UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-Q

[X] QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the quarterly period ended March 31, 2011

OR

[ ] TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the Transition period from _______ to _______

Commission File No. 1-15973

NORTHWEST NATURAL GAS COMPANY

(Exact name of registrant as specified in its charter)

|

Oregon

|

93-0256722

|

|

(State or other jurisdiction of

incorporation or organization)

|

(I.R.S. Employer

Identification No.)

|

220 N.W. Second Avenue, Portland, Oregon 97209

(Address of principal executive offices) (Zip Code)

Registrant’s telephone number, including area code: (503) 226-4211

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes [ X ] No [ ]

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes [ X ] No [ ]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See the definitions of "large accelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act. (Check one):

|

Large accelerated filer [ X ]

|

Accelerated filer [ ]

|

|

Non-accelerated filer [ ]

|

Smaller reporting company [ ]

|

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Yes [ ] No [ X ]

At April 30, 2011, 26,672,812 shares of the registrant’s Common Stock (the only class of Common Stock) were outstanding.

NORTHWEST NATURAL GAS COMPANY

For the Quarterly Period Ended March 31, 2011

|

PART I. FINANCIAL INFORMATION

|

||

|

Page Number

|

||

|

1

|

||

|

2

|

||

|

3

|

||

|

5

|

||

|

6

|

||

|

20

|

||

|

38

|

||

|

39

|

||

|

PART II. OTHER INFORMATION

|

||

|

40

|

||

|

40

|

||

|

40

|

||

|

40

|

||

|

41

|

Forward-Looking Statements

This report contains “forward-looking statements” within the meaning of the U.S. Private Securities Litigation Reform Act of 1995. Forward-looking statements can be identified by words such as “anticipates,” “intends,” “plans,” “seeks,” “believes,” “estimates,” “expects” and similar references to future periods. Examples of forward-looking statements include, but are not limited to statements regarding the following:

|

·

|

plans;

|

|

·

|

objectives;

|

|

·

|

goals;

|

|

·

|

strategies;

|

|

·

|

future events or performance;

|

|

·

|

trends;

|

|

·

|

cyclicality;

|

|

·

|

earnings and dividends;

|

|

·

|

growth;

|

|

·

|

customer rates;

|

|

·

|

commodity costs;

|

|

·

|

operational performance and costs;

|

|

·

|

liquidity and financial positions;

|

|

·

|

project development and expansion;

|

|

·

|

competition;

|

|

·

|

procurement and development of new gas supplies;

|

|

·

|

liquefied natural gas;

|

|

·

|

estimated expenditures;

|

|

·

|

costs of compliance;

|

|

·

|

credit exposures;

|

|

·

|

potential efficiencies;

|

|

·

|

impacts of laws, rules and regulations;

|

|

·

|

tax liabilities or refunds;

|

|

·

|

outcomes and effects of litigation, regulatory actions, and other administrative matters;

|

|

·

|

projected obligations under retirement plans;

|

|

·

|

adequacy of, and shift in mix of, gas supplies;

|

|

·

|

approval and adequacy of regulatory deferrals; and

|

|

·

|

environmental, regulatory, litigation and insurance costs and recoveries.

|

Forward-looking statements are based on our current expectations and assumptions regarding our business, the economy and other future conditions. Because forward-looking statements relate to the future, they are subject to inherent uncertainties, risks, and changes in circumstances that are difficult to predict. Our actual results may differ materially from those contemplated by the forward-looking statements. We therefore caution you against relying on any of these forward-looking statements. They are neither statements of historical fact nor guarantees or assurances of future performance. Important factors that could cause actual results to differ materially from those in the forward-looking statements are discussed in our 2010 Annual Report on Form 10-K, Part I, Item 1A. “Risk Factors” and Part II, Item 7. and Item 7A., “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and “Quantitative and Qualitative Disclosures about Market Risk,” and in Part I, Items 2 and 3, “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and Quantitative and Qualitative Disclosures About Market Risk,” and Part II, Item 1A “Risk Factors,” herein.

Any forward-looking statement made by us in this report speaks only as of the date on which it is made. Factors or events that could cause our actual results to differ may emerge from time to time, and it is not possible for us to predict all of them. We undertake no obligation to publicly update any forward-looking statement, whether as a result of new information, future developments or otherwise, except as may be required by law.

1

NORTHWEST NATURAL GAS COMPANY

PART I. FINANCIAL INFORMATION

|

Consolidated Statements of Income

|

||||||||

|

(Unaudited)

|

||||||||

|

Three Months Ended

|

||||||||

|

March 31,

|

||||||||

|

Thousands, except per share amounts

|

2011

|

2010

|

||||||

|

Operating revenues:

|

||||||||

|

Gross operating revenues

|

$ | 323,088 | $ | 286,529 | ||||

|

Less: Cost of sales

|

180,625 | 148,561 | ||||||

|

Revenue taxes

|

7,955 | 7,042 | ||||||

|

Net operating revenues

|

134,508 | 130,926 | ||||||

|

Operating expenses:

|

||||||||

|

Operations and maintenance

|

31,172 | 30,666 | ||||||

|

General taxes

|

8,165 | 3,249 | ||||||

|

Depreciation and amortization

|

17,309 | 15,901 | ||||||

|

Total operating expenses

|

56,646 | 49,816 | ||||||

|

Income from operations

|

77,862 | 81,110 | ||||||

|

Other income and expense - net

|

1,214 | 3,023 | ||||||

|

Interest expense - net

|

10,449 | 10,489 | ||||||

|

Income before income taxes

|

68,627 | 73,644 | ||||||

|

Income tax expense

|

27,854 | 30,036 | ||||||

|

Net income

|

$ | 40,773 | $ | 43,608 | ||||

|

Average common shares outstanding:

|

||||||||

|

Basic

|

26,670 | 26,538 | ||||||

|

Diluted

|

26,724 | 26,601 | ||||||

|

Earnings per share of common stock:

|

||||||||

|

Basic

|

$ | 1.53 | $ | 1.64 | ||||

|

Diluted

|

$ | 1.53 | $ | 1.64 | ||||

|

Dividends declared per share of common stock

|

$ | 0.435 | $ | 0.415 | ||||

|

See Notes to Consolidated Financial Statements.

|

||||||||

2

NORTHWEST NATURAL GAS COMPANY

PART I. FINANCIAL INFORMATION

|

Consolidated Balance Sheets

|

||||||||||||

|

(Unaudited)

|

||||||||||||

|

March 31,

|

March 31,

|

December 31,

|

||||||||||

|

Thousands

|

2011

|

2010

|

2010

|

|||||||||

|

Assets:

|

||||||||||||

|

Current assets:

|

||||||||||||

|

Cash and cash equivalents

|

$ | 3,480 | $ | 8,839 | $ | 3,457 | ||||||

|

Restricted cash

|

924 | 40,924 | 924 | |||||||||

|

Accounts receivable

|

94,521 | 78,347 | 67,969 | |||||||||

|

Accrued unbilled revenue

|

42,342 | 39,244 | 64,803 | |||||||||

|

Allowance for uncollectible accounts

|

(3,821 | ) | (3,999 | ) | (2,950 | ) | ||||||

|

Regulatory assets

|

48,195 | 55,872 | 52,714 | |||||||||

|

Derivative instruments

|

4,861 | 450 | 2,245 | |||||||||

|

Inventories:

|

||||||||||||

|

Gas

|

43,501 | 61,918 | 70,672 | |||||||||

|

Materials and supplies

|

9,765 | 9,235 | 9,713 | |||||||||

|

Income taxes receivable

|

23,645 | - | 41,066 | |||||||||

|

Other current assets

|

13,292 | 15,481 | 19,652 | |||||||||

|

Total current assets

|

280,705 | 306,311 | 330,265 | |||||||||

|

Non-current assets:

|

||||||||||||

|

Property, plant and equipment

|

2,593,553 | 2,409,534 | 2,576,402 | |||||||||

|

Less: Accumulated depreciation

|

733,639 | 702,307 | 722,239 | |||||||||

|

Total property, plant and equipment - net

|

1,859,914 | 1,707,227 | 1,854,163 | |||||||||

|

Regulatory assets

|

345,452 | 331,962 | 348,897 | |||||||||

|

Derivative instruments

|

1,560 | 5 | 628 | |||||||||

|

Other investments

|

69,501 | 67,558 | 69,094 | |||||||||

|

Other non-current assets

|

14,421 | 15,970 | 13,569 | |||||||||

|

Total non-current assets

|

2,290,848 | 2,122,722 | 2,286,351 | |||||||||

|

Total assets

|

$ | 2,571,553 | $ | 2,429,033 | $ | 2,616,616 | ||||||

|

See Notes to Consolidated Financial Statements.

