UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

(Mark One):

| ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended January 31, 2021 .

OR

| TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission file number 001-14077

(Exact name of registrant as specified in its charter)

| (State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification No.) | |

| (Address of principal executive offices) | (Zip Code) | |

Registrant’s telephone number, including area code:

(415 ) 421-7900

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class: |

Trading Symbol(s): |

Name of each exchange on which registered: | ||

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☒ No ☐

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation Yes ☒ No ☐

S-T

(§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a

non-accelerated

filer, a smaller reporting company, or emerging growth company. See definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2

of the Exchange Act. filer

☒ Accelerated filer ☐ Non-accelerated

filer ☐ Smaller reporting company ☐ Emerging growth company ☐

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☒

Indicate by check mark whether the registrant is a shell company (as defined in Rule ☒

12b-2

of the Act). Yes ☐ No As of August 2, 2020, the approximate aggregate market value of the registrant’s common stock held by 6,720,032,000 . It is assumed for purposes of this computation that an affiliate includes all persons as of August 2, 2020 listed as executive officers and directors with the Securities and Exchange Commission. This aggregate market value includes all shares held in the Williams-Sonoma, Inc. Stock Fund within the registrant’s 401(k) Plan.

non-affiliates

was $As of March 21, 2021, 76,192,973 shares of the registrant’s common stock were outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of our definitive Proxy Statement for the 2021 Annual Meeting of Stockholders, also referred to in this Annual Report on Form

10-K

as our Proxy Statement, which will be filed with the Securities and Exchange Commission, or SEC, have been incorporated in Part III hereof. FORWARD-LOOKING STATEMENTS

This Annual Report on Form

10-K

and the letter to stockholders contained in this Annual Report contain forward-looking statements within the “safe harbor” provisions of the Private Securities Litigation Reform Act of 1995 that involve risks and uncertainties, as well as assumptions that, if they do not fully materialize or prove incorrect, could cause our business and operating results to differ materially from those expressed or implied by such forward-looking statements. Such forward-looking statements include, without limitation, statements related to: projections of earnings, revenues, growth and other financial items; the strength of our business and our brands; our ability to execute strategic priorities and growth initiatives regarding digital leadership, product and technology innovation, cross-brand initiatives, retail transformation and operational excellence; our beliefs about our competitive advantages and areas of potential future growth in the market; our ability to drive long-term sustainable returns; the plans, strategies, initiatives and objectives of management for future operations; our brands, products and related initiatives, including our ability to introduce new brands, brand extensions, products and product lines and bring in new customers; our belief that our e-commerce

websites and direct-mail catalogs act as a cost-efficient means of testing market acceptance of new products and new brands; the complementary nature of our e-commerce

and retail channels; our marketing efforts; our acquisition of Outward, Inc., including the valuation of intangible assets acquired; our global business and expansion efforts, including franchise, other third-party arrangements and company-owned operations; our ability to attract new customers; the seasonal variations in demand; our ability to recruit, retain and motivate skilled personnel; our belief in the reasonableness of the steps taken to protect the security and confidentiality of the information we collect; our belief in the adequacy of our facilities and the availability of suitable additional or substitute space; our belief in the ultimate resolution of current legal proceedings; the payment of dividends; our stock repurchase program; our capital allocation strategy in fiscal 2021; our planned use of cash in fiscal 2021; our compliance with financial covenants; our belief that our cash on hand and available credit facilities will provide adequate liquidity for our business operations over the next 12 months; the impact of the 2017 Tax Cuts and Jobs Act; the impact of tariffs on our business and our results of operations; our belief regarding the effects of potential losses under our indemnification obligations; the impact of inflation; the effects of changes in our inventory reserves; the impact of new accounting pronouncements; the impact of the coronavirus on our retail store operations, global supply chain and customer spending and demand; and statements of belief and statements of assumptions underlying any of the foregoing. You can identify these and other forward-looking statements by the use of words such as “will,” “may,” “should,” “expects,” “plans,” “anticipates,” “believes,” “estimates,” “predicts,” “intends,” “potential,” “continue,” or the negative of such terms, or other comparable terminology. The risks, uncertainties and assumptions referred to above that could cause our results to differ materially from the results expressed or implied by such forward-looking statements include, but are not limited to, those discussed under the heading “Risk Factors” in Item 1A hereto and the risks, uncertainties and assumptions discussed from time to time in our other public filings and public announcements. All forward-looking statements included in this document are based on information available to us as of the date hereof, and we assume no obligation to update these forward-looking statements.

1

WILLIAMS-SONOMA, INC.

ANNUAL REPORT ON FORM

10-K

FISCAL YEAR ENDED JANUARY 31, 2021

TABLE OF CONTENTS

PAGE |

||||||

PART I |

||||||

| Item 1. | 3 | |||||

| Item 1A. | 8 | |||||

| Item 1B. | 29 | |||||

| Item 2. | 29 | |||||

| Item 3. | 30 | |||||

| Item 4. | 30 | |||||

PART II |

||||||

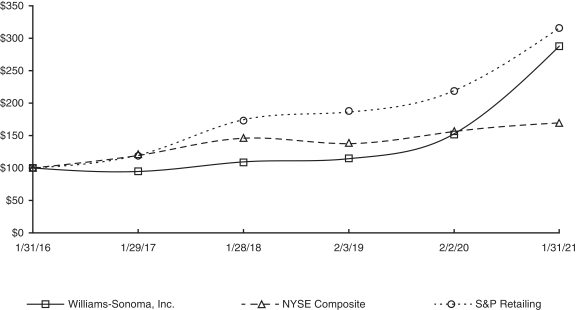

| Item 5. | Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities | 31 | ||||

| Item 6. | 33 | |||||

| Item 7. | 34 | |||||

| Item 7A. | 45 | |||||

| Item 8. | 46 | |||||

| Item 9. | 72 | |||||

| Item 9A. | 72 | |||||

| Item 9B. | 73 | |||||

PART III |

||||||

| Item 10. | 74 | |||||

| Item 11. | 74 | |||||

| Item 12. | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | 74 | ||||

| Item 13. | 74 | |||||

| Item 14. | 74 | |||||

PART IV |

||||||

| Item 15. | 75 | |||||

| Item 16. | 81 | |||||

2

PART I

ITEM 1. |

BUSINESS |

OVERVIEW

Williams-Sonoma, Inc., (“the Company”) incorporated in 1973, is an omni-channel specialty retailer of high-quality products for the home.

In 1956, our founder, Chuck Williams, turned a passion for cooking and eating with friends into a small business with a big idea. He opened a store in Sonoma, California, to sell the French cookware that intrigued him while visiting Europe but that could not be found in America. Chuck’s business, which set a standard for customer service, took off and helped fuel a revolution in American cooking and entertaining that continues today.

