As filed with the Securities and Exchange Commission on March 22, 2019

1933 Act File No. [ ]

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-14

REGISTRATION STATEMENT UNDER THE

SECURITIES ACT OF 1933

oPre-Effective Amendment No. o Post-Effective Amendment No.

(Check appropriate box or boxes)

Touchstone Strategic Trust

(Exact Name of Registrant as Specified in Charter)

1-800-543-0407

(Area Code and Telephone Number)

303 Broadway, Suite 1100, Cincinnati, Ohio 45202

(Address of Principal Executive Offices: Number, Street, City, State, Zip Code)

Jill T. McGruder

303 Broadway, Suite 1100

Cincinnati, Ohio 45202

(Name and Address of Agent for Service)

Copies to:

Deborah Bielicke Eades, Esq.

Vedder Price P.C.

222 North LaSalle Street

Chicago, Illinois 60601

(312) 609-7661

Renee M. Hardt, Esq.

Vedder Price P.C.

222 North LaSalle Street

Chicago, Illinois 60601

(312) 609-7616

Approximate Date of Proposed Public Offering: As soon as practicable after this Registration Statement becomes effective under the Securities Act of 1933, as amended.

Title of Securities Being Registered: Class A, Class C, and Class Y shares of beneficial interest, no par value per share, of Touchstone Dynamic Diversified Income Fund, a series of the Registrant, are being registered. No filing fee is due because Registrant is relying on Section 24(f) of the Investment Company Act of 1940, as amended.

It is proposed that this filing will become effective on April 22, 2019, pursuant to Rule 488 under the Securities Act of 1933.

______________________________________________________________________________________________________

TOUCHSTONE CONTROLLED GROWTH WITH INCOME FUND

a series of

TOUCHSTONE STRATEGIC TRUST

303 Broadway, Suite 1100

Cincinnati, Ohio 45202

(800) 543-0407

a series of

TOUCHSTONE STRATEGIC TRUST

303 Broadway, Suite 1100

Cincinnati, Ohio 45202

(800) 543-0407

[•], 2019

Dear Shareholder:

We have important information concerning your investment in the Touchstone Controlled Growth with Income Fund (the “Target Fund”), a series of Touchstone Strategic Trust (the “Trust”). As a shareholder of the Target Fund, we wish to inform you that the Board of Trustees of the Trust (the “Board”) has approved the reorganization of the Target Fund into the Touchstone Dynamic Diversified Income Fund (the “Acquiring Fund,” and together with the Target Fund, the “Funds”), another series of the Trust (the “Reorganization”).

The Reorganization is intended to eliminate the offering of multiple funds with similar investment goals and similar principal investment strategies, and has the potential to provide efficiencies, enhanced marketability and economies of scale for the combined Fund.

Pursuant to an Agreement and Plan of Reorganization, the Target Fund will transfer all of its assets and liabilities to the Acquiring Fund. As a result of the Reorganization, you will receive shares of the Acquiring Fund that will have a total value equal to the total value of your shares in the Target Fund as of the close of business on the closing date of the Reorganization. The Target Fund will then cease operations and liquidate. The Reorganization is expected to be completed on or about May 10, 2019.

The following table shows the share class of the Acquiring Fund that will be issued to each corresponding share class of the Target Fund.

Target Fund and Share Classes | Acquiring Fund and Share Classes |

Touchstone Controlled Growth with Income Fund, a series of the Trust | Touchstone Dynamic Diversified Income Fund, a series of the Trust |

Class A Class C Class Y | Class A Class C Class Y |

Shareholder approval is not required to effect the Reorganization. We have enclosed a Prospectus/Information Statement that describes the Reorganization proposal in greater detail, as well as important information about the Acquiring Fund.

Sincerely,

Jill T. McGruder

President

Touchstone Strategic Trust

QUESTIONS & ANSWERS

We recommend that you read the enclosed Prospectus/Information Statement. In addition to the detailed information in the Prospectus/Information Statement, the following questions and answers provide an overview of key features of the Reorganization.

Q. | Why are we sending you the Prospectus/Information Statement? |

A. | On February 12, 2019, the Board of Trustees of the Trust (the “Board”) approved the Reorganization of the Target Fund into the Acquiring Fund. The Reorganization does not require approval by shareholders. The Prospectus/Information Statement provides important information regarding the Reorganization and the Acquiring Fund that you should consider carefully. |

Q. | What will happen to my existing shares? |

A. | Immediately after the Reorganization, you will own shares of the Acquiring Fund that are equal in total value to the shares of the Target Fund that you hold as of the close of business on the date of the Reorganization (although the number of shares and the net asset value per share may be different). |

Q. | How do the fees and expenses of the Funds compare? |

A. | The advisory fee rate of the combined Fund after the Reorganization will be the same as the advisory fee rate for each of the Funds prior to the Reorganization. For Classes A and C shares, the Funds have the same Rule 12b-1 fees and sales charges. Class Y shares of each Fund are not subject to any Rule 12b-1 fees or sales charges. |

In addition, each Fund has entered into an expense limitation agreement with Touchstone Advisors, Inc. (“Touchstone Advisors”), each Fund’s investment advisor. Touchstone Advisors has contractually agreed to waive a portion of its fees and reimburse certain Fund expenses in order to limit annual fund operating expenses for each Fund. The expense limitation and fee structure for each share class of the Acquiring Fund is the same as the expense limitation and fee structure for the corresponding share class of the Target Fund. The expense limitation agreement is effective through April 29, 2020 for each Fund. In addition, as of the most recent fiscal year end, the annual fund operating expenses of Class A, Class C and Class Y shares of the Acquiring Fund, as a percentage of average net assets, are lower than the annual fund operating expenses of the corresponding class of shares of the Target Fund.

The section titled “Summary—Reorganization—How do the Funds’ fees and expenses compare?” of the Prospectus/Information Statement compares the fees and expenses of the Funds in detail and the section titled “The Funds’ Management—Expense Limitation Agreement” provides additional information regarding the expense limitation agreements.

Q. | How do the Funds’ investment goals and principal investment strategies compare? |

A. | The investment goals and principal investment strategies of the Funds are similar, and both Funds are managed by the same sub-advisor Wilshire Associates Incorporated (“Wilshire” or “Sub-Advisor”). The section of the Prospectus/Information Statement titled “Summary—Reorganization—How do the Funds’ investment goals and principal investment strategies compare?” describes the investment goal and principal investment strategies of the Target Fund and the investment goal and principal investment strategies of the Acquiring Fund. |

Q. | Will I have to pay federal income taxes as a result of the Reorganization? |

A. | You are not expected to recognize any gain or loss for federal income tax purposes on the exchange of your shares of the Target Fund for shares of the Acquiring Fund. The Reorganization is intended to qualify as a tax-free reorganization for federal income tax purposes. The sections of the Prospectus/Information Statement titled “Summary—Reorganization—What will be the primary federal income tax consequences |

of the Reorganization?” and “Information About the Reorganization—Material Federal Income Tax Consequences” provide additional information regarding the federal income tax consequences of the Reorganization.

After the Reorganization, it is expected that the Acquiring Fund will sell a portion of the Target Fund’s portfolio received in the Reorganization. If such transition had occurred as of December 31, 2018, the Acquiring Fund would have sold approximately 60% (or $28 million) of the Target Fund’s investment portfolio. The Acquiring Fund may realize gains as a result of such repositioning, which may increase the net investment income and net capital gains to be distributed by the Acquiring Fund as a taxable dividend to its shareholders after the Reorganization. For more information, please see the sections of the Prospectus/Information Statement titled “Summary—Reorganization—What will be the primary federal income tax consequences of the Reorganization?,” “Summary—Reorganization—Will there be any repositioning costs?” and “Information About the Reorganization—Material Federal Income Tax Consequences.”

