Prospectus

Fixed income mutual funds

Fixed income mutual funds

December 30, 2014

|

Nasdaq ticker symbols |

|||

|

Class A |

Class C |

Inst. Class |

|

|

Delaware Tax-Free Arizona Fund |

VAZIX |

DVACX |

DAZIX |

|

Delaware Tax-Free California Fund |

DVTAX |

DVFTX |

DCTIX |

|

Delaware Tax-Free Colorado Fund |

VCTFX |

DVCTX |

DCOIX |

|

Delaware Tax-Free Idaho Fund |

VIDAX |

DVICX |

DTIDX |

|

Delaware Tax-Free New York Fund |

FTNYX |

DVFNX |

DTNIX |

|

Delaware Tax-Free Pennsylvania Fund |

DELIX |

DPTCX |

DTPIX |

|

Delaware Tax-Free Minnesota Fund |

DEFFX |

DMOCX |

DMNIX |

|

Delaware Tax-Free Minnesota |

DXCCX |

DVSCX |

DMIIX |

|

Delaware Minnesota High-Yield Municipal Bond Fund |

DVMHX |

DVMMX |

DMHIX |

The U.S. Securities and Exchange Commission has not approved or disapproved these Get shareholder reports and prospectuses online instead of in the mail.

securities or passed upon the adequacy of this Prospectus. Any representation to the

contrary is a criminal offense.

Visit delawareinvestments.com/edelivery.

|

|

| Table of contents | |

|

1 |

|

|

1 |

|

|

6 |

|

|

10 |

|

|

14 |

|

|

18 |

|

|

22 |

|

|

27 |

|

|

32 |

|

|

37 |

|

|

42 |

|

|

42 |

|

|

42 |

|

|

46 |

|

|

47 |

|

|

50 |

|

|

51 |

|

|

51 |

|

|

51 |

|

|

52 |

|

|

53 |

|

|

54 |

|

|

54 |

|

|

54 |

|

|

56 |

|

|

56 |

|

|

57 |

|

|

57 |

|

|

58 |

|

|

58 |

|

|

59 |

|

|

59 |

|

|

60 |

|

|

60 |

|

|

60 |

|

|

61 |

|

|

61 |

|

|

63 |

|

|

64 |

|

|

68 |

|

|

97 |

Delaware Tax-Free Arizona Fund

What is the Fund's investment objective?

Delaware Tax-Free Arizona Fund seeks as high a level of current income exempt from federal income tax and from the Arizona state personal income tax as is consistent with preservation of capital.

What are the Fund's fees and expenses?

The following table describes the fees and expenses that you may pay if you buy and hold shares of the Fund. You may qualify for sales-charge discounts if you and your family invest, or agree to invest in the future, at least $100,000 in Delaware Investments® Funds. More information about these and other discounts is available from your financial advisor, in the Fund's prospectus under the section entitled "About your account," and in the Fund's statement of additional information (SAI) under the section entitled "Purchasing Shares."

| Shareholder fees (fees paid directly from your investment) | |||||

| Class | A | C | Inst. | ||

| Maximum sales charge (load) imposed on purchases as a percentage of offering price |

4.50% | none | none | ||

| Maximum contingent deferred sales charge (load) as a percentage of original purchase price or redemption price, whichever is lower | none | 1.00%1 | none | ||

| Annual fund operating expenses (expenses that you pay each year as a percentage of the value of your investment) | |||||

| Class | A | C | Inst. | ||

| Management fees | 0.50% | 0.50% | 0.50% | ||

| Distribution and service (12b-1) fees | 0.25% | 1.00% | none | ||

| Other expenses | 0.21% | 0.21% | 0.21% | ||

| Total annual fund operating expenses | 0.96% | 1.71% | 0.71% | ||

| Fee waivers and expense reimbursements | (0.12%)2 | (0.12%)2 | (0.12%)2 | ||

| Total annual fund operating expenses after fee waivers and expense reimbursements |

0.84% | 1.59% | 0.59% | ||

| 1 |

Class C shares redeemed within one year of purchase are subject to a 1.00% contingent deferred sales charge (CDSC). |

| 2 |

The Fund's investment manager, Delaware Management Company (Manager), has contractually agreed to waive all or a portion of its investment advisory fees and/or pay/reimburse expenses (excluding any 12b-1 fees, acquired fund fees and expenses, taxes, interest, inverse floater program expenses, short sale and dividend interest expenses, brokerage fees, certain insurance costs, and nonroutine expenses or costs, including, but not limited to, those relating to reorganizations, litigation, conducting shareholder meetings, and liquidations) in order to prevent total annual fund operating expenses from exceeding 0.59% of the Fund's average daily net assets from Dec. 29, 2014 through Dec. 29, 2015. These waivers and reimbursements may only be terminated by agreement of the Manager and the Fund. |

Example

This example is intended to help you compare the cost of investing in the Fund with the cost of investing in other mutual

funds. The example assumes that you invest $10,000 in the Fund for the time periods indicated and then redeem all of your

shares at the end of those periods. The example also assumes that your investment has a 5% return each year and reflects the

Manager's expense waivers and reimbursements for the 1-year contractual period and the total operating expenses without waivers

for years 2 through 10. Although your actual costs may be higher or lower, based on these assumptions your costs would be:

| (if not redeemed) | ||||

| Class | A | C | C | Inst. |

| 1 year | $532 | $162 | $262 | $60 |

| 3 years | $731 | $527 | $527 | $215 |

| 5 years | $946 | $917 | $917 | $383 |

| 10 years | $1,565 | $2,009 | $2,009 | $871 |

Portfolio turnover

The Fund pays transaction costs, such as commissions, when it buys and sells securities (or "turns over" its portfolio). A higher portfolio turnover rate may indicate higher transaction costs and may result in higher taxes when Fund shares are held in a taxable account. These costs, which are not reflected in the annual fund operating expenses or in the example, affect the Fund's performance. During the most recent fiscal year, the Fund's portfolio turnover rate was 11% of the average value of its portfolio.

What are the Fund's principal investment strategies?

Under normal circumstances, the Fund will invest at least 80% of its net assets, plus the amount of any borrowings for investment purposes, in municipal securities the income from which is exempt from federal income tax, including the federal alternative minimum tax, and from Arizona state personal income taxes. This is a fundamental investment policy that may not be changed without prior shareholder approval.

Municipal debt obligations are issued by state and local governments to raise funds for various public purposes such as hospitals, schools, and general capital expenses. Municipal debt obligations may also include securities issued by U.S. territories and possessions (such as the Commonwealth of Puerto Rico, Guam, and the U.S. Virgin Islands) to the extent that these securities are also exempt from federal income tax and Arizona state personal income taxes. The Fund will invest its assets in securities with maturities of various lengths, depending on market conditions. The investment manager will adjust the average maturity of the bonds in the portfolio to attempt to provide a high level of tax-exempt income consistent with preservation of capital. The Fund's income level will vary depending on current interest rates and the specific securities in the portfolio. The Fund may concentrate its investments in certain types of bonds or in a certain segment of the municipal bond market when the supply of bonds in other sectors does not suit its investment needs. The Fund may invest in insured municipal bonds. The Fund will generally have a dollar-weighted average effective maturity of between 5 and 30 years.

What are the principal risks of investing in the Fund?

Investing in any mutual fund involves the risk that you may lose part or all of the money you invest. Over time, the value of your investment in the Fund will increase and decrease according to changes in the value of the securities in the Fund's portfolio. Principal risks include:

Investments not guaranteed by Delaware Management Company (Manager) or its affiliates — Investments in the Fund are not and will not be deposits with or liabilities of Macquarie Bank Limited ABN 46 008 583 542 and its holding companies, including their subsidiaries or related companies (Macquarie Group), and are subject to investment risk, including possible delays in repayment and loss of income and capital invested. No Macquarie Group company guarantees or will guarantee the performance of the Fund, the repayment of capital from the Fund, or any particular rate of return.

Market risk — The risk that all or a majority of the securities in a certain market — such as the stock or bond market — will decline in value because of factors such as adverse political or economic conditions, future expectations, investor confidence, or heavy institutional selling.

