QuickLinks -- Click here to rapidly navigate through this document

Exhibit 22.1

Notice of Annual and Special Meeting of Shareholders

| Date: | Thursday, May 5, 2016 |

Time: |

10:00 a.m. (Toronto time) |

Place: |

The Westin Prince 900 York Mills Road Toronto, Ontario Canada |

The Meeting is being held to:

| 1. | receive Magna's consolidated financial statements and the independent auditors' report thereon for the fiscal year ended December 31, 2015; | |

2. |

elect ten directors; |

|

3. |

reappoint Deloitte LLP as our independent auditors and authorize the Audit Committee to fix the independent auditors' remuneration; |

|

4. |

vote, in an advisory, non-binding manner, on Magna's approach to executive compensation described in the accompanying Management Information Circular/Proxy Statement; |

|

5. |

vote on a special resolution to approve the amendment of Magna's articles of incorporation; |

|

6. |

vote on a resolution ratifying and confirming a new general by-law; and |

|

7. |

transact any other business that may properly come before the Meeting. |

As a holder of record of Magna Common Shares at the close of business on March 18, 2016, you are entitled to receive notice of and vote at the Meeting.

If you are unable to attend the Meeting and want to ensure that your shares are voted, please submit your votes by proxy as described under "How to Vote Your Shares" in the accompanying circular. To be valid, our transfer agent, Computershare Trust Company of Canada, must receive your proxy by 5:00 p.m. (Toronto time) on May 3, 2016. If the Meeting is adjourned or postponed, Computershare must receive your proxy not later than 48 hours (excluding Saturdays, Sundays and holidays) prior to the time of the adjourned or postponed Meeting. The time limit for deposit of proxies may be waived or extended by the Chair of the Meeting at his or her discretion, without notice.

A live webcast of the Meeting will also be available through Magna's website at www.magna.com.

Accompanying this Notice of Annual and Special Meeting is Magna's Management Information Circular/Proxy Statement, which contains more information on the matters to be addressed at the Meeting.

By order of the Board of Directors.

/s/ "Bassem A. Shakeel" |

|

| March 28, 2016 | BASSEM A. SHAKEEL |

| Aurora, Ontario | Vice-President and Corporate Secretary |

Management Information Circular/Proxy Statement

This Circular is being provided to you in connection with the Annual and Special Meeting of Magna's shareholders (the "Meeting"), which will be held on Thursday, May 5, 2016 commencing at 10:00 a.m. (Toronto time) at The Westin Prince, 900 York Mills Road, Toronto, Ontario, Canada.

Voting Information

| Record Date | March 18, 2016 is the record date for the Meeting (the "Record Date"). Only holders of our Common Shares as of the close of business on the Record Date are entitled to receive notice of and to attend (in person or by proxy) and vote at the Meeting. | |

Shares and Votes |

As of the Record Date, 398,592,739 Magna Common Shares were issued and outstanding. Each Magna Common Share is entitled to one vote. |

|

Principal Shareholders |

To our knowledge, no shareholder beneficially owns or exercises control or direction, directly or indirectly, over 10% or more of Magna's Common Shares outstanding as at the Record Date. |

|

All of Magna's directors and executive officers as a group (19 persons) owned beneficially or exercised control or direction over 3,155,005 Common Shares representing approximately 0.8% of the class as at the Record Date. |

||

The Magna Deferred Profit Sharing Plan (Canada) and Employees Deferred Profit Sharing Plan (U.S.) (the "NADPSPs"), deferred profit sharing plans for Magna's participating employees, collectively hold 20,678,502 Magna Common Shares representing approximately 5.2% of the class as at the Record Date. The shares held by the NADPSPs will be voted FOR each of the items to be voted on at the Meeting. |

Meeting Information 3

How To Vote Your Shares

| Your Vote Is Important | Your vote is important. Please read the information below to ensure your shares are properly voted. | |

Registered vs. Non-Registered Shareholder |

How you vote your shares depends on whether you are a registered shareholder or a non-registered shareholder. In either case, there are two ways you can vote at the Meeting – by appointing a proxyholder or by attending in person, although the specifics may differ slightly. |

|

Registered Shareholder: You are a registered shareholder if you hold one or more share certificates which indicate your name and the number of Magna Common Shares which you own. As a registered shareholder, you will receive a form of proxy from Computershare Trust Company of Canada ("Computershare") representing the shares you hold. If you are a registered shareholder, refer to "How to Vote – Registered Shareholders". |

||

Non-Registered Shareholder: You are a non-registered shareholder if a securities dealer, broker, bank, trust company or other nominee holds your shares for you, or for someone else on your behalf. As a non-registered shareholder, you will most likely receive a Voting Instruction Form from either Broadridge Canada or Broadridge US, although in some cases you may receive a form of proxy from the securities dealer, broker, bank, trust company or other nominee holding your shares. If you are a non-registered shareholder, refer to "How to Vote – Non-Registered Shareholders". |

||

Proxies Are Being Solicited by Management |

Management is soliciting your proxy in connection with the matters to be addressed at the Meeting (or any adjournment(s) or postponement(s) thereof) to be held at the time and place set out in the accompanying Notice of Annual Meeting. We will bear all costs incurred in connection with Management's solicitation of proxies, including the cost of preparing and mailing this Circular and accompanying materials. Proxies will be solicited primarily by mail, although our officers and employees may (for no additional compensation) also directly solicit proxies by phone, fax or other electronic methods. Banks, brokerage houses and other custodians, nominees or fiduciaries will be requested to forward proxy solicitation material to the persons on whose behalf they hold Magna shares and to obtain authorizations for the execution of proxies. These institutions will be reimbursed for their reasonable expenses in doing so. |

|

Proxy Solicitor – Kingsdale |

Magna has also retained Kingsdale as proxy solicitation agent and will pay a fee of C$22,050 for such service, in addition to certain out-of-pocket expenses. Magna may also reimburse brokers and other persons holding Common Shares in their name or in the name of nominees for their costs incurred in sending proxy material to their principals in order to obtain their proxies. If you have any questions about the information contained in this Circular or need assistance in completing your proxy form, please contact Kingsdale by e-mail at contactus@kingsdaleshareholder.com or at the following telephone numbers: |

|

• within Canada or the U.S. (toll-free): 1-888-518-1552 |

||

• outside Canada and the U.S. (by collect call): 416-867-2272 |

4 Meeting Information

These securityholder materials are being sent to both registered

and non-registered owners of Magna Common Shares.

HOW TO VOTE – REGISTERED SHAREHOLDERS |

HOW TO VOTE – NON-REGISTERED SHAREHOLDERS |

|

|---|---|---|

| If you are a registered shareholder, you may vote either by proxy or in person at the Meeting. Submitting Votes by Proxy There are three ways to submit your vote by proxy: in accordance with the instructions on the form of proxy. If you are voting by phone or internet, you will need the pre-printed Control Number, Holder Account Number and Access Number on your form of proxy. A proxy submitted by mail must be in writing, dated the date on which you signed it and be signed by you (or your authorized attorney). If such a proxy is being submitted on behalf of a corporate shareholder, the proxy must be signed by an authorized officer or attorney of that corporation. If a proxy submitted by mail is not dated, it will be deemed to bear the date on which it was sent to you. If you are voting your shares by proxy, you must ensure that your completed and signed proxy form or your phone or internet vote is received by Computershare not later than 5:00 p.m. (Toronto time) on May 3, 2016. If the Meeting is adjourned or postponed, you must ensure that your completed and signed proxy form or your phone or internet vote is received by Computershare not later than 48 hours (excluding Saturdays, Sundays and holidays) prior to the time of the Meeting. Appointment of Proxyholder Unless you specify a different proxyholder or specify how you want your shares to be voted, the Magna officers whose names are pre-printed on the form of proxy will vote your shares: • FOR the election to the Magna Board of Directors of all of the nominees named in this Circular; • FOR the reappointment of Deloitte as Magna's independent auditors and the authorization of the Audit Committee to fix the independent auditors' remuneration; • FOR the advisory resolution to accept the approach to executive compensation disclosed in this Circular; • FOR the special resolution amending the articles; and • FOR the resolution ratifying and confirming the new general by-law. You have the right to appoint someone else (who need not be a shareholder) as your proxyholder; however, if you do, that person must vote your shares in person on your behalf at the Meeting. To appoint someone else as your proxyholder, insert the person's name in the blank space provided on the form of proxy or complete, sign, date and submit another proper form of proxy naming that person as your proxyholder. |