Q. | Who will manage the Acquiring Fund after the Reorganization? |

A. | Touchstone Advisors serves as the investment advisor to both Funds. Wilshire serves as the investment sub-advisor to both Funds and Nathan Palmer, CFA, and Anthony Wicklund, CFA, CAIA, the current portfolio managers of the Funds, will continue to serve as the Acquiring Fund’s portfolio managers. For more information please see the sections of the Prospectus/Information Statement titled “Summary—Reorganization—Who will be the Advisor, Sub-Advisor, and Portfolio Managers of my Fund after the Reorganization?,” “The Funds’ Management—Investment Advisor” and “The Funds’ Management—Sub-Advisor and Portfolio Managers.” |

Q. | Will I have to pay any sales load, commission, or other similar fee in connection with the Reorganization? |

A. | No, you will not pay any sales load, commission, or other similar fee in connection with the shares of the Acquiring Fund you will receive in the Reorganization, and any contingent deferred sales charge (“CDSC”) holding period on your shares of the Target Fund will carry over to the shares of the Acquiring Fund that you receive in the Reorganization. However, following the Reorganization, additional purchases, exchanges and redemptions of shares of the Acquiring Fund will be subject to any applicable sales loads, commissions, and other similar fees. |

Q. | Who will pay the costs of the Reorganization? |

A. | Touchstone Advisors will pay the costs of the Reorganization (other than brokerage transaction costs associated with portfolio repositioning) whether or not the Reorganization is completed. For a discussion of brokerage transaction costs associated with portfolio repositioning, please see the sections of the Prospectus/Information Statement titled “Summary—Reorganization—Will there be any repositioning costs?” |

Q. | What if I redeem my shares before the Reorganization takes place? |

A. | If you choose to redeem your shares before the Reorganization takes place, then the redemption will be treated as a normal sale of shares and, generally, will be a taxable transaction. |

Q. | Why is no shareholder action necessary? |

A. | The Trust’s Declaration of Trust provides that any series may be reorganized into another series by a vote of a majority of the trustees of the Trust without the approval of shareholders. In addition, the Reorganization of the Target Fund into the Acquiring Fund satisfies the requisite conditions of Rule 17a-8 under the Investment Company Act of 1940, as amended (the “1940 Act”), such that shareholder approval is not required by the 1940 Act. |

Q. | When will the Reorganization occur? |

A. | The Reorganization is expected to be completed on or about May 10, 2019. |

Q. | Who should I contact for more information? |

A. | You can contact Shareholder Services at (800) 543-0407 for more information. |

The information contained in this Prospectus/Information Statement is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This Prospectus/Information Statement is not an offer to sell these securities, and it is not a solicitation of an offer to buy these securities, in any jurisdiction where the offer or sale is not permitted.

SUBJECT TO COMPLETION

DATED MARCH 22, 2019

PROSPECTUS/INFORMATION STATEMENT

[•], 2019

TOUCHSTONE CONTROLLED GROWTH WITH INCOME FUND

TOUCHSTONE DYNAMIC DIVERSIFIED INCOME FUND

each, a series of

TOUCHSTONE STRATEGIC TRUST

303 Broadway, Suite 1100

Cincinnati, Ohio 45202

(800) 543-0407

TOUCHSTONE DYNAMIC DIVERSIFIED INCOME FUND

each, a series of

TOUCHSTONE STRATEGIC TRUST

303 Broadway, Suite 1100

Cincinnati, Ohio 45202

(800) 543-0407

This Prospectus/Information Statement is being furnished to shareholders of the Touchstone Controlled Growth with Income Fund (the “Target Fund”), a series of Touchstone Strategic Trust (the “Trust”), in connection with an Agreement and Plan of Reorganization (the “Plan”) between the Target Fund and the Touchstone Dynamic Diversified Income Fund (the “Acquiring Fund”), a series of the Trust, providing for (i) the transfer of all the assets of the Target Fund to the Acquiring Fund in exchange solely for Class A, Class C and Class Y shares of the Acquiring Fund and the assumption by the Acquiring Fund of all the liabilities of the Target Fund; and (ii) the pro rata distribution by class of the Acquiring Fund’s shares to the Target Fund’s shareholders in complete liquidation and termination of the Target Fund (the “Reorganization”).

The Board of Trustees of the Trust (the “Board”) has approved the proposed Reorganization. In the Reorganization, you will receive shares of the Acquiring Fund in an amount equal in value to the shares of the Target Fund that you hold as of the close of business on the date of the Reorganization (although the number of shares and the net asset value per share may be different). The Reorganization is expected to be completed on or about May 10, 2019.

This Prospectus/Information Statement is first being sent to shareholders of the Target Fund on or about [__], 2019.

Each of the Target Fund and the Acquiring Fund is a series of a registered open-end investment company (mutual fund). The Target Fund and the Acquiring Fund are sometimes referred to in this Prospectus/Information Statement individually as a “Fund” and collectively as the “Funds.”

This Prospectus/Information Statement, which you should read carefully and retain for future reference, concisely presents the information that you should know about the Funds and the Reorganization. This document also serves as a prospectus for the offering and issuance of shares of the Acquiring Fund to be issued in the Reorganization. A Statement of Additional Information (“SAI”) dated [__], 2019 relating to this Prospectus/Information Statement and the Reorganization has been filed with the U.S. Securities and Exchange Commission (the “SEC”) and is incorporated by reference into this Prospectus/Information Statement (meaning it is legally a part of this Prospectus/Information Statement).

Additional information concerning the Target Fund and the Acquiring Fund is contained in the documents described below, all of which have been filed with the SEC.

THIS IS NOT A PROXY STATEMENT. WE ARE NOT ASKING YOU FOR A PROXY AND YOU ARE REQUESTED NOT TO SEND US A PROXY.

Information About the Target Fund and the Acquiring Fund: | How to Obtain this Information: | |

Prospectus 1. Prospectus relating to the Touchstone Controlled Growth with Income Fund and the Touchstone Dynamic Diversified Income Fund dated April 30, 2018, as supplemented through the date of this Prospectus/Information Statement (File No. 002-80859). Statement of Additional Information 1. SAI relating to the Touchstone Controlled Growth with Income Fund and the Touchstone Dynamic Diversified Income Fund dated April 30, 2018, as supplemented through the date of this Prospectus/Information Statement (File No. 002-80859). Annual Report 1. Annual Report relating to the Touchstone Controlled Growth with Income Fund and Touchstone Dynamic Diversified Income Fund for the fiscal year ended December 31, 2018 (File No. 811-03651). | Copies are available upon request and without charge if you: · Write to Touchstone Strategic Trust, P.O. Box 9878, Providence, Rhode Island 02940; or · Call (800) 543-0407 toll-free; or · Download a copy from TouchstoneInvestments.com/Resources. | |

You can also obtain copies of any of the above-referenced documents without charge on the EDGAR database on the SEC’s Internet site at http://www.sec.gov. Copies are available for a fee by electronic request at the following e-mail address: publicinfo@sec.gov.

This Prospectus/Information Statement sets forth the information shareholders of the Target Fund should know before the Reorganization (in effect, investing in shares of the Acquiring Fund) and constitutes an offering of shares of beneficial interest, without par value per share, of the Acquiring Fund. Please read this Prospectus/Information Statement carefully and retain it for future reference.

THE SEC HAS NOT DETERMINED THAT THE INFORMATION IN THIS PROSPECTUS/ INFORMATION STATEMENT IS ACCURATE OR ADEQUATE, NOR HAS IT APPROVED OR DISAPPROVED THESE SECURITIES. ANYONE WHO TELLS YOU OTHERWISE IS COMMITTING A CRIMINAL OFFENSE.

An investment in the Acquiring Fund:

• | is not a deposit of, or guaranteed by, any bank |

• | is not insured by the FDIC, the Federal Reserve Board or any other government agency |

• | is not endorsed by any bank or government agency |

• | involves investment risk, including possible loss of your original investment |

TABLE OF CONTENTS

Page | |

SUMMARY | 1 |

Background | 1 |

Reorganization | 1 |

Principal Risks | 10 |

INFORMATION ABOUT THE REORGANIZATION | 15 |

Reasons for the Reorganization | 15 |

Agreement and Plan of Reorganization | 16 |

Description of the Securities to be Issued | 16 |

Material Federal Income Tax Consequences | 16 |

Pro Forma Capitalization | 19 |

THE FUNDS’ MANAGEMENT | 20 |

Investment Advisor | 20 |

Sub-Advisor and Portfolio Managers | 21 |

Advisory and Sub-Advisory Agreement Approval | 21 |

Expense Limitation Agreement | 21 |

Other Service Providers | 22 |

CHOOSING A CLASS OF SHARES | 22 |

Class A Shares | 22 |

Class C Shares | 23 |

Class Y Shares | 24 |

Buying and Selling Fund Shares | 24 |

Exchange Privileges of the Funds | 25 |

Distribution Policy | 25 |

DISTRIBUTION AND SHAREHOLDER SERVICING ARRANGEMENTS | 25 |

INFORMATION ON SHAREHOLDERS’ RIGHTS | 26 |

FINANCIAL STATEMENTS AND EXPERTS | 28 |

LEGAL MATTERS | 29 |

ADDITIONAL INFORMATION | 29 |

FINANCIAL HIGHLIGHTS | 29 |

EXHIBIT A: FORM OF AGREEMENT AND PLAN OF REORGANIZATION | A-1 |

EXHIBIT B: FUNDAMENTAL INVESTMENT LIMITATIONS | B-1 |

EXHIBIT C: CONTROL PERSONS AND PRINCIPAL HOLDERS OF SECURITIES | C-1 |

i | ||

SUMMARY

This section summarizes the primary features of the Reorganization. It may not contain all of the information that is important to you. To understand the Reorganization, you should read this entire Prospectus/Information Statement and the exhibits. This summary is qualified in its entirety by reference to the additional information contained elsewhere in this Prospectus/Information Statement, the SAI, and the Plan, a form of which is attached to this Prospectus/Information Statement as Exhibit A.