Interest rate risk — The risk that securities will decrease in value if interest rates rise. This risk is generally associated with bonds.

Credit risk — The risk that an issuer of a debt security, including a governmental issuer or an entity that insures a bond, may be unable to make interest payments and repay principal in a timely manner.

High yield (junk bond) risk — The risk that high yield securities, commonly known as "junk bonds," are subject to reduced creditworthiness of issuers; increased risk of default and a more limited and less liquid secondary market; and greater price volatility and risk of loss of income and principal than are higher-rated securities. High yield bonds are sometimes issued by municipalities with less financial strength and therefore have less ability to make projected debt payments on the bonds.

Call risk — The risk that a bond issuer will prepay the bond during periods of low interest rates, forcing a fund to reinvest that money at interest rates that might be lower than rates on the called bond.

Liquidity risk — The possibility that securities cannot be readily sold within seven days at approximately the price at which a portfolio

has

valued them.

Geographic concentration risk — The risk that heightened sensitivity to regional, state, U.S. territories or possessions (such as the Commonwealth of Puerto Rico, Guam, or the U.S. Virgin Islands), and local political and economic conditions could adversely affect the holdings in and performance of a fund. There is also the risk that there could be an inadequate supply of municipal bonds in a particular state or U.S. territory or possession.

Alternative minimum tax risk — If a fund invests in bonds whose income is subject to the alternative minimum tax, that portion of the fund's distributions would be taxable for shareholders who are subject to this tax.

Government and regulatory risk — The risk that governments or regulatory authorities have, from time to time, taken or considered actions that could adversely affect various sectors of the securities markets and significantly affect fund performance. For example, a tax-exempt security may be reclassified by the Internal Revenue Service or a state tax authority as taxable, and/or future legislative, administrative, or court actions could cause interest from a tax-exempt security to become taxable, possibly retroactively.

How has Delaware Tax-Free Arizona Fund performed?

The bar chart and table below provide some indication of the risks of investing in the Fund by showing changes in the Fund's performance from year to year and by showing how the Fund's average annual total returns for the 1-, 5-, and 10-year or lifetime periods compare with those of a broad measure of market performance. The Fund's past performance (before and after taxes) is not necessarily an indication of how it will perform in the future. The returns reflect any expense caps in effect during these periods. The returns would be lower without the expense caps. You may obtain the Fund's most recently available month-end performance by calling 800 523-1918 or by visiting our website at delawareinvestments.com/performance.

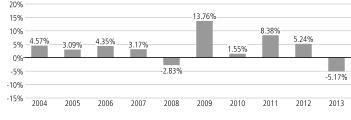

Year-by-year total return (Class A)

|

|

As of Sept. 30, 2014, the Fund's Class A shares had a calendar year-to-date return of 9.13%. During the periods illustrated in this bar chart, Class A's highest quarterly return was 8.33% for the quarter ended Sept. 30, 2009 and its lowest quarterly return was -4.98% for the quarter ended Dec. 31, 2010. The maximum Class A sales charge of 4.50%, which is normally deducted when you purchase shares, is not reflected in the highest/lowest quarterly returns or in the bar chart. If this fee were included, the returns would be less than those shown. The average annual total returns in the table below do include the sales charge.

Average annual total returns for periods ended December 31, 2013

| 1 year | 5 years | 10 years or lifetime | |

| Class A return before taxes | -9.61% | 4.36% | 3.14% |

| Class A return after taxes on distributions | -9.67% | 4.31% | 3.12% |

| Class A return after taxes on distributions and sale of Fund shares | -3.83% | 4.35% | 3.34% |

| Class C return before taxes | -6.94% | 4.53% | 2.84% |

| Institutional Class return before taxes (lifetime: 12/31/13–12/31/13)* | — | — | 0.09% |

| Barclays Municipal Bond Index (reflects no deduction for fees, expenses, or taxes) | -2.55% | 5.89% | 4.29% |

* Institutional Class shares commenced operations on Dec. 31, 2013. The returns shown have not been annualized.

After-tax performance is presented only for Class A shares of the Fund. The after-tax returns for other Fund classes may vary. Actual after-tax returns depend on the investor's individual tax situation and may differ from the returns shown. After-tax returns are not relevant for shares held in tax-deferred investment vehicles such as employer-sponsored 401(k) plans and individual retirement accounts (IRAs). The after-tax returns shown are calculated using the highest individual federal marginal income tax rates in effect during the periods presented and do not reflect the impact of state and local taxes.

Who manages the Fund?

Investment manager

Delaware Management Company, a series of Delaware Management Business Trust

|

Portfolio managers |

Title with Delaware Management Company |

Start date on the Fund |

|

Joseph R. Baxter |

Senior Vice President, Head of Municipal Bond Department, Senior Portfolio Manager |

April 2004 |

|

Stephen J. Czepiel |

Senior Vice President, Senior Portfolio Manager |

July 2007 |

|

Gregory A. Gizzi |

Senior Vice President, Senior Portfolio Manager |

December 2012 |

Purchase and redemption of Fund shares

You may purchase or redeem shares of the Fund on any day that the New York Stock Exchange (NYSE) is open for business (Business

Day). Shares may be purchased or redeemed: through your financial advisor; through the Fund's website at delawareinvestments.com;

by calling 800 523-1918; by regular mail (c/o Delaware Investments, P.O. Box 9876, Providence, RI 02940-8076); by overnight

courier service (c/o Delaware Service Center,

4400 Computer Drive, Westborough, MA 01581-1722); or by wire.

For Class A and Class C shares, the minimum initial investment is generally $1,000 and subsequent investments can be made for as little as $100. For Institutional Class shares (except those shares purchased through an automatic investment plan), there is no minimum initial purchase requirement, but certain eligibility requirements must be met. The eligibility requirements are described in the prospectus under "Choosing a share class" and on the Fund's website. We may reduce or waive the minimums or eligibility requirements in certain cases.

Tax information

The Fund's distributions primarily are exempt from regular federal and state income taxes for residents of Arizona. A portion of these distributions, however, may be subject to the federal alternative minimum tax. The Fund may also make distributions that are taxable to you as ordinary income or capital gains.

Payments to broker/dealers and other financial intermediaries

If you purchase shares of the Fund through a broker/dealer or other financial intermediary (such as a bank), the Fund and its related companies may pay the intermediary for the sale of Fund shares and related services. These payments may create a conflict of interest by influencing the broker/dealer or other intermediary and your salesperson to recommend the Fund over another investment. Ask your salesperson or visit your financial intermediary's website for more information.

Delaware Tax-Free California Fund

What is the Fund's investment objective?

Delaware Tax-Free California Fund seeks as high a level of current income exempt from federal income tax and from the California state personal income tax as is consistent with preservation of capital.

What are the Fund's fees and expenses?

The following table describes the fees and expenses that you may pay if you buy and hold shares of the Fund. You may qualify for sales-charge discounts if you and your family invest, or agree to invest in the future, at least $100,000 in Delaware Investments® Funds. More information about these and other discounts is available from your financial advisor, in the Fund's prospectus under the section entitled "About your account," and in the Fund's statement of additional information (SAI) under the section entitled "Purchasing Shares."

| Shareholder fees (fees paid directly from your investment) | |||||

| Class | A | C | Inst. | ||

| Maximum sales charge (load) imposed on purchases as a percentage of offering price |

4.50% | none | none | ||

| Maximum contingent deferred sales charge (load) as a percentage of original purchase price or redemption price, whichever is lower | none | 1.00%1 | none | ||

| Annual fund operating expenses (expenses that you pay each year as a percentage of the value of your investment) | |||||

| Class | A | C | Inst. | ||

| Management fees | 0.55% | 0.55% | 0.55% | ||

| Distribution and service (12b-1) fees | 0.25% | 1.00% | none | ||

| Other expenses | 0.20% | 0.20% | 0.20% | ||

| Total annual fund operating expenses | 1.00% | 1.75% | 0.75% | ||

| Fee waivers and expense reimbursements | (0.18%)2 | (0.18%)2 | (0.18%)2 | ||

| Total annual fund operating expenses after fee waivers and expense reimbursements |