If you are a non-registered shareholder, the intermediary holding on your behalf (and not Magna) has assumed responsibility for (i) delivering these materials to you and (ii) executing your

proper voting instructions. Submitting Voting Instructions There are three ways to submit your vote by Voting Instruction Form: in accordance with the instructions on the Voting Instruction Form. If you are a non-registered shareholder and have received a Voting Instruction Form from Broadridge, you must complete and submit your vote by phone, internet or mail, in accordance with the instructions on the form. We have been advised by Broadridge that, on receipt of a properly completed and submitted form, a form of proxy will be submitted on your behalf. You must ensure that your completed, signed and dated Voting Instruction Form or your phone or internet vote is received by no later than any deadline specified by Broadridge, which we expect will be 5:00 p.m. (Toronto time) on May 2, 2016. If the Meeting is adjourned or postponed, you must ensure that your completed, signed and dated Voting Instruction Form or your phone or internet vote is received by Broadridge Canada or Broadridge US, as applicable, not later than 72 hours (excluding Saturdays, Sundays and holidays) prior to the time of the Meeting. If a Voting Instruction Form submitted by mail or fax is not dated, it will be deemed to bear the date on which it was sent to you. In some cases, you may have received a form of proxy instead of a Voting Instruction Form, even though you are a non-registered shareholder. Such a form of proxy will likely be stamped by the securities dealer, broker, bank, trust company or other nominee or intermediary holding your shares and be restricted as to the number of shares to which it relates. In this case, you must complete the form of proxy and submit it to Computershare as described to the left under "How to Vote – Registered Shareholders – Submitting Votes By Proxy". |

Meeting Information 5

HOW TO VOTE – REGISTERED SHAREHOLDERS (cont'd) |

HOW TO VOTE – NON-REGISTERED SHAREHOLDERS (cont'd) |

|

|---|---|---|

| Appointment of Proxyholder (cont'd) If you choose to vote by proxy, you are giving the person (referred to as a "proxyholder") or people named on your form of proxy the authority to vote your shares on your behalf at the Meeting (including any adjournment or postponement of the Meeting). You may indicate on the form of proxy how you want your proxyholder to vote your shares, or you can let your proxyholder decide for you. If you do not specify on the form of proxy how you want your shares to be voted, your proxyholder will have the discretion to vote your shares as they see fit. The form of proxy accompanying this Circular gives the proxyholder discretion with respect to any amendments or changes to matters described in the Notice of Annual Meeting and with respect to any other matters which may properly come before the Meeting (including any adjournment or postponement of the Meeting). As of the date of this Circular, we are not aware of any amendments, changes or other matters to be addressed at the Meeting. Voting in Person If you attend in person, you do not need to complete or return your form of proxy. When you arrive at the Meeting, a Computershare representative will register your attendance before you enter the Meeting. If you vote in person at the Meeting and had previously completed and returned your form of proxy, your proxy will be automatically revoked and any votes you cast on a poll at the Meeting will count. Revoking a Vote Made by Proxy You have the right to revoke a proxy by ANY of the following methods: • Vote again by phone or internet not later than 5:00 p.m. (Toronto time) on May 3, 2016 (or not later than 48 hours prior to the time of the adjourned or postponed Meeting); • Deliver by mail another completed and signed form of proxy, dated later than the first form of proxy, such that it is received by Computershare not later than 5:00 p.m. (Toronto time) on May 3, 2016 (or not later than 48 hours prior to the time of the adjourned or postponed Meeting); • Deliver to us at the following address a signed written notice revoking the proxy, provided it is received not later than 5:00 p.m. (Toronto time) on May 4, 2016 (or not later than 5:00 p.m. on the last business day prior to the date of the adjourned or postponed Meeting): Magna International Inc. 337 Magna Drive Aurora, Ontario, Canada L4G 7K1 Attention: Corporate Secretary • Deliver a signed written notice revoking the proxy to the scrutineers of the Meeting, to the attention of the Chair of the Meeting, at or prior to the commencement of the Meeting (including in the case of any adjournment or postponement of the Meeting). |

Voting in Person If you have received a Voting Instruction Form from your Canadian intermediary and wish to attend the Meeting in person or have someone else attend on your behalf, you must complete, sign and return the Voting Instruction Form or complete the equivalent electronic form online, in each case in accordance with the instructions on the form. If you have received a Voting Instruction Form from your US intermediary and wish to attend the Meeting in person or have someone else attend on your behalf, you must complete, sign and return the Voting Instruction Form in accordance with the instructions on the form. Your intermediary will send you a legal proxy giving you or your designate the right to attend the meeting. If you have received a form of proxy and wish to attend the Meeting in person or have someone else attend on your behalf, you must insert your name, or the name of the person you wish to attend on your behalf, in the blank space provided on the form of proxy. If you are voting your shares by proxy, you must ensure that your completed and signed proxy form or your phone or internet vote is received by Computershare not later than 5:00 p.m. (Toronto time) on May 3, 2016. If the Meeting is adjourned or postponed, you must ensure that: • your completed and signed Voting Instruction Form (or equivalent electronic form online) is received by Broadridge Canada or Broadridge US, as applicable, not later than 72 hours (excluding Saturdays, Sundays and holidays) prior to the time of the adjourned or postponed Meeting; or • your completed and signed proxy form or your phone or internet vote is received by Computershare not later than 48 hours (excluding Saturdays, Sundays and holidays) prior to any adjournment or postponement of the Meeting. When you arrive at the Meeting, a Computershare representative will register your attendance before you enter the Meeting. Revoking a Voting Instruction Form or Proxy If you wish to revoke a Voting Instruction Form or form of proxy for any matter on which a vote has not already been cast, you must contact your securities dealer, broker, bank, trust company or other nominee or intermediary (for a form of proxy sent to you by such intermediary) and comply with any applicable requirements relating to the revocation of votes made by Voting Instruction Form or proxy. |

6 Meeting Information

Business of the Meeting

Purpose of the Meeting |

The Meeting is being held for shareholders to: 1. receive Magna's consolidated financial statements and the independent auditors' report thereon for the fiscal year ended December 31, 2015; |

|

2. elect ten directors; |

||

3. reappoint Deloitte as our independent auditors and authorize the Audit Committee to fix the independent auditors' remuneration; |

||

4. vote, in an advisory, non-binding manner, on Magna's approach to executive compensation described in this Circular; |

||

5. vote on a special resolution to approve the amendment of Magna's articles of incorporation; |

||

6. vote on a resolution ratifying and confirming a new general by-law; and |

||

7. transact any other business that may properly come before the Meeting. |

||

As of the date of this Circular, we are not aware of any other business to be transacted at the Meeting. |

||

1. Financial Statements |

Magna's consolidated financial statements and the independent auditors' report thereon for the fiscal year ended December 31, 2015 are included in the Annual Report, which was provided to shareholders with this Circular. The financial statements will be presented at the Meeting, but no shareholder vote is required in connection with them. |

|

2. Election of Directors |

Directors are elected by shareholders to act as stewards of the company. The Board is Magna's highest decision-making body, except to the extent certain rights have been reserved for shareholders under applicable law or Magna's articles of incorporation or by-laws. Among other things, the Board is responsible for appointing our Chief Executive Officer and overseeing Management. In fulfilling their duties, directors are required under applicable law to act in the best interests of the company. |

|

Board Size and Term |

||

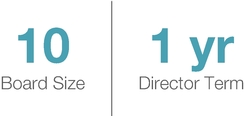

The CGCNC is responsible for making recommendations to the Board regarding optimal Board size and candidates for service on the Board. Some of the factors relevant to the CGCNC's consideration of optimal Board size include the scale and complexity of Magna's business, the markets in which it operates, the company's strategic priorities, the need for a diverse range of skills and perspectives, Committee staffing needs and other factors. Magna's articles of incorporation permit the Board to determine its size within a range of five to fifteen directors. Over the last ten years, the Board size has ranged between nine and fourteen, with an average of eleven directors. The number of directors to be elected at the Meeting is ten and the CGCNC believes that to be an appropriate size at the present time. |

||

Meeting Information 7

|

Each director is elected for a one-year term expiring at our next annual meeting of shareholders.

