UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

———————

FORM 10-K

———————

þANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2014

Commission file number: 000-51354

AEMETIS, INC.

(Exact name of registrant as specified in its charter)

|

Nevada

|

26-1407544

|

|

|

(State or other jurisdiction of incorporation or organization)

|

(I.R.S. Employer Identification Number)

|

20400 Stevens Creek Blvd., Suite 700

Cupertino, CA 95014

(Address of principal executive offices)

Registrant’s telephone number (including area code): (408) 213-0940

Securities registered under Section 12(g) of the Exchange Act:

Common Stock, Par Value $0.001

(Title of class)

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes oNo þ

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes oNo þ

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or Section 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes þ No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes þ No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. Yes o No þ

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

|

Large accelerated filer

|

o

|

Accelerated filer þ

|

|

Non-accelerated filer

|

o (Do not check if a smaller reporting company)

|

Smaller reporting company o

|

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No þ

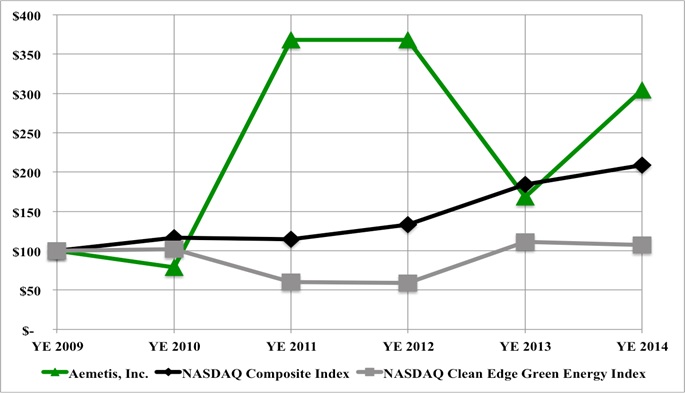

The aggregate market value of the voting and non-voting common equity held by non-affiliates of the registrant was approximately $100,884,800 as of June 30, 2014 based on the average bid and asked price on the NASDAQ Markets reported for such date. This calculation does not reflect a determination that certain persons are affiliates of the registrant for any other purpose.

The number of shares outstanding of the registrant’s Common Stock on March 5, 2015 was 20,771,914 shares.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the Proxy Statement for the Registrant’s 2015 Annual Meeting of Stockholders are incorporated by reference in Part III of this Form 10-K.

TABLE OF CONTENTS

|

Page

|

|

|

PART I

|

|

|

Special Note Regarding Forward-Looking Statements

|

3

|

|

Item 1. Business

|

3 |

|

Item 1A. Risk Factors

|

11

|

|

Item 2. Properties

|

21

|

|

Item 3. Legal Proceedings

|

22

|

|

Item 4. Mine Safety Disclosures

|

23

|

PART II

|

Item 5. Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities

|

24

|

|

Item 6. Selected Financial Data

|

27

|

|

Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations

|

27

|

|

Item 8. Financial Statements and Supplementary Data

|

41

|

|

Item 9. Changes in and Disagreements with Accountants on Accounting and Financial Disclosure

|

41

|

|

Item 9A. Controls and Procedures

|

41

|

|

Item 9B. Other Information

|

44

|

PART III

|

Item 10. Directors, Executive Officers and Corporate Governance

|

44

|

|

Item 11. Executive Compensation

|

44

|

|

Item 12. Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters

|

44

|

|

Item 13. Certain Relationships and Related Transactions, and Director Independence

|

44

|

|

Item 14. Principal Accounting Fees and Services

|

44

|

PART IV

|

Item 15. Exhibits and Financial Statement Schedules

|

44

|

|

Index to Financial Statements

|

50

|

|

Signatures

|

86

|

2

SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS

On one or more occasions, we may make forward-looking statements in this Annual Report on Form 10-K, including statements regarding our assumptions, projections, expectations, targets, intentions or beliefs about future events or other statements that are not historical facts. Forward-looking statements in this Annual Report on Form 10-K, include without limitation, statements regarding trends in demand for renewable fuels; trends in market conditions with respect to prices for inputs for our products verses prices for our products; our ability to leverage approved feedstock pathways; our ability to leverage our location and infrastructure; our ability to incorporate lower-cost, non-food advanced biofuels feedstock at the Keyes plant; our ability to adopt value-add byproduct processing systems; our ability to expand into alternative markets for biodiesel and its byproducts, including continuing to expand our sales into international markets; the impact of changes in regulatory policies on our performance, including the Indian government’s recent changes to tax policies, diesel prices and related subsidies; our ability to continue to develop new, and to maintain and protect new and existing, intellectual property rights; our ability to adopt, develop and commercialize new technologies; our ability to refinance our senior debt on more commercial terms or at all; our ability to continue to fund operations; our ability to sell additional notes under our EB-5 note program and our expectations regarding the release of funds from escrow under our EB-5 note program; our ability to improve margins; our ability to raise the expected costs to complete our fractionation unit; and our ability to raise additional capital. Words or phrases such as “anticipates,” “may,” “will,” “should,” “believes,” “estimates,” “expects,” “intends,” “plans,” “predicts,” “projects,” “targets,” “will likely result,” “will continue” or similar expressions are intended to identify forward-looking statements. These forward-looking statements are based on current assumptions and predictions and are subject to numerous risks and uncertainties. Actual results or events could differ materially from those set forth or implied by such forward-looking statements and related assumptions due to certain factors, including, without limitation, the risks set forth under the caption “Risk Factors” below, which are incorporated herein by reference as well as those business risks and factors described elsewhere in this report and in our other filings with the Securities and Exchange Commission (the “SEC”).

We undertake no obligation to publicly update or revise any forward-looking statements, whether as a result of new information, future events or otherwise.

We obtained the market data used in this report from internal company reports and industry publications. Industry publications generally state that the information contained in those publications has been obtained from sources believed to be reliable, but their accuracy and completeness are not guaranteed and their reliability cannot be assured. Although we believe market data used in this 10-K is reliable, it has not been independently verified.

Unless the context requires otherwise, references to “we,” “us,” “our,” and “the Company” refer specifically to Aemetis, Inc. and its subsidiaries.

General

Aemetis is an international renewable fuels and biochemicals company focused on the production of advanced fuels and chemicals through the acquisition, development and commercialization of innovative technologies that replace traditional petroleum-based products by conversion of first-generation ethanol and biodiesel plants into advanced biorefineries. Aemetis operates in two reportable geographic segments: “North America” and “India.” For revenue and other information regarding Aemetis’ operating segments, see Note 13- Segment Information, of the Notes to Consolidated Financial Statements in Part II, Item 8 of this Form 10-K.

Aemetis was incorporated in Nevada in 2006.

We own and operate a 55 million gallon per year capacity ethanol production facility located in Keyes, California. The facility produces its own combined heat and power (CHP) through the use of a natural gas-powered steam turbine, and is designed to reuse 100% of its process water with zero water discharge. In addition to ethanol, the Keyes plant produces Wet Distillers Grains (WDG), corn oil, and Condensed Distillers Soluables (CDS), all of which are sold to local dairies and feedlots for animal consumption. The primary feedstock for the production of low carbon fuel ethanol at the Keyes facility is yellow dent corn specified as number two. The corn is procured from various Midwestern grain facilities and shipped, via Union Pacific Rail Road, to an unloading facility adjacent to the plant.

