As filed with the United States Securities and Exchange Commission on May 24, 2019

Registration No. 333-

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM S-1

REGISTRATION STATEMENT UNDER THE SECURITIES ACT OF 1933

CHINA RECYCLING ENERGY CORPORATION

(Name of Registrant as specified in its charter)

| Nevada | 7389 | 90-0093373 | ||

|

(State or other jurisdiction of incorporation) |

(Primary Standard Industrial Classification Code Number) |

(IRS Employer Identification No.) |

4/F, Tower C

Rong Cheng Yun Gu Building

Keji 3rd Road, Yanta District

Xi’an City, Shaanxi Province

China 710068

+ 86-29-8769-1097

(Address and telephone number of principal executive offices and principal place of business)

Guohua Ku, Chief Executive Officer

4/F, Tower C

Rong Cheng Yun Gu Building

Keji 3rd Road, Yanta District

Xi An City, Shaanxi Province

China

+ 86-29-8769-1097

(Name address and telephone number of agent for service)

Copies to:

Jeffrey Li

Ada Danelo

Garvey Schubert Barer, P.C.

Flour Mill Building

1000 Potomac Street NW, Suite 200

Washington, D.C. 20007-3501

(202) 298-1735

Approximate date of commencement of proposed sale to the public: From time to time after this registration statement is declared effective.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box: ☒

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer ☐ | Accelerated filer ☐ |

| Non-accelerated filer ☒ | Smaller reporting company ☒ |

| Emerging growth company ☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided to Section 7(a)(2)(B) of the Securities Act. ☐

CALCULATION OF REGISTRATION FEE

| Title of each class of securities to be registered | Amount to be registered |

Proposed maximum |

Proposed maximum offering price |

Amount of registration fee |

||||||||||||

| Common Stock, par value $0.001 per share | 5,658,641 | (1) | $ | 0.5182 | (2) | $ | 2,932,307.77 | $ | 355.40 | |||||||

| (1) | This registration statement registers for resale by the selling shareholders (i) 3,754,536 shares of common stock of the registrant, par value $0.001 per share (“Common Stock”), that are issuable upon the exercise of common stock purchase warrants of the registrant issued pursuant to private placements; (ii) 304,105 shares of Common Stock that are issuable upon the exercise of common stock purchase warrants of the registrant issued to the placement agent’s designees in connection with such private placements; and (iii) 1,600,000 shares of Common Stock sold to a selling shareholder in a prior private placement. In accordance with Rule 416(a), there also are being registered hereunder an indeterminate number of shares that may be issued and resold resulting from stock splits, stock dividends, recapitalizations or similar transactions. |

| (2) | Estimated pursuant to Rule 457(c) of the Securities Act of 1933 solely for the purpose of computing the amount of the registration fee based on the average of the high and low prices reported on the Nasdaq Capital Market on May 22, 2019. |

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the Registration Statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

The information in this prospectus is not complete and may be changed. These securities may not be sold until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

SUBJECT TO COMPLETION, DATED MAY 24, 2019

![]()

CHINA RECYCLING ENERGY CORPORATION

5,658,641 Shares of Common Stock

The selling shareholders identified in this prospectus may offer and sell up to 5,658,641 shares of our common stock, of which (i) 3,754,536 shares of common stock of the registrant, par value $0.001 per share (“Common Stock”), are issuable upon the exercise of common stock purchase warrants of the registrant issued pursuant to private placements (the “Investor Warrants”); (ii) 304,105 shares of Common Stock are issuable upon the exercise of common stock purchase warrants of the registrant issued to the placement agent’s designees in connection with such private placements (the “Agent Warrants,” and together with the Investor Warrants, the “Warrants”); and (iii) 1,600,000 shares of Common Stock were sold to a selling shareholder in a prior private placement.

We are not selling any shares of our common stock in this offering and will not receive any proceeds from this offering. However, upon a cash exercise of the Warrants by the selling stockholders, we will receive a per share exercise price of $1.3725 or $0.9365 for Investor Warrants and $1.875 or $1.00 for Agent Warrants, depending on the terms of the Warrant, before any adjustments as set forth in the Warrants. If the Warrants are exercised in a cashless exercise, we will not receive any proceeds from the exercise of the Warrants. We have agreed to pay certain registration expenses, other than underwriting discounts and commissions.

The selling stockholders may from time to time sell, transfer or otherwise dispose of any or all of their shares of Common Stock in a number of different ways and at varying prices. See “Plan of Distribution” for more information.

We may amend or supplement this prospectus from time to time by filing amendments or supplements as required. You should read this entire prospectus and any amendments or supplements carefully before you make your investment decision.

Our common stock trades on the Nasdaq Capital Market under the symbol “CREG.” The closing price of our common stock on the Nasdaq Capital Market on May 22, 2019, was $0.501 per share.

Investing in our Common Stock involves significant risks. See “Risk Factors” beginning on page 11 of this prospectus.

Neither the Securities and Exchange Commission (the “SEC”) nor any state securities commission has approved or disapproved of these securities or passed upon the accuracy or adequacy of this prospectus. Any representation to the contrary is a criminal offense.

The date of this prospectus is , 2019.

This prospectus is part of a registration statement that we filed with the SEC pursuant to which the selling stockholders named herein may, from time to time, offer and sell or otherwise dispose of the shares of our common stock covered by this prospectus. You should not assume that the information contained in this prospectus is accurate on any date subsequent to the date set forth on the front cover of this prospectus or that any information we have incorporated by reference is correct on any date subsequent to the date of the document incorporated by reference, even though this prospectus is delivered or shares of common stock are sold or otherwise disposed of on a later date. It is important for you to read and consider all information contained in this prospectus, including the documents incorporated by reference herein, in making your investment decision. You should also read and consider the information in the documents to which we have referred you under the captions “Where You Can Find More Information” and “Incorporation of Certain Information by Reference” in this prospectus.

We have not authorized any dealer, salesman or other person to give any information or to make any representation other than those contained or incorporated by reference in this prospectus. You must not rely upon any information or representation not contained or incorporated by reference in this prospectus. This prospectus does not constitute an offer to sell or the solicitation of an offer to buy any of our shares of common stock other than the shares of our common stock covered hereby, nor does this prospectus constitute an offer to sell or the solicitation of an offer to buy any securities in any jurisdiction to any person to whom it is unlawful to make such offer or solicitation in such jurisdiction.

This prospectus contains forward-looking statements that are subject to a number of risks and uncertainties, many of which are beyond our control. See “Risk Factors” and “Cautionary Note Regarding Forward-Looking Statements.”

Unless the context otherwise requires, the terms “CREG,” “the Company,” “we,” “us” and “our” in this prospectus refer to China Recycling Energy Corporation, our subsidiaries and consolidated entities. “China” and the “PRC” refer to the People’s Republic of China.

i

This summary highlights information contained elsewhere in this prospectus, is not complete, and does not contain all of the information that you should consider before making your investment decision. You should carefully read the entire prospectus, including the information presented under the sections entitled “Risk Factors” and “Cautionary Note Regarding Forward-Looking Statements” and the consolidated financial statements and the notes thereto and other documents incorporated by reference in this prospectus before making an investment decision.

Overview

We are currently engaged in the recycling energy business, providing energy savings and recycling products and services. We are a leading developer of waste energy recycling projects for industrial applications in China, and we believe we are the only developer to use a Build-Operate-Transfer (“BOT”) model to provide energy saving and recovery facilities for multiple energy intensive industries in China. Our waste energy recycling projects allow customers which use substantial amounts of electricity to recapture previously wasted pressure, heat, and gas from their manufacturing processes to generate electricity. We currently offer waste energy recycling systems to companies for use in iron and steel, nonferrous metal, cement, coal and petrochemical plants. We construct our projects at our customer’s facility and the electricity produced is used on-site by the customer. While some of our competitors offer projects targeting one or two verticals, we serve multiple verticals.

