UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

| ☑ | ANNUAL REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended June 30, 2016.

| ☐ | TRANSITION REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from __________ to ____________.

Commission file number 0-12697

DYNATRONICS CORPORATION

(Exact name of registrant as specified in its charter)

|

UTAH

|

87-0398434

|

| (STATE OR OTHER JURISDICTION OF INCORPORATION OR ORGANIZATION) |

(I.R.S. EMPLOYER IDENTIFICATION NO.)

|

|

7030 PARK CENTRE DRIVE, COTTONWOOD HEIGHTS, UTAH

|

84121-6618

|

|

(ADDDRESS OF PRINCIPAL EXECUTIVE OFFICES)

|

(zIP CODE)

|

|

REGISTRANT'S TELEPHONE NUMBER, INCLUDING AREA CODE (801) 568-7000

|

|

Securities registered under Section 12(b) of the Exchange Act: None

Securities registered under Section 12(g) of the Exchange Act:

Common Stock, no par value

(Title of class)

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Act. Yes ☐ No ☑

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☑

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☑ No ☐

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes þ No ☐

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K.☑

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of "large accelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12(b)-2 of the Exchange Act.

|

LARGE ACCELERATED FILER ☐

|

ACCELERATED FILER ☐

|

|

NON-ACCELERATED FILER ☐ (DO NOT CHECK IF A SMALLER REPORTING COMPANY)

|

SMALLER REPORTING COMPANY ☑

|

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12(b)-2 of the Act). Yes ☐ No ☑

The aggregate market value of the voting and non-voting common stock held by non-affiliates of the registrant as of December 31, 2015 (the last day of the registrant's most recently completed second fiscal quarter) was approximately $7.0 million, based on the average bid and asked price of the common stock on that date.

As of September 22, 2016, there were 2,846,678 shares of the registrant's common stock outstanding.

Documents Incorporated by Reference

The registrant incorporates information required by Part III (Items 10, 11, 12, 13, and 14) of this report by reference to the registrant's definitive proxy statement to be filed pursuant to Regulation 14A for its 2016 Annual Shareholders Meeting.

TABLE OF CONTENTS

PART I

PART I

Forward-Looking Statements

The statements contained in this Annual Report on Form 10-K that are not purely historical are considered to be "forward-looking statements" within the meaning of the Private Securities Litigation Reform Act of 1995 and Section 21E of the Securities Exchange Act of 1934, as amended (the "Exchange Act"). These forward-looking statements include, but are not limited to: any projections of net sales, earnings, or other financial items; any statements of the strategies, plans and objectives of management for future operations; any statements concerning proposed new products or developments; any statements regarding future economic conditions or performance; any statements of belief; and any statements of assumptions underlying any of the foregoing. Forward-looking statements may include the words "may," "will," "estimate," "intend," "continue," "believe," "expect" or "anticipate" and any other similar words. These statements represent our expectations, beliefs, anticipations, commitments, intentions, and strategies regarding the future and include, but are not limited to, the risks and uncertainties outlined in Item 1A Risk Factors and Item 7 Management's Discussion and Analysis of Financial Condition and Results of Operations. Readers are cautioned that actual results could differ materially from the anticipated results or other expectations that are expressed in forward-looking statements within this report. The forward-looking statements included in this report speak only as of the date hereof, and we undertake no obligation to publicly update or revise any forward-looking statement, whether as a result of new information, future events or otherwise, except as required by law.

Unless the context otherwise requires, all references in this report to "registrant," "we," "us," "our," "Dynatronics" or the "Company" refer to Dynatronics Corporation, a Utah corporation and its wholly owned subsidiary. In this Annual Report on Form 10-K, unless otherwise expressly indicated, references to "dollars" and "$" are to United States dollars.

ITEM 1. Business

Overview

Dynatronics Corporation, headquartered in Cottonwood Heights, Utah, is a manufacturer and distributor of physical medicine products. We employ 153 people in the United States who are dedicated to providing innovative therapeutic solutions to practitioners, so they can concentrate on providing the best care to their patients. We offer customers a one-stop shop for their medical equipment and supply needs, including electrotherapy and ultrasound therapy, phototherapy, medical supplies, treatment tables, and exercise products. Revenues grew to $30.4 million in 2016, an increase of 4.4% from $29.1 million in 2015.

Dynatronics was founded on a technology platform to treat patients non-invasively using microprocessor-based therapeutic devices. Over the past 35+ years, we have grown by building upon these core therapeutic technologies, acquiring businesses in related medical fields, vertically integrating with our distribution channel and developing products to further meet the needs of our target customers.

Vision

We aspire to become a global leader in providing therapeutic equipment and physical medicine technology that helps medical professionals treat their patients effectively and non-invasively, while at the same time, providing a high quality investment for shareholders. We believe we will achieve these goals by evaluating and pursuing the best business combinations, strengthening our brand and generally becoming a top player in the markets in which we compete.

Strategy

There are three areas of focus for increasing growth: 1) introducing new products to the market through internal development, 2) geographic expansion, and 3) strategic corporate development.

Our executive leadership team has set forth the following near-term objectives aligned to this strategy:

New Product Development. Our investment in product development is intended to result in a pipeline of innovative products. Consistent with our competitive advantage as a manufacturer, our product development efforts will focus on therapeutic technologies and other projects with the potential for timely and material returns on investment.

1

Geographic and Market Expansion. We see an opportunity to accelerate revenue growth by strengthening our U.S. presence through the addition of direct sales reps and dealers in several key areas around the country. In addition, we generate less than 5% of our revenues from markets outside the United States, whereas competing medical technology companies in our market produce a much larger percentage of their revenues internationally. Therefore, we see an opportunity to accelerate revenue growth by increasing our international presence and we are expanding our distribution network in key international markets. We expect the commercial focus on key markets and a mix of products that carry both high margins and relevant price points will increase our international business as a share of our overall revenues.

We continue to show strength in the private practice market of physical therapy as well as the sports medicine market. Our expansion efforts over the next year will include strategic plans for the post-acute care market characterized by rehab hospitals, skilled nursing facilities and nursing homes. This market expansion dovetails well with the geographic expansions we are planning.

Strategic Business Development. Over the years, we have successfully acquired businesses to grow our operations. Going forward, our business development program will be an important part of our strategy to increase scale. Acquisitions, in particular, may be pursued as a means of expanding product offerings, growing domestic or international distribution, adding a technology, increasing the scale of one of our current portfolios, or providing access to complementary or strategic growth areas. We intend to focus primarily on the therapeutic areas of patient care and medical supply products. In addition to acquisitions, we will be investing in targeted additions to our sales organization to improve market coverage. Our business development capabilities are increasingly important to remain competitive in today's environment.

Company

Dynatronics is a Utah corporation formed on April 29, 1983. Our predecessor company, Dynatronics Research Company, was formed in 1979. We operate on a fiscal year basis, ending on June 30. For example, reference to fiscal year 2016 refers to the fiscal year ended June 30, 2016. All references to financial statements in this report refer to the consolidated financial statements of Dynatronics Corporation.