|

||||||||||||

3

NORTHWEST NATURAL GAS COMPANY

PART I. FINANCIAL INFORMATION

|

Consolidated Balance Sheets

|

||||||||||||

|

(Unaudited)

|

||||||||||||

|

March 31,

|

March 31,

|

December 31,

|

||||||||||

|

Thousands

|

2011

|

2010

|

2010

|

|||||||||

|

Capitalization and liabilities:

|

||||||||||||

|

Capitalization:

|

||||||||||||

|

Common stock - no par value; authorized 100,000 shares; issued and outstanding 26,673, 26,564 and 26,668 at March 31, 2011 and 2010, and December 31, 2010, respectively

|

$ | 343,787 | $ | 338,012 | $ | 342,978 | ||||||

|

Retained earnings

|

385,899 | 361,310 | 356,727 | |||||||||

|

Accumulated other comprehensive income (loss)

|

(6,458 | ) | (5,870 | ) | (6,604 | ) | ||||||

|

Total common stock equity

|

723,228 | 693,452 | 693,101 | |||||||||

|

Long-term debt

|

551,700 | 601,700 | 591,700 | |||||||||

|

Total capitalization

|

1,274,928 | 1,295,152 | 1,284,801 | |||||||||

|

Current liabilities:

|

||||||||||||

|

Short-term debt

|

186,435 | 96,000 | 257,435 | |||||||||

|

Current maturities of long-term debt

|

50,000 | 35,000 | 10,000 | |||||||||

|

Accounts payable

|

71,839 | 93,534 | 93,243 | |||||||||

|

Taxes accrued

|

10,063 | 27,325 | 10,579 | |||||||||

|

Interest accrued

|

11,470 | 12,232 | 5,182 | |||||||||

|

Regulatory liabilities

|

29,016 | 36,032 | 17,828 | |||||||||

|

Derivative instruments

|

25,655 | 39,365 | 38,437 | |||||||||

|

Other current liabilities

|

38,433 | 36,060 | 35,457 | |||||||||

|

Total current liabilities

|

422,911 | 375,548 | 468,161 | |||||||||

|

Deferred credits and other non-current liabilities:

|

||||||||||||

|

Deferred tax liabilities

|

396,357 | 311,691 | 373,409 | |||||||||

|

Regulatory liabilities

|

263,876 | 247,517 | 258,031 | |||||||||

|

Pension and other postretirement benefit liabilities

|

132,053 | 118,848 | 144,250 | |||||||||

|

Derivative instruments

|

13,914 | 18,637 | 17,022 | |||||||||

|

Other non-current liabilities

|

67,514 | 61,640 | 70,942 | |||||||||

|

Total deferred credits and other non-current liabilities

|

873,714 | 758,333 | 863,654 | |||||||||

|

Commitments and contingencies (see Note 14)

|

- | - | - | |||||||||

|

Total capitalization and liabilities

|

$ | 2,571,553 | $ | 2,429,033 | $ | 2,616,616 | ||||||

|

See Notes to Consolidated Financial Statements.

|

||||||||||||

4

NORTHWEST NATURAL GAS COMPANY

PART I. FINANCIAL INFORMATION

|

Consolidated Statement of Cash Flows

|

||||||||

|

(Unaudited)

|

||||||||

|

Three Months Ended

|

||||||||

|

March 31,

|

||||||||

|

Thousands

|

2011

|

2010

|

||||||

|

Operating activities:

|

||||||||

|

Net income

|

$ | 40,773 | $ | 43,608 | ||||

|

Adjustments to reconcile net income to cash provided by operations:

|

||||||||

|

Depreciation and amortization

|

17,309 | 15,901 | ||||||

|

Undistributed earnings from equity investments

|

25 | (356 | ) | |||||

|

Non-cash expenses related to qualified defined benefit pension plans

|

1,817 | 2,001 | ||||||

|

Contributions to qualified defined benefit pension plans

|

(13,645 | ) | (10,000 | ) | ||||

|

Deferred environmental expenditures

|

(1,759 | ) | (3,632 | ) | ||||

|

Other

|

(443 | ) | (2,431 | ) | ||||

|

Changes in assets and liabilities:

|

||||||||

|

Receivables

|

(3,122 | ) | 31,951 | |||||

|

Inventories

|

27,119 | 9,804 | ||||||

|

Taxes accrued

|

16,905 | 6,288 | ||||||

|

Accounts payable

|

(14,406 | ) | (24,882 | ) | ||||

|

Interest accrued

|

6,288 | 6,797 | ||||||

|

Deferred gas costs

|

196 | (15,428 | ) | |||||

|

Deferred tax liabilities

|

25,048 | 11,517 | ||||||

|

Other - net

|

5,959 | 3,018 | ||||||

|

Cash provided by operating activities

|

108,064 | 74,156 | ||||||

|

Investing activities:

|

||||||||

|

Capital expenditures

|

(25,403 | ) | (52,774 | ) | ||||

|

Restricted cash

|

- | (5,381 | ) | |||||

|

Other

|

(121 | ) | 782 | |||||

|

Cash used in investing activities

|

(25,524 | ) | (57,373 | ) | ||||

|

Financing activities:

|

||||||||

|

Common stock issued (purchased) - net

|

(244 | ) | 566 | |||||

|

Change in short-term debt

|

(71,000 | ) | (6,000 | ) | ||||

|

Cash dividend payments on common stock

|

(11,601 | ) | (11,011 | ) | ||||

|

Other

|

328 | 69 | ||||||

|

Cash used in financing activities

|

(82,517 | ) | (16,376 | ) | ||||

|

Increase in cash and cash equivalents

|

23 | 407 | ||||||

|

Cash and cash equivalents - beginning of period

|

3,457 | 8,432 | ||||||

|

Cash and cash equivalents - end of period

|

$ | 3,480 | $ | 8,839 | ||||

|

Supplemental disclosure of cash flow information:

|

||||||||

|

Interest paid

|

$ | 4,162 | $ | 3,325 | ||||

|

Income taxes paid

|

$ | - | $ | 9,000 | ||||

|

See Notes to Consolidated Financial Statements.

|

||||||||

5

NORTHWEST NATURAL GAS COMPANY

PART I. FINANCIAL INFORMATION

Notes to Consolidated Financial Statements

(Unaudited)

|

1.

|

Organization and Principles of Consolidation

|

The accompanying consolidated financial statements represent the consolidation of Northwest Natural Gas Company (NW Natural) and all companies that we directly or indirectly control, either through majority ownership or otherwise. Our direct and indirect wholly-owned subsidiaries include Gill Ranch Storage, LLC (Gill Ranch), NW Natural Energy, LLC (NWN Energy), NW Natural Gas Storage, LLC (NWN Gas Storage), and NNG Financial Corporation (NNG Financial). Investments in corporate joint ventures and partnerships that we do not directly or indirectly control, and for which we are not the primary beneficiary, are accounted for under the equity method or the cost method, which includes NWN Energy’s investment in Palomar Gas Holdings, LLC (PGH). NW Natural and its affiliated companies are collectively referred to herein as “NW Natural.” The consolidated financial statements are presented after elimination of all significant intercompany balances and transactions, except for amounts required to be included under regulatory accounting standards to reflect the effect of such regulation. In this report, the term “utility” is used to describe our regulated gas distribution business, and the term “non-utility” is used to describe our gas storage business and other non-utility investments and business activities (see Note 4).