We develop fully customized projects across several verticals to better meet customer’s energy recovery needs. Our waste pressure-to-energy solution primarily consists of the Blast Furnace Top Gas Recovery Turbine Unit (“TRT”), a system that utilizes high pressure gas emitted from the blast furnace top to drive turbine units and generate electricity. Our waste heat-to-energy solution primarily consists of heat power generation projects for applications in cement, steel, coking coal, and nonferrous metal industries, which collect the residual heat from various manufacturing processes, e.g. the entrance and exit ends of the cement rotary kilns, to generate electricity. Our waste gas-to-energy solution primarily consists of the Waste Gas Power Generation system (“WGPG”) and the Combined Cycle Power Plant (the “CCPP”). A WGPG system utilizes flammable waste gas from coal mining, petroleum exploitation, refinery processing or other sources as a fuel source to generate electricity through the use of a gas turbine. A CCPP system employs more than one power generating cycle to utilize the waste gas, which not only generates electricity by burning the flammable waste gas in a gas turbine (as a WGPG) but also uses the waste heat from burning the gas to make steam to generate additional electricity via a steam turbine.

We provide a clean-technology and energy-efficient solution aimed at reducing the air pollution and energy shortage problems in China. Our projects capture industrial waste energy to produce low-cost electricity, enabling industrial manufacturers to reduce their energy costs, lower their operating costs, and extend the life of primary manufacturing equipment. In addition, our waste energy recycling projects allow our industrial customers to reduce their reliance on China’s centralized national power grid, which is prone to black-outs or brown-outs or is completely inaccessible from certain remote areas. Our projects generally produce lower carbon dioxide emissions and other pollutants, and are hence more environmentally friendly than other forms of power generation.

Since 2007, we have primarily used the BOT model to serve our customers. For each project, we design, finance, construct and install the waste energy recycling projects for our customers, operate the projects for five to 20 years, and then transfer the projects to the owners. The BOT model creates a win-win solution for both our customers and us. We provide the capital expenditure financing in exchange for attractive returns on each project; our customers can focus their capital resources on their core businesses, do not need to invest additional capitals to comply with government environmental regulations, reduce noise and emissions and reduce their energy costs. We in turn efficiently recapture our costs through the stream of lease payments.

1

Our Projects

We design, finance, construct, operate and eventually transfer waste energy recycling projects to meet the energy saving and recovery needs of our customers. Our waste energy recycling projects use the pressure, heat or gas, which is generated as a byproduct of a variety of industrial processes, to create electricity. The residual energy from industrial processes, which was traditionally wasted, may be captured in a recovery process and utilized by our waste energy recycling projects to generate electricity burning additional fuel and additional emissions. Among a wide variety of waste-to-energy technologies and solutions, we primarily focus on waste pressure to energy systems, waste heat to energy systems and waste gas power generation systems. We do not manufacture the equipment and materials that are used in the construction of our waste energy recycling projects. Rather, we incorporate standard power generating equipment into a fully integrated onsite project for our customers.

Waste Pressure to Energy Systems

TRT is a power generating system utilizing the exhaust pressure and heat from industrial processes in the iron, steel, petrochemical, chemical and non-ferrous metals industries, often from blast furnace gases in the metal production industries. Without TRT power systems, blast furnace gas is treated by various de-pressurizing valves to decrease its pressure and temperature before the gas is transmitted to end users. No electricity is generated during the process and noise and heat pollution is released. In a TRT system, the blast furnace gas produced during the smelting process is directed through the system to decrease its pressure and temperature. The released pressure and heat is then utilized to drive the turbine unit to generate electricity, which is then transmitted back to the producer. We believe our projects are superior to those of our competitors due to the inclusion of advanced dry-type de-dusting technology, joined turbine systems, and automatic power grid synchronization.

Waste Heat to Energy Systems

Waste heat to energy systems utilize waste heat generated in industrial production to generate electricity. The waste heat is trapped to heat a boiler to create steam and power a steam turbine. Our waste heat to energy systems have used waste heat from cement production and from metal production. We invested in and have built two cement low temperature heat power generation systems. These projects can use about 35% of the waste heat generated by the cement kiln, and generate up to 50% of the electricity needed to operate the cement plant.

Waste Gas to Energy Systems

Our Waste Gas to Energy Systems primarily include Waste Gas Power Generation (“WGPG”) systems and Combined Cycle Power Plant (“CCPP”) systems. WGPG uses the flammable waste gases emitted from industrial production processes such as blast furnace gas, coke furnace gas, and oil gas, to power gas-fired generators to create energy. A CCPP system employs more than one power generating cycle to utilize the waste gas, which is more efficient because it not only generates electricity by burning the flammable waste gas in a gas-fired generator (WGPG) but also uses the waste heat from burning the gas to make steam to generate additional electricity via a steam generator (CCPP).

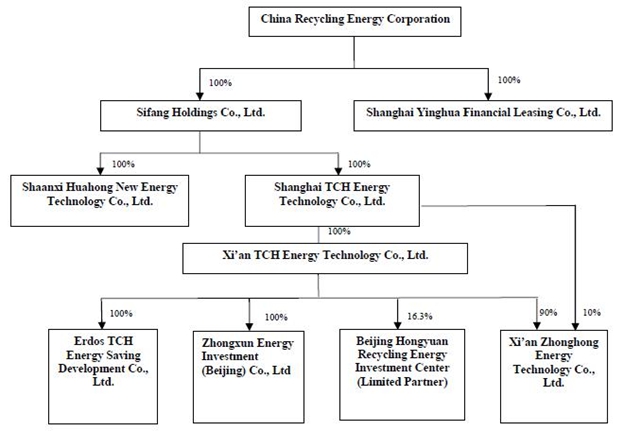

Shanghai TCH and its Subsidiaries

Shanghai TCH was established as a foreign investment enterprise in Shanghai under the laws of the PRC on May 25, 2004 and has a registered capital of $29.80 million. Xi’an TCH was incorporated in Xi’an, Shaanxi Province under the laws of the PRC on November 8, 2007. In February 2009, Huahong was incorporated in Xi’an, Shaanxi province. Erdos TCH was incorporated in April 2009 in Erdos, Inner Mongolia Autonomous Region. On July 19, 2013, Xi’an TCH formed Xi’an Zhonghong New Energy Technology Co., Ltd (“Zhonghong”). Xi’an TCH owns 90% and Shanghai TCH owns 10% of Zhonghong, which provides energy saving solutions and services, including constructing, selling and leasing energy saving systems and equipment to customers.

As of March 31, 2019, Shanghai TCH, through its subsidiaries, had sales or sales-type leases with Pucheng (for two biomass power generation (“BMPG”) systems). In addition, as of March 31, 2019, Erdos TCH leased power and steam generating systems from waste heat from metal refining to Erdos (a total of five systems) and charges Erdos a leasing fee based on actual electricity generated.

2

Erdos TCH – Joint Venture

On April 14, 2009, the Company formed Erdos TCH as a joint venture (the “JV” or “Erdos TCH”) with Erdos Metallurgy Co., Ltd. (“Erdos”) to recycle waste heat from Erdos’ metal refining plants to generate power and steam to be sold back to Erdos. The JV has a term of 20 years with a total investment for the project estimated at $79 million (RMB 500 million) and an initial investment of $17.55 million (RMB 120 million). Erdos contributed 7% of the total investment for the project, and Xi’an TCH contributed 93%. According to Xi’an TCH and Erdos’ agreement on profit distribution, Xi’an TCH and Erdos will receive 80% and 20%, respectively, of the profit from the JV until Xi’an TCH receives the complete return of its investment. Xi’an TCH and Erdos will then receive 60% and 40%, respectively, of the profit from the JV. On June 15, 2013, Xi’an TCH and Erdos entered into a share transfer agreement, pursuant to which Erdos transferred and sold its 7% ownership interest in the JV to Xi’an TCH for $1.29 million (RMB 8 million), plus certain accumulated profits as described below. Xi’an TCH paid the $1.29 million in July 2013 and, as a result, became the sole stockholder of Erdos TCH. In addition, Xi’an TCH is required to pay Erdos accumulated profits from inception up to June 30, 2013 in accordance with the supplementary agreement entered on August 6, 2013. In August 2013, Xi’an TCH paid 20% of the accumulated profit (calculated under PRC GAAP) of $226,000 to Erdos. Erdos TCH currently has two power generation systems in Phase I with a total of 18 MW power capacity, and three power generation systems in Phase II with a total of 27 MW power capacity.

With the current economic conditions in China, the government has limited and reduced over capacity and production in the iron and steel industry, which has resulted in a sharp decrease of Erdos Metallurgy Co., Ltd’s production of ferrosilicon, its revenue and cash flows, and has made it difficult for Erdos to make the monthly minimum lease payment.

