EXHIBIT 99.2

To Form 8-K dated October 28, 2013

Seacoast Banking Corporation of Florida

Third Quarter 2013 Earnings Conference

Call

October 28, 2013

10:00 AM Eastern Time

Company Participants:

Dennis S. Hudson, III, Chairman and Chief Executive Officer,

Seacoast Banking Corporation of Florida

William R. Hahl, Executive Vice President

and Chief Financial Officer, Seacoast Banking Corporation of Florida

Other Participants:

Scott J. Valentin, Analyst, FBR Capital Markets

Robert S. Madsen, Analyst, Stephens, Inc.

Jefferson Harralson, Analyst, Keefe, Bruyette & Woods, Inc.

Kyle A. Oliver, Analyst, Raymond James & Associates, Inc.

Management Discussion:

Operator: Good morning

and welcome to the Seacoast Third Quarter 2013 Earnings Conference Call. My name is Brandon, and I'll be the operator for today's

call. At this time, all participants are in a listen-only mode. Later, we will conduct a question-and-answer session. Please note

that this conference is being recorded.

I will now turn it over to Mr. Dennis

Hudson. Sir, you may begin.

Dennis S. Hudson III: Thank you

very much, and welcome to Seacoast's Third Quarter 2013 Conference Call. Before we begin, as always, I direct your attention to

the statement contained at the end of our press release regarding forward statements. During the call, we may be discussing certain

issues that constitute forward-looking statements within the meaning of the SEC Act. Accordingly, our comments are intended to

be covered within the meaning of Section 27A of that Act.

With me today is Bill Hahl, our CFO, and

David Houdeshell, our Chief Credit Officer.

Well, we certainly achieved some critical

milestones this quarter. Our regulatory and capital agreement and capital restrictions were completely terminated over the summer,

as we had previously announced, and, as indicated this morning in our release, our sustained earnings' improvements and our earnings'

outlook allowed us to bring the deferred tax asset back onto the balance sheet. Most pleasing to me anyway, however, was our continued

earnings improvement this quarter. When you exclude the one-time impact of the DTA recapture, our Q3 earnings before tax increased

62 percent over last quarter to $4.7 million. This is the third quarter in a row with greater than a 50 percent sequential growth

in earnings. So our before-tax earnings trend has been quite positive this year with us earning $2 million in Q1, $3 million

in Q2, and well over $4 million in Q3, and we expect to close out the year with continued strength. This improvement is the

result of our expense reductions, a portion of which was redeployed into new investments that are designed to grow revenue, and

also it was due to reduced credit cost.

These improvements in quarterly earnings,

together with the DTA recapture, resulted in GAAP earnings for the quarter of $45.9 million. Our tangible book value per common

share increased as a result and stood at $1.62 at September 30. Return on average assets for the quarter, including a normal tax

provision, but excluding the impact of the DTA recapture, was 0.53 on an ROA basis and return on average equity was 6.78 percent.

