Ultra Series Fund | December 31, 2012

Table of Contents

| Page | ||

| Management’s Discussion of Fund Performance | ||

| 2012 in Review | 2 | |

| Outlook | 3 | |

| Conservative Allocation Fund | 4 | |

| Moderate Allocation Fund | 6 | |

| Aggressive Allocation Fund | 8 | |

| Money Market Fund | 10 | |

| Bond Fund | 12 | |

| High Income Fund | 14 | |

| Diversified Income Fund | 16 | |

| Large Cap Value Fund | 18 | |

| Large Cap Growth Fund | 20 | |

| Mid Cap Fund | 22 | |

| Small Cap Fund | 24 | |

| International Stock Fund | 26 | |

| Madison Target Retirement 2020 Fund | 28 | |

| Madison Target Retirement 2030 Fund | 30 | |

| Madison Target Retirement 2040 Fund | 32 | |

| Madison Target Retirement 2050 Fund | 34 | |

| Notes to Management’s Discussion of Fund Performance | 36 | |

| Portfolios of Investments | ||

| Conservative Allocation Fund | 38 | |

| Moderate Allocation Fund | 39 | |

| Aggressive Allocation Fund | 40 | |

| Money Market Fund | 41 | |

| Bond Fund | 43 | |

| High Income Fund | 46 | |

| Diversified Income Fund | 49 | |

| Large Cap Value Fund | 52 | |

| Large Cap Growth Fund | 53 | |

| Mid Cap Fund | 55 | |

| Small Cap Fund | 56 | |

| International Stock Fund | 58 | |

| Madison Target Retirement 2020 Fund | 60 | |

| Madison Target Retirement 2030 Fund | 61 | |

| Madison Target Retirement 2040 Fund | 62 | |

| Madison Target Retirement 2050 Fund | 63 | |

| Financial Statements | ||

| Statements of Assets and Liabilities | 64 | |

| Statements of Operations | 67 | |

| Statements of Changes in Net Assets | 70 | |

| Financial Highlights | 76 | |

| Notes to Financial Statements | 92 | |

| Report of Independent Registered Public Accounting Firm | 108 | |

| Other Information | 109 | |

| Trustees and Officers | 114 |

Nondeposit investment products are not federally insured, involve investment risk, may lose value and are not obligations of or guaranteed by any financial institution. For more complete information about Ultra Series Fund, including charges and expenses, request a prospectus from your financial advisor or from CMFG Life Insurance Company, 2000 Heritage Way, Waverly, IA 50677. Consider the investment objectives, risks, and charges and expenses of any fund carefully before investing. The prospectus contains this and other information about the investment company. For more current Ultra Series Fund performance information, please call 1-800-670-3600. Current performance may be lower or higher than the performance data quoted within. Past performance does not guarantee future results. Nothing in this report represents a recommendation of a security by the investment adviser. Portfolio holdings may have changed since the date of this report.

1

Ultra Series Fund | December 31, 2012

Management’s Discussion of Fund Performance

2012 IN REVIEW

The old adage that markets climb “a wall of worry” was demonstrated by domestic and international stock and bond markets in 2012. Despite signs of sluggish economic growth in the U.S., a recession in Europe, and slowing growth in the emerging markets, investors were well rewarded for holding stocks. The domestic stock market, as measured by the S&P 500, was up 16.0%, while the broad international market, as measured by the MSCI EAFE Index advanced 17.9%. The Russell Emerging Markets Index advanced 19.2%, and even investors in Europe found enough good news in the midst of a still-uncertain sovereign debt crisis to push stock valuations up strongly. The Morningstar Europe Stock Category showed mutual funds specializing in this region up 20.9% for the year. We believe the largest reason for these positive returns was the continued, unprecedented stimulus from the Federal Reserve and central banks around the world.

Stocks were not uniformly positive for the year, with a wide disparity of returns among U.S. Sectors. The Utilities Sector trailed with a loss of -2.9%, while the Financials Sector led the market with a 26.3% return, followed by the Consumer Discretionary Sector, with a 21.9% return. In general, more economically sensitive and lower-quality stocks rallied, while the more defensive sectors such as Utilities and Consumer Staples lagged the broader market. Lower demand and increased energy production, particularly in domestic natural gas, dampened commodity returns, with the S&P Energy Sector up just 2.3% for the year. In general, small and mid-cap stocks advanced in the same range as large stocks, while value stocks had a slight advantage over similarly sized stocks classified as “growth.”

Bond investors enjoyed positive returns, with the most conservative short-term government issuances producing minor advances, while riskier long-term and lower-quality bonds flourished. The bond markets were led by high-yield bonds, which tend to move in tandem with the stock markets. The Barclays High-Yield Bond Index was up 15.8%, the broader Barclay’s Corporate Bond Index advanced 9.8%, while the thin-yielding U.S. Treasuries showed a more modest 2.0% gain, as measured by Barclays U.S. Treasury Bond Index.

While investment returns were heartening to investors, the journey was uneven. Headlines seemed to provide an endless stream of uncertainties from around the world. The most potent of these influences was the sovereign debt crisis in Europe. Worries over the possible default of debt by the most economically troubled countries in southern Europe took the steam out of the year’s first quarter rally, as the S&P 500 dipped -9.6% between April 2 and June 1 when perceived progress on resolving Greece’s debt crisis fueled a rally. The S&P 500 advanced 15.4% between June 1 and September 14, as confidence rose for a positive resolution in Europe, fueled by European Central bank President Mario Draghi’s July statement that he would do “whatever it takes” to hold the Eurozone together. As the year progressed the nation’s attention turned away from Europe to the presidential election and only late in the period did investors begin to focus on the so-called “fiscal cliff.” The January 2013 deadline for automatic shifts to higher taxes and lower spending was partially fended off with a late-December, last-minute compromise which came too late to make up for the stock market’s December losses in response to nervousness regarding the pending fiscal cliff.

2

Ultra Series Fund | Management’s Discussion of Fund Performance | December 31, 2012

OUTLOOK

While optimism prevailed in 2012, we believe that the market may be overlooking the wide variety of risks that remain unresolved. These include worldwide credit issues, the upcoming battle over the domestic debt ceiling, and the possibility that the Federal Reserve may begin to shift its long-standing policy of near-zero rates. A sign that the “risk on” trade prevailed in 2012 was the rally in the stocks of speculative and highly leveraged companies, matched in the bond market by the preference for long-term and low-quality issuance. This risk concern shouldn’t suggest that we recommend shifting sensible asset allocation strategies. Instead, we believe investors should consider rebalancing portfolios and examining the underlying risks of their holdings.

In stocks, we remain convinced that fundamentals continue to count, and investors may benefit from owning solid companies with the ability to potentially produce strong results in all kinds of environments.

In bonds, we anticipate the 10-year Treasury yield will fluctuate in a much wider range than experienced in 2012 and volatility will increase. We believe the high corporate bond valuations have largely run their course and anticipate increased volatility in 2013 as demand for corporate bonds transitions to more normal levels, especially if investors begin to rebalance their portfolios to a more normal stock allocation. We estimate investment-grade bond returns in 2013 may equal the yield to maturity, and at worst believe a moderate increase in rates could challenge returns in 2013. As a result, we encourage investors to look beyond the broad classification such as “bond” to see what sort of interest-rate and credit risks they may be holding. Our outlook suggests that risk-averse investors with an interest in capital preservation should focus on higher-quality, and lower to intermediate maturity issues to mitigate the potential damages of rising rates or lower valuations on corporate bonds.

3

Ultra Series Fund | Management’s Discussion of Fund Performance | December 31, 2012

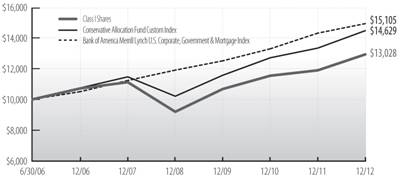

CONSERVATIVE ALLOCATION FUND

INVESTMENT STRATEGY HIGHLIGHTS

The Ultra Series Conservative Allocation Fund invests primarily in shares of registered investment companies (the “underlying funds”). The fund will be diversified among a number of asset classes and its allocation among underlying funds will be based on an asset allocation model developed by Madison Asset Management, LLC (“Madison”), the fund’s investment adviser.

The team may use multiple analytical approaches to determine the appropriate asset allocation, including, but not limited to:

| • | Asset allocation optimization analysis – considers the degree to which returns in different asset classes do or do not move together, and the fund’s aim to achieve a favorable overall risk profile for any targeted portfolio return. |

| • | Scenario analysis – historical and expected return data is analyzed to model how individual asset classes and combinations of asset classes would affect the fund under different economic and market conditions. |

| • | Fundamental analysis – draws upon Madison’s investment teams to judge each asset class against current and forecasted market condi-tions. Economic, industry and security analysis is used to develop return and risk expectations that may influence asset class selection. |

In addition, Madison employs a risk management sleeve within the fund for the purpose of risk reduction when and if conditions exist that require reduction of equity exposure.

