EXHIBIT 99.2

To Form 8-K dated February 2, 2017

Transcript

|

Seacoast Banking Corporation

of Florida

Fourth Quarter Earnings

Conference Call

February 2, 2017

10:00 AM Eastern Time

|

SPEAKERS

Dennis Hudson - Chairman & CEO

Chuck Shaffer - Executive Vice President

Steve Fowle - Executive Vice President & CFO

Chuck Cross - Executive Vice President Commercial Banking

Julie Kleffel - Executive Vice President Community Banking

ANALYSTS

Michael Young - SunTrust Robinson Humphrey

Bob Ramsey - FBR

Stephen Scouten - Sandler O’Neill

David Feaster - Raymond James

PRESENTATION

Operator: Welcome to the Seacoast

Fourth Quarter Earnings Conference Call. My name is Richard and I will be your operator for today’s call. At this time, all

participants are in a listen-only mode. Later, we will conduct a question and answer session. Please note that this conference

is being recorded.

I will now turn the call over to Mr. Dennis

Hudson. You may begin.

Dennis Hudson: Thank you very much

and thank you all for joining us today for our Fourth Quarter 2016 Earnings Conference Call. Our press release issued yesterday

after the market closed and then updated investor presentation with supplementary information are posted on the Investor portion

of our website at SeacoastBanking.com. You can find that information under Presentations.

Seacoast Banking Corporation of Florida

Exhibit 99.2

to Form 8-K Dated February 2, 2017

Page 2

Before we begin, as always, I’ll

direct your attention to the statement contained at the end of our press release regarding forward-looking statements that we will

be making during the call. We’ll be discussing issues that constitute forward-looking statements within the meaning of the

Securities and Exchange Act and our comments today are intended to be covered within the meaning of that section of the Act.

With me today is Chuck Shaffer, who

will discuss our financial and operating results. Also joining us in the room is Steve Fowle, our Chief Financial Officer;

Chuck Cross, our Commercial Banking Executive; David Houdeshell, our Chief Credit Officer; and Jeff Lee, our Chief Marketing

and Analytics Officer.

Last week, we issued a press release describing

a management transition that will drive our growth into 2017 and beyond. Effective on March 15th, Chuck Shaffer will

assume the newly created position of CFO and Head of Strategy, a role for which he has the experience, the skill, and vision for

our business to lead our financial and strategic objectives. Julie Kleffel, who’s also on the call today, a home-grown Floridian

who has headed our small business banking unit for the past two years, will succeed Chuck as head of our community banking division,

which includes small business banking. In addition, we announced last December, the appointment of Jeff Bray as an Executive Vice

President for Service and Operations. These appointments position us well for continued success as the community banking industry

continues to undergo its rapid evolution.

Steve Fowle, our current CFO will continue

in that role until mid-March to ensure a smooth transition. I just want to say Steve has played an invaluable part in our transformation

and fulfilled his mission to help put the bank on a more robust growth trajectory. And we wish him well in his success as he moves

on to his next endeavor.

Chuck has the ideal expertise and experience

to build on Steve’s work and to take Seacoast to the next level of performance.

Seacoast Banking Corporation of Florida

Exhibit 99.2

to Form 8-K Dated February 2, 2017

Page 3

Looking at our financial and operating

results, it’s clear that 2016 was a breakout year for Seacoast. Our balanced growth strategy, combining investments in organic

growth with well-conceived acquisitions, continued to deliver results for shareholders. At the beginning of 2016, we set an aggressive

adjusted earnings target of $1 per share. We achieved that target and we achieved it despite interest rate environment related

changes that we encountered along the way. We responded to those changes by growing organically, executing smart M&A and exhibiting

strong expense management.

Our focus on executing our model, even

during changing times like today, led to strong results. For perspective, I’d like to share what we achieved in 2016 for

our shareholders. During the year, we increased our adjusted earnings per share 56% year-on-year. We achieved an 880 basis point

improvement in our adjusted efficiency ratio which moved from 69.6% in our first quarter to 60.8% by year end. We increased our

adjusted return on average assets up to 0.99% almost a 1% return, up from 0.75% in the first quarter. And we increased our adjusted

return on tangible common equity, 460 basis points, to 13.1% in the quarter, the last quarter of this year, compared to 8.5% in

the first quarter.

These results evidence a remarkable turnaround

for Seacoast over the past three years. While these and other key metrics are clearly at more respectable levels than they were

a few years ago, we believe our model still has plenty of room to run. Before I go on, I’d like to just thank all of our

associates for the role they played in getting us to this point. Their focus every day on serving our customers and helping them

achieve their financial goals is what makes the difference.

Building on a strong third quarter, we

continued our momentum, producing strong organic growth last quarter. Loan production continued at a record pace across all of

our business lines, growing 16% annualized during the fourth quarter. In particular, commercial loan originations hit $145 million

during the fourth quarter up more than 81% over the year-ago number. Our investment four years ago in our innovative commercial

banking delivery model - our Accelerate platform - has certainly paid off, and it has grown to become a significant part of our

business.

Seacoast Banking Corporation of Florida

Exhibit 99.2

to Form 8-K Dated February 2, 2017

Page 4

Our business units’ results continue

to meet or exceed our expectation. In the fourth quarter, consumer and small business originations totaled $83 million, up 38%

year-over-year. Mortgage loan originations exceeded $119 million, up 98% year-over-year. The transformation of our retail network

continued during the quarter, highlighted by our momentum in moving routine transactions out of the branch and into our digital

channels. The pace of customers choosing these convenient lower cost channels continues to accelerate. One proof point: In the

fourth quarter, nearly 37% of all paper checks were deposited remotely, compared to the just 22% in the fourth quarter of 2015.

Mobile adoption continues to rise, now

up to 30% of eligible customers compared with 26% in last year’s fourth quarter. Moreover because we’re able to serve

customers more efficiently through non-branched channels we were able to continue to rationalize our physical footprint as shown

by the deposits per branch, which now exceeds $78 million at yearend. These metrics compare very favorably to top money center

banks and are far ahead of most community banks. In fact that increase was very substantial; I think in the beginning of the year

that average number was down in the 50s.

I would add that we have achieved this

performance while competing very differently than many of Florida banking peers. We continue to maintain a very granular loan portfolio

with very modest levels of CRE exposure.

Our M&A work during 2016 performed

well, as we expected, and our playbook that we use is now proven and effective. We completed two transactions in Orlando in 2016,

the Floridian and BMO Harris branch acquisition that built on top of our 2014 foothold which was completed with the acquisition

of BankFIRST. Combined, all of these acquisitions made us a top ten bank in Orlando, Orlando being Florida’s third largest

market at year-end.

