UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

_____________________________

FORM 10-K

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES

EXCHANGE ACT OF 1934

For the fiscal year ended May 31, 2013

Commission file number 0-11330

____________________________

Paychex, Inc.

911 Panorama Trail South

Rochester, New York 14625-2396

(585) 385-6666

A Delaware Corporation

IRS Employer Identification Number: 16-1124166

Securities registered pursuant to Section 12(b) of the Act: | Common Stock, $0.01 Par Value | |

Name of exchange on which registered: | NASDAQ Global Select Market | |

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes þ No ¨

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No þ

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes þ No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes þ No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. þ

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer þ | Accelerated filer ¨ | Non-accelerated filer o | Smaller reporting company o | |||

(Do not check if a smaller reporting company) | ||||||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ¨ No þ

As of November 30, 2012, the last business day of the most recently completed second fiscal quarter, shares held by non-affiliates of the registrant had an aggregate market value of $10,580,591,534 based on the closing price reported for such date on the NASDAQ Global Select Market.

As of June 30, 2013, 365,531,897 shares of the registrant’s common stock, $.01 par value, were outstanding.

Documents Incorporated by Reference

Portions of the registrant’s definitive proxy statement to be issued in connection with its Annual Meeting of Stockholders to be held on or about October 16, 2013, to the extent not set forth herein, are incorporated by reference into Part III, Items 10 through 14, inclusive.

PAYCHEX, INC.

INDEX TO FORM 10-K

For the fiscal year ended May 31, 2013

Description | Page | ||

PART I | |||

Cautionary Note Regarding Forward-Looking Statements Pursuant to the United States Private Securities Litigation Reform Act of 1995 | 1 | ||

Item 1 | Business | 2 | |

Item 1A | Risk Factors | 7 | |

Item 1B | Unresolved Staff Comments | 9 | |

Item 2 | Properties | 10 | |

Item 3 | Legal Proceedings | 10 | |

Item 4 | Mine Safety Disclosures | 10 | |

PART II | |||

Item 5 | Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities | 10 | |

Item 6 | Selected Financial Data | 12 | |

Item 7 | Management’s Discussion and Analysis of Financial Condition and Results of Operations | 13 | |

Item 7A | Quantitative and Qualitative Disclosures About Market Risk | 25 | |

Item 8 | Financial Statements and Supplementary Data | 27 | |

Item 9 | Changes in and Disagreements with Accountants on Accounting and Financial Disclosure | 54 | |

Item 9A | Controls and Procedures | 54 | |

Item 9B | Other Information | 55 | |

PART III | |||

Item 10 | Directors, Executive Officers and Corporate Governance | 55 | |

Item 11 | Executive Compensation | 56 | |

Item 12 | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | 56 | |

Item 13 | Certain Relationships and Related Transactions, and Director Independence | 57 | |

Item 14 | Principal Accounting Fees and Services | 57 | |

PART IV | |||

Item 15 | Exhibits and Financial Statement Schedules | 57 | |

Signatures | 60 | ||

i

PART I

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS PURSUANT TO THE UNITED STATES PRIVATE SECURITIES LITIGATION REFORM ACT OF 1995

Certain written and oral statements made by management of Paychex, Inc. and its wholly owned subsidiaries (“we,” “our,” “us,” “Paychex,” or the “Company”) may constitute “forward-looking statements” within the meaning of the safe harbor provisions of the United States (“U.S.”) Private Securities Litigation Reform Act of 1995. Forward-looking statements can be identified by such words and phrases as “we expect,” “expected to,” “estimates,” “estimated,” “current outlook,” “we look forward to,” “would equate to,” “projects,” “projections,” “projected to be,” “anticipates,” “anticipated,” “we believe,” “could be,” and other similar phrases. Examples of forward-looking statements include, among others, statements we make regarding operating performance, events, or developments that we expect or anticipate will occur in the future, including statements relating to revenue growth, earnings, earnings-per-share growth, or similar projections.

Forward-looking statements are neither historical facts nor assurances of future performance. Instead, they are based only on our current beliefs, expectations, and assumptions regarding the future of our business, future plans and strategies, projections, anticipated events and trends, the economy, and other future conditions. Because forward-looking statements relate to the future, they are subject to inherent uncertainties, risks, and changes in circumstances that are difficult to predict, many of which are outside our control. Our actual results and financial conditions may differ materially from those indicated in the forward-looking statements. Therefore, you should not place undue reliance upon any of these forward-looking statements. Important factors that could cause our actual results and financial condition to differ materially from those indicated in the forward-looking statements include, among others, the following:

• | general market and economic conditions including, among others, changes in U.S. employment and wage levels, changes to new hiring trends, legislative changes to stimulate the economy, changes in short- and long-term interest rates, changes in the fair value and the credit rating of securities held by us, and accessibility of financing; |

• | changes in demand for our services and products, ability to develop and market new services and products effectively, pricing changes and the impact of competition; |

• | changes in the availability of skilled workers; |

• | changes in the laws regulating collection and payment of payroll taxes, professional employer organizations, and employee benefits, including retirement plans, workers’ compensation, health insurance, state unemployment, and section 125 plans; |

• | changes in health insurance and workers’ compensation rates and underlying claims trends; |

• | changes in technology that adversely affect our products and services and impact our ability to provide timely enhancements to services and products; |

• | the possibility of a security breach that disrupts operations or exposes client confidential data; |

• | the possibility of failure of our operating facilities, computer systems, and communication systems during a catastrophic event; |

• | the possibility of third-party service providers failing to perform their functions; |

• | the possibility of a failure of internal controls or our inability to implement business processing improvements; |

• | the possibility that we may be subject to liability for violations of employment or discrimination laws by our clients and acts or omissions of client employees who may be deemed to be our agents, even if we do not participate in any such acts or violations; and |

• | potentially unfavorable outcomes related to pending legal matters. |

Any of these factors, as well as such other factors as discussed in Part I, Item 1A Risk Factors and throughout Part II, Item 7 Management’s Discussion and Analysis of Financial Condition and Results of Operations of this Annual Report on Form 10-K (“Form 10-K”), as well as in our periodic filings with the Securities and Exchange Commission (“SEC” or “Commission”), could cause our actual results to differ materially from our anticipated results. The information provided in this Form 10-K is based upon the facts and circumstances known at this time, and any forward-looking statement made by us in this Form 10-K speaks only as of the date on which it is made. Except as required by law, we undertake no obligation to update these forward-looking statements after the date of filing of this Form 10-K with the SEC to reflect events or circumstances after such date, or to reflect the occurrence of unanticipated events.

1

Item 1. | Business |

We are a leading provider of payroll, human resource, insurance, and benefits outsourcing solutions for small- to medium-sized businesses. As of May 31, 2013, we serviced approximately 570,000 clients, including approximately 2,000 clients through four offices in Germany. We maintain our corporate headquarters in Rochester, New York, and have more than 100 offices nationwide.

Our company was formed as a Delaware corporation in 1979. We report our results of operations and financial condition as one business segment. Our fiscal year ends May 31st.