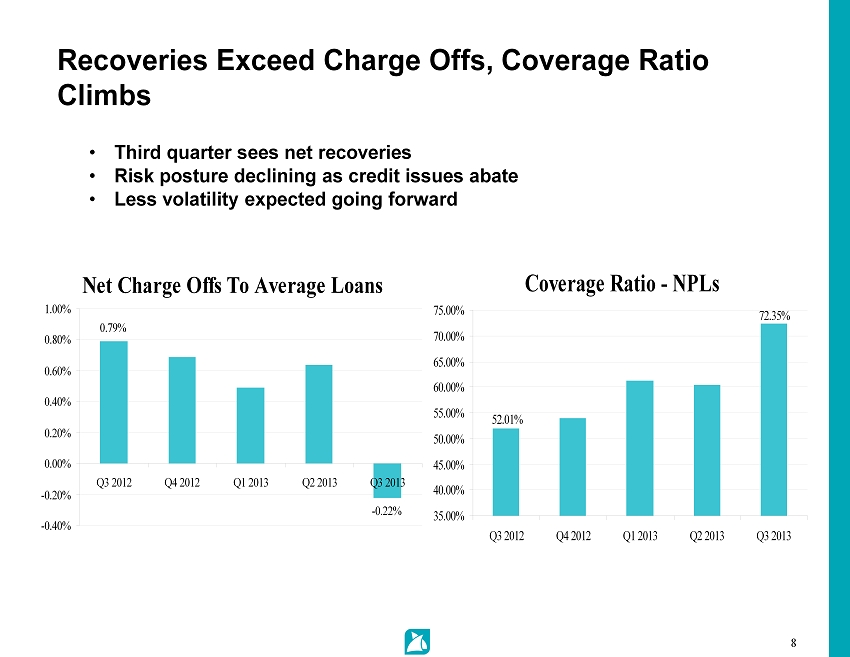

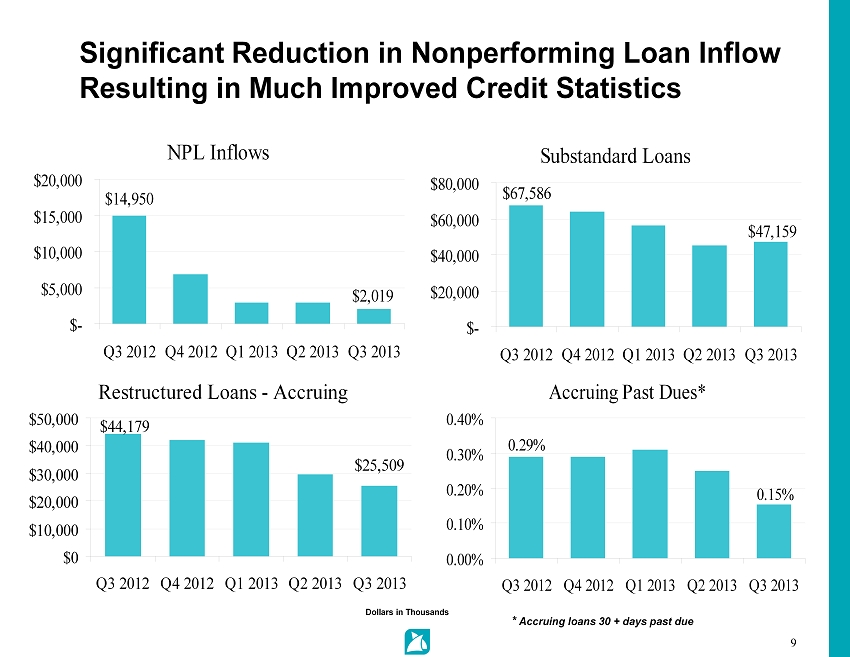

Our asset quality continued to improve this quarter, as it has done for many quarters. Nonperforming assets, which last quarter

fell below 2 percent of assets, were further reduced during the quarter to 1.6 percent of assets. We booked net recoveries during

the quarter, which negated the need for a provision. The allowance for loan losses actually increased to 1.64 percent of loans

from 1.59 percent last quarter. Coverage ratios have clearly increased substantially, and we believe our asset quality today is,

simply stated, now satisfactory.

Looking ahead, we see an improving local

economy; we see population growth returning to Florida; and most importantly, we now see construction activities starting to increase

all over our markets, all of which suggest to me that the state is now moving through an important inflection point and improving

economy. I believe now is a critical time for Seacoast to push forward faster with our revenue and our growth initiatives, again

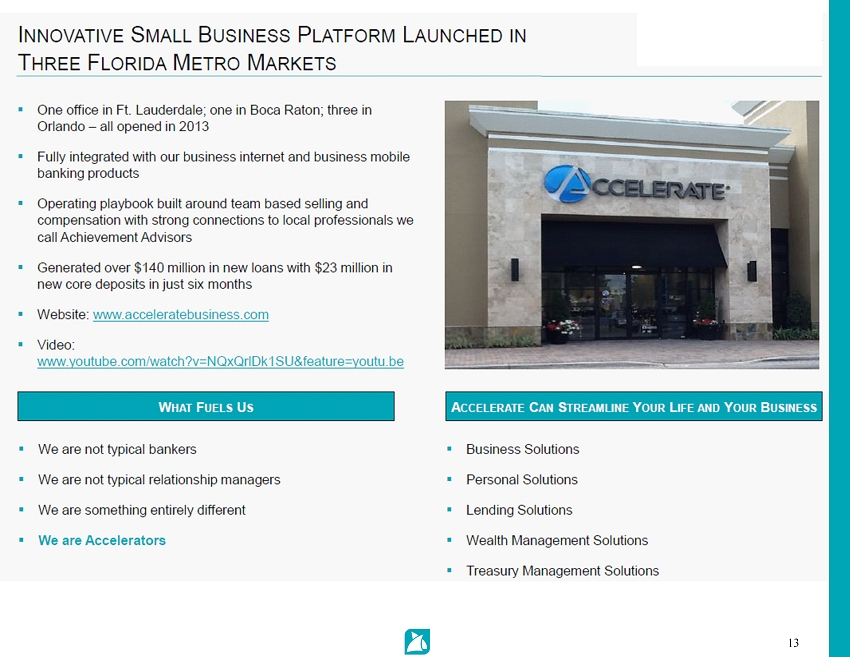

to drive better results, and I’ve been challenging our team to do just that. Earlier this year, we rolled out an innovative

