UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

For the fiscal year ended December 31 , 2022

or

For the transition period from __________ to __________

Commission File Number: 001-02960

(Exact name of registrant as specified in its charter)

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |||||||

| (Address of principal executive offices) | (Zip Code) | |||||||

Registrant’s telephone number, including area code: (281 ) 362-6800

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||||||

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes ☐ No ☑

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

Yes ☐ No ☑

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | ☑ | ||||||||||||

| Non-accelerated filer | ☐ | Smaller reporting company | ||||||||||||

| Emerging growth company | ||||||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act.

☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report.

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements.

☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b).

☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act).

Yes ☐ No ☑

The aggregate market value of the voting and non-voting common equity held by non-affiliates of the registrant, computed by reference to the price at which the common equity was last sold as of June 30, 2022, was $283.1 million. The aggregate market value has been computed by reference to the closing sales price on such date, as reported by The New York Stock Exchange.

As of February 17, 2023, a total of 89,700,767 shares of common stock, $0.01 par value per share, were outstanding.

Documents Incorporated by Reference:

NEWPARK RESOURCES, INC.

INDEX TO ANNUAL REPORT ON FORM 10-K

FOR THE YEAR ENDED DECEMBER 31, 2022

1

CAUTIONARY STATEMENT CONCERNING FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K contains “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933, as amended, Section 21E of the Securities Exchange Act of 1934, as amended, and the Private Securities Litigation Reform Act of 1995, as amended. We also may provide oral or written forward-looking statements in other materials we release to the public. Words such as “will,” “may,” “could,” “would,” “should,” “anticipates,” “believes,” “estimates,” “expects,” “plans,” “intends,” and similar expressions are intended to identify these forward-looking statements but are not the exclusive means of identifying them. These forward-looking statements reflect the current views of our management as of the filing date of this Annual Report on Form 10-K; however, various risks, uncertainties, contingencies, and other factors, some of which are beyond our control, are difficult to predict and could cause our actual results, performance, or achievements to differ materially from those expressed in, or implied by, these statements.

We assume no obligation to update, amend, or clarify publicly any forward-looking statements, whether as a result of new information, future events, or otherwise, except as required by securities laws. In light of these risks, uncertainties, and assumptions, the forward-looking events discussed in this Annual Report on Form 10-K might not occur.

For additional information regarding these and other factors, risks, and uncertainties that could cause actual results to differ, we refer you to the risk factors set forth in Item 1A "Risk Factors" in this Annual Report on Form 10-K.

2

PART I

ITEM 1. Business

General

Newpark Resources, Inc. is a geographically diversified supplier providing environmentally-sensitive products, as well as rentals and services to customers across multiple industries. Our business currently operates through two reportable segments: Industrial Solutions and Fluids Systems. In addition, we had a third reportable segment, Industrial Blending, which was exited in 2022.

Our Industrial Solutions segment provides temporary worksite access solutions, including the rental of our recyclable composite matting systems, along with related site construction and services to customers in various markets including power transmission, oil and natural gas exploration and production (“E&P”), pipeline, renewable energy, petrochemical, construction and other industries, primarily in the United States and Europe. We also manufacture and sell our recyclable composite mats to customers around the world, with power transmission being the primary end-market.

Our Fluids Systems segment provides drilling, completion, and stimulation fluids products and related technical services to customers for oil, natural gas, and geothermal projects primarily in North America and Europe, the Middle East and Africa (“EMEA”), as well as certain countries in Asia Pacific and Latin America. In the fourth quarter of 2022, we exited two of our Fluids Systems business units, including our U.S.-based mineral grinding business as well as our Gulf of Mexico fluids operations.

Newpark Resources, Inc. was organized in 1932 as a Nevada corporation. In 1991, we changed our state of incorporation to Delaware. Our principal executive offices are located at 9320 Lakeside Boulevard, Suite 100, The Woodlands, Texas 77381. Our telephone number is (281) 362-6800. You can find more information about us on our website located at www.newpark.com. We file or furnish annual, quarterly and current reports, proxy statements and other documents with the Securities and Exchange Commission (“SEC”). Our Annual Report on Form 10-K, our Quarterly Reports on Form 10-Q, our Current Reports on Form 8-K and any amendments to those reports are available free of charge through our website. These reports are available as soon as reasonably practicable after we electronically file these materials with, or furnish them to, the SEC. Our Code of Ethics, our Corporate Governance Guidelines, our Audit Committee Charter, our Compensation Committee Charter, and our Environmental, Social and Governance Committee Charter are also posted to the governance section of our website. We make our website content available for informational purposes only. It should not be relied upon for investment purposes, nor is any information contained on our website incorporated by reference in this Form 10-K. The SEC also maintains a website at www.sec.gov that contains reports, proxy and information statements, and other information regarding issuers that file electronically with the SEC, including us.

When referring to Newpark Resources, Inc. (“Newpark,” the “Company,” “we,” “our,” or “us”), the intent is to refer to Newpark Resources, Inc. and its subsidiaries as a whole or on a segment basis, depending on the context in which the statements are made. The reference to a “Note” herein refers to the accompanying Notes to Consolidated Financial Statements contained in Item 8 “Financial Statements and Supplementary Data.”

Industry Fundamentals

Our Industrial Solutions segment, which has been our primary source of operating income, cash flows, and financial returns in recent years, provides temporary worksite access products and services to a variety of industries, including power transmission, E&P, pipeline, renewable energy, petrochemical, construction and other industries. The demand for our products and services from customers in these industries is driven, in part, by infrastructure construction and maintenance activity levels within the United States and the United Kingdom, including required infrastructure investments to support energy transition efforts. During 2020, our business was impacted by the COVID-19 pandemic, as customers delayed purchases and planned projects. As markets recovered in 2021 following the COVID-related economic slowdown, the impacts of global supply chain disruptions caused elevated cost inflation to the resin and other materials used to manufacture our composite mats, although this impact moderated during 2022. While these raw material cost increases and increased competitive pressures have negatively impacted the profitability of our business, we have worked with customers to substantially mitigate the inflationary impacts on our business. Product sales, which represent approximately one-third of our Industrial Solutions segment revenues, largely reflect sales to power transmission customers and other industrial markets, and typically fluctuate based on the timing of customer orders. The power transmission sector contributes the majority of our Industrial Solutions segment revenues, and we expect customer activity in this sector will grow over the next several years, driven in part by the impacts of increasing investments in energy transition and grid reliance initiatives.

Our Fluids Systems segment operating results remain dependent on oil and natural gas drilling activity levels in the markets we serve and the nature of the drilling operations, which governs the revenue potential of each well. Drilling activity levels depend on a variety of factors, including oil and natural gas commodity pricing, inventory levels, product demand, and

3

regulatory restrictions. Oil and natural gas prices and activity are cyclical and volatile, and this market volatility has had significant impacts on our operating results.

