UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

| (Mark one) | ||||||||

| QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | ||||||||

For the quarterly period ended March 31, 2024

OR

| TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | ||||||||

| For the transition period from to | ||||||||

Commission file number: 1-8606

(Exact name of registrant as specified in its charter)

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |||||||

| (Address of principal executive offices) | (Zip Code) | ||||||||||

Registrant’s telephone number, including area code: (212 ) 395-1000

Securities registered pursuant to Section 12(b) of the Act:

| Title of Each Class | Trading Symbol(s) | Name of Each Exchange on Which Registered | ||||||||||||

Securities registered pursuant to Section 12(b) of the Act (continued):

| Title of Each Class | Trading Symbol(s) | Name of Each Exchange on Which Registered | ||||||||||||

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. ☒ Yes ☐ No

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). ☒ Yes ☐ No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of "large accelerated filer," "accelerated filer," "smaller reporting company," and "emerging growth company" in Rule 12b-2 of the Exchange Act. | |||||||||||||||||

| ☒ | Accelerated filer | ☐ | |||||||||||||||

Non-accelerated filer | ☐ | Smaller reporting company | |||||||||||||||

Emerging growth company | |||||||||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). ☐ Yes ☒ No

At March 31, 2024, 4,209,254,894 shares of the registrant’s common stock were outstanding, after deducting 82,178,752 shares held in treasury.

| TABLE OF CONTENTS | ||

| Item No. | Page | |||||||

| Item 1. | ||||||||

| Three months ended March 31, 2024 and 2023 | ||||||||

| Three months ended March 31, 2024 and 2023 | ||||||||

| At March 31, 2024 and December 31, 2023 | ||||||||

| Three months ended March 31, 2024 and 2023 | ||||||||

| Item 2. | ||||||||

| Item 3. | ||||||||

| Item 4. | ||||||||

| Item 1. | ||||||||

| Item 1A. | ||||||||

| Item 2. | ||||||||

| Item 5. | ||||||||

| Item 6. | ||||||||

| Part I - Financial Information | ||

| Item 1. Financial Statements (Unaudited) | ||

Condensed Consolidated Statements of Income | ||

Verizon Communications Inc. and Subsidiaries | ||

| Three Months Ended | |||||||||||

| March 31, | |||||||||||

| (dollars in millions, except per share amounts) (unaudited) | 2024 | 2023 | |||||||||

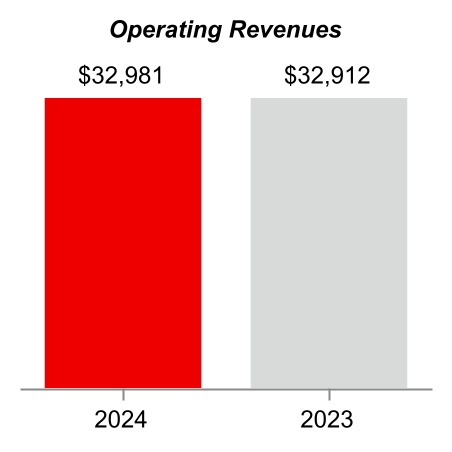

| Operating Revenues | |||||||||||

Service revenues and other | $ | $ | |||||||||

Wireless equipment revenues | |||||||||||

| Total Operating Revenues | |||||||||||

| Operating Expenses | |||||||||||

Cost of services (exclusive of items shown below) | |||||||||||

Cost of wireless equipment | |||||||||||

Selling, general and administrative expense | |||||||||||

Depreciation and amortization expense | |||||||||||

| Total Operating Expenses | |||||||||||

| Operating Income | |||||||||||

| Equity in earnings (losses) of unconsolidated businesses | ( | ||||||||||

| Other income, net | |||||||||||

| Interest expense | ( | ( | |||||||||

| Income Before Provision For Income Taxes | |||||||||||

| Provision for income taxes | ( | ( | |||||||||

| Net Income | $ | $ | |||||||||

| Net income attributable to noncontrolling interests | $ | $ | |||||||||

| Net income attributable to Verizon | |||||||||||

| Net Income | $ | $ | |||||||||

| Basic Earnings Per Common Share | |||||||||||

| Net income attributable to Verizon | $ | $ | |||||||||

| Weighted-average shares outstanding (in millions) | |||||||||||

| Diluted Earnings Per Common Share | |||||||||||

| Net income attributable to Verizon | $ | $ | |||||||||

| Weighted-average shares outstanding (in millions) | |||||||||||

See Notes to Condensed Consolidated Financial Statements

4

Condensed Consolidated Statements of Comprehensive Income | ||

| Verizon Communications Inc. and Subsidiaries | ||

| Three Months Ended | |||||||||||

| March 31, | |||||||||||

| (dollars in millions) (unaudited) | 2024 | 2023 | |||||||||

| Net Income | $ | $ | |||||||||

| Other Comprehensive Income (Loss), Net of Tax (Expense) Benefit | |||||||||||

Foreign currency translation adjustments, net of tax of $( | ( | ||||||||||

Unrealized gain on cash flow hedges, net of tax of $( | |||||||||||

Unrealized gain (loss) on fair value hedges, net of tax of $( | ( | ||||||||||

Unrealized gain (loss) on marketable securities, net of tax of $ | ( | ||||||||||

Defined benefit pension and postretirement plans, net of tax of $ | ( | ( | |||||||||

| Other comprehensive income (loss) attributable to Verizon | ( | ||||||||||

| Total Comprehensive Income | $ | $ | |||||||||

| Comprehensive income attributable to noncontrolling interests | $ | $ | |||||||||

| Comprehensive income attributable to Verizon | |||||||||||

| Total Comprehensive Income | $ | $ | |||||||||

See Notes to Condensed Consolidated Financial Statements

5

| Condensed Consolidated Balance Sheets | ||

| Verizon Communications Inc. and Subsidiaries | ||

| At March 31, | At December 31, | ||||||||||

| (dollars in millions, except per share amounts) (unaudited) | 2024 | 2023 | |||||||||

| Assets | |||||||||||

| Current assets | |||||||||||

Cash and cash equivalents | $ | $ | |||||||||

Accounts receivable | |||||||||||

Less Allowance for credit losses | |||||||||||

| Accounts receivable, net | |||||||||||

Inventories | |||||||||||

Prepaid expenses and other | |||||||||||

| Total current assets | |||||||||||

| Property, plant and equipment | |||||||||||

Less Accumulated depreciation | |||||||||||

| Property, plant and equipment, net | |||||||||||

| Investments in unconsolidated businesses | |||||||||||

| Wireless licenses | |||||||||||

| Goodwill | |||||||||||

| Other intangible assets, net | |||||||||||

| Operating lease right-of-use assets | |||||||||||

| Other assets | |||||||||||

| Total assets | $ | $ | |||||||||

| Liabilities and Equity | |||||||||||

| Current liabilities | |||||||||||

| Debt maturing within one year | $ | $ | |||||||||

| Accounts payable and accrued liabilities | |||||||||||

| Current operating lease liabilities | |||||||||||

| Other current liabilities | |||||||||||

| Total current liabilities | |||||||||||

| Long-term debt | |||||||||||

| Employee benefit obligations | |||||||||||

| Deferred income taxes | |||||||||||

| Non-current operating lease liabilities | |||||||||||

| Other liabilities | |||||||||||

| Total long-term liabilities | |||||||||||

| Commitments and Contingencies (Note 12) | |||||||||||

| Equity | |||||||||||

Series preferred stock ($ | |||||||||||

Common stock ($ | |||||||||||

| Additional paid in capital | |||||||||||

| Retained earnings | |||||||||||

| Accumulated other comprehensive loss | ( | ( | |||||||||

Common stock in treasury, at cost ( | ( | ( | |||||||||

| Deferred compensation – employee stock ownership plans (ESOPs) and other | |||||||||||

| Noncontrolling interests | |||||||||||

| Total equity | |||||||||||

| Total liabilities and equity | $ | $ | |||||||||

See Notes to Condensed Consolidated Financial Statements

6

| Condensed Consolidated Statements of Cash Flows | ||

| Verizon Communications Inc. and Subsidiaries | ||

| Three Months Ended | |||||||||||

| March 31, | |||||||||||

| (dollars in millions) (unaudited) | 2024 | 2023 | |||||||||

| Cash Flows from Operating Activities | |||||||||||

| Net Income | $ | $ | |||||||||

| Adjustments to reconcile net income to net cash provided by operating activities: | |||||||||||