In the decades that followed, the quality of our products, our ability to identify new opportunities in the market and our people-first approach to business have facilitated our expansion beyond the kitchen into nearly every area of the home. Growth across the Williams-Sonoma, Inc. portfolio has been fueled by three areas of strategic investment: brand experimentation and innovation, for a approach to omni-channel retail experiences; operational excellence across the enterprise, from quality product and sourcing, to efficient manufacturing and supply chain; and culture and corporate social responsibility, from commitments to foster women in leadership and embrace diversity, to a healthy impact on our community and environment.

best-in-class

Williams-Sonoma, Inc. is the world’s largest digital-first, design-led and sustainable home retailer. Our products represent distinct merchandise strategies — Williams Sonoma, Pottery Barn, Pottery Barn Kids, Pottery Barn Teen, West Elm, Williams Sonoma Home, Rejuvenation, and Mark and Graham — are marketed through loyalty program that offers members exclusive benefits across the Williams-Sonoma family of brands. We operate in the U.S., Puerto Rico, Canada, Australia and the United Kingdom, offer international shipping to customers worldwide, and have unaffiliated franchisees that operate stores in the Middle East, the Philippines, Mexico, South Korea and India, as well as

e-commerce

websites, direct-mail catalogs and retail stores. These brands are also part of The Key Rewards, our free-to-join

e-commerce

websites in certain locations. We are also proud to lead the industry with our Environmental, Social and Governance (“ESG”) efforts. Williams Sonoma

From the beginning, our namesake brand, Williams Sonoma, has been bringing people together around food. A leading specialty retailer of high-quality products for the kitchen and home, the brand seeks to provide world-class service and an engaging customer experience. Williams Sonoma products include everything for cooking, dining and entertaining, including: cookware, tools, electrics, cutlery, tabletop and bar, outdoor, furniture and a vast library of cookbooks. The brand also includes Williams Sonoma Home, a premium concept that offers classic home furnishings and decorative accessories, extending the Williams Sonoma lifestyle beyond the kitchen into every room of the home.

Pottery Barn

Established in 1949 and acquired by Williams-Sonoma, Inc. in 1986, Pottery Barn is a premier omni-channel home furnishings retailer. America’s most meaningful, beautiful design source, Pottery Barn brings together good products, people and values — seeking inspiration, quality, sustainability and service in everything we do. Thoughtfully designed and crafted to last, Pottery Barn’s furniture, bedding, lighting, rugs, table essentials, decorative accessories and more can be loved for a lifetime.

Pottery Barn Kids

Kids are, and have always been, the inspiration behind what we do at Pottery Barn Kids. Since 1999, it’s been our mission to bring the utmost in quality, sustainability, safety and style into every family’s home. Most importantly, all our designs are rigorously tested to meet the highest child safety standards and expertly crafted from the best materials to last beyond their childhood years.

3

West Elm

Born in Brooklyn in 2002, West Elm is dedicated to transforming people’s lives and spaces through creativity, style and purpose. West Elm creates unique, modern and affordable home decor and curate a global selection of local, ethically-sourced and Fair Trade Certified products, available online and in our stores worldwide.

Pottery Barn Teen

Launched in 2003, Pottery Barn Teen is the first home concept to focus exclusively on the teen market. Our purpose is to make safe and sustainable designs that inspire teens to create the world they want to live in. We’re designing everything from organic bedding to multi-purpose furniture that adapts and lasts. Our mission is to create for the future.

Rejuvenation

Rejuvenation, founded in 1977 with a passion for timeless design and quality craftsmanship, was acquired by Williams-Sonoma, Inc. in 2011. With design, manufacturing and distribution facilities in Portland, Oregon, Rejuvenation offers a wide assortment of lighting, hardware, furniture and home décor inspired by history, designed for today and made to last for years to come.

made-to-order

Mark and Graham

Launched in 2012, Mark and Graham is designed to be a premier online destination for personalized gift buying. With over 100 monograms and font types to choose from, a Mark and Graham purchase is uniquely personal. The brand’s product lines include women’s and men’s accessories, small leather goods, jewelry, key item apparel, paper, entertaining and bar, home décor and seasonal items.

Outward

In 2017, we acquired Outward, Inc., a

3-D

imaging and augmented reality platform for the home furnishings and décor industry. Headquartered in San Jose, California, Outward’s technology enables scalable applications in product visualization, digital room design and augmented and virtual reality. OPERATIONS

As of January 31, 2021, we had the following merchandise strategies: Williams Sonoma, Pottery Barn, Pottery Barn Kids, Pottery Barn Teen, West Elm, Williams Sonoma Home, Rejuvenation and Mark and Graham, which sell our products through our

e-commerce

websites, direct-mail catalogs and retail stores. We offer shipping from many of our brands to countries worldwide, while our catalogs reach customers throughout the U.S. The e-commerce

business complements the retail business by building brand awareness and acting as an effective advertising vehicle. We believe that our e-commerce

websites and our direct-mail catalogs act as a cost-efficient means of testing market acceptance of new products and new brands. Leveraging these insights and our omni-channel positioning, our marketing efforts, including digital advertising and the circulation of catalogs, are targeted toward driving sales to each of our channels. Consistent with our published privacy policies, we send our catalogs to addresses from our proprietary customer list, as well as to addresses from lists of other mail order direct marketers, magazines and companies with which we establish a business relationship. In accordance with prevailing industry practice and our privacy policies, we may also rent our list to select mailers. Our customer mailings are continually updated to include new prospects and to eliminate non-responders.

In addition, the retail business complements the e-commerce

business by building brand awareness and attracting new customers to our brands. Our retail stores serve as billboards for our brands, which we believe inspires our customers to also shop online and through our catalogs. We operate 581 stores, which include 538 stores in 42 states, Washington, D.C. and Puerto Rico, 21 stores in Canada, 19 stores in Australia and 3 stores in the United Kingdom. We also have multi-year franchise agreements with third parties in the Middle East, the Philippines, Mexico, South Korea and India that currently operate 136 franchised locations as well as e-commerce

websites in certain locations. 4

SUPPLIERS

We purchase most of our merchandise from numerous foreign and domestic manufacturers and importers, the largest of which accounted for approximately 4% of our purchases during fiscal 2020. Approximately 65% of our merchandise purchases in fiscal 2020 were sourced from foreign vendors, predominantly in Asia and Europe. Substantially all of these purchases were negotiated and paid for in U.S. dollars. In addition, we manufacture merchandise, primarily upholstered furniture and lighting, at our facilities located in North Carolina, California, Oregon and Mississippi.

COMPETITION AND SEASONALITY

The specialty industry within the last decade, particularly in

e-commerce

and retail businesses are highly competitive. Our e-commerce

websites, direct-mail catalogs and retail stores compete with other retailers, including e-commerce

retailers, large department stores, discount retailers, other specialty retailers offering home-centered assortments and other direct-mail catalogs. The substantial sales growth in the direct-to-customer

e-commerce,

has encouraged the entry of many new competitors, including discount retailers selling undifferentiated products at reduced prices, new business models and has resulted in increased competition from established companies. We compete on the basis of our brand authority, the quality of our merchandise, our customer service, our proprietary customer list, our e-commerce websites and marketing capabilities, the location and appearance of our stores, as well as our in-house design, our digital-first channel strategy, and our values, which we believe have become increasingly relevant and set us apart from our competitors. Our in-house teams design our own products and work with our talented vendors to bring quality, sustainable products to market through our high-touch multichannel platform. Our business is subject to substantial seasonal variations in demand. Historically, a significant portion of our net revenues and net earnings have been realized during the period from October through January, and levels of net revenues and net earnings have typically been lower during the period from February through September. We believe this is the general pattern associated with the retail industry. In preparation for and during our holiday selling season, we hire a substantial number of additional temporary employees, primarily in our retail stores, customer care centers and distribution facilities, and incur significant fixed catalog production and mailing costs.

