29,985 | -- | 29,985 | -- |

| Total Investments in Securities: | $3,768,931 | $954,708 | $2,814,223 | $-- |

| Derivative Instruments: | ||||

| Assets | ||||

| Futures Contracts | $5,393 | $5,393 | $-- | $-- |

| Swaps | 2,018 | -- | 2,018 | -- |

| Total Assets | $7,411 | $5,393 | $2,018 | $-- |

| Liabilities | ||||

| Futures Contracts | $(6) | $(6) | $-- | $-- |

| Swaps | (6,485) | -- | (6,485) | -- |

| Written Swaptions | (7,062) | -- | (7,062) | -- |

| Total Liabilities | $(13,553) | $(6) | $(13,547) | $-- |

| Total Derivative Instruments: | $(6,142) | $5,387 | $(11,529) | $-- |

| Other Financial Instruments: | ||||

| TBA Sale Commitments | $(194,019) | $-- | $(194,019) | $-- |

| Total Other Financial Instruments: | $(194,019) | $-- | $(194,019) | $-- |

Value of Derivative Instruments

The following table is a summary of the Fund's value of derivative instruments by primary risk exposure as of February 29, 2020. For additional information on derivative instruments, please refer to the Derivative Instruments section in the accompanying Notes to Financial Statements.

| Primary Risk Exposure / Derivative Type | Value | |

| Asset | Liability | |

| (Amounts in thousands) | ||

| Interest Rate Risk | ||

| Futures Contracts(a) | $5,393 | $(6) |

| Purchased Swaptions(b) | 29,985 | 0 |

| Swaps(c) | 2,018 | (6,485) |

| Written Swaptions(d) | 0 | (7,062) |

| Total Interest Rate Risk | 37,396 | (13,553) |

| Total Value of Derivatives | $37,396 | $(13,553) |

(a) Reflects gross cumulative appreciation (depreciation) on futures contracts as presented in the Schedule of Investments. In the Statement of Assets and Liabilities, the period end daily variation margin is included in receivable or payable for daily variation margin on futures contracts, and the net cumulative appreciation (depreciation) is included in Total accumulated earnings (loss).

(b) Gross value is included in the Statement of Assets and Liabilities in the investments, at value line-item.

(c) For centrally cleared over-the-counter (OTC) swaps, reflects gross cumulative appreciation (depreciation) as presented in the Schedule of Investments. In the Statement of Assets and Liabilities, the period end daily variation margin for centrally cleared OTC swaps is included in receivable or payable for daily variation margin on centrally cleared OTC swaps, and the net cumulative appreciation (depreciation) for centrally cleared OTC swaps is included in Total accumulated earnings (loss).

(d) Gross value is presented in the Statement of Assets and Liabilities in the written options, at value line-item.

Other Information

# Additional information on each counterparty to the repurchase agreement is as follows:

| Repurchase Agreement / Counterparty | Value (000s) |

| $158,558,000 due 3/02/20 at 1.59% | |

| J.P. Morgan Securities, Inc. | $3,311 |

| Nomura Securities International | 513 |

| RBC Dominion Securities, Inc. | 23,081 |

| Societe Generale (PARIS) | 2,565 |

| Sumitomo Mitsu Bk Corp Ny (DI) | 14,420 |

| Wells Fargo Securities LLC | 114,668 |

| $158,558 |

See accompanying notes which are an integral part of the financial statements.

Financial Statements

Statement of Assets and Liabilities

| Amounts in thousands (except per-share amounts) | February 29, 2020 (Unaudited) | |

| Assets | ||

| Investment in securities, at value (including securities loaned of $155,366 and repurchase agreements of $158,558) — See accompanying schedule: Unaffiliated issuers (cost $2,654,916) | $2,814,223 | |