The Company owns and operates a biodiesel production facility in Kakinada, India with a nameplate capacity of 50 million gallons per year which is equal to 150,000 metric tons per year. We believe this facility is one of the largest biodiesel production facilities in India on a nameplate capacity basis. Our objective is to continue to capitalize on the substantial growth potential of the industry in India and established markets in the EU and US.

3

Strategy

Key elements of our strategy include:

North America

Leverage Approved Feedstock Pathways. When economically advantageous, we will also utilize grain sorghum (“milo”) as a lower carbon, advanced feedstock for the production of EPA-approved advanced biofuels. Aemetis has been approved to use the grain sorghum Pathway (in combination with landfill gas and CHP) for the production of Advanced Biofuels and associated higher value D5 RINs. While Aemetis has processed a significant amount of grain sorghum through the Keyes facility during 2013, economics in 2014 favored the use of corn over milo. This was largely due to the significant export demand for milo by China. These conditions continued into 2015.

Leverage the Keyes plant infrastructure and location. As milo becomes price-competitive with corn, Aemetis Keyes has the brokerage and infrastructure relationships in place to incorporate this feedstock into production without delay. Through its strategic location near the Port of Stockton and adjacent access to the Union Pacific railroad, the Aemetis Keyes facility can, and has, procured grain sorghum from both international and domestic sources. Additionally, the Keyes facility has ready access to biogas through its existing infrastructure for the production of Advanced Biofuels under the approved EPA Pathway. We have also entered into a multi-year contract with Chromatin, Inc., an advanced grain sorghum seed and technology provider, to establish a multi-thousand acre local grain sorghum growing program with farmers in California’s Central Valley. In 2014, Aemetis was awarded a $3 million dollar matching grant from the California Energy Commission for the acquisition of milo for the production of lower carbon fuel ethanol, and to fully develop the in-state grain sorghum growing program.

Leverage technology for the development and production of additional Advanced Biofuels and renewable chemicals. In July 2011, we acquired Zymetis, Inc., a biochemical research and development firm, with several patents pending and in-process R&D utilizing the Z-microbe™ to produce renewable chemicals and advanced fuels from renewable feedstocks. Aemetis now has nine granted patents for the production of advanced biofuels. Our objective is to continue to commercialize this technology and expand the production of advanced biofuel technologies and other bio-chemicals in the United States.

Diversify and expand revenue and cash flow by continuing to develop and adopt value-added byproduct processing systems. During April 2012, we installed a corn oil extraction unit at the Keyes plant and began extracting corn oil for sale into the livestock feed market beginning in May 2012. During 2014, we installed a second corn oil extraction system to further improve corn oil yields from this process. During the fourth quarter of 2014, we entered into an agreement to construct a liquid CO2 facility at the Keyes plant. We continue to evaluate and, as allowed by available financing and incremental profitability, adopt additional value-added processes that increase the value of the ethanol, distillers grain, corn oil and CO2 produced at the Keyes plant, including, as described further below, adding liquefied CO2 processing capability.

Joint venture or license Aemetis technologies to other ethanol and biodiesel plants. After developing and commercially demonstrating technologies at the Keyes and/or India plants, we plan to explore and evaluate opportunities for joint ventures or to license our technologies to the other approximately 200 ethanol plants and hundreds of biodiesel plants in the US, as well as plants in Brazil, Argentina, India and elsewhere.

Evaluate and pursue technology acquisition opportunities. We intend to evaluate and pursue opportunities to acquire technologies and processes that result in accretive value opportunities as financial resources and business prospects make the acquisition of these technologies advisable. In addition, we may also seek to acquire companies or form licensing agreements or joint ventures with companies that offer prospects for the adoption of accretive technologies.

Acquire additional biofuels production facilities. There are approximately 200 ethanol plants in the US that could be upgraded to expand revenues and improve cash flow using technology commercially deployed or licensed by Aemetis. On an opportunistic basis, we will evaluate the benefit of acquiring ownership of a portion of or all of other or biodiesel production facilities, or entering into joint-venture or licensing agreements with other ethanol, renewable diesel, or renewable jet fuel facilities.

4

India

Capitalize on recent policy changes by the Government of India, particularly those to reduce the subsidies on diesel and to reduce restrictions on sales of fuel into the transportation markets. We plan to expand our marketing channels for the traditional bulk and transportation biodiesel markets, which are becoming more economically attractive as a result of the reduction of government subsidies on petroleum diesel (biodiesel is not subsidized in India) and policies to further open sales into the bulk fuel markets.

Expand alternative market demand for biodiesel and its byproducts. We plan to create additional demand for our biodiesel and its byproducts by developing additional alternative markets. In 2011, we began selling biodiesel to textile manufacturers for use as an anti-static chemical. In the first quarter of 2012, we completed glycerin refining and oil pre-treatment units and began selling refined glycerin to manufacturers of paints and adhesives. In 2012, our India subsidiary received an Indian Pharmacopeia license, which enables the sale of refined glycerin to the pharmaceutical industry in India.

Continue to develop international markets. We expect to increase sales by selling our biodiesel into international markets during the summer months, when biodiesel use in Europe increases with the onset of warmer weather. In 2014 and 2013, we had sales of $4.5 million and $11.6 million into the European market, respectively. During 2014, we received the certifications necessary to meet the ISCC standard, allowing for further access to European markets for our biodiesel products.

Diversify and expand our products. In 2012, we completed a glycerin refinery, enabling the upgrade of crude glycerin to refined glycerin using glycerin from our own biodiesel production (the byproduct of biodiesel production is crude glycerin) or crude glycerin purchased from domestic or foreign sources. In 2014, we completed the construction of a biodiesel distillation column, which allows us to produce a high-quality biodiesel product meeting European Union standards.

Diversify our feedstocks from India and international sources. We designed our Kakinada plant with the capability to produce biodiesel from multiple feedstocks. In 2009, we began to produce biodiesel from NRPO. In 2012, we completed an oil pre-treatment unit, which enables us to convert crude palm oil into NRPO, which can either be sold or used to produce biodiesel. During 2014, we further diversified our feedstock with the introduction of animal oils and fats, which we used for the production of biodiesel to be sold into the European markets. The plant is capable of producing biodiesel from used cooking oil (UCO), which can be supplied from China, the Middle East and other foreign markets, as well as domestic India suppliers.

Develop and commercially deploy technologies to produce high-margin products. The technology applicable to the Keyes ethanol plant for the upgrade of corn oil into valuable, high-margin products also applies to the Kakinada plant in India. By using the existing equipment, process controls, utilities and personnel at the India plant, we plan to produce high-value products more quickly and at a lower capital and operating cost than greenfield projects.

2014 Highlights

North America

During 2014, we produced four products at the Keyes plant: denatured ethanol, WDG, corn oil, and CDS. We sold 100% of the ethanol and WDG produced to J.D. Heiskell pursuant to a Purchase Agreement established with J.D. Heiskell. J.D. Heiskell in turn sells 100% of our ethanol to Kinergy and 100% of our WDG to A.L. Gilbert, a local feed and grain business. Corn oil is sold directly by Aemetis to local animal feedlots (primarily poultry) as well as feed mills for use in various animal feed products. Small amounts of CDS were sold to various local third parties as an animal feed supplement. Ethanol pricing for sales to J.D. Heiskell is determined pursuant to a marketing agreement between the Company and Kinergy Marketing LLC, and is generally based on daily and monthly pricing for ethanol delivered to the San Francisco Bay Area as published by the Oil Price Information Service (OPIS), as well as quarterly contracts negotiated by Kinergy with numerous fuel blenders. The price for WDG is determined monthly pursuant to a marketing agreement between the Company and A.L. Gilbert Co., and is generally determined in reference to the local price of dry distillers grains (DDG), corn, and other protein feedstuffs.