PERFORMANCE HISTORY

Cumulative Performance of $10,000 Investment Since Inception1,2

| Average Annual Total Return through December 31, 20121,2 | ||||||||||||||||

| 1 Year | 3 Years | 5 Years | Since 6/30/06 Inception |

Since 5/1/09 Inception |

||||||||||||

| Ultra Series Conservative Allocation, Class I | 8.98 | % | 6.80 | % | 3.15 | % | 4.15 | % | — | |||||||

| Ultra Series Conservative Allocation, Class II | 8.71 | 6.53 | — | — | 9.38 | % | ||||||||||

| Conservative Allocation Fund Custom Index | 8.75 | 7.98 | 4.91 | 6.02 | 11.46 | |||||||||||

| Bank of America Merrill Lynch US Corp, Govt & Mortg Index | 4.43 | 6.24 | 6.03 | 6.54 | 6.46 | |||||||||||

See accompanying Notes to Management’s Discussion of Fund Performance.

4

Ultra Series Fund | Management’s Discussion of Fund Performance | December 31, 2012

Conservative Allocation Fund (concluded)

| PORTFOLIO ALLOCATION AS A PERCENTAGE OF NET ASSETS

AS OF 12/31/12 |

|||

| Bond Funds | 60 | % | |

| Foreign Bond Funds | 6 | % | |

| Stock Funds | 26 | % | |

| Foreign Stock Funds | 6 | % | |

| Money Market Funds and Other Net Assets | 2 | % | |

PERFORMANCE DISCUSSION

For the twelve-month period ended December 31, 2012, the Conservative Allocation Fund returned 8.98% (Class I Shares), while the custom blended Conservative Allocation benchmark returned 8.75%. While the fund beat its blended benchmark, it finished behind the Morningstar Conservative Allocation Category average return of 9.40%. We believe outperformance against the benchmark was a result of strong manager performance within the fixed income holdings and an overweight position to corporate bonds. In general, our allocation and manager selection leaned toward lower-risk, which we believe made a difference when compared to the Morningstar peer group in a year in which riskier assets showed a large gap over more conservative securities.

FUND CHANGES

After beginning the year with a modest underweight to equities, the fund ended the year roughly neutral relative to its benchmark. Our confidence to increase equities was underpinned by improved economic data and massive global central bank liquidity measures. In the middle of the year, we began to increase foreign equity exposure. This came on the heels of decisive action by Mario Draghi and the European Central Bank, which we believed removed much of the near-term tail risk from the European markets. However, the fund still remains underweight in comparison to its benchmark in foreign equities as we believe risks from Europe are still very much present. Late in the year, we began to materially reduce the level of both investment grade and high yield credit in the fund. We believe the credit markets have become fully valued and wanted to profit from these investments and dampen the risk level of the fixed income holdings. Finally, throughout the year we opportunistically increased exchange traded fund (“ETF”) holdings to better align the underlying cost structure and upside participation level of the fund.

5

Ultra Series Fund | Management’s Discussion of Fund Performance | December 31, 2012

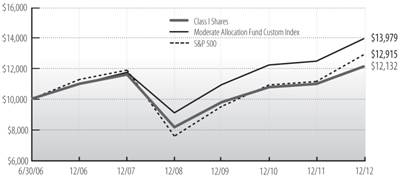

MODERATE ALLOCATION FUND

INVESTMENT STRATEGY HIGHLIGHTS

The Ultra Series Moderate Allocation Fund invests primarily in shares of registered investment companies (the “underlying funds”). The fund will be diversified among a number of asset classes and its allocation among underlying funds will be based on an asset allocation model developed by Madison Asset Management, LLC (“Madison”), the fund’s investment adviser.

The team may use multiple analytical approaches to determine the appropriate asset allocation, including, but not limited to:

| • | Asset allocation optimization analysis – considers the degree to which returns in different asset classes do or do not move together, and the fund’s aim to achieve a favorable overall risk profile for any targeted portfolio return. |

| • | Scenario analysis – historical and expected return data is analyzed to model how individual asset classes and combinations of asset classes would affect the fund under different economic and market conditions. |

| • | Fundamental analysis – draws upon Madison’s investment teams to judge each asset class against current and forecasted market conditions. Economic, industry and security analysis is used to develop return and risk expectations that may influence asset class selection. |

In addition, Madison employs a risk management sleeve within the fund for the purpose of risk reduction when and if conditions exist that require reduction of equity exposure.

PERFORMANCE HISTORY

Cumulative Performance of $10,000 Investment Since Inception1,2

| Average Annual Total Return through December 31, 20121,2 | ||||||||||||||||

| 1 Year | 3 Years | 5 Years | Since 6/30/06 Inception |

Since 5/1/09 Inception |

||||||||||||

| Ultra Series Moderate Allocation, Class I | 10.54 | % | 7.52 | % | 0.90 | % | 3.01 | % | — | |||||||

| Ultra Series Moderate Allocation, Class II | 10.26 | 7.26 | — | — | 10.99 | % | ||||||||||

| Moderate Allocation Fund Custom Index | 11.94 | 8.55 | 3.55 | 5.28 | 14.75 | |||||||||||

| S&P 500 Index | 16.00 | 10.87 | 1.66 | 4.01 | 16.77 | |||||||||||

See accompanying Notes to Management’s Discussion of Fund Performance.

6

Ultra Series Fund | Management’s Discussion of Fund Performance | December 31, 2012

Moderate Allocation Fund (concluded)

| PORTFOLIO ALLOCATION AS A PERCENTAGE OF NET ASSETS

AS OF 12/31/12 |

|||

| Bond Funds | 37 | % | |

| Foreign Bond Funds | 3 | % | |

| Stock Funds | 47 | % | |

| Foreign Stock Funds | 11 | % | |

| Money Market Funds and Other Net Assets | 2 | % | |

PERFORMANCE DISCUSSION

For the twelve-month period ended December 31, 2012, the Moderate Allocation Fund returned 10.54% (Class I Shares), while the custom blended Moderate Allocation benchmark returned 11.94%. The fund also trailed the Morningstar Moderate Allocation Category average return of 11.72%. In a year of strong equity returns, the fund was hurt by an underweight position to equities at the start of the period, even as it ended the year roughly neutral relative to its benchmark. We also underweighted foreign equities in a year in which the broad international indices were stronger than the domestic indices. Our confidence to increase equities was underpinned by improved economic data and massive global central bank liquidity measures.

FUND CHANGES

In the middle of the year, we began to increase foreign equity exposure. This came on the heels of decisive action by Mario Draghi and the European Central Bank, which we believed removed much of the near-term tail risk from the European markets. However, the fund still remains underweight in comparison to our benchmark in foreign equities as we believe risks from Europe are still very much present. Late in the year, we began to materially reduce the level of both investment grade and high yield credit in the fund. We believe that the credit markets have become fully valued and wanted to profit from these investments and dampen the risk level of the fixed income holdings. Finally, throughout the year we opportunistically increased exchange traded fund (“ETF”) holdings to better align the underlying cost structure and upside participation level of the fund.

7

Ultra Series Fund | Management’s Discussion of Fund Performance | December 31, 2012

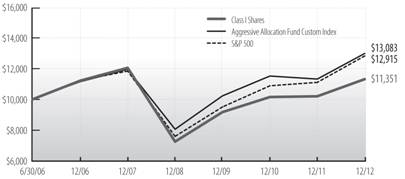

AGGRESSIVE ALLOCATION FUND

INVESTMENT STRATEGY HIGHLIGHTS

The Ultra Series Aggressive Allocation Fund invests primarily in shares of registered investment companies (the “underlying funds”). The fund will be diversified among a number of asset classes and its allocation among underlying funds will be based on an asset allocation model developed by Madison Asset Management, LLC (“Madison”), the fund’s investment adviser.

The team may use multiple analytical approaches to determine the appropriate asset allocation, including, but not limited to:

| • | Asset allocation optimization analysis – considers the degree to which returns in different asset classes do or do not move together, and the fund’s aim to achieve a favorable overall risk profile for any targeted portfolio return. |

| • | Scenario analysis – historical and expected return data is analyzed to model how individual asset classes and combinations of asset classes would affect the fund under different economic and market conditions. |

| • | Fundamental analysis – draws upon Madison’s investment teams to judge each asset class against current and forecasted market conditions. Economic, industry and security analysis is used to develop return and risk expectations that may influence asset class selection. |

In addition, Madison employs a risk management sleeve within the fund for the purpose of risk reduction when and if conditions exist that require reduction of equity exposure.

PERFORMANCE HISTORY

Cumulative Performance of $10,000 Investment Since Inception1,2

| Average Annual Total Return through December 31, 20121,2 | ||||||||||||||||

| 1 Year | 3 Years | 5 Years | Since 6/30/06 Inception |

Since 5/1/09 Inception |

||||||||||||

| Ultra Series Aggressive Allocation, Class I | 11.34 | % | 7.53 | % | -1.29 | % | 1.97 | % | — | |||||||

| Ultra Series Aggressive Allocation, Class II | 11.06 | 7.27 | — | — | 12.56 | % | ||||||||||

| Aggressive Allocation Fund Custom Index | 15.18 | 8.56 | 1.71 | 4.21 | 17.77 | |||||||||||

| S&P 500 Index | 16.00 | 10.87 | 1.66 | 4.01 | 16.77 | |||||||||||

See accompanying Notes to Management’s Discussion of Fund Performance.