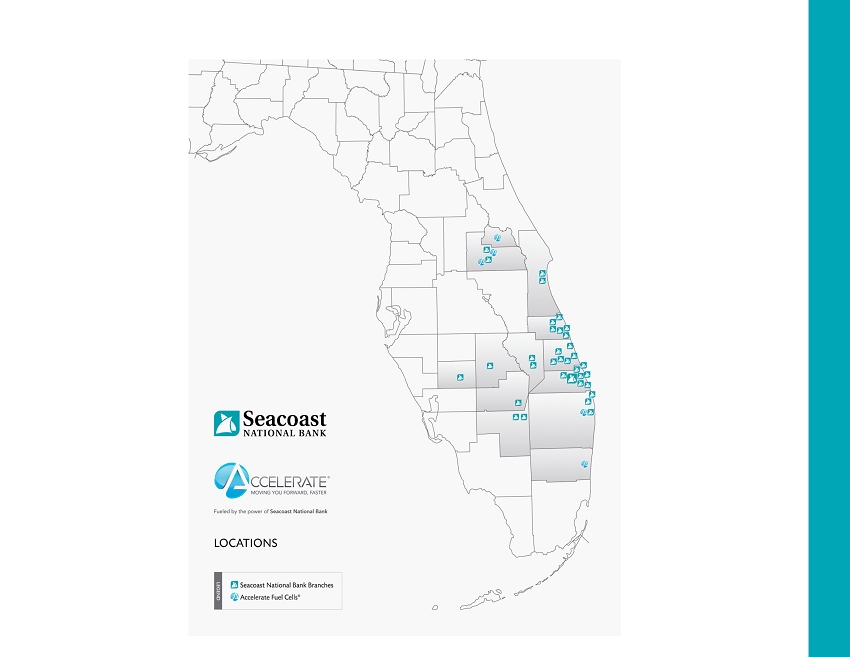

business banking platform in three metro Florida markets. Accelerate business is an integrated business banking solution built

around strong and experienced commercial leading teams, called Accelerators, and local professionals that we call Achievement Advisors,

who’ve been operating in markets together for many, many years. Accelerate Business is fueled by Seacoast to help move small

and medium sized businesses forward further and move them faster. We’ve integrated our comprehensive suite of Internet banking

services with our new business mobile platforms and have added deposit capture across all of our digital channels to bring branch

services right into the office of every one of our business clients. The bank comes to you, not the other way around; and when

we’re asked where our nearest branch is, we tell them it’s right here in your office. We added a couple of slides towards

the end of our deck that was posted for this call that provide a little more color on this latest growth initiative, and I invite

you to take a look. So far the results that have been produced have been quite impressive. Since rollout, we have more than doubled

our pace of business loan production and our new core business deposits. We expect this project will help us drive better performance

going forward into 2014 and we expect it to drive revenue growth at a higher pace in 2014 than we’ve achieved in 2013. I

want us to find more ways to redeploy our legacy expense structure into further expansion of both this platform and other digital

innovation projects our teams are working on.

So with that, I’d like to turn the

call over to Bill for a few more comments on the quarter. Bill.

William R. Hahl: Thanks, Denny;

and good morning, everyone. My remarks will reference the slide deck we posted for this call on our website, and I will begin on

slide three, and then Denny and I will take your questions.

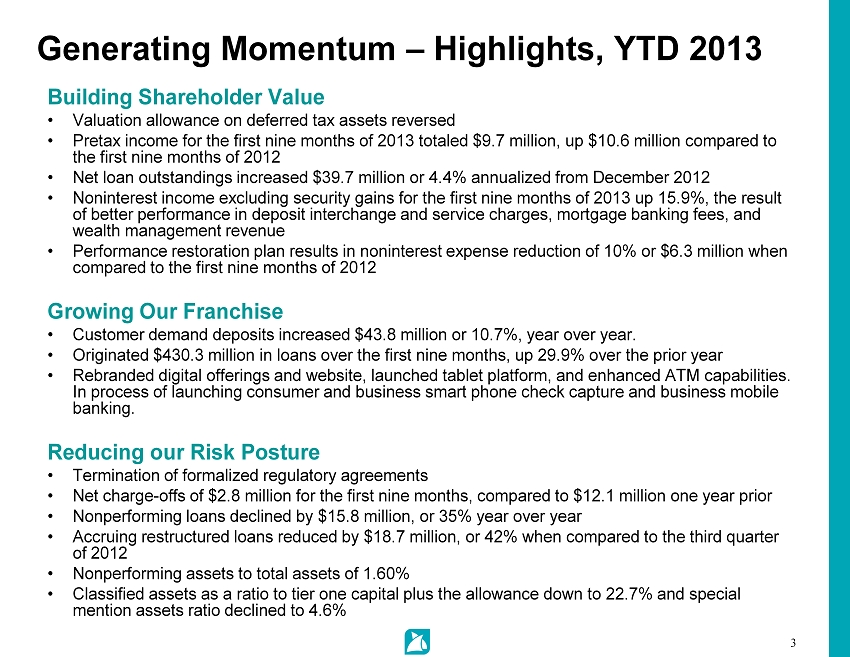

As Denny mentioned, we did reverse the

deferred tax valuation allowance, which increased net income for the quarter by $41.2 million. Without the reversal, it was still

a much improved quarter without any negative surprises with net income before tax of $4.7 million, up $1.7 million linked quarter,

and up $4 million compared to the prior year. Pre-tax income for the first nine months, excluding the DTA reversal, was $9.7 million,

up $10.6 million from last year’s net loss of $950,000. Net income available to common shareholders year-to-date was $48.1

million, or $0.51 per diluted common share compared to a net loss of $0.04 last year. Total revenue, excluding security gains,

for the third quarter were $22.9 million and were up $1.3 million compared to a year ago. On a linked quarter basis, revenues were

up approximately $500,000, reflecting the seasonally slower third quarter and the impact of higher interest rates which lowered

residential loan demand and fees from mortgage banking.