| Depreciation and amortization expense | |||||||||||

| Employee retirement benefits | |||||||||||

| Deferred income taxes | |||||||||||

| Provision for expected credit losses | |||||||||||

| Equity in losses of unconsolidated businesses, net of dividends received | |||||||||||

| Changes in current assets and liabilities, net of effects from acquisition/disposition of businesses | ( | ( | |||||||||

| Other, net | ( | ( | |||||||||

| Net cash provided by operating activities | |||||||||||

| Cash Flows from Investing Activities | |||||||||||

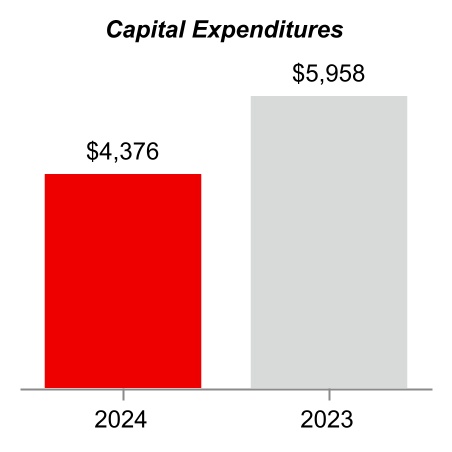

| Capital expenditures (including capitalized software) | ( | ( | |||||||||

| Acquisitions of wireless licenses | ( | ( | |||||||||

| Collateral receipts (payments) related to derivative contracts, net | ( | ||||||||||

| Other, net | |||||||||||

| Net cash used in investing activities | ( | ( | |||||||||

| Cash Flows from Financing Activities | |||||||||||

| Proceeds from long-term borrowings | |||||||||||

| Proceeds from asset-backed long-term borrowings | |||||||||||

| Net proceeds from short-term commercial paper | |||||||||||

| Repayments of long-term borrowings and finance lease obligations | ( | ( | |||||||||

| Repayments of asset-backed long-term borrowings | ( | ( | |||||||||

| Dividends paid | ( | ( | |||||||||

| Other, net | ( | ||||||||||

| Net cash used in financing activities | ( | ( | |||||||||

| Increase (decrease) in cash, cash equivalents and restricted cash | ( | ||||||||||

| Cash, cash equivalents and restricted cash, beginning of period | |||||||||||

| Cash, cash equivalents and restricted cash, end of period (Note 1) | $ | $ | |||||||||

See Notes to Condensed Consolidated Financial Statements

7

Notes to Condensed Consolidated Financial Statements (Unaudited) | ||

| Verizon Communications Inc. and Subsidiaries | ||

| Note 1. Basis of Presentation | ||

Verizon Communications Inc. (the Company) is a holding company that, acting through its subsidiaries (together with the Company, collectively, Verizon), is one of the world’s leading providers of communications, technology, information and entertainment products and services to consumers, businesses and government entities. With a presence around the world, we offer data, video and voice services and solutions on our networks and platforms that are designed to meet customers’ demand for mobility, reliable network connectivity and security.

The accompanying unaudited condensed consolidated financial statements have been prepared in accordance with generally accepted accounting principles (GAAP) in the United States (U.S.) and based upon Securities and Exchange Commission rules that permit reduced disclosure for interim periods. For a more complete discussion of significant accounting policies and certain other information, you should refer to the financial statements included in the Company's Annual Report on Form 10-K for the year ended December 31, 2023. These financial statements reflect all adjustments that are necessary for a fair presentation of results of operations and financial condition for the interim periods shown, including normal recurring accruals and other items. The results for the interim periods are not necessarily indicative of results for the full year.

Earnings Per Common Share

There were a total of approximately 3.7 million and 3.6 million outstanding dilutive securities, primarily consisting of performance stock units and restricted stock units, included in the computation of diluted earnings per common share for the three months ended March 31, 2024 and 2023, respectively.

Cash, Cash Equivalents and Restricted Cash

We consider all highly liquid investments with an original maturity of 90 days or less when purchased to be cash equivalents. Cash equivalents are stated at cost, which approximates quoted market value and includes amounts held in money market funds.

Cash, cash equivalents and restricted cash are included in the following line items in the condensed consolidated balance sheets:

| At March 31, | At December 31, | Increase | |||||||||||||||

(dollars in millions) | 2024 | 2023 | |||||||||||||||

| Cash and cash equivalents | $ | $ | $ | ||||||||||||||

| Restricted cash: | |||||||||||||||||

Prepaid expenses and other | |||||||||||||||||

Other assets | |||||||||||||||||

| Cash, cash equivalents and restricted cash | $ | $ | $ | ||||||||||||||

| Note 2. Revenues and Contract Costs | ||

We earn revenue from contracts with customers, primarily through the provision of telecommunications and other services and through the sale of wireless equipment.

Revenue by Category

We have two reportable segments that we operate and manage as strategic business units, Consumer and Business. Revenue is disaggregated by products and services within Consumer, and customer groups (Enterprise and Public Sector, Business Markets and Other, and Wholesale) within Business. See Note 10 for additional information on revenue by segment, including Corporate and other.

8

Remaining Performance Obligations

Additionally, certain contracts provide customers the option to purchase additional services. The fees related to these additional services are recognized when the customer exercises the option (typically on a month-to-month basis).

Contracts for wireless services, with or without promotional credits that require maintenance of service, are generally either month-to-month and cancellable at any time, or considered to contain terms ranging from greater than one month to up to thirty-six months (typically under a device payment plan), or contain terms ranging from greater than one month to up to twenty-four months (typically under a fixed-term plan). Additionally, customers may incur charges based on usage or additional optional services purchased in conjunction with entering into a contract that can be cancelled at any time and therefore are not included in the transaction price. The transaction price allocated to service performance obligations, which are not satisfied or are partially satisfied as of the end of the reporting period, are generally related to contracts that are not accounted for as month-to-month contracts.

Our Consumer group customers also include traditional wholesale resellers that purchase and resell wireless service under their own brands to their respective customers. Reseller arrangements generally include a stated contract term, which typically extends longer than two years and, in some cases, include a periodic minimum revenue commitment over the contract term for which revenues will be recognized in future periods.

Consumer customer contracts for wireline services are generally month-to-month; however, they may have a service term of two years or shorter than twelve months . Certain contracts with Business customers for wireline services extend into future periods, contain fixed monthly fees and usage-based fees, and can include annual commitments in each year of the contract or commitments over the entire specified contract term; however, a significant number of contracts for wireline services with our Business customers have a contract term that is twelve months or less.

Additionally, there are certain contracts with Business customers for wireline services that have a contractual minimum fee over the total contract term. We cannot predict the time period when revenue will be recognized related to those contracts; thus, they are excluded from the time bands below. These contracts have varying terms spanning over approximately twenty-nine years ending in September 2053 and have aggregate contract minimum payments totaling $2.0 billion.

At March 31, 2024, the transaction price related to unsatisfied performance obligations that are expected to be recognized for the remainder of 2024, 2025 and thereafter was $21.1 billion, $23.2 billion and $13.3 billion, respectively. Remaining performance obligation estimates are subject to change and are affected by several factors, including terminations and changes in the timing and scope of contracts, arising from contract modifications.

Accounts Receivable and Contract Balances

The timing of revenue recognition may differ from the time of billing to our customers. Receivables presented in our condensed consolidated balance sheets represent an unconditional right to consideration. Contract balances represent amounts from an arrangement when either Verizon has performed, by transferring goods or services to the customer in advance of receiving all or partial consideration for such goods and services from the customer, or the customer has made payment to Verizon in advance of obtaining control of the goods and/or services promised to the customer in the contract.

The following table presents information about receivables from contracts with customers:

| At March 31, | At December 31, | ||||||||||

| (dollars in millions) | 2024 | 2023 | |||||||||

Accounts Receivable(1) | $ | $ | |||||||||

Device payment plan agreement receivables(2) | |||||||||||

(1)Balances do not include receivables related to the following: activity associated with certain vendor agreements, leasing arrangements (such as those for towers and equipment), captive reinsurance arrangements primarily related to wireless device insurance and device payment plan agreement receivables presented separately.

