Exhibit 99.2

www.thorindustries.com INVESTOR PRESENTATION JUNE 10, 2019

Forward Looking Statements 2 This presentation includes certain statements that are “forward looking” statements within the meaning of the U . S . Private Securities Litigation Reform Act of 1995 , Section 27 A of the Securities Act of 1933 , as amended, and Section 21 E of the Securities Exchange Act of 1934 , as amended . These forward looking statements are made based on management’s current expectations and beliefs regarding future and anticipated developments and their effects upon Thor, and inherently involve uncertainties and risks . These forward looking statements are not a guarantee of future performance . We cannot assure you that actual results will not differ materially from our expectations . Factors which could cause materially different results include, among others, raw material and commodity price fluctuations ; raw material, commodity or chassis supply restrictions ; the impact of tariffs on material or other input costs ; the level and magnitude of warranty claims incurred ; legislative, regulatory and tax law and/or policy developments including their potential impact on our dealers and their retail customers or on our suppliers ; the costs of compliance with governmental regulation ; legal and compliance issues including those that may arise in conjunction with recently completed transactions ; lower consumer confidence and the level of discretionary consumer spending ; interest rate fluctuations ; the potential impact of interest rate fluctuations on the general economy and specifically on our dealers and consumers ; restrictive lending practices ; management changes ; the success of new and existing products and services ; consumer preferences ; the ability to efficiently utilize production facilities ; the pace of acquisitions and the successful closing, integration and financial impact thereof ; the potential loss of existing customers of acquisitions ; our ability to retain key management personnel of acquired companies ; a shortage of necessary personnel for production ; the loss or reduction of sales to key dealers ; disruption of the delivery of units to dealers ; increasing costs for freight and transportation ; asset impairment charges ; cost structure changes ; competition ; the impact of potential losses under repurchase or financed receivable agreements ; the potential impact of the strength of the U . S . dollar on international demand for products priced in U . S . dollars ; general economic, market and political conditions ; the impact of changing emissions standards in the various jurisdictions in which our products are sold ; and changes to investment and capital allocation strategies or other facets of our strategic plan . Additional risks and uncertainties surrounding the acquisition of Erwin Hymer Group SE ("EHG") include risks regarding the potential benefits of the acquisition and the anticipated operating synergies, the integration of the business, the impact of exchange rate fluctuations and unknown or understated liabilities related to the acquisition and EHG's business . These and other risks and uncertainties are discussed more fully in Item 1 A of our Annual Report on Form 10 - K for the year ended July 31 , 2018 and Part II, Item 1 A of our quarterly reports on Form 10 - Q for the periods ended January 31 , 2019 and April 30 , 2019 . We disclaim any obligation or undertaking to disseminate any updates or revisions to any forward looking statements contained in this presentation or to reflect any change in our expectations after the date hereof or any change in events, conditions or circumstances on which any statement is based, except as required by law .

Third Quarter Update 2019 Overview & Current Industry Conditions Appendix: Financial & Market Data 4 11 19 Table of Contents 3

Third Quarter Update 2019 4

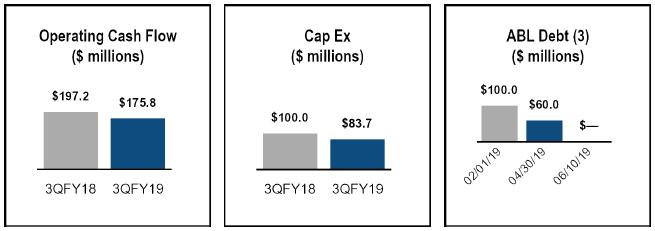

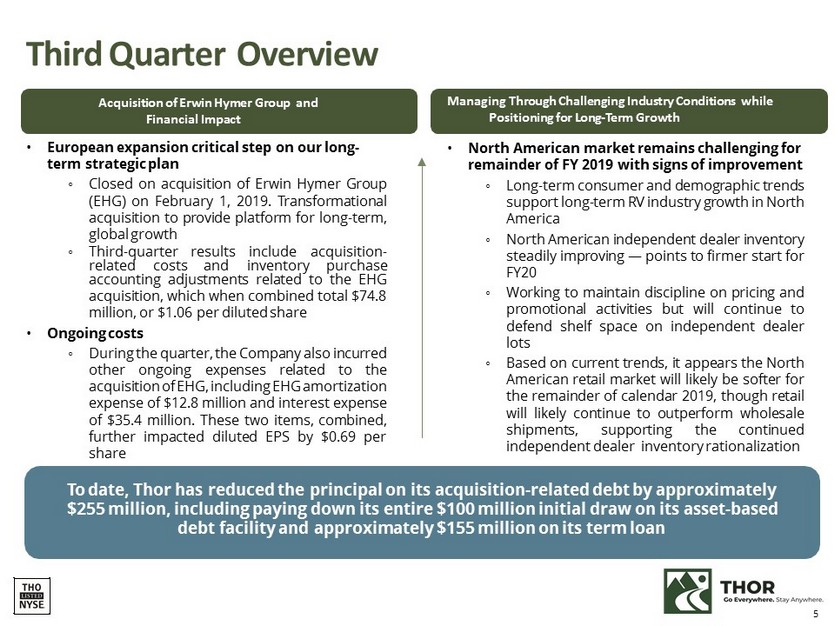

Third Quarter Overview • European expansion critical step on our long - term strategic plan ◦ Closed on acquisition of Erwin Hymer Group (EHG) on February 1 , 2019 . Transformational acquisition to provide platform for long - term, global growth ◦ Thi r d - quarter r esults include acquisition - r elated costs and inventory pu r chase accounting adjustments related to the EHG acquisition, which when combined total $ 74 . 8 million, or $ 1 . 06 per diluted share • Ongoing costs ◦ During the quarter, the Company also incurred other ongoing expenses related to the acquisition of EHG, including EHG amortization expense of $ 12 . 8 million and interest expense of $ 35 . 4 million . These two items, combined, further impacted diluted EPS by $ 0 . 69 per sh are • North American market remains challenging for remainder of FY 2019 with signs of improvement ◦ Long - term consumer and demographic trends support long - term RV industry growth in North America ◦ North American independent dealer inventory steadily improving — points to firmer start for FY 20 ◦ Working to maintain discipline on pricing and promotional activities but will continue to defend shelf space on independent dealer lots ◦ Based on current trends, it appears the North American retail market will likely be softer for the remainder of calendar 2019 , though retail will likely continue to outperform wholesale shipments, supporting the continued independent dealer inventory rationalization Acquisition of Erwin Hymer Group and Financial Impact Managing Through Challenging Industry Conditions while Positioning for Long - Term Growth To date, Thor has reduced the principal on its acquisition - related debt by approximately $255 million, including paying down its entire $100 million initial draw on its asset - based debt facility and approximately $155 million on its term loan 5

