Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-Q

(Mark One)

| x | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the quarterly period ended September 30, 2011

or

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission File Number 1-8462

GRAHAM CORPORATION

(Exact name of registrant as specified in its charter)

| DELAWARE | 16-1194720 | |

| (State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification No.) | |

| 20 Florence Avenue, Batavia, New York | 14020 | |

| (Address of principal executive offices) | (Zip Code) | |

585-343-2216

(Registrant’s telephone number, including area code)

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ¨ | Accelerated filer | x | |||

| Non-accelerated filer | ¨ (Do not check if a smaller reporting company) | Smaller reporting company | ¨ | |||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

As of October 31, 2011, there were outstanding 9,913,634 shares of the registrant’s common stock, par value $.10 per share.

Table of Contents

Graham Corporation and Subsidiaries

As of September 30, 2011 and March 31, 2011 and for the Three and Six-Month Periods

Ended September 30, 2011 and 2010

| Page | ||||||

| Part I. |

FINANCIAL INFORMATION | |||||

| Item 1. |

Unaudited Condensed Consolidated Financial Statements | 4 | ||||

| Item 2. |

Management’s Discussion and Analysis of Financial Condition and Results of Operations | 18 | ||||

| Item 3. |

Quantitative and Qualitative Disclosure About Market Risk | 29 | ||||

| Item 4. |

Controls and Procedures | 30 | ||||

| Part II. |

OTHER INFORMATION | |||||

| Item 2. |

Unregistered Sales of Equity Securities and Use of Proceeds | 31 | ||||

| Item 6. |

Exhibits | 31 | ||||

| 32 | ||||||

| 33 | ||||||

2

Table of Contents

GRAHAM CORPORATION AND SUBSIDIARIES

FORM 10-Q

September 30, 2011

3

Table of Contents

Item 1. Unaudited Condensed Consolidated Financial Statements

GRAHAM CORPORATION AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS AND RETAINED EARNINGS

(Unaudited)

| Three Months Ended September 30, |

Six Months Ended September 30, |

|||||||||||||||

| 2011 | 2010 | 2011 | 2010 | |||||||||||||

| (Amounts in thousands, except per share data) | ||||||||||||||||

| Net sales |

$ | 33,595 | $ | 15,723 | $ | 58,607 | $ | 29,074 | ||||||||

| Cost of products sold |

20,794 | 10,376 | 37,501 | 19,877 | ||||||||||||

| Cost of goods sold – amortization |

1 | — | 109 | — | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total cost of goods sold |

20,795 | 10,376 | 37,610 | 19,877 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Gross profit |

12,800 | 5,347 | 20,997 | 9,197 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Other expenses (income): |

||||||||||||||||

| Selling, general and administrative |

4,339 | 3,016 | 7,990 | 5,580 | ||||||||||||

| Amortization |

57 | 3 | 107 | 6 | ||||||||||||

| Interest income |

(15 | ) | (18 | ) | (36 | ) | (34 | ) | ||||||||

| Interest expense |

185 | 9 | 205 | 16 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total other expenses and income |

4,566 | 3,010 | 8,266 | 5,568 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Income before income taxes |

8,234 | 2,337 | 12,731 | 3,629 | ||||||||||||

| Provision for income taxes |

2,766 | 780 | 4,247 | 1,194 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Net income |

5,468 | 1,557 | 8,484 | 2,435 | ||||||||||||

| Retained earnings at beginning of period |

67,441 | 60,219 | 64,623 | 59,539 | ||||||||||||

| Dividends |

(198 | ) | (198 | ) | (396 | ) | (396 | ) | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Retained earnings at end of period |

$ | 72,711 | $ | 61,578 | $ | 72,711 | $ | 61,578 | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Per share data: |

||||||||||||||||

| Basic: |

||||||||||||||||

| Net income |

$ | .55 | $ | .16 | $ | .85 | $ | .25 | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Diluted: |

||||||||||||||||

| Net income |

$ | .55 | $ | .16 | $ | .85 | $ | .24 | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Weighted average common shares outstanding: |

||||||||||||||||

| Basic: |

9,968 | 9,937 | 9,954 | 9,929 | ||||||||||||

| Diluted: |

10,000 | 9,977 | 9,991 | 9,970 | ||||||||||||

| Dividends declared per share |

$ | .02 | $ | .02 | $ | .04 | $ | .04 | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

See Notes to Condensed Consolidated Financial Statements.

4

Table of Contents

GRAHAM CORPORATION AND SUBSIDIARIES

CONDENSED CONSOLIDATED BALANCE SHEETS

(Unaudited)

| September 30, 2011 |

March 31, 2011 |

|||||||

| (Amounts in thousands, except per share data) | ||||||||

| Assets |

||||||||

| Current assets: |

||||||||

| Cash and cash equivalents |

$ | 33,043 | $ | 19,565 | ||||

| Investments |

4,700 | 23,518 | ||||||

| Trade accounts receivable, net of allowances ($50 and $26 at September 30 and March 31, 2011, respectively) |

18,130 | 8,681 | ||||||

| Unbilled revenue |

14,130 | 14,280 | ||||||

| Inventories |

6,609 | 8,257 | ||||||

| Prepaid expenses and other current assets |

828 | 826 | ||||||

| Deferred income tax asset |

2,010 | 2,015 | ||||||

|

|

|

|

|

|||||

| Total current assets |

79,450 | 77,142 | ||||||

| Property, plant and equipment, net |

12,757 | 11,705 | ||||||

| Prepaid pension asset |

7,096 | 6,680 | ||||||

| Goodwill |

6,914 | 6,914 | ||||||

| Permits |

10,300 | 10,300 | ||||||

| Other intangible assets, net |

5,057 | 5,218 | ||||||

| Other assets |

110 | 112 | ||||||

|

|

|

|

|

|||||

| Total assets |

$ | 121,684 | $ | 118,071 | ||||

|

|

|

|

|

|||||

| Liabilities and stockholders’ equity |

||||||||

| Current liabilities: |

||||||||

| Current portion of capital lease obligations |

$ | 64 | $ | 47 | ||||

| Accounts payable |

6,335 | 9,948 | ||||||

| Accrued compensation |

5,073 | 4,580 | ||||||

| Accrued expenses and other current liabilities |

3,371 | 3,448 | ||||||

| Customer deposits |

9,702 | 12,854 | ||||||

| Income taxes payable |

2,276 | 1,772 | ||||||

|

|

|

|

|

|||||

| Total current liabilities |

26,821 | 32,649 | ||||||

| Capital lease obligations |

267 | 116 | ||||||

| Accrued compensation |

271 | 259 | ||||||

| Deferred income tax liability |

9,158 | 8,969 | ||||||

| Accrued pension liability |

232 | 234 | ||||||

| Accrued postretirement benefits |

909 | 892 | ||||||

| Other long-term liabilities |

1,459 | 1,297 | ||||||

|

|

|

|

|

|||||

| Total liabilities |

39,117 | 44,416 | ||||||

|

|

|

|

|

|||||

| Commitments and contingencies (Note 13) |

||||||||

| Stockholders’ equity: |

||||||||

| Preferred stock, $1.00 par value—Authorized, 500 shares |

||||||||

| Common stock, $.10 par value—Authorized, 25,500 shares Issued, 10,253 and 10,216 shares at September 30 and March 31, 2011, respectively |

$ | 1,025 | $ | 1,022 | ||||

| Capital in excess of par value |

16,883 | 16,322 | ||||||

| Retained earnings |

72,711 | 64,623 | ||||||

| Accumulated other comprehensive loss |

(4,830 | ) | (5,012 | ) | ||||

| Treasury stock (339 and 350 shares at September 30 and March 31, 2011, respectively) |

(3,222 | ) | (3,300 | ) | ||||

|

|

|

|

|

|||||

| Total stockholders’ equity |

82,567 | 73,655 | ||||||

|

|

|

|

|

|||||

| Total liabilities and stockholders’ equity |

$ | 121,684 | $ | 118,071 | ||||

|

|

|

|

|

|||||

See Notes to Condensed Consolidated Financial Statements.