| Fidelity Central Funds (cost $915,770) | 954,708 | |

| Total Investment in Securities (cost $3,570,686) | $3,768,931 | |

| Cash | 11 | |

| Receivable for investments sold | 15 | |

| Receivable for premium on written options | 6,700 | |

| Receivable for TBA sale commitments | 192,571 | |

| Receivable for fund shares sold | 54,484 | |

| Interest receivable | 8,746 | |

| Distributions receivable from Fidelity Central Funds | 277 | |

| Receivable for daily variation margin on futures contracts | 2,700 | |

| Receivable from investment adviser for expense reductions | 22 | |

| Other receivables | 63 | |

| Total assets | 4,034,520 | |

| Liabilities | ||

| Payable for investments purchased | ||

| Regular delivery | $52,574 | |

| Delayed delivery | 192,540 | |

| TBA sale commitments, at value | 194,019 | |

| Payable for fund shares redeemed | 16,552 | |

| Distributions payable | 254 | |

| Accrued management fee | 789 | |

| Distribution and service plan fees payable | 96 | |

| Payable for daily variation margin on centrally cleared OTC swaps | 618 | |

| Written options, at value (premium receivable $6,700) | 7,062 | |

| Other affiliated payables | 397 | |

| Other payables and accrued expenses | 64 | |

| Collateral on securities loaned | 158,558 | |

| Total liabilities | 623,523 | |

| Net Assets | $3,410,997 | |

| Net Assets consist of: | ||

| Paid in capital | $3,256,458 | |

| Total accumulated earnings (loss) | 154,539 | |

| Net Assets | $3,410,997 | |

| Net Asset Value and Maximum Offering Price | ||

| Class A: | ||

| Net Asset Value and redemption price per share ($140,915 ÷ 12,906 shares)(a) | $10.92 | |

| Maximum offering price per share (100/96.00 of $10.92) | $11.38 | |

| Class M: | ||

| Net Asset Value and redemption price per share ($133,416 ÷ 12,221 shares)(a) | $10.92 | |

| Maximum offering price per share (100/96.00 of $10.92) | $11.38 | |

| Class C: | ||

| Net Asset Value and offering price per share ($54,108 ÷ 4,957 shares)(a) | $10.92 | |

| Government Income: | ||

| Net Asset Value, offering price and redemption price per share ($2,227,672 ÷ 204,364 shares) | $10.90 | |

| Class I: | ||

| Net Asset Value, offering price and redemption price per share ($292,256 ÷ 26,770 shares) | $10.92 | |

| Class Z: | ||

| Net Asset Value, offering price and redemption price per share ($562,630 ÷ 51,514 shares) | $10.92 |

(a) Redemption price per share is equal to net asset value less any applicable contingent deferred sales charge.

See accompanying notes which are an integral part of the financial statements.

Statement of Operations

| Amounts in thousands | Six months ended February 29, 2020 (Unaudited) | |

| Investment Income | ||

| Interest (including $41 from security lending) | $25,400 | |

| Income from Fidelity Central Funds | 8,969 | |

| Total income | 34,369 | |

| Expenses | ||

| Management fee | $4,446 | |

| Transfer agent fees | 1,584 | |

| Distribution and service plan fees | 578 | |

| Fund wide operations fee | 705 | |

| Independent trustees' fees and expenses | 5 | |

| Commitment fees | 5 | |

| Total expenses before reductions | 7,323 | |

| Expense reductions | (46) | |

| Total expenses after reductions | 7,277 | |

| Net investment income (loss) | 27,092 | |

| Realized and Unrealized Gain (Loss) | ||

| Net realized gain (loss) on: | ||

| Investment securities: | ||

| Unaffiliated issuers | 9,565 | |

| Redemptions in-kind with affiliated entities | 22,832 | |

| Fidelity Central Funds | 8,398 | |

| Futures contracts | 1,249 | |

| Swaps | 3,320 | |

| Written options | 342 | |

| Total net realized gain (loss) | 45,706 | |

| Change in net unrealized appreciation (depreciation) on: | ||

| Investment securities: | ||

| Unaffiliated issuers | 18,274 | |

| Fidelity Central Funds | (990) | |

| Futures contracts | 5,126 | |

| Swaps | (4,636) | |

| Written options | 283 | |

| Delayed delivery commitments | (205) | |

| Total change in net unrealized appreciation (depreciation) | 17,852 | |

| Net gain (loss) | 63,558 | |

| Net increase (decrease) in net assets resulting from operations | $90,650 |

See accompanying notes which are an integral part of the financial statements.