HUMAN CAPITAL MANAGEMENT

As of January 31, 2021, we had approximately 21,000 employees, of whom approximately 12,200 were full-time. In preparation for and during our fiscal 2020 holiday selling season, we hired approximately 10,000 temporary employees, primarily in our retail stores, customer care centers and distribution facilities. None of our employees are represented by a collective bargaining agreement.

In fiscal 2020, we announced three new ESG pillars as key areas of focus for our company. One of those three pillars is “People” in keeping with our long-held “People First” culture. This includes the following areas of focus:

Employee Engagement

We conduct an annual Associate Opinion Survey to directly engage with and collect feedback from our associates, which we use to improve the experience of our teams. Our human resources department maintains an open-door policy for associates to report concerns, and we provide an anonymous reporting hotline, available in multiple languages and managed by an independent company not affiliated with us. We strive to deliver a workplace experience where the quality of our engagement with fellow associates, business partners and customers matches the quality of the products and services we bring to the marketplace.

Talent Development

We invest in our employees through accessible resources and structured training programs that help our associates to create the career they envision for themselves. We offer a large selection of development opportunities for our employees including

in-person

and online learning, as well as professional development courses, such as goal setting, unconscious bias and inclusive leadership training. We have a company-wide 5

Advisor Program, which matches associates in a Manager and above role with

non-managers

to form advisor/advisee relationships to provide career guidance and receive support in working through career and development challenges. Additionally, our LEAD program — Leadership Education and Development — provides a leadership training program for nominated Directors and Vice Presidents. We also foster other team-based programs to develop talent at all levels of the Company, supplying associates with new skills and training. Through these programs, we give our associates the tools to succeed, learn new skills and develop their careers. Diversity, Equity and Inclusion

Associate engagement and retention require an understanding of the needs of a diverse, creative and purpose-driven workforce. We firmly believe that working in a culture focused on diversity, equity and inclusion spurs innovation, creates healthy and high-performing teams, and delivers superior customer experiences. We aim to provide equal opportunity for all employees. As of October 2019, 69% of our total workforce identified as female and 38% were minorities. Additionally, 52% of our Vice Presidents and above identified as female.

We are focused on increasing the representation of minority talent through hiring and career development. In June 2020, we established an Equity Action Plan and formed an Equity Action Committee, including a diverse group of executives and associates, to drive positive change in the fight for racial justice. We also have several systems under which associates can report incidents or discrimination confidentially or anonymously and without fear of reprisal.

We are currently building relationships with over 175 organizations, universities, colleges and networks to expand our reach to potential candidates. As of the end of fiscal 2020, 100% of open roles have a diverse slate of candidates, and we have had a double-digit increase in Black representation since we launched our Equity Action Plan. We are also a member of CEO Action for Diversity & Inclusion, in which we announced a goal to “identify and establish associate networks for underrepresented communities to promote diversity and inclusion throughout the Company.” In furtherance of our stated goal, we have developed associate groups including an LGBTQ+ Alliance, Black Associate Network, Veterans Appreciation Group, Hispanic Heritage Group, and an Asian American Pacific Islander Network.

Safety/Health and Wellness

Our vision is to provide a safe and healthy work environment for our associates and customers. Aligned with our values, we strive to continuously improve our work environments to keep our associates and customers as safe as possible. Our efforts include:

| • | Incident and hazard reporting; |

| • | Standard operating procedures aimed at reducing risk of injury; |

| • | Associate and management training; |

| • | Promotion of best practices; and |

| • | Measurement of key safety metrics. |

During fiscal 2020, to address the safety and health of our workforce due to the

COVID-19

pandemic, we implemented a number of safety-related protocols, including: | • | Temporarily closing our stores and corporate offices, and implementing temporary work-from-home-policies; |

| • | Establishing strict safety protocols and procedures company-wide, including social distancing measures, enhanced sanitization, daily wellness checks and supplying personal protective gear such as masks and gloves; |

| • | Developing and distributing a playbook to guide the safe return to offices, stores, and work sites; and |

| • | Creating and refining protocols to address actual and suspected COVID-19 cases and potential exposure of our team members, customers, and trade partners. |

6

Compensation and Benefits

We offer a benefits package designed to put our associates’ health and well-being, and that of their families, at the forefront. Depending on position and location, associates may be eligible for: 401(k) plan and other investment opportunities; paid vacations, holidays and other

time-off

programs; health, dental and vision insurance; health and dependent care tax-free

spending accounts; medical, family and bereavement leave; paid maternity/primary caregiver benefits; tax-free

commuter benefits; wellness programs; time off to volunteer, and matching donations to qualifying nonprofit organizations. In addition, consistent with our commitment to diversity and inclusion, we have expanded our benefit offerings to include coverage for transgender-inclusive services, including gender confirmation surgery and hormone therapy. In connection with the

COVID-19

pandemic, we acted quickly to meet the needs of our team members, by providing certain enhanced benefits, such as: | • | Increased company minimum wage to $14 per hour; |

| • | Provided special bonuses to all frontline workers; |

| • | Approved special bonuses to high-performing non-executive associates to reward extraordinary efforts in COVID-19 environment; |

| • | Created a dedicated associate hotline to provide real time support for any COVID-19-related issues; |

| • | Reinforced social distancing through signage, floor markers, taped grid patterns on floors, and directional arrows; |

| • | Continued telehealth support and employee assistance programs; and |

| • | Provided special wellness resources and tools. |

Community Involvement

Since 2017 we have donated over $42 million in corporate, customer and associate donations. Our partners include organizations that promote and strengthen the wellbeing of children, women, families and LGBTQ+ communities, such as St. Jude Children’s Research Hospital, No Kid Hungry, AIDS Walk and Canada Children’s Hospitals. We raised $5 million for St. Jude Children’s Research Hospital during the fiscal 2020 St. Jude Campaign, which included donations from our customers at time of purchase, special St. Jude-designated product sales where a portion of the sale was donated, employee donations, and donations from the Company. We also support organizations and partners, such as GlobalGiving and Good360, which assist those whose homes have been damaged or lost. We give charitable grants, donate our merchandise, donate proceeds from the sale of certain products, and provide matching grants for charitable donations made by our associates. Our Williams-Sonoma, Inc. Foundation also provides need-based grants to our associates directly impacted by the

Thanks and Giving

COVID-19

pandemic. We also support our communities through our associates’ time and leadership, and we provide 8 hours of paid Community Involvement Time each year. We believe volunteering deepens our presence in the community, enhances our relationships with customers and strengthens employee engagement.

INTELLECTUAL PROPERTY

As of January 31, 2021, we own and/or have applied to register approximately 179 unique trademarks or service marks. We own and/or have applied to register our key brand names in the U.S. as well as in 95 additional jurisdictions. Generally, exclusive rights to the trademarks and service marks are held by Williams-Sonoma, Inc. and are used by our subsidiaries and franchisees under license. These marks include our core brand names as well as brand names for selected products and services. The core brand names in particular, including “Williams Sonoma,” “Pottery Barn,” “pottery barn kids,” “Pottery Barn Teen,” “west elm,” “Williams Sonoma Home,” “Rejuvenation” and “Mark and Graham” are of material importance to us. Trademarks are generally valid as long as they are in use and/or their registrations are properly maintained, and they have not been found to have become generic. Trademark registrations can generally be renewed indefinitely so long as the marks are in use. We also own numerous copyrights and trade dress rights for our products, product packaging, catalogs, books,

7

publications, website designs and store designs, among other things, which are used by our subsidiaries and franchisees under license. As of January 31, 2021, we own or have applied to register approximately 322 patents in connection with certain product designs, inventions and proprietary technology. Patents in the U.S. are generally valid for 14 to 20 years as long as their registrations are properly maintained. In addition, we have registered and maintain numerous Internet domain names, including “williams-sonoma.com,” “potterybarn.com,” “potterybarnkids.com,” “potterybarnteen.com,” “westelm.com,” “wshome.com,” “williams-sonomainc.com,” “rejuvenation.com” and “markandgraham.com.” Collectively, the trademarks, patents, copyrights, trade dress rights, domain names, trade secrets and other proprietary technology that we hold are of material importance to us.

AVAILABLE INFORMATION

We file annual reports on Form

10-K,

quarterly reports on Form 10-Q,

current reports on Form 8-K,

proxy and information statements and amendments to reports filed or furnished pursuant to Sections 13(a), 14 and 15(d) of the Securities Exchange Act of 1934, as amended. The SEC maintains a website at www.sec.gov that contains reports, proxy and information statements and other information regarding Williams-Sonoma, Inc. and other companies that file materials electronically with the SEC. Our annual reports, Forms 10-K,

Forms 10-Q,

Forms 8-K

and proxy and information statements are also available, free of charge, on our website at www.williams-sonomainc.com. Investors and others should note that we announce material financial and operational information to our investors on our Investor Relations website (http://ir.williams-sonomainc.com), press releases, SEC filings and public conference calls and webcasts. Information on our website is not, and will not, be deemed a part of this report or incorporated into any other filings we make with the SEC.

ITEM 1A. |

RISK FACTORS |

A description of the risks and uncertainties associated with our business is set forth below. You should carefully consider such risks and uncertainties, together with the other information contained in this report and in our other public filings before investing in our common stock. If any of such risks and uncertainties actually occurs, our business, financial condition or operating results could differ materially from the plans, projections and other forward-looking statements included in the section titled “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and elsewhere in this report and in our other public filings. In addition, if any of the following risks and uncertainties, or if any other risks and uncertainties, actually occurs, our business, financial condition or operating results could be harmed substantially, which could cause the market price of our stock to decline, perhaps significantly.

8

Risk Factor Summary

The following is a summary of the risks and uncertainties that could cause our business, financial condition or operating results to be harmed. We encourage you to carefully review the full risk factors contained in this report in their entirety for additional information regarding these risks and uncertainties.

Risks Related to Our Business

| • | Our business has been and may continue to be materially impacted by the COVID-19 pandemic, and the duration and extent to which this will impact our future financial performance remains uncertain. |

| • | Declines in general economic conditions, and the resulting impact on consumer confidence and consumer spending, could adversely impact our results of operations. |

| • | We are unable to control many of the factors affecting consumer spending, and declines in consumer spending on home furnishings and kitchen products in general could reduce demand for our products. |

| • | If we are unable to identify and analyze factors affecting our business, anticipate changing consumer preferences and buying trends, and manage our inventory commensurate with customer demand, our sales levels and operating results may decline. |

| • | Our business and operating results may be harmed if we are unable to timely and effectively deliver merchandise to our stores and customers. |

| • | Our failure to successfully manage our order-taking and fulfillment operations could have a negative impact on our business and operating results |

| • | We must protect and maintain our brand image and reputation. |

| • | Our sales may be negatively impacted by increasing competition from companies with brands or products similar to ours. |

| • | Our facilities and systems, as well as those of our vendors, are vulnerable to natural disasters, adverse weather conditions, technology issues and other unexpected events, any of which could result in an interruption in our business and harm our operating results. |

| • | If we are unable to effectively manage our e-commerce business and digital marketing efforts, our reputation and operating results may be harmed. |

| • | Declines in our comparable brand revenues may harm our operating results and cause a decline in the market price of our common stock. |

| • | Our failure to successfully anticipate merchandise returns might have a negative impact on our business. |

| • | Our failure to successfully manage the costs and performance of our catalog mailings might have a negative impact on our business. |

| • | If we are unable to successfully manage the complexities associated with an omni-channel and multi-brand business, we may suffer declines in our existing business and our ability to attract new business. |

| • | A number of factors that affect our ability to successfully open new stores or close existing stores are beyond our control, and these factors may harm our ability to expand or contract our retail operations and harm our ability to increase our sales and profits. |

| • | Our inability or failure to protect our intellectual property would have a negative impact on our brands, reputation and operating results. |

| • | We outsource certain aspects of our business to third-party vendors and are in the process of insourcing certain business functions from third-party vendors, both of which subject us to risks. |

| • | If we fail to attract and retain key personnel, our business and operating results may be harmed. |

| • | If we are unable to introduce new brands and brand extensions successfully, or to reposition or close existing brands, our business and operating results may be negatively impacted. |

| • | We may be subject to legal proceedings that could result in costly litigation, require significant amounts of management time and result in the diversion of significant operational resources. |

Risks Related to Technology

| • | We may be exposed to cybersecurity risks and costs associated with credit card fraud, identity theft and business interruption that could cause us to incur unexpected expenses and loss of revenue. |

9

| • | We receive, process, store, use and share data, some of which contains personal information, which subjects us to complex and evolving governmental regulation and other legal obligations related to data privacy, data protection and other matters. |

| • | We are undertaking certain systems changes that might disrupt our business operations. |

Risks Related to Our Vendors and Our Global Operations

| • | Our dependence on foreign vendors and our increased global operations subject us to a variety of risks and uncertainties that could impact our operations and financial results. |

| • | We depend on foreign vendors and third-party agents for timely and effective sourcing of our merchandise, and we may not be able to acquire products in sufficient quantities and at acceptable prices to meet our needs. |

| • | If our vendors fail to adhere to our quality control standards and test protocols, we may delay a product launch or recall a product, which could damage our reputation and negatively affect our operations and financial results. |

| • | Our efforts to expand globally may not be successful and could negatively impact the value of our brands. |

| • | We have limited experience operating on a global basis and our failure to effectively manage the risks and challenges inherent in a global business could adversely affect our business, operating results and financial condition and growth prospects. |

Risks Related to Taxes and Tariffs

| • | Any significant changes in tax, trade or other policies in the U.S. or other countries, including policies that restrict imports or increase import tariffs, could have a material adverse effect on our results of operations. |

| • | Tariffs could result in increased prices and/or costs of goods or delays in product received from our vendors and could adversely affect our results of operations. |

| • | Fluctuations in our tax obligations and effective tax rate may result in volatility of our operating results. |

Risks Related to Our Financial Statements and Liquidity

| • | We may require funding from external sources, which may not be available at the levels we require, or may cost more than we expect. |

| • | Our operating results may be harmed by unsuccessful management of our employment, occupancy and other operating costs, and the operation and growth of our business may be harmed if we are unable to attract qualified personnel. |

| • | Our inability to obtain commercial insurance at acceptable rates or our failure to adequately reserve for self-insured exposures might increase our expenses and have a negative impact on our business. |

| • | If our operating and financial performance in any given period does not meet the guidance that we have provided to the public or the expectations of our investors and analysts, our stock price may decline. |

| • | A variety of factors, including seasonality and the economic environment, may cause our quarterly operating results to fluctuate, leading to volatility in our stock price. |

| • | Disruptions in the financial markets may adversely affect our liquidity and capital resources and our business. |

| • | Changes in the method of determining the London Interbank Offered Rate, or LIBOR, or the replacement of LIBOR with an alternative reference rate, may adversely affect our financial condition and results of operations. |

| • | If we are unable to pay quarterly dividends or repurchase our stock at intended levels, our reputation and stock price may be harmed. |

| • | If we fail to maintain proper and effective internal controls, our ability to produce accurate and timely financial statements could be impaired and our investors’ views of us could be harmed. |

| • | Changes to accounting rules or regulations may adversely affect our operating results. |

| • | In preparing our financial statements we make certain assumptions, judgments and estimates that affect the amounts reported, which, if not accurate, may impact our financial results. |

| • | Changes to estimates related to our cash flow projections may cause us to incur impairment charges related to our long-lived assets for our retail store locations and other property and equipment, including information technology systems, as well as goodwill. |

10

Risks Related to our Business

Our business has been and may continue to be materially impacted by the

COVID-19

pandemic, and the duration and extent to which this will impact our future results of operations and overall financial performance remains uncertain. Our business has been and may continue to be materially impacted by the

COVID-19

pandemic, which has negatively affected the U.S. and global economies, disrupted businesses and financial markets, and led to significant travel and transportation restrictions, mandatory closures of non-essential

retailers and other businesses, and orders to “shelter-in-place”.

On March 11, 2020, the World Health Organization declared

COVID-19

to be a global pandemic and recommended containment and mitigation measures worldwide. In March 2020, we announced the temporary closures of all of our retail store operations to protect our employees, customers and the communities in which we operate and to help contain the COVID-19

pandemic. The preventative or protective actions that governments and businesses around the world have taken to contain the spread of COVID-19

have resulted in a period of disruption that has and may continue to negatively impact our retail store revenues which comprised approximately 30% of our net revenues in fiscal 2020. As of January 31, 2021, the majority of our retail stores had reopened for in-person

shopping. However, given the continued uncertainty around COVID-19

due to high rates of infections in certain areas, state and local officials in certain geographies have extended closures or restrictions on retail capacity, which may continue to impact our store traffic and retail revenues, and may result in future store impairments. Additionally, federal, state and local governments may impose new restrictions on retail operations, which could affect our ability to operate our retail stores until such restrictions are lifted. Such reduced traffic and store closures have and may continue to result in material reductions in our retail store revenues and operating income as well as store asset impairment charges and write-offs, which have and may continue to negatively affect our operating results. Further, while we have implemented strict safety protocols based on Center for Disease Control and Prevention and government recommendations in stores that we have re-opened,

there is no guarantee that such protocols will be effective, and any virus-related illnesses linked or alleged to be linked to our stores, whether accurate or not, may negatively affect our reputation, operating results and/or financial condition. Although to date, the impact of our store closures on our retail store revenues has been more than offset by growth in our

e-commerce

business, there is no guarantee that such growth will continue over a prolonged period of time when the pandemic subsides and consumers spend less time at home, or if the COVID-19

pandemic worsens due to new variants, either of which could result in decreased consumer spending in the markets in which we operate. We have also implemented temporary work-from-home policies for certain employees, which continue to be in effect. While such policies have not significantly impacted productivity or disrupted our business to date, over a prolonged period of time, such policies could adversely impact our ability to conduct our business in the ordinary course.

Governmental mandates, illness or the absence of a substantial number of distribution center employees may require in the future that we temporarily close one or more of our distribution centers, or may prohibit or significantly limit us, or our third-party logistics providers from delivering packages to our customers and our stores, which could complicate or prevent us from fulfilling

e-commerce

orders and could complicate or prevent our ability to supply merchandise to our stores. As of the date of this report, all our distribution centers remain open and operational, but we continue to experience delays resulting from a shortage of shipping containers needed to ship our products, port congestion, and capacity constraints by our carriers in the delivery of our products. We also have incurred and expect to continue to incur higher shipping costs due to the various surcharges that have been announced by third party shippers on retailers, which are related to the increased shipping demand resulting from the

COVID-19

pandemic. These higher costs affected us in the third quarter of 2020 and even more so in the fourth quarter of 2020 as a result of peak surcharges during the holiday season and could continue to affect us thereafter. 11

Further,

COVID-19

related containment efforts and illnesses could also impact our vendors who manufacture or deliver our merchandise to us or our customers, which could adversely affect our ability to acquire and sell our merchandise, thus adversely affecting our results of operations, cash flows and liquidity. The

COVID-19

pandemic continues to rapidly evolve. The ultimate impact of the COVID-19

pandemic on our results, financial position and liquidity will depend on future developments, which are highly uncertain and cannot be predicted, such as the transmission rate of the disease, including the impact from new variants, the extent and effectiveness of containment actions and vaccination rollout, particularly as areas are reopened, and the impact of these and other factors on our stores, offices, employees, distributors, vendors and customers. If we are not able to respond to and manage the impact of such events effectively, our business, operating results, financial condition and cash flows could be adversely affected. Declines in general economic conditions, and the resulting impact on consumer confidence and consumer spending, could adversely impact our results of operations.

Our financial performance is subject to declines in general economic conditions and the impact of such economic conditions on levels of consumer confidence and consumer spending. Consumer confidence and consumer spending may deteriorate significantly, and could remain depressed for an extended period of time. Consumer purchases of discretionary items, including our merchandise, generally decline during periods when disposable income is limited, unemployment rates increase or there is economic uncertainty. An uncertain economic environment could also cause our vendors to go out of business or our banks to discontinue lending to us or our vendors, or it could cause us to undergo restructurings, any of which would adversely impact our business and operating results.

We are unable to control many of the factors affecting consumer spending, and declines in consumer spending on home furnishings and kitchen products in general could reduce demand for our products.