Rig count data remains the most widely accepted indicator of drilling activity. During March 2020, oil prices collapsed due to geopolitical events along with the worldwide effects of the COVID-19 pandemic. As a result, U.S. rig count declined significantly beginning in March 2020 before reaching a low of 244 rigs in August 2020. During 2021, oil prices rebounded, and the average U.S. rig count gradually increased, ending 2021 at 586 rigs. During 2022, oil prices significantly increased due in part to geopolitical events, and the average U.S. rig count continued to increase, ending 2022 at 779 rigs. We anticipate that market activity in the U.S. will remain fairly stable in the near-term, but will remain well below 2019 levels as many of our customers maintain stronger capital discipline and prioritize cash flow generation over growth. Further, in the wake of the COVID-19 pandemic, an uncertain economic environment, including widespread supply chain disruptions, as well as enacted and proposed legislative changes in the U.S. impacting the oil and natural gas industry, make market activity levels difficult to predict.

Outside of North America land markets, drilling activity is generally more stable as this drilling activity is based on longer-term economic projections and multi-year drilling programs, which typically reduces the impact of short-term changes in commodity prices on overall drilling activity. However, operations in several countries in the EMEA region experienced activity disruptions and project delays beginning in early 2020 and continuing through 2021, driven by government-imposed restrictions on movements of personnel, quarantines of staffing, and logistical limitations as a result of the COVID-19 pandemic. Drilling activity within international markets gradually recovered in 2021 and 2022, though the combination of increasing activity levels combined with the impacts of global supply chain disruptions have caused significant cost inflation to many hydrocarbon-based products and chemicals used in our fluids systems. While we have worked, and continue to work, with customers to mitigate the inflationary impact, in some cases, we are unable to adjust, or there may be delays in being able to adjust, our customer pricing on certain international contracts due to the long-term contracts in place. Consequently, the inflationary impacts negatively impacted the profitability of our international operations in 2022. Although we expect this situation to improve in the near-term, the impact of cost inflation is very difficult to predict.

Looking ahead, the combination of recent geopolitical events, including the ongoing conflict between Russia and Ukraine, and elevated oil and natural gas prices are causing several markets to increase drilling activity levels, to help ensure reliable energy supply in the coming years, while reducing their dependency on Russia-sourced oil and natural gas. Consequently, the outlook for several markets, including North America and the EMEA region, continues to strengthen, with growth in activity expected over the next few years.

Strategy

Our long-term strategy includes key foundational elements that are intended to enhance long-term shareholder value creation:

•Expansion in end-markets aligned to energy transition – In recent years, the majority of our profitability and cash flow has been derived from the utilities and other industrial end-markets and our continued expansion into these end-markets reflects our highest priority for capital deployment in the foreseeable future. During 2022, approximately 83% of our capital investments were directed to our Industrial Solutions segment, the majority of which was to grow our rental fleet in support of our expanding presence in the power and transmission sector. Meanwhile, we also divested certain underperforming business units in 2022 within our Fluids Systems segment, which has reduced our dependency on customers in the volatile E&P industry. The continued expansion of revenues in industrial markets, and particularly end-markets that are likely to benefit from ongoing energy transition efforts around the world, such as power transmission, renewable energy, and geothermal, remains a strategic priority going forward, and we anticipate that our capital investments will primarily focus on supporting this objective.

•Provide products that enhance environmental sustainability – We have a long history of providing environmentally-sensitive technologies to our customers. In the Industrial Solutions segment, we believe that the lightweight design of our fully recyclable DURA-BASE® matting system provides a distinct environmental advantage for our customers as compared to alternative wood mat products in the market, by eliminating deforestation required to produce wood mat products while also reducing greenhouse gas emissions associated with product transportation. We also continue to leverage our investments in research and development capabilities and adaptable manufacturing processes to increase the use of recycled and alternate materials in our composite mat production, providing further potential economic benefits along with a significant reduction in lifecycle greenhouse gas emissions when compared to using traditional virgin resin. During 2022, our manufacturing operations consumed over 450,000 pounds of recycled resin, and we look to expand our usage of recycled materials going forward. In our Fluids Systems segment, our family of high-performance water-based fluids systems, which we market as Evolution® and DeepDrill® systems, are designed to enhance drilling performance while also providing a variety of environmental benefits relative to traditional oil-based fluids. Our Fluids Systems segment has also developed a water-based fluids system designed specifically for clean-

4

energy geothermal drilling, which we market as TerraThermTM. The continued advancement of technology that provides our customers with economic benefits, while also enhancing their environmental and safety programs, remains a priority for our research and development efforts.

•Focus on value creation, balancing growth with return of capital to shareholders – We are committed to a disciplined growth strategy, balancing our investments in high-returning business activities with the return of capital through share repurchases. During the fourth quarter of 2022, we purchased approximately 5% of our outstanding shares of common stock and are committed to returning a substantial portion of our future free cash flow generation to our shareholders.

Segment Overview

Industrial Solutions

Our Industrial Solutions segment provides temporary worksite access solutions, including the rental of our recyclable composite matting systems, along with related site construction and services to customers in various markets including power transmission, E&P, pipeline, renewable energy, petrochemical, construction and other industries, primarily in the United States and Europe (70% of 2022 segment revenues represented rental and service). We also manufacture and sell our recyclable composite mats to customers around the world, with power transmission being the primary end-market (30% of 2022 segment revenues represented product sales).

Raw Materials — The resins, chemicals, and other materials used to manufacture our recyclable composite mats are widely available. Resin is the largest material component in the manufacturing of our recyclable composite mat products. We believe that our sources of supply for materials used in our business are adequate for our needs. We are not dependent upon any one supplier, and we have encountered no significant shortages or delays in obtaining any raw materials. In recent years, we have also expanded the use of recycled materials in our manufacturing process, which we believe provides further protection against potential shortages of virgin raw materials.

Technology — We have patents related to the design and manufacturing of our recyclable DURA-BASE mats and several of the components, as well as other products and systems related to these mats (including the connecting pins and the EPZ Grounding System™), although certain key patents have since expired in recent years. Using proprietary technology and systems is an important aspect of our business strategy. We believe the lightweight design of our recyclable matting system provides a distinct environmental benefit for our customers as compared to alternative wood mat products in the market, by eliminating deforestation required to produce wood mat products and also reducing CO2 emissions associated with product transportation. While we continue to enhance the performance, environmental, and safety benefits of our products and add to our patent portfolio, we believe that our scale, responsiveness to customers, and reputation in the industry with respect to our technical development and know-how, understanding of regulatory requirements, and our ability to deliver superior worksite access solutions also have competitive significance in the markets we serve.

Competition — Our market is fragmented and competitive, with many competitors providing various forms of worksite access products and services. Wood mats and stone continue to be the primary solutions utilized for temporary worksite access across industries, though composite matting solutions continue to gain market share. The competitive landscape for composite mat sales is less fragmented than rental and services, with only a few competitors providing various alternatives to our DURA-BASE composite mat products, including Signature Systems Group and Spartan Mat. This is due to many factors, including large capital start-up costs and proprietary technology associated with these products. We believe that the principal competitive factors in our businesses include reputation, product capabilities, price, innovation through R&D, and reliability, and that our competitive position is enhanced by our proprietary products, manufacturing expertise, services, and experience.

Customers — Our customers are principally utility companies, infrastructure construction companies, and oil and natural gas E&P companies operating in the markets that we serve. Wood mats and stone continue to be the primary solutions utilized for temporary worksite access across industries, though composite matting solutions continue to gain market share. During 2022, approximately 71% of our segment revenues were derived from our 20 largest segment customers. No single customer accounted for more than 10% of our segment revenues. The segment also generated 93% of its revenues domestically during 2022. Typically, we perform services either under short-term contracts or rental service agreements. As most agreements with our customers are cancellable upon short notice, our backlog is not significant. We do not derive a significant portion of our revenues from government contracts.

5

Fluids Systems

Our Fluids Systems segment provides drilling, completion, and stimulation fluids products and related technical services to customers for oil, natural gas, and geothermal projects primarily in North America (67% of 2022 segment revenues) and EMEA (30% of 2022 segment revenues), as well as certain countries in Asia Pacific and Latin America. We offer customized solutions for complex subsurface conditions such as horizontal, directional, geologically deep, or drilling in deep water. These projects require high levels of monitoring and technical support of the fluids system during the drilling process. In the fourth quarter of 2022, we exited two of our Fluids Systems business units, including our U.S.-based mineral grinding business as well as our Gulf of Mexico fluids operations (see Note 2 for additional information).

Raw Materials — We believe that our sources of supply for materials and equipment used in our fluids business are adequate for our needs. In connection with the sale of our U.S.-based mineral grinding business, we entered into a four-year barite supply agreement for certain regions of our U.S. drilling fluids business. We also obtain barite and other materials used in the fluids business from various third-party suppliers. In 2022, as a result of the global supply chain disruptions, including the effect of the ongoing conflict between Russia and Ukraine, we experienced shortages and significant cost increases associated with many of our raw materials, however, none of the product shortages materially impacted our operations.

Technology — Proprietary technology and systems are an important aspect of our business strategy, though we believe that our reputation in the industry, the range of services we offer, ongoing technical development and know-how, and responsiveness to customers, are of equal or greater competitive significance than our existing proprietary rights. We seek patents and licenses on new developments whenever we believe it creates a competitive advantage in the marketplace. We own patent rights in a family of high-performance water-based fluids systems, which we market as Evolution® and DeepDrill® systems, which are designed to enhance drilling performance while also providing a variety of environmental benefits relative to traditional oil-based fluids. In addition, we have developed the TerraThermTM water-based fluids system designed specifically for clean-energy geothermal drilling. We also rely on a variety of unpatented proprietary technologies and know-how in many of our applications.

Competition — Globally, we face competition from larger companies, including Halliburton, Schlumberger, and Baker Hughes, which compete vigorously on fluids performance and/or price. Moreover, these companies have broad product and service offerings in addition to their fluids systems. Within North America, the drilling fluids market is more fragmented, with many smaller regional competitors competing with us primarily on price and local relationships. We believe that the principal competitive factors in our businesses include a combination of technical proficiency, reputation, price, reliability, quality, and experience, and that our competitive position is enhanced by our best-in-class customer experience and value enhancing products and services.

Customers — Our customers are principally major integrated and independent oil and natural gas E&P companies operating in the markets that we serve. During 2022, approximately 47% of segment revenues were derived from our 20 largest segment customers. No single customer accounted for more than 10% of our segment revenues. The segment also generated 57% of its revenues domestically during 2022. In North America, we primarily perform services either under short-term standard contracts or under “master” service agreements. Internationally, some customers issue multi-year contracts, but many are on a well-by-well or project basis. As most agreements with our customers can be terminated upon short notice, our backlog is not significant. We do not derive a significant portion of our revenues from government contracts.

Industrial Blending

Our Industrial Blending segment began operations in 2020 and supported industrial end-markets, including the production of disinfectants and industrial cleaning products. In 2022, we completed the wind down of the Industrial Blending business, and sold the industrial blending and warehouse facility and related equipment located in Conroe, Texas (see Note 2 for additional information).

6

Human Capital

We are committed to providing a diverse and inclusive environment for all employees and for those with whom we conduct business. We recognize our greatest assets are our people, and our long-term sustainability depends on our ability to attract, motivate, and retain the highly talented individuals that make up the Newpark team, while protecting each other like family and sustaining the environment in which we work. We appreciate our people and their achievements as we recognize they are integral to fully implementing our business strategy, which directly translates to improving our long-term profitability and increasing shareholder value.

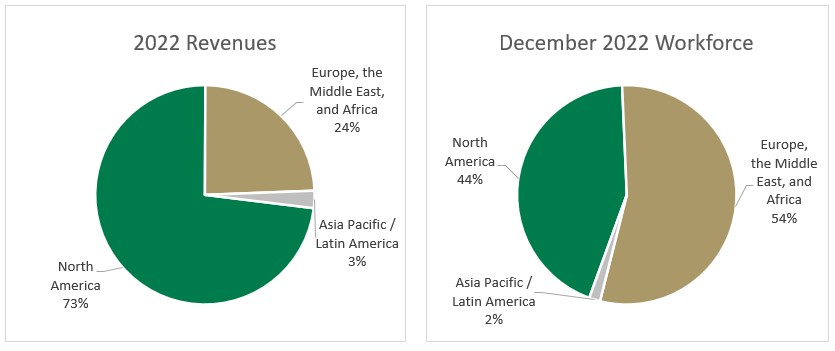

As a global company, the Newpark team supporting our customers spans more than 20 countries, and more than half of our employees reside outside of the United States. Our global footprint provides natural diversity within our organization and serves as a foundation to support an inclusive approach to everything that we do. At December 31, 2022, we employed approximately 1,540 full and part-time personnel, none of which are represented by labor unions. We consider our relations with our employees to be satisfactory and through various company-culture initiatives, strive to reinforce our commitment to our Core Values of safety, integrity, respect, excellence, and accountability. The following charts present the geographic composition of our revenues and workforce.

Governmental Regulations

Our business exposes us to regulatory risks associated with the various industries that we serve, including governmental regulations relating to the oil and natural gas industry in general, as well as environmental, health, and safety regulations that have specific application to our business. Our activities are impacted by various federal, state, local, and foreign laws, regulations, and policies related to pollution control, health, and safety programs that are administered and enforced by regulatory agencies.