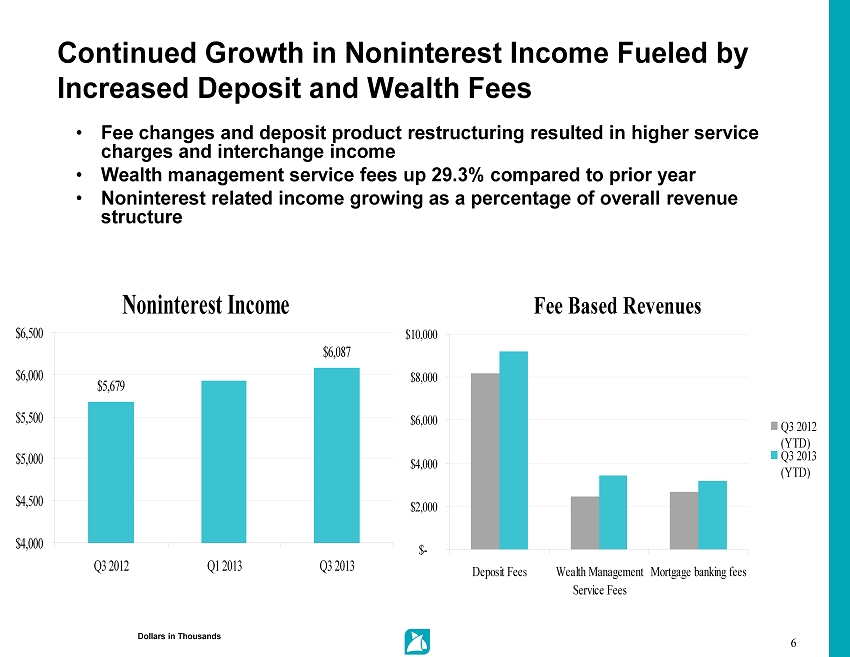

Year-to-date our tactics designed to build

noninterest income had positive impacts with fees higher by 15.9 percent year-over-year. Total revenues year-to-date grew year-over-year

by $2.9 million, or 4.5 percent, with mortgage banking up 28.5 percent, service charges up 8.0 percent, interchange fees up 19.9

percent. Slide six has some additional highlights about noninterest income growth for the quarter. Total assets increased year-over-year

by $67 million, funded by core customer funds with solid growth in noninterest-bearing transaction accounts which were up 10.7

percent year-over-year and now comprise about 27 percent of total deposits. Likewise, total transaction accounts were up 7.7 percent

year-over-year and they now comprise 53 percent of total deposits. Loan production year-to-date has increased nearly 30 percent

compared to 2012 and totaled $430 million and is the result of our investments in additional loan production personnel over the

last 12 to 15 months.

We look forward to taking advantage of

all the opportunities ahead of us and to positively leverage the strong core franchise we’ve built. Our focus has been on

expanding our products and services through to already stellar deposit franchise and enhancing customer experience by providing

convenient access to their accounts through digital technology. Nearly 40 percent of online customers have already adopted our

mobile products, and the annual growth rate for the mobile product adoption in the current quarter was over 92 percent. We have

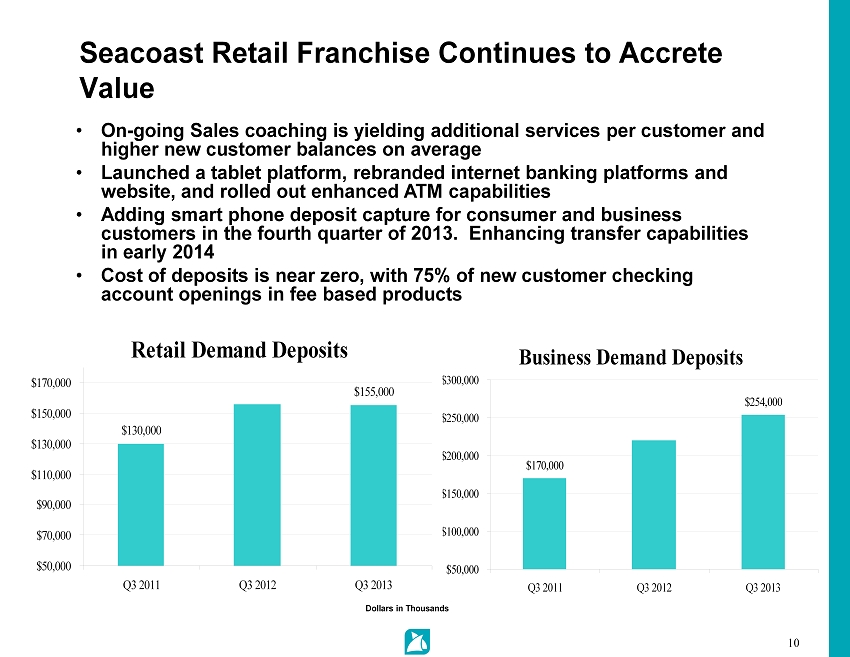

more to come as we increase our services per household and our revenues from our core deposit accounts. If you take a look at slide

10, you can see some of the things that we are doing to grow the franchise and the results we are producing.