Minimum Qualifications for Service as a Director of Magna In addition to the minimum qualifications specified in the OBCA, our Board Charter requires that each director possess the following attributes: • personal and professional integrity; • significant achievement in his or her field; • experience and expertise relevant to our business; • a reputation for sound and mature business judgment; • the commitment and ability to devote the necessary time and effort in order to conduct his or her duties effectively; and • financial literacy. |

|

2016 Nominees The CGCNC has unanimously recommended, and the Board has unanimously approved, the nomination of the following individuals for election at the Meeting: |

| • Scott B. Bonham • Peter G. Bowie • Hon. J. Trevor Eyton • Lady Barbara Judge • Dr. Kurt J. Lauk |

• Cynthia A. Niekamp • Dr. Indira V. Samarasekera • Donald J. Walker • Lawrence D. Worrall • William L. Young |

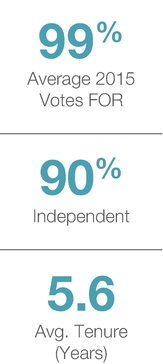

All of the nominees for election at the Meeting were previously elected at our 2015 annual meeting of shareholders. On average, the nominees received 99% support at our 2015 annual meeting of shareholders. Two of our directors (Ms. Samarasekera and Mr. Bonham) serve together on one other board, but no directors serve on any other board together with a member of Magna's Management. |

||

One director who was elected at our 2015 annual meeting of shareholders, V. Peter Harder, resigned effective March 21, 2016 to accept an appointment to the Senate of Canada and thus is not standing for re-election. |

||

8 Meeting Information

In recommending the ten nominees to the Board, the CGCNC considered a number of factors, including: • the nominees' respective skills, expertise and experience, as well as the extent to which the nominees meet the minimum qualifications described above; • results of the Board's annual self-assessment process, which incorporates both a self-evaluation and a peer review process; • individual voting results from the 2015 annual meeting; and • feedback from the Board's independent advisors and others. The CGCNC and the Board are confident that each of the ten nominees: • exceeds the minimum requirements set out in our Board Charter and the OBCA; • has skills, experience and expertise that provide the Board with the necessary insight to effectively carry out its mandate; and • will, if elected, provide responsible oversight as a steward of the corporation, including prudent oversight of Management. Refer to "Nominees for Election to the Board" for detailed information regarding the skills, expertise and other relevant information which you should consider in casting your vote for each nominee. |

||

CGCNC / Board Recommendation |

||

The CGCNC and the Board of Directors unanimously recommend that shareholders vote FOR the election of each nominee listed above and described in detail in "Nominees for Election to the Board" below. |

||

Unless otherwise instructed, the Magna officers whose names have been pre-printed on the form of proxy or Voting Instruction Form intend to vote FOR each such nominee. |

||

Individual Elections, Majority Voting and Disclosure of Voting Results |

||

|

At the Meeting, you will have the opportunity to vote for each nominee individually. We do not utilize slate voting. Under Ontario corporate law, shareholders can only vote "for" or "withhold" (i.e. abstain) their vote for director nominees. As a result, a single "for" vote can result in a nominee being elected, no matter how many votes were withheld. We have adopted a majority voting policy under which we treat "withhold" votes as if they were votes against a nominee in the case of an uncontested election (i.e. one in which the number of nominees equals the number of Board positions). A nominee who receives more "withhold" votes than "for" votes must promptly tender a resignation to the Chair of the CGCNC for its consideration. Our majority voting policy is described in further detail below under "Corporate Governance" and each nominee has agreed to abide by such policy. Detailed voting results are promptly disclosed after shareholder meetings, so that shareholders can easily understand the level of support for each nominee, as well as each other item of business at the meeting. |

|

Meeting Information 9

3. Reappointment of Deloitte as Magna's Independent Auditors |

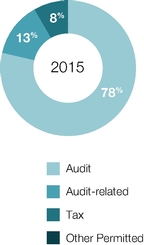

Deloitte, an Independent Registered Public Accounting Firm, was first appointed Magna's independent auditors on May 8, 2014 and has audited Magna's consolidated financial statements for the fiscal years ended December 31, 2014 and 2015. Services provided by independent auditors may fall into one of the following categories: |

|

Audit Services: |

services performed in order to comply with the standards of the Public Company Accounting Oversight Board (United States) ("PCAOB"), including integrated audit of the consolidated financial statements, quarterly reviews and statutory audits of foreign subsidiaries. In some cases, these may include an appropriate allocation of fees for tax services or accounting consultations, to the extent such services were necessary to comply with the standards of the PCAOB. This category includes the audit of our internal control over financial reporting for purposes of Section 404 of the Sarbanes-Oxley Act of 2002. |

|

Audit- Related Services: |

assurance and related services, including such things as due diligence relating to mergers and acquisitions, accounting consultations and audits in connection with acquisitions, attest services that are not required by statute or regulation and consultation concerning financial accounting and reporting standards. Audit-related services actually provided by Deloitte in respect of 2015 consisted of: assurance services and procedures related to the audit of carve-out financial statements for Magna's interiors business, issuance of comfort letters for prospectus supplements, assessments in connection with the COSO 2013 Internal Controls Integrated Framework and other assurance services. |

|

Tax Services: |

tax compliance, planning and advisory services, excluding any such services required in order to comply with the standards of the PCAOB which are included under "Audit Services". The tax services actually provided by Deloitte in respect of 2015 consisted of: domestic and international tax advisory, compliance and research services, as well as transfer pricing advisory services. |

|

Other Permitted Services: |

all permitted services not falling under any of the previous categories. |

|

10 Meeting Information

|

Deloitte's Independence In order to protect Deloitte's independence from being compromised by engagements for other services, the Audit Committee has established and maintains a process for the review and pre-approval of all services and related fees to be paid to Deloitte. Pursuant to this approval process, the Audit Committee approved and Magna was billed the following fees for services provided by Deloitte in respect of 2015: |

| 2015 | 2014 | |||||||

| TYPE OF SERVICES |

FEES ($) |

% OF TOTAL |

FEES ($) |

% OF TOTAL |

||||

| Audit | 10,016,000 | 78 | 12,159,000 | 91 | ||||

| Audit-related | 1,726,000 | 13 | 99,000 | 1 | ||||

| Tax | 1,044,000 | 8 | 1,075,000 | 8 | ||||

| Other Permitted | 49,000 | <1 | 4,000 | <1 | ||||

| Total | 12,835,000 | 100 | 13,337,000 | 100 | ||||

The Audit Committee has also established a process to pre-approve the future hiring (if any) of current and former partners and employees of Deloitte engaged on Magna's account. No such partners or employees were hired in 2015. |

||

Audit Committee Recommendation |

||

The Audit Committee unanimously recommends that shareholders vote FOR the resolution reappointing Deloitte as Magna's independent auditors and authorizing the Audit Committee to fix Deloitte's remuneration. |

||

Unless otherwise instructed, the persons designated in the form of proxy or Voting Instruction Form intend to vote FOR the resolution reappointing Deloitte. |

||

Representatives of Deloitte are expected to attend the Meeting, will have the opportunity to make a statement if they so desire and are expected to be available to respond to appropriate questions from shareholders. |

||

Meeting Information 11

4. Advisory Vote on Approach to Executive Compensation |

At the Meeting, shareholders will again have the opportunity to cast an advisory, non-binding vote on Magna's approach to executive compensation – this is often referred to as "say on pay". Although the vote is non-binding, the CGCNC will consider the results when assessing future compensation decisions. The text of the resolution reads as follows: "Resolved, on an advisory basis and not to diminish the roles and responsibilities of the board of directors, that the shareholders accept the approach to executive compensation disclosed in the accompanying Management Information Circular/Proxy Statement." |

|

Our approach to executive compensation is set out in detail in the Compensation and Performance Report and the Compensation Discussion & Analysis in this Circular. Included in the Compensation and Performance Report is a detailed discussion and benchmarking results demonstrating the strong connection between executive compensation and corporate performance over a three-year period. We encourage you to carefully read these sections of this Circular. |

||

We most recently held an advisory vote on executive compensation at our May 7, 2015 annual meeting of shareholders. The say on pay resolution was supported by a significant majority (93%) of the votes cast on the resolution. |

||

Board Recommendation |

||

The Board of Directors unanimously recommends that shareholders vote FOR the resolution relating to Magna's approach to executive compensation. |

||

Unless otherwise instructed, the Magna officers whose names have been pre-printed on the form of proxy or Voting Instruction Form intend to vote FOR such resolution. |

||

5. Amendment of Articles of Incorporation |

At the Meeting, shareholders will be asked to approve the following special resolution amending Magna's articles to remove the Corporate Constitution: "Resolved as a special resolution that the articles of the corporation be amended to remove the Corporate Constitution contained in Section 10 thereof." A special resolution requires the support of two-thirds of the votes cast at the Meeting. |