8

Ultra Series Fund | Management’s Discussion of Fund Performance | December 31, 2012

Aggressive Allocation Fund (concluded)

| PORTFOLIO ALLOCATION AS A PERCENTAGE OF NET ASSETS

AS OF 12/31/12 |

|||

| Bond Funds | 13 | % | |

| Foreign Bond Funds | 1 | % | |

| Stock Funds | 67 | % | |

| Foreign Stock Funds | 18 | % | |

| Money Market Funds and Other Net Assets | 1 | % | |

PERFORMANCE DISCUSSION

For the twelve-month period ended December 31, 2012, the Aggressive Allocation Fund returned 11.34% (Class I Shares), while the custom blended Aggressive Allocation benchmark return of 15.18%. The fund’s performance also trailed the Morningstar Aggressive Allocation Category average return of 13.42%. Underperformance was largely a result of our underweighting to equities during the first months of the year versus the benchmark during a very strong, double-digit quarter. Additionally, weak relative returns in the fund’s core U.S. equities provided a drag on performance. In general, these results reflect the fund’s overall risk posture. We believe that even an aggressive allocation fund should be constructed to have lower volatility than a pure equity portfolio. This philosophy does have the potential to constrain performance when worldwide equities are not only up strongly, but favor lower-quality, speculative companies as was the case in 2012.

FUND CHANGES

After beginning the year with a modest underweight to equities, the fund ended the year roughly neutral relative to its benchmark. Our confidence to increase equities was underpinned by improved economic data and massive global central bank liquidity measures. In the middle of the year, we began to increase foreign equity exposure. This came on the heels of decisive action by Mario Draghi and the European Central Bank, which we believed removed much of the near-term tail risk from the European markets. By the end of the year, the fund’s overall international equity allocation moved to roughly neutral relative to the benchmark, although the fund still remains underweight European equities. Finally, late in the year we began to materially reduce the level of both investment grade and high yield credit in the fund. We believe that the credit markets have become fully valued and wanted to profit from these investments and dampen the risk level of the fixed income holdings. Finally, throughout the year we opportunistically increased exchange traded fund (“ETF”) holdings to better align the underlying cost structure and upside participation level of the fund.

9

Ultra Series Fund | Management’s Discussion of Fund Performance | December 31, 2012

MONEY MARKET FUND

INVESTMENT STRATEGY HIGHLIGHTS

The Ultra Series Money Market Fund invests exclusively in U.S. dollar-denominated money market securities maturing in thirteen months or less from the date of purchase. These securities will be obligations of the U.S. Government and its agencies and instrumentalities, but may also include securities issued by U.S. and foreign financial institutions, corporations, municipalities, foreign governments, and multi-national organizations, such as the World Bank. The fund may invest in mortgage-backed and asset-backed securities, including those representing pools of mortgage, commercial, or consumer loans originated by credit unions or other financial institutions.

| PORTFOLIO ALLOCATION AS A PERCENTAGE OF NET ASSETS

AS OF 12/31/12 |

|||

| Federal Farm Credit Bank | 5 | % | |

| Fannie Mae | 17 | % | |

| Federal Home Loan Bank | 23 | % | |

| Freddie Mac | 22 | % | |

| U.S. Treasury Notes | 8 | % | |

| Commercial Paper | 19 | % | |

| Cash and Other Net Assets | 6 | % | |

10

Ultra Series Fund | Management’s Discussion of Fund Performance | December 31, 2012

This page was intentionally left blank.

11

Ultra Series Fund | Management’s Discussion of Fund Performance | December 31, 2012

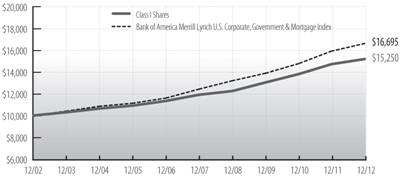

BOND FUND

INVESTMENT STRATEGY HIGHLIGHTS

Under normal circumstances, the Ultra Series Bond Fund invests at least 80% of its assets in bonds. To keep current income relatively stable and to limit share price volatility, the fund emphasizes investment grade securities and maintains an intermediate (typically 3-6 year) average portfolio duration (a measure of a security’s price sensitivity to changes in interest rates). The fund also strives to minimize risk in the portfolio by making strategic decisions relating to credit risk and yield curve outlook. The fund may invest in corporate debt securities, U.S. Government debt securities, foreign government debt securities, non-rated debt securities, and asset-backed, mortgage-backed and commercial mortgage-backed securities.

PERFORMANCE HISTORY

Cumulative Performance of $10,000 Investment Since Inception1

| Average Annual Total Return through December 31, 20121 | ||||||||||||||||

| 1 Year | 3 Years | 5 Years | 10 Years | Since 5/1/09 Inception |

||||||||||||

| Ultra Series Bond, Class I | 3.21 | % | 5.28 | % | 5.03 | % | 4.31 | % | — | |||||||

| Ultra Series Bond, Class II | 2.96 | 5.02 | — | — | 5.63 | % | ||||||||||

| Bank of America Merrill Lynch US Corp, Govt & Mortg Index | 4.43 | 6.24 | 6.03 | 5.26 | 6.46 | |||||||||||

See accompanying Notes to Management’s Discussion of Fund Performance.

12

Ultra Series Fund | Management’s Discussion of Fund Performance | December 31, 2012

Bond Fund (concluded)

| PORTFOLIO ALLOCATION AS A PERCENTAGE OF NET ASSETS

AS OF 12/31/12 |

|||

| Asset Backed | 1 | % | |

| Corporate Notes and Bonds | 28 | % | |

| Mortgage Backed | 16 | % | |

| U.S. Government and Agency Obligations | 51 | % | |

| Cash and Other Net Assets | 4 | % | |

PERFORMANCE DISCUSSION

For the twelve-month period ended December 31, 2012, the Ultra Series Bond Fund returned 3.21% (Class I shares), while the Bank of America Merrill Lynch U.S. Corp. Government & Mortgage Index returned 4.43%. The most important factor for the underperformance was a significant underweighting to banks and to financials in general. The banking sector earned an excess return over Treasuries of more than 13% which was almost as high a return as the high yield market in 2012. Sector allocation relative to this sector helps explain performance in 2012. Fund performance was also modestly hurt by an underweighting to the mortgage sector and by its relatively shorter duration in a declining rate environment. The performance was positively impacted by an overweighting of corporate bonds in general and BBB rated securities in particular. It also benefitted from individual security selection in that a number of investments such as Transocean Inc. and Westvaco Corp. were perceived as improving. Sector allocation and duration remained stable throughout the period.

13

Ultra Series Fund | Management’s Discussion of Fund Performance | December 31, 2012

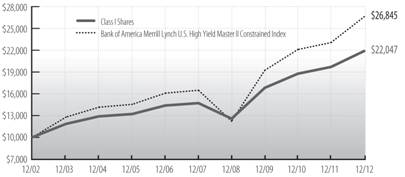

HIGH INCOME FUND

INVESTMENT STRATEGY HIGHLIGHTS

The Ultra Series High Income Fund invests primarily in lower-rated, higher-yielding income bearing securities, such as “junk” bonds. Because the performance of these securities has historically been strongly influenced by economic conditions, the fund may emphasize security selection in business sectors that favor the economic outlook. Under normal market conditions, the fund invests at least 80% of its assets in bonds rated lower than investment grade (BBB/Baa) and their unrated equivalents or other high-yielding securities.

PERFORMANCE HISTORY

Cumulative Performance of $10,000 Investment Since Inception1

| Average Annual Total Return through December 31, 20121 | ||||||||||||||||

| 1 Year | 3 Years | 5 Years | 10 Years | Since 5/1/09 Inception |

||||||||||||

| Ultra Series High Income, Class I | 11.23 | % | 9.28 | % | 8.36 | % | 8.23 | % | — | |||||||

| Ultra Series High Income, Class II | 10.95 | 9.01 | — | — | 12.12 | % | ||||||||||

| Bank of America Merrill Lynch US High Yield Master II, Constrained | 15.55 | 11.54 | 10.14 | 10.38 | 18.54 | |||||||||||

See accompanying Notes to Management’s Discussion of Fund Performance.

14

Ultra Series Fund | Management’s Discussion of Fund Performance | December 31, 2012

High Income Fund (concluded)

| SECTOR ALLOCATION AS A PERCENTAGE OF NET ASSETS

AS OF 12/31/12 |

|||

| Consumer Discretionary† | 35 | % | |

| Consumer Staples | 6 | % | |

| Energy | 14 | % | |

| Financials | 3 | % | |

| Health Care | 9 | % | |

| Industrials | 7 | % | |

| Information Technology | 3 | % | |

| Materials | 9 | % | |

| Telecommunication Services | 6 | % | |

| Utilities | 2 | % | |

| Cash and Other Net Assets | 6 | % | |

| †Consumer Discretionary includes securities in the following industries: auto components; automobiles; hotels, restaurants & leisure; household durables; media; specialty retail; and textiles, apparel & luxury goods. | |||

PERFORMANCE DISCUSSION

The Ultra Series High Income Fund was more conservative and less volatile than the overall high yield market during 2012. The fund produced a return of 11.23% (Class I shares), underperforming the Bank of America Merrill Lynch U.S. High Yield Master II Constrained Index (HUCO), which returned 15.55%. Being underweight the Financials Sector was a key detractor, as was negative selection within the Telecommunication Services Sector. However, being underweight the Energy Sector contributed strongly to performance, as did positive selection within the Utilities Sector.

