Exhibit 99.1

Armstrong World Industries Reports Fourth Quarter and Full Year 2014 Results

Key Highlights

| • | Fourth quarter operating income from continuing operations of $35.9 million, down 17% over the 2013 period impacted by a non-cash intangible asset impairment charge of $10 million |

| • | Fourth quarter adjusted EBITDA from continuing operations of $78 million, up 8% over the 2013 period |

| • | Worldwide Building Products achieves record adjusted EBITDA earnings for the quarter and full year |

| • | Board of Directors approves plan to separate Flooring and Building Products businesses into two independent public companies |

LANCASTER, Pa., February 23, 2015 —Armstrong World Industries, Inc. (NYSE: AWI), a global leader in the design and manufacture of floors and ceilings, today reported fourth quarter and full year 2014 results.

Fourth Quarter Results from continuing operations

| (Amounts in millions except per share data) | Three Months Ended December 31, | |||||||||||

| 2014 | 2013 | Change | ||||||||||

| Net sales |

$ | 587.3 | $ | 614.8 | (4.5 | )% | ||||||

| Operating income |

35.9 | 43.0 | (16.5 | )% | ||||||||

| Net income |

10.6 | 23.4 | (54.7 | )% | ||||||||

| Diluted earnings per share |

$ | 0.19 | $ | 0.42 | (54.8 | )% | ||||||

Excluding the unfavorable impact from foreign exchange of $12 million, consolidated net sales decreased 2.5% compared to the prior year period, driven by lower volumes across all businesses in the Americas, which more than offset the impact from favorable price and mix.

Operating income and net income both declined compared to the prior year period, driven primarily by a non-cash impairment charge of $10 million to reduce the carrying value of a Wood Flooring trademark to its estimated fair value. The declines in operating income and net income were also driven by the margin impact of lower volumes and higher input costs, which were only partially offset by favorable price and mix, lower SG&A spending and improvements in productivity.

“We delivered fourth quarter and full year results within our guidance range when adjusting for the exit of our European Flooring business. Our worldwide ceilings business delivered yet another record quarterly and full year earnings result despite the slow pace of the recovery,” said Matt Espe, CEO. “As we separately disclosed today, I’m also pleased to announce that our Board of Directors has unanimously approved a plan to separate Armstrong into two independent industry-leading public companies, which we believe will enhance the strategic, operational and financial flexibility of both businesses and create value for our shareholders.”

Additional (non-GAAP*) Financial Metrics from continuing operations

| (Amounts in millions except per share data) | Three Months Ended December 31, | |||||||||||