Recent Developments

In May and June 2016, we announced several changes in executive management. Larry K. Beardall, former Executive Vice-President of Marketing and Strategic Planning, left the Company management team and Board of Directors effective June 3, 2016. His management responsibilities have been assumed by our Senior Vice-President of Sales, Jeff Gephart. We also announced the planned retirement of Kelvyn H. Cullimore, Sr., the Company's founder and former chairman and president, effective December 31, 2016. He has been on part time status for the past several years with duties that included managing the Company's international efforts. He will transition his responsibilities to our new Director of International Sales over the remainder of the calendar year. Finally, effective July 8, 2016, Bob Cardon, Vice President of Administration announced his retirement. These changes in executive management are consistent with the implementation of the strategic plans outlined in our corporate strategy.

In August 2016, we completed the release of an upgraded version of our core Dynatron Solaris® and 25 SeriesTM lines of therapeutic modalities. This new product innovation provides incremental improvements that qualify these products to meet the latest medical device safety standards (IEC 60601-1), enables us to simplify manufacturability and serviceability, upgrades components, and adds usability features for ultrasound and better positions the products internationally without raising the price to our customers. While these are incremental improvements, the cumulative effect will make the product line more attractive to the market and easier to manufacture and service.

In September 2016, we introduced the new Dynatron® 125B stand-alone ultrasound device. This device is a successor to the Dynatron® 125B stand-alone product which was discontinued last year due to component obsolescence. The new Dynatron® 125B incorporates the proprietary features of its predecessor but is designed to be lower cost and even more user friendly.

2

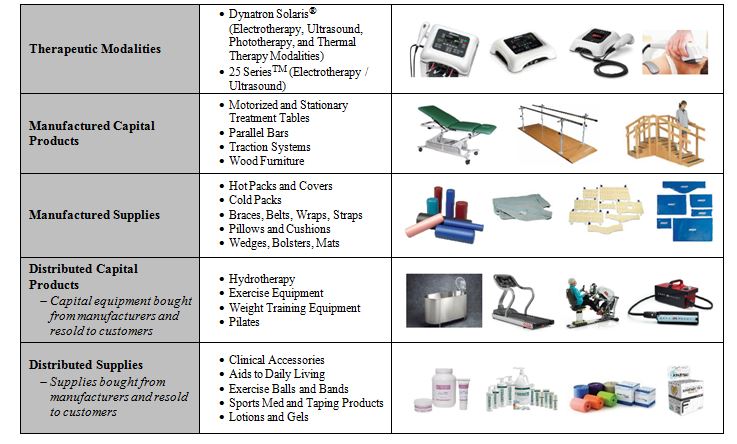

Our Products

We sell products we manufacture as well as those manufactured by others. Net sales (excluding freight, repairs, and miscellaneous items) in fiscal year 2016 were split 56%-44%, favoring distribution of products manufactured by others. However, 55% of gross profit for the year was generated by products that we manufacture.

Our products include a broad line of medical equipment for physical medicine applications including therapy devices, medical supplies and soft goods, treatment tables and rehabilitation equipment. They are used primarily by physical therapists, chiropractors, sports medicine practitioners, podiatrists, physicians and other physical medicine professionals.

Physical Medicine Products

Electrotherapy – The therapeutic effects of electrical energy have occupied an important position in physical medicine for over six decades. There has been an evolution through the years to use the most effective and painless waveforms and frequencies to produce patient comfort and successful treatment of pain and related physical ailments. Medium frequency alternating currents, which we use primarily in our electrotherapy devices, are believed to be the most effective and comfortable for patients. Electrotherapy can be effective in treating chronic intractable pain and/or acute post-traumatic pain, increasing local blood circulation, relaxation of muscle spasms, prevention or retardation of disuse atrophy, and muscle re-education.

Therapeutic Ultrasound – Ultrasound therapy provides therapeutic deep heat to soft tissue through the introduction of sound waves into the body. It is one of the most common modalities used in physical therapy for treating pain, muscle spasms and joint contractures. The new stand-alone Dynatron® 125B ultrasound device was introduced in September 2016.

We market a broad line of devices that include electrotherapy, ultrasound or a combination of both of these modalities in a single device. The Dynatron Solaris® Plus and Dynatron 25 SeriesTM include combination devices that provide electrotherapy and ultrasound therapy treatments to patients. The Dynatron 25 SeriesTM devices target the lower-priced segment of the market. The Dynatron Solaris® Plus products add Tri-Wave phototherapy capabilities as well as thermal therapy available through the patented ThermoStim probe accessory to electrotherapy and ultrasound combination devices. In August 2016, we released upgraded versions of these combination products which have improved their design, manufacturing process, and international reach. We will continue to develop our core therapy technology and remain a leader in the design, manufacture and sale of therapy equipment.

3

Phototherapy – Phototherapy has been popular among physical medicine practitioners for its ability to provide topical heating to increase local blood circulation, provide temporary relief of minor muscle and joint aches, pain and stiffness, as well as to treat minor pain and stiffness associated with arthritis. The wavelength of the light determines the depth of penetration – the longer the wavelength, the deeper the penetration. The benefits of phototherapy have been documented by numerous research studies published over the past four decades that indicate applications beyond those approved for use in the United States including such areas as accelerated wound healing.

Our Dynatron Solaris® 709Plus, 708Plus, 707Plus, 706Plus, and 705Plus units, as well as the DX2 devices, all feature phototherapy technology. The Dynatron Solaris® Plus products are capable of powering either the handheld Tri-Wave phototherapy probe or the larger Tri-Wave phototherapy pads. The Dynatron® Tri-Wave pad is capable of treating larger areas of the body via unattended infrared, red and blue wavelength phototherapy. The Dynatron® Tri-Wave phototherapy probe is used in an attended mode targeting specific treatment sites by the practitioner. The DX2 device powers other phototherapy products such as the 880 probe that provides primarily infrared therapy at 880nm.

Thermal Therapy – For many decades, physical therapists and other medical practitioners have relied on cold compression therapy as a primary standard of care for treating patient injuries and for post-surgical conditions. In August 2015, we announced a patent for "Systems and Methods for Providing a Thermo-electro-stimulation Probe Device". The innovative ThermoStim Probe incorporates technology designed to deliver thermal therapy (hot or cold) together with electrotherapy treatments. Over the past year, this novel technology has become popular among physical therapists, sports medicine practitioners and athletic trainers for increasing blood circulation, reducing muscle spasm and relieving pain in patients and athletes.

The Dynatron® ThermoStim Probe employs state-of-the-art technology providing precise temperature control while moving beyond the current standard by eliminating the need for ice when providing cold therapy. This probe is an accessory to the Dynatron Solaris® Plus family of products.

Oscillation Therapy – Soft tissue oscillation therapy has been used for the treatment of pain in Europe for over 16 years, yet it has been used in the United States market for only approximately 10 years. The Dynatron® X5 Oscillation Therapy device creates an electrostatic field within the patient, resulting in a highly effective treatment for reducing minor muscle aches and pains.