12 Meeting Information

Our Corporate Constitution was adopted by shareholders as part of the articles in 1984. At that time, Magna was a controlled company through a dual class share structure and, in that context, the Corporate Constitution served to balance the interests of various stakeholders, including shareholders, employees and management by prescribing their respective rights to participate in our profits. The Corporate Constitution also acted as a restraint on the exercise of voting power by our former controlling shareholder, who had sufficient votes through multiple voting shares to elect the entire board of directors. For example, one of the key features of the Corporate Constitution was a provision which gave minority shareholders the right to separately elect two directors to our Board if we failed to fulfill certain obligations to shareholders. This provision was deleted from the Corporate Constitution when Magna became a widely-held company with a single class of shares in August 2010. In the years which followed the elimination of the dual class share structure, we have adopted multiple corporate governance best practices aimed at enhancing board oversight and direct accountability to shareholders, including a minimum two-thirds board independence requirement, majority voting and say on pay. In light of all of these factors, the Board believes that the Corporate Constitution is no longer necessary as it does not provide relevant or meaningful protections and its removal from our articles will not adversely affect the corporation or the rights of shareholders. The Corporate Constitution contains a dividend policy which requires distribution annually of 10% and, on average over a three-year period not less than 20%, of our after-tax profits. We intend to continue paying a quarterly dividend from our cash flow from operations, with the aim of regularly increasing the dividend consistent with our practice since 2010. The declaration and payment of dividends, including the dividend rate, is subject to the Board's discretion taking into account our cash flow, earnings, capital requirements, financial condition and other relevant factors. One element of the Corporate Constitution that remains relevant is the 10% profit sharing for eligible employees. Employee profit sharing remains a core element of our unique corporate culture and, accordingly, we intend to maintain it as a way of incenting, motivating and rewarding employees for their contribution to our success. Employee profit sharing remains entrenched in our Employee's Charter, a key continuing policy articulating our operating philosophy and approach towards employees. The Employee's Charter is reinforced by our Operational Principles, another continuing policy which articulates core elements of our operating philosophy and culture. Magna's unique culture, including the core principles on which the company's success was built, is not expected to change and will continue to be reflected in the Employee's Charter and Operational Principles. |

||

Board Recommendation |

||

The Board of Directors unanimously recommends that shareholders vote FOR the special resolution approving the amendment of Magna's articles of incorporation to remove the Corporate Constitution contained in Section 10 thereof. |

||

Unless otherwise instructed, the Magna officers whose names have been pre-printed on the form of proxy or Voting Instruction Form intend to vote FOR such special resolution. |

||

Meeting Information 13

6. Adoption of New General By-Laws |

Magna's former general by-law, By-Law No. 1B-92 (the "Former By-Law"), largely dates back to 1992, with minor amendments made in 2007 and 2010. The Former By-law did not reflect a state-of-the-art public company by-law, contained some provisions which reflected the company's prior status as a controlled company and omitted some elements which are advisable for a widely-held public company. Accordingly, Magna's Board adopted a new by-law on March 17, 2016 ("By-Law No. 1"), which is included as an appendix to this Circular, and shareholders are being asked to approve the following resolution at the Meeting: |

|

"Resolved that the repeal of By-Law 1B-92 and the adoption of By-Law No. 1 are hereby ratified and confirmed." |

||

The most significant change reflected in By-Law No. 1 is the inclusion of an advance notice provision relating to nominations of directors by shareholders. This advance notice provision has been drafted to comply with best practices in Canada aimed at: • enabling all shareholders to have sufficient notice regarding the intention of a shareholder to nominate one or more directors at a shareholder meeting; and • not unduly restricting shareholders from exercising their right to nominate directors. |

||

In order for a shareholder's nomination of a director to be valid, notice must generally be given to the company at least 30 days prior to the date of the company's annual shareholder meeting. Where an annual shareholder meeting has been called on less than 50 days' notice, a shareholder's nomination of a director will be valid if the shareholder notifies the company by the close of business on the tenth day following the first public announcement of the meeting. Where the company has called a special meeting, a shareholder's nomination of a director will be valid if the shareholder notifies the company by close of business on the fifteenth day following the first public announcement of the special shareholders' meeting. There is no maximum notice period for a shareholder's nomination of a director. |

||

In addition to the advance notice provision, By-Law No. 1 provides a more complete set of default rules relating to procedural matters than the Former By-Law, including: |

||

• Calling Directors' Meetings — each of the Chair, Chief Executive Officer and any director, or the Secretary on the direction of one of the foregoing, now has the power to call a directors' meeting. The Former By-Law did not permit any director (other than the Chair) to call a directors' meeting, requiring instead a quorum of such directors to call such a meeting. |

||

• Participation in Directors' Meetings by Electronic Means — By-Law No. 1 contains an express provision allowing directors to participate in directors' meetings by electronic means which permit simultaneous/instantaneous communication among participants. |

||

• Voting at Directors' Meetings — By-Law No. 1 expressly states that the Chair does not have a second/casting vote in the event of a deadlock on any matter voted on at a directors' meeting. |

14 Meeting Information

• Delegation to Board Committees — By-Law No. 1 lists specific matters which cannot lawfully be delegated to a committee of the board. |

||

• Issuance of Securities — in contemplation of the future transition away from physical share certificates for registered shareholders, By-Law No. 1 specifically gives the board the authority to provide by resolution that any securities of the company can be represented by uncertificated securities. |

||

• Shareholder Meetings by Electronic Means — similar to the provision allowing for directors' meetings held by electronic means, By-Law No. 1 expressly allows for shareholder meetings to be held by electronic means that permit all participants to adequately communicate with each other. |

||

• More Detailed Provisions Relating to Shareholder Meetings — By-Law No. 1 contains more detailed provisions relating to matters such as the notice period for shareholder meetings, the impact of an accidental omission in giving notice, rights of representatives of corporate shareholders, rights of joint security holders, the use and revocation of proxies, as well as matters relating to shareholder meeting procedure, including votes by show of hands and use of ballots. |

||

• Quorum and Voting at Shareholder Meetings — consistent with current best practices, By-Law No. 1 sets quorum for shareholder meetings at two shareholders representing at least 25% of the issued and outstanding votes eligible to be cast at the meeting. Additionally, in the event of a deadlock on any matter voted at a shareholder meeting, the Chair does not have a second/casting vote. |

||

• Unclaimed Dividends — By-Law No. 1 states that dividends which remain unclaimed two years after the date they were declared will be forfeited. The two-year period is consistent with the current statutory limitation period in Ontario, but represents a change from the six-year period under the Former By-Law, which reflected the former statutory limitation period. |

||

Board Recommendation |

||

The Board of Directors unanimously recommends that shareholders vote FOR the resolution ratifying and confirming the repeal of By-Law 1B-92 and the adoption of By-Law No. 1. |

||

Unless otherwise instructed, the Magna officers whose names have been pre-printed on the form of proxy or Voting Instruction Form intend to vote FOR such resolution. |

Meeting Information 15

Nominees for Election to the Board

Board Skills and Expertise

The CGCNC seeks to recruit candidates who reflect a diversity of skills, experience and perspectives which are relevant to Magna's business. While the specific mix may vary from time to time and alternative categories may be considered in addition to or instead of those below, the following skills and types of experience are generally sought by the CGCNC:

- •

- Accounting/Audit: accounting and audit expertise are valued in order to enable the Board to oversee Management's handling

of

financial and financial reporting matters, including by: critically assessing Magna's financial performance and projections; understanding the company's critical accounting policies, as well as

technical issues relevant to the internal and external audit; and evaluating the robustness of the company's internal controls.

- •

- Automotive: as substantially all of Magna's business is derived from sales within the automotive

industry, the CGCNC seeks

candidates who possess a solid understanding of industry dynamics on a global and regional basis, preferably gained through management or board service with the company's customers or with other

automotive suppliers. Automotive expertise also serves to align the Board with one of Magna's key strategic priorities – achieving World Class Manufacturing

excellence on a consistent basis, globally. From time to time, we may also consider candidates with experience in capital-intensive manufacturing industries, since the experience gained in such

industries is typically applicable to the automotive industry.

- •

- Emerging Markets: the CGCNC values candidates who have a track record of success in markets other than

North America and

Western Europe, since much of our and the automotive industry's growth is forecast to be in such markets. Priority markets include China and India, but the automotive industry continues to grow in

other markets such as Indonesia, Thailand and Turkey, as well as various countries in Eastern Europe.