Background

The inception date of the Target Fund and the Acquiring Fund was September 30, 2004. As of December 31, 2018, the Target Fund had total assets of $47.5 million. As of December 31, 2018, the Acquiring Fund had total assets of $48.0 million.

Reorganization

What are the reasons for the Reorganization?

At a meeting on February 12, 2019, the Board, including those trustees who are not “interested persons,” as such term is defined in the Investment Company Act of 1940, as amended (the “1940 Act”) (the “Independent Trustees”), determined that the Reorganization was in the best interests of the Funds and that the interests of existing shareholders of the Funds will not be diluted as a result of the Reorganization. The Board approved the Reorganization.

The Reorganization is intended to eliminate the offering of multiple funds with similar investment goals and similar principal investment strategies, and has the potential to provide efficiencies, enhanced marketability and economies of scale for the combined Fund. The Board considered the following factors, among others: the investment goals, principal investment strategies, sub-advisor and portfolio managers of the Funds; the historical investment performance record of the Funds; the advice and recommendation of Touchstone Advisors, Inc. (“Touchstone Advisors”), including its opinion that the Reorganization would be in the best interests of the Funds and that the combined Fund would have enhanced marketability and a greater opportunity to achieve economies of scale than either Fund operating individually; and the investment advisory fee and other fees paid by the Funds, the expense ratios of the Funds and the contractual limitations on the Funds’ expenses.

For more information, please see the section titled “Information About the Reorganization—Reasons for the Reorganization.”

What are the key features of the Reorganization?

The Plan sets forth the key features of the Reorganization. The Plan provides for the following:

• | the transfer of all the assets of the Target Fund to the Acquiring Fund in exchange solely for Class A, Class C and Class Y shares of the Acquiring Fund and the assumption by the Acquiring Fund of all the liabilities of the Target Fund; |

• | the pro rata distribution by class of the Acquiring Fund's shares to the Target Fund shareholders in complete liquidation and termination of the Target Fund; and |

• | the receipt of an opinion of counsel that the Reorganization qualifies as a tax-free reorganization for federal income tax purposes. |

The Reorganization is expected to be completed on or about May 10, 2019.

1 | ||

After the Reorganization, what shares of the Acquiring Fund will I own?

Each Fund is a series of a registered open-end management investment company (i.e., a mutual fund). In the Reorganization, you will receive the same class of shares in the Acquiring Fund as you currently own in the Target Fund. The Acquiring Fund shares you receive will have the same total value as your shares of the Target Fund, in each case measured as of the close of business on the date of the Reorganization.

How do the Funds’ fees and expenses compare?

Comparative Fee Tables. The following tables allow you to compare the various fees and expenses that you may pay for buying and holding shares of each Fund. Pro forma expenses project anticipated expenses of the Acquiring Fund following the Reorganization. Actual expenses may be greater or less than those shown. The shareholder transaction expenses presented below show the maximum sales charge (load) on purchases of Fund shares as a percentage of offering price. The Target Fund shareholders will not pay any front-end sales charge on any shares of the Acquiring Fund received as part of the Reorganization. However, the holding period related to any contingent deferred sales charge (“CDSC”) applicable to shares of the Target Fund will carry over to shares of the Acquiring Fund received as part of the Reorganization. You may qualify for sales charge discounts for Class A shares if you and your family invest, or agree to invest in the future, at least $25,000 in the Funds. More information about these and other discounts is available from your financial professional, in the section titled “Choosing a Class of Shares—Class A Shares” below, and in the Funds' prospectus (dated April 30, 2018) in the section titled Appendix A–Intermediary-Specific Sales Charge Waivers and Discounts and on page 43 of the Funds' SAI (dated April 30, 2018) in the section titled “Choosing a Class of Shares”. If you purchase Class Y shares through a broker acting solely as an agent on behalf of its customers, that broker may charge you a commission. Such commissions, if any, are not charged by the Fund and are not reflected in the fee table or expense example below. Expense ratios reflect annual fund operating expenses for the twelve months ended December 31, 2018 for the Target Fund and the Acquiring Fund. Pro forma numbers are estimated as if the Reorganization had been completed as of December 31, 2018 and do not include the estimated costs of the Reorganization, which will be borne by Touchstone Advisors and not the Funds, or the costs of portfolio repositioning.

Touchstone Controlled Growth with Income Fund Class A | Touchstone Dynamic Diversified Income Fund Class A | Acquiring Fund after Reorganization (pro forma combined) Class A | ||||

Shareholder Fees (fees paid directly from your investment) | ||||||

Maximum Sales Charge (Load) Imposed on Purchases (as a percentage of offering price) | 5.00% | 5.00% | 5.00% | |||

Maximum Deferred Sales Charge (Load) (as a percentage of original purchase price or the amount redeemed, whichever is less) | None | None | None | |||

Wire Redemption Fee | Up to $15 | Up to $15 | Up to $15 | |||

Annual Fund Operating Expenses (expenses that you pay each year as a % of the value of your investment) | ||||||

Management Fees | 0.20% | 0.20% | 0.20% | |||

Distribution and/or Shareholder Service (12b-1) Fees | 0.25% | 0.25% | 0.25% | |||

Other Expenses | 0.59% | 0.48% | 0.43%(1) | |||

Acquired Fund Fees and Expenses (AFFE) | 1.32% | 0.73% | 0.73%(1) | |||

Total Annual Fund Operating Expenses | 2.36%(2) | 1.66%(2) | 1.61% | |||

Fee Waiver or Expense Reimbursement(3) | (0.55)% | (0.44)% | (0.39)% | |||

Total Annual Fund Operating Expenses After Fee Waiver or Expense Reimbursement(3) | 1.81%(2) | 1.22%(2) | 1.22% | |||

2 | ||

Touchstone Controlled Growth with Income Fund Class C | Touchstone Dynamic Diversified Income Fund Class C | Acquiring Fund after Reorganization (pro forma combined) Class C | ||||

Shareholder Fees (fees paid directly from your investment) | ||||||

Maximum Deferred Sales Charge (Load) (as a percentage of original purchase price or the amount redeemed, whichever is less) | 1.00% | 1.00% | 1.00% | |||

Wire Redemption Fee | Up to $15 | Up to $15 | Up to $15 | |||

Annual Fund Operating Expenses (expenses that you pay each year as a % of the value of your investment) | ||||||

Management Fees | 0.20% | 0.20% | 0.20% | |||

Distribution or Service (12b-1) Fees | 1.00% | 1.00% | 1.00% | |||

Other Expenses | 0.73% | 0.52% | 0.46%(1) | |||

Acquired Fund Fees and Expenses (AFFE) | 1.32% | 0.73% | 0.73%(1) | |||

Total Annual Fund Operating Expenses | 3.25%(2) | 2.45%(2) | 2.39% | |||

Fee Waiver or Expense Reimbursement(3) | (0.69)% | (0.48)% | (0.42)% | |||

Total Annual Fund Operating Expenses After Fee Waiver or Expense Reimbursement(3) | 2.56%(2) | 1.97%(2) | 1.97% | |||

Touchstone Controlled Growth with Income Fund Class Y | Touchstone Dynamic Diversified Income Fund Class Y | Acquiring Fund after Reorganization (pro forma combined) Class Y | ||||

Shareholder Fees (fees paid directly from your investment) | ||||||

Maximum Deferred Sales Charge (Load) (as a percentage of original purchase price or the amount redeemed, whichever is less) | None | None | None | |||

Wire Redemption Fee | Up to $15 | Up to $15 | Up to $15 | |||

Annual Fund Operating Expenses (expenses that you pay each year as a % of the value of your investment) | ||||||

Management Fees | 0.20% | 0.20% | 0.20% | |||

Distribution or Service (12b-1) Fees | None | None | None | |||

Other Expenses | 0.57% | 0.83% | 0.51%(1) | |||

Acquired Fund Fees and Expenses (AFFE) | 1.32% | 0.73% | 0.73%(1) | |||

Total Annual Fund Operating Expenses | 2.09%(2) | 1.76%(2) | 1.44% | |||

Fee Waiver or Expense Reimbursement(3) | (0.53)% | (0.79)% | (0.47)% | |||

Total Annual Fund Operating Expenses After Fee Waiver or Expense Reimbursement(3) | 1.56%(2) | 0.97%(2) | 0.97% | |||

__________________________

(1) Other Expenses and Acquired Fund Fees and Expenses are estimated based on fees and expenses of the Acquiring Fund assuming the Reorganization had been consummated as of the beginning of the twelve-month period ended December 31, 2018.