(2)Included in device payment plan agreement receivables presented in Note 6. Receivables derived from the sale of equipment on a device payment plan through an authorized agent are excluded.

9

Contract assets primarily relate to our rights to consideration for goods or services provided to customers but for which we do not have an unconditional right at the reporting date. Under a fixed-term plan, total contract revenue is allocated between wireless service and equipment revenues. In conjunction with these arrangements, a contract asset is created, which represents the difference between the amount of equipment revenue recognized upon sale and the amount of consideration received from the customer when the performance obligation related to the transfer of control of the equipment is satisfied. The contract asset is reclassified to accounts receivable as wireless services are provided and billed. We have the right to bill the customer as service is provided over time, which results in our right to the payment being unconditional. The contract asset balances are presented in our condensed consolidated balance sheets as Prepaid expenses and other and Other assets. We recognize the allowance for credit losses at inception and reassess quarterly based on management’s expectation of the asset’s collectability.

Contract liabilities arise when we bill our customers and receive consideration in advance of providing the goods or services promised in the contract. We typically bill service one month in advance, which is the primary component of the contract liability balance. Contract liabilities are recognized as revenue when services are provided to the customer. The contract liability balances are presented in our condensed consolidated balance sheets as Other current liabilities and Other liabilities.

Revenue recognized related to contract liabilities existing at January 1, 2024 and January 1, 2023 were $4.4 billion and $4.3 billion for the three months ended March 31, 2024 and March 31, 2023, respectively.

The balances of contract assets and contract liabilities recorded in our condensed consolidated balance sheets were as follows:

| At March 31, | At December 31, | ||||||||||

| (dollars in millions) | 2024 | 2023 | |||||||||

| Assets | |||||||||||

| Prepaid expenses and other | $ | $ | |||||||||

| Other assets | |||||||||||

| Total Contract Assets | $ | $ | |||||||||

| Liabilities | |||||||||||

| Other current liabilities | $ | $ | |||||||||

| Other liabilities | |||||||||||

| Total Contract Liabilities | $ | $ | |||||||||

Contract Costs

Topic 606 requires the recognition of an asset for incremental costs to obtain a customer contract, which are then amortized to expense over the respective periods of expected benefit. We recognize an asset for incremental commission expenses paid to internal and external sales personnel and agents in conjunction with obtaining customer contracts. We only defer these costs when we have determined the commissions are incremental costs that would not have been incurred absent the customer contract and are expected to be recoverable. Costs to obtain a contract are amortized and recorded ratably as commission expense over the period representing the transfer of goods or services to which the assets relate. Costs to obtain wireless contracts are amortized over both of our Consumer and Business customers' estimated upgrade cycles, as such costs are typically incurred each time a customer upgrades. Costs to obtain wireline contracts are amortized as expense over the estimated customer relationship period for our Consumer customers. Incremental costs to obtain wireline contracts for our Business customers are insignificant. Costs to obtain contracts are recorded in Selling, general and administrative expense.

We also defer costs incurred to fulfill contracts that: (1) relate directly to the contract; (2) are expected to generate resources that will be used to satisfy our performance obligation under the contract; and (3) are expected to be recovered through revenue generated under the contract. Contract fulfillment costs are expensed as we satisfy our performance obligations and recorded in Cost of services. These costs principally relate to direct costs that enhance our wireline business resources, such as costs incurred to install circuits.

We determine the amortization periods for our costs incurred to obtain or fulfill a customer contract at a portfolio level due to the similarities within these customer contract portfolios.

Other costs, such as general costs or costs related to past performance obligations, are expensed as incurred.

Collectively, costs to obtain a contract and costs to fulfill a contract are referred to as deferred contract costs, and amortized over a -to-seven year period. Deferred contract costs are classified as current or non-current within Prepaid expenses and other and Other assets, respectively.

10

The balances of deferred contract costs included in our condensed consolidated balance sheets were as follows:

| At March 31, | At December 31, | ||||||||||

| (dollars in millions) | 2024 | 2023 | |||||||||

| Assets | |||||||||||

| Prepaid expenses and other | $ | $ | |||||||||

| Other assets | |||||||||||

| Total | $ | $ | |||||||||

For the three months ended March 31, 2024 and March 31, 2023, we recognized expense of $829 million and $795 million, respectively, associated with the amortization of deferred contract costs, primarily within Selling, general and administrative expense in our condensed consolidated statements of income.

| Note 3. Acquisitions and Divestitures | ||

Spectrum License Transactions

In February 2021, the Federal Communications Commission (FCC) concluded Auction 107 for C-Band wireless spectrum. In accordance with the rules applicable to the auction, Verizon is required to make payments for our allocable share of clearing costs incurred by, and incentive payments due to, the incumbent license holders associated with the auction, which are estimated to be $7.6 billion. During the three months ended March 31, 2024 and March 31, 2023, we made payments of $269 million and $114 million, respectively, for obligations related to clearing costs and accelerated clearing incentives. We expect to continue to make payments of approximately $100 million for the remaining obligations in 2024. The final timing and amounts of these payments could differ based on the actual amount of incumbent holders’ reimbursement claims and the speed with which those claims are approved and processed. The carrying value of the wireless spectrum won in Auction 107 consists of all payments required to participate and purchase licenses in the auction, including Verizon’s allocable share of clearing costs incurred by, and incentive payments due to, the incumbent license holders associated with the auction that we are obligated to pay in order to acquire the licenses, as well as capitalized interest to the extent qualifying activities have occurred.

TracFone Wireless, Inc.

On November 23, 2021 (the Acquisition Date), we completed the acquisition of TracFone Wireless, Inc. (TracFone). Verizon acquired all of TracFone's outstanding stock in exchange for approximately $3.5 billion in cash, net of cash acquired and working capital and other adjustments, 57,596,544 shares of common stock of the Company valued at approximately $3.0 billion, and up to an additional $650 million in future cash contingent consideration related to the achievement of certain performance measures and other commercial arrangements. The fair value of the Verizon common stock was determined on the basis of its closing market price on the Acquisition Date. The estimated fair value of the contingent consideration as of the Acquisition Date was approximately $560 million and represented a Level 3 measurement as defined in ASC 820, Fair Value Measurements and Disclosures. See Note 7 for additional information. The contingent consideration payable was based on the achievement of certain revenue and operational targets, measured over a two-year earn out period. Contingent consideration payments were completed in January of 2024.

| Note 4. Wireless Licenses, Goodwill, and Other Intangible Assets | ||

Wireless Licenses

The carrying amounts of our Wireless licenses are as follows:

| At March 31, | At December 31, | |||||||

| (dollars in millions) | 2024 | 2023 | ||||||

| Wireless licenses | $ | $ | ||||||

During the three months ended March 31, 2024 and March 31, 2023, we made payments of $269 million and $114 million, respectively, for obligations related to clearing costs and accelerated clearing incentives for wireless licenses in connection with Auction 107. See Note 3 for additional information.

11

At March 31, 2024 and 2023, approximately $13.9 billion and $38.9 billion, respectively, of wireless licenses were under development for commercial service for which we were capitalizing interest costs. We recorded approximately $180 million and $449 million of capitalized interest on wireless licenses for the three months ended March 31, 2024 and 2023, respectively.

During the three months ended March 31, 2024, we renewed various wireless licenses in accordance with FCC regulations. The average renewal period for these licenses was 10 years.

Goodwill

Changes in the carrying amount of Goodwill are as follows:

| (dollars in millions) | Consumer | Business | Total | ||||||||||||||

Balance at January 1, 2024(1) | $ | $ | $ | ||||||||||||||

Reclassifications, adjustments and other | ( | ( | |||||||||||||||

Balance at March 31, 2024 | $ | $ | $ | ||||||||||||||

(1) Goodwill is net of accumulated impairment charges of $5.8 billion related to our Business reporting unit.

Other Intangible Assets

The following table displays the composition of Other intangible assets, net as well as the respective amortization periods:

| At March 31, 2024 | At December 31, 2023 | ||||||||||||||||||||||||||||||||||

| (dollars in millions) | Gross Amount | Accumulated Amortization | Net Amount | Gross Amount | Accumulated Amortization | Net Amount | |||||||||||||||||||||||||||||

Customer lists ( | $ | $ | ( | $ | $ | $ | ( | $ | |||||||||||||||||||||||||||

Non-network internal-use software ( | ( | ( | |||||||||||||||||||||||||||||||||

Other ( | ( | ( | |||||||||||||||||||||||||||||||||

| Total | $ | $ | ( | $ | $ | $ | ( | $ | |||||||||||||||||||||||||||

The amortization expense for Other intangible assets was as follows:

| Three Months Ended | |||||

| (dollars in millions) | March 31, | ||||

| 2024 | $ | ||||

| 2023 | |||||

The estimated future amortization expense for Other intangible assets for the remainder of the current year and next 5 years is as follows:

| Years | (dollars in millions) | ||||

| Remainder of 2024 | $ | ||||

| 2025 | |||||

| 2026 | |||||

| 2027 | |||||

| 2028 | |||||

| 2029 | |||||

| Note 5. Debt | ||

Significant Debt Transactions

Debt or equity financing may be needed to fund additional investments or development activities or to maintain an appropriate capital structure to ensure our financial flexibility.

The following tables show the significant transactions involving the senior unsecured debt securities of the Company and its subsidiaries that occurred during the three months ended March 31, 2024.

12

Tender Offers

| (dollars in millions) | Principal Amount Purchased | Cash Consideration(1) | |||||||||

Verizon | € | $ | |||||||||

(1) The total cash consideration includes the tender offer consideration, plus any accrued and unpaid interest to the date of purchase. In addition, for securities denominated in a currency other than the U.S. dollar, cash consideration is shown on a U.S. dollar equivalent basis and includes the amount payable per the derivatives entered into in connection with the transaction. See Note 7 for additional information on cross currency swap transactions related to the transaction.

Repayments and Repurchases

| (dollars in millions) | Principal Repaid/ Repurchased | Amount Paid(1) | |||||||||

Verizon | € | $ | |||||||||

Verizon | $ | ||||||||||

| Verizon floating rate notes due 2024 | |||||||||||

| Open market repurchases of various Verizon notes | |||||||||||

| Total | $ | ||||||||||

(1) Represents amount paid to repay or repurchase, including any accrued interest. In addition, for securities denominated in a currency other than the U.S. dollar, amount paid is shown on a U.S. dollar equivalent basis and includes the amount payable per the derivatives entered into in connection with the transaction. See Note 7 for additional information on cross currency swap transactions related to the transaction.

Issuances

| (dollars in millions) | Principal Amount Issued | Net Proceeds(1) | |||||||||

Verizon | € | $ | |||||||||

Verizon | € | ||||||||||

Verizon | $ | ||||||||||

| Total | $ | ||||||||||

(1) Net proceeds were net of underwriting discounts and other issuance costs. In addition, for securities denominated in a currency other than the U.S. dollar, net proceeds are shown on a U.S. dollar equivalent basis. See Note 7 for additional information on cross currency swap transactions related to the issuances.

(2) An amount equal to the net proceeds from these notes is expected to be used to fund, in whole or in part, certain renewable energy projects, including new and existing investments made by us during the period from May 1, 2023 through the maturity date of the notes.

Commercial Paper Program

During the three months ended March 31, 2024, we issued $9.6 billion in commercial paper and we repaid $7.2 billion of commercial paper. As of March 31, 2024, we had $2.4 billion of commercial paper outstanding. These transactions are reflected within Cash flows from financing activities in our condensed consolidated statements of cash flows on a net basis.

Asset-Backed Debt

As of March 31, 2024, the carrying value of our asset-backed debt was $23.3 billion. Our asset-backed debt includes Asset-Backed Notes (ABS Notes) issued to third-party investors (Investors) and loans (ABS Financing Facilities) received from banks and their conduit facilities (collectively, the Banks). Our consolidated asset-backed debt bankruptcy remote legal entities (each, an ABS Entity, or collectively, the ABS Entities) issue the debt or are otherwise party to the transaction documentation in connection with our asset-backed debt transactions. Under the terms of our asset-backed debt, Cellco Partnership (Cellco), a wholly-owned subsidiary of the Company, and certain other Company affiliates (collectively, the Originators) transfer device payment plan agreement receivables and certain other receivables (collectively referred to as certain receivables) or a participation interest in certain other receivables to one of the ABS Entities, which in turn transfers such receivables and participation interest to another ABS Entity that issues the debt. Verizon entities retain the equity interests and residual interests, as applicable, in the ABS Entities, which represent the rights to all funds not needed to make required payments on the asset-backed debt and other related payments and expenses.

Our asset-backed debt is secured by the transferred receivables and participation interest, and future collections on such receivables and underlying receivables related to such participation interest. These receivables and participation interest transferred to the ABS Entities and related assets, consisting primarily of restricted cash, will only be available for payment of asset-backed debt and expenses related thereto, payments to the Originators in respect of additional transfers of certain receivables and participation interest, and other obligations arising from our asset-backed debt transactions, and will not be available to pay other obligations or claims of Verizon’s creditors until the associated asset-backed debt and other obligations are

13

satisfied. The Investors or Banks, as applicable, which hold our asset-backed debt have legal recourse to the assets securing the debt, but do not have any recourse to Verizon with respect to the payment of principal and interest on the debt. Under a parent support agreement, the Company has agreed to guarantee certain of the payment obligations of Cellco and the Originators to the ABS Entities.

Cash collections on the receivables and on the underlying receivables related to the participation interest collateralizing our asset-backed debt securities are required at certain specified times to be placed into segregated accounts. Deposits to the segregated accounts are considered restricted cash and are included in Prepaid expenses and other and Other assets in our condensed consolidated balance sheets.

Proceeds from our asset-backed debt transactions are reflected in Cash flows from financing activities in our condensed consolidated statements of cash flows. The asset-backed debt issued is included in Debt maturing within one year and Long-term debt in our condensed consolidated balance sheets.

ABS Notes

During the three months ended March 31, 2024, we completed the following ABS Notes transactions:

| (dollars in millions) | Interest Rates % | Expected Weighted-average Life to Maturity (in years) | Principal Amount Issued | |||||||||||

| January 2024 | ||||||||||||||

| Series 2024-1 | ||||||||||||||

| A-1a Senior class notes | $ | |||||||||||||

| A-1b Senior class notes | Compounded SOFR + | |||||||||||||

| B Junior class notes | ||||||||||||||

| C Junior class notes | ||||||||||||||

| Series 2024-2 | ||||||||||||||

| A Senior class notes | ||||||||||||||

| B Junior class notes | ||||||||||||||

| C Junior class notes | ||||||||||||||

| Total | $ | |||||||||||||

(1) Compounded Secured Overnight Financing Rate (SOFR) is calculated using SOFR as published by the Federal Reserve Bank of New York in accordance with the terms of such notes. Compounded SOFR for the interest payment made in March 2024 was 5.319 %.

Under the terms of each series of ABS Notes outstanding as of March 31, 2024, there is a revolving period of up to two years , three years , or five years , as applicable, during which we may transfer additional receivables to the ABS Entity. During the three months ended March 31, 2024, we made aggregate principal repayments of $508 million in connection with an anticipated redemption of ABS Notes and notes that have entered the amortization period, including payments in connection with any note redemptions.

In April 2024, we issued $875 million aggregate principal amount of senior and junior ABS Notes, with a blended interest rate of approximately 5.370 %, through an ABS Entity.

ABS Financing Facilities

Under the two loan agreements outstanding in connection with the ABS Financing Facility originally entered into in 2021 and most recently renewed in 2023 (2021 ABS Financing Facility), we prepaid an aggregate of $900 million in January 2024 and borrowed an additional $600 million in March 2024. The aggregate outstanding balance under the 2021 ABS Financing Facility was $8.2 billion as of March 31, 2024. In April 2024, we prepaid an aggregate of $900 million under a loan agreement outstanding in connection with the 2021 ABS Financing Facility.