The high-yield bond market rallied strong through most of 2012, capping off a banner year in which overwhelmingly positive technical forces and strong fundamentals herded yield-hungry investors to the high yield bond market’s relative value in a low-interest rate environment. We believe high yield was a direct beneficiary of the U.S. Federal Reserve’s latest round of quantitative easing and near-zero interest rate policies, which drove investors to purchase riskier assets and issuers to capitalize on the favorable market conditions. While 15% returns for 2013 are unlikely, we believe the market is well positioned to continue on a strong path. Demand for high yield remained solid through the fourth quarter and showed little sign of slowing. With anemic economic growth, an entrenched low-interest rate environment, modest defaults and strong corporate balance sheets, high yield seems well positioned heading into 2013.

FUND CHANGES

The fund was selectively active as we increased exposure in more stable credits with higher earnings predictability and reduced holdings of volatile components. For the year, there were 130 purchases aggregating $45.3 million and 183 sales totaling $50.8 million. In terms of new issues, the fund participated in 48 new deals. We increased sector allocations in Oil & Gas, Media-Cable, and Automotive while reducing holdings in Utilities, Telecommunication Services and Media-Diversified & Services. The portfolio also shifted towards higher ratings categories, with a roughly 1% increase in B rated bonds and 1% decrease in CCC rated exposure. As such, the portfolio’s ratings weightings were 33% in BB rated bonds, 48% in B rated bonds and 13% in CCC rated bonds. Also, as of year-end, the fund had fully exited all convertible bond positions.

15

Ultra Series Fund | Management’s Discussion of Fund Performance | December 31, 2012

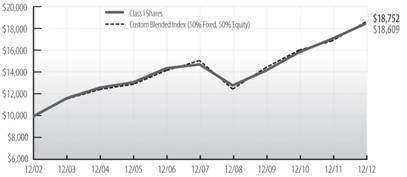

DIVERSIFIED INCOME FUND

INVESTMENT STRATEGY HIGHLIGHTS

The Ultra Series Diversified Income Fund seeks income by investing in a broadly diversified array of securities including bonds, common stocks, real estate securities, foreign market bonds and stocks and money market instruments. Bonds, stock and cash components will vary, reflecting the portfolio managers’ judgments of the relative availability of attractively yielding and priced stocks and bonds. Generally, however, bonds will constitute up to 80% of the fund’s assets, stocks will constitute up to 60% of the fund’s assets, real estate securities will constitute up to 25% of the fund’s assets, foreign stocks and bonds will constitute up to 25% of the fund’s assets and money market instruments may constitute up to 25% of the fund’s assets. The fund intends to limit the investment in lower credit quality bonds to less than 50% of the fund’s assets. The balance between the two strategies of the fund (fixed income and equity investing) is determined after reviewing the risks associated with each type of investment, with the goal of meaningful risk reduction as market conditions demand. The fund typically sells a stock when the fundamental expectations for producing competitive yields at an acceptable level of price risk no longer apply, the price exceeds the intrinsic value or other stocks appear more attractive.

PERFORMANCE HISTORY

Cumulative Performance of $10,000 Investment Since Inception1

| Average Annual Total Return through December 31, 20121 | ||||||||||||||||

| 1 Year | 3 Years | 5 Years | 10 Years | Since 5/1/09 Inception |

||||||||||||

| Ultra Series Diversified Income, Class I | 8.16 | % | 9.33 | % | 4.66 | % | 6.41 | % | — | |||||||

| Ultra Series Diversified Income, Class II | 7.89 | 9.06 | — | — | 11.36 | % | ||||||||||

| Custom Blended Index (50% Fixed, 50% Equity) | 10.24 | 8.90 | 4.31 | 6.49 | 11.85 | |||||||||||

| S&P 500 Index | 16.00 | 10.87 | 1.66 | 7.10 | 16.77 | |||||||||||

| Bank of America Merrill Lynch US Corp, Govt & Mortg Index | 4.43 | 6.24 | 6.03 | 5.26 | 6.46 | |||||||||||

See accompanying Notes to Management’s Discussion of Fund Performance.

16

Ultra Series Fund | Management’s Discussion of Fund Performance | December 31, 2012

Diversified Income Fund (concluded)

| PORTFOLIO ALLOCATION AS A PERCENTAGE OF NET ASSETS

AS OF 12/31/12 |

|||

| Common Stocks | 55 | % | |

| Corporate Notes and Bonds | 16 | % | |

| Mortgage Backed | 7 | % | |

| U.S. Government and Agency Obligations | 18 | % | |

| Cash and Other Net Assets | 4 | % | |

PERFORMANCE DISCUSSION

During the twelve-month period, the Diversified Income Fund gained 8.16% (Class I Shares), while the Custom Blended Index returned 10.24%. The S&P 500 Index of large-cap stocks returned 16.00%, and the broad bond market returned 4.43% as measured by the Bank of America Merrill Lynch U.S. Corporate, Government & Mortgage Index. The portfolio was conservatively positioned during the period, with approximately 55% of the fund invested in mature dividend-paying stocks and 45% in bonds. The fund’s stock portfolio did not keep up with the market as measured by the S&P 500 Index. Compared to the S&P 500 Index, sector allocation was positive due mainly to the fund’s underweight position in Technology, while stock selection was detractive with the largest impact from underperforming stocks in Technology, Health Care and Industrial Sectors. Intel and Broadridge Financial Solutions hurt results in Technology, while Johnson & Johnson, Merck and Medtronic negatively impact performance in Health Care. Within Industrials, Norfolk Southern and UPS lagged. On the positive side, Ensco, Diageo and Time Warner contributed positively to returns.

The bond portion of the fund contributed positively to overall fund performance, but did not pace the overall market as measured by the Bank of America Merrill Lynch U.S. Corporate, Government & Mortgage Index. The market heavily favored lower quality and longer bonds, the areas of the market subject to the greatest potential volatility. During the annual period, Barclays measured the top-rated intermediate-term corporate bonds (AAA) advancing 3.19% while the lowest-rated segment (CA-D) rose 27.61%. The fund is managed with an emphasis on risk control and the goal of moderating losses in a down market. As a result, the fund held shorter bonds and higher quality issuance, areas which had modest returns in a year in which more speculative issues with higher yields were preferred.

FUND CHANGES

Stock sector allocation was generally stable through this period, even as we made a number of portfolio changes. We sold Broadridge and Norfolk Southern due to worries about sub-par earnings growth related to a lack of pricing power. The other stocks mentioned above appear to us to have solid prospects and we continue to hold them. We will look to add on weakness or fundamental improvement. We have maintained a conservative posture on the bond side, believing that the long bull market in bonds has squeezed the bulk of the value out of this sector. Our strategy is to emphasize capital preservation, giving us the ability to add yield should the opportunity arise.

17

Ultra Series Fund | Management’s Discussion of Fund Performance | December 31, 2012

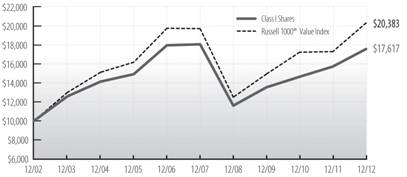

LARGE CAP VALUE FUND

INVESTMENT STRATEGY HIGHLIGHTS

The Ultra Series Large Cap Value Fund will, under normal market conditions, invest primarily in large cap stocks. The fund follows a “value” approach, meaning the portfolio managers seek to invest in stocks at prices below their perceived intrinsic value as estimated based on fundamental analysis of the issuing company and its prospects. By investing in value stocks, the fund attempts to limit the downside risk over time but may also produce smaller gains than other stock funds if their intrinsic values are not realized by the market or if growth-oriented investments are favored by investors. The fund will diversify its holdings among various industries and among companies within those industries. The fund typically sells a stock when the fundamental expectations for buying it no longer apply, the price exceeds its intrinsic value or other stocks appear more attractively priced relative to their intrinsic values.

PERFORMANCE HISTORY

Cumulative Performance of $10,000 Investment Since Inception1

| Average Annual Total Return through December 31, 20121 | ||||||||||||||||

| 1 Year | 3 Years | 5 Years | 10 Years | Since 5/1/09 Inception |

||||||||||||

| Ultra Series Large Cap Value, Class I | 11.82 | % | 9.15 | % | -0.56 | % | 5.83 | % | — | |||||||

| Ultra Series Large Cap Value, Class II | 11.55 | 8.88 | — | — | 14.19 | % | ||||||||||

| Russell 1000 Value Index | 17.51 | 10.86 | 0.59 | 7.38 | 16.81 | |||||||||||

See accompanying Notes to Management’s Discussion of Fund Performance.