5

The following table sets forth information about our production and sales of ethanol and WDG for 2014 compared with 2013:

|

2014

|

2013

|

% Change

|

||||||||||

|

Ethanol

|

||||||||||||

|

Gallons Sold (in 000s)

|

60,197 | 42,390 | 42 | % | ||||||||

|

Average Sales Price/Gallon

|

$ | 2.54 | $ | 2.62 | (3 | )% | ||||||

|

WDG

|

||||||||||||

|

Tons Sold (in 000s)

|

408 | 301 | 36 | % | ||||||||

|

Average Sales Price/Ton

|

$ | 91.81 | $ | 100.47 | (9 | )% | ||||||

On January 15, 2013 our ethanol production facility was idled due to unfavorable market conditions and to conduct maintenance on the plant for the first time since commencing ethanol production in April 2011. In April 2013, we restarted our ethanol production facility and ran the plant on a continual basis through the rest of the year.

India

The market for biodiesel showed signs of improving during early 2014 upon completion of our biodiesel distillation facility and receipt of the certifications necessary to meet the ISCC standard which opened sales channels into the European Union. The Company’s production of biodiesel in 2014 decreased compared to 2013 due to the rising price of NRPO resulting in uncompetitive pricing for sales into European markets. In 2014, we expanded our feedstock to include oils and fats as well as NRPO, a byproduct of palm oil refining and a non-edible feedstock, which we sourced principally from suppliers in India.

In 2014, we produced four products at the India plant: biodiesel, crude glycerin, refined glycerin, and NRPO / Stearin. Crude glycerin held in inventory or produced as a by-product of the biodiesel production was further processed into refined glycerin and crude palm oil was further processed into refined palm oil for sale to customers. During portions of 2013 and 2014, we were able to utilize our refining unit to refine crude palm oil into NRPO and subsequently sell the NRPO at a more attractive margin than converting NRPO into biodiesel or earn a fixed fee for processing the NRPO. Additionally, crude glycerin was purchased on the open market and further processed to fill the demand for refined glycerin.

The following table sets forth information about our production and sales of biodiesel, crude and refined glycerin and NRPO in 2014 and 2013:

|

2014

|

2013

|

% Change

|

||||||||||

|

Biodiesel

|

||||||||||||

|

Tons sold (1)

|

9,036 | 19,354 | (53 | )% | ||||||||

|

Average Sales Price/Ton

|

$ | 985 | $ | 929 | 6 | % | ||||||

|

Refined Glycerin

|

||||||||||||

|

Tons sold

|

2,236 | 4,913 | (54 | )% | ||||||||

|

Average Sales Price/Ton

|

$ | 933 | $ | 940 | (1 | )% | ||||||

|

NRPO / Stearin

|

||||||||||||

|

Tons Sold

|

- | 8,227 | (100 | )% | ||||||||

|

Average Sales Price/Ton

|

- | $ | 980 | (100 | )% | |||||||

|

CPO

|

||||||||||||

|

Tons Sold

|

- | 2,000 | (100 | )% | ||||||||

|

Average Sales Price/Ton

|

- | $ | 958 | (100 | )% | |||||||

|

(1)

|

1 metric ton is equal to 1,000 kilograms (approximately 2,204 pounds).

|

The plant was originally designed to include four production units: biodiesel, refined glycerin, oil refining and fractionation. To date, the biodiesel, refined glycerin and oil refining units have been completed. In order to complete the fractionation unit, the Company will need to purchase and install additional equipment at an additional cost of approximately $2 million.

During 2014 the Indian government completed their plan to eliminate subsidies for diesel and allowed the domestic price to float to the market price. Our biodiesel pricing is indexed to the price of petroleum diesel, and as such, the increase in the price of petroleum diesel is expected to favorably impact the profitability of our Indian operations. During 2013, the Company began construction of a biodiesel distillation column allowing for the biodiesel produced at the Kakinada plant to be more readily adopted by customers in the European Union due to its higher purity levels, and began certification requirements necessary to meet the European Union International Sustainability and Carbon Certification (“ISCC”) standard. The biodiesel distillation column and the ISCC certification were completed in January 2014, allowing for further access to European markets for our biodiesel products.

6

Competition

North America

In 2014, there were approximately 200 operating commercial corn ethanol production facilities in the U.S. with a combined production of approximately 14.033 BGY and operating capacity of 15.6 BGY, according to the Renewable Fuels Association (RFA). The production of ethanol is a commodity-based business, and producers compete on the basis of price. We sell ethanol into the Northern California market; however, since insufficient production capacity exists in California to supply the state’s total fuel demand (in excess of one billion gallons), we compete with ethanol transported into California from the Midwest. Similarly, our co-products, principally WDG and corn oil, are sold into California markets and compete with distillers grains and corn oil transported into the California markets as well as alternative feed products including corn.

India

With respect to biodiesel sold as fuel, we compete primarily with the producers of petroleum diesel, which are the three state-controlled oil companies: Indian Oil Corporation, Bharat Petroleum and Hindustan Petroleum, and two private oil companies: Reliance Petroleum and Essar Oil, all of whom have significantly larger market shares than we do and control a significant share of the distribution network. These competitors may also purchase our product for blending and further sales to their customers. We compete primarily on the basis of price. The price of biodiesel is indexed to the price of petroleum diesel, which, during 2014, was allowed to float to market pricing by the Indian government. Prior to 2014, the Indian government subsidized state-controlled oil companies creating a disparity between the cost of oil on the open market and the price we could obtain from sales of biodiesel. In 2014, the Indian government eliminated its subsidization of the State-controlled oil float. We believe the elimination of subsidies and the lifting of certain restrictions to the sale of bulk fuels will have a positive effect on our margins and will increase the business, operating results and financial condition of our India segment during 2015. With respect to international markets, principally the European markets, we compete with biodiesel from Europe, Argentina, Indonesia and Malaysia, some of which subsidize their biodiesel industry using government payment and taxation programs to promote the sales of their products into these markets.

With respect to biodiesel sold for manufacturing purposes, we compete with specialty chemical manufacturers selling products into the textile industries primarily on the basis of price; and with respect to crude and refined glycerin, we compete with other glycerin producers and refiners selling products into the personal care, paints and adhesive markets primarily on the basis of price and product quality.

Customers

North America

All of our ethanol and WDG are sold to J.D. Heiskell pursuant to a purchase agreement. J.D. Heiskell in turn sells all of our ethanol to Kinergy and all of our WDG to A.L. Gilbert. Kinergy markets and sells our ethanol to petroleum refiners and blenders in Northern California. A.L. Gilbert markets and sells our WDG to approximately 200 dairy and feeding operators in Northern California.

India

During 2014, three customers in paints and personal care products industries within India accounted for 80% of our refined glycerin sales and, three customers from India and one customer from Europe accounted for 80% of biodiesel sales. During 2013, three customers in paints and personal care products industries within India accounted for 79% of our refined glycerin sales, two customers in edible oils and products industry within India accounted for 97% of our refined palm oil sales, one customer from European continent accounted for 69% of biodiesel sales. Three customers and two customers exceeded 10% of total sales during the year ended 2014 and 2013, respectively.