Information presented in these interim consolidated financial statements is unaudited, but includes all material adjustments, including normal recurring accruals, that management considers necessary for a fair statement of the results for each period reported. These consolidated financial statements should be read in conjunction with the audited consolidated financial statements and related notes included in our 2010 Annual Report on Form 10-K (2010 Form 10-K). A significant part of our business is of a seasonal nature; therefore, results of operations for interim periods are not necessarily indicative of the results for a full year.

Our significant accounting policies are described in Note 2 of the 2010 Form 10-K. There were no material changes to those accounting policies during the three months ended March 31, 2011, except for a change in the application of our accounting policy with respect to revenue recognition for the regulatory adjustment for income taxes paid. For further discussion of significant accounting policies, see Note 2 below. Subsequent events are reported in Note 15.

Certain prior year balances in our consolidated financial statements have been combined or reclassified to conform with the current presentation. These changes had no impact on our prior year’s consolidated results of operations and no material impact on financial condition or cash flows.

6

2. Summary of Significant Accounting Policies

Industry Regulation

At March 31, 2011 and 2010 and at December 31, 2010, the amounts deferred as regulatory assets and liabilities were as follows:

|

Regulatory Assets

|

||||||||||||

|

March 31,

|

March 31,

|

December 31,

|

||||||||||

|

Thousands

|

2011

|

2010

|

2010

|

|||||||||

|

Current:

|

||||||||||||

|

Unrealized loss on derivatives(1)

|

$ | 25,655 | $ | 39,365 | $ | 38,437 | ||||||

|

Pension and other postretirement benefit liabilities(2)

|

10,988 | 7,502 | 10,988 | |||||||||

|

Other(3)

|

11,552 | 9,005 | 3,289 | |||||||||

|

Total current

|

$ | 48,195 | $ | 55,872 | $ | 52,714 | ||||||

|

Non-current:

|

||||||||||||

|

Unrealized loss on derivatives(1)

|

$ | 13,914 | $ | 18,637 | $ | 17,022 | ||||||

|

Income tax asset

|

70,241 | 75,515 | 72,341 | |||||||||

|

Pension and other postretirement benefit liabilities(2)

|

115,490 | 108,010 | 118,248 | |||||||||

|

Environmental costs(4)

|

117,544 | 107,537 | 114,311 | |||||||||

|

Other(3)

|

28,263 | 22,263 | 26,975 | |||||||||

|

Total non-current

|

$ | 345,452 | $ | 331,962 | $ | 348,897 | ||||||

|

Regulatory Liabilities

|

||||||||||||

|

March 31,

|

March 31,

|

December 31,

|

||||||||||

|

Thousands

|

2011 | 2010 | 2010 | |||||||||

|

Current:

|

||||||||||||

|

Gas costs payable

|

$ | 14,144 | $ | 26,164 | $ | 15,583 | ||||||

|

Unrealized gain on derivatives(1)

|

4,861 | 450 | 2,245 | |||||||||

|

Other(3)

|

10,011 | 9,418 | - | |||||||||

|

Total current

|

$ | 29,016 | $ | 36,032 | $ | 17,828 | ||||||

|

Non-current:

|

||||||||||||

|

Gas costs payable

|

$ | 3,932 | $ | 2,377 | $ | 2,297 | ||||||

|

Unrealized gain on derivatives(1)

|

1,560 | 5 | 628 | |||||||||

|

Accrued asset removal costs

|

256,203 | 242,952 | 252,941 | |||||||||

|

Other(3)

|

2,181 | 2,183 | 2,165 | |||||||||

|

Total non-current

|

$ | 263,876 | $ | 247,517 | $ | 258,031 | ||||||

|

(1)

|

An unrealized gain or loss on derivatives does not earn a rate of return or a carrying charge. These amounts, when realized at settlement, are recoverable through utility rates as part of the Purchased Gas Adjustment mechanism.

|

|

(2)

|

Certain pension and other postretirement benefit liabilities of the utility are approved for regulatory deferral. Such amounts are recoverable in rates, including an interest component, when recognized in pension expense or net periodic benefit cost (see Note 9).

|

|

(3)

|

Other primarily consists of deferrals and amortizations under other approved regulatory mechanisms. The accounts being amortized typically earn a rate of return or carrying charge.

|

|

(4)

|

Environmental costs are related to certain utility sites that are approved for regulatory deferral. We earn the utility’s authorized rate of return as a carrying charge on amounts paid, whereas the amounts accrued but not yet paid do not earn a rate of return or a carrying charge until expended.

|

7

Revenue Recognition

Utility and non-utility revenues, which are derived primarily from the sale, transportation or storage of natural gas, are recognized upon the delivery of gas commodity or service to customers. Since 2007, utility revenues have also included the recognition of a regulatory adjustment for income taxes paid pursuant to a legislative rule (commonly referred to as SB 408) in effect for certain gas and electric utilities in Oregon. Under SB 408, we are required to automatically implement a rate refund, or a rate surcharge, to utility customers on an annual basis. The refund or surcharge amount is based on the estimated difference between income taxes paid and income taxes authorized to be collected in customer rates. We have recorded the estimated refund, or surcharge, each quarter since 2007 based on the estimated annual amount to be recognized. However, on March 29, 2011, a legislative bill was introduced that would repeal SB 408 if enacted as drafted in its current form (SB 967 or Bill). As of May 4, 2011, the Oregon Senate had approved SB 967, but the Bill has not been approved by the Oregon House of Representatives or signed by the Governor of Oregon. We currently believe there is substantial uncertainty surrounding the continuation of the current legal requirements of SB 408. Accordingly, we determined that the threshold for recognizing revenues under the accounting standard for the effects of regulation had not been met, and therefore we did not record an estimated refund, or surcharge, in the first quarter of 2011 for this regulatory adjustment for income taxes paid.

New Accounting Standards

Adopted Standards

Fair Value Disclosures. In January 2010, the Financial Accounting Standards Board issued authoritative guidance on new fair value measurements and disclosures. This guidance requires additional disclosures for fair value measurements that use significant assumptions not observable in active markets (i.e. level 3 valuations), including a rollforward schedule. These changes were effective for periods beginning after December 15, 2010; however, we elected to early adopt these disclosure requirements, as shown in Note 9 in our 2010 Form 10-K. The adoption of this standard did not have a material effect on our financial statement disclosures.

Recent Accounting Pronouncements

There have been no recent accounting pronouncements issued, but not yet effective, which are expected to have a material impact on our financial condition, results of operations or cash flows.

|

3.

|

Earnings Per Share

|

Basic earnings per share are computed using the weighted average number of common shares outstanding during each period presented. Diluted earnings per share are computed using the weighted average number of common shares outstanding plus the potential effects of the assumed exercise of stock options, and payment of estimated stock awards from other stock-based compensation plans that are outstanding, at the end of each period presented. Diluted earnings per share are calculated as follows:

|

Three Months Ended

|

||||||||

|

March 31,

|

||||||||

|

Thousands, except per share amounts

|

2011

|

2010

|

||||||

|

Net income

|

$ | 40,773 | $ | 43,608 | ||||

|

Average common shares outstanding - basic

|

26,670 | 26,538 | ||||||

|

Additional shares for stock-based compensation plans

|

54 | 63 | ||||||

|

Average common shares outstanding - diluted

|

26,724 | 26,601 | ||||||

|

Earnings per share of common stock - basic

|

$ | 1.53 | $ | 1.64 | ||||

|

Earnings per share of common stock - diluted

|

$ | 1.53 | $ | 1.64 | ||||

8

For the three months ended March 31, 2011 and 2010, 2,150 and 5,120 common share equivalents, respectively, were excluded from the calculation of diluted earnings per share because the effect of these additional shares on the net income for both periods would have been anti-dilutive.

|

4.

|

Segment Information

|

We operate in two primary reportable business segments, local gas distribution and gas storage. We also have other investments and business activities not specifically related to one of these two reporting segments, which we aggregate and report as “other.” We refer to our local gas distribution business as the “utility,” and our “gas storage” and “other” business segments as “non-utility.” Our “gas storage” segment includes NWN Gas Storage, a wholly-owned subsidiary of NWN Energy, Gill Ranch, a wholly-owned subsidiary of NWN Gas Storage, the non-utility portion of our Mist underground storage facility in Oregon (Mist) and third-party optimization services. Our “other” segment includes NNG Financial and our equity investment in PGH which is pursuing development of the Palomar pipeline project. For further discussion of our segments, see Note 4 in our 2010 Form 10-K.

