UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

| | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the quarterly period ended

or

| | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

| Commission file number | |

HECLA MINING COMPANY

(Exact name of registrant as specified in its Charter)

| | | |||

| State or Other Jurisdiction of | I.R.S. Employer | |||

| Incorporation or Organization | Identification No. | |||

| | ||||

| | | |||

| Address of Principal Executive Offices | Zip Code | |||

| | ||||

| Registrant's Telephone Number, Including Area Code | ||||

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered |

| | | |

| | | |

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act:

| | Accelerated filer ☐ |

| Non-accelerated filer ☐ | Smaller reporting company |

| Emerging growth company |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes

Indicate the number of shares outstanding of each of the issuer’s classes of common stock, as of the latest practicable date.

| Class | Shares Outstanding May 5, 2022 | |

| Common stock, par value $0.25 per share |

Hecla Mining Company and Subsidiaries

Form 10-Q

For the Quarter Ended March 31, 2022

INDEX*

| *Items 2, 3 and 5 of Part II are omitted as they are not applicable. |

Part I - Financial Information

Item 1. Financial Statements

Hecla Mining Company and Subsidiaries

Condensed Consolidated Statements of Operations and Comprehensive (Loss) Income (Unaudited)

(Dollars and shares in thousands, except for per-share amounts)

| Three Months Ended |

||||||||

| March 31, 2022 |

March 31, 2021 |

|||||||

| Sales of products |

$ | $ | ||||||

| Cost of sales and other direct production costs |

||||||||

| Depreciation, depletion and amortization |

||||||||

| Total cost of sales |

||||||||

| Gross profit |

||||||||

| Other operating expenses: |

||||||||

| General and administrative |

||||||||

| Exploration and pre-development |

||||||||

| Care and maintenance |

||||||||

| Provision for closed operations and reclamation |

||||||||

| Other operating expense |

||||||||

| Total other operating expense |

||||||||

| Income from operations |

||||||||

| Other income (expense): |

||||||||

| Interest expense |

( |

) | ( |

) | ||||

| Fair value adjustments, net |

( |

) | ||||||

| Net foreign exchange loss |

( |

) | ( |

) | ||||

| Other non-operating income (expense) |

( |

) | ||||||

| Total other expense |

( |

) | ( |

) | ||||

| Income before income and mining taxes |

||||||||

| Income and mining tax provision |

( |

) | ( |

) | ||||

| Net income |

||||||||

| Preferred stock dividends |

( |

) | ( |

) | ||||

| Income applicable to common stockholders |

$ | $ | ||||||

| Comprehensive income: |

||||||||

| Net income |

$ | $ | ||||||

| Change in fair value of derivative contracts designated as hedge transactions |

( |

) | ||||||

| Comprehensive (loss) income |

$ | ( |

) | $ | ||||

| Basic income per common share after preferred dividends |

$ | $ | ||||||

| Diluted income per common share after preferred dividends |

$ | $ | ||||||

| Weighted average number of common shares outstanding - basic |

||||||||

| Weighted average number of common shares outstanding - diluted |

||||||||

| Cash dividends per common share |

$ | $ | ||||||

The accompanying notes are an integral part of the interim condensed consolidated financial statements.

Hecla Mining Company and Subsidiaries

Condensed Consolidated Statements of Cash Flows (Unaudited)

(In thousands)

| Three Months Ended |

||||||||

| March 31, 2022 |

March 31, 2021 |

|||||||

| Operating activities: |

||||||||

| Net income |

$ | $ | ||||||

| Non-cash elements included in net income: |

||||||||

| Depreciation, depletion and amortization |

||||||||

| Provision for reclamation and closure costs |

||||||||

| Stock-based compensation expense |

||||||||

| Deferred taxes |

||||||||

| Fair value adjustments, net |

( |

) | ( |

) | ||||

| Foreign exchange loss |

||||||||

| Other non-cash items, net |

||||||||

| Change in assets and liabilities: |

||||||||

| Accounts receivable |

( |

) | ||||||

| Inventories |

( |

) | ||||||

| Other current and non-current assets |

||||||||

| Accounts payable and accrued liabilities |

( |

) | ( |

) | ||||

| Accrued payroll and related benefits |

( |

) | ||||||

| Accrued taxes |

||||||||

| Accrued reclamation and closure costs and other non-current liabilities |

( |

) | ||||||

| Cash provided by operating activities |

||||||||

| Investing activities: |

||||||||

| Additions to properties, plants, equipment and mineral interests |

( |

) | ( |

) | ||||

| Proceeds from sale of investments |

||||||||

| Proceeds from disposition of properties, plants and equipment |

||||||||

| Purchases of investments |

( |

) | ||||||

| Net cash used in investing activities |

( |

) | ( |

) | ||||

| Financing activities: |

||||||||

| Acquisition of treasury shares |

( |

) | ||||||

| Dividends paid to common and preferred stockholders |

( |

) | ( |

) | ||||

| Credit facility fees paid |

( |

) | ( |

) | ||||

| Repayments of finance leases |

( |

) | ( |

) | ||||

| Net cash used in financing activities |

( |

) | ( |

) | ||||

| Effect of exchange rates on cash |

||||||||

| Net increase in cash, cash equivalents and restricted cash and cash equivalents |

||||||||

| Cash, cash equivalents and restricted cash and cash equivalents at beginning of period |

||||||||

| Cash, cash equivalents and restricted cash and cash equivalents at end of period |

$ | $ | ||||||

| Supplemental disclosure of cash flow information: |

||||||||

| Cash paid for interest |

$ | $ | ||||||

| Cash paid for income and mining taxes |

$ | $ | ||||||

| Significant non-cash investing and financing activities: |

||||||||

| Addition of finance lease obligations and right-of-use assets |

$ | $ | ||||||

| Accounts receivable for proceeds on exchange of investments |

$ | $ | ||||||

The accompanying notes are an integral part of the interim condensed consolidated financial statements.

Hecla Mining Company and Subsidiaries

Condensed Consolidated Balance Sheets (Unaudited)

(In thousands, except shares)

| March 31, | December 31, 2021 | |||||||

| ASSETS | ||||||||

| Current assets: | ||||||||

| Cash and cash equivalents | $ | $ | ||||||

| Accounts receivable: | ||||||||

| Trade | ||||||||

| Other, net | ||||||||

| Inventories: | ||||||||

| Concentrates, doré, and stockpiled ore | ||||||||

| Materials and supplies | ||||||||

| Other current assets | ||||||||

| Total current assets | ||||||||

| Investments | ||||||||

| Restricted cash and investments | ||||||||

| Properties, plants, equipment and mineral interests, net | ||||||||

| Operating lease right-of-use assets | ||||||||

| Deferred taxes | ||||||||

| Other non-current assets | ||||||||

| Total assets | $ | $ | ||||||

| LIABILITIES | ||||||||

| Current liabilities: | ||||||||

| Accounts payable and accrued liabilities | $ | $ | ||||||

| Accrued payroll and related benefits | ||||||||

| Accrued taxes | ||||||||

| Finance and operating leases | ||||||||

| Accrued reclamation and closure costs | ||||||||

| Accrued interest | ||||||||

| Derivatives liabilities | ||||||||

| Other current liabilities | ||||||||

| Total current liabilities | ||||||||

| Finance and operating leases | ||||||||

| Accrued reclamation and closure costs | ||||||||

| Long-term debt | ||||||||

| Deferred tax liability | ||||||||

| Derivatives liabilities | ||||||||

| Other non-current liabilities | ||||||||

| Total liabilities | ||||||||

| Commitments and contingencies (Notes 4, 7, 8, and 10) | ||||||||

| STOCKHOLDERS’ EQUITY | ||||||||

| Preferred stock, shares authorized: | ||||||||

| Series B preferred stock, $ par value, shares issued and outstanding, liquidation preference — $ | ||||||||

| Common stock, $ par value, authorized shares; issued March 31, 2022 — shares and December 31, 2021 — shares | ||||||||

| Capital surplus | ||||||||

| Accumulated deficit | ( | ) | ( | ) | ||||

| Accumulated other comprehensive loss | ( | ) | ( | ) | ||||

| Less treasury stock, at cost; March 31, 2022 — shares and December 31, 2021 - shares issued and held in treasury | ( | ) | ( | ) | ||||

| Total stockholders’ equity | ||||||||

| Total liabilities and stockholders’ equity | $ | $ | ||||||

The accompanying notes are an integral part of the interim condensed consolidated financial statements.