PERFORMANCE DISCUSSION

The Ultra Large Cap Value Fund returned 11.82% (Class I Shares) for the annual period. During the twelve-month period ended December 31, 2012, large-cap value stocks demonstrated somewhat better performance than the robust returns of the overall market. With the S&P 500 up 16.00%, the S&P 500 Value Index rose 17.76% and the Russell 1000® Value Index rose 17.51%. While we were pleased to deliver double-digit returns to shareholders, the fund’s return of 11.82% was disappointing in light of the strength in the value indices. However, the underperformance in 2012 was very much in line with the outperformance in 2011. This is an often-observed market pattern of market

18

Ultra Series Fund | Management’s Discussion of Fund Performance | December 31, 2012

Large Cap Value Fund (concluded)

| SECTOR ALLOCATION AS A PERCENTAGE OF NET ASSETS

AS OF 12/31/12 |

|||||||

| Fund | Russell 1000® Value Index |

||||||

| Consumer Discretionary | 9 | % | 8 | % | |||

| Consumer Staples | 10 | % | 7 | % | |||

| Energy | 14 | % | 16 | % | |||

| Financials† | 26 | % | 28 | % | |||

| Health Care | 17 | % | 12 | % | |||

| Industrials | 12 | % | 9 | % | |||

| Information Technology | 4 | % | 6 | % | |||

| Materials | 3 | % | 4 | % | |||

| Telecommunication Services | 1 | % | 3 | % | |||

| Utilities | — | % | 7 | % | |||

| Cash and Other Net Assets | 4 | % | — | % | |||

| †Financials includes securities in the following industries: capital markets; commercial banks; insurance; and real estate management & development. | |||||||

fluctuation, as the stocks that outperform during one period revert back to the mean over the subsequent one.

The most important component of the fund’s underperformance was the relative returns across the quality spectrum. As measured by Merrill Lynch Quantitative Strategy, A+ and A-rated stocks each returned 10.4% while B-rated stocks were up 18.9% and the lowest-rated segment of C&D stocks returned 25.3%. We have a preference for stocks whose strong fundamentals put them in the higher quality categories.

Stock selection and sector allocation were also a relative drag on performance. The fund’s stocks underperformed their S&P Sectors in Industrial, Financials and Energy. While we have great confidence in insurance holding Markel, it was punished for an acquisition which we believe will turn out to be profitable. While Markel contributed to the financial underperformance, the greater impact came from not owning what we believe to be the riskier, credit-sensitive banks. Other lagging stocks included Norfolk Southern and UPS in Industrials and Canadian Natural Resources and Occidental in Energy.

We continue to find value in stocks that have above-average dividend yields and that are likely to provide dividend growth. These stocks make up 75% of the Large Cap Value portfolio. We have a favorable outlook for this group of blue chip, dividend-paying stocks. The average yield of stock held in the portfolio at year-end was 2.5%, higher than the yield on the S&P 500 of 2.1% and the 10-year Treasury bond yield of 1.8%. High dividend stocks have historically been more resilient in times of stress and sharply dropping markets, which makes the Large-Cap Value portfolio particularly attractive to investors who want the growth potential of stocks, but have concerns regarding downside volatility.

FUND CHANGES

Over the course of the year the fund did not undergo any major strategic or sector shifts. Weighting in the top-performing Financials Sector was up 2.6%, Health Care was up 2.8% and Consumer Discretionary was up 2.9%. The weighting in Technology fell -3.5%, Utilities decreased -2.8% as we stepped out of the sector entirely, and Telecommunication Services fell -1.2%. Among the new issues in the portfolio were Health Care stock Becton Dickinson, and Consumer Discretionary holding Viacom. We sold Broadridge Financial Solutions, IBM and Paychex out of Information Technology, added Accenture and Automatic Data Processing, and trimmed positions in Intel and Microsoft. In exiting the Utilities Sector we sold Exelon and First Energy.

19

Ultra Series Fund | Management’s Discussion of Fund Performance | December 31, 2012

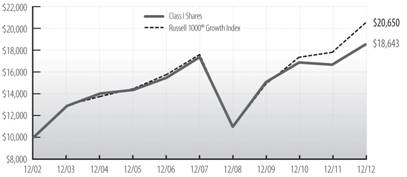

LARGE CAP GROWTH FUND

INVESTMENT STRATEGY HIGHLIGHTS

The Ultra Series Large Cap Growth Fund invests primarily in common stocks of larger companies and will, under normal market conditions, maintain at least 80% of its assets in large cap stocks. The fund follows a “growth” approach, meaning the portfolio managers seek stocks that have low market prices relative to their perceived growth capabilities as estimated based on fundamental analysis of the issuing companies and their prospects. The fund typically seeks higher earnings growth capabilities in the stocks it purchases, and may include some companies undergoing more significant changes in their operations or experiencing significant changes in their markets. The fund will diversify its holdings among various industries and among companies within those industries. The fund has an active trading strategy which will lead to more portfolio turnover than a more passively-managed fund. The fund typically sells a stock when the fundamental expectations for buying it no longer apply, the price exceeds its perceived value or other stocks appear more attractively priced relative to their prospects.

PERFORMANCE HISTORY

Cumulative Performance of $10,000 Investment Since Inception1

| Average Annual Total Return through December 31, 20121 | ||||||||||||||||

| 1 Year | 3 Years | 5 Years | 10 Years | Since 5/1/09 Inception |

||||||||||||

| Ultra Series Large Cap Growth, Class I | 11.20 | % | 7.21 | % | 1.32 | % | 6.43 | % | — | |||||||

| Ultra Series Large Cap Growth, Class II | 10.93 | 6.94 | — | — | 12.56 | % | ||||||||||

| Russell 1000® Growth Index | 15.26 | 11.35 | 3.12 | 7.52 | 17.40 | |||||||||||

See accompanying Notes to Management’s Discussion of Fund Performance.

PERFORMANCE DISCUSSION

For the twelve-month period ended December 31, 2012 the Large Cap Growth Fund returned 11.20% (Class I Shares), while the Russell 1000® Growth Index returned 15.26%. We were disappointed by this relative return, which was handicapped by the outperformance of lower-quality stocks over higher-quality companies and underperformance in individual stock selection.

From a sector attribution perspective, the fund’s two largest detractors were Health Care and Information Technology. Health Care as a sector produced above-benchmark results for the period, with particular strength in the biotech

20

Ultra Series Fund | Management’s Discussion of Fund Performance | December 31, 2012

Large Cap Growth Fund (concluded)

| SECTOR ALLOCATION AS A PERCENTAGE OF NET ASSETS

AS OF 12/31/12 |

|||||||

| Fund | Russell 1000® Growth Index |

||||||

| Consumer Discretionary | 17 | % | 17 | % | |||

| Consumer Staples | 8 | % | 12 | % | |||

| Energy | 5 | % | 4 | % | |||

| Financials | 5 | % | 5 | % | |||

| Health Care | 10 | % | 12 | % | |||

| Industrials | 12 | % | 13 | % | |||

| Information Technology† | 33 | % | 31 | % | |||

| Materials | 4 | % | 4 | % | |||

| Telecommunication Services | 2 | % | 2 | % | |||

| Utilities | — | % | — | % | |||

| Cash and Other Net Assets | 4 | % | — | % | |||

| †Information Technology includes securities in the following industries: communications equipment; computers and peripherals; electrical equipment; internet software & services; IT services; semiconductors & semiconductor equipment; and software. | |||||||

area. The fund’s biotech holdings produced positive returns, but did not include the sector leaders. For instance, the portfolio’s largest biotech holding was Celgene, one of the five largest domestic biotech firms. It returned 16.08% in 2012, while the average return of the other top four largest biotechs, none of which were held by the fund, was 46.92%. We believe this leaves Celgene with unrealized upside potential in upcoming quarters.

The technology holdings in the Russell 1000® Growth benchmark advanced 17.52%, ahead of the overall return of the boarder Russell 1000® Index’s 16.42%. The portfolio had some strong stocks in this area, including Apple. However, the fund had two disappointing holdings, Sandisk and MICROS Systems. Sandisk is a flash memory company whose products appear in tablets and smart phones. Excess industry-wide capacity restrained expected pricing advances. Micros, a provider of hotel and restaurant reservation systems, is one of our higher conviction holdings. The stock dropped over the course of the year as the hospitality industry continued to struggle in the slow-growth economic climate, depressing sales of new product.

The fund had strong relative performance in Consumer Staples and Energy, producing returns above the Index sectors of 0.75% and 0.60% respectively. In Consumer Staples Hershey was additive as it gained almost 20% for the year. The fund’s holding in Petrobras, a Brazilian based international oil company, was also additive to performance.

Finally, the fund began the year with exposure to several smaller companies which appeared poised for strong returns. This strategy did not work as planned. For instance, Acme Packet, a technology company whose products are essential to the build-out of higher speed digital networks, received reduced orders from some major telecom companies and the stock price declined.

FUND CHANGES

With a recognition near mid-year that global growth was likely to remain tepid for some time, we reduced the fund’s exposure to economically sensitive, smaller companies. We deployed the proceeds into larger, higher-quality issues while sector diversification increased within the portfolio. Entering 2013, we believe the operating environment for companies should continue to be challenging, but absent another major unforeseen economic shock, can continue to produce selective opportunities for growth. Consequently, the fund remains focused on companies which have intrinsic reasons for driving success. For example, Google in the internet space, continues its innovation in global search and to maintain global leadership with its Android operating system for smart phones and tablets. Given expectations for the continued strength in mobile computing, the fund invested in a number of companies which continue to gain share from older ways of doing business, such as Nuance, the leading voice recognition company whose products are used in Apple’s Siri offering as well as in health care transcription services.