Seacoast Banking Corporation of Florida

Exhibit 99.2

to Form 8-K Dated February 2, 2017

Page 5

We’ve now taken the first step to

executing the Orlando playbook in the Tampa market with the acquisition of GulfShore Bank announced last November, and we’re

on target to close sometime towards the end of this quarter. Our acquisition of Grand Bank, which strengthened our position in

Palm Beach County in 2015, is going strong, with households up 9% to 10% since that deal was closed.

At Seacoast our aim is to be able to meet

the financial needs of the customers we serve, just like we did 90 years ago when this bank was founded. We firmly believe that

while the way we addressed customers’ financial needs has changed dramatically, the needs themselves really haven’t

changed at all. We believe that a strong locally relevant brand combined with a digitally enabled low cost delivery structure combines

really the best of both worlds, enabling us to generate consistent lower risk returns for our shareholders.

Let me share two final thoughts. The convenience

of mobile always in service is now expected by everyone regardless of age or industry. From commercial businesses to small businesses

to consumers we now live in a world where everyone expects convenience and they expect their bank - and their banker - to always

be on demand.

For the past few years we have been methodically

executing a digital transformation strategy that is now positioning us very well. The digital explosion certainly can’t be

denied. It is not something that will happen in the distant future. It’s really happening right now and we’re seeing

it in our numbers. And banks that aren’t executing and showing progress both to their customers and the shareholders I believe

are at serious risk.

The second point I’d like to make

that as I look across the state of Florida, now the nation’s third largest state, and our position within it, I continue

to see opportunity ahead for our franchise. Our legacy of establishing relationships with customers, understanding and meeting

their financial service needs, and serving them through cost-effective distribution channels is very much relevant in the world

ahead. And as our experience with digital delivery continues to grow, I think it positions us well.

Seacoast Banking Corporation of Florida

Exhibit 99.2

to Form 8-K Dated February 2, 2017

Page 6

With all that said, after a lot of hard

work and commitment to executing on our balanced growth strategy, we are entering 2017 we believe from a position of strength.

We’re proud of our financial performance that we delivered for our shareholders in 2016, and as we address in detail momentarily

our expectations for the full year 2017, I think we’ll underline the opportunity that lies ahead for Seacoast and what we

believe we can achieve.

Finally before I hand off to Chuck to share

a few financial highlights and take your questions, I want to invite all of you to attend our first Investor Day on February 22nd.

It will be held in New York at the Westin on West 43rd Street and it will also be webcast. We’re also excited

in that venue to be able to provide all of you with a much closer look at our differentiated business model to discuss how we think

about the future and to discuss the value-creating implications that we see for shareholders over the next couple of years. Thanks

a lot for your attention.

Now over to you, Chuck, for some financial

highlights.

Chuck Shaffer: Thank you, Denny,

and thank you all for joining us this morning. As I provide my comments I will reference the slide deck which can be found at www.seacoastbanking.com.

Let me open by congratulating all of our

team members on helping achieve our dollar per share goal announced at the start of the prior year. This was a significant accomplishment,

and it was a result of our continued strategy of growing topline revenue through better execution of our business units, the successful

integration of two acquisition targets in 2016, and a disciplined and focused program to become a much more efficient organization.

Seacoast Banking Corporation of Florida

Exhibit 99.2

to Form 8-K Dated February 2, 2017

Page 7

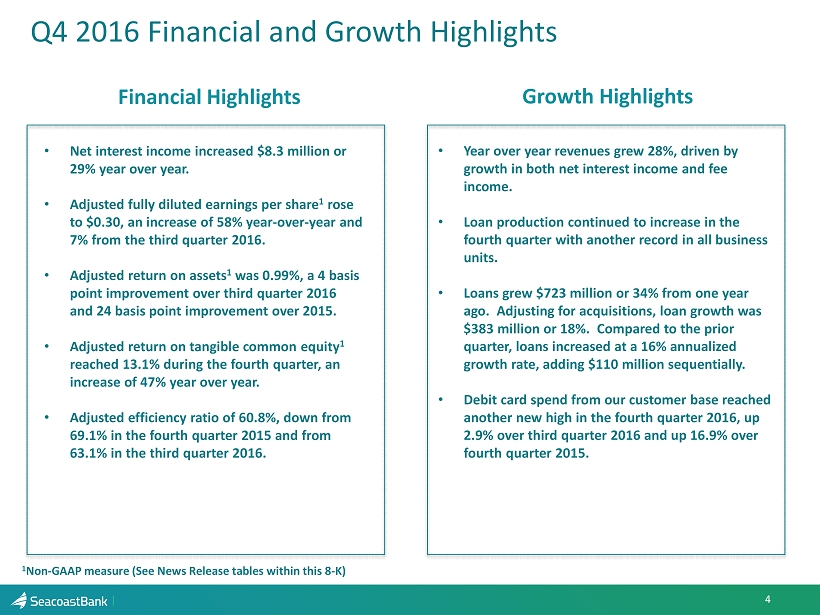

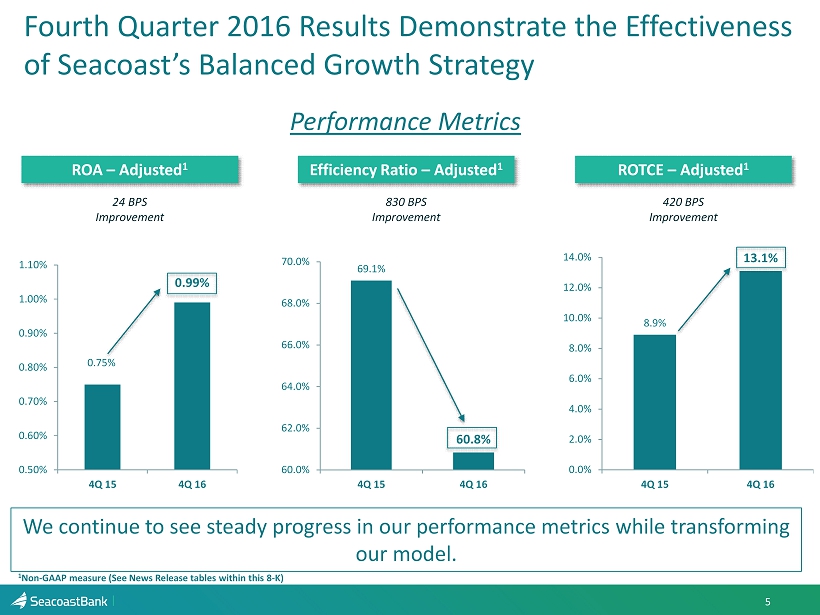

As shown on slide 5 of the deck, our

results signal a significant improvement of performance over the past year accomplished without taking outside lending or

operational risk. On an adjusted basis, our return on assets ended the year 0.99% up from 0.75% at the end of the

prior year. Adjusted return on tangible common equity ended the year at 13.1% up from 8.9% at the end of the prior year, and

our adjusted efficiency ratio declined to 60.8%, reflecting the additional operating leverage and efficiency gains created

throughout 2016. We believe we are now operating at a level performance that is inline, or ahead of most peers, with a

trajectory to improve this performance into 2017.

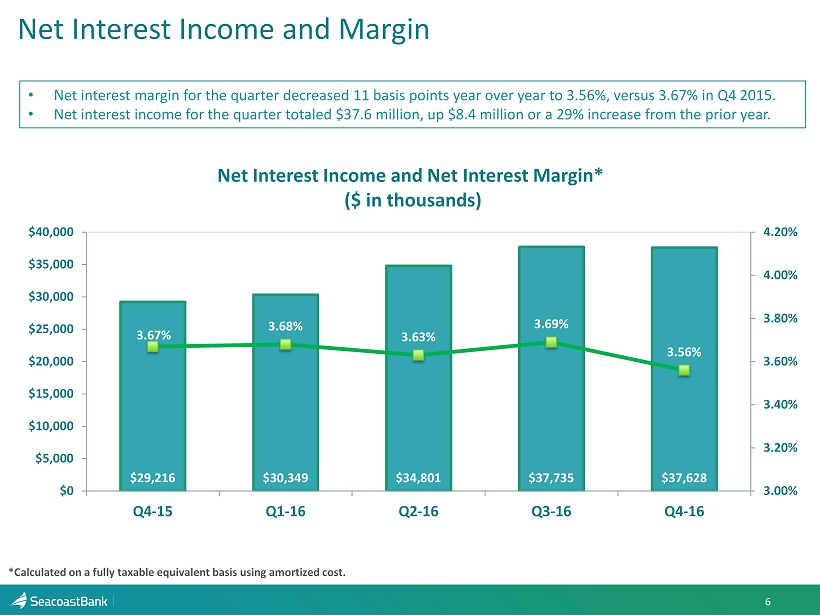

Looking more deeply at the quarter, moving

to slide 6, net interest income remained roughly in line with the third quarter and up $8.4 million from the prior year’s

fourth quarter, reflecting the full impact of integrating BMO and Floridian and strong loan demand throughout the year. Net interest

margin declined 13 basis points from the prior quarter, largely due to less loan accretion and additional balance sheet leverage.

Looking forward, we expect the net interest margin to be in the high 350’s and likely increase to the mid-360’s by

yearend 2017. The NIM trend will be dependent on where interest rates head in 2017. And we remain moderately asset sensitive with

100 to 200 basis point increase in rates, equating to approximately 2% to 4% improvement in net interest income.

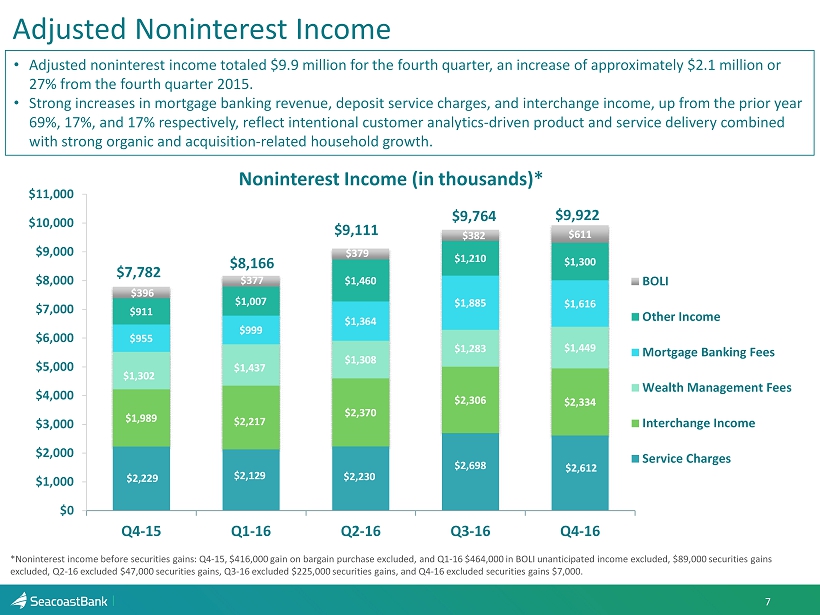

Moving to slide 7, adjusted non-interest

income remained relatively in line with the third quarter and is up $2.1 million from the prior year’s fourth quarter, the

result of stronger service charges on deposits primarily due to the acquisition of BMO’s operations in Orlando, better performance

in our wealth and mortgage banking units, expansion of our BOLI program and continued increases in interchange income, the result

of driving spin and activation using our automated marketing tools, and continued household acquisition. As a reminder, our operating

markets were impacted by Hurricane Matthew, negatively impacting our transactional fee categories during the quarter.

Seacoast Banking Corporation of Florida

Exhibit 99.2

to Form 8-K Dated February 2, 2017

Page 8

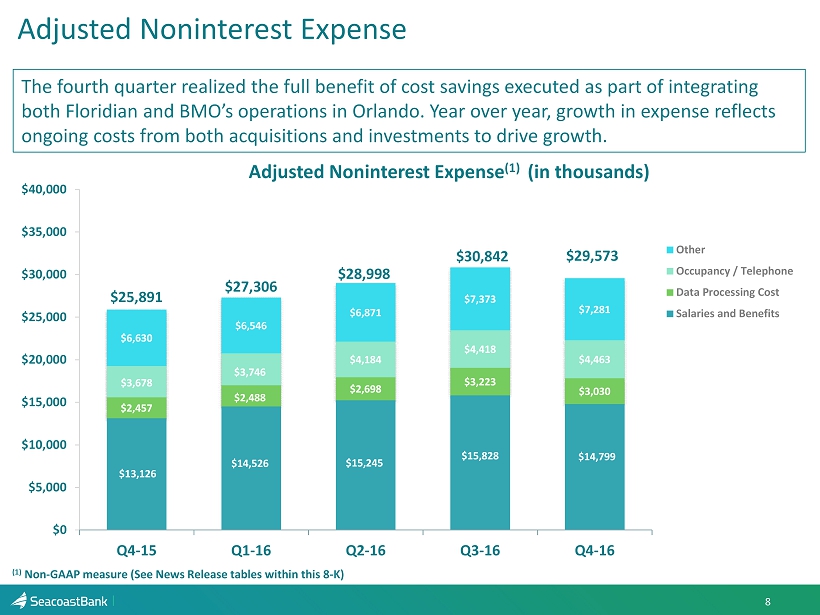

Moving to slide 8, adjusted noninterest

expense was down $1.3 million from the prior quarter and up $3.7 million from the prior year’s fourth quarter. The fourth

quarter realized the full benefit of cost savings executed from the Floridian and BMO mergers, as we finalized and closed ten locations

in the central Florida market during the third quarter. The year-over-year increase reflects ongoing costs associated with two

bank acquisitions, investments in technology and investments to drive our franchise’s growth.