After considering the challenging economic conditions facing Erdos, and to maintain the long-term cooperative relationship between the parties, which we believe will continue to produce long-term benefits, on April 28, 2016, Erdos TCH and Erdos entered into a supplemental agreement, effective May 1, 2016. Under the supplemental agreement, Erdos TCH cancelled monthly minimum lease payments from Erdos, and agreed to charge Erdos based on actual electricity sold at RMB 0.30 / KWH, which such price will be adjusted annually based on prevailing market conditions.

The Company evaluated the modified terms for payments based on actual electricity sold as minimum lease payments as defined in ASC 840-10-25-4, since lease payments that depend on a factor directly related to the future use of the leased property are contingent rentals and, accordingly, are excluded from minimum lease payments in their entirety. The Company wrote off the net investment receivables of these leases at the lease modification date.

Pucheng Biomass Power Generation Projects

On June 29, 2010, Xi’an TCH entered into a Biomass Power Generation (“BMPG”) Project Lease Agreement with PuchengXinHeng Yuan Biomass Power Generation Co., Ltd. (“Pucheng”), a limited liability company incorporated in China. Under this lease agreement, Xi’an TCH leased a set of 12MW BMPG systems to Pucheng at a minimum of $279,400 (RMB 1,900,000) per month for a term of 15 years. (“Pucheng Phase I”).

On September 11, 2013, Xi’an TCH entered into a BMPG Asset Transfer Agreement (the “Pucheng Transfer Agreement”) with Pucheng Xin Heng Yuan Biomass Power Generation Corporation (“Pucheng”), a limited liability company incorporated in China. The Pucheng Transfer Agreement provided for the sale by Pucheng to Xi’an TCH of a set of 12 MW BMPG systems with the completion of system transformation for a purchase price of RMB 100 million ($16.48 million) in the form of 8,766,547 shares of common stock of the Company at $1.87 per share. Also on September 11, 2013, Xi’an TCH also entered into a BMPG Project Lease Agreement with Pucheng (the “Pucheng Lease”). Under the Pucheng Lease, Xi’an TCH leases this same set of 12 MW BMPG system to Pucheng, and combines this lease with the lease for the 12 MW BMPG station of Pucheng Phase I project, under a single lease to Pucheng for RMB 3.8 million ($0.63 million) per month (the “Pucheng Phase II Project”). The term for the consolidated lease is from September 2013 to June 2025. The lease agreement for the 12 MW station from Pucheng Phase I project terminated upon the effective date of the Pucheng Lease. The ownership of two 12 MW BMPG systems will transfer to Pucheng at no additional charge when the Pucheng Lease expires.

3

Shenqiu Yuneng Biomass Power Generation Projects

On May 25, 2011, Xi’an TCH entered into a Letter of Intent with Shenqiu YuNeng Thermal Power Co., Ltd. (“Shenqiu”) to reconstruct and transform a Thermal Power Generation System owned by Shenqiu into a 75T/H BMPG System for $3.57 million (RMB 22.5 million). The project commenced in June 2011 and was completed in the third quarter of 2011. On September 28, 2011, Xi’an TCH entered into a Biomass Power Generation Asset Transfer Agreement with Shenqiu (the “Shenqiu Transfer Agreement”). Pursuant to the Shenqiu Transfer Agreement, Shenqiu sold Xi’an TCH a set of 12 MW BMPG systems (after Xi’an TCH converted the system for BMPG purposes). As consideration for the BMPG systems, Xi’an TCH paid Shenqiu $10.94 million (RMB 70 million) in cash in three installments within six months upon the transfer of ownership of the systems. By the end of 2012, all the consideration was paid. On September 28, 2011, Xi’an TCH and Shenqiu also entered into a Biomass Power Generation Project Lease Agreement (the “2011 Shenqiu Lease”). Under the 2011 Shenqiu Lease, Xi’an TCH agreed to lease a set of 12 MW BMPG systems to Shenqiu at a monthly rental rate of $286,000 (RMB 1.8 million) for 11 years. Upon expiration of the 2011 Shenqiu Lease, ownership of this system will transfer from Xi’an TCH to Shenqiu at no additional cost. In connection with the 2011 Shenqiu Lease, Shenqiu paid one month’s rent as a security deposit to Xi’an TCH, in addition to providing personal guarantees.

On October 8, 2012, Xi’an TCH entered into a Letter of Intent for technical reformation of Shenqiu Project Phase II with Shenqiu for technical reformation to enlarge the capacity of the Shenqiu Project Phase I (the “Shenqiu Phase II Project”). The technical reformation involved the construction of another 12 MW BMPG system. After the reformation, the generation capacity of the power plant increased to 24 MW. The project commenced on October 25, 2012 and was completed during the first quarter of 2013. The total cost of the project was $11.1 million (RMB 68 million). On March 30, 2013, Xi’an TCH and Shenqiu entered into a BMPG Project Lease Agreement (the “2013 Shenqiu Lease”). Under the 2013 Shenqiu Lease, Xi’an TCH agreed to lease the second set of 12 MW BMPG systems to Shenqiu for $239,000 (RMB 1.5 million) per month for 9.5 years. When the 2022 Shenqiu Lease expires, ownership of this system will transfer from Xi’an TCH to Shenqiu at no additional cost.

On January 4, 2019, Xi’an Zhonghong, Xi’an TCH, and Mr. Chonggong Bai, a resident of China, entered into a Projects Transfer Agreement (the “Agreement”), pursuant to which Xi’an TCH will transfer two Biomass Power Generation Projects in Shenqiu (“Shenqiu Phase I and II Projects”) to Mr. Bai for RMB 127,066,000 ($18.55 million). Mr. Bai agreed to transfer all the equity shares of his wholly owned company, Xi’an Hanneng Enterprises Management Consulting Co. Ltd. (“Xi’an Hanneng”) to Beijing Hongyuan Recycling Energy Investment Center, LLP (the “HYREF”) as repayment for the loan made by Xi’an Zhonghong to HYREE as consideration for the transfer of the Shenqiu Phase I and II Projects. The transfer was completed on February 15, 2019.

Yida Coke Oven Gas Power Generation Projects

On June 28, 2014, Xi’an TCH entered into an Asset Transfer Agreement (the “Transfer Agreement”) with Qitaihe City Boli Yida Coal Selection Co., Ltd. (“Yida”), a limited liability company incorporated in China. The Transfer Agreement provided for the sale to Xi’an TCH of a 15 MW coke oven WGPG station, which was converted from a 15 MW coal gangue power generation station from Yida. As consideration for the Transfer Asset, Xi’an TCH paid Yida RMB 115 million ($18.69 million) in the form of the common stock shares of the Company at the average closing price per share of the Stock for the 10 trading days prior to the closing date of the transaction (the “Shares”). The exchange rate between US Dollar and Chinese RMB in connection with the stock issuance was the rate equal to the middle rate published by the People’s Bank of China on the closing date of the assets transfer.

On June 28, 2014, Xi’an TCH also entered into a Coke Oven Gas Power Generation Project Lease Agreement (the “Lease Agreement”) with Yida. Under the Lease Agreement, Xi’an TCH leased the Transfer Asset to Yida for RMB 3 million ($0.49 million) per month, and the term of the lease is from June 28, 2014 to June 27, 2029. Yida will also provide an RMB 3 million ($0.49 million) security deposit (without interest) for the lease. Xi’an TCH will transfer the Transfer Asset back to Yida at no cost at the end of the lease term.

On June 22, 2016, Xi’an TCH entered into a Coal Oven Gas Power Generation Project Repurchase Agreement (the “Repurchase Agreement”) with Yida. Under the Repurchase Agreement, Xi’an TCH agreed to transfer to Yida all the project assets for RMB 112,000,000 ($16.89 million) (the “Transfer Price”) with Yida’s retention of ownership of the Shares. Yida agreed to make the following payments: (i) the outstanding monthly leasing fees for April and May 2016 of RMB 6,000,000 ($0.90 million) to Xi’an TCH within 5 business days from the execution of the Repurchase Agreement; (ii) a payment of RMB 50,000,000 ($7.54 million) of the Transfer Price to Xi’an TCH within 5 business days from the execution of the Repurchase Agreement; and (iii) a payment of the remaining RMB 62,000,000 ($9.35 million) of the Transfer Price to Xi’an TCH within 15 business days from the execution of the Repurchase Agreement. Under the Repurchase Agreement, ownership of the project assets was transferred from Xi’an TCH to Yida within 3 business days after Xi’an TCH received the full Transfer Price and the outstanding monthly leasing fees. In July 2016, the Company received the full payment of the Transfer Price and title to the system was transferred at that time. The Company recorded a $0.42 million loss from this transaction in 2016.