- •

- Finance/Financial Advisory: while we generally seek to ensure that all candidates have a baseline level

of financial

literacy, we value candidates who have experience in senior financial roles and/or in financial advisory roles. Such experience enhances the Board's oversight of financial performance, assists it in

its assessment of strategic opportunities and risks and allows it to more effectively address issues relevant to capital and capital structure.

- •

- Governance/Board: in light of the competing demands of stakeholders and the increasingly complex

governance environment in

which public companies operate, the CGCNC values candidates who possess a sophisticated understanding of corporate governance practices and norms, and/or board expertise.

- •

- Large Cap Company: while experience with companies of different scale can be valuable, the CGCNC seeks candidates who have board, management and/or other applicable experience with companies that have a market capitalization in excess of $10 billion. Magna's own market capitalization significantly exceeds that threshold and the CGCNC's prioritization of large cap company experience reflects the fact that companies of such size face different challenges and opportunities than small and mid-cap companies.

16 Meeting Information

- •

- Legal/Regulatory/Public Policy: Magna operates in, and is required to comply with, the laws of dozens of countries around

the

world. Candidates who possess an understanding of different legal systems and regulatory perspectives are valued by the CGCNC since such experiences assist the Board in more effectively carrying out

its compliance oversight responsibilities. Additionally, the CGCNC values candidates with experience in relevant areas of government and public policy to support the Board in understanding the

regulatory trends shaping the automotive industry and assessing the company's strategic response to such trends.

- •

- Mergers & Acquisitions ("M&A"): the CGCNC views board-level M&A expertise as

critical to the Board's ability to

effectively fulfill its oversight responsibilities relating to corporate strategy, particularly since Magna intends to pursue strategic M&A opportunities in certain automotive product areas.

- •

- R&D/Innovation/Technology: Magna has a long history of developing and bringing to market innovative

automotive products and

manufacturing techniques which have been significant contributors to the company's historic success. The CGCNC seeks candidates with technological expertise and skill to support the Board in assessing

Magna's efforts to build upon its technological advantages and thus further enhance long-term value. Board-level expertise and skill in technology/innovation also serves to align the Board with one of

Magna's key strategic priorities – innovation.

- •

- Risk Management: the CGCNC seeks candidates with practical expertise in enterprise risk management

frameworks, systems,

processes, tools and techniques, to assist the Board in understanding and assessing the risks and opportunities faced by the company generally, including those inherent in its strategic plan.

- •

- Senior/Executive Leadership: the CGCNC seeks business and other leaders who have demonstrated

leadership, mature judgment,

operating success and an understanding of complex organizations in progressively challenging roles. Such individuals are believed to provide the most effective counsel to Management, as well as

critical oversight on behalf of stakeholders.

- •

- Strategy Development: recognizing the importance of the Board's oversight role with respect to

corporate strategy, the CGCNC

seeks candidates who possess board, senior management and/or other experience in strategy development or analysis.

- •

- Talent Management/Compensation: the CGCNC values candidates with hands-on roles in developing, managing, compensating and motivating employees. Such skills and experience assist the Board in fulfilling its responsibility to ensure that the company maintains effective incentive programs which attract, motivate and retain top talent, while at the same time reinforcing the company's strategic priorities. Talent management and compensation expertise also serve to align the Board with one of Magna's key strategic priorities – leadership development/succession planning.

Meeting Information 17

A skills matrix showing the skills, expertise and qualifications for each of the nominees is set forth below.

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Scott B. Bonham | /*/ | /*/ | /*/ | /*/ | /*/ | /*/ | /*/ | /*/ | /*/ | /*/ | /*/ | /*/ | MBA | |||||||||||||||

| Peter G. Bowie | /*/ | /*/ | /*/ | /*/ | /*/ | /*/ | /*/ | /*/ | /*/ | FCA, MBA | ||||||||||||||||||

| Hon. J. Trevor Eyton | /*/ | /*/ | /*/ | /*/ | /*/ | /*/ | /*/ | /*/ | /*/ | /*/ | JD | |||||||||||||||||

| Lady Barbara Judge | /*/ | /*/ | /*/ | /*/ | /*/ | /*/ | /*/ | /*/ | /*/ | /*/ | /*/ | JD | ||||||||||||||||

| Dr. Kurt J. Lauk | /*/ | /*/ | /*/ | /*/ | /*/ | /*/ | /*/ | /*/ | /*/ | /*/ | /*/ | /*/ | MBA, PhD | |||||||||||||||

| Cynthia A. Niekamp | /*/ | /*/ | /*/ | /*/ | /*/ | /*/ | /*/ | /*/ | /*/ | /*/ | /*/ | MBA | ||||||||||||||||

| Dr. Indira V. Samarasekera | /*/ | /*/ | /*/ | /*/ | /*/ | /*/ | /*/ | PhD, PEng | ||||||||||||||||||||

| Donald J. Walker | /*/ | /*/ | /*/ | /*/ | /*/ | /*/ | /*/ | /*/ | /*/ | /*/ | PEng | |||||||||||||||||

| Lawrence D. Worrall | /*/ | /*/ | /*/ | /*/ | /*/ | /*/ | /*/ | /*/ | CMA | |||||||||||||||||||

| William L. Young | /*/ | /*/ | /*/ | /*/ | /*/ | /*/ | MBA, PEng | |||||||||||||||||||||

Nominee Independence

Nine out of ten, or 90%, of the nominees for election at the Meeting are independent. A summary of the independence determination for each nominee is set forth below:

| NOMINEE NAME |

INDEPENDENT |

NON- INDEPENDENT |

BASIS FOR DETERMINATION |

|||

|---|---|---|---|---|---|---|

| Scott B. Bonham | ü | No material relationship | ||||

| Peter G. Bowie | ü | No material relationship | ||||

| Hon. J. Trevor Eyton | ü | No material relationship | ||||

| Lady Barbara Judge | ü | No material relationship | ||||

| Dr. Kurt J. Lauk | ü | No material relationship | ||||

| Cynthia A. Niekamp | ü | No material relationship | ||||

| Dr. Indira V. Samarasekera | ü | No material relationship | ||||

| Donald J. Walker | ü | Management | ||||

| Lawrence D. Worrall | ü | No material relationship | ||||

| William L. Young | ü | No material relationship | ||||

18 Meeting Information

Nominees' Meeting Attendance

Directors are expected to attend all Board meetings, as well as all meetings of standing Committees on which they serve, and are welcome to attend any other Committee meetings. However, we recognize that scheduling conflicts are unavoidable from time to time, particularly where meetings are called on short notice. Our Board Charter requires Directors to attend a minimum of 75% of regularly scheduled Board and applicable standing Committee meetings, except where an absence is due to medical or other valid reason. The ten nominees standing for re-election at the Meeting achieved 100% attendance at all Board and applicable Committee meetings (in aggregate), as set forth below.

| BOARD | AUDIT(1) | CGCNC(1) | EROC(1) | TOTAL |

||||||||||||||||

| NOMINEE | # | % | # | % | # | % | # | % | # | % | ||||||||||

| Scott B. Bonham | 7/7 | 100 | 6/6 | 100 | – | – | 6/6 | 100 | 19/19 | 100 | ||||||||||

| Peter G. Bowie | 7/7 | 100 | 6/6 | 100 | – | – | – | – | 13/13 | 100 | ||||||||||

| Hon. J. Trevor Eyton | 7/7 | 100 | – | – | 8/8 | 100 | – | – | 15/15 | 100 | ||||||||||

| Lady Barbara Judge | 7/7 | 100 | – | – | – | – | 6/6 | 100 | 13/13 | 100 | ||||||||||

| Dr. Kurt J. Lauk | 7/7 | 100 | 6/6 | 100 | – | – | – | – | 13/13 | 100 | ||||||||||

| Cynthia A. Niekamp | 7/7 | 100 | – | – | – | – | 6/6 | 100 | 13/13 | 100 | ||||||||||

| Dr. Indira V. Samarasekera | 7/7 | 100 | – | – | 8/8 | 100 | – | – | 15/15 | 100 | ||||||||||

| Donald J. Walker | 7/7 | 100 | – | – | – | – | – | – | 7/7 | 100 | ||||||||||

| Lawrence D. Worrall | 7/7 | 100 | 6/6 | 100 | – | – | 6/6 | 100 | 19/19 | 100 | ||||||||||

| William L. Young | 7/7 | 100 | – | – | 8/8 | 100 | – | – | 15/15 | 100 | ||||||||||

Notes:

- 1.