And as a remainder, salary and wages should

increase by approximately 10% from the fourth quarter of 2016 to the first quarter of 2017, as seasonal increases in 401(k) and

related payroll taxes begin to reappear at the start of a new year and accrual levels for compensation return to more normalized

levels. We’ll continue to carefully manage the expenses as we move forward and become more efficient in our retail network.

We believe branches are still valuable

to our customers for more complex transactions, but simple tasks such as depositing or withdrawing funds are rapidly migrating

to a digital world. During the fourth quarter deposits outside the branch network increased to 37% from 22% in the same quarter

one year prior. We expect to close 20% of our locations over the next 24 to 36 months and some of this operational expense savings

will be reinvested into technology and talent, to deliver products and services in new more convenient ways. We will continue to

carefully balance our investments for growth to bottom line performance as we move forward.

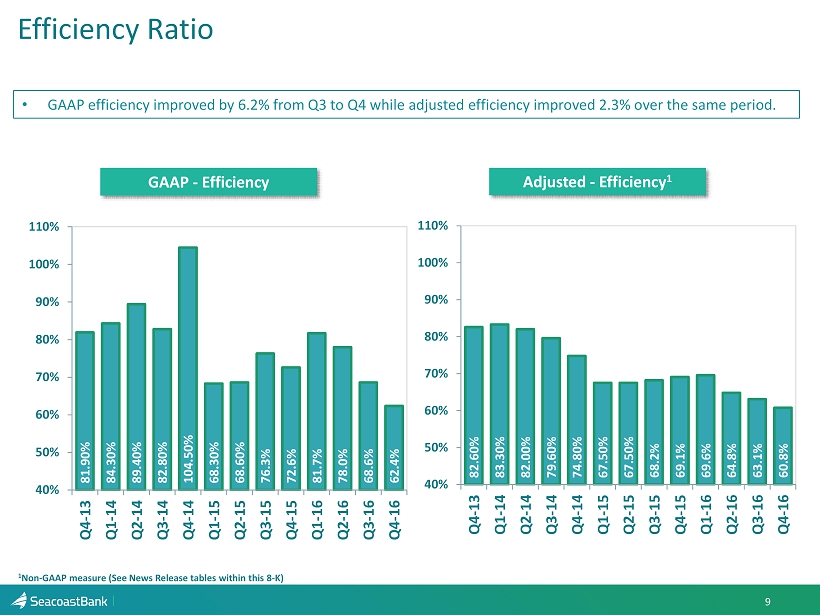

Moving to slide 9, our adjusted efficiency

ratio improved to 60.8%, evidencing that our transformation continues to get meaningful traction. We remain highly focused on driving

shareholder value by executing a transformative strategy, meeting our customer needs with digital offerings and reducing our traditional

cost to serve. We recorded a $5.3 million in income tax provision in the fourth quarter of 2016, compared to $4.3 million in the

third quarter of 2016 and $3.7 million in the prior year. The fourth and third quarter 2016 tax provisions have been benefited

from the early adoption of ASU2016-9, Improvements to Employee Share-Based payment accounting. As a result the company recorded

a benefit of $383,000 and $418,000 in the fourth and third quarter, respectively, adding $0.01 per diluted share to each quarter.

Looking forward, we expect our effective tax rate to be 36%.

Seacoast Banking Corporation of Florida

Exhibit 99.2

to Form 8-K Dated February 2, 2017

Page 9

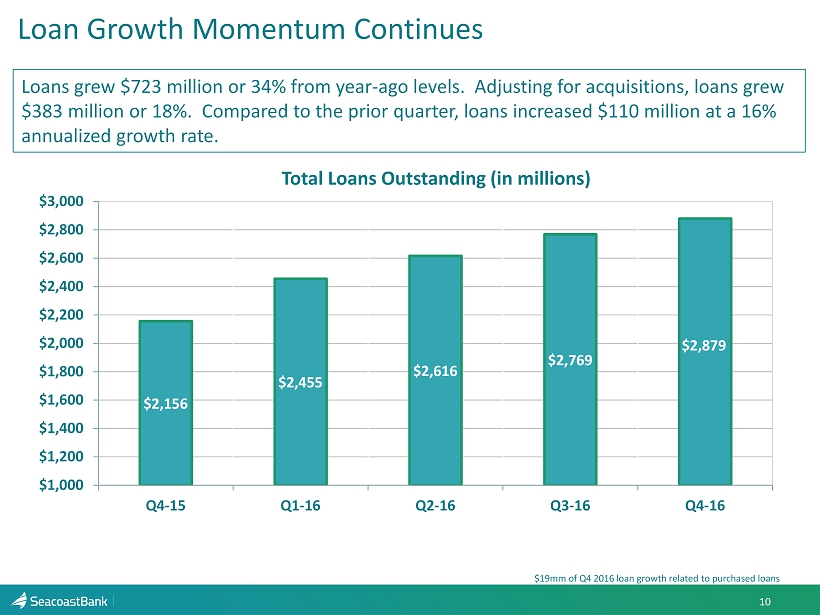

Turning to slide 10, loan outstandings

again grew at record pace during the fourth quarter, up $110 million from the third quarter, or 16% annualized. Loan outstandings

grew $723 million or 34% from the fourth quarter in the prior year.

Four years ago we made an investment in

an innovative commercial banking platform, we call it Accelerate Business Banking. This platform has matured and is now producing

over $100 million per quarter in commercial loan originations with production increasing from approximately $200 million in 2013

to $432 million in 2016. The following year we invested in a data-driven lead program in automated marketing, which began to fuel

our consumer and small business franchise, increasing total aggregate consumer and small business funding from $31 million in 2013

to $300 million in 2016. We believe we’re still early on the growth curve in this business and expect productivity to continue

to improve as we move into 2017.

Our mortgage banking business has

also grown substantially in 2016, growing overall originations to $403 million up from $251 million in 2013. The expansion

into Orlando, South Florida and ultimately Tampa with the GulfShore acquisition should continue to provide opportunity for

our mortgage business. We also continue to focus on building a well-diversified loan book. Our average commercial loan size

of $339 million. Our top ten relationships as a percentage of total capital are 40%, up from 36% at the end of the prior

year. Looking forward, we expect organic loan growth to continue to be in mid to high teens.