The following table presents summary financial information about the reportable segments for the three months ended March 31, 2011, and 2010. Inter-segment transactions were insignificant.

|

Three Months Ended March 31

|

||||||||||||||||

|

Non-Utility

|

||||||||||||||||

|

Thousands

|

Utility

|

Gas Storage

|

Other

|

Total

|

||||||||||||

|

2011

|

||||||||||||||||

|

Net operating revenues

|

$ | 129,162 | $ | 5,304 | $ | 42 | $ | 134,508 | ||||||||

|

Depreciation and amortization

|

15,914 | 1,395 | - | 17,309 | ||||||||||||

|

Income from operations

|

76,124 | 1,716 | 22 | 77,862 | ||||||||||||

|

Net income (loss)

|

40,130 | 688 | (45 | ) | 40,773 | |||||||||||

|

Total assets at March 31, 2011

|

2,304,731 | 244,403 | 22,419 | 2,571,553 | ||||||||||||

|

2010

|

||||||||||||||||

|

Net operating revenues

|

$ | 125,473 | $ | 5,411 | $ | 42 | $ | 130,926 | ||||||||

|

Depreciation and amortization

|

15,566 | 335 | - | 15,901 | ||||||||||||

|

Income from operations

|

76,582 | 4,511 | 17 | 81,110 | ||||||||||||

|

Net income

|

40,892 | 2,501 | 215 | 43,608 | ||||||||||||

|

Total assets at March 31, 2010

|

2,190,849 | 217,266 | 20,918 | 2,429,033 | ||||||||||||

|

Total assets at December 31, 2010

|

$ | 2,310,388 | $ | 282,945 | $ | 23,283 | $ | 2,616,616 | ||||||||

9

|

5.

|

Common Stock

|

As of March 31, 2011, our common shares authorized were 100,000,000 and our outstanding shares were 26,672,812.

We have a share repurchase program for our common stock under which we purchase shares on the open market or through privately negotiated transactions. We currently have Board authorization through May 2011 to repurchase up to an aggregate of 2.8 million shares, or up to $100 million. No shares of common stock were repurchased pursuant to this program during the three months ended March 31, 2011, but since inception in 2000 a total of 2.1 million shares have been repurchased at a total cost of $83.3 million.

|

6.

|

Stock-Based Compensation

|

We have several stock-based compensation plans, including a Long-Term Incentive Plan (LTIP), a Restated Stock Option Plan (Restated SOP) and an Employee Stock Purchase Plan. These plans are designed to promote stock ownership in NW Natural by employees and officers. For additional information on our stock-based compensation plans, see Part II, Item 8., Note 6, in the 2010 Form 10-K and current updates provided below.

Long-Term Incentive Plan. On February 23, 2011, 37,950 performance-based shares were granted under the LTIP, which include a market condition, based on target-level awards and a weighted-average grant date fair value of $25.25 per share. Fair value was estimated as of the date of grant using a Monte-Carlo option pricing model based on the following assumptions:

|

Stock price on valuation date

|

$ | 45.74 | ||

|

Performance term (in years)

|

3.0 | |||

|

Quarterly dividends paid per share

|

$ | 0.435 | ||

|

Expected dividend yield

|

3.7 | % | ||

|

Dividend discount factor

|

0.8930 |

In February 2011, the Board approved a payout of performance-based stock awards under the LTIP for the 2008-10 award period. Shares of common stock were purchased on the open market to satisfy these awards.

Restated Stock Option Plan. On February 23, 2011, options to purchase 122,700 shares were granted under the Restated SOP, with an exercise price equal to the closing market price of $45.74 per share on the date of grant, vesting over a four-year period following the date of grant and with a term of 10 years and 7 days. The weighted-average grant date fair value was $6.73 per share. Fair value was estimated as of the date of grant using the Black-Scholes option pricing model based on the following assumptions:

|

Risk-free interest rate

|

2.0 | % | ||

|

Expected life (in years)

|

4.5 | |||

|

Expected market price volatility factor

|

24.5 | % | ||

|

Expected dividend yield

|

3.8 | % | ||

|

Forfeiture rate

|

3.1 | % |

As of March 31, 2011, there was $1.3 million of unrecognized compensation cost related to the unvested portion of outstanding Restated SOP awards expected to be recognized over a period extending through 2014.

|

7.

|

Cost and Fair Value Basis of Long-Term Debt

|

Cost of Long-Term Debt

Our long-term debt consists of medium-term notes (MTNs) with maturity dates from 2011 through 2035, interest rates ranging from 3.95 percent to 9.05 percent, and a weighted-average coupon rate of 6.17 percent. For the three months ended March 31, 2011, we did not issue or redeem any MTNs. For more detail on our outstanding long-term debt, see Note 7 in our 2010 Form 10-K.

10

Fair Value of Long-Term Debt

The following table provides an estimate of the fair value of our long-term debt, including current maturities of long-term debt, using market prices in effect on the valuation date. Because our debt outstanding does not trade in active markets, we used interest rates for other company’s outstanding debt issues that actively trade and have similar credit ratings, terms and remaining maturities to estimate fair value of our long-term debt issues. These are significant other observable inputs, or level 2 inputs, in the fair value hierarchy.

|

March 31,

|

December 31,

|

|||||||||||

|

Thousands

|

2011

|

2010

|

2010

|

|||||||||

|

Carrying amount

|

$ | 601,700 | $ | 636,700 | $ | 601,700 | ||||||

|

Estimated fair value

|

$ | 680,436 | $ | 687,937 | $ | 690,126 | ||||||

|

8.

|

Comprehensive Income

|

Items excluded from net income and charged directly to stockholders’ equity are included in accumulated other comprehensive income (loss), net of tax. The amount of accumulated other comprehensive loss in stockholders’ equity is $6.5 million and $5.9 million as of March 31, 2011 and 2010, respectively, which is related to employee benefit plan liabilities. The following table provides a reconciliation of net income to total comprehensive income for the three months ended March 31, 2011 and 2010.

|

Three Months Ended

|

||||||||

|

March 31,

|

||||||||

|

Thousands

|

2011

|

2010

|

||||||

|

Net income

|

$ | 40,773 | $ | 43,608 | ||||

|

Amortization of employee benefit plan liability, net of tax

|

146 | 98 | ||||||

|

Total comprehensive income

|

$ | 40,919 | $ | 43,706 | ||||

11

|

9.

|

Pension and Other Postretirement Benefit Costs

|

The following tables provide the components of net periodic benefit cost for our company-sponsored qualified and non-qualified defined benefit pension plans and other postretirement benefit plans:

|

Three Months Ended March 31,

|

||||||||||||

|

Other Postretirement

|

||||||||||||

|

Pension Benefits

|

Benefits

|

|||||||||||

|

Thousands

|

2011

|

2010

|

2011

|

2010

|

||||||||

|

Service cost

|

$ | 1,899 | $ | 1,773 | $ | 168 | $ | 156 | ||||

|

Interest cost

|

4,527 | 4,491 | 344 | 343 | ||||||||

|

Expected return on plan assets

|

(4,456 | ) | (4,564 | ) | - | - | ||||||

|

Amortization of net actuarial loss

|

2,692 | 1,768 | 68 | 7 | ||||||||

|

Amortization of prior service costs

|

88 | 206 | 49 | 49 | ||||||||

|

Amortization of transition obligations

|

- | - | 103 | 103 | ||||||||

|

Net periodic benefit cost

|

4,750 | 3,674 | 732 | 658 | ||||||||

|

Amount allocated to construction

|

(1,235 | ) | (953 | ) | (226 | ) | (208 | ) | ||||

|

Net amount charged to expense

|

$ | 3,515 | $ | 2,721 | $ | 506 | $ | 450 | ||||

See Part II, Item 8., Note 9, in the 2010 Form 10-K for more information about our pension and other postretirement benefit plans.