Company Strategy

We are focused on achieving strong, long-term financial performance by:

• | providing high-quality, timely, accurate, and affordable comprehensive payroll and integrated human resource services; |

• | delivering these services utilizing a well-trained and responsive work force through a network of local and corporate offices servicing more than 100 of the largest markets in the U.S., and in Germany; |

• | growing our client base, primarily through the efforts of our direct sales force, along with other marketing channels such as accountants, banks, national associations and franchise organizations, and search engine marketing; |

• | continually improving client service, through leveraging our leading-edge technology, to maximize client retention; |

• | capitalizing on the growth opportunities within our existing client base and from new clients by increasing utilization of our payroll and human resource ancillary services and products; |

• | investing in our business through expansion of our service and product offerings to continually add value for our clients; and |

• | supplementing our growth through strategic acquisitions when appropriate opportunities arise. |

Services and Products

We offer a comprehensive portfolio of services and products that allow our clients to meet their diverse payroll and human resource needs. These include:

• | payroll processing; |

• | payroll tax administration services; |

• | employee payment services; |

• | regulatory compliance services (new-hire reporting and garnishment processing); |

• | Paychex HR Solutions; |

• | retirement services administration; |

• | insurance services; |

• | eServices; and |

• | other human resource services and products. |

By offering ancillary services that leverage the information gathered in the base payroll processing service, we are able to provide comprehensive outsourcing services that allow employers to expand their employee benefits offerings at an affordable cost. We mainly earn our revenue through recurring fees for services performed. Service revenue is primarily driven by the number of clients, checks or transactions per client per pay period, and utilization of ancillary services.

At Paychex, innovative technology meets superior customer service. The integration of service and technology allows us to meet our clients' diverse needs by providing them information and products when, where, and how they want it. Our Software-as-a-Service ("SaaS") solutions, operating in the cloud, allow us to offer such versatility. Our Paychex Mobile Applications add greater value and convenience for our clients and their employees by allowing them instant access and increased productivity. Our mobile apps are available for iPad® and AndroidTM tablets and smartphones, and allow our clients and their employees to have full access to our products, offering diverse capabilities for both the employer and employee. During the fiscal year ended

2

May 31, 2013 ("fiscal 2013"), we introduced an industry-leading, web-based report center and robust report writer. This provides a one-stop shop for standard or on-demand reporting needs, ad-hoc and customized reporting, data-extract templates, and more.

We are integrating our leading-edge technology and mobility platform with our world class customer service through the Paychex Next Generation suite of innovative products. This technology creates an integrated workforce management tool for our clients by bringing together the services those clients need, including our payroll products and various human resource and employee benefit management services.

Payroll

Payroll processing is the foundation of our service portfolio. Our payroll service includes the calculation, preparation, and delivery of employee payroll checks; production of internal accounting records and management reports; preparation of federal, state, and local payroll tax returns; and collection and remittance of clients’ payroll obligations. Our payroll services support the small business market through our core payroll and SurePayroll, Inc. ("SurePayroll") products. Our core payroll clients can opt for our full-service customer service model through our branch operations or use Paychex Online, our secure Internet portal, which offers a suite of self-service, interactive services twenty-four hours a day, seven days a week. These services include Paychex Online Payroll®, Internet Time Sheet, Paychex Online Reports, and General Ledger Reporting Service. Using these services, clients can communicate payroll information, access current and historical payroll information, and transfer payroll information calculated by us to their general ledger accounting software, eliminating manual entries and improving the accuracy of bookkeeping. In addition, our SurePayroll SaaS solution offers "do-it-yourself," self-service and mobile applications for small business.

Mid-market companies typically have more sophisticated payroll and benefits needs, and are primarily serviced through our Major Market Services ("MMS") payroll product. We offer a SaaS solution to meet the payroll and human resource administrative needs of our MMS clients. This allows our mid-market payroll product to be integrated with various Internet-based services offered to assist clients with their administrative human resource and payroll needs through every step of the employee life cycle. Ancillary services particularly beneficial to our MMS clients include the following:

• | Paychex HR Online, our Internet-based human resource management system, offers powerful tools for managing employee benefits, personnel information, and critical human resource compliance and reporting needs. In addition, its self-service features allow for better communication between management and employees. |

• | BeneTrac, our employee benefits management and administration system, provides our clients a simple, accurate, and cost-effective solution for streamlined benefits management. |

• | Paychex Time and Labor Online makes the time and attendance process more efficient. This solution can reduce time spent on preparing timesheets, minimize redundant data entry, increase awareness of critical labor information, and aid in compliance with federal time recording requirements. |

• | Paychex Expense Manager is an integrated expense management solution that allows clients to control discretionary spending while giving employees an easy-to-use, secure tool to prepare and submit expense reports online. |

• | Applicant tracking provides our clients with a tool to manage their recruiting process in order to better hire and retain talented employees. |

MMS clients can select Paychex One-Source Solutions, which seamlessly integrates our mid-market payroll product, Paychex Time and Labor Online, and Paychex HR Online applications through a single, web-based client portal. MMS clients also have the option to select from a number of á la carte payroll and human resource ancillary services or opt for our comprehensive human resource and payroll outsourcing solution, Paychex HR Solutions. This flexibility allows our clients to define the solution that best meets their particular needs.

Payroll tax administration services: Our payroll tax administration services (including Taxpay®) provide accurate preparation and timely filing of quarterly and year-end tax returns, as well as the electronic transfer of funds to the applicable tax or regulatory agencies (federal, state, and local). In connection with these services, we electronically collect payroll taxes from clients’ bank accounts, typically on payday, prepare and file the applicable tax returns, and remit taxes to the applicable tax or regulatory agencies on the respective due dates. These taxes are typically paid between one and 30 days after receipt of collections from clients, with some items extending to 90 days. We handle regulatory correspondence, amendments, and penalty and interest disputes, and we are subject to cash penalties imposed by tax or regulatory agencies for late filings and late or under payment of taxes.

Employee payment services: Our employee payment services provide the employer the option of paying their employees by direct deposit, payroll debit card, a check drawn on a Paychex account (Readychex®), or a check drawn on the employer’s

3

account and electronically signed by us. For the first three methods, we electronically collect net payroll from the clients’ bank accounts, typically one business day before payday, and provide payment to the employees on payday. Our Readychex service provides a cost-effective solution that offers the benefit of convenient, one-step payroll account reconciliation for employers.

Regulatory compliance services: We offer new-hire reporting services, which enable clients to comply with federal and state requirements to report information on newly hired employees. This information aids the government in enforcing child support orders and minimizes fraudulent unemployment and workers’ compensation insurance claims. Our garnishment processing service provides deductions from employees’ pay, forwards payments to third-party agencies, including those that require electronic payments, and tracks the obligations to fulfillment. These services enable employers to comply with legal requirements and reduce the risk of penalties.

Human Resource Services

Paychex HR Solutions: We offer comprehensive human resource outsourcing solutions that provide businesses a full-service approach to the outsourcing of employer and employee administrative needs. Our Paychex HR Solutions offering is available as an administrative services organization (“ASO”) and a professional employer organization (“PEO”). Both options offer businesses a combined package of services that includes payroll, employer compliance, human resource and employee benefits administration, risk management outsourcing, and the on-site availability of a professionally trained human resource representative. These comprehensive bundles of services are designed to make it easier for businesses to manage their payroll and related benefit costs while providing a benefits package equal to that of larger companies. Our PEO differs from the ASO in that we serve as a co-employer of the clients’ employees, assume the risks and rewards of workers’ compensation insurance, and provide health care coverage to PEO client employees. PEO services are sold through our registered and licensed subsidiary, Paychex Business Solutions, Inc. The integration of the sales and service models of the ASO and PEO under Paychex HR Solutions has reduced redundancies and created more flexible options for business owners to find the solution that best meets their needs. We also offer Paychex HR Essentials, which is an ASO product that provides support to our clients over the phone or online to help manage employee-related topics. As of May 31, 2013, Paychex HR Solutions was utilized by 25,000 clients with approximately 672,000 client employees.

Retirement services administration: Our retirement services product line offers a variety of options to clients, including 401(k) plans, 401(k) SIMPLE plans, SIMPLE IRAs, 401(k) plans with safe harbor provisions, profit sharing plans, and money purchase plans. These services provide plan implementation, ongoing compliance with government regulations, employee and employer reporting, participant and employer online access, electronic funds transfer, and other administrative services. Auto enrollment is an optional plan feature that allows employers to automatically enroll employees in their company’s 401(k) plan and increase overall plan participation. Clients have the ability to choose from a group of pre-defined fund selections or to customize their investment options within their plan. We are one of the largest 401(k) recordkeepers for small businesses in the U.S. For fiscal 2013 and the fiscal year ended May 31, 2012 ("fiscal 2012"), we earned an average fee of approximately twenty to twenty-five basis points from the external fund managers based on the total asset value of participants' funds. In May 2011, we acquired ePlan Services, Inc., a provider of recordkeeping and administrative solutions to the defined contribution marketplace. This acquisition allowed us to expand our retirement services to financial advisors. As of May 31, 2013, retirement services covered approximately 62,000 plans and the asset value of participants' funds externally managed totaled approximately $19.3 billion.

Insurance services: Our licensed insurance agency, Paychex Insurance Agency, Inc. (“PIA”), provides insurance through a variety of carriers. Insurance offerings include property and casualty coverage such as workers’ compensation, business-owner policies, commercial auto, and health and benefits coverage, including health, dental, vision, and life. Our insurance services simplify the insurance process to make it easy to find plans with the features and affordability to meet the client’s needs. With access to numerous top national and regional insurance carriers, our professional insurance agents enjoy a wide selection of plans from which they can best match the insurance needs of small businesses. Additionally, clients have the option to integrate their insurance plans with Paychex payroll processing for easy, accurate plan administration. PIA has a website, www.paychexinsurance.com, with information and interactive tools to help educate visitors on insurance and aid in making business insurance decisions. As of May 31, 2013, approximately 108,000 clients have appointed PIA as their agent for servicing their business insurance needs.

eServices: We offer online human resource administration software products for employee benefits management and administration and time and attendance solutions. Paychex HR Online offers powerful tools for managing employee benefits, personnel information, and human resource compliance and reporting. Time and Labor Online helps minimize the time spent compiling time sheet information. It allows the employer to handle multiple payroll scenarios and results in improved productivity, accuracy, and reliability in the payroll process. In fiscal 2013, we expanded our eServices product line through two acquisitions in the areas of expense reporting and applicant tracking. The expense reporting solution is a web-based solution that provides

4

clients with tools to manage and control the expense reporting process. The applicant tracking suite provides technology that streamlines, simplifies, and drives the applicant workflow and hiring process for companies of all sizes.

Other human resource services and products: We offer the outsourcing of plan administration under section 125 of the Internal Revenue Code, allowing employees to use pre-tax dollars to pay for certain health insurance benefits and health and dependent care expenses not covered by insurance. All required implementation, administration, compliance, claims processing and reimbursement, and coverage tests are provided with these services. We offer state unemployment insurance services, which provide clients with prompt processing for all claims, appeals, determinations, change statements, and requests for separation documents. Other Human Resource Services products include employee handbooks, management manuals, and personnel and required regulatory forms. These products are designed to simplify clients’ office processes and enhance their employee benefits programs.

Sales and Marketing

We market our services primarily through our direct sales force based in the metropolitan markets we serve, with sales representatives specializing within our portfolio of services. Our sales representatives are also supported by marketing, advertising, public relations, trade shows, and telemarketing programs. In recent years, we have increased our emphasis on the selling of ancillary services and products to both new clients and our existing client base.

In fiscal 2013, we added new territories and focused on market segmentation in payroll and retirement services. Within payroll, we differentiate the markets we serve between the small business market and mid-market companies. Within retirement services, we expanded our sales efforts by creating a dedicated, wholesale sales force focused solely on enhancing our relationships with financial advisors.

In addition to our direct selling and marketing efforts, we utilize relationships with existing clients, certified public accountants (“CPAs”), and banks for new client referrals. Approximately 60% of our new core payroll clients (excluding business acquisitions) come from these referral sources.

We recently celebrated the ten year anniversary of our partnership with the American Institute of Certified Public Accountants (“AICPA”) as the preferred payroll provider for its AICPA Business SolutionsTM Program. More than half of the CPA firms in the U.S. are enrolled and actively participating in the Paychex Partner Program from AICPA Business Solutions. Our current partnership agreement with the AICPA is in place through September 2016. We enhanced our relationships with CPAs by partnering with various state CPA society organizations. In addition, we recently created a dedicated business development group to drive sales in the banking and franchise channels.

Our website available at www.paychex.com, which includes online payroll sales presentations and service and product information, is a cost-efficient tool that serves as a source of leads and new sales, while complementing the efforts of our direct sales force. This online tool allows us to market to clients and prospective clients in other geographical areas where we do not have a direct sales presence. In addition, our insurance services website available at www.paychexinsurance.com provides information to help small businesses navigate the insurance industry, and generates leads by allowing interested parties to get in contact with one of our professional insurance agents.

In addition, Advantage Payroll Services Inc. (“Advantage”), a wholly owned subsidiary of Paychex, Inc., has license agreements with independently owned associate offices (“Associates”), which are responsible for selling and marketing Advantage payroll services and performing certain operational functions, while Paychex and Advantage provide all centralized back-office payroll processing and payroll tax administration services. The marketing and selling by the Associates is conducted under their own logos.

Paychex also builds on its reputation as an expert in the payroll and human resources industry by providing education and assistance to clients and other interested parties. We provide free webinars, white papers, and other information on our website to aid existing and prospective clients with the impact of regulatory changes. We track current regulatory issues that impact the small business community and provide a monthly regulatory update. Our newly redesigned Paychex Accountant Knowledge Center is a free online resource available through our website that brings valuable information and time-saving online tools to accounting professionals. During fiscal 2013, in an effort to help entrepreneurs and small-business owners achieve success, we launched a new and improved website, BuildMyBiz.com, that provides tools and resources for starting, growing, and managing a business.

A section of both the Paychex website, www.paychex.com, and our insurance services website, www.paychexinsurance.com, is designated to the topic of health care reform to provide answers, information, and solutions that employers need to prepare for and take action relating to the Patient Protection and Affordable Care Act of 2010 ("PPACA") and the Health Care and Education

5

Reconciliation Act of 2010. Paychex is positioned to assist our clients and their employees as they navigate the complexity of this legislation.

Markets and Competition

We remain focused on servicing small- to medium-sized businesses based upon the growth potential that we believe exists in the markets we serve. Industry data indicates there are approximately 12 million businesses in the geographic markets that we currently serve within the U.S. Of those businesses, greater than 99% have fewer than 100 employees and are our primary customers and target market.

We serve a diverse base of small- to medium-sized clients operating in a broad range of industries located throughout the U.S. and in Germany. We utilize service agreements and arrangements with clients that are generally terminable by the client at any time or upon relatively short notice. For fiscal 2013, client retention reached record levels, in excess of 81% of our beginning client base. No single client has a material impact on total service revenue or results of operations.

The composition of the U.S. market and the client base we serve by number of employees is as follows:

Business size (Number of employees) | Estimated market distribution(1) | Paychex, Inc. distribution of client base | ||

1-4 | 83% | 42% | ||

5-19 | 13% | 40% | ||

20-49 | 3% | 12% | ||

50-99 | 1% | 4% | ||

100+ | —% | 2% | ||

(1) | Based on current available market data from Dun & Bradstreet. |

The market for payroll processing and human resource services is highly competitive and fragmented. We have one primary national competitor and we also compete with other national, regional, local, and online service providers, all of which we believe have significantly smaller client bases than us.

In addition to traditional payroll processing and human resource service providers, we compete with in-house payroll and human resource systems and departments. Payroll and human resource systems and software are sold by many vendors. Our Human Resource Services also compete with a variety of providers of human resource services, such as retirement services companies, insurance companies, and human resources and benefits consulting firms.

Competition in the payroll processing and human resource services industry is primarily based on service responsiveness; product quality and reputation, including ease of use and accessibility of technology; breadth of service and product offering; and price. We believe we are competitive in each of these areas.

Software Maintenance and Development

The ever-changing mandates of federal, state, and local tax and regulatory agencies require us to regularly update the proprietary software we utilize to provide payroll and human resource services to our clients. We are continually engaged in developing enhancements to and the maintenance of our various software platforms to meet the changing requirements of our clients and the marketplace.

We continue to enhance our Paychex Next Generation platform, with its suite of innovative products, as we believe it is a key building block to our future success. We also continue to add more capabilities to our mobility applications.

Employees

As of May 31, 2013, we employed approximately 12,400 people. None of our employees were covered by collective bargaining agreements.

6

Intellectual Property

We own or license and use a number of trademarks, trade names, copyrights, service marks, trade secrets, computer programs and software, and other intellectual property rights. Taken as a whole, our intellectual property rights are material to the conduct of our business. Where it is determined to be appropriate, we take measures to protect our intellectual property rights, including, but not limited to, confidentiality/non-disclosure agreements or policies with employees, vendors, and others; license agreements with licensees and licensors of intellectual property; and registration of certain trademarks. We believe that the “Paychex” name, trademark, and logo are of material importance to us.

Seasonality

There is no significant seasonality to our business. However, during our third fiscal quarter, which ends in February, the number of new payroll clients, new retirement services clients, and new Paychex HR Solutions worksite employees tends to be higher than during the rest of the fiscal year, primarily because many new clients prefer to start using our services at the beginning of a calendar year. In addition, calendar year-end transaction processing and client funds activity are traditionally higher during our third fiscal quarter due to clients paying year-end bonuses and requesting additional year-end services. Historically, as a result of these factors, our total revenue has been slightly higher in our third fiscal quarter, with greater sales commission expenses also reported in the third quarter.

Other

We are subject to the informational and reporting requirements of the Securities Exchange Act of 1934, as amended (the “Exchange Act”). Therefore, we file periodic reports, proxy statements, and other information with the SEC. Such reports may be read and copied at the SEC’s Public Reference Room at 100 F Street NE, Washington, D.C. 20549. Information regarding the operation of the Public Reference Room may be obtained by calling the SEC at (800) SEC-0330. The SEC also maintains a website (www.sec.gov) that includes our reports, proxy statements, and other information.

Information about our services and products, stockholder information, press releases, and filings with the SEC can be found on our website at www.paychex.com. Our Form 10-Ks, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K, and other SEC filings, as well as any amendments to such reports and filings, are made available, free of charge, on our website. You can access them under the Corporate tab on the Investor Relations section of our website. They are made available as soon as reasonably practical after such material is filed or furnished pursuant to Section 13(a) or 15(d) of the Exchange Act to the SEC. Also, copies of our Annual Report to Stockholders and Proxy Statement, to be issued in connection with our 2013 Annual Meeting of Stockholders, will be made available, free of charge, upon written request submitted to Paychex, Inc., c/o Corporate Secretary, 911 Panorama Trail South, Rochester, New York 14625-2396.

Item 1A. | Risk Factors |

Our future results of operations are subject to a number of risks and uncertainties. These risks and uncertainties could cause actual results to differ materially from historical and current results, and from our projections. The risk factors described below represent our current view of some of the most important risks facing our business and are important to understanding our business. The risks described below are not the only risks we face. Additional factors not presently known to us or that we currently deem to be immaterial also may adversely affect, to a material extent, our business, cash flows, financial condition, or results of operations in future periods. In addition, you should refer to the description of forward-looking statements at the beginning of Part I of this Form 10-K.

Our services may be adversely impacted by changes in government regulations and policies: Many of our services, particularly payroll tax administration services and employee benefit plan administration services, are designed according to government regulations that continually change. Changes in regulations could affect the extent and type of benefits employers are required, or may choose, to provide employees or the amount and type of taxes employers and employees are required to pay. Such changes could reduce or eliminate the need for some of our services and substantially decrease our revenue. Added requirements could also increase our cost of doing business. Failure to educate and assist our clients regarding new or revised legislation that impacts them could have an adverse impact on our reputation. Failure by us to modify our services in a timely fashion in response to regulatory changes could have a material adverse effect on our business and results of operations.

Our clients and our business could be adversely impacted by health care reform: The PPACA was enacted on March 23, 2010 and was subsequently modified by the Health Care and Education Reconciliation Act of 2010 on March 30, 2010 (together with PPACA hereafter referred to as the “Act”). The Act entails sweeping health care reforms with staggered effective dates from

7

2010 through 2018, and many provisions of the Act require the issuance of additional guidance from the U.S. Departments of Labor and Heath & Human Services, the Internal Revenue Service (the “IRS”), and the states.

The complexity of federal and state regulations facing employers has continued to increase over time, including the enactment of the Act. As a service provider, we have a responsibility to our clients to help them understand these increased regulations. Failure to provide clients with appropriate information or solutions to effectively manage their health care benefits and related costs could have an adverse impact on our reputation and a negative impact on our client base. There is no guarantee that solutions we have developed to help clients navigate health care legislation will be readily accepted by clients, which could have a material adverse impact on our insurance services business. Insurance services revenue is at risk for lower commission revenue from underwriters if clients move away from traditional insurance policies utilized in the past or as a result of pressure on commission rates, driven by restrictions on insurers as to use of premiums. Refer to the discussion below regarding changes in health insurance and workers' compensation insurance rates and underlying claims trends for discussion of health care reform as it impacts our PEO.

We may not be able to keep pace with changes in technology or provide timely enhancements to our products and services: To maintain our growth strategy, we must adapt and respond to technological advances and technological requirements of our clients. Our future success will depend on our ability to enhance capabilities and increase the performance of our internal use systems, particularly our systems that meet our clients’ requirements. We continue to make significant investments related to the development of new technology. If our systems become outdated, we may be at a disadvantage when competing in our industry. There can be no assurance that our efforts to update and integrate systems will be successful. If we do not integrate and update our systems in a timely manner, or if our investments in technology fail to provide the expected results, there could be a material adverse effect to our business and results of operations.

Our business and reputation may be affected by security breaches and other disruptions to our information technology infrastructure, which could compromise Company and personal customer information: We rely upon information technology networks and systems to process, transmit, and store electronic information, and to support a variety of business processes. If we experience a problem with the functioning of key systems or a security breach of our systems, the resulting disruptions could have a material adverse effect on our business.

We also collect, use, and retain large amounts of personal information about our clients and their employees that is critical to the accurate and timely provision of services to our clients. This information includes bank account numbers, credit card numbers, tax return information, social security numbers, health care information, retirement account information, payroll information, and Paychex system passwords. In addition, we also collect and maintain personal information on our employees in the ordinary course of our business. As many of our services are web-based and mobile-application-based, the amount of data we store for our users on our servers has been increasing. Vulnerabilities, threats, and more sophisticated and targeted computer crime pose a risk to the security of our systems and networks, and the confidentiality, availability, and integrity of our data. We have security systems and information technology infrastructure in place designed to detect and protect against unauthorized access to such information. However, there is no guarantee that our systems and processes are adequate to protect against all security breaches. Third parties, including vendors that provide services for our operations, could also be a source of security risk to us in the event of a failure of their own security systems and infrastructure.

If our systems are disrupted or fail for any reason, or if our systems are infiltrated by unauthorized persons, both the Company and our clients could experience data loss, financial loss, harm to reputation, or significant business interruption. We may be required to incur significant costs to protect against damage caused by disruptions or security breaches in the future. Such events may expose us to unexpected liability, litigation, regulatory investigation and penalties, loss of clients’ business, unfavorable impact to business reputation, and there could be a material adverse effect on our business and results of operations.

In the event of a catastrophe, our business continuity plan may fail, which could result in the loss of client data and adversely interrupt operations: Our operations are dependent on our ability to protect our infrastructure against damage from catastrophe or natural disaster, severe weather including events resulting from climate change, unauthorized security breach, power loss, telecommunications failure, terrorist attack, or other events that could have a significant disruptive effect on our operations. We have a business continuity plan in place in the event of system failure due to any of these events. Our business continuity plan has been tested in the past by circumstances of severe weather, including hurricanes, floods, and snowstorms, and has been successful. However, these past successes are not an indicator of success in the future. If the business continuity plan is unsuccessful in a disaster recovery scenario, we could potentially lose client data or experience material adverse interruptions to our operations or delivery of services to our clients.

We may be adversely impacted by any failure of third-party service providers to perform their functions: As part of providing services to clients, we rely on a number of third-party service providers. These service providers include, but are not limited to, couriers used to deliver client payroll checks and banks used to electronically transfer funds from clients to their

8

employees. Failure by these service providers, for any reason, to deliver their services in a timely manner could result in material interruptions to our operations, impact client relations, and result in significant penalties or liabilities to us.

We may be exposed to additional risks related to our co-employment relationship within our PEO business: Many federal and state laws that apply to the employer-employee relationship do not specifically address the obligations and responsibilities of the “co-employment” relationship. As a result, there is a possibility that we may be subject to liability for violations of employment or discrimination laws by our clients and acts or omissions of client employees, who may be deemed to be our agents, even if we do not participate in any such acts or violations. Although our agreements with the clients provide that the client will indemnify us for any liability attributable to its own or its employees’ conduct, we may not be able to effectively enforce or collect such contractual obligations. In addition, we could be subject to liabilities with respect to our employee benefit plans if it were determined that we are not the “employer” under any applicable state or federal laws.

We may be adversely impacted by changes in health insurance and workers’ compensation rates and underlying claims trends: Within our PEO business, we maintain health and workers’ compensation insurance covering worksite employees. The insurance costs are impacted by claims experience and are a significant portion of our PEO direct costs. If we experience a sudden or unexpected increase in claims activity, our costs could increase. In addition, in the event of expiration or cancellation of existing contracts, we may not be able to secure replacement contracts on competitive terms. Also, as a co-employer in the PEO, we assume or share many of the employer-related responsibilities associated with health care reform, which may result in increased costs. Increases in costs not incorporated into service fees timely or fully, could have a material adverse effect on our results of operations. Incorporating cost increases into service fees could also impact our ability to attract and retain clients.

Our interest earned on funds held for clients may be impacted by changes in government regulations mandating the amount of tax withheld or timing of remittance: We receive interest income from investing client funds collected but not yet remitted to applicable tax or regulatory agencies or to client employees. A change in regulations either decreasing the amount of taxes to be withheld or allowing less time to remit taxes to applicable tax or regulatory agencies would adversely impact this interest income.

We may be adversely impacted by volatility in the financial and economic environment: During periods of weak economic conditions, employment levels tend to decrease and interest rates may become more volatile. These conditions may impact our business due to lower transaction volumes or an increase in the number of clients going out of business. Current or potential clients may decide to reduce their spending on payroll and other outsourcing services. In addition, new business formation may be affected by an inability to obtain credit. The interest we earn on funds held for clients may decrease as a result of a decline in funds available to invest and lower interest rates. In addition, during periods of volatility in the credit markets, certain types of investments may not be available to us or may become too risky for us to invest in, further reducing the interest we may earn on client funds. Constriction in the credit markets may impact the availability of financing, even to borrowers with the highest credit ratings. We historically have not borrowed against available credit arrangements to meet liquidity needs. However, should we require additional short-term liquidity during days of large outflows of client funds, a credit constriction may limit our ability to access those funds or the flexibility to obtain them at interest rates that would be acceptable to us. If all of these financial and economic circumstances were to remain in effect for an extended period of time, there could be a material adverse effect on our results of operations.

Quantitative and qualitative disclosures about market risk: Refer to Item 7A of this Form 10-K for a discussion on Market Risk Factors, which would could have a material adverse effect on our business and results of operations.

Item 1B. | Unresolved Staff Comments |

None.

9

Item 2. | Properties |

We owned and leased the following properties as of May 31, 2013:

Square feet | ||

Owned facilities: | ||

Rochester, New York | 721,000 | |

Other U.S. locations | 65,000 | |

Total owned facilities | 786,000 | |

Leased facilities: | ||

Rochester, New York | 134,000 | |

Other U.S. locations | 2,084,000 | |

Germany | 1,000 | |

Total leased facilities | 2,219,000 | |

Our facilities in Rochester, New York house various distribution, processing, and technology functions; certain ancillary functions; a telemarketing unit; and other back-office functions. Facilities outside of Rochester, New York are at various locations throughout the U.S. and Germany and house our regional, branch, and sales offices and data processing centers. These locations are concentrated in metropolitan areas. We believe that adequate, suitable lease space will continue to be available to meet our needs.

Item 3. | Legal Proceedings |

We are subject to various claims and legal matters that arise in the normal course of our business. These include disputes or potential disputes related to breach of contract, breach of fiduciary duty, employment-related claims, tax claims, and other matters.

Our management currently believes that resolution of outstanding legal matters will not have a material adverse effect on our financial position or results of operations. However, legal matters are subject to inherent uncertainties and there exists the possibility that the ultimate resolution of these matters could have a material adverse impact on the Company’s financial position and the results of operations in the period in which any such effect is recorded.

Item 4. | Mine Safety Disclosures |

Not applicable.

PART II

Item 5. | Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities |

Our common stock trades on the NASDAQ Global Select Market under the symbol “PAYX.” Dividends have historically been paid on our common stock in August, November, February, and May. In fiscal 2013, the dividends that would typically have been paid in February 2013 and May 2013 were accelerated and paid in December 2012. The level and continuation of future dividends are dependent on our future earnings and cash flows, and are subject to the discretion of our Board of Directors (the "Board.")

As of June 30, 2013, there were 14,456 holders of record of our common stock, which includes registered holders and participants in the Paychex, Inc. Dividend Reinvestment and Stock Purchase Plan. There were also 7,222 participants in the Paychex, Inc. Employee Stock Purchase Plan and 5,367 participants in the Paychex, Inc. Employee Stock Ownership Plan.

10

The high and low sale prices for our common stock as reported on the NASDAQ Global Select Market and dividends for fiscal 2013 and fiscal 2012 are as follows:

Fiscal 2013 | Fiscal 2012 | ||||||||||||

Sales Prices | Cash dividends declared per share | Sales prices | Cash dividends declared per share | ||||||||||

High | Low | High | Low | ||||||||||

First quarter | $33.44 | $29.12 | $0.32 | $32.27 | $25.12 | $0.31 | |||||||

Second quarter | $34.70 | $31.27 | $0.33 | $30.12 | $25.20 | $0.32 | |||||||

Third quarter | $34.06 | $30.55 | $0.66 | $32.73 | $28.76 | $0.32 | |||||||

Fourth quarter | $38.66 | $32.73 | — | $32.24 | $29.12 | $0.32 | |||||||

The closing price of our common stock as of May 31, 2013, as reported on the NASDAQ Global Select Market, was $37.23 per share.

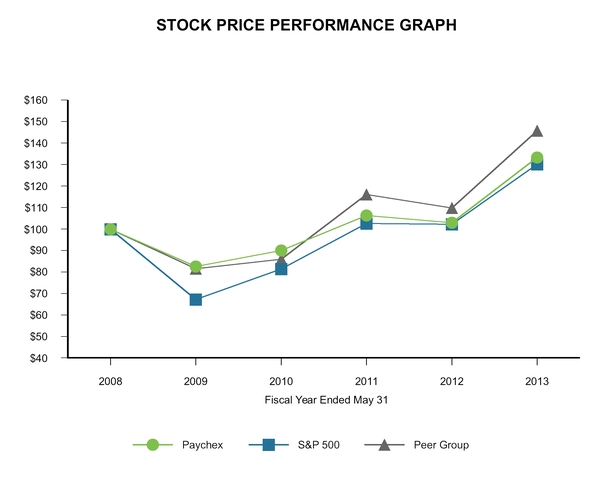

The following graph shows a five-year comparison of the total cumulative returns of investing $100 on May 31, 2008, in Paychex common stock, the S&P 500 Index, and a Peer Group Index. All comparisons of stock price performance shown assume reinvestment of dividends. We are a participant in the S&P 500 Index, a market group of companies with a larger than average market capitalization. Our Peer Group is a group of companies with comparable revenue and net income, who are in a comparable industry, or who are direct competitors of Paychex (as detailed on the next page).

11

May 31, | 2008 | 2009 | 2010 | 2011 | 2012 | 2013 | ||||||

Paychex | $100.00 | $82.72 | $90.17 | $106.43 | $103.05 | $133.33 | ||||||

S&P 500 | $100.00 | $67.42 | $81.56 | $102.72 | $102.30 | $130.20 | ||||||

Peer Group | $100.00 | $81.72 | $86.04 | $116.18 | $109.92 | $145.76 | ||||||

There can be no assurance that our stock performance will continue into the future with the same or similar trends depicted in the graph on the previous page. We will neither make nor endorse any predictions as to future stock performance.

Our Peer Group is comprised of the following companies:

Automatic Data Processing, Inc. (direct competitor) | Broadridge Financial Solutions, Inc. | |

Fiserv, Inc. | Robert Half International Inc. | |

The Western Union Company | Intuit Inc. | |

Total Systems Services, Inc. | Iron Mountain Incorporated | |

Global Payments Inc. | Moody’s Corporation | |

The Brink’s Company | H&R Block, Inc. | |

DST System, Inc. | TD AMERITRADE Holding Corporation | |

The Dun & Bradstreet Corporation | ||

Equifax, Inc. was removed from our Peer Group during fiscal 2013. Our Peer Group is utilized primarily for analysis of executive compensation, and the Governance and Compensation Committee of the Board felt that Equifax executive compensation was an outlier in comparison to the Peer Group in its entirety.

Item 6. | Selected Financial Data |

In millions, except per share amounts Year ended May 31, | 2013 (1) | 2012 | 2011 | 2010 (2) | 2009 | |||||||||||||||

Service revenue | $ | 2,285.2 | $ | 2,186.2 | $ | 2,036.2 | $ | 1,945.8 | $ | 2,007.3 | ||||||||||

Interest on funds held for clients | 41.0 | 43.6 | 48.1 | 55.0 | 75.5 | |||||||||||||||

Total revenue | $ | 2,326.2 | $ | 2,229.8 | $ | 2,084.3 | $ | 2,000.8 | $ | 2,082.8 | ||||||||||

Operating income | $ | 904.8 | $ | 853.9 | $ | 786.4 | $ | 724.8 | $ | 805.2 | ||||||||||

Net income | $ | 569.0 | $ | 548.0 | $ | 515.3 | $ | 477.0 | $ | 533.5 | ||||||||||

Diluted earnings per share | $ | 1.56 | $ | 1.51 | $ | 1.42 | $ | 1.32 | $ | 1.48 | ||||||||||

Cash dividends per common share | $ | 1.31 | $ | 1.27 | $ | 1.24 | $ | 1.24 | $ | 1.24 | ||||||||||

Purchases of property and equipment | $ | 98.7 | $ | 89.6 | $ | 100.5 | $ | 61.3 | $ | 64.7 | ||||||||||

Cash and total corporate investments | $ | 874.6 | $ | 790.0 | $ | 671.3 | $ | 656.9 | $ | 574.7 | ||||||||||

Total assets | $ | 6,163.7 | $ | 6,479.6 | $ | 5,393.8 | $ | 5,226.3 | $ | 5,127.4 | ||||||||||

Total debt | $ | — | $ | — | $ | — | $ | — | $ | — | ||||||||||

Stockholders’ equity | $ | 1,773.7 | $ | 1,604.5 | $ | 1,496.2 | $ | 1,402.0 | $ | 1,341.5 | ||||||||||

Return on stockholders’ equity | 34 | % | 34 | % | 35 | % | 34 | % | 41 | % | ||||||||||

(1) | In the fourth quarter of fiscal 2013, the Company increased its tax provision related to the settlement of a state income tax matter. This reduced diluted earnings per share by approximately $0.04 per share. |

(2) | Includes an expense charge of $18.7 million to increase the Rapid Payroll litigation reserve. |

12

Item 7. | Management’s Discussion and Analysis of Financial Condition and Results of Operations |

Management’s Discussion and Analysis of Financial Condition and Results of Operations reviews the operating results of Paychex, Inc. and its wholly owned subsidiaries (“Paychex,” “we,” “our,” or “us”) for each of the three fiscal years ended May 31, 2013 (“fiscal 2013”), May 31, 2012 (“fiscal 2012”), and May 31, 2011 (“fiscal 2011”), and our financial condition as of May 31, 2013. This review should be read in conjunction with the accompanying consolidated financial statements and the related notes to consolidated financial statements contained in Item 8 of this Annual Report on Form 10-K (“Form 10-K”) and the “Risk Factors” discussed in Item 1A of this Form 10-K. Forward-looking statements in this review are qualified by the cautionary statement under the heading “Cautionary Note Regarding Forward-Looking Statements Pursuant to the United States Private Securities Litigation Reform Act of 1995” contained at the beginning of Part I of this Form 10-K.

Overview

We are a leading provider of payroll, human resource, insurance, and benefits outsourcing solutions for small- to medium-sized businesses. Our Payroll and Human Resource Services (“HRS”) offer a portfolio of services and products that allow our clients to meet their diverse payroll and human resource needs. Our payroll services are the foundation of our service portfolio and include:

• | payroll processing; |

• | payroll tax administration services; |

• | employee payment services; and |

• | regulatory compliance services (new-hire reporting and garnishment processing). |

We support small market companies through our core payroll and SurePayroll, Inc. (“SurePayroll”) product lines. Mid-market companies typically have more sophisticated payroll and benefits needs, and are primarily serviced through our Major Market Services (“MMS”). Our software-as-a-service (“SaaS”) solution through our MMS platform provides human resource management, employee benefits management, time and attendance systems, online expense reporting, and applicant tracking.

Our HRS products include:

• | Paychex HR Solutions, under which we offer our administrative services organization (“ASO”) and our professional employer organization (“PEO”). We also offer Paychex HR Essentials, an ASO product that provides support to our clients over the phone or online to help manage employee-related topics; |

• | retirement services administration; |

• | insurance services; |

• | eServices; and |

• | other human resource services and products. |

Our primary goal is to transform the way businesses do business. We strive to achieve this goal by leveraging our industry-leading technology to provide outstanding customer service. Our business strategy is focused on strong long-term financial performance by providing high-quality, timely, accurate, and affordable services; growing our client base; increasing utilization of our ancillary services; leveraging our technology through our service organization; and expanding our product offerings. We continue to focus on driving growth in clients, revenue, and profits. We are managing our personnel costs and expenses while continuing to invest in our business, particularly in leading-edge technology. We believe these investments are critical to our success. Looking to the future, we continue to focus on investing in our products, people, and service capabilities, positioning ourselves to capitalize on opportunities for long-term growth.

Our financial results for fiscal 2013 reflected sustained growth in our business. Checks per payroll and revenue per check continued to show improvement. Checks per payroll grew 1.6% for fiscal 2013, slightly less than the 2.0% growth experienced for fiscal 2012. Our service execution was strong as we achieved our highest levels of customer satisfaction in our history and record levels of client retention.