Statement of Changes in Net Assets

| Amounts in thousands | Six months ended February 29, 2020 (Unaudited) | Year ended August 31, 2019 |

| Increase (Decrease) in Net Assets | ||

| Operations | ||

| Net investment income (loss) | $27,092 | $78,603 |

| Net realized gain (loss) | 45,706 | 13,799 |

| Change in net unrealized appreciation (depreciation) | 17,852 | 217,158 |

| Net increase (decrease) in net assets resulting from operations | 90,650 | 309,560 |

| Distributions to shareholders | (27,281) | (77,199) |

| Share transactions - net increase (decrease) | (152,086) | (432,607) |

| Total increase (decrease) in net assets | (88,717) | (200,246) |

| Net Assets | ||

| Beginning of period | 3,499,714 | 3,699,960 |

| End of period | $3,410,997 | $3,499,714 |

See accompanying notes which are an integral part of the financial statements.

Financial Highlights

Fidelity Government Income Fund Class A

| Six months ended (Unaudited) February 29, | Years endedAugust 31, | |||||

| 2020 | 2019 | 2018 | 2017 | 2016 | 2015 | |

| Selected Per–Share Data | ||||||

| Net asset value, beginning of period | $10.70 | $10.00 | $10.36 | $10.66 | $10.50 | $10.47 |

| Income from Investment Operations | ||||||

| Net investment income (loss)A | .082 | .199 | .166 | .149 | .135 | .126 |

| Net realized and unrealized gain (loss) | .221 | .696 | (.362) | (.230) | .270 | .048 |

| Total from investment operations | .303 | .895 | (.196) | (.081) | .405 | .174 |

| Distributions from net investment income | (.083) | (.195) | (.164) | (.143) | (.150) | (.116) |

| Distributions from net realized gain | – | – | – | (.076) | (.095) | (.028) |

| Total distributions | (.083) | (.195) | (.164) | (.219) | (.245) | (.144) |

| Net asset value, end of period | $10.92 | $10.70 | $10.00 | $10.36 | $10.66 | $10.50 |

| Total ReturnB,C,D | 2.85% | 9.06% | (1.89)% | (.73)% | 3.92% | 1.67% |

| Ratios to Average Net AssetsE,F | ||||||

| Expenses before reductions | .78%G | .78% | .77% | .77% | .76% | .77% |

| Expenses net of fee waivers, if any | .78%G | .78% | .77% | .77% | .76% | .77% |

| Expenses net of all reductions | .78%G | .78% | .77% | .77% | .76% | .77% |

| Net investment income (loss) | 1.57%G | 1.96% | 1.64% | 1.44% | 1.28% | 1.20% |

| Supplemental Data | ||||||

| Net assets, end of period (in millions) | $141 | $139 | $131 | $174 | $261 | $222 |

| Portfolio turnover rateH | 313%G,I | 246% | 123% | 157% | 93% | 83% |

A Calculated based on average shares outstanding during the period.

B Total returns for periods of less than one year are not annualized.

C Total returns would have been lower if certain expenses had not been reduced during the applicable periods shown.

D Total returns do not include the effect of the sales charges.

E Fees and expenses of any underlying Fidelity Central Funds are not included in the Fund's expense ratio. The Fund indirectly bears its proportionate share of the expenses of any underlying Fidelity Central Funds. Based on their most recent shareholder report date, the expenses of any underlying non-money market Fidelity Central Funds were .01%.

F Expense ratios reflect operating expenses of the class. Expenses before reductions do not reflect amounts reimbursed by the investment adviser or reductions from expense offset arrangements and do not represent the amount paid by the class during periods when reimbursements or reductions occur. Expenses net of fee waivers reflect expenses after reimbursement by the investment adviser but prior to reductions from expense offset arrangements. Expenses net of all reductions represent the net expenses paid by the class.

G Annualized

H Amount does not include the portfolio activity of any underlying Fidelity Central Funds.

