Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2010

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission File Number: 0-13468

EXPEDITORS INTERNATIONAL OF WASHINGTON, INC.

(Exact name of registrant as specified in its charter)

| Washington | 91-1069248 | |

| (State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification Number) | |

| 1015 Third Avenue, 12th Floor, Seattle, Washington | 98104 | |

| (Address of principal executive offices) | (Zip Code) | |

(206) 674-3400

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class |

Name of each exchange on which registered | |

| Common Stock, par value $.01 per share | NASDAQ Global Select Market |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes x No ¨

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer x |

Accelerated filer ¨ | |

| Non-accelerated filer ¨ (Do not check if a smaller reporting company) |

Smaller reporting company ¨ |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ¨ No x

At June 30, 2010, the aggregate market value of the registrant’s Common Stock held by non-affiliates of the registrant was approximately $7,209,494,453.

At February 18, 2011, the number of shares outstanding of registrant’s Common Stock was 212,197,775.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the definitive proxy statement for the Registrant’s 2011 Annual Meeting of Shareholders to be held on May 4, 2011 are incorporated by reference into Part III of this Form 10-K.

Table of Contents

Forward-Looking Statements

In accordance with the provisions of the Private Securities Litigation Reform Act of 1995, the Company is making readers aware that forward-looking statements, because they relate to future events, are by their very nature subject to many important risk factors which could cause actual results to differ materially from those contained in the forward-looking statements. For additional information about forward-looking statements and for an identification of risk factors and their potential significance, see “Safe Harbor for Forward-Looking Statements Under Private Securities Litigation Reform Act of 1995; Certain Cautionary Statements” immediately preceding Part II, Item 7 “Management’s Discussion and Analysis of Financial Condition and Results of Operations” in this report.

PART I

ITEM 1 — BUSINESS

Expeditors International of Washington, Inc. is engaged in the business of providing global logistics services. The Company offers its customers a seamless international network supporting the movement and strategic positioning of goods. The Company’s services include the consolidation or forwarding of air and ocean freight. In each United States office, and in many overseas offices, the Company acts as a customs broker. The Company also provides additional services including distribution management, vendor consolidation, cargo insurance, purchase order management and customized logistics information. The Company does not compete for overnight courier or small parcel business and does not own aircraft or steamships.

Beginning in 1981, the Company’s primary business focus was on airfreight shipments from Asia to the United States and related customs brokerage and other services. In the mid-1980’s, the Company began to expand its service capabilities in export airfreight, ocean freight and distribution services. Today the Company offers a complete range of global logistics services to a diversified group of customers, both in terms of industry specialization and geographic location. As opportunities for profitable growth arise, the Company plans to create new offices. While the Company has historically expanded through organic growth, the Company has also been open to growth through acquisition of, or establishing joint ventures with, existing agents or others within the industry.

The Company, including its majority-owned subsidiaries, operates full service offices (•) in the cities identified below. Full service offices have also been established in locations where the Company maintains unilateral control over assets and operations and where the existence of the parent-subsidiary relationship is maintained by means other than record ownership of voting stock (#). In other cities, the Company contracts with independent agents to provide required services and has established approximately 48 such relationships world-wide. Locations where Company employees perform sales and customer service functions are identified below as international service centers (*). Wholly-owned locations operating under the supervision and control of another full service office are identified as satellite offices (+). In each case, the opening date for the full service office, international service center or satellite office is set forth in parenthesis.

| UNITED STATES AND OTHER NORTH AMERICA | ||||||

| UNITED STATES • Seattle (5/79) • Chicago (7/81) • San Francisco (7/81) • New York (11/81) • Los Angeles (5/82) • Atlanta (8/83) • Boston (11/85) • Miami (3/86) • Minneapolis (7/86) • Denver (2/88) |

• Baltimore (4/92) • Dallas (5/92) • Columbus (6/92) • Charlotte (7/92) • Newark (9/94) • Philadelphia (3/95) • Charleston (6/95) • Memphis (8/95) • Salt Lake City (11/95) • Norfolk (9/96) • Indianapolis (11/96) |

• McAllen (4/98) • Pittsburgh (6/99) • Savannah (3/00) • Milwaukee (7/00) • Kansas City (8/00) • Washington, D.C. (9/00) • Nashville (10/01) + Huntsville (12/02) • Austin (2/03) • Orlando (8/03) • Tampa (9/03) |

• Vancouver (9/95) + Windsor (6/98) • Montreal (4/99) • Calgary (9/04)

MEXICO • Mexico City (6/95) • Nuevo Laredo (4/97) • Guadalajara (9/97) • Nogales (1/99) • Ciudad Juarez (5/00) • Monterrey (1/05) | |||

| 1.

Table of Contents

| UNITED STATES AND OTHER NORTH AMERICA | ||||||

| • Detroit (7/88) • Portland (7/88) • Cincinnati (8/89) • Cleveland (7/90) • Phoenix (7/91) • Louisville (10/91) • St. Louis (4/92) • Houston (4/92) |

+ Port Huron-Blue Water Bridge (12/96) + Detroit-Ambassador Bridge (12/96) • Buffalo-Peace Bridge (1/97) • El Paso (1/97) • Laredo (2/97) • Nogales (2/97) • San Diego (7/97) + Rochester (10/97) |

• New Orleans (9/04) + Omaha (7/06) + Calexico (6/06) + Knoxville (5/07) • Raleigh Durham (1/08) + Tulsa (1/09)

CANADA • Toronto (5/84) |

• Reynosa (6/06) + Querétaro (9/06) + Lázaro Cárdenas (7/08)

PUERTO RICO • San Juan (5/95) | |||

| LATIN AMERICA | ||||||

| ARGENTINA • Buenos Aires (1/98)

BRAZIL • Sao Paulo (9/95) • Rio de Janeiro (9/95) • Campinas (9/95) + Santos (10/97) • Manaus (7/00) • Porto Alegre (1/05) |

• Curitiba (10/10) + Belo Horizonte (10/10)

CHILE • Santiago (2/95)

COLOMBIA • Bogota (12/98) + Cali (12/98) + Medellin (7/00) |

COSTA RICA • San Jose (10/03)

GUATEMALA • Guatemala City (1/07)

PERU • Lima (12/05) |

||||

| ASIA PACIFIC | ||||||

| AUSTRALIA • Sydney (8/88) • Melbourne (8/88) • Brisbane (10/93) • Perth (12/94) • Adelaide (10/97)

BANGLADESH • Dhaka (6/89) + Chittagong (8/93)

CAMBODIA • Phnom Penh (4/00)

PEOPLE’S REPUBLIC OF CHINA • Guangzhou (4/94) • Beijing (7/94) • Dalian (7/94) • Shanghai (7/94) • Shenzhen (7/94) • Qingdao (7/94) • Tianjin (7/94) • Xi’an (7/94) • Xiamen (7/94) + Chengdu (9/00) • Ningbo (7/01) |

• Suzhou (9/01) • Zhongshan (9/01) • Hangzhou (10/01) + Kunshan (12/01) • Fuzhou (6/02) • Yantai (11/02) + Shenyang (12/02) • Wuhan (1/03) + Huizhou (12/03) + Zhuhai (12/03) + Foshan (1/04) • Chongqing (7/04) • Dongguan (2/05) • Nanjing (3/05) + Macau (5/05) + Shantou (12/06) + Changzhou (10/07)

FIJI * Nadi (7/96) * Suva (5/97)

HONG KONG • Kowloon (6/81) |

INDONESIA • Jakarta (12/90) • Surabaya (2/92) + Batam (3/07)

JAPAN • Tokyo (1/01) • Osaka (1/01) + Nagoya (8/03)

MALAYSIA • Penang (11/87) • Kuala Lumpur (6/90) • Johor Bahru (11/94)

NEW ZEALAND • Auckland (8/88) + Christchurch (10/07)

PHILIPPINES • Manila (8/98) + Olongapo City (8/98) + Cebu City (9/99)