Iontophoresis – Iontophoresis uses electrical current to transdermally deliver drugs such as lidocaine for localized treatment of inflammation without the use of needles. The Dynatron® iBoxTM, our proprietary iontophoresis device, provides support for this market. We also distribute a line of proprietary iontophoresis electrodes under the brand name of Dynatron® Ion electrodes, along with other types of iontophoresis electrodes from other manufacturers. Since the Medical Device Amendment was added to the Food Drug and Cosmetic Act in 1976, iontophoresis has been classified as a Class III device pending final determination by the Food and Drug Administration (FDA) as to whether manufacturers would be required to submit a Pre-Market Approval Application (PMA) to legally market the device. On July 26, 2016, FDA announced that iontophoresis applications for all uses other than cystic fibrosis would be permanently reclassified as a Class II device and no PMA would be required.

Traction Therapy – Dynatronics offers a complete line of traction equipment including traction devices, traction tables, traction harnesses and related positioning products. Our traction products are designed to provide static, intermittent, and cycling distraction forces to relieve pressures on structures that may be causing low back or neck pain. It relieves pain through decompression of intervertebral discs or unloading due to distraction and positioning.

Manufactured Medical Supplies and Soft Goods – We currently manufacture or have manufactured for us over 700 medical supply and soft goods products including hot packs, cold packs, lumbar rolls, exercise balls, wrist splints, ankle weights, cervical collars, slings, cervical pillows, bolsters, positioning wedges, back cushions, weight racks, rehabilitation products, back and wrist braces, mat tables, work tables, training stairs, and parallel bars.

Manufactured Treatment Tables and Rehabilitation Equipment – We sell motorized and manually operated physical therapy treatment tables, rehabilitation parallel bars, and other specialty rehabilitation products that we manufacture or have manufactured to our specifications.

Distributed Medical Equipment, Supplies and Soft Goods – Over the years, we have significantly expanded the number of products from other manufacturers that we distribute including additional exercise equipment, massage therapy products, treatment tables, parallel bars, hand therapy products, hot and cold therapy products, lotions and gels, paper products, athletic tape, canes and crutches, reflex hammers, stethoscopes, splints, elastic wraps, exercise weights, exercise bands and tubing, walkers, treadmills, stair climbers, heating units for hot packs, whirlpools, gloves, electrodes, hydrotherapy and aquatic exercise products, clinical supplies, aids to daily living products, cardio equipment, diagnostic and evaluation products, orthopedic supports, patient positioners, rehabilitation equipment, traction equipment, wound and edema care products, Pilates and yoga equipment, nutritional supplements, emergency care products and portable electrotherapy products.

4

We market our products through direct sales representatives, independent dealers, our e-commerce website and our product catalog. We continually seek to update our line of manufactured and distributed medical supplies and soft goods.

Sales Mix among Key Products

No single product accounted for more than 10% of total revenues in fiscal years 2016 and 2015. Sales of products manufactured by the Company represented approximately 44% of total product sales in fiscal years 2016 and 2015. Distribution of products manufactured by other suppliers accounted for the balance of our product sales in those years.

Patents and Trademarks

Patents. We hold two United States patents on our thermoelectric technology that will remain in effect until July 2032. We also hold a United States patent on our combination traction/phototherapy technology that will remain in effect until December 2026 and a United States patent on our phototherapy technology that will remain in effect until August 2025. In addition, we hold a United States patent on our microdermabrasion technology, featured in our discontinued Synergie® product line. This patent will remain in effect until February 2020.

Trademarks. We have developed and we use registered trademarks in our business, particularly relating to our corporate and product names. The trademark "Dynatron®" has been registered with the United States Patent and Trademark Office. In addition, United States trademark registrations have been obtained for the trademarks: Dynatron Solaris®, Synergie®, Synergie Peel®, Dynaheat®, BodyIce®, and Nutura®. Our materials are also protected under copyright laws, both in the United States and internationally.

Federal registration of a trademark enables the registered owner of the mark to bar the unauthorized use of the registered mark in connection with a similar product in the same channels of trade by any third party anywhere in the United States, regardless of whether the registered owner has ever used the trademark in the area where the unauthorized use occurs. We may register additional trademarks in countries where our products are or may be sold in the future. Protection of registered trademarks in some jurisdictions may not be as extensive as the protection in the United States.

We also claim ownership and protection of certain product names, unregistered trademarks, and service marks under common law. Common law trademark rights do not provide the same level of protection that is afforded by the registration of a trademark. In addition, common law trademark rights are limited to the geographic area in which the trademark is actually used. We believe these trademarks, whether registered or claimed under common law, constitute valuable assets, adding to recognition of Dynatronics and the effective marketing of Dynatronics products. As long as a registered mark is in use on the goods or services claimed in the registration, the registered owner of the mark may renew the registration. There is no limit to how many times registration can be renewed, subject to the payment of a renewal fee. We believe these proprietary rights have been and will continue to be important in enabling us to compete.

Trade Secrets. We own certain intellectual property, including trade secrets that we seek to protect, in part, through confidentiality agreements with key employees and other parties involved in research and development. Even where these agreements exist, there can be no assurance that these agreements will not be breached, that we would have adequate remedies for any breach, or that our trade secrets will not otherwise become known to or independently developed by competitors.

We intend to protect our legal rights in our intellectual property by all appropriate legal action. Consequently, we may become involved from time to time in litigation to determine the enforceability, scope, and validity of any of the foregoing proprietary rights. Any patent litigation could result in substantial cost and divert the efforts of management and technical personnel.

5

Warranty Service

We provide a warranty on all products we manufacture for time periods ranging in length from 90 days to five years from the date of sale. We service warranty claims on these products primarily at our Cottonwood Heights, Utah and Chattanooga, Tennessee facilities depending on the service required. We also have field service available in other parts of the United States and Canada. Our warranty policies are comparable to warranties generally available in the industry. Warranty claims were approximately $144,000 and $146,000 in fiscal years 2016 and 2015, respectively.

Products we distribute carry warranties provided by the manufacturers of those products. We do not generally supplement these warranties or provide unreimbursed warranty services for distributed products. We also sell accessory items for our manufactured products that are supplied by other manufacturers. These accessory products carry warranties from their original manufacturers without supplement from us.

Customers and Markets

We sell our products primarily to licensed practitioners such as physical therapists, chiropractors, podiatrists, sports medicine specialists, medical doctors, hospitals and clinics, and athletic trainers. We utilize direct sales representatives and independent sales representatives to sell our products together with a network of over 40 independent dealers, with revenue greater than $50,000, throughout the United States and internationally. We have relationships with more than 100 additional independent dealers we are working with to strengthen distribution. Most dealers purchase and take title to the products, which they then sell to end users.

We have entered into agreements with Group Purchasing Organizations (GPOs) and regional/national chains of physical therapy clinics and hospitals. We sell our products directly to these clinics and hospitals as well as member facilities of the GPO's pursuant to preferred pricing arrangements. We also have preferred pricing arrangements with key customers who commit to purchase certain volumes and varieties of products. No single customer or group of related accounts was responsible for 10% or more of net sales in fiscal years 2016 and 2015.