Hecla Mining Company and Subsidiaries

Condensed Consolidated Statements of Changes in Stockholders’ Equity (Unaudited)

(Dollars are in thousands, except for share and per share amounts)

| Three Months Ended March 31, 2022 | ||||||||||||||||||||||||||||

| Series B Preferred Stock | Common Stock | Additional Paid-In Capital | Accumulated Deficit | Accumulated Other Comprehensive Loss, net | Treasury Stock | Total | ||||||||||||||||||||||

| Balances, January 1, 2022 | $ | $ | $ | $ | ( | ) | $ | ( | ) | $ | ( | ) | $ | |||||||||||||||

| Net income | ||||||||||||||||||||||||||||

| Stock-based compensation expense | ||||||||||||||||||||||||||||

| Incentive compensation units distributed ( shares) | ( | ) | ( | ) | ( | ) | ||||||||||||||||||||||

| Common stock ($ per share) and Series B Preferred Stock ($ per share) dividends declared | ( | ) | ( | ) | ||||||||||||||||||||||||

| Common stock issued for 401(k) match ( shares) | ||||||||||||||||||||||||||||

| Other comprehensive income | ( | ) | ( | ) | ||||||||||||||||||||||||

| Balances, March 31, 2022 | $ | $ | $ | $ | ( | ) | $ | ( | ) | $ | ( | ) | $ | |||||||||||||||

| Three Months Ended March 31, 2021 | ||||||||||||||||||||||||||||

| Series B Preferred Stock | Common Stock | Additional Paid-In Capital | Accumulated Deficit | Accumulated Other Comprehensive Loss, net | Treasury Stock | Total | ||||||||||||||||||||||

| Balances, January 1, 2021 | $ | $ | $ | $ | ( | ) | $ | ( | ) | $ | ( | ) | $ | |||||||||||||||

| Net income | ||||||||||||||||||||||||||||

| Stock-based compensation expense | ||||||||||||||||||||||||||||

| Common stock ($ per share) and Series B Preferred Stock ($ per share) dividends declared | ( | ) | ( | ) | ||||||||||||||||||||||||

| Common stock issued for 401(k) match ( shares) | ||||||||||||||||||||||||||||

| Shares issued to pension plans ( shares) | ||||||||||||||||||||||||||||

| Other comprehensive income | ||||||||||||||||||||||||||||

| Balances, March 31, 2021 | $ | $ | $ | $ | ( | ) | $ | ( | ) | $ | ( | ) | $ | |||||||||||||||

The accompanying notes are an integral part of the interim condensed consolidated financial statements.

Note 1. Basis of Preparation of Financial Statements

The accompanying unaudited interim condensed consolidated financial statements of Hecla Mining Company and its subsidiaries (collectively, “Hecla,” “the Company,” “we,” “our,” or “us,” except where the context requires otherwise) have been prepared in accordance with the instructions to Form 10-Q and do not include all information and disclosures required annually by generally accepted accounting principles in the United States (“GAAP”). Therefore, this information should be read in conjunction with Hecla’s consolidated financial statements and notes contained in our annual report on Form 10-K for the year ended December 31, 2021 (“2021 Form 10-K”). The consolidated December 31, 2021 balance sheet data was derived from our audited consolidated financial statements. The information furnished herein reflects all adjustments that are, in the opinion of management, necessary for a fair statement of the results for the interim periods reported. All such adjustments are, in the opinion of management, of a normal recurring nature. Operating results for the three-month period ended March 31, 2022 are not necessarily indicative of the results that may be expected for the year ending December 31, 2022.

The 2019 novel strain of coronavirus (“COVID-19”) was characterized as a global pandemic by the World Health Organization on March 11, 2020. We continue to take precautionary measures to mitigate the impact of COVID-19, including implementing operational plans and practices. As long as they are required, the operational practices implemented could continue to have an adverse impact on our operating results due to deferred production and revenues or additional costs. We incurred $

Certain amounts in the prior year have been reclassified to conform to the current year presentation.

Note 2. Business Segments and Sales of Products

We discover, acquire and develop mines and other mineral interests and produce and market (i) concentrates, containing silver, gold, lead and zinc, (ii) carbon material containing silver and gold, and (iii) doré containing silver and gold. We are currently organized and managed in four segments: Greens Creek, Lucky Friday, Casa Berardi and Nevada Operations.

General corporate activities not associated with operating mines and their various exploration activities, as well as discontinued operations and idle properties, are presented as “other.” Interest expense, interest income and income and mining taxes are considered general corporate items, and are not allocated to our segments.

The following tables present information about our reportable segments for the three months ended March 31, 2022 and 2021 (in thousands):

| Three Months Ended |

||||||||

| 2022 |

2021 |

|||||||

| Sales of products: |

||||||||

| Greens Creek |

$ | $ | ||||||

| Lucky Friday |

||||||||

| Casa Berardi |

||||||||

| Nevada Operations |

||||||||

| Other |

||||||||

| $ | $ | |||||||

| Income (loss) from operations: |

||||||||

| Greens Creek |

$ | $ | ||||||

| Lucky Friday |

||||||||

| Casa Berardi |

( |

) | ||||||

| Nevada Operations |

( |

) | ( |

) | ||||

| Other |

( |

) | ( |

) | ||||

| $ | $ | |||||||

The following table presents identifiable assets by reportable segment as of March 31, 2022 and December 31, 2021 (in thousands):

| March 31, 2022 |

December 31, 2021 |

|||||||

| Identifiable assets: |

||||||||

| Greens Creek |

$ | $ | ||||||

| Lucky Friday |

||||||||

| Casa Berardi |

||||||||

| Nevada Operations |

||||||||

| Other |

||||||||

| $ | $ | |||||||

Sales of products by metal for the three-month periods ended March 31, 2022 and 2021 were as follows (in thousands):

| Three Months Ended March 31, |

||||||||

| 2022 |

2021 |

|||||||

| Silver |

$ | $ | ||||||

| Gold |

||||||||

| Lead |

||||||||

| Zinc |

||||||||

| Less: Smelter and refining charges |

( |

) | ( |

) | ||||

| Sales of products |

$ | $ | ||||||

Sales of products for the first three months of 2022 and 2021 included a net loss of $

Note 3. Income and Mining Taxes

Major components of our income and mining tax (provision) benefit for the three months ended March 31, 2022 and 2021 are as follows (in thousands):

| Three Months Ended | ||||||||

| March 31, | ||||||||

| 2022 | 2021 | |||||||

| Current: | ||||||||

| Domestic | $ | ( | ) | $ | ( | ) | ||

| Foreign | ( | ) | ( | ) | ||||

| Total current income and mining tax provision | ( | ) | ( | ) | ||||

| Deferred: | ||||||||

| Domestic | ( | ) | ||||||

| Foreign | ( | ) | ||||||

| Total deferred income and mining tax provision | ( | ) | ( | ) | ||||

| Total income and mining tax provision | $ | ( | ) | $ | ( | ) | ||

The income and mining tax provision for the three-month periods ended March 31, 2022 and 2021 varies from the amounts that would have resulted from applying the statutory tax rates to pre-tax income due primarily to the impact of taxation in foreign jurisdictions and non-recognition of net operating losses and foreign exchange gains and losses in certain jurisdictions.

For the three-month period ended March 31, 2022, we used the annual effective tax rate method to calculate the tax provision, a change from the discrete method used for the three-month period ended March 31, 2021, due to reversal of valuation allowance in the fourth quarter of 2021. Valuation allowances on Nevada, Mexico and certain Canadian net operating losses were treated as discrete adjustments to the annual effective tax rate method calculation, partially causing the increase in the income tax rate for the three-month period ended March 31, 2022 as compared to March 31, 2021.

Note 4. Employee Benefit Plans

We sponsor defined benefit pension plans covering substantially all U.S. employees. Net periodic pension cost for the plans consisted of the following for the three-month periods ended March 31, 2022 and 2021 (in thousands):

| Three Months Ended March 31, |

||||||||

| 2022 |

2021 |

|||||||

| Service cost |

$ | $ | ||||||

| Interest cost |

||||||||

| Expected return on plan assets |

( |

) | ( |

) | ||||

| Amortization of prior service cost |

||||||||

| Amortization of net loss |

||||||||

| Net periodic pension cost |

$ | $ | ||||||

The service cost component of net periodic pension cost is included in the same line items of our condensed consolidated financial statements as other employee compensation costs, and the net gain of $

We do not expect to be required to contribute to our defined benefit pension plans in 2022, but may do so.