SINGAPORE • Singapore (9/81)

SRI LANKA • Colombo (3/95) |

SOUTH KOREA • Seoul (10/94) + Pusan (10/94) + Chonan (6/96) + Kwangju (6/96) + Masan (6/96) + Taegu (6/96)

TAIWAN • Taipei (7/81) + Kaohsiung (9/81) + Taichung (9/81) + Hsin-Chu (9/89)

THAILAND • Bangkok (9/94) + Laem Chabang (8/05)

VIETNAM • Ho Chi Minh City (5/00) • Hanoi (3/04) + Da Nang (9/05) | |||

2. |

Table of Contents

| EUROPE AND AFRICA | ||||||

| AUSTRIA • Vienna (11/95)

BELGIUM • Brussels (7/90) +Antwerp(4/91)

THE CZECH REPUBLIC • Prague (6/98)

FINLAND • Helsinki (4/94)

FRANCE • Paris (1/97) • Mulhouse (1/97) • Lyon (1/97) • Lille (3/97) • Bordeaux (7/00)

GERMANY • Frankfurt (4/92) • Munich (4/92) • Dusseldorf (4/92) |

• Stuttgart (4/92) • Hamburg (1/93) • Nuremberg (1/01) + Hannover (1/05)

HUNGARY • Budapest (4/00)

IRELAND • Dublin (3/97) • Cork (3/97) • Shannon (3/97)

ITALY • Milan (4/93) • Verona (4/93) • Florence (3/98) + Turin (4/05) + Rome (1/10)

THE NETHERLANDS • Amsterdam (6/94) • Rotterdam (3/95) |

+ Maastricht (9/07)

NORWAY • Oslo (6/10)

POLAND • Warsaw (2/05) + Krakow (8/07)

PORTUGAL • Lisbon (10/91) • Oporto (10/91)

ROMANIA • Bucharest (9/08)

SPAIN • Barcelona (1/94) • Madrid (1/94) • Alicante (4/96)

SWEDEN • Stockholm (1/94) • Goteborg (1/94) + Malmoe (3/05) |

SWITZERLAND • Chiasso (2/01) • Zurich (10/05)

UNITED KINGDOM • London (4/86) • Manchester (11/88) • Birmingham (3/90) • Glasgow (4/92) • Bristol (3/97) • East Midlands (1/99) + Hull (1/00) • Belfast (9/01) • Aberdeen (9/05)

SOUTH AFRICA • Johannesburg (3/94) • Durban (3/94) • Capetown (1/97)

MADAGASCAR • Antananarivo (11/01) | |||

| MIDDLE EAST AND INDIA | ||||||

| BAHRAIN • Manama (1/08)

EGYPT • Cairo (2/95) + Alexandria (2/95)

GREECE • Athens (2/99) + Thessaloniki (2/99)

INDIA • New Delhi (7/96) • Mumbai (Bombay) (1/97) • Bangalore (6/97) • Chennai (Madras) (6/97) + Jaipur (6/99) + Cochin (4/01) + Hyderabad (9/01) |

+ Tuticorin (11/03) + Ahmedabad (1/05) + Tiruppur (3/05) + Ludhiana (6/05) + Pune (10/06) + Kolkata (1/08) + Coimbatore (1/08) + Mundra (4/08)

JORDAN • Amman (9/07)

KUWAIT # Kuwait City (7/97)

LEBANON • Beirut (8/99)

OMAN • Muscat (4/09) |

PAKISTAN • Karachi (9/96) • Lahore (9/96) + Sialkot (6/03) + Faisalabad (5/06) + Islamabad (10/06)

QATAR • Doha (1/07)

SAUDI ARABIA # Riyadh (7/92) # Jeddah (7/92) # Dammam (6/05) |

TURKEY • Ankara (1/99) • Istanbul (1/99) • Izmir (1/99) • Mersin (1/99) + Adana (1/99)

U.A.E. • Abu Dhabi (1/94) • Dubai (10/98) | |||

The Company was incorporated in the State of Washington in May 1979. Its executive offices are located at 1015 Third Avenue, 12th Floor, Seattle, Washington, and its telephone number is (206) 674-3400.

The Company’s internet address is http://www.expeditors.com. The Company makes available free of charge through its internet website its annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and all amendments to those reports as soon as reasonably practicable after such material is electronically filed with or furnished to the Securities and Exchange Commission (SEC).

For information concerning the amount of revenues, net revenues, operating income, identifiable assets, capital expenditures and depreciation and amortization attributable to the geographic areas in which the Company conducts its business, see Note 9 to the consolidated financial statements.

| 3.

Table of Contents

Airfreight Services

Airfreight services accounted for approximately 38, 35 and 36 percent of the Company’s 2010, 2009 and 2008 consolidated revenues net of freight consolidation expenses (“net revenues”), respectively. When performing airfreight services, the Company typically acts either as a freight consolidator or as an agent for the airline which carries the shipment. When acting as a freight consolidator, the Company purchases cargo space from airlines on a volume basis and resells that space to its customers at lower rates than the customers could obtain directly from airlines. When moving shipments between points where the volume of business does not facilitate consolidation, the Company receives and forwards individual shipments as the agent of the airline which carries the shipment. Whether acting as a consolidator or agent, the Company offers its customers knowledge of optimum routing, familiarity with local business practices, knowledge of export and import documentation and procedures, the ability to arrange for ancillary services, and assistance with space availability in periods of peak demand.

In its airfreight forwarding operations, the Company procures shipments from its customers, determines the routing, consolidates shipments bound for a particular airport distribution point, and selects the airline for transportation to the distribution point. At the distribution point, the Company or its agent arranges for the consolidated lot to be broken down into its component shipments and for the transportation of the individual shipments to their final destinations.

The Company estimates its average airfreight consolidation weighs approximately 3,900 pounds and a typical consolidation includes merchandise from several shippers. Because shipment by air is relatively expensive compared with ocean transportation, air shipments are generally characterized by a high value-to-weight ratio, the need for rapid delivery, or both.

The Company typically delivers shipments from a Company warehouse at the origin to the airline after consolidating the freight into containers or onto pallets. Shipments normally arrive at the destination distribution point within forty-eight hours after such delivery. During peak shipment periods, cargo space available from the scheduled air carriers can be limited and backlogs of freight shipments may occur. When these conditions exist, the Company may charter aircraft to meet customer demand.

The Company consolidates individual shipments based on weight and volume characteristics in cost-effective combinations. Typically, as the weight or volume of a shipment increases, the cost per pound/kilo or cubic inch/centimeter charged by the Company decreases. The rates charged by airlines to forwarders and others also generally decrease as the weight or volume of the shipment increases. As a result, by aggregating shipments and presenting them to an airline as a single shipment, the Company is able to obtain a lower rate per pound/kilo or cubic inch/centimeter than that which it charges to its customers for the individual shipment, while generally offering the customer a lower rate than could be obtained from the airline for an unconsolidated shipment.

The Company’s airfreight forwarding net revenues from a consolidated shipment include the differential between the rate charged to the Company by an airline and the rate which the Company charges to its customers, commissions paid to the Company by the airline carrying the freight and fees for ancillary services. Such ancillary services provided by the Company include preparation of shipping and customs documentation, packing, crating and insurance services, negotiation of letters of credit, and preparation of documentation to comply with local export laws. When the Company acts as an agent for an airline handling an unconsolidated shipment, its net revenues are primarily derived from commissions paid by the airline and fees for ancillary services paid by the customer.

The Company also performs breakbulk services which involve receiving and breaking down consolidated airfreight lots and arranging for distribution of the individual shipments. Breakbulk service revenues also include commissions from agents for airfreight shipments.

The Company does not own aircraft and does not plan to do so. Management believes that the ownership of aircraft would subject the Company to undue business risks, including large capital outlays, increased fixed operating expenses, problems of fully utilizing aircraft and competition with airlines. Because the Company relies on commercial airlines to transport its shipments, changes in carrier financial stability, policies and practices such as pricing, payment terms, scheduling, capacity and frequency of service may affect its business.