Pricing

North America

We sell 100% of the ethanol and WDG we produce to J.D. Heiskell. Ethanol pricing is determined pursuant to a marketing agreement between the Company and Kinergy Marketing LLC, and is generally based on daily and monthly pricing for ethanol delivered to the San Francisco Bay area in California, as published by the Oil Price Information Service (OPIS), as well as the terms of quarterly contracts negotiated by Kinergy with local fuel blenders and available premiums for fuel with low Carbon Intensity (CI) as provided by California’s Low Carbon Fuel Standard (LCFS). The price for WDG is determined monthly pursuant to a marketing agreement between the Company and A.L. Gilbert Co., and is generally determined in reference to the price of dry distillers grains (DDG), corn, and other protein feedstuffs.

7

India

In India, the price of biodiesel is based on the price of petroleum diesel, which floats with changes in the price determined by the international markets. Biodiesel sold into Europe is based on the spot market price. We sell our biodiesel primarily to resellers, distributors and refiners on an as-needed basis. We have no long-term sales contracts. Our biodiesel pricing is indexed to the price of petroleum diesel, and the increase in the price of petroleum diesel is expected to favorably impact the profitability of our India operations.

Raw Materials and Suppliers

North America

We entered into a Corn Procurement and Working Capital Agreement with J.D. Heiskell in March 2011 which we amended in May 2013 (the “Heiskell Agreement”). Under the Heiskell Agreement, we agreed to procure yellow dent corn from J.D. Heiskell. We have the ability to obtain corn from other sources subject to certain conditions, however, in 2014, all of our corn requirements were purchased from Heiskell. Title to the corn and risk of loss pass to us when the corn is ground for production at our Keyes facility. We also purchased grain sorghum from J.D. Heiskell during 2014. The initial term of the Heiskell Agreement expired on December 31, 2013, but the agreement is automatically renewed for additional one-year terms. The current term is set to expire on December 31, 2015.

India

Surrounding our plant in Kakinada, India, a number of edible oil processing facilities produce NRPO as a byproduct. In 2013, all of our biodiesel was produced from NRPO, which we obtained from sources surrounding the plant. The receiving capabilities of the plant allow for import of feedstock using the local port at Kakinada. During 2014 and 2013 we imported crude palm oil for further processing into refined palm oil and imported crude glycerin for further processing into refined glycerin. In addition to feedstock, our plant requires quantities of methanol and chemical catalysts for use in the biodiesel production process. These chemicals are also readily available and sourced from a number of suppliers surrounding the plant. We are not dependent on sole source or limited source suppliers for any of our raw materials or chemicals.

Sales and Marketing

North America

As part of our obligations under the Corn Procurement Agreement, we entered into a purchase agreement with Heiskell, pursuant to which we granted Heiskell exclusive rights to purchase 100% of the ethanol and WDG we produce at prices based upon the price established by the marketing agreements with Kinergy and A.L. Gilbert. In turn, Heiskell agreed to resell all the ethanol to Kinergy (or any other purchaser we designate) and all of the WDG to A.L. Gilbert.

In March 2011, we entered into a WDG Purchase and Sale Agreement with A.L. Gilbert Company, pursuant to which A.L. Gilbert agreed to market on an exclusive basis all of the WDG we produce. The initial term of the Agreement expired on December 31, 2011 and is automatically renewed for additional one-year terms, currently to December 31, 2015.

In October 2010, we entered into an exclusive marketing agreement with Kinergy Marketing LLC to market and sell our ethanol. The initial term of the Agreement expired on August 31, 2013, but the agreement is automatically renewed for additional one-year terms. The current term is set to expire on August 31, 2015.

India

We sell our biodiesel and crude glycerin (i) to end-users utilizing our own sales force and independent sales agents and (ii) to brokers who resell the product to end-users. We pay a sales commission on sales arranged by independent sales agents.

8

Commodity Risk Management Practices

North America

The cost of corn and the price of ethanol are volatile and the correlation of these commodities form the basis for the profit margin at our Keyes Plant. We are, therefore, exposed to commodity price risk. Our risk management strategy is to operate in the physical market by purchasing corn and selling ethanol on a daily basis at the then prevailing market price. We monitor these prices daily to test for an overall positive variable contribution margin. We periodically explore methods of mitigating the volatility of our commodity prices and during the fourth quarter of 2014 entered into a contract that fixed our pricing on the transportation and corn basis components of price as a measure to limit the risk of a rapidly rising transportation cost component. In second half of 2013, we purchased grain sorghum as a substitute for corn with generally positive economic results. We intend to opportunistically purchase grain sorghum and use it to produce lower carbon advanced biofuel, when market conditions present favorable conditions. Similarly, with the EPA certification received in August 2013, we intend to opportunistically purchase the combination of grain sorghum and biogas to generate Advanced Biofuel RIN credits, when market conditions present favorable margins.

India

The cost of NRPO and the price of biodiesel are volatile and are generally uncorrelated. We therefore are exposed to ongoing and substantial commodity price risk. Our risk management strategy is to produce biodiesel in India only when we believe we can generate positive gross margins and to idle the plant during periods of low or negative gross margins. In 2013, we continued to develop markets and expand our customer base outside of the fuels market. During 2014, we introduced animal oil and fats as a means of further diversifying our feedstock and improving margins.

In addition, to minimize our commodity risk, we modified the processes within our facility to utilize lower cost NRPO, which enables us to reduce our feedstock costs. Our ability to mitigate the risk of falling biodiesel prices is more limited. The price of our biodiesel is generally indexed to the price of petroleum diesel, which is set by the Indian government. During January 2014 the Indian government fully lifted subsidies for diesel by increasing the sales price of diesel to the market price.

We have in the past, and may in the future, use forward purchase contracts and other hedging strategies; however, the extent to which we engage in these risk management strategies may vary substantially from time to time depending on market conditions and other factors.

Research and Development

Our R&D efforts consist of working to develop and commercialize our existing microbial technology, to evaluate third party technologies, and to expand the production of ethanol and other renewable bio-chemicals in the United States. The primary objective of this development activity is to optimize the production of ethanol using either our proprietary, patent-pending enzyme technology for large-scale commercial production or the evaluation of third party technologies which have promise for large-scale commercial adoption at one of our operating facilities. Our innovations are protected by several issued or pending patents. We are in the process of filing additional patents that will further strengthen the Company’s portfolio. Some core intellectual property has been exclusively and indefinitely licensed from the University of Maryland. R&D expense was $0.5 million in each of 2014 and 2013.

Patents and Trademarks

We have filed a number of trademark applications within the U.S. We do not consider the success of our business, as a whole, to be dependent on these trademarks. In addition, we hold nine patents and have applied for five additional patents in the United States. We also hold related patents and have applied for patents in major foreign jurisdictions. Our patents cover the Z-microbe and production of cellulosic ethanol. We intend to develop, maintain and secure further intellectual property rights and pursue new patents to expand upon our current patent base.

We have acquired exclusive rights to patented technology in support of the development and commercialization of our products, and we also rely on trade secrets and proprietary technology in developing potential products. We continue to place significant emphasis on securing global intellectual property rights and we are pursuing new patents to expand upon our strong foundation for commercializing products in development.

The company has received, and in the future may receive additional, claims of infringement of other parties’ proprietary rights. See Item 3. Legal Proceedings, below. Infringement or other claims could be asserted or prosecuted against the Company in the future, and it is possible that future assertions or prosecutions could harm our business. Any such claims, with or without merit, could be time-consuming, result in costly litigation and diversion of technical and management personnel, cause delays in the development of our products, or require the Company to develop non-infringing technology or enter into royalty or licensing arrangements. Such royalty or licensing arrangements, if required, may require the Company to license back its technology or may not be available on terms acceptable to the Company, or at all.

9

Environmental and Regulatory Matters

North America

We are subject to federal, state and local environmental laws, regulations and permit conditions, including those relating to the discharge of materials into the air, water and ground, the generation, storage, handling, use, transportation and disposal of hazardous materials, and the health and safety of our employees. These laws, regulations, and permits require us to incur, on an annual basis, significant capital costs. These include, but are not limited to, testing and monitoring plant emissions, and where necessary, obtaining and maintaining mitigation processes to comply with regulations. They may also require us to make operational changes to limit actual or potential impacts to the environment. A significant violation of these laws, regulations, permits or license conditions could result in substantial fines, criminal sanctions, permit revocations and/or facility shutdowns. In addition, environmental laws and regulations change over time, and any such changes, more vigorous enforcement policies or the discovery of currently unknown conditions may require substantial additional environmental expenditures.

We are also subject to potential liability for the investigation and cleanup of environmental contamination at each of the properties that we own or operate and at off-site locations where we arrange for the disposal of hazardous wastes. If significant contamination is identified at our properties in the future, costs to investigate and remediate this contamination as well as costs to investigate or remediate associated damage could be significant. If any of these sites are subject to investigation and/or remediation requirements, we may be responsible under the Comprehensive Environmental Response, Compensation and Liability Act of 1980 (“CERCLA”) or other environmental laws for all or part of the costs of such investigation and/or remediation, and for damage to natural resources. We may also be subject to related claims by private parties alleging property damage or personal injury due to exposure to hazardous or other materials at or from such properties. While costs to address contamination or related third-party claims could be significant, based upon currently available information, we are not aware of any material contamination or any such third party claims. Based on our current assessment of the environmental and regulatory risks, we have not accrued any amounts for environmental matters as of December 31, 2014. The ultimate costs of any liabilities that may be identified or the discovery of additional contaminants could materially adversely impact our results of operation or financial condition.

In addition, the production and transportation of our products may result in spills or releases of hazardous substances, which could result in claims from governmental authorities or third parties relating to actual or alleged personal injury, property damage, or damage to natural resources. We maintain insurance coverage against some, but not all, potential losses caused by our operations. Our general and umbrella liability policy coverage includes, but is not limited to, physical damage to assets, employer’s liability, comprehensive general liability, automobile liability and workers’ compensation. We do not carry environmental insurance. We believe that our insurance is adequate for our industry, but losses could occur for uninsurable or uninsured risks or in amounts in excess of existing insurance coverage. The occurrence of events which result in significant personal injury or damage to our property, natural resources or third parties that is not covered by insurance could have a material adverse impact on our results of operations and financial condition.

Our air emissions are subject to the federal Clean Air Act, and similar State laws, which generally require us to obtain and maintain air emission permits for our ongoing operations as well as for any expansion of existing facilities or any new facilities. Obtaining and maintaining those permits requires us to incur costs, and any future more stringent standards may result in increased costs and may limit or interfere with our operating flexibility. These costs could have a material adverse effect on our financial condition and results of operations. Because other ethanol manufacturers in the U.S. are and will continue to be subject to similar laws and restrictions, we do not currently believe that our costs to comply with current or future environmental laws and regulations will adversely affect our competitive position with other U.S. ethanol producers. However, because ethanol is produced and traded internationally, these costs could adversely affect us in our efforts to compete with foreign producers who are not subject to such stringent requirements.

New laws or regulations relating to the production, disposal or emission of carbon dioxide and other greenhouse gases may require us to incur significant additional costs with respect to ethanol plants that we build or acquire. For example, in 2007, Illinois and four other Midwestern states entered into the Midwestern Greenhouse Gas Reduction Accord, which directs participating states to develop a multi-sector cap-and-trade mechanism to help achieve reductions in greenhouse gases, including carbon dioxide. We currently conduct our North American commercial activities exclusively in California, however, it is possible that other states in which we plan to conduct business could join this accord or require other carbon dioxide emissions reductions. Climate change legislation is being considered in Washington, D.C. this year which may significantly impact the biofuels industry’s emissions regulations, as will the Renewable Fuel Standard, California’s Low Carbon Fuel Standard, and other potentially significant changes in existing transportation fuels regulations.

10

India

We are subject to national, state and local environmental laws, regulations and permits, including with respect to the generation, storage, handling, use, transportation and disposal of hazardous materials, and the health and safety of our employees. These laws may require us to make operational changes to limit actual or potential impacts to the environment. A violation of these laws, regulations or permits can result in substantial fines, natural resource damages, criminal sanctions, permit revocations and/or facility shutdowns. In addition, environmental laws and regulations (and interpretations thereof) change over time, and any such changes, more vigorous enforcement policies or the discovery of currently unknown conditions may require substantial additional environmental expenditures.

Employees

At December 31, 2014, we had a total of 131 full-time equivalent employees, comprised of 15 full-time equivalent employees in our corporate offices, 45 full-time equivalent employees at our plant in Keyes, California, two full-time equivalent employees in our Maryland research and development facility and 69 full-time equivalent employees in India.

We believe that our employees are highly-skilled, and our success will depend in part upon our ability to retain our employees and attract new qualified employees, many of whom are in great demand. We have never had a work stoppage or strike, and no employees are presently represented by a labor union or covered by a collective bargaining agreement. We believe our relations with our employees are good.

Available Information

We file reports with the Securities and Exchange Commission (“SEC”). We make available on our website under “Investor Relations,” free of charge, our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and amendments to those reports as soon as reasonably practicable after we electronically file such materials with or furnish them to the SEC. Our website address is www.aemetis.com. Our website address is provided as an inactive textual reference only, and the contents of that website are not incorporated in or otherwise to be regarded as part of this report. You can also read and copy any materials we file with the SEC at the SEC’s Public Reference Room at 100 F Street, NE, Washington, DC 20549. You may also obtain additional information about the operation of the Public Reference Room by calling the SEC at 1-800-SEC-0330. In addition, the SEC maintains an Internet site (www.sec.gov) that contains reports, proxy and information statements, and other information regarding issuers that file electronically with the SEC, including us.

|

Item 1A. Risk Factors

|

We operate in an evolving industry that presents numerous risks beyond our control that are driven by factors that cannot be predicted. Should any of the risks described in this section or in the documents incorporated by reference in this report actually occur, our business, results of operations, financial condition, or stock price could be materially and adversely affected. Investors should carefully consider the risks factors discussed below, in addition to the other information in this report, before making any investment in our securities.

Risks Related to our Overall Business

We are currently profitable, but historically, we have incurred significant losses. If we incur losses, we may have to curtail our operations, which may prevent us from successfully operating and expanding our business.