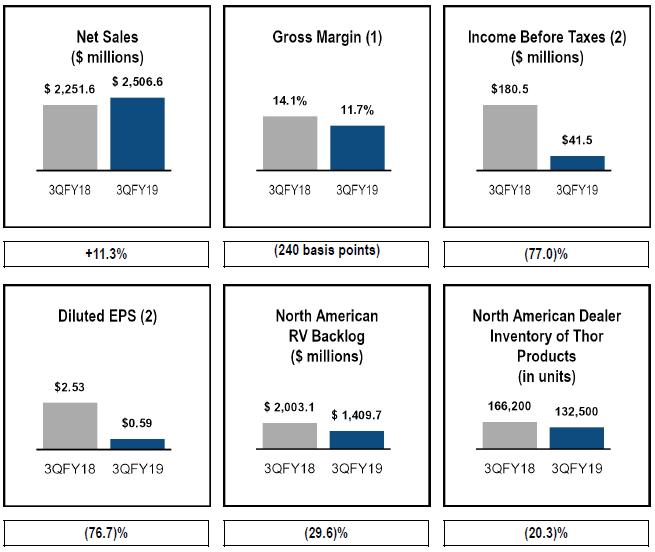

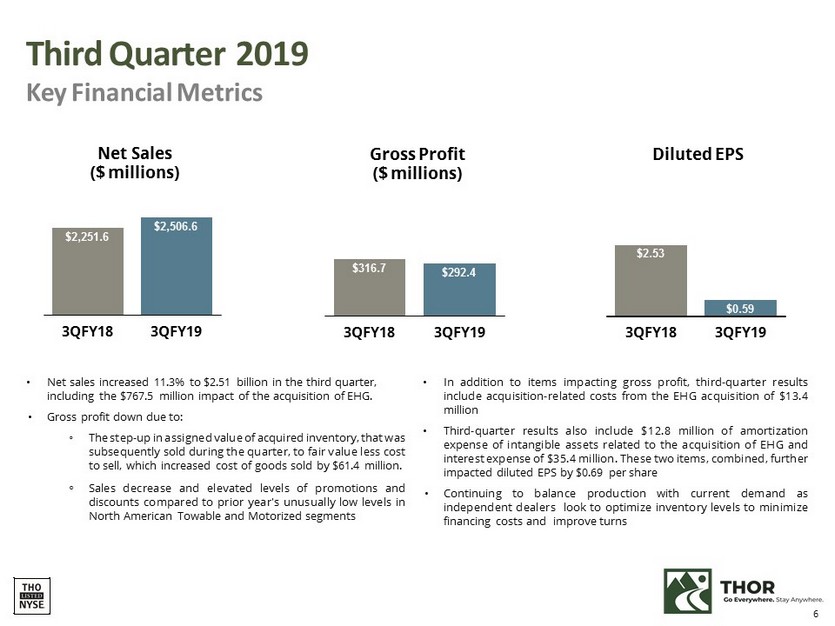

Third Quarter 2019 Key Financial Metrics Net Sales ($ millions) 3QFY18 3QFY19 $2,251.6 $2,506.6 Gross Profit ($ millions) 3QFY18 $316.7 $292.4 Diluted EPS 6 $2.53 $0.59 • Net sales increased 11.3% to $2.51 billion in the third quarter, including the $767.5 million impact of the acquisition of EHG. • Gross profit down due to: ◦ The step - up in assigned value of acquired inventory, that was subsequently sold during the quarter, to fair value less cost to sell, which increased cost of goods sold by $ 61 . 4 million . ◦ Sales decrease and elevated levels of promotions and discounts compared to prior year's unusually low levels in North American Towable and Motorized segments 3QFY19 3QFY18 3QFY19 • In addition to items impacting gross profit, third - quarter results include acquisition - related costs from the EHG acquisition of $ 13 . 4 million • Third - quarter results also include $ 12 . 8 million of amortization expense of intangible assets related to the acquisition of EHG and interest expense of $ 35 . 4 million . These two items, combined, further impacted diluted EPS by $ 0 . 69 per share • Continuing to balance production with current demand as independent dealers look to optimize inventory levels to minimize financing costs and improve turns

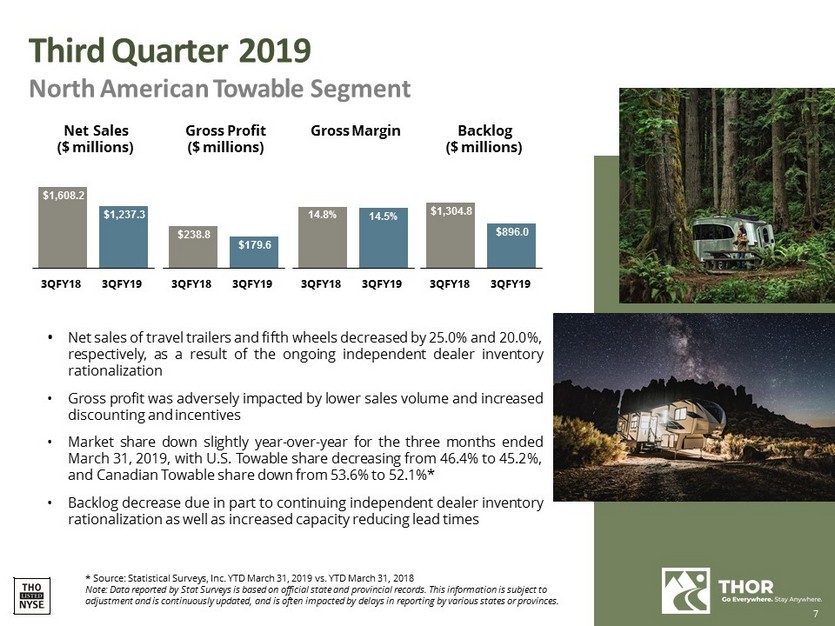

Third Quarter 2019 North American Towable Segment • Net sales of travel trailers and fifth wheels decreased by 25 . 0 % and 20 . 0 % , respectively, as a result of the ongoing independent dealer inventory rationalization • Gross profit was adversely impacted by lower sales volume and increased discounting and incentives • Market share down slightly year - over - year for the three months ended March 31 , 2019 , with U . S . Towable share decreasing from 46 . 4 % to 45 . 2 % , and Canadian Towable share down from 53 . 6 % to 52 . 1 % * • Backlog decrease due in part to continuing independent dealer inventory rationalization as well as increased capacity reducing lead times * Source: Statistical Surveys, Inc. YTD March 31, 2019 vs. YTD March 31, 2018 Note: Data reported by Stat Surveys is based on official state and provincial records. This information is subject to adjustment and is continuously updated, and is often impacted by delays in reporting by various states or provinces. Net Sales ($ millions) 3QFY18 3QFY19 $1,608.2 $1,237.3 3QFY18 3QFY19 14.8% 14.5% Gross Profit Gross Margin ($ millions) 3QFY18 3QFY19 $238.8 $179.6 Backlog ($ millions) 7 3QFY18 3QFY19 $1,304.8 $896.0