Under the loan agreement outstanding in connection with the ABS Financing Facility originally entered into in 2022 and most recently renewed in 2023 (2022 ABS Financing Facility), the aggregate outstanding balance was $3.0 billion as of March 31, 2024.

Variable Interest Entities (VIEs)

The ABS Entities meet the definition of a VIE for which we have determined that we are the primary beneficiary as we have both the power to direct the activities of the entity that most significantly impact the entity’s performance and the obligation to absorb losses or the right to receive benefits of the entity. Therefore, the assets, liabilities and activities of the ABS Entities are

14

consolidated in our financial results and are included in amounts presented on the face of our condensed consolidated balance sheets.

The assets and liabilities related to our asset-backed debt arrangements included in our condensed consolidated balance sheets were as follows:

At March 31, | At December 31, | ||||||||||

| (dollars in millions) | 2024 | 2023 | |||||||||

| Assets | |||||||||||

| Accounts receivable, net | $ | $ | |||||||||

| Prepaid expenses and other | |||||||||||

| Other assets | |||||||||||

| Liabilities | |||||||||||

| Accounts payable and accrued liabilities | |||||||||||

| Debt maturing within one year | |||||||||||

| Long-term debt | |||||||||||

The Accounts receivable, net amounts above does not include underlying receivables for which a participation interest has been transferred to the ABS Entities. See Note 6 for additional information on certain receivables and participation interest used to secure asset-backed debt.

Long-Term Credit Facilities

At March 31, 2024 | |||||||||||||||||||||||

| (dollars in millions) | Maturities | Facility Capacity | Unused Capacity | Principal Amount Outstanding | |||||||||||||||||||

Verizon revolving credit facility(1) | 2028 | $ | $ | $ | |||||||||||||||||||

Various export credit facilities(2) | 2024 - 2031 | ||||||||||||||||||||||

| Total | $ | $ | $ | ||||||||||||||||||||

(1) The revolving credit facility does not require us to comply with financial covenants or maintain specified credit ratings, and it permits us to borrow even if our business has incurred a material adverse change. The revolving credit facility provides for the issuance of letters of credit. As of March 31, 2024, there have been no drawings against the revolving credit facility since its inception.

(2) During the three months ended March 31, 2024, there were no drawings from these facilities. During the three months ended March 31, 2023, we drew down $515 million from these facilities. Borrowings under certain of these facilities are repaid semi-annually in equal installments up to the applicable maturity dates. Maturities reflect maturity dates of principal amounts outstanding. Any amounts borrowed under these facilities and subsequently repaid cannot be reborrowed.

In March 2024, we amended our $9.5 billion revolving credit facility to increase the capacity to $12.0 billion and extended its maturity to 2028.

Non-Cash Transactions

During the three months ended March 31, 2024 and 2023, we financed, primarily through alternative financing arrangements, the purchase of approximately $463 million and $284 million, respectively, of long-lived assets consisting primarily of network equipment. As of March 31, 2024 and December 31, 2023, $2.4 billion and $2.2 billion, respectively, relating to these financing arrangements, including those entered into in prior years and liabilities assumed through acquisitions, remained outstanding. These purchases are non-cash financing activities and therefore are not reflected within Capital expenditures in our condensed consolidated statements of cash flows.

Net Debt Extinguishment Gains

During the three months ended March 31, 2024 and 2023, we recorded net debt extinguishment gains of $110 million and $70 million, respectively. The net gains are recorded in Other income, net in our condensed consolidated statements of income. Additionally, during the three months ended March 31, 2024 and 2023, we recorded insignificant transaction fees and interest expense as a result of the debt extinguishments. The total debt extinguishment gains are reflected within Other, net cash flow from operating activities, and the cash payments to extinguish the debt are reflected within Other, net cash flow from financing activities in our condensed consolidated statements of cash flows.

Guarantees

We guarantee the debentures of our operating telephone company subsidiaries. As of March 31, 2024, $614 million aggregate principal amount of these obligations remained outstanding. Each guarantee will remain in place for the life of the obligation

15

unless terminated pursuant to its terms, including the operating telephone company no longer being a wholly-owned subsidiary of the Company.

Debt Covenants

We and our consolidated subsidiaries are in compliance with all of our restrictive covenants in our debt agreements.

| Note 6. Device Payment Plan Agreement and Wireless Service Receivables | ||

The following table presents information about accounts receivable, net of allowances, recorded in our condensed consolidated balance sheet:

| At March 31, 2024 | |||||||||||||||||||||||

| (dollars in millions) | Device payment plan agreement | Wireless service | Other receivables(1) | Total | |||||||||||||||||||

| Accounts receivable | $ | $ | $ | $ | |||||||||||||||||||

| Less Allowance for credit losses | |||||||||||||||||||||||

| Accounts receivable, net of allowance | $ | $ | $ | $ | |||||||||||||||||||

(1) Other receivables primarily include wireline and other receivables, of which the allowances are individually insignificant.

Included in Other assets and Accounts receivable, net at March 31, 2024 and December 31, 2023, are net device payment plan agreement receivables and net wireless service receivables of $27.6 billion and $26.1 billion, respectively, which have been transferred to ABS Entities and continue to be reported in our condensed consolidated balance sheets. Included in Accounts receivable, net at March 31, 2024 and December 31, 2023, are net other receivables of $767 million and $911 million, respectively, on which a participation interest has been transferred to ABS Entities and continue to be reported in our condensed consolidated balance sheets. See Note 5 for additional information. We believe the carrying value of these receivables approximate their fair value using a Level 3 expected cash flow model.

Under the Verizon device payment program, our eligible wireless customers purchase wireless devices under a device payment plan agreement. Customers that activate service on devices purchased under the device payment program pay lower service fees as compared to those under our fixed-term service plans, and their device payment plan charge is included on their wireless monthly bill. While we no longer offer Consumer customers fixed-term subsidized service plans for devices, we continue to offer subsidized plans to our Business customers. We also continue to service existing plans for customers who have not yet purchased and activated devices under the Verizon device payment program.

Wireless Device Payment Plan Agreement Receivables

The following table displays both the current and non-current portions of device payment plan agreement receivables, net, recognized in our condensed consolidated balance sheets:

| At March 31, | At December 31, | ||||||||||

| (dollars in millions) | 2024 | 2023 | |||||||||

| Device payment plan agreement receivables, gross | $ | $ | |||||||||

| Unamortized imputed interest | ( | ( | |||||||||

| Device payment plan agreement receivables, at amortized cost | |||||||||||

Allowance(1) | ( | ( | |||||||||

| Device payment plan agreement receivables, net | $ | $ | |||||||||

| Classified in our condensed consolidated balance sheets: | |||||||||||

| Accounts receivable, net | $ | $ | |||||||||

| Other assets | |||||||||||

| Device payment plan agreement receivables, net | $ | $ | |||||||||

For indirect channel wireless contracts with customers, we impute risk adjusted interest on the device payment plan agreement receivables. We record the imputed interest as a reduction to the related accounts receivable. The associated interest income, which is included within Service revenues and other in our condensed consolidated statements of income, is recognized over the financed device payment term.

Promotions

In connection with certain device payment plan agreements, we may offer a promotion to allow our customers to upgrade to a new device after paying down a certain specified portion of the required device payment plan agreement amount as well as trading in their device in good working order. When a customer enters into a device payment plan agreement with the right to upgrade to a new device, we account for this trade-in right as a guarantee obligation.

16

We may offer certain promotions that allow a customer to trade in their owned device in connection with the purchase of a new device. Under these types of promotions, the customer receives a credit for the value of the trade-in device. At March 31, 2024 and December 31, 2023, the amount of trade-in liability was $522 million and $566 million, respectively.

In addition, we may provide the customer with additional future billing credits that will be applied against the customer’s monthly bill as long as service is maintained. These future billing credits are accounted for as consideration payable to a customer and are included in the determination of total transaction price, resulting in a contract liability.

Device payment plan agreement receivables, net, disclosed in the table above, does not reflect the trade-in liability, additional future credits or the guarantee liability.

Origination of Device Payment Plan Agreements

When originating device payment plan agreements, we use internal and external data sources to create a credit risk score to measure the credit quality of a customer and to determine eligibility for the device payment program. Verizon’s experience has been that the payment attributes of longer tenured customers are highly predictive for estimating their reliability to make future payments. Customers with longer tenures tend to exhibit similar risk characteristics to other customers with longer tenures, and receivables due from customers with longer tenures tend to perform better than receivables from customers that have not previously been Verizon customers. As a result of this experience, we make initial lending decisions based upon whether the customers are "established customers" or "short-tenured customers." If a Consumer customer has been a customer for 45 days or more, or if a Business customer has been a customer for 12 months or more, the customer is considered an "established customer." For established customers, the credit decision and ongoing credit monitoring processes rely on a combination of internal and external data sources. If a Consumer customer has been a customer less than 45 days, or a Business customer has been a customer for less than 12 months, the customer is considered a "short-tenured customer." For short-tenured customers, the credit decision and credit monitoring processes rely more heavily on external data sources.

Available external credit data from credit reporting agencies along with internal data are used to create custom credit risk scores for Consumer customers. The custom credit risk score is generated automatically from the applicant’s credit data using proprietary custom credit models. The credit risk score measures the likelihood that the potential customer will become severely delinquent and be disconnected for non-payment. For a small portion of short-tenured customer applications, a traditional credit report is not available from one of the national credit reporting agencies because the potential customer does not have sufficient credit history. In those instances, alternative credit data is used for the risk assessment. For Business customers, we also verify the existence of the business with external data sources.

Based on the custom credit risk score, we assign each customer a credit class, each of which has specified offers of credit. This includes an account level spending limit and a maximum amount of credit allowed per device for Consumer customers or a required down payment percentage for Business customers.

Credit Quality Information

Subsequent to origination, we assess indicators for the quality of our wireless device payment plan agreement portfolio using two models, one for new customers and one for existing customers. The model for new customers pools all Consumer and Business wireless customers based on less than 210 days as "new customers." The model for existing customers pools all Consumer and Business wireless customers based on 210 days or more as "existing customers."

The following table presents device payment plan agreement receivables, at amortized cost, and gross write-offs recorded, as of and for the three months ended March 31, 2024, by credit quality indicator and year of origination:

Year of Origination(1) | |||||||||||||||||||||||

| (dollars in millions) | 2024 | 2023 | 2022 and prior | Total | |||||||||||||||||||

| Device payment plan agreement receivables, at amortized cost | |||||||||||||||||||||||

| New customers | $ | $ | $ | $ | |||||||||||||||||||

| Existing customers | |||||||||||||||||||||||

| Total | $ | $ | $ | $ | |||||||||||||||||||

| Gross write-offs | |||||||||||||||||||||||

| New customers | $ | $ | $ | $ | |||||||||||||||||||

| Existing customers | |||||||||||||||||||||||

| Total | $ | $ | $ | $ | |||||||||||||||||||

(1) Includes accounts that have been suspended at a point in time.

The data presented in the table above was last updated on March 31, 2024.

17

We assess indicators for the quality of our wireless service receivables portfolio as one overall pool. The following table presents wireless service receivables, at amortized cost, and gross write-offs recorded, as of and for the three months ended March 31, 2024, by year of origination:

| Year of Origination | |||||||||||||||||

| (dollars in millions) | 2024 | 2023 and prior | Total | ||||||||||||||

| Wireless service receivables, at amortized cost | $ | $ | $ | ||||||||||||||

| Gross write-offs | |||||||||||||||||

The data presented in the table above was last updated on March 31, 2024.

Allowance for Credit Losses

The credit quality indicators are used in determining the estimated amount and the timing of expected credit losses for the device payment plan agreement and wireless service receivables portfolios.

For device payment plan agreement receivables, we record bad debt expense based on a default and loss calculation using our proprietary loss model. The expected loss rate is determined based on customer credit scores and other qualitative factors as noted above. The loss rate is assigned individually on a customer by customer basis and the custom credit scores are then aggregated by vintage and used in our proprietary loss model to calculate the weighted-average loss rate used for determining the allowance balance.

We monitor the collectability of our wireless service receivables as one overall pool. Wireline service receivables are disaggregated and pooled by the following types of customers and related contracts: consumer, small and medium business, enterprise, public sector and wholesale. For wireless service receivables and wireline consumer and small and medium business receivables, the allowance is calculated based on a 12 month rolling average write-off balance multiplied by the average life-cycle of an account from billing to write-off. The risk of loss is assessed over the contractual life of the receivables and is adjusted based on the historical loss amounts for current and future conditions based on management’s qualitative considerations. For enterprise, public sector and wholesale wireline receivables, the allowance for credit losses is based on historical write-off experience and individual customer credit risk, if applicable.

Activity in the allowance for credit losses by portfolio segment of receivables was as follows:

| (dollars in millions) | Device Payment Plan Agreement Receivables(1) | Wireless Service Plan Receivables | |||||||||

Balance at January 1, 2024 | $ | $ | |||||||||

| Current period provision for expected credit losses | |||||||||||

| Write-offs charged against the allowance | ( | ( | |||||||||

| Recoveries collected | |||||||||||

| Balance at March 31, 2024 | $ | $ | |||||||||

(1) Includes allowance for both short-term and long-term device payment plan agreement receivables.

We monitor delinquency and write-off experience based on the quality of our device payment plan agreement and wireless service receivables portfolios. The extent of our collection efforts with respect to a particular customer are based on the results of our proprietary custom internal scoring models that analyze the customer’s past performance to predict the likelihood of the customer falling further delinquent. These custom scoring models assess a number of variables, including origination characteristics, customer account history and payment patterns. Since our customers’ behaviors may be impacted by general economic conditions, we analyzed whether changes in macroeconomic conditions impact our credit loss experience and have concluded that our credit loss estimates are generally not materially impacted by reasonable and supportable forecasts of future economic conditions. Based on the score derived from these models, accounts are grouped by risk category to determine the collection strategy to be applied to such accounts. For device payment plan agreement receivables and wireless service receivables, we consider an account to be delinquent and in default status if there are unpaid charges remaining on the account on the day after the bill’s due date. The risk class determines the speed and severity of the collections effort including initiatives taken to facilitate customer payment.

The balance and aging of the device payment plan agreement receivables, at amortized cost, were as follows:

| At March 31, | |||||

| (dollars in millions) | 2024 | ||||

| Unbilled | $ | ||||

| Billed: | |||||

Current | |||||

Past due | |||||

| Device payment plan agreement receivables, at amortized cost | $ | ||||

18

| Note 7. Fair Value Measurements and Financial Instruments | ||

Recurring Fair Value Measurements

The following table presents the balances of assets and liabilities measured at fair value on a recurring basis as of March 31, 2024:

| (dollars in millions) | Level 1(1) | Level 2(2) | Level 3(3) | Total | |||||||||||||||||||

| Assets: | |||||||||||||||||||||||

| Prepaid expenses and other: | |||||||||||||||||||||||

| Fixed income securities | $ | $ | $ | $ | |||||||||||||||||||

| Cross currency swaps | |||||||||||||||||||||||

| Interest rate caps | |||||||||||||||||||||||

| Other assets: | |||||||||||||||||||||||

| Fixed income securities | |||||||||||||||||||||||

| Cross currency swaps | |||||||||||||||||||||||

| Interest rate caps | |||||||||||||||||||||||

| Total | $ | $ | $ | $ | |||||||||||||||||||

| Liabilities: | |||||||||||||||||||||||

| Other current liabilities: | |||||||||||||||||||||||

| Interest rate swaps | $ | $ | $ | $ | |||||||||||||||||||

| Cross currency swaps | |||||||||||||||||||||||

| Foreign exchange forwards | |||||||||||||||||||||||

| Interest rate caps | |||||||||||||||||||||||

| Other liabilities: | |||||||||||||||||||||||

| Interest rate swaps | |||||||||||||||||||||||

| Cross currency swaps | |||||||||||||||||||||||

| Interest rate caps | |||||||||||||||||||||||

| Total | $ | $ | $ | $ | |||||||||||||||||||

(1)Quoted prices in active markets for identical assets or liabilities.

(2)Observable inputs other than quoted prices in active markets for identical assets and liabilities.

(3)Unobservable pricing inputs in the market.

19

The following table presents the balances of assets and liabilities measured at fair value on a recurring basis as of December 31, 2023:

| (dollars in millions) | Level 1(1) | Level 2(2) | Level 3(3) | Total | |||||||||||||||||||

| Assets: | |||||||||||||||||||||||

| Prepaid expenses and other: | |||||||||||||||||||||||

| Fixed income securities | $ | $ | $ | $ | |||||||||||||||||||

| Cross currency swaps | |||||||||||||||||||||||

| Foreign exchange forwards | |||||||||||||||||||||||

| Interest rate caps | |||||||||||||||||||||||

| Other assets: | |||||||||||||||||||||||

| Fixed income securities | |||||||||||||||||||||||

| Cross currency swaps | |||||||||||||||||||||||

| Interest rate caps | |||||||||||||||||||||||

| Total | $ | $ | $ | $ | |||||||||||||||||||

| Liabilities: | |||||||||||||||||||||||

| Other current liabilities: | |||||||||||||||||||||||

Interest rate swaps | $ | $ | $ | $ | |||||||||||||||||||

Cross currency swaps | |||||||||||||||||||||||

Foreign exchange forwards | |||||||||||||||||||||||

Interest rate caps | |||||||||||||||||||||||

| Contingent consideration | |||||||||||||||||||||||

| Other liabilities: | |||||||||||||||||||||||

Interest rate swaps | |||||||||||||||||||||||

Cross currency swaps | |||||||||||||||||||||||

Interest rate caps | |||||||||||||||||||||||

| Total | $ | $ | $ | $ | |||||||||||||||||||

(1)Quoted prices in active markets for identical assets or liabilities.

(2)Observable inputs other than quoted prices in active markets for identical assets and liabilities.

(3)Unobservable pricing inputs in the market.

Certain of our equity investments do not have readily determinable fair values and are excluded from the tables above. Such investments are measured at cost, less any impairment, plus or minus changes resulting from observable price changes in orderly transactions for an identical or similar investment of the same issuer and are included in Investments in unconsolidated businesses in our condensed consolidated balance sheets. As of both March 31, 2024 and December 31, 2023, the carrying amount of our investments without readily determinable fair values was $764 209 million and $99 million, respectively.

Verizon had a liability for contingent consideration related to its acquisition of TracFone, completed in November 2021. The fair value was calculated using a probability-weighted discounted cash flow model and represented a Level 3 measurement. Level 3 instruments include valuation based on unobservable inputs reflecting our own assumptions, consistent with reasonably available assumptions made by other market participants. Subsequent to the Acquisition Date, at each reporting date, the contingent consideration liability was remeasured to fair value. Contingent consideration payments were completed in January of 2024. During the three months ended March 31, 2024 and March 31, 2023, we made payments of $52 million and $102 million, respectively, related to the contingent consideration. See Note 3 for additional information.

Fixed income securities consist primarily of investments in municipal bonds. The valuation of the fixed income securities is based on the quoted prices for similar assets in active markets or identical assets in inactive markets or models that apply inputs from observable market data. The valuation determines that these securities are classified as Level 2.

Derivative contracts are valued using models based on readily observable market parameters for all substantial terms of our derivative contracts and thus are classified within Level 2. We use mid-market pricing for fair value measurements of our derivative instruments. Our derivative instruments are recorded on a gross basis.

We recognize transfers between levels of the fair value hierarchy as of the end of the reporting period.

Fair Value of Short-term and Long-term Debt

The fair value of our debt is determined using various methods, including quoted prices for identical debt instruments, which is a Level 1 measurement, as well as quoted prices for similar debt instruments with comparable terms and maturities, which is a Level 2 measurement.

20

The fair value of our short-term and long-term debt, excluding finance leases, was as follows:

| Fair Value | |||||||||||||||||||||||||||||

| (dollars in millions) | Carrying Amount | Level 1 | Level 2 | Level 3 | Total | ||||||||||||||||||||||||

| At March 31, 2024 | $ | $ | $ | $ | $ | ||||||||||||||||||||||||

| At December 31, 2023 | |||||||||||||||||||||||||||||

Derivative Instruments

We enter into derivative transactions primarily to manage our exposure to fluctuations in foreign currency exchange rates and interest rates. We employ risk management strategies, which may include the use of a variety of derivatives including interest rate swaps, cross currency swaps, forward starting interest rate swaps, treasury rate locks, interest rate caps, swaptions and foreign exchange forwards. We do not hold derivatives for trading purposes.

The following table sets forth the notional amounts of our outstanding derivative instruments:

| At March 31, | At December 31, | ||||||||||

| (dollars in millions) | 2024 | 2023 | |||||||||

| Interest rate swaps | $ | $ | |||||||||

| Cross currency swaps | |||||||||||

| Foreign exchange forwards | |||||||||||

The following tables summarize the activities of our designated derivatives:

| Three Months Ended | |||||||||||

| March 31, | |||||||||||

| (dollars in millions) | 2024 | 2023 | |||||||||

| Interest Rate Swaps: | |||||||||||

| Notional value entered into | $ | $ | |||||||||

| Notional value settled | |||||||||||

| Pre-tax gain (loss) recognized in Interest expense | ( | ||||||||||

| Cross Currency Swaps: | |||||||||||

| Notional value entered into | |||||||||||

| Notional value settled | |||||||||||

Pre-tax gain (loss) on cross currency swaps recognized in Interest expense | ( | ||||||||||

Pre-tax gain (loss) on hedged debt recognized in Interest expense | ( | ||||||||||

Excluded components recognized in Other comprehensive income (loss) | ( | ||||||||||

| Initial value of the excluded component amortized into Interest expense | |||||||||||

| Three Months Ended | |||||||||||

| March 31, | |||||||||||

| (dollars in millions) | 2024 | 2023 | |||||||||

| Other, net Cash Flows from Financing Activities: | |||||||||||

| Cash paid for settlement of cross currency swaps, net | $ | ( | $ | ( | |||||||

The following table displays the amounts recorded in Long-term debt in our condensed consolidated balance sheets related to cumulative basis adjustments for our interest rate swaps designated as fair value hedges. The cumulative amounts exclude cumulative basis adjustments related to foreign exchange risk.

| At March 31, | At December 31, | ||||||||||

| (dollars in millions) | 2024 | 2023 | |||||||||

| Carrying amount of hedged liabilities | $ | $ | |||||||||

| Cumulative amount of fair value hedging adjustment included in the carrying amount of the hedged liabilities | ( | ( | |||||||||

| Cumulative amount of fair value hedging adjustment remaining for which hedge accounting has been discontinued | |||||||||||

21

Interest Rate Swaps

We enter into interest rate swaps to achieve a targeted mix of fixed and variable rate debt. We principally receive fixed rates and pay variable rates, resulting in a net increase or decrease to Interest expense. These swaps are designated as fair value hedges and hedge against interest rate risk exposure of designated debt issuances. We record the interest rate swaps at fair value in our condensed consolidated balance sheets as assets and liabilities. Changes in the fair value of the interest rate swaps are recorded to Interest expense, which are primarily offset by changes in the fair value of the hedged debt due to changes in interest rates.

Cross Currency Swaps

We have entered into cross currency swaps to exchange our British Pound Sterling, Euro, Swiss Franc, Canadian Dollar and Australian Dollar-denominated cash flows into U.S. dollars and to fix our cash payments in U.S. dollars, as well as to mitigate the impact of foreign currency transaction gains or losses. These swaps are designated as fair value hedges. We record the cross currency swaps at fair value in our condensed consolidated balance sheets as assets and liabilities. Changes in the fair value of the cross currency swaps attributable to changes in the spot rate of the hedged item and changes in the recorded value of the hedged debt due to changes in spot rates are recorded in the same income statement line item. We present exchange gains and losses from the conversion of foreign currency denominated debt as a part of Interest expense. During the three months ended March 31, 2024 and March 31, 2023, these amounts completely offset each other and no net gain or loss was recorded.

Changes in the fair value of cross currency swaps attributable to time value and cross currency basis spread are initially recorded to Other comprehensive income (loss). Unrealized gains or losses on excluded components are recorded in Other comprehensive income (loss) and are recognized into Interest expense on a systematic and rational basis through the swap accrual over the life of the hedging instrument. The amount remaining in Accumulated other comprehensive loss related to cash flow hedges on the date of transition will be reclassified to earnings when the hedged item is recognized in earnings or when it becomes probable that the forecasted transactions will not occur.