I Portfolio turnover rate excludes securities received or delivered in-kind.

See accompanying notes which are an integral part of the financial statements.

Fidelity Government Income Fund Class M

| Six months ended (Unaudited) February 29, | Years endedAugust 31, | |||||

| 2020 | 2019 | 2018 | 2017 | 2016 | 2015 | |

| Selected Per–Share Data | ||||||

| Net asset value, beginning of period | $10.70 | $10.00 | $10.36 | $10.66 | $10.50 | $10.47 |

| Income from Investment Operations | ||||||

| Net investment income (loss)A | .083 | .201 | .167 | .149 | .135 | .127 |

| Net realized and unrealized gain (loss) | .221 | .696 | (.362) | (.229) | .270 | .048 |

| Total from investment operations | .304 | .897 | (.195) | (.080) | .405 | .175 |

| Distributions from net investment income | (.084) | (.197) | (.165) | (.144) | (.150) | (.117) |

| Distributions from net realized gain | – | – | – | (.076) | (.095) | (.028) |

| Total distributions | (.084) | (.197) | (.165) | (.220) | (.245) | (.145) |

| Net asset value, end of period | $10.92 | $10.70 | $10.00 | $10.36 | $10.66 | $10.50 |

| Total ReturnB,C,D | 2.86% | 9.08% | (1.88)% | (.73)% | 3.92% | 1.68% |

| Ratios to Average Net AssetsE,F | ||||||

| Expenses before reductions | .76%G | .76% | .76% | .76% | .76% | .76% |

| Expenses net of fee waivers, if any | .76%G | .76% | .76% | .76% | .76% | .76% |

| Expenses net of all reductions | .76%G | .76% | .76% | .76% | .76% | .76% |

| Net investment income (loss) | 1.58%G | 1.98% | 1.65% | 1.44% | 1.28% | 1.20% |

| Supplemental Data | ||||||

| Net assets, end of period (in millions) | $133 | $131 | $137 | $157 | $197 | $181 |

| Portfolio turnover rateH | 313%G,I | 246% | 123% | 157% | 93% | 83% |

A Calculated based on average shares outstanding during the period.

B Total returns for periods of less than one year are not annualized.

C Total returns would have been lower if certain expenses had not been reduced during the applicable periods shown.

D Total returns do not include the effect of the sales charges.

E Fees and expenses of any underlying Fidelity Central Funds are not included in the Fund's expense ratio. The Fund indirectly bears its proportionate share of the expenses of any underlying Fidelity Central Funds. Based on their most recent shareholder report date, the expenses of any underlying non-money market Fidelity Central Funds were .01%.

F Expense ratios reflect operating expenses of the class. Expenses before reductions do not reflect amounts reimbursed by the investment adviser or reductions from expense offset arrangements and do not represent the amount paid by the class during periods when reimbursements or reductions occur. Expenses net of fee waivers reflect expenses after reimbursement by the investment adviser but prior to reductions from expense offset arrangements. Expenses net of all reductions represent the net expenses paid by the class.

G Annualized

H Amount does not include the portfolio activity of any underlying Fidelity Central Funds.

I Portfolio turnover rate excludes securities received or delivered in-kind.

See accompanying notes which are an integral part of the financial statements.

Fidelity Government Income Fund Class C

| Six months ended (Unaudited) February 29, | Years endedAugust 31, | |||||

| 2020 | 2019 | 2018 | 2017 | 2016 | 2015 | |

| Selected Per–Share Data | ||||||

| Net asset value, beginning of period | $10.70 | $10.00 | $10.36 | $10.66 | $10.50 | $10.47 |

| Income from Investment Operations | ||||||

| Net investment income (loss)A | .042 | .122 | .088 | .069 | .053 | .044 |

| Net realized and unrealized gain (loss) | .220 | .695 | (.361) | (.229) | .270 | .048 |

| Total from investment operations | .262 | .817 | (.273) | (.160) | .323 | .092 |

| Distributions from net investment income | (.042) | (.117) | (.087) | (.064) | (.068) | (.034) |