13

Our financial results continue to be adversely impacted by the interest rate environment as interest rates available on high quality financial instruments remain low. The Federal Funds rate has been at a range of zero to 0.25% since December 2008. Our combined funds held for clients and corporate investment portfolios earned an average rate of return of 1.0% for fiscal 2013, compared to 1.1% for fiscal 2012 and 1.3% for fiscal 2011.

Highlights of our financial results for fiscal 2013, compared to fiscal 2012, are as follows:

• | Payroll service revenue increased 2% to $1.5 billion. |

• | HRS revenue increased 10% to $746.0 million. |

• | Interest on funds held for clients decreased 6% to $41.0 million. |

• | Total revenue increased 4% to $2.3 billion. |

• | Operating income increased 6% to $904.8 million, and operating income, net of certain items, increased 7% to $863.8 million. Refer to the “Non-GAAP Financial Measure” discussion below for further information on operating income, net of certain items. |

• | Net income increased 4% to $569.0 million and diluted earnings per share increased 3% to $1.56 per share. Net income and diluted earnings per share were impacted by the settlement of a state income tax matter, which reduced diluted earnings per share by approximately $0.04 per share. |

• | Dividends of $476.7 million were paid to stockholders, representing 84% of net income. |

Non-GAAP Financial Measure

In addition to reporting operating income, a United States (“U.S.”) generally accepted accounting principle (“GAAP”) measure, we present operating income, net of certain items, which is a non-GAAP measure. We believe operating income, net of certain items, is an appropriate additional measure, as it is an indicator of our core business operations performance period over period. It is also the basis of the measure used internally for establishing the following year’s targets and measuring management’s performance in connection with certain performance-based compensation payments and awards. Operating income, net of certain items, excludes interest on funds held for clients. Interest on funds held for clients is an adjustment to operating income due to the volatility of interest rates, which are not within the control of management. Operating income, net of certain items, is not calculated through the application of GAAP and is not the required form of disclosure by the Securities and Exchange Commission. As such, it should not be considered as a substitute for the GAAP measure of operating income and, therefore, should not be used in isolation, but in conjunction with the GAAP measure. The use of any non-GAAP measure may produce results that vary from the GAAP measure and may not be comparable to a similarly defined non-GAAP measure used by other companies.

Business Outlook

Our client base totaled approximately 570,000 clients as of May 31, 2013, compared to approximately 567,000 clients as of May 31, 2012, and approximately 564,000 clients as of May 31, 2011. Our client base increased approximately 1% for fiscal 2013, compared to approximately 1% for fiscal 2012 and approximately 5% (1% decline on an organic basis) for fiscal 2011.

For fiscal 2013, payroll services client retention was at record levels, exceeding 81% of our beginning client base. We received the highest client satisfaction results in our history, which we believe is a result of our focus on providing high-quality service to our customers utilizing leading-edge technology to maximize client retention.

Our ancillary services provide services to employers and employees beyond payroll, but effectively leverage payroll processing data and, therefore, are beneficial to our operating margin. eServices ancillary services are often included as part of the SaaS solutions for mid-market clients. The following statistics demonstrate the growth in certain of our HRS ancillary service offerings:

Balance at May 31, 2013 | Growth rates for fiscal year | ||||||||||||

2013 | 2012 | 2011 | |||||||||||

Paychex HR Solutions client employees served | 672,000 | 9 | % | 8 | % | 12 | % | ||||||

Paychex HR Solutions clients | 25,000 | 10 | % | 8 | % | 8 | % | ||||||

Insurance services clients(1) | 108,000 | 1 | % | 6 | % | 8 | % | ||||||

Health and benefits services applicants | 131,000 | 8 | % | 23 | % | 23 | % | ||||||

Retirement services plans (2) | 62,000 | 4 | % | 4 | % | 568,000 | 12 | % | |||||

(1) | Includes workers’ compensation insurance services clients and health and benefits services clients. |

14

(2) | Retirement services plans include ePlan Services, Inc. ("ePlan") plans. ePlan was acquired in May 2011. The organic growth rate for retirement services plans for fiscal 2011 would have been approximately 5%. |

Ongoing investment in our business is critical to our success. During fiscal 2013, we continued to expand our product portfolio through internal development and acquisitions to add value for our clients. We have positioned ourselves to capture the opportunity created by a greater interest in online SaaS solutions through both product development and recent acquisitions with SaaS-oriented business models, including our SurePayroll product, which continues to perform well. The combination of our market-leading SaaS solutions combined with our service model allow us to offer a unique value proposition in the market.

We enhanced our online and mobile offerings, adding greater value and convenience for our clients. These mobile applications allow our clients instant access and increased productivity. Our single-sign-on feature provides a new and improved interface and mobility enhancer. During fiscal 2013, we launched our mobile application for the smartphone. We also added access to flexible spending account ("FSA") and health and benefits employer and employee information to our mobile offerings. Early in fiscal 2013, we launched an industry-leading report center and robust report writer. This provides a one-stop shop for standard or on-demand reporting needs, ad-hoc and customized reporting, data-extract templates and more.

We continued to enhance our Paychex Next Generation platform and its suite of innovative products, as we believe this is a key building block to our future success. This platform allows us to leverage efficiencies in our processes and to continue to provide excellent customer service to our clients. This technology creates a truly integrated workforce management solution for our clients, bringing together the services those clients need, including our small and mid-market payroll products and various human resource and employee benefit management services.

In our retirement services area, we have also experienced success in driving more sales through an enhanced approach to our direct relationships with financial advisors. We recently announced a partnership with FSAStore.com, a national online store stocked exclusively with FSA-eligible products and services, to provide participants in the Paychex FSA a simple and convenient way to use their FSA funds.

We have strengthened our position as an expert in our industry by serving as a source of education and information to clients, small businesses, and other interested parties. During fiscal 2013, we launched a newly redesigned Paychex Accountant Knowledge Center, a free online resource available through www.paychex.com that brings valuable information and time-saving online tools to accounting professionals. We also launched a new and improved BuildMyBiz.com that includes a number of new features that provide enhanced resources for entrepreneurs and small business owners. In addition, we provide free webinars, white papers, and other information on our website to aid existing and prospective clients with the impact of regulatory changes. The Paychex Insurance Agency, Inc. website, www.paychexinsurance.com, helps small business owners navigate the area of insurance coverage and both this website and www.paychex.com have sections dedicated to the topic of health care reform.

Financial position and liquidity

The supply of high credit quality securities has been limited with the continued volatility in the global financial markets, thereby limiting our investment choices. Despite this macroeconomic environment, our financial position as of May 31, 2013 remained strong with cash and total corporate investments of $874.6 million and no debt.

Our investment strategy focuses on protecting principal and optimizing liquidity. Yields on high quality financial instruments remain low, negatively impacting our income earned on funds held for clients and corporate investments. We invest predominately in municipal bonds including general obligation bonds, pre-refunded bonds that are secured by a U.S. government escrow, and essential services revenue bonds. During fiscal 2013, our primary short-term investment vehicles were high quality variable rate demand notes (“VRDNs”) and bank demand deposit accounts.

A substantial portion of our portfolio is invested in high credit quality securities with AAA and AA ratings and A-1/P-1 ratings on short-term securities. We limit the amounts that can be invested in any single issuer and invest in short- to intermediate-term instruments whose fair value is less sensitive to interest rate changes. We believe that our investments as of May 31, 2013 were not other-than-temporarily impaired, nor has any event occurred subsequent to that date that would indicate any other-than-temporary impairment.