We are currently reporting a profitable year during 2014, but incurred significant losses in the past. Historically, we have relied upon cash from debt and equity financing activities to fund substantially all of the cash requirements of our activities. As of December 31, 2014, we had an accumulated deficit of approximately $87.1 million. For our fiscal years ended December 31, 2014, 2013 and 2012, we reported a net income of $7.1 million, net loss of $24.4 million and net loss of $4.3 million, respectively, primarily comprised of interest and fees related to our senior debt. Despite recent profitability and positive cash flow from operations, we may incur losses for an indeterminate period of time and may not achieve consistent profitability. An extended period of losses or negative cash flow may prevent us from successfully operating and expanding our business.

We are dependent upon our working capital agreements with J.D. Heiskell and Secunderabad Oils Limited.

Our ability to operate our Keyes plant depends on maintaining our working capital agreement with J.D. Heiskell (Heiskell), and our ability to operate our biodiesel plant in India depends on maintaining our working capital agreement with Secunderabad Oils Limited. The Heiskell agreement provides for an initial term of one year with automatic one-year renewals; provided, however, that Heiskell may terminate the agreement by notice 90 days prior to the end of the initial term or any renewal term. The current term extends through December 31, 2015. In addition, the agreement may be terminated at any time upon a default, such as payment default, bankruptcy, acts of fraud or material breach under one of our related agreements with Heiskell. The Secunderabad agreement may be terminated at any time by either party upon written notice. If we are unable to maintain these strategic relationships, we will be required to locate alternative sources of working capital and corn or sorghum supply, which we may be unable to do in a timely manner or at all. If we are unable to maintain our current working capital arrangements or locate alternative sources of working capital, our ability to operate our plants will be negatively affected.

11

Disruptions in ethanol production infrastructure may adversely affect our business, results of operations and financial condition.

Our business depends on the continuing availability of rail, road, port, storage and distribution infrastructure. In particular, due to limited storage capacity at the Keyes Plant and other considerations related to production efficiencies, the Keyes Plant depends on just-in-time delivery of corn and grain sorghum. The delivery and transformation of feedstock requires a significant and uninterrupted supply of corn and grain sorghum, principally delivered by rail, as well as other raw materials and energy, primarily electricity and natural gas. The prices of rail, electricity and natural gas have fluctuated significantly in the past and may fluctuate significantly in the future. The national rail system, as well as local electricity and gas utilities may not be able to reliably supply the rail logistics, electricity and natural gas that the Keyes Plant will need or may not be able to supply those resources on acceptable terms. Any disruptions in the ethanol production infrastructure, whether caused by labor difficulties, earthquakes, storms, other natural disasters or human error or malfeasance or other reasons, could prevent timely deliveries of corn, grain sorghum or other raw materials and energy and may require the Keyes Plants to halt production which could have a material adverse effect on our business, results of operations and financial condition.

Our results from operations are primarily dependent on the spread between the feedstock and energy we purchase and the fuel, animal feed and other products we sell.

The results of our ethanol production business in the U.S. are significantly affected by the spread between the cost of the corn and natural gas that we purchase and the price of the ethanol, distillers grains and corn oil that we sell. Similarly, in India our biodiesel business is primarily dependent on the price difference between the costs of the feedstock we purchase (principally NRPO and crude glycerin) and the products we sell (principally distilled biodiesel and refined glycerin). The markets for ethanol, biodiesel, distiller grains, corn oil and glycerin are highly volatile and subject to significant fluctuations. Any decrease in the spread between prices of the commodities we buy and sell, whether as a result of an increase in feedstock prices or a reduction in ethanol or biodiesel prices, would adversely affect our financial performance and cash flow and may cause us to suspend production at either of our plants.

The price of ethanol is volatile and subject to large fluctuations, and increased ethanol production may cause a decline in ethanol prices or prevent ethanol prices from rising, either of which could adversely impact our results of operations, cash flows and financial condition.

The market price of ethanol is volatile and subject to large fluctuations. The market price of ethanol is dependent upon many factors, including the supply of ethanol and the demand for gasoline, which is in turn dependent upon the price of petroleum which is also highly volatile and difficult to forecast. Fluctuations in the market price of ethanol may cause our profitability or losses to fluctuate significantly. In addition, domestic ethanol production capacity increased significantly in the last decade. Demand for ethanol may not increase commensurate with increases in supply, which could lead to lower ethanol prices. Demand for ethanol could be impaired due to a number of factors, including regulatory developments and reduced United States gasoline consumption. Reduced gasoline consumption has occurred in the past and could occur in the future as a result of increased gasoline or oil prices.

Decreasing gasoline prices may negatively impact the selling price of ethanol which could reduce our ability to operate profitably.

The price of ethanol tends to change in relation to the price of gasoline. Recently, as a result of a number of factors including the current world economy, the price of gasoline has decreased. In correlation to the decrease in the price of gasoline, the price of ethanol has also decreased. Decreases in the price of ethanol reduce our revenue. Our profitability depends on a favorable spread between our corn and natural gas costs and the price we receive for our ethanol. If ethanol prices fall during times when corn and/or natural gas prices are high, we may not be able to operate profitably.

We may be unable to execute our business plan.

The value of our long-lived assets is based on our ability to execute our business plan and generate sufficient cash flow to justify the carrying value of our assets. Should we fall short of our cash flow projections, we may be required to write down the value of these assets under accounting rules and further reduce the value of our assets. We can make no assurances that future cash flows will develop and provide us with sufficient cash to maintain the value of these assets, thus avoiding future impairment to our asset carrying values. As a result, we may need to write down the carrying value of our long-lived assets.

In addition, we intend to modify or adapt third party technologies at the Keyes ethanol plant and at the India biodiesel plant to accommodate alternative feedstocks and improve operations. After we design and engineer a specific integrated upgrade to either or both plants to allow us to produce products other than their existing products, we may not receive permission from the regulatory agencies to install the process at one or both plants. Additionally, even if we are able to install and begin operations of an integrated advanced fuels and/or bio-chemical plant, we cannot assure you that the technology will work and produce cost effective products because we have never designed, engineered nor built this technology into an existing bio-refinery. Similarly, our plans to add a CO2 conversion unit at the Keyes plant may not be successful as a result of financing, issues in the design or construction process, or our ability to sell liquid CO2 at cost effective prices. Any inability to execute our business plan may have a material adverse effect on our operations, financial position, and ability to pay dividends and continue as a going concern.

12

We are dependent on, and vulnerable to any difficulties of, our principal suppliers and customers.

We buy all of the feedstock for the Keyes plant from one supplier, J.D. Heiskell. Under our Agreements with Heiskell, we are only permitted to purchase feedstock from other suppliers upon the satisfaction of certain conditions. In addition, we have contracted to sell all of the WDG, CDS, corn oil and ethanol we produce at the Keyes Plant to Heiskell. Heiskell, in turn, sells all ethanol produced at the Keyes plant to Kinergy Marketing and all WDG and syrup to A.L. Gilbert. If Heiskell were to fail to deliver adequate feedstock to our plant or fail to purchase all the product we produce, if Kinergy were to fail to purchase all of the ethanol we produce, if A.L. Gilbert were to fail to purchase all of the WDG and syrup we produce, or if any of them were otherwise to default on our agreements with them or fail to perform as expected, we may be unable to find replacement suppliers or purchasers, or both, in a reasonable time or on favorable terms, any of which could materially adversely affect our results from operations and financial results.

We are currently in default on our term loan with the State Bank of India.

