Fiscal Year 2023 to Fiscal Year 2022

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

(Mark One)

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended

OR

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 FOR THE TRANSITION PERIOD FROM TO |

Commission File Number

GRESHAM WORLDWIDE, INC.

(Exact name of Registrant as specified in its Charter)

(State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification No.) |

(Address of principal executive offices) |

(Zip Code) |

Registrant’s telephone number, including area code: (

Securities registered pursuant to Section 12(b) of the Act: None

Title of each class |

|

Trading Symbol(s) |

|

Name of each exchange on which registered |

|

|

|

||

|

|

|

|

|

Securities registered pursuant to Section 12(g) of the Act: Common Stock, par value $0.001 per share

Indicate by check mark if the Registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐

Indicate by check mark if the Registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. Yes ☐

Indicate by check mark whether the Registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Indicate by check mark whether the Registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the Registrant was required to submit such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer |

|

☐ |

|

Accelerated filer |

|

☐ |

|

|

|

|

|||

|

☒ |

|

Smaller reporting company |

|

||

|

|

|

|

|

|

|

Emerging growth company |

|

|

|

|

|

|

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report.

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements.

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark whether the Registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No

The aggregate market value of the voting and non-voting common equity held by non-affiliates of the Registrant, based on the closing price of the shares of common stock on June 30, 2023, was $

The number of shares of Registrant’s Common Stock outstanding as of April 10, 2024 was

DOCUMENTS INCORPORATED BY REFERENCE

Auditor Firm Id: |

[# of Firm Id] |

Auditor Name: |

[Name of Auditor Firm] |

Auditor Location: |

[City, State/Province, Country] |

1

TABLE OF CONTENTS

|

|

Page No. |

|

||

|

|

|

Item 1 |

3 |

|

Item 1A |

13 |

|

Item 1B |

28 |

|

Item 2 |

29 |

|

Item 3 |

29 |

|

Item 4 |

29 |

|

|

|

|

|

|

|

|

|

|

Item 5 |

29 |

|

Item 6 |

30 |

|

Item 7 |

Management’s Discussion and Analysis of Financial Condition and Results of Operations |

31 |

Item 7A |

39 |

|

Item 8 |

40 |

|

Item 9 |

Changes in and Disagreements with Accountants on Accounting and Financial Disclosure |

40 |

Item 9A |

40 |

|

Item 9B |

41 |

|

Item 9C |

Disclosure Regarding Foreign Jurisdictions that Prevent Inspections |

41 |

|

|

|

|

||

|

|

|

Item 10. |

42 |

|

Item 11 |

45 |

|

Item 12 |

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters |

48 |

Item 13 |

Certain Relationships and Related Transactions, and Director Independence |

49 |

Item 14 |

50 |

|

|

|

|

|

|

|

|

|

|

Item 15 |

51 |

|

Item 16 |

53 |

|

|

|

|

|

|

|

2

FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K (the “Report”) contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933 (the “Securities Act”), and Section 21E of the Securities Exchange Act of 1934. These statements relate to future events or our future financial performance, including our liquidity, our receipt of future orders and whether our backlog will result in orders. We have attempted to identify forward-looking statements by terminology including “anticipates,” “believes,” “expects,” “can,” “continue,” “could,” “estimates,” “expects,” “intends,” “may,” “plans,” “potential,” “predict,” “should” or “will” or the negative of these terms or other comparable terminology. These statements are only predictions; uncertainties and other factors may cause our actual results, levels of activity, performance or achievements to be materially different from any future results, levels or activity, performance or achievements expressed or implied by these forward-looking statements. Although we believe that the expectations reflected in the forward-looking statements are reasonable, we cannot guarantee future results, levels of activity, performance or achievements. Our expectations are as of the date this Report is filed, and we do not intend to update any of the forward-looking statements after the date this Report is filed to confirm these statements to actual results, unless required by law.

This Report also contains estimates and other statistical data made by independent parties and by us relating to market size and growth and other industry data. This data involves a number of assumptions and limitations, and you are cautioned not to give undue weight to such estimates. We have not independently verified the statistical and other industry data generated by independent parties and contained in this Report and, accordingly, we cannot guarantee their accuracy or completeness, though we do generally believe the data to be reliable. In addition, projections, assumptions and estimates of our future performance and the future performance of the industries in which we operate are necessarily subject to a high degree of risks and uncertainties due to a variety of factors, including that (i) we will continue to secure orders and backlog in 2024 and that our Giga-tronics legacy business development efforts to generate new orders will improve, (ii) we will secure adequate cash to bridge operations, (iii) the ongoing geopolitical military conflict (including, the war in Israel, the Russian war on Ukraine, tensions with China and Taiwan and other unrest in the Middle East) will continue, (iv) supply chain turmoil and inflation will continue to affect customer demand for our product offerings, (v) defense budgets for electronic technology solutions that we provide will not decrease, (vi) our key medical customer will not reduce expected orders, and (vii) those other risks and described in “Item 1A - Risk Factors” and in this Report. These and other factors could cause results to differ materially from those expressed in the estimates made by the independent parties and by us.

PART I

ITEM 1. BUSINESS

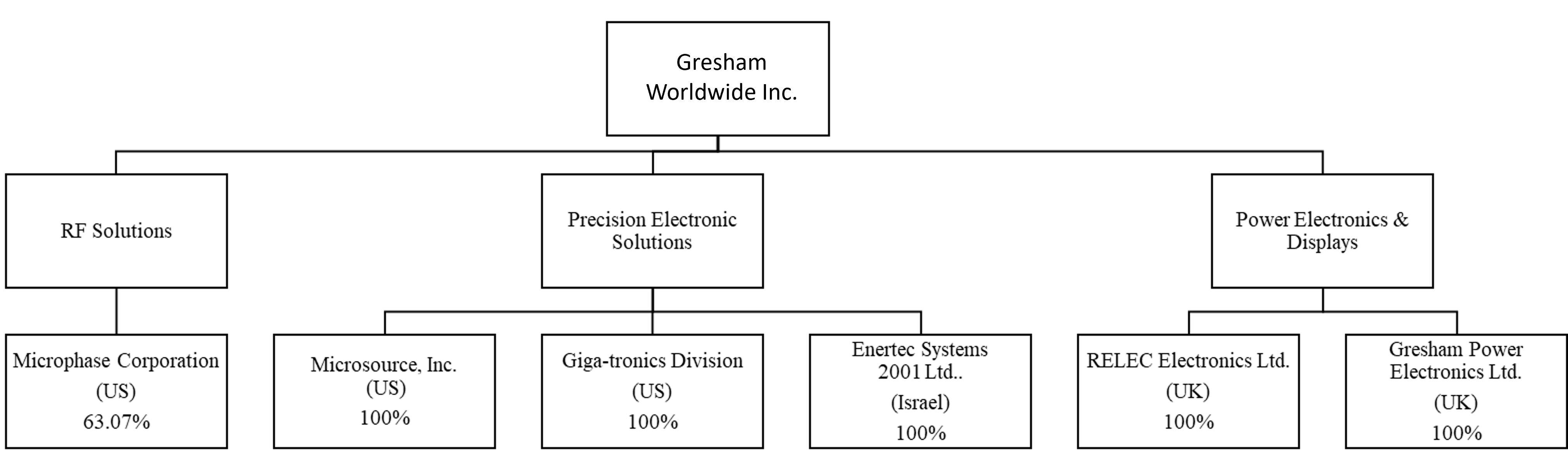

Gresham Worldwide, Inc., formerly Giga-tronics, Incorporated (“Gresham” or the “Company”) designs, manufactures and distributes purpose-built electronics equipment, automated test solutions, power electronics, supply and distribution solutions, as well as radio, microwave and millimeter wave communication systems and components for a variety of applications with a focus on the global defense industry and the healthcare market.