4

The Fund Management Company and the HYREF Fund

On June 25, 2013, Xi’an TCH and Hongyuan Huifu Venture Capital Co. Ltd (“Hongyuan Huifu”) jointly established Hongyuan Recycling Energy Investment Management Beijing Co., Ltd (the “Fund Management Company”) with registered capital of RMB 10 million ($1.45 million). Xi’an TCH made an initial capital contribution of RMB 4 million ($650,000) and had a 40% ownership interest in the Fund Management Company. With respect to the Fund Management Company, voting rights and dividend rights were allocated 80% and 20% between Hongyuan Huifu and Xi’an TCH, respectively.

The Fund Management Company is the general partner of Beijing Hongyuan Recycling Energy Investment Center, LLP (the “HYREF Fund”), a limited liability partnership established July 18, 2013 in Beijing. The Fund Management Company made an initial capital contribution of RMB 5 million ($830,000) to the HYREF Fund. An initial amount of RMB 460 million ($77 million) was fully subscribed by all partners for the HYREF Fund. The HYREF Fund has three limited partners: (1) China Orient Asset Management Co., Ltd., which made an initial capital contribution of RMB 280 million ($46.67 million) to the HYREF Fund and is a preferred limited partner; (2) Hongyuan Huifu, which made an initial capital contribution of RMB 100 million ($16.67 million) to the HYREF Fund and is an ordinary limited partner; and (3) the Company’s wholly-owned subsidiary, Xi’an TCH, which made an initial capital contribution of RMB 75 million ($12.5 million) to the HYREF Fund and is a secondary limited partner. The term of the HYREF Fund’s partnership is six years from the date of its establishment, expiring on July 18, 2019. The term is four years from the date of contribution for the preferred limited partner, and four years from the date of contribution for the ordinary limited partner. The size of the HYREF Fund is RMB 460 million ($76.66 million). The HYREF Fund was formed to invest in Xi’an Zhonghong New Energy Technology Co., Ltd., a then 90% owned subsidiary of Xi’an TCH, for the construction of two coke dry quenching (“CDQ”) waste heat power generation (“WHPG”) stations with Jiangsu Tianyu Energy and Chemical Group Co., Ltd. (“Tianyu”) and one CDQ WHPG station with Boxing County Chengli Gas Supply Co., Ltd. (“Chengli”).

Chengli Waste Heat Power Generation Projects

On July 19, 2013, Xi’an TCH formed a new company, “Xi’an Zhonghong New Energy Technology Co., Ltd.” (“Zhonghong”), with registered capital of RMB 30 million ($4.85 million). Xi’an TCH paid RMB 27 million ($4.37 million) and owns 90% of Zhonghong. Zhonghong is engaged to provide energy saving solution and services, including constructing, selling and leasing energy saving systems and equipment to customers. On December 29, 2018, Shanghai TCH entered into a Share Transfer Agreement with HYREF, pursuant to which HYREF transferred its 10% ownership in Xi’an Zhonghong to Shanghai TCH for consideration of RMB 3 million ($0.44 million). The transfer was completed January 22, 2019.

On July 24, 2013, Zhonghong entered into a Cooperative Agreement of CDQ and CDQ WHPG Project with Boxing County Chengli Gas Supply Co., Ltd. (“Chengli”). The parties entered into a supplement agreement on July 26, 2013. Pursuant to these agreements, Zhonghong agreed to design, build and maintain a 25 MW CDQ system and a CDQ WHPG system to supply power to Chengli, and Chengli agreed to pay energy saving fees (the “Chengli Project”). Chengli will contract the operation of the system to a third party contractor that is mutually agreed to by Zhonghong. In addition, Chengli will provide the land for the CDQ system and CDQ WHPG system at no cost to Zhonghong. The term of these Agreements is 20 years. The watt hours generated by the Chengli Project will be charged at RMB 0.42 ($0.068) per KWH (excluding tax). The operating time shall be based upon an average 8,000 hours annually. If the operating time is less than 8,000 hours per year due to a reason attributable to Chengli, then time charged shall be 8,000 hours a year, and if it is less than 8,000 hours due to a reason attributable to Zhonghong, then it shall be charged at actual operating hours. The construction of the Chengli Project was completed in the second quarter of 2015 and the project successfully completed commissioning tests in the first quarter of 2017. The Chengli Project is now operational, however, due to intensifying environmental protection, the local environmental authorities required the project owner constructing CDQ sewage treatment to complete supporting works, which were completed and passed through acceptance inspection during the quarter ended September 30, 2018. However, the owner of Chengli Project changed from Chengli to Shandong Boxing Shengli Technology Company Ltd. (“Shengli”). This change resulted from transfer of the equity ownership of Chengli to Shengli (a private company). Chengli, a 100% state-owned enterprise that is 100% owned by the local Power Supply Bureau, is not allowed to carry out business activities, and Shengli, the new owner, is not entitled to the high on-grid prices, and thus demanded a renegotiation of the settlement terms for the project.

5

On July 22, 2013, Zhonghong entered into an Engineering, Procurement and Construction (“EPC”) General Contractor Agreement for the Boxing County Chengli Gas Supply Co., Ltd. CDQ Power Generation Project (the “Chengli Project”) with Xi’an Huaxin New Energy Co., Ltd. (“Huaxin”). Zhonghong, as the owner of the Chengli Project, contracted EPC services for a CDQ system and a 25 MW CDQ WHPG system for Chengli to Huaxin. Huaxin shall provide construction, equipment procurement, transportation, installation and adjustment, test run, construction engineering management and other necessary services to complete the Chengli Project and ensure the CDQ system and CDQ WHPG system for Chengli meet the inspection and acceptance requirements and work normally. The Chengli Project is a turn-key project in which Huaxin is responsible for monitoring the quality, safety, duration and cost of the Chengli Project. The total contract price is RMB 200 million ($33.34 million), which includes all materials, equipment, labor, transportation, electricity, water, waste disposal, machinery and safety costs.

On December 29, 2018, Xi’an Zhonghong, Xi’an TCH, the “HYREF”, Guohua Ku, and Mr. Chonggong Bai entered into a CDQ WHPG Station Fixed Assets Transfer Agreement, pursuant to which Xi’an Zhonghong transferred Chengli CDQ WHPG station as the repayment of loan at RMB 188,639,400 ($27.54 million) to HYREF. Xi’an Zhonghong, Xi’an TCH, Guohua Ku and Chonggong Bai also agreed to buy back the CDQ WHPG Station when conditions under the Buy Back Agreement are met. The transfer was completed January 22, 2019.

Tianyu Waste Heat Power Generation Project

On July 19, 2013, Zhonghong entered into a Cooperative Agreement (the “Tianyu Agreement”) for Energy Management of CDQ and CDQ WHPG with Jiangsu Tianyu Energy and Chemical Group Co., Ltd (“Tianyu”). Pursuant to the Tianyu Agreement, Zhonghong will design, build, operate and maintain two sets of 25 MW CDQ and CDQ WHPG systems for two subsidiaries of Tianyu – Xuzhou Tian’an Chemical Co., Ltd (“Xuzhou Tian’an”) and Xuzhou Huayu Coking Co., Ltd. (“Xuzhou Huayu”) – to be located at Xuzhou Tian’an and Xuzhou Huayu’s respective locations (the “Tianyu Project”). Upon completion of the Tianyu Project, Zhonghong will charge Tianyu an energy saving fee of RMB 0.534 ($0.087) per KWH (excluding tax). The operating time will be based upon an average 8,000 hours annually for each of Xuzhou Tian’an and Xuzhou Huayu. If the operating time is less than 8,000 hours per year due to a reason attributable to Tianyu, then time charged will be 8,000 hours a year. Because of the overcapacity and pollution of the iron and steel and related industries, the government has imposed production limitations for the energy-intensive enterprises with heavy pollution, including Xuzhou Tian’an. Xuzhou Tian’an has slowed the construction process for its dry quenching production line which caused the delay of our project. The construction of the Xuzhou Tian’an Project is anticipated to be completed by the second quarter of 2019. Xuzhou Tian’an will provide the land for the CDQ and CDQ WHPG systems for free. Xuzhou Tian’an has also guaranteed that it will purchase all of the power generated by the CDQ WHPG systems. The Xuzhou Huayu Project is currently on hold due to a conflict between Xuzhou Huayu Coking Co., Ltd. and local residents on certain pollution-related issues. The local government has acted in its capacity to coordinate the resolution of this issue. The local residents were requested to move from the hygienic buffer zone of the project location with compensatory payments from the government. Xuzhou Huayu was required to stop production and implement technical innovations to mitigate pollution discharge including sewage treatment, dust collection, noise control, and recycling of coal gas. Currently, some local residents have moved. Xuzhou Huayu has completed the implementation of the technical innovations of sewage treatment, dust collection, and noise control, and the Company is waiting for local governmental agencies to approve these technical innovations so that we can resume construction. Due to the stricter administration of environmental protection policies and recent increase of environmental protections for the coking industry in Xuzhou, all local coking, as well as steel iron enterprises, are facing a similar situation of suspended production while rectifying technologies and procedures. The Company expects to receive governmental acceptance and approval and to resume construction in the second quarter of 2019.