5

Table of Contents

GRAHAM CORPORATION AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS

(Unaudited)

| Six Months Ended September 30, |

||||||||

| 2011 | 2010 | |||||||

| (Amounts in thousands) | ||||||||

| Operating activities: |

||||||||

| Net income |

$ | 8,484 | $ | 2,435 | ||||

| Adjustments to reconcile net income to net cash used by operating activities: |

||||||||

| Depreciation |

719 | 576 | ||||||

| Amortization |

216 | 6 | ||||||

| Amortization of unrecognized prior service cost and actuarial losses |

195 | 145 | ||||||

| Discount accretion on investments |

(4 | ) | (32 | ) | ||||

| Stock-based compensation expense |

320 | 184 | ||||||

| Gain (loss) on disposal of property, plant and equipment |

4 | (10 | ) | |||||

| Deferred income taxes |

174 | 156 | ||||||

| (Increase) decrease in operating assets: |

||||||||

| Accounts receivable |

(9,384 | ) | (1,847 | ) | ||||

| Unbilled revenue |

149 | (972 | ) | |||||

| Inventories |

1,629 | 2,109 | ||||||

| Prepaid expenses and other current and non-current assets |

(62 | ) | (259 | ) | ||||

| Prepaid pension asset |

(416 | ) | (388 | ) | ||||

| Increase (decrease) in operating liabilities: |

||||||||

| Accounts payable |

(3,727 | ) | 121 | |||||

| Accrued compensation, accrued expenses and other current and non-current liabilities |

764 | (864 | ) | |||||

| Customer deposits |

(3,171 | ) | (3,231 | ) | ||||

| Income taxes payable/receivable |

504 | (357 | ) | |||||

| Long-term portion of accrued compensation, accrued pension liability and accrued postretirement benefits |

27 | 33 | ||||||

|

|

|

|

|

|||||

| Net cash used by operating activities |

(3,579 | ) | (2,195 | ) | ||||

|

|

|

|

|

|||||

| Investing activities: |

||||||||

| Purchase of property, plant and equipment |

(1,494 | ) | (689 | ) | ||||

| Proceeds from disposal of property, plant and equipment |

4 | 14 | ||||||

| Purchase of investments |

(14,398 | ) | (114,888 | ) | ||||

| Redemption of investments at maturity |

33,220 | 120,920 | ||||||

|

|

|

|

|

|||||

| Net cash provided by investing activities |

17,332 | 5,357 | ||||||

|

|

|

|

|

|||||

| Financing activities: |

||||||||

| Principal repayments on capital lease obligations |

(38 | ) | (33 | ) | ||||

| Issuance of common stock |

66 | 104 | ||||||

| Dividends paid |

(396 | ) | (396 | ) | ||||

| Purchase of treasury stock |

(8 | ) | (721 | ) | ||||

| Excess tax deduction on stock awards |

72 | 52 | ||||||

|

|

|

|

|

|||||

| Net cash used by financing activities |

(304 | ) | (994 | ) | ||||

|

|

|

|

|

|||||

| Effect of exchange rate changes on cash |

29 | 42 | ||||||

|

|

|

|

|

|||||

| Net increase in cash and cash equivalents |

13,478 | 2,210 | ||||||

| Cash and cash equivalents at beginning of year |

19,565 | 4,530 | ||||||

|

|

|

|

|

|||||

| Cash and cash equivalents at end of year |

$ | 33,043 | $ | 6,740 | ||||

|

|

|

|

|

|||||

See Notes to Condensed Consolidated Financial Statements.

6

Table of Contents

GRAHAM CORPORATION AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

September 30, 2011 and 2010

(Unaudited)

(Amounts in thousands, except per share data)

NOTE 1 – BASIS OF PRESENTATION:

Graham Corporation’s (the “Company’s”) Condensed Consolidated Financial Statements include (i) its wholly-owned foreign subsidiary located in China at September 30, 2011 and March 31, 2011 and for the three and six months ended September 30, 2011 and 2010 and (ii) its wholly-owned domestic subsidiary located in Lapeer, Michigan at September 30, 2011 and March 31, 2011 and for the three and six months ended September 30, 2011. See Note 2. The Condensed Consolidated Financial Statements have been prepared in accordance with accounting principles generally accepted in the U.S. (“GAAP”) for interim financial information and the instructions to Form 10-Q and Rule 10-01 of Regulation S-X, each as promulgated by the Securities and Exchange Commission. The Company’s Condensed Consolidated Financial Statements do not include all information and notes required by GAAP for complete financial statements. The unaudited Condensed Consolidated Balance Sheet as of March 31, 2011 was derived from the Company’s audited Consolidated Balance Sheet as of March 31, 2011. For additional information, please refer to the consolidated financial statements and notes included in the Company’s Annual Report on Form 10-K for the fiscal year ended March 31, 2011 (“fiscal 2011”). In the opinion of management, all adjustments, including normal recurring accruals considered necessary for a fair presentation, have been included in the Company’s Condensed Consolidated Financial Statements.

The Company’s results of operations and cash flows for the three and six months ended September 30, 2011 are not necessarily indicative of the results that may be expected for the fiscal year ending March 31, 2012 (“fiscal 2012”).

NOTE 2 – ACQUISITION:

On December 14, 2010, the Company completed its acquisition of Energy Steel & Supply Co. (“Energy Steel”), a privately-owned nuclear code accredited fabrication and specialty machining company located in Lapeer, Michigan dedicated primarily to the nuclear power industry. The Company believes that this acquisition furthers its growth strategy through market and product diversification, broadens its offerings to the energy markets and strengthens its presence in the nuclear sector.

The transaction was accounted for under the acquisition method of accounting. Accordingly, the results of Energy Steel were included in the Company’s Consolidated Financial Statements from the date of acquisition. The purchase price was $17,899 in cash, subject to the adjustments described below.

7

Table of Contents

During the second quarter of fiscal 2012, the Company received $384 from the seller due to a reduction in purchase price based upon the final determination of the working capital acquired in accordance with the purchase agreement. The Company’s Condensed Consolidated Balance Sheet at March 31, 2011 was recast to reflect this adjustment to the purchase price and is included in the table below.

The purchase agreement also included a contingent earn-out, which ranges from $0 to $2,000, dependent upon Energy Steel’s earnings performance in calendar years 2011 and 2012. If achieved, the earn-out will be payable in fiscal 2012 and in the fiscal year ending March 31, 2013 (“fiscal 2013”). A liability of $1,498 was recorded on the acquisition date for the contingent earn-out and was treated as additional purchase price. Based on Energy Steel’s performance to date, the expected value of the earn out, including discounting the future payments back to September 30, 2011, has increased to $1,887. The Condensed Consolidated Statements of Operations for the three and six months ended September 30, 2011 includes $230 in selling, general and administrative expense and $159 in interest expense for this adjustment.

In addition, the Company and Energy Steel entered into a five-year lease agreement with ESSC Investments, LLC for Energy Steel’s manufacturing and office facilities located in Lapeer, Michigan, which lease includes an option to renew for an additional five-year term. The Company and Energy Steel also have an option to purchase the leased facility for $2,500 at any time during the first two years of the lease term. ESSC Investments, LLC is partly owned by the President and former sole shareholder of Energy Steel.