Gresham has two subsidiaries Gresham Holdings, Inc. (“Gresham Holdings”) and Microsource Inc. (“Microsource”). Gresham has also one division. Gresham is a majority-owned subsidiary of Ault Alliance, Inc., a Delaware corporation (“AAI”) and currently operates as an operating segment of AAI. Gresham Holdings has three wholly-owned subsidiaries, Gresham Power Electronics Ltd. (“Gresham Power”), Relec Electronics Ltd. (“Relec”), and Enertec Systems 2001 Ltd. (“Enertec”), and one majority-owned subsidiary, Microphase Corporation (“Microphase”). Our operations consist of three business segments:

We are focused on products that are getting designed in to military systems such as fighter jet, ships and ground vehicles or missiles, which provide a recurring revenue stream for years to come and eliminate competition because the cost of replacing designed in products is prohibitive for both the competition and the customer.

Gresham was incorporated in California on March 5, 1980 as Giga-tronics Incorporated. We changed our name to Gresham effective March 1, 2024. Our common stock continues to trade under the Giga-tronics name and symbol “GIGA” on the OTCQB. We have obtained shareholder

3

approval to reincorporate in Delaware. Both our name change and reincorporation are subject to Financial Industry Regulatory Authority approval.

Business Combination

On September 8, 2022 (the “Closing Date”), we acquired Gresham Holdings. We refer to this transaction as the “Business Combination.” Pursuant to the Business Combination, the Company acquired all of the outstanding shares of capital stock of Gresham Holdings and, in exchange the Company issued AAI 2,920,085 shares of the Company’s common stock and 514.8 shares of Series F preferred stock (“Series F”) that are convertible into an aggregate of 3,960,043 shares of the Company’s common stock, subject to potential adjustments, and the assumption of Gresham’s outstanding equity awards representing, on an as-assumed basis, 749,626 shares of the Company’s common stock. AAI beneficially owns 69.6% of the Company’s outstanding shares (excluding shares issuable upon conversion of convertible notes described elsewhere in this Report). The parties had previously entered into a Share Exchange Agreement dated December 27, 2021 (the “Agreement”) for which the Company obtained the requisite stockholder approval on September 8, 2022.

In connection with the consummation of the Business Combination, Gresham Holdings was deemed to be the accounting acquirer in the Business Combination based on an analysis of the criteria outlined in Accounting Standards Codification 805 “Business Combinations”. While we were the legal acquirer in the Business Combination, because Gresham Holdings was deemed the accounting acquirer, the historical financial statements of Gresham Holdings became the historical financial statements of the combined company, upon the consummation of the Business Combination.

We operate both within the United States (the “U.S.”) and at three locations abroad. A summary of our locations and high level review of our operations at each facility is provided in the table below:

Name |

|

Location |

|

Nature of Business |

Corporate Headquarters |

|

Scottsdale, Arizona |

|

Offices |

Microsource and Giga-tronics Division |

|

Livermore, California |

|

Offices, research and development, engineering, fabrication, sourcing, assembly, tuning and testing |

Microphase Corporation* |

|

Shelton, Connecticut |

|

Offices, research and development, engineering, fabrication, sourcing, assembly, tuning and testing |

Enertec Systems 2001 Ltd. |

|

Karmiel, Israel |

|

Offices, research and development, engineering, fabrication, sourcing, assembly, tuning and testing |

Relec Electronics Ltd. |

|

Wareham, Dorset, England UK |

|

Offices and warehouse operations |

Gresham Power Electronics Ltd. |

|

Salisbury, Wiltshire, England UK |

|

Offices, research and development, engineering, fabrication, sourcing, assembly, tuning and testing |

* |

63% owned |

Our Industry

Our operations focus exclusively on the market for electronic solutions that support the defense industry and other mission critical applications, including medical technology, transportation, and telecommunication. The essential nature of these applications provides a degree of insulation from volatility associated with other segments of the global economy while accounting for stability and steady growth of the addressable market opportunities available in segments that we serve. Demand for solutions to meet these requirements continues unaffected, and in many instances increases, in times of global crisis. Total defense spending in the three countries in which we currently operate was expected to total more than an estimated $919 billion in 2023 (https://www.globalfirepower.com/defense-spending-budget.php). We sell to the militaries and defense contractors in 15 other countries as well. Overall global defense spending hit $2.1 trillion in 2023 and is expected to grow at a CAGR of 3% through 2028 with U.S. spending continuing to lead the world in the same period (ASD Reports, Global Defense Budget Analysis - Forecast to 2028). The current wars in the Ukraine and Israel and tensions with China and in the Middle East have intensified interest and investment in defense platforms throughout the UK and Europe.

We believe that the increasing emphasis on electromagnetic spectrum operations and close coordination of air, land, sea, space and cyber operations will fuel an increase in defense modernization, force protection and situational awareness, all of which will drive increased spending in procurement of components and systems to enable electronic warfare, countermeasures and unattended solutions. The Defense Electronics Market was estimated to be $220.3 billion in 2023 and is projected to reach $ 289.0 billion by 2028, at a CAGR of 5.6%. (https://www.marketsandmarkets.com/Market-Reports/defense-electronics-market-183642563.html). The drive for greater connectivity and analytics will in turn increase demand for radio frequency (“RF”) communications, power electronics and electronic control solutions content in new major military platforms, which are the core offerings of our operating units.

Thousands of companies compete in this market to deliver electronics solutions to meet defense and other mission critical applications. However, our operating units have longstanding relationships with dominant defense contractors in the U.S., in the UK, in Israel and other countries who hold contracts for major defense platforms with very long life cycles. Our customers typically have unique needs, and they engage with Gresham in funding development contracts for custom solutions. Once a solution is proven in its application, the company typically realizes a secure,

4

recurring revenue stream for products, services and/or repairs for many years (sometimes decades) until the technology becomes outdated. Because the Company is often sole-sourced for developmental projects, it is highly unlikely that a competitor will replace such a designed-in product as the cost and re-qualification time to do so is prohibitive. These relationships enable us to narrow the field of competition considerably and grow based on repeat business with relatively low selling costs. As technology evolves, prime contractors may, over subsequent years, migrate to systems other than those we produce.

Beyond the defense arena, initiatives to complete $42 billion in upgrades to the current National Railway System in the UK over the next three years while spending $115 billion over the next 10 years to build high speed rail to link London with the Midlands cities of Birmingham, Leeds and Manchester will generate significant opportunities for growth in demand for power electronics to upgrade and replace current infrastructure, both in rolling stock and track side controls. Relec’s current relationships and track record for supplying power solutions to the UK rail industry position us ideally to capitalize on these ongoing refurbishment and expansion efforts. A similarly robust market in the medical power supply markets with a compound annual growth rate of 6.9% to reach $1.8 billion in 2025 creates growth opportunities for Relec in the UK. Increases in contracts for the precision manufacturing of medical diagnostic and calibration tools drive growth opportunities for Enertec as well.