Note 5. Income Per Common Share

We calculate basic income per common share on the basis of the weighted average number of shares of common stock outstanding during the period. Diluted income per share is calculated using the weighted average number of shares of common stock outstanding during the period plus the effect of potential dilutive common shares during the period using the treasury stock and if-converted methods.

Potential dilutive shares of common stock include outstanding unvested restricted stock awards, performance-based share awards, stock units, warrants and convertible preferred stock for periods in which we have reported net income. For periods in which we report net losses, potential dilutive shares of common stock are excluded, as their conversion and exercise would be anti-dilutive.

The following table represents net income per common share – basic and diluted (in thousands, except income (loss) per share):

| Three Months Ended March 31, |

||||||||

| 2022 |

2021 |

|||||||

| Numerator |

||||||||

| Net income |

$ | $ | ||||||

| Preferred stock dividends |

( |

) | ( |

) | ||||

| Net income applicable to common shares |

$ | $ | ||||||

| Denominator |

||||||||

| Basic weighted average common shares |

||||||||

| Dilutive incentive compensation units, warrants and deferred shares |

||||||||

| Diluted weighted average common shares |

||||||||

| Basic income per common share |

$ | $ | ||||||

| Diluted income per common share |

$ | $ | ||||||

Diluted income per common share for the three-month periods ended March 31, 2022 and 2021 excludes the potential effects of outstanding shares of our convertible preferred stock, as their conversion would have no effect on the calculation of dilutive shares.

For the three months ended March 31, 2022, the calculation of diluted income per common share included (i)

Note 6. Stockholders’ Equity

Stock-based Compensation Plans

Stock-based compensation expense for restricted stock unit and performance-based grants to employees and shares issued to non-employee directors totaled $

Common Stock Dividends

On , our Board of Directors declared a quarterly cash dividend of $

Note 7. Debt, Credit Facility and Leases

Our debt as of March 31, 2022 and December 31, 2021 consisted of our

| March 31, 2022 | ||||||||||||

| Senior Notes | IQ Notes | Total | ||||||||||

| Principal | $ | $ | $ | |||||||||

| Unamortized discount/premium and issuance costs | ( | ) | ( | ) | ||||||||

| Long-term debt balance | $ | $ | $ | |||||||||

| December 31, 2021 | ||||||||||||

| Senior Notes | IQ Notes | Total | ||||||||||

| Principal | $ | $ | $ | |||||||||

| Unamortized discount/premium and issuance costs | ( | ) | ( | ) | ||||||||

| Long-term debt balance | $ | $ | $ | |||||||||

The following table summarizes the scheduled annual future payments, including interest, for our Senior Notes, IQ Notes, and finance and operating leases as of March 31, 2022 (in thousands). The amounts for the IQ Notes are stated in U.S. dollars (“USD”) based on the USD/Canadian dollar (“CAD”) exchange rate as of March 31, 2022.

| Twelve-month period ending March 31, | Senior Notes | IQ Notes | Finance Leases | Operating Leases | ||||||||||||

| 2023 | $ | $ | $ | $ | ||||||||||||

| 2024 | ||||||||||||||||

| 2025 | ||||||||||||||||

| 2026 | ||||||||||||||||

| 2027 | ||||||||||||||||

| Thereafter | ||||||||||||||||

| Total | $ | $ | $ | $ | ||||||||||||

Credit Facility

In July 2018, we entered into a $

We are also able to obtain letters of credit under the facility, and for any such letters we are required to pay a participation fee of between

We believe we were in compliance with all covenants under the credit agreement as of March 31, 2022.

Note 8. Derivative Instruments

General

Our current risk management policy provides that up to

| • |

our future foreign currency-related operating cost exposure for years into the future may be hedged; |

| • |

our planned lead and zinc metals price exposure for five years into the future, with certain other limitations, to be covered under derivatives programs that would establish a ceiling for prices to be realized on future metals sales; and |

| • |

our planned silver and gold metals price exposure for five years into the future, with certain other limitations, may be covered under derivatives programs that would establish a floor, but not a ceiling, for prices to be realized on future metals sales. We currently do not utilize this program. |

In addition, our risk management policy provides for (i) potential additional programs to manage other foreign currency exposures and (ii) that price exposure between the time of shipment and final settlement on silver, gold, lead and zinc contained in our concentrate shipments may be covered under derivatives programs that would establish prices to be realized on those sales.

These instruments expose us to (i) credit risk in the form of non-performance by counterparties for contracts in which the contract price exceeds the spot price of the hedged commodity or foreign currency and (ii) price risk to the extent that the spot price exceeds the contract price for quantities of our production and/or forecasted costs covered under contract positions.

Foreign Currency

Our wholly-owned subsidiaries owning the Casa Berardi and San Sebastian operations are USD-functional entities which routinely incur expenses denominated in CAD and Mexican pesos (“MXN”), respectively. Such expenses expose us to exchange rate fluctuations between the USD and CAD and MXN. We utilize a program to manage our exposure to fluctuations in the exchange rate between the USD and CAD and the impact on our future operating costs denominated in CAD. In November 2021, we initiated a similar program related to future development costs denominated in CAD, and have used a similar program, on a limited basis, related to interest payments on our IQ Notes (see Note 7). The programs utilize forward contracts to buy CAD. Each contract related to operating costs is designated as a cash flow hedge, while contracts related to development and interest costs have not been designated as hedges as of March 31, 2022. As of March 31, 2022, we have

As of March 31, 2022 and December 31, 2021, we recorded the following balances for the fair value of the contracts (in millions):

| March 31, |

December 31, |

|||||||

| Balance sheet line item: |

2022 |

2021 |

||||||

| Other current assets |

$ | $ | ||||||

| Other non-current assets |

||||||||

Net unrealized gains of approximately $

Metals Prices

We are currently using financially-settled forward contracts to manage the exposure to:

| • |

changes in prices of silver, gold, zinc and lead contained in our concentrate shipments between the time of shipment and final settlement; and |

| • |

changes in prices of zinc and lead (but not silver and gold) contained in our forecasted future concentrate shipments. |

The following tables summarize the quantities of metals committed under forward sales contracts at March 31, 2022 and December 31, 2021:

| March 31, 2022 |

Ounces/pounds under contract (in 000's) |

Average price per ounce/pound |

||||||||||||||||||||||||||||||

| Silver |

Gold |

Zinc |

Lead |

Silver |

Gold |

Zinc |

Lead |

|||||||||||||||||||||||||

| (ounces) |

(ounces) |

(pounds) |

(pounds) |

(ounces) |

(ounces) |

(pounds) |

(pounds) |

|||||||||||||||||||||||||

| Contracts on provisional sales |

||||||||||||||||||||||||||||||||

| 2022 settlements |

$ | $ | $ | $ | ||||||||||||||||||||||||||||

| Contracts on forecasted sales |

||||||||||||||||||||||||||||||||

| 2022 settlements |

N/A | N/A | $ | $ | ||||||||||||||||||||||||||||

| 2023 settlements |

N/A | N/A | $ | $ | ||||||||||||||||||||||||||||

| 2024 settlements |

N/A | N/A | $ | $ | ||||||||||||||||||||||||||||

| December 31, 2021 |

Ounces/pounds under contract (in 000's) |

Average price per ounce/pound |

||||||||||||||||||||||||||||||

| Silver |

Gold |

Zinc |

Lead |

Silver |

Gold |

Zinc |

Lead |

|||||||||||||||||||||||||

| (ounces) |

(ounces) |

(pounds) |

(pounds) |

(ounces) |

(ounces) |

(pounds) |

(pounds) |

|||||||||||||||||||||||||

| Contracts on provisional sales |

||||||||||||||||||||||||||||||||

| 2022 settlements |

$ | $ | $ | $ | ||||||||||||||||||||||||||||

| Contracts on forecasted sales |

||||||||||||||||||||||||||||||||

| 2022 settlements |

N/A | N/A | $ | $ | ||||||||||||||||||||||||||||

| 2023 settlements |

N/A | N/A | $ | $ | ||||||||||||||||||||||||||||

Effective November 1, 2021, we designated the contracts for lead and zinc contained in our forecasted future shipments as hedges for accounting purposes, with gains and losses deferred to accumulated other comprehensive loss until the hedged product ships. Prior to November 1, 2021, these contracts had not been designated as hedges for hedge accounting and were therefore marked-to-market through earnings each period. The forward contracts for silver and gold contained in our concentrate shipments have not been designated as hedges and are marked-to-market through earnings each period.

We recorded the following balances for the fair value of the forward contracts as of March 31, 2022 and forward and put option contracts as of December 31, 2021 (in millions):

| March 31, 2022 |

December 31, 2021 |

|||||||||||||||||||||||

| Balance sheet line item: |

Contracts in an asset position |

Contracts in a liability position |

Net asset (liability) |

Contracts in an asset position |

Contracts in a liability position |

Net asset (liability) |

||||||||||||||||||

| Other current assets |

$ | $ | ( |

) | $ | $ | $ | $ | ||||||||||||||||

| Current derivatives liability |

( |

) | ( |

) | ( |

) | ( |

) | ||||||||||||||||

| Other non-current liabilities |

( |

) | ( |

) | ( |

) | ( |

) | ||||||||||||||||

Net unrealized losses of approximately $

We recognized $

Credit-risk-related Contingent Features

Certain of our derivative contracts contain cross default provisions which provide that a default under our revolving credit agreement would cause a default under the derivative contract. As of March 31, 2022, we have not posted any separate collateral related to these contracts. The fair value of derivatives in a net liability position related to these agreements was $

Note 9. Fair Value Measurement

Fair value adjustments, net is comprised of the following:

| Three Months Ended March 31, | ||||||||

| 2022 | 2021 | |||||||

| (Loss) gain on derivative contracts | $ | ( | ) | $ | ||||

| Unrealized gain (loss) on investments in equity securities | ( | ) | ||||||

| Gain on disposition or exchange of investments | ||||||||

| Total fair value adjustments, net | $ | $ | ( | ) | ||||

Accounting guidance has established a hierarchy for inputs used to measure assets and liabilities at fair value on a recurring basis. The three levels included in the hierarchy are:

Level 1: quoted prices in active markets for identical assets or liabilities;

Level 2: significant other observable inputs; and

Level 3: significant unobservable inputs.

The table below sets forth our assets and liabilities that were accounted for at fair value on a recurring basis and the fair value calculation input hierarchy level that we have determined applies to each asset and liability category (in thousands).

| Description | Balance at March 31, 2022 | Balance at December 31, 2021 | Input Hierarchy Level | ||||||

| Assets: | |||||||||

| Cash and cash equivalents: | |||||||||

| Money market funds and other bank deposits | $ | $ | Level 1 | ||||||

| Current and non-current investments: | |||||||||

| Equity securities – mining industry | Level 1 | ||||||||

| Trade accounts receivable: | |||||||||

| Receivables from provisional concentrate sales | Level 2 | ||||||||

| Restricted cash balances: | |||||||||

| Certificates of deposit and other bank deposits | Level 1 | ||||||||

| Derivative contracts - other current assets and other non-current assets: | |||||||||

| Metal forward contracts | Level 2 | ||||||||

| Foreign exchange contracts | Level 2 | ||||||||

| Total assets | $ | $ | |||||||

| Liabilities: | |||||||||

| Derivative contracts - current and non-current derivatives liabilities: | |||||||||

| Metal forward contracts | $ | $ | Level 2 | ||||||

| Foreign exchange contracts | Level 2 | ||||||||

| Total Liabilities | $ | $ | |||||||

Cash and cash equivalents consist primarily of money market funds and are valued at cost, which approximates fair value, and a small portion consists of municipal bonds having maturities of less than 90 days, which are recorded at fair value.

Current and non-current restricted cash balances consist primarily of certificates of deposit, U.S. Treasury securities, and other deposits and are valued at cost, which approximates fair value.

Non-current investments consist of marketable equity securities of mining companies which are valued using quoted market prices for each security. During the first quarter of 2022, we acquired equity securities of various mining companies for a total cost of $

Trade accounts receivable from provisional concentrate sales are subject to final pricing and valued using quoted prices based on forward curves for the particular metal.

We use financially-settled forward contracts to manage exposure to changes in the exchange rate between USD and CAD, and the impact on CAD-denominated operating and capital costs incurred at Casa Berardi (see Note 8 for more information). The fair value of each contract represents the present value of the difference between the forward exchange rate for the contract settlement period as of the measurement date and the contract settlement exchange rate.

We use financially-settled forward contracts to manage the exposure to changes in prices of silver, gold, zinc and lead contained in our concentrate shipments that have not reached final settlement (see Note 8 for more information). The fair value of each forward contract represents the present value of the difference between the forward metal price for the contract settlement period as of the measurement date and the contract settlement metal price.

At March 31, 2022, our Senior Notes and IQ Notes were recorded at their carrying value of $

Note 10. Commitments, Contingencies and Obligations

General

We follow GAAP guidance in determining our accruals and disclosures with respect to loss contingencies, and evaluate such accruals and contingencies for each reporting period. Accordingly, estimated losses from loss contingencies are accrued by a charge to income when information available prior to issuance of the financial statements indicates that it is probable that a liability could be incurred and the amount of the loss can be reasonably estimated. Legal expenses associated with the contingency are expensed as incurred. If a loss contingency is not probable or reasonably estimable, disclosure of the loss contingency is made in the financial statements when it is at least reasonably possible that a material loss could be incurred.

Johnny M Mine Area near San Mateo, McKinley County and San Mateo Creek Basin, New Mexico

In August 2012, Hecla Limited and the EPA entered into a Settlement Agreement and Administrative Order on Consent for Removal Action (“Consent Order”) regarding the Johnny M Mine Area near San Mateo, McKinley County, New Mexico. Mining at the Johnny M Mine was conducted for a limited period of time by a predecessor of Hecla Limited, and the EPA had previously asserted that Hecla Limited may be responsible under the Comprehensive Environmental Response, Compensation and Liability Act (“CERCLA”) for environmental remediation and past costs incurred by the EPA at the site. Under the Consent Order, Hecla Limited agreed to pay (i) $

The Johnny M Mine is in an area known as the San Mateo Creek Basin (“SMCB”), which is an approximately 321 square mile area in New Mexico that contains numerous legacy uranium mines and mills. In addition to Johnny M, Hecla Limited’s predecessor was involved at other mining sites within the SMCB. The EPA appears to have deferred consideration of listing the SMCB site on CERCLA’s National Priorities List (“Superfund”) by removing the site from its emphasis list, and is working with various potentially responsible parties (“PRPs”) at the site in order to study and potentially address perceived groundwater issues within the SMCB. The EE/CA discussed above relates primarily to contaminated rock and soil at the Johnny M site, not groundwater and not elsewhere within the SMCB site. It is possible that Hecla Limited’s liability at the Johnny M Site, and for any other mine site within the SMCB at which Hecla Limited’s predecessor may have operated, will be greater than our current accrual of $9.0 million due to the increased scope of required remediation.

In July 2018, the EPA informed Hecla Limited that it and several other PRPs may be liable for cleanup of the SMCB site or for costs incurred by the EPA in cleaning up the site. The EPA stated it has incurred approximately $

Carpenter Snow Creek and Barker-Hughesville Sites in Montana

In July 2010, the EPA made a formal request to Hecla for information regarding the Carpenter Snow Creek Superfund site located in Cascade County, Montana. The Carpenter Snow Creek site is located in a historic mining district, and in the early 1980s Hecla Limited leased 6 mining claims and performed limited exploration activities at the site. Hecla Limited terminated the mining lease in 1988.

In June 2011, the EPA informed Hecla Limited that it believes Hecla Limited, and several other PRPs, may be liable for cleanup of the site or for costs incurred by the EPA in cleaning up the site. The EPA stated in the letter that it has incurred approximately $

In February 2017, the EPA made a formal request to Hecla for information regarding the Barker-Hughesville Mining District Superfund site located in Judith Basin and Cascade Counties, Montana. Hecla Limited submitted a response in April 2017. The Barker-Hughesville site is located in a historic mining district, and between approximately June and December 1983, Hecla Limited was party to an agreement with another mining company under which limited exploration activities occurred at or near the site.

In August 2018, the EPA informed Hecla Limited that it and several other PRPs may be liable for cleanup of the site or for costs incurred by the EPA in cleaning up the site. The EPA did not include an amount of its alleged response costs to date. Hecla Limited cannot with reasonable certainty estimate the amount or range of liability, if any, relating to this matter because of, among other reasons, the lack of information concerning past or anticipated future costs at the site and the relative contributions of contamination by various other PRPs.

Litigation Related to Klondex Acquisition

On May 24, 2019, a purported Hecla stockholder filed a putative class action lawsuit in the U.S. District Court for the Southern District of New York against Hecla and certain of our executive officers, one of whom is also a director. The complaint, purportedly brought on behalf of all purchasers of Hecla common stock from March 19, 2018 through and including May 8, 2019, asserts claims under Sections 10(b) and 20(a) of the Securities Exchange Act of 1934 and Rule 10b-5 promulgated thereunder and seeks, among other things, damages and costs and expenses. Specifically, the complaint alleges that Hecla, under the authority and control of the individual defendants, made certain material false and misleading statements and omitted certain material information regarding Hecla’s Nevada Operations. The complaint alleges that these misstatements and omissions artificially inflated the market price of Hecla common stock during the class period, thus purportedly harming investors. Filings with the court regarding our motion to dismiss the lawsuit were completed in the first quarter of 2021. We cannot predict the outcome of this lawsuit or estimate damages if plaintiffs were to prevail. We believe that these claims are without merit and intend to defend them vigorously.

Related to this class action lawsuit, Hecla has been named as a nominal defendant in a shareholder derivative lawsuit which also names as defendants certain current and past (i) members of Hecla’s board of directors and (ii) officers of Hecla. The case was filed on May 4, 2022 in the Delaware Chancery Court. In general terms, the suit alleges breaches of fiduciary duties by the individual defendants, waste of corporate assets and unjust enrichment, and seeks damages, purportedly on behalf of Hecla.

Debt

See Note 7 for information on the commitments related to our debt arrangements as of March 31, 2022.

Other Commitments

Our contractual obligations as of March 31, 2022 included open purchase orders and commitments of approximately $

Other Contingencies

We also have certain other contingencies resulting from litigation, claims, EPA investigations, and other commitments and are subject to a variety of environmental and safety laws and regulations incident to the ordinary course of business. We currently have no basis to conclude that any or all of such contingencies will materially affect our financial position, results of operations or cash flows. However, in the future, there may be changes to these contingencies, or additional contingencies may occur, any of which might result in an accrual or a change in current accruals recorded by us, and there can be no assurance that their ultimate disposition will not have a material adverse effect on our financial position, results of operations or cash flows.

Note 11. Developments in Accounting Pronouncements

Accounting Standards Updates Adopted

In August 2020, the Financial Accounting Standards Board ("FASB") issued ASU No. 2020-06 Debt - Debt with Conversion and Other Options (Subtopic 470-20) and Derivatives and Hedging—Contracts in Entity’s Own Equity (Subtopic 815-40): Accounting for Convertible Instruments and Contracts in an Entity’s Own Equity. The update is to address issues identified as a result of the complexity associated with applying generally accepted accounting principles to certain financial instruments with characteristics of liabilities and equity. The update is effective for fiscal years beginning after December 15, 2021, including interim periods within those fiscal years and with early adoption permitted. We adopted the update as of January 1, 2022, which did not have a material impact on our consolidated financial statements or disclosures.

In October 2021, the FASB issued ASU 2021-08, Business Combinations (Topic 805): Accounting for Contract Assets and Contract Liabilities from Contracts with Customers, which requires entities to recognize and measure contract assets and contract liabilities acquired in a business combination in accordance with ASC 2014-09, Revenue from Contracts with Customers (Topic 606). The update will generally result in an entity recognizing contract assets and contract liabilities at amounts consistent with those recorded by the acquiree immediately before the acquisition date rather than at fair value. The update is effective on a prospective basis for fiscal years beginning after December 15, 2022, with early adoption permitted. We adopted the new standard effective January 1, 2022, which did not have a material impact on our consolidated financial statements or disclosures.

Accounting Standards Updates to Become Effective in Future Periods

In 2017, the United Kingdom’s Financial Conduct Authority ("FCA") announced that after 2021 it would no longer compel banks to submit the rates required to calculate the London Interbank Offered Rate ("LIBOR"), which have been widely used as reference rates for various securities and financial contracts, including loans, debt and derivatives. This announcement indicated that the continuation of LIBOR on the current basis would not be guaranteed after 2021. Subsequently in March 2021, the FCA announced some USD LIBOR tenors (overnight, 1 month, 3 month, 6 month and 12 month) will continue to be published until June 30, 2023. Regulators in the U.S. and other jurisdictions have been working to replace these rates with alternative reference interest rates that are supported by transactions in liquid and observable markets, such as the Secured Overnight Financing Rate ("SOFR"). Currently, our credit facility and certain of our derivative instruments reference LIBOR-based rates. Our credit facility contains provisions specifying alternative interest rate calculations to be employed when LIBOR ceases to be available as a benchmark and we have adhered to the ISDA 2020 IBOR Fallbacks Protocol, which will govern our derivatives upon the final cessation of USD LIBOR. ASU 2020-04, Reference Rate Reform (Topic 848): Facilitation of the Effects of Reference Rate Reform on Financial Reporting, as amended, helps limit the accounting impact from contract modifications, including hedging relationships, due to the transition from LIBOR to alternative reference rates that are completed by December 31, 2022. We do not expect a significant impact to our financial results, financial position or cash flows from the transition from LIBOR to alternative reference interest rates, but we will continue to monitor the impact of this transition until it is completed.

Note 12. Subsequent Events

During April 2022, we invested approximately $

Certain statements contained in this Form 10-Q, including in Management’s Discussion and Analysis of Financial Condition and Results of Operations and Quantitative and Qualitative Disclosures About Market Risk, are intended to be covered by the safe harbor provided for under Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. Our forward-looking statements include our current expectations and projections about future results, performance, results of litigation, prospects and opportunities, including reserves and other mineralization. We have tried to identify these forward-looking statements by using words such as “may,” “will,” “expect,” “anticipate,” “believe,” “intend,” “feel,” “plan,” “estimate,” “project,” “forecast” and similar expressions. These forward-looking statements are based on information currently available to us and are expressed in good faith and believed to have a reasonable basis. However, our forward-looking statements are subject to a number of risks, uncertainties and other factors that could cause our actual results, performance, prospects or opportunities to differ materially from those expressed in, or implied by, these forward-looking statements.

These risks, uncertainties and other factors include, but are not limited to, those set forth under Part I, Item 1A – Risk Factors in our annual report filed on Form 10-K for the year ended December 31, 2021 (“2021 Form 10-K”). Given these risks and uncertainties, readers are cautioned not to place undue reliance on our forward-looking statements. All subsequent written and oral forward-looking statements attributable to Hecla Mining Company or to persons acting on our behalf are expressly qualified in their entirety by these cautionary statements. Except as required by federal securities laws, we do not intend to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise.

Item 2. Management's Discussion and Analysis of Financial Condition and Results of Operations

In this Management’s Discussion and Analysis of Financial Condition and Results of Operations (“MD&A”), “Hecla,” “the Company,” “we,” “us” and “our” refer to Hecla Mining Company and its consolidated subsidiaries, except where the context requires otherwise. You should read this discussion in conjunction with our consolidated financial statements, the related MD&A and the discussion of our Business and Properties in our 2021 Form 10-K filed with the United States Securities and Exchange Commission (the “SEC”). The results of operations reported and summarized below are not necessarily indicative of future operating results (refer to “Forward-Looking Statements” above for further discussion). References to “Notes” are Notes included in our Notes to Condensed Consolidated Financial Statements (Unaudited). Throughout MD&A, all references to losses or income per share are on a diluted basis.

Overview

Established in 1891, we believe we are the oldest operating precious metals mining company in the United States. We are the largest silver producer in the United States, producing over 40% of the United States silver production at our Greens Creek and Lucky Friday operations. We produce gold at our Casa Berardi operation in Quebec, Canada, and Greens Creek, and at our Nevada Operations segment prior to suspension of operations during 2021. Based upon our operational footprint, we believe we have low political and economic risk compared to other mines located in other parts of the world. Our exploration interests are located in the United States, Canada and Mexico. Our operating and strategic framework is based on expanding our production and locating and developing new resource potential in a safe and responsible manner.