On July 22, 2013, Xi’an Zhonghong New Energy Technology Co., Ltd. entered into an EPC General Contractor Agreement for the Xuzhou Tianyu Group CDQ Power Generation Project (the “Project”) with Xi’an Huaxin New Energy Co., Ltd. (“Huaxin”). Zhonghong as the owner of the Project contracted EPC for the two sets of CDQ and 25 MW CDQ WHPG systems for Tianyu to Huaxin—one for Xuzhou Tian’an and one for Xuzhou Huayu. Huaxin shall provide construction, equipment procurement, transportation, installation and adjustment, test run, construction engineering management and other necessary works to complete the Project and ensure the CDQ and CDQ WHPG systems for Tianyu meet the inspection and acceptance requirements and work normally. The Project is a turn-key project and Huaxin is responsible for the quality, safety, duration and cost of the Project. The total contract price is RMB 400 million ($66.67 million), of which RMB 200 million ($33.34 million) is for the Xuzhou Tian’an system and RMB 200 million is for the Xuzhou Huayu system. The price is a cover-all price, which includes but not limited to all the materials, equipment, labor, transportation, electricity, water, waste disposal, machinery and safety matters.

6

On January 4, 2019, Xi’an Zhonghong, Xi’an TCH, and Mr. Chonggong Bai, entered into a Projects Transfer Agreement (the “Agreement”), pursuant to which Xi’an Zhonghong will transfer a CDQ WHPG station (under construction) located in Xuzhou City for Xuzhou Huayu Coking Co., Ltd. (“Xuzhou Huayu Project”) to Mr. Bai for RMB 120,000,000 ($17.52 million). Mr. Bai agreed to transfer all the equity shares of his wholly owned company, Xi’an Hanneng, to the HYREF as repayment for the loan made by Xi’an Zhonghong to HYREF as consideration for the transfer of the Xuzhou Huayu Project. The transfer was completed on February 15, 2019.

Zhongtai Waste Heat Power Generation Energy Management Cooperative Agreement

On December 6, 2013, Xi’an TCH entered into a CDQ and WHPG Energy Management Cooperative Agreement (the “Zhongtai Agreement”) with Xuzhou Zhongtai Energy Technology Co., Ltd. (“Zhongtai”), a limited liability company incorporated in Jiangsu Province, China.

Pursuant to the Zhongtai Agreement, Xi’an TCH will design, build and maintain a 150 ton per hour CDQ system and a 25 MW CDQ WHPG system (the “Project”) and sell the power to Zhongtai, and Xi’an TCH will also build a furnace to generate steam from the waste heat of the smoke pipeline and sell the steam to Zhongtai.

The construction period of the Project is expected to be 18 months from the date when conditions are ready for construction to begin. Zhongtai will start to pay an energy saving fee from the date when the WHPG station passes the required 72-hour test run. The term of payment is 20 years. For the first 10 years of the term, Zhongtai shall pay an energy saving fee at RMB 0.534 ($0.089) per KWH (including value added tax) for the power generated from the system. For the second 10 years of the term, Zhongtai shall pay an energy saving fee at RMB 0.402 ($0.067) per KWH (including value added tax). During the term of the contract the energy saving fee shall be adjusted at the same percentage as the change of local grid electricity price. Zhongtai shall also pay an energy saving service fee for the steam supplied by Xi’an TCH at RMB 100 ($16.67) per ton (including value added tax). Zhongtai and its parent company will provide guarantees to ensure Zhongtai will fulfill its obligations under the Agreement. Upon the completion of the term, Xi’an TCH will transfer the systems to Zhongtai at RMB 1 ($0.16). Zhongtai shall provide waste heat to the systems for no less than 8,000 hours per year and waste gas volume no less than 150,000 Nm3 per hour with a temperature no less than 950°C. If these requirements are not met, the term of the Zhongtai Agreement will be extended accordingly. If Zhongtai wants to terminate the Zhongtai Agreement early, it shall provide Xi’an TCH a 60 day notice and pay the termination fee and compensation for the damages to Xi’an TCH according to the following formula: (i) if it is less than five years into the term when Zhongtai requests termination, Zhongtai shall pay: Xi’an TCH’s total investment amount plus Xi’an TCH’s annual investment return times five years minus the years in which the system has already operated; or (ii) if it is more than five years into the term when Zhongtai requests the termination, Zhongtai shall pay Xi’an TCH’s total investment amount minus total amortization cost (the amortization period is 10 years).

On March 14, 2016, Xi’an TCH entered into a Xuzhou Zhongtai CDQ and Waste Heat Power Generation System Transfer Agreement (the “Transfer Agreement”) with Zhongtai and Xi’an Huaxin New Energy Co., Ltd., a limited liability company incorporated in China (the “Contractor”).

7

The Transfer Agreement provides for the sale to Zhongtai of all the assets of the Project under construction from Xi’an TCH. Additionally, Xi’an TCH will transfer to Zhongtai the Engineering, Procurement and Construction (“EPC”) Contract for the Project, which Xi’an TCH had entered into with the Contractor in connection with the Project. As consideration for the transfer of the Project, Zhongtai is to pay to Xi’an TCH an aggregate purchase price of RMB 167,360,000 ($25.75 million and the “Transfer Price”), on the following schedule: (i) RMB 50,000,000 ($7.69 million) of the Transfer Price was paid within 20 business days from the execution of the Transfer Agreement; (ii) RMB 30,000,000 ($4.32 million) of the Transfer Price was paid within 20 business days upon the completion of the construction of the Project but not later than July 30, 2016; and (iii) RMB 87,360,000 ($13.45 million) of the Transfer Price was to be paid before July 30, 2017. The temporary ownership of the Project was transferred from Xi’an TCH to Zhongtai after the Xi’an TCH received the first payment of RMB 50,000,000, and the full ownership of the Project is to be officially transferred to Zhongtai upon full payment of the Transfer Price. The Zhongtai Agreement is to be terminated and Xi’an TCH will agree not to pursue any breach of contract liability against the Zhongtai under the Zhongtai Agreement when Zhongtai fully pays the Transfer Price according to the terms of the Transfer Agreement. If the Transfer Price is not fully paid on time pursuant to the Transfer Agreement, the Transfer Agreement automatically terminates and Xi’an TCH retains ownership of the Project, and both parties would continue to possess their respective rights and obligations according to the Zhongtai Agreement and assume the liabilities for breach of the Zhongtai Agreement. Xuzhou Taifa Special Steel Technology Co., Ltd. (“Xuzhou Taifa”) has guaranteed the payments by Zhongtai. The Company recorded a $2.82 million loss from this transaction in 2016. In 2016, Xi’an TCH received the first payment of $7.70 million and the second payment of $4.32 million. However, the Company received a repayment commitment letter from Zhongtai on February 23, 2018, in which Zhongtai committed to pay the remaining payment of RMB 87,360,000 ($13.45 million) no later than the end of July 2018; in July 2018, Zhongtai and the Company reached a further oral agreement to extend the repayment term of RMB 87,360,000 ($13.45 million) by another two to three months. In August 2018, the Company received $1,070,000 from Zhongtai; as of March 31, 2019 and December 31, 2018, the Company had receivable from Zhongtai for $11.88 million (with bad debt allowance of $3.56 million). Zhongtai provided an acknowledgement letter to the Company stating they expect to repay the remaining balance of $11.88 million by the end of October 2019, once it resumes normal production.