We export products to approximately 30 different countries. Sales outside North America totaled approximately $850,000 in fiscal year 2016 (or 2.8% of net sales) and $880,000 in fiscal year 2015 (approximately 3.0% of net sales). We are working to expand our distribution channel in international markets. Our Utah facility is certified to the ISO 13485 quality standard for medical device manufacturing. We also have CE Mark approval for our Dynatron Solaris® Plus family of products. In May 2016, we announced the hiring of a new Director of International Sales to lead our international expansion efforts. This new director previously established a global training program for sales representatives at DJO Global and Chattanooga Group. Over the past 10 years, he led the technical sales support effort globally at his former employer and is certified as a Lean and Kaizen facilitator. In the last 12 months, we have sought and received clearance to sell our advanced technology devices in numerous markets around the world. With this new leadership we expect international sales growth to accelerate over the coming year. We have no foreign manufacturing operations. However, we purchase certain products and components from foreign manufacturers.

Competition

We believe our key products are distinguished competitively by our use of the latest technology. Several of our products are protected by patents, or where patents have expired, the proprietary technology on which those patents were based. We believe that the integration of advanced technology in the design of each product has distinguished Dynatronics-branded products in a very competitive market. For example, we were the first company to integrate infrared phototherapy as part of a combination therapy device. The introduction of the ThermoStim probe was the first of its product type on the market. With almost half of our sales generated by products we manufacture, we can focus on quality engineered products at competitive prices. We believe these factors give us an edge over many competitors who are solely distributors of competing products. Furthermore, the addition of direct sales representatives over the course of the last nine years, together with our current expansion of general line dealers, has provided us with improved distribution channels for our products. These distribution channels provide important competitive advantages due to many established relationships with clinics which directly affect the sale and distribution of our manufactured products as well as products of other manufacturers that we distribute, including products from competitors such as Mettler Electronics, manufacturer of the Sonicator brand of electrotherapy and ultrasound therapy products and DJO, manufacturer of the Chattanooga brand of electrotherapy products, and many manufacturers of treatment tables, medical supplies and soft goods. Generally, since the migration of our business model nine years ago from being primarily a manufacturer to being both a manufacturer and a distributor, the competitive landscape takes on different dimensions as outlined below. We believe that Dynatronics is one of only two companies in the physical medicine industry that has a comprehensive direct sales force; the other is Patterson Medical (formerly Sammons Preston), which was purchased in 2015 by Madison Dearborn Partners.

6

Information necessary to determine or reasonably estimate our market share or that of any competitor in any of these markets is not readily available.

Electrotherapy/Ultrasound

We compete in the clinical market for electrotherapy and ultrasound devices with both domestic and foreign companies. Approximately 10 -15 companies produce electrotherapy and/or ultrasound devices directly competitive with our products. Some of these competitors are larger and better established, and have greater resources than Dynatronics. Other than Dynatronics, few companies, domestic or foreign, provide multiple-modality devices, which is one important distinction between us and our competition. Furthermore, we believe no competitor offers three frequencies on multiple-sized soundheads or provides the proprietary electrotherapy features offered in our electrotherapy devices. We believe that our primary domestic competitors that manufacture competitive clinical electrotherapy and ultrasound equipment include DJO Global (Chattanooga Brand), Rich-Mar, Mettler Electronics, and the Metron Division of Patterson Medical.

Phototherapy

Competitors that manufacture and market phototherapy devices include DJO (Chattanooga Brand), Rich-Mar, Erchonia, Apollo, Multi Radiance and MedX. We are aware of only two competitors, DJO and Rich-Mar, that offer a device that includes phototherapy in combination with electrotherapy and ultrasound capabilities in the same device as we do.

Thermal Therapy

Dynatronics is the only company that offers a hand-held accessory, the ThermoStim Probe, that provides thermal therapy in combination with electrotherapy. Other manufacturers such as Game Ready or Thermo-Tek offer thermal therapy in combination with compression therapy, but these are not directly competitive with the Dynatronics ThermoStim probe. Dynatronics is a distributor of Game Ready products.

Medical Supplies and Soft Goods

We compete against various manufacturers and distributors of medical supplies and soft goods, some of which are larger, more established and have greater resources than Dynatronics. Excellent customer service, along with providing online ordering capability and value to customers is of key importance for us to remain competitive in this market. We distribute our own proprietary and manufactured products, as well products manufactured by other companies. While there are many specialized manufacturers in this area such as Core Products International, Inc., DJO, and Performance Health, Inc., most of our competitors are primarily distributors such as Patterson Medical, North Coast Medical and Meyer Distributing. It is not common for manufacturers of products in this category to have direct distribution of their products. Historically these manufacturers have relied on distribution companies like Dynatronics, or the competitors mentioned in this section, for sale of their products. Dynatronics and Patterson Medical are the only two companies with a comprehensive direct sales force. All other competitors of distributed products rely primarily on catalog, inside sales, or internet sales.

Iontophoresis

Our competitors in the iontophoresis market include DJO (Iomed), Rich-Mar, Travanti Pharma and North Coast Medical. DJO (Iomed division) likely enjoys the largest market share. We believe that our strong distribution network is important to our continued ability to compete in this increasingly competitive market. In addition, our products target a lower selling price than the products in this product category.

Treatment Tables

Our primary competition in the treatment table market is from domestic manufacturers including Hill Laboratories Company, Hausmann Industries, Patterson Medical, Bailey Manufacturing, Tri-W-G, DJO, Armedica, Stonehaven, and Clinton Industries. Cardon Industries from Canada is also a competitor. We believe we compete based on our industry experience and product quality. In addition, certain components of the treatment tables are manufactured overseas, which we believe allows for pricing advantages over competitors.

7

Manufacturing and Quality Assurance

We manufacture therapy devices, soft goods and other medical products at our facilities in Cottonwood Heights, Utah and Chattanooga, Tennessee. We purchase some components for our manufactured products from third-party suppliers. All parts and components purchased from these suppliers meet specifications we have established. Trained staff performs all sub-assembly, final assembly and quality assurance procedures. Every effort is made to design Dynatronics products to incorporate component parts and raw materials that are readily available from suppliers.

The development and manufacture of our products is subject to rigorous and extensive regulation by the FDA and other regulatory agencies and authorities in the United States and abroad. In compliance with the FDA's Good Manufacturing Practices, or GMP, we have developed a comprehensive program for processing customer feedback and analyzing product performance trends. By ensuring prompt processing of timely information, we are better able to respond to customer needs and ensure proper operation of the products.

Our Cottonwood Heights facility is certified to ISO 13485:2003 standards for medical products. ISO 13485 is an internationally recognized quality management system standard adopted by over 90 countries. The ISO 13485 certification also allows us to qualify for CE Mark certification. With the CE Mark certification, we are able to market qualified products throughout the European Union and in other countries where CE Mark certification and ISO 13485 certification are recognized.

Products manufactured at our facility in Tennessee are subject to our own internal quality system which is modeled on the quality system implemented at our facility in Utah. While we have not sought ISO certification for the Tennessee facility, we believe our quality system is rigorous and adequate for producing the quality products to which our customers have become accustomed.