0.82% | 1.57% | 0.57% | ||

| 1 |

Class C shares redeemed within one year of purchase are subject to a 1.00% contingent deferred sales charge (CDSC). |

| 2 |

The Fund's investment manager, Delaware Management Company (Manager), has contractually agreed to waive all or a portion of its investment advisory fees and/or pay/reimburse expenses (excluding any 12b-1 fees, acquired fund fees and expenses, taxes, interest, inverse floater program expenses, short sale and dividend interest expenses, brokerage fees, certain insurance costs, and nonroutine expenses or costs, including, but not limited to, those relating to reorganizations, litigation, conducting shareholder meetings, and liquidations) in order to prevent total annual fund operating expenses from exceeding 0.57% of the Fund's average daily net assets from Dec. 29, 2014 through Dec. 29, 2015. These waivers and reimbursements may only be terminated by agreement of the Manager and the Fund. |

Example

This example is intended to help you compare the cost of investing in the Fund with the cost of investing in other mutual

funds. The example assumes that you invest $10,000 in the Fund for the time periods indicated and then redeem all of your

shares at the end of those periods. The example also assumes that your investment has a 5% return each year and reflects the

Manager's expense waivers and reimbursements for the 1-year contractual period and the total operating expenses without waivers

for years 2 through 10. Although your actual costs may be higher or lower, based on these assumptions your costs would be:

| (if not redeemed) | ||||

| Class | A | C | C | Inst. |

| 1 year | $530 | $160 | $260 | $58 |

| 3 years | $737 | $534 | $534 | $222 |

| 5 years | $961 | $932 | $932 | $399 |

| 10 years | $1,604 | $2,048 | $2,048 | $913 |

Portfolio turnover

The Fund pays transaction costs, such as commissions, when it buys and sells securities (or "turns over" its portfolio). A higher portfolio turnover rate may indicate higher transaction costs and may result in higher taxes when Fund shares are held in a taxable account. These costs, which are not reflected in the annual fund operating expenses or in the example, affect the Fund's performance. During the most recent fiscal year, the Fund's portfolio turnover rate was 13% of the average value of its portfolio.

What are the Fund's principal investment strategies?

Under normal circumstances, the Fund will invest at least 80% of its net assets, plus the amount of any borrowings for investment purposes, in municipal securities the income from which is exempt from federal income tax, including the federal alternative minimum tax, and from California state personal income taxes. This is a fundamental investment policy that may not be changed without prior shareholder approval.

Municipal debt obligations are issued by state and local governments to raise funds for various public purposes such as hospitals, schools, and general capital expenses. Municipal debt obligations may also include securities issued by U.S. territories and possessions (such as the Commonwealth of Puerto Rico, Guam, and the U.S. Virgin Islands) to the extent that these securities are also exempt from federal income tax and California state personal income taxes. The Fund will invest its assets in securities with maturities of various lengths, depending on market conditions. The investment manager will adjust the average maturity of the bonds in the portfolio to attempt to provide a high level of tax-exempt income consistent with preservation of capital. The Fund's income level will vary depending on current interest rates and the specific securities in the portfolio. The Fund may concentrate its investments in certain types of bonds or in a certain segment of the municipal bond market when the supply of bonds in other sectors does not suit its investment needs. The Fund may invest in insured municipal bonds. The Fund will generally have a dollar-weighted average effective maturity of between 5 and 30 years.

What are the principal risks of investing in the Fund?

Investing in any mutual fund involves the risk that you may lose part or all of the money you invest. Over time, the value of your investment in the Fund will increase and decrease according to changes in the value of the securities in the Fund's portfolio. Principal risks include:

Investments not guaranteed by Delaware Management Company (Manager) or its affiliates — Investments in the Fund are not and will not be deposits with or liabilities of Macquarie Bank Limited ABN 46 008 583 542 and its holding companies, including their subsidiaries or related companies (Macquarie Group), and are subject to investment risk, including possible delays in repayment and loss of income and capital invested. No Macquarie Group company guarantees or will guarantee the performance of the Fund, the repayment of capital from the Fund, or any particular rate of return.

Market risk — The risk that all or a majority of the securities in a certain market — such as the stock or bond market — will decline in value because of factors such as adverse political or economic conditions, future expectations, investor confidence, or heavy institutional selling.

Interest rate risk — The risk that securities will decrease in value if interest rates rise. This risk is generally associated with bonds.

Credit risk — The risk that an issuer of a debt security, including a governmental issuer or an entity that insures a bond, may be unable to make interest payments and repay principal in a timely manner.

High yield (junk bond) risk — The risk that high yield securities, commonly known as "junk bonds," are subject to reduced creditworthiness of issuers; increased risk of default and a more limited and less liquid secondary market; and greater price volatility and risk of loss of income and principal than are higher-rated securities. High yield bonds are sometimes issued by municipalities with less financial strength and therefore have less ability to make projected debt payments on the bonds.

Call risk — The risk that a bond issuer will prepay the bond during periods of low interest rates, forcing a fund to reinvest that money at interest rates that might be lower than rates on the called bond.

Liquidity risk — The possibility that securities cannot be readily sold within seven days at approximately the price at which a portfolio

has

valued them.

Geographic concentration risk — The risk that heightened sensitivity to regional, state, U.S. territories or possessions (such as the Commonwealth of Puerto Rico, Guam, or the U.S. Virgin Islands), and local political and economic conditions could adversely affect the holdings in and performance of a fund. There is also the risk that there could be an inadequate supply of municipal bonds in a particular state or U.S. territory or possession.

Alternative minimum tax risk — If a fund invests in bonds whose income is subject to the alternative minimum tax, that portion of the fund's distributions would be taxable for shareholders who are subject to this tax.

Government and regulatory risk — The risk that governments or regulatory authorities have, from time to time, taken or considered actions that could adversely affect various sectors of the securities markets and significantly affect fund performance. For example, a tax-exempt security may be reclassified by the Internal Revenue Service or a state tax authority as taxable, and/or future legislative, administrative, or court actions could cause interest from a tax-exempt security to become taxable, possibly retroactively.

How has Delaware Tax-Free California Fund performed?

The bar chart and table below provide some indication of the risks of investing in the Fund by showing changes in the Fund's performance from year to year and by showing how the Fund's average annual total returns for the 1-, 5-, and 10-year or lifetime periods compare with those of a broad measure of market performance. The Fund's past performance (before and after taxes) is not necessarily an indication of how it will perform in the future. The returns reflect any expense caps in effect during these periods. The returns would be lower without the expense caps. You may obtain the Fund's most recently available month-end performance by calling 800 523-1918 or by visiting our website at delawareinvestments.com/performance.

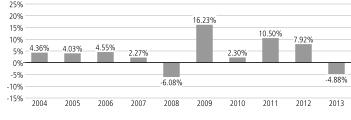

Year-by-year total return (Class A)

|

|

As of Sept. 30, 2014, the Fund's Class A shares had a calendar year-to-date return of 10.29%. During the periods illustrated

in this bar chart, Class A's highest quarterly return was 12.14% for the quarter ended Sept. 30, 2009 and its lowest quarterly

return was -5.79% for the quarter ended

Dec. 31, 2010. The maximum Class A sales charge of 4.50%, which is normally deducted when you purchase shares, is not reflected

in the highest/lowest quarterly returns or in the bar chart. If this fee were included, the returns would be less than those

shown. The average annual total returns in the table below do include the sales charge.

Average annual total returns for periods ended December 31, 2013

| 1 year | 5 years | 10 years or lifetime | |

| Class A return before taxes | -9.30% | 6.42% | 3.95% |

| Class A return after taxes on distributions | -9.30% | 6.42% | 3.95% |

| Class A return after taxes on distributions and sale of Fund shares | -3.79% | 6.01% | 3.99% |

| Class C return before taxes | -6.64% | 6.62% | 3.66% |

| Institutional Class return before taxes (lifetime: 12/31/13–12/31/13)* | — | — | 0.09% |

| Barclays Municipal Bond Index (reflects no deduction for fees, expenses, or taxes) | -2.55% | 5.89% | 4.29% |

* Institutional Class shares commenced operations on Dec. 31, 2013. The returns shown have not been annualized.