| Distributions from net realized gain | – | – | – | (.076) | (.095) | (.028) |

| Total distributions | (.042) | (.117) | (.087) | (.140) | (.163) | (.062) |

| Net asset value, end of period | $10.92 | $10.70 | $10.00 | $10.36 | $10.66 | $10.50 |

| Total ReturnB,C,D | 2.46% | 8.24% | (2.64)% | (1.49)% | 3.12% | .88% |

| Ratios to Average Net AssetsE,F | ||||||

| Expenses before reductions | 1.55%G | 1.54% | 1.54% | 1.54% | 1.54% | 1.55% |

| Expenses net of fee waivers, if any | 1.55%G | 1.54% | 1.54% | 1.54% | 1.54% | 1.55% |

| Expenses net of all reductions | 1.55%G | 1.54% | 1.54% | 1.54% | 1.54% | 1.55% |

| Net investment income (loss) | .79%G | 1.20% | .87% | .67% | .50% | .42% |

| Supplemental Data | ||||||

| Net assets, end of period (in millions) | $54 | $51 | $57 | $72 | $94 | $54 |

| Portfolio turnover rateH | 313%G,I | 246% | 123% | 157% | 93% | 83% |

A Calculated based on average shares outstanding during the period.

B Total returns for periods of less than one year are not annualized.

C Total returns would have been lower if certain expenses had not been reduced during the applicable periods shown.

D Total returns do not include the effect of the contingent deferred sales charge.

E Fees and expenses of any underlying Fidelity Central Funds are not included in the Fund's expense ratio. The Fund indirectly bears its proportionate share of the expenses of any underlying Fidelity Central Funds. Based on their most recent shareholder report date, the expenses of any underlying non-money market Fidelity Central Funds were .01%.

F Expense ratios reflect operating expenses of the class. Expenses before reductions do not reflect amounts reimbursed by the investment adviser or reductions from expense offset arrangements and do not represent the amount paid by the class during periods when reimbursements or reductions occur. Expenses net of fee waivers reflect expenses after reimbursement by the investment adviser but prior to reductions from expense offset arrangements. Expenses net of all reductions represent the net expenses paid by the class.

G Annualized

H Amount does not include the portfolio activity of any underlying Fidelity Central Funds.

I Portfolio turnover rate excludes securities received or delivered in-kind.

See accompanying notes which are an integral part of the financial statements.

Fidelity Government Income Fund

| Six months ended (Unaudited) February 29, | Years endedAugust 31, | |||||

| 2020 | 2019 | 2018 | 2017 | 2016 | 2015 | |

| Selected Per–Share Data | ||||||

| Net asset value, beginning of period | $10.68 | $9.99 | $10.35 | $10.65 | $10.48 | $10.45 |

| Income from Investment Operations | ||||||

| Net investment income (loss)A | .100 | .232 | .198 | .181 | .167 | .159 |

| Net realized and unrealized gain (loss) | .220 | .686 | (.361) | (.229) | .281 | .048 |

| Total from investment operations | .320 | .918 | (.163) | (.048) | .448 | .207 |

| Distributions from net investment income | (.100) | (.228) | (.197) | (.176) | (.183) | (.149) |

| Distributions from net realized gain | – | – | – | (.076) | (.095) | (.028) |

| Total distributions | (.100) | (.228) | (.197) | (.252) | (.278) | (.177) |

| Net asset value, end of period | $10.90 | $10.68 | $9.99 | $10.35 | $10.65 | $10.48 |

| Total ReturnB,C | 3.03% | 9.33% | (1.58)% | (.42)% | 4.35% | 1.99% |

| Ratios to Average Net AssetsD,E | ||||||

| Expenses before reductions | .45%F | .45% | .45% | .45% | .45% | .45% |

| Expenses net of fee waivers, if any | .45%F | .45% | .45% | .45% | .45% | .45% |

| Expenses net of all reductions | .45%F | .45% | .45% | .45% | .45% | .45% |

| Net investment income (loss) | 1.89%F | 2.29% | 1.96% | 1.76% | 1.59% | 1.51% |

| Supplemental Data | ||||||

| Net assets, end of period (in millions) | $2,228 | $2,633 | $2,964 | $3,467 | $3,896 | $3,489 |

| Portfolio turnover rateG | 313%F,H | 246% | 123% | 157% | 93% | 83% |

A Calculated based on average shares outstanding during the period.