(2) Total Annual Fund Operating Expenses have been restated to reflect Acquired Fund Fees and Expenses and will differ from the ratio of expenses to average net assets that is included in the Fund's annual report for the fiscal year ended December 31, 2018.

(3) Touchstone Advisors and the Trust have entered into a contractual expense limitation agreement whereby Touchstone Advisors will waive a portion of its fees or reimburse certain Fund expenses (excluding dividend and

3 | ||

interest expenses relating to short sales; interest; taxes; brokerage commissions and other transaction costs; portfolio transaction and investment related expenses, including expenses associated with the Fund's liquidity providers; other expenditures which are capitalized in accordance with U.S. generally accepted accounting principles; the cost of “Acquired Fund Fees and Expenses,” if any; and other extraordinary expenses not incurred in the ordinary course of business) in order to limit annual Fund operating expenses to 0.49%, 1.24% and 0.24% of average daily net assets for Classes A, C and Y shares, respectively. This contractual expense limitation is effective through April 29, 2020, but can be terminated by a vote of the Board if it deems the termination to be beneficial to the Fund’s shareholders. The terms of the contractual expense limitation agreement provide that Touchstone Advisors is entitled to recoup, subject to approval by the Board, such amounts waived or reimbursed for a period of up to three years from the date on which the Advisor reduced its compensation or assumed expenses for the Fund. The Fund will make repayments to the Advisor only if such repayment does not cause the annual fund operating expenses (after the repayment is taken into account) to exceed both (1) the expense cap in place when such amounts were waived or reimbursed and (2) the Fund’s current expense limitation. See the discussion entitled “The Funds’ Management—Expense Limitation Agreement” in this Prospectus/Information Statement for more information.

Expense Example. The example is intended to help you compare the cost of investing in each Fund and the Acquiring Fund (pro forma), assuming the Reorganization takes place. The example assumes that you invest $10,000 for the time periods indicated and redeem all of your shares at the end of those periods. The example also assumes that your investment has a 5% return each year, that the operating expenses remain as shown above and that the contractual expense limitation agreement for the Acquiring Fund after the Reorganization (pro forma) is in place for the first year. Although your actual costs may be higher or lower, based on these assumptions your costs would be:

Assuming Redemption | |||||||||||

Classes | 1 Year | 3 Years | 5 Years | 10 Years | |||||||

Class A | |||||||||||

Touchstone Controlled Growth with Income Fund | $ | 675 | $ | 1,150 | $ | 1,650 | $ | 3,021 | |||

Touchstone Dynamic Diversified Income Fund | $ | 618 | $ | 956 | $ | 1,318 | $ | 2,332 | |||

Acquiring Fund after Reorganization (Pro Forma Combined) | $ | 618 | $ | 946 | $ | 1,297 | $ | 2,284 | |||

Class C | |||||||||||

Touchstone Controlled Growth with Income Fund | $ | 359 | $ | 937 | $ | 1,638 | $ | 3,502 | |||

Touchstone Dynamic Diversified Income Fund | $ | 300 | $ | 718 | $ | 1,262 | $ | 2,750 | |||

Acquiring Fund after Reorganization (Pro Forma Combined) | $ | 300 | $ | 705 | $ | 1,238 | $ | 2,694 | |||

Class Y | |||||||||||

Touchstone Controlled Growth with Income Fund | $ | 159 | $ | 604 | $ | 1,075 | $ | 2,379 | |||

Touchstone Dynamic Diversified Income Fund | $ | 99 | $ | 477 | $ | 880 | $ | 2,008 | |||

Acquiring Fund after Reorganization (Pro Forma Combined) | $ | 99 | $ | 409 | $ | 742 | $ | 1,684 | |||

Assuming No Redemption | |||||||||||

Class | 1 Year | 3 Years | 5 Years | 10 Years | |||||||

Class C | |||||||||||

Touchstone Controlled Growth with Income Fund | $ | 259 | $ | 937 | $ | 1,638 | $ | 3,502 | |||

Touchstone Dynamic Diversified Income Fund | $ | 200 | $ | 718 | $ | 1,262 | $ | 2,750 | |||

Acquiring Fund after Reorganization (Pro Forma Combined) | $ | 200 | $ | 705 | $ | 1,238 | $ | 2,694 | |||

4 | ||

Portfolio Turnover. Each Fund pays transaction costs, such as brokerage commissions, when it buys and sells securities (or “turns over” its portfolio). A higher portfolio turnover rate may indicate higher transaction costs and may result in higher taxes when Fund shares are held in a taxable account. These costs, which are not reflected in Total Annual Fund Operating Expenses or in the Example, affect the Funds’ performance. As of its most recent fiscal year end, the portfolio turnover rates for the Target Fund and the Acquiring Fund were 62% and 20%, respectively.

How do the Funds’ performance records compare?

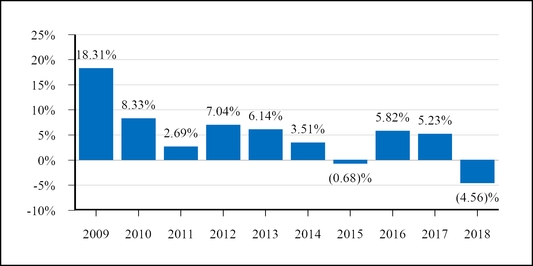

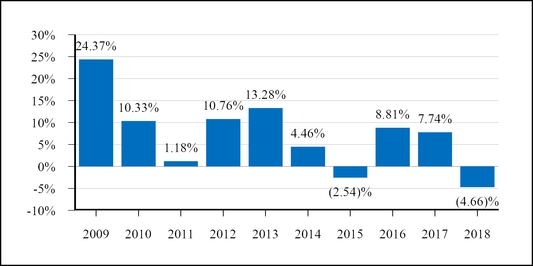

The bar charts and performance tables below illustrate some indication of the risks of investing in the Funds by showing changes in the Funds’ performance from year to year as compared to each of ICE BofA Merrill Lynch 3-Month U.S. Treasury Bill Index and Wilshire Liquid Alternative IndexSM (the current benchmark indexes for the Target Fund) and the Bloomberg Barclays U.S. Aggregate Bond Index and MSCI All Country World Index (ACWI) (the current benchmark indexes for the Acquiring Fund). The bar charts do not reflect any sales charges, which would reduce your return. The performance table does reflect any applicable sales charges. Past performance (before and after taxes) does not indicate how the Funds will perform in the future. On November 23, 2015, each Fund changed its name, principal investment strategies and sub-advisor. Consequently, prior period performance may have been different if the Funds had not been managed by the prior sub-advisor using that sub-advisor’s asset allocation strategy. Updated performance is available at no cost by visiting TouchstoneInvestments.com or by calling (800) 543-0407.

Touchstone Controlled Growth with Income Fund—Class A Shares Total Return as of December 31

Best Quarter: Second Quarter 2009 9.23% | Worst Quarter: Fourth Quarter 2018 (5.79)% |

After-tax returns are calculated using the historical highest individual federal marginal income tax rates and do not reflect the impact of state and local taxes. Your after-tax returns may differ from those shown and depend on your tax situation. The after-tax returns do not apply to shares held in an IRA, 401(k), or other tax-advantaged account. After-tax returns are only shown for Class A shares and after-tax returns for other classes will vary.