After-tax performance is presented only for Class A shares of the Fund. The after-tax returns for other Fund classes may vary. Actual after-tax returns depend on the investor's individual tax situation and may differ from the returns shown. After-tax returns are not relevant for shares held in tax-deferred investment vehicles such as employer-sponsored 401(k) plans and individual retirement accounts (IRAs). The after-tax returns shown are calculated using the highest individual federal marginal income tax rates in effect during the periods presented and do not reflect the impact of state and local taxes.

Who manages the Fund?

Investment manager

Delaware Management Company, a series of Delaware Management Business Trust

|

Portfolio managers |

Title with Delaware Management Company |

Start date on the Fund |

|

Joseph R. Baxter |

Senior Vice President, Head of Municipal Bond Department, Senior Portfolio Manager |

April 2004 |

|

Stephen J. Czepiel |

Senior Vice President, Senior Portfolio Manager |

July 2007 |

|

Gregory A. Gizzi |

Senior Vice President, Senior Portfolio Manager |

December 2012 |

Purchase and redemption of Fund shares

You may purchase or redeem shares of the Fund on any day that the New York Stock Exchange (NYSE) is open for business (Business

Day). Shares may be purchased or redeemed: through your financial advisor; through the Fund's website at delawareinvestments.com;

by calling 800 523-1918; by regular mail (c/o Delaware Investments, P.O. Box 9876, Providence, RI 02940-8076); by overnight

courier service (c/o Delaware Service Center,

4400 Computer Drive, Westborough, MA 01581-1722); or by wire.

For Class A and Class C shares, the minimum initial investment is generally $1,000 and subsequent investments can be made for as little as $100. For Institutional Class shares (except those shares purchased through an automatic investment plan), there is no minimum initial purchase requirement, but certain eligibility requirements must be met. The eligibility requirements are described in the prospectus under "Choosing a share class" and on the Fund's website. We may reduce or waive the minimums or eligibility requirements in certain cases.

Tax information

The Fund's distributions primarily are exempt from regular federal and state income taxes for residents of California. A portion of these distributions, however, may be subject to the federal alternative minimum tax. The Fund may also make distributions that are taxable to you as ordinary income or capital gains.

Payments to broker/dealers and other financial intermediaries

If you purchase shares of the Fund through a broker/dealer or other financial intermediary (such as a bank), the Fund and its related companies may pay the intermediary for the sale of Fund shares and related services. These payments may create a conflict of interest by influencing the broker/dealer or other intermediary and your salesperson to recommend the Fund over another investment. Ask your salesperson or visit your financial intermediary's website for more information.

Delaware Tax-Free Colorado Fund

What is the Fund's investment objective?

Delaware Tax-Free Colorado Fund seeks as high a level of current income exempt from federal income tax and from the personal income tax in Colorado as is consistent with preservation of capital.

What are the Fund's fees and expenses?

The following table describes the fees and expenses that you may pay if you buy and hold shares of the Fund. You may qualify for sales-charge discounts if you and your family invest, or agree to invest in the future, at least $100,000 in Delaware Investments® Funds. More information about these and other discounts is available from your financial advisor, in the Fund's prospectus under the section entitled "About your account," and in the Fund's statement of additional information (SAI) under the section entitled "Purchasing Shares."

| Shareholder fees (fees paid directly from your investment) | |||||

| Class | A | C | Inst. | ||

| Maximum sales charge (load) imposed on purchases as a percentage of offering price |

4.50% | none | none | ||

| Maximum contingent deferred sales charge (load) as a percentage of original purchase price or redemption price, whichever is lower | none | 1.00%1 | none | ||

| Annual fund operating expenses (expenses that you pay each year as a percentage of the value of your investment) | |||||

| Class | A | C | Inst. | ||

| Management fees | 0.55% | 0.55% | 0.55% | ||

| Distribution and service (12b-1) fees | 0.25% | 1.00% | none | ||

| Other expenses | 0.17% | 0.17% | 0.17% | ||

| Total annual fund operating expenses | 0.97% | 1.72% | 0.72% | ||

| Fee waivers and expense reimbursements | (0.13%)2 | (0.13%)2 | (0.13%)2 | ||

| Total annual fund operating expenses after fee waivers and expense reimbursements |

0.84% | 1.59% | 0.59% | ||

| 1 |

Class C shares redeemed within one year of purchase are subject to a 1.00% contingent deferred sales charge (CDSC). |

| 2 |

The Fund's investment manager, Delaware Management Company (Manager), has contractually agreed to waive all or a portion of its investment advisory fees and/or pay/reimburse expenses (excluding any 12b-1 fees, acquired fund fees and expenses, taxes, interest, inverse floater program expenses, short sale and dividend interest expenses, brokerage fees, certain insurance costs, and nonroutine expenses or costs, including, but not limited to, those relating to reorganizations, litigation, conducting shareholder meetings, and liquidations) in order to prevent total annual fund operating expenses from exceeding 0.59% of the Fund's average daily net assets from Dec. 29, 2014 through Dec. 29, 2015. These waivers and reimbursements may only be terminated by agreement of the Manager and the Fund. |

Example

This example is intended to help you compare the cost of investing in the Fund with the cost of investing in other mutual

funds. The example assumes that you invest $10,000 in the Fund for the time periods indicated and then redeem all of your

shares at the end of those periods. The example also assumes that your investment has a 5% return each year and reflects the

Manager's expense waivers and reimbursements for the 1-year contractual period and the total operating expenses without waivers

for years 2 through 10. Although your actual costs may be higher or lower, based on these assumptions your costs would be:

| (if not redeemed) | ||||

| Class | A | C | C | Inst |

| 1 year | $532 | $162 | $262 | $60 |

| 3 years | $733 | $529 | $529 | $217 |

| 5 years | $950 | $921 | $921 | $388 |

| 10 years | $1,575 | $2,019 | $2,019 | $882 |

Portfolio turnover

The Fund pays transaction costs, such as commissions, when it buys and sells securities (or "turns over" its portfolio). A higher portfolio turnover rate may indicate higher transaction costs and may result in higher taxes when Fund shares are held in a taxable account. These costs, which are not reflected in the annual fund operating expenses or in the example, affect the Fund's performance. During the most recent fiscal year, the Fund's portfolio turnover rate was 22% of the average value of its portfolio.

What are the Fund's principal investment strategies?

Under normal circumstances, the Fund will invest at least 80% of its net assets, plus the amount of any borrowings for investment purposes, in municipal securities the income from which is exempt from federal income tax, including the federal alternative minimum tax, and from Colorado state personal income taxes. This is a fundamental investment policy that may not be changed without prior shareholder approval.

Municipal debt obligations are issued by state and local governments to raise funds for various public purposes such as hospitals, schools, and general capital expenses. Municipal debt obligations may also include securities issued by U.S. territories and possessions (such as the Commonwealth of Puerto Rico, Guam, and the U.S. Virgin Islands) to the extent that these securities are also exempt from federal income tax and Colorado state personal income taxes. The Fund will invest its assets in securities with maturities of various lengths, depending on market conditions. The investment manager will adjust the average maturity of the bonds in the portfolio to attempt to provide a high level of tax-exempt income consistent with preservation of capital. The Fund's income level will vary depending on current interest rates and the specific securities in the portfolio. The Fund may concentrate its investments in certain types of bonds or in a certain segment of the municipal bond market when the supply of bonds in other sectors does not suit its investment needs. The Fund may invest in insured municipal bonds. The Fund will generally have a dollar-weighted average effective maturity of between 5 and 30 years.

What are the principal risks of investing in the Fund?

Investing in any mutual fund involves the risk that you may lose part or all of the money you invest. Over time, the value of your investment in the Fund will increase and decrease according to changes in the value of the securities in the Fund's portfolio. Principal risks include:

Investments not guaranteed by Delaware Management Company (Manager) or its affiliates — Investments in the Fund are not and will not be deposits with or liabilities of Macquarie Bank Limited ABN 46 008 583 542 and its holding companies, including their subsidiaries or related companies (Macquarie Group), and are subject to investment risk, including possible delays in repayment and loss of income and capital invested. No Macquarie Group company guarantees or will guarantee the performance of the Fund, the repayment of capital from the Fund, or any particular rate of return.

Market risk — The risk that all or a majority of the securities in a certain market — such as the stock or bond market — will decline in value because of factors such as adverse political or economic conditions, future expectations, investor confidence, or heavy institutional selling.

Interest rate risk — The risk that securities will decrease in value if interest rates rise. This risk is generally associated with bonds.

Credit risk — The risk that an issuer of a debt security, including a governmental issuer or an entity that insures a bond, may be unable to make interest payments and repay principal in a timely manner.

High yield (junk bond) risk — The risk that high yield securities, commonly known as "junk bonds," are subject to reduced creditworthiness of issuers; increased risk of default and a more limited and less liquid secondary market; and greater price volatility and risk of loss of income and principal than are higher-rated securities. High yield bonds are sometimes issued by municipalities with less financial strength and therefore have less ability to make projected debt payments on the bonds.

Call risk — The risk that a bond issuer will prepay the bond during periods of low interest rates, forcing a fund to reinvest that money at interest rates that might be lower than rates on the called bond.

Liquidity risk — The possibility that securities cannot be readily sold within seven days at approximately the price at which a portfolio

has

valued them.

Geographic concentration risk — The risk that heightened sensitivity to regional, state, U.S. territories or possessions (such as the Commonwealth of Puerto Rico, Guam, or the U.S. Virgin Islands), and local political and economic conditions could adversely affect the holdings in and performance of a fund. There is also the risk that there could be an inadequate supply of municipal bonds in a particular state or U.S. territory or possession.

Alternative minimum tax risk — If a fund invests in bonds whose income is subject to the alternative minimum tax, that portion of the fund's distributions would be taxable for shareholders who are subject to this tax.

Government and regulatory risk — The risk that governments or regulatory authorities have, from time to time, taken or considered actions that could adversely affect various sectors of the securities markets and significantly affect fund performance. For example, a tax-exempt security may be reclassified by the Internal Revenue Service or a state tax authority as taxable, and/or future legislative, administrative, or court actions could cause interest from a tax-exempt security to become taxable, possibly retroactively.

How has Delaware Tax-Free Colorado Fund performed?

The bar chart and table below provide some indication of the risks of investing in the Fund by showing changes in the Fund's performance from year to year and by showing how the Fund's average annual total returns for the 1-, 5-, and 10-year or lifetime periods compare with those of a broad measure of market performance. The Fund's past performance (before and after taxes) is not necessarily an indication of how it will perform in the future. The returns reflect any expense caps in effect during these periods. The returns would be lower without the expense caps. You may obtain the Fund's most recently available month-end performance by calling 800 523-1918 or by visiting our website at delawareinvestments.com/performance.

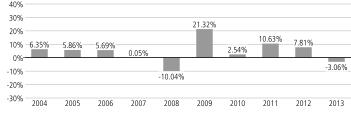

Year-by-year total return (Class A)

|

|

As of Sept. 30, 2014, the Fund's Class A shares had a calendar year-to-date return of 9.72%. During the periods illustrated in this bar chart, Class A's highest quarterly return was 8.43% for the quarter ended Sept. 30, 2009 and its lowest quarterly return was -4.97% for the quarter ended Dec. 31, 2010. The maximum Class A sales charge of 4.50%, which is normally deducted when you purchase shares, is not reflected in the highest/lowest quarterly returns or in the bar chart. If this fee were included, the returns would be less than those shown. The average annual total returns in the table below do include the sales charge.

Average annual total returns for periods ended December 31, 2013

| 1 year | 5 years | 10 years or lifetime | |

| Class A return before taxes | -9.67% | 4.57% | 3.28% |

| Class A return after taxes on distributions | -9.67% | 4.57% | 3.28% |

| Class A return after taxes on distributions and sale of Fund shares | -4.00% | 4.51% | 3.47% |

| Class C return before taxes | -6.98% | 4.76% | 2.99% |

| Institutional Class return before taxes (lifetime: 12/31/13–12/31/13)* | — | — | 0.09% |

| Barclays Municipal Bond Index (reflects no deduction for fees, expenses, or taxes) | -2.55% | 5.89% | 4.29% |

* Institutional Class shares commenced operations on Dec. 31, 2013. The returns shown have not been annualized.

After-tax performance is presented only for Class A shares of the Fund. The after-tax returns for other Fund classes may vary. Actual after-tax returns depend on the investor's individual tax situation and may differ from the returns shown. After-tax returns are not relevant for shares held in tax-deferred investment vehicles such as employer-sponsored 401(k) plans and individual retirement accounts (IRAs). The after-tax returns shown are calculated using the highest individual federal marginal income tax rates in effect during the periods presented and do not reflect the impact of state and local taxes.

Who manages the Fund?

Investment manager

Delaware Management Company, a series of Delaware Management Business Trust

|

Portfolio managers |

Title with Delaware Management Company |

Start date on the Fund |

|

Joseph R. Baxter |

Senior Vice President, Head of Municipal Bond Department, Senior Portfolio Manager |

April 2004 |

|

Stephen J. Czepiel |

Senior Vice President, Senior Portfolio Manager |

July 2007 |

|

Gregory A. Gizzi |

Senior Vice President, Senior Portfolio Manager |

December 2012 |

Purchase and redemption of Fund shares

You may purchase or redeem shares of the Fund on any day that the New York Stock Exchange (NYSE) is open for business (Business

Day). Shares may be purchased or redeemed: through your financial advisor; through the Fund's website at delawareinvestments.com;

by calling 800 523-1918; by regular mail (c/o Delaware Investments, P.O. Box 9876, Providence, RI 02940-8076); by overnight

courier service (c/o Delaware Service Center,

4400 Computer Drive, Westborough, MA 01581-1722); or by wire.

For Class A and Class C shares, the minimum initial investment is generally $1,000 and subsequent investments can be made for as little as $100. For Institutional Class shares (except those shares purchased through an automatic investment plan), there is no minimum initial purchase requirement, but certain eligibility requirements must be met. The eligibility requirements are described in the prospectus under "Choosing a share class" and on the Fund's website. We may reduce or waive the minimums or eligibility requirements in certain cases.

Tax information

The Fund's distributions primarily are exempt from regular federal and state income taxes for residents of Colorado. A portion of these distributions, however, may be subject to the federal alternative minimum tax. The Fund may also make distributions that are taxable to you as ordinary income or capital gains.

Payments to broker/dealers and other financial intermediaries

If you purchase shares of the Fund through a broker/dealer or other financial intermediary (such as a bank), the Fund and its related companies may pay the intermediary for the sale of Fund shares and related services. These payments may create a conflict of interest by influencing the broker/dealer or other intermediary and your salesperson to recommend the Fund over another investment. Ask your salesperson or visit your financial intermediary's website for more information.

What is the Fund's investment objective?

Delaware Tax-Free Idaho Fund seeks as high a level of current income exempt from federal income tax and from Idaho personal income taxes as is consistent with preservation of capital.

What are the Fund's fees and expenses?