We have implemented various procedures designed to ensure compliance with applicable regulations and reduce the risk of damage or loss. These include specified handling procedures and guidelines for waste, ongoing employee training, and monitoring, as well as maintaining insurance coverage. We also utilize a corporate-wide health, safety, and environmental management system (“HSEMS”). The HSEMS is designed to capture information related to the planning, decision-making, and general operations of environmental regulatory activities within our operations. We also use the HSEMS to capture the information generated by regularly scheduled independent audits that are performed to validate the findings of our internal monitoring and auditing procedures.

7

ITEM 1A. Risk Factors

The following summarizes the most significant risks to our business. In addition to these risks, we are subject to a variety of risks that affect many other companies generally, as well as other risks and uncertainties that are not known to us as of the date of this Annual Report. Our success will depend, in part, on our ability to anticipate and effectively manage these and other risks. Any of these risk factors, either individually or in combination, could have a material adverse effect on our results of operations or financial condition, or prevent us from meeting our profitability or growth objectives. If you hold our securities or are considering an investment in our securities, you should carefully consider the following risks, together with the other information contained in this Annual Report.

Risks in this section are grouped in the following categories: (1) Business and Industry Risks; (2) Indebtedness Risks; (3) Legal and Regulatory Risks; (4) Financial Risks; and (5) General Risks. Many risks affect more than one category, and the risks are not in order of significance or probability of occurrence because they have been grouped by categories.

Business and Industry Risks

Risks Related to the Worldwide Oil and Natural Gas Industry

Although we continue to diversify our operations and expand into a variety of end-markets, we derive a significant portion of our revenues from customers in the worldwide oil and natural gas industry; therefore, our risk factors include those factors that impact the demand for oil and natural gas. Spending by our customers for exploration, development, and production of oil and natural gas is based on a number of factors, including expectations of future hydrocarbon demand, energy prices, the risks associated with developing reserves, our customers’ ability to finance exploration and development of reserves, regulatory developments, and the future value of the reserves. Reductions in customer spending levels adversely affect the demand for our products and services, and consequently, our revenues and operating results. The key risk factors that we believe influence the worldwide oil and natural gas markets are discussed below.

Demand for oil and natural gas is subject to factors beyond our control

Demand for oil and natural gas, and consequently the demand for our products and services, is highly correlated with global economic growth and in particular by the economic growth of countries such as the U.S., India, China, and developing countries in Asia and the Middle East. Weakness in global economic activity, as well as the global energy transition, could reduce demand for oil and natural gas and result in lower oil and natural gas prices. For example, demand for oil and natural gas has been and could continue to be impacted by, among other things, the effects of global health crises, geopolitical issues, supply chain disruptions and inflation. There remains significant uncertainty regarding the long-term impact to global oil demand, which will ultimately depend on various factors and consequences beyond our control. Continued weakness or deterioration of the global economy could further reduce our customers’ spending levels and could reduce our revenues and operating results.

Regulatory agencies and environmental advocacy groups in the European Union, the U.S. and other regions or countries have been focusing considerable attention on the emissions of carbon dioxide, methane and other greenhouse gases and their role in climate change. There is also increased focus, including by governments and our customers, investors and other stakeholders, on these and other sustainability and energy transition matters. Existing or future legislation and regulations related to greenhouse gas emissions and climate change, as well as initiatives by governments, nongovernmental organizations, and companies to conserve energy or promote the use of alternative energy sources, and negative attitudes toward or perceptions of fossil fuel products and their relationship to the environment, may significantly curtail demand for and production of oil and gas in areas of the world where our customers operate, and thus reduce future demand for our products and services. This may, in turn, have a material adverse effect on our business, financial condition, results of operations, and cash flows.

Supply of oil and natural gas is subject to factors beyond our control

Supply of oil and natural gas can be affected by the availability of quality drilling prospects, exploration success, and the number and productivity of new wells drilled and completed, as well as the rate of production and resulting depletion of existing wells. Oil and natural gas storage inventory levels are indicators of the relative balance between supply and demand. Supply can also be impacted by the degree to which individual Organization of Petroleum Exporting Countries nations and other large oil and natural gas producing countries are willing and able to control production and exports of hydrocarbons, to decrease or increase supply, and to support their targeted oil price or meet market share objectives. Any of these factors could affect the supply of oil and natural gas and could have a material effect on our results of operations.

Volatility of oil and natural gas prices can adversely affect demand for our products and services

Volatility of oil and natural gas prices can also impact our customers’ activity levels and spending for our products and services. The level of energy prices is important to the cash flow for our customers and their ability to fund exploration and

8

development activities. Expectations about future commodity prices and price volatility are important for determining future spending levels. Our customers also consider the volatility of energy prices and other risk factors by requiring higher returns for individual projects if there is higher perceived risk.

Our customers’ activity levels, spending for our products and services, and ability to pay amounts owed us could be impacted by the ability of our customers to access equity or credit markets

Our customers’ activity levels are dependent on their ability to access the funds necessary to develop oil and natural gas prospects and their ability to generate sufficient returns on investments. In recent years, limited access to external sources of funding, including the impacts of the global energy transition and pressures from their investors to generate consistent cash flow has, at times, caused customers in the oil and natural gas industry to reduce their capital spending plans. In addition, a reduction of cash flow to our customers resulting from declines in commodity prices or the lack of available debt or equity financing may impact the ability of our customers to pay amounts owed to us.

A heightened focus by our customers on cost-saving measures rather than the quality of products and services could reduce the demand for our products and services

Our customers are continually seeking to implement measures aimed at greater cost savings, which may include the acceptance of lesser quality products and services in order to improve short term cost efficiencies as opposed to total cost efficiencies. The continued implementation of these kinds of cost saving measures could reduce the demand or pricing for our products and services and have a material adverse effect on our business, financial condition, and results of operations.

Risks Related to Our Ability to Generate Internal Growth

Our ability to generate internal growth may be affected by, among other factors, our ability to:

•attract new customers;

•increase the number of projects performed for existing customers;

•successfully bid for new projects;

•hire and retain qualified personnel;

•obtain necessary levels of equipment; and

•adapt the range of products and services we offer to address our customers’ evolving needs.

In addition, our customers may reduce the number or size of projects available to us due to their inability to obtain capital or in response to economic conditions.

Furthermore, the growth of our Industrial Solutions segment is heavily dependent upon the production of our recyclable composite mat products, which in turn is dependent on the operations and capacity of our manufacturing facilities in Carencro, Louisiana.

Many of the factors affecting our ability to generate internal growth may be beyond our control, and we cannot be certain that our strategies will be successful or that we will be able to generate cash flow sufficient to fund our operations and to support internal growth. If we are unsuccessful, we may not be able to achieve internal growth, expand our operations or grow our business.

Risks Related to Economic and Market Conditions that May Impact Our Customers’ Future Spending

A substantial portion of our operating income, cash flows, and financial returns is generated from construction projects, the awarding of which we do not directly control. The construction industry historically has experienced cyclical fluctuations in financial results due to economic recessions, downturns in business cycles of our customers, material shortages, price increases by subcontractors, interest rate fluctuations and other economic factors beyond our control. When the general level of economic activity deteriorates, our customers may delay, or cancel upgrades, expansions, and/or maintenance and repairs to their systems. Many factors, including the financial condition of the industry, could adversely affect our customers and their willingness to fund capital expenditures in the future.

In addition, economic, regulatory and market conditions affecting our specific end markets may adversely impact the demand for our services, resulting in the delay, reduction or cancellation of certain projects and these conditions may continue to adversely affect us in the future.

Risks Related to Customer Concentration and Reliance on the U.S. E&P Market

9

In 2022, approximately 38% of our consolidated revenues were derived from our 20 largest customers, although no customer accounted for more than 10% of our consolidated revenues. While we are not dependent on any one customer or group of customers, the loss of one or more of our significant customers could have an adverse effect on our results of operations and cash flows. In addition, approximately 66% of our consolidated revenues in 2022 were derived from our U.S. operations, including approximately $400 million from the exploration and production market.

Over the past several years, the U.S. oil and natural gas market has experienced periods of significant declines which reduced the demand for our services and negatively impacted customer pricing in our U.S. operations. Due in part to these changes, our quarterly and annual operating results have fluctuated significantly and may continue to fluctuate in future periods. Because our business has substantial fixed costs, including significant facility and personnel expenses, downtime or low productivity due to reduced demand could have a material adverse effect on our business, financial condition, and results of operations.

While our continued expansion into a variety of non-E&P markets, the 2022 divestitures of the Excalibar U.S. mineral grinding business and Gulf of Mexico drilling fluids operations, as well as the geographic diversification into select foreign E&P markets, is intended to grow the business and reduce our dependency on the cyclical U.S. oil and natural gas market, these efforts may not be successful or sufficient to offset this volatility.

Risks Related to International Operations

We have significant operations outside of the U.S., including Canada and certain areas of Europe, the Middle East and Africa. In 2022, our international operations generated approximately 34% of consolidated revenues. Substantially all of our cash balance at December 31, 2022 resides within our international subsidiaries. Algeria represented our largest international market outside of North America, with our Algerian operations representing 7% of our consolidated revenues for 2022 and 7% of our total assets at December 31, 2022, including 24% of our total cash balance at December 31, 2022.

In addition, we may seek to expand to other areas outside the U.S. in the future. International operations are subject to a number of risks and uncertainties which could negatively impact our results from operations, including:

▪difficulties and cost associated with complying with a wide variety of complex foreign laws, treaties, and regulations;

▪uncertainties in or unexpected changes in regulatory environments or tax laws, including with respect to climate change;

▪legal uncertainties, timing delays, and expenses associated with tariffs, export licenses, and other trade barriers;

▪difficulties enforcing agreements and collecting receivables through foreign legal systems;

▪risks associated with failing to comply with the U.S. Foreign Corrupt Practices Act, the U.K. Bribery Act, export laws, and other similar laws applicable to our operations in international markets;

▪exchange controls or other limitations on international currency movements, including restrictions on the repatriation of funds to the U.S. from certain countries;

▪sanctions imposed by the U.S. government that prevent us from engaging in business in certain countries or with certain counter-parties;

▪expropriation or nationalization of assets;

▪inability to obtain or preserve certain intellectual property rights in the foreign countries in which we operate;

▪our inexperience in certain international markets;

▪health emergencies or pandemics (such as the COVID-19 pandemic);

▪fluctuations in foreign currency exchange rates;

▪political and economic instability; and

▪acts of terrorism.

In addition, several North African markets in which we operate, including Tunisia, Egypt, Libya, and Algeria have experienced social and political unrest in past years, which, when they occur, negatively impact our operating results and can include the temporary suspension of our operations.

Risks Related to the Ongoing Conflict Between Russia and Ukraine

Given the nature of our business and our global operations, the current conflict between Russia and Ukraine may adversely affect our business and results of operations. Although we do not have any operations in Russia or Ukraine, the broader consequences of this conflict, which may include sanctions, embargoes, supply chain disruptions, regional instability, and geopolitical shifts, and the extent of the conflict’s effect on our business and results of operations as well as the global economy, cannot be predicted.

10

The ongoing conflict may also have the effect of heightening many of the other risks specified in our Risk Factors or disclosed in our public filings, any of which could materially and adversely affect our business and results of operations. Such risks include, but are not limited to, the volatility of oil and natural gas prices that can adversely affect demand for our products and services; our customers’ activity levels, spending for our products and services, and ability to pay amounts owed us that could be impacted by the ability of our customers to access equity or credit markets; the price and availability of raw materials; the cost and continued availability of borrowed funds; and cybersecurity breaches or business system disruptions.

Risks Related to Operating Hazards Present in the Oil and Natural Gas and Utilities Industries and Substantial Liability Claims, Including Catastrophic Well Incidents

We are exposed to significant health, safety, and environmental risks. Our operations are subject to hazards present in the oil and natural gas industry, such as fires, explosions, blowouts, oil spills, and leaks or spills of hazardous materials (both onshore and offshore), as well as hazards in the electrical utility industry, such as exposure to wildfires, high voltage electrocution, among other risks. These incidents as well as accidents or problems in normal operations can cause personal injury or death and damage to property or the environment. From time to time, customers seek recovery for damage to their equipment or property that occurred during the course of our service obligations. Damage to our customers’ property and any related spills of hazardous materials could be extensive if a major problem occurs.

Generally, we rely on contractual indemnities, releases, limitations on liability with our customers, and insurance to protect us from potential liability related to such events. However, our insurance and contractual indemnification may not be sufficient or effective to protect us under all circumstances or against all risks. In addition, our customers’ changing views on risk allocation together with deteriorating market conditions could force us to accept greater risks to obtain new business or retain renewing business and could result in us losing business if we are not prepared to take such risks. Moreover, we may not be able to maintain insurance at levels of risk coverage or policy limits that we deem adequate. Any damages caused by our services or products that are not covered by insurance or contractual indemnification, or are in excess of policy limits or subject to substantial deductibles, could adversely affect our financial condition, results of operations, and cash flows. See “Risks Related to the Inherent Limitations of Insurance Coverage” below for additional information.

Risks Related to Contracts that Can Be Terminated or Downsized by Our Customers Without Penalty

Many of our fixed-term contracts contain provisions permitting early termination by the customer at their convenience, generally without penalty, and with limited notice requirements. In addition, many of our contracts permit our customers to decrease the products or services without penalty, which could result in a decrease in our revenues and profitability. As a result, you should not place undue reliance on the strength of our customer contracts or the terms of those contracts.

Risks Related to Product Offering and Market Expansion

As a key component of our long-term strategy to diversify our revenue streams generated from both operating segments, we seek to continue to expand our product and service offerings and enter new customer markets with our existing products. As with any market expansion effort, new customer and product markets require additional capital investment and include inherent uncertainties regarding customer expectations, industry-specific regulatory requirements, product performance, and customer-specific risk profiles. In addition, we likely will not have the same level of operational experience with respect to the new customer and product markets as will our competitors. As such, new market entry is subject to a number of risks and uncertainties, which could have an adverse effect on our business, financial condition, or results of operations.

Risks Related to Our Ability to Attract, Retain, and Develop Qualified Leaders, Key Employees, and Skilled Personnel

Our failure to attract, retain, and develop qualified leaders and key employees could have a material adverse effect on our business. In addition, all of our businesses are highly dependent on our ability to attract and retain highly-skilled product specialists, technical sales personnel, and service personnel. The market for qualified employees is extremely competitive. If we cannot attract and retain qualified personnel, our ability to compete effectively and grow our business will be severely limited. Also, a significant increase in wages paid by competing employers could result in a reduction in our skilled labor force or an increase in our operating costs.

We have experienced, and expect to continue to experience, a shortage of labor for certain functions, which has increased our labor costs and negatively impacted our profitability. The extent and duration of the effect of these labor market challenges are subject to numerous factors, including the availability of qualified persons in the markets where we and our contracted service providers operate and unemployment levels within these markets, behavioral changes, prevailing wage rates and other benefits, inflation, adoption of new or revised employment and labor laws and regulations (including increased

11

minimum wage requirements) or government programs, safety levels of our operations, and our reputation within the labor market.

Risks Related to Expanding Our Services in the Utilities Sector, Which May Require Unionized Labor

Although none of our employees are currently represented by labor unions, we may expand our services offered in the utilities sector, the customers of which may require unionized labor. If we, a subsidiary, or a business partner were to have a unionized workforce, we may be subject to strikes or work stoppages, wage and hour regulations, or other regulations associated with a collective bargaining agreement, which could adversely impact our relationships with our customers and cause us to lose business, and could result in an increase in our operating costs.

Risks Related to the Price and Availability of Raw Materials

Our ability to provide products and services to our customers is dependent upon our ability to obtain raw materials necessary to operate our business. Certain of the raw materials essential to our business are sourced globally and require various freight services to transport the materials to our job sites. These services may be impacted by periodic supply chain disruptions and, particularly during times of high demand, may cause delays in the arrival of or otherwise constrain our supply of raw materials. These constraints could have a material adverse effect on our business and consolidated results of operations. In addition, price increases, whether as a result of inflation, geopolitical issues, or otherwise, imposed by our vendors for raw materials used in our business and the inability to pass these increases through to our customers could have a material adverse effect on our business and results of operations.

Our Industrial Solutions business is highly dependent on the availability of high-density polyethylene (“HDPE”), which is the primary raw material used in the manufacture of our recyclable composite mats. The cost of HDPE increased significantly in 2021, and although these costs moderated somewhat in 2022, remain higher than recent years. Our costs can vary based on the energy costs of the producers of HDPE, demand for this material, and the capacity or operations of the plants used to make HDPE. We may not be able to increase our customer pricing to cover the cost increases that we have experienced, which could result in a reduction in future profitability.

In addition, our Fluids Systems business is highly dependent on the availability of barite, which is a naturally occurring mineral that constitutes a significant portion of our fluids systems. In connection with the sale of our U.S.-based mineral grinding business in the fourth quarter of 2022, we entered a four-year barite supply agreement for certain regions of our U.S. drilling fluids business. We also obtain barite and other materials used in the fluids business from various third-party suppliers. The availability and cost of barite ore is dependent on factors beyond our control, including transportation, political priorities, U.S. tariffs, and government-imposed export fees in the exporting countries, as well as the impact of weather and natural disasters. The future supply of barite ore from existing sources may be inadequate to meet the market demand, particularly during periods of increasing world-wide demand, which could ultimately restrict industry activity or our ability to meet our customers’ needs.

Risks Related to Inflation

Increases in the cost of wages, materials, parts, equipment and other operational components has the potential to adversely affect our results of operations, cash flows and financial position by increasing our overall cost structure, particularly if we are unable to achieve commensurate increases in the prices we charge our customers for our products and services. In addition, inflation has also resulted in higher interest rates, which could cause an increase in the cost of debt borrowing in the future, as well as supply chain shortages, an increase in the costs of labor, currency fluctuations and other similar effects.

Risks Related to Capital Investments, Business Acquisitions, and Joint Ventures

Our ability to successfully execute our business strategy will depend, among other things, on our ability to make capital investments, complete acquisitions, and enter joint ventures, which provide us with financial benefits. These investments, acquisitions, and joint ventures are subject to a number of risks and uncertainties, including:

▪incorrect assumptions regarding business activity levels or results from our capital investments, acquired operations, or assets;

▪insufficient revenues to offset liabilities assumed;

▪potential loss of significant revenue and income streams;

▪increased or unexpected expenses;

▪inadequate return of capital;

▪regulatory or compliance issues;

▪potential loss of key employees, customers, or suppliers of the acquired company;

▪the triggering of certain covenants in our debt agreements (including accelerated repayment);

12

▪unidentified issues not discovered in due diligence;

▪failure to complete a planned acquisition transaction or to successfully integrate the operations or management of any acquired businesses or assets in a timely manner;

▪diversion of management’s attention from existing operations or other priorities;

▪unanticipated disruptions to our business associated with the implementation of our enterprise-wide operational and financial system; and

▪delays in completion and cost overruns associated with large capital investments.

Any of the factors above could have an adverse effect on our business, financial condition, or results of operations. Additionally, the anticipated benefits of a capital investment, acquisition, or joint venture may not be realized fully or at all, or may take longer to realize than expected.

In addition, we may enter into joint ventures and other similar arrangements where control may be shared with unaffiliated third parties, or where we are not a controlling party. In such instances, we may have limited control over joint venture decisions and actions, which may have an impact on our business. If our joint venture partners fail to satisfactorily perform their joint venture obligations, the joint venture may be unable to adequately perform or deliver its contracted services. Under these circumstances, we may be required to make additional investments or provide additional services to ensure the adequate performance and delivery of the contracted services. These additional obligations could result in reduced profit and may impact our reputation in the industry. We may also be held to be jointly and severally liable for the obligations and liabilities of our joint venture partners.

Risks Related to Market Competition

We face competition and compete vigorously on product performance and/or price. Our competition in the North America Fluids Systems business and U.S. Industrial Solutions business is fragmented. Our competition in the international Fluids Systems business includes larger companies, such as Halliburton, Schlumberger, and Baker Hughes. These larger companies have broad product and service offerings in addition to their drilling and completion fluids, and at times, attempt to compete by offering discounts to customers to use multiple products and services, some of which we do not offer. The smaller regional competitors compete with us mainly on price and local relationships.

