2024-03-31

DEUTSCHE DWS STATE TAX-FREE INCOME SERIES

0000714287

false

2024-07-25

2024-08-01

2024-08-01

N-1A

485BPOS

0.0991

0.0272

0.0024

0.0470

0.0007

0.0711

0.0439

0.0098

0.1073

0.0572

0000714287

ddstfis:ClassesACSMember

ddstfis:S000033433Member

2024-08-01

2024-08-01

0000714287

ddstfis:ClassesACSMember

ddstfis:S000033433Member

ddstfis:C000102799Member

2024-08-01

2024-08-01

0000714287

ddstfis:ClassesACSMember

ddstfis:S000033433Member

ddstfis:C000102801Member

2024-08-01

2024-08-01

0000714287

ddstfis:ClassesACSMember

ddstfis:S000033433Member

ddstfis:C000223772Member

2024-08-01

2024-08-01

0000714287

ddstfis:ClassesACSMember

ddstfis:S000033433Member

ddstfis:C000102802Member

2024-08-01

2024-08-01

0000714287

ddstfis:ClassesACSMember

ddstfis:S000033433Member

rr:RiskLoseMoneyMember

2024-08-01

2024-08-01

0000714287

ddstfis:ClassesACSMember

ddstfis:S000033433Member

rr:RiskNotInsuredDepositoryInstitutionMember

2024-08-01

2024-08-01

0000714287

ddstfis:ClassesACSMember

ddstfis:S000033433Member

ddstfis:RiskInterestRateMember

2024-08-01

2024-08-01

0000714287

ddstfis:ClassesACSMember

ddstfis:S000033433Member

ddstfis:RiskCreditMember

2024-08-01

2024-08-01

0000714287

ddstfis:ClassesACSMember

ddstfis:S000033433Member

ddstfis:RiskMunicipalSecuritiesMember

2024-08-01

2024-08-01

0000714287

ddstfis:ClassesACSMember

ddstfis:S000033433Member

ddstfis:RiskMarketMember

2024-08-01

2024-08-01

0000714287

ddstfis:ClassesACSMember

ddstfis:S000033433Member

ddstfis:RiskMarketDisruptionMember

2024-08-01

2024-08-01

0000714287

ddstfis:ClassesACSMember

ddstfis:S000033433Member

ddstfis:RiskInflationMember

2024-08-01

2024-08-01

0000714287

ddstfis:ClassesACSMember

ddstfis:S000033433Member

ddstfis:RiskTaxMember

2024-08-01

2024-08-01

0000714287

ddstfis:ClassesACSMember

ddstfis:S000033433Member

ddstfis:RiskPrivateActivityIDBsMember

2024-08-01

2024-08-01

0000714287

ddstfis:ClassesACSMember

ddstfis:S000033433Member

rr:RiskNondiversifiedStatusMember

2024-08-01

2024-08-01

0000714287

ddstfis:ClassesACSMember

ddstfis:S000033433Member

ddstfis:RiskSecuritySelectionMember

2024-08-01

2024-08-01

0000714287

ddstfis:ClassesACSMember

ddstfis:S000033433Member

ddstfis:RiskForwardCommitmentMember

2024-08-01

2024-08-01

0000714287

ddstfis:ClassesACSMember

ddstfis:S000033433Member

ddstfis:RiskCounterpartyMember

2024-08-01

2024-08-01

0000714287

ddstfis:ClassesACSMember

ddstfis:S000033433Member

ddstfis:RiskLiquidityMember

2024-08-01

2024-08-01

0000714287

ddstfis:ClassesACSMember

ddstfis:S000033433Member

ddstfis:RiskPrepaymentMember

2024-08-01

2024-08-01

0000714287

ddstfis:ClassesACSMember

ddstfis:S000033433Member

ddstfis:RiskPricingMember

2024-08-01

2024-08-01

0000714287

ddstfis:ClassesACSMember

ddstfis:S000033433Member

ddstfis:RiskOperationalAndTechnologyMember

2024-08-01

2024-08-01

0000714287

ddstfis:ClassesACSMember

ddstfis:S000033433Member

ddstfis:C000102799Member

ddstfis:beforetaxMember

2024-08-01

2024-08-01

0000714287

ddstfis:ClassesACSMember

ddstfis:S000033433Member

ddstfis:C000102799Member

ddstfis:AftertaxondistributionsMember

2024-08-01

2024-08-01

0000714287

ddstfis:ClassesACSMember

ddstfis:S000033433Member

ddstfis:C000102799Member

ddstfis:AftertaxondistributionsandsaleoffundsharesMember

2024-08-01

2024-08-01

0000714287

ddstfis:ClassesACSMember

ddstfis:S000033433Member

ddstfis:C000102801Member

ddstfis:beforetaxMember

2024-08-01

2024-08-01

0000714287

ddstfis:ClassesACSMember

ddstfis:S000033433Member

ddstfis:C000102802Member

ddstfis:beforetaxMember

2024-08-01

2024-08-01

0000714287

ddstfis:ClassesACSMember

ddstfis:S000033433Member

ddstfis:BloombergMunicipalBondIndexMember

2024-08-01

2024-08-01

0000714287

ddstfis:ClassesACSMember

ddstfis:S000033433Member

ddstfis:BloombergMassachusettsExemptMunicipalBondIndexMember

2024-08-01

2024-08-01

0000714287

ddstfis:ClassesACSMember

ddstfis:S000033433Member

ddstfis:C000223772Member

ddstfis:beforetaxMember

2024-08-01

2024-08-01

0000714287

ddstfis:ClassesACSMember

ddstfis:S000033433Member

ddstfis:C000223772Member

ddstfis:BloombergMunicipalBondIndexMember

2024-08-01

2024-08-01

0000714287

ddstfis:ClassesACSMember

ddstfis:S000033433Member

ddstfis:C000223772Member

ddstfis:BloombergMassachusettsExemptMunicipalBondIndexMember

2024-08-01

2024-08-01

0000714287

2024-08-01

2024-08-01

xbrli:pure

iso4217:USD

Filed electronically with the Securities and Exchange

Commission on July 25, 2024

1933 Act File No. 002-81549

1940 Act File No. 811-03657

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D. C. 20549

FORM N-1A

| REGISTRATION STATEMENT UNDER THE

SECURITIES |

|

| ACT OF 1933 |

|X|

|

| Pre-Effective Amendment No. |

|__| |

| Post-Effective Amendment No. 100 |

|X| |

| and/or |

|

| REGISTRATION STATEMENT UNDER THE |

|

| INVESTMENT COMPANY ACT OF 1940 |

|X| |

| |

|

| Amendment No. 100 |

|

Deutsche

DWS State Tax-Free Income Series

(Exact Name of Registrant as Specified in Charter)

875 Third

Avenue, New York, NY 10022-6225

(Address of Principal Executive Offices)

Registrant's Telephone Number, including Area

Code: (212) 454-4500

John Millette

Vice President and Secretary

Deutsche DWS State Tax-Free Income Series

100 Summer

Street, Boston, MA 02110-2146

(Name and Address of Agent for Service)

Copy to:

John S. Marten

Vedder Price P.C.

222 N. LaSalle Street, Chicago, Illinois 60601-1104

It is proposed that this filing will become effective (check appropriate

box):

| |__| |

Immediately upon filing pursuant to paragraph (b) |

| |X | |

On August 1, 2024 pursuant to paragraph (b) |

| |__| |

60 days after filing pursuant to paragraph (a) |

| |__| |

On ________________ pursuant to paragraph (a) |

| |__| |

75 days after filing pursuant to paragraph (a)(2) |

| |__| |

On ________________ pursuant to paragraph (a)(2) of Rule 485 |

If appropriate, check the following box:

| |__| |

This post-effective amendment designates a new effective

date for a previously filed post-effective amendment. |

EXPLANATORY

NOTE

This Post-Effective Amendment contains the Prospectus and Statement

of Additional Information relating to the following series and classes of shares of the Registrant:

- DWS Massachusetts Tax-Free Fund – Class A, Class C, Institutional

Class, and Class S

This Post-Effective Amendment is not intended to update or amend any other

Prospectuses or Statements of Additional Information of the Registrant’s other series or classes.