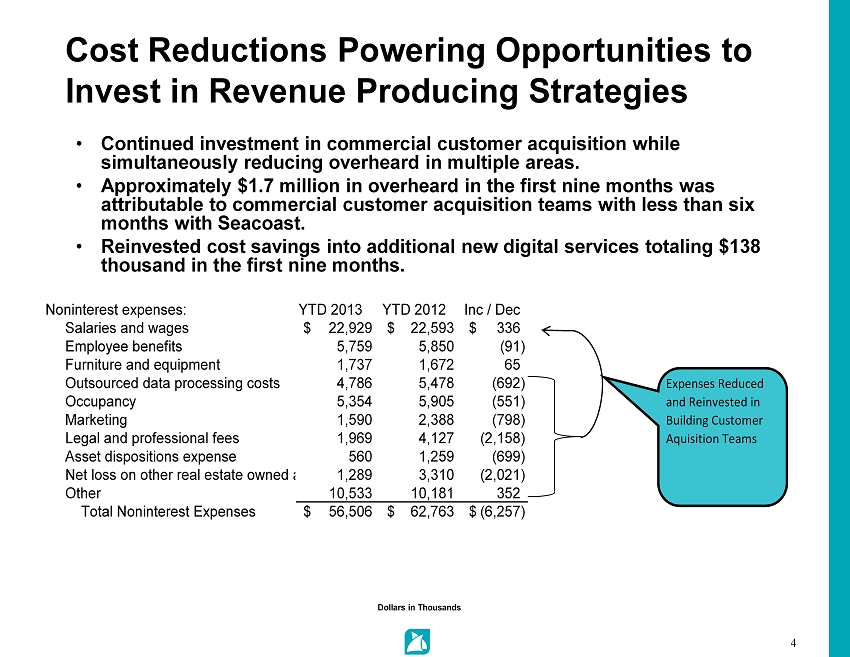

Now I’ll turn to slide four for a

few comments about cost reductions of noninterest expenses compared to a year ago. Over the last year, quarterly expenses have

been managed lower as a result of cyclical credit costs declining and our branch consolidations as well as other cost cutting initiatives.

In order to improve the margin and continue to grow loans, we have invested a significant portion of the expense reductions into

additional business bankers and credit support personnel and, more recently, enhancing the customer experience with additional

ways our customers can access their accounts through our digital channel. This quarter expenses are lower by $1.8 million, or 9

percent, compared to a year ago and are down $6.3 million year-to-date. This, together with revenue improvement, is reducing efficiency

ratio, indicating operating leverage is improving. We want to continue to grow revenues at a faster pace and to look for ways to

redeploy and reduce our legacy costs as we better align our delivery channels with evolving customer needs. The goal is to continue

to improve operating leverage while improving our overall top line growth rates.

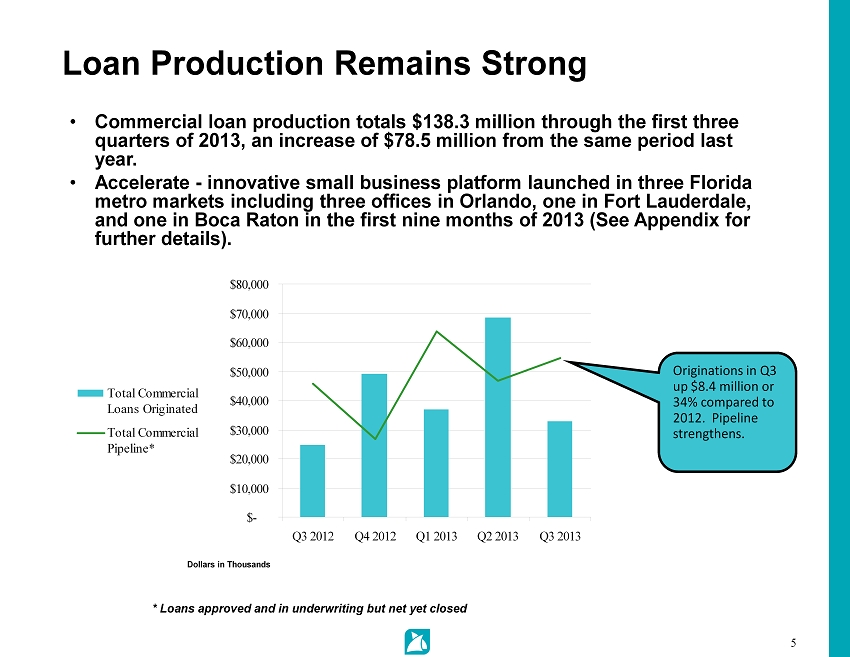

Loan production over the last twelve months

totaled $573 million and is up 120 percent compared to a year ago. Net loans were up 5.2 percent year-over-year. The improvement

in loan growth is the result of continued growth across most of our portfolios, including much better growth this year coming from

the commercial and business lending. We predicted on last quarter’s call that our commercial volume would be a little softer

due to the summer season and the higher interest rate environment, and it was. However, we are seeing stronger pipelines and expect

higher production through the rest of the year.