In addition to the company-sponsored defined benefit plans referred to above, we contribute to a multiemployer pension plan for our bargaining unit employees in accordance with our collective bargaining agreement, known as the Western States Office and Professional Employees International Union Pension Fund (Western States Plan). The cost of this plan is in addition to pension expense in the table above. The Western States Plan has reported an accumulated funding deficit for the current plan year and remains in critical status. The Western States Plan trustees adopted a rehabilitation plan that reduced benefit accrual rates and adjustable benefits for active employee participants and increased future employer contribution rates. These changes are expected to improve the funding status of the plan. We made contributions totaling $0.1 million to the Western States Plan for both the three months ended March 31, 2011 and 2010. If we withdraw and the plan is underfunded, we could be assessed a withdrawal liability. Currently, we have no intent to withdraw from the plan, so we have not recorded a withdrawal liability.

Employer Pension Contributions

During the first quarter of 2011 we made cash contributions totaling $13.6 million to our qualified defined benefit pension plans. We also expect to contribute up to an additional $10 million to these qualified plans over the last nine months of 2011, plus we expect to make ongoing benefit payments under our unfunded, non-qualified pension plans and other postretirement benefit plans. For more information see Part II, Item 8., Note 9, in the 2010 Form 10-K.

12

10. Income Tax

The effective income tax rate for the three months ended March 31, 2011 and 2010 varied from the combined federal and state statutory tax rates principally due to the following:

|

March 31,

|

||||||||

|

2011

|

2010

|

|||||||

|

Federal statutory tax rate

|

35.0 | % | 35.0 | % | ||||

|

Increase (decrease):

|

||||||||

|

Current state income tax, net of federal tax benefit

|

4.6 | % | 4.9 | % | ||||

|

Amortization of investment and energy tax credits

|

-0.4 | % | -0.5 | % | ||||

|

Differences required to be flowed-through by regulatory commissions

|

1.5 | % | 1.5 | % | ||||

|

Gains on company and trust-owned life insurance

|

-0.2 | % | -0.2 | % | ||||

|

Other - net

|

0.1 | % | 0.1 | % | ||||

|

Effective income tax rate

|

40.6 | % | 40.8 | % | ||||

The decrease in our effective tax rate for the three months ended March 31, 2011 compared to the same period in 2010 was minor and primarily due to a change in state income tax rates. See Note 10 in our 2010 Form 10-K.

|

11.

|

Property, Plant and Equipment

|

The following table sets forth the major classifications of our property, plant and equipment and accumulated depreciation as of March 31, 2011 and 2010 and December 31, 2010:

|

March 31,

|

December 31,

|

|||||||||||

|

Thousands

|

2011

|

2010

|

2010

|

|||||||||

|

Utility plant in service

|

$ | 2,264,055 | $ | 2,206,571 | $ | 2,247,952 | ||||||

|

Utility construction work in progress

|

28,464 | 25,736 | 29,324 | |||||||||

|

Less: Accumulated depreciation

|

720,134 | 691,420 | 710,214 | |||||||||

|

Utility plant-net

|

1,572,385 | 1,540,887 | 1,567,062 | |||||||||

|

Non-utility plant in service

|

292,089 | 66,084 | 290,038 | |||||||||

|

Non-utility construction work in progress

|

8,945 | 111,143 | 9,088 | |||||||||

|

Less: Accumulated depreciation

|

13,505 | 10,887 | 12,025 | |||||||||

|

Non-utility plant-net

|

$ | 287,529 | $ | 166,340 | $ | 287,101 | ||||||

|

Total property, plant and equipment

|

$ | 1,859,914 | $ | 1,707,227 | $ | 1,854,163 | ||||||

13

12. Investments

Our other long-term investments include financial investments in life insurance policies, which are accounted for at fair value, and equity investments in certain partnerships and limited liability companies, which are accounted for under the equity or cost methods. See Part II, Item 8., Note 12, in the 2010 Form 10-K for more detail on our investments.

Variable Interest Entities. PGH is a development stage variable interest entity. Palomar, a wholly-owned subsidiary of PGH, is pursuing the development of a new gas transmission pipeline that would provide an interconnection with our utility distribution system. PGH is owned 50 percent by NWN Energy and 50 percent by Gas Transmission Northwest Corporation (GTN), an indirect wholly-owned subsidiary of TransCanada Corporation. As of March 31, 2011, we updated our VIE analysis and determined that we are not the primary beneficiary of PGH’s activities as defined by the authoritative guidance related to consolidations. Therefore, we account for our investment in PGH and the Palomar project under the equity method, which is included in other investments on our balance sheet. Our maximum loss exposure related to PGH is limited to our equity investment balance, less our share of any cash or other assets available to us as a 50 percent owner.

PGH Impairment Analysis. In March 2011, Palomar withdrew its original application with the Federal Energy Regulatory Commission (FERC) for a proposed natural gas pipeline in Oregon. At the same time, Palomar informed FERC that it intends to file an application later this year or in 2012 to reflect changes in the project and more closely align with the region’s current and future gas needs. Palomar is working with customers in the Northwest to further understand their gas transportation needs. Assuming Palomar obtains commercial support for its revised pipeline proposal, Palomar expects to file a new certificate application with FERC.

We performed an impairment analysis of our equity investment as of March 31, 2011 and determined that we did not have any impairment because the fair value of expected cash flows from development of this pipeline project exceeds our equity investment. If, however, we learn that the project is not viable or will not go forward, then we could be required to recognize an impairment charge of up to approximately $14.4 million based on the amount of our equity investment of $14.8 million as of March 31, 2011 net of cash and working capital at Palomar. We will continue to monitor and update our impairment analysis as needed.

|

13.

|

Derivative Instruments

|

We enter into swap, option and various option combinations for the purpose of hedging natural gas. We primarily use these derivative financial instruments to manage commodity prices related to our natural gas purchase requirements. A small portion of the derivatives are also related to foreign currency exchange transactions.

In the normal course of business, we enter into indexed-price physical forward natural gas commodity purchase (gas supply) contracts to meet the requirements of core utility customers. We also enter into financial derivatives, up to prescribed limits, to hedge price variability related to the physical gas supply contracts. Derivatives entered into prudently for future gas years prior to our annual PGA filing receive regulatory deferred accounting treatment. Derivative contracts entered into after the annual PGA rate was set on November 1, 2010 that are for the current gas contract year are subject to our PGA incentive sharing mechanism, which provides for a 90 percent deferral of any gains and losses as regulatory assets or liabilities, with the remaining 10 percent recognized on the income statement.

Most of our commodity hedging for the upcoming gas year is completed prior to the start of each gas year, and these hedge prices are included in our annual PGA filing. We typically hedge approximately 75 percent of our anticipated year-round sales volumes based on normal weather. We entered the 2010-11 gas year (November 1, 2010 – October 31, 2011) hedged at a level of approximately 77 percent, including 62 percent financially hedged and 15 percent physically hedged with gas in storage.

14

At March 31, 2011, we were hedged with financial contracts for the upcoming 2011-12 gas year at approximately 50 percent based on anticipated sales volumes. Of the amount currently hedged for the 2011-12 gas year approximately 35 percent was hedged with financial contracts and an additional 15 percent attributable to storage from future purchases and current storage levels.

The following table discloses the income statement presentation for the unrealized gains and losses from our derivative instruments for the years ended March 31, 2011 and 2010. All of our currently outstanding derivative instruments are related to regulated utility operations as illustrated by the derivative gains and losses being deferred to the balance sheet accounts in accordance with regulatory accounting.

|

Three Months Ended

|

|||||||||||||||||

|

March 31, 2011

|

March 31, 2010

|

||||||||||||||||

|

Thousands

|

Natural gas commodity(1)

|

Foreign currency (2)

|

Natural gas commodity(1)

|

Foreign currency (2)

|

|||||||||||||

|

Cost of sales

|

$ | (33,750 | ) | $ | - | $ | (57,564 | ) | $ | - | |||||||

|

Other comprehensive income (loss)

|

- | 602 | - | (17 | ) | ||||||||||||

|

Less:

|

|||||||||||||||||

|

Amounts deferred to regulatory accounts on balance sheet

|

33,750 | (602 | ) | 57,564 | 17 | ||||||||||||

|

Total impact on earnings

|

$ | - | $ | - | $ | - | $ | - | |||||||||

|

(1)

|

Unrealized gain (loss) from natural gas commodity hedge contracts is recorded in cost of sales and reclassified to regulatory deferral accounts on the balance sheet.

|

||||||||||||||||

|

(2)

|

Unrealized gain (loss) from foreign currency exchange contracts is recorded in other comprehensive income, and reclassified to regulatory deferral accounts on the balance sheet.

|

||||||||||||||||

We had no collateral posted with our counterparties as of March 31, 2011 or 2010. We attempt to minimize the potential exposure to collateral calls by our counterparties to manage our liquidity risk. Based on our current credit ratings, most counterparties allow us credit limits ranging from $25 million to $50 million before collateral postings are required. Our collateral call exposure is set forth under credit support agreements, which generally contain credit limits. We also could be subject to collateral call exposure where we have agreed to provide adequate assurance, which is not specific as to the amount of credit limit allowed, but could potentially require additional collateral in the event of a material adverse change. Based upon current contracts outstanding, which reflect unrealized losses of $33.1 million at March 31, 2011, we have estimated the level of collateral demands, with and without potential adequate assurance calls, using current gas prices and various downgrade credit rating scenarios for NW Natural as follows:

|

Credit Rating Downgrade Scenarios

|

||||||||||||||||||||

|

Thousands

|

(Current Ratings) A+/A3

|

BBB+/Baa1

|

BBB/Baa2

|

BBB-/Baa3

|

Speculative

|

|||||||||||||||

|

With Adequate Assurance Calls

|

$ | - | $ | - | $ | - | $ | 3,223 | $ | 18,058 | ||||||||||

|

Without Adequate Assurance Calls

|

$ | - | $ | - | $ | - | $ | 3,223 | $ | 14,897 | ||||||||||

In the three months ended March 31, 2011 and 2010, we realized net losses of $20.9 million and $6.2 million, respectively, from the settlement of natural gas hedge contracts at maturity, which were recorded as increases to the cost of gas. The exchange rate in all foreign currency forward purchase contracts is included in our purchased cost of gas at settlement; therefore, no gain or loss is recorded from the settlement of those contracts.

15

We are exposed to derivative credit and liquidity risk primarily through securing fixed price natural gas commodity swaps to hedge the risk of price increases for our natural gas purchases made on behalf of our customers. For more information on our derivative instruments, see Note 13 in our 2010 Form 10-K.

Fair Value

In accordance with fair value accounting, we include nonperformance risk in calculating fair value adjustments. This includes a credit risk adjustment based on the credit spreads of our counterparties when we are in an unrealized gain position, or on our own credit spread when we are in an unrealized loss position. Our assessment of non-performance risk is generally derived from the credit default swap market and from bond market credit spreads. The impact of the credit risk adjustments for all outstanding derivatives was immaterial to the fair value calculation at March 31, 2011. As of March 31, 2011 and 2010 and December 31, 2010, the fair value was $33.1 million, $57.5 million and $52.6 million, respectively, using significant other observable, or level 2, inputs. We have used no level 3 inputs in our derivative valuations. We also did not have any transfers between level 1 or level 2 during the three months ended March 31, 2011 and 2010.

|

14.

|

Commitments and Contingencies

|

Environmental Matters

We own, or previously owned, properties that may require environmental remediation or action. We accrue all material loss contingencies relating to these properties that we believe to be probable of assertion and reasonably estimable. We continue to study and evaluate the extent of our potential environmental liabilities, but due to the numerous uncertainties surrounding the course of environmental remediation and the preliminary nature of several site investigations, in some cases, we may not be able to reasonably estimate the high end of the range of possible loss. In those cases we have disclosed the nature of the potential loss and the fact that the high end of the range cannot be reasonably estimated.

We regularly review our environmental liability for each site where we may be exposed to remediation responsibilities. The costs of environmental remediation are difficult to estimate. A number of steps are involved in each environmental remediation effort, including site investigations, remediation, operations and maintenance, monitoring and site closure. Each of these steps may, over time, involve a number of alternative actions, each of which can change the course and scope of the effort. Many of these steps are dependent upon the approval and direction of federal and state environmental regulators. The policies, determinations and directions of the regulators may develop and change over time and different regulators may take different positions on the various steps, creating further uncertainty as to the timing and scope of remediation activities. In certain cases, in addition to us, there are a number of other potentially responsible parties, each of which, in proceedings and negotiations with other potentially responsible parties and regulators, may influence the course and scope of the remediation effort. The allocation of liabilities among the potentially responsible parties is often subject to dispute and can be highly uncertain. The events giving rise to environmental liabilities often occurred many decades ago, which complicates the determination of allocating liabilities among potentially responsible parties. Site investigations and remediation efforts often develop slowly over many years. In addition, disputes may arise between potentially responsible parties and regulators as to the severity of particular environmental matters and what remediation efforts are appropriate. These disputes could lead to adversarial administrative proceedings or litigation, with uncertain outcomes.

We estimate the range of loss for environmental liabilities using current technology, enacted laws and regulations, industry experience gained at similar sites and an assessment of the probable level of involvement and financial condition of other potentially responsible parties. Unless there is an estimate within this range of possible losses that is more likely than other cost estimates, we record the liability at the lower end of this range. It is likely that changes in these estimates and ranges will occur throughout the remediation process for each of these sites due to uncertainty concerning our responsibility, the complexity of environmental laws and regulations and the selection of compliance alternatives. The status of each of the sites currently under investigation is provided below.

16

Gasco site. We own property in Multnomah County, Oregon that is the site of a former gas manufacturing plant that was closed in 1956 (Gasco site). The Gasco site has been under investigation by us for environmental contamination under the Oregon Department of Environmental Quality’s (ODEQ) Voluntary Clean-Up Program. In June 2003, we filed a Feasibility Scoping Plan and an Ecological and Human Health Risk Assessment with the ODEQ, which outlined a range of remedial alternatives for the most contaminated portion of the Gasco site. In May 2007, we completed a revised Remediation Investigation Report and submitted it to the ODEQ for review. We also submitted a Focused Feasibility Study (FFS) for the groundwater source control portion of the Gasco site, which ODEQ conditionally approved in March 2008, subject to the submission of additional information. We provided that information to ODEQ and are now working with the agency on the final design for the source control system. Based on the information currently available for groundwater source control at the Gasco site and our current assumptions regarding remediation, we have estimated a range of liability between $11 million and $30 million, for which we have recorded an accrued liability of $11.8 million at March 31, 2011. The range of liability will be reassessed when ODEQ makes a final source control design decision. In addition to groundwater source control, we signed a joint Order on Consent with the Environmental Protection Agency (EPA), which requires the design of remedial action for sediments from the Gasco site. This design project is underway. We also have other investigation and clean-up work, including work on the uplands portion of the Gasco site, that we expect to be required. For the sediments project and other work, we have recorded an additional accrued liability of $38.0 million, which reflects the low end of the range of potential liability. We have accrued at the low end of the range of potential liability for the sediments project and other environmental work at the Gasco site because no amount within the range is considered to be more likely than another, and the high end of the range cannot reasonably be estimated.

Siltronic site. We previously owned property adjacent to the Gasco site that now is the location of a manufacturing plant owned by Siltronic Corporation (the Siltronic site). We are currently conducting an investigation of manufactured gas plant wastes on the uplands at this site for the ODEQ. The liability accrued at March 31, 2011 for the Siltronic site is $1 million, which is at the low end of the range of potential liability because no amount within the range is considered to be more likely than another, and the high end of the range cannot reasonably be estimated.