4. |

Table of Contents

The commercial airline industry as a whole incurred substantial operating losses in 2009. While their operations improved in 2010, many airlines are highly leveraged with debt. Carriers continue to merge and consolidate operations and reduce available capacity to improve financial results. Some airlines have significantly reduced their reliance on cargo-only aircraft to service their airfreight customers. The reduction in capacity allows asset-based carriers to raise rates in the face of declining or stable demand. When fewer planes are flying, the Company has fewer shipping options from which to craft service offerings to meet customers’ needs. The combination of reduced capacity, higher rates and more infrequent flights could challenge the Company’s ability to maintain historical unitary profitability.

Ocean Freight and Ocean Services

Ocean freight services accounted for approximately 23, 24, and 25 percent of the Company’s 2010, 2009 and 2008 consolidated net revenues, respectively. The Company operates Expeditors International Ocean (“EIO”), an Ocean Transportation Intermediary, sometimes referred to as a Non-Vessel Operating Common Carrier (“NVOCC”) specializing in ocean freight consolidation in most major trade lanes in the world. As an NVOCC, EIO contracts with ocean shipping lines to obtain transportation for a fixed number of containers between various points during a specified time period at an agreed rate. EIO handles full container loads for customers that do not have annual shipping volumes sufficient to negotiate comparable contracts directly with the ocean carriers. EIO also solicits Less-than Container Load (“LCL”) freight to fill the containers and charges lower rates than those available directly from shipping lines. The Company’s revenues as an ocean freight forwarder are also derived from commissions paid by the carrier and revenues from fees charged to customers for ancillary services which the Company may provide, such as preparing documentation, procuring insurance, arranging for packing and crating services, and providing consultation. The Company does not own vessels and generally does not physically handle the cargo.

Ocean carriers incurred substantial operating losses in 2009. Operations improved in 2010, but many carriers are highly leveraged with debt. Carriers continue to manage available capacity and modify sailing schedules to improve financial results. The combination of lower capacity, slower sailing schedules and pricing volatility could impact the Company’s ability to maintain historical unitary profitability.

Order Management provides services which manage origin consolidation, supplier performance, carrier allocation and performance, container management, document management, destination management and PO/SKU visibility through a web based application. Customers have the ability to monitor and report against real time status of purchase orders from the date of creation through final delivery. Item quantities, required ship dates, commodity descriptions, estimated vs. actual ex factory dates, container utilization, supplier performance and document visibility are many of the managed functions that are visible and reportable via the web. Order Management is available for various modes of transportation including ocean, air, truck and rail. Order Management revenues are derived from services provided to the shipper as well as management fees associated with managing purchase order execution against customer specific rules. One basic function of Order Management involves the taking of cargo from many suppliers in a particular origin and “consolidating” these shipments into the fewest possible number of containers to maximize space and minimize cost. Through origin consolidation customers can reduce the number of containers shipped by putting more product in larger and fewer containers. Data integrity is an increasingly critical function of Order Management. Efficient data management is a by-product of our operational processes.

Customs Brokerage and Other Services

Customs brokerage and other services accounted for approximately 39, 41 and 39 percent of the Company’s 2010, 2009 and 2008 consolidated net revenues, respectively. As a customs broker, the Company assists importers to clear shipments through customs by preparing required documentation, calculating and providing for payment of duties on behalf of the importer, arranging for any required inspections by governmental agencies, and arranging for delivery. The Company also provides other value added services at destination such as warehousing and

| 5.

Table of Contents

product distribution, time definite transportation and inventory management. None of these other services are currently individually significant to the Company’s net revenues.

The Company provides customs clearance services in connection with many of the shipments it handles as a freight forwarder. However, substantial customs brokerage revenues are derived from customers that elect to use a competing forwarder. Conversely, shipments handled by the Company as a forwarder may be processed by another customs broker selected by the customer.

The Company also provides custom clearances for goods moving by rail and truck between the United States, Canada and/or Mexico. The commodities being cleared and the time sensitive nature of the border brokerage business require the Company to continue to make enhancements to its systems in order to provide competitive service.

The Company’s wholly-owned subsidiary, Expeditors Tradewin, L.L.C., responds to customer driven requests for high-end customs consulting services. Fees for these non-transactional services are based upon hourly billing rates and bids for mutually agreed projects.

Marketing and Customers

The Company provides customer specific solutions and seeks to understand the needs of the customers from order inception through to order delivery. Although the domestic importer usually designates the logistics company and the services that will be required, the foreign shipper may also participate in this selection process. Therefore, the Company coordinates its marketing program to reach both domestic importers and their overseas suppliers.

The Company’s marketing efforts are focused on interacting with our customers’ supply chain, including logistics, transportation, customs, compliance and purchasing departments of existing and potential customers. The district manager of each office is responsible for marketing, sales coordination, and implementation in the area in which he or she is located. All employees are responsible for customer service and retention.

The Company staffs its offices largely with managers and other key personnel who are citizens of the nations in which they operate and who have extensive experience in global logistics. Marketing and customer service staffs are responsible for marketing the Company’s services directly to customers and prospects who may select or influence the selection of logistics service providers and for ensuring that customers receive timely and efficient service. The Company believes that its expertise in supplying solutions customized to the needs of its customers, its emphasis on coordinating its origin and destination customer service and marketing activities, and the incentives it gives to its managers have been important elements of its success.

The goods handled by the Company are generally a function of the products which dominate international trade between any particular origin and destination. Shipments of computer components, electronic goods, medical equipment, sporting goods, machine parts, aviation parts and toys comprise a significant percentage of the Company’s business. Typical import customers include retailers and distributors of consumer electronics, department store chains, clothing and shoe wholesalers, manufacturers and catalogue stores. Historically, no single customer has accounted for five percent or more of the Company’s net revenues.

Competition

The global logistics services industry is intensely competitive and is expected to remain so for the foreseeable future. There are a large number of companies competing in one or more segments of the industry, but the number of firms with a global network that offer a full complement of logistics services is more limited. Depending on the location of the shipper and the importer, the Company must compete against both the niche players and larger entities. Historically, the industry has experienced consolidations into larger firms striving for stronger and more complete multinational and multi-service networks. However, regional and local competitors still maintain a strong market presence in certain areas.

6. |

Table of Contents

The primary competitive factors in the global logistics services industry continue to be price and quality of service, including reliability, responsiveness, expertise, convenience, and scope of operations. The Company emphasizes quality service and believes that its prices are competitive with the prices of others in the industry. Larger customers utilize more sophisticated and efficient procedures for the management of their logistics supply chains by embracing strategies such as just-in-time inventory management. Accordingly, timely and accurate information integrated into customer service capabilities are a significant factor in attracting and retaining customers. This information integrated into customer service capabilities include customized Electronic Data Interchange, (“EDI”), on-line freight tracing and tracking applications and customized on-line reporting. The customized EDI applications allow the transfer of key information between the customers’ systems and the Company’s systems. Freight tracing and tracking applications provide customers with real time visibility to the location, transit time and estimated delivery time of inventory in transit.

Management believes that the ability to develop and deliver innovative solutions to meet customers’ increasingly sophisticated information requirements is a critical factor in the ongoing success of the Company. The Company devotes a significant amount of resources towards the maintenance and enhancement of systems that will meet these customer demands. Management believes that the Company’s existing systems are competitive with the systems currently in use by other logistics services companies with which it competes.

Unlike many of its competitors, who have tended to grow by merger and acquisition, the Company operates the same accounting and transportation computer software, running on a common hardware platform, in all of its full-service locations. Small and middle-tier competitors, in general, do not have the resources available to develop these customized systems. Historically, growth through aggressive acquisition has proven to be a challenge for many of the Company’s competitors and typically involves the purchase of significant “goodwill.” As a result, the Company has pursued a strategy emphasizing organic growth supplemented by certain strategic acquisitions.