Our Business Strengths

We have the following core strengths that we believe give us a competitive advantage:

Our Strategy

Our goal is to become the supplier of choice for the major players in the defense industry and provide for solutions for mission critical applications in health care.

Our near-term strategies are focused on developing synergies as a result of the acquisition of Gresham Holdings:

In addition, we are focused on securing sufficient working capital to execute on a substantial backlog of orders with definite delivery dates, take on additional significant orders and further improve access to capital resources.

Our long-term strategy includes the following key elements:

5

Our Operations

We conduct our business through our subsidiaries. After the Business Combination, we aligned the operations of our subsidiaries into three key market groups as follows:

RF Solutions

Microphase focuses on designing, engineering, assembling, tuning and testing components, integrated assemblies and subsystems that detect, filter, analyze and process radio frequency, microwave and millimeter wave signals for defense applications.

Precision Electronic Solutions

In the Precision Electronic Solutions group, Enertec, and the Giga-tronics Division and Microsource focus on designing, engineering, developing and producing turnkey precision electronic solutions for mission critical applications primarily focused on defense customers and large global healthcare customers.

Power Electronics and Display Solutions

Gresham Power focuses on providing power electronics solutions to defense customers in the UK and non-U.S. countries. Relec distributes power electronics and displays for mission critical applications to customers in health care, transportation, telecommunications and industrial businesses.

A detailed description of three market groups and associated product offerings follows.

RF Solutions

Microphase Corporation

Microphase designs, engineers, manufactures and distributes components, integrated assemblies and subsystems for a variety of military and telecommunications applications. Such components include RF and microwave filters, diplexers, multiplexers, detectors, switch filters, integrated assemblies and Detector Logarithmic Video Amplifiers. Microphase engineers, tunes and tests all its products under stress conditions per defined in tuning protocols and test procedures it developed as part of the production process. This approach ensures that its customers can use and incorporate Microphase products into systems with confidence that the products will perform reliably under extreme operating conditions.

Microphase’s customers include the U.S. military, and contractors to the U.S. military and to militaries of other countries including prime contractors and sub-contractors. Microphase’s technology innovations are used in many significant U.S. Government defense programs, including the F-16, the F-18, the F-35, the JAS Gripen Fighter and the B-1B Bomber.

Microphase’s advanced technology products include:

|

• |

|

filters that sort and clarify microwave signals, including multiplexers that are a series of filters combined in a single package; |

|

• |

|

solid state amplifiers that amplify microwave signals; |

|

• |

|

detectors and limiters that are semiconductor devices for detection of radar signals and protection of receivers from damage from high power signals and jamming; |

|

• |

|

detector log video amplifiers that are fully integrated, ruggedized, “mil-spec” signal detection systems; and |

|

• |

|

integrated assemblies that combine multiple functions from a range of components and devices, including transmitters, receivers, filters, amplifiers, detectors, and other functionality into single, efficient, high performance, multifunction assemblies. |

6

|

|

|

|

Microphase’ revenue has grown 34% to $8.2 million in 2023 from $6.1 million in 2022.

Precision Electronic Solutions

Enertec Systems 2001 Ltd.

Based in Israel, Enertec designs, develops, manufactures and maintains advanced end-to-end high technology precision electronic solutions for military, medical and industrial markets. Those solutions include custom computer-based automated test equipment and turnkey systems to ensure combat readiness, provide command and control, and direct and deploy resources in military operations in harsh environments and battlefield conditions.

Enertec delivers complete end-to-end project management with requirements definition, systems engineering, design/development, production, testing, integration, field support, maintenance and optimization. Its custom engineered solutions enable and support mission critical air, land and sea military platforms, e.g., missiles, UAVs, combat aircraft, boats, submarines, trailers and satellites. Enertec’s primary customers include the largest major defense contractor in Israel. In addition, Enertec has a strategic partnership to build and deliver solutions for the Indian military.

Enertec is among Israel’s largest, most well-established manufacturers of test equipment and simulators. Enertec develops and manufacture test systems and simulators for all types of weapons systems at all levels of maintenance, development, and integration. Enertec is currently working on developing a new generation of electronics cards and assemblies to build a new generation of test systems. Enertec complies with all information security requirements included in its customer contracts as well as all the confidentiality laws that Israel mandates for work related to defense of the country.

In addition, Enertec designs, develops, and provides precision equipment to calibrate cardiac catheters for a global health care products company. This business has grown to 27% of revenues in 2023 from 7% of Enertec’s annual revenues in 2021. The US healthcare provider is very satisfied with the current product and is requesting an additional product design which the customer will pay for its development.

Enertec’s offices and engineering and assembly facility are located in Karmiel, Israel, which is near the border with Lebanon. The Hezbollah, an Iranian Proxy, who is located near the Lebanese border, threatens to expand the war to Northern Israel and is increasing its rocket attacks. As such, several employees had to relocate to a more southern location to avoid attacks from the north. In addition, several employees were drafted into military service.

Enertec is a material subsidiary and through December 31, 2023, approximately 41% of the Company’s revenues were derived from Enertec.

The war in Israel poses significant risks to Enertec including possible rocket launches from Lebanon that could destroy Enertec’s facility. Enertec has no alternative facility and the cost of locating a new facility and equipping it would effectively cause it to cease operations for at least six months. If the war continues, it could have a material adverse effect on our operations and financial condition.

Enertec’s revenue has grown approximately 24% in 2023 from $12.5 million in 2022.

Giga-tronics Division

Our Giga-tronics Division designs, manufactures, and markets functional test products and integrates those test products along with third-party hardware and software to deliver solutions for evaluating and validating radar and electronic warfare product performance. The Division developed a Threat Emulation System (“TEmS”) using an agile, phase coherent wide bandwidth upconverter hosted within the compact industry standard AXIe modular platform. The TEmS solution is smaller in size, lower in cost than currently used threat simulation systems and when coupled with a tracking antenna, operates at lower power levels making it an ideal solution for outdoor installations with multiple locations for simulating integrated air defense systems.

Giga-tronics Division’s revenue has increased to $1.3 million in 2023 from $0.9 million in 2022. It currently has a $185,000 backlog.

Microsource, Inc.

Microsource’s two largest customers are prime contractors for which we developed and manufactured sophisticated RADAR filters used in fighter aircraft. Microsource serves the market for operational hardware associated with the U.S. Government’s RADAR Modernization Program for prior generation fighter aircraft (i.e., the F-15D, F-16, and F/A-18E jets) to extend their useful lives. We design these filters to operate under extreme conditions. Currently the platforms on which Microsource filter technologies are used are in various stages of product life cycle. Both F-15 and F-16 fighter jet fleets are aging out and programs are nearing end-of-life and are in maintenance and sustainment phases. This will result in reduced revenue

As a result, revenue has declined to $2.7 million in 2023. The current backlog is $336,000.

Power Electronics and Displays

Our subsidiaries in the UK design, develop, manufacture and distribute advanced electronic technology solutions which convert, regulate, purify, manage or distribute electrical power for electronic equipment. Our power solutions are intended for mission-critical defense, industrial, health care and transportation applications in, and generally convert Alternating Current (“AC”) from the power grid to Direct Current (“DC”), or

7

modify the voltage being delivered (DC to DC). Our subsidiaries also offer standard off-the-shelf, modified-standard and purpose-built products. Although our subsidiaries sell standard products unmodified to its customers, those standard offerings are designed into specific customer product configurations in most instances. Our Power Electronics and Displays Group also designs, engineers and builds power systems and display solutions to specific customer requirements for mission critical applications in defense, medicine, transportation, telecommunications and manufacturing.