On March 31, 2022, we elected to de-designate our cross currency swaps previously designated as cash flow hedges and re-designated these swaps as fair value hedges. For these hedges, we elected to exclude the change in fair value of the cross currency swaps related to both time value and cross currency basis spread from the assessment of hedge effectiveness (the excluded components). The initial value of the excluded components of $1.0 billion as of March 31, 2022 will continue to be amortized into Interest expense over the remaining life of the hedging instruments. During the three months ended March 31, 2024 and March 31, 2023, the amortization of the initial value of the excluded component completely offset the amortization related to the amount remaining in Other comprehensive income (loss) related to cash flow hedges. See Note 9 for additional information. We estimate that $93 million will be amortized into Interest expense within the next 12 months.

Net Investment Hedges

We have designated certain foreign currency debt instruments as net investment hedges to mitigate foreign exchange exposure related to non-U.S. dollar net investments in certain foreign subsidiaries against changes in foreign exchange rates. The notional amount of Euro-denominated debt designated as a net investment hedge was €750

Undesignated Derivatives

We also have the following derivative contracts which we use as economic hedges but for which we have elected not to apply hedge accounting.

The following table summarizes the activity of our derivatives not designated in hedging relationships:

| Three Months Ended | |||||||||||

| March 31, | |||||||||||

| (dollars in millions) | 2024 | 2023 | |||||||||

| Foreign Exchange Forwards: | |||||||||||

| Notional value entered into | $ | $ | |||||||||

| Notional value settled | |||||||||||

| Pre-tax gain (loss) recognized in Other income, net | ( | ||||||||||

Foreign Exchange Forwards

We enter into British Pound Sterling and Euro foreign exchange forwards to mitigate our foreign exchange rate risk related to non-functional currency denominated monetary assets and liabilities of international subsidiaries.

22

Concentrations of Credit Risk

Financial instruments that subject us to concentrations of credit risk consist primarily of temporary cash investments, short-term and long-term investments, trade receivables, including device payment plan agreement receivables, certain notes receivable, including lease receivables, and derivative contracts.

| Note 8. Employee Benefits | ||

We maintain non-contributory defined benefit pension plans for certain employees. In addition, we maintain postretirement health care and life insurance plans for certain retirees and their dependents, which are both contributory and non-contributory, and include a limit on our share of the cost for certain current and future retirees. In accordance with our accounting policy for pension and other postretirement benefits, operating expenses include service costs associated with pension and other postretirement benefits while other credits and/or charges based on actuarial assumptions, including projected discount rates, an estimated return on plan assets, and impact from health care trend rates are reported in Other income, net. These estimates are updated in the fourth quarter or upon a remeasurement event, to reflect actual return on plan assets and updated actuarial assumptions. The adjustment is recognized in the income statement during the fourth quarter and upon a remeasurement event pursuant to our accounting policy for the recognition of actuarial gains and losses.

Net Periodic Benefit Cost (Income)

The following table summarizes the components of net periodic benefit cost (income) related to our pension and postretirement health care and life insurance plans:

| (dollars in millions) | |||||||||||||||||||||||

| Pension | Health Care and Life | ||||||||||||||||||||||

| Three Months Ended March 31, | 2024 | 2023 | 2024 | 2023 | |||||||||||||||||||

| Service cost - Cost of services | $ | $ | $ | $ | |||||||||||||||||||

| Service cost - Selling, general and administrative expense | |||||||||||||||||||||||

| Service cost | $ | $ | $ | $ | |||||||||||||||||||

| Amortization of prior service cost (credit) | $ | $ | $ | ( | $ | ( | |||||||||||||||||

| Expected return on plan assets | ( | ( | ( | ( | |||||||||||||||||||

| Interest cost | |||||||||||||||||||||||

| Remeasurement gain, net | ( | ||||||||||||||||||||||

| Other components | $ | ( | $ | ( | $ | $ | |||||||||||||||||

| Total | $ | ( | $ | $ | $ | ||||||||||||||||||

The service cost component of net periodic benefit cost (income) is recorded in Cost of services and Selling, general and administrative expense in the condensed consolidated statements of income while the other components, including mark-to-market adjustments, if any, are recorded in Other income, net.

During the three months ended March 31, 2024, we updated the expected return on plan assets assumption for our pension plans from 7.50 % at December 31, 2023 to 8.00 % based upon the expected market returns from the March 31, 2024 asset allocation.

Pension Annuitization

On February 29, 2024, we entered into two separate commitment agreements, one by and between the Company, State Street Global Advisors Trust Company (“State Street”), as independent fiduciary of the Verizon Management Pension Plan and Verizon Pension Plan for Associates (the “Pension Plans”), and The Prudential Insurance Company of America (“Prudential”), and one by and between the Company, State Street and RGA Reinsurance Company (“RGA”), under which the Pension Plans purchased

23

nonparticipating single premium group annuity contracts from Prudential and RGA, respectively, to settle approximately $5.9 billion of benefit liabilities of the Pension Plans.

The purchase of the group annuity contracts closed on March 6, 2024. The group annuity contracts primarily cover a population that includes 56,000 retirees who commenced benefit payments from the Pension Plans prior to January 1, 2023 (“Transferred Participants”). Prudential and RGA each irrevocably guarantee and assume the sole obligation to make future payments to the Transferred Participants as provided under their respective group annuity contracts, with direct payments beginning July 1, 2024. The aggregate amount of each Transferred Participant’s payment under the group annuity contracts will be equal to the amount of each individual’s payment under the Pension Plans.

The purchase of the group annuity contracts was funded directly by transferring $5.7 billion of assets of the Pension Plans. The Company made additional contributions to the Pension Plans prior to the closing date of the transaction, as discussed below. With these contributions, the funded ratio of each of the Pension Plans does not change as a result of this transaction. During the three months ended March 31, 2024, we recorded a net pre-tax settlement gain as a result of this transaction, as discussed below.

Pension plan assets and liabilities are primarily presented within Employee benefit obligations in our condensed consolidated balance sheets.

Severance Payments

During the three months ended March 31, 2024, we paid severance benefits of $118 million. At March 31, 2024, we had a remaining severance liability of $456 million, a portion of which includes future contractual payments to separated employees.

Employer Contributions

During the three months ended March 31, 2024, we made discretionary contributions to the Pension Plans in the aggregate amount of $365 million. During the three months ended March 31, 2023, we made no contributions to our qualified pension plans. During the three months ended March 31, 2024 and March 31, 2023, we made insignificant contributions to our nonqualified pension plans. No mandatory qualified pension plans contributions are expected or required through December 31, 2024. No significant changes are expected with respect to the nonqualified pension and other postretirement benefit plans contributions in 2024.

Remeasurement gain, net

During the three months ended March 31, 2024, we recorded a net pre-tax remeasurement gain of $73 million in our pension plans due to a net pre-tax settlement gain of $200 million resulting from the pension annuitization transaction discussed above, partially offset by a net pre-tax remeasurement loss of $127 million triggered by settlements.

The net pre-tax remeasurement loss recorded for the three months ended March 31, 2024, was primarily driven by a $613 million charge resulting from the difference between our estimated and actual return on assets, partially offset by a credit of $486 million due to changes in our discount rate assumption used to determine the current year liabilities of our pension plans.

24

| Note 9. Equity and Accumulated Other Comprehensive Loss | ||

Equity

Changes in the components of Total equity were as follows:

| Three Months Ended March 31, | ||||||||||||||||||||||||||

| 2024 | 2023 | |||||||||||||||||||||||||

| (dollars in millions, except per share amounts, and shares in thousands) | Shares | Amount | Shares | Amount | ||||||||||||||||||||||

| Common Stock | ||||||||||||||||||||||||||

| Balance at beginning of period | $ | $ | ||||||||||||||||||||||||

| Balance at end of period | ||||||||||||||||||||||||||

| Additional Paid In Capital | ||||||||||||||||||||||||||

| Balance at beginning of period | ||||||||||||||||||||||||||

| Other | ( | |||||||||||||||||||||||||