| 2014 | 2013 | Change | ||||||||||

| Adjusted operating income |

$ | 47 | $ | 44 | 7 | % | ||||||

| Adjusted net income |

$ | 21 | $ | 19 | 8 | % | ||||||

| Adjusted diluted earnings per share |

$ | 0.38 | $ | 0.35 | 7 | % | ||||||

| Free cash flow |

$ | 49 | ($ | 7 | ) | Favorable | ||||||

| (Amounts in millions) | Three Months Ended December 31, | |||||||||||

| 2014 | 2013 | Change | ||||||||||

| Adjusted EBITDA |

||||||||||||

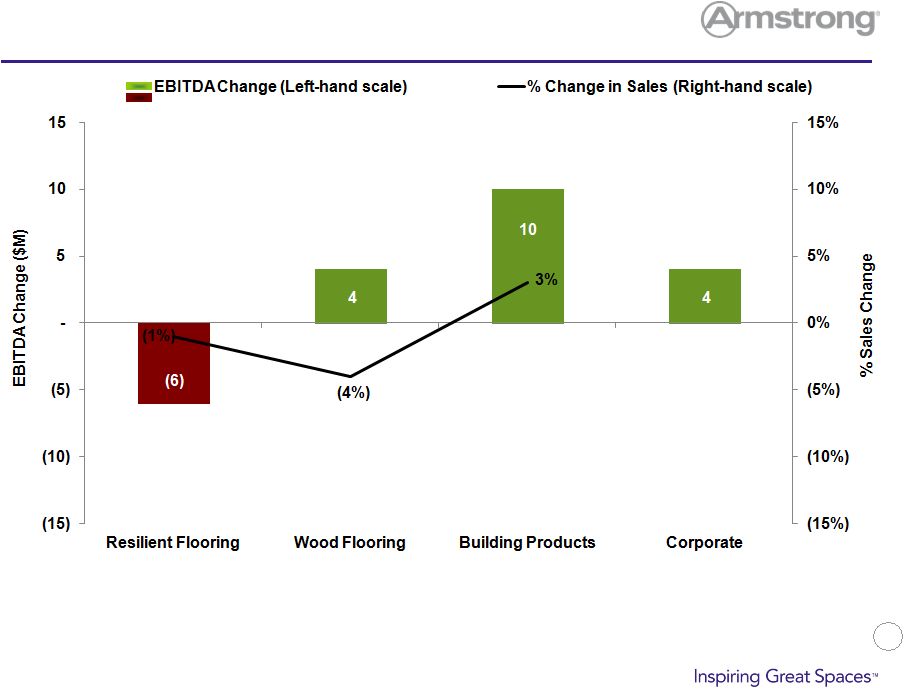

| Building Products |

$ | 73 | $ | 68 | 7 | % | ||||||

| Resilient Flooring |

21 | 18 | 20 | % | ||||||||

| Wood Flooring |

(4 | ) | 4 | Unfavorable | ||||||||

| Unallocated Corporate |

(12 | ) | (18 | ) | 28 | % | ||||||

|

|

|

|

|

|

|

|||||||

| Consolidated Adjusted EBITDA |

$ | 78 | $ | 72 | 8 | % | ||||||

| * | The Company uses the above non-GAAP adjusted measures, as well as other non-GAAP measures mentioned below, in managing the business and believes the adjustments provide meaningful comparisons of operating performance between periods. Adjusted operating income, adjusted EBITDA, adjusted net income, and adjusted EPS exclude the impact of foreign exchange, restructuring charges and related costs, impairments, the non-cash impact of the U.S. pension plan, and certain other nonrecurring gains and losses. Free cash flow is defined as cash from operations and dividends received from the WAVE joint venture, less expenditures for property and equipment, less restricted cash, and is adjusted to remove the impact of cash used or proceeds received for acquisitions and divestitures. The company believes free cash flow is useful because it provides insight into the amount of cash that the Company has available for discretionary uses, after expenditures for capital commitments and adjustments for acquisitions/divestitures. Adjusted figures are reported in comparable dollars using the budgeted exchange rate for 2014, and are reconciled to the most comparable GAAP measures in tables at the end of this release. |

Adjusted operating income and adjusted EBITDA improved by 7% and 8%, respectively, in the fourth quarter of 2014 when compared to the prior year period. The improvement in adjusted EBITDA was

driven by favorable price and mix, lower SG&A spending and improvements in productivity which more than offset the margin impact of lower volumes and higher input costs. Adjusted earnings per share is calculated using a 39% adjusted tax rate in both periods. The improvement in free cash flow was driven by the cash settlement of a Ruble hedge related to the funding of our Russia plant construction project and higher cash earnings aided by our exit from the European flooring business when compared to the prior year period.

Fourth Quarter Segment Highlights

Building Products

| Three Months Ended December 31, | ||||||||||||

| 2014 | 2013 | Change | ||||||||||

| Total segment net sales |

$ | 310.9 | $ | 320.0 | (2.8 | )% | ||||||

| Operating income |

$ | 55.4 | $ | 52.4 | 5.7 | % | ||||||

Excluding the unfavorable impact of foreign exchange of approximately $10 million, net sales increased slightly over a very strong base period as sales in the fourth quarter of 2013 were up over 9%. When looking at the net sales comparison for the fourth quarter of 2014 versus the fourth quarter of 2013, favorable price and mix offset the impact of lower volumes, primarily in the Americas. Including the favorable impact from foreign exchange of approximately $1 million, operating income increased 5.7% in the fourth quarter of 2014, driven by favorable price and mix, reductions in SG&A expenses and lower manufacturing and input costs, as strong productivity in the Americas more than offset Russia plant construction expenses. Combined, these factors more than offset the margin impact from lower volumes.

Resilient Flooring

| Three Months Ended December 31, | ||||||||||||

| 2014 | 2013 | Change | ||||||||||

| Total segment net sales |

$ | 162.8 | $ | 161.7 | 0.7 | % | ||||||

| Operating income |

$ | 15.6 | $ | 9.4 | 66.0 | % | ||||||

Net sales increased slightly, driven by positive mix performance in the Americas and volume growth in the Pacific Rim, which more than offset lower volumes in the Americas. Including the unfavorable impact from foreign exchange of approximately $1 million, operating income improved as strong productivity and favorable mix more than offset higher input costs and the margin impact of lower volumes.