Relec

Relec develops custom, designed-in solutions for various applications ranging from light industrial to heavily ruggedized for the harshest of environments. Relec customizes product features and functionality to achieve optimum performance and service delivery for specific customer requirements. Relec currently operates in specific fields, specializing in AC-DC Power Supplies, DC-DC Converters, Displays and EMC Filters.

Relec’s revenue has grown 3% to $8.5 million in 2023 from $8.2 million in 2022.

Gresham Power

Gresham Power specializes in engineering, designing and developing power conversion, power supplies, uninterruptible power supplies and distribution solutions for Naval applications, with equipment installed on virtually all the UK Royal Navy’s submarine and surface fleet. Many of Gresham Power’s ultra-reliable offerings support shipboard distribution of electrical power in emergencies (such as loss of main ship’s power) to enable continued operation of weapons systems, tactical communications and lighting.

Gresham Power products add diversity to Gresham’s product line, provide greater access to defense customers in the UK and European markets, and strengthen Gresham’s engineering and technical resources.

Gresham Power’s revenue has declined 10% to $1.7 million in 2023 from $1.9 million in 2022.

Research and Development

In 2023, the research and development expenditures were approximately $2,827,000 or 7.4% of revenue. In 2022, the research and development expenditures were approximately $2,137,000 or 7.1% of revenue.

We are focusing our development effort on military products which require (1) the handling of classified documents and an infrastructure that is secure such as a SPIC, CMMC and ITAR compliance, and (2) personnel that has security clearance and (3) meeting the military AS9100 quality standard. In addition, we are focused on products that are getting designed in to military systems such as fighter jet, ships and ground vehicles or missiles, which provide a recurring revenue stream for years to come and eliminate competition because the cost of replacing designed in products is prohibitive for both the competition and the customer.

Our engineering and product development efforts vary with each operating subsidiary. Most of these efforts focus on designing and developing new products in connection with custom product design and modification of standard electronics offerings to provide solutions tailored to specific customer requirements. Our engineers work closely with customers and specialist partners to incorporate modifications or create custom designs for specific project requirements. The customer typically pays for such engineering services which are charged to the cost of revenue.

Enertec provides full-service design and development of turnkey Precision Electronic Solutions. Microphase designs custom RF solutions to meet customer unique specifications. When required, other subsidiaries modify standard products to meet specific customer requirements, including, but not limited to, redesigning commercial products to meet requirements for military applications based on commercial off-the-shelf products and for other customized product requirements, when applicable. We continually seek to improve our product offerings while anticipating changing market demands for increased functionality, customized firmware and improved EMI (electromagnetic interference) filtering.

The legacy Giga-tronics Division historically has funded product development activities internally, through product line sales, or through outside equity investment and debt financing. Microsource and Microphase typically have designed, engineered and developed new product offerings in close collaboration with and funded by its customers.

There can be no assurance that future technologies, processes, or product developments will not render our current product offerings obsolete or that we will be able to develop and introduce new products or enhancements to existing products that satisfy customer needs in a timely manner or achieve market acceptance. Failure to do so could adversely affect our business.

Competition

The defense electronic technology solutions industry is highly fragmented and characterized by intense competition. Our competition includes thousands of companies located throughout the world, some of which have advantages in terms of labor and component costs, and some of which may offer products superior or comparable in quality to us. Each operating subsidiary confronts a different set of competitors depending on solutions offered, vertical markets targeted and geographic scope of operations. We also face competition from current and prospective customers who may decide to design and manufacture power electronics, communications components and precision electronic solutions needed to satisfy their internal programmatic requirements.

8

Consolidation in the defense technology solutions market, including through mergers, acquisitions and/or strategic alliances among major primes to whom we sell our products, has the potential to intensify the competitive pressures that we face. Many of our existing and potential competitors may be better positioned than us to acquire other companies, technologies or products. We compete favorably on the basis of multiple factors, including product quality and reliability, technological capabilities, service, past performance, design flexibility and ability to develop and implement complex, integrated solutions customized to its customers’ needs, and cost-effectiveness. Focusing on products with relatively low volumes and high margins enables our operating subsidiaries to compete favorably on price against larger companies with much high indirect cost structures (overhead and G&A) and cumbersome internal bureaucracies. Finally, the fragmentation of the defense technology market also creates opportunities to grow through acquiring competitors and/or potential competitors.

Many competitors have substantially greater financial and marketing resources and geographic presence than we have. However, cost-effective designs, elegant engineering, a collaborative/consultative approach to managing customer relations and a long history of delivering high quality, ultra-reliable, custom designed components and subsystems have enabled us to compete effectively and carve out a defensible niche position against competitors with more resources.

Manufacturing and Testing

We fabricate components and performs product assembly, integration and testing at production facilities in Livermore, California (Microsource and the Giga-tronics Division), Shelton, Connecticut (Microphase), Karmiel, Israel (Enertec) and Salisbury, England (Gresham Power). Each of our operating business has built a robust network of trusted supply chain partners to provide components, materials and parts for assembly into products or products for resale.

We continually strive to improve our production and test processes, to ensure the highest quality and consistent manufacturing of its solutions. Each operating business maintains rigorous quality control to ensure that our solutions conform to all customer specifications and will perform reliably in the customer’s application. We test our products under stress operating conditions per defined test procedures we developed in conjunction with our customers. This approach ensures that our customers can use its solutions right out of the box on their production line or installed directly in the field. We offer customer specific testing services with custom designed tests to simulate operation within our customer applications.

All operating units comply with all applicable safety and EMC standards for electronics solutions.

Compliance with international safety agency standards is critical in every application, and power solutions play a major role in meeting these compliance requirements. Our safety engineers and quality assurance teams help ensure that our custom products are designed to meet all safety requirements and are appropriately documented to expedite safety approval processes.

We maintain ISO 9001:2008 (Enertec), ISO 9001:2015 (Microphase, Gresham Power and Relec) and AS9100D (Enertec, Microphase, Microsource and the Giga-tronics Division) certification in our manufacturing operations. ISO 9001 and AS9100 are universally recognized and accepted international standards for quality management.

Customer Service and Support

Our operating companies offer a “high touch” approach to optimizing and customizing solution offerings to meet customer unique requirements. Working closely with customers, we design, engineer, develop and produce offerings to the highest standards of performance, durability and reliability to meet unique customer requirements. All operating units constantly track performance against cost, quality and on-time delivery metrics with an intense focus on customer satisfaction. Following the Business Combination, regular communications and direct collaboration at all levels with customers have become hallmarks of all our operations.

Given the mission critical nature of the customer applications which our product and solution offerings support, we respond promptly and take necessary corrective action to ensure our offerings conform to the specifications and work to that specific customer’s expectations. We provide warranties on all products offered. The length and terms of the warranties vary with the product type and application in which the product gets used. In addition, even after warranties expire, our operating units will provide maintenance, repair and post-delivery support for the full expected life of the product.

Suppliers

Given the demanding performance requirements and challenging operating envelopes for Gresham products and the Platforms on which they’re used, component vendor selection and management is a key success factor. While substantially most of the components required to make our assemblies are available from multiple sources, we occasionally use sole source arrangements to obtain leading-edge technology or favorable pricing or supply terms, but not in any material volume. Furthermore, the longevity of the programs on which our products are used occasionally presents a parts obsolescence challenge which the Company is continuously monitoring and managing. In our opinion, the loss of any sole source arrangement we have would not materially affect our operations, though we could experience production delays as we seek new suppliers or re-design components of our products. Some suppliers are also competitors of ours. In the event a competitor-supplier chooses not to sell its products to us, production delays that could significantly affect our business could occur as we seek new suppliers or re-design components of our products.

Our operating businesses purchase electronic components, materials, parts and assemblies, including power supplies, converters, transformers, rectifiers, inverters, housings, blocks, covers, machined parts, substrates, resistors, diodes, detectors, amplifiers, integrated circuits, printed circuit

9

boards, cables, connectors, metal work, and capacitors, from outside suppliers. We also purchase certain precious metals used in manufacturing of our products (plating, sealing, painting, finishing). We carefully select suppliers based on their ability to provide quality parts and components which meet technical specifications and volume requirements. For defense work, our subsidiaries have built supply chain networks from sources only in the U.S. (Microphase and Microsource source exclusively from the U.S.), Enertec and Relec also source from the U.S., the UK (Gresham Power, Relec) and Israel (Enertec) with no sourcing from China. Relec does work with suppliers in China for some commercial applications.

Customers

Gresham’s defense customers include the Israeli MOD and Israel Air Industries (“IAI”), Rafael and Elbit Systems, the four major defense contractors in Israel, the United States Department of Defense (“U.S. DOD”) and major defense contractors such as BAE Systems North America, L3Harris, Boeing, Lockheed Martin, Raytheon and Sierra Nevada Corporation in the U.S., the UK Ministry of Defense including the Royal Navy, and major defense contractors in the UK and Europe, including BAE Systems PLC, Rolls Royce, Babcock and Thales, SAAB (Sweden), Indra (Spain) and Aselsan (Turkey). In addition, Enertec has a strategic partnership through IAI with Cyient to build and deliver solutions for the Indian military.

Gresham’s commercial customers include Elma GmbH, BioSense Webster, a subsidiary of Johnson & Johnson (a key Enertec customer), RS Components, Farnell, Parker Hannifin, Vanderbilt, Bombardier.

For 2023, Gresham’s two largest customers accounted in the aggregate for 40% of its consolidated revenues. The following table describes Gresham’s customer concentration as of December 31, 2023, based on the percentage of revenue during 2023:

Customer |

|

Country |

|

Revenue |

|

|

% of Total Revenue |

|

|

||

Customer A |

|

Israel |

|

$ |

11,129 |

|

|

|

29 |

% |

|

Customer B |

|

Israel |

|

|

4,042 |

|

|

|

11 |

% |

|

Total |

|

|

|

$ |

15,172 |

|

|

|

40 |

% |

|

Our business depends largely on defense spending and program budgets which expand and contract across fiscal year periods. Revenues from orders for our products and services often span several years with deliveries varying across both interim and annual fiscal year periods. We therefore expect that a major customer in one year may not be a major customer in the following year. Accordingly, our net revenue and earnings may vary significantly from one period to the next and will decline if we are unable to gain new customers or cannot increase our business with other existing customers to replace declining net revenue from the previous year’s major customers.

Proprietary Technology and Intellectual Property

Our competitive position is largely dependent upon our ability to deliver systems and products that (a) effectively and reliably meet customers’ needs and (b) selectively surpass competitors’ specifications in competing products. While patents may provide protection of proprietary designs, with the rapid progress of technological development in our industry, such protection is often short-lived. Therefore, although we occasionally pursue patent coverage, we emphasize the development of new products with superior performance specifications and the upgrading of existing products toward this same end.

Our trade names, trademarks, trade secrets, customer relationships, domain names, proprietary technologies and similar intellectual property are important to our success. We rely upon a combination of trade secrets, industry expertise, confidential procedures, and contractual provisions to protect our intellectual property. We believe that because our products are continually updated and revised, obtaining patents would be costly and not beneficial. It is policy to enter into confidentiality and invention assignment agreements with our employees and contractors as well as nondisclosure agreements with our suppliers and strategic partners in order to limit access to and disclosure of our proprietary information.

Microphase and Enertec typically design custom products to their customer specifications as “work for hire” and therefore own no intellectual property in the design. As the ultimate end user, the U.S. military and the Israeli MOD typically acquire and retain rights in all such technical data. Microphase does acquire and own intellectual property in the fabrication, assembly, tuning and testing protocols followed for its products.

In the UK, Gresham Power typically will retain ownership of the intellectual property of the designs of products developed for defense applications. However, neither Relec nor Gresham Power typically retain intellectual property in any of the standard power products that they sell on the commercial market.

Our Giga-tronics Division products are primarily based on our own designs, which are derived from our own engineering abilities. If our new product engineering efforts fall behind, our competitive position weakens. Conversely, effective product development greatly enhances our competitive status. While we utilize certain software licenses in certain functional aspects for some of our products, such licenses are generally readily available, non-exclusive and are obtained at either no cost or for a relatively small fee.

We have maintained three patents related to our 2500B parametric signal generator and two patents related to the Company’s Advanced Signal Generator & Analysis product lines (ASGA platform). A third patent for the ASGA platform was recently granted.

In February 2020, the Company was granted a U.S. patent relating to its ASGA Platform. The patent describes the internal design of the Advanced Signal Generator and the Advanced Signal Analyzer (“ASGA”) along with the architecture of how the components work together to facilitate building multi-channel test systems with reduced size, weight and cost as compared to present solutions. A second patent was granted in

10

November 2020 describing uses of the ASGA system in high channel-count situations. A third patent application which was filed in April 2020 describing how the ASGA platform achieves its low noise performance while achieving fast frequency switching speeds was granted by the U.S. Patent and Trademark Office on May 30, 2023.

The Company has paid the U.S. Patent and Trademark Office fees to keep the patents open to allow adding new claims as they arise for continued intellectual property protection.

Operating Capital

We generally strive to maintain adequate levels of inventory and we generally sell to customers on 30-day payment terms in the U.S while allowing more time for our international customers. Typically, we receive payment terms of 30 days from our suppliers. We believe that these practices are consistent with typical industry practices. Beyond financing, our primary sources of liquidity come from customer sales, which are dependent on our receipt and shipment of customer orders.

Gresham’s liquidity was historically supported by AAI’s injection of cash consisting of contributions to capital and loans. AAI has continued to support us with $2.4 million of loans in fiscal 2023. We are seeking additional capital to fund our operations, although we may not be successful in our efforts to do so. See “Risk Factors - Risks Related to Our Financial Condition”. We will need additional capital to fund our operations, and our inability to generate or obtain such capital on acceptable terms, or at all, could harm our business, operating results, financial condition and prospects.”

See “Management’s Discussion and Analysis of Financial Condition and Results of Operations -Liquidity and Capital Resources - Our Recent Financings” for the discussion of our financing activities.

Sales and Marketing

We market our products directly to our customers and rely on internal sales forces within each of our operating subsidiaries primarily to identify leads and complete sales. We also engage independent sales representatives who are perceived to have expertise with targeted markets and/or customers. Our marketing and sales efforts target specific types of customers such as major defense contractors, manufacturers of industrial products, health care solutions and infrastructure components in transportation and telecommunications.