Research and Development

Total research and development ("R&D") expenses in fiscal year 2016 were $1.1 million, compared to approximately $925,000 in fiscal year 2015. R&D expenses in 2016 were related to development of therapeutic devices expected to be introduced in fiscal year 2017. R&D expenses represented approximately 3.5% and 3.2% of our net sales in fiscal years 2016 and 2015, respectively. R&D expenditures are expected to remain near current levels in fiscal year 2017.

Regulatory Matters

The manufacture, packaging, labeling, advertising, promotion, distribution and sale of our products are subject to regulation by numerous national and local governmental agencies in the United States and other countries. In the United States, the FDA regulates our products pursuant to the Medical Device Amendment of the Food, Drug, and Cosmetic Act, or FDC Act, and regulations promulgated thereunder. Advertising and other forms of promotion and methods of marketing of the products are subject to regulation by the Federal Trade Commission, or FTC, under the Federal Trade Commission Act.

As a device manufacturer, we are required to register with the FDA and once registered we are subject to inspection for compliance with the FDA's Quality Systems regulations. These regulations require us to manufacture our products and maintain our documents in a prescribed manner with respect to manufacturing, testing, and control activities. Further, we are required to comply with various FDA requirements for reporting. The FDC Act and medical device reporting regulations require us to provide information to the FDA on deaths or serious injuries alleged to have been caused or contributed to by the use of our products, as well as product malfunctions that would likely cause or contribute to death or serious injury if the malfunction were to occur. The FDA also prohibits an approved device from being marketed for unapproved uses. All of our therapeutic treatment devices as currently designed are cleared for marketing under section 510(k) of the Medical Device Amendment to the FDC Act or are considered 510(k) exempt. If a device is subject to section 510(k) approval requirements, the FDA must receive pre-market notification from the manufacturer of its intent to market the device. The FDA must find that the device is substantially equivalent to a legally marketed predicate device before the agency will clear the new device for marketing.

8

We intend to continuously improve our products after they have been introduced to the market. Certain modifications to our marketed devices may require a premarket notification and clearance under section 510(k) before the changed device may be marketed, if the change or modification could significantly affect safety or effectiveness. As appropriate, we may therefore submit future 510(k) notifications to the FDA. No assurance can be given that clearance or approval of such new applications will be granted by the FDA on a timely basis, or at all. Furthermore, we may be required to submit extensive preclinical and clinical data depending on the nature of the product changes. All of our devices, unless specifically exempted by regulation, are subject to the FDC Act's general controls, which include, among other things, registration and listing, adherence to the Quality System Regulation requirements for manufacturing, medical device reporting and the potential for voluntary and mandatory recalls described above.

The passage of the Patient Protection and Affordable Care Act and the Health Care and Educational Reconciliation Act (the "Health Care Reform Law") in 2010, has affected and will continue to affect our operations. Although an increase in utilization was expected as a result of the new law, so far in 2016, there has been no perceptible increase in demand for services due to increases in the ranks of the insured through the Health Care Reform Law.

The Health Care Reform Law also includes new reporting and disclosure requirements for device manufacturers with regard to payments or other transfers of value made to certain healthcare providers. Specifically, any transfer of value exceeding $10 in a single transfer or cumulative transfers over a one-year period exceeding $100 to any statutorily defined practitioner (primarily physicians, podiatrists, dentists and chiropractors, or a teaching hospital) must be reported to the federal government by March 31st of each year for the prior calendar year. The data will be assembled and posted to a publicly accessible website by September 30th following the March 31st reporting date. If we fail to provide these reports, or if the reports we provide are not accurate, we could be subject to significant penalties. Several states have adopted similar reporting requirements. We believe we are in compliance with the Health Care Reform Law and have systems in place to assure continued compliance.

Since the Medical Device Amendment was added to the FDC Act in 1976, iontophoresis products had been classified as Class III devices pending final determination by FDA as to whether manufacturers would be required to submit a Pre-Market Approval Application (PMA) to legally market the device. In the interim, iontophoresis devices were conditionally allowed to market based on Class II device requirements for pre-market notification. On July 26, 2016, FDA announced that iontophoresis applications for all uses other than cystic fibrosis would be permanently reclassified into Class II and no PMA would be required. This may make it easier for competitors to enter the market, but we do not expect this reclassification to have a material impact on our financial results.

Failure to comply with applicable FDA regulatory requirements may result in, among other things, injunctions, product withdrawals, recalls, product seizures, fines, and criminal prosecutions. Any such action by the FDA could materially adversely affect our ability to successfully market our products. Our Utah and Tennessee facilities are inspected periodically by the FDA for compliance with the FDA's GMP and other requirements, including appropriate reporting regulations and various requirements for labeling and promotion. The FDA Quality Systems Regulations are similar to the ISO 13485 Quality Standard. The GMP regulation requires, among other things, that (i) the manufacturing process be regulated and controlled by the use of written procedures, and (ii) the ability to produce devices that meet the manufacturer's specifications be validated by extensive and detailed testing of every aspect of the process.

Advertising of our products is subject to regulation by the FTC under the FTC Act. Section 5 of the FTC Act prohibits unfair methods of competition and unfair or deceptive acts or practices in or affecting commerce. Section 12 of the FTC Act provides that the dissemination or the causing to be disseminated of any false advertisement pertaining to, among other things, drugs, cosmetics, devices or foods, is an unfair or deceptive act or practice. Pursuant to this FTC requirement, we are required to have adequate substantiation for all advertising claims made about our products. The type of substantiation required depends upon the product claims made.

If the FTC has reason to believe the law is being violated (e.g., the manufacturer or distributor does not possess adequate substantiation for product claims), it can initiate an enforcement action. The FTC has a variety of processes and remedies available to it for enforcement, both administratively and judicially, including compulsory process authority, cease and desist orders, and injunctions. FTC enforcement could result in orders requiring, among other things, limits on advertising, consumer redress, divestiture of assets, rescission of contracts, and such other relief as may be deemed necessary. Violation of such orders could result in substantial financial or other penalties. Any such action by the FTC could materially adversely affect our ability to successfully market our products.

From time to time, legislation is introduced in the Congress of the United States or in state legislatures that could significantly change the statutory provisions governing the approval, manufacturing, and marketing of medical devices and products like those we manufacture. In addition, FDA regulations and guidance are often revised or reinterpreted by the agency in ways that may significantly affect our business and our products. It is impossible to predict whether legislative changes will be enacted, or FDA regulations, guidance, or interpretations will be changed, and what the impact of such changes, if any, may be on our business and our results of operations. We cannot predict the nature of any future laws, regulations, interpretations, or applications, nor can we determine what effect additional governmental regulations or administrative orders, when and if promulgated, domestically or internationally, would have on our business in the future. They could include, however, the recall or discontinuance of certain products, additional record keeping, expanded documentation of the properties of certain products, expanded or different labeling, and additional scientific substantiation. The necessity of complying with any or all such requirements could have a material adverse effect on our business, results of operations or financial condition.

9

In addition to compliance with FDA rules and regulations, we are also required to comply with international regulatory laws including Health Canada, CE Mark, or other regulatory schemes used by other countries. We believe all of our present products are in compliance in all material respects with all applicable performance standards in countries where the products are sold. We also believe that our products comply with GMP, record keeping and reporting requirements in the production and distribution of the products in the United States.

Environment

Environmental regulations and the cost of compliance with them are not material to our business. We do not discharge into the environment any pollutants that are regulated by a governmental agency with the exception of the requirement to provide proper filtering of discharges into the air from the painting processes at our Tennessee location.

Seasonality

We believe that the effect of seasonality on the results of our operations is not material.

Backlog

Our backlog represents orders received and waiting to be shipped on a given day either because of lead time delays or because of customer requests for specific delivery dates beyond the period end. Backlog is not a term recognized under United States generally accepted accounting principles (GAAP); however, it is a common measurement used in our industry. As of June 30, 2016, we had a backlog of orders of approximately $1.5 million, compared to approximately $540,000 as of June 30, 2015. The increase in the backlog of approximately $1.0 million as of June 30, 2016, compared to June 30, 2015, was due primarily to increased order flow in the latter half of the quarter and specifically a singularly large order of over $500,000. The current level of backlog represents a record high amount due primarily to the singular order received late in the quarter. While we do not expect the sales backlog to continue at these record levels, increasing order flow and sales have resulted in higher backlogs at the end of reporting periods this year compared to historic levels. We expect to see the backlog of orders gradually increase over historic levels as sales continue to grow.

Employees

On June 30, 2016, we had a total of 153 employees, of which 139 were full-time employees and 14 were part-time employees, compared to a total of 141 employees (129 full-time and 12 part-time) on June 30, 2015.

Item 1A. Risk Factors

An investment in our common stock involves a high degree of risk. You should carefully consider the risks and uncertainties described below before making a decision to invest in our common stock. Our business, operating results, financial condition or prospects could be materially and adversely affected by any of these risks and uncertainties. In that case, the trading price of our common stock could decline and you might lose all or part of your investment. In addition, the risks and uncertainties discussed below are not the only ones we face. Our business, operating results, financial performance or prospects could also be harmed by risks and uncertainties not currently known to us or that we currently do not believe are material. In assessing the risks and uncertainties described below, you should also refer to the other information contained in this Annual Report on Form 10-K, before making a decision to invest in our common stock.

10

Risks Related to Our Business and Industry

We have a recent history of losses, and we may not return to or sustain profitability in the future. We have incurred net losses for five consecutive fiscal years. In recent years, we have made substantial investments in research and development, infrastructure, distribution channel expansion and acquisitions to support anticipated future revenue growth. We expect to continue to make significant investments in the development and expansion of our business, which may make it difficult for us to return to profitability. Our present business strategy is to improve cash flow by adding to our existing product line and expanding our sales and marketing efforts, including the addition of in-house sales personnel and acquisitions. We cannot predict when we will again achieve profitable operations or that we will not require additional financing to fulfill our business objectives. We may not be able to increase revenue in future periods, and our revenue could continue to decline or grow more slowly than we expect. We may incur significant losses in the future for many reasons, including due to the risks described in this Annual Report on Form 10-K.

We may need additional funding and may be unable to raise additional capital when needed, which could adversely affect our results of operations and financial condition. In the future, we may require additional capital to pursue business opportunities or acquisitions or respond to challenges and unforeseen circumstances. We may also decide to engage in equity or debt financings or enter into credit facilities for other reasons. We may not be able to secure additional debt or equity financing in a timely manner, on favorable terms, or at all. Any debt financing obtained by us in the future could involve restrictive covenants relating to our capital raising activities and other financial and operational matters, which may make it more difficult for us to obtain additional capital and to pursue business opportunities, including potential acquisitions. Failure to obtain additional financing when needed or on acceptable terms would have a material adverse effect on our business operations.

Our level of indebtedness may harm our financial condition and results of operations. Our level of indebtedness will impact our future operations in many important ways, including, without limitation, by:

|

·

|

Requiring that a portion of our cash flows from operations be dedicated to the payment of any interest or amortization required with respect to outstanding indebtedness;

|

|

·

|

Increasing our vulnerability to adverse changes in general economic and industry conditions, as well as to competitive pressure; and

|

|

·

|

Limiting our ability to obtain additional financing for working capital, acquisitions, capital expenditures, general corporate and other purposes.

|

At the scheduled maturity of our credit facilities or in the event of an acceleration of a debt facility following an event of default, the entire outstanding principal amount of the indebtedness under such facility, together with all other amounts payable thereunder from time to time, will become due and payable. It is possible that we may not have sufficient funds to pay such obligations in full at maturity or upon such acceleration. If we default and are not able to pay any such obligations due, our lenders have liens on substantially all of our assets and could foreclose on our assets in order to satisfy our obligations. If we are unable to meet our debt service obligations and other financial obligations, we could be forced to restructure or refinance our indebtedness and other financial transactions, seek additional equity capital or sell our assets. We might then be unable to obtain such financing or capital or sell our assets on satisfactory terms, if at all. Our line of credit with a lender matures in September 2017, which will require that we renew the facility at that time. There is no assurance we will be successful in renewing the credit facility from our current or another lender. In addition, any refinancing of our indebtedness could be at significantly higher interest rates, and/or result in significant transaction fees.

If we fail to effectively expand our sales and marketing capabilities and teams, we may not be able to increase our customer base and increase revenues. Increasing our customer base and achieving broader market acceptance of our products will depend on our ability to expand our sales and marketing teams and their capabilities to obtain new customers and sell additional products and services to existing customers. We believe there is significant competition for direct sales professionals with the skills and technical knowledge that we require, and we may be unable to hire or retain sufficient numbers of qualified individuals in the future. New hires require significant training and time before they become fully productive, and may not become as productive as quickly as we anticipate. Our growth prospects will be harmed if our efforts to expand, train and retain our direct sales team do not generate a corresponding significant increase in revenue. In addition to our direct sales team, we also extend our sales distribution through relationships with independent sales representatives and marketing service providers. These providers do not have exclusive relationships with us, and we cannot be certain that these partners will prioritize or provide adequate resources for selling our products.

Our inability to acquire and integrate other businesses, products or technologies could harm our operating results. Our business plan includes the acquisition of other businesses, products and technologies. Since 2007, we have acquired six former distributors. In the future we expect to acquire or invest in businesses, products or technologies that we believe could complement or expand our existing product lines, expand our customer base and operations, enhance our technical capabilities or otherwise offer growth or cost-saving opportunities. We have limited experience in successfully acquiring and integrating businesses, products and technologies. If we identify an appropriate acquisition candidate, we may not be successful in negotiating favorable terms of the acquisition, financing the acquisition or effectively integrating the acquired business, product or technology into our existing business and operations. Our due diligence may fail to identify all of the problems, liabilities or other shortcomings or challenges of an acquired business, product or technology, including issues related to intellectual property, product quality or product architecture, regulatory compliance practices, revenue recognition or other accounting practices, or employee or customer issues.

11

Additionally, in connection with any acquisitions we complete, we may not achieve the synergies or other benefits we expected to achieve, and we may incur write-downs, impairment charges or unforeseen liabilities that could negatively affect our operating results or financial position or could otherwise harm our business. If we finance acquisitions by issuing convertible debt or equity securities, the ownership interest of our existing shareholders may be significantly diluted, which could adversely affect the market price of our stock. Further, contemplating or completing an acquisition and integrating an acquired business, product or technology could divert management and employee time and resources from other matters.

Changing market patterns may affect demand for our products. Increasingly, medical markets are moving toward evidence-based practices. Such a move could shrink demand for products we offer if it is deemed there is inadequate evidence to support the efficacy of the products. Likewise, to achieve market acceptance in such environments may require expenditure of funds to do clinical research that may or may not prove adequate efficacy to satisfy all customers.

Uncertain or weakened global economic conditions may adversely affect our industry, business and results of operations. Our overall performance depends on domestic and worldwide economic conditions, which may remain challenging for the foreseeable future. Financial developments seemingly unrelated to us or to our industry may adversely affect us. The U.S. economy and other key international economies have been impacted by threatened sovereign defaults and ratings downgrades, falling demand for a variety of goods and services, restricted credit, threats to major multinational companies, poor liquidity, reduced corporate profitability, volatility in credit, equity and foreign exchange markets, bankruptcies, acts of terrorism and overall uncertainty. Healthcare reform in the United States has created a great deal of confusion and reduced capital expenditures for medical equipment and products such as those we manufacture and distribute. These conditions affect the rate of medical device spending and could adversely affect our customers' ability or willingness to purchase our products, or delay prospective customers' purchasing decisions, any of which could adversely affect our operating results. We cannot predict the timing, strength or duration of the economic recovery or any subsequent economic slowdown worldwide, in the United States, or in our industry.

We rely on our management team and other key employees, and the loss of one or more key employees could harm our business. Our success and future growth depend upon the continued services of our management team and other key employees, including in the areas of research and development, marketing, sales, services and general and administrative functions. From time to time, there may be changes in our management team resulting from the hiring or departure of executives, which could disrupt our business. If new key employees and other members of our senior management team cannot work together effectively, or if other members of our senior management team resign, our ability to effectively manage our business may be impacted. We may terminate any executive officer's employment at any time, with or without cause, and any executive officer may resign at any time, with or without cause. We do not maintain key person life insurance on any of our employees. The loss of any of our key employees could harm our business.

Healthcare reform in the United States has had and is expected to continue to have a significant effect on our business and on our ability to expand and grow our business. The Patient Protection and Affordable Care Act as amended by the Health Care and Education Reconciliation Act, generally known as the Health Care Reform Law, significantly expanded health insurance coverage to uninsured Americans and changed the way health care is financed by both governmental and private payers. We expect expansion of access to health insurance may eventually increase the demand for our products and services and pressure to reduce costs of healthcare will likely increase demand for less costly services such as physical therapy in both prehabilitation and rehabilitation settings, but other provisions of the Health Care Reform Law have affected us adversely. Additionally, further federal and state proposals for health care reform are likely. The reform has created uncertainty regarding reimbursement and delivery of services and has, in past years, resulted in reluctance on the part of health care providers to expand or improve their practices with new products and equipment, which has adversely affected our revenues. We cannot predict what further reform proposals, if any, will be adopted, when they may be adopted, or what impact they may have on us.

12

Medical Device Tax. In December 2015, Congress passed legislation known as the PATH Act. This legislation suspended the medical device tax imposed by The Health Care Reform Law for calendar years 2016 and 2017. Although the excise tax has been suspended by Congress until the end of calendar 2017, its status is unclear for 2018 and subsequent years. Without specific action by Congress to extend the suspension, the medical device tax is scheduled to be reinstated in January 2018.

As a participant in the healthcare industry, our operations and products, and those of our customers, are regulated by numerous government agencies, both inside and outside the United States. The impact of this on us is direct, to the extent we are subject to these laws and regulations, and indirect in that in a number of situations, even though we may not be directly regulated by specific healthcare laws and regulations, our products must be capable of being used by our customers in a manner that complies with those laws and regulations. The manufacture, distribution, marketing and use of our products are subject to extensive regulation and increased scrutiny by the Food and Drug Administration (FDA) and other regulatory authorities globally. Any new product must undergo lengthy and rigorous testing and other extensive, costly and time-consuming procedures mandated by FDA and foreign regulatory authorities. Changes to current products may be subject to vigorous review, including additional 510(k) and other regulatory submissions, and approvals are not certain. Our facilities must be approved and licensed prior to production and remain subject to inspection from time to time thereafter. Failure to comply with the requirements of FDA or other regulatory authorities, including a failed inspection or a failure in our adverse event reporting system, could result in adverse inspection reports, warning letters, product recalls or seizures, monetary sanctions, injunctions to halt the manufacture and distribution of products, civil or criminal sanctions, refusal of a government to grant approvals or licenses, restrictions on operations or withdrawal of existing approvals and licenses. Any of these actions could cause a loss of customer confidence in us and our products, which could adversely affect our sales. The requirements of regulatory authorities, including interpretative guidance, are subject to change and compliance with additional or changing requirements or interpretative guidance may subject the Company or our products to further review, result in product launch delays or otherwise increase our costs.

The sales, marketing and pricing of products and relationships that medical device companies have with healthcare providers are under increased scrutiny by federal, state and foreign government agencies. Compliance with the Anti-Kickback Statute, False Claims Act, Food, Drug and Cosmetic Act (including as these laws relate to off-label promotion of products) and other healthcare related laws, as well as competition, data and patient privacy, and export and import laws, is under increased focus by the agencies charged with overseeing such activities, including FDA, Office of Inspector General (OIG), Department of Justice (DOJ) and the Federal Trade Commission. The DOJ and the SEC have also increased their focus on the enforcement of the US Foreign Corrupt Practices Act (FCPA). The FCPA and similar anti-bribery laws generally prohibit companies and their employees, contractors or agents from making improper payments to government officials for the purpose of obtaining or retaining business. The FCPA also imposes recordkeeping and internal controls requirements on public companies. The laws and standards governing the promotion, sale and reimbursement of our products and those governing our relationships with healthcare providers and governments can be complicated, are subject to frequent change and may be violated unknowingly. Violations or allegations of violations of these laws may result in large civil and criminal penalties, debarment from participating in government programs, diversion of management time, attention and resources and may otherwise have an adverse effect on our business, financial condition and results of operations. The laws and regulations discussed above are broad in scope and subject to evolving interpretations, which could require us to incur substantial costs associated with compliance or to alter one or more of our sales and marketing practices and may subject us to enforcement actions which could adversely affect our business, financial condition and results of operations.

Market access could be a limiting factor in our growth. The emergence of Group Purchasing Organizations (GPO's) that control a significant amount of product flow to acute care customers may limit our ability to grow in the acute care space. GPO's issue contracts to manufacturers approximately every three years through a bidding process. Despite repeated efforts, we have been relatively unsuccessful in landing any significant GPO contracts other than one with Amerinet two years ago. The process for being placed on contract with a GPO is rigorous and non-transparent. Patterson Medical, a large competitor, controls the majority of GPO contracts in our market space holding in many instances a sole source contract.

We rely on a combination of patents, trade secrets, and nondisclosure and non-competition agreements to protect our proprietary intellectual property, and we will continue to do so. While we intend to defend against any threats to our intellectual property, these patents, trade secrets, or other agreements may not adequately protect our intellectual property. Third parties could obtain patents that may require us to negotiate licenses to conduct our business, and the required licenses may not be available on reasonable terms or at all. We also rely on nondisclosure and non-competition agreements with certain employees, consultants, and other parties to protect, in part, trade secrets and other proprietary rights. We cannot be certain that these agreements will not be breached, that we will have adequate remedies for any breach, that others will not independently develop substantially equivalent proprietary information, or that third parties will not otherwise gain access to our trade secrets or proprietary knowledge.

13

The cost of healthcare has risen significantly over the past decade and numerous initiatives and reforms initiated by legislators, regulators and third-party payers to curb these costs have resulted in a consolidation trend in the medical device industry as well as among our customers, including healthcare providers. These conditions could result in greater pricing pressures and limitations on our ability to sell to important market segments, such as group purchasing organizations, integrated delivery networks and large single accounts. We expect that market demand, government regulation, third-party reimbursement policies and societal pressures will continue to change the worldwide healthcare industry, resulting in further business consolidations and alliances which may exert further downward pressure on the prices of our products and adversely impact our business, financial condition and results of operations.

We are dependent on our suppliers because we do not manufacture the majority of the products we sell. Approximately 56% of our physical medicine revenues are derived from the sale and distribution of products we do not manufacture. Interruptions in supply of these products could adversely affect our operating results. If a supplier is unable to deliver product in a timely and efficient manner, whether due to financial difficulties, natural disasters or other reasons, we could experience lost sales. We generally do not have long-term contracts with our suppliers that commit them to produce products for us.

The products we sell are subject to market and technological obsolescence. We offer approximately 15,000 variations of products. Some of these products are subject to technological obsolescence outside of our control, since we do not manufacture the majority of the products we sell. If our customers discontinue purchasing a given product, we might have to record expense related to the diminution in value of inventories we have in stock, and depending on the magnitude, that expense could adversely impact our operating results. In addition to the products of others that we distribute, we design and manufacture our own medical devices and products. We may be unable to effectively develop and market products against the products of our competitors in a highly competitive industry. Our present or future products could be rendered obsolete or uneconomical by technological advances by our competitors. Competitive factors include price, customer service, technology, innovation, quality, reputation and reliability. Our competition may respond more quickly to new or emerging technologies, undertake more extensive marketing campaigns, have greater financial, marketing and other resources than us or be more successful in attracting potential customers, employees and strategic partners. Given these factors, we cannot guarantee that we will be able to continue our level of success in the industry.

Competition in research, involving the development and improvement of new and existing products, is particularly significant and results from time to time in product obsolescence. The markets in which we operate are highly competitive, and new products are introduced on an ongoing basis. Such marketplace changes may cause some of our products to become obsolete. If actual product life cycles, product demand or acceptance of new product introductions are less favorable than projected by management, a higher level of inventory write downs may result.

We may be adversely affected by product liability claims, unfavorable court decisions or legal settlements. Our business exposes us to potential product liability risks that are inherent in the design, manufacture and marketing of medical devices. We maintain product liability insurance coverage which we deem to be adequate based on historical experience; however, there can be no assurance that coverage will be available for such risks in the future or that, if available, it would prove sufficient to cover potential claims or that the present amount of insurance can be maintained in force at an acceptable cost. In addition, we may incur significant legal expenses regardless of whether we are found to be liable. Furthermore, the assertion of such claims, regardless of their merit or eventual outcome, also may have a material adverse effect on our business reputation and results of operations.

Intellectual property litigation and infringement claims could cause us to incur significant expenses or prevent us from selling certain of our products. The medical device industry is characterized by extensive intellectual property litigation and, from time to time, we are the subject of claims by third parties of potential infringement or misappropriation. Regardless of outcome, such claims are expensive to defend and divert the time and effort of management and operating personnel from other business issues. A successful claim or claims of patent or other intellectual property infringement against us could result in our payment of significant monetary damages and/or royalty payments or negatively impact our ability to sell current or future products in the affected category.

Our success is dependent in large part on the accuracy, reliability and proper use of sophisticated and dependable information processing systems and management information technology. Our information technology systems are designed and selected in order to facilitate order entry and customer billing, maintain records, accurately track purchases, accounts receivable and accounts payable, manage accounting, finance and manufacturing operations, generate reports and provide customer service and technical support. Any interruption in these systems could have a material adverse effect on our business, financial condition and results of operations.

14

Changes in financial accounting standards or practices may cause adverse, unexpected financial reporting fluctuations and affect our reported results of operations. Financial accounting standards may change or their interpretation may change. A change in accounting standards or practices can have a significant effect on our reported results and may even affect our reporting of transactions completed before the change becomes effective. Changes to existing rules or the re-examining of current practices may adversely affect our reported financial results or the way we conduct our business. Accounting for revenue from sales of our solutions is particularly complex, is often the subject of intense scrutiny by the SEC, and will evolve as the Financial Accounting Standards Board (''FASB'') continues to consider applicable accounting standards in this area.

Risks Related to Our Common Stock

A decline in the price of our common stock could affect our ability to raise working capital and adversely impact our operations. Our operating results, including components of operating results such as gross margin and cost of product sales, may fluctuate from time to time, and such fluctuations could adversely affect our stock price. Our operating results have fluctuated in the past and can be expected to fluctuate from time to time in the future. The market price for our common stock may also be affected by our ability to meet or exceed expectations of analysts or investors. Any failure to meet these expectations, even if minor, could materially adversely affect the market price of our common stock. A prolonged decline in the price of our common stock for any reason could result in a reduction in our ability to raise capital.

Our stock price has been volatile and we expect that it will continue to be volatile. For example during the year ended June 30, 2016, the selling price of our common stock ranged from a high of $4.44 to a low of $2.55. The volatility of our stock price can be due to many factors, including:

|

·

|

quarterly variations in our operating results;

|

|

·

|

changes in the market's expectations about our operating results;

|

|

·

|

our operating results failing to meet the expectation of securities analysts or investors in a particular period;

|

|

·

|

changes in financial estimates and recommendations by securities analysts concerning our Company or of the healthcare industry in general;

|

|

·

|

strategic decisions by us or our competitors, such as acquisitions, divestments, spin-offs, joint ventures, strategic investments or changes in business strategy;

|

|

·

|

operating and stock price performance of other companies that investors deem comparable to us;

|

|

·

|

news reports relating to trends in our markets;

|

|

·

|

changes in laws and regulations affecting our business;

|

|

·

|

material announcements by us or our competitors;

|

|

·

|

material announcements by the manufacturers and suppliers we use;

|

|

·

|

sales of substantial amounts of our common stock by our directors, executive officers or significant shareholders or the perception that such sales could occur; and

|

|

·

|

general economic and political conditions such as recessions and acts of war or terrorism.

|