Portland Harbor site. In 1998, the ODEQ and the EPA completed a study of sediments in a 5.5-mile segment of the Willamette River (Portland Harbor) that includes an area adjacent to the Gasco and Siltronic sites. The Portland Harbor was listed by the EPA as a Superfund site in 2000 and we were notified that we are a potentially responsible party. We then joined with other potentially responsible parties, referred to as the Lower Willamette Group, to fund environmental studies in the Portland Harbor. Subsequently, the EPA approved a Programmatic Work Plan, Field Sampling Plan and Quality Assurance Project Plan for the Portland Harbor Remedial Investigation/Feasibility Study (RI/FS), completion of which is scheduled for 2011. The EPA and the Lower Willamette Group are conducting focused studies on approximately nine miles of the lower Willamette River, including the 5.5-mile segment previously studied by the EPA. In August 2008, we signed a cooperative agreement to participate in a phased natural resource damage assessment, with the intent to identify what, if any, additional information is necessary to estimate further liabilities sufficient to support an early restoration-based settlement of natural resource damage claims. As of March 31, 2011, we have a liability accrued of $8 million for this site, which is at the low end of the range of the potential liability because no amount within the range is considered to be more likely than another, and the high end of the range cannot reasonably be estimated.

Central Service Center site. In 2006, we received notice from the ODEQ that our Central Service Center in southeast Portland (Central Service Center site) was assigned a high priority for further environmental investigation. Previously there were three manufactured gas storage tanks on the premises. The ODEQ believes there could be site contamination associated with releases of condensate from stored manufactured gas as a result of historic gas handling practices. In the early 1990s, we excavated waste piles and much of the contaminated surface soils and removed accessible waste from some of the abandoned piping. In early 2008, we received notice that this site was added to the ODEQ’s list of sites where releases of hazardous substances have been confirmed and to its list where additional investigation or cleanup is necessary. We are currently performing an environmental investigation of the property with the ODEQ’s Independent Cleanup Pathway. As of March 31, 2011, we have a liability accrued of $0.5 million for investigation at this site. The estimate is at the low end of the range of potential liability because no amount within the range is considered to be more likely than another and the high end of the range cannot reasonably be estimated.

17

Front Street site. The Front Street site was the former location of a gas manufacturing plant we operated. It is near but outside the geographic scope of the current Portland Harbor site sediment studies. The EPA directed the Lower Willamette Group to collect a series of surface and subsurface sediment samples off the river bank adjacent to where that facility was located. Based on the results of that sampling, the EPA notified the Lower Willamette Group that additional sampling would be required. As the Front Street site is upstream from the Portland Harbor site, the EPA agreed that it could be managed separately from the Portland Harbor site under ODEQ authority. Work plans for source control investigation and a historical report were submitted to ODEQ and initial studies were completed. In 2010, ODEQ required additional studies which are underway. As of March 31, 2011, we have an estimated liability accrued of $0.9 million for the study of the sediments and riverbank groundwater and soils at the site. The estimate is at the low end of the range of potential liability because no amount within the range is considered to be more likely than another and the high end of the range cannot reasonably be estimated.

Oregon Steel Mills site. See “Legal Proceedings,” below.

Accrued Liabilities Relating to Environmental Sites. The following table summarizes the accrued liabilities relating to environmental sites at March 31, 2011 and 2010 and December 31 2010:

|

Current Liabilities

|

Non-Current Liabilities

|

|||||||||||||||||||||||

|

Mar. 31,

|

Mar. 31,

|

Dec. 31,

|

Mar. 31,

|

Mar. 31,

|

Dec. 31,

|

|||||||||||||||||||

|

Thousands

|

2011

|

2010

|

2010

|

2011

|

2010

|

2010

|

||||||||||||||||||

|

Gasco site

|

$ | 13,718 | $ | 9,924 | $ | 11,366 | $ | 36,099 | $ | 42,165 | $ | 38,921 | ||||||||||||

|

Siltronic site

|

730 | 679 | 720 | 291 | 508 | 201 | ||||||||||||||||||

|

Portland Harbor site

|

2,219 | 1,873 | 2,304 | 5,829 | 7,041 | 5,784 | ||||||||||||||||||

|

Central Service Center site

|

5 | 5 | 5 | 501 | 511 | 510 | ||||||||||||||||||

|

Front Street site

|

- | 72 | 1 | 947 | 252 | 1,097 | ||||||||||||||||||

|

Other sites

|

- | - | - | 117 | 106 | 108 | ||||||||||||||||||

|

Total

|

$ | 16,672 | $ | 12,553 | $ | 14,396 | $ | 43,784 | $ | 50,583 | $ | 46,621 | ||||||||||||

Regulatory and Insurance Recovery for Environmental Costs. In May 2003, the Public Utility Commission of Oregon (OPUC) approved our request to defer unreimbursed environmental costs associated with certain named sites, including those described above. Beginning in 2006, the OPUC granted us additional authorization to accrue interest on deferred environmental cost balances, subject to an annual demonstration that we have maximized our insurance recovery or made substantial progress in securing insurance recovery for unrecovered environmental expenses. Through a series of extensions, the authorized cost deferral and interest accrual was extended through January 2010. We have filed a request with the OPUC to extend this deferral, and expect authorization during the second quarter of 2011. In addition, we filed a request with the Washington Utilities and Transportation Commission (WUTC) in February 2011 to defer certain environmental costs associated with services provided to Washington customers, and expect an order from the WUTC during the second quarter of 2011.

On a cumulative basis, we have recognized a total of $106.3 million for environmental costs, including legal, investigation, monitoring and remediation costs, including $4.9 million accrued and paid prior to regulatory deferral order approval. At March 31, 2011, we had a regulatory asset of $117.5 million, which includes $47.1 million of total paid expenditures to date, $60.5 million for additional environmental costs expected to be paid in the future and accrued interest of $15.3 million, partially offset by $5.4 million of environmental costs expensed in prior years. See table below.

In December 2010, NW Natural commenced litigation against certain of its historical liability insurers in Multnomah County Circuit Court, State of Oregon, Case Number 1012-17532. The defendants include Associated Electric & Gas Insurance Services Limited, Allianz Global Risk US Insurance Company, certain underwriters at Lloyd's London, certain London market insurance companies and ten other insurance companies. In the suit, NW Natural alleges that the defendant insurance companies issued third party liability insurance policies to NW Natural and that the defendants have breached the terms of those policies by failing to indemnify NW Natural for liabilities arising from environmental contamination at certain sites caused or alleged to be caused by its historical operations. NW Natural seeks damages in excess of $40 million in losses it has incurred to date, as well as declaratory relief for additional losses it expects to incur in the future. After seeking recovery of our environmental costs from our insurers, we believe recovery of the remainder of our deferred charges, if any, is probable through the regulatory process. Our regulatory asset will be reduced by the amount of any corresponding insurance recoveries. We continue to anticipate that our overall insurance recovery effort will extend over several years.

18

We anticipate that our regulatory recovery of environmental cost deferrals will not be initiated within the next 12 months because we do not expect to have concluded our insurance recovery efforts during that time period, and because recovery would be expected to occur through the implementation of new rates through a general rate proceeding. As such we have classified our regulatory assets for environmental cost deferrals as non-current. The following table summarizes the non-current regulatory assets relating to environmental sites at March 31, 2011 and 2010 and December 31, 2010:

|

Non-Current Regulatory Assets

|

||||||||||||

|

March 31,

|

March 31,

|

December 31,

|

||||||||||

|

Thousands

|

2011

|

2010

|

2010

|

|||||||||

|

Gasco site

|

$ | 76,338 | $ | 70,411 | $ | 74,205 | ||||||

|

Siltronic site

|

3,440 | 3,020 | 3,174 | |||||||||

|

Portland Harbor site

|

34,732 | 32,140 | 33,940 | |||||||||

|

Central Service Center site

|

558 | 550 | 553 | |||||||||

|

Front Street site

|

2,042 | 1,032 | 2,020 | |||||||||

|

Other sites

|

434 | 384 | 420 | |||||||||

|

Total

|

$ | 117,544 | $ | 107,537 | $ | 114,312 | ||||||

We are subject to claims and litigation arising in the ordinary course of business. Although the final outcome of any of these legal proceedings cannot be predicted with certainty, including the matter described below, we do not expect that the ultimate disposition of any of these matters will have a material effect on our financial condition, results of operations or cash flows.