In the Industrial Solutions business, many competitors provide various forms of worksite access products and services. More recently, several competitors have begun marketing composite products to compete with our DURA-BASE matting system. While we believe the design and manufacturing quality of our products provide a differentiated value to our customers, many of our competitors seek to compete on pricing. In addition, certain patents related to our DURA-BASE matting system have expired, and competitors may begin offering mats that include features described in those patents. We have filed additional patent applications on improvements to the structure of, features of, and uses of the DURA-BASE matting system, but there is no assurance that our competitors will not be able to offer products that are similar to these improvements, features, or uses of the DURA-BASE matting system.

In addition, certain customer contracts are awarded through a competitive bidding process. The strong competition in our markets requires maintaining skilled personnel and investing in technology, and also puts pressure on profit margins. We do not obtain contracts from all of our bids and our inability to win bids at acceptable profit margins would adversely affect our business and results of operations.

Risks Related to Technological Developments and Intellectual Property

The market for our products and services requires technological developments that generate improvements in product performance or service delivery. If we are not successful in continuing to develop new products, enhancements, or improved service delivery that are accepted in the marketplace or that comply with industry standards, we could lose market share to competitors, which could have a material adverse effect on our results of operations and financial condition.

Our success can be affected by our development and implementation of new product designs and improvements, or software developments, and by our ability to protect and maintain critical intellectual property assets related to these developments. Although in many cases our products are not protected by any registered intellectual property rights, in other cases we rely on a combination of patents and trade secret laws to establish and protect this proprietary technology. While patent rights give the owner of a patent the right to exclude third parties from making, using, selling, and offering for sale the inventions claimed in the patents, they do not necessarily grant the owner of a patent the right to practice the invention claimed in a patent. It may also be possible for a third party to design around our patents. We do not have patents in every country in which we conduct business and our patent portfolio will not protect all aspects of our business. When patent rights expire, competitors are generally free to offer the technology and products that were covered by the patents. Additionally, the trade secret laws of some foreign countries may not protect our proprietary technology in the same manner as the laws of the United States.

13

We also protect our trade secrets by customarily entering into confidentiality and/or license agreements with our employees, customers and potential customers, and suppliers. Our rights in our confidential information, trade secrets, and confidential know-how will not prevent third parties from independently developing similar information. Publicly available information (such as information in expired patents, published patent applications, and scientific literature) can also be used by third parties to independently develop technology. We cannot provide assurance that this independently developed technology will not be equivalent or superior to our proprietary technology.

We may from time to time engage in expensive and time-consuming litigation to determine the enforceability, scope, and validity of our patent rights. In addition, we can seek to enforce our rights in trade secrets, or “know-how,” and other proprietary information and technology in the conduct of our business. However, it is possible that our competitors may infringe upon, misappropriate, violate or challenge the validity or enforceability of our intellectual property, and we may not be able to adequately protect or enforce our intellectual property rights in the future.

The tools, techniques, methodologies, programs, and components we use to provide our services may infringe upon the intellectual property rights of others. Infringement claims generally result in significant legal and other costs, and may distract management from running our business. Royalty payments under licenses from third parties, if applicable, could increase our costs. Additionally, developing non-infringing technologies could increase our costs. If a license were not available, we might not be able to continue providing a particular service or product, which could adversely affect our financial condition, results of operations and cash flows.

Risks Related to Severe Weather, Natural Disasters, and Seasonality

We have significant operations located in market areas around the world that are negatively impacted by severe adverse weather events or natural disasters, particularly the U.S. A potential result of climate change is more frequent or more severe weather events or natural disasters. To the extent such weather events or natural disasters become more frequent or severe, disruptions to our business and costs to repair damaged facilities could increase.

These severe weather events or natural disasters, such as excessive rains, hurricanes, fires, or droughts, could disrupt our operations and result in damage to our properties, including the manufacturing facilities and technology center for our Industrial Solutions business located in Carencro, Louisiana, or our leased fluids industrial space in Fourchon, Louisiana. Additionally, there are market areas around the world in which our operations are subject to seasonality such as Canada where the Spring “break-up” (an industry term used to describe the time of year when the frost comes out of the ground causing the earth to become soft and muddy and strict weight restrictions are implemented by the government to prevent potholes forming on roads) results in a significant slowdown in the oil and natural gas industry and our fluids business each year.

Severe weather, natural disasters, and seasonality could adversely affect our or our customers’ financial condition, results of operations and cash flows.

Risks Related to Public Health Crises, Epidemics, and Pandemics

The effects of public health crises, epidemics, and pandemics, such as the COVID-19 pandemic have resulted and may in the future result in a significant and swift reduction in U.S. and international economic activity, including adversely affecting the demand for and price of oil and natural gas, as well as the demand for our products and services. In response to reduced demand for our products and services, we would take (and have in the past taken) actions aimed at protecting our liquidity and reshaping the business for the new market realities, including reducing our workforce and cost structure. However, our business contains high levels of fixed costs, including significant facility and personnel expenses, which limits the effectiveness of such actions. The extent to which our operating and financial results are affected by a public health crisis, epidemic or pandemic will depend on various factors beyond our control, such as the duration and scope of such event, including any resurgences and the emergence and spread of a subject pathogen; actions taken by businesses and governments in response to such event; and the speed and effectiveness of responses to combat the subject pathogen, including the availability and public acceptance of effective treatments or vaccines, and how quickly and to what extent normal economic activity can resume, all of which are highly uncertain and cannot be predicted. Any such public health crisis, epidemic or pandemic could also materially and adversely impact our operating and financial results in a manner that is not currently known to us or that we do not currently consider as presenting material risks to our operations.

Indebtedness Risks

Risks Related to the Cost and Continued Availability of Borrowed Funds, including Risks of Noncompliance with Debt Covenants

We use borrowed funds as an integral part of our long-term capital structure and our future success is dependent upon continued access to borrowed funds to support our operations. The availability of borrowed funds on reasonable terms is dependent on the condition of credit markets and financial institutions from which these funds are obtained. Adverse events in the financial markets, or restrictions on lenders ability or willingness to lend to companies that have significant exposure to

14

customers in the oil and natural gas industry, may significantly reduce the availability of funds, which may have an adverse effect on our cost of borrowings and our ability to fund our business strategy. Our ability to meet our debt service requirements and the continued availability of funds under our existing or future loan agreements is dependent upon our ability to generate operating income and generate sufficient cash flow to remain in compliance with the covenants in our debt agreements. This, in turn, is subject to the volatile nature of the oil and natural gas industry, and to competitive, economic, financial, and other factors that are beyond our control.