The cost of the acquisition was preliminarily allocated to the assets acquired and liabilities assumed based upon their estimated fair values at the date of the acquisition and the amount exceeding the fair value of $7,404 was recorded as goodwill, which is not deductible for tax purposes. During the second quarter of fiscal 2012, the allocation of the purchase price was finalized and the Company’s Condensed Consolidated Balance Sheet at March 31, 2011 was recast to reflect the adjustments. The following table presents the impact of the adjustments on individual line items in the Company’s Condensed Consolidated Balance Sheet at March 31, 2011:

| Balance Sheet Caption |

Before Adjustment of Final Allocation of Purchase Price |

Adjustment | After Adjustment of Final Allocation of Purchase Price |

|||||||||

| Prepaid expenses and other current assets |

$ | 424 | $ | 402 | $ | 826 | ||||||

| Deferred income tax asset |

$ | 1,906 | $ | 109 | $ | 2,015 | ||||||

| Goodwill |

$ | 7,404 | $ | (490 | ) | $ | 6,914 | |||||

| Accrued expenses and other current liabilities |

$ | (3,427 | ) | $ | (21 | ) | $ | (3,448 | ) | |||

8

Table of Contents

The following table summarizes the final allocation of the cost of the acquisition to the assets acquired and liabilities assumed as of the close of the acquisition:

| December 14, 2010 | ||||

| Assets acquired: |

||||

| Current assets |

$ | 2,954 | ||

| Property, plant & equipment |

1,295 | |||

| Backlog |

170 | |||

| Customer relationships |

2,700 | |||

| Tradename |

2,500 | |||

| Permits |

10,300 | |||

| Goodwill |

6,914 | |||

| Other assets |

14 | |||

|

|

|

|||

| Total assets acquired |

26,847 | |||

| Liabilities assumed: |

||||

| Current liabilities |

1,910 | |||

| Deferred income tax liability |

5,924 | |||

|

|

|

|||

| Total liabilities assumed |

7,834 | |||

|

|

|

|||

| Purchase price |

$ | 19,013 | ||

|

|

|

|||

The fair values of the assets acquired and liabilities assumed were determined using one of three valuation approaches: (i) market; (ii) income; and (iii) cost. The selection of a particular method for a given asset depended on the reliability of available data and the nature of the asset, among other considerations. The market approach, which estimates the value for a subject asset based on available market pricing for comparable assets, was utilized for work in process inventory. The income approach, which estimates the value for a subject asset based on the present value of cash flows projected to be generated by the asset, was used for certain intangible assets such as permits, tradename and backlog. The projected cash flows were discounted at a required rate of return that reflects the relative risk of the Energy Steel transaction and the time value of money. The projected cash flow for each asset considered multiple factors, including current revenue from existing customers, the competition-limiting effect of nuclear permits due to the significant time, effort and resources required to obtain them, and expected profit margins giving consideration to historical and expected margins. The cost approach was used for the majority of personal property, raw materials inventory and customer relationships. The cost to replace a given asset reflects the estimated replacement cost for the asset, less an allowance for loss in value due to depreciation or obsolescence, with specific consideration given to economic obsolescence if indicated.

The fair value of the work in process inventory acquired was estimated by applying a version of the market approach known as the comparable sales method. This approach estimates the fair value of the asset by calculating the potential sales generated from selling the inventory and subtracting from it the costs related to the sale of that inventory and a reasonable profit allowance. Based upon this methodology, the Company recorded the inventory acquired at fair value resulting in an increase in inventory of $196. During the six months ended September 30, 2011, the Company expensed as cost of sales $38 of the step-up value relating to the acquired inventory sold during the first quarter of fiscal 2012. As of September 30, 2011, there was $11 of inventory step-up value remaining in inventory to be expensed. Raw materials inventory was valued at replacement cost.

9

Table of Contents

The purchase price was allocated to specific intangible assets as follows:

| Fair

Value assigned |

Weighted average amortization period |

|||||||

| Intangibles subject to amortization |

||||||||

| Backlog |

$ | 170 | 6 months | |||||

| Customer relationships |

2,700 | 15 years | ||||||

|

|

|

|||||||

| $ | 2,870 | 14 years | ||||||

|

|

|

|||||||

| Intangibles not subject to amortization |

||||||||

| Permits |

$ | 10,300 | indefinite | |||||

| Tradename |

2,500 | indefinite | ||||||

|

|

|

|||||||

| $ | 12,800 | |||||||

|

|

|

|||||||

Backlog consists of firm purchase orders received from customers that had not yet entered production or were in production at the date of the acquisition. The fair value of backlog was computed as the present value of the expected sales attributable to backlog less the remaining costs to fulfill the backlog. The life was based upon the period of time in which the backlog is expected to be converted to sales.

Customer relationships represent the estimated fair value of customer relationships Energy Steel has with nuclear power plants as of the acquisition date. These relationships were valued using the replacement cost method based upon the cost to obtain and retain the limited number of customers in the nuclear power market. The Company determined that the estimated useful life of the intangible assets associated with the existing customer relationships is 15 years. This life was based upon historical customer attrition and management’s understanding of the industry and regulatory environment.

Nuclear permits are required and critical to generate substantially all of the revenue of Energy Steel, due to the strict regulatory environment of the nuclear industry. The permits are inherently valuable as a result of their competition-limiting effect due to the significant time, effort and resources required to obtain them. The Company intends to continually renew the permits and maintain all quality programs and processes, as well as abide by all required regulations of the nuclear industry, therefore, an indefinite life has been assigned to the permits. The permits will be tested annually for impairment. In the first quarter of fiscal 2012, the Company renewed the permits.

The tradename represents the estimated fair value of the corporate name acquired from Energy Steel which will be utilized by the Company in the future. The Company believes the use of the tradename, which the Company expects will be instrumental in enabling it to maintain or expand its market share, is inherently valuable. The Company currently intends to utilize the tradename for an indefinite period of time, therefore, the intangible asset is not being amortized but will be tested for impairment on an annual basis.

The excess of the purchase price over the fair value of net tangible and intangible assets acquired of $6,914 was allocated to goodwill. Various factors contributed to the establishment of goodwill, including the value of Energy Steel’s highly trained assembled workforce and management team and the expected revenue growth over time that is attributable to increased market penetration.

10

Table of Contents

NOTE 3 – REVENUE RECOGNITION:

The Company recognizes revenue on all contracts with a planned manufacturing process in excess of four weeks (which approximates 575 direct labor hours) using the percentage-of-completion method. The majority of the Company’s revenue is recognized under this methodology. The percentage-of-completion method is determined by comparing actual labor incurred to a specific date to management’s estimate of the total labor to be incurred on each contract. Contracts in progress are reviewed monthly, and sales and earnings are adjusted in current accounting periods based on revisions in the contract value and estimated costs at completion. Losses on contracts are recognized immediately when evident. There is no reserve for credit losses related to unbilled revenue recorded for contracts accounted for on the percentage-of-completion method. Any reserve for credit losses related to unbilled revenue is recorded as a reduction to revenue.

Revenue on contracts not accounted for using the percentage-of-completion method is recognized utilizing the completed contract method. The majority of the Company’s contracts have a planned manufacturing process of less than four weeks and the results reported under this method do not vary materially from the percentage-of-completion method. The Company recognizes revenue and all related costs on these contracts upon substantial completion or shipment to the customer. Substantial completion is consistently defined as at least 95% complete with regard to direct labor hours. Customer acceptance is generally required throughout the construction process and the Company has no further material obligations under its contracts after the revenue is recognized.

NOTE 4 – INVESTMENTS:

Investments consist solely of fixed-income debt securities issued by the U.S. Treasury with original maturities of greater than three months and less than one year. All investments are classified as held-to-maturity, as the Company has the intent and ability to hold the securities to maturity. The investments are stated at amortized cost which approximates fair value. All investments held by the Company at September 30, 2011 are scheduled to mature in October 2011.

NOTE 5 – INVENTORIES:

Inventories are stated at the lower of cost or market, using the average cost method. For contracts accounted for on the completed contract method, progress payments received are netted against inventory to the extent the payment is less than the inventory balance relating to the applicable contract. Progress payments that are in excess of the corresponding inventory balance are presented as customer deposits in the Condensed Consolidated Balance Sheets. Unbilled revenue in the Condensed Consolidated Balance Sheets represents revenue recognized that has not been billed to customers on contracts accounted for on the percentage-of-completion method. For contracts accounted for on the percentage-of–completion method, progress payments are netted against unbilled revenue to the extent the payment is less than the unbilled revenue for the applicable contract. Progress payments exceeding unbilled revenue are netted against inventory to the extent the payment is less than or equal to the inventory balance relating to the applicable contract, and the excess is presented as customer deposits in the Condensed Consolidated Balance Sheets.

11

Table of Contents

Major classifications of inventories are as follows:

| September

30, 2011 |

March

31, 2011 |

|||||||

| Raw materials and supplies |

$ | 2,119 | $ | 2,293 | ||||

| Work in process |

11,350 | 12,983 | ||||||

| Finished products |

535 | 543 | ||||||

|

|

|

|

|

|||||

| 14,004 | 15,819 | |||||||

| Less – progress payments |

7,395 | 7,562 | ||||||

|

|

|

|

|

|||||

| Total |

$ | 6,609 | $ | 8,257 | ||||

|

|

|

|

|

|||||

NOTE 6 – INTANGIBLE ASSETS:

Intangible assets are comprised of the following:

| Gross Carrying Amount |

Accumulated Amortization |

Net Carrying Amount |

||||||||||

| At September 30, 2011 |

||||||||||||

| Intangibles subject to amortization: |

||||||||||||

| Backlog |

$ | 170 | $ | 170 | $ | — | ||||||

| Customer relationships |

2,700 | 143 | 2,557 | |||||||||

|

|

|

|

|

|

|

|||||||

| $ | 2,870 | $ | 313 | $ | 2,557 | |||||||

|

|

|

|

|

|

|

|||||||

| Intangibles not subject to amortization: |

||||||||||||

| Permits |

$ | 10,300 | $ | — | $ | 10,300 | ||||||

| Tradename |

2,500 | — | 2,500 | |||||||||

|

|

|

|

|

|

|

|||||||

| $ | 12,800 | $ | — | $ | 12,800 | |||||||

|

|

|

|

|

|

|

|||||||

| At March 31, 2011 |

||||||||||||

| Intangibles subject to amortization: |

||||||||||||

| Backlog |

$ | 170 | $ | 99 | $ | 71 | ||||||

| Customer relationships |

2,700 | 53 | 2,647 | |||||||||

|

|

|

|

|

|

|

|||||||

| $ | 2,870 | $ | 152 | $ | 2,718 | |||||||

|

|

|

|

|

|

|

|||||||

| Intangibles not subject to amortization: |

||||||||||||

| Permits |

$ | 10,300 | $ | — | $ | 10,300 | ||||||

| Tradename |

2,500 | — | 2,500 | |||||||||

|

|

|

|

|

|

|

|||||||

| $ | 12,800 | $ | — | $ | 12,800 | |||||||

|

|

|

|

|

|

|

|||||||

Intangible assets are amortized on a straight line basis over their estimated useful lives. Intangible amortization expense for the three and six months ended September 30, 2011 was $45 and $161, respectively. Amortization expense for the three and six months ended September 30, 2010 was $0. As of September 30, 2011, amortization expense is estimated to be $90 for the remainder of fiscal 2012 and $180 in each of fiscal 2013, fiscal 2014, fiscal 2015 and fiscal 2016.

12

Table of Contents

NOTE 7 – STOCK-BASED COMPENSATION:

The Amended and Restated 2000 Graham Corporation Incentive Plan to Increase Shareholder Value provides for the issuance of up to 1,375 shares of common stock in connection with grants of incentive stock options, non-qualified stock options, stock awards and performance awards to officers, key employees and outside directors; provided, however, that no more than 250 shares of common stock may be used for awards other than stock options. Stock options may be granted at prices not less than the fair market value at the date of grant and expire no later than ten years after the date of grant.

There were no stock option awards granted in the three months ended September 30, 2011 and 2010. Stock option awards granted in the six months ended September 30, 2011 and 2010 were 9 and 20, respectively. The stock option awards vest 33 1/3% per year over a three-year term. All stock options have a term of ten years from their grant date.

Restricted stock awards granted in the three-month periods ended September 30, 2011 and 2010 were 1 and 0, respectively. Restricted stock awards granted in the six-month periods ended September 30, 2011 and 2010 were 28 and 24, respectively. Performance-vested restricted stock awards granted to officers in fiscal 2012 and fiscal 2011 vest 100% on the third anniversary of the grant date, subject to the satisfaction of the performance metrics established for the applicable three-year period. Time-vested restricted stock awards granted to officers in fiscal 2012 vest 50% on the second anniversary of the grant date and 50% on the fourth anniversary of the grant date. Time-vested restricted stock awards granted to directors in fiscal 2012 and fiscal 2011 vest 100% on the first anniversary of the grant date.

During the three and six months ended September 30, 2011, the Company recognized stock-based compensation costs related to stock option and restricted stock awards of $173 and $290, respectively. The income tax benefit recognized related to stock-based compensation was $62 and $103 for the three and six months ended September 30, 2011, respectively. During the three and six months ended September 30, 2010, the Company recognized stock-based compensation costs related to stock option and restricted stock awards of $125 and $184, respectively. The income tax benefit recognized related to stock-based compensation was $43 and $63 for the three and six months ended September 30, 2010, respectively.

On July 29, 2010, the Company’s stockholders approved the Graham Corporation Employee Stock Purchase Plan (the “ESPP”), which allows eligible employees to purchase shares of the Company’s common stock on the last day of a six-month offering period at a purchase price equal to the lesser of 85 percent of the fair market value of the common stock on either the first day or the last day of the offering period. A total of 200 shares of common stock may be purchased under the ESPP. During the three and six months ended September 30, 2011, the Company recognized stock-based compensation costs of $12 and $30, respectively, related to the ESPP and $4 and $10, respectively, of related tax benefits.

NOTE 8 – INCOME PER SHARE:

Basic income per share is computed by dividing net income by the weighted average number of common shares outstanding for the period. Common shares outstanding include share equivalent

13

Table of Contents

units, which are contingently issuable shares. Diluted income per share is calculated by dividing net income by the weighted average number of common shares outstanding and, when applicable, potential common shares outstanding during the period. A reconciliation of the numerators and denominators of basic and diluted income per share is presented below:

| Three Months Ended September 30, |

Six Months Ended September 30, |

|||||||||||||||

| 2011 | 2010 | 2011 | 2010 | |||||||||||||

| Basic income per share |

||||||||||||||||

| Numerator: |

||||||||||||||||

| Net income |

$ | 5,468 | $ | 1,557 | $ | 8,484 | $ | 2,435 | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Denominator: |

||||||||||||||||

| Weighted common shares outstanding |

9,913 | 9,877 | 9,896 | 9,871 | ||||||||||||

| Share equivalent units (“SEUs”) |

55 | 60 | 58 | 58 | ||||||||||||

| Weighted average common shares and SEUs |

9,968 | 9,937 | 9,954 | 9,929 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Basic income per share |

$ | .55 | $ | .16 | $ | .85 | $ | .25 | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Diluted income per share |

||||||||||||||||

| Numerator: |

||||||||||||||||

| Net income |

$ | 5,468 | $ | 1,557 | $ | 8,484 | $ | 2,435 | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Denominator: |

||||||||||||||||

| Weighted average shares and SEUs outstanding |

9,968 | 9,937 | 9,954 | 9,929 | ||||||||||||

| Stock options outstanding |

31 | 40 | 36 | 41 | ||||||||||||

| Contingently issuable SEUs |

1 | — | 1 | — | ||||||||||||

| Weighted average common and potential common shares outstanding |

10,000 | 9,977 | 9,991 | 9,970 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Diluted income per share |

$ | .55 | $ | .16 | $ | .85 | $ | .24 | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

Options to purchase a total of 24 and 61 shares of common stock were outstanding at September 30, 2011 and 2010, respectively, but were not included in the above computation of diluted income per share as they would be anti-dilutive upon issuance given their exercise prices.

NOTE 9 – PRODUCT WARRANTY LIABILITY:

The reconciliation of the changes in the product warranty liability is as follows:

| Three Months Ended September 30, |

Six Months Ended September 30, |

|||||||||||||||

| 2011 | 2010 | 2011 | 2010 | |||||||||||||

| Balance at beginning of period |

$ | 217 | $ | 335 | $ | 202 | $ | 369 | ||||||||

| Expense for product warranties |

40 | 120 | 73 | 150 | ||||||||||||

| Product warranty claims paid |

(18 | ) | (24 | ) | (36 | ) | (88 | ) | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Balance at end of period |

$ | 239 | $ | 431 | $ | 239 | $ | 431 | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

14

Table of Contents

The product warranty liability is included in the line item “Accrued expenses and other liabilities” in the Condensed Consolidated Balance Sheets.

NOTE 10 – CASH FLOW STATEMENT:

Interest paid was $6 and $2 for the six-month periods ended September 30, 2011 and 2010, respectively. In addition, income taxes paid for the six months ended September 30, 2011 and 2010 were $3,488 and $1,297, respectively.

During the six months ended September 30, 2011 and 2010, stock option awards were exercised and restricted stock awards vested. In connection with such stock option exercises and vesting, the related income tax benefit realized exceeded the tax benefit that had been recorded pertaining to the compensation cost recognized by $72 and $52, respectively, for such periods. This excess tax deduction has been separately reported under “Financing activities” in the Condensed Consolidated Statements of Cash Flows.

At September 30, 2011 and 2010, there were $81 and $20 of capital purchases that were recorded in accounts payable and are not included in the caption “Purchase of property, plant and equipment” in the Condensed Consolidated Statements of Cash Flows. In the three months ended September 30, 2011 and 2010, capital expenditures totaling $205 and $0, respectively, were financed through the issuance of capital leases.

NOTE 11 – COMPREHENSIVE INCOME:

Total comprehensive income was as follows:

| Three Months Ended | Six Months Ended | |||||||||||||||

| September 30, | September 30, | |||||||||||||||

| 2011 | 2010 | 2011 | 2010 | |||||||||||||

| Net income |

$ | 5,468 | $ | 1,557 | $ | 8,484 | $ | 2,435 | ||||||||

| Other comprehensive income: |

||||||||||||||||

| Foreign currency translation adjustment |

29 | 33 | 56 | 43 | ||||||||||||

| Defined benefit pension and other postretirement plans |

63 | 50 | 126 | 96 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total comprehensive income |

$ | 5,560 | $ | 1,640 | $ | 8,666 | $ | 2,574 | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

Defined benefit pension and other postretirement plans reflect the amortization of prior service costs and recognized gains and losses related to such plans during the periods.

15

Table of Contents

NOTE 12 – EMPLOYEE BENEFIT PLANS:

The components of pension income are as follows:

| Three Months Ended | Six Months Ended | |||||||||||||||

| September 30, | September 30, | |||||||||||||||

| 2011 | 2010 | 2011 | 2010 | |||||||||||||

| Service cost |

$ | 115 | $ | 96 | $ | 230 | $ | 192 | ||||||||

| Interest cost |

355 | 335 | 710 | 670 | ||||||||||||

| Expected return on assets |

(678 | ) | (625 | ) | (1,356 | ) | (1,250 | ) | ||||||||

| Amortization of: |

||||||||||||||||

| Unrecognized prior service cost |

1 | 1 | 2 | 2 | ||||||||||||

| Actuarial loss |

129 | 106 | 258 | 211 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Net pension income |

$ | (78 | ) | $ | (87 | ) | $ | (156 | ) | $ | (175 | ) | ||||

|

|

|

|

|

|

|

|

|

|||||||||

The Company made no contributions to its defined benefit pension plan during the six months ended September 30, 2011 and does not expect to make any contributions to the plan for the balance of fiscal 2012.

The components of the postretirement benefit income are as follows:

| Three Months Ended | Six Months Ended | |||||||||||||||

| September 30, | September 30, | |||||||||||||||

| 2011 | 2010 | 2011 | 2010 | |||||||||||||

| Service cost |

$ | — | $ | — | $ | — | $ | — | ||||||||

| Interest cost |

11 | 9 | 22 | 24 | ||||||||||||

| Amortization of prior service cost |

(42 | ) | (42 | ) | (83 | ) | (83 | ) | ||||||||

| Amortization of actuarial loss |

9 | 10 | 18 | 15 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Net postretirement benefit income |

$ | (22 | ) | $ | (23 | ) | $ | (43 | ) | $ | (44 | ) | ||||

|

|

|

|

|

|

|

|

|

|||||||||

The Company paid benefits of $5 related to its postretirement benefit plan during the three months ended September 30, 2011. The Company expects to pay benefits of approximately $102 for the balance of fiscal 2012.

NOTE 13 –COMMITMENTS AND CONTINGENCIES:

The Company has been named as a defendant in certain lawsuits alleging personal injury from exposure to asbestos contained in products made by the Company. The Company is a co-defendant with numerous other defendants in these lawsuits and intends to vigorously defend itself against these claims. The claims are similar to previous asbestos suits that named the Company as defendant, which either were dismissed when it was shown that the Company had not supplied products to the plaintiffs’ places of work or were settled for amounts below the expected defense costs. The outcome of these lawsuits cannot be determined at this time.

16

Table of Contents

From time to time in the ordinary course of business, the Company is subject to legal proceedings and potential claims. At September 30, 2011, other than noted above, management was unaware of any other material litigation matters.

NOTE 14 – INCOME TAXES:

The Company files federal and state income tax returns in several domestic and international jurisdictions. In most tax jurisdictions, returns are subject to examination by the relevant tax authorities for a number of years after the returns have been filed. The Company is currently under examination by the U.S. Internal Revenue Service (the “IRS”) for tax years 2009 and 2010. The IRS has completed its examination for tax years 2006 through 2008. In June 2010, the IRS proposed an adjustment, plus interest, to disallow substantially all of the research and development tax credit claimed by the Company in tax years 2006 through 2008. The Company filed a protest to appeal the adjustment in July 2010. In August 2011, the IRS proposed an adjustment, plus interest, to disallow all of the research and development tax credit claimed by the Company in tax years 2009 and 2010. The Company plans to file a protest to appeal the adjustment. The Company believes its tax position is correct and will continue to take appropriate actions to vigorously defend its position.

The cumulative tax benefit related to the research and development tax credit for the tax years ended March 31, 1999 through March 31, 2011 was $2,381. The liability for unrecognized tax benefits related to this tax position was $477 at September 30 and March 31, 2011, which represents management’s estimate of the potential resolution of this issue. Any additional impact on the Company’s income tax liability cannot be determined at this time. The tax benefit and liability for unrecognized tax benefits were recorded in the Company’s Consolidated Statement of Operations as follows:

| Year Ended March 31, | ||||||||||||||||||||||||

| 2007 | 2008 | 2009 | 2010 | 2011 | Total | |||||||||||||||||||

| Tax benefit of research and development tax credit |

$ | 1,653 | $ | 218 | $ | 238 | $ | 135 | $ | 137 | $ | 2,381 | ||||||||||||

| Unrecognized tax benefit |

— | — | — | (445 | ) | (32 | ) | (477 | ) | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Net tax benefit of research and development tax credit |

$ | 1,653 | $ | 218 | $ | 238 | $ | (310 | ) | $ | 105 | $ | 1,904 | |||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

The Company is subject to examination in state and international tax jurisdictions for tax years 2007 through 2010 and tax years 2008 through 2010, respectively. It is the Company’s policy to recognize any interest related to uncertain tax positions in interest expense and any penalties related to uncertain tax positions in selling, general and administrative expense. The Company had one additional unrecognized tax benefit of $888 as of September 30 and March 31, 2011. During the three months ended September 30, 2011 and 2010, the Company recorded $23 and $8, respectively, for interest related to its uncertain tax positions. During the six months ended September 30, 2011 and 2010, the Company recorded $40 and $14, respectively, for interest related to its uncertain tax positions. No penalties related to uncertain tax positions were recorded in the three- or six-month periods ended September 30, 2011 or 2010.