The Company’s ability to attract, retain, and motivate highly qualified personnel with experience in global logistics services is an essential, if not the most important, element of its ability to compete in the industry. To this end, the Company has adopted incentive compensation programs which make percentages of branch net revenues or profits available to managers for distribution among key personnel. The Company believes that these incentive compensation programs, combined with its experienced personnel and its ability to coordinate global marketing efforts, provide it with a distinct competitive advantage and account for historical growth that competitors have generally matched only through acquisition.

Currency and Other Risk Factors

The nature of the Company’s worldwide operations necessitate the Company dealing with a multitude of currencies other than the U.S. dollar. This results in the Company being exposed to the inherent risks of the international currency markets and governmental interference. Many of the countries where the Company maintains offices and/or agency relationships have strict currency control regulations which influence the Company’s ability to hedge foreign currency exposure. The Company tries to compensate for these exposures by accelerating international currency settlements among these offices or agents.

In addition, the Company’s ability to provide service to its customers is highly dependent on good working relationships with a variety of entities including airlines, steamship lines and governmental agencies. The Company considers its current working relationships with these entities to be satisfactory. However, changes in the financial stability and operating capabilities of asset-based carriers, space allotments available from carriers, governmental deregulation efforts, “modernization” of the regulations governing customs clearance, and/or changes in governmental quota restrictions could affect the Company’s business in unpredictable ways.

| 7.

Table of Contents

Seasonality

Historically, the Company’s operating results have been subject to seasonal trends when measured on a quarterly basis. The first quarter has traditionally been the weakest and the third and fourth quarters have traditionally been the strongest. This pattern has been the result of, or influenced by, numerous factors including weather patterns, national holidays, consumer demand, economic conditions and a myriad of other similar and subtle forces. In addition, this historical quarterly trend has been influenced by the growth and diversification of the Company’s international network and service offerings. The Company cannot accurately forecast many of these factors, nor can the Company estimate accurately the relative influence of any particular factor and, as a result, there can be no assurance that historical patterns will continue in future periods.

Environmental

In the United States, the Company is subject to Federal, state and local provisions regulating the discharge of materials into the environment or otherwise for the protection of the environment. Similar laws apply in many other jurisdictions in which the Company operates. Although current operations have not been significantly affected by compliance with these environmental laws, governments are becoming increasingly sensitive to environmental issues, and the Company cannot predict what impact future environmental regulations may have on its business. The Company does not anticipate making any material capital expenditures for environmental control purposes during the remainder of the current or succeeding fiscal years.

Employees

At January 31, 2011, the Company employed approximately 12,880 people, 4,410 in the United States and 730 in the balance of North America, 620 in Latin America, 3,850 in Asia Pacific, 2,100 in Europe and Africa, and 1,170 in the Middle East. Approximately 1,730 of the Company’s employees are engaged principally in sales and marketing and customer service, 7,550 in operations and 3,600 in finance and administration. The Company is not a party to any collective bargaining agreement and considers its relations with its employees to be satisfactory.

In order to retain the services of highly qualified, experienced, and motivated employees, the Company places considerable emphasis on its non-equity incentive compensation programs and stock option plans.

Executive Officers of the Registrant

The following table sets forth the names, ages, and positions of current executive officers of the Company.

| Name | Age | Position | ||||

| Peter J. Rose |

67 | Chairman and Chief Executive Officer and director | ||||

| James L.K. Wang |

63 | President-Asia Pacific and director | ||||

| R. Jordan Gates |

55 | President and Chief Operating Officer, director | ||||

| Rommel C. Saber |

53 | President-Europe, Africa, Near/Middle East and Indian Subcontinent | ||||

| Robert L. Villanueva |

58 | President-The Americas | ||||

| Timothy C. Barber |

51 | President-Global Sales and Marketing | ||||

| Rosanne Esposito |

59 | Executive Vice President-Global Customs | ||||

| Eugene K. Alger |

50 | Executive Vice President-North America | ||||

| Philip M. Coughlin |

50 | Executive Vice President-North America | ||||

| Jeffrey S. Musser |

45 | Executive Vice President and Chief Information Officer | ||||

| Charles J. Lynch |

50 | Senior Vice President-Corporate Controller | ||||

| Daniel R. Wall |

42 | Senior Vice President-Ocean Services | ||||

| Jose A. Ubeda |

44 | Senior Vice President-Air Cargo | ||||

| Amy J. Tangeman |

42 | Vice President-General Counsel and Secretary | ||||

| Bradley S. Powell |

50 | Chief Financial Officer | ||||

8. |

Table of Contents

Peter J. Rose has served as a director and Vice President of the Company since July 1981. Mr. Rose was elected a Senior Vice President of the Company in May 1986, Executive Vice President in May 1987, President and Chief Executive Officer in October 1988, and Chairman and Chief Executive Officer in May 1991.

James L.K. Wang has served as a director and the Managing Director of Expeditors International Taiwan Ltd., the Company’s former exclusive Taiwan agent, since September 1981. In 1991, Mr. Wang’s employment agreement was assigned to E.I. Freight (Taiwan), Ltd., the Company’s exclusive Taiwan agent through 2004. Mr. Wang’s contract is now assigned to ECI Taiwan Co. Ltd., a wholly-owned subsidiary of the Company. In October 1988, Mr. Wang became a director of the Company and its Director-Far East, and Executive Vice President in January 1996. In May 2000, Mr. Wang was elected President-Asia.

R. Jordan Gates joined the Company as its Controller-Europe in February 1991. Mr. Gates was elected Chief Financial Officer and Treasurer of the Company in August 1994 and Senior Vice President-Chief Financial Officer and Treasurer in January 1998. In May 2000, Mr. Gates was elected Executive Vice President-Chief Financial Officer and Treasurer. Mr. Gates was also elected as a director in May 2000. On January 1, 2008, Mr. Gates assumed the role of President and Chief Operating Officer.

Rommel C. Saber joined the Company as Director-Near/Middle East in February 1990 and was elected Senior Vice President-Sales and Marketing in January 1993. Mr. Saber was elected Senior Vice President-Air Export in September 1993. In July 1997, Mr. Saber was elected Senior Vice President Near/Middle East and Indian Subcontinent and Executive Vice President-Europe, Africa and Near/Middle East in August 2000. In February 2006, Mr. Saber was elected President-Europe, Africa, Near/Middle East and Indian Subcontinent.

Robert L. Villanueva joined the Company as Regional Vice President Northwest U.S. Region in April 1994. In September 1999, he was elected Executive Vice President-The Americas and President-The Americas in May 2004.

Timothy C. Barber joined the Company in May 1986. Mr. Barber was promoted to District Manager of the Seattle office in January 1987 and Regional Vice President in January 1993. Mr. Barber was elected Vice President-Sales and Marketing in September 1993 and Senior Vice President-Sales and Marketing in January 1998. In September 1999, Mr. Barber was elected Executive Vice President-Global Sales. On January 1, 2008, Mr. Barber assumed the role of President-Global Sales and Marketing.

Rosanne Esposito joined the Company as its Director-U.S. Import Services in January 1996. Ms. Esposito was promoted to Vice President in May 1997 and Senior Vice President-Global Customs in May 2001. In May 2004, Ms. Esposito was promoted to Executive Vice President-Global Customs.

Eugene K. Alger joined the Company in October 1982. Mr. Alger was promoted to District Manager and Regional Vice President of the Los Angeles office in May 1983. He was elected Regional Vice President-Southwestern U.S. and Mexico Region in January 1992, and Senior Vice President of North America in September 1999. In March, 2008, he was promoted to Executive Vice President-North America.

Philip M. Coughlin joined the Company in October 1985. In August 1986, Mr. Coughlin was promoted to District Manager. Mr. Coughlin was elected Regional Manager for New England and Canada in January 1991, Regional Vice President-Northeastern U.S. and Northern Border in January 1992, and Senior Vice President of North America in September 1999. In March, 2008, he was promoted to Executive Vice President-North America.