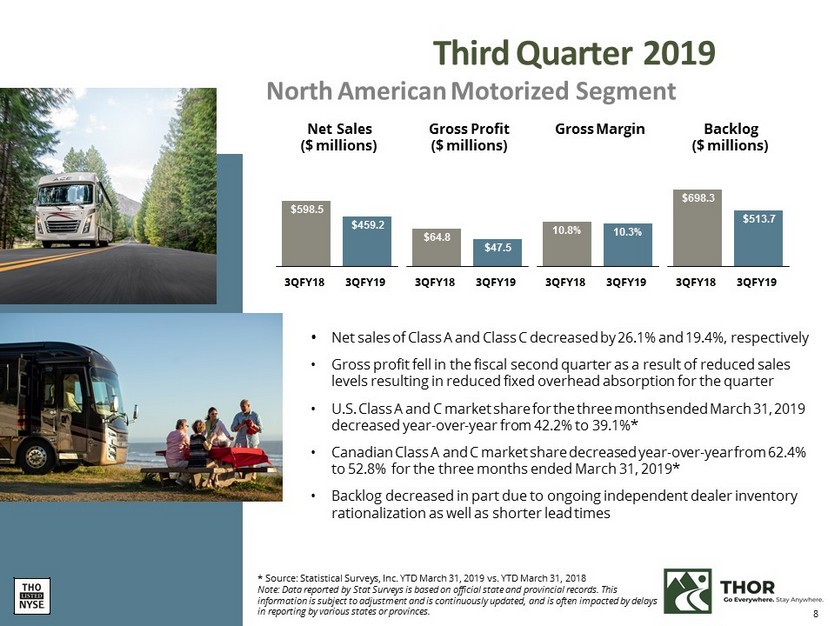

8 • Net sales of Class A and Class C decreased by 26.1% and 19.4%, respectively • Gross profit fell in the fiscal second quarter as a result of reduced sales levels resulting in reduced fixed overhead absorption for the quarter • U.S. Class A and C market share for the three months ended March 31, 2019 decreased year - over - year from 42.2% to 39.1%* • Canadian Class A and C market share decreased year - over - year from 62.4% to 52.8% for the three months ended March 31, 2019* • Backlog decreased in part due to ongoing independent dealer inventory rationalization as well as shorter lead times * Source: Statistical Surveys, Inc. YTD March 31, 2019 vs. YTD March 31, 2018 Note: Data reported by Stat Surveys is based on official state and provincial records. This information is subject to adjustment and is continuously updated, and is often impacted by delays in reporting by various states or provinces. Net Sales ($ millions) 3QFY18 3QFY19 $598.5 $459.2 3QFY19 10.8% 10.3% Gross Profit Gross Margin ($ millions) 3QFY18 3QFY19 3QFY18 $64.8 $47.5 Backlog ($ millions) 3QFY18 3QFY19 $698.3 $513.7 Third Quarter 2019 North American Motorized Segment

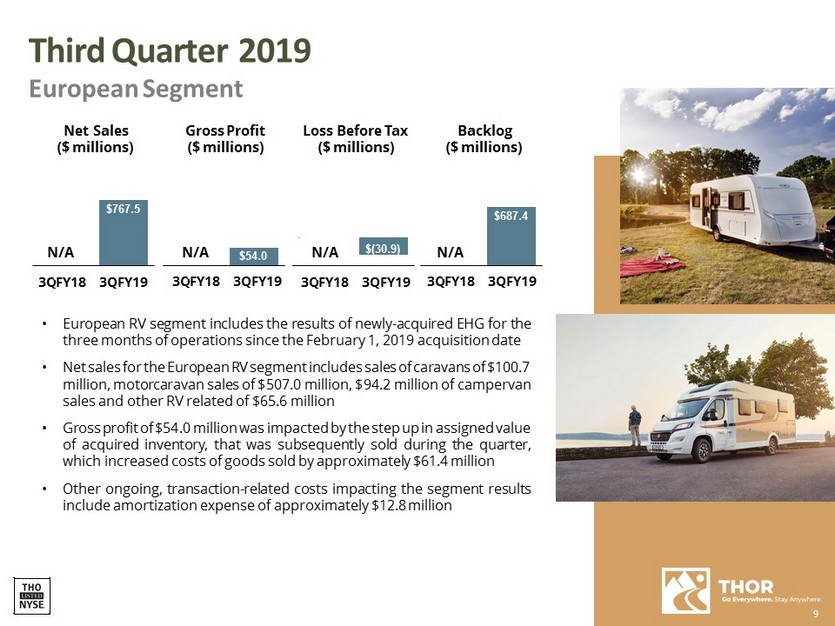

Third Quarter 2019 European Segment • European RV segment includes the results of newly - acquired EHG for the three months of operations since the February 1 , 2019 acquisition date • Net sales for the European RV segment includes sales of caravans of $ 100 . 7 million, motorcaravan sales of $ 507 . 0 million, $ 94 . 2 million of campervan sales and other RV related of $ 65 . 6 million • Gross profit of $ 54 . 0 million was impacted by the step up in assigned value of acquired inventory, that was subsequently sold during the quarter, which increased costs of goods sold by approximately $ 61 . 4 million • Other ongoing, transaction - related costs impacting the segment results include amortization expense of approximately $ 12 . 8 million Net Sales ($ millions) $767.5 Loss Before Tax ($ millions) $(30.9) Gross Profit ($ millions) $54.0 Backlog ($ millions) 9 3 Q $ F — Y18 3QFY19 $687.4 N/A N/A N/A N/A 3 Q $ F — Y18 3QFY19 3 Q $ F — Y18 3QFY19 3 Q $ F — Y18 3QFY19