DWS Massachusetts Tax-Free Fund |

|

|

|

|

|

|

|

|

|

|

As with all mutual funds, the Securities and Exchange Commission (SEC) does not approve or disapprove these shares or determine whether the information in this prospectus is truthful or complete. It is a criminal offense for anyone to inform you otherwise.

Your investment in the fund is not a bank deposit and is not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency, entity or person.

DWS Massachusetts Tax-Free Fund

Investment Objective

The fund seeks income that is exempt from Massachusetts personal and federal income taxes.

These are the fees and expenses you may pay when you buy, hold and sell shares. You may pay other fees, such as brokerage commissions and other fees to financial intermediaries, which are not reflected in the tables and examples below.You may qualify for sales charge discounts in Class A shares if you and your immediate family invest, or agree to invest in the future, at least $100,000 in DWS funds. More information about these and other discounts and waivers is available from your financial representative and in Choosing a Share Class (p. 16), Sales Charge Waivers and Discounts Available Through Intermediaries (Appendix B, p. 42) and Purchase and Redemption of Shares in the fund’s Statement of Additional Information (SAI) (p. II-15).

SHAREHOLDER FEES (paid directly from your investment)

|

|

|

|

|

|

Maximum sales charge (load) imposed on

purchases, as % of offering price |

|

|

|

|

Maximum deferred sales charge (load), as

% of redemption proceeds1

|

|

|

|

|

Account Maintenance Fee (annually, for

fund account balances below $10,000 and

subject to certain exceptions) |

|

|

|

|

ANNUAL FUND OPERATING EXPENSES

(expenses that you pay each year as a % of the value of your investment)

|

|

|

|

|

|

|

|

|

|

|

|

Distribution/service (12b-1) fees |

|

|

|

|

|

|

|

|

|

|

Total annual fund operating expenses |

|

|

|

|

Fee waiver/expense reimbursement |

|

|

|

|

Total annual fund operating expenses

after fee waiver/expense reimbursement |

|

|

|

|

1Investments of $250,000 or more may be eligible to buy Class A shares without a sales charge (load), but may be subject to a contingent deferred sales charge of 1.00% if redeemed within 12 months of the original purchase date.

The Advisor has contractually agreed through July 31, 2025 to waive its fees and/or reimburse fund expenses to the extent necessary to maintain the fund’s total annual operating expenses (excluding certain expenses such as extraordinary expenses, taxes, brokerage, interest expense and acquired fund fees and expenses) at ratios no higher than 0.85%, 1.60%, 0.60% and 0.60% for Class A, Class C, Institutional Class and Class S, respectively. The agreement may only be terminated with the consent of the fund’s Board.

This Example is intended to help you compare the cost of investing in the fund with the cost of investing in other mutual funds. The Example assumes that you invest $10,000 in the fund for the time periods indicated and then redeem all of your shares at the end of those periods. The Example also assumes that your investment has a 5% return each year and that the fund's operating expenses (including one year of capped expenses in each period)

remain the same. Class C shares generally convert automatically to Class A shares after 8 years. The information presented in the Example for Class C reflects the conversion of Class C shares to Class A shares after 8 years. See “Class C Shares” in the “Choosing a Share Class” section

| Prospectus August 1, 2024 | 1 | DWS Massachusetts Tax-Free Fund |

of the prospectus for more information. Although your actual costs may be higher or lower, based on these assumptions your costs would be:

You would pay the following expenses if you did not redeem your shares:

The fund pays transaction costs, such as commissions, when it buys and sells securities (or “turns over” its portfolio). A higher portfolio turnover may indicate higher transaction costs and may mean higher taxes if you are investing in a taxable account. These costs are not reflected in annual fund operating expenses or in the expense example, and can affect the fund's performance. During the most recent fiscal year, the fund’s portfolio turnover rate was 52% of the average value of its portfolio.

Principal Investment Strategies

Main investments. Under normal circumstances, the fund invests at least 80% of net assets, plus the amount of any borrowings for investment purposes, in Massachusetts municipal securities. For purposes of this 80% requirement, Massachusetts municipal securities are securities whose income is exempt from regular federal and Massachusetts state income taxes. The fund can also invest in obligations of US territories and Commonwealths (such as Puerto Rico, the US Virgin Islands and Guam) and their agencies and authorities, whose income is free from regular federal and Massachusetts state income tax. The fund may invest up to 20% of net assets in securities whose income is subject to the federal alternative minimum tax (AMT).

The fund can buy many types of municipal securities with no maturity restrictions. These may include, without limitation, revenue bonds (which are backed by revenues from a particular source) and general obligation bonds (which are typically backed by the issuer’s ability to levy taxes). They may also include private activity and industrial development bonds, pre-refunded bonds, municipal lease obligations and investments representing an interest therein.

The fund normally invests at least 80% of total assets in municipal securities of the top four grades of credit quality or, if unrated, determined by the fund’s investment advisor to be of similar quality. The fund could invest up to 20% of total assets in high yield, below investment-grade bonds (commonly referred to as “junk” bonds), which are those rated below the fourth highest rating category (i.e., grade BB/Ba and below). Compared to investment-grade bonds, junk bonds generally pay higher yields but have higher volatility and higher risk of default on payments.

The fund may use forward delivery bonds, which are bonds priced on a determined date but that are not issued and settled until a later period (ranging from several weeks to more than a year). Forward delivery bonds with settlement dates greater than 35 days are treated as derivatives by the fund and are subject to the fund's policies and procedures with respect to derivatives. Forward delivery bonds with settlement dates greater than 35 days generally are used for non-hedging purposes to seek to enhance potential gains.

Management process. Portfolio management looks for securities that appear to offer the best total return potential. In making buy and sell decisions, portfolio management typically weighs a number of factors, including economic outlooks, possible interest rate movements, yield levels across varying maturities, and changes in supply and demand within the municipal bond market. When evaluating any individual security and its issuer, portfolio management may consider a number of factors including the security's credit quality and terms, such as coupon, maturity date and call date, as well as the issuer's capital structure, leverage and ability to meet its current obligations. Portfolio management may also consider financially material environmental, social, and governance (ESG) factors. Such factors may include, but are not limited to, exposure to climate change risks, income levels and unemployment data, and an issuer’s governance structure and practices.

Although portfolio management may adjust the fund’s duration (a measure of sensitivity to interest rates) over a wider range, they generally intend to keep it similar to that of the Bloomberg Municipal Bond Index, which is generally between five and nine years.

There are several risk factors that could hurt the fund’s performance, cause you to lose money or cause the fund’s performance to trail that of other investments. The fund may not achieve its investment objective, and is not intended to be a complete investment program. An investment in the fund is not a deposit of a bank and is not insured or guaranteed by the Federal Deposit Insurance Corporation or any other governmental agency.