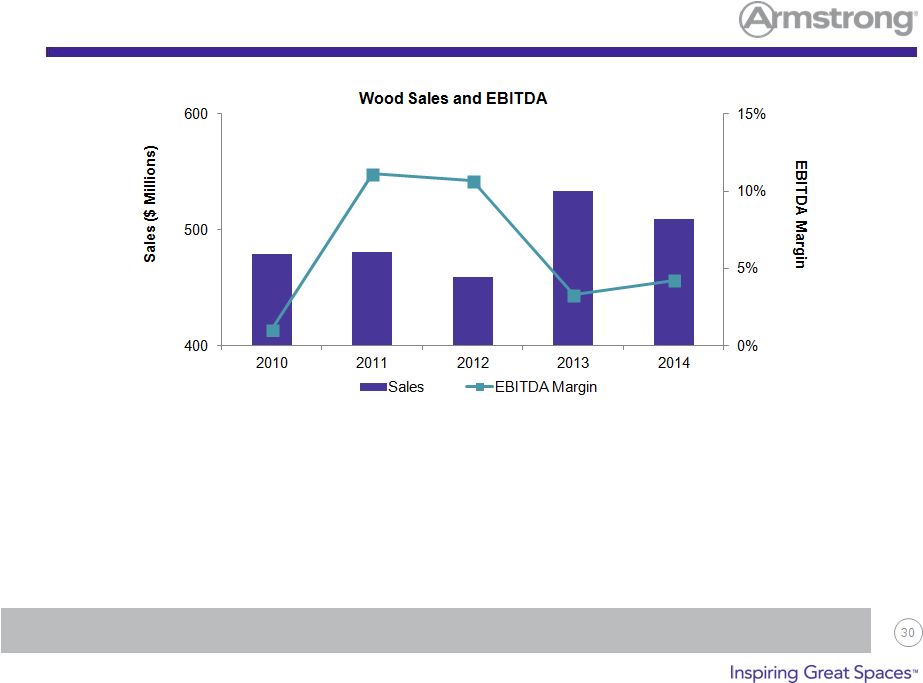

Wood Flooring

| Three Months Ended December 31, | ||||||||||||

| 2014 | 2013 | Change | ||||||||||

| Total segment net sales |

$ | 113.6 | $ | 133.1 | (14.7 | %) | ||||||

| Operating (loss) income |

($ | 19.4 | ) | $ | 0.4 | Unfavorable | ||||||

Net sales declined as improvements in price and mix were more than offset by volume declines.

Operating income declined primarily due the margin impact of lower volumes, increased manufacturing and input costs driven by higher year on year lumber costs and a slight increase in SG&A expense, which were only partially offset by positive price and mix. The comparison was impacted by a non-cash impairment charge of $10 million recorded in the fourth quarter of 2014 in cost of goods sold to reduce the carrying value of a Wood Flooring trademark to its estimated fair value in connection with an annual impairment test. Operating income was also lower due to additional expenses associated with the closure of the Kunshan, China engineered wood flooring plant.

Corporate

Unallocated corporate expense of $15.7 million decreased from $19.2 million in the prior year due to lower spending across corporate functions and lower incentive compensation accruals when compared to the prior year.