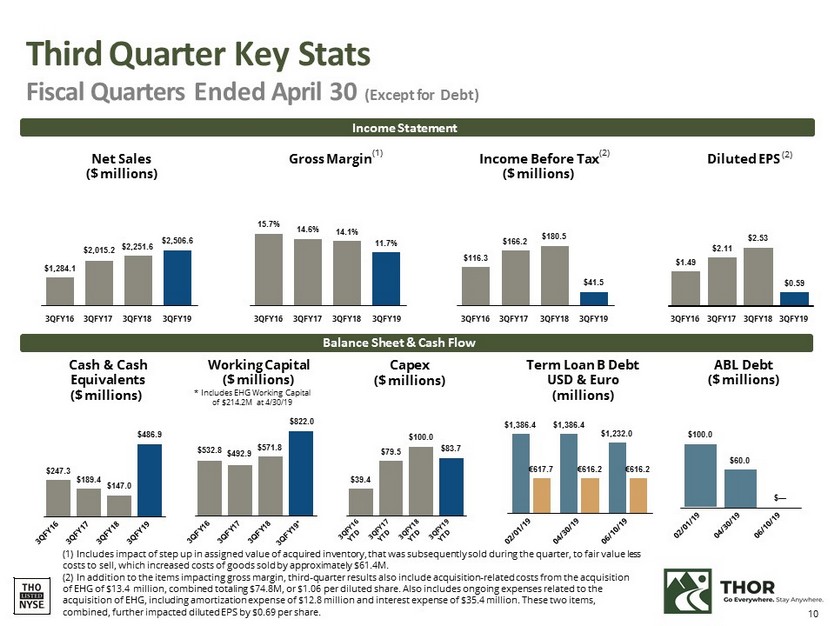

Third Quarter Key Stats Fiscal Quarters Ended April 30 (Except for Debt) Income Statement Net Sales ($ millions) 3QFY16 3QFY17 3QFY18 3QFY19 $1,284.1 $2,015.2 $2,251.6 $2,506.6 3QFY18 3QFY19 $ 11 6.3 $166.2 $180.5 $41.5 3QFY16 3QFY17 3QFY18 3QFY19 3QFY16 3QFY17 15.7% 14.6% 14.1% 11 .7% 3QFY16 3QFY17 3QFY18 3QFY19 $1.49 $2. 1 1 $2.53 $0.59 Cash & Cash Equivalents ( $ millions) $247.3 $189.4 $147.0 $486.9 Balance Sheet & Cash Flow Capex ($ millions) $39.4 $79.5 $100.0 $83.7 $532.8 $492.9 $571.8 (1) Includes impact of step up in assigned value of acquired inventory, that was subsequently sold during the quarter, to fair value less costs to sell, which increased costs of goods sold by approximately $61.4M. (2) In addition to the items impacting gross margin, third - quarter results also include acquisition - related costs from the acquisition of EHG of $13.4 million, combined totaling $74.8M, or $1.06 per diluted share. Also includes ongoing expenses related to the acquisition of EHG, including amortization expense of $12.8 million and interest expense of $35.4 million. These two items, combined, further impacted diluted EPS by $0.69 per share. Working Capital ($ millions) * Includes EHG Working Capital of $214.2M at 4/30/19 $822.0 Gross Margin (1) Income Before Tax (2) ($ millions) Diluted EPS (2) Term Loan B Debt USD & Euro (millions) $1,386.4 $1,386.4 $1,232.0 €617.7 €616.2 €616.2 ABL Debt ($ millions) 10 $100.0 $60.0 $ —

Overview & Current Industry Conditions 11

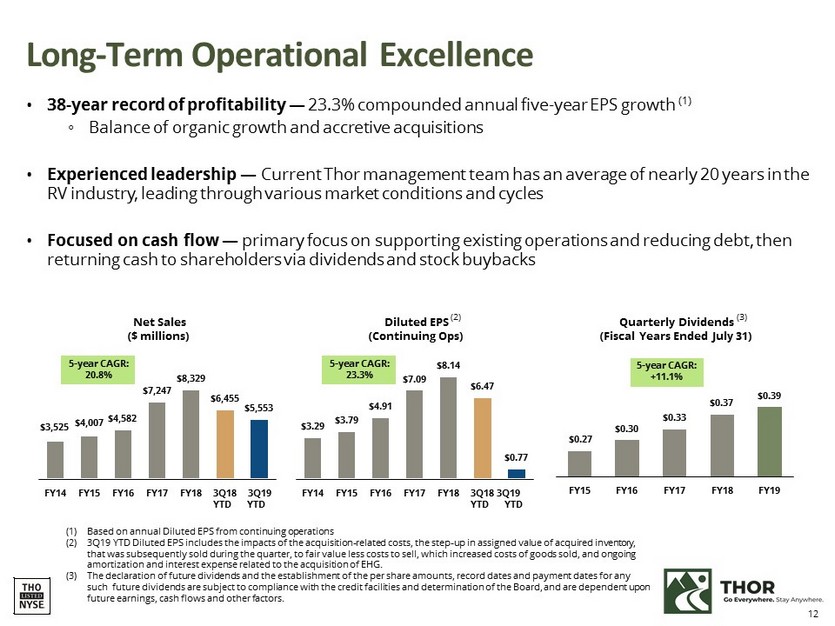

FY15 FY16 FY17 FY18 FY19 $0.30 $0.33 $0.37 $0.39 Long - Term Operational Excellence • 38 - year record of profitability — 23.3% compounded annual five - year EPS growth (1) ◦ Balance of organic growth and accretive acquisitions • Experienced leadership — Current Thor management team has an average of nearly 20 years in the RV industry, leading through various market conditions and cycles • Focused on cash flow — primary focus on supporting existing operations and reducing debt, then returning cash to shareholders via dividends and stock buybacks (1) Based on annual Diluted EPS from continuing operations (2) 3Q19 YTD Diluted EPS includes the impacts of the acquisition - related costs, the step - up in assigned value of acquired inventory, that was subsequently sold during the quarter, to fair value less costs to sell, which increased costs of goods sold, and ongoing amortization and interest expense related to the acquisition of EHG. (3) The declaration of future dividends and the establishment of the per share amounts, record dates and payment dates for any such future dividends are subject to compliance with the credit facilities and determination of the Board, and are dependent upon future earnings, cash flows and other factors. Net Sales ($ millions) FY14 FY15 FY16 $3,525 $4,007 $4,582 $7,247 $8,329 $6,455 $5,553 FY17 FY18 3Q18 3Q19 FY14 FY15 FY16 FY17 FY18 YTD YTD 12 3Q18 3Q19 YTD YTD $3.29 $3.79 $4.91 $7.09 $8.14 $6.47 $0.27 $0.77 5 - year CAGR: 20.8% 5 - year CAGR: 23.3% 5 - year CAGR: +11.1% Diluted EPS (2) (Continuing Ops) Quarterly Dividends (3) (Fiscal Years Ended July 31)

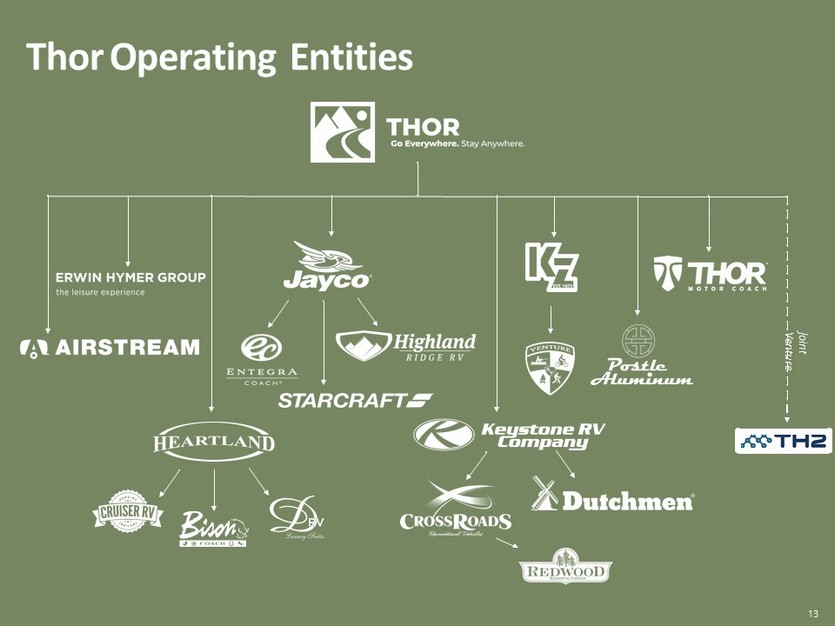

Thor Operating Entities Joint V entu r e 13

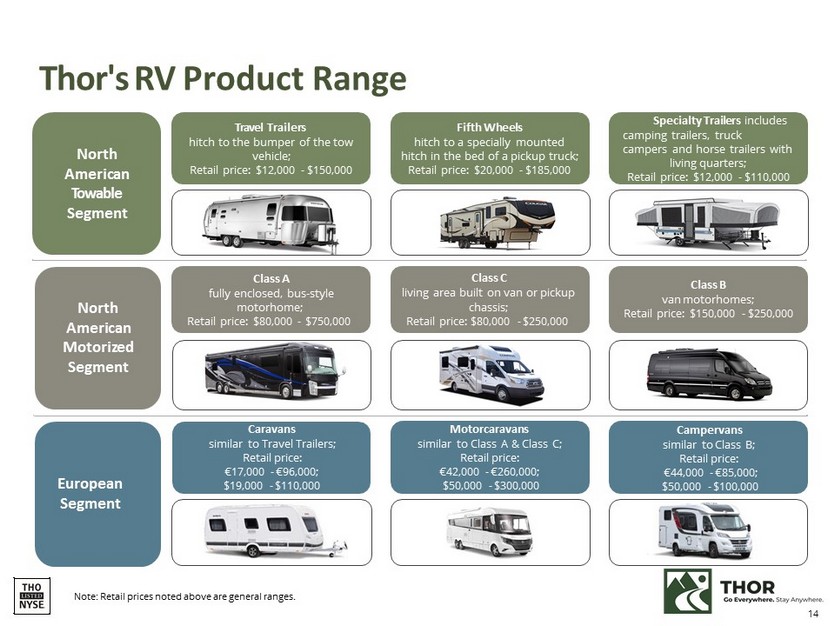

Thor's RV Product Range North Ameri c an Towable Segment North American Mo t ori z ed Segment Note: Retail prices noted above are general ranges. Class A fully enclosed, bus - style Retail price: $80,000 - motorhome; $750,000 Class C living area built on van or pickup Retail price: $80,000 chassis; - $250,000 Class B van motorhomes; Retail price: $150,000 - $250,000 Specialty Trailers includes camping trailers, truck campers and horse trailers with living quarters; Retail price: $12,000 - $110,000 Travel Trailers hitch to the bumper of the tow vehicle; Retail price: $12,000 - $150,000 Fifth Wheels hitch to a specially mounted hitch in the bed of a pickup truck; Retail price: $20,000 - $185,000 European Segment Caravans similar to Travel Trailers; Retail price: €17,000 - €96,000; $19,000 - $110,000 Motorcaravans similar to Class A & Class C; Retail price: €42,000 - €260,000; $50,000 - $300,000 Campervans similar to Class B; Retail price: €44,000 - €85,000; $50,000 - $100,000 14

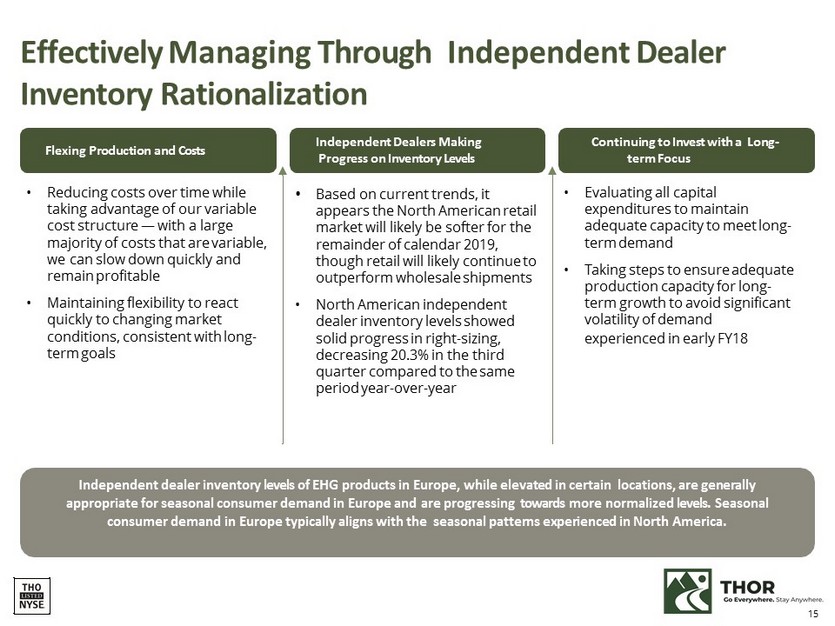

Effectively Managing Through Independent Dealer Inventory Rationalization Flexing Production and Costs Independent Dealers Making Progress on Inventory Levels Continuing to Invest with a Long - term Focus • Based on current trends, it appears the North American retail market will likely be softer for the remainder of calendar 2019, though retail will likely continue to outperform wholesale shipments • North American independent dealer inventory levels showed solid progress in right - sizing, decreasing 20.3% in the third quarter compared to the same period year - over - year • Evaluating all capital expenditures to maintain adequate capacity to meet long - term demand • Taking steps to ensure adequate production capacity for long - term growth to avoid significant volatility of demand experienced in early FY18 • Reducing costs over time while taking advantage of our variable cost structure — with a large majority of costs that are variable, we can slow down quickly and remain profitable • Maintaining flexibility to react quickly to changing market conditions, consistent with long - term goals Independent dealer inventory levels of EHG products in Europe, while elevated in certain locations, are generally appropriate for seasonal consumer demand in Europe and are progressing towards more normalized levels. Seasonal consumer demand in Europe typically aligns with the seasonal patterns experienced in North America. 15

Healthy North American RV Channel 16 Independent Dealer Inventory Approaching Normalized Levels: • Following inventory shortages in FY 17 , independent dealers ordered aggressively in early FY 18 • Although retail demand grew modestly in calendar 2018 , that growth was not sufficient to bring independent dealer inventory levels down • Thor responded by reducing production levels to meet current demand • Average age of RV inventory on independent dealer lots remains healthy • Used inventory levels generally remain low, supporting trade - in values and demand for new RVs Wholesale Financing Prompting Better Inventory Management: • Credit broadly available • Normal seasonal credit line utilization • Lenders remain disciplined with curtailments, which combined with modestly higher interest rates is motivating independent dealers to focus on turning inventory Retail Financing is Supportive of Growth: • Credit broadly available • Lenders remain disciplined on down payments and terms • Minimal sub - prime exposure ; RV loan delinquency rates among the lowest of consumer loans tracked by the American Bankers Association, most recently at 0 . 77 % in the fourth quarter of 2018 1 (1) Source: American Bankers Association ABA Report, April 2019

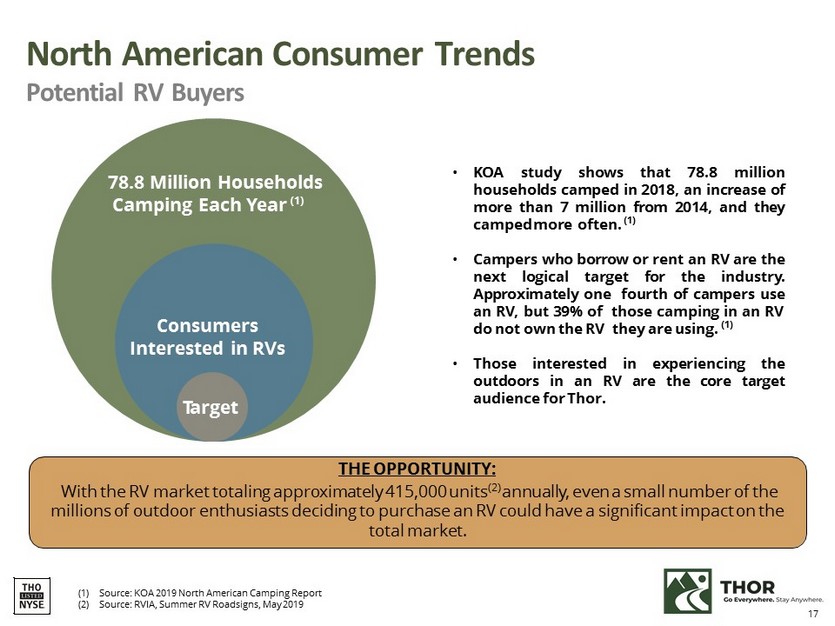

North

American Consumer Trends Potential RV Buyers 7 8.8 Million Households Camping Each Year (1) Consumers Interested in RVs T a r

get ? KOA study shows that 78 . 8 million households camped in 2018 , an increase of more than 7 million from 2014 , and they

camped more often . ( 1 ) ? Campers who borrow or rent an RV are the next logical target for the industry . Approximately o ne

fourth of campers use an RV, but 39 % of those camping in an RV do not own the RV they are using . ( 1 ) ? Those interested in

experiencing the outdoors in an RV are the core target audience for Thor . (1) Source: KOA 2019 North American Camping Report

(2) Source: RVIA, Summer RV Roadsigns, May 2019 THE OPPORTUNITY: With the RV market totaling approximately 415,000 units (2) annually,

even a small number of the millions of outdoor enthusiasts deciding to purchase an RV could have a significant impact on the total

market. 17

Younger, More Diverse Consumers The Future of the RV Market 18 • Millennials represented 41 % of active campers in 2018 , but made up 56 % of new campers, illustrating the continued growth of this group • Among millennials, 32 % consider themselves "lifelong campers," while 38 % of Gen X identify themselves as such • Among Gen Z, 96 % enjoy time camping with family and friends, and 8 9 % want to camp as adults . • For the first time in 2018 , non - white households represented the majority of new campers at 51 % , with significant growth among Hispanic campers • Interest among campers in alternative experiences, such as "glamping" and "van life," have more than doubled in 2018 , with 45 % of campers interested in "glamping" and 14 % interested in full - time RVing, or living the "van life" Source: KOA 2019 North American Camping Report

Appendix: Financial & Market Data 19

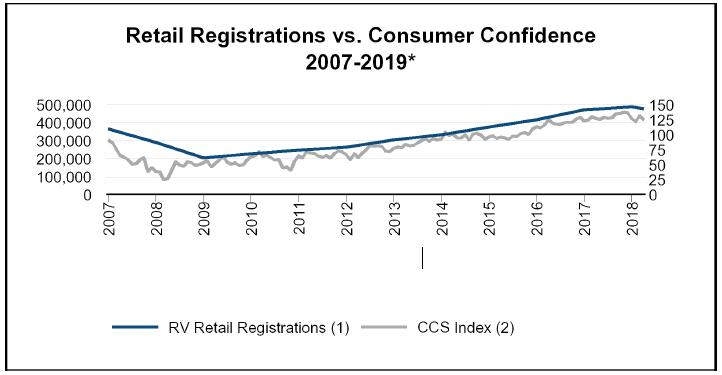

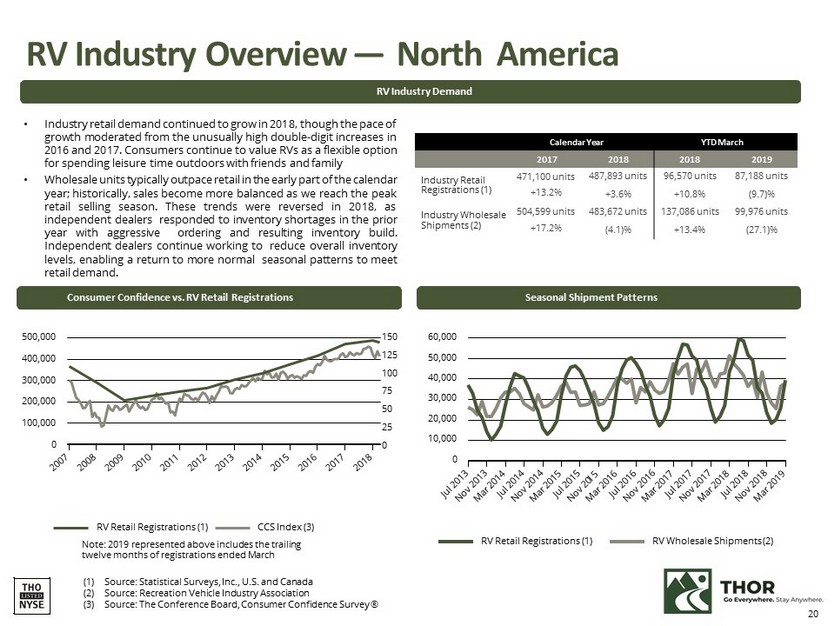

RV Industry Overview — North America Seasonal Shipment Patterns RV Retail Registrations (1) RV Wholesale Shipments (2) 60,000 50,000 40,000 30,000 20,000 10,000 0 RV Industry Demand • Industry retail demand continued to grow in 2018 , though the pace of growth moderated from the unusually high double - digit increases in 2016 and 2017 . Consumers continue to value RVs as a flexible option for spending leisure time outdoors with friends and family • Wholesale units typically outpace retail in the early part of the calendar year ; historically, sales become more balanced as we reach the peak retail selling season . These trends were reversed in 2018 , as independent dealers responded to inventory shortages in the prior year with aggressive ordering and resulting inventory build . Independent d ealers continue working to reduce overall inventory levels, enabling a return to more normal seasonal patterns to meet retail demand . Calendar Year YTD March 2017 2018 2018 2019 Industry Retail 471,100 units 487,893 units 96,570 units 87,188 units Registrations (1) +13.2% +3.6% +10.8% (9.7)% Industry Wholesale 504,599 units 483,672 units 137,086 units 99,976 units Shipments (2) +17.2% (4.1)% +13.4% (27.1)% Consumer Confidence vs. RV Retail Registrations 500,000 400,000 300,000 200,000 100,000 0 20 150 125 100 75 50 25 0 (1) Source: Statistical Surveys, Inc., U.S. and Canada (2) Source: Recreation Vehicle Industry Association (3) Source: The Conference Board, Consumer Confidence Survey ® RV Retail Registrations (1) CCS Index (3) Note: 2019 represented above includes the trailing twelve months of registrations ended March