Formation of Zhongxun

On March 24, 2014, Xi’an TCH incorporated a new subsidiary, Zhongxun Energy Investment (Beijing) Co., Ltd (“Zhongxun”) with registered capital of $5,695,502 (RMB 35,000,000), to be paid no later than October 1, 2028. Zhongxun is 100% owned by Xi’an TCH and is mainly engaged in project investment, investment management, economic information consulting, and technical services. Zhongxun has not yet commenced operations as of the date of this report.

Formation of Yinghua

On February 11, 2015, the Company incorporated a new subsidiary, Shanghai Yinghua Financial Leasing Co., Ltd (“Yinghua”) with registered capital of $30,000,000, to be paid within 10 years from the date the business license is issued. Yinghua is 100% owned by the Company and is mainly engaged in financial leasing, purchase of financial leasing assets, disposal and repair of financial leasing assets, consulting and ensuring of financial leasing transactions, and related factoring business. Yinghua has not yet commenced operations as of the date of this report.

Summary of Sales-Type Leases at March 31, 2019

As of March 31, 2019, the Company had the following sales-type leases: BMPG systems to Pucheng Phase I and II (15 and 11-year terms, respectively).

Asset Repurchase Agreement

During the years ended December 31, 2018 and 2017, the Company entered into or completed the following Asset Repurchase Agreements:

On November 16, 2015, Xi’an TCH entered into a Transfer Agreement of CDQ and a CDQ WHPG system with Rongfeng and Xi’an Huaxin New Energy Co., Ltd., a limited liability company incorporated in China (“Xi’an Huaxin”). The Transfer Agreement provided for the sale to Rongfeng of the CDQ Waste Heat Power Generation Project (the “Project”) from Xi’an TCH. Additionally, Xi’an TCH agreed to transfer to Rongfeng the Engineering, Procurement and Construction (“EPC”) Contract for the CDQ Waste Heat Power Generation Project which Xi’an TCH had entered into with Xi’an Huaxin in connection with the Project. As consideration for the transfer of the Project, Rongfeng will pay to Xi’an TCH an aggregate purchase price of RMB 165,200,000 ($25.45 million), whereby (a) RMB 65,200,000 ($10.05 million) will be paid by Rongfeng to Xi’an TCH within 20 business days after the Transfer Agreement is signed, (b) RMB 50,000,000 ($7.70 million) will be paid by Rongfeng to Xi’an TCH within 20 business days after the Project is completed, but no later than March 31, 2016 and (c) RMB 50,000,000 ($7.70 million) will be paid by Rongfeng to Xi’an TCH no later than September 30, 2016. Mr. Cheng Li, the largest stockholder of Rongfeng, has personally guaranteed the payments. The ownership of the Project was conditionally transferred to Rongfeng within 3 business days following the initial payment of RMB 65,200,000 ($10.05 million) by Rongfeng to Xi’an TCH and the full ownership of the Project has been officially transferred to Rongfeng after it completes the entire payment pursuant to the Transfer Agreement. The Company recorded a $3.78 million loss from this transaction in 2015. The Company received full payment of $25.45 million in 2016.

8

In March 2016, Xi’an TCH entered into a Transfer Agreement of CDQ and a CDQ WHPG system with Zhongtai and Xi’an Huaxin (the “Transfer Agreement”). Under the Transfer Agreement, Xi’an TCH agreed to transfer to Zhongtai all of the assets associated with the CDQ Waste Heat Power Generation Project (the “Project”), which is under construction pursuant to the Zhongtai Agreement. Xi’an Huaxin will continue to construct and complete the Project and Xi’an TCH agreed to transfer all its rights and obligation under the “EPC” Contract to Zhongtai. As consideration for the transfer of the Project, Zhongtai agreed to pay to Xi’an TCH an aggregate transfer price of RMB 167,360,000 ($25.77 million) including payments of: (i) RMB 152,360,000 ($23.46 million) for the construction of the Project; and (ii) RMB 15,000,000 ($2.31 million) as payment for partial loan interest accrued during the construction period. Those amounts have been, or will be, paid by Zhongtai to Xi’an TCH according to the following schedule: (a) RMB 50,000,000 ($7.70 million) was paid within 20 business days after the Transfer Agreement was signed; (b) RMB 30,000,000 ($4.32 million) will be paid within 20 business days after the Project is completed, but no later than July 30, 2016; and (c) RMB 87,360,000 ($13.45 million) will be paid no later than July 30, 2017. Xuzhou Taifa Special Steel Technology Co., Ltd. (“Xuzhou Taifa”) has guaranteed the payments from Zhongtai to Xi’an TCH. The ownership of the Project was conditionally transferred to Zhongtai following the initial payment of RMB 50,000,000 ($7.70 million) by Zhongtai to Xi’an TCH and the full ownership of the Project will be officially transferred to Zhongtai after it completes all payments pursuant to the Transfer Agreement. Xi’an TCH received the first payment of $7.70 million and the second payment of $4.32 million in 2016. The Company recorded a $2.82 million loss from this transaction. As of the date of this report, the Company has not yet received the remaining payment of RMB 87,360,000 ($13.45 million). However, the Company received a repayment commitment letter from Zhongtai on February 23, 2018, in which Zhongtai committed to pay the remaining payment of RMB 87,360,000 ($13.45 million) no later than the end of July 2018. In July 2018, Zhongtai and the Company reached a further oral agreement to extend the repayment term of RMB 87,360,000 ($13.45 million) by another two to three months. In August 2018, the Company received $1,070,000 from Zhongtai. As of March 31, 2019, the Company had receivables from Zhongtai for $11.66 million (with bad debt allowance of $3.50 million). On January 23, 2019, Zhongtai provided an ackno

Corporate History

The Company was incorporated on May 8, 1980 as Boulder Brewing Company under the laws of the State of Colorado. On September 6, 2001, the Company changed its state of incorporation to the State of Nevada. In 2004, the Company changed its name from Boulder Brewing Company to China Digital Wireless, Inc. and on March 8, 2007, again changed its name from China Digital Wireless, Inc. to its current name, China Recycling Energy Corporation. The Company, through its subsidiaries, provides energy saving solutions and services, including selling and leasing energy saving systems and equipment to customers, project investment, investment management, economic information consulting, technical services, financial leasing, purchase of financial leasing assets, disposal and repair of financial leasing assets, consulting and ensuring of financial leasing transactions in the Peoples Republic of China (“PRC”).

Our business is primarily conducted through our wholly-owned subsidiaries, Yinghua and Sifeng, Sifeng’s wholly-owned subsidiaries, Huahong and Shanghai TCH, Shanghai TCH’s wholly-owned subsidiaries, Xi’an TCH, Xi’an TCH’s wholly-owned subsidiary Erdos TCH and Xi’an TCH’s 90% owned and Shanghai TCH’s 10% owned subsidiary Xi’an Zhonghong New Energy Technology Co., Ltd., and Zhongxun. Shanghai TCH was established as a foreign investment enterprise in Shanghai under the laws of the PRC on May 25, 2004, and currently has registered capital of $29.80 million. Xi’an TCH was incorporated in Xi’an, Shaanxi Province under the laws of the PRC in November 2007. Erdos TCH was incorporated in April 2009. Huahong was incorporated in February 2009. Xi’an Zhonghong New Energy Technology Co., Ltd. was incorporated in July 2013. Xi’an TCH owns 90% and Shanghai TCH owns 10% of Zhonghong. Zhonghong provides energy saving solutions and services, including constructing, selling and leasing energy saving systems and equipment to customers. Zhongxun was incorporated in March 2014, and is a wholly-owned subsidiary of Xi’an TCH.

Our Offices

We are headquartered in China. Our principal executive offices are located at 4/F, Tower C, Rong Cheng Yun Gu Building, Keji 3rd Road, Beilin District, Xi’an City, Shaanxi Province, China, and our telephone number at this location is +86-29-8769-1098.

Other Information

For a complete description of our business, financial condition, results of operations and other important information, we refer you to our filings with the Securities and Exchange Commission (the “SEC”) that are incorporated by reference in this prospectus, including our Annual Report on Form 10-K for the year ended December 31, 2018. For instructions on how to find copies of these documents, please see the section titled “Incorporation of Certain Information by reference” beginning on page 54 of this prospectus.

9

THE OFFERING

| Common stock offered by selling shareholders | Up to 5,658,641 shares, of which (i) 3,754,536 shares of common stock of the registrant, par value $0.001 per share (“Common Stock”), are issuable upon the exercise of common stock purchase warrants of the registrant issued pursuant to private placement concurrently with our registered direct offerings on April 15, 2019 (the “April Warrants”) and October 29, 2018 (the “October Warrants” and together with the April Warrants, the “Investor Warrants”); (ii) 304,105 shares of Common Stock that are issuable upon the exercise of common stock purchase warrants of the registrant issued to the placement agent’s designees in connection with such private placements (the “Agent Warrants,” and together with the Investor Warrants, the “Warrants”); and (iii) 1,600,000 shares of Common Stock sold to a selling shareholder in a prior private placement, dated February 13, 2019. |

| Common stock to be outstanding after the offering | Up to 16,106,498 shares. |

|

Exercise prices, conditions and terms

Use of proceeds |

The October Warrants are currently exercisable, and the April Warrants will be exercisable beginning on the six month anniversary of the date of issuance. The Investor Warrants will expire on the five and one-half year anniversaries of their respective dates of issuance.

138,956 shares of Agent Warrants are current exercisable and the remaining 165,149 shares of Agent Warrants will be exercisable on the later of (i) October 16, 2019, which is six months of the issuance date or (ii) the date on which the Company increases the number of its authorized shares, and shall expire on October 29, 2023 and April 15, 2024, respectively.

We will not receive any proceeds from the sale of shares of our Common Stock by the selling stockholders in this offering. See “Use of Proceeds” for a complete description. |

| Nasdaq Capital Market ticker symbol | CREG |

| Risk Factors | Investing in our Common Stock involves a high degree of risk. You should carefully review and consider the “Risk Factors” beginning on page 11 of this prospectus, which incorporates by reference risk factors set forth in our most recent Annual Report on Form 10-K. |

The number of shares of our common stock outstanding after the offering is based on 16,106,498 shares of our common stock outstanding as of May 23, 2019, which excludes 4,058,641 shares of our Common Stock reserved for issuance upon exercise of the Warrants outstanding as of May 23, 2019.

10

An investment in our securities involves significant risks. You should carefully consider each of the risk factors set forth in our most recent Annual Report on Form 10-K, which was filed with the SEC on April 16, 2019, as amended by that Form 10-K/A filed on April 29, 2019, and as may be updated from time to time by our Quarterly Reports on Form 10-Q and other SEC filings filed after such annual report, and future filings with the SEC, which are incorporated by reference into this prospectus. Before making an investment decision, you should carefully consider these risks as well as other information we include or incorporate by reference in this prospectus and any prospectus supplement. Any of these risks and uncertainties could have a material adverse effect on our business, financial condition, cash flows and results of operations. If that occurs, the trading price of our common stock could decline materially and you could lose all or part of your investment.

The risks we have incorporated by reference into this prospectus are not the only risks we face. We may experience additional risks and uncertainties not currently known to us, or as a result of developments occurring in the future. Conditions that we currently deem to be immaterial may also materially and adversely affect our business, financial condition, cash flows, results of operations and prospects.

Risks Related to our Common Stock

The market price for our common stock may be volatile.

The market price for our common stock is highly volatile and subject to wide fluctuations in response to factors including the following:

| ● | actual or anticipated fluctuations in our quarterly operating results; |

| ● | announcements of new services by us or our competitors; |

| ● | announcements by our competitors of significant acquisitions, strategic partnerships, joint ventures or capital commitments; |

| ● | changes in financial estimates by securities analysts; |

| ● | conditions in the energy recycling market; |

| ● | changes in the economic performance or market valuations of other companies involved in the same industry; |

| ● | changes in accounting standards, policies, guidance, interpretation or principles; |

| ● | loss of external funding sources; |

| ● | failure to maintain compliance with NASDAQ listing rules; |

| ● | additions or departures of key personnel; |

| ● | potential litigation; |

| ● | conditions in the market; or |

| ● | relatively small size of shares of our common stock available for purchase. |

In addition, the securities markets from time to time experience significant price and volume fluctuations that are not related to the operating performance of particular companies. These market fluctuations may also materially and adversely affect the market price of our common stock.

11

Shareholders could experience substantial dilution.

We may issue additional shares of our capital stock to raise additional cash for working capital. If we issue additional shares of our capital stock, our shareholders will experience dilution in their respective percentage ownership in the company.

We have no present intention to pay dividends.

We have not paid dividends or made other cash distributions on our common stock during any of the past three years, and we do not expect to declare or pay any dividends in the foreseeable future. We intend to retain any future earnings for working capital and to finance current operations and expansion of our business.

A large portion of our common stock is controlled by a small number of shareholders.

A large portion of our common stock is held by a small number of shareholders. As a result, these shareholders are able to influence the outcome of shareholder votes on various matters, including the election of directors and extraordinary corporate transactions including business combinations. In addition, the occurrence of sales of a large number of shares of our common stock, or the perception that these sales could occur, may affect our stock price and could impair our ability to obtain capital through an offering of equity securities. Furthermore, the current ratios of ownership of our common stock reduce the public float and liquidity of our common stock which can in turn affect the market price of our common stock.

We may be unable to maintain compliance with NASDAQ Marketplace Rules which could cause our common stock to be delisted from the NASDAQ Capital Market. This could result in the lack of a market for our common stock, cause a decrease in the value of our common stock, and adversely affect our business, financial condition and results of operations.

Under the NASDAQ Marketplace Rules our common stock must maintain a minimum price of $1.00 per share for continued inclusion on the NASDAQ Capital Market. The per share price of our common stock has fluctuated significantly. We cannot guarantee that our stock price will remain at or above $1.00 per share and if the price again drops below $1.00 per share, the stock could become subject to delisting. If our common stock is delisted, trading of the stock will most likely take place on an over-the-counter market established for unlisted securities. An investor is likely to find it less convenient to sell, or to obtain accurate quotations in seeking to buy, our common stock on an over-the-counter market, and many investors may not buy or sell our common stock due to difficulty in accessing over-the-counter markets, or due to policies preventing them from trading in securities not listed on a national exchange or other reasons. For these reasons and others, delisting would adversely affect the liquidity, trading volume and price of our common stock, causing the value of an investment in us to decrease and having an adverse effect on our business, financial condition and results of operations by limiting our ability to attract and retain qualified executives and employees and limiting our ability to raise capital.

On June 19, 2015, the Company was notified by The NASDAQ Stock Market (the “NASDAQ”) that the Company was not in compliance with the $1.00 minimum closing bid price requirement under the NASDAQ Listing Rules (the “Minimum Closing Bid Price”) and the Company was afforded 180 calendar days, or until December 16, 2015, to regain compliance with the requirement of Minimum Closing Bid Price. The Company did not regain compliance with the minimum $1.00 bid price per share by December 16, 2015. On December 7, 2015, the Company transferred the listing of its securities from The NASDAQ Global Market to The Nasdaq Capital Market (the “Capital Market”). On December 17, 2015, the Company received a letter from NASDAQ indicating that NASDAQ determined that the Company is eligible for an additional 180 calendar day period, or until June 13, 2016 (the “Second Compliance Period”), to regain compliance. NASDAQ’s determination was based on the Company meeting the continued listing requirement for market value of publicly held shares and all other applicable requirements for initial listing on the Capital Market with the exception of the bid price requirement, and the Company’s written notice to NASDAQ of its intention to cure the deficiency during the Second Compliance Period by effecting a reverse stock split, if necessary.

On May 24, 2016, the Company filed with the Nevada Secretary of State’s office a Certificate of Change, by which the Company authorized and approved a 1-for-10 reverse stock split of the Company’s authorized shares of common stock from 200,000,000 shares to 20,000,000 shares, accompanied by a corresponding decrease in the Company’s issued and outstanding shares of common stock (the “Reverse Stock Split”). The common stock continues to have a par value of $0.001. The Certificate of Change became effective on May 25, 2016, and the Reverse Stock Split became effective for trading purposes at the market opening on May 26, 2016, at which time the Company’s common stock began trading on the Nasdaq Capital Market on a split-adjusted basis under the symbol “CREG.” The CUSIP number for the Company’s common stock post-Reverse Stock Split is 168913200.