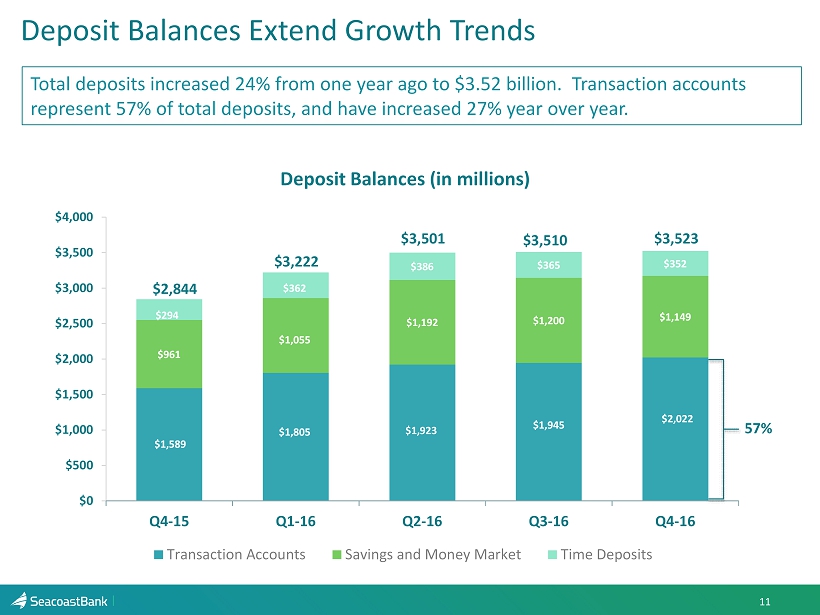

Turning to slide 11, deposit outstandings

grew modestly during the fourth quarter, up $13 million from the third quarter, and up $679 million from the fourth quarter in

the prior year. Deposits per branch increased to $78 million from $66 million one year ago. Core customer funding, which excludes

CDs, increased $63 million or 8% annualized. Rates paid on deposits remain stable quarter-over-quarter. And looking ahead we expect

to grow deposit outstandings in the 7% range with some minor increases in deposit rates paid to customers.

Seacoast Banking Corporation of Florida

Exhibit 99.2

to Form 8-K Dated February 2, 2017

Page 10

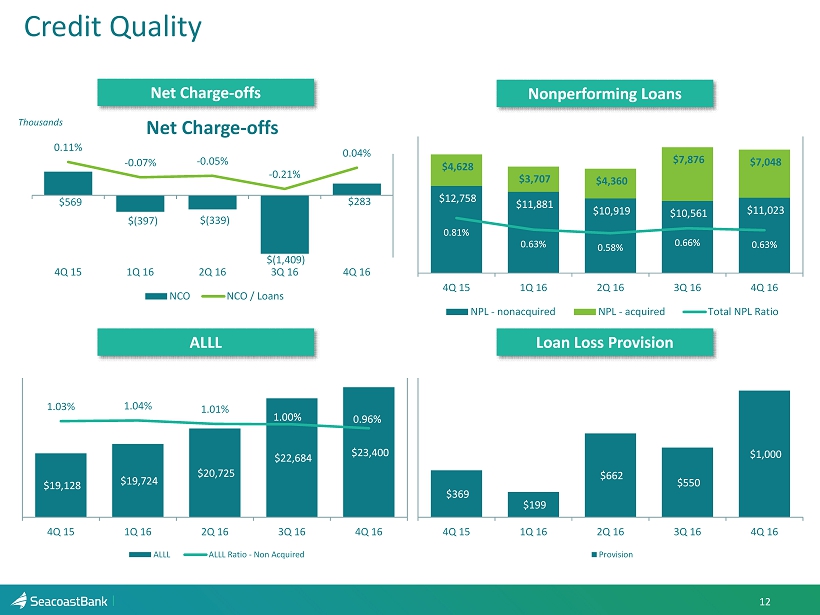

Turning to slide 12, credit quality range

continues to be strong, and our risk profile well maintained. In the legacy portfolio, the ALLL ended the quarter at 0.96% of loan

outstandings down from 1% at the end of the prior quarter. Net charge-offs were $283,000 for the quarter compared to $1.4 million

in recoveries in the prior quarter and charge-offs of $569,000 in the fourth quarter of the prior year. Looking forward the provision

for credit losses will continue to be influenced by loan growth.

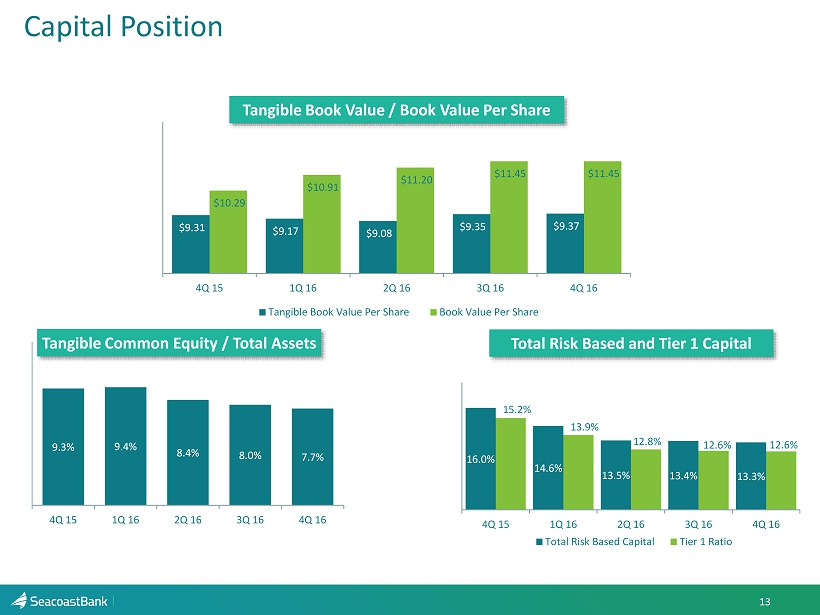

Turning to slide 13, our capital

position remains strong. The common equity tier 1 capital ratio was 12.6%, total capital ratio was 13.3%, and the tier 1

leverage ratio was 9.2% at December 31, 2016. Our ratios increased slightly as earnings outpaced balance sheet growth.

We’re issuing guidance for adjusted earnings per share of $1.24 to $1.28 for the fiscal year 2017. This assumes the

yield curve remains unchanged and continued forward progress in our Florida economy. We’re excited about the year ahead

and we work diligently and improved our ability to execute. We’ve made investments in technology and talent in prior

years that are now paying off, and we believe we’re operating in some of the best markets of Florida.

I’ll turn to call back over to Denny.

Dennis Hudson: Thank you,

Chuck, and I appreciate you hitting a few of highlights for the quarter. Just again, I’d like to remind everybody,

we’re going to take a deeper dive into our go-forward strategy at our Investor Day which is scheduled to be in New York

on February 22nd. During that meeting, we’ll have a greater number of our key team players presenting

different sections of the discussion during that morning and I think it will give investors an opportunity to again take a

deeper dive into the business model that we’re creating here, and the implications looking forward for value creation

out in the medium term. So we look forward to seeing you then.

I’d like to throw the floor open

to any questions that we might have. Operator?

Seacoast Banking Corporation of Florida

Exhibit 99.2

to Form 8-K Dated February 2, 2017

Page 11

Operator: Thank you. We will now

begin the question and answer session. [Operator instructions]. Our first question comes from Mr. Michael Young from SunTrust

Robinson Humphrey. Please go ahead.

Michael Young: Hi, good morning,

everyone.

Dennis Hudson: Hi, Michael.

Michael Young: I wanted to start,

Chuck, I think you mentioned you’re going to close ten branches in 2017. Is that the right number?

Chuck Shaffer: We closed 10 branches

in the third quarter in the Orlando market and looking forward, we plan to close 20% in the next 24 to 36 months.

Michael Young: Okay. Over two to

three years, okay. Got it, yes. And so maybe just backing that up and hold then on the expense line item for next year, do you

expect continued sort of net declines, maybe absent the first quarter from the first quarter run rate?

Chuck Shaffer: Yes, the first quarter

will, yes as I mentioned in my comments, we shouldn’t expect that to go back up due to normalized sort of compensation type

issues. But looking forward through the remainder of the year, I would expect non-interest income to remain relatively flat to

down. We’ll continue to focus on efficiency throughout the year and as we continue to work through some of that consolidation

work, we should see some benefit.

Dennis Hudson: You’re speaking

about non-interest expenses, flat to down?

Chuck Shaffer: Non-interest expenses.

Yes, right.

Seacoast Banking Corporation of Florida

Exhibit 99.2

to Form 8-K Dated February 2, 2017

Page 12

Michael Young: Okay and also just

on the deposit side, I think earlier this year you guys were hoping for maybe about $80 million in deposits per branch, we’re

a little light of that. I just wasn’t sure, was there more deposit outflow maybe from the BMO branches or did you decide

to keep a couple of extra branches that maybe you weren’t planning on originally?

Chuck Shaffer: If you look at our

core customer funding, it continues to grow quarter-over-quarter. One of the things that did impact that number is that we purposely

allowed some of the higher rate CDs acquired through some of the acquisitions to run off; the core deposits underneath that continue

to grow, the two acquisitions that performed basically in line with what we expected on the customer side of the transactions,

as well as we are impacted a little bit on public funds. We chose not to compete for some public funds. As rates have increased

here, the public fund market has gotten more competitive and we saw some money move up to the state of Florida SBA fund as well

as some competition at some prices and some rates that we were unwilling to pay.

Dennis Hudson: In fact that brought

down our deposit growth rate on a total basis in Q4. If you take that out I think our deposit growth was actually right in line

with what we expected in 6% or 7% range.

Michael Young: All right, and maybe

just lastly hitting on M&A. Obviously you got the Tampa deal is going to close, kind of midyear, but I assume you’re

still kind of in the market looking selectively for new acquisitions. Do you still bias towards market expansion at this point?

Dennis Hudson: Good question, we

continue to focus our attention on organic growth, as you’ve heard through most of the call, and we look for selective M&A

opportunities when we see value in the customer base that we can further monetize and create revenue growth. And

so we’re continuing to look for those opportunities and when we see one, we get excited about it and try to tackle it. I

wouldn’t say it’s our primary goal, but it’s an important part of the balanced growth strategy.

Seacoast Banking Corporation of Florida

Exhibit 99.2

to Form 8-K Dated February 2, 2017

Page 13

Michael Young: Okay, congrats on

the good quarter and good luck to Steve and Chuck and everyone else.

Dennis Hudson: Thanks, Mike.

Operator: Thank you. Our next question

comes from Mr. Bob Ramsey from FBR. Please go ahead.

Bob Ramsey: Hi, good morning, guys.

I just wanted to follow up a little bit on the deposit conversation there, it sounds like there were some areas you pulled back

on. I’m curious if you see ongoing pressure in those areas, obviously you grew some of the wholesale funding this quarter,

and how you’re thinking about funding loan growth as we go forward, where the opportunities and challenges are.

Chuck Shaffer: Thanks, Bob. We

have a strong retail bank. We’ll continue to use that retail bank to produce low cost retail deposits and that will be

our first source as we move forward. You’re right, the deposit environment is changing here, particularly as the yield

curve increases and as banks sort of fill up on loan to deposit ratio. That being said, we’ve been a good deposit

gatherer over time and we’ll begin to focus more of our attention there and focus on growing small business in retail,

and the public fund market is always there for us if we want to go back into that to fund loan growth.

Dennis Hudson: As we

said earlier, the underlying deposit trend actually was quite positive during the quarter. The big impact was the reduction in

some of the balances that we might have expected in the public funds area and that was directly related to what has happened with

some of that funding as some of our excess deposits that we would normally get out of that class, at yearend and end of the fourth

quarter, kind of moved over into SBA funds, which are invested in mortgage backs and things like that.

Seacoast Banking Corporation of Florida

Exhibit 99.2

to Form 8-K Dated February 2, 2017

Page 14

Chuck Shaffer: And Bob just to add

on to that, too, if you think about the full balance sheet, the investment portfolio runs off about $180 million in cash over the

next 12 months. We don’t expect to rebuild that investment portfolio so that helps fund run loan growth as we move forward

as well.

Bob Ramsey: Okay, that’s helpful.

Then sort of I guess somewhat related, could you sort of provide an update for us on where you stand in terms of interest rate

sensitivity particularly in light of the Fed’s December move and what further moves may mean for you?

Dennis Hudson: Sure. I made a comment

in my address, but I’ll repeat it. We’re moderately asset sensitive, 100 to 200 basis point increase in rates basically

equates to 2% to 4% improvement in net interest income, and I think that’s the best way to think about it. If we do see the

Fed increase rates throughout the year depending on how the yield curve reacts that’s assuming kind of a parallel shift,

but we are asset sensitive and any increase in rates does work to our benefit.

Bob Ramsey: Okay, all right, great.

I think I did not quite pull that out of the intro comments. I think at the same time you were talking about margin guidance for

the year. Did I catch you correct that you expect high 350s this quarter and maybe low 360s by yearend?

Dennis Hudson: Yes, the exact language

was mid-360s, but the driver to that is as we allow the investment portfolio decline and fund loan growth as we move forward that

should positively impact the margin.

Bob Ramsey: Got it. So mix shift

is the biggest driver.

Dennis Hudson: Yes.

Seacoast Banking Corporation of Florida

Exhibit 99.2

to Form 8-K Dated February 2, 2017

Page 15

Bob Ramsey: In terms of the margin

this quarter, I know you guys highlighted 6 basis point hit from lower purchase accounting accretion. What was the amount of purchase

accounting accretion this quarter and is this a good level you think as we sort of run through next year?

Dennis Hudson: Yes, I think this

is an okay way to think about it this quarter, but good ways is it runs around 10 basis points, somewhere 10 to 15 basis points

depending on the quarter. It’s volatile, you have to be careful and assuming that loan payoffs and things can impact that

meaningfully but that’s probably about the way to think about it.

Bob Ramsey: And I’m sorry,

how much was it this quarter?

Chuck Shaffer: I don’t

have the exact number, but yes I think you can say about 10 to 15 basis points is about we have in loan accretion in any

normalized quarter.

Bob Ramsey: Okay, all right, fair

enough. Last question and then I’ll hop out. This was definitely a good quarter for loan growth, loan originations. It looked

like the commercial pipeline was lower at period end. I’m just kind of curious, was there any element of pulling volume forward

or how you’re thinking about that commercial pipeline headed into the first quarter?

Dennis Hudson: Chuck Cross, do you

want to take a stab at that?

Chuck Shaffer: We might not have

Cross.

Dennis Hudson: I’m sorry?

I guess they must have dropped off or something.

Seacoast Banking Corporation of Florida

Exhibit 99.2

to Form 8-K Dated February 2, 2017

Page 16

Chuck Shaffer: Yes, I’ll take

it, since Cross has dropped off. I think we just cleared pipeline as we normally do. The first quarter is the toughest quarter

and that’s usual as we enter yearend that the pipelines get cleared, but we expect that to build here as we go.

Dennis Hudson: The other thing I

would say is what we disclosed I think is our solid parts of the pipeline. I know the discovery and underway kind of parts of the

pipeline have actually grown in January and we have a pretty optimistic view of Q1 and it should be fine. We’re actually

looking for pretty decent Q1. But you’re right, we did clear out a lot of the approved weighting at year end. And we’re now seeing it build back as we’ve gotten further into Q1.

Bob Ramsey: Okay, great, thank you,

guys.

Dennis Hudson: Thanks, Bob.

Operator: Thank you. [Operator instructions].

Our next question on line comes from Stephen Scouten from Sandler O’Neill. Please go ahead.

Stephen Scouten: Hi, guys, good

morning.

Chuck Shaffer: Hi, Stephen.

Stephen Scouten: Question for you

maybe to follow up on the loan growth conversation there. You guys noted that you have an opportunity to a degree with the CRE

level at about 214 on risk based capital. Is that something with competitors facing some constraints in your market, that you might

look to pursue more aggressively? And within that, do you think you’ll shift away from any of the granularity of your portfolio

and maybe start to take a stab at some larger deals on the CRE side?

Seacoast Banking Corporation of Florida

Exhibit 99.2

to Form 8-K Dated February 2, 2017

Page 17

Dennis Hudson: I’ll take a

stab at that, I would say we established guardrails covering credit risk back in 2009, and we haven’t changed any of those

guardrails nor do we have any intent to change those guardrails. So one of the key metrics that we keep an eye on is granularity

and we’re going to continue to focus on that. We have built the loan growth that we’ve been talking about here across

a whole host of asset classes on the balance sheet and certainly CRE is one of those, but it is by no means the only thing that

we focus on.

Having said that, I think we have an opportunity

to have some focus there. It’s not something currently under way, nor that is really currently anticipated. We also note

that as we look at acquisitions, often times we see larger CRE exposures in the smaller companies, and I think this provides us

some room for that. We can acquire those assets at the right marks, put them in the portfolio and while it may increase our CRE

exposure a little bit, it’s the right kind of exposure with the right kind of marks, and we feel pretty good about that.

Having said that, our guardrails are going to require us to keep a lower focus on CRE.

Chuck Cross, are you back on line, did

you have any comments on that?

Chuck Cross: Yes, my comment to

Stephen would be we had 18% year-over-year growth last year excluding acquisitions. The loan production last year was over a billion

dollars. It was about 50% consumer and residential, 25% C&I, and 25% CRE. Since that time, we added BMO and Floridian about

mid-year, so we think we’re going to have extra production capacity in 2017 in addition to the GulfShore acquisition in Tampa

and the teams that we’re building over in the Tampa market.

So those new markets will help us continue

with the loan production we’ve had in the past, but as Denny said, sticking to our guardrails.

Seacoast Banking Corporation of Florida

Exhibit 99.2

to Form 8-K Dated February 2, 2017

Page 18

Stephen Scouten: Okay, yes that’s

great, that makes a lot of sense. And then maybe if I could go back to the NIM here for a second, I know, Chuck, you gave kind

of a range for Q1 there, but I’m wondering what the kind of puts and takes are there. Do you have a way to quantify what

the benefit of the recent rate high case into Q1 numbers? I mean will that provide a little bit of a lift? And then with the wholesale

fundings, you mentioned not reinvesting in securities, so should we see those wholesale fundings kind of come down throughout the

year?

Chuck Shaffer: I think to

answer the question I’ll start with the wholesale fundings. I don’t think from this point forward, we may see a

small build in wholesale funding, but we don’t plan to continue to build that as we move through the remainder of the

year. So that’s the approach for wholesale funding.

On the NIM drivers, the three sort of biggest

issues there are going to be loan growth, as that builds throughout the year, as the investment portfolio declines, as well as the

voluntarily around accretion in that 10 to 15 basis points, but we generally should see it improve as we move through the year.

Steve Fowle: And that’s assuming

flat rates. So an up rate environment would only benefit us from there.

Chuck Shaffer: And around the increase

in the most recent Fed, that’ll benefit us. I don’t have the number here to talk about today, but it is beneficial

and it’s worked into the guidance that we provided for 2017.

Stephen Scouten: Okay, okay, so

the mid-350 in 1Q and mid-360 by yearend, that all assumes no further rate hikes.

Chuck Shaffer: Correct.

Stephen Scouten: Okay, great that’s

good to know. Okay and then last one for me, just on the expense front, I know this quarter there was obviously a big move down

in salary, some of that was an accrual reversal, a big move down in occupancy and a big move up in the other non-interest expense,

can you give any—I know there’s some color in the release—but maybe a good starting point for 1Q expense run

rate or kind of how this—with any unusual items that was within there that we’re not aware?

Seacoast Banking Corporation of Florida

Exhibit 99.2

to Form 8-K Dated February 2, 2017

Page 19

Chuck Shaffer: The best way to think

about Q3 to Q4 is the biggest change there was the consolidation of the ten branches in Orlando and the final sort of closure to

the Floridian and BMO mergers.

Dennis Hudson: And a full quarter

impact of everything that had happened in Q3 and a little bit in Q2.

Chuck Shaffer: Correct. Except for salary and wages, I think it reflects the real trends. We should see increased payroll and 401(k),

as well as some more normalized compensation accruals will come back in. The way to think about salaries and wages we should expect

it to go up about 10% Q4 to Q1. Outside of that the rest of the line items are pretty normalized.

Stephen Scouten: Okay. So, that

jump to $3.7 million from $1.6 million in the other that’s going to be something that’ll stick around?

Steve Fowle: The other expenses

were flat, Stephen, flat or down quarter-to-quarter.

Stephen Scouten: Okay. Alright,

I’ll have to go back and look at my numbers, maybe that’s me, sorry about that.

Steve Fowle: Yes, okay. And as a

reminder Q1, I think we said this already, but as a reminder, Q1 is for like for the rest of the industry, Q1 is a tough quarter.

Less days to earn fees on, less days to earn net interest income on and expenses pop up with the salary and benefits dynamics Chuck

talked about.

Operator: [Operator instructions].

Our question online comes from Mr. David Feaster from Raymond James. Please go ahead. Your line is open.

Seacoast Banking Corporation of Florida

Exhibit 99.2

to Form 8-K Dated February 2, 2017

Page 20

David Feaster: Good morning, guys.

I would like to talk about fee income for a second. It was up nicely in 2016. As we head into 2017 obviously mortgage is going

to be under some pressure. Could you just give us some color on your expectations for fee income businesses and how you think about

trends and would you consider maybe doing some non-bank M&A to supplement some of your trust or what management lines of the

business?

Chuck Shaffer: Yes, thanks, David.

So, the way to think about it, as you think about the components of our non-interest income, our service charges on deposits

are largely correlated with growth in the organization and household growth. So, continuing our focus on organic growth should

benefit that as we move through the year. And our trust and wealth businesses, we began to reinvest in that in 2016. Looking forward

into 2017 we’d like to see that continue to grow. We have considered all kinds of options, things are always on the table.

We’re always considering M&A in various ways so that’s out there. There’s nothing M&A or nothing

that’s being worked out currently but we are open to it.

In mortgage banking we expect a good

year as we continue to build out in Orlando and continue to build out into south Florida. We should continue to see check and

debit card interchange continuing to perform well. Some of the investments we made in the talent in the automation and the marketing

team we brought in over the past few years, has led to good results there that’s driving spend and we continue to focus on

that line item moving forward as well.

So, I think you’d continue to see

positive trends throughout 2017.

David Feaster: Okay that’s

helpful. On provision expense, it was a bit higher than expected. You actually saw charge-offs after several quarters of net recoveries.

Do you think we’re kind of ending the credit cycle or entering the credit cycle and that reserve releases should slow and

that we should start to see more normalized levels of provisioning and charge-offs going forward?

Seacoast Banking Corporation of Florida

Exhibit 99.2

to Form 8-K Dated February 2, 2017

Page 21

Dennis Hudson: I would just say

that you’re right. We didn’t have the recoveries this quarter. We’ve had kind of an unusual series of recoveries

during a good part of 2016 that kind of went to basically nothing or very low this quarter. And I think that was certainly impactful,

but of course the driver to provision in the quarter and really throughout the year has been loan growth. It’s been covered

to some degree with unusual levels of recoveries; those recoveries did not occur this quarter. I think we would expect to see those

recoveries continue to remain a little more modest going forward than they were in 2016. So, we’re counting on generally

higher provisioning in ‘17 than we would have seen in ‘16 primarily driven, all totally driven, by more aggressive

loan growth.

David Feaster: Okay, that’s

helpful. Last one from me, more of a high level question, you have a pretty wide footprint across Florida’s West Coast. Could

you just give us a pulse of the Florida economy? It’s still 1,000 people moving here a day. Are you seeing increased optimism

in your clients and after the election and increased willingness to grow and invest in their businesses? What are some notable

trends that you’re seeing in the Florida economy?

Dennis Hudson: I think there’s

no doubt that we are now seeing increased optimism on the part of our customer base as we talk with small businesses (and) as we

talk with larger commercial clients. What I see and some of the things that we’re working on are folks more willing to invest

and grow, but I think it’s more fundamental than that, I think the economy in Florida continues to perform extremely well.

I think the thing that has kicked in the

last quarter or two which I’ve been talking about all year, is a return of broader base construction primarily around residential

and that’s being driven by a lack of inventory for new product across the state. So, whether it would be Orlando or

South Florida or Tampa, we’re seeing much higher levels of constructions spend. I’m not talking high rise; I’m

talking more broad-based type construction which is certainly helping with the employment situation. There was kind of the lapse,

the structure component to GDP growth is back, and so I think we’ll continue to see positive things there.

Seacoast Banking Corporation of Florida

Exhibit 99.2

to Form 8-K Dated February 2, 2017

Page 22

Any insights, Chuck or Julie, that you’ve

noticed?

Julie Kleffel: Denny, this is Julie.

I would echo your comments as we spend a lot of time with small business owners, optimism is very high and investments in their

business continue both in expansion and in innovation and so I believe that it’s a forward-looking positivity across the

state of Florida.

David Feaster: That’s helpful.

Thanks.

Dennis Hudson: So, optimism got

huge. But I think it’s more fundamental than that and really I have a pretty positive outlook. I think we have some nice

runway ahead of us over the next couple of years in the state as things have fully come back on line. And the other thing that’s

no surprise to any of us, is the number of folks moving to the state is back up to a pretty high level now, and we’re seeing

it consistently across the state.

I guess one other final comment I’ll

make is I’m amazed with some of the industrial growth. We’re seeing industrial warehouse really advancing very quickly,

particularly around the center part of the state, and I think it’s a function of what’s happening to a great degree

in the way the business model is changing for retailing and other things like that; we see tremendous growth there. That is not

something I am interested in having us participate in very strongly. It tends to be more speculative and not something that fits

our risk profile, and they also tends to be larger than our risk appetite in terms of size. But that’s been big delta, I’d

say, over the last 12 months in those markets.

David Feaster: That’s very

helpful. Thank you.

Dennis Hudson: Great. Thanks, David.

Seacoast Banking Corporation of Florida

Exhibit 99.2

to Form 8-K Dated February 2, 2017

Page 23

Operator: And this time I see we

have no further question in queue. I would like to turn the call back over to Mr. Dennis Hudson for closing remarks.

Dennis Hudson: Great. Well, thank

you all for joining us today. Again we look forward to seeing you hopefully on February 22nd in New York where we’re

going to be talking more deeply about our go-forward strategy and implications in the medium term. Thank you for attending today.

Look forward to seeing you then and on next quarter’s call.

Operator: Thank you, ladies and

gentlemen. This concludes today’s conference. Thank you for participating. You may now disconnect.