Full Year Results from continuing operations

| (Amounts in millions) | Year Ended December 31, | |||||||||||

| 2014 | 2013 | Change | ||||||||||

| Net sales (as reported) |

$ | 2,515.3 | $ | 2,527.4 | (0.5 | %) | ||||||

| Operating income (as reported) |

239.1 | 265.6 | (10.0 | %) | ||||||||

| Adjusted EBITDA |

384 | 372 | 3 | % | ||||||||

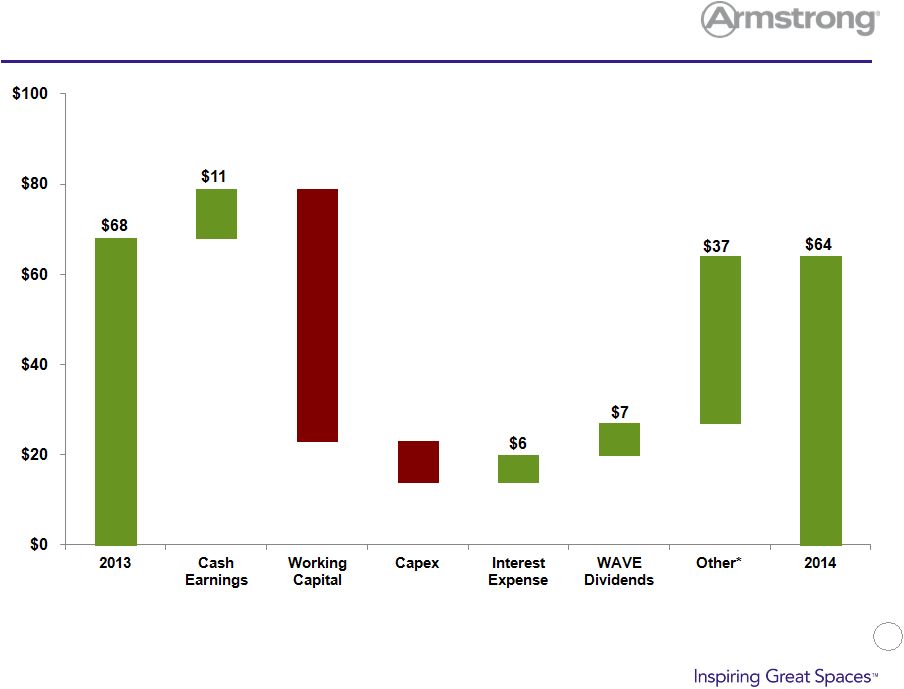

| Free cash flow |

64 | 68 | (6 | %) | ||||||||

Excluding the unfavorable impact from foreign exchange of $19 million, consolidated net sales increased slightly compared to the prior year period as the favorable impact from price and mix offset volume declines.

Operating income declined by 10% and adjusted EBITDA improved by 3% when compared to the prior year. Despite higher SG&A, input costs and the negative margin impact of lower volumes, adjusted EBITDA increased driven by favorable price and mix, manufacturing productivity and higher earnings from WAVE. Increased depreciation and amortization expense and additional severance, asset impairments and other charges associated with cost reduction actions, primarily in the Wood Flooring

business and Pacific Rim, drove the decline in operating income when compared to the prior year period. The reduction in free cash flow was attributable to changes in working capital, which was unusually favorable in 2013 and increased capital expenditures, which were partially offset by the cash settlement of a Ruble hedge related to the funding of our Russia plant construction project, higher cash earnings, increased dividends from the WAVE joint venture and lower interest expense.

Market Outlook and 2015 Guidance (1)

The Company expects 2015 full year sales to be in the $2.53 to $2.63 billion range and adjusted EBITDA to be in the $350 to $390 million range. Adjusted EPS is expected to be $2.05 to $2.45 per diluted share.

“We anticipate improving market conditions in the U.S. will support modest sales growth despite some anticipated pressure from foreign exchange in our international operations,” said Dave Schulz, CFO. “While earnings are expected to be lower than 2014, the investments we are making will position our businesses to succeed as two independent industry-leading public companies and benefit 2016 and beyond.”

| (1) | Sales guidance includes the impact of foreign exchange. Guidance metrics, other than sales, are presented using 2015 budgeted foreign exchange rates. Adjusted EPS guidance for 2015 is calculated based on an adjusted effective tax rate of 39%. |

Earnings Webcast

Management will host a live Internet broadcast beginning at 11:00 a.m. Eastern time today, to discuss fourth quarter and full year 2014 results. This event will be broadcast live on the Company’s Web site. To access the call and accompanying slide presentation, go to www.armstrong.com and click “For Investors.” The replay of this event will also be available on the Company’s Web site for up to one year after the date of the call.

Uncertainties Affecting Forward-Looking Statements

Disclosures in this release, including without limitation, those relating to future financial results guidance and our plan to separate our Flooring business from our Ceilings (Building Products) business into two independent, publicly traded companies, and in our other public documents and comments contain forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. Those statements provide our future expectations or forecasts and can be identified by our use of words such as “anticipate,” “estimate,” “expect,” “project,” “intend,” “plan,” “believe,” “outlook,” “target,” “predict,” “may,” “will,” “would,” “could,” “should,” “seek,” and other words or phrases of similar meaning in connection with any discussion of future operating or financial performance. Forward-looking statements, by their nature, address matters that are uncertain and involve risks because they relate to

events and depend on circumstances that may or may not occur in the future. As a result, our actual results may differ materially from our expected results and from those expressed in our forward-looking statements. A more detailed discussion of the risks and uncertainties that could cause our actual results to differ materially from those projected, anticipated or implied is included in the “Risk Factors” and “Management’s Discussion and Analysis” sections of our reports on Forms 10-K and 10-Q filed with the U.S. Securities and Exchange Commission (“SEC”). Forward-looking statements speak only as of the date they are made. We undertake no obligation to update any forward-looking statements beyond what is required under applicable securities law.

About Armstrong and Additional Information

More details on the Company’s performance can be found in its annual report on Form 10-K for the year ended December 31, 2014 that the Company expects to file with the SEC today.

Armstrong World Industries, Inc. is a global leader in the design and manufacture of floors and ceilings. In 2014, Armstrong’s consolidated net sales from continuing operations totaled approximately $2.5 billion. As of December 31, 2014, Armstrong operated 31 plants in eight countries and had approximately 7,400 employees worldwide.

Additional forward looking non-GAAP metrics are available on the Company’s web site at http://www.armstrong.com/ under the Investor Relations tab. The website is not part of this release and references to our website address in this release are intended to be inactive textual references only.

As Reported Financial Highlights

FINANCIAL HIGHLIGHTS

Armstrong World Industries, Inc. and Subsidiaries

(amounts in millions, except for per-share amounts, quarterly data is unaudited)

| Three Months Ended December 31, | Year Ended December 31, | |||||||||||||||

| 2014 | 2013 | 2014 | 2013 | |||||||||||||

| Net Sales |

$ | 587.3 | $ | 614.8 | $ | 2,515.3 | $ | 2,527.4 | ||||||||

| Costs of goods sold |

461.1 | 482.1 | 1,932.0 | 1,934.4 | ||||||||||||

| Selling general and administrative expenses |

94.2 | 102.9 | 398.5 | 386.9 | ||||||||||||

| Intangible asset impairment |

10.0 | — | 10.8 | — | ||||||||||||

| Restructuring charges, net |

— | — | — | (0.1 | ) | |||||||||||

| Equity (earnings) from joint venture |

(13.9 | ) | (13.2 | ) | (65.1 | ) | (59.4 | ) | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Operating income |

35.9 | 43.0 | 239.1 | 265.6 | ||||||||||||

| Interest expense |

11.7 | 12.4 | 46.0 | 68.7 | ||||||||||||

| Other non-operating expense |

1.3 | 1.0 | 10.5 | 2.0 | ||||||||||||

| Other non-operating (income) |

(0.7 | ) | (1.2 | ) | (2.6 | ) | (3.8 | ) | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Earnings from continuing operations before income taxes |

23.6 | 30.8 | 185.2 | 198.7 | ||||||||||||

| Income tax expense |

13.0 | 7.4 | 83.2 | 71.4 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Earnings from continuing operations |

$ | 10.6 | $ | 23.4 | $ | 102.0 | $ | 127.3 | ||||||||

| Net (loss) from discontinued operations, net of tax (benefit) of $-, $-, $- and $- |

(2.0 | ) | (12.6 | ) | (23.7 | ) | (26.8 | ) | ||||||||

| Loss on sale of discontinued business, net of tax (benefit) of ($1.3), ($0.2), ($2.5) and ($3.6) |

(12.2 | ) | — | (14.5 | ) | (6.4 | ) | |||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Net (loss) from discontinued operations |

(14.2 | ) | (12.6 | ) | (38.2 | ) | (33.2 | ) | ||||||||

| Net (loss) earnings |

($ | 3.6 | ) | $ | 10.8 | $ | 63.8 | $ | 94.1 | |||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Other comprehensive income (loss), net of tax: |

||||||||||||||||

| Foreign currency translation adjustments |

(19.6 | ) | (0.1 | ) | (29.6 | ) | (8.8 | ) | ||||||||

| Derivative (loss) gain |

(2.0 | ) | 4.7 | (3.3 | ) | 18.5 | ||||||||||

| Pension and postretirement adjustments |

(112.3 | ) | 71.3 | (91.0 | ) | 90.1 | ||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total other comprehensive (loss) income |

(133.9 | ) | 75.9 | (123.9 | ) | 99.8 | ||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total comprehensive (loss) income |

($ | 137.5 | ) | $ | 86.7 | ($ | 60.1 | ) | $ | 193.9 | ||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Earnings per share of common stock, continuing operations |

||||||||||||||||

| Basic |

$ | 0.19 | $ | 0.43 | $ | 1.85 | $ | 2.19 | ||||||||

| Diluted |

$ | 0.19 | $ | 0.42 | $ | 1.83 | $ | 2.17 | ||||||||

| Loss per share of common stock, discontinued operations |

||||||||||||||||

| Basic |

($ | 0.26 | ) | ($ | 0.23 | ) | ($ | 0.70 | ) | ($ | 0.57 | ) | ||||

| Diluted |

($ | 0.26 | ) | ($ | 0.23 | ) | ($ | 0.69 | ) | ($ | 0.57 | ) | ||||

| Net (loss) earnings per share of common stock: |

||||||||||||||||

| Basic |

($ | 0.06 | ) | $ | 0.20 | $ | 1.15 | $ | 1.62 | |||||||

| Diluted |

($ | 0.06 | ) | $ | 0.20 | $ | 1.14 | $ | 1.60 | |||||||

| Average number of common shares outstanding |

||||||||||||||||

| Basic |

55.2 | 54.3 | 55.0 | 57.8 | ||||||||||||

| Diluted |

55.5 | 55.0 | 55.4 | 58.4 | ||||||||||||

SEGMENT RESULTS

Armstrong World Industries, Inc. and Subsidiaries

(amounts in millions)

(Unaudited)

| Three Months Ended December 31, | Year Ended December 31, | |||||||||||||||

| 2014 | 2013 | 2014 | 2013 | |||||||||||||

| Net Sales |

||||||||||||||||

| Building Products |

$ | 310.9 | $ | 320.0 | $ | 1,294.3 | $ | 1,264.6 | ||||||||

| Resilient Flooring |

162.8 | 161.7 | 712.9 | 728.8 | ||||||||||||

| Wood Flooring |

113.6 | 133.1 | 508.1 | 534.0 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total net sales |

$ | 587.3 | $ | 614.8 | $ | 2,515.3 | $ | 2,527.4 | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Operating Income (loss) |

||||||||||||||||

| Building Products |

$ | 55.4 | $ | 52.4 | $ | 264.7 | $ | 263.1 | ||||||||

| Resilient Flooring |

15.6 | 9.4 | 61.6 | 69.8 | ||||||||||||

| Wood Flooring |

(19.4 | ) | 0.4 | (14.9 | ) | 6.0 | ||||||||||

| Unallocated Corporate (expense) |

(15.7 | ) | (19.2 | ) | (72.3 | ) | (73.3 | ) | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total Operating Income |

$ | 35.9 | $ | 43.0 | $ | 239.1 | $ | 265.6 | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

Selected Balance Sheet Information

(amounts in millions)

| December 31, 2014 | December 31, 2013 | |||||||

| Assets |

||||||||

| Current assets |

$ | 811.5 | $ | 884.0 | ||||

| Property, plant and equipment, net |

1,062.4 | 1,014.8 | ||||||

| Other noncurrent assets |

732.3 | 1,017.8 | ||||||

|

|

|

|

|

|||||

| Total assets |

$ | 2,606.2 | $ | 2,916.6 | ||||

|

|

|

|

|

|||||

| Liabilities and shareholders’ equity |

||||||||

| Current liabilities |

$ | 388.1 | $ | 410.9 | ||||

| Noncurrent liabilities |

1,569.0 | 1,832.5 | ||||||

| Equity |

649.1 | 673.2 | ||||||

|

|

|

|

|

|||||

| Total liabilities and shareholders’ equity |

$ | 2,606.2 | $ | 2,916.6 | ||||

|

|

|

|

|

|||||

Selected Cash Flow Information

(amounts in millions)

| Year Ended December 31, | ||||||||

| 2014 | 2013 | |||||||

| Net income |

$ | 63.8 | $ | 94.1 | ||||

| Other adjustments to reconcile net income to net cash provided by operating activities |

189.9 | 124.7 | ||||||

| Changes in operating assets and liabilities, net |

(44.9 | ) | (5.1 | ) | ||||

|

|

|

|

|

|||||

| Net cash provided by operating activities |

208.8 | 213.7 | ||||||

| Net cash (used for) investing activities |

(149.3 | ) | (145.8 | ) | ||||

| Net cash provided by (used for) financing activities |

3.3 | (263.7 | ) | |||||

| Effect of exchange rate changes on cash and cash equivalents |

(12.7 | ) | (5.4 | ) | ||||

|

|

|

|

|

|||||

| Net increase (decrease) in cash and cash equivalents |

50.1 | (201.2 | ) | |||||

| Cash and cash equivalents, beginning of period |

135.2 | 336.4 | ||||||

|

|

|

|

|

|||||

| Cash and cash equivalents, end of period |

$ | 185.3 | $ | 135.2 | ||||

| Cash and cash equivalents at end of year of discontinued operations |

— | $ | 22.9 | |||||

| Cash and cash equivalents at end of year of continuing operations |

$ | 185.3 | $ | 112.3 | ||||

|

|

|

|

|

|||||

Supplemental Reconciliations of GAAP to non-GAAP Results (unaudited)

(Amounts in millions, except per share data)

To supplement its consolidated financial statements presented in accordance with accounting principles generally accepted in the United States (GAAP), the Company provides additional measures of performance adjusted to exclude the impact of foreign exchange, restructuring charges and related costs, impairments, the non-cash impact of the U.S. pension plan and certain other gains and losses. Adjusted figures are reported in comparable dollars using the budgeted exchange rate for 2014. The Company uses these adjusted performance measures in managing the business, including communications with its Board of Directors and employees, and believes that they provide users of this financial information with meaningful comparisons of operating performance between current results and results in prior periods. The Company believes that these non-GAAP financial measures are appropriate to enhance understanding of its past performance, as well as prospects for its future performance. A reconciliation of these adjustments to the most directly comparable GAAP measures is included in this release and on the Company’s website. These non-GAAP measures should not be considered in isolation or as a substitute for the most comparable GAAP measures. Non-GAAP financial measures utilized by the Company may not be comparable to non-GAAP financial measures used by other companies.