17

Table of Contents

Item 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations

(Dollar amounts in thousands, except per share data)

Overview

We are a global designer and manufacturer of custom-engineered ejectors, vacuum systems, condensers, liquid ring pump packages and heat exchangers to the refining and petrochemical industries, and a nuclear code accredited supplier of components and raw materials to the nuclear power generating market. Our equipment is used in critical applications in the petrochemical, oil refining and electric power generation industries, including nuclear, cogeneration and geothermal plants. Our equipment can also be found in alternative energy, including ethanol, biodiesel and coal and gas-to-liquids, and other diverse applications, such as metal refining, pulp and paper processing, shipbuilding, water heating, refrigeration, desalination, soap manufacturing, food processing, pharmaceuticals, and heating, ventilating and air conditioning.

Our corporate offices are located in Batavia, New York and we have production facilities in both Batavia, New York and at our wholly-owned subsidiary, Energy Steel & Supply Co., located in Lapeer, Michigan. We also have a wholly-owned foreign subsidiary, Graham Vacuum and Heat Transfer Technology (Suzhou) Co., Ltd., located in Suzhou, China, which supports sales orders from China and provides engineering support and supervision of subcontracted fabrication.

On December 14, 2010, we acquired Energy Steel to advance our strategy to diversify our products and broaden our offerings to the energy industry. This transaction was accounted for under the acquisition method of accounting. Accordingly, the results of Energy Steel were included in our consolidated financial statements and comparisons to our prior fiscal year will be enhanced by the inclusion of Energy Steel in this fiscal year’s results.

Highlights

Highlights for the three and six months ended September 30, 2011 (the fiscal year ending March 31, 2012 is referred to as “fiscal 2012”) include:

| • | Net sales for the second quarter of fiscal 2012 were $33,595, an increase of 114% compared with $15,723 for the second quarter of the fiscal year ended March 31, 2011, referred to as “fiscal 2011.” Net sales for the second quarter of fiscal 2012 included $7,212 attributable to Energy Steel. |

| • | Net sales for the first six months of fiscal 2012 were $58,607, up 102% compared with net sales of $29,074 for the first six months of fiscal 2011. Net sales for the first six months of fiscal 2012 included $11,077 attributable to Energy Steel. |

| • | Net income and income per diluted share for the second quarter of fiscal 2012 were $5,468 and $0.55, compared with net income of $1,557 and income per diluted share of $0.16 for the second quarter of fiscal 2011. |

| • | Net income and income per diluted share for the first six months of fiscal 2012 were $8,484 and $0.85, respectively, compared with net income of $2,435 and income per diluted share of $0.24 for the first six months of fiscal 2011. |

| • | Orders booked in the second quarter of fiscal 2012 were $23,464, up 124% compared with the second quarter of fiscal 2011, when orders were $10,476. Orders in the second quarter of fiscal 2012 included $4,264 attributable to Energy Steel. |

18

Table of Contents

| • | Orders booked in the first six months of fiscal 2012 were $42,507, up 129% compared with the first six months of fiscal 2011, when orders were $18,600. Orders in the first six months of fiscal 2012 included $9,442 attributable to Energy Steel. |

| • | Backlog decreased to $75,094 at September 30, 2011, representing a 12% decrease compared with June 30, 2011, when our backlog was $85,199. Included in backlog at September 30, 2011 was $6,763 associated with Energy Steel. |

| • | Gross profit margin and operating margin for the second quarter of fiscal 2012 were 38% and 25% compared with 34% and 15%, respectively, for the second quarter of fiscal 2011. |

| • | Gross profit margin and operating margin for the first six months of fiscal 2012 were 36% and 22% compared with 32% and 12%, respectively, for the second quarter of fiscal 2011. |

| • | Cash and short-term investments at September 30, 2011 were $37,743 compared with $43,083 at March 31, 2011. |

Forward-Looking Statements

This report and other documents we file with the Securities and Exchange Commission include “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended.

These statements involve known and unknown risks, uncertainties and other factors that may cause actual results to be materially different from any future results implied by the forward-looking statements. Such factors include, but are not limited to, the risks and uncertainties identified by us under the heading “Risk Factors” in Item 1A of our Annual Report on Form 10-K for fiscal 2011.

Forward-looking statements may also include, but are not limited to, statements about:

| • | the current and future economic environments affecting us and the markets we serve; |

| • | expectations regarding investments in new projects by our customers; |

| • | sources of revenue and anticipated revenue, including the contribution from the growth of new products, services and markets; |

| • | plans for future products and services and for enhancements to existing products and services; |

| • | our operations in foreign countries; |

| • | our ability to integrate our acquisition of Energy Steel and continue to pursue our acquisition and growth strategy; |

| • | our ability to expand nuclear power work into new markets; |

| • | estimates regarding our liquidity and capital requirements; |

| • | timing of conversion of backlog to sales; |

| • | our ability to attract or retain customers; |

| • | the outcome of any existing or future litigation; and |

| • | our ability to increase our productivity and capacity. |

19

Table of Contents

Forward-looking statements are usually accompanied by words such as “anticipate,” “believe,” “estimate,” “may,” “intend,” “expect” and similar expressions. Actual results could differ materially from historical results or those implied by the forward-looking statements contained in this report.

Undue reliance should not be placed on our forward-looking statements. Except as required by law, we undertake no obligation to update or announce any revisions to forward-looking statements contained in this report, whether as a result of new information, future events or otherwise.

Fiscal 2012 and the Near-Term Market Conditions

The downturn in the global economy which commenced in fiscal year ending March 31, 2008 led to reduced demand for petroleum-based products, which in turn led our customers to defer investment in major capital projects. We have seen an improved business environment over the past four quarters, compared with 12 to 18 months ago, and believe that we are in the early stages of a business recovery. While there continues to be uncertainty as to whether a sustained global economic recovery is occurring, we believe current signs are more positive than a year ago.

In addition, we believe that the significant increase in construction costs, including raw material costs, which had occurred over the four-to-five-year period prior to the recent downturn, also led to delays in new commitments by our customers. The increase in costs resulted in the economics of projects becoming less feasible. While some material costs have improved, others continue to be volatile.

Near-term demand trends that we believe are affecting our customers’ investments include:

| • | As the world recovers slowly from the global recession, many emerging economies continue to have relatively strong economic growth. This expansion is driving growing energy requirements and the need for more refined petroleum products. Although uncertainty in the capital and sovereign debt markets continues, there has been some improved access to capital, which has resulted in certain previously stalled projects being released. |

| • | The expansion of the economies of oil producing Middle Eastern countries, their desire to extract greater value from their oil and gas resources, and the continued growth in demand for oil and refined products has renewed investment activity in that region. We do not believe that the recent political unrest in the Middle East has impacted our business. Moreover, the planned timeline of refinery projects in the major Middle Eastern countries is encouraging. |

| • | Asia, specifically China, is experiencing renewed demand for refined petroleum products such as gasoline. This renewed demand is driving increased investment in petrochemical and refining projects. |

| • | South America, specifically Brazil, Venezuela and Colombia, is seeing increased refining and petrochemical investments that are driven by their expanding economies and increased local demand for gasoline and other products that are made from oil as the feedstock. |

| • | The U.S. refining market has recently exhibited improvement, including near-term increases in orders of short cycle and spare parts. Historically, these types of orders have suggested a recovery, as delayed spending is released. We expect that the U.S. refining markets will not return to the levels experienced during the last up cycle, but |

20

Table of Contents

| will improve compared with its levels over the past few years. We expect that the U.S. refining markets will continue to be an important aspect of our business. We are beginning to see renewed signs of planned investments to convert greater percentages of crude oil to transportation fuels, such as revamping distillation columns to extract residual higher-value components from the low-value waste stream. We are also seeing renewed investment to expand the flexibility of facilities to allow them to utilize multiple feedstocks. |

| • | Investments, including foreign investments, in North American oil sands projects have recently increased, especially for extraction projects in Alberta. Such investments suggest that downstream spending involving our equipment might increase in the next one to three years. |

| • | Investment in new nuclear power capacity may become subject to increased uncertainty due to political and social pressures, enhanced by the tragic earthquake and tsunami which occurred in Japan in March 2011. However, the need for additional safety and back up redundancies at existing plants could increase demand for Energy Steel’s products in the near-term. We are also continuing to see investment in existing U.S. nuclear plants to extend their operating life. |

We expect that the consequences of these near-term trends, and specifically projected expansion in petrochemical and oil refining that will most likely occur outside of North America, primarily in the growing Asian and South American markets, will result in more pressure on our pricing and gross margins, as these markets historically provided lower margins than North American refining markets.