Interest rate risk. When interest rates rise, prices of debt securities generally decline. The longer the duration of the fund’s debt securities, the more sensitive the fund will

Prospectus August 1, 2024

2

DWS Massachusetts Tax-Free Fund

be to interest rate changes. (As a general rule, a 1% rise in interest rates means a 1% fall in value for every year of duration.) When interest rates change, the values of longer-duration municipal bonds usually change more than the values of shorter-duration municipal bonds. Conversely, municipal bonds with shorter durations or maturities will be less volatile but may provide lower returns than municipal bonds with longer durations or maturities. Rising interest rates also may lengthen the duration of municipal bonds with call features, since exercise of the call becomes less likely as interest rates rise, which in turn will make the securities more sensitive to changes in interest rates and result in even steeper price declines in the event of further interest rate increases. Interest rates can change in response to the supply and demand for credit, government and/or central bank monetary policy and action, inflation rates, and other factors. Recent and potential future changes in monetary policy made by central banks or governments are likely to affect the level of interest rates. Changing interest rates may have unpredictable effects on markets, may result in heightened market volatility and potential illiquidity and may detract from fund performance to the extent the fund is exposed to such interest rates and/or volatility. Rising interest rates could cause the value of the fund’s investments — and therefore its share price as well — to decline. A rising interest rate environment may cause investors to move out of fixed-income securities and related markets on a large scale, which could adversely affect the price and liquidity of such securities and could also result in increased redemptions from the fund. Increased redemptions from the fund may force the fund to sell investments at a time when it is not advantageous to do so, which could result in losses. Beginning in 2022, the US Federal Reserve (“Fed”) raised interest rates significantly in response to increased inflation. It is unclear if and when the Fed may begin to implement interest rate cuts, if rates will remain at current levels for a prolonged period or, if the Fed deems necessary in response to certain economic developments such as a turnaround in the decline of inflation, the Fed may consider additional rate increases. As a result, fixed-income and related markets may experience heightened levels of volatility and liquidity risk.

Credit risk. The fund's performance could be hurt if an issuer of a debt security suffers an adverse change in financial condition that results in the issuer not making timely payments of interest or principal, a security downgrade or an inability to meet a financial obligation. Credit risk is greater for lower-rated securities.

Because the issuers of high yield debt securities, or junk bonds (debt securities rated below the fourth highest credit rating category), may be in uncertain financial health, the prices of their debt securities can be more vulnerable to bad economic news, or even the expectation of bad news, than investment-grade debt securities. Credit risk for high yield securities is greater than for higher-rated securities.

Because securities in default generally have missed one or more payments of interest and/or principal, an investment in such securities has an increased risk of loss. Issuers of securities in default have an increased likelihood of entering bankruptcy or beginning liquidation procedures which could impact the fund's ability to recoup its investment. Securities in default may be illiquid or trade in low volumes and thus may be difficult to value.

For securities that rely on third-party guarantors to support their credit quality, the same risks may apply if the financial condition of the guarantor deteriorates or the guarantor ceases to insure securities. Because guarantors may insure many types of securities, including subprime mortgage bonds and other high-risk bonds, their financial condition could deteriorate as a result of events that have little or no connection to securities owned by the fund.

Focus risk – Massachusetts municipal securities. The municipal securities market in general can be susceptible to increases in volatility and decreases in liquidity. Liquidity can decline unpredictably in response to overall economic conditions or credit tightening. Increases in volatility and decreases in liquidity may be caused by a rise in interest rates (or the expectation of a rise in interest rates). Because the fund focuses its investments in Massachusetts municipal securities, its performance can be more volatile than that of a fund that invests more broadly, and it has a relatively large exposure to financial stresses affecting Massachusetts. For example, industries significant to the state’s economy, such as the technology, biotech, financial services or healthcare industries could experience downturns or fail to develop as expected, hurting the local economy. Fluctuations in unemployment levels or in the state or national economy could result in decreased tax revenues, including decreases in personal income tax, corporate business tax, or sales and use tax revenues, and other sources of revenue. Massachusetts could also face severe fiscal difficulties, for example, an economic downturn, increased expenditures on domestic security, reduced monetary support from the federal government or costs and disruption caused by natural disasters. A default or credit rating downgrade of a small number of municipal security issuers could affect the market values and marketability of all Massachusetts municipal securities and hurt the fund’s performance.

Over time, these issues may impair the ability of the state, municipalities, or other authorities to repay their obligations or to pay debt service on those obligations and could result in a downgrade of Massachusetts' credit rating or the ratings of authorities or political subdivisions of Massachusetts, which may negatively impact the value of bonds issued by those entities.

Market risk. Deteriorating market conditions might cause a general weakness in the market that reduces the prices of securities in that market. Developments in a particular

Prospectus August 1, 2024

3

DWS Massachusetts Tax-Free Fund

class of debt securities or the stock market could also adversely affect the fund by reducing the relative attractiveness of debt securities as an investment.

Market disruption risk. Economies and financial markets throughout the world have become increasingly interconnected, which has increased the likelihood that events or conditions in one country or region will adversely impact markets or issuers in other countries or regions. This includes reliance on global supply chains that are susceptible to disruptions resulting from, among other things, war and other armed conflicts, extreme weather events, and natural disasters. Such supply chain disruptions can lead to, and have led to, economic and market disruptions that have far-reaching effects on financial markets worldwide. The value of the fund’s investments may be negatively affected by adverse changes in overall economic or market conditions, such as the level of economic activity and productivity, unemployment and labor force participation rates, inflation or deflation (and expectations for inflation or deflation), interest rates, demand and supply for particular products or resources including labor, and debt levels and credit ratings, among other factors. Such adverse conditions may contribute to an overall economic contraction across entire economies or markets, which may negatively impact the profitability of issuers operating in those economies or markets. In addition, geopolitical and other globally interconnected occurrences, including war, terrorism, economic uncertainty or financial crises, contagion, trade disputes, government debt crises (including defaults or downgrades) or uncertainty about government debt payments, government shutdowns, public health crises, natural disasters, supply chain disruptions, climate change and related events or conditions, have led, and in the future may lead, to disruptions in the US and world economies and markets, which may increase financial market volatility and have significant adverse direct or indirect effects on the fund and its investments. Adverse market conditions or disruptions could cause the fund to lose money, experience significant redemptions, and encounter operational difficulties. Although multiple asset classes may be affected by adverse market conditions or a particular market disruption, the duration and effects may not be the same for all types of assets.

Current military and other armed conflicts in various geographic regions, including those in Europe and the Middle East, can lead to, and have led to, economic and market disruptions, which may not be limited to the geographic region in which the conflict is occurring. Such conflicts can also result, and have resulted in some cases, in sanctions being levied by the United States, the European Union and/or other countries against countries or other actors involved in the conflict. In addition, such conflicts and related sanctions can adversely affect regional and global energy, commodities, financial and other markets and thus could affect the value of the fund's investments. The extent and duration of any military

conflict, related sanctions and resulting economic and market disruptions are impossible to predict, but could be substantial.

Other market disruption events include pandemic spread of viruses, such as the novel coronavirus known as COVID-19, which have caused significant uncertainty, market volatility, decreased economic and other activity, increased government activity, including economic stimulus measures, and supply chain disruptions. While COVID-19 is no longer considered to be a public health emergency, the fund and its investments may be adversely affected by lingering effects of this virus or future pandemic spread of viruses.

In addition, markets are becoming increasingly susceptible to disruption events resulting from the use of new and emerging technologies to engage in cyber-attacks or to take over the websites and/or social media accounts of companies, governmental entities or public officials, or to otherwise pose as or impersonate such, which then may be used to disseminate false or misleading information that can cause volatility in financial markets or for the stock of a particular company, group of companies, industry or other class of assets.

Adverse market conditions or particular market disruptions, such as those discussed above, may magnify the impact of each of the other risks described in this “MAIN RISKS” section and may increase volatility in one or more markets in which the fund invests leading to the potential for greater losses for the fund.

Inflation risk. Inflation risk is the risk that the real value of certain assets or real income from investments (the value of such assets or income after accounting for inflation) will be less in the future as inflation decreases the value of money. Inflation, and investors’ expectation of future inflation, can impact the current value of the fund's portfolio, resulting in lower asset values and losses to shareholders. This risk may be elevated compared to historical market conditions and could be impacted by monetary policy measures and the current interest rate environment.

Tax risk. Income from municipal securities held by the fund could be declared taxable because of unfavorable changes in tax laws, adverse interpretations by the Internal Revenue Service or state tax authorities, or noncompliant conduct of a securities issuer. In such event, the value of such securities would likely fall, hurting fund performance and shareholders may be required to pay additional taxes. In addition, a portion of the fund’s otherwise exempt-interest distributions may be taxable to those shareholders subject to the federal AMT.