12

Risks Related to Our Business Operations

In recent years, the growth of Chinese economy has experienced slowdown, and if the growth of the economy continues to slow or if the economy contracts, our financial condition may be materially and adversely affected.

The rapid growth of the PRC economy has historically resulted in widespread growth opportunities in industries across China. As a result of the global financial crisis and the inability of enterprises to gain comparable access to the same amounts of capital available in past years, the business climate has changed and growth of private enterprise in the PRC have slowed down. An economic slowdown could have an adverse effect on our financial condition. Further, if economic growth slows, and if, in conjunction, inflation is allowed to proceed unchecked, our costs would likely increase, and there can be no assurance that we would be able to increase our prices to an extent that would offset the increase in our expenses.

We depend on the waste energy of our customers to generate electricity.

We acquire waste pressure, heat and gases from steelworks, cement, coking or metallurgy plants and use these to generate power. Therefore, our power generating capacity depends on the availability of an adequate supply of our “raw materials” from our customers. If we do not have enough supply, power generated for those customers will be impeded. Since our contracts are often structured so that we receive compensation based on the amount of energy we supply, a reduction in production may cause problems for our revenues and results of operations.

Our revenue depends on gaining new customers and project contracts and purchase commitments from customers.

Currently and historically, we have only had a limited number of projects in process at any time. Thus, our revenues have historically resulted, and are expected to continue in the immediate future to result, primarily from the sale and operation of our waste energy recycling projects that, once completed, typically produce ongoing revenues from energy production. Customers may change or delay orders for any number of reasons, such as force majeure or government approval factors that are unrelated to us. As a result, in order to maintain and expand our business, we must continue to develop and obtain new orders. However, it is difficult to predict whether and when we will receive such orders or project contracts due to the lengthy process, which may be affected by factors that we do not control, such as market and economic conditions, financing arrangements, commodity prices, environmental issues and government approvals.

We may require additional funds to run our business and may be required to raise these funds on terms which are not favorable to us or which reduce our stock price.

We may need to complete additional equity or debt financings to fund our operations. Our inability to obtain additional financing could adversely affect our business. Financings may not be available at all or on terms favorable to us. In addition, these financings, if completed, may not meet our capital needs and could result in substantial dilution to our stockholders.

Changes in the economic and credit environment could have an adverse effect on demand for our projects, which would in turn have a negative impact on our results of operations, our cash flows, our financial condition, our ability to borrow and our stock price.

Since late 2008 and continuing through 2018, global market and economic conditions have been disrupted and volatile. Concerns over slowdown of Chinese economy, geopolitical issues, the availability and cost of credit, to this increased volatility. These factors, combined with declining business and consumer confidence and increased unemployment, precipitated a global recession. It is difficult to predict how long the current economic conditions will persist or whether they will deteriorate further. As a result, these conditions could adversely affect our financial condition and results of operations.

The slow growth of global economy has also resulted in tighter credit conditions, which may lead to higher financing costs. Although poor market conditions can act as an incentive for our customers to reduce their energy costs, if the global economic slowdown persists and has material adverse effects on our customers’ business, our customers may delay or cancel their plan of installing waste energy recycling projects.

13

Decreases in the price of coal, oil and gas or a decline in popular support for “green” energy technologies could reduce demand for our waste energy recycling projects, which could materially harm our ability to grow our business.

Higher coal, oil and gas prices provide incentives for customers to invest in “green” energy technologies such as our waste energy recycling projects that reduce their need for fossil fuels. Conversely, lower coal, oil and gas prices would tend to reduce the incentive for customers to invest in capital equipment to produce electric power or seek out alternative energy sources. Demand for our projects and services depends in part on the current and future commodity prices of coal, oil and gas. We have no control over the current or future prices of these commodities.

In addition, popular support by governments, corporations and individuals for “green” energy technologies may change. Because of the ongoing development of, and the possible change in support for, “green” energy technologies we cannot assure you that negative changes to this industry will not occur. Changes in government or popular support for “green” energy technologies could have a material adverse effect on our business, prospects and results of operations.

Changes in the growth of demand for or pricing of electricity could reduce demand for our waste energy recycling projects, which could materially harm our ability to grow our business.

Our revenues depend on our ability to provide savings on energy costs for our clients. According to the National Bureau of Statistics of the PRC, China’s total electricity consumption in 2018 was 6.84 trillion kilowatt-hours, up 8.5 percent year on year, the highest growth rate since 2012. The growth in electricity consumption increases due to the continued development of the Chinese economy. However, such growth is unpredictable and depends on general economic conditions and consumer demand, both of which are beyond our control. Furthermore, pricing of electricity in the PRC is set in advance by the state or local electricity administration and may be artificially depressed by governmental regulation or influenced by supply and demand imbalances. If these changes reduce the cost of electricity from traditional sources of supply, the demand for our waste energy recycling projects could be reduced, and therefore, could materially harm our ability to grow our business.

Our insurance may not cover all liabilities and damages.

Our industry can be dangerous and hazardous. The insurance we carry might not be enough to cover all the liabilities and damages that may be caused by potential accidents.

A downturn in the Chinese economy may slow down our growth and profitability.

The growth of the Chinese economy has been uneven across geographic regions and economic sectors. There is no assurance that growth of the Chinese economy will be steady or that any downturn will not have a negative effect on our business. Our profitability will decrease if less energy is consumed due to a downturn in the Chinese economy.

14

Our heavy reliance on the experience and expertise of our management may cause adverse impacts on us if a management member departs.

We depend on key personnel for the success of our business. Our business may be severely disrupted if we lose the services of our key executives and employees or fail to add new senior and middle managers to our management.

Our future success is heavily dependent upon the continued service of our key executives. We also rely on a number of key technology staff for the operation of our company. Our future success is also dependent upon our ability to attract and retain qualified senior and middle managers to our management team. If one or more of our current or future key executives or employees are unable or unwilling to continue in their present positions, we may not be able to easily replace them, and our business may be severely disrupted. In addition, if any of these key executives or employees joins a competitor or forms a competing company, we could lose customers and suppliers and incur additional expenses to recruit and train personnel. We do not maintain key-man life insurance for any of our key executives.

We may need more capital for the operation and failure to raise capital we need may delay the development plan and reduce the profits.

If we do not have adequate income or our capital cannot meet the requirement for expansion of operations, we will need to seek financing to continue our business development. If we fail to acquire adequate financial resources at acceptable terms, we might have to postpone our proposed business development plans and reduce projections of our future incomes.

Our use of a “Build-Operate-Transfer” model requires us to invest substantial financial and technical resources in a project before we deliver a waste energy recycling project.

We use a “Build-Operate-Transfer” model to provide our waste energy recycling projects to our customers. This process requires us to provide significant capital at the beginning of each project. The design, construction and completion of a waste energy recycling project is highly technical and the time necessary to complete a project can take three to 12 months without any delays, including delays outside our control such as from the result of customer’s operations, and we incur significant expenses as part of this process. Our initial cash outlay and the length of the delivery time makes us particularly vulnerable to the loss of a significant customer or contract because we may be unable to quickly replace the lost cash flow.

Our BOT model and the accounting for our projects as sales-type leases could result in a difference between our revenue recognition and our cash flows.

While we recognize a large portion of the revenue from each project when it goes on-line, all of the cash flow from the project is received in even monthly payments across the term of the lease. Although our revenues may be high, the initial cash outlay required for each project is substantial and even with the recovery of this cost in the early years of each lease, we may need to raise additional capital resulting in a dilution in your holdings. This discrepancy between revenue recognition and cash flow could also contribute to volatility in our stock price.

There is collection risk associated with payments to be received over the terms of agreements with customers of our waste energy recycling projects.

We depend in part on the viability of our customers for collections under our BOT model. Customers may experience financial difficulties that could cause them to be unable to fulfill their contractual payment obligations to us. Although our customers usually provide collateral or other guarantees to secure their obligations to provide the minimum electricity income from the waste energy recycling projects, there is no guarantee that such collateral will be sufficient to meet all obligations under the respective contract. As a result, our future revenues and cash flows could be adversely affected.

15

We may not be able to assemble and deliver our waste energy recycling projects as quickly as customers may require which could cause us to lose sales and could harm our reputation.