Our business depends on consumer demand for our products and, consequently, is sensitive to a number of factors that influence consumer spending, including general economic conditions, consumer disposable income, fuel prices, recession and fears of recession, unemployment, war and fears of war, outbreaks of disease (such as the

COVID-19

pandemic), adverse weather, availability of consumer credit, consumer debt levels, conditions in the housing market, interest rates, sales tax rates and rate increases, inflation, consumer confidence in future economic and political conditions, and consumer perceptions of personal well-being and security. In particular, past economic downturns have led to decreased discretionary spending, which adversely impacted our business. In addition, periods of decreased home purchases typically lead to decreased consumer spending on home products. These factors have affected, and may in the future affect, our various brands and channels differently. Adverse changes in factors affecting discretionary consumer spending have reduced and may in the future reduce consumer demand for our products, thus reducing our sales and harming our business and operating results. If we are unable to identify and analyze factors affecting our business, anticipate changing consumer preferences and buying trends, and manage our inventory commensurate with customer demand, our sales levels and operating results may decline.

Our success depends, in large part, upon our ability to identify and analyze factors affecting our business and to anticipate and respond in a timely manner to changing merchandise trends and customer demands in order to maintain and attract customers. For example, in the specialty home products business, style and color trends are constantly evolving. As a result, consumer preferences cannot be predicted with certainty and may change between selling seasons. We must be able to stay current with preferences and trends in our brands and address the customer tastes for each of our target customer demographics. Additionally, changes in customer preferences and buying trends may also affect our brands differently. We must also be able to identify and adjust the customer offerings in our brands to cater to customer demands. For example, a change in customer preferences for children’s room furnishings may not correlate to a similar change in buying trends for other home furnishings. If we misjudge either the market for our merchandise or our customers’ purchasing habits, our sales may decline significantly or may be delayed while we work to fill related backorders. Alternatively, we may be

12

required to mark down certain products to sell any excess inventory or to sell such inventory through our outlet stores or other liquidation channels at prices which are significantly lower than our retail prices, any of which would negatively impact our business and operating results.

In addition, we must manage our inventory effectively and commensurate with customer demand. Much of our inventory is sourced from vendors located outside of the U.S. Thus, we usually must order merchandise, and enter into contracts for the purchase and manufacturing of such merchandise, up to twelve months and generally multiple seasons in advance of the applicable selling season and frequently before trends are known. The extended lead times for many of our purchases may make it difficult for us to respond rapidly to new or changing trends. Our vendors also may not have the capacity to handle our demands or may go out of business or have other delays in production in times of economic crisis. In addition, the seasonal nature of the specialty home products business requires us to carry a significant amount of inventory prior to peak selling season. As a result, we are vulnerable to demand and pricing shifts and to misjudgments in the selection and timing of merchandise purchases. If we do not accurately predict our customers’ preferences and acceptance levels of our products, our inventory levels will not be appropriate, and our business and operating results may be negatively impacted.

There is also increased focus, including by governmental and

non-governmental

organizations, investors, customers, consumers and other stakeholders, on corporate social responsibility and sustainability matters. Our reputation could be damaged if we do not (or are perceived not to) act responsibly with respect to any social or sustainability matters, which could negatively impact our business and results of operations. Our business and operating results may be harmed if we are unable to timely and effectively deliver merchandise to our stores and customers.

If we are unable to effectively manage our inventory levels and responsiveness of our supply chain, including predicting the appropriate levels and type of inventory to stock within each of our distribution facilities, our business and operating results may be harmed. For example, we continue to experience elevated levels of demand for many of our products, and as a result, we may encounter delays in fulfilling this demand and replenishing to appropriate inventory levels. Continued or lengthy delays in fulfilling customer demand could cause our customers to shop with our competitors instead of us, which could harm our business. Additionally, although we continue to insource furniture delivery hubs in certain geographies and continue with the regionalization of our retail and

e-commerce

fulfillment capabilities, we are subject to risks that may disrupt our supply chain operations or regionalization efforts, such as increasing labor costs, union organizing activity and our ability to effectively locate real estate for our distribution facilities or other supply chain operations. Further, we cannot control all of the various factors that might affect our

e-commerce

fulfillment rates and timely and effective merchandise delivery to our stores. We rely upon third-party carriers for our merchandise shipments and reliable data regarding the timing of those shipments, including shipments to our customers and to and from our stores. In addition, we are heavily dependent upon two carriers for the delivery of our merchandise to our customers. As a result of our dependence on all of these third-party providers, we are subject to risks, including labor disputes, union organizing activity, adverse weather, natural disasters, climate change, the closure of such carriers’ offices or a reduction in operational hours due to an economic slowdown or the inability to sufficiently ramp up operational hours during an economic recovery or upturn, availability of adequate trucking or railway providers, possible acts of terrorism, outbreaks of disease (such as the COVID-19

pandemic) or other factors affecting such carriers’ ability to provide delivery services to meet our shipping needs, disruptions or increased fuel costs and costs associated with any regulations to address climate change. For example, our third-party providers have experienced transportation disruptions and restrictions due to the COVID-19

pandemic and delays stemming from delayed shipments from Asian ports, congestion at west coast ports, and a shortage of shipping containers needed to ship our products, which has adversely impacted our inventory levels and resulted in elevated, and sometimes lengthy, customer backorders. Further, we have experienced, and may continue to experience shortages of raw materials used to make our products. Failure to deliver merchandise in a timely and effective manner could cause customers to cancel their orders and could damage our reputation and brands. In addition, fuel costs have been volatile and airline and other transportation companies continue to struggle to operate profitably, which could lead to increased fulfillment expenses. Any rise in fulfillment expenses could negatively affect our business and operating results. 13

Our failure to successfully manage our order-taking and fulfillment operations could have a negative impact on our business and operating results.

Our

e-commerce

business depends, in part, on our ability to maintain efficient and uninterrupted order-taking and fulfillment operations in our distribution facilities, our customer care centers and on our e-commerce

websites. Disruptions or slowdowns in these areas could result from disruptions in telephone or network services, power outages, inadequate system capacity, system hardware or software issues, computer viruses, security breaches, human error, changes in programming, union organizing activity, insufficient or inadequate labor to fulfill the orders, disruptions in our third-party labor contracts, inefficiencies due to inventory levels and limited distribution facility space, issues with third-party order fulfillment and drop shipping, natural disasters, adverse weather conditions, outbreaks of disease (such as the COVID-19

pandemic) or acts of terrorism. Industries that are particularly seasonal, such as the home furnishings business, face a higher risk of harm from operational disruptions during peak sales seasons. These problems could result in a reduction in sales as well as increased expenses. In addition, we face the risk that we cannot hire enough qualified employees to support our

e-commerce

operations, or that there will be a disruption in the workforce we hire from our third-party providers, especially during our peak season. The need to operate with fewer employees could negatively impact our customer service levels and our operations. We must protect and maintain our brand image and reputation.

Our brands have wide recognition, and our success has been due in large part to our ability to maintain, enhance and protect our brand image and reputation and our customers’ connection to our brands. Our continued success depends in part on our ability to adapt to a rapidly changing media environment, including our increasing reliance on social media and online dissemination of advertising campaigns. Even if we react appropriately to negative posts or comments about us and/or our brands on social media and online, our customers’ perception of our brand image and our reputation could be negatively impacted. In addition, customer sentiment could be shaped by our sustainability policies and related design, sourcing and operations decisions. Failure to maintain, enhance and protect our brand image could have a material adverse effect on our results of operations.

Our sales may be negatively impacted by increasing competition from companies with brands or products similar to ours.

The specialty businesses and specialty stores. The substantial sales growth in the

e-commerce

and retail businesses are highly competitive. We compete with other retailers that market lines of merchandise similar to ours. We compete with national, regional and local businesses that utilize a similar retail store strategy, as well as traditional furniture stores, department stores, direct-to-consumer

e-commerce

industry within the last decade has encouraged the entry of many new competitors, including discount retailers selling similar products at reduced prices, new business models, and an increase in competition from established companies, many of whom are willing to spend significant funds and/or reduce pricing in order to gain market share. The competitive challenges facing us include:

| • | anticipating and quickly responding to changing consumer demands or preferences better than our competitors; |

| • | maintaining favorable brand recognition and achieving customer perception of value; |

| • | effectively marketing and competitively pricing our products to consumers in several diverse market segments; |

| • | effectively managing and controlling our costs; |

| • | effectively managing increasingly competitive promotional activity; |

| • | effectively attracting new customers; |

| • | developing new innovative shopping experiences, like mobile and tablet applications that effectively engage today’s digital customers; |

14

| • | developing innovative, high-quality products in colors and styles that appeal to consumers of varying age groups, tastes and regions, and in ways that favorably distinguish us from our competitors; and |

| • | effectively managing our supply chain and distribution strategies in order to provide our products to our consumers on a timely basis and minimize returns, replacements and damaged products. |

In light of the many competitive challenges facing us, we may not be able to compete successfully. Increased competition could reduce our sales and harm our operating results and business.

Our facilities and systems, as well as those of our vendors, are vulnerable to natural disasters, adverse weather conditions, technology issues and other unexpected events, any of which could result in an interruption in our business and harm our operating results.

Our retail stores, corporate offices, distribution and manufacturing facilities, infrastructure and

e-commerce

operations, as well as the operations of our vendors from which we receive goods and services, are vulnerable to damage from earthquakes, tornadoes, hurricanes, fires, floods or other volatile weather, power losses, telecommunications failures, hardware and software failures, computer viruses and similar events. If any of these events result in damage to our facilities or systems, or those of our vendors, we may experience interruptions in our business until the damage is repaired, resulting in the potential loss of customers and revenues. In addition, we may incur costs in repairing any damage beyond our applicable insurance coverage. If we are unable to effectively manage our

e-commerce

business and digital marketing efforts, our reputation and operating results may be harmed. Our

e-commerce

channel has been our fastest growing business over the last several years and represented more than 70% of our net revenues and profits in fiscal 2020. The success of our e-commerce

business depends, in part, on third parties and factors over which we have limited control. We must continually respond to changing consumer preferences and buying trends relating to e-commerce

usage, including an emphasis on mobile e-commerce.

Our success in e-commerce

has been strengthened in part by our ability to leverage the information we have on our customers to infer customer interests and affinities such that we can personalize the experience they have with us. We also utilize digital advertising to target internet and mobile users whose behavior indicates they might be interested in our products. Current or future legislation may reduce or restrict our ability to use these techniques, which could reduce the effectiveness of our marketing efforts. We are also vulnerable to certain additional risks and uncertainties associated with our

e-commerce

and mobile websites and digital marketing efforts, including: changes in required technology interfaces; website downtime and other technical failures; internet connectivity issues; costs and technical issues as we upgrade our website software; computer viruses; vendor reliability; changes in applicable federal and state regulations, such as the California Consumer Privacy Act (“CCPA”), and related compliance costs; security breaches; and consumer privacy concerns. We must keep up to date with competitive technology trends and opportunities that are emerging throughout the retail environment, including the use of new or improved technology, evolving creative user interfaces, and other e-commerce

marketing trends such as paid search, re-targeting,

loyalty programs and the proliferation of mobile usage, among others. While we endeavor to predict and invest in technology that is most relevant and beneficial to our company, such as our acquisition of Outward, Inc. in 2017, our initiatives may not prove to be successful, may increase our costs, or may not succeed in driving sales or attracting customers. Our failure to successfully respond to these risks and uncertainties might adversely affect the sales or margin in our e-commerce

business, require us to impair certain assets, and damage our reputation and brands. Declines in our comparable brand revenues may harm our operating results and cause a decline in the market price of our common stock.

Various factors affect comparable brand revenues, including the number, size and location of stores we open, close, remodel or expand in any period, the overall economic and general retail sales environment, consumer preferences and buying trends, changes in sales mix among distribution channels, our ability to efficiently source and distribute products, changes in our merchandise mix, competition (including competitive promotional activity and discount retailers), current local and global economic conditions, the timing of our releases of new

15

merchandise and promotional events, the success of marketing programs, the cannibalization of existing store sales by our new stores, changes in catalog circulation and in our

e-commerce

business and fluctuations in foreign exchange rates. Among other things, weather conditions have affected, and may continue to affect, comparable brand revenues by limiting our ability to deliver our products to our stores, altering consumer behavior, or requiring us to close certain stores temporarily, thus reducing store traffic. Even if stores are not closed, many customers may decide to avoid going to stores in bad weather. These factors have caused, and may continue to cause, our comparable brand revenue results to differ materially from prior periods and from earnings guidance we have provided. For example, the overall economic and general retail sales environment, as well as local and global economic conditions, has caused a significant decline in our comparable brand revenue results in the past. In addition, public health conditions (such as the COVID-19

pandemic), or other unforeseen events, could affect our ability to deliver our products to our stores, alter consumer behavior, or require us to close certain stores temporarily or reduce customer capacity within certain stores temporarily, thus reducing store traffic and materially impacting our comparable brand revenues. Our comparable brand revenues have fluctuated significantly in the past on an annual, quarterly and monthly basis, and we expect that comparable brand revenues will continue to fluctuate in the future. In addition, past comparable brand revenues are not necessarily an indication of future results and comparable brand revenues may decrease in the future. Our ability to improve our comparable brand revenue results depends, in large part, on maintaining and improving our forecasting of customer demand and buying trends, selecting effective marketing techniques, effectively driving traffic to our stores,

e-commerce

websites and direct-mail catalogs through marketing and various promotional events, providing an appropriate mix of merchandise for our broad and diverse customer base and using effective pricing strategies. Any failure to meet the comparable brand revenue expectations of investors and securities analysts in one or more future periods could significantly reduce the market price of our common stock. Our failure to successfully anticipate merchandise returns might have a negative impact on our business.

We record a reserve for merchandise returns based on historical return trends together with current product sales performance in each reporting period. If actual returns are greater than those projected and reserved for by management, additional sales returns might be recorded in the future. In addition, to the extent that returned merchandise is damaged, we often do not receive full retail value from the resale or liquidation of the merchandise. Further, the introduction of new merchandise, changes in merchandise mix, changes in consumer confidence, or other competitive and general economic conditions may cause actual returns to differ from merchandise return reserves. Any significant increase in merchandise returns that exceeds our reserves could harm our business and operating results.

Our failure to successfully manage the costs and performance of our catalog mailings might have a negative impact on our business.