Private activity and industrial development bond risk. The payment of principal and interest on these bonds is generally dependent solely on the ability of the facility’s user to meet its financial obligations and the pledge, if any, of property financed as security for such payment.

Prospectus August 1, 2024

4

DWS Massachusetts Tax-Free Fund

Non-diversification risk. The fund is classified as non-diversified under the Investment Company Act of 1940, as amended. This means that the fund may invest in securities of relatively few issuers. Thus, the performance of one or a small number of portfolio holdings can affect overall performance.

Security selection risk. The securities in the fund’s portfolio may decline in value. Portfolio management could be wrong in its analysis of municipalities, industries, companies, economic trends, ESG factors, the relative attractiveness of different securities or other matters.

Forward commitment risk. When the fund engages in forward or delayed delivery transactions, the fund relies on the counterparty to consummate the transaction. Failure to do so may result in the fund missing the opportunity to obtain a price or yield considered to be advantageous. Such transactions may also have the effect of leverage on the fund and may cause the fund to be more volatile.

Counterparty risk. A financial institution or other counterparty with whom the fund does business, or that underwrites, distributes or guarantees any investments or contracts that the fund owns or is otherwise exposed to, may decline in financial health and become unable to honor its commitments. This could cause losses for the fund or could delay the return or delivery of collateral or other assets to the fund.

Liquidity risk. In certain situations, it may be difficult or impossible to sell an investment and/or the fund may sell certain investments at a price or time that is not advantageous in order to meet redemption requests or other cash needs. Unusual market conditions, such as an unusually high volume of redemptions or other similar conditions could increase liquidity risk for the fund, and in extreme conditions, the fund could have difficulty meeting redemption requests.

Prepayment and extension risk. When interest rates fall, issuers of high interest debt obligations may pay off the debts earlier than expected (prepayment risk), and the fund may have to reinvest the proceeds at lower yields. When interest rates rise, issuers of lower interest debt obligations may pay off the debts later than expected (extension risk), thus keeping the fund’s assets tied up in lower interest debt obligations. Ultimately, any unexpected behavior in interest rates could increase the volatility of the fund’s share price and yield and could hurt fund performance. Prepayments could also create capital gains tax liability in some instances.

Pricing risk. If market conditions make it difficult to value some investments, the fund may value these investments using more subjective methods, such as fair value pricing. In such cases, the value determined for an investment could be different from the value realized upon such investment’s sale. As a result, you could pay more than the market value when buying fund shares or receive less than the market value when selling fund shares.

Operational and technology risk. Cyber-attacks, disruptions or failures that affect the fund’s service providers or counterparties, issuers of securities held by the fund, or other market participants may adversely affect the fund and its shareholders, including by causing losses for the fund or impairing fund operations. For example, the fund’s or its service providers’ assets or sensitive or confidential information may be misappropriated, data may be corrupted and operations may be disrupted (e.g., cyber-attacks, operational failures or broader disruptions may cause the release of private shareholder information or confidential fund information, interfere with the processing of shareholder transactions, impact the ability to calculate the fund’s net asset value and impede trading). Market events and disruptions also may trigger a volume of transactions that overloads current information technology and communication systems and processes, impacting the ability to conduct the fund’s operations.

While the fund and its service providers may establish business continuity and other plans and processes that seek to address the possibility of and fallout from cyber-attacks, disruptions or failures, there are inherent limitations in such plans and systems, including that they do not apply to third parties, such as fund counterparties, issuers of securities held by the fund or other market participants, as well as the possibility that certain risks have not been identified or that unknown threats may emerge in the future and there is no assurance that such plans and processes will be effective. Among other situations, disruptions (for example, pandemics or health crises) that cause prolonged periods of remote work or significant employee absences at the fund’s service providers could impact the ability to conduct the fund’s operations. In addition, the fund cannot directly control any cybersecurity plans and systems put in place by its service providers, fund counterparties, issuers of securities held by the fund or other market participants.

How a fund's returns vary from year to year can give an idea of its risk; so can comparing fund performance to overall market performance (as measured by an appropriate broad-based securities market index).Past performance may not indicate future results. All performance figures below assume that dividends and distributions were reinvested. For more recent performance figures, go to dws.com (the Web site does not form a part of this prospectus) or call the telephone number included in this prospectus.

Prospectus August 1, 2024

5

DWS Massachusetts Tax-Free Fund

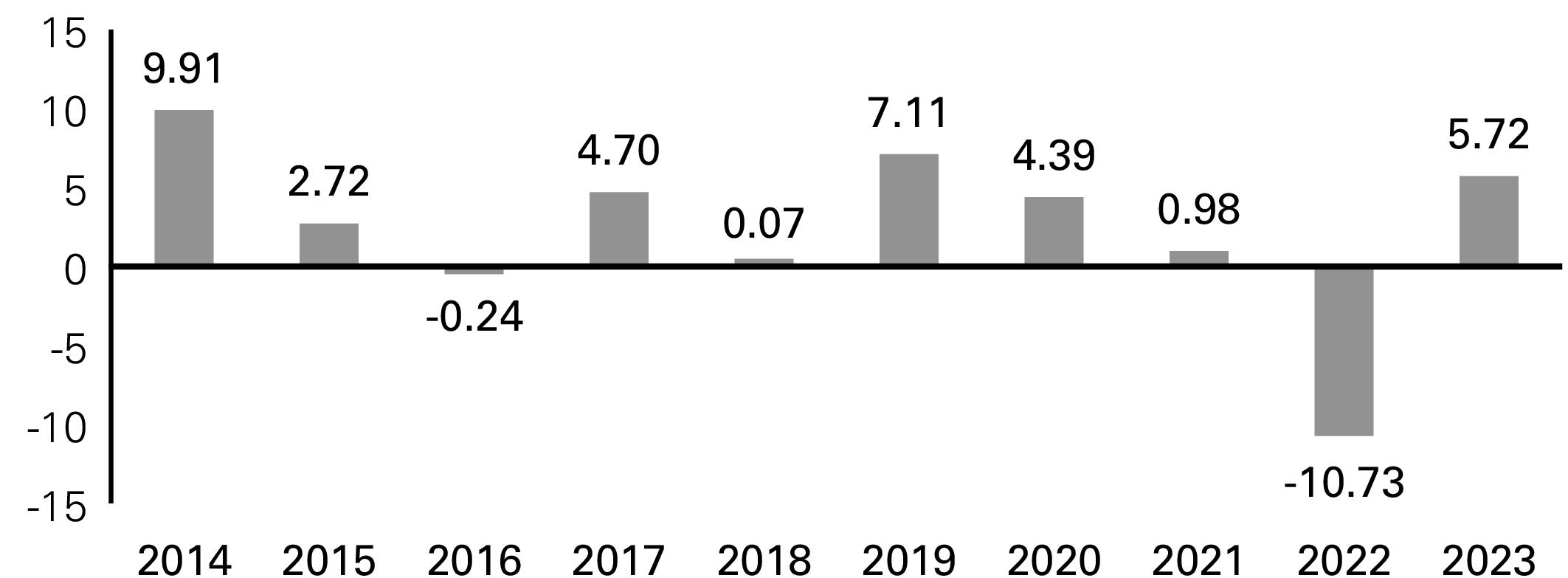

CALENDAR YEAR TOTAL RETURNS (%) (Class A)

These year-by-year returns do not include sales charges, if any, and would be lower if they did. Returns for other classes were different and are not shown here.

Average Annual Total Returns

(For periods ended 12/31/2023 expressed as a %)

After-tax returns (which are shown only for Class A and would be different for other classes) reflect the historical highest individual federal income tax rates, but do not reflect any state or local taxes. Your actual after-tax returns may be different. After-tax returns are not relevant to shares held in an IRA, 401(k) or other tax-advantaged investment plan.

|

|

|

|

|

|

|

|

|

|

|

|

After tax on distribu-

tions |

|

|

|

|

After tax on distribu-

tions and sale of fund

shares |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Bloomberg Municipal

Bond Index (reflects no

deduction for fees,

expenses or taxes) |

|

|

|

|

Bloomberg Massachu-

setts Exempt Municipal

Bond Index (reflects no

deduction for fees,

expenses or taxes) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Bloomberg Municipal

Bond Index (reflects no

deduction for fees,

expenses or taxes) |

|

|

|

Bloomberg Massachu-

setts Exempt Municipal

Bond Index (reflects no

deduction for fees,

expenses or taxes) |

|

|

|

The Advisor believes the additional Bloomberg Massachusetts Exempt Municipal Bond Index reasonably represents the fund's investment objective and strategies.

DWS Investment Management Americas, Inc.

Michael J. Generazo, Senior Portfolio Manager Fixed Income. Portfolio Manager of the fund. Began managing the fund in 2018.

Matthew J. Caggiano, CFA, Head of Investment Strategy Fixed Income. Portfolio Manager of the fund. Began managing the fund in 2021.

Purchase and Sale of Fund Shares

Minimum Initial Investment ($)

|

|

|

|

|

Automatic

Investment

Plans |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

For participants in all group retirement plans, and in certain fee-based and wrap programs approved by the Advisor, there is no minimum initial investment and no minimum additional investment for Class A, C and S shares. For Section 529 college savings plans, there is no minimum initial investment and no minimum additional investment for Class S shares. The minimum initial investment for Class S shares may be waived for eligible intermediaries that have agreements with DDI to offer Class S shares in their brokerage platforms when such Class S shares are held in omnibus accounts on such brokerage platforms. In certain instances, the minimum initial investment may be waived for Institutional Class shares. For more information regarding available Institutional Class investment minimum waivers, see “Institutional Class Shares – Investment Minimum” in the “Choosing a Share Class” section of the prospectus. There is no minimum additional investment for Institutional Class shares. The minimum additional investment in all other instances is $50.

Prospectus August 1, 2024

6

DWS Massachusetts Tax-Free Fund

To Place Orders

|

|

|

DWS

PO Box 219151

Kansas City, MO 64121-9151 |

|

|

DWS

430 West 7th Street

Suite 219151

Kansas City, MO 64105-1407 |

|

|

|

|

|

(800) 728-3337, M – F 8 a.m. – 7 p.m. ET |

|

|

For hearing impaired assistance, please

call us using a relay service |

The fund is generally open on days when the New York Stock Exchange is open for regular trading. If you invest with the fund directly through the transfer agent, you can open a new fund account (Class S shares only) and make an initial investment on the Internet at dws.com, by using the mobile app or by mail. You can make additional investments or sell shares of the fund on any business day by visiting the fund’s Web site, by using the mobile app, by mail, or by telephone; however you may have to elect certain privileges on your initial account application. The ability to open new fund accounts and to transact online or using the mobile app varies depending on share class and account type. If you are working with a financial representative, contact your financial representative for assistance with buying or selling fund shares. A financial representative separately may impose its own policies and procedures for buying and selling fund shares.

Institutional Class shares are generally available only to qualified institutions. Class S shares are available through certain intermediary relationships with financial services firms, or can be purchased by establishing an account directly with the fund’s transfer agent.

The fund's distributions are generally exempt from regular federal and Massachusetts state income tax. All or a portion of the fund's dividends may be subject to the federal alternative minimum tax.

Payments to Broker-Dealers and

Other Financial Intermediaries

If you purchase shares of the fund through a broker-dealer or other financial intermediary (such as a bank), the fund, the Advisor, and/or the Advisor’s affiliates may pay the intermediary for the sale of fund shares and related services. These payments may create a conflict of interest by influencing the broker-dealer or other intermediary and your salesperson to recommend the fund over another investment. Ask your salesperson or visit your financial intermediary’s Web site for more information.

Prospectus August 1, 2024

7

DWS Massachusetts Tax-Free Fund

Additional Information About Fund Strategies and Risks

The fund seeks income that is exempt from Massachusetts personal and federal income taxes.

Principal Investment Strategies

Main investments. Under normal circumstances, the fund invests at least 80% of net assets, plus the amount of any borrowings for investment purposes, in Massachusetts municipal securities. For purposes of this 80% requirement, Massachusetts municipal securities are securities whose income is exempt from regular federal and Massachusetts state income taxes. The fund can also invest in obligations of US territories and Commonwealths (such as Puerto Rico, the US Virgin Islands and Guam) and their agencies and authorities, whose income is free from regular federal and Massachusetts state income tax. The fund may invest up to 20% of net assets in securities whose income is subject to the federal alternative minimum tax (AMT).

The fund can buy many types of municipal securities with no maturity restrictions. These may include, without limitation, revenue bonds (which are backed by revenues from a particular source) and general obligation bonds (which are typically backed by the issuer’s ability to levy taxes). They may also include private activity and industrial development bonds, pre-refunded bonds, municipal lease obligations and investments representing an interest therein.

The fund normally invests at least 80% of total assets in municipal securities of the top four grades of credit quality or, if unrated, determined by the fund’s investment advisor to be of similar quality. The fund could invest up to 20% of total assets in high yield, below investment-grade bonds (commonly referred to as “junk” bonds), which are those rated below the fourth highest rating category (i.e., grade BB/Ba and below). Compared to investment-grade bonds, junk bonds generally pay higher yields but have higher volatility and higher risk of default on payments.

The fund may use forward delivery bonds, which are bonds priced on a determined date but that are not issued and settled until a later period (ranging from several weeks to more than a year). Forward delivery bonds with settlement dates greater than 35 days are treated as derivatives by the fund and are subject to the fund's policies and procedures with respect to derivatives. Forward delivery bonds with settlement dates greater than 35 days generally are used for non-hedging purposes to seek to enhance potential gains.

If a fixed income security is rated differently among the three major ratings agencies (i.e., Moody’s Investor Services, Inc., Fitch Investors Services, Inc., and Standard & Poor’s Ratings Group), portfolio management would rely on the highest credit rating for purposes of the fund’s investment policies.

The fund may also invest in exchange-traded funds (ETFs). The fund’s investments in ETFs will be limited to 5% of total assets in any one ETF and 10% of total assets in the aggregate in ETFs.

Management process. Portfolio management looks for securities that appear to offer the best total return potential. In making buy and sell decisions, portfolio management typically weighs a number of factors, including economic outlooks, possible interest rate movements, yield levels across varying maturities, and changes in supply and demand within the municipal bond market. When evaluating any individual security and its issuer, portfolio management may consider a number of factors including the security's credit quality and terms, such as coupon, maturity date and call date, as well as the issuer's capital structure, leverage and ability to meet its current obligations. Portfolio management may also consider financially material environmental, social, and governance (ESG) factors. Such factors may include, but are not limited to, exposure to climate change risks, income levels and unemployment data, and an issuer’s governance structure and practices.

Although portfolio management may adjust the fund’s duration (a measure of sensitivity to interest rates) over a wider range, they generally intend to keep it similar to that of the Bloomberg Municipal Bond Index, which is generally between five and nine years.

| Prospectus August 1, 2024 | 8 | Fund Details |

Portfolio management may consider information about Environmental, Social and Governance (ESG) issues in its fundamental research process.

Other Investment Strategies

Tender option bonds. The fund may engage in tender option bond transactions. In a tender option bond transaction, the fund transfers fixed-rate long-term municipal bonds into a special purpose entity (a “TOB Trust”), which then typically issues two classes of beneficial interests: short-term floating rate interests (“TOB Floaters”), which are sold to third party investors, and residual inverse floating rate interests (“TOB Inverse Floater Residual Interests”), which are generally held by the fund. Tender option bond transactions are treated as derivatives by the fund and are subject to the fund's policies and procedures with respect to derivatives. The fund may leverage its assets and seek to enhance potential gains through the use of proceeds received from TOB Floaters.