Now some color on the net interest margin.

After declining 7 basis points in Q1 and 3 basis points in Q2, the margin increased 13 basis points this quarter. Several factors

contributed to this improvement. The loan portfolio positively impacted by lower nonaccruals and higher average balances. Additionally,

the margin was positively impacted by 10 basis points from the recovery of interest income on a loan that had been on nonaccrual,

so net of this recovery the margin improved 3 basis points. Prepay speeds declined and yields increased by 6 basis points in the

securities portfolio in response to the increase in yield curve. Our continued progress improving core customer funding and the

improved deposit mix reduced both noninterest-bearing and sweep repo costs by one basis point. These results all contributed to

the increase in the margin for the quarter. Growing our net interest income remains our focus, and we believe we can continue to

generate growth even in this low rate environment. The primary opportunities for growth in net interest margin remain an improved

earning asset mix in favor of loans and further growth in core customer funding.

With that, I’ll turn the call back

to Denny.

Dennis S. Hudson III: Thank you,

Bill. You know something Bill said earlier in his comments I think bears repeating. He said our goal is to continue to improve

operating leverage while also improving our overall top line growth rates. I said earlier that I felt the Florida economy is an

important inflection point and I’m convinced this is going to drive more opportunities for growth here at Seacoast, but I

also believe we’re well into a critical inflection point of our own here at Seacoast. All of us are challenging each other

to find innovative ways to grow our revenues faster and to fund innovation required with the redeployment of our heavy legacy costs,

even as we continue to bring down our overall expense structure, and we must bring down legacy costs by discovering ways to better

align and integrate our delivery channels with customer preferences that are now starting to rapidly change. This is not a process

that is going to occur overnight, but it must occur over a more compressed timeframe than most community banks believe, and it’ll

result I think in greater convenience and an improved experience for our customers. What I’ve just said is going to drive

a lot of innovation over the next couple of years and it’s going to separate the winners from the losers in the marketplace.

For me it’s an invigorating challenge and I’m going to have fun reporting back to you our progress as we continue to

discover new opportunities for growth.

With that, I’d like to open it up

for a few questions.

Question & Answer Section:

Operator: Thank you, and

we will now begin the question-and-answer session. If you have a question, please press star/one on your touchtone phone. If you

wish to be removed from the queue, please press the pound sign or the hash key. There may be a delay before the first question

is announced. If you’re on a speakerphone, please pick up your handset first before pressing the numbers. Once again, if

you have a question, please press star/one on your touchtone phone.

And from FBR Capital Markets we have

Scott Valentin online. Please go ahead.

Scott Valentin: Good morning, and

thanks for taking my question. Just with regard - - you mentioned regulatory agreements have been lifted, the DTA valuation

allowance has been recovered. Can you address maybe the TARP repayment, and you still have some preferreds outstanding, just wondering

as we approach the reset date in early ’14 if you have any plans?

Dennis S. Hudson III: Yeah, we haven’t

announced any plans. It’s obviously something we continue to focus on and explore all of our options and when we have something

to say, we will. I would say that we have many options. We’re considering all of them. We’ll take a look at it, anywhere

from funding it internally to other capital transactions. So we’ll look at everything and we’ll let you know when we

have something to say.

Scott Valentin: Okay, thanks, and

then just a follow-up question. Loan origination volume was pretty strong, but the overall loan growth was less than we expected.

Is that just a function of high payoffs during the quarter I assume?

Dennis S. Hudson III: Yeah, we actually

did have some fairly unusual and high payoffs this quarter and it included some larger troubled debt restructures, which of course

were accruing and so forth, so we continue to work through those. I would say our outlook, Bill, is probably for fewer payoffs

as we look ahead. We’re running out of large credits to get refi’d and paid off.

William R. Hahl: Yep.

Dennis S. Hudson III: And David’s

shaking his head as well, so probably continued decent volume will result in a little better loan growth as we look forward. That’s

our plan.

Scott Valentin: Okay, thanks. I’ll

get back in the queue. Thank you.

Operator: From Stephens

we have Robert Madsen online. Please go ahead.

Robert Madsen: Yeah, good morning,

gentlemen.

William R. Hahl: Good morning.

Robert Madsen: I was just curious, how

many new lenders did you hire during the quarter and how does that shake out year-to-date, and then what is your expectation for

the size of books that these lenders should have and the timeline for them to get to a full book?

Dennis S. Hudson III: In the press

release, we disclosed quite a bit of information about the incremental costs associated with those hires. There’s a table

in the back or the body of the release that describes the investment, and today we’re carrying… One way we look at

it is we expect in 90 days we should see a pipeline growing after a new hire, and at the six-month mark we expect to see production

actually hitting the books. We firmly believe the first six months are really an investment period; and we’re carrying about

$0.5 million a quarter of incremental expense, which is a pretty significant number on an $18 million core overall expense structure.