We use catalog mailings in the course of our marketing activities. The cost of paper, printing and catalog distribution impacts our catalog business. Postal rates affect the cost of our catalog mailings, which may be increased at any time. Postal service delays can affect the timing of catalog delivery, which could cause customers to forego or defer purchases. We have also consolidated all of our catalog printing work with one printer and all of our paper purchasing through a single broker, which subjects us to various risks if the vendor or broker fails to perform under our agreements. Paper costs have also fluctuated significantly in the past and may continue to fluctuate in the future, due, in part, to consolidation within the paper industry. Our dependence on a single broker and/or further consolidation in the paper industry could limit our ability in the future to obtain favorable terms including price, custom paper quality, paper quantity and service.

We have historically experienced fluctuations in our customers’ response to our catalogs. Customer response to our catalogs is substantially dependent on merchandise assortment, availability and creative presentation, as well as the selection of customers to whom the catalogs are mailed, timing of delivery of our mailings, the general retail sales environment and current domestic and global economic conditions. In addition, environmental organizations and other consumer advocacy groups may attempt to create an unfavorable impression of our paper use in catalogs and our distribution of catalogs generally, which may have a negative effect on our sales and our

16

reputation. In addition, if we misjudge the correlation between our catalog circulation and net sales, or if our catalog strategy overall does not continue to be successful, our results of operations could be negatively impacted.

If we are unable to successfully manage the complexities associated with an omni-channel and multi-brand business, we may suffer declines in our existing business and our ability to attract new business.

With the expansion of our

e-commerce

business, the development of new brands, acquired brands, and brand extensions, our overall business has become substantially more complex. The changes in our business have forced us to develop new expertise and face new challenges, risks and uncertainties. For example, we face the risk that our e-commerce

business, including our catalog circulation, might cannibalize a significant portion of our retail sales or our newer brands, brand extensions and products may result in a decrease in sales of existing brands and products. While we recognize that our e-commerce

sales and sales from new brands and products cannot be entirely incremental to sales through our retail channel or from existing brands and products, respectively, we seek to attract as many new customers as possible with the most relevant channels, brands and products to meet customer needs and grow our market share. We continually analyze the business results of our channels, brands and products in an effort to find opportunities to build incremental sales. A number of factors that affect our ability to successfully open new stores or close existing stores are beyond our control, and these factors may harm our ability to expand or contract our retail operations and harm our ability to increase our sales and profits.

As noted above, approximately 30% of our net revenues are generated by our retail stores. Our ability to open additional stores or close existing stores successfully will depend upon a number of factors, including:

| • | general economic conditions; |

| • | our identification of, and the availability of, suitable store locations; |

| • | our success in negotiating new leases and amending, subleasing or terminating existing leases on acceptable terms; |

| • | the success of other retail stores in and around our retail locations; |

| • | our ability to secure required governmental permits and approvals; |

| • | our hiring and training of skilled store operating personnel, especially management; |

| • | the availability of financing on acceptable terms, if at all; and |

| • | the financial stability of our landlords and potential landlords. |

Many of these factors are beyond our control. For example, for the purpose of identifying suitable store locations, we rely, in part, on demographic surveys regarding the location of consumers in our target market segments. While we believe that the surveys and other relevant information are helpful indicators of suitable store locations, we recognize that these information sources cannot predict future consumer preferences and buying trends with complete accuracy. In addition, changes in demographics, in consumer shopping patterns, such as a reduction in mall traffic, in the types of merchandise that we sell and in the pricing of our products, may reduce the number of suitable store locations or cause formerly suitable locations to become less desirable. Further, time frames for lease negotiations and store development vary from location to location and can be subject to unforeseen delays or unexpected cancellations. We may not be able to open new stores or, if opened, operate those stores profitably. Construction and other delays in store openings could have a negative impact on our business and operating results. Additionally, we may not be able to renegotiate the terms of our current leases or close our underperforming stores on terms favorable to us, any of which could negatively impact our operating results. As a result of the

COVID-19

pandemic, the above factors have become even more unpredictable than they have been historically. Our typical methods of managing these risks and uncertainties may not be sufficient, and as a result, our business and operating results could be negatively impacted. Our inability or failure to protect our intellectual property would have a negative impact on our brands, reputation and operating results.

We may not be able to effectively protect our intellectual property in the U.S. or in foreign jurisdictions, particularly as we continue to expand globally. Our trademarks, service marks, copyrights, trade dress rights,

17

trade secrets, domain names, patents, designs, proprietary technology and other intellectual property are valuable assets that are critical to our success. The unauthorized reproduction, theft or other misappropriation of our intellectual property could diminish the value of our brands or reputation and cause a decline in our sales. Protection of our intellectual property and maintenance of distinct branding are particularly important as they distinguish our products and services from our competitors. In addition, the costs of protecting and policing our intellectual property assets may adversely affect our operating results.

We outsource certain aspects of our business to third-party vendors and are in the process of insourcing certain business functions from third-party vendors, both of which subject us to risks, including disruptions in our business and increased costs.

We outsource certain aspects of our business to third-party vendors that subject us to risks of disruptions in our business as well as increased costs. For example, we utilize outside vendors for such things as payroll processing, email and other digital marketing and various distribution facilities and delivery services. In some cases, we rely on a single vendor for such services. Accordingly, we are subject to the risks associated with their ability to successfully provide the necessary services to meet our needs. If our vendors are unable to adequately protect our data and information is lost, our ability to deliver our services is interrupted, our vendors’ fees are higher than expected, or our vendors make mistakes in the execution of operations support, then our business and operating results may be negatively impacted.

In addition, in the past, we have insourced certain aspects of our business, including certain technology services and the management of certain furniture manufacturing and delivery, each of which were previously outsourced to third-party providers. We may also need to continue to insource other aspects of our business in the future in order to control our costs and to stay competitive. This may cause disruptions in our business and result in increased cost to us. In addition, if we are unable to perform these functions better than, or at least as well as, our third-party providers, our business may be harmed.

If we fail to attract and retain key personnel, our business and operating results may be harmed.

Our future success depends to a significant degree on the skills, experience and efforts of key personnel in our senior management, whose vision for our company, knowledge of our business and expertise would be difficult to replace. If any one of our key employees leaves, is seriously injured or unable to work, or fails to perform and we are unable to find a qualified replacement, we may be unable to execute our business strategy. In addition, our main offices are located in the San Francisco Bay Area, where competition for personnel with retail and technology skills can be intense. In addition, several of our strategic initiatives, including our technology and supply chain initiatives, require that we hire and/or develop employees with appropriate experience. We may not be successful in recruiting, retaining and motivating skilled personnel domestically or globally who have the requisite experience to achieve our global business goals, and failure to do so may harm our business. Further, in the event we need to hire additional personnel, we may experience difficulties in attracting and successfully hiring such individuals due to competition for highly skilled personnel, as well as the significantly higher cost of living expenses in our markets. Additionally, as a result the

COVID-19

pandemic, if long-term, remote or flexible work options become more commonplace, potential employees may choose to move to lower cost of living areas, which could negatively impact our ability to recruit appropriately skilled personnel for positions that cannot be performed remotely. If we are unable to introduce new brands and brand extensions successfully, or to reposition or close existing brands, our business and operating results may be negatively impacted.