5 | ||

Average Annual Total Returns

For the periods ended December 31, 2018

For the periods ended December 31, 2018

1 Year | 5 Years | 10 Years | |||||

Touchstone Controlled Growth with Income Fund—Class A | |||||||

Return Before Taxes | (10.07) | % | 0.58 | % | 4.41 | % | |

Return After Taxes on Distributions | (10.75) | % | (0.31) | % | 3.20 | % | |

Return After Taxes on Distributions and Sale of Fund Shares(1) | (5.75) | % | 0.17 | % | 3.03 | % | |

Touchstone Controlled Growth with Income Fund—Class C | |||||||

Return Before Taxes | (6.26) | % | 1.01 | % | 4.24 | % | |

Touchstone Controlled Growth with Income Fund—Class Y | |||||||

Return Before Taxes | (4.32) | % | 2.05 | % | 5.30 | % | |

ICE BofA Merrill Lynch 3-Month U.S. Treasury Bill Index (reflects no deduction for fees, expenses or taxes) | 1.87 | % | 0.63 | % | 0.37 | % | |

Wilshire Liquid Alternative IndexSM (reflects no deduction for fees, expenses or taxes) | (4.24) | % | 0.19 | % | 2.28 | % | |

(1) The Return After Taxes on Distributions and Sale of Fund Shares may be greater than other returns for the same period due to a tax benefit of realizing a capital loss on the sale of Fund shares.

Touchstone Dynamic Diversified Income Fund—Class A Shares Total Return as of December 31

Best Quarter: Second Quarter 2009 14.84% | Worst Quarter: Third Quarter 2011 (9.94)% |

After-tax returns are calculated using the historical highest individual federal marginal income tax rates and do not reflect the impact of state and local taxes. Your after-tax returns may differ from those shown and depend on your tax situation. The after-tax returns do not apply to shares held in an IRA, 401(k), or other tax-advantaged account. After-tax returns are only shown for Class A shares and after-tax returns for other classes will vary.

6 | ||

Average Annual Total Returns

For the periods ended December 31, 2018

For the periods ended December 31, 2018

1 Year | 5 Years | 10 Years | |||||

Touchstone Dynamic Diversified Income Fund—Class A | |||||||

Return Before Taxes | (10.16) | % | 1.41 | % | 6.45 | % | |

Return After Taxes on Distributions | (11.47) | % | 0.32 | % | 5.35 | % | |

Return After Taxes on Distributions and Sale of Fund Shares(1) | (5.85) | % | 0.70 | % | 4.75 | % | |

Touchstone Dynamic Diversified Income Fund—Class C | |||||||

Return Before Taxes | (6.25) | % | 1.85 | % | 6.29 | % | |

Touchstone Dynamic Diversified Income Fund—Class Y | |||||||

Return Before Taxes | (4.40) | % | 2.89 | % | 7.36 | % | |

Bloomberg Barclays U.S. Aggregate Bond Index (reflects no deduction for fees, expenses or taxes) | 0.01 | % | 2.52 | % | 3.48 | % | |

MSCI ACWI(2) (reflects no deduction for fees, expenses or taxes) | (9.42) | % | 4.26 | % | 9.46 | % | |

(1) The Return After Taxes on Distributions and Sale of Fund Shares may be greater than other returns for the same period due to a tax benefit of realizing a capital loss on the sale of Fund shares.

(2) The MSCI ACWI returns disclosed are net of withholding taxes.

Will I be able to purchase, redeem, and exchange shares the same way?

Yes, after the Reorganization you will be able to purchase, redeem, and exchange shares of the Acquiring Fund the same way that you purchase, redeem, and exchange shares of the Target Fund. For more information, see the sections titled “Choosing a Class of Shares—Buying and Selling Fund Shares” and “Choosing a Class of Shares—Exchange Privileges of the Funds.”

Will I be able to receive distributions the same way?

Like the Target Fund, the Acquiring Fund intends to distribute to its shareholders substantially all of its net investment income and capital gains. Each Fund declares and pays any net investment income dividends quarterly. Each Fund makes distributions of capital gains, if any, at least annually. After the Reorganization, any income and capital gains will be reinvested in the class of shares of the Acquiring Fund you receive in the Reorganization or, if you have so elected, distributed in cash. Each Fund intends to make distributions that may be taxed as ordinary income or capital gains except when shares are held through a tax-advantaged account, such as a 401(k) plan or an IRA. Withdrawals from a tax-advantaged account, however, may be taxable. For more information, see the section titled “Choosing a Class of Shares—Distribution Policy.”

Who will be the Advisor, Sub-Advisor, and Portfolio Managers of my Fund after the Reorganization?

For each Fund, Touchstone Advisors serves as the investment advisor.

Wilshire Associates Incorporated (“Wilshire” or “Sub-Advisor”) serves as sub-advisor to each Fund, with Nathan Palmer, CFA and Anthony Wicklund, CFA, CAIA serving as portfolio managers.

Nathan Palmer, CFA, Portfolio Manager, is a Managing Director with Wilshire and heads Wilshire Funds Management’s portfolio management group. Mr. Palmer has more than 19 years of industry experience and is responsible for creating multi-asset class, multi-manager investment solutions for financial intermediary clients. Prior to joining Wilshire in 2011, Mr. Palmer provided investment advice to endowment, foundation, and family office clients at Convergent Wealth Advisors since 2009.

Anthony Wicklund, CFA, CAIA, Portfolio Manager, is a Managing Director with Wilshire and a Portfolio Manager with Wilshire Funds Management. Mr. Wicklund has more than 16 years of industry experience and is a Portfolio

7 | ||

Manager for multi-manager portfolios, including target-risk, target-date, and alternative portfolios for a range of financial intermediary clients. Prior to joining Wilshire in 2013, Mr. Wicklund was the Director of Risk Management at Convergent Wealth Advisors, where he led the firm’s investment risk management and operational due diligence efforts since 2006.

After the Reorganization, Touchstone Advisors will continue to serve as investment advisor to the Acquiring Fund, with Wilshire and Messrs. Palmer and Wicklund continuing in their capacity as sub-advisor and portfolio managers, respectively.

For additional information regarding Touchstone Advisors, the sub-advisor, and the portfolio managers, please see the section titled “The Funds’ Management—Investment Advisor” and “The Funds’ Management—Sub-Advisor and Portfolio Managers.”

What will be the primary federal income tax consequences of the Reorganization?

The Reorganization is expected to qualify as a tax-free reorganization for federal income tax purposes. If the Reorganization so qualifies, then generally no gain or loss will be recognized for federal income tax purposes by the Funds or their respective shareholders as a direct result of the Reorganization. As a condition to the closing of the Reorganization, the Funds will each receive an opinion from the law firm of Vedder Price P.C. that the Reorganization qualifies as a tax-free reorganization within the meaning of Section 368(a) of the United States Internal Revenue Code of 1986, as amended (the “Code”). The opinion, however, is not binding on the Internal Revenue Service (the “IRS”) or any court and thus does not preclude the IRS or a court from taking a contrary position. See “Information About the Reorganization—Material Federal Income Tax Consequences” for more information on the material federal income tax consequences of the Reorganization.

Will there be any repositioning costs?

After the Reorganization, it is expected that the Acquiring Fund will sell a portion of the Target Fund’s portfolio received in the Reorganization. If such transition had occurred as of December 31, 2018, the Acquiring Fund would have sold approximately 60% (or $28 million) of the Target Fund’s investment portfolio. The Acquiring Fund may realize gains as a result of such repositioning, which may increase the net investment income and net capital gains to be distributed by the Acquiring Fund as a taxable dividend to its shareholders after the Reorganization.

It is estimated that portfolio repositioning of the Acquiring Fund, following the Reorganization, would have resulted in brokerage commissions or other transaction costs of approximately $4,275 for the Acquiring Fund, based on average commission rates, if such sales occurred on December 31, 2018, and realized losses of approximately $2.8 million or $(0.38) per share, if the securities had been sold on December 31, 2018. These transaction costs represent expenses of the Acquiring Fund that are not subject to the Fund’s expense cap and will be borne by the Fund and indirectly borne by the Fund’s shareholders (including Target Fund shareholders who receive shares in the Reorganization). The Acquiring Fund may realize gains as a result of such repositioning, which may increase the net investment income and net capital gains to be distributed by the Acquiring Fund as a taxable dividend to its shareholders following the Reorganization.

How do the Funds’ investment goals and principal investment strategies compare?

The Funds have similar investment goals. The Target Fund’s investment goal is to seek to provide investors with growth and income. The Acquiring Fund’s investment goal is to seek to provide investors with current income.

Each Fund is a “fund-of-funds.” The Target Fund seeks to achieve its investment goals by primarily investing in a diversified portfolio of fixed-income, equity-income oriented and alternative underlying funds, and the Acquiring Fund seeks to achieve its investment goal by investing primarily in a diversified portfolio of fixed-income and equity-income oriented underlying funds (although a portion of each Fund’s assets may also be invested in cash, cash equivalents, or in money market funds). A key difference of the Target Fund’s investment strategy from the Acquiring Fund is that the Target Fund will allocate a significant portion of its assets to underlying funds utilizing alternative or non-traditional investment strategies, such as long-short and merger arbitrage strategies.