We’re carrying $0.5 million a quarter, maybe $2.0 million a year of incremental expense related to people who have been here

six months or less. I don’t think we’ve published the number in terms of what we’ve hired this quarter. But in

aggregate, if you go back to the middle of ’12 when we started some of this hiring, we’ve probably hired 30 plus guys,

I would say.

Robert Madsen: Okay. So then

just moving onto the expense side, so you’ve targeted it looks like $7.4 million of expense reductions for the year and then

you’re adding these lenders, you’re getting - - you’re going to get increased loan growth. So could you talk

a little bit about your goals for the efficiency ratio and where you can see that going over the next year or so?

Dennis S. Hudson III: Yeah, we haven’t

said anything about the next year, but clearly we need to get our overall efficiency ratio in much better shape. It’s begun

to move a little better in the last couple of quarters, as you can see, but we are targeting that down in the mid 60s over the

next couple of years. It’s going to come through a combination of all the things we talked about during the call—revenue

growth as well as redeployment as well as just wringing costs out. One big factor to that over time clearly is adjusting our distribution

costs, so we have a lot of plans in and around that. We’re not pleased with where our efficiency ratio is today. We want

to get it down, but we also want to take advantage of what we see as a pretty significant turn in the economy here, so we want

to be investing and driving revenue growth in this period. That’s the most important thing for us to be doing, but all the

while finding ways to rationalize our expense structure, and we think in a couple of years it could be in a much better position.

It’ll take a little bit of time, but we’re making good progress every quarter.

Robert Madsen: Okay, thank you.

Operator: We have Jefferson

Harralson online. Please go ahead.

Jefferson Harralson: Hi, thanks.

I want to ask my first question on the business model change that you were talking about—the Accelerators and your Achievement

Advisors. Can you just talk about just what you’re doing there and how’d you characterize that relative to the former

model and why you went to it and what you expect to get out of that change?

Dennis S. Hudson III: We did a lot

of work contacting some of our existing business clients and shadowed them in terms of what they do every day with respect to their

need for financial services and banking services. It really, Jefferson, answers the question: As more and more of our transactions

get ported over to digital channels, particularly in the business area, we think there’s a great opportunity to do a much

better job serving our business clients. And we think the way we serve those business clients is take the bank into their office.

It answers the question for us, as a community bank: How do we grow our exposure, particularly in more metro markets where we’re

currently operating in South Florida and Orlando? How do we grow our franchise and our customer base there without a huge branch

infrastructure, and couldn’t that actually be a competitive advantage for us to approach it that way? This project, which

we developed about a year ago, was something that we felt answered that question and most importantly met customer needs. With

continuing growth in remote deposit capture now rolling out in all of our digital products, we just don’t see the need for

the branch, particularly when it comes to the business customer. We also focused our selling effort and our marketing into businesses

that can connect with this technology more easily. I think that’s a key focus for us in that business line, and yet it also

comes with a guy that you know as a business owner and he is your guy and he takes care of everything you need because he’s

backed by a good-sized community organization with all of the products and services that you need, but he brings them into your

office. So these guys are less about big office buildings, they’re more about being in our customers’ offices.

Jefferson Harralson: All right,

awesome, thank you. I want to follow up just with a model question: Can I get the bank level leverage ratio and the holding

company cash for the model?

Dennis S. Hudson III: We’ll

get back to you on those ratios. They’re stronger than the consolidated ratios a little bit, so we’ll get back with

you on that.

Jefferson Harralson: All right,

thank you.

Operator: From Raymond

James, we have Kyle Oliver online. Please go ahead.

Kyle Oliver: Hey, guys, how’s

it going?

Dennis S. Hudson III: Good.

Kyle Oliver: Just looking at loan growth

during the quarter, I know you said there were some large payoffs, but where are you seeing the most strength by market?

Dennis S. Hudson III: I would say

the South Florida market. Wouldn’t you agree, David?

David D. Houdeshell: Yes, I certainly

would.

Dennis S. Hudson III: Yeah, the

South Florida market is extremely busy today. We’re doing quite a bit in Broward County, which would be Boca and South. Palm

Beach County is doing much better, and our Treasure Coast region is doing… I mean we’re really seeing strengthening

occurring all over, but clearly a lot of opportunities in South Florida. The Orlando market has also improved quite a bit for us

and we’re seeing sort of continued growth in that market. So it’s kind of all over, but I would say it’s particularly

strong the further south we go. Miami was very quick to come back and that’s spreading up the East Coast and we’re

feeling that big time I would say up here in Palm Beach County and north finally, which is great. One thing I mentioned on the

call was the return of construction. That’s a key industry in the State of Florida and it was a pummeled industry during

the downturn. You know you saw a lot of construction cranes in Miami early on as things turned, but we’re now seeing lots

of houses and construction starting to occur in Orlando and even in the Treasure Coast area where we have a big concentration.