- Attendance figures for Audit, CGCNC and EROC include only those directors who served as members of such committees during 2015.

2015 Annual Meeting Vote Results

Each of the ten nominees standing for re-election received a substantial majority of votes "for" his or her election at our 2015 annual meeting of shareholders, as set forth in the table below.

| 2015 | ||||

| VOTES FOR (%) |

VOTES WITHHELD (%) |

|||

| Scott B. Bonham | 99.5 | 0.5 | ||

| Peter G. Bowie | 99.9 | 0.1 | ||

| Hon. J. Trevor Eyton | 97.8 | 2.2 | ||

| Lady Barbara Judge | 99.9 | 0.1 | ||

| Dr. Kurt J. Lauk | 99.5 | 0.5 | ||

| Cynthia A. Niekamp | 99.9 | 0.1 | ||

| Dr. Indira V. Samarasekera | 99.9 | 0.1 | ||

| Donald J. Walker | 99.9 | 0.1 | ||

| Lawrence D. Worrall | 99.7 | 0.3 | ||

| William L. Young | 99.3 | 0.7 | ||

Meeting Information 19

Nominees' Magna Equity Ownership

We believe it is important that each Independent Director be economically aligned with shareholders. We try to achieve such alignment in two principal ways:

- •

- Deferred Share Units ("DSUs"): 60% of the Independent Director annual retainer is paid in the form of DSUs. DSUs are

notional

units, the value of which is tied to the market value of our Common Shares. The value represented by an Independent Director's DSUs can only be realized following his or her retirement from the Board

and remains "at risk" until that time.

- •

- Equity Maintenance Requirement: Each Independent Director other than the Chairman is required to hold a minimum of $750,000 of Magna Common Shares and/or DSUs within five years of joining the Board. The Chairman is required to hold a minimum of $1,500,000 of Magna Common Shares and/or DSUs within three years of becoming Chairman.

Each of Magna's nominees is in compliance with the minimum equity maintenance requirement and many exceed it. New directors are entitled to a five year period in which to accumulate the minimum required value of Common Shares and/or DSUs.

The ten nominees held Magna Common Shares and/or DSUs with the following total value, as of December 31, 2015:

| |

COMMON SHARES |

DSUS |

TOTAL EQUITY "AT RISK"(1) ($) |

EQUITY MAINTENANCE REQUIREMENT |

||||

|---|---|---|---|---|---|---|---|---|

| Scott B. Bonham | – | 32,778 | 1,329,000 | Exceeds | ||||

| Peter G. Bowie | 7,000 | 25,388 | 1,314,000 | Exceeds | ||||

| Hon. J. Trevor Eyton | – | 26,355 | 1,069,000 | Exceeds | ||||

| Lady Barbara Judge | 8,000 | 101,814 | 4,454,000 | Exceeds | ||||

| Dr. Kurt J. Lauk | 110 | 19,835 | 809,000 | Exceeds | ||||

| Cynthia A. Niekamp | 1,000 | 2,905 | 158,000 | Complies | ||||

| Dr. Indira V. Samarasekera | – | 8,310 | 337,000 | Complies | ||||

| Donald J. Walker | 1,400,210 | 244,305 | (2) | 66,702,000 | Exceeds | |||

| Lawrence D. Worrall | 13,628 | 46,535 | 2,440,000 | Exceeds | ||||

| William L. Young | 1,860 | 59,708 | 2,497,000 | Exceeds | ||||

Notes:

- 1.

- In

calculating the value of total equity at risk, we have used the closing price of Magna Common Shares on NYSE on December 31, 2015.

- 2.

- Represents Mr. Walker's RSUs, as discussed further in the Compensation Discussion & Analysis section of this Circular.

20 Meeting Information

Biographies of 2016 Nominees

| Independent | ||

|

Scott B. Bonham California, U.S.A. Age: 54 Director Since: May 10, 2012 |

Mr. Bonham brings to the Board a technology/innovation-centred perspective which reflects his deep understanding of the long-term value creation potential possessed by some of the world's most innovative companies.

Mr. Bonham is the Co-Founder and Partner of The Fueling Station, a real estate management company that manages properties serving Canadian entrepreneurs and start-up companies. He co-founded GGV Capital, an expansion stage venture capital firm with investments in the U.S. and China, where he served as a Venture Partner (2011-2015) and a Partner (2000-2011). Prior to co-founding GGV in 2000, Mr. Bonham served as Vice-President of the Capital Group of Companies, where he managed technology investments across several mutual funds (1996-2000). Mr. Bonham also previously served in various marketing roles at Silicon Graphics (1992-1996), as a manufacturing and information systems strategy consultant at Booz, Allen & Hamilton (1989-1992) and systems engineer and maintenance foreman at General Motors of Canada. Mr. Bonham has previously served on a number of private and public company boards and audit committees, including Hurray! Holding Co. Ltd., the shares of which were quoted on the Nasdaq National Market. He is currently a board member of the C100, an association that connects Canadian entrepreneurs and companies with its Silicon Valley network. Mr. Bonham has a B.Sc in electrical engineering (Queen's) and an MBA (Harvard).

Mr. Bonham serves as a director of the Bank of Nova Scotia, which provides routine banking services to Magna. Magna's fees to the Bank of Nova Scotia in 2015 amounted to approximately $2.5 million, in relation to the bank's total 2015 revenues of over $24 billion. In the event of a conflict of interest on any matter, Mr. Bonham will not participate in the portion of the meeting at which the matter is discussed, nor in any Board decision on the matter. No such issues arose in 2015.

Other Public Company Boards: Bank of Nova Scotia

| Independent | ||

|

Peter G. Bowie Ontario, Canada Age: 69 Director Since: May 10, 2012 |

Mr. Bowie brings to the Board financial expertise, a dedication to Audit Committee excellence, a strong understanding of strategy and risk, as well as detailed insight of political and economic dynamics within China.

Mr. Bowie is a corporate director who most recently served as the Chief Executive of Deloitte China from 2003 to 2008, as well as senior partner and a member of the board and the management committee of Deloitte China until his retirement from the firm in 2010. Mr. Bowie was previously Chairman of Deloitte Canada (1998-2000), a member of the firm's management committee and a member of the board and governance committees of Deloitte International. He is a past member of the board of the Asian Corporate Governance Association and has served on a variety of boards in the private and non-governmental organization sectors. Mr. Bowie has a B.Comm (St. Mary's), as well as an MBA (Ottawa) and has received an honorary doctorate (Ottawa). Mr. Bowie completed the Advanced Management Program (Harvard) and is a Fellow of the Institute of Chartered Accountants of Ontario, as well as the Australian Institute of Corporate Directors.

Other Public Company Boards: China COSCO Holding Company Ltd. (Strategic Development (Chair); Risk)

Meeting Information 21

| Independent | ||

|

Hon. J. Trevor Eyton Ontario, Canada Age: 81 Director Since: May 6, 2010 |

Mr. Eyton brings to the Board broad-based counsel which reflects his extensive legal expertise, business acumen and "blue-chip" board experience. He also brings a balanced perspective reflecting a strong appreciation for issues from the perspectives of both senior management and board.

Mr. Eyton is a corporate director who served as a Member of the Senate of Canada from 1990 until his retirement in 2009. He is highly respected for his lengthy service with Brascan Limited, now known as Brookfield Asset Management, a Canadian-based, global asset manager focused on property, renewable power, infrastructure assets and private equity. Mr. Eyton served as Brascan's President and Chief Executive Officer (1979 to 1991), as well as its Chairman and Senior Chairman (to 1997) and as a director (to 2014). Prior to his service with Brascan, Mr. Eyton was a partner with the law firm Torys and has served on numerous public and private company boards, including that of General Motors Canada. Mr. Eyton has been appointed an Officer of the Order of Canada and Queen's Counsel for Ontario. He has a B.A. (Toronto), as well as a J.D. (Toronto) and has received two honorary doctorates of law (Waterloo; King's College (Dalhousie)).