Jeffrey S. Musser joined the Company in February 1983. Mr. Musser was promoted to District Manager in October 1989 and Regional Vice President in September 1999. Mr. Musser was elected Senior Vice President-Chief Information Officer in January 2005. In May 2009, Mr. Musser was promoted to Executive Vice President and Chief Information Officer.

Charles J. Lynch joined the Company in September 1984. Mr. Lynch was promoted to Assistant Controller in July 1985 and Controller-Domestic Operations in January 1989. Mr. Lynch was elected Corporate Controller in January 1991 and Vice President-Corporate Controller in January 1998. In May 2002, Mr. Lynch was elected Senior Vice President-Corporate Controller.

Daniel R. Wall joined the Company in March 1987. Mr. Wall was promoted to District Manager in May 1992 and Global Director-Account Management in March 2002. Mr. Wall was elected Vice President-ECMS in January 2004 and Senior Vice President-Ocean Services in September 2004.

| 9.

Table of Contents

Jose A. Ubeda joined the Company in May 1984. Mr. Ubeda was promoted to District Manager in February 1993 and to Regional Vice President-Northwest U.S. Region in May 2000. In April 2010, Mr. Ubeda was promoted to Senior Vice President-Air Cargo.

Amy J. Tangeman joined the Company in January 1997. Ms. Tangeman was promoted to Assistant General Counsel in November 2001. In October 2006, Ms. Tangeman was elected Vice-President-General Counsel and Secretary.

Bradley S. Powell joined the Company as Chief Financial Officer in October 2008. Prior to joining the Company, Mr. Powell served as President and Chief Financial Officer of Eden Bioscience Corporation, a publicly-traded biotechnology company, from December 2006 to September 2008 and as Vice President and Chief Financial Officer from July 1998 to December 2006.

Regulation and Security

With respect to the Company’s activities in the air transportation industry in the United States, it is subject to regulation by the Transportation Security Administration (“TSA”) of the Department of Homeland Security as an indirect air carrier. All United States indirect air carriers are required to maintain prescribed security procedures and are subject to periodic audits by TSA. The Company’s overseas offices and agents are licensed as airfreight forwarders in their respective countries of operation. The Company is licensed in each of its offices, or in the case of its newer offices, has made application for a license as an airfreight forwarder by the International Air Transport Association (“IATA”). IATA is a voluntary association of airlines and air transport related entities which prescribes certain operating procedures for airfreight forwarders acting as agents for its members. The majority of the Company’s airfreight forwarding business is conducted with airlines which are IATA members.

The Company is licensed as an Ocean Transportation Intermediary (“OTI”) (sometimes referred to as NVOCC-Non-Vessel Operating Common Carrier) by the Federal Maritime Commission (“FMC”). The FMC has established certain qualifications for shipping agents, including certain surety bonding requirements. The FMC is also responsible for the economic regulation of OTI/NVOCC activity originating or terminating in the United States. To comply with these economic regulations, vessel operators and NVOCCs, such as EIO, are required to file tariffs electronically which establish the rates to be charged for the movement of specified commodities into and out of the United States. The FMC has the power to enforce these regulations by assessing penalties.

The Company is licensed as a customs broker by Customs and Border Protection (“CBP”) of the Department of Homeland Security nationally and in each U.S. customs district in which it does business. All United States customs brokers are required to maintain prescribed records and are subject to periodic audits by CBP. In other jurisdictions in which the Company performs clearance services, the Company is licensed by the appropriate governmental authority (where such license is required to perform these services). The Company participates in various governmental supply chain security programs, such as the Customs-Trade Partnership Against Terrorism (“C-TPAT”) in the United States and additional security initiatives as they continue to be enacted by different governments, such as Authorized Economic Operator (“AEO”).

The Company does not believe that current United States and foreign governmental regulations impose significant economic restraint upon its business operations. In general, the Company conducts its business activities in each country through a majority-owned subsidiary corporation that is organized and existing under the laws of that country. However, the regulations of foreign governments can impose barriers to the Company’s ability to provide the full range of its business activities in a wholly or majority United States-owned subsidiary. For example, foreign ownership of a customs brokerage business is prohibited in some jurisdictions and less frequently the ownership of the licenses required for freight forwarding and/or freight consolidation is restricted to local entities. When the Company encounters this sort of governmental restriction, it works to establish a legal structure that meets the requirements of the local regulations while also giving the Company the substantive operating and economic advantages that would be available in the absence of such regulation. This can be accomplished by creating a joint venture or exclusive agency relationship with a qualified local entity that holds the required license. The war on terror and governments’ overriding concern for the safety of passengers and citizens who import and/or export goods into and out of their respective countries has resulted in a proliferation

10. |

Table of Contents

of cargo security regulations over the past several years. While these cargo regulations have already created a marked difference in the security arrangements required to move shipments around the globe, regulations are expected to become more stringent in the future. As governments look for ways to minimize the exposure of their citizens to potential terror related incidents, the Company and its competitors in the transportation business may be required to incorporate security procedures within their scope of services to a far greater degree than has been required in the past. The Company feels that increased security requirements may involve further investments in technology and more sophisticated screening procedures being applied to potential customers, vendors and employees. The Company’s position is that any increased cost of compliance with security regulations will be passed through to those who are beneficiaries of the Company’s services.

Cargo Liability

When acting as an airfreight consolidator, the Company assumes a carrier’s liability for lost or damaged shipments. This legal liability is typically limited by contract to the lower of the transaction value or the released value (17 Special Drawing Rights per kilo unless the customer declares a higher value and pays a surcharge), except if the loss or damage is caused by willful misconduct or in the absence of an appropriate airway bill. The airline which the Company utilizes to make the actual shipment is generally liable to the Company in the same manner and to the same extent. When acting solely as the agent of the airline or shipper, the Company does not assume any contractual liability for loss or damage to shipments tendered to the airline.

When acting as an ocean freight consolidator, the Company assumes a carrier’s liability for lost or damaged shipments. This liability is typically limited by contract to the lower of the transaction value or the released value ($500 per package or customary freight unit unless the customer declares a higher value and pays a surcharge). The steamship line which the Company utilizes to make the actual shipment is generally liable to the Company in the same manner and to the same extent. In its ocean freight forwarding and customs clearance operations, the Company does not assume cargo liability.

When providing warehouse and distribution services, the Company limits its legal liability by contract and tariff to an amount generally equal to the lower of fair value or $0.50 per pound with a maximum of $50 per “lot” — which is defined as the smallest unit that the warehouse is required to track. Upon payment of a surcharge for warehouse and distribution services, the Company will assume additional liability.

The Company maintains cargo legal liability insurance covering claims for losses attributable to missing or damaged shipments for which it is legally liable. The Company also maintains insurance coverage for the property of others which is stored in Company warehouse facilities. This insurance coverage is provided by a Vermont U.S. based insurance entity wholly-owned by the Company. The coverage is fronted and reinsured by a global insurance company. The total risk retained by the Company in 2010 was approximately $4 million. In addition, the Company is licensed as an insurance broker through its subsidiary, Expeditors Cargo Insurance Brokers, Inc. and places insurance coverage for other customers.

| 11.