Corporate Chief Development Officer

Following the Business Combination, we began relying on Gresham Holdings then Chief Operating Officer to lead our sales and marketing team. Prior to that executive’s retirement in November 2023, he had recruited our Chief Development Officer whose principal role is to drive organic growth and identify prospects for further growth through mergers and/or acquisitions. We have implemented Gresham’s Hub Spot to capture and track the opportunity stream within and among the operating subsidiaries.

RF Solutions

In recent years, much of the business development effort at Microphase comes through engineer to engineer collaboration resulting into products that are designed-in to military systems, as well as our Chief Development Officer holding and maintaining most customer relationships. For the foreseeable future, the backlog of designed-in products is driving the RF Solutions business.

Precision Electronic Solutions

Much of business development and sales effort at Enertec has historically taken place at the senior executive level. The two largest customers of Enertec resulted in 98% of Enertec’s revenue in 2023. Enertec’s former Chief Executive Officer passed away in early March 2024. Our Chief Operating Officer Mr. Nissim Ovadia worked closely with Mr. Avni and has been promoted to Chief Executive Officer at Enertec. Mr. Ovadia while Chief Operating Officer was able to interface with Enertec’s key customers. Additionally, our Chief Executive Officer, Mr. Jonathan Read is the new Chairman of Enertec and is focusing additional efforts to its business. Going forward, we are hopeful that our Precision Electronic Solutions will benefit from Mr. Ovadia’s continuing effort to develop business for turnkey precision electronic solutions.

Power Electronics and Displays

The Power Electronics and Displays group has a high performing team of four sales professionals supported by a sales administrator and two inside sales professionals to continue drive new business and growth in the UK and European markets. If we can solve our liquidity issues, we plan to add more business development resources in 2024 focused specifically on defense customers for Power Electronics and Displays while the group also expands use of strategic third-party channel partners and or Manufacturer’s Representatives in the Middle East, India and Australia in 2024. These representatives will promote our products and serve as the customer interface for Power Electronics and Displays in specific parts of the world as agreed. Typically, either we or the manufacturing representatives are entitled to terminate the manufacturer representative agreement upon 30 days’ written notice.

Relec and Gresham Power advertise in highly targeted industry-specific publications such as Electronics Weekly, New Electronics, Electronic Product Design & Test, Electronics Specifier, Components in Electronics, Design Products & Applications, Rail Technology Magazine, Rail Engineer, Rail Professional. In addition, Relec also posts regular podcasts on topics of interest to customers and prospect as well as running an active public relations campaign to get placements of earned media and coverage in a wide range of media. We look to replicate similar campaigns in other operating subsidiaries to generate inquiries/leads, raise awareness of us and support talent recruiting efforts.

11

Other Marketing Activities

We promote our products and solutions by attending trade shows such as the Association of Old Crows Conferences, Defense Manufacturing Conference, Land Forces Conference (Australia), Doha International Maritime Defense Exhibition & Conference (DIMDEX) Electronica (Europe), Southern Manufacturing and Electronics, and Railtex.

Each of our operating businesses maintain a comprehensive website emphasizing its respective capabilities and expertise. We plan to upgrade all our websites to standardize corporate identification while adding more features and functionality to drive inquiries, generate leads from prospective customers and support recruiting efforts.

Government Regulation

We must meet applicable regulatory, environmental, emissions, safety and other requirements where specified by the customer and accepted by it or as required by local regulatory or legal requirements. The products that we market and sell in Europe may be subject to the 2003 European Directive on Restriction of Hazardous Substances (“RoHS”), which restricts the use of six hazardous materials in the manufacture of certain electronic and electrical equipment, as well as the 2002 European Directive on Waste Electrical and Electronic Equipment (“WEEE”), which determines collection, recycling and recovery goals for electrical goods. In July 2006, our industry began phasing in RoHS and WEEE requirements in most geographical markets with specific emphasis on consumer-based products. We believe that RoHS and WEEE-compliant components may be subject to longer lead-times and higher prices as the industry transitions to these new requirements. REACH Registration, Evaluation, Authorization and Restriction of Chemicals Registration, is a European Union regulation dating from December 18, 2006. REACH addresses the production and use of chemical substances, and their potential impacts on both human health and the environment.

In addition to these requirements for our dealings with customers in the EU, similar regulatory mandates from the U.S., the UK and Israel apply to all our operating subsidiaries. We have structured operations to comply with these requirements and have experienced little to no impact on lead times or prices. Given the applicability of these requirements to all competitors alike, we believe that compliance has had no impact on the competitive position of any operating subsidiary.

Some of our products are subject to the International Traffic in Arms Regulation (”ITAR”), which is administered by the U.S. Department of State. ITAR controls not only the export of certain products specifically designed, modified, configured or adapted for military systems, but also the export of related technical data and defense services and foreign production. We obtain required export licenses for any exports subject to ITAR. Compliance with ITAR may require a prolonged period of time; if the process of obtaining required export licenses for products subject to ITAR is delayed, it could have a materially adverse effect on our business, financial condition, and operating results. Any future restrictions or charges may be imposed by the U.S. or any other foreign country. In addition, from time-to-time, we enter into defense contracts to supply technology and products to foreign countries for programs that are funded and governed by the U.S. Foreign Military Financing program.

We are also subject to heightened government scrutiny of our operations pursuant to certain of our contracts.

Security Clearances

As a U.S. Government contractor, we are required to maintain facility and personnel security clearances complying with the U.S. DOD and other Federal agency requirements. All Gresham operating companies in the U.S. maintain strict protocols for handling classified information and Confidential Unclassified Information associated with its work for the U.S. DOD. We have built within both our production facilities in Shelton, CT and Livermore, CA “Restricted Areas” certified for generating, storing and reviewing classified information. Our U.S. subsidiaries and Division also must obtain and maintain “authority to operate” equipment to perform classified work. The process to secure these authorities is long and laborious. Our U.S. subsidiaries have an experienced information security team to oversee applications to secure these authorities as well as ongoing monitoring to maintain the security of these systems.

Gresham Power works on contracts classified as “Official Sensitive” that require individual security clearances and adherence to information security protocols for receiving, handling and storing confidential information as required in the UK Official Secrets Act and its implementing regulations. Relec does not work on classified, sensitive defense work.

Enertec complies with all information security requirements included in its customer contracts as well as all the confidentiality laws that the State of Israel mandates for work related to defense of the country.

Audits and Investigations

As a government contractor, we are subject to audits and investigations by U.S. Government agencies including the Defense Contract Audit Agency (the “DCAA”), the Defense Contract Management Agency (the “DCMA”), the Inspector General of the U.S. DOD and other departments and agencies, the Government Accountability Office, the Department of Justice (the “DoJ”) and Congressional Committees. From time-to-time, these and other agencies investigate or conduct audits to determine whether a contractor’s operations are being conducted in accordance with applicable requirements. The DCAA and DCMA also review the adequacy of, and compliance with, a contractor’s internal control systems and policies, including the contractor’s accounting, purchasing, property, estimating, earned value management and material management accounting systems. Our final allowable incurred costs for each year are also subject to audit and have from time to time resulted in disputes between us and the U.S. Government. Any costs found to be improperly allocated to a specific contract will not be reimbursed or must be refunded if already reimbursed. If an audit or investigation uncovers improper or illegal activities, we may be subject to civil and criminal penalties and administrative

12

sanctions, which may include termination of contracts, forfeiture of profits, suspension of payments, fines and suspension or prohibition from doing business with the U.S. Government.