21

Ultra Series Fund | Management’s Discussion of Fund Performance | December 31, 2012

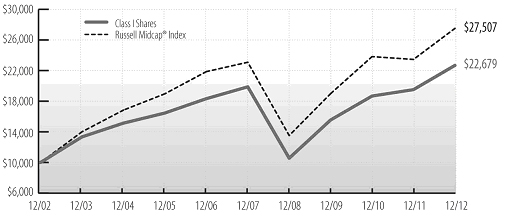

MID CAP FUND

INVESTMENT STRATEGY HIGHLIGHTS

The Ultra Series Mid Cap Fund generally invests in common stocks of midsize companies and will, under normal market conditions, maintain at least 80% of its assets in mid cap securities. However, the fund will not automatically sell a stock because its market capitalization has changed and such positions may be increased through additional purchases. The fund seeks attractive long-term returns through bottom-up security selection based on fundamental analysis in a diversified portfolio of high-quality growth companies with attractive valuations. These will typically be industry leading companies in niches with strong growth prospects. The fund’s portfolio managers believe in selecting stocks for the fund that show steady, sustainable growth and reasonable valuations. As a result, stocks of issuers that are believed to have a blend of both value and growth potential will be selected for investment. Stocks are generally sold when target prices are reached, company fundamentals deteriorate or more attractive stocks are identified.

PERFORMANCE HISTORY

Cumulative Performance of $10,000 Investment Since Inception1

| Average Annual Total Return through December 31, 20121 | ||||||||||||||||||||

| Since | ||||||||||||||||||||

| 5/1/09 | ||||||||||||||||||||

| 1 Year | 3 Years | 5 Years | 10 Years | Inception | ||||||||||||||||

| Ultra Series Mid Cap, Class I | 16.24 | % | 13.41 | % | 2.67 | % | 8.53 | % | — | |||||||||||

| Ultra Series Mid Cap, Class II | 15.95 | 13.13 | — | — | 17.84 | % | ||||||||||||||

| Russell Midcap Index | 17.28 | 13.15 | 3.57 | 10.65 | 19.73 | |||||||||||||||

See accompanying Notes to Management’s

Discussion of Fund Performance.

PERFORMANCE DISCUSSION

For the year ended December 31, 2012, the Mid Cap Fund gained 16.24% (Class I Shares), while the Russell Midcap® Index returned 17.28%. While the fund trailed the benchmark slightly, we were content with performance for the year, considering the market environment which favored riskier stocks over fundamentally solid ones. The strongest returns came from the market’s best returning sectors: Financials and Consumer Discretionary. The fund’s financials holdings, which emphasized insurance firms over credit-sensitive banks, did not keep up with the 24.1% return of the Russell Midcap® Index’s Financials Sector, but did contribute to the fund’s positive results second only to Consumer

22

Ultra Series Fund | Management’s Discussion of Fund Performance | December 31, 2012

Mid Cap Fund (concluded)

|

SECTOR ALLOCATION AS A PERCENTAGE OF NET ASSETS AS OF 12/31/12 |

||||||||

| Russell | ||||||||

| Midcap® | ||||||||

| Fund | Index | |||||||

| Consumer Discretionary | 21 | % | 17 | % | ||||

| Consumer Staples | 3 | % | 6 | % | ||||

| Energy | 7 | % | 7 | % | ||||

| Financials | 23 | % | 20 | % | ||||

| Health Care | 8 | % | 10 | % | ||||

| Industrials | 20 | % | 13 | % | ||||

| Information Technology | 4 | % | 13 | % | ||||

| Materials | 7 | % | 7 | % | ||||

| Telecommunication | ||||||||

| Services | – | 2 | % | |||||

| Utilities | – | 5 | % | |||||

| Cash and Other Net Assets | 7 | % | – | |||||

Discretionary. The fund’s Consumer Discretionary holdings were mixed, but overall additive to performance. While the Energy Sector was relatively weak, with the Index sector up 7.2%, the fund’s Energy holdings saw relative strength. The fund lost ground to the Index in the Health Care and Technology Sectors. Among individual holdings, the largest contributions to return came from Brookfield Asset Management, Copart Inc. and M&T Bank. On the other hand, stocks which trailed the market’s return included technology holdings Micros Systems, Broadridge Financial Solutions and FLIR Systems, the latter two of which were sold during the course of the year.

FUND CHANGES

We made relatively few changes to the portfolio

over the year, but did find some attractive opportunities. Examining two of these

illustrates our bottom-up stock selection process. Expeditors International is a

stock we purchased early in the fall and a good example of the sort of company we

like to hold when valuations are attractive. We had an opportunity to purchase the

company at 15 times forward earnings, excluding the cash on the balance sheet. We

think of Expeditors as a travel agent for freight movement across the globe. In

addition to shipping goods it provides other services such as distribution management,

cargo insurance, and customs clearance. The business model is “asset light” since there is very little need for capital expenditures. The company has

what we believe to be a solid balance sheet, with over six dollars a share in net

cash, and a highly capable management team. Recent valuation has been compressed

due to concerns over global growth and weak air travel and ocean travel volumes.

We believe these are temporary issues and conditions will improve once the global

macro-economy and global trade improve.

Another addition of the portfolio early

in the fourth quarter was Crown Holding, a manufacturer of aluminum cans which are

used for beverages, food products and other consumer products. The industry in which

it participates is a global oligopoly, so there are just a few players. Management

is shareholder friendly and has a track record of wise allocation of capital. Crown

Holding has invested to build capacity in developing markets, particularly China

and Brazil. These markets may generate higher returns on invested capital than developed

markets, and future growth should be stronger. We believe this investment will pay

off, going forward. We purchased the stock at what we calculate to be about 8.5

times future normalized free cash flow, which we believe was an attractive multiple.

23

Ultra Series Fund | Management’s Discussion of Fund Performance | December 31, 2012

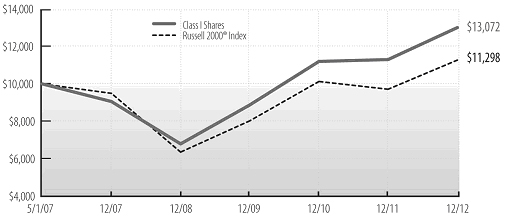

SMALL CAP FUND

INVESTMENT STRATEGY HIGHLIGHTS

The Ultra Series Small Cap Fund invests primarily in a diversified mix of common stocks of small cap U.S. companies that are believed to be undervalued by various measures and offer sound prospects for capital appreciation. The portfolio managers employ a value-oriented investment approach in selecting stocks, using proprietary fundamental research to identify securities of companies they believe have attractive valuations. The portfolio managers focus on companies with a record of above average rates of profitability that sell at a discount relative to the overall small cap market. Through fundamental research, the portfolio managers seek to identify those companies that possess one or more of the following characteristics: sustainable competitive advantages within a market niche; strong profitability and free cash flows; strong market share positions and trends; quality of and share ownership by management; and financial structures that are more conservative than the relevant industry average.

PERFORMANCE HISTORY

Cumulative Performance of $10,000 Investment Since Inception1

| Average Annual Total Return through December 31, 20121 | ||||||||||||||||||||

| Since | Since | |||||||||||||||||||

| 5/1/07 | 5/1/09 | |||||||||||||||||||

| 1 Year | 3 Years | 5 Years | 10 Years | Inception | ||||||||||||||||

| Class I Shares | 15.39 | % | 13.87 | % | 7.66 | % | 4.84 | % | — | |||||||||||

| Class II Shares | 15.10 | 13.59 | — | — | 19.60 | % | ||||||||||||||

| Russell 2000® Index | 16.35 | 12.26 | 3.56 | 2.17 | 17.91 | |||||||||||||||

See accompanying Notes to Management’s Discussion of Fund Performance.

24

Ultra Series Fund | Management’s Discussion of Fund Performance | December 31, 2012

Small Cap Fund (concluded)

|

SECTOR ALLOCATION AS A PERCENTAGE OF NET ASSETS AS OF 12/31/12 |

||||||||

| Russell | ||||||||

| Midcap® | ||||||||

| Fund | Index | |||||||

| Consumer Discretionary | 14 | % | 12 | % | ||||

| Consumer Staples | 2 | % | 3 | % | ||||

| Energy | 4 | % | 6 | % | ||||

| Financials | 19 | % | 37 | % | ||||

| Health Care | 11 | % | 4 | % | ||||

| Industrials† | 27 | % | 13 | % | ||||

| Information Technology | 8 | % | 12 | % | ||||

| Materials | 8 | % | 6 | % | ||||

| Telecommunication | ||||||||

| Services | – | 1 | % | |||||

| Utilities | 4 | % | 6 | % | ||||

| Cash and Other Net Assets | 3 | % | – | |||||

|

||||||||

PERFORMANCE DISCUSSION

The Ultra Series Small Cap Fund returned 15.39% (Class I Shares) for the twelve-month period ended December 31, 2012, underperforming its benchmark, the Russell 2000® Index, which returned 16.35% for the same period.

Sector allocation, a residual of the bottom-up stock selection process, was a significant contributor to relative results primarily due to underweight exposure to the Energy and Information Technology sectors and an overweight exposure to the Industrials sector. Cash held during the period had a negative impact on relative results. Weak selection in the Financials, Materials, and Industrials sectors was partially offset by strong stock selection within Health Care, Energy, and Information Technology.

The fund’s largest contributors to relative and absolute performance during the period included retailer Stage Stores, contract research organization ICON, and Maximus, an outsourcing provider for government health and human services. Diversified industrial manufacturer Carlisle Companies was also among top contributors to absolute performance. The fund’s largest detractors from relative returns during the period included office supplier ACCO Brands, office product wholesaler United Stationers, and packaging company Aptargroup. PSS World Medical, a distributor of medical products and equipment to physi-cian offices and assisted living facilities, and Websense were also among the largest detractors from absolute returns during the period.

FUND CHANGES

The fund’s investment approach emphasizes individual stock selection; sector weights are a residual of our bottom-up investment process. The manager does, however, carefully consider diversification across economic sectors to limit risk. Based on bottom-up stock decisions, exposure to the Materials and Industrials Sectors increased during the period and exposure to the Financials and Consumer Discretionary Sectors fell. We initiated positions in Materials companies Innospec and Sensient Technologies. In Industrials, we initiated positions in Atlas Air Worldwide and Cubic. Within Financials, we eliminated positions in Delphi Financial Group, Alleghany, and Education Realty Trust. As of the end of the period, the fund was most overweight in the Industrials and Materials Sectors relative to the Russell 2000® Index, and most underweight in Information Technology. Based on our two- to three-year time horizon, we continue to find opportunities created by the inefficiencies frequently found among small-cap companies.

25

Ultra Series Fund | Management’s Discussion of Fund Performance | December 31, 2012

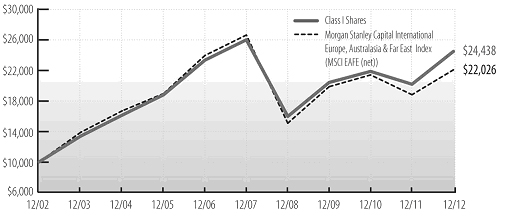

INTERNATIONAL STOCK FUND

INVESTMENT STRATEGY HIGHLIGHTS

The Ultra Series International Stock Fund will invest, under normal market conditions, primarily in foreign equity securities. Typically, a majority of the fund’s assets are invested in relatively large capitalization stocks of companies located or operating in developed countries. The fund may also invest up to 30% of its assets in securities of companies whose principal business activities are located in emerging market countries. The portfolio managers typically maintain this segment of the fund’s portfolio in such stocks which it believes have a low market price relative to their perceived value based on fundamental analysis of the issuing company and its prospects. The fund may also invest in foreign debt and other income bearing securities at times when it believes that income bearing securities have greater capital appreciation potential than equity securities.

PERFORMANCE HISTORY

Cumulative Performance of $10,000 Investment Since Inception1

| Average Annual Total Return through December 31, 20121 | ||||||||||||||||||||

| Since | ||||||||||||||||||||

| 5/1/09 | ||||||||||||||||||||

| 1 Year | 3 Years | 5 Years | 10 Years | Inception | ||||||||||||||||

| Ultra Series International Stock, Class I | 21.31 | % | 6.24 | % | -1.20 | % | 9.35 | % | — | |||||||||||

| Ultra Series International Stock, Class II | 21.01 | 5.98 | — | — | 13.18 | % | ||||||||||||||

| MSCI EAFE Index (net) | 17.32 | 3.56 | -3.69 | 8.21 | 11.81 | |||||||||||||||

See accompanying Notes to Management’s Discussion of Fund Performance.

26

Ultra Series Fund | Management’s Discussion of Fund Performance | December 31, 2012

International Stock Fund (concluded)

|

SECTOR ALLOCATION AS A PERCENTAGE OF NET ASSETS AS OF 12/31/12 |

||||||||

| Africa | 1 | % | ||||||

| Europe (excluding United Kingdom) | 42 | % | ||||||

| Japan | 15 | % | ||||||

| Latin America | 3 | % | ||||||

| Pacific Basin | 8 | % | ||||||

| United Kingdom | 23 | % | ||||||

| Other Countries | 6 | % | ||||||

| Cash and Other Net Assets | 2 | % | ||||||

PERFORMANCE DISCUSSION

The Ultra Series International Stock fund’s 21.31% return for the year bested the MSCI EAFE Index (net), which was up 17.32%.This strong performance was primarily driven by stock selection. Within the Materials Sector, James Hardie performed well on strong demand from a recovering U.S. housing industry. In the Information Technology Sector, Samsung continued to outperform on strong smart phone sales.

The fund was negatively impacted by the Financials Sector, as Credit Suisse Group underperformed following a report which called for a strengthening of its capital base. Stock selection in Japan also detracted from relative returns, as SoftBank declined following the announced acquisition of 70% of Sprint Nextel.

FUND CHANGES

During the period attractive stock-specific opportunities led to changes in the portfolio’s exposures. Additions included Bayer (Germany), Genomma Lab Internacional (Mexico) and Getinge (Sweden), increasing exposure to the Health Care Sector. Purchasing Red Electrica (Spain) and RWE (Germany) increased exposure to the Utilities Sector. The fund sold positions in AXA (France), Banco do Brasil (Brazil), QBE Insurance (Australia), and Credit Suisse Group (Switzerland), reducing exposure to the Financials Sector. Selling a position in Amadeus IT Holding (Spain) and trimming other existing positions lowered holdings in Information Technology stocks. From a regional perspective, exposure to emerging markets increased by purchasing the aforementioned Genomma Lab Internacional in addition to Mediclinic International (South Africa) and Bank Mandiri (Indonesia). Purchasing Bayer, Getinge, and RWE led to increased continental Europe exposure. Lastly, the sale of British Sky Broadcasting, GlaxoSmithKline, and International Power reduced UK exposure.

27

Ultra Series Fund | Management’s Discussion of Fund Performance | December 31, 2012

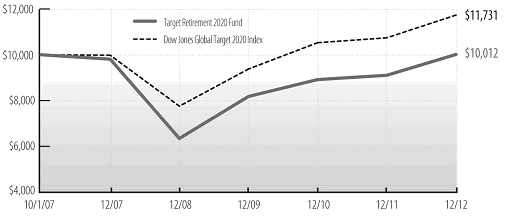

MADISON TARGET RETIREMENT 2020 FUND

INVESTMENT STRATEGY HIGHLIGHTS

The Ultra Series Target Retirement 2020 Fund invests primarily in shares of registered investment companies (the “underlying funds”) according to an asset allocation strategy developed by Madison Asset Management, LLC (“Madison”), the fund’s investment adviser, for investors planning to retire in or within a few years of 2020. Over time, the fund’s asset allocation will become more conservative until it reaches approximately 15-30% in stock funds and 70-85% in bond funds. The asset allocation strategy is designed to reduce the volatility of investment returns in the later years while still providing the potential for higher total returns over the target period.

On a periodic basis, Madison will evaluate and sometimes revise the fund’s asset allocations, including revising the asset class weightings and adding and/or removing underlying funds. Madison will also monitor the underlying funds on an ongoing basis and may increase or decrease the fund’s investment in one or several underlying funds. The underlying fund selections are made based on several considerations, including the fund’s style or asset class exposures, portfolio characteristics, risk profile, and investment process.

PERFORMANCE HISTORY

Cumulative Performance of $10,000 Investment Since Inception1,2

| Average Annual Total Return through December 31, 20121,2 | ||||||||||||||||||||

| Since | ||||||||||||||||||||

| 10/1/07 | ||||||||||||||||||||

| 1 Year | 3 Years | 5 Years | Inception | |||||||||||||||||

| Ultra Series Target Retirement 2020, Class I | 9.98 | % | 6.98 | % | 0.42 | % | 0.02 | % | ||||||||||||

| Dow Jones Global Target 2020 Index | 9.23 | 7.80 | 3.32 | 3.08 | ||||||||||||||||

See accompanying Notes to Management’s Discussion of Fund Performance.

28

Ultra Series Fund | Management’s Discussion of Fund Performance | December 31, 2012

Madison Target Retirement 2020 Fund (concluded)

|

PORTFOLIO ALLOCATION AS A PERCENTAGE OF NET ASSETS AS OF 12/31/12 |

||||||||

| Bond Funds | 52 | % | ||||||

| Foreign Bond Funds | 3 | % | ||||||

| Stock Funds | 34 | % | ||||||

| Foreign Stock Funds | 8 | % | ||||||

| Money Market Funds and Other Net Assets | 3 | % | ||||||

PERFORMANCE DISCUSSION

For the twelve-month period ended December 31, 2012, the Ultra Series Target Retirement 2020 Fund returned 9.98%, ahead the benchmark Dow Jones Global Target 2020 Index return of 9.23%. The fund’s performance trailed the Morningstar Target Date 2016-2020 peer average return of 11.68%. Outperformance against the benchmark was a result of strong manager performance within the fixed income holdings, an overweight position to corporate bonds, and a slight overweight position to equities relative to the benchmark. With the S&P 500 up 16.00%, the Barclays Capital U.S. Corporate High Yield Bond Index up 15.81%, and broad international indices outpacing the domestic indices, portfolios willing to take a more aggressive stance generally would have outpaced the fund’s performance. We believe that our conservative approach was the reason for underperformance compared to the Morningstar peer group, as we began the period leery of international equities given the underlying and unresolved sovereign debt crisis in Europe.

FUND CHANGES

We began the year with a sizable underweight position to international equities based on concerns over the ongoing European debt crisis. By the middle of the year, we began to increase foreign equity exposure. Our decision to increase equities exposure was a result of improved economic data and massive global central bank liquidity measures. Most notably, the decisive action by Mario Draghi and the European Central Bank, which we believed removed much of the near-term tail risk from the European markets. The increase proved timely as international equities rallied hard through the rest of the year. We remain underweight to foreign equities as we believe risks from Europe are still present.