Other Public Company Boards: Silver Bear Resources Inc. (Audit; Compensation; Governance & Environmental); LeadFX (Compensation (Chair)); Cancana Resources Corp. (Audit, Compensation & Governance); and Brookfield Real Estate Services Inc. (Compensation and Governance)

| Independent | ||

|

Lady Barbara Judge London, England Age: 69 Director Since: September 20, 2007 |

Lady Judge brings to the Board a broad-based global business perspective, complemented by significant legal and regulatory expertise, as well as practical corporate governance and risk management experience. Lady Judge's risk awareness and understanding of risk management processes, drawn in part from her experience in the nuclear industry and as a securities regulator, have been particularly valuable to the EROC, which she chairs.

Lady Judge is a corporate director who previously enjoyed a successful international career as a law firm partner, senior executive, chairman and non-executive director in both the private and public sectors and is highly regarded for her governance expertise. In 2015, Lady Judge assumed the role of National Chair of the Institute of Directors (U.K.), a representative organization for directors with approximately 38,000 members in the U.K. and elsewhere. Lady Judge previously served as Chairman of the Board of the United Kingdom Atomic Energy Authority (from 2004 to 2010), prior to which she was a Board member (since 2002). In addition, Lady Judge formerly served as a Commissioner of the U.S. Securities Exchange Commission and Deputy Chairman of the U.K. Financial Reporting Council. In 2010, she was appointed a Commander of the Order of the British Empire for her contributions to the financial services and nuclear industries. Lady Judge has a B.A. (U. Penn) and a J.D. (NYU School of Law).

Lady Judge serves as the non-executive chair of the U.K. Pension Protection Fund (the "PPF"), but will retire in June 2016. In 2015, Magna purchased a U.K.-based automotive supplier, Stadco Automotive Limited, the largest shareholder of which was the PPF. Lady Judge declared her interest, recused herself from the discussion of the transaction and abstained from approval of the transaction.

Other Public Company Boards*: Portmeirion Group plc (Audit; Compensation); Lixil Group Corporation

- *

- Lady Judge also serves on the Board of Bekaert NV, from which she will retire on May 4, 2016.

22 Meeting Information

| Independent | ||

|

Dr. Kurt J. Lauk Baden-Württemberg, Germany Age: 69 Director Since: May 4, 2011 |

Dr. Lauk brings to the Board valuable insights regarding the European automotive industry and the global activities of European OEMs and suppliers, together with a focus on long-term strategy and a strong understanding of technology/innovation both within and outside the automotive industry. Dr. Lauk's analytical perspective also draws upon his significant expertise in global political, economic and strategic affairs.

Dr. Lauk is the co-founder and President of Globe CP GmbH, a private investment firm. He possesses extensive European automotive industry experience, primarily through his positions as Member of the Board of Management and Head of World Wide Commercial Vehicles Division of Daimler Chrysler (1996-1999), as well as Deputy Chief Executive Officer and Chief Financial Officer (with responsibility for finance, controlling and marketing) of Audi AG (1989-1992). Dr. Lauk has other extensive senior management experience, including as Chief Financial Officer and Controller of Veba AG (now known as E.On AG) (1992-1996), Chief Executive Officer of Zinser Textil Machinery GmbH (1984-1989) and as a Partner and Vice-President of the German practice of Boston Consulting Group (1978-1984). Dr. Lauk served as a Member of European Parliament (2004-2009), including as a Member of the Economic and Monetary Affairs Committee and Deputy Member of the Foreign and Security Affairs Committee. He currently serves as a Trustee of the International Institute for Strategic Studies in London and is an honorary professor with a chair for international studies at the prestigious European Business School in Reichartshausen, Germany. Dr. Lauk possesses both a PhD in international politics (Kiel), as well as an MBA (Stanford).

Other Public Company Boards*: Solera Holdings Inc. (Audit; Corporate Governance)

- *

- Dr. Lauk was a director of Papierfabrik Scheuffelen GmbH, a private company, when it filed for bankruptcy protection under German law on July 17, 2008.

| Independent | ||

|

Cynthia A. Niekamp Michigan, U.S.A. Age: 56 Director Since: May 8, 2014 |

Ms. Niekamp brings to the Board extensive senior management experience within the automotive parts industry, including a highly technical understanding of operational matters derived from her engineering background.

Ms. Niekamp is a corporate director who most recently served as the Senior Vice-President, Automotive Coatings, of PPG Industries, Inc. She possesses over 30 years of automotive and other industrial manufacturing experience through her prior roles at PPG (2009 to 2016); BorgWarner, where she served as President & General Manager, BorgWarner Torq Transfer Systems (2004 to 2008); MeadWestvaco Corporation, where she served in various roles (1995 to 2004), including Senior Vice-President & Chief Financial Officer (2003 to 2004) and President, Special Paper Division (1998 to 2002); TRW (1990 to 1995); and General Motors (1983 to 1990). Ms. Niekamp currently serves as a Trustee of Kettering University and previously served on the boards of Rockwood Holdings, Delphi Corp. and Cooper Tire and Rubber, as well as Berkshire Applied Technology Council. Ms. Niekamp has a B.S. in industrial engineering (Purdue), as well as an MBA (Harvard).

During 2015, Ms. Niekamp was employed by PPG Industries, which is a supplier to Magna with global sales to the company of approximately $75 million on consolidated sales of over $15 billion. No conflicts of interest arose during 2015 in respect of Ms. Niekamp's role as an officer of PPG and service as a director of Magna.

Other Public Company Boards: None

Meeting Information 23

| Independent | ||

|

Dr. Indira V. Samarasekera British Columbia, Canada Age: 63 Director Since: May 8, 2014 |

Dr. Samarasekera brings to the Board a proven record of technical expertise, demonstrated leadership success, tangible success in building international relationships and a long-standing commitment to R&D/innovation, which is one of the company's top priorities.

Dr. Samarasekera is a corporate director and Senior Advisor at Bennett Jones, LLP, who most recently served as the President and Vice-Chancellor of the University of Alberta (2005 to 2015). Dr. Samarasekera is internationally recognized as a leading metallurgical engineer, including for her work on steel process engineering for which she was appointed an Officer of the Order of Canada. Prior to becoming the President of the University of Alberta, Dr. Samarasekera was Vice-President Research and held the Dofasco Chair in Advanced Steel Processing at the University of British Columbia (1996 to 2001). Among other things, Dr. Samarasekera formerly served as Chair of the Worldwide Universities Network and was previously a member of Canada's Science, Technology and Innovation Council as well as Canada's Global Commerce Strategy. Dr. Samarasekera has an M.Sc in mechanical engineering (California), as well as a PhD in metallurgical engineering (British Columbia) and is a Professional Engineer (P.Eng) who has been elected as a Foreign Associate of the National Academy of Engineering in the U.S.

Dr. Samarasekera serves as a director at the Bank of Nova Scotia, which provides routine banking services to Magna. Magna's fees to the Bank of Nova Scotia in 2015 amounted to approximately $2.5 million, in relation to the bank's total 2015 revenues of over $24 billion. In the event of a potential conflict of interest on any matter, Dr. Samarasekera will not participate in the portion of the meeting at which the matter is discussed, nor in any Board decision on the matter. No such issues arose in 2015.

Other Public Company Boards: Bank of Nova Scotia (Human Resources; Corporate Governance); TransCanada Corporation

| Management | ||

|

Donald J. Walker Ontario, Canada Age: 59 Director Since: November 7, 2005 |

Mr. Walker, Magna's Chief Executive Officer, is Management's sole representative on the Board. He brings extensive knowledge and understanding of the automotive industry, as well as the company's culture, operations, key personnel, customers, suppliers and the complex drivers of its success. He has demonstrated a commitment to transparent and effective leadership, responsiveness to the Board and integrity in all aspects of the company's business, while pushing the organization to reach its full potential through World Class Manufacturing, innovation and leadership development. Mr. Walker continues to actively shape Magna's strategic vision and mission in conjunction with the Board, with an unwavering focus on excellence in execution/implementation and legal/regulatory compliance, as well as prudence in stewardship over the company's assets, employees, reputation and value. Mr. Walker was Canada's 2014 Outstanding CEO of the Year™ and named to Fortune Magazine's Businessperson of the Year list in 2015.

Mr. Walker previously served as Magna's Co-Chief Executive Officer (2005-2010) and President and Chief Executive Officer (1994-2001). He was formerly the President, Chief Executive Officer and Chairman of Intier Automotive Inc. (2001-2005), one of Magna's former "spinco" public subsidiaries. Prior to joining Magna in 1987, Mr. Walker spent seven years at General Motors in various engineering and manufacturing positions. He is currently the Chair (since October 2011, previously Co-Chair since 2002), of the Canadian Automotive Partnership Council (CAPC) with the Canadian federal and provincial governments, which serves to identify both short- and long-term priorities to help ensure the future health of the automotive industry in Canada. Mr. Walker is also the past Chairman of the Automotive Parts Manufacturers Association (APMA). Mr. Walker is a professional engineer with a B.Sc in mechanical engineering (Waterloo).

Other Public Company Boards: None

24 Meeting Information

| Independent | ||

|

Lawrence D. Worrall Ontario, Canada Age: 72 Director Since: November 7, 2005 |

Mr. Worrall brings to the Board extensive automotive industry experience, together with a dedication to Audit Committee excellence and a commitment to the integrity of Magna's financial statements. As Chairman of Magna's Audit Committee, Mr. Worrall worked extensively with representatives of Deloitte and Management to help maximize the benefits to the Board, Audit Committee and the company's shareholders arising from the rotation of auditors in 2014.

Mr. Worrall is a corporate director and certified management accountant who formerly served as the Vice-President, Purchasing, Strategic Planning and Operations, as well as a Director of General Motors of Canada Limited (1995-2000). In his capacity as an officer of GM Canada, Mr. Worrall had responsibility for a number of significant matters, including: purchasing, logistics, GM Canada's manufacturing facilities, forward product planning and the execution of the manufacturing plan for all plants.

Other Public Company Boards: None

| Independent | ||

|

William L. Young Massachusetts, U.S.A. Age: 61 Director Since: May 4, 2011 |

Mr. Young, the Chairman of the Board (since 2012), brings to the Board a highly effective consensus-building leadership style anchored by strong business acumen developed across a broad range of businesses and industries. He has been highly effective in cultivating a constructive but independent relationship with Management, as well as an open, constructive dialogue with shareholders, potential investors, shareholder representative organizations and others in the corporate governance community. In his capacity as Chairman of the CGCNC, Mr. Young has been active in engagement with shareholders and instrumental in the evolution of Magna's unique compensation structure in a manner which reasonably preserves its core elements while responsively addressing constructive feedback received from shareholders and others.

Mr. Young is a co-founder and partner of Monitor Clipper Partners, a private equity firm established in 1998. Through his role at Monitor Clipper Partners, together with roles as founding partner of Westbourne Management Group (since 1988) and a partner in the European practice of Bain & Company (1981-1988), Mr. Young possesses significant operational experience, as well as extensive mergers and acquisitions experience. He is Chair Emeritus of the Board of Trustees of Queen's University (Kingston, Ontario) (which he chaired from 2006 to 2012) and has significant private company board and board leadership experience over the last 20 years, including a number of European and U.S.-based companies. Mr. Young has a B.Sc in chemical engineering (Queen's) and an MBA (Harvard).

Other Public Company Boards*: None

- *

- Mr. Young was a director of American Fiber & Yarns and Recycled Paper Greetings, both of which were private companies, when they filed voluntary petitions for bankruptcy protection under Chapter 11 of the U.S. Bankruptcy Code on September 23, 2008 and January 2, 2009, respectively.

Meeting Information 25

Director Compensation

Objectives of Director Compensation

We have structured the compensation for our Independent Directors with the aim of attracting and retaining skilled independent directors and aligning their interests with the interests of our long-term shareholders. To accomplish these objectives, we believe that such compensation must be competitive with that paid by our S&P/TSX60 peer companies, as well as the global automotive and industrial peers in our executive compensation peer group. Additionally, we believe that the majority of such compensation must be deferred until retirement, thus tying the redemption value to the market value of our Common Shares and placing it "at risk" to align the interests of Independent Directors with those of shareholders. Management directors do not receive any compensation for serving as directors.

Compensation Structure

We compensate Independent Directors through a combination of:

- •

- Annual Retainer: Since 2008, this retainer has been fixed at $150,000, of which $90,000 (60%) is automatically deferred

until

retirement in the form of DSUs and $60,000 (40%) is paid in cash. In addition to the portion automatically deferred in the form of DSUs, Independent Directors may defer up to 100% of their cash

compensation in the form of DSUs.

- •

- Board Chair Retainer: The Chair is paid a flat annual retainer of $500,000 for all work performed in

any capacity other than

as a special committee chair. Of such amount, $300,000 (60%) is automatically deferred in the form of DSUs and $200,000 (40%) is paid in cash, subject to the Chair's election to defer up to 100% of

his cash compensation in the form of DSUs.

- •

- Committee Chair and Committee Member Retainers: In recognition of the additional workload of our

Committee Chairs and

Committee members, additional retainers are paid to each Independent Director acting in any such capacity. These retainers are set at $25,000 for each standing Board Committee. In the case of special

committees which may be formed from time to time, the retainer is set at $25,000, unless otherwise determined by the Board. Committee Chair retainers are payable in cash, subject to an Independent

Director's election to defer up to 100% of his or her cash compensation in the form of DSUs.

- •

- Meeting and Work Fees: Meeting and work fees are intended to compensate Independent Directors based on their respective contributions of time and effort to Magna matters. The amounts of these fees are listed in the fee schedule below and are payable in cash, subject to an Independent Director's election to defer up to 100% of his or her cash compensation in the form of DSUs.

The CGCNC has responsibility for reviewing Independent Director compensation and typically reviews it approximately every two years. When last reviewed in 2014, the CGCNC engaged its independent compensation advisor, Hugessen Consulting, to review and benchmark Magna's compensation for Independent Directors against two peer groups – one consisting of large capitalization companies in the S&P/TSX60 index and the other consisting of the global automotive and industrial peers in Magna's executive compensation peer group. Hugessen reviewed both the structure of Magna's director compensation program and actual compensation earned against the two peer groups. Its analysis found that while director compensation levels in the industry peer group were

26 Meeting Information

higher than those of the S&P/TSX60 peer group, Magna fell within the competitive norms of both peer groups. Hugessen also noted that Magna's Independent Directors had a greater proportion of their compensation paid in equity (DSUs) and they were subject to more stringent equity maintenance requirements than their peers. Based on Hugessen's review, the CGCNC kept Magna's Independent Director compensation unchanged.

The current schedule of retainers and fees payable to our Independent Directors is set forth below.

| RETAINER/FEE TYPE |

AMOUNT ($) |

||

|---|---|---|---|

| Comprehensive Board Chair annual retainer (minimum 60% DSUs; maximum 40% cash) | 500,000 | ||

| Independent Director annual retainer (minimum 60% DSUs; maximum 40% cash) | 150,000 | ||

| Committee member annual retainer | 25,000 | ||

| Additional Committee Chair annual retainer | |||

| Audit | 25,000 | ||

| CGCNC | 25,000 | ||

| EROC | 25,000 | ||

| Special Committees (unless otherwise determined by the Board) | 25,000 | ||

| Per meeting fee | 2,000 | ||

| Written resolution | 400 | ||

| Additional services (per day) | 4,000 | ||

| Travel days (per day) | 4,000 | ||

2015 Independent Directors' Compensation

The following table sets forth a summary of the compensation earned by all individuals who served as Independent Directors during the year ended December 31, 2015.

| FEES EARNED(1) |

SHARE- BASED AWARDS(2) |

||||||||||||||||||

| NAME | ($) | % OF FEES |

($) | % OF FEES |

OPTION- BASED AWARDS ($) |

NON-EQUITY INCENTIVE PLAN COMPENSATION ($) |

PENSION VALUE ($) |

ALL OTHER(3) ($) |

TOTAL ($) |

||||||||||

| Scott B. Bonham | NIL | – | 394,000 | 100% | NIL | NIL | NIL | NIL | 394,000 | (3) | |||||||||

| Peter G. Bowie | NIL | – | 219,000 | 100% | NIL | NIL | NIL | NIL | 219,000 | ||||||||||

| Hon. J. Trevor Eyton | 66,000 | 30% | 156,000 | 70% | NIL | NIL | NIL | NIL | 222,000 | ||||||||||

| V. Peter Harder | NIL | – | 276,000 | 100% | NIL | NIL | NIL | NIL | 276,000 | ||||||||||

| Lady Barbara Judge | NIL | – | 277,000 | 100% | NIL | NIL | NIL | NIL | 277,000 | ||||||||||

| Dr. Kurt J. Lauk | 43,000 | 16% | 218,000 | 84% | NIL | NIL | NIL | NIL | 261,000 | ||||||||||

| Cynthia A. Niekamp | 137,000 | 60% | 90,000 | 40% | NIL | NIL | NIL | NIL | 227,000 | ||||||||||