The following table describes the fees and expenses that you may pay if you buy and hold shares of the Fund. You may qualify for sales-charge discounts if you and your family invest, or agree to invest in the future, at least $100,000 in Delaware Investments® Funds. More information about these and other discounts is available from your financial advisor, in the Fund's prospectus under the section entitled "About your account," and in the Fund's statement of additional information (SAI) under the section entitled "Purchasing Shares."

| Shareholder fees (fees paid directly from your investment) | |||||

| Class | A | C | Inst. | ||

| Maximum sales charge (load) imposed on purchases as a percentage of offering price |

4.50% | none | none | ||

| Maximum contingent deferred sales charge (load) as a percentage of original purchase price or redemption price, whichever is lower | none | 1.00%1 | none | ||

| Annual fund operating expenses (expenses that you pay each year as a percentage of the value of your investment) | |||||

| Class | A | C | Inst. | ||

| Management fees | 0.55% | 0.55% | 0.55% | ||

| Distribution and service (12b-1) fees | 0.25% | 1.00% | none | ||

| Other expenses | 0.19% | 0.19% | 0.19% | ||

| Total annual fund operating expenses | 0.99% | 1.74% | 0.74% | ||

| Fee waivers and expense reimbursements | (0.13%)2 | (0.13%)2 | (0.13%)2 | ||

| Total annual fund operating expenses after fee waivers and expense reimbursements |

0.86% | 1.61% | 0.61% | ||

| 1 |

Class C shares redeemed within one year of purchase are subject to a 1.00% contingent deferred sales charge (CDSC). |

| 2 |

The Fund's investment manager, Delaware Management Company (Manager), has contractually agreed to waive all or a portion of its investment advisory fees and/or pay/reimburse expenses (excluding any 12b-1 fees, acquired fund fees and expenses, taxes, interest, inverse floater program expenses, short sale and dividend interest expenses, brokerage fees, certain insurance costs, and nonroutine expenses or costs, including, but not limited to, those relating to reorganizations, litigation, conducting shareholder meetings, and liquidations) in order to prevent total annual fund operating expenses from exceeding 0.61% of the Fund's average daily net assets from Dec. 29, 2014 through Dec. 29, 2015. These waivers and reimbursements may only be terminated by agreement of the Manager and the Fund. |

Example

This example is intended to help you compare the cost of investing in the Fund with the cost of investing in other mutual

funds. The example assumes that you invest $10,000 in the Fund for the time periods indicated and then redeem all of your

shares at the end of those periods. The example also assumes that your investment has a 5% return each year and reflects the

Manager's expense waivers and reimbursements for the 1-year contractual period and the total operating expenses without waivers

for years 2 through 10. Although your actual costs may be higher or lower, based on these assumptions your costs would be:

| (if not redeemed) | ||||

| Class | A | C | C | Inst. |

| 1 year | $534 | $164 | $264 | $62 |

| 3 years | $739 | $535 | $535 | $223 |

| 5 years | $960 | $932 | $932 | $399 |

| 10 years | $1,597 | $2,041 | $2,041 | $906 |

Portfolio turnover

The Fund pays transaction costs, such as commissions, when it buys and sells securities (or "turns over" its portfolio). A higher portfolio turnover rate may indicate higher transaction costs and may result in higher taxes when Fund shares are held in a taxable account. These costs, which are not reflected in the annual fund operating expenses or in the example, affect the Fund's performance. During the most recent fiscal year, the Fund's portfolio turnover rate was 16% of the average value of its portfolio.

What are the Fund's principal investment strategies?

Under normal circumstances, the Fund will invest at least 80% of its net assets, plus the amount of any borrowings for investment purposes, in municipal securities the income from which is exempt from federal income tax, including the federal alternative minimum tax, and from Idaho state personal income taxes. This is a fundamental investment policy that may not be changed without prior shareholder approval.

Municipal debt obligations are issued by state and local governments to raise funds for various public purposes such as hospitals, schools, and general capital expenses. Municipal debt obligations may also include securities issued by U.S. territories and possessions (such as the Commonwealth of Puerto Rico, Guam, and the U.S. Virgin Islands) to the extent that these securities are also exempt from federal income tax and Idaho state personal income taxes. The Fund will invest its assets in securities with maturities of various lengths, depending on market conditions. The investment manager will adjust the average maturity of the bonds in the portfolio to attempt to provide a high level of tax-exempt income consistent with preservation of capital. The Fund's income level will vary depending on current interest rates and the specific securities in the portfolio. The Fund may concentrate its investments in certain types of bonds or in a certain segment of the municipal bond market when the supply of bonds in other sectors does not suit its investment needs. The Fund may invest in insured municipal bonds. The Fund will generally have a dollar-weighted average effective maturity of between 5 and 30 years.

What are the principal risks of investing in the Fund?

Investing in any mutual fund involves the risk that you may lose part or all of the money you invest. Over time, the value of your investment in the Fund will increase and decrease according to changes in the value of the securities in the Fund's portfolio. Principal risks include:

Investments not guaranteed by Delaware Management Company (Manager) or its affiliates — Investments in the Fund are not and will not be deposits with or liabilities of Macquarie Bank Limited ABN 46 008 583 542 and its holding companies, including their subsidiaries or related companies (Macquarie Group), and are subject to investment risk, including possible delays in repayment and loss of income and capital invested. No Macquarie Group company guarantees or will guarantee the performance of the Fund, the repayment of capital from the Fund, or any particular rate of return.

Market risk — The risk that all or a majority of the securities in a certain market — such as the stock or bond market — will decline in value because of factors such as adverse political or economic conditions, future expectations, investor confidence, or heavy institutional selling.

Interest rate risk — The risk that securities will decrease in value if interest rates rise. This risk is generally associated with bonds.

Credit risk — The risk that an issuer of a debt security, including a governmental issuer or an entity that insures a bond, may be unable to make interest payments and repay principal in a timely manner.

High yield (junk bond) risk — The risk that high yield securities, commonly known as "junk bonds," are subject to reduced creditworthiness of issuers; increased risk of default and a more limited and less liquid secondary market; and greater price volatility and risk of loss of income and principal than are higher-rated securities. High yield bonds are sometimes issued by municipalities with less financial strength and therefore have less ability to make projected debt payments on the bonds.

Call risk — The risk that a bond issuer will prepay the bond during periods of low interest rates, forcing a fund to reinvest that money at interest rates that might be lower than rates on the called bond.

Liquidity risk — The possibility that securities cannot be readily sold within seven days at approximately the price at which a portfolio

has

valued them.

Geographic concentration risk — The risk that heightened sensitivity to regional, state, U.S. territories or possessions (such as the Commonwealth of Puerto Rico, Guam, or the U.S. Virgin Islands), and local political and economic conditions could adversely affect the holdings in and performance of a fund. There is also the risk that there could be an inadequate supply of municipal bonds in a particular state or U.S. territory or possession.

Alternative minimum tax risk — If a fund invests in bonds whose income is subject to the alternative minimum tax, that portion of the fund's distributions would be taxable for shareholders who are subject to this tax.

Government and regulatory risk — The risk that governments or regulatory authorities have, from time to time, taken or considered actions that could adversely affect various sectors of the securities markets and significantly affect fund performance. For example, a tax-exempt security may be reclassified by the Internal Revenue Service or a state tax authority as taxable, and/or future legislative, administrative, or court actions could cause interest from a tax-exempt security to become taxable, possibly retroactively.

How has Delaware Tax-Free Idaho Fund performed?

The bar chart and table below provide some indication of the risks of investing in the Fund by showing changes in the Fund's performance from year to year and by showing how the Fund's average annual total returns for the 1-, 5-, and 10-year or lifetime periods compare with those of a broad measure of market performance. The Fund's past performance (before and after taxes) is not necessarily an indication of how it will perform in the future. The returns reflect any expense caps in effect during these periods. The returns would be lower without the expense caps. You may obtain the Fund's most recently available month-end performance by calling 800 523-1918 or by visiting our website at delawareinvestments.com/performance.

Year-by-year total return (Class A)

|

|

As of Sept. 30, 2014, the Fund's Class A shares had a calendar year-to-date return of 6.76%. During the periods illustrated in this bar chart, Class A's highest quarterly return was 7.07% for the quarter ended Sept. 30, 2009 and its lowest quarterly return was -4.60% for the quarter ended Dec. 31, 2010. The maximum Class A sales charge of 4.50%, which is normally deducted when you purchase shares, is not reflected in the highest/lowest quarterly returns or in the bar chart. If this fee were included, the returns would be less than those shown. The average annual total returns in the table below do include the sales charge.

Average annual total returns for periods ended December 31, 2013

| 1 year | 5 years | 10 years or lifetime | |

| Class A return before taxes | -9.45% | 3.60% | 3.01% |

| Class A return after taxes on distributions | -9.45% | 3.59% | 3.01% |

| Class A return after taxes on distributions and sale of Fund shares | -3.94% | 3.67% | 3.19% |

| Class C return before taxes | -6.81% | 3.75% | 2.71% |

| Institutional Class return before taxes (lifetime: 12/31/13–12/31/13)* | — | — | 0.09% |

| Barclays Municipal Bond Index (reflects no deduction for fees, expenses, or taxes) | -2.55% | 5.89% | 4.29% |

* Institutional Class shares commenced operations on Dec. 31, 2013. The returns shown have not been annualized.