We primarily fund our ongoing operational needs through a $175 million asset-based revolving credit agreement (the “Amended ABL Facility”). The Amended ABL Facility terminates in May 2027. Borrowing availability under the Amended ABL Facility is calculated based on eligible U.S. accounts receivable, inventory and composite mats included in the rental fleet, net of reserves and subject to limits on certain of the assets included in the borrowing base calculation. To the extent pledged by the borrowers, the borrowing base calculation also includes the amount of eligible pledged cash. The administrative agent may establish reserves in accordance with the Amended ABL Facility, in part based on appraisals of the asset base, and other limits in its discretion, which could reduce the amounts otherwise available under the Amended ABL Facility.

The Amended ABL Facility is a senior secured obligation of the Company and certain of our U.S. subsidiaries constituting borrowers thereunder, secured by a first priority lien on substantially all of the personal property and certain real property of the borrowers, including a first priority lien on certain equity interests of direct or indirect domestic subsidiaries of the borrowers and certain equity interests issued by certain foreign subsidiaries of the borrowers. The Amended ABL Facility contains certain financial covenants, customary representations, warranties and covenants that, among other things, and subject to certain specified circumstances and exceptions, restrict or limit the ability of the borrowers and certain of their subsidiaries to incur indebtedness (including guarantees), grant liens, make investments, pay dividends or distributions with respect to capital stock and make other restricted payments, make prepayments on certain indebtedness, engage in mergers or other fundamental changes, dispose of property, and change the nature of their business.

If we fail to comply with the various covenants and other requirements of the Amended ABL Facility, we would be in default thereunder, which would permit the holders of the indebtedness to accelerate the maturity thereof and proceed against their collateral. The acceleration of any of our indebtedness and the election to exercise any remedies could have a material adverse effect on our business and financial condition and we may not be able to make all of the required payments or borrow sufficient funds to refinance such indebtedness.

If we are unable to generate sufficient cash flows to repay our indebtedness when due or to fund our other liquidity needs, we may be required to adopt one or more alternatives, such as selling assets, restructuring debt or obtaining additional financing. Our ability to refinance our indebtedness will depend on the capital markets and our financial condition at such time. We may not be able to engage in any of these activities or engage in these activities on desirable terms, which could result in a default on our debt obligations and could have a material adverse effect on our business and financial condition.

Legal and Regulatory Risks

Risks Related to Environmental Laws and Regulations

We are responsible for complying with numerous federal, state, local, and foreign laws, regulations and policies that govern environmental protection, zoning and other matters applicable to our current and past business activities, including the activities of our former subsidiaries. Failure to remain compliant with these laws, regulations and policies may result in, among other things, fines, penalties, costs, investigation and/or cleanup of contaminated sites and site closure obligations, costs of remedying noncompliance, termination or suspension of certain operations, or other expenditures. We could be exposed to strict, joint and several liability for cleanup costs, natural resource damages and other damages as a result of our conduct that was lawful at the time it occurred or the conduct of, or conditions caused by, prior operators or other third parties. Private parties may also pursue legal actions against us based on alleged non-compliance with or liability under certain of these laws, rules and regulations. Further, any changes in the current legal and regulatory environment could impact industry activity and the demands for our products and services, the scope of products and services that we provide, or our cost structure required to provide our products and services, or the costs incurred by our customers.

Many of the markets for our products and services are dependent on the continued exploration for and production of fossil fuels (predominantly oil and natural gas). In recent years, the topic of climate change has received increased attention worldwide. Many scientists, legislators and others attribute climate change to increased levels of greenhouse gases, including carbon dioxide attributed to the use of fossil fuels, which has led to significant legislative and regulatory efforts to limit greenhouse gas emissions. The Environmental Protection Agency (the “EPA”) and other domestic and foreign regulatory agencies have adopted regulations that potentially limit greenhouse gas emissions and impose reporting obligations on large greenhouse gas emission sources. In addition, the EPA has adopted rules that could require the reduction of certain air emissions during exploration and production of oil and natural gas. President Biden’s administration officially reentered the U.S. into the Paris Agreement in February 2021 and committed the U.S. to reducing its greenhouse gas emissions by 50-52%

15

from 2005 levels by 2030. In November 2021, the U.S. and other countries entered into the Glasgow Climate Pact, which includes a range of measures designed to address climate change, including but not limited to the phase-out of fossil fuel subsidies, reducing methane emissions 30% by 2030, and cooperating toward the advancement of the development of clean energy. In August 2022, President Biden also signed into law the Inflation Reduction Act, which contains tax inducements and other provisions that incentivize investment, development, and deployment of alternative energy sources and technologies, which could increase operating costs within the oil and gas industry and accelerate the transition away from fossil fuels. To the extent that laws and regulations enacted as part of climate change legislation increase the costs of drilling for or producing such fossil fuels, limit or restrict oil and natural gas exploration and production, or reduce the demand for fossil fuels, such legislation could have a material adverse effect on our operations and profitability.

The continued expansion of revenues in industrial markets, and particularly end-markets that are likely to benefit from ongoing energy transition efforts around the world, such as power transmission, renewable energy, and geothermal, remains a strategic priority going forward, and we anticipate that our capital investments will primarily focus on supporting this objective. However, it is unclear whether these initiatives, when implemented, will create sufficient incentives for projects or result in increased demand for our services.

There have also been efforts in recent years to influence the investment community, including investment advisors and certain sovereign wealth, pension and endowment funds, promoting divestment of fossil fuel equities and pressuring lenders to limit funding to companies engaged in the extraction of fossil fuel reserves. Such environmental activism and initiatives aimed at limiting climate change and reducing air pollution could interfere with our business activities, operations, and ability to access capital. Furthermore, members of the investment community are increasing their focus on Environmental, Social, and Governance (“ESG”) practices and disclosures by public companies, and regulations have been proposed that may subject us to enhanced climate change reporting obligations. As a result, we may continue to face increasing pressure regarding our ESG disclosures and practices. If our ESG disclosures and practices do not meet investor or other stakeholder expectations and standards, which continue to evolve, it could have a material adverse effect on our business or demand for our services.

In addition, hydraulic fracturing is a common practice used by E&P operators to stimulate production of hydrocarbons, particularly from shale oil and natural gas formations in the U.S. The process of hydraulic fracturing, which involves the injection of sand (or other forms of proppants) laden fluids into oil and natural gas bearing zones, has come under increased scrutiny from a variety of regulatory agencies, including the EPA and various state authorities. Several states have adopted regulations requiring operators to identify the chemicals used in fracturing operations, others have adopted moratoriums on the use of fracturing, and the State of New York has banned the practice altogether. In addition, concerns have been raised about whether injection of waste associated with hydraulic fracturing operations, or from the fracturing operations themselves, may cause or increase the impact of earthquakes. Although we do not provide hydraulic fracturing services, we offer stimulation chemicals used in the hydraulic fracturing process. Regulations which have the effect of prohibiting, limiting the use, or significantly increasing the costs of hydraulic fracturing could have a material adverse effect on both the drilling and stimulation activity levels of our customers, and, therefore, the demand for our products and services.

Risks Related to Legal Compliance