Around the same time, with interest rates near record lows in the late summer/early fall, we significantly reduced the fund’s exchange traded fund (“ETF”) bond holdings in favor of actively managed funds. We believe the current ultra-low interest rate environment should favor active bond funds moving forward. Finally, late in the year, we began to trim the level of both investment grade and high yield credit investments in the fund. We believe that the credit markets have become fully valued and wanted to take advantage of potential profits while dampening the risk level of our fixed income holdings.

29

Ultra Series Fund | Management’s Discussion of Fund Performance | December 31, 2012

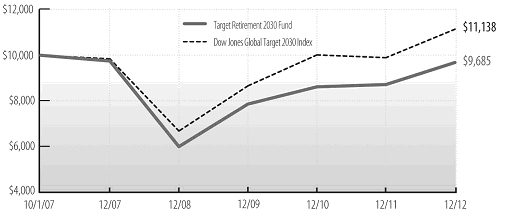

MADISON TARGET RETIREMENT 2030 FUND

INVESTMENT STRATEGY HIGHLIGHTS

The Ultra Series Target Retirement 2030 Fund invests primarily in shares of registered investment companies (the “"underlying funds”) according to an asset allocation strategy developed by Madison Asset Management, LLC (“Madison”), the fund’s investment adviser, for investors planning to retire in or within a few years of 2030. Over time, the fund’s asset allocation will become more conservative until it reaches approximately 15-30% in stock funds and 70-85% in bond funds. The asset allocation strategy is designed to reduce the volatility of investment returns in the later years while still providing the potential for higher total returns over the target period.

On a periodic basis, Madison will evaluate and sometimes revise the fund’s asset allocations, including revising the asset class weightings and adding and/or removing underlying funds. Madison will also monitor the underlying funds on an ongoing basis and may increase or decrease the fund’s investment in one or several underlying funds. The underlying fund selections are made based on several considerations, including the fund’s style or asset class exposures, portfolio characteristics, risk profile, and investment process.

PERFORMANCE HISTORY

Cumulative Performance of $10,000 Investment Since Inception1,2

| Average Annual Total Return through December 31, 20121,2 | ||||||||||||||||||||

| Since | ||||||||||||||||||||

| 10/1/07 | ||||||||||||||||||||

| 1 Year | 3 Years | 5 Years | Inception | |||||||||||||||||

| Ultra Series Target Retirement 2030, Class I | 11.05 | % | 7.17 | % | -0.13 | % | -0.61 | % | ||||||||||||

| Dow Jones Global Target 2030 Index | 12.56 | 8.76 | 2.52 | 2.07 | ||||||||||||||||

See accompanying Notes to Management’s Discussion of Fund Performance.

30

Ultra Series Fund | Management’s Discussion of Fund Performance | December 31, 2012

Madison Target Retirement 2030 Fund (concluded)

|

PORTFOLIO ALLOCATION AS A PERCENTAGE OF NET ASSETS AS OF 12/31/12 |

||||||||

| Bond Funds | 36 | % | ||||||

| Foreign Bond Funds | 3 | % | ||||||

| Stock Funds | 48 | % | ||||||

| Foreign Stock Funds | 12 | % | ||||||

| Money Market Funds and Other Net Assets | 1 | % | ||||||

PERFORMANCE DISCUSSION

For the twelve-month period ended December 31, 2012, the Ultra Series Target Retirement 2030 Fund returned 11.05%, while the Dow Jones Global Target 2030 Index returned 12.56%. The fund’s performance also trailed the Morningstar Target Date 2026-2030 peer average return of 13.59%. With the S&P 500 Index up 16.00% for the year, the Barclays Capital U.S. Corporate High Yield Bond Index up 15.81%, and broad international indices outpacing the domestic indices, portfolios willing to take a more aggressive stance would have likely outpaced the fund’s performance. We believe the reason for underperformance compared to the Morningstar peer group was primarily due to the fund’s relatively light equity exposure associated with our conservative approach towards the fund’s target asset allocation position.

FUND CHANGES

We began the year with a sizable underweight to international equities based on concerns over the ongoing European debt crisis. By the middle of the year, we began to increase foreign equity exposure. Our decision to increase equities exposure was a result of improved economic data and massive global central bank liquidity measures. Most notably, the decisive action by Mario Draghi and the European Central Bank, which we believed removed much of the near-term tail risk from the European markets. The increase proved timely as international equities rallied hard through the rest of the year. We remain underweighted to foreign equities as we believe risks from Europe are still present.

With interest rates near record lows in the late summer/early fall, we significantly reduced the fund’s exchange traded fund (“ETF”) bond holdings in favor of actively managed funds. We believe the current ultra-low interest rate environment should favor active bond funds moving forward. Finally, late in the year, we began to materially trim the level of both investment grade and high yield credit in the fund. We believe that the credit markets have become fully valued and wanted to take advantage of potential profits while dampening the risk level of our fixed income holdings.

31

Ultra Series Fund | Management’s Discussion of Fund Performance | December 31, 2012

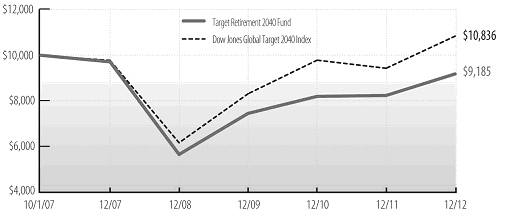

MADISON TARGET RETIREMENT 2040 FUND

INVESTMENT STRATEGY HIGHLIGHTS

The Ultra Series Target Retirement 2040 Fund invests primarily in shares of registered investment companies (the “"underlying funds”) according to an asset allocation strategy developed by Madison Asset Management, LLC (“Madison”), the fund’s investment adviser, for investors planning to retire in or within a few years of 2040. Over time, the fund’s asset allocation will become more conservative until it reaches approximately 15-30% in stock funds and 70-85% in bond funds. The asset allocation strategy is designed to reduce the volatility of investment returns in the later years while still providing the potential for higher total returns over the target period.

On a periodic basis, Madison will evaluate and sometimes revise the fund’s asset allocations, including revising the asset class weightings and adding and/or removing underlying funds. Madison will also monitor the underlying funds on an ongoing basis and may increase or decrease the fund’s investment in one or several underlying funds. The underlying fund selections are made based on several considerations, including the fund’s style or asset class exposures, portfolio characteristics, risk profile, and investment process.

PERFORMANCE HISTORY

Cumulative Performance of $10,000 Investment Since Inception1,2

| Average Annual Total Return through December 31, 20121,2 | ||||||||||||||||||||

| Since | ||||||||||||||||||||

| 10/1/07 | ||||||||||||||||||||

| 1 Year | 3 Years | 5 Years | Inception | |||||||||||||||||

| Ultra Series Target Retirement 2040, Class I | 11.42 | % | 7.17 | % | -1.11 | % | -1.60 | % | ||||||||||||

| Dow Jones Global Target 2040 Index | 14.88 | 9.23 | 2.09 | 1.54 | ||||||||||||||||

See accompanying Notes to Management’s Discussion of Fund Performance.

32

Ultra Series Fund | Management’s Discussion of Fund Performance | December 31, 2012

Madison Target Retirement 2040 Fund (concluded)

|

PORTFOLIO ALLOCATION AS A PERCENTAGE OF NET ASSETS AS OF 12/31/12 |

||||||||

| Bond Funds | 26 | % | ||||||

| Foreign Bond Funds | 2 | % | ||||||

| Stock Funds | 56 | % | ||||||

| Foreign Stock Funds | 15 | % | ||||||

| Money Market Funds and Other Net Assets | 1 | % | ||||||

PERFORMANCE DISCUSSION

For the twelve-month period ended December 31, 2012, the Madison Target Retirement 2040 Fund returned 11.42%, while the Dow Jones Global Target 2040 Index returned 14.88%. The fund’s performance also trailed the Morningstar Target Date 2036-2040 peer average return of 14.64%. With the S&P 500 Index up 16.00%, the Barclays Capital U.S. Corporate High Yield Bond Index up 15.81%, and broad international indices outpacing the domestic indices, portfolios willing to take a more aggressive stance would have likely outpaced the fund’s performance. We believe the reason for underperformance compared to the Morningstar peer group was primarily due to the fund’s relatively low equity exposure associated with our conservative approach towards the target asset allocation position.

FUND CHANGES

We began the year with a sizable underweight to international equities based on concerns over the ongoing European debt crisis. By the middle of the year, we began to increase foreign equity exposure. Our decision to increase equities exposure was a result of improved economic data and massive global central bank liquidity measures. Most notably, the decisive action by Mario Draghi and the European Central Bank, which we believed removed much of the near-term tail risk from the European markets. The increase proved timely as international equities rallied hard through the rest of the year. We remain underweighted to foreign equities as we believe risks from Europe are still very much present.

Around the same time, with interest rates near record lows in the late summer/early fall, we significantly reduced the fund’s exchange traded fund (“ETF”) bond holdings in favor of actively managed funds. We believe the current ultra-low interest rate environment should favor active bond funds moving forward. And finally, late in the year, we began to materially trim the level of both investment grade and high yield credit in the fund. We believe that the credit markets have become fully valued and wanted to take advantage of potential profits while dampening the risk level of our fixed income holdings.

33

Ultra Series Fund | Management’s Discussion of Fund Performance | December 31, 2012