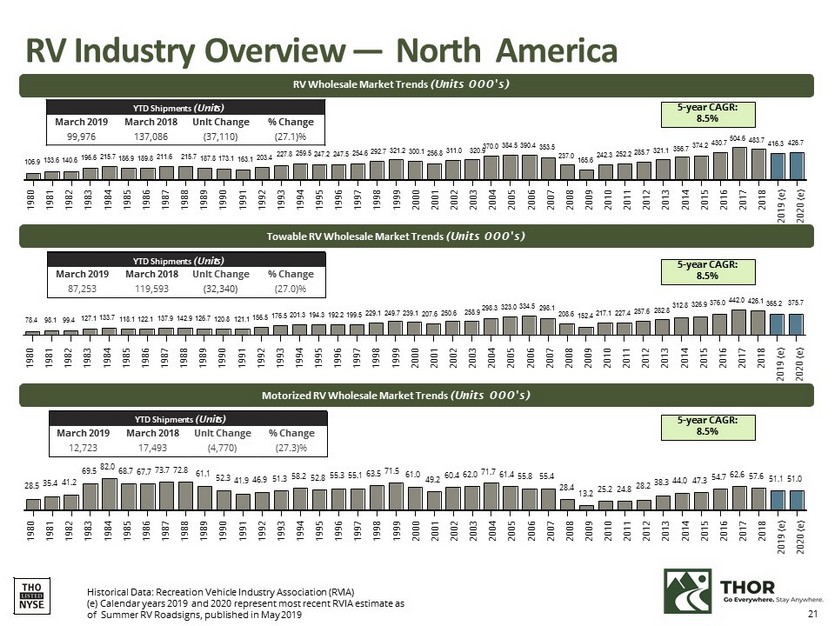

21 RV Industry Overview — North America RV Wholesale Market Trends (Units 000's) 1980 1981 1982 1983 1984 1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 (e) 2020 (e) 106.9 133.6 140.6 196.6 215.7 186.9 189.8 211.6 215.7 187.8 173.1 163.1 203.4 227.8 259.5 247.2 247.5 254.6 292.7 321.2 300.1 256.8 311.0 320.9 370.0 384.5 390.4 353.5 237.0 165.6 242.3 252.2 285.7 321.1 356.7 374.2 430.7 504.6 483.7 416.3 426.7 Towable RV Wholesale Market Trends (Units 000's) YTD Shipments (Units) March 2019 99,976 March 2018 137,086 Unit Change (37,110) % Change (27.1)% 1980 1981 1982 1983 1984 1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 (e) 2020 (e) 78.4 98.1 99.4 127.1 133.7 118.1 122.1 137.9 142.9 126.7 120.8 121.1 156.5 176.5 201.3 194.3 192.2 199.5 229.1 249.7 239.1 207.6 250.6 258.9 298.3 323.0 334.5 298.1 208.6 152.4 217.1 227.4 257.6 282.8 312.8 326.9 376.0 442.0 426.1 365.2 375.7 YTD Shipments (Units) March 2019 87,253 March 2018 119,593 Unit Change (32,340) % Change (27.0)% Motorized RV Wholesale Market Trends (Units 000's) 1980 1981 1982 1983 1984 1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 (e) 2020 (e) 28.5 35.4 41.2 69.5 82.0 68.7 67.7 73.7 72.8 61.1 52.3 41.9 46.9 51.3 58.2 52.8 55.3 55.1 63.5 71.5 61.0 49.2 60.4 62.0 71.7 61.4 55.8 55.4 28.4 13.2 25.2 24.8 28.2 38.3 44.0 47.3 54.7 62.6 57.6 51.1 51.0 YTD Shipments (Units) March 2019 12,723 March 2018 17,493 Unit Change (4,770) % Change (27.3)% Historical Data: Recreation Vehicle Industry Association (RVIA) (e) Calendar years 2019 and 2020 represent most recent RVIA estimate as of Summer RV Roadsigns, published in May 2019 5 - year CAGR: 8.5% 5 - year CAGR: 8.5% 5 - year CAGR: 8.5%

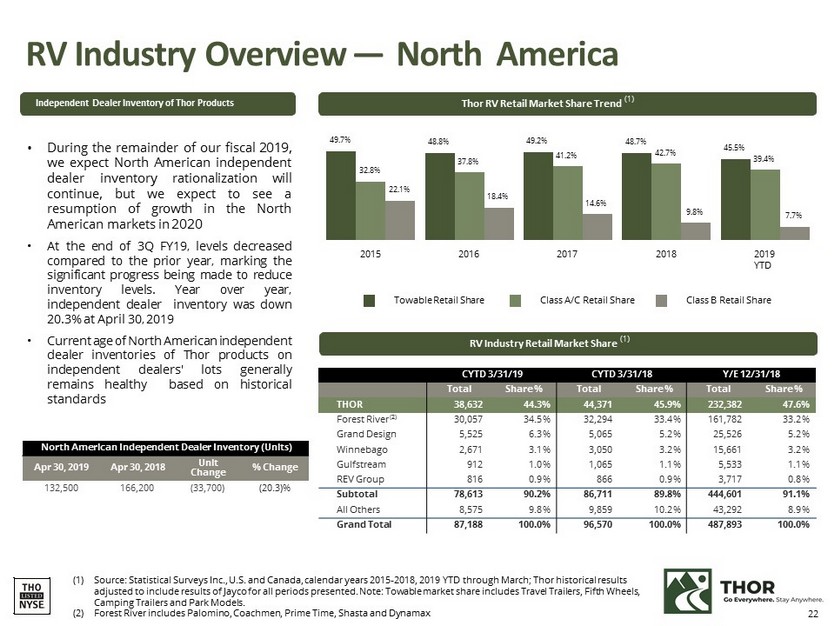

22 RV Industry Overview — North America Thor RV Retail Market Share Trend (1) Independent Dealer Inventory of Thor Products RV Industry Retail Market Share (1) (1) Source: Statistical Surveys Inc., U.S. and Canada, calendar years 2015 - 2018, 2019 YTD through March; Thor historical results adjusted to include results of Jayco for all periods presented. Note: Towable market share includes Travel Trailers, Fifth Wheels, Camping Trailers and Park Models. (2) Forest River includes Palomino, Coachmen, Prime Time, Shasta and Dynamax Towable Retail Share Class A/C Retail Share Class B Retail Share 2015 2016 2017 2018 2019 YTD 49.7% 48.8% 49.2% 48.7% 45.5% 32.8% 37.8% 41.2% 42.7% 39.4% 22.1% 18.4% 14.6% 9.8% 7.7% • During the remainder of our fiscal 2019 , we expect North American independent dealer inventory rationalization will continue, but we expect to see a resumption of growth in the North American markets in 2020 • At the end of 3 Q FY 19 , levels decreased compared to the prior year, marking the significant progress being made to reduce inventory levels . Year over year , independent dealer inventory was down 20 . 3 % at April 30 , 2019 • Current age of North American independent dealer inventories of Thor products on independent dealers' lots generally remains healthy based on historical standards 132,500 166,200 (33,700) (20.3)% North American Independent Dealer Inventory (Units) Apr 30, 2019 Apr 30, 2018 Unit Change % Change CYTD 3/31/19 CYTD 3/31/18 Y/E 12/31/18 Total Share % Total Share % Total Share % THOR 38,632 44.3% 44,371 45.9% 232,382 47.6% Forest River (2) 30,057 34. 5 % 32,294 33. 4 % 161,782 33. 2 % Grand Design 5,525 6. 3 % 5,065 5. 2 % 25,526 5. 2 % Winnebago 2,671 3. 1 % 3,050 3. 2 % 15,661 3. 2 % Gulfstream 912 1. 0 % 1,065 1. 1 % 5,533 1. 1 % REV Group 816 0. 9 % 866 0. 9 % 3,717 0. 8 % Subtotal 78,613 90.2% 86,711 89.8% 444,601 91.1% All Others 8,575 9. 8 % 9,859 10. 2 % 43,292 8. 9 % Grand Total 87,188 100.0% 96,570 100.0% 487,893 100.0%