Oregon Steel Mills site. In 2004, NW Natural was served with a third-party complaint by the Port of Portland (Port) in a Multnomah County Circuit Court case, Oregon Steel Mills, Inc. v. The Port of Portland. The Port alleges that in the 1940s and 1950s petroleum wastes generated by our predecessor, Portland Gas & Coke Company, and 10 other third-party defendants were disposed of in a waste oil disposal facility operated by the United States or Shaver Transportation Company on property then owned by the Port and now owned by Oregon Steel Mills. The complaint seeks contribution for unspecified past remedial action costs incurred by the Port regarding the former waste oil disposal facility as well as a declaratory judgment allocating liability for future remedial action costs. No date has been set for trial and discovery is ongoing. Although the final outcome of this proceeding cannot be predicted with certainty, we do not expect that the ultimate disposition of this matter will have a material effect on our financial condition, results of operations or cash flows.

15. Subsequent Event

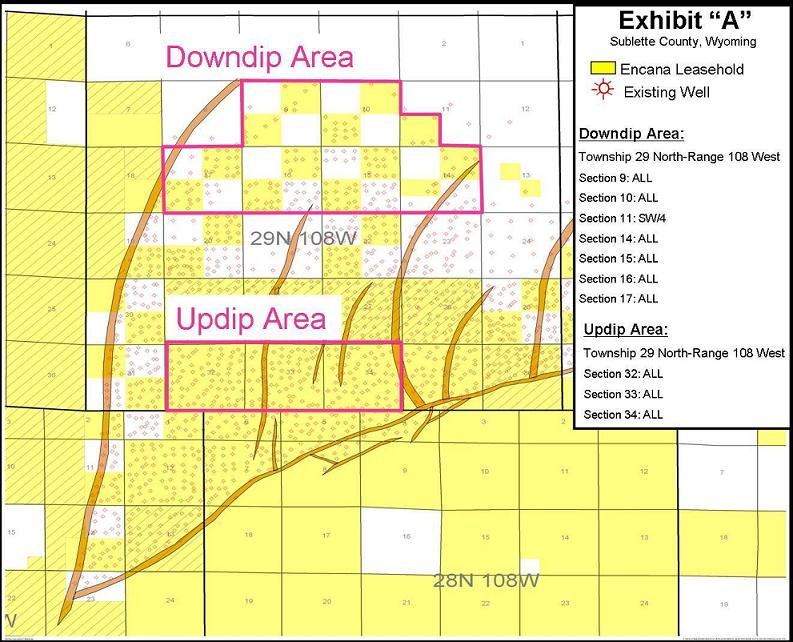

On April 28, 2011 the OPUC issued an order approving our investment to develop gas reserves on behalf of our Oregon customers under an agreement with Encana Oil & Gas (USA) Inc. Under the agreement, we expect to invest approximately $45-55 million a year, over a five-year period, for a total investment of about $250 million, which will cover a portion of drilling costs in exchange for working interests in certain sections of the Jonah Field located north of Rock Springs, Wyoming. These sections include both future and current producing wells. The gas reserves will provide long-term gas supplies for our Oregon utility customers over a period expected to be about 30 years. During the first 10 years of the agreement, we forecast to receive approximately 58 billion cubic feet (Bcf) from the transaction, or 8-10 percent of our average annual requirements for utility operations. Our total investment under the agreement is expected to result in about 93 Bcf of gas at an average all-in price of approximately $5.15 per dekatherm. We estimate net present value savings to customers of over $50 million over the life of the investment as compared to other long-term supply alternatives.

Under the order, the OPUC determined that the investment was prudent and that the Company is allowed to recover its costs under the agreement on an ongoing basis through its Purchased Gas Adjustment (PGA) cost sharing mechanism, including the deferral process for the commodity cost of gas. Annually, the Company will forecast amounts related to the costs and volumes expected, and variances will be subject to the PGA’s normal sharing mechanism up to $10 million of variance. Any variance in excess of $10 million, either negative or positive, will be passed through to customers at 100 percent, rather than at the 80 or 90 percent level associated with the normal sharing mechanism. As part of the decision by the OPUC to approve the Company’s investment, we will file a general rate case in Oregon no later than December 31, 2011.

19

|

|

ITEM 2. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

|

The following is management’s assessment of Northwest Natural Gas Company’s (NW Natural) financial condition, including the principal factors that affect results of operations. The discussion refers to our consolidated activities for the three months ended March 31, 2011 and 2010. Unless otherwise indicated, references in this discussion to “Notes” are to the Notes to Consolidated Financial Statements in this report. This discussion should be read in conjunction with our 2010 Annual Report on Form 10-K (2010 Form 10-K).

The consolidated financial statements include the accounts of NW Natural and its direct and indirect wholly-owned subsidiaries which include: Gill Ranch Storage, LLC (Gill Ranch), NW Natural Energy, LLC (NWN Energy), NW Natural Gas Storage, LLC (NWN Gas Storage), and NNG Financial Corporation (NNG Financial). These statements also include accounts related to an equity investment in Palomar Gas Holdings, LLC (PGH), which is pursuing the development of a proposed natural gas pipeline through its wholly-owned subsidiary Palomar Gas Transmission LLC (Palomar). Together these accounts make up our regulated local gas distribution business, our gas storage businesses, and other regulated and non-regulated investments primarily engaged in energy-related businesses. In this report, the term “utility” is used to describe our regulated gas distribution business (local distribution company), and the term “non-utility” is used to describe our gas storage businesses (gas storage) as well as our other regulated and non-regulated investments and business activities (other). For a further discussion of our business segments, see Note 4.

In addition to presenting results of operations and earnings amounts in total, certain measures are expressed in cents per share. These amounts reflect factors that directly impact earnings. We believe this per share information is useful because it enables readers to better understand the impact of these factors on consolidated earnings. All references in this section to earnings per share are on the basis of diluted shares (see Part II, Item 8., Note 3, “Earnings Per Share,” in our 2010 Form 10-K).

Executive Summary

Highlights of the first quarter of 2011 as compared to the same period in 2010 include:

|

|

|

·

|

Consolidated earnings of $40.8 million or $1.53 per share in the first quarter of 2011, as compared to $43.6 million and $1.64 in the first quarter of 2010;

|

|

·

|

Net income from utility operations decreased $0.8 million, from $40.9 million in 2010 to $40.1 million in 2011, largely due to benefits received last year from a property tax refund and the regulatory adjustment for income taxes paid (see Revenue Recognition below under Application of Critical Accounting Policies and Estimates for further discussion of the regulatory adjustment for income taxes paid);

|

|

·

|

Net income from gas storage operations decreased $1.8 million, from $2.5 million in 2010 to $0.7 million in 2011, primarily reflecting Gill Ranch’s initial start-up costs and lower level of contracted capacity prior to its first injection season beginning April 1, 2011;

|

|

·

|

Consolidated net operating revenues (margin) increased $3.6 million or 3 percent over 2010, with utility margin up $3.7 million and gas storage margin down $0.1 million;

|

|

·

|

Consolidated total operating expenses increased $6.8 million or 14 percent over 2010, but that was largely attributed to a $5.2 million refund of property tax expense at the utility in 2010 and start-up costs at Gill Ranch;

|

|

·

|

Other income decreased $1.8 million in 2011 compared to 2010, primarily due to $1.9 million of interest income received by the utility in 2010 in connection with the property tax refund referred to above;

|

|

·

|

Cash flow from operating activities in 2011 was $108.0 million, for an increase of $33.9 million or 46 percent over 2010; and

|

|

·

|

The utility added more than 6,000 new customers over the last 12 months, for an annual growth rate of 0.9 percent compared to 0.7 percent a year ago.

|

20

Issues, Challenges and Performance Measures

Economic Environment. Weakness in the local, national and global economies has continued to adversely impact utility customer growth, the demand for natural gas, and the value of natural gas storage services. Most recently, our utility’s annual customer growth rate increased slightly to 0.9 percent at March 31, 2011, as compared to 0.7 percent at March 31, 2010. Although total delivered volumes to utility customers in the first quarter of 2011 increased 20 percent, we are still faced with unemployment rates around 10 percent in our service territories of Oregon and southwest Washington and a sluggish business environment. Despite these challenges, we believe we are well positioned to continue adding utility customers due to lower natural gas prices, a relatively low market penetration rate, our ongoing efforts to convert homes to natural gas, and the potential for environmental initiatives that could favor natural gas use in our region.