First Quarter 2022 Highlights

Operational:

| • |

Produced 3.3 million ounces of silver and 41,642 ounces of gold. See Consolidated Results of Operations below for information on total cost of sales and cash costs and AISC, after by-product credits, per silver and gold ounce for the three-month periods ended March 31, 2022 and 2021. |

| • |

Continued our trend of strong safety performance, as our All Injury Frequency Rate (“AIFR”) for the first quarter of 2022 was 1.48, 30% below the U.S. national average for MSHA's “metal and nonmetal” category and within 3% of our AIFR of 1.45 for the full year of 2021. |

| • |

Continued mitigation of the impacts of COVID-19 through refinement of our operational plans and procedures to protect our workforce, operations and communities while maintaining liquidity. |

Financial:

| • |

Reported sales of products of $186.5 million. |

| • |

Generated $37.9 million in net cash provided by operating activities after bi-annual interest payments totaling $18.5 million on the Senior Notes and IQ Notes. See the Financial Liquidity and Capital Resources section below for further discussion. |

| • |

Made capital expenditures (excluding lease additions and other non-cash items) of approximately $21.5 million, including $3.1 million at Greens Creek, $9.7 million at Lucky Friday, $7.8 million at Casa Berardi and $0.9 million at the Nevada Operations. |

| • |

Generated $16.4 million in free cash flow. A reconciliation of the non-GAAP measure free cash flow to net cash provided by operating activities, the nearest GAAP measure, is included in the Reconciliation of Cash Flows From Operating Activities (GAAP) to Free Cash Flow (Non-GAAP) section below. |

| • |

Returned $3.5 million, or 21% of free cash flows, to our shareholders through payment of dividends. |

| • |

Spent $12.8 million on exploration and pre-development activities. |

| • |

Achieved the above while increasing our cash balance to $212.0 million, which was $2.0 million higher than at December 31, 2021, with no borrowings on our revolving credit facility, as of March 31, 2022. |

Our current business strategy is to focus our financial and human resources in the following areas:

| • |

rapidly responding to the threats from the COVID-19 pandemic to protect our workforce, operations and communities while maintaining liquidity; |

| • |

operating our properties safely, in an environmentally responsible and cost-effective manner; |

| • |

maintaining and investing in exploration and pre-development projects in the vicinities of eleven mining districts and projects we believe to be under-explored and under-invested: Greens Creek on Alaska's Admiralty Island located near Juneau; North Idaho's Silver Valley in the historic Coeur d'Alene Mining District; the silver-producing district near Durango, Mexico; in the vicinity of our Casa Berardi mine and the Heva-Hosco project in the Abitibi region of northwestern Quebec, Canada; our projects located in two districts in Nevada; our projects in northwestern Montana; the Creede district of southwestern Colorado; the Kinskuch project in British Columbia, Canada; and the Republic mining district in Washington state; |

| • |

improving operations at each of our mines, which includes incurring costs for new technologies and equipment; |

| • |

expanding our proven and probable reserves, mineral resources and production capacity at our properties; |

| • |

conducting our business with financial stewardship to preserve our financial position in varying metals price and operational environments; |

| • |

advancing permitting of one or both of our Montana projects; and |

| • |

continuing to seek opportunities to acquire and invest in mining and exploration properties and companies. |

We strive to achieve excellent mine safety and health performance. We seek to implement this goal by: training employees in safe work practices; establishing, following and improving safety standards; investigating accidents, incidents and losses to avoid recurrence; involving employees in the establishment of safety standards; and participating in the National Mining Association’s CORESafety program. We seek to implement reasonable best practices with respect to mine safety and emergency preparedness. We respond to issues outlined in investigations and inspections by MSHA, the Commission of Labor Standards, Pay Equity and Occupational Health and Safety in Quebec, and the Mexico Ministry of Economy and Mining and continue to evaluate our safety practices. There can be no assurance that our practices will mitigate or eliminate all safety risks. Achieving and maintaining compliance with regulations will be challenging and may increase our operating costs. See Item 1A. Risk Factors - We face substantial governmental regulation, including the Mine Safety and Health Act, various environmental laws and regulations and the 1872 Mining Law in our 2021 Form 10-K.

Since its outbreak in 2020, the COVID-19 pandemic continues to impact our operational practices and we continue to incur incremental costs and modify our operational plans to keep our workforce safe. In 2020, the pandemic adversely impacted our expected production of gold at Casa Berardi and exploration drilling at Greens Creek. We incurred $0.4 million and $1.6 million in COVID-19 mitigation costs during the three months ended March 31, 2022 and 2021, respectively. To mitigate the impact of COVID-19, we have taken precautionary measures, including implementing operational plans and practices and increasing our cash reserves. As long as they are required, the operational practices implemented could continue to have an adverse impact on our operating results due to additional costs or deferred production and revenues. There is uncertainty related to the potential additional impacts COVID-19 and any subsequent variants could have on our operations and financial results for the rest of 2022. In our 2021 Form 10-K, see Item IA. Risk Factors - Natural disasters, public health crises (including COVID-19), political crises, and other catastrophic events or other events outside of our control may materially and adversely affect our business or financial results and COVID-19 virus pandemic may heighten other risks for information on how restrictions related to COVID-19 have recently affected some of our operations.

A number of key factors may impact the execution of our strategy, including regulatory issues and metals prices. Metals prices can be very volatile and are influenced by a number of factors beyond our control (except on a limited basis through the use of derivative contracts). See Item 7. Critical Accounting Estimates in our 2021 Form 10-K and above in Note 8 of Notes to Condensed Consolidated Financial Statements (Unaudited). The average realized prices of gold, lead and zinc were higher, with the average realized price for silver lower, in the first three months of 2022 than in the comparable period last year, as illustrated by the table in Results of Operations below. While we believe longer-term global economic and industrial trends could result in continued demand for the metals we produce, prices have been volatile and there can be no assurance that current prices will continue.

Volatility in global financial markets and other factors can pose a significant challenge to our ability to access credit and equity markets, should we need to do so, and to predict sales prices for our products. To help mitigate this challenge, we utilize forward contracts to manage exposure to declines in the prices of (i) silver, gold, zinc and lead contained in our concentrates that have been shipped but have not yet settled, and (ii) zinc and lead that we forecast for future concentrate shipments. In addition, we have in place a $250 million revolving credit agreement, of which $17.3 million was used as of March 31, 2022 for letters of credit, leaving approximately $232.7 million available for borrowing.

Another challenge for us is the risk associated with environmental litigation and ongoing reclamation activities. As described Item 1A. Risk Factors in our 2021 Form 10-K and above in Note 10 of Notes to Condensed Consolidated Financial Statements (Unaudited), it is possible that our estimate of these liabilities (and our ability to estimate liabilities in general) may change in the future, affecting our strategic plans. We are involved in various environmental legal matters and the estimate of our environmental liabilities and liquidity needs, as well as our strategic plans, may be significantly impacted as a result of these matters or new matters that may arise. We strive to ensure that our activities are conducted in compliance with applicable laws and regulations and attempt to resolve environmental litigation on terms as favorable to us as possible.

Consolidated Results of Operations

Sales of products by metal for the three-month periods ended March 31, 2022 and 2021, and the approximate variances attributed to differences in metals prices, sales volumes and smelter terms, were as follows:

| (in thousands) |

Silver |

Gold |

Base metals |

Less: smelter and refining charges |

Total sales of products |

|||||||||||||||

| Three months ended March 31, 2021 |

$ | 77,760 | $ | 101,408 | $ | 45,084 | $ | (13,400 | ) | $ | 210,852 | |||||||||

| Variances - 2022 versus 2021: |

||||||||||||||||||||

| Price |

(2,613 | ) | 4,298 | 12,316 | (76 | ) | 13,925 | |||||||||||||

| Volume |

(8,726 | ) | (28,453 | ) | (2,198 | ) | 1,369 | (38,008 | ) | |||||||||||

| Smelter terms |

(89 | ) | (85 | ) | — | (96 | ) | (270 | ) | |||||||||||

| Three months ended March 31, 2022 |

$ | 66,332 | $ | 77,168 | $ | 55,202 | $ | (12,203 | ) | $ | 186,499 | |||||||||

Average market and realized metals prices for the three-month periods ended March 31, 2022 and 2021 were as follows:

| Three months ended March 31, |

|||||||||

| 2022 |

2021 |

||||||||

| Silver – |

London PM Fix ($/ounce) |

$ | 23.95 | $ | 26.29 | ||||

| Realized price per ounce |

$ | 24.68 | $ | 25.66 | |||||

| Gold – |

London PM Fix ($/ounce) |

$ | 1,874 | $ | 1,798 | ||||

| Realized price per ounce |

$ | 1,880 | $ | 1,770 | |||||

| Lead – |

LME Final Cash Buyer ($/pound) |

$ | 1.06 | $ | 0.92 | ||||

| Realized price per pound |

$ | 1.08 | $ | 0.92 | |||||

| Zinc – |

LME Final Cash Buyer ($/pound) |

$ | 1.70 | $ | 1.25 | ||||

| Realized price per pound |

$ | 1.79 | $ | 1.32 | |||||

Average realized prices typically differ from average market prices primarily because concentrate sales are generally recorded as revenues at the time of shipment at forward prices for the estimated month of settlement, which differ from average market prices. Due to the time elapsed between shipment of concentrates and final settlement with the customers, we must estimate the prices at which sales of our metals will be settled. Previously recorded sales are adjusted to estimated settlement metals prices each period through final settlement. For the first quarters of 2022 and 2021, we recorded net positive price adjustments to provisional settlements of $1.0 million and $0.6 million, respectively. The price adjustments related to silver, gold, lead and zinc contained in our concentrate shipments were largely offset by gains and losses on forward contracts for those metals. See Note 8 of Notes to Condensed Consolidated Financial Statements (Unaudited) for more information. The gains and losses on these contracts are included in revenues and impact the realized prices for silver, gold, lead and zinc. Realized prices are calculated by dividing gross revenues for each metal (which include the price adjustments and gains and losses on the forward contracts discussed above) by the payable quantities of each metal included in concentrate and doré shipped during the period.