On March 10, 2011, one of our subsidiaries, Universal Biofuels Pvt. Ltd. (“UBPL”), received a demand notice from the State Bank of India under the Agreement of Loan for Overall Limit dated as of June 26, 2008. The notice informed UBPL that an event of default had occurred for failure to make an installment payment on the loan commencing June 2009 and demanded repayment of the entire outstanding indebtedness of 19.60 crores (approximately $3.2 million) together with all accrued interest thereon and any applicable fees and expenses. Upon the occurrence and during the continuance of the default, interest accrues at the default interest rate of 2% above the State Bank of India Advance Rate pursuant to the agreement. The State Bank of India has filed a legal case before the Debt Recovery Tribunal (“DRT”), Hyderabad, for recovery of approximately $5.9 million against the Company and also impleaded Andhra Pradesh Industrial Infrastructure Corporation (“APIIC”) to expedite the registration of the sale deed of the property on which the UBPL facility is located. If the Company is unable to prevail with in this legal case, DRT may pass a decree for recovery of the amount due, which may include seizing property. Interest continues to accrue at the default rate in the amount of approximately $66,000 per month during the continuance of default. If the DRT were to issue an order to seize our India plant and we were unable to successfully stay the order, our operations and financial position would be adversely affected.

We may be unable to repay or refinance our Third Eye Capital Notes upon maturity.

Under our note facilities with Third Eye Capital Corporation, we owe approximately $57.6 million, excluding debt discounts, as of December 31, 2014. Our indebtedness and interests payments under these note facilities are currently substantial and may adversely affect our cash flow, cash position and stock price. These notes are currently due in July 2015 although the maturity can be extended to January 2016 upon payment of certain fees. We have been able to extend our indebtedness in the past, but we may not be able to continue to extend the maturity of these notes. We may not have sufficient cash available at the time of maturity to repay this indebtedness. We have default covenants that may accelerate the maturities of these notes. We may not have sufficient assets or cash flow available to support refinancing these notes at market rates or on terms that are satisfactory to us. If we are unable to extend the maturity of the notes or refinance on terms satisfactory to us, we may be forced to refinance on terms that are materially less favorable, seek funds through other means such as a sale of some of our assets, or otherwise significantly alter our operating plan, any of which could have a material adverse effect on our business, financial condition, and results of operations. Additionally, if we are unable to amend our current note purchase agreement with Third Eye Capital, our ability to pay dividends could be restrained.

Our business is dependent on external financing and cash from operations to service debt and provide future growth.

The adoptions of new technologies at our ethanol and biodiesel plants, along with working capital, are financed in part through debt facilities. We may need to seek additional financing to continue or grow our operations. However, generally unfavorable credit market conditions may make it difficult to obtain necessary capital or additional debt financing on commercially viable terms or at all. If we are unable to pay our debt we may be forced to delay or cancel capital expenditures, sell assets, restructure our indebtedness, seek additional financing, or file for bankruptcy protection. Debt levels or debt service requirements may limit our ability to borrow additional capital, make us vulnerable to increases in prevailing interest rates, subject our assets to liens, limit our ability to adjust to changing market conditions, or place us at a competitive disadvantage to our competitors. Should we be unable to generate enough cash from our operations or secure additional financing to fund our operations and debt service requirements, we may be required to postpone or cancel growth projects, reduce our operations, or may be unable to meet our debt repayment schedules. Any one of these events would likely have a material adverse effect on our operations and financial position.

13

There can be no assurance that our existing cash flow from operations will be sufficient to sustain operations and to the extent that we are dependent on credit facilities to fund operations or service debt there can be no assurances that we will be successful at securing funding from our senior lender or significant shareholders. Should the Company require additional financing, there can be no assurances that the additional financing will be available on terms satisfactory to the Company. Our ability to identify and enter into commercial arrangements with feedstock suppliers in India depends on maintaining our operations agreement with Secunderabad Oil Limited, who is currently providing us with working capital for our Kakinada facility. If we are unable to maintain this strategic relationship, our business may be negatively affected. In addition, the ability of Secunderabad to continue to provide us with working capital depends in part on the financial strength of Secunderabad and its banking relationships. If Secunderabad is unable or unwilling to continue to provide us with working capital, our business may be negatively affected. Our ability to enter into commercial arrangements with feedstock suppliers in California depends on maintaining our operations agreement with J.D. Heiskell, who is currently providing us with working capital for our California ethanol plant. If we are unable to maintain this strategic relationship, our business may be negatively affected. In addition, the ability of J.D. Heiskell to continue to provide us with working capital depends in part on the financial strength of J.D. Heiskell and its banking relationships. If J.D. Heiskell is unable or unwilling to continue to provide us with working capital, our business may be negatively affected. There is no assurance that UBPL or the Company will be able to obtain alternative funding in the event the State Bank of India demands payment and immediate acceleration would have a significant adverse impact on UBPL or the Company’s near term liquidity and our ability to operate our biodiesel plant. Our consolidated financial statements do not include any adjustments to the classification or carrying values of our assets or liabilities that might be necessary as a result of the outcome of this uncertainty.

We may not receive the funds we expect under our EB-5 program

The EB-5 program allows for the issuance of up to 72 subordinated convertible promissory notes, each in the amount of $0.5 million due and payable four years from the date of the note for a total aggregate principal amount of up to $36.0 million. Deposits held in escrow pending investor approval by the U.S. Citizenship and Immigration Services were $22.0 million at December 31, 2014. While $22 million of EB-5 program funds have been received into escrow as of December 31, 2014, the release of those funds to us is subject to the approval of the USCIS, which could take a year or more to obtain. Additionally, the USCIS could deny approval of the loans, and then we would not receive some or all of the subscribed funds. If the USCIS takes longer to approve the release of funds in escrow, or does not approve the loans at all, it would have a material adverse effect on our cash flows available for operations, and thus could have a material adverse effect on our results of operations.

We face competition for our bio-chemical and transportation fuels products from providers of petroleum-based products and from other companies seeking to provide alternatives to these products, many of whom have greater resources and experience than we do, and if we cannot compete effectively against these companies we may not be successful.

Our renewable products compete with both the traditional, largely petroleum-based bio-chemical and fuels products that are currently being used in our target markets and with the alternatives to these existing products that established enterprises and new companies are seeking to produce. The oil companies, large chemical companies and well-established agricultural products companies with whom we compete are much larger than we are, and have, in many cases, well developed distribution systems and networks for their products.

In the transportation fuels market, we compete with independent and integrated oil refiners, advanced biofuels companies and biodiesel companies. Refiners compete with us by selling traditional fuel products and some are also pursuing hydrocarbon fuel production using non-renewable feedstocks, such as natural gas and coal, as well as processes using renewable feedstocks, such as vegetable oil and biomass. We also expect to compete with companies that are developing the capacity to produce diesel and other transportation fuels from renewable resources in other ways.

With the emergence of many new companies seeking to produce chemicals and fuels from alternative sources, we may face increasing competition from alternative fuels and chemicals companies. As they emerge, some of these companies may be able to establish production capacity and commercial partnerships to compete with us. If we are unable to establish production and sales channels that allow us to offer comparable products at attractive prices, we may not be able to compete effectively with these companies.

The high concentration of our sales within the ethanol production industry could result in a significant reduction in sales and negatively affect our profitability if demand for ethanol declines.

We expect our US operations are to be substantially focused on the production of ethanol and its co-products for the foreseeable future. We may be unable to shift our business focus away from the production of ethanol to other renewable fuels or competing products. Accordingly, an industry shift away from ethanol or the emergence of new competing products may reduce the demand for ethanol. A downturn in the demand for ethanol could materially and adversely affect our sales and profitability.