8 | ||

Each Fund also has identical fundamental investment limitations, which are set forth in Exhibit B.

The following tables describe the investment goals and principal investment strategies of the Target Fund and the Acquiring Fund.

Target Fund | Acquiring Fund | |

Investment Goal | The Fund seeks growth and income. | The Fund seeks current income. |

Principal Investment Strategy | The Target Fund is a “fund-of-funds,” which seeks to achieve its investment goal by investing primarily in a diversified portfolio of underlying equity, fixed-income, and alternative funds (although a portion of its assets may be invested in cash, cash equivalents, or in money market funds). These underlying funds, in turn, invest in a variety of U.S. and foreign equity securities, fixed-income instruments and other investments. The Target Fund will allocate a significant portion of its assets to underlying funds utilizing alternative or non-traditional investment strategies, such as long-short and merger arbitrage strategies. | The Acquiring Fund is a “fund-of-funds,” which seeks to achieve its investment goal by investing primarily in a diversified portfolio of fixed-income and equity-income oriented underlying funds (although a portion of its assets may be invested in cash, cash equivalents, or in money market funds). |

The majority of the underlying funds in which the Target Fund invests will be affiliated funds; however, the Target Fund will have the ability to invest in unaffiliated underlying funds, including ETFs and ETNs, to the extent that the desired asset class exposure is not available through affiliated funds. | The majority of the underlying funds in which the Acquiring Fund invests will be affiliated funds; however, the Acquiring Fund will have the ability to invest in unaffiliated underlying funds, including ETFs and ETNs, to the extent that the desired asset class exposure is not available through affiliated funds. | |

The Target Fund currently expects to allocate 0-25% of its assets to equity funds, 25-50% of its assets to fixed-income funds and 50-75% of its assets to alternative funds. | The Acquiring Fund currently expects to allocate 25-55% of its assets to equity funds, 25-55% of its assets to fixed-income funds and 0-30% of its assets to alternative funds. | |

The Target Fund may invest up to 45% of its assets in any individual underlying fund. Several of the underlying funds in which the Target Fund invests may invest without limit in securities of issuers outside of the United States. As a result, the Target Fund will have exposure to foreign markets. | The Acquiring Fund may invest up to 45% of its assets in any individual underlying fund. Several of the underlying funds in which the Acquiring Fund invests may invest without limit in securities of issuers outside of the United States. As a result, the Acquiring Fund will have exposure to foreign markets (including emerging markets). | |

The Target Fund, through its investment in underlying funds, may also be exposed to equity securities of companies of all market capitalizations, including small-, mid-, and large-cap companies. | The Acquiring Fund, through its investment in underlying funds, may also be exposed to equity securities of companies of all market capitalizations, including small-, mid-, and large-cap companies. | |

9 | ||

Target Fund | Acquiring Fund | |

Though not expected to be a substantial part of the overall strategy of the Target Fund, the Target Fund, through its investment in underlying funds, will gain exposure to additional strategies and instruments of the underlying funds, including: collateralized loan obligations, derivatives (such as futures contracts, options, and swaps), and real estate investments. | Though not expected to be a substantial part of the overall strategy of the Acquiring Fund, the Acquiring Fund, through its investment in underlying funds, will gain exposure to additional strategies and instruments of the underlying funds, including: collateralized loan obligations, derivatives (such as futures contracts, options, and swaps), and real estate investments. | |

The Target Fund’s sub-advisor, Wilshire, seeks to develop an optimal allocation among underlying funds in accordance with these principles: • “Controlled” Growth — seeks growth through lower volatility equities and alternative strategy exposure; • Rising Rate Protection — seeks lower duration and lower bond correlation; • Attractive Income — seeks higher yielding debt to produce attractive income. | The Acquiring Fund’s sub-advisor, Wilshire, seeks to develop an optimal model allocation among underlying funds that seeks to maximize “income efficiency,” or yield achieved per unit of risk. The Acquiring Fund primarily invests in fixed-income and equity-income oriented funds, ETFs, and ETNs and is dynamically managed as yield and volatility environments change. | |

Wilshire and Touchstone Advisors periodically agree on the universe of underlying funds that Wilshire may consider when making allocation decisions. Wilshire, subject to approval by Touchstone Advisors, may change the Target Fund’s target allocation to each asset class, the underlying funds in each asset class (including the addition or removal of funds from the universe of underlying funds), or target allocations to each underlying fund without prior approval from or notice to shareholders. | Wilshire and Touchstone Advisors routinely agree on the universe of underlying funds that Wilshire may consider when making allocation decisions. Wilshire, subject to approval by Touchstone Advisors, may change the Acquiring Fund’s target allocation to each asset class, the underlying funds or other securities in each asset class (including the addition or removal of funds from the universe of underlying funds), or target allocations to each underlying fund without prior approval from or notice to shareholders. | |

Principal Risks

Each Fund’s share price will fluctuate. You could lose money on your investment in each Fund, and each Fund could return less than other investments. As with any mutual fund, there is no guarantee that either Fund will achieve its investment goal. Each Fund is exposed to the risks of the underlying funds in which it invests in direct proportion to the amount of assets a Fund allocates to each underlying fund. To the extent that a Fund invests more of its assets in one underlying fund than another, a Fund will have greater exposure to the risks of that underlying fund. One underlying fund may buy the same security that another underlying fund is selling. You would indirectly bear the costs of both trades. In addition, you may receive taxable gains from portfolio transactions by the underlying funds, as well as taxable gains from a Fund’s transactions in shares of the underlying funds. Each Fund’s ability to achieve its investment goal depends, in part, upon Wilshire’s skill in selecting the best mix of underlying funds. There is the risk that Wilshire’s evaluations and assumptions regarding the underlying funds may be incorrect in view of actual market conditions.

The principal risks of investing in the Funds are similar, as their investment goals are similar and their principal investment strategies are similar. The principal risks of the Funds are set forth below, and such risks apply to both Funds unless otherwise noted. The Target Fund is subject to the following principal risks, which the Acquiring Fund is not: call options risk, covered call options risk and merger arbitrage risk. The Acquiring Fund is subject to the following principal risks, which the Target Fund is not: emerging markets risk, prepayment risk and real estate industry risk.

10 | ||

Call Options Risk (Target Fund Only): Writing index and exchange-traded fund call options is intended to reduce an underlying fund’s volatility and provide income, although it may also reduce an underlying fund’s ability to profit from increases in the value of its equity portfolio.

Collateralized Loan Obligations Risk: Typically, collateralized loan obligations (“CLOs”) are privately offered and sold, and thus are not registered under the securities laws. As a result, an underlying fund may in certain circumstances characterize its investments in CLOs as illiquid. In assessing liquidity, an underlying fund will consider various factors including whether the CLO may be purchased and sold in Rule 144A transactions and whether an active dealer market exists. CLOs are subject to the typical risks associated with debt instruments (i.e., interest rate risk and credit risk). Additional risks of CLOs include the possibility that distributions from collateral securities will be insufficient to make interest or other payments, the potential for a decline in the quality of the collateral, and the possibility that an underlying fund may invest in a subordinate tranche of a CLO.

Convertible Securities Risk: Convertible securities are subject to the risks of both debt securities and equity securities. The values of convertible securities tend to decline as interest rates rise and, due to the conversion feature, tend to vary with fluctuations in the market value of the underlying security.

Counterparty Risk: A counterparty (the other party to a transaction or an agreement or the party with whom an underlying fund executes transactions) to a transaction with an underlying fund may be unable or unwilling to make timely principal, interest or settlement payments, or otherwise honor its obligations.

Covered Call Options Risk (Target Fund Only): Investments in covered calls involve certain risks. These risks include:

• | Limited Gains. When an underlying fund writes a covered call option, the underlying fund makes an obligation to deliver a security it already owns at an agreed-upon strike price on or before a predetermined date in the future in return for a premium. By selling a covered call option, an underlying fund may forego the opportunity to benefit from an increase in the price of the underlying stock above the exercise price, but continues to bear the risk of a decline in the value of the underlying stock. |

• | Lack of Liquidity. If an underlying fund is not able to close out an option transaction, the underlying fund will not be able to sell the underlying security until the option expires or is exercised. Because an underlying fund will generally hold the stocks underlying the call option, an underlying fund may be less likely to sell the stocks in its portfolio to take advantage of new investment opportunities. |

Derivatives Risk: The use of derivatives may expose an underlying fund to additional risks that it would not be subject to if it invested directly in the securities underlying those derivatives. Risks associated with derivatives may include correlation risk, which is the risk that the derivative does not correlate well with the security, index, or currency to which it relates, and the risk that the derivative may not have the intended effects. The use of derivatives to hedge risk may reduce the opportunity for gain by offsetting the positive effect of favorable price movements.