CONSOLIDATED RESULTS FROM

CONTINUTING OPERATIONS

| Three Months Ended December 31, |

Year Ended December 31, | |||||||||||||||

| 2014 | 2013 | 2014 | 2013 | |||||||||||||

| Adjusted EBITDA |

$ | 78 | $ | 72 | $ | 384 | $ | 372 | ||||||||

| D&A/Fx* |

(31 | ) | (28 | ) | (118 | ) | (103 | ) | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Operating Income, Adjusted |

$ | 47 | $ | 44 | $ | 266 | $ | 269 | ||||||||

| Non-cash impact of U.S. Pension |

— | (1 | ) | 1 | (2 | ) | ||||||||||

| Cost reduction initiatives expenses |

2 | 2 | 14 | 7 | ||||||||||||

| Impairment |

10 | — | 13 | — | ||||||||||||

| Foreign exchange impact |

(1 | ) | — | (1 | ) | (2 | ) | |||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Operating Income, Reported |

$ | 36 | $ | 43 | $ | 239 | $ | 266 | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| * | Excludes accelerated depreciation associated with cost reduction initiatives reflected below. Actual D&A as reported is; $31.3 million for the three months ended December 31, 2014, $29.6 million for the three months ended December 31, 2013, $129.4 million for the year ended December 31, 2014, and $109.0 million for the year ended December 31, 2013. |

BUILDING PRODUCTS

| Three Months Ended December 31, |

Year Ended December 31, | |||||||||||||||

| 2014 | 2013 | 2014 | 2013 | |||||||||||||

| Adjusted EBITDA |

$ | 73 | $ | 68 | $ | 330 | $ | 320 | ||||||||

| D&A/Fx |

(18 | ) | (15 | ) | (67 | ) | (57 | ) | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Operating Income, Adjusted |

$ | 55 | $ | 53 | $ | 263 | $ | 263 | ||||||||

| Cost reduction initiatives expenses |

1 | — | 1 | 1 | ||||||||||||

| Foreign exchange impact |

(1 | ) | 1 | (3 | ) | (1 | ) | |||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Operating Income, Reported |

$ | 55 | $ | 52 | $ | 265 | $ | 263 | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

RESILIENT FLOORING

| Three Months Ended December 31, |

Year Ended December 31, | |||||||||||||||

| 2014 | 2013 | 2014 | 2013 | |||||||||||||

| Adjusted EBITDA |

$ | 21 | $ | 18 | $ | 93 | $ | 99 | ||||||||

| D&A/Fx |

(6 | ) | (7 | ) | (27 | ) | (26 | ) | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Operating Income, Adjusted |

$ | 15 | $ | 11 | $ | 66 | $ | 73 | ||||||||

| Cost reduction initiatives expenses |

(1 | ) | 2 | 4 | 4 | |||||||||||

| Foreign exchange impact |

— | (1 | ) | 1 | (1 | ) | ||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Operating Income, Reported |

$ | 16 | $ | 10 | $ | 61 | $ | 70 | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

WOOD FLOORING

| Three Months Ended December 31, |

Year Ended December 31, | |||||||||||||||

| 2014 | 2013 | 2014 | 2013 | |||||||||||||

| Adjusted EBITDA (1) |

($ | 4 | ) | $ | 4 | $ | 21 | $ | 17 | |||||||

| D&A/Fx |

(3 | ) | (4 | ) | (13 | ) | (11 | ) | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Operating (Loss) Income, Adjusted (1) |

($ | 7 | ) | $ | 0 | $ | 8 | $ | 6 | |||||||

| Cost reduction initiatives expenses |

2 | — | 9 | — | ||||||||||||

| Impairment |

10 | — | 13 | — | ||||||||||||

| Foreign exchange impact |

— | — | 1 | — | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Operating (Loss) Income, Reported(1) |

($ | 19 | ) | $ | 0 | ($ | 15 | ) | $ | 6 | ||||||

|

|

|

|

|

|

|

|

|

|||||||||

| (1) | Includes a $1 million gain that occurred in the second quarter of 2014 related to a refund of previously paid duties on imports of engineered wood flooring |