14

Our operations are subject to environmental, health, and safety laws, regulations, and liabilities.

Our operations are subject to various federal, state and local environmental laws and regulations, including those relating to the discharge of materials into the air, water and ground, the generation, storage, handling, use, transportation and disposal of hazardous materials, access to and impacts on water supply, and the health and safety of our employees. In addition, our operations and sales in India subject us to risks associated with foreign laws, policies, and regulations. Some of these laws and regulations require our facilities to operate under permits or licenses that are subject to renewal or modification. These laws, regulations and permits can require expensive emissions testing and pollution control equipment or operational changes to limit actual or potential impacts to the environment. A violation of these laws and regulations or permits or license conditions can result in substantial fines, natural resource damages, criminal sanctions, permit revocations and facility shutdowns. We may not be at all times in compliance with these laws, regulations, permits or licenses or we may not have all permits or licenses required to operate our business. We may be subject to legal actions brought by environmental advocacy groups and other parties for actual or alleged violations of environmental laws, permits or licenses. In addition, we may be required to make significant capital expenditures on an ongoing basis to comply with increasingly stringent environmental laws, regulations, permit and license requirements.

We may be liable for the investigation and cleanup of environmental contamination at the Keyes plant and at off-site locations where we arrange for the disposal of hazardous substances. If hazardous substances have been or are disposed of or released at sites that undergo investigation or remediation by regulatory agencies, we may be responsible under CERCLA or other environmental laws for all or part of the costs of investigation and remediation, and for damage to natural resources. We also may be subject to related claims by private parties alleging property damage and personal injury due to exposure to hazardous or other materials at or from those properties. Some of these matters may require us to expend significant amounts for investigation, cleanup or other costs.

New laws, new interpretations of existing laws, increased governmental enforcement of environmental laws or other developments could require us to make additional significant expenditures. Continued government and public emphasis on environmental issues can be expected to result in increased future investments for environmental controls at our production facilities. Environmental laws and regulations applicable to our operations now or in the future, more vigorous enforcement policies and discovery of currently unknown conditions may require substantial expenditures that could have a negative impact on our results of operations and financial condition.

Emissions of carbon dioxide resulting from manufacturing ethanol are not currently subject to permit requirements. If new laws or regulations are passed relating to the production, disposal or emissions of carbon dioxide, we may be required to incur significant costs to comply with such new laws or regulations.

Our business is affected by greenhouse gas and climate change regulation.

The operations at our Keyes plant will result in the emission of carbon dioxide into the atmosphere. In March 2010, the EPA released its final regulations on the Renewable Fuels Standard Program, or RFS2. We believe the EPA’s final RFS2 regulations grandfather the Keyes facility we operate at its current capacity, however, compliance with future legislation may require us to take action unknown to us at this time that could be costly, and require the use of working capital, which may or may not be available, preventing us from operating as planned, which may have a material adverse effect on our operations and cash flow.

A change in government policies may cause a decline in the demand for our products.

The domestic ethanol industry is highly dependent upon a myriad of federal and state regulations and legislation, and any changes in legislation or regulation could adversely affect our results of operations and financial position. Other federal and state programs benefiting ethanol generally are subject to U.S. government obligations under international trade agreements, including those under the World Trade Organization Agreement on Subsidies and Countervailing Measures, and may be the subject of challenges, in whole or in part. Growth and demand for ethanol and biodiesel is largely driven by federal and state government mandates or blending requirements, such as the Renewable Fuel Standard (RFS). Any change in government policies could have a material adverse effect our business and the results of our operations.

Ethanol can be imported into the United States duty-free from some countries, which may undermine the domestic ethanol industry. Production costs for ethanol in these countries can be significantly less than in the United States and the import of lower price or lower carbon value ethanol from these countries may reduce the demand for domestic ethanol and depress the price at which we sell our ethanol.

Waivers of the RFS minimum levels of renewable fuels included in gasoline could have a material adverse effect on our results of operations. Under the Energy Policy Act, the U.S. Department of Energy, in consultation with the Secretary of Agriculture and the Secretary of Energy, may waive the renewable fuels mandate with respect to one or more states if the Administrator of the Environmental Protection Agency determines that implementing the requirements would severely harm the economy or the environment of a state, a region or the nation, or that there is inadequate supply to meet the requirement. Any waiver of the RFS with respect to one or more states would reduce demand for ethanol and could cause our results of operations to decline and our financial condition to suffer.

15

In November 2013, the EPA initially proposed a waiver to the RFS by reducing the RFS for 2014 from the previous requirement of 18.15 billion gallons to a revised level of 15.21 billion gallons. The EPA proposal represents a reduction of approximately 16% from the original RFS fuel volume for 2014. The EPA subsequently indicated that they would release the requirements in late fall, and then again pushed the final rule release date to early 2015. As of the date of this report, the EPA has yet to release the final determination on the revised 2014 RFS requirements.

We may encounter unanticipated difficulties in converting the Keyes plant to accommodate alternative feedstocks, new chemicals used in the fermentation and distillation process, or new mechanical production equipment.

In order to improve the operations of the Keyes plant and execute on our business plan, we intend to modify the plant to accommodate alternative feedstocks and new chemical and/or mechanical production processes. We may not be able successfully to implement these modifications, and they may not function as we expect them to. These modifications may cost significantly more to complete than our estimates. The plant may not operate at nameplate capacity once the changes are complete. If any of these risks materialize, they could have a material adverse impact on our results of operation and financial position.

We may be subject to liabilities and losses that may not be covered by insurance.

Our employees and facilities are subject to the hazards associated with producing ethanol and biodiesel. Operating hazards can cause personal injury and loss of life, damage to, or destruction of, property, plant and equipment and environmental damage. We maintain insurance coverage in amounts and against the risks that we believe are consistent with industry practice. However, we could sustain losses for uninsurable or uninsured risks, or in amounts in excess of existing insurance coverage. Events that result in significant personal injury or damage to our property or to property owned by third parties or other losses that are not fully covered by insurance could have a material adverse effect on our results of operations and financial position.

Insurance liabilities are difficult to assess and quantify due to unknown factors, including the severity of an injury, the determination of our liability in proportion to other parties, the number of incidents not reported and the effectiveness of our safety program. If we were to experience insurance claims or costs above our coverage limits or that are not covered by our insurance, we might be required to use working capital to satisfy these claims rather than to maintain or expand our operations. To the extent that we experience a material increase in the frequency or severity of accidents or workers’ compensation claims, or unfavorable developments on existing claims, our operating results and financial condition could be materially and adversely affected.

Our success depends in part on recruiting and retaining key personnel and, if we fail to do so, it may be more difficult for us to execute our business strategy.

Our success depends on our continued ability to attract, retain and motivate highly qualified management, manufacturing and scientific personnel, in particular our Chairman and Chief Executive Officer, Eric McAfee. We do not maintain any key man insurance. Competition for qualified personnel in the renewable fuel and bio-chemicals manufacturing fields is intense. Our future success will depend on, among other factors, our ability to retain our current key personnel and attract and retain qualified future key personnel, particularly executive management. Failure to attract or retain key personnel could have a material adverse effect on our business and results of operations.

Our operations subject us to risks associated with foreign laws, policies, regulations, and markets.