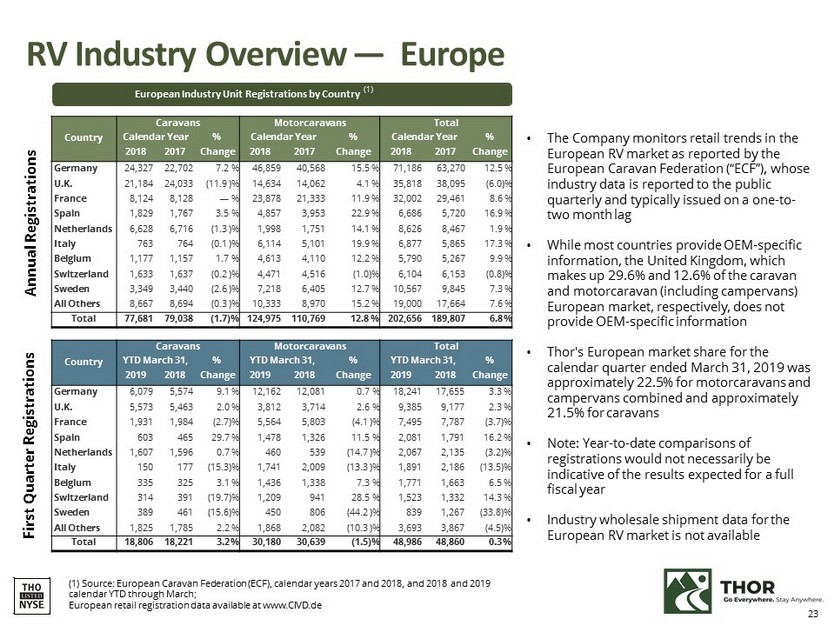

RV Industry Overview — Europe Country Caravans YTD March 31, % 2019 2018 Change Motorcaravans YTD March 31, % 2019 2018 Change Total YTD March 31, % 2019 2018 Change Germany 6,079 5,574 9.1 % 12,162 12,081 0.7 % 18,241 17,655 3.3 % U.K. 5,573 5,463 2.0 % 3,812 3,714 2.6 % 9,385 9,177 2.3 % France 1,931 1,984 (2.7)% 5,564 5,803 (4.1 )% 7,495 7,787 (3.7)% Spain 603 465 29.7 % 1,478 1,326 11.5 % 2,081 1,791 16.2 % Netherlands 1,607 1,596 0.7 % 460 539 (14.7 )% 2,067 2,135 (3.2)% Italy 150 177 (15.3)% 1,741 2,009 (13.3 )% 1,891 2,186 (13.5)% Belgium 335 325 3.1 % 1,436 1,338 7.3 % 1,771 1,663 6.5 % Switzerland 314 391 (19.7)% 1,209 941 28.5 % 1,523 1,332 14.3 % Sweden 389 461 (15.6)% 450 806 (44.2 )% 839 1,267 (33.8)% All Others 1,825 1,785 2.2 % 1,868 2,082 (10.3 )% 3,693 3,867 (4.5)% Total 18,806 18,221 3.2 % 30,180 30,639 (1.5)% 48,986 48,860 0.3 % Country Caravans Calendar Year % 2018 2017 Change Motorcaravans Calendar Year % 2018 2017 Change Total Calendar Year % 2018 2017 Change Germany 24,327 22,702 7.2 % 46,859 40,568 15.5 % 71,186 63,270 12.5 % U.K. 21,184 24,033 (11.9 )% 14,634 14,062 4.1 % 35,818 38,095 (6.0)% France 8,124 8,128 — % 23,878 21,333 11.9 % 32,002 29,461 8.6 % Spain 1,829 1,767 3.5 % 4,857 3,953 22.9 % 6,686 5,720 16.9 % Netherlands 6,628 6,716 (1.3 )% 1,998 1,751 14.1 % 8,626 8,467 1.9 % Italy 763 764 (0.1 )% 6,114 5,101 19.9 % 6,877 5,865 17.3 % Belgium 1,177 1,157 1.7 % 4,613 4,110 12.2 % 5,790 5,267 9.9 % Switzerland 1,633 1,637 (0.2 )% 4,471 4,516 (1.0)% 6,104 6,153 (0.8)% Sweden 3,349 3,440 (2.6 )% 7,218 6,405 12.7 % 10,567 9,845 7.3 % All Others 8,667 8,694 (0.3 )% 10,333 8,970 15.2 % 19,000 17,664 7.6 % Total 77,681 79,038 (1.7)% 124,975 110,769 12.8 % 202,656 189,807 6.8 % Annual Regist r ations 23 European Industry Unit Registrations by Country (1) • The Company monitors retail trends in the European RV market as reported by the European Caravan Federation (“ECF”), whose industry data is reported to the public quarterly and typically issued on a one - to - two month lag • While most countries provide OEM - specific information, the United Kingdom, which makes up 29.6% and 12.6% of the caravan and motorcaravan (including campervans) European market, respectively, does not provide OEM - specific information • Thor's European market share for the calendar quarter ended March 31, 2019 was approximately 22.5% for motorcaravans and campervans combined and approximately 21.5% for caravans • Note: Year - to - date comparisons of registrations would not necessarily be indicative of the results expected for a full fiscal year • Industry wholesale shipment data for the European RV market is not available (1) Source: European Caravan Federation (ECF), calendar years 2017 and 2018, and 2018 and 2019 calendar YTD through March ; European retail registration data available at www.CIVD.de First Quarter Regist r ations

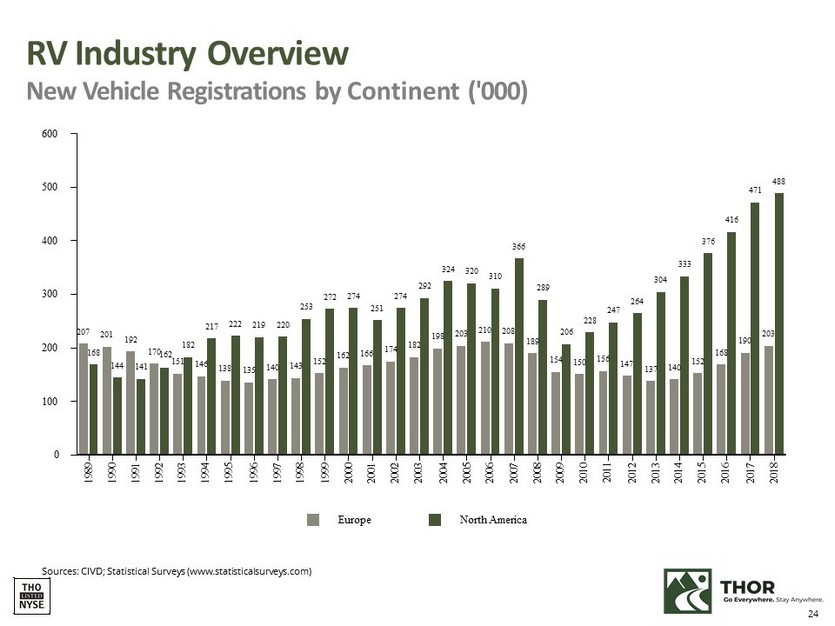

Sources: CIVD; Statistical Surveys (www.statisticalsurveys.com) RV Industry Overview New Vehicle Registrations by Continent ('000) Europe North America 600 24 500 400 300 200 100 0 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 20 1 1 2012 2013 2014 2015 2016 2017 2018 207 201 192 151 146 138 135 140 143 152 162 166 174 182 198 203 210 208 189 154 150 156 147 137 140 152 168 190 203 168 144 141 17 0 162 182 217 222 219 220 253 272 274 251 274 292 324 320 310 366 289 206 228 247 264 304 333 376 416 471 488

www.thorindustries.com