UNALLOCATED CORPORATE

| Three Months Ended December 31, |

Year Ended December 31, | |||||||||||||||

| 2014 | 2013 | 2014 | 2013 | |||||||||||||

| Adjusted EBITDA |

($ | 12 | ) | ($ | 18 | ) | ($ | 60 | ) | ($ | 64 | ) | ||||

| D&A/Fx |

(4 | ) | (2 | ) | (11 | ) | (9 | ) | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Operating (Loss), Adjusted |

($ | 16 | ) | ($ | 20 | ) | ($ | 71 | ) | ($ | 73 | ) | ||||

| Non-cash impact of U.S. Pension |

— | (1 | ) | 1 | (2 | ) | ||||||||||

| Cost Reduction initiatives expenses |

— | — | — | 2 | ||||||||||||

| Foreign exchange impact |

— | — | — | — | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Operating (Loss), Reported |

($ | 16 | ) | ($ | 19 | ) | ($ | 72 | ) | ($ | 73 | ) | ||||

|

|

|

|

|

|

|

|

|

|||||||||

CASH FLOW(1)

| Three Months Ended December 31, | Year Ended December 31, | |||||||||||||||

| 2014 | 2013 | 2014 | 2013 | |||||||||||||

| Net cash from operations |

$ | 98 | $ | 52 | $ | 209 | $ | 214 | ||||||||

| Less: net cash (used for) investing |

(52 | ) | (59 | ) | (149 | ) | (146 | ) | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Add back (subtract) adjustments to reconcile to free cash flow |

||||||||||||||||

| Net cash effect from deconsolidation of European Flooring business |

4 | — | 4 | — | ||||||||||||

| Other |

(1 | ) | — | — | — | |||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Free Cash Flow |

$ | 49 | ($ | 7 | ) | $ | 64 | $ | 68 | |||||||

| (1) | Cash flow includes cash flows attributable to European Flooring business |

CONSOLIDATED RESULTS FROM CONTINUING OPERATIONS

| Three Months Ended December 31, | Year Ended December 31, | |||||||||||||||||||||||||||||||

| 2014 | 2013 | 2014 | 2013 | |||||||||||||||||||||||||||||

| Total | Per Share |

Total | Per Share |

Total | Per Share |

Total | Per Share |

|||||||||||||||||||||||||

| Adjusted EBITDA |

$ | 78 | $ | 72 | $ | 384 | $ | 372 | ||||||||||||||||||||||||

| D&A as reported |

(31 | ) | (30 | ) | (129 | ) | (109 | ) | ||||||||||||||||||||||||

| Fx/Accelerated Deprecation |

— | 2 | 11 | 6 | ||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||

| Operating Income, Adjusted |

$ | 47 | $ | 44 | $ | 266 | $ | 269 | ||||||||||||||||||||||||

| Other non-operating (expense) |

(13 | ) | (12 | ) | (55 | ) | (67 | ) | ||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||

| Earnings Before Taxes, Adjusted |

34 | 32 | 211 | 202 | ||||||||||||||||||||||||||||

| Adjusted tax (expense) @ 39% for 2014 and 2013 |

(13 | ) | (13 | ) | (82 | ) | (79 | ) | ||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||

| Net Earnings, Adjusted |

$ | 21 | $ | 0.38 | $ | 19 | $ | 0.35 | $ | 129 | $ | 2.32 | $ | 123 | $ | 2.11 | ||||||||||||||||

| Pre-tax adjustment items |

(11 | ) | (2 | ) | (26 | ) | (5 | ) | ||||||||||||||||||||||||

| Non-cash impact of U.S. Pension |

— | 1 | (1 | ) | 2 | |||||||||||||||||||||||||||

| Reversal of adjusted tax expense @ 39% for 2014 and 2013 |

13 | 13 | 82 | 79 | ||||||||||||||||||||||||||||

| Ordinary tax |

(7 | ) | (7 | ) | (59 | ) | (59 | ) | ||||||||||||||||||||||||

| Unbenefitted foreign losses |

(3 | ) | (6 | ) | (24 | ) | (23 | ) | ||||||||||||||||||||||||

| Tax adjustment items |

(2 | ) | 5 | 1 | 10 | |||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||

| Net Earnings, Reported |

$ | 11 | $ | 0.19 | $ | 23 | $ | 0.42 | $ | 102 | $ | 1.83 | $ | 127 | $ | 2.17 | ||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||

Source: Armstrong World Industries