Table of Contents

ITEM 1A — RISK FACTORS

| RISK FACTORS | DISCUSSION AND POTENTIAL SIGNIFICANCE | |

| International Trade |

The Company primarily provides services to customers engaged in international commerce. Everything that affects international trade has the potential to expand or contract the Company’s primary market and impact its operating results. For example, international trade is influenced by: | |

| • currency exchange rate and currency control regulations; | ||

| • interest rate fluctuations; | ||

| • changes in governmental policies, such as taxation, quota restrictions, other forms of trade barriers and/or restrictions and trade accords; | ||

| • changes in and application of international and domestic customs, trade and security regulations; | ||

| • wars, strikes, civil unrest, acts of terrorism, and other conflicts; | ||

| • natural disasters and pandemics; | ||

| • changes in consumer attitudes regarding goods made in countries other than their own; | ||

| • changes in availability of credit; | ||

| • changes in the price and readily available quantities of oil and other petroleum-related products; and | ||

| • increased global concerns regarding environmental sustainability. | ||

| Third Party Suppliers |

The Company is a non-asset based provider of global logistics services. As a result, the Company depends on a variety of asset-based third party suppliers. The quality and profitability of the Company’s services depend upon effective selection, management and discipline of third party suppliers, while operations have improved in 2010, many of the Company’s third party suppliers have incurred significant operating losses in 2009 and are highly leveraged with debt. Changes in the financial stability, operating capabilities and capacity of asset-based carriers and space allotment made available to the Company by asset-based carriers could affect the Company in unpredictable ways, including volatility of pricing, and challenge the Company’s ability to maintain historical unitary profitability. | |

| Predictability of Results |

The Company is not aware of any accurate means of forecasting short-term customer requirements. However, long-term customer satisfaction depends upon the Company’s ability to meet these unpredictable short-term customer requirements. Personnel costs, the Company’s single largest variable expense, are always less flexible in the very near term as the Company must staff to meet uncertain demand. As a result, short-term operating results could be disproportionately affected. | |

12. |

Table of Contents

| RISK FACTORS | DISCUSSION AND POTENTIAL SIGNIFICANCE | |

| A significant portion of the Company’s revenues are derived from customers in retail industries whose shipping patterns are tied closely to consumer demand, and from customers in industries whose shipping patterns are dependent upon just-in-time production schedules. Therefore, the timing of the Company’s revenues are, to a large degree, impacted by factors out of the Company’s control, such as a sudden change in consumer demand for retail goods and/or manufacturing production delays. Additionally, many customers ship a significant portion of their goods at or near the end of a quarter, and therefore, the Company may not learn of a shortfall in revenues until late in a quarter. To the extent that a shortfall in revenues or earnings was not expected by securities analysts, any such shortfall from levels predicted by securities analysts could have an immediate and adverse effect on the trading price of the Company’s stock. | ||

| Foreign Operations |

The majority of the Company’s revenues and operating income comes from operations conducted outside the United States. To maintain a global service network, the Company may be required to operate in hostile locations and in dangerous situations.

In addition, the Company operates in parts of the world where common business practices could constitute violations of the anti-corruption laws, rules, regulations and decrees of the United States, including the U.S. Foreign Corrupt Practices Act, and of all other countries in which the Company conducts business; as well as trade control laws, or laws, regulations and Executive Orders imposing embargoes and sanctions; and anti-boycott laws and regulations. Compliance with these laws, rules, regulations and decrees is dependent on the Company’s employees, subcontractors, agents, third party brokers and customers, whose individual actions could violate these laws, rules, regulations and decrees. Failure to comply could result in substantial penalties and additional expenses, damages to the Company’s reputation and restrictions on its ability to conduct business. | |

| Key Personnel |

The Company is a service business. The quality of this service is directly related to the quality of the Company’s employees. Identifying, training and retaining key employees is essential to continued growth and future profitability. Continued loyalty to the Company will not be assured by contract.

The Company believes that its compensation programs, which have been in place since the Company became a publicly traded entity, are one of the unique characteristics responsible for differentiating its performance from that of many of its competitors. Significant changes to its compensation programs could affect the Company’s performance. | |

| Technology |

Increasingly, the Company must compete based upon the flexibility and sophistication of the technologies utilized in performing its core businesses. Future results depend upon the Company’s success in the cost effective development, maintenance and integration of communication and information systems technologies, including those of third party suppliers. Any significant disruptions to these systems could negatively affect the Company’s results. | |

| 13.

Table of Contents

| RISK FACTORS | DISCUSSION AND POTENTIAL SIGNIFICANCE | |

| Growth |

To date, the Company has relied primarily upon organic growth and has tended to avoid growth through acquisition. Future results will depend upon the Company’s ability to continue to grow internally or to demonstrate the ability to successfully identify and integrate non-dilutive acquisitions. | |

| Regulatory Environment |

The Company is affected by ever increasing regulations from a number of sources. The current business environment tends to stress the avoidance of risk through regulation and oversight, the effect of which is likely to be unforeseen costs and potentially unforeseen consequences.

In reaction to the global war on terror, governments around the world are continuously enacting or updating security regulations. These regulations are multi-layered, increasingly technical in nature and characterized by a lack of harmonization of substantive requirements amongst various governmental authorities. Furthermore, the implementation of these regulations, including deadlines and substantive requirements, is driven by political urgencies rather than the industries’ realistic ability to comply. Failure to consistently and timely comply with these regulations, or the failure, breach or compromise of the Company’s security procedures or those of its subcontractors or agents, may result in increased operating costs, damage to the Company’s reputation, restrictions on operations and/or fines and penalties. | |

| Competition |

The global logistics services industry is intensely competitive and is expected to remain so for the foreseeable future. There are a large number of companies competing in one or more segments of the industry, but the number of firms with a global network that offer a full complement of logistics services is more limited. Depending on the location of the shipper and the importer, the Company must compete against both the niche players and larger entities. | |

| Taxes |

The Company is subject to many taxes in the United States and foreign jurisdictions. In many of these jurisdictions, the tax laws are very complex and are open to different interpretations and application. Tax authorities frequently change their tax rules, reconciliations and rates. The Company is regularly under audit by tax authorities. Although the Company believes its tax estimates are reasonable, the final determination of tax audits could be materially different from the Company’s tax provisions and accruals and negatively impact its financial results. | |

| Litigation/Investigations |

As a multinational corporation, the Company is subject to formal or informal investigations or litigation from governmental authorities or others in the countries in which it does business. The Company is currently subject to, and is cooperating fully with, an investigation by the U.S. Department of Justice (DOJ) of air cargo freight forwarders. In addition, the Company and its Hong Kong subsidiary received a Statement of Objections from the European Commission (EC) relating to an ongoing investigation of freight forwarders. The Company and its Brazilian subsidiary also received an Administrative Proceeding from the Brazilian Ministry of Justice (MOJ) relating to an on-going investigation of freight forwarders. These investigations will require further management time and cause the Company to incur substantial additional legal and related costs, which could include fines and/or penalties if the DOJ, EC and/or MOJ concludes that the Company has engaged in anti-competitive behavior and such fines and/or penalties could have a material impact on the Company’s financial position, results of operations and operating cash flows. | |

14. |

Table of Contents

| RISK FACTORS | DISCUSSION AND POTENTIAL SIGNIFICANCE | |

| The Company is currently subject to and may become subject to other civil litigation arising from these investigations, including but not limited to shareholder class action lawsuits and derivative claims made on behalf of the Company. The Company has been named as a defendant in a Federal anti-trust class action lawsuit filed in New York and will incur additional costs related to defending itself in these proceedings. | ||

| Economic Conditions |

The global economy and capital and credit markets continue to experience uncertainty and volatility. Unfavorable changes in economic conditions may result in lower freight volumes and adversely affect the Company’s revenues and operating results, as experienced in 2009. These conditions may adversely affect certain of the Company’s customers and third party suppliers. Were that to occur, the Company’s revenues and net earnings could also be adversely affected. Should customers’ ability to pay deteriorate, additional bad debts may be incurred.

These unfavorable conditions can create situations where rate increases charged by carriers and other suppliers are implemented with little or no advanced notice. The Company often times cannot pass these rate increases on to its customers in the same time frame, if at all. As a result, the Company’s yields and margins can be negatively impacted. | |

| Catastrophic Events |

A disruption or failure of the Company’s systems or operations in the event of a major earthquake, weather event, cyber-attack, terrorist attack, strike, civil unrest, pandemic or other catastrophic event could cause delays in providing services or performing other mission-critical functions. The Company’s corporate headquarters, and certain other critical business operations are in the Seattle, Washington area, which is near major earthquake faults. A catastrophic event that results in the destruction or disruption of any of the Company’s critical business or information technology systems could harm the Company’s ability to conduct normal business operations and its operating results. | |

ITEM 1B — UNRESOLVED STAFF COMMENTS

Not applicable.

| 15.