Our primary source of cash is our ongoing operations. Cash flow from operations was $675.3 million for fiscal 2013. Historically, we have funded our operations, capital purchases, business acquisitions, and dividend payments from our operating activities. Our positive cash flows in fiscal 2013 allowed us to support our business growth and to pay substantial dividends to our stockholders. During fiscal 2013, dividends paid to stockholders were 84% of net income. It is anticipated that cash and total

15

corporate investments as of May 31, 2013, along with projected operating cash flows, will support our normal business operations, capital purchases, and dividend payments for the foreseeable future.

For further analysis of our results of operations for fiscal years 2013, 2012, and 2011, and our financial position as of May 31, 2013, refer to the tables and analysis in the “Results of Operations” and “Liquidity and Capital Resources” sections of this Item 7 and the discussion in the “Critical Accounting Policies” section of this Item 7.

Outlook

Our outlook for the fiscal year ending May 31, 2014 (“fiscal 2014”) is based upon current economic and interest rate conditions continuing with no significant changes. Our expected fiscal 2014 payroll revenue growth rate is based upon anticipated client base growth and increases in revenue per check. HRS revenue growth is expected to remain in line with our recent organic experience.

Our fiscal 2014 guidance is as follows:

Low | High | |||||||

Payroll service revenue | 3 | % | — | 4 | % | |||

HRS revenue | 9 | % | — | 10 | % | |||

Total service revenue | 5 | % | — | 6 | % | |||

Interest on funds held for clients | (9 | )% | — | (7 | )% | |||

Investment income, net | — | % | — | 5 | % | |||

Net income | 8 | % | — | 9 | % | |||

We believe that net income growth for fiscal 2014 is expected to benefit from a strong comparison mainly due to results in the fourth quarter of fiscal 2013. In the fourth quarter of fiscal 2013, we settled a state income tax matter which reduced diluted earnings per share by approximately $0.04 per share. Operating income, net of certain items, as a percent of service revenue, is expected to be approximately 38% for fiscal 2014. The effective income tax rate for fiscal 2014 is expected to be in the range of 36% to 37%. The settlement of a state income tax matter in fiscal 2013 is not expected to have an impact on the effective income tax rate for fiscal 2014.

Interest on funds held for clients and investment income for fiscal 2014 are expected to continue to be impacted by the low interest rate environment. The average rate of return on our combined funds held for clients and corporate investment portfolios is expected to remain at 1.0% for fiscal 2014. As of May 31, 2013, the long-term investment portfolio had an average yield-to-maturity of 1.8% and an average duration of 3.1 years. In the next twelve months, slightly less than 15% of this portfolio will mature, and it is currently anticipated that these proceeds will be reinvested at a lower average interest rate of approximately 1.1%. Investment income is expected to benefit from ongoing investment of cash generated from operations.

Purchases of property and equipment for fiscal 2014 are expected to be in the range of $100 million to $110 million. This includes costs for internally developed software as we continue to invest in our service supporting technology. Fiscal 2014 depreciation expense is projected to be in the range of $85 million to $90 million, and we project amortization of intangible assets for fiscal 2014 to be approximately $15 million.

16

Results of Operations

Summary of Results of Operations for the Fiscal Years Ended May 31:

In millions, except per share amounts | 2013 | Change | 2012 | Change | 2011 | |||||||||||||

Revenue: | ||||||||||||||||||

Payroll service revenue | $ | 1,539.2 | 2 | % | $ | 1,510.0 | 5 | % | $ | 1,438.8 | ||||||||

HRS revenue | 746.0 | 10 | % | 676.2 | 13 | % | 597.4 | |||||||||||

Total service revenue | 2,285.2 | 5 | % | 2,186.2 | 7 | % | 2,036.2 | |||||||||||

Interest on funds held for clients | 41.0 | (6 | )% | 43.6 | (9 | )% | 48.1 | |||||||||||

Total revenue | 2,326.2 | 4 | % | 2,229.8 | 7 | % | 2,084.3 | |||||||||||

Combined operating and SG&A expenses | 1,421.4 | 3 | % | 1,375.9 | 6 | % | 1,297.9 | |||||||||||

Operating income | 904.8 | 6 | % | 853.9 | 9 | % | 786.4 | |||||||||||

Investment income, net | 6.6 | 4 | % | 6.4 | 9 | % | 5.8 | |||||||||||

Income before income taxes | 911.4 | 6 | % | 860.3 | 9 | % | 792.2 | |||||||||||

Income taxes | 342.4 | 10 | % | 312.3 | 13 | % | 276.9 | |||||||||||

Effective income tax rate | 37.6 | % | 36.3 | % | 35.0 | % | ||||||||||||

Net income | 569.0 | 4 | % | $ | 548.0 | 6 | % | $ | 515.3 | |||||||||

Diluted earnings per share | $ | 1.56 | 3 | % | $ | 1.51 | 6 | % | $ | 1.42 | ||||||||

We invest in highly liquid, investment-grade fixed income securities and do not utilize derivative instruments to manage interest rate risk. As of May 31, 2013, we had no exposure to high-risk or illiquid investments and had insignificant exposure to European investments. Details regarding our combined funds held for clients and corporate investment portfolios are as follows:

Year ended May 31, | ||||||||||||

$ in millions | 2013 | 2012 | 2011 | |||||||||

Average investment balances: | ||||||||||||

Funds held for clients | $ | 3,715.6 | $ | 3,584.3 | $ | 3,350.3 | ||||||

Corporate investments | 756.9 | 685.9 | 662.4 | |||||||||

Total | $ | 4,472.5 | $ | 4,270.2 | $ | 4,012.7 | ||||||

Average interest rates earned (exclusive of net realized gains): | ||||||||||||

Funds held for clients | 1.1 | % | 1.2 | % | 1.4 | % | ||||||

Corporate investments | 0.8 | % | 0.9 | % | 0.9 | % | ||||||

Combined funds held for clients and corporate investments | 1.0 | % | 1.1 | % | 1.3 | % | ||||||

Total net realized gains | $ | 0.9 | $ | 1.0 | $ | 1.3 | ||||||

$ in millions As of May 31, | 2013 | 2012 | 2011 | |||||||||

Net unrealized gains on available-for-sale securities(1) | $ | 34.7 | $ | 59.5 | $ | 59.3 | ||||||

Federal Funds rate(2) | 0.25 | % | 0.25 | % | 0.25 | % | ||||||

Total fair value of available-for-sale securities | $ | 3,691.4 | $ | 3,059.0 | $ | 2,737.2 | ||||||

Weighted-average duration of available-for-sale securities in years(3) | 3.1 | 3.0 | 2.4 | |||||||||

Weighted-average yield-to-maturity of available-for-sale securities(3) | 1.8 | % | 2.2 | % | 2.6 | % | ||||||

(1) | The net unrealized gain on our investment portfolios was approximately $2.7 million as of July 15, 2013. |

(2) | The Federal Funds rate was a range of zero to 0.25% as of May 31, 2013, 2012, and 2011. |

(3) | These items exclude the impact of VRDNs, as they are tied to short-term interest rates. |

17

Payroll service revenue: Payroll service revenue increased 2% for fiscal 2013 and 5% for fiscal 2012 to $1.5 billion for both periods. Organic growth in payroll service revenue for fiscal 2012, which excludes the impact of acquisitions during fiscal 2011, was approximately 4%. Both fiscal 2013 and fiscal 2012 revenue benefited from increases in checks per payroll and revenue per check. Checks per payroll increased 1.6% and 2.0% for fiscal 2013 and fiscal 2012, respectively. Revenue per check in both periods was positively impacted by price increases, partially offset by discounting. Payroll service revenue for fiscal 2013 was modestly affected by the impact of Hurricane Sandy in the fall of 2012 and one less payroll processing day overall due to the leap year in fiscal 2012. Our client base growth was approximately 1% for both fiscal 2013 and fiscal 2012. Client retention reached record levels for fiscal 2013, following a year of further improvement.