The Defense Federal Acquisition Regulation, as implemented in standard contract clauses, mandates that our U.S. business establish and follow extensive detailed processes and protocols to protect classified and Confidential Unclassified Information (CUI) from disclosure and unauthorized access. That mandate includes a requirement that Microphase formulate and implement a System Security Plan with 110 different elements and protocols for handling and protecting classified information and CUI. Over the next two years the U.S. DOD will require all participants in the defense supply chain to demonstrate compliance with the Capability Model Maturity Cybersecurity as verified through an independent third-party auditor. Compliance with these mandates requires and will require Gresham’s U.S. subsidiaries to invest significant resources to maintain compliance. For instance, compliance requires extensive security controls on access to IT systems, strong firewalls and intrusion monitoring. We have in place an experienced team to ensure information security for all subsidiaries in the U.S. as well as oversee security of all employees and facilities in U.S. operations. These investments add to indirect cost pools that our U.S. operations must recover in the price of its products for U.S. DOD and contractors.

Enertec conducts operations under constant supervision of the Ministry of Defense of Israel. All its contracts are subject to audits of performance, quality and price reasonableness. Enertec has implemented the strongest possible cybersecurity protections consistent with the resources available to a company its size.

Gresham Power contracts with UK Ministry of Defense, Royal Navy or major contractors serving those agencies include standard provisions which give the customer the right to audit its performance under those contracts when they see fit. Audits are part of doing business with the government and typically focus on deliveries - on time project milestones as well as quality. The Royal Navy reviews Gresham Power pricing of services provided under support contract every 12 months for reasonableness.

Gresham Power is fully certified as “Cyber Essentials Plus Compliant.” Cyber Essentials Plus is a government backed, industry-supported scheme to help organizations protect themselves against common online threats. The UK Government requires all suppliers bidding for contracts involving the handling of sensitive and personal information to be certified against the Cyber Essentials program criteria.

Other Compliance Issues

In addition, we are subject to the local, state and national laws and regulations of the jurisdictions where we operate that affect companies generally, including laws and regulations governing commerce, intellectual property, trade, health and safety, the environment contracts, privacy and communications, cybersecurity, web services, tax, and corporate laws and securities laws. These regulations and laws may change over time. Unfavorable changes in existing and new laws and regulations could increase our cost of doing business and impede its growth.

Employees

As of April 15, 2024, we had a total of 179 employees located in the U.S., the UK and Israel. All but seven of these employees are employed on a full-time basis. We believe that our future success depends on our ability to attract and retain skilled personnel. Competition for skilled personnel in our markets is competitive. While our size and capital resources constrain our ability to attract and retain employees with cash compensation, we attempt to compensate for this constraint by offering opportunities for training and internal promotion. None of our employees is currently represented by a trade union. We consider our relations with our employees to be good. From time-to-time, we may hire additional workers on an independent contractor basis as the need arises. Presently, due to its backlog and expected orders, Microphase needs to add employees in addition to its planned use of Microsource employees.

ITEM 1A. RISK FACTORS

An investment in our common stock involves significant risks. Before investing in our common stock, you should consider each of the following risk factors and any other information set forth in this Report and the other reports filed by the Company with the Securities and Exchange Commission (the “SEC”),including the Company’s financial statements and related notes, in evaluating the Company’s business and prospects. The risks and uncertainties described below are not the only ones that impact on the Company’s operations and business. Additional risks and uncertainties not presently known to the Company, or that the Company currently considers immaterial, may also impair its business or operations. If any of the following risks actually occurs, the Company’s business and financial condition, results or prospects could be harmed. Please also read carefully the section entitled “Forward-Looking Statements” at the beginning of this Report. If any of the events or developments described below occurs, our business, financial condition and results of operations may suffer. In that case, the value of our common stock may decline and you could lose all or part of your investment.

Risk Factors Summary

Our business and an investment in our common stock are subject to numerous risks and uncertainties, including those highlighted in this “Risk Factors” section below. Some of these risks include:

Risks related to our Financial Condition

13

Economic, Policy and Business Risks

Sales, Business Development and Competitive Risks

Performance and Operational Risks

Risks Related to our Foreign Operations

14

Regulatory and Compliance Risks

Risks Related to the Ownership of our Common Stock

Risks Related to our Financial Condition

We have doubts about our ability to continue as a going concern.

We believe that there is doubt about our ability to continue as a going concern because we have incurred recurring net losses and we have not been able to procure funding for our negative cashflows. Convertible notes issued to two lenders mature in October 2024 and convertible notes issued to AAI mature in January 2025. Our inability to continue as a going concern could have a negative impact on the Company, including our ability to obtain needed financing, and could adversely affect the trading price of our common stock.

We have historically incurred net losses and negative cash flow and our operating results may significantly vary from quarter-to-quarter, so we may not be able to achieve or sustain profitability.

For the years ended December 31, 2023 and 2022, Gresham reported revenue of $38.0 million and $30.3 and net losses of $15.3 million and $18.4 million, respectively. We expect to continue to incur substantial expenditures to develop and market our products and services and we could continue to incur losses and negative operating cash flow in the near future. As the result of our lack of working capital, we face a number of challenges:

In addition, our operating results have in the past been subject to quarter-to-quarter fluctuations, and we expect that these fluctuations will continue, and may increase in magnitude, in future periods. Demand for our products is driven by many factors, including the availability of funding for our products in our customers’ budgets. There is a trend for some of our customers to place large orders near the end of a quarter or fiscal year, in part to spend remaining available budget funds. Seasonal fluctuations in customer demand for our products driven by budgetary and other concerns can create corresponding fluctuations in period-to-period revenue, and we therefore cannot assure you that our results in one period are necessarily indicative of our revenue in any future period. In addition, the number and timing of large individual sales and the ability to obtain acceptances of those sales, where applicable, have been difficult for us to predict, and large individual sales have, in some cases, occurred in quarters subsequent to those we anticipated, or have not occurred at all. The loss or deferral of one or more significant sales in a quarter could harm our operating results for such quarter. It is possible that, in some quarters, our operating results will be below the expectations of public market analysts or investors. Finally, supply chain issues have in the past and may in the future affect future quarters.

We will need additional capital to fund our operations, and our inability to generate or obtain such capital on acceptable terms, or at all, could harm our business, operating results, financial condition and prospects.

15

We will need to raise additional capital to pay our indebtedness and to support our working capital requirements and our planned growth. Any other future financing may include shares of common stock, shares of preferred stock, warrants to purchase shares of common stock or preferred stock, debt securities, units consisting of the foregoing securities, equity investments from strategic development partners or some combination of the foregoing. There is no assurance that additional financing will be available, or if available, will be on acceptable terms. If we are unable to raise additional capital, we may be required to curtail our operations and take additional measures to reduce costs, including reducing our workforce and eliminating outside consultants in order to conserve cash in amounts sufficient to sustain operations and meet our obligations. This could in its turn have a material adverse effect on our business, operating results and future prospects. There can be no assurance that we will be able to complete any future financing.

Because we require consents to obtain new financings, we may not be able to pursue these transactions if we cannot obtain the consents.