Derivatives. The fund may invest in derivatives, which are financial instruments whose performance is derived, at least in part, from the performance of an underlying asset, security or index. The fund may use various types of derivatives (i) for hedging purposes; (ii) for risk management; (iii) for non-hedging purposes to seek to enhance potential gains; or (iv) as a substitute for direct investment in a particular asset class or to keep cash on hand to meet shareholder redemptions.

There are several risk factors that could hurt the fund’s performance, cause you to lose money or cause the fund’s performance to trail that of other investments. The fund may not achieve its investment objective, and is not intended to be a complete investment program. An investment in the fund is not a deposit of a bank and is not insured or guaranteed by the Federal Deposit Insurance Corporation or any other governmental agency.

Interest rate risk. When interest rates rise, prices of debt securities generally decline. The longer the duration of the fund’s debt securities, the more sensitive the fund will be to interest rate changes. (As a general rule, a 1% rise in interest rates means a 1% fall in value for every year of duration.) When interest rates change, the values of longer-duration municipal bonds usually change more than the values of shorter-duration municipal bonds. Conversely, municipal bonds with shorter durations or maturities will be less volatile but may provide lower returns than municipal bonds with longer durations or maturities. Rising interest rates also may lengthen the duration of municipal bonds with call features, since exercise of the call becomes less likely as interest rates rise, which in turn will make the securities more sensitive to changes in interest rates and result in even steeper price declines in the event of further interest rate increases. Interest rates can change in response to the supply and demand for credit,

government and/or central bank monetary policy and action, inflation rates, and other factors. Recent and potential future changes in monetary policy made by central banks or governments are likely to affect the level of interest rates. Changing interest rates may have unpredictable effects on markets, may result in heightened market volatility and potential illiquidity and may detract from fund performance to the extent the fund is exposed to such interest rates and/or volatility. Rising interest rates could cause the value of the fund’s investments — and therefore its share price as well — to decline. A rising interest rate environment may cause investors to move out of fixed-income securities and related markets on a large scale, which could adversely affect the price and liquidity of such securities and could also result in increased redemptions from the fund. Increased redemptions from the fund may force the fund to sell investments at a time when it is not advantageous to do so, which could result in losses. Beginning in 2022, the US Federal Reserve (“Fed”) raised interest rates significantly in response to increased inflation. It is unclear if and when the Fed may begin to implement interest rate cuts, if rates will remain at current levels for a prolonged period or, if the Fed deems necessary in response to certain economic developments such as a turnaround in the decline of inflation, the Fed may consider additional rate increases. As a result, fixed-income and related markets may experience heightened levels of volatility and liquidity risk.

Credit risk. The fund's performance could be hurt if an issuer of a debt security suffers an adverse change in financial condition that results in the issuer not making timely payments of interest or principal, a security downgrade or an inability to meet a financial obligation. Credit risk is greater for lower-rated securities.

Because the issuers of high yield debt securities, or junk bonds (debt securities rated below the fourth highest credit rating category), may be in uncertain financial health, the prices of their debt securities can be more vulnerable to bad economic news, or even the expectation of bad news, than investment-grade debt securities. Credit risk for high yield securities is greater than for higher-rated securities.

Because securities in default generally have missed one or more payments of interest and/or principal, an investment in such securities has an increased risk of loss. Issuers of securities in default have an increased likelihood of entering bankruptcy or beginning liquidation procedures which could impact the fund's ability to recoup its investment. Securities in default may be illiquid or trade in low volumes and thus may be difficult to value.

For securities that rely on third-party guarantors to support their credit quality, the same risks may apply if the financial condition of the guarantor deteriorates or the guarantor ceases to insure securities. Because guarantors may

Prospectus August 1, 2024

9

Fund Details

insure many types of securities, including subprime mortgage bonds and other high-risk bonds, their financial condition could deteriorate as a result of events that have little or no connection to securities owned by the fund.

Focus risk – Massachusetts municipal securities. The municipal securities market in general can be susceptible to increases in volatility and decreases in liquidity. Liquidity can decline unpredictably in response to overall economic conditions or credit tightening. Increases in volatility and decreases in liquidity may be caused by a rise in interest rates (or the expectation of a rise in interest rates). Because the fund focuses its investments in Massachusetts municipal securities, its performance can be more volatile than that of a fund that invests more broadly, and it has a relatively large exposure to financial stresses affecting Massachusetts. For example, industries significant to the state’s economy, such as the technology, biotech, financial services or healthcare industries could experience downturns or fail to develop as expected, hurting the local economy. Fluctuations in unemployment levels or in the state or national economy could result in decreased tax revenues, including decreases in personal income tax, corporate business tax, or sales and use tax revenues, and other sources of revenue. Massachusetts could also face severe fiscal difficulties, for example, an economic downturn, increased expenditures on domestic security, reduced monetary support from the federal government or costs and disruption caused by natural disasters. A default or credit rating downgrade of a small number of municipal security issuers could affect the market values and marketability of all Massachusetts municipal securities and hurt the fund’s performance.

Over time, these issues may impair the ability of the state, municipalities, or other authorities to repay their obligations or to pay debt service on those obligations and could result in a downgrade of Massachusetts' credit rating or the ratings of authorities or political subdivisions of Massachusetts, which may negatively impact the value of bonds issued by those entities.

Massachusetts municipal securities may also have exposure to potential physical risks resulting from climate change, including extreme weather, flooding and fires. Climate risks, if they materialize, can adversely impact a Massachusetts municipal issuer’s financial plans in current or future years or may impair a facility or other source generating revenues backing a Massachusetts municipal issuer’s revenue bonds. As a result, the impact of climate risks may adversely impact the value of the Fund’s shares.

Market risk. Deteriorating market conditions might cause a general weakness in the market that reduces the prices of securities in that market. Developments in a particular class of debt securities or the stock market could also adversely affect the fund by reducing the relative attractiveness of debt securities as an investment.

Market disruption risk. Economies and financial markets throughout the world have become increasingly interconnected, which has increased the likelihood that events or conditions in one country or region will adversely impact markets or issuers in other countries or regions. This includes reliance on global supply chains that are susceptible to disruptions resulting from, among other things, war and other armed conflicts, extreme weather events, and natural disasters. Such supply chain disruptions can lead to, and have led to, economic and market disruptions that have far-reaching effects on financial markets worldwide. The value of the fund’s investments may be negatively affected by adverse changes in overall economic or market conditions, such as the level of economic activity and productivity, unemployment and labor force participation rates, inflation or deflation (and expectations for inflation or deflation), interest rates, demand and supply for particular products or resources including labor, and debt levels and credit ratings, among other factors. Such adverse conditions may contribute to an overall economic contraction across entire economies or markets, which may negatively impact the profitability of issuers operating in those economies or markets. In addition, geopolitical and other globally interconnected occurrences, including war, terrorism, economic uncertainty or financial crises, contagion, trade disputes, government debt crises (including defaults or downgrades) or uncertainty about government debt payments, government shutdowns, public health crises, natural disasters, supply chain disruptions, climate change and related events or conditions, have led, and in the future may lead, to disruptions in the US and world economies and markets, which may increase financial market volatility and have significant adverse direct or indirect effects on the fund and its investments. Adverse market conditions or disruptions could cause the fund to lose money, experience significant redemptions, and encounter operational difficulties. Although multiple asset classes may be affected by adverse market conditions or a particular market disruption, the duration and effects may not be the same for all types of assets.