Table of Contents

ITEM 2 — PROPERTIES

The Company owns the following properties:

| Location | Nature of Property | |

| United States: |

||

| Seattle, Washington |

Office buildings | |

| Near Seattle-Tacoma International Airport (in Washington) |

Office building | |

| Houston, Texas |

Office and warehouse | |

| Nassau County, New York |

Office and warehouse | |

| Middlesex County, New Jersey |

Office and warehouse | |

| Near San Francisco International Airport (in California) |

Office and warehouse | |

| Near Los Angeles International Airport (in California) |

Office and warehouse | |

| Near O’Hare International Airport (in Illinois) |

Office and warehouse | |

| Miami, Florida |

Office, warehouse and free trade zone* | |

| Spokane, Washington |

Office building | |

| Asia: |

||

| Kowloon, Hong Kong |

Offices | |

| Taipei, Taiwan |

Office | |

| Seoul, Korea |

Office | |

| Shanghai, China |

Office building | |

| Europe: |

||

| Brussels, Belgium |

Office and warehouse | |

| Dublin, Ireland |

Office and warehouse | |

| Cork, Ireland |

Office and warehouse | |

| Near Heathrow Airport (in London, England) |

Acreage | |

| Latin America: |

||

| Alajuela, Costa Rica |

Office building | |

| Middle East: |

||

| Cairo, Egypt |

Office and warehouse | |

| * | Company directly owns 50% with Cargo Ventures, LLC, a private, non-affiliated real estate development company. |

The Company leases and maintains 68 additional offices and satellite locations in the United States and 356 leased locations throughout the world, each located close to an airport, ocean port, or on an important border crossing. The majority of these facilities contain warehouse facilities. Lease terms are either on a month-to-month basis or terminate at various times through 2020. See Note 7 to the Company’s consolidated financial statements for lease commitments. As an office matures, the Company will investigate the possibility of building or buying suitable facilities. The Company believes that current leases can be extended and that suitable alternative facilities are available in the vicinity of each present facility should extensions be unavailable at the conclusion of current leases.

16. |

Table of Contents

ITEM 3 — LEGAL PROCEEDINGS

On October 10, 2007, the U. S. Department of Justice (DOJ) issued a subpoena ordering the Company to produce certain information and records relating to an investigation of alleged anti-competitive behavior amongst air cargo freight forwarders. The Company has retained the services of a law firm to assist in complying with the DOJ’s subpoena. As part of this process, the Company has met with and continues to co-operate with the DOJ. The Company expects to incur additional costs during the course of this ongoing investigation, which could include fines and/or penalties if the DOJ concludes that the Company has engaged in anti-competitive behavior and such fines and/or penalties could have a material impact on the Company’s financial position, results of operations and operating cash flows.

On January 3, 2008, the Company was named as a defendant, with seven other European and North American-based global logistics providers, in a Federal antitrust class action lawsuit filed in the United States District Court of the Eastern District of New York, Precision Associates, Inc. et al v. Panalpina World Transport, No. 08-CV0042. On July 21, 2009, the plaintiffs filed an amended complaint adding a number of new third party defendants and various claims which they assert to violate the Sherman Act. The plaintiffs’ amended complaint, which purports to be brought on behalf of a class of customers (and has not yet been certified), asserts claims that the defendants engaged in price fixing regarding eight discrete surcharges in violation of the Sherman Act. The allegations concerning the Company relate to two of these surcharges. The amended complaint seeks unspecified damages and injunctive relief. The Company believes that these allegations are without merit and intends to vigorously defend itself. On August 13, 2009, the Company filed a motion to dismiss the amended complaint for failure to state a claim. Plaintiffs filed their opposition to the Company’s motion on January 30, 2010, to which the Company filed a reply, and the motion is currently pending before the Court.

On June 18, 2008, the European Commission (EC) issued a request for information to the Company’s UK subsidiary, Expeditors International (UK) Ltd., requesting certain information relating to an ongoing investigation of freight forwarders. The Company replied to the request. On February 18, 2009, the EC issued another request for information to the same subsidiary requesting certain additional information in connection with the EC’s ongoing investigation of freight forwarders. The Company replied to the request. On February 10, 2010, the Company and its Hong Kong subsidiary, Expeditors Hong Kong Limited, received a Statement of Objections (SO) from the EC. The SO initiates a proceeding against the Company alleging anti-competitive behavior contrary to European Union rules on competition. Specific to the Company, the allegations in the SO are limited to the period from August 2005 to June 2006 and only concern airfreight trade lanes between South China/Hong Kong and the European Economic Area. The Company filed a response to the allegations in the SO on April 12, 2010 and participated in an oral hearing on July 6, 2010. On January 20, 2011, the EC issued another request for information to the Company and its Hong Kong subsidiary requesting certain additional information in connection with its on-going investigation of freight forwarders. The Company replied to the request. The Company continues to vigorously defend itself against the allegations. The Company expects to incur additional costs during the course of this ongoing proceeding, which could include administrative fines if the EC concludes that the Company has engaged in anti-competitive behavior and such fines could have a material impact on the Company’s financial position, results of operations and operating cash flows.

On August 17, 2010, the Company and its Brazilian subsidiary, Expeditors Internacional do Brasil Ltda received an Administrative Proceeding (AP) from the Brazilian Ministry of Justice (MOJ). The AP initiates a proceeding against the Company and one of its employees, alleging possible anti-competitive behavior. The Company intends to vigorously defend itself against the allegations. The Company expects to incur additional costs during the course of this proceeding, which could include administrative fines if the MOJ concludes that the Company has engaged in anti-competitive behavior and such fines could have a material impact on the Company’s financial position, results of operations and operating cash flows.

The proceedings described above generally relate to investigations of freight forwarders or allegations of anti-competitive behavior. The distractions caused by these proceedings and the legal and other costs associated with these proceedings have been significant. The Company has incurred approximately $1 million, less than $1 million, and approximately $10 million for the years ended December 31, 2010, 2009 and 2008, respectively, in legal

| 17.

Table of Contents

and associated costs on the above matters. Since the beginning of the proceedings in 2007, the Company has incurred approximately $15 million in legal and associated costs on the above matters. At this time the Company is unable to estimate the range of loss or damages, if any, that might result as an outcome of any of these proceedings. The Company assumes, as should investors, that these challenges could continue for a significant period of time and may require the investment of substantial additional management time and substantial financial resources. These government investigations and the related litigation matters are subject to inherent uncertainties, and unfavorable rulings could occur. An unfavorable ruling could include substantial monetary damages and, in matters in which injunctive relief or other conduct remedies are sought, an injunction or other order relating to business conduct. Were unfavorable final outcomes to occur, the Company’s business, financial position, results of operations, and operating cash flows could be materially harmed.

The Company is involved in other claims and lawsuits which arise in the ordinary course of business, none of which currently, in management’s opinion, will have a significant effect on the Company’s operations or financial position.

18. |

Table of Contents

PART II

ITEM 5 — MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES

The following table sets forth the high and low sale prices for the Company’s common stock as reported by The NASDAQ Global Select Market under the symbol EXPD.

| Common Stock | Common Stock | |||||||||||||||||

| Quarter | High | Low | Quarter | High | Low | |||||||||||||

| 2010 |

2009 |

|||||||||||||||||

| First |

$ | 38.93 | $ | 32.36 | First |

$ | 34.59 | $ | 23.86 | |||||||||

| Second |

$ | 42.39 | $ | 34.46 | Second |

$ | 38.10 | $ | 27.26 | |||||||||

| Third |

$ | 47.58 | $ | 33.65 | Third |

$ | 37.04 | $ | 24.50 | |||||||||

| Fourth |

$ | 57.15 | $ | 45.23 | Fourth |

$ | 35.83 | $ | 31.27 | |||||||||

There were 1,347 shareholders of record as of February 18, 2011. This figure does not include a substantially greater number of beneficial holders of the Company’s common stock, whose shares are held of record by banks, brokers and other financial institutions.