Total metals production and sales volumes for each period are shown in the following table:

| Three Months Ended March 31, |

|||||||||

| 2022 |

2021 |

||||||||

| Silver - |

Ounces produced |

3,324,708 | 3,459,446 | ||||||

| Payable ounces sold |

2,687,261 | 3,030,026 | |||||||

| Gold - |

Ounces produced |

41,642 | 52,004 | ||||||

| Payable ounces sold |

41,053 | 57,286 | |||||||

| Lead - |

Tons produced |

10,863 | 10,704 | ||||||

| Payable tons sold |

9,054 | 8,668 | |||||||

| Zinc - |

Tons produced |

14,946 | 16,107 | ||||||

| Payable tons sold |

9,947 | 11,027 | |||||||

The difference between what we report as “ounces/tons produced” and “payable ounces/tons sold” is attributable to the difference between the quantities of metals contained in our products versus the portion of those metals actually paid for by our customers pursuant to our sales contracts. Differences can also arise from inventory changes incidental to shipping schedules, or variances in ore grades which impact the amount of metals contained in concentrates produced and sold.

Sales, total cost of sales, gross profit, Cash Cost, After By-product Credits, per Ounce (“Cash Cost”) (non-GAAP) and All-In Sustaining Cost, After By-product Credits, per Ounce (“AISC”) (non-GAAP) at our operations for the three-month periods ended March 31, 2022 and 2021 were as follows (in thousands, except for Cash Cost and AISC):

| Silver |

Gold |

|||||||||||||||||||||||||||

| Greens Creek |

Lucky Friday |

Other (2) |

Total Silver (3) |

Casa Berardi |

Nevada Operations |

Total Gold |

||||||||||||||||||||||

| Three Months Ended March 31, 2022: |

||||||||||||||||||||||||||||

| Sales |

$ | 86,090 | $ | 38,040 | $ | — | $ | 124,130 | $ | 62,101 | $ | 268 | $ | 62,369 | ||||||||||||||

| Total cost of sales |

(49,638 | ) | (29,264 | ) | — | (78,902 | ) | (62,168 | ) | — | (62,168 | ) | ||||||||||||||||

| Gross profit (loss) |

$ | 36,452 | $ | 8,776 | $ | — | $ | 45,228 | $ | (67 | ) | $ | 268 | $ | 201 | |||||||||||||

| Cash Cost After By-product Credits, per Silver or Gold Ounce (1) |

$ | (0.90 | ) | $ | 6.57 | $ | — | $ | 1.09 | $ | 1,516 | $ | — | $ | 1,516 | |||||||||||||

| AISC, After By-product Credits, per Silver or Gold ounce (1) |

$ | 1.90 | $ | 13.15 | $ | — | $ | 7.64 | $ | 1,810 | $ | — | $ | 1,810 | ||||||||||||||

| Three Months Ended March 31, 2021: |

||||||||||||||||||||||||||||

| Sales |

$ | 98,409 | $ | 29,122 | $ | 173 | $ | 127,704 | $ | 72,911 | $ | 10,237 | $ | 83,148 | ||||||||||||||

| Total cost of sales |

(53,181 | ) | (22,794 | ) | (94 | ) | (76,069 | ) | (59,927 | ) | (7,455 | ) | (67,382 | ) | ||||||||||||||

| Gross profit |

$ | 45,228 | $ | 6,328 | $ | 79 | $ | 51,635 | $ | 12,984 | $ | 2,782 | $ | 15,766 | ||||||||||||||

| Cash Cost After By-product Credits, per Silver or Gold Ounce (1) |

$ | (0.67 | ) | $ | 7.62 | $ | — | $ | 1.40 | $ | 1,027 | $ | 1,416 | $ | 1,052 | |||||||||||||

| AISC, After By-product Credits, per Silver or Gold ounce (1) |

$ | 1.59 | $ | 14.24 | $ | — | $ | 7.21 | $ | 1,272 | $ | 1,461 | $ | 1,284 | ||||||||||||||

| (1) |

A reconciliation of these non-GAAP measures to total cost of sales, the most comparable GAAP measure, can be found below in Reconciliation of Total Cost of Sales (GAAP) to Cash Cost, Before By-product Credits and Cash Cost, After By-product Credits (non-GAAP) and All-In Sustaining Cost, Before By-product Credits and All-In Sustaining Cost, After By-product Credits (non-GAAP). |

| (2) |

Includes results for San Sebastian, which was an operating segment prior to 2021. |

| (3) |

The calculation of AISC, After By-product Credits, per Ounce for our consolidated silver properties includes corporate costs for general and administrative expense and sustaining exploration and capital costs. |

While revenue from zinc, lead and gold by-products is significant, we believe that identification of silver as the primary product of Greens Creek and Lucky Friday is appropriate because:

| • |

silver has historically accounted for a higher proportion of revenue than any other metal and is expected to do so in the future; |

| • |

we have historically presented each of these operations as a producer primarily of silver, based on the original analysis that justified putting the project into production, and believe that consistency in disclosure is important to our investors regardless of the relationships of metals prices and production from year to year; |

| • |

metallurgical treatment maximizes silver recovery; |

| • |

the Greens Creek and Lucky Friday deposits are massive sulfide deposits containing an unusually high proportion of silver; and |

| • |

in most of their working areas, Greens Creek and Lucky Friday utilize selective mining methods in which silver is the metal targeted for highest recovery. |

Likewise, we believe the identification of gold, lead and zinc as by-product credits at Greens Creek and Lucky Friday is appropriate because of their lower economic value compared to silver and due to the fact that silver is the primary product we intend to produce. In addition, we have not consistently received sufficient revenue from any single by-product metal to warrant classification of such as a co-product.

We periodically review our revenues to ensure that reporting of primary products and by-products is appropriate. Because for Greens Creek and Lucky Friday we consider zinc, lead and gold to be by-products of our silver production, the values of these metals offset operating costs within our calculations of Cash Cost, After By-product Credits, per Silver Ounce and AISC, After By-product Credits, per Silver Ounce.

We believe the identification of silver as a by-product credit is appropriate at Casa Berardi and Nevada Operations because of its lower economic value compared to gold and due to the fact that gold is the primary product we intend to produce there. In addition, we do not receive sufficient revenue from silver at Casa Berardi and Nevada Operations to warrant classification of such as a co-product. Because we consider silver to be a by-product of our gold production at Casa Berardi and Nevada Operations, the value of silver offsets operating costs within our calculations of Cash Cost, After By-product Credits, per Gold Ounce and AISC, After By-product Credits, per Gold Ounce.

For the first quarter of 2022, we recorded income applicable to common stockholders of $4.0 million ($0.01 per basic common share), compared to income of $21.3 million ($0.04 per basic common share) during the first quarter of 2021. The following factors contributed to the results for the first three months of 2022 compared to the first quarter of 2021:

| • |

Variances in gross profit (loss) at our operations as illustrated in the table above. See the Greens Creek, Lucky Friday, Casa Berardi and Nevada Operations sections below. |

| • |

Exploration and pre-development expense increased by $6.1 million in the first quarter of 2022 compared to the first quarter of 2021. In the first quarter of 2022, exploration was primarily at San Sebastian, Casa Berardi, Nevada Operations and Greens Creek. Pre-development expense for the first quarter of 2022 totaled $3.1 million compared to $0.7 million in the first quarter of 2021, with the increase for development of a decline to the Hatter Graben area at the Hollister mine in Nevada. |

| • |

Care and maintenance costs increased by $1.9 million in the first quarter of 2022 compared to the first quarter of 2021 due to suspension of production at Nevada Operations. See the Nevada Operations section below. |

The impact of these factors was partially offset by the following:

| • |

Fair value adjustments, net resulted in a gain of $6.0 million in the first quarter of 2022 compared to a loss of $1.9 million the first quarter of 2021 (see Note 9 of Notes to Condensed Consolidated Financial Statements (Unaudited) for more information). |

| • |

Provision for closed operations and environmental matters decreased by $2.8 million in the first quarter of 2022 compared to the first quarter of 2021 primarily due to a $2.9 million increase in the accrual for estimated costs at the Johnny M site in New Mexico in the first quarter of 2021 (see Note 10 of Notes to Condensed Consolidated Financial Statements (Unaudited) for more information). |

| • |

Lower other operating expense by $1.2 million in the first quarter of 2022 compared to the first quarter of 2021 primarily due to project costs incurred to identify and implement potential operational improvements at Casa Berardi in the first quarter 2021, partially offset by similar project costs incurred at Greens Creek in the first quarter of 2022. |

| • |

An income and mining tax provision of $5.6 million in the first quarter of 2022 compared to a provision of $4.7 million in the first quarter of 2021 (see Note 3 of Notes to Condensed Consolidated Financial Statements (Unaudited) for more information). |

Greens Creek

| Dollars are in thousands (except per ounce and per ton amounts) |

Three months ended March 31, |

|||||||

| 2022 |

2021 |

|||||||

| Sales |

$ | 86,090 | $ | 98,409 | ||||

| Cost of sales and other direct production costs |

(38,218 | ) | (38,360 | ) | ||||

| Depreciation, depletion and amortization |

(11,420 | ) | (14,821 | ) | ||||

| Total cost of sales |

(49,638 | ) | (53,181 | ) | ||||

| Gross profit |

$ | 36,452 | $ | 45,228 | ||||

| Tons of ore milled |

211,687 | 194,080 | ||||||

| Production: |

||||||||

| Silver (ounces) |

2,429,782 | 2,584,870 | ||||||

| Gold (ounces) |

11,402 | 13,266 | ||||||

| Zinc (tons) |

12,494 | 13,354 | ||||||

| Lead (tons) |

4,883 | 4,924 | ||||||

| Payable metal quantities sold: |

||||||||

| Silver (ounces) |

1,772,391 | 2,247,274 | ||||||

| Gold (ounces) |

7,922 | 10,547 | ||||||

| Zinc (tons) |

8,092 | 9,097 | ||||||

| Lead (tons) |

3,063 | 3,645 | ||||||

| Ore grades: |

||||||||

| Silver ounces per ton |

13.84 | 16.01 | ||||||

| Gold ounces per ton |

0.07 | 0.09 | ||||||

| Zinc percent |

6.56 | 7.62 | ||||||

| Lead percent |

2.76 | 3.06 | ||||||

| Total production cost per ton |

$ | 192.16 | $ | 182.61 | ||||

| Cash Cost, After By-product Credits, per Silver Ounce (1) |

$ | (0.90 | ) | $ | (0.67 | ) | ||

| AISC, After By-product Credits, per Silver Ounce (1) |

$ | 1.90 | $ | 1.59 | ||||

| Capital additions |

$ | 3,092 | $ | 1,772 | ||||

| (1) |

A reconciliation of these non-GAAP measures to total cost of sales, the most comparable GAAP measure, can be found below in Reconciliation of Total Cost of Sales (GAAP) to Cash Cost, Before By-product Credits and Cash Cost, After By-product Credits (non-GAAP) and All-In Sustaining Cost, Before By-product Credits and All-In Sustaining Cost, After By-product Credits (non-GAAP). |

The $8.8 million decrease in gross profit during the first quarter of 2022 compared to the same 2021 period was the result of lower sales volumes, as a result of lower ore grades and the timing of concentrate shipments, and lower average silver prices, partially offset by higher average gold, zinc and lead prices.

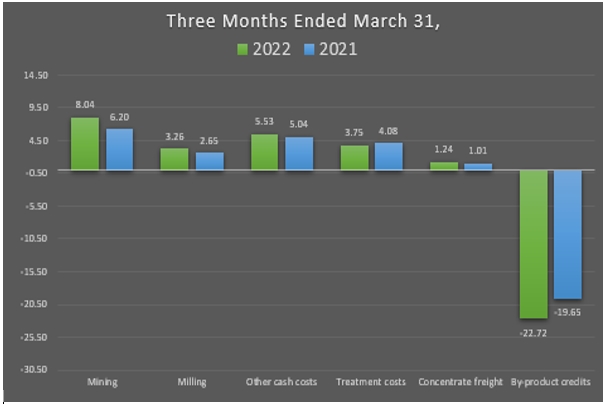

The chart below illustrates the factors contributing to the variances in Cash Cost, After By-product Credits, per Silver Ounce for the first quarter of 2022 compared to the first quarter of 2021:

The following table summarizes the components of Cash Cost, After By-product Credits, per Silver Ounce:

| Three Months Ended March 31, |

||||||||

| 2022 |

2021 |

|||||||

| Cash Cost, Before By-product Credits, per Silver Ounce |

$ | 21.82 | $ | 18.98 | ||||

| By-product credits |

(22.72 | ) | (19.65 | ) | ||||

| Cash Cost, After By-product Credits, per Silver Ounce |

$ | (0.90 | ) | $ | (0.67 | ) | ||

The following table summarizes the components of AISC, After By-product Credits, per Silver Ounce:

| Three Months Ended March 31, |

||||||||

| 2022 |

2021 |

|||||||

| AISC, Before By-product Credits, per Silver Ounce |

$ | 24.62 | $ | 21.24 | ||||

| By-product credits |

(22.72 | ) | (19.65 | ) | ||||

| AISC, After By-product Credits, per Silver Ounce |

$ | 1.90 | $ | 1.59 | ||||

The decrease in Cash Costs, After By-Product Credits, per Silver Ounce for the first quarter of 2022 compared to 2021 was primarily due to the higher by-product credits, partially offset by higher mining and milling costs. The net impact of these factors was outweighed by higher sustaining capital spending, resulting in the increase in AISC, After By-Product Credits, per Silver Ounce for the first quarter of 2022 compared to 2021.

Lucky Friday

| Dollars are in thousands (except per ounce and per ton amounts) |

Three Months Ended March 31, |

|||||||

| 2022 |

2021 |

|||||||

| Sales |

$ | 38,040 | $ | 29,122 | ||||

| Cost of sales and other direct production costs |

(21,232 | ) | (16,458 | ) | ||||

| Depreciation, depletion and amortization |

(8,032 | ) | (6,336 | ) | ||||

| Total cost of sales |

(29,264 | ) | (22,794 | ) | ||||

| Gross profit (loss) |

$ | 8,776 | $ | 6,328 | ||||

| Tons of ore milled |

77,725 | 81,071 | ||||||

| Production: |

||||||||

| Silver (ounces) |

887,858 | 863,901 | ||||||

| Lead (tons) |

5,980 | 5,780 | ||||||

| Zinc (tons) |

2,452 | 2,753 | ||||||

| Payable metal quantities sold: |

||||||||

| Silver (ounces) |

899,454 | 763,823 | ||||||

| Lead (tons) |

5,991 | 5,023 | ||||||

| Zinc (tons) |

1,855 | 1,930 | ||||||

| Ore grades: |

||||||||

| Silver ounces per ton |

12.04 | 11.18 | ||||||

| Lead percent |

8.16 | 7.51 | ||||||

| Zinc percent |

3.61 | 3.70 | ||||||

| Total production cost per ton |

$ | 247.17 | $ | 190.54 | ||||

| Cash Cost, After By-product Credits, per Silver Ounce (1) |

$ | 6.57 | $ | 7.62 | ||||

| AISC, After By-product Credits, per Silver Ounce (1) |

$ | 13.15 | 14.24 | |||||

| Capital additions |

$ | 9,652 | $ | 5,912 | ||||

| (1) |

A reconciliation of these non-GAAP measures to total cost of sales, the most comparable GAAP measure, can be found below in Reconciliation of Total Cost of Sales (GAAP) to Cash Cost, Before By-product Credits and Cash Cost, After By-product Credits (non-GAAP) and All-In Sustaining Cost, Before By-product Credits and All-In Sustaining Cost, After By-product Credits (non-GAAP). |

The increase in gross profit in the first quarter of 2022 compared to the first quarter of 2021 was the result of higher sales volume and lead and zinc prices, partially offset by lower average silver prices.