Current military and other armed conflicts in various geographic regions, including those in Europe and the Middle East, can lead to, and have led to, economic and market disruptions, which may not be limited to the geographic region in which the conflict is occurring. Such conflicts can also result, and have resulted in some cases, in sanctions being levied by the United States, the European Union and/or other countries against countries or other actors involved in the conflict. In addition, such conflicts and related sanctions can adversely affect regional and global energy, commodities, financial and other markets and thus could affect the value of the fund's investments. The extent and duration of any military conflict, related sanctions and resulting economic and market disruptions are impossible to predict, but could be substantial.

Prospectus August 1, 2024

10

Fund Details

Other market disruption events include pandemic spread of viruses, such as the novel coronavirus known as COVID-19, which have caused significant uncertainty, market volatility, decreased economic and other activity, increased government activity, including economic stimulus measures, and supply chain disruptions. While COVID-19 is no longer considered to be a public health emergency, the fund and its investments may be adversely affected by lingering effects of this virus or future pandemic spread of viruses.

In addition, markets are becoming increasingly susceptible to disruption events resulting from the use of new and emerging technologies to engage in cyber-attacks or to take over the websites and/or social media accounts of companies, governmental entities or public officials, or to otherwise pose as or impersonate such, which then may be used to disseminate false or misleading information that can cause volatility in financial markets or for the stock of a particular company, group of companies, industry or other class of assets.

Adverse market conditions or particular market disruptions, such as those discussed above, may magnify the impact of each of the other risks described in this “MAIN RISKS” section and may increase volatility in one or more markets in which the fund invests leading to the potential for greater losses for the fund.

Inflation risk. Inflation risk is the risk that the real value of certain assets or real income from investments (the value of such assets or income after accounting for inflation) will be less in the future as inflation decreases the value of money. Inflation, and investors’ expectation of future inflation, can impact the current value of the fund's portfolio, resulting in lower asset values and losses to shareholders. This risk may be elevated compared to historical market conditions and could be impacted by monetary policy measures and the current interest rate environment.

Tax risk. Income from municipal securities held by the fund could be declared taxable because of unfavorable changes in tax laws, adverse interpretations by the Internal Revenue Service or state tax authorities, or noncompliant conduct of a securities issuer. In such event, the value of such securities would likely fall, hurting fund performance and shareholders may be required to pay additional taxes. In addition, a portion of the fund’s otherwise exempt-interest distributions may be taxable to those shareholders subject to the federal AMT.

Private activity and industrial development bond risk. The payment of principal and interest on these bonds is generally dependent solely on the ability of the facility’s user to meet its financial obligations and the pledge, if any, of property financed as security for such payment.

Non-diversification risk. The fund is classified as non-diversified under the Investment Company Act of 1940, as amended. This means that the fund may invest in

securities of relatively few issuers. Thus, the performance of one or a small number of portfolio holdings can affect overall performance.

Security selection risk. The securities in the fund’s portfolio may decline in value. Portfolio management could be wrong in its analysis of municipalities, industries, companies, economic trends, ESG factors, the relative attractiveness of different securities or other matters.

US territory and Commonwealth obligations risk. Adverse political and economic conditions and developments affecting any territory or Commonwealth of the US may, in turn, negatively affect the value of the fund’s holdings in such obligations. For example, Puerto Rico has experienced a recession and difficult economic conditions, along with a severe natural disaster, which may negatively affect the value of any holdings the fund may have in Puerto Rico municipal obligations.

Forward commitment risk. When the fund engages in forward or delayed delivery transactions, the fund relies on the counterparty to consummate the transaction. Failure to do so may result in the fund missing the opportunity to obtain a price or yield considered to be advantageous. Such transactions may also have the effect of leverage on the fund and may cause the fund to be more volatile.

Counterparty risk. A financial institution or other counterparty with whom the fund does business, or that underwrites, distributes or guarantees any investments or contracts that the fund owns or is otherwise exposed to, may decline in financial health and become unable to honor its commitments. This could cause losses for the fund or could delay the return or delivery of collateral or other assets to the fund.

Liquidity risk. In certain situations, it may be difficult or impossible to sell an investment and/or the fund may sell certain investments at a price or time that is not advantageous in order to meet redemption requests or other cash needs. Unusual market conditions, such as an unusually high volume of redemptions or other similar conditions could increase liquidity risk for the fund, and in extreme conditions, the fund could have difficulty meeting redemption requests.

This risk can be ongoing for any security that does not trade actively or in large volumes, for any security that trades primarily on smaller markets, and for investments that typically trade only among a limited number of large investors (such as certain types of derivatives or restricted securities). In unusual market conditions, even normally liquid securities may be affected by a degree of liquidity risk (i.e., if the number and capacity of traditional market participants is reduced). This may affect only certain securities or an overall securities market.

The potential for liquidity risk may be magnified by a rising interest rate environment or other circumstances where investor redemptions from fixed-income mutual funds may be higher than normal, potentially causing increased

Prospectus August 1, 2024

11

Fund Details

supply in the market due to selling activity. If dealer capacity in fixed-income markets is insufficient for market conditions, it may further inhibit liquidity and increase volatility in the fixed-income markets. Additionally, market participants, other than the fund, may attempt to sell fixed income holdings at the same time as the fund, which could cause downward pricing pressure and contribute to illiquidity.

Prepayment and extension risk. When interest rates fall, issuers of high interest debt obligations may pay off the debts earlier than expected (prepayment risk), and the fund may have to reinvest the proceeds at lower yields. When interest rates rise, issuers of lower interest debt obligations may pay off the debts later than expected (extension risk), thus keeping the fund’s assets tied up in lower interest debt obligations. Ultimately, any unexpected behavior in interest rates could increase the volatility of the fund’s share price and yield and could hurt fund performance. Prepayments could also create capital gains tax liability in some instances.

Pricing risk. If market conditions make it difficult to value some investments, the fund may value these investments using more subjective methods, such as fair value pricing. In such cases, the value determined for an investment could be different from the value realized upon such investment’s sale. As a result, you could pay more than the market value when buying fund shares or receive less than the market value when selling fund shares.

Secondary markets may be subject to irregular trading activity, wide bid/ask spreads and extended trade settlement periods, which may prevent the fund from being able to realize full value and thus sell a security for its full valuation. This could cause a material decline in the fund’s net asset value.

Tender option bonds risk. The fund’s participation in tender option bond transactions may reduce the fund’s returns or increase volatility. Tender option bond transactions create leverage. Leverage magnifies returns, both positive and negative, and risk by magnifying the volatility of returns. An investment in TOB Inverse Floater Residual Interests will typically involve more risk than an investment in the underlying municipal bonds. The interest payment on TOB Inverse Floater Residual Interests generally will decrease when short-term interest rates increase. There are also risks associated with the tender option bond structure, which could result in terminating the trust. If a TOB Trust is terminated, the fund must sell other assets to buy back the TOB Floaters, which could negatively impact performance. Events that could cause a termination of the TOB Trust include a deterioration in the financial condition of the liquidity provider, a deterioration in the credit quality of underlying municipal bonds, or a decrease in the value of the underlying bonds due to rising interest rates.

The fund may invest in TOB Inverse Floater Residual Interests on a non-recourse or recourse basis. If the fund invests in TOB Inverse Floater Residual Interests on a recourse basis, the fund could suffer losses in excess of the value of the TOB Inverse Floater Residual Interests.

Changes to the structure of TOBs to address the Volcker Rule could make early unwinds of TOB Trusts more likely, may make the use of TOB Trusts more expensive, and may make it more difficult to use TOB Trusts in general.

Derivatives risk. Derivatives involve risks different from, and possibly greater than, the risks associated with investing directly in securities and other more traditional investments. Risks associated with derivatives may include the risk that the derivative is not well correlated with the underlying asset, security or index to which it relates; the risk that derivatives may result in losses or missed opportunities; the risk that the fund will be unable to sell the derivative because of an illiquid secondary market; the risk that a counterparty is unwilling or unable to meet its obligation, which risk may be heightened in derivative transactions entered into “over-the-counter” (i.e., not on an exchange or contract market); and the risk that the derivative transaction could expose the fund to the effects of leverage, which could increase the fund's exposure to the market and magnify potential losses.