• | Forward Currency Exchange Contract Risk: A forward foreign currency exchange contract is an agreement to buy or sell a specific currency at a future date and at a price set at the time of the contract. Forward foreign currency exchange contracts may reduce the risk of loss from a change in value of a currency, but they also limit any potential gains and do not protect against fluctuations in the value of the underlying position. |

• | Futures Contracts Risk: The risks associated with an underlying fund’s futures positions include liquidity and counterparty risks associated with derivative instruments. |

• | Leverage Risk: Leverage occurs when an underlying fund uses derivatives (such as futures or options), or similar instruments or techniques to gain exposure to investments in an amount that exceeds an underlying fund’s initial investment. The use of leverage magnifies changes in an underlying fund’s net asset value and |

11 | ||

thus results in increased portfolio volatility and increased risk of loss. Leverage can create an interest expense that may lower the underlying fund's overall returns. There can be no guarantee that a leveraging strategy will be successful.

• | Options Risk: Options trading is a highly specialized activity that involves investment techniques and risks different from those associated with ordinary portfolio securities transactions. The value of options can be highly volatile, and their use can result in loss if the Sub-Advisor is incorrect in its expectation of price fluctuations. Options, whether exchange traded or over-the-counter, may also be illiquid. |

• | Swap Agreement Risk: Swap agreements (“swaps”) are individually negotiated and structured to include exposure to a variety of different types of investments or market factors. Swaps may increase or decrease the overall volatility of the investments of the underlying fund and its share price. The performance of swaps may be affected by a change in the specific interest rate, currency, or other factors that determine the amounts of payments due to and from the underlying fund. A swap can be a form of leverage, which can magnify the underlying fund’s gains or losses. |

Equity Securities Risk: An underlying fund is subject to the risk that stock prices will fall over short or extended periods of time. Individual companies may report poor results or be negatively affected by industry or economic trends and developments. The prices of securities issued by these companies may decline in response to developments, which could result in a decline in the value of the underlying fund’s shares.

• | Large-Cap Risk: Large-cap companies may be unable to respond quickly to new competitive challenges, such as changes in technology and consumer tastes, and also may not be able to attain the high growth rate of successful smaller companies, especially during extended periods of economic expansion. |

• | Mid-Cap Risk: Stocks of mid-sized companies may be subject to more abrupt or erratic market movements than stocks of larger, more established companies. Mid-sized companies may have limited product lines or financial resources, and may be dependent upon a particular niche of the market. |

• | Preferred Stock Risk: In the event an issuer is liquidated or declares bankruptcy, the claims of owners of bonds take precedence over the claims of those who own preferred and common stock. If interest rates rise, the fixed dividend on preferred stocks may be less attractive, causing the price of preferred stocks to decline. |

• | Real Estate Investment Trust Risk: Real Estate Investment Trusts (“REITs”) are pooled investment vehicles that primarily invest in commercial real estate or real estate-related loans. REITs are susceptible to the risks associated with direct ownership of real estate, such as declines in property values and rental rates and increases in property taxes. Additionally, REITs typically incur fees that are separate from those of an underlying fund. |

• | Small-Cap Risk: Stocks of smaller companies may be subject to more abrupt or erratic market movements than stocks of larger, more established companies. Small companies may have limited product lines or financial resources and may be dependent upon a small or inexperienced management group. |

Fixed-Income Risk: The market value of an underlying fund’s fixed-income investments responds to economic developments, particularly interest rate changes, as well as to perceptions about the creditworthiness of individual issuers. Generally, an underlying fund’s fixed-income investments will decrease in value if interest rates rise and increase in value if interest rates fall. Normally, the longer an underlying fund’s maturity or duration, the more sensitive the value of an underlying fund’s shares will be to changes in interest rates.

• | Asset-Backed Securities Risk: Asset-backed securities are fixed-income securities backed by other assets such as credit card, automobile or consumer loan receivables, retail installment loans, or participations in pools of leases. The values of these securities are sensitive to changes in the credit quality of the underlying |

12 | ||

collateral, the credit strength of any credit enhancement feature, changes in interest rates, and, at times, the financial condition of the issuer.

• | Corporate Loan Risk: The corporate loans in which an underlying fund invests may be rated below investment grade. As a result, such corporate loans will be considered speculative with respect to the borrowers’ ability to make payments of interest and principal and will otherwise generally bear risks similar to those associated with non-investment grade securities. There is a high risk that an underlying fund could suffer a loss from investments in lower rated corporate loans as a result of a default by the borrower. |

• | Credit Risk: The fixed-income securities in an underlying fund’s portfolio are subject to the possibility that a deterioration, whether sudden or gradual, in the financial condition of an issuer, or a deterioration in general economic conditions, could cause an issuer to fail to make timely payments of principal or interest, when due. This may cause the issuer’s securities to decline in value. |

• | Interest Rate Risk: As interest rates rise, the value of fixed-income securities the underlying fund owns will likely decrease. The price of debt securities is generally linked to the prevailing market interest rates. In general, when interest rates rise, the prices of debt securities fall, and when interest rates fall, the prices of debt securities rise. The price volatility of a debt security also depends on its maturity. Longer-term securities are generally more volatile, so the longer the average maturity or duration of these securities, the greater their price risk. |

• | Investment-Grade Debt Securities Risk: Investment-grade debt securities may be downgraded by a NRSRO to below-investment-grade status, which would increase the risk of holding these securities. Investment-grade debt securities rated in the lowest rating category by a NRSRO involve a higher degree of risk than fixed-income securities with higher credit ratings. |

• | Mortgage-Backed Securities Risk: Some underlying funds may invest in mortgage-backed securities, some of which may not be backed by the full faith and credit of the U.S. government. Mortgage-backed securities are subject to call risk and extension risk. Because of these risks, mortgage-backed securities react differently to changes in interest rates than other bonds. Small movements in interest rates (both increases and decreases) may quickly and significantly reduce the value of certain mortgage-backed securities. |

• | Non-Investment-Grade Debt Securities Risk: Non-investment-grade debt securities are sometimes referred to as “junk bonds” and are considered speculative with respect to their issuers’ ability to make payments of interest and principal. There is a high risk that an underlying fund could suffer a loss from investments in non-investment-grade debt securities caused by the default of an issuer of such securities. Non-investment-grade debt securities may also be less liquid than investment-grade debt securities. |

• | Stressed and Distressed Securities Risk: Distressed securities are speculative and involve significant risks in addition to the risks generally applicable to non-investment grade debt securities. Distressed securities bear a substantial risk of default, and may be in default at the time of investment. An underlying fund will generally not receive interest payments on distressed securities, and there is a significant risk that principal will not be repaid, in full or at all. Distressed securities will likely be illiquid and may be subject to restrictions on resale. |

• | U.S. Government Agencies Securities Risk: Certain U.S. government agency securities are backed by the right of the issuer to borrow from the U.S. Treasury while others are supported only by the credit of the issuer or instrumentality. While the U.S. government is able to provide financial support to U.S. government-sponsored agencies or instrumentalities, no assurance can be given that it will always do so. |

Foreign Securities Risk: Investing in foreign securities poses additional risks since political and economic events unique in a country or region will affect those markets and their issuers, while such events may not necessarily affect the U.S. economy or issuers located in the United States. In addition, investments in foreign securities are generally denominated in foreign currency. As a result, changes in the value of those currencies compared to the U.S. dollar

13 | ||

may affect (positively or negatively) the value of an underlying fund’s investments. There are also risks associated with foreign accounting standards, government regulation, market information, imposition of foreign withholding and other taxes, and clearance and settlement procedures. Foreign markets may be less liquid and more volatile than U.S. markets and offer less protection to investors.

• | Depositary Receipts Risk: Foreign receipts, which include ADRs, Global Depositary Receipts, and European Depositary Receipts, are securities that evidence ownership interests in a security or a pool of securities issued by a foreign issuer. The risks of depositary receipts include many risks associated with investing directly in foreign securities. |

• | Emerging Markets Risk (Acquiring Fund Only): Emerging markets may be more likely to experience political turmoil or rapid changes in market or economic conditions than more developed countries. In addition, the financial stability of issuers (including governments) in emerging market countries may be more precarious than that of issuers in other countries. |

Liquidity Risk: Liquidity risk exists when particular investments are difficult to purchase or sell. This can reduce an underlying fund’s returns because an underlying fund may be unable to transact at advantageous times or prices, or at all.