B Total returns for periods of less than one year are not annualized.

C Total returns would have been lower if certain expenses had not been reduced during the applicable periods shown.

D Fees and expenses of any underlying Fidelity Central Funds are not included in the Fund's expense ratio. The Fund indirectly bears its proportionate share of the expenses of any underlying Fidelity Central Funds. Based on their most recent shareholder report date, the expenses of any underlying non-money market Fidelity Central Funds were .01%.

E Expense ratios reflect operating expenses of the class. Expenses before reductions do not reflect amounts reimbursed by the investment adviser or reductions from expense offset arrangements and do not represent the amount paid by the class during periods when reimbursements or reductions occur. Expenses net of fee waivers reflect expenses after reimbursement by the investment adviser but prior to reductions from expense offset arrangements. Expenses net of all reductions represent the net expenses paid by the class.

F Annualized

G Amount does not include the portfolio activity of any underlying Fidelity Central Funds.

H Portfolio turnover rate excludes securities received or delivered in-kind.

See accompanying notes which are an integral part of the financial statements.

Fidelity Government Income Fund Class I

| Six months ended (Unaudited) February 29, | Years endedAugust 31, | |||||

| 2020 | 2019 | 2018 | 2017 | 2016 | 2015 | |

| Selected Per–Share Data | ||||||

| Net asset value, beginning of period | $10.70 | $10.00 | $10.36 | $10.66 | $10.50 | $10.47 |

| Income from Investment Operations | ||||||

| Net investment income (loss)A | .099 | .228 | .194 | .177 | .162 | .154 |

| Net realized and unrealized gain (loss) | .220 | .696 | (.361) | (.230) | .271 | .048 |

| Total from investment operations | .319 | .924 | (.167) | (.053) | .433 | .202 |

| Distributions from net investment income | (.099) | (.224) | (.193) | (.171) | (.178) | (.144) |

| Distributions from net realized gain | – | – | – | (.076) | (.095) | (.028) |

| Total distributions | (.099) | (.224) | (.193) | (.247) | (.273) | (.172) |

| Net asset value, end of period | $10.92 | $10.70 | $10.00 | $10.36 | $10.66 | $10.50 |

| Total ReturnB,C | 3.00% | 9.38% | (1.61)% | (.46)% | 4.19% | 1.94% |

| Ratios to Average Net AssetsD,E | ||||||

| Expenses before reductions | .49%F | .49% | .49% | .49% | .50% | .50% |

| Expenses net of fee waivers, if any | .49%F | .49% | .49% | .49% | .50% | .50% |

| Expenses net of all reductions | .49%F | .49% | .49% | .49% | .50% | .50% |

| Net investment income (loss) | 1.86%F | 2.25% | 1.92% | 1.71% | 1.54% | 1.46% |

| Supplemental Data | ||||||

| Net assets, end of period (in millions) | $292 | $407 | $411 | $496 | $494 | $412 |

| Portfolio turnover rateG | 313%F,H | 246% | 123% | 157% | 93% | 83% |

A Calculated based on average shares outstanding during the period.

B Total returns for periods of less than one year are not annualized.

C Total returns would have been lower if certain expenses had not been reduced during the applicable periods shown.

D Fees and expenses of any underlying Fidelity Central Funds are not included in the Fund's expense ratio. The Fund indirectly bears its proportionate share of the expenses of any underlying Fidelity Central Funds. Based on their most recent shareholder report date, the expenses of any underlying non-money market Fidelity Central Funds were .01%.

E Expense ratios reflect operating expenses of the class. Expenses before reductions do not reflect amounts reimbursed by the investment adviser or reductions from expense offset arrangements and do not represent the amount paid by the class during periods when reimbursements or reductions occur. Expenses net of fee waivers reflect expenses after reimbursement by the investment adviser but prior to reductions from expense offset arrangements. Expenses net of all reductions represent the net expenses paid by the class.

F Annualized

G Amount does not include the portfolio activity of any underlying Fidelity Central Funds.

H Portfolio turnover rate excludes securities received or delivered in-kind.

See accompanying notes which are an integral part of the financial statements.

Fidelity Government Income Fund Class Z

| Six months ended (Unaudited) February 29, | Year endedAugust 31, | |

| 2020 | 2019 A | |

| Selected Per–Share Data | ||

| Net asset value, beginning of period | $10.70 | $9.91 |

| Income from Investment Operations | ||

| Net investment income (loss)B | .104 | .198 |

| Net realized and unrealized gain (loss) | .221 | .808 |

| Total from investment operations | .325 | 1.006 |

| Distributions from net investment income | (.105) | (.216) |

| Distributions from net realized gain | – | – |

| Total distributions | (.105) | (.216) |

| Net asset value, end of period | $10.92 | $10.70 |

| Total ReturnC,D | 3.07% | 10.27% |

| Ratios to Average Net AssetsE,F | ||

| Expenses before reductions | .40%G | .40%G |

| Expenses net of fee waivers, if any | .36%G | .36%G |

| Expenses net of all reductions | .36%G | .36%G |

| Net investment income (loss) | 1.99%G | 2.27%G |

| Supplemental Data | ||

| Net assets, end of period (in millions) | $563 | $139 |

| Portfolio turnover rateH | 313%G,I | 246% |

A For the period October 2, 2018 (commencement of sale of shares) to August 31, 2019.

B Calculated based on average shares outstanding during the period.

C Total returns for periods of less than one year are not annualized.

D Total returns would have been lower if certain expenses had not been reduced during the applicable periods shown.

E Fees and expenses of any underlying Fidelity Central Funds are not included in the Fund's expense ratio. The Fund indirectly bears its proportionate share of the expenses of any underlying Fidelity Central Funds. Based on their most recent shareholder report date, the expenses of any underlying non-money market Fidelity Central Funds were .01%.

F Expense ratios reflect operating expenses of the class. Expenses before reductions do not reflect amounts reimbursed by the investment adviser or reductions from expense offset arrangements and do not represent the amount paid by the class during periods when reimbursements or reductions occur. Expense ratios before reductions for start-up periods may not be representative of longer-term operating periods. Expenses net of fee waivers reflect expenses after reimbursement by the investment adviser but prior to reductions from expense offset arrangements. Expenses net of all reductions represent the net expenses paid by the class.

G Annualized

H Amount does not include the portfolio activity of any underlying Fidelity Central Funds.

I Portfolio turnover rate excludes securities received or delivered in-kind.

See accompanying notes which are an integral part of the financial statements.

Notes to Financial Statements (Unaudited)

For the period ended February 29, 2020

(Amounts in thousands except percentages)

1. Organization.

Fidelity Government Income Fund (the Fund) is a fund of Fidelity Income Fund (the Trust) and is authorized to issue an unlimited number of shares. The Trust is registered under the Investment Company Act of 1940, as amended (the 1940 Act), as an open-end management investment company organized as a Massachusetts business trust. The Fund offers Class A, Class M, Class C, Government Income, Class I and Class Z shares, each of which has equal rights as to assets and voting privileges. Each class has exclusive voting rights with respect to matters that affect that class. Effective March 1, 2019, Class C shares will automatically convert to Class A shares after a holding period of ten years from the initial date of purchase, with certain exceptions.

Effective January 1, 2020:

Investment advisers Fidelity Investments Money Management, Inc., FMR Co., Inc., and Fidelity SelectCo, LLC, merged with and into Fidelity Management & Research Company. In connection with the merger transactions, the resulting, merged investment adviser was then redomiciled from Massachusetts to Delaware, changed its corporate structure from a corporation to a limited liability company, and changed its name to "Fidelity Management & Research Company LLC".

Broker-dealer Fidelity Distributors Corporation merged with and into Fidelity Investments Institutional Services Company, Inc. ("FIISC"). FIISC was then redomiciled from Massachusetts to Delaware, changed its corporate structure from a corporation to a limited liability company, and changed its name to "Fidelity Distributors Company LLC".

Fidelity Investments Institutional Operations Company, Inc. converted from a Massachusetts corporation to a Massachusetts LLC, and changed its name to "Fidelity Investments Institutional Operations Company LLC".

2. Investments in Fidelity Central Funds.

The Fund invests in Fidelity Central Funds, which are open-end investment companies generally available only to other investment companies and accounts managed by the investment adviser and its affiliates. The Fund's Schedule of Investments lists each of the Fidelity Central Funds held as of period end, if any, as an investment of the Fund, but does not include the underlying holdings of each Fidelity Central Fund. As an Investing Fund, the Fund indirectly bears its proportionate share of the expenses of the underlying Fidelity Central Funds.

Based on its investment objective, each Fidelity Central Fund may invest or participate in various investment vehicles or strategies that are similar to those of the Fund. These strategies are consistent with the investment objectives of the Fund and may involve certain economic risks which may cause a decline in value of each of the Fidelity Central Funds and thus a decline in the value of the Fund. The Money Market Central Funds seek preservation of capital and current income and are managed by the investment adviser. Annualized expenses of the Money Market Central Funds as of their most recent shareholder report date ranged from less than .005% to .01%. The following summarizes the Fund's investment in each non-money market Fidelity Central Fund.

| Fidelity Central Fund | Investment Manager | Investment Objective | Investment Practices | Expense Ratio(a) |

| Fidelity Mortgage Backed Securities Central Fund | FMR | Seeks a high level of income by normally investing in investment-grade mortgage-related securities and repurchase agreements for those securities. | Delayed Delivery & When Issued Securities Futures Options Swaps | .01% |

(a) Expenses expressed as a percentage of average net assets and are as of each underlying Central Fund's most recent annual or semi-annual shareholder report.

An unaudited holdings listing for the Fund, which presents direct holdings as well as the pro-rata share of any securities and other investments held indirectly through its investment in underlying non-money market Fidelity Central Funds, is available at fidelity.com and/or institutional.fidelity.com, as applicable. A complete unaudited list of holdings for each Fidelity Central Fund is available upon request or at the Securities and Exchange Commission (the SEC) website at www.sec.gov. In addition, the financial statements of the Fidelity Central Funds which contain the significant accounting policies (including investment valuation policies) of those funds are available on the SEC website or upon request.

3. Significant Accounting Policies.

The Fund is an investment company and applies the accounting and reporting guidance of the Financial Accounting Standards Board (FASB) Accounting Standards Codification Topic 946 Financial Services – Investments Companies. The financial statements have been prepared in conformity with accounting principles generally accepted in the United States of America (GAAP), which require management to make certain estimates and assumptions at the date of the financial statements. Actual results could differ from those estimates. Subsequent events, if any, through the date that the financial statements were issued have been evaluated in the preparation of the financial statements. The following summarizes the significant accounting policies of the Fund:

Investment Valuation. Investments are valued as of 4:00 p.m. Eastern time on the last calendar day of the period. The Board of Trustees (the Board) has delegated the day to day responsibility for the valuation of the Fund's investments to the Fair Value Committee (the Committee) established by the Fund's investment adviser. In accordance with valuation policies and procedures approved by the Board, the Fund attempts to obtain prices from one or more third party pricing vendors or brokers to value its investments. When current market prices, quotations or currency exchange rates are not readily available or reliable, investments will be fair valued in good faith by the Committee, in accordance with procedures adopted by the Board. Factors used in determining fair value vary by investment type and may include market or investment specific events, changes in interest rates and credit quality. The frequency with which these procedures are used cannot be predicted and they may be utilized to a significant extent. The Committee oversees the Fund's valuation policies and procedures and reports to the Board on the Committee's activities and fair value determinations. The Board monitors the appropriateness of the procedures used in valuing the Fund's investments and ratifies the fair value determinations of the Committee.

The Fund categorizes the inputs to valuation techniques used to value its investments into a disclosure hierarchy consisting of three levels as shown below:

- Level 1 – quoted prices in active markets for identical investments