There is no guarantee that derivatives, to the extent employed, will have the intended effect, and their use could cause lower returns or even losses to the fund. The use of derivatives by the fund to hedge risk may reduce the opportunity for gain by offsetting the positive effect of favorable price movements.

ETF risk. Because ETFs trade on a securities exchange, their shares may trade at a premium or discount to their net asset value. An ETF is subject to the risks of the assets in which it invests as well as those of the investment strategy it follows. The fund may incur brokerage costs when it buys and sells shares of an ETF and also bears its proportionate share of the ETF’s fees and expenses, which are passed through to ETF shareholders.

Fees and expenses incurred by an ETF may include trading costs, operating expenses, licensing fees, trustee fees and marketing expenses. With an index ETF, these costs may contribute to the ETF not fully matching the performance of the index it is designed to track.

Operational and technology risk. Cyber-attacks, disruptions or failures that affect the fund’s service providers or counterparties, issuers of securities held by the fund, or other market participants may adversely affect the fund and its shareholders, including by causing losses for the fund or impairing fund operations. For example, the fund’s or its service providers’ assets or sensitive or confidential information may be misappropriated, data may be corrupted and operations may be disrupted (e.g., cyber-attacks, operational failures or broader disruptions may cause the release of private shareholder information or

Prospectus August 1, 2024

12

Fund Details

confidential fund information, interfere with the processing of shareholder transactions, impact the ability to calculate the fund’s net asset value and impede trading). Market events and disruptions also may trigger a volume of transactions that overloads current information technology and communication systems and processes, impacting the ability to conduct the fund’s operations.

While the fund and its service providers may establish business continuity and other plans and processes that seek to address the possibility of and fallout from cyber-attacks, disruptions or failures, there are inherent limitations in such plans and systems, including that they do not apply to third parties, such as fund counterparties, issuers of securities held by the fund or other market participants, as well as the possibility that certain risks have not been identified or that unknown threats may emerge in the future and there is no assurance that such plans and processes will be effective. Among other situations, disruptions (for example, pandemics or health crises) that cause prolonged periods of remote work or significant employee absences at the fund’s service providers could impact the ability to conduct the fund’s operations. In addition, the fund cannot directly control any cybersecurity plans and systems put in place by its service providers, fund counterparties, issuers of securities held by the fund or other market participants.

Cyber-attacks may include unauthorized attempts by third parties to improperly access, modify, disrupt the operations of, or prevent access to the systems of the fund’s service providers or counterparties, issuers of securities held by the fund or other market participants or data within them. In addition, power or communications outages, acts of god, information technology equipment malfunctions, operational errors, and inaccuracies within software or data processing systems may also disrupt business operations or impact critical data.

Cyber-attacks, disruptions, or failures may adversely affect the fund and its shareholders or cause reputational damage and subject the fund to regulatory fines, litigation costs, penalties or financial losses, reimbursement or other compensation costs, and/or additional compliance costs. In addition, cyber-attacks, disruptions, or failures involving a fund counterparty could affect such counterparty’s ability to meet its obligations to the fund, which may result in losses to the fund and its shareholders. Similar types of operational and technology risks are also present for issuers of securities held by the fund, which could have material adverse consequences for such issuers, and may cause the fund’s investments to lose value. Furthermore, as a result of cyber-attacks, disruptions, or failures, an exchange or market may close or issue trading halts on specific securities or the entire market, which may result in the fund being, among other things, unable to buy or sell certain securities or financial instruments or unable to accurately price its investments.

For example, the fund relies on various sources to calculate its NAV. Therefore, the fund is subject to certain operational risks associated with reliance on third party service providers and data sources. NAV calculation may be impacted by operational risks arising from factors such as failures in systems and technology. Such failures may result in delays in the calculation of the fund’s NAV and/or the inability to calculate NAV over extended time periods. The fund may be unable to recover any losses associated with such failures.

While the previous pages describe the main points of the fund’s strategy and risks, there are a few other matters to know about:

■

Although major changes tend to be infrequent, the fund’s Board could change the fund's investment objective without seeking shareholder approval. However, the fund's policy of investing at least 80% of net assets, plus the amount of any borrowings for investment purposes, in Massachusetts municipal securities whose income is exempt from federal and Massachusetts personal income taxes cannot be changed without shareholder approval.

■

When, in the Advisor's opinion, (1) it is advisable to adopt a temporary defensive position because of unusual and adverse or other market conditions or (2) an unusual disparity between after-tax income on taxable and municipal securities makes it advisable, up to 100% of the fund's assets may be held in cash or invested in taxable money market securities or other short-term investments, which may produce taxable income. Short-term investments consist of (1) foreign and domestic obligations of sovereign governments and their agencies and instrumentalities, authorities and political subdivisions; (2) other short-term high quality rated debt securities or, if unrated, determined to be of comparable quality in the opinion of the Advisor; (3) commercial paper; (4) bank obligations, including negotiable certificates of deposit, time deposits and bankers' acceptances; and (5) repurchase agreements. Short-term investments may also include shares of money market mutual funds. To the extent the fund invests in such instruments, the fund will not be pursuing its investment objective. However, portfolio management may choose to not use these strategies for various reasons, even in volatile market conditions.

■

Portfolio management measures credit quality at the time it buys securities, using independent rating agencies or, for unrated securities, its own judgment. All securities must meet the credit quality standards applied by portfolio management at the time they are purchased. If a security’s credit quality changes, portfolio management will decide what to do with the security, based on its assessment of what would most benefit the fund.

Prospectus August 1, 2024

13

Fund Details

■

From time to time, the fund may have a concentration of shareholder accounts holding a significant percentage of shares outstanding. Investment activities of these shareholders could have a material impact on the fund.

■

Your fund assets may be at risk of being transferred to the appropriate state if you fail to maintain a valid address and/or if certain activity does not occur in your account within the time specified by state abandoned property law. Contact your financial representative or the transfer agent for additional information.

■

Shareholders of the fund (which may include affiliated and/or non-affiliated registered investment companies that invest in the fund) may make relatively large redemptions or purchases of fund shares. These transactions may cause the fund to have to sell securities or invest additional cash, as the case may be. While it is impossible to predict the overall impact of these transactions over time, there could be adverse effects on the fund’s performance to the extent that the fund may be required to sell securities or invest cash at times when it would not otherwise do so. These transactions could adversely impact the fund’s liquidity, accelerate the recognition of taxable income if sales of securities resulted in capital gains or other income and increase transaction costs, which may adversely affect the fund’s performance. These transactions could also adversely impact the fund’s ability to implement its investment strategies and pursue its investment objective, and, as a result, a larger portion of the fund’s assets may be held in cash or cash equivalents. In addition, large redemptions could significantly reduce the fund’s assets, which may result in an increase in the fund’s expense ratio on account of expenses being spread over a smaller asset base and/or the loss of fee breakpoints.

This prospectus doesn’t tell you about every policy or risk of investing in the fund. If you want more information on the fund’s allowable securities and investment practices and the characteristics and risks of each one, you may want to request a copy of the Statement of Additional Information (the back cover tells you how to do this).

Keep in mind that there is no assurance that the fund will achieve its investment objective.

A complete list of the fund’s portfolio holdings as of the month-end is posted on dws.com on or after the last day of the following month. More frequent posting of portfolio holdings information may be made from time to time on dws.com. The posted portfolio holdings information is available by fund and generally remains accessible at least until the date on which the fund files its Form N-CSR or publicly available Form N-PORT with the SEC for the period that includes the date as of which the posted information is current. The fund’s Statement of Additional Information includes a description of the fund’s policies and procedures with respect to the disclosure of the fund’s portfolio holdings.

Who Manages and Oversees the Fund