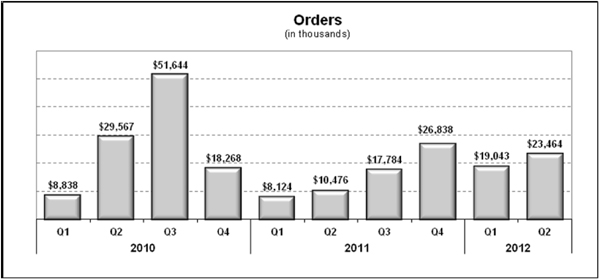

Because of continued global economic and financial uncertainty and the risk associated with growth in emerging economies, we also expect that we will have continued volatility in our order pattern. We continue to expect our new order levels to remain volatile, resulting in both strong and weak quarters. As the chart below indicates, quarterly orders can vary significantly.

We believe that looking at our order level in any one quarter does not provide an accurate indication of our future expectations or performance. Rather, we believe that looking at our orders and backlog over a rolling four-quarter time period provides a better measure of our business. For the next several quarters, we also expect to see smaller value projects than what we saw during the beginning of the last expansion cycle. This will require more orders for us to achieve a similar revenue level and will adversely impact our ability to realize margin gains through volume leverage.

21

Table of Contents

Mix Shift: Expected Stronger International Growth in Refining and Chemical Processing with Domestic Growth in Nuclear Power and U.S. Navy Projects

We expect growth in the refining and chemical processing markets to be driven by emerging markets. We have also expanded our addressable markets through the acquisition of Energy Steel and our focus on U.S. Navy nuclear propulsion projects. We believe our revenue opportunities during the coming years will be equivalent between the domestic and international markets.

Over the long-term, we expect our customers’ markets to regain their strength and, while remaining cyclical, continue to grow. We believe the long-term trends remain strong and that the drivers of future growth include:

Demand Trends

| • | Global consumption of crude oil is estimated to expand significantly over the next two decades, primarily in emerging markets. This is expected to offset estimated flat to slightly declining demand in North America and Europe. |

| • | Global oil refining capacity is projected to increase, and is expected to be addressed through new facilities, refinery upgrades, revamps and expansions. |

| • | Increased demand is expected for power, refinery and petrochemical products, stimulated by an expanding middle class in Asia and the Middle East. |

| • | Increased development of geothermal electrical power plants in certain regions is expected to address projected growth in demand for electrical power. |

| • | Increased global regulations over the refining, petrochemical and nuclear power industries are expected to continue to drive requirements for capital investments. |

| • | Increased number of refineries converting to use heavier, more readily available and lower cost crude oil as a feedstock is expected. |

| • | Increased focus on safety and redundancy is anticipated in existing nuclear power facilities. |

| • | Long-term increased project development of international nuclear facilities is expected, despite the recent tragedy in Japan. |

| • | Construction of new petrochemical plants in the Middle East, where natural gas is plentiful and less expensive, is expected to continue. |

| • | Increased investments in new power projects are expected in Asia and South America to meet projected consumer demand increases. |

| • | Long-term growth potential is believed to exist in alternative energy markets, such as geothermal, coal-to-liquids, gas-to-liquids and other emerging technologies, such as biodiesel, ethanol and waste-to-energy. |

22

Table of Contents

| • | Shale gas development and the resulting availability of affordable natural gas as feedstock to U.S.-based chemical/petrochemical facilities is expected to lead to renewed investment in chemical/petrochemical facilities in the U.S. |

We believe that all of the above factors offer us long-term growth opportunities to meet our customers’ expected capital project needs. In addition, we believe we can continue to grow our less cyclical smaller product lines and aftermarket businesses.

Emerging markets that require petroleum-based products are expected to continue to grow at rates faster than the U.S. However, because of our access to the nuclear power industry as a result of the Energy Steel acquisition and our expanding market penetration with the U.S. Navy, we believe the domestic and international markets will offer similar opportunities for us in the near term. Our domestic sales as a percentage of aggregate product sales, which had increased from 50% in our fiscal year ended March 31, 2007 to 54% in our fiscal year ended March 31, 2008 to 63% in our fiscal year ended March 31, 2009, decreased to 45% in each of our fiscal years ended March 31, 2010 and fiscal 2011, and was at 50% in the first six months of fiscal 2012.

Results of Operations

For an understanding of the significant factors that influenced our performance, the following discussion should be read in conjunction with our condensed consolidated financial statements and the notes to our condensed consolidated financial statements included in Part I, Item 1, of this Quarterly Report on Form 10-Q.

The following table summarizes our results of operations for the periods indicated:

| Three Months

Ended September 30, |

Six Months

Ended September 30, |

|||||||||||||||||

| 2011 | 2010 | 2011 | 2010 | |||||||||||||||

| Net sales |

$ | 33,595 | $ | 15,723 | $ | 58,607 | $ | 29,074 | ||||||||||

| Net income |

$ | 5,468 | $ | 1,557 | $ | 8,484 | $ | 2,435 | ||||||||||

| Diluted income per share |

$ | 0.55 | $ | 0.16 | $ | 0.85 | $ | 0.24 | ||||||||||

| Total assets |

$ | 121,684 | $ | 107,048 | $ | 121,684 | $ | 107,048 | ||||||||||

The Second Quarter and First Six Months of Fiscal 2012 Compared With the Second Quarter and First Six Months of Fiscal 2011

Sales for the second quarter of fiscal 2012 were $33,595, a 114% increase as compared with sales of $15,723 for the second quarter of fiscal 2011. The increase in the current quarter’s sales was due to higher volume in the majority of our product lines and the benefit of the acquisition of the Energy Steel business, which was purchased in December 2010 and contributed $7,212 in sales for the quarter. Organic growth in the second quarter of fiscal 2012 was $10,660, or 68%, compared with the second quarter of fiscal 2011. International sales year-over-year increased $7,636, or 93%, driven by stronger sales to the Middle East, Asia and Canada. Domestic sales increased $10,236, or 136%, in the second quarter of fiscal 2012 compared with the second quarter of fiscal 2011. Approximately two thirds of this growth was due to the addition of the Energy Steel business. Sales in the three months ended September 30, 2011 were 36% to the refining industry, 12% to the chemical and petrochemical industries, 31% to the power industry, including the nuclear market and 21% to other commercial and industrial applications. Sales in the three months ended September 30, 2010 were 34% to the refining industry, 32% to the chemical and petrochemical industries, 15%

23

Table of Contents

to the power industry, and 19% to other commercial and industrial applications. Fluctuations in sales among products and geographic locations can vary measurably from quarter-to-quarter based on timing and magnitude of projects. For additional information on future sales and our markets, see “Orders and Backlog” below.

Sales for the first six months of fiscal 2012 were $58,607, an increase of 102% compared with sales of $29,074 for the first six months of fiscal 2011. The increase in year-to-date sales was due to higher demand in all product lines. The addition of Energy Steel contributed $11,077, or 38% of the increase, in sales compared with the first six months of fiscal 2011. International sales accounted for 50% and 55% of total sales for the first six months of fiscal 2012 and fiscal 2011, respectively. International sales year-over-year increased $13,580, or 85%. Due to the production of a large refinery project, $9,499 or 70%, of the total increase in international sales came from the Middle East. The remaining sales increase came from Asia, South America and Canada. Domestic sales increased $15,953, or 122%, in the six months ended September 30, 2011 compared with the six months ended September 30, 2010. Nearly 70% of the total increase in domestic sales is attributable to Energy Steel. Sales in the first six months of fiscal 2012 were 42% to the refining industry, 12% to the chemical and petrochemical industries, 27% to the power industry, including the nuclear market and 19% to other commercial and industrial applications. Sales in the first six months of fiscal 2011 were 30% to the refining industry, 35% to the chemical and petrochemical industries, 12% to the power industry, and 23% to other commercial and industrial applications. For additional information on future anticipated sales and our markets, see “Orders and Backlog” below.