After-tax performance is presented only for Class A shares of the Fund. The after-tax returns for other Fund classes may vary. Actual after-tax returns depend on the investor's individual tax situation and may differ from the returns shown. After-tax returns are not relevant for shares held in tax-deferred investment vehicles such as employer-sponsored 401(k) plans and individual retirement accounts (IRAs). The after-tax returns shown are calculated using the highest individual federal marginal income tax rates in effect during the periods presented and do not reflect the impact of state and local taxes.

Who manages the Fund?

Investment manager

Delaware Management Company, a series of Delaware Management Business Trust

|

Portfolio managers |

Title with Delaware Management Company |

Start date on the Fund |

|

Joseph R. Baxter |

Senior Vice President, Head of Municipal Bond Department, Senior Portfolio Manager |

May 2003 |

|

Stephen J. Czepiel |

Senior Vice President, Senior Portfolio Manager |

July 2007 |

|

Gregory A. Gizzi |

Senior Vice President, Senior Portfolio Manager |

December 2012 |

Purchase and redemption of Fund shares

You may purchase or redeem shares of the Fund on any day that the New York Stock Exchange (NYSE) is open for business (Business

Day). Shares may be purchased or redeemed: through your financial advisor; through the Fund's website at delawareinvestments.com;

by calling 800 523-1918; by regular mail (c/o Delaware Investments, P.O. Box 9876, Providence, RI 02940-8076); by overnight

courier service (c/o Delaware Service Center,

4400 Computer Drive, Westborough, MA 01581-1722); or by wire.

For Class A and Class C shares, the minimum initial investment is generally $1,000 and subsequent investments can be made for as little as $100. For Institutional Class shares (except those shares purchased through an automatic investment plan), there is no minimum initial purchase requirement, but certain eligibility requirements must be met. The eligibility requirements are described in the prospectus under "Choosing a share class" and on the Fund's website. We may reduce or waive the minimums or eligibility requirements in certain cases.

Tax information

The Fund's distributions primarily are exempt from regular federal and state income taxes for residents of Idaho. A portion of these distributions, however, may be subject to the federal alternative minimum tax. The Fund may also make distributions that are taxable to you as ordinary income or capital gains.

Payments to broker/dealers and other financial intermediaries

If you purchase shares of the Fund through a broker/dealer or other financial intermediary (such as a bank), the Fund and its related companies may pay the intermediary for the sale of Fund shares and related services. These payments may create a conflict of interest by influencing the broker/dealer or other intermediary and your salesperson to recommend the Fund over another investment. Ask your salesperson or visit your financial intermediary's website for more information.

Delaware Tax-Free New York Fund

What is the Fund's investment objective?

Delaware Tax-Free New York Fund seeks as high a level of current income exempt from federal income tax and from New York state personal income taxes as is consistent with preservation of capital.

What are the Fund's fees and expenses?

The following table describes the fees and expenses that you may pay if you buy and hold shares of the Fund. You may qualify for sales-charge discounts if you and your family invest, or agree to invest in the future, at least $100,000 in Delaware Investments® Funds. More information about these and other discounts is available from your financial advisor, in the Fund's prospectus under the section entitled "About your account," and in the Fund's statement of additional information (SAI) under the section entitled "Purchasing Shares."

| Shareholder fees (fees paid directly from your investment) | |||||

| Class | A | C | Inst. | ||

| Maximum sales charge (load) imposed on purchases as a percentage of offering price |

4.50% | none | none | ||

| Maximum contingent deferred sales charge (load) as a percentage of original purchase price or redemption price, whichever is lower | none | 1.00%1 | none | ||

| Annual fund operating expenses (expenses that you pay each year as a percentage of the value of your investment) | |||||

| Class | A | C | Inst. | ||

| Management fees | 0.55% | 0.55% | 0.55% | ||

| Distribution and service (12b-1) fees | 0.25% | 1.00% | none | ||

| Other expenses | 0.26% | 0.26% | 0.26% | ||

| Total annual fund operating expenses | 1.06% | 1.81% | 0.81% | ||

| Fee waivers and expense reimbursements | (0.26%)2 | (0.26%)2 | (0.26%)2 | ||

| Total annual fund operating expenses after fee waivers and expense reimbursements |

0.80% | 1.55% | 0.55% | ||

| 1 |

Class C shares redeemed within one year of purchase are subject to a 1.00% contingent deferred sales charge (CDSC). |

| 2 |

The Fund's investment manager, Delaware Management Company (Manager), has contractually agreed to waive all or a portion of its investment advisory fees and/or pay/reimburse expenses (excluding any 12b-1 fees, acquired fund fees and expenses, taxes, interest, inverse floater program expenses, short sale and dividend interest expenses, brokerage fees, certain insurance costs, and nonroutine expenses or costs, including, but not limited to, those relating to reorganizations, litigation, conducting shareholder meetings, and liquidations) in order to prevent total annual fund operating expenses from exceeding 0.55% of the Fund's average daily net assets from Dec. 29, 2014 through Dec. 29, 2015. These waivers and reimbursements may only be terminated by agreement of the Manager and the Fund. |

Example

This example is intended to help you compare the cost of investing in the Fund with the cost of investing in other mutual

funds. The example assumes that you invest $10,000 in the Fund for the time periods indicated and then redeem all of your

shares at the end of those periods. The example also assumes that your investment has a 5% return each year and reflects the

Manager's expense waivers and reimbursements for the 1-year contractual period and the total operating expenses without waivers

for years 2 through 10. Although your actual costs may be higher or lower, based on these assumptions your costs would be:

| (if not redeemed) | ||||

| Class | A | C | C | Inst. |

| 1 year | $528 | $158 | $258 | $56 |

| 3 years | $747 | $544 | $544 | $233 |

| 5 years | $984 | $956 | $956 | $424 |

| 10 years | $1,663 | $2,105 | $2,105 | $977 |

Portfolio turnover

The Fund pays transaction costs, such as commissions, when it buys and sells securities (or "turns over" its portfolio). A higher portfolio turnover rate may indicate higher transaction costs and may result in higher taxes when Fund shares are held in a taxable account. These costs, which are not reflected in the annual fund operating expenses or in the example, affect the Fund's performance. During the most recent fiscal year, the Fund's portfolio turnover rate was 20% of the average value of its portfolio.

What are the Fund's principal investment strategies?

Under normal circumstances, the Fund will invest at least 80% of its net assets, plus the amount of any borrowings for investment purposes, in municipal securities the income from which is exempt from federal income tax, including the federal alternative minimum tax, and from New York state personal income taxes. This is a fundamental investment policy that may not be changed without prior shareholder approval.

Municipal debt obligations are issued by state and local governments to raise funds for various public purposes such as hospitals, schools, and general capital expenses. Municipal debt obligations may also include securities issued by U.S. territories and possessions (such as the Commonwealth of Puerto Rico, Guam, and the U.S. Virgin Islands) to the extent that these securities are also exempt from federal income tax and New York state personal income taxes. The Fund will invest its assets in securities with maturities of various lengths, depending on market conditions. The investment manager will adjust the average maturity of the bonds in the portfolio to attempt to provide a high level of tax-exempt income consistent with preservation of capital. The Fund's income level will vary depending on current interest rates and the specific securities in the portfolio. The Fund may concentrate its investments in certain types of bonds or in a certain segment of the municipal bond market when the supply of bonds in other sectors does not suit its investment needs. The Fund may invest in insured municipal bonds. The Fund will generally have a dollar-weighted average effective maturity of between 5 and 30 years.

What are the principal risks of investing in the Fund?