The Board of Directors declared semi-annual dividends during the two most recent fiscal years paid as follows:

| June 15, 2010 |

$ | .20 | ||

| December 15, 2010 |

$ | .20 | ||

| June 15, 2009 |

$ | .19 | ||

| December 15, 2009 |

$ | .19 | ||

ISSUER PURCHASES OF EQUITY SECURITIES

| Period | Total Number of Shares Purchased |

Average Price Paid per Share |

Total Number of Shares Purchased as Part of Publicly Announced Plans or Programs |

Maximum Number of Shares that May Yet Be Purchased Under the Plans or Programs |

||||||||||||

| October 1-31, 2010 |

64 | $ | 48.09 | 64 | 31,241,990 | |||||||||||

| November 1-30, 2010 |

1,244,011 | $ | 51.33 | 1,244,011 | 30,637,955 | |||||||||||

| December 1-31, 2010 |

763,818 | $ | 56.30 | 763,818 | 30,177,722 | |||||||||||

| Total |

2,007,893 | $ | 53.22 | 2,007,893 | 30,177,722 | |||||||||||

In November 1993, the Company’s Board of Directors authorized a Non-Discretionary Stock Repurchase Plan for the purpose of repurchasing the Company’s common stock in the open market with the proceeds received from the exercise of stock options. On February 9, 2009, the Plan was amended to increase the authorization to repurchase up to 40 million shares of the Company’s common stock. This authorization has no expiration date. This plan was disclosed in the Company’s report on Form 10-K filed March 31, 1995. In the fourth quarter of 2010, 755,736 shares of common stock were repurchased under the Non-Discretionary Stock Repurchase Plan.

| 19.

Table of Contents

In November 2001, under a Discretionary Stock Repurchase Plan, the Company’s Board of Directors authorized the repurchase of such shares as may be necessary to reduce the issued and outstanding stock to 200 million shares of common stock. The maximum number of shares available for repurchase under this plan will increase as the total number of outstanding shares increases. This authorization has no expiration date. This plan was announced on November 13, 2001. In the fourth quarter of 2010, 1,252,157 shares of common stock were repurchased under the Discretionary Stock Repurchase Plan. These discretionary repurchases were made to limit the growth in the number of issued and outstanding shares resulting from stock option exercises and the exercise of employee stock purchase rights.

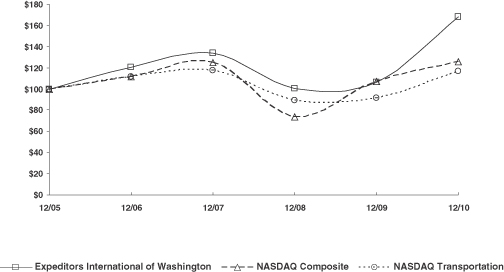

The graph below matches the cumulative 5-year total return of holders of Expeditors International of Washington’s common stock with the cumulative total returns of the NASDAQ Composite index and the NASDAQ Transportation index. The graph assumes that the value of the investment in the company’s common stock and in each of the indexes (including reinvestment of dividends) was $100 on 12/31/2005 and tracks it through 12/31/2010.

COMPARISON OF 5 YEAR CUMULATIVE TOTAL RETURN*

Among Expeditors International of Washington, the NASDAQ Composite Index

and the NASDAQ Transportation Index

* $100 invested on 12/31/05 in stock or index, including reinvestment of dividends. Fiscal year ending December 31.

| 12/05 | 12/06 | 12/07 | 12/08 | 12/09 | 12/10 | |||||||||||||||||||

| Expeditors International of Washington |

100.00 | 120.54 | 133.83 | 100.47 | 106.24 | 168.33 | ||||||||||||||||||

| NASDAQ Composite |

100.00 | 111.74 | 124.67 | 73.77 | 107.12 | 125.93 | ||||||||||||||||||

| NASDAQ Transportation |

100.00 | 111.57 | 117.39 | 88.90 | 91.15 | 117.01 | ||||||||||||||||||

The stock price performance included in this graph is not necessarily indicative of future stock price performance.

20. |

Table of Contents

ITEM 6 — SELECTED FINANCIAL DATA

Financial Highlights

In thousands except per share data

| 2010 | 2009 | 2008 | 2007 | 2006 | ||||||||||||||||

| Revenues |

$ | 5,967,573 | 4,092,283 | 5,633,878 | 5,235,171 | 4,633,987 | ||||||||||||||

| Net revenues |

1,692,786 | 1,382,786 | 1,603,261 | 1,452,961 | 1,290,960 | |||||||||||||||

| Net earnings attributable to shareholders |

344,172 | 240,217 | 301,014 | 269,154 | 235,094 | |||||||||||||||

| Diluted earnings attributable to shareholders per share |

1.59 | 1.11 | 1.37 | 1.21 | 1.06 | |||||||||||||||

| Basic earnings attributable to shareholders per share |

1.62 | 1.13 | 1.41 | 1.26 | 1.10 | |||||||||||||||

| Dividends declared and paid per common share |

.40 | .38 | .32 | .28 | .22 | |||||||||||||||

| Working capital |

1,278,377 | 1,079,444 | 903,010 | 764,944 | 632,691 | |||||||||||||||

| Total assets |

2,679,179 | 2,323,722 | 2,100,839 | 2,068,605 | 1,821,878 | |||||||||||||||

| Shareholders’ equity |

1,740,906 | 1,553,007 | 1,366,418 | 1,226,571 | 1,070,091 | |||||||||||||||

| Weighted average diluted shares outstanding |

216,446,656 | 216,533,240 | 219,170,003 | 221,799,868 | 222,223,312 | |||||||||||||||

| Weighted average basic shares outstanding |

212,283,966 | 212,112,744 | 212,755,946 | 213,314,761 | 213,454,579 | |||||||||||||||

All share and per share information have been adjusted to reflect a 2-for-1 stock split effected in June, 2006.

SAFE HARBOR FOR FORWARD-LOOKING STATEMENTS UNDER PRIVATE SECURITIES LITIGATION REFORM ACT OF 1995; CERTAIN CAUTIONARY STATEMENTS

From time to time, the Company or its representatives have made or may make forward-looking statements, orally or in writing. Such forward-looking statements may be included in, but not limited to, press releases, oral statements made with the approval of an authorized executive officer or in various filings made by the Company with the Securities and Exchange Commission. The words or phrases “will likely result”, “are expected to”, “will continue”, “is anticipated”, “estimate”, “project” or similar expressions are intended to identify “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. Such statements are qualified in their entirety by reference to and are accompanied by the discussion in Item 1A of certain important factors that could cause actual results to differ materially from such forward-looking statements.

The risks included in Item 1A are not exhaustive. Furthermore, reference is also made to other sections of this report which include additional factors which could adversely impact the Company’s business and financial performance. Moreover, the Company operates in a very competitive and rapidly changing environment. New risk factors emerge from time to time and it is not possible for management to predict all of such risk factors, nor can it assess the impact of all of such risk factors on the Company’s business or the extent to which any factor, or combination of factors, may cause actual results to differ materially from those contained in any forward-looking statements. Accordingly, forward-looking statements cannot be relied upon as a guarantee of actual results.

Shareholders should be aware that while the Company does, from time to time, communicate with securities analysts, it is against the Company’s policy to disclose to such analysts any material non-public information or other confidential commercial information. Accordingly, shareholders should not assume that the Company agrees with any statement or report issued by any analyst irrespective of the content of such statement or report. Furthermore, the Company has a policy against issuing financial forecasts or projections or confirming the accuracy of forecasts or projections issued by others. Accordingly, to the extent that reports issued by securities analysts contain any projections, forecasts or opinions, such reports are not the responsibility of the Company.

| 21.

Table of Contents

ITEM 7 — MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

Executive Summary