Our gross profit margin for the second quarter of fiscal 2012 was 38% compared with 34% for the second quarter of fiscal 2011. Gross profit for the second quarter of fiscal 2012 increased to $12,800 from $5,347, or 139%, compared with the same period in fiscal 2011. Thirty nine percent of the total increase in gross profit, or $2,913, was due to the addition of Energy Steel. Higher organic volume and facility utilization, as well as conversion of certain refining projects provided the remaining gross profit gain.

Our gross profit margin for the first six months of fiscal 2012 was 36% compared with 32% for the first six months of fiscal 2011. Gross profit dollars for the first six months of fiscal 2012 increased 128% to $20,997 compared with the same period in fiscal 2011, which had gross profit of $9,197. As with the most recent three months, the addition of Energy Steel provided 35% of the total increase, or $4,094, with higher organic volume and facility utilization, as well as conversion of certain refining projects having provided the remaining gross profit gain.

Selling, general and administrative (“SG&A”) expense in the three and six-month periods ended September 30, 2011 increased $1,323, or 44%, and $2,410, or 43%, respectively, compared with the same periods of the prior year. Half of the increase for both the three and six-month periods was organic and due to increased headcount and higher variable costs related to higher sales and income. The remaining portion of the added SG&A costs was due to the addition of Energy Steel. Included in SG&A was a $230 charge related to the revaluation of the expected value of the earn-out from the Energy Steel acquisition (described in more detail below).

SG&A expense as a percent of sales for the three- and six-month periods ended September 30, 2011 was 13% and 14%, respectively. This compared with 19% for the both periods ended September 30, 2010. SG&A expense as a percent of sales decreased, with spending increasing at a much lower rate than sales increased.

Interest income was $15 and $36 for the three and six-month periods ended September 30, 2011, compared with $18 and $34 for the same periods ended September 30, 2010. The low level

24

Table of Contents

of interest income relative to the amount of cash invested reflects the persistent low level of interest rates on short term U.S. government securities.

Interest expense was $185 and $205 for the three and six-month periods ended September 30, 2011, up from $9 and $16 for the same periods ended September 30, 2010. The majority of the increase, $159, which occurred in the second quarter of fiscal 2011 was related to the revaluation of the expected value of the earn-out from the Energy Steel acquisition (described below).

The acquisition of Energy Steel included the opportunity for the seller to achieve an earn-out of up to $2,000 based on the profitability of the business in calendar years 2011 and 2012. At the time of acquisition, we were required to estimate the likelihood of the earn-out being achieved and then discount the expected payouts, which would occur in January 2012 and January 2013, back to the date of acquisition. At the time of acquisition, we expected a significant portion of the earn-out would be achieved. Uncertainty regarding the amount of the earn-out that would be achieved, combined with the discounting of the payments to the date of acquisition, yielded an expected earn-out present value of $1,498 (compared with the potential payout of $2,000). Based on Energy Steel’s performance to date, the expected value of the $2,000 earn-out, including discounting the January 2012 and 2013 payments back to September 30, 2011, has now increased to $1,887. The increase in expected value was recorded in the Condensed Consolidated Statement of Operations in the second quarter of fiscal 2012: $230 of such increase was recorded in SG&A and the remaining $159 in Interest Expense.

Our effective tax rate in fiscal 2012 is projected to be between 33% and 35%, which represents the tax rate used to reflect income tax expense in the current quarter, which was 34%, and the tax rate for the first six months of fiscal 2012, which was 33%. The actual annual effective tax rate for fiscal 2011 was 33%.

Net income for the three and six months ended September 30, 2011 was $5,468 and $8,484, respectively, compared with $1,557 and $2,435, respectively, for the same periods in the prior fiscal year. Income per diluted share in fiscal 2012 was $0.55 and $0.85 for the three and six-month periods, compared with $0.16 and $0.24 for the same periods of fiscal 2011.

Liquidity and Capital Resources

The following discussion should be read in conjunction with our condensed consolidated statements of cash flows:

| September 30, | March 31, | |||||||

| 2011 | 2011 | |||||||

| Cash and investments |

$ | 37,743 | $ | 43,083 | ||||

| Working capital |

$ | 52,629 | $ | 44,493 | ||||

| Working capital ratio(1) |

3.0 | 2.4 | ||||||

| 1) | Working capital ratio equals current assets divided by current liabilities. |

Net cash used by operating activities for the first six months of fiscal 2012 was $3,579, compared with $2,195 used by operating activities for the first six months of fiscal 2011. The cash usage primarily came from three areas: (i) an increase in accounts receivable, $9,384 (compared with an increase of $1,847 for the same period last year); (ii) a decrease in accounts payable, $3,727 (compared with a small increase, $121, for the same period last year); and (iii) a decrease in customer deposits of $3,171 (similar to the $3,231 decrease in the first six months of the last fiscal year). We believe the increase in accounts receivable, coupled with a high unbilled revenue level, while primarily driven by increased sales, is artificially high and should reduce over the remaining two quarters of fiscal 2012. Partly offsetting these items, is an increase in net income of $8,484, compared with $2,435 in the same period last year.

25

Table of Contents

Dividend payments and capital expenditures in the first six months of fiscal 2012 were $396 and $1,494, respectively, compared with $396 and $689, respectively, for the first six months of fiscal 2011.

Capital expenditures for fiscal 2012 are expected to be between $3,000 and $3,500. Over 85% of our fiscal 2012 capital expenditures are expected to be for machinery and equipment, with the remaining amounts to be used for information technology and other items.

Cash and investments were $37,743 on September 30, 2011 compared with $43,083 on March 31, 2011, down 12%. As a result of the increase in accounts receivable in the first six months of fiscal 2012, as projects are completed and shipped to customers, we expect cash and investments to increase over the next quarter or two.

We invest net cash generated from operations in excess of cash held for near-term needs in either a money market account or in U.S. government instruments, generally with maturity periods of up to 180 days. Our money market account is used to securitize our outstanding letters of credit and allows us to pay a lower cost on those letters of credit.

Our revolving credit facility with Bank of America, N.A. provides us with a line of credit of $25,000, including letters of credit and bank guarantees. In addition, the agreement allows us to increase the line of credit, at our discretion, up to another $25,000, for total availability of $50,000. Borrowings under our credit facility are secured by all of our assets. Letters of credit outstanding under our credit facility on September 30, 2011 and March 31, 2011 were $15,396 and $13,751, respectively. There were no other amounts outstanding on our credit facility at September 30, 2011 and March 31, 2011. Our borrowing rate as of September 30 and March 31, 2011 was Bank of America’s prime rate, or 3.25%. Availability under the line of credit was $9,604 at September 30, 2011. We believe that cash generated from operations, combined with our investments and available financing capacity under our credit facility, will be adequate to meet our cash needs for the foreseeable future.

Orders and Backlog

Orders for the three month period ended September 30, 2011 were $23,464, compared with $10,476 for the same period last year, an increase of 124%. Organic growth represented $8,724 of the increase, or 83%, with the remaining $4,264 coming from Energy Steel. For the three months ended September 30, 2011, orders increased in chemical and petrochemical, up $9,118, power, up $5,388 (with $4,264 attributable to Energy Steel), and other up $1,578. These were partially offset by lower refining orders, down $3,096. Orders represent communications received from customers requesting us to supply products and services.

During the first six months of fiscal 2012, orders were $42,507, compared with $18,600 for the same period of fiscal 2011, an increase of 129%. Organic growth accounted for $14,465, or 61% of the growth, with Energy Steel accounting for the remaining $9,442. For the first six months of fiscal 2012, orders increased in power, up $12,301 (with $9,442 attributable to Energy Steel), chemical and petrochemical, up $8,708, other up $1,675 and refining, up $1,223.