Investing in any mutual fund involves the risk that you may lose part or all of the money you invest. Over time, the value of your investment in the Fund will increase and decrease according to changes in the value of the securities in the Fund's portfolio. Principal risks include:

Investments not guaranteed by Delaware Management Company (Manager) or its affiliates — Investments in the Fund are not and will not be deposits with or liabilities of Macquarie Bank Limited ABN 46 008 583 542 and its holding companies, including their subsidiaries or related companies (Macquarie Group), and are subject to investment risk, including possible delays in repayment and loss of income and capital invested. No Macquarie Group company guarantees or will guarantee the performance of the Fund, the repayment of capital from the Fund, or any particular rate of return.

Market risk — The risk that all or a majority of the securities in a certain market — such as the stock or bond market — will decline in value because of factors such as adverse political or economic conditions, future expectations, investor confidence, or heavy institutional selling.

Interest rate risk — The risk that securities will decrease in value if interest rates rise. This risk is generally associated with bonds.

Credit risk — The risk that an issuer of a debt security, including a governmental issuer or an entity that insures a bond, may be unable to make interest payments and repay principal in a timely manner.

High yield (junk bond) risk — The risk that high yield securities, commonly known as "junk bonds," are subject to reduced creditworthiness of issuers; increased risk of default and a more limited and less liquid secondary market; and greater price volatility and risk of loss of income and principal than are higher-rated securities. High yield bonds are sometimes issued by municipalities with less financial strength and therefore have less ability to make projected debt payments on the bonds.

Call risk — The risk that a bond issuer will prepay the bond during periods of low interest rates, forcing a fund to reinvest that money at interest rates that might be lower than rates on the called bond.

Liquidity risk — The possibility that securities cannot be readily sold within seven days at approximately the price at which a portfolio

has

valued them.

Geographic concentration risk — The risk that heightened sensitivity to regional, state, U.S. territories or possessions (such as the Commonwealth of Puerto Rico, Guam, or the U.S. Virgin Islands), and local political and economic conditions could adversely affect the holdings in and performance of a fund. There is also the risk that there could be an inadequate supply of municipal bonds in a particular state or U.S. territory or possession.

Alternative minimum tax risk — If a fund invests in bonds whose income is subject to the alternative minimum tax, that portion of the fund's distributions would be taxable for shareholders who are subject to this tax.

Government and regulatory risk — The risk that governments or regulatory authorities have, from time to time, taken or considered actions that could adversely affect various sectors of the securities markets and significantly affect fund performance. For example, a tax-exempt security may be reclassified by the Internal Revenue Service or a state tax authority as taxable, and/or future legislative, administrative, or court actions could cause interest from a tax-exempt security to become taxable, possibly retroactively.

How has Delaware Tax-Free New York Fund performed?

The bar chart and table below provide some indication of the risks of investing in the Fund by showing changes in the Fund's performance from year to year and by showing how the Fund's average annual total returns for the 1-, 5-, and 10-year or lifetime periods compare with those of a broad measure of market performance. The Fund's past performance (before and after taxes) is not necessarily an indication of how it will perform in the future. The returns reflect any expense caps in effect during these periods. The returns would be lower without the expense caps. You may obtain the Fund's most recently available month-end performance by calling 800 523-1918 or by visiting our website at delawareinvestments.com/performance.

Year-by-year total return (Class A)

|

|

As of Sept. 30, 2014, the Fund's Class A shares had a calendar year-to-date return of 9.66%. During the periods illustrated in this bar chart, Class A's highest quarterly return was 8.61% for the quarter ended Sept. 30, 2009 and its lowest quarterly return was -5.10% for the quarter ended Dec. 31, 2010. The maximum Class A sales charge of 4.50%, which is normally deducted when you purchase shares, is not reflected in the highest/lowest quarterly returns or in the bar chart. If this fee were included, the returns would be less than those shown. The average annual total returns in the table below do include the sales charge.

Average annual total returns for periods ended December 31, 2013

| 1 year | 5 years | 10 years or lifetime | |

| Class A return before taxes | -9.77% | 4.98% | 3.77% |

| Class A return after taxes on distributions | -9.77% | 4.97% | 3.77% |

| Class A return after taxes on distributions and sale of Fund shares | -4.24% | 4.76% | 3.82% |

| Class C return before taxes | -7.09% | 5.17% | 3.47% |

| Institutional Class return before taxes (lifetime: 12/31/13–12/31/13)* | — | — | 0.09% |

| Barclays Municipal Bond Index (reflects no deduction for fees, expenses, or taxes) | -2.55% | 5.89% | 4.29% |

* Institutional Class shares commenced operations on Dec. 31, 2013. The returns shown have not been annualized.

After-tax performance is presented only for Class A shares of the Fund. The after-tax returns for other Fund classes may vary. Actual after-tax returns depend on the investor's individual tax situation and may differ from the returns shown. After-tax returns are not relevant for shares held in tax-deferred investment vehicles such as employer-sponsored 401(k) plans and individual retirement accounts (IRAs). The after-tax returns shown are calculated using the highest individual federal marginal income tax rates in effect during the periods presented and do not reflect the impact of state and local taxes.

Who manages the Fund?

Investment manager

Delaware Management Company, a series of Delaware Management Business Trust

|

Portfolio managers |

Title with Delaware Management Company |

Start date on the Fund |

|

Joseph R. Baxter |

Senior Vice President, Head of Municipal Bond Department, Senior Portfolio Manager |

May 2003 |

|

Stephen J. Czepiel |

Senior Vice President, Senior Portfolio Manager |

July 2007 |

|

Gregory A. Gizzi |

Senior Vice President, Senior Portfolio Manager |

December 2012 |

Purchase and redemption of Fund shares

You may purchase or redeem shares of the Fund on any day that the New York Stock Exchange (NYSE) is open for business (Business

Day). Shares may be purchased or redeemed: through your financial advisor; through the Fund's website at delawareinvestments.com;

by calling 800 523-1918; by regular mail (c/o Delaware Investments, P.O. Box 9876, Providence, RI 02940-8076); by overnight

courier service (c/o Delaware Service Center,

4400 Computer Drive, Westborough, MA 01581-1722); or by wire.

For Class A and Class C shares, the minimum initial investment is generally $1,000 and subsequent investments can be made for as little as $100. For Institutional Class shares (except those shares purchased through an automatic investment plan), there is no minimum initial purchase requirement, but certain eligibility requirements must be met. The eligibility requirements are described in the prospectus under "Choosing a share class" and on the Fund's website. We may reduce or waive the minimums or eligibility requirements in certain cases.

Tax information

The Fund's distributions primarily are exempt from regular federal and state income taxes for residents of New York. A portion of these distributions, however, may be subject to the federal alternative minimum tax. The Fund may also make distributions that are taxable to you as ordinary income or capital gains.

Payments to broker/dealers and other financial intermediaries

If you purchase shares of the Fund through a broker/dealer or other financial intermediary (such as a bank), the Fund and its related companies may pay the intermediary for the sale of Fund shares and related services. These payments may create a conflict of interest by influencing the broker/dealer or other intermediary and your salesperson to recommend the Fund over another investment. Ask your salesperson or visit your financial intermediary's website for more information.

Delaware Tax-Free Pennsylvania Fund

What is the Fund's investment objective?

Delaware Tax-Free Pennsylvania Fund seeks as high a level of current income exempt from federal income tax and from Pennsylvania state personal income tax as is consistent with preservation of capital.

What are the Fund's fees and expenses?

The following table describes the fees and expenses that you may pay if you buy and hold shares of the Fund. You may qualify for sales-charge discounts if you and your family invest, or agree to invest in the future, at least $100,000 in Delaware Investments® Funds. More information about these and other discounts is available from your financial advisor, in the Fund's prospectus under the section entitled "About your account," and in the Fund's statement of additional information (SAI) under the section entitled "Purchasing Shares."

| Shareholder fees (fees paid directly from your investment) | |||||

| Class | A | C | Inst. | ||

| Maximum sales charge (load) imposed on purchases as a percentage of offering price |

4.50% | none | none | ||

| Maximum contingent deferred sales charge (load) as a percentage of original purchase price or redemption price, whichever is lower |

none | 1.00%1 | none | ||

| Annual fund operating expenses (expenses that you pay each year as a percentage of the value of your investment) | |||||

| Class | A | C | Inst. | ||

| Management fees | 0.55% | 0.55% | 0.55% | ||