Merger Arbitrage Risk (Target Fund Only): Investments in companies that are expected to be, or already are, the subject of a publicly announced transaction carry the risk that the proposed or expected transaction may not be completed or may be completed on less favorable terms than originally expected.

Non-Diversification Risk: An underlying fund may be non-diversified, which means that it may invest a greater percentage of its assets than a diversified mutual fund in the securities of a limited number of issuers. The use of a non-diversified investment strategy may increase the volatility of an underlying fund’s investment performance, as an underlying fund may be more susceptible to risks associated with a single economic, political, or regulatory event.

Pay-In-Kind Bonds Risk: Pay-in-kind bonds, a type of mezzanine financing, are securities that, at the issuer’s option, pay interest in either cash or additional securities for a specified period. Pay-in-kind bonds, like zero coupon bonds, are designed to give an issuer flexibility in managing cash flow. Pay-in-kind bonds are expected to reflect the market value of the underlying debt plus an amount representing accrued interest since the last payment. Pay-in-kind bonds are usually less volatile than zero coupon bonds, but more volatile than cash pay securities.

Portfolio Turnover Risk: An underlying fund may engage in active and frequent trading, which may result in increased transaction costs to the underlying fund. This risk also applies to each Fund, which may engage in active and frequent trading of underlying funds resulting in increased transaction costs to the Fund.

Prepayment Risk (Acquiring Fund Only): The risk that a debt security may be paid off and proceeds invested earlier than anticipated. Prepayment impacts both the interest rate sensitivity of the underlying asset, such as an asset-backed or mortgage-backed security and its cash flow projections. Therefore, prepayment risk may make it difficult to calculate the average duration of an underlying fund’s asset- or mortgage-backed securities which in turn would make it difficult to assess the interest rate risk of an underlying fund.

Real Estate Industry Risk (Acquiring Fund Only): Since an underlying fund’s investments may be concentrated in the real estate industry, it is subject to the risk that the real estate industry will underperform the broader market, as well as the risk that issuers in the industry will be similarly impacted by market conditions, legislative or regulatory changes, or competition. The real estate industry is particularly sensitive to economic downturns.

Rule 144A Securities Risk: Rule 144A securities are restricted securities that may be purchased only by qualified institutional buyers in reliance on an exemption from federal registration requirements. Investing in Rule 144A securities may reduce the liquidity of the underlying fund's portfolio if an adequate institutional trading market for these securities does not exist. Prices of Rule 144A securities often reflect a discount, which may be significant, from the market price of comparable exchange-listed securities for which a liquid trading market exists.

14 | ||

Short Sales Risk: In a short sale, an underlying fund sells a security or other financial instrument, such as a futures contract, that it does not own. To complete the transaction, the underlying fund must borrow the security to make delivery to the buyer. An underlying fund is then obligated to replace the borrowed security by purchasing the security at the market price at the time of replacement. If the price of the security sold short rises between the time an underlying fund sells the security short and the time an underlying fund replaces the security sold short, an underlying fund will realize a loss on the transaction.

Value Investing Risk: Value investing presents the risk that an underlying fund’s security holdings may never reach their full market value because the market fails to recognize what the portfolio managers consider the true business value or because the portfolio managers have misjudged those values. In addition, value investing may fall out of favor and underperform growth or other styles of investing during given certain periods.

INFORMATION ABOUT THE REORGANIZATION

Reasons for the Reorganization

The Reorganization is intended to eliminate the offering of multiple funds with similar investment goals and similar principal investment strategies. The Reorganization has the potential to provide efficiencies, enhanced marketability and economies of scale for the combined Fund. At a meeting held on February 12, 2019, the Board, including the Independent Trustees, determined that the Reorganization was in the best interests of the Funds and that the interests of existing shareholders of the Funds will not be diluted as a result of the Reorganization. The Board approved the Reorganization.

In evaluating the Reorganization, the Board requested and reviewed, with the assistance of independent legal counsel, materials furnished by Touchstone Advisors, the investment advisor to the Funds. These materials included information regarding the operations and financial condition of the Funds and the principal terms and conditions of the Reorganization, including that the Reorganization is expected to qualify as a tax-free reorganization for federal income tax purposes. The Board considered the following factors, among others:

• the investment goals, principal investment strategies, sub-advisor and portfolio managers of the Funds;

• the historical investment performance record of the Funds;

• the advice and recommendation of Touchstone Advisors, including its opinion that the Reorganization would be in the best interests of the Funds and that the combined Fund would have enhanced marketability and a greater opportunity to achieve economies of scale than either Fund operating individually;

• the investment advisory fee and other fees paid by the Funds, the expense ratios of the Funds and the contractual limitations on the Funds’ expenses;

• the anticipated benefits to the Funds, including operating efficiencies, that may be achieved from the Reorganization;

• that the expenses of the Reorganization would not be borne by the Funds’ shareholders;

• the terms and conditions of the Reorganization, including the Acquiring Fund’s assumption of all of the liabilities of the Target Fund;

• the Reorganization is intended to be a tax-free reorganization for federal income tax purposes; and

• alternatives available to shareholders of the Target Fund, including the ability to redeem or exchange their shares.

During their assessment, the Board met with independent legal counsel regarding the legal issues involved. After consideration of the factors noted above, together with other factors and information considered to be relevant, and recognizing that there can be no assurance that any potential operating efficiencies or other benefits will in fact be

15 | ||

realized, the Board concluded that the Reorganization would be in the best interests of each Fund and the interests of existing shareholders of the Funds would not be diluted as a result of the Reorganization.

Agreement and Plan of Reorganization

A form of the Plan is set forth in Exhibit A. The Plan provides that all of the assets of the Target Fund will be transferred to the Acquiring Fund solely in exchange for shares of the Acquiring Fund and the assumption by the Acquiring Fund of all the liabilities of the Target Fund on or about May 10, 2019 or such other date as may be agreed upon by the parties (the “Closing Date”). The class or classes of the Acquiring Fund shares that you will receive in connection with the Reorganization will be the same as the class or classes of the Target Fund shares that you own immediately prior to the closing of the Reorganization.

Prior to the close of business on the Closing Date, the Target Fund will endeavor to discharge all of its known liabilities and obligations. In addition, prior to the close of business on the Closing Date, for tax reasons, the Target Fund will distribute to its shareholders all of the Target Fund’s investment company taxable income for all taxable periods ending on or before the Closing Date, all of the Target Fund’s net tax-exempt income for all taxable periods ending on or before the Closing Date, and all of its net capital gains realized in all taxable periods ending on or before the Closing Date (after reduction for any available capital loss carryforwards and excluding any net capital gain on which the Target Fund paid federal income tax).

The Bank of New York Mellon, the sub-administrator for the Funds, will compute the value of the Target Fund’s portfolio of securities. The method of valuation employed will be consistent with the valuation procedures described in the Trust’s declaration of trust and the Target Fund’s prospectus and statement of additional information or such other valuation procedures as shall be mutually agreed upon by the Funds.

As soon after the closing as practicable, the Target Fund will distribute pro rata by class to its shareholders of record as of the time of such distribution the full and fractional shares of the Acquiring Fund received by the Target Fund. The liquidation and distribution will be accomplished by the establishment of accounts in the names of the Target Fund’s shareholders on the Acquiring Fund’s share records of its transfer agent. Each account will receive the respective pro rata number of full and fractional shares of the appropriate class of the Acquiring Fund due a Target Fund shareholder. All issued and outstanding shares of the Target Fund will be cancelled. After these distributions and the winding up of its affairs, the Target Fund will be terminated.

The Reorganization is subject to the satisfaction or waiver of the conditions set forth in the Plan. The Plan may be terminated (1) by the mutual agreement of the Target Fund and the Acquiring Fund; or (2) at or prior to the closing by either party (a) because of a breach by the other of any representation, warranty, or agreement contained in the Plan to be performed at or prior to the closing, if not cured within 30 days, or (b) because a condition in the Plan expressed to be precedent to the obligations of the terminating party has not been met and it reasonably appears that it will not or cannot be met.

Whether or not the Reorganization is consummated, Touchstone Advisors will pay the expenses incurred by the Funds in connection with the Reorganization, other than repositioning costs.

Description of the Securities to be Issued