We issued AAI Series F preferred stock and common stock upon the consummation of the Business Combination. The term of the Series F contains negative covenants that apply such as incurring indebtedness of $1,000,000 in any individual transaction or $2,500,000 in the aggregate, or acquiring any business in which the aggregate consideration payable by us is $1 million or more. In addition, if we issue further equity, subject to exceptions for certain excluded securities, such limited issuances pursuant to equity incentive plans, AAI will have the right to purchase additional equity to maintain its ownership interest. Even if AAI fully converts the Series F into shares of our common stock, the Convertible Notes that we issued in connection with the AAI Financing and the transaction documents that we entered into in connection with our January 2023 sale of Senior Secured Convertible Notes with the two investment funds contain substantially similar covenants that are included in the Series F. These provisions could limit our ability to raise capital or make future acquisitions, particularly larger acquisitions. For more information about these negative covenants, see “Management’s Discussion and Analysis of Financial Condition and Results of Operations - Liquidity and Capital Resources – Our Financings.”

As a result of our outstanding convertible notes and related warrants, our stockholders are subject to significant future dilution.

As of April 8, 2024 we had $18.2 million in outstanding indebtedness evidenced by convertible notes which are convertible into 72.9 million shares of our common stock, subject to possible increases, and 2 million warrants exercisable for nominal consideration. Because of our cash needs, we will have to engage in a new financing or modify of our existing financings. Any new financing or modification may be even further dilutive to our stockholders. Further, the convertible notes have price protection so if we enter into a new financing with a lower conversion or exercise price, those instruments will automatically be adjusted resulting in further dilution.

Economic, Policy and Business Risks

A large percentage of our current revenue is derived from prime defense contractors to the U.S. government and its allies, and the loss of these relationships, a reduction in government funding or a change in government spending priorities or bidding processes could have an adverse impact on our business, financial condition, results of operations and cash flows.

The defense programs may compete with other policy needs, which may be viewed as more necessary. For example, budget and appropriations decisions made by the governments of the U.S, the UK and Israel are outside of our control and have long-term consequences for its business. Government spending priorities and levels remain uncertain and difficult to predict and are affected by numerous factors, and the purchase of our products could be superseded by alternate arrangements. The current prolonged delay in providing new aid to Ukraine and Israel are evidence of the political uncertainties. While defense budgets in countries around the world have generally increased, there can be no assurance that such increases will continue for the foreseeable future. A change in government spending priorities or an increase in non-procurement spending at the expense of our programs, or a reduction in total defense spending, could have material adverse consequences on our future business.

If our reputation or relationships with the governments of the U.S., the UK or Israel or the limited number of defense contractors with whom we work were harmed, our future revenues and cash flows would be adversely affected.

Gresham derives most of its revenue from the governments of the U.S., the UK and Israel as well defense contractors across the world that supply those countries and their allies. Our reputation and relationships with various government entities and agencies, in particular with the U.S. DOD and Ministries of Defense in the UK and Israel, and the limited number of defense contractors serving these agencies, are key factors in maintaining and growing these revenues and winning bids for new business. Negative press reports or publicity, regardless of accuracy, could harm our reputation. If our reputation or relationships with government agencies were to be negatively affected, or if we are suspended or debarred from contracting with government agencies for any reason, the amount of business with government and other customers would decrease and our financial condition and results of operations could be adversely affected.

Because we engage in fixed fee contracts with our customers, we face pressure on our gross profit margins and operating costs from inflation.

Our financial condition, results of operations, and liquidity may be negatively impacted by increased levels of inflation. We are not able to predict the timing and effect of inflation, or its duration and severity. Inflation may cause our costs to purchase inventory to be higher than we planned, and reduce our gross profit margins. Also inflation tends to increase our compensation and other costs. Because of the fixed price contracts we enter into,we may not be able to sell our products to our customers at correspondingly increased prices to cover the impact of inflation, resulting in decreased profit margins.

We may have liabilities that are not known, probable or estimable at this time.

16

We remain subject to certain past, current, and future liabilities. There could be unasserted claims or assessments against or affecting us, including the failure to comply with applicable laws and regulations. In addition, there may be liabilities of ours that are neither probable nor estimable at this time that may become probable or estimable in the future, including indemnification requests received from our customers relating to claims of infringement or misappropriation of third party intellectual property or other proprietary rights, tax liabilities arising in connection with ongoing or future tax audits and liabilities in connection with other past, current and future legal claims and litigation. Any such liabilities, individually or in the aggregate, could have a material adverse effect on our financial condition. We may learn additional information that adversely affects us, such as unknown, unasserted, or contingent liabilities and issues relating to compliance with applicable laws or infringement or misappropriation of third-party intellectual property or other proprietary rights.

The effects of Russia’s invasion of Ukraine, the war in Israel and tensions elsewhere in the world on the capital markets and the economy is uncertain, and we may have to deal with a recessionary economy and economic uncertainty including possible adverse effects upon the capital markets.

Russia’s invasion of Ukraine, the war in Israel and tensions with China and Iran have created increased uncertainty in the capital markets and caused in part increased inflation. This may make it more difficult for us to raise capital and the result may be more expense and dilution. We cannot predict how these factors will affect the capital markets, but the impact may be adverse and may delay or prevent us from completing future financings or make any financings.

If the inflationary pressures in the U.S. and elsewhere where we operate continue, we could experience reduced margins and lose future business.

While the inflation rate is lower than it had been, the current inflationary pressures are affecting our gross profit margins particularly since we have lacked the capital to accumulate material inventory. Most of our contracts (except with Relec) are fixed price, which reduces our margins when inflation occurs. Reducing our selling prices results in further reduction of our margins. This customer pricing pressure may also result in the loss of contracts and/or future business. Finally, we are experiencing rising labor and other costs which may further increase our losses.

If we lose key personnel, it could have a material adverse effect on our financial condition, results of operations, and growth prospects.

Our success will depend on the continued contributions of key officers and employees. The loss of the services of key officers and employees, whether such loss is through resignation or other causes, or the inability to attract additional qualified personnel, could have a material adverse effect on our financial condition, results of operations, and growth prospects. In November 2023, our Chief Operating Officer retired. He was a key employee, and he is not being replaced as his duties have been assumed by our Chief Technology Officer. While we believe the replacement of Enertec’s former Chief Executive Officer by its Chief Operating Officer will not have a material adverse effect, it is possible that our expectations will be proved to be incorrect. Further, Gresham Power’s Chief Executive Officer passed away in March 2024. With Gresham Power, the loss of Ms. Karen Jay must be viewed against its declining business. We are uncertain whether we will be able to replace her.

Our success will depend on the continued contributions of key officers and employees. The loss of the services of key officers and employees, whether such loss is through resignation or other causes, or the inability to attract additional qualified personnel, could have a material adverse effect on our financial condition, results of operations, and growth prospects. In November 2023, our Chief Operating Officer retired. He was a key employee, and he is not being replaced as his duties have been assumed by our Chief Technology Officer. The loss of Zvika Avni, Enertec’s Chief executive Officer, due to illness who managed our Israeli operations in the past, could also materially harm our business.

We do not know if the loss of key employees will result in any adverse effects. However, if we were to lose Jonathan Read, Robin Shaffer, Sean Lyle and/or Lutz Henckels, our Chief Executive Officer, Chief Operating Officer, Chief Development Officer and Chief Financial Officer respectively, or Nissim Ovadia, Enertec’s Chief Executive Officer, our business would be materially and adversely affected.

Our sales and profitability may be affected by changes in economic, business and industry conditions.