That’s really beginning to drive I think employment numbers in the right direction; and it’ll be interesting to see

as we hit the end of the year what kind of impact that has, but a lot of houses, a lot of construction. Things are starting to

turn in a more remarkable way.

Kyle Oliver: Okay, great. And

just along with the growth, have you started to see the big box competitors come back in those markets or is it still mostly community

banks?

Dennis S. Hudson III: Well, I would

say many of the community banks were wiped out and many of the competitors that we had prior to the crisis no longer exist. Frankly,

we find in most of our markets that it’s us competing with the mega banks. The mega banks have become more competitive in

the last year as they have struggled I think to maintain some of their lending balances and struggled with the same things all

of us are in this low rate environment. We find it’s become a more stark, bifurcated market that actually is an advantage

for us. So that’s one reason we’re so excited about some of the new projects we have to grow revenues. We think we

look very different compared to the mega banks and there are very few community banks out there today that are able to compete.

Kyle Oliver: Okay, great, guys.

Thank you very much.

Operator: And from FBR

Capital Markets we have Scott Valentin back online. Please go ahead.

Scott Valentin: Thanks for taking

the follow-up question. With regards to margin, I know you pointed out I think in the 13 basis points, 10 basis points was recovery

of accrued interest, but yet you had about 3 basis points of core expansion. Is it fair to assume going forward we can get a couple

of basis points every quarter due to mix shift?

Dennis S. Hudson III: Generally

I would say yes; however, we are going in, Bill, into Q4, which we tend to see the balance sheet grow there.

William R. Hahl: Right.

Dennis S. Hudson III: And we’re

going to probably have too much liquidity as we go into Q4, which could limit the margin in Q4. So if you go back and …

Well, you really can’t because of the last several years we really haven’t had a normal seasonal growth, but we’re

looking to try to preserve that I would say in Q4 and then it starts growing as we get beyond the seasonal growth impact that happens

in the winter to us.

Scott Valentin: Okay. And then just

a follow-up on the… Oh, sorry.

Dennis S. Hudson III: Just to be

clear, we are seeing margin expansion out over the next few quarters, but there may be some short-term mitigation due to the seasonal

impacts, but it is going to yield higher net interest income.

Scott Valentin: Okay, and then…

Dennis S. Hudson III: Yeah, you

had a follow-up.

Scott Valentin: Yep, just a follow-up

on the deferred tax asset valuation allowance, is there anything left, or you fully used the valuation - - recovered the valuation

allowance?

William R. Hahl: Yeah, we fully

recovered it.

Scott Valentin: Fully recovered

it, okay. And then the effective tax rate going forward you expect?

William R. Hahl: Thirty-eight percent.

Scott Valentin: Thirty-eight, okay.

Thank you.

Operator: And we are standing

by for any further questions.

From Stephens, we have Robert Madsen

back online. Please go ahead.

Dennis S. Hudson III: Robert.

Robert Madsen: With the improvement…

Yeah, sorry about that. With the improvement in your credit quality and the removal of the regulatory orders, when do you think

you could start seeing an improvement in the FDIC assessment expense?

William R. Hahl: Those two aren’t

really tied for community banks at all. It’s just a straight calculation, so there won’t be any improvement in the

FDIC expense. We had all the improvement a year ago I think when we switched over.

Dennis S. Hudson III: Does that

answer your question?

Robert Madsen: Yeah, thank you.

Dennis S. Hudson III: Thank you.

Operator: And we have

Jefferson Harralson back online. Please go ahead.

Jefferson Harralson: Hi. A quick

one on the regulatory capital. How much of the DTA has come back into regulatory capital and how much still will come in over time?

William R. Hahl: Yeah, Jefferson,

nothing really additional. We’ve been recognizing in the past from some tax planning strategies and so we were including

some of the deferred tax asset in regulatory capital, so there really won’t be a big change to our regulatory capital ratios

as a result of the recovery.

Dennis S. Hudson III: But, as you

know, as earnings improve and our forward view of earnings improves, it will gradually increase more of that deferred asset that

can be pulled into regulatory capital. You know there are severe limitations on it, but you can look at the next year’s earnings

estimates and come up with a conservative number you can throw into regulatory capital. Up until recently, that obviously has not

been as significant as it will be going forward, so Bill’s right. Obviously we don’t look for any immediate change

of any significance, but over time, and I’m talking over the next year, that will gradually increase.

Jefferson Harralson: Okay. And

so how much is allowed to come through? Is it in the 40s?

William R. Hahl: How much that’s

excluded?

Jefferson Harralson: Right.

William R. Hahl: About 50 million

- - about 50 million is excluded.

Jefferson Harralson: All right,

great. Thank you.

Operator: And once again,

we'll stand by for any further questions. Okay, it looks like no further questions at the moment. Mr. Hudson, I’ll turn it

back to you for any closing remarks.

Dennis S. Hudson III: Thank you

very much. We appreciate your attendance today and look forward to next quarter’s results. Thank you.

Operator: And this concludes

today’s conference. Thank you for joining. You may now disconnect.