CALCULATION OF REGISTRATION FEE

|

| ||||||||

| Title of Each Class of Securities to be Registered |

Amount to be Registered |

Proposed Maximum Offering Price Per Unit |

Proposed Maximum Offering Price |

Amount of Fee(1) | ||||

| $7,349,000 Fixed to Floating Rate Notes with a Cap, due June 26, 2023 |

7,349 | $1,000.00 | $7,349,000.00 | $1,002.41 | ||||

|

| ||||||||

|

| ||||||||

| (1) | Calculated in accordance with Rule 457(r) of the Securities Act of 1933. |

| Fixed to Floating Rate Notes with a Cap, due June 26, 2023 $1,000 principal amount per unit Term Sheet No. 1185 |

Filed Pursuant to Rule 424(b)(2) Registration No. 333-180488 |

![]()

$7,349,000 Fixed to Floating Rate Notes with a Cap, due June 26, 2023

| • | The notes are senior unsecured debt securities issued by Bank of America Corporation. All payments and the return of the principal amount at maturity are subject to our credit risk. |

| • | The notes will mature on June 26, 2023. |

| • | Interest will be paid quarterly, beginning on September 26, 2013. |

| • | The notes will accrue interest at the following rates per annum during the indicated years of their term: |

| • | Year 1: at a fixed rate of 3.00%. |

| • | Years 2 to 10: at a floating rate equal to 3-Month U.S. Dollar LIBOR plus a spread equal to 1.60%. The maximum interest rate payable during years 2 to 10 will be capped at 6.00% per annum. In no event will the minimum rate of interest payable on the notes be less than 0.00%. |

| • | The notes will be issued in minimum denominations of $1,000 and whole multiples of $1,000. |

| • | The notes will not be listed on any securities exchange. |

The Fixed to Floating Rate Notes with a Cap (the “notes”) are being offered by Bank of America Corporation (“BAC”). An investment in the notes involves significant investment risks. See “Risk Factors” beginning on page TS-4 of this term sheet and beginning on page S-5 of the MTN prospectus supplement. The notes:

|

Are Not FDIC Insured

|

Are Not Bank Guaranteed

|

May Lose Value

|

None of the Securities and Exchange Commission (the “SEC”), any state securities commission, or any other regulatory body has approved or disapproved of these securities or determined if this prospectus (as defined below) is truthful or complete. Any representation to the contrary is a criminal offense.

| Per Unit | Total | |||||||

| Public offering price(1) |

$ | 1,000.00 | $ | 7,349,000.00 | ||||

| Underwriting commission(1) |

$ | 17.50 | $ | 128,607.50 | ||||

| Proceeds, before expenses, to BAC |

$ | 982.50 | $ | 7,220,392.50 | ||||

| (1) | Plus accrued interest from the scheduled settlement date, if settlement occurs after that date. |

Merrill Lynch & Co.

June 24, 2013

SUMMARY OF TERMS

This term sheet supplements the terms and conditions in the prospectus, dated March 30, 2012, as supplemented by the Series L prospectus supplement, dated March 30, 2012 (the prospectus, as so supplemented, together with all documents incorporated by reference, the “prospectus”), and should be read with the prospectus. Unless otherwise defined in this term sheet, terms used herein have the same meanings as are given to them in the prospectus.

The Fixed to Floating Rate Notes with a Cap, due June 26, 2023 (the “notes”), are our senior debt securities and are not secured by collateral. They are not guaranteed by, and are not savings accounts or deposits of, any bank. They are not insured by the Federal Deposit Insurance Corporation.

The notes will rank equally with all of our other senior unsecured indebtedness. Any payments due on the notes, including any repayment of principal, will be subject to the credit risk of BAC.

From the settlement date to, but excluding, June 26, 2014, the notes will bear interest at the fixed rate of 3.00% per annum. From June 26, 2014 to, but excluding, the maturity date, the notes will bear interest at a floating rate equal to 3-month U.S. Dollar LIBOR (the “Reference Rate”) plus a spread equal to 1.60%. During the floating rate period, the interest rate payable on the notes will never be greater than 6.00% per annum.

Payments on the notes depend on our credit risk and the level of the Reference Rate during the floating rate period. The economic terms of the notes (including the spread) are based in part on the terms of certain related hedging arrangements. The underwriting commission and the additional charge, described below, will reduce the economic terms of the notes to you.

| Issuer: | Bank of America Corporation (“BAC”) | |

| Original Offering Price: | $1,000.00 per unit | |

| Pricing Date: | June 24, 2013 | |

| Settlement Date: | June 26, 2013 | |

| Maturity Date: | June 26, 2023 (a term of approximately ten years) | |

| Payment at Maturity: | At maturity, you will receive for each unit of your notes a cash payment of $1,000 plus any accrued and unpaid interest, subject to our credit risk. | |

| Interest Periods: | Quarterly | |

| Interest Payment Dates: |

September 26, December 26, March 26, and June 26 of each year, beginning on September 26, 2013, with the final interest payment due on the maturity date. | |

| Interest Rate: | Fixed Rate Period. From the settlement date to, but excluding, June 26, 2014, the notes will bear interest at a fixed rate of 3.00% per annum.

Floating Rate Period. From June 26, 2014 to, but excluding, the maturity date, the notes will bear interest at a floating rate equal to the Reference Rate plus a spread equal to 1.60%. | |

| Interest Rate Cap during Floating Rate Period: |

The maximum interest rate payable on the notes during the floating rate period will be capped at 6.00% per annum, regardless of how much the Reference Rate may rise. | |

| Reference Rate: | 3-Month U.S. Dollar LIBOR as it appears on Reuters page LIBOR01, or any substitute page, as of 11:00 A.M., London time, on the applicable interest determination date, as determined by the calculation agent in the manner described on page TS-6. | |

| Interest Determination Date: |

The second London Banking Day preceding the applicable Interest Reset Date | |

| Day Count Fraction: | 30/360 | |

| Payment Business Day: |

New York | |

| Listing: | The notes will not be listed on any securities exchange. | |

| Fees and Charges: | The public offering price of the notes includes the underwriting commission of $17.50 per unit as listed on the cover page and an additional charge of $7.50 per unit as more fully described on page TS-7. | |

| Minimum Denominations: | The notes are issued in minimum denominations of $1,000 and whole multiples of $1,000. | |

| CUSIP No.: | 06048WNX4 | |

| Calculation Agent: | Merrill Lynch Capital Services, Inc. (“MLCS”), a subsidiary of BAC | |

TS-2

The terms and risks of the notes are contained in this term sheet and in the following:

| • | Series L MTN prospectus supplement dated March 30, 2012 and prospectus dated March 30, 2012: |

http://www.sec.gov/Archives/edgar/data/70858/000119312512143855/d323958d424b5.htm

The prospectus has been filed as part of a registration statement with the SEC, which may, without cost, be accessed on the SEC website as indicated above or obtained from MLPF&S by calling 1-866-500-5408. Before you invest, you should read the prospectus, including this term sheet, for information about us and this offering. Any prior or contemporaneous oral statements and any other written materials you may have received are superseded by the prospectus. Capitalized terms used but not defined in this term sheet have the meanings set forth in the prospectus. Unless otherwise indicated or unless the context requires otherwise, all references in this document to “we,” “us,” “our,” or similar references are to BAC.

INVESTOR CONSIDERATIONS

You may wish to consider an investment in the notes if:

| • | You seek current income of a fixed 3.00% interest rate per annum until June 26, 2014 and are willing to accept a floating interest rate thereafter. |

| • | You anticipate that the sum of the interest payments on the notes will be sufficient to provide you with your desired return. |

| • | You accept that the interest rate during the floating rate period will never be greater than 6.00% per annum, regardless of how much the Reference Rate may rise. |

| • | You are willing to accept that a trading market is not expected to develop for the notes. You understand that secondary market prices for the notes, if any, will be affected by various factors, including our actual and perceived creditworthiness and fees and charges on the notes. |

| • | You are willing to assume our credit risk, as issuer of the notes, for all payments under the notes. |

The notes may not be an appropriate investment for you if:

| • | You seek an investment with a fixed or guaranteed rate of return throughout the term of the notes. |

| • | You anticipate that the sum of the interest payments on the notes will not be sufficient to provide you with your desired return. |

| • | You seek an uncapped return on your investment. |

| • | You seek assurances that there will be a liquid market if and when you want to sell the notes prior to maturity. |

| • | You are unwilling or are unable to take our credit risk as issuer of the notes. |

We urge you to consult your investment, legal, tax, accounting and other advisors before you invest in the notes.

HYPOTHETICAL INTEREST RATES DURING THE FLOATING RATE PERIOD

The following table illustrates the hypothetical annual interest rates on the notes during the floating rate period based on a range of hypothetical 3-month U.S. Dollar LIBOR rates, the spread of 1.60%, the cap on the maximum interest rate of 6.00% per annum. The following examples do not take into account any tax consequences from investing in the notes.

The actual interest rates on the notes will depend on the actual levels of 3-month U.S. Dollar LIBOR. For recent actual levels of the Reference Rate, see “The Reference Rate: 3-Month U.S. Dollar LIBOR” section below. In addition, all payments on the notes are subject to issuer credit risk.

| 3-Month U.S. Dollar LIBOR |

|

Spread |

|

Interest Rate (per annum) | ||||

| 10.00% |

+ | 1.60% | = | 6.00%(1) | ||||

| 8.00% |

+ | 1.60% | = | 6.00%(1) | ||||

| 6.00% |

+ | 1.60% | = | 6.00%(1) | ||||

| 4.00% |

+ | 1.60% | = | 5.60% | ||||

| 2.00% |

+ | 1.60% | = | 3.60% | ||||

| 0.00% |

+ | 1.60% | = | 1.60% | ||||

| -2.00% |

+ | 1.60% | = | 0.00% |

| (1) | The maximum interest rate during the floating rate period cannot exceed the cap of 6.00% per annum. |

TS-3

RISK FACTORS

An investment in the notes involves significant risks, including those listed below. You should carefully review the more detailed explanation of risks relating to the notes in the “Risk Factors” sections beginning on page S-5 of the MTN prospectus supplement identified above. We also urge you to consult your investment, legal, tax, accounting, and other advisors before you invest in the notes.

Payments on the notes are subject to our credit risk, and actual or perceived changes in our creditworthiness are expected to affect the value of the notes.

The notes are our senior unsecured debt securities. As a result, your receipt of each payment of interest and the principal amount at maturity is dependent upon our ability to repay our obligations on the applicable interest payment date and the maturity date. No assurance can be given as to what our financial condition will be on any payment date. If we default upon our financial obligations, you may not receive any payments due on the notes.

Our credit ratings are an assessment by ratings agencies of our ability to pay our obligations. Consequently, our perceived creditworthiness and actual or anticipated decreases in our credit ratings or increases in our credit spreads prior to the maturity date may adversely affect the market value of the notes. However, because your return on the notes depends upon factors in addition to our ability to pay our obligations, such as the level of the Reference Rate during the floating rate period, an improvement in our credit ratings will not reduce the other investment risks related to the notes.

The interest rate on the notes during the floating rate period is capped.

Although the interest payable on the notes during the floating rate period is based on the Reference Rate, in no event will you receive any interest payment that is greater than 6% per annum. In other words, you will not be able to participate in any increases in the Reference Rate, that when added to the spread, would exceed 6% per annum.

A trading market is not expected to develop for the notes. Neither we nor MLPF&S is not obligated to make a market for, or to repurchase, the notes. There is no assurance that any party will be willing to purchase your notes at any price in any secondary market.

We will not list the notes on any securities exchange. We cannot predict how the notes will trade in any secondary market or whether that market will be liquid or illiquid.

The development of a trading market for the notes will depend on our financial performance and other factors. The number of potential buyers of your notes in any secondary market may be limited. We anticipate that MLPF&S will act as a market-maker for the notes, but it is not required to do so. MLPF&S may discontinue its market-making activities as to the notes at any time. To the extent that MLPF&S engages in any market-making activities, it may bid for or offer the notes. Any price at which MLPF&S may bid for, offer, purchase, or sell any notes may differ from the values determined by pricing models that it may use, whether as a result of dealer discounts, mark-ups, or other transaction costs. These bids, offers, or completed transactions may affect the prices, if any, at which the notes might otherwise trade in the market.

In addition, if at any time MLPF&S were to cease acting as a market-maker for the notes, it is likely that there would be significantly less liquidity in the secondary market. In such a case, the price at which the notes could be sold likely would be less than if an active market existed.

We have included in the terms of the notes the costs of developing, hedging, and distributing them, and the price, if any, at which you may sell the notes in any secondary market transaction will likely be less than the public offering price due to, among other things, the inclusion of these costs.

In determining the economic terms of notes, and consequently the potential return on notes to you, a number of factors are taken into account. Among these factors are certain costs associated with developing, hedging, and offering the notes. In addition to the underwriting commission, the applicable public offering price may include a hedging related charge, which reflects an estimated profit earned by one of our affiliates from the hedging related transactions associated with the notes, as described on page TS-7. In entering into the hedging arrangements for the notes, we seek competitive terms and may enter into hedging transactions with one of our affiliates. All of these charges related to the notes reduce the economic terms of the notes.

Assuming there is no change in market conditions or any other relevant factors, the price, if any, at which MLPF&S or another purchaser might be willing to purchase your notes in a secondary market transaction is expected to be less than the applicable public offering price due to, among other things,

TS-4

the inclusion of these costs and the costs of unwinding any related hedging. The quoted price of any of our affiliates for the notes could be higher or less than the public offering price.

If you attempt to sell the notes prior to maturity, their market value, if any, will be affected by various factors that interrelate in complex ways, and their market value may be less than the principal amount of the notes.

Unlike savings accounts, certificates of deposit, and other similar investment products, you have no right to have your notes redeemed prior to maturity. If you wish to liquidate your investment in the notes prior to maturity, your only option would be to sell them. At that time, there may be an illiquid market for your notes or no market at all. Even if you were able to sell your notes, there are many factors outside of our control that may affect their market value, some of which, but not all, are stated below. Some of these factors are interrelated in complex ways. As a result, the effect of any one factor may be offset or magnified by the effect of another factor. The following paragraphs describe the expected impact on the market value of the notes from a change in a specific factor, assuming all other conditions remain constant.

| • | Changes in Interest Rates. Changes in prevailing interest rates may adversely impact the market value of the notes. However, as the levels of prevailing interest rates increase or decrease, the market value of the notes is not expected to increase or decrease at the same rate. |

| • | Volatility of Market Interest Rates. Volatility is the term used to describe the size and frequency of market fluctuations. An unsettled international environment and related uncertainties may result in greater interest rate volatility, which may continue over the term of the notes. Increases or decreases in the volatility of market interest rates have an adverse impact on the market value of the notes. |

| • | Economic and Other Conditions Generally. The general economic conditions of the capital markets in the U.S. and globally, as well as geopolitical conditions and other financial, political, regulatory, and judicial events that affect the capital markets generally, may affect the value of the notes. |

| • | Our Financial Condition and Creditworthiness. Our perceived creditworthiness, including any increases in our credit spreads and any actual or anticipated decreases in our credit ratings, may adversely affect the market value of the notes. In general, we expect the longer the amount of time that remains until maturity, the more significant the impact will be on the value of the notes. However, a decrease in our credit spreads or an improvement in our credit ratings will not necessarily increase the market value of the notes. |

| • | Time to Maturity. There may be a disparity between the market value of the notes prior to maturity and their value at maturity. This disparity is often called a time “value,” “premium,” or “discount,” and reflects expectations concerning market interest rates prior to the maturity date. As the time to maturity decreases, this disparity will likely decrease, such that the value of the notes will approach the expected remaining payments on the notes. |

Our hedging activities may affect the market value of the notes.

We, or one or more of our affiliates, including MLPF&S, may engage in hedging activities that may increase or decrease the market value of the notes prior to maturity. In addition, we or one or more of our affiliates, including MLPF&S, may purchase or otherwise acquire a long or short position in the notes. We or any of our affiliates, including MLPF&S, may hold or resell the notes. We cannot assure you that these activities will not affect the market value of the notes prior to maturity.

Our trading and hedging activities may create conflicts of interest with you.

We or one or more of our affiliates, including MLPF&S, may engage in trading activities that are not for your account or on your behalf. We expect to enter into arrangements to hedge the market risks associated with our obligation to pay the amounts due under the notes. We may seek competitive terms in entering into the hedging arrangements for the notes, but are not required to do so, and we may enter into such hedging arrangements with one of our subsidiaries or affiliates. This hedging activity is expected to result in a profit to those engaging in the hedging activity, which could be more or less than initially expected, but which could also result in a loss for the hedging counterparty. These trading and hedging activities may present a conflict of interest between your interest in the notes and the interests we and our affiliates may have in our and our affiliates’ proprietary accounts, in facilitating transactions for our and our affiliates’ customers, and in accounts under our and our affiliates’ management. These trading and underwriting activities could affect secondary trading in the notes in a manner that would be adverse to your interests as a beneficial owner of the notes.

TS-5

There may be potential conflicts of interest involving the calculation agent. We have the right to appoint and remove the calculation agent.

Our subsidiary, MLCS, is the calculation agent for the notes and, as such, will determine the rate of interest on the notes for each interest period during the floating rate period. Under some circumstances, these duties could result in a conflict of interest between MLCS’s status as our subsidiary and its responsibilities as calculation agent. These conflicts could occur, for instance, in connection with judgments that it would be required to make if the Reference Rate is unavailable on any interest determination period, as described beginning on page 18 of the prospectus. The calculation agent will be required to carry out its duties in good faith and using its reasonable judgment. However, because we expect to control the calculation agent, potential conflicts of interest could arise.

THE REFERENCE RATE: 3-MONTH U.S. DOLLAR LIBOR

The Reference Rate, 3-Month U.S. Dollar LIBOR, is a daily reference rate that is based on the interest rates at which banks borrow U.S. dollars from each other for a term of three months in the London interbank market. The calculation agent will determine the Reference Rate on the applicable interest determination date according to the rate or rates that appear on Reuters page LIBOR01, or any page substituted for that page, as of 11:00 A.M. London time, on the applicable interest determination date. For additional information as to the determination of the Reference Rate, see “Description of Debt Securities—Floating-Rate Notes—LIBOR Notes” beginning on page 18 of the prospectus. However, if on the first interest determination date for the floating rate period, fewer than two of the rates described above appear on the applicable page or no rate appears on a page on which only one rate normally appears, and the calculation agent cannot determine the Reference Rate using the provisions set forth in the first three bullets on page 19 of the prospectus, the calculation agent will determine the Reference Rate according to the most recently available level of the Reference Rate.

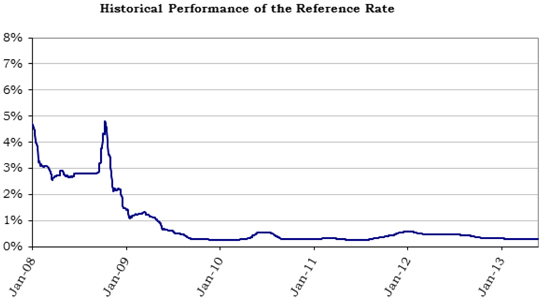

The following graph shows the historical performance of the Reference Rate in the period from January 1, 2008 through June 24, 2013. We obtained this historical data from Bloomberg L.P. We have not independently verified the accuracy or completeness of the information obtained from Bloomberg L.P. On June 24, 2013, the Reference Rate was 0.27675%.

This historical data on the Reference Rate is not necessarily indicative of the future performance of the Reference Rate or what the value of the notes may be. Any historical upward or downward trend in the Reference Rate during any period set forth above is not an indication that the Reference Rate is more or less likely to increase or decrease at any time over the term of the notes.

TS-6

SUPPLEMENT TO THE PLAN OF DISTRIBUTION; ROLE OF MLPF&S AND CONFLICTS OF INTEREST

The notes will not be listed on any securities exchange. If you place an order with MLPF&S to purchase the notes, you are consenting to MLPF&S acting as a principal in effecting the transaction for your account.

MLPF&S, a broker-dealer subsidiary of BAC, is a member of the Financial Industry Regulatory Authority, Inc. (“FINRA”) and will participate as selling agent in the distribution of the notes. Accordingly, offerings of the notes will conform to the requirements of Rule 5121 applicable to FINRA members. MLPF&S may not make sales in this offering to any of its discretionary accounts without the prior written approval of the account holder.

Under our distribution agreement with MLPF&S, MLPF&S will purchase the notes from us as principal at the public offering price indicated on the cover of this term sheet, and will receive the indicated underwriting commission. MLPF&S may sell a portion of the notes to one or more other broker-dealers that will participate in the offering at a purchase price equal to 98.25% of the principal amount.

In order to meet our payment obligations under the notes, at the time we issue them, we may choose to enter into certain hedging arrangements with MLPF&S or one of its affiliates. The terms of these hedging arrangements are determined by seeking bids from market participants, including MLPF&S and its affiliates, and take into account a number of factors, including our creditworthiness, interest rate movements, the tenor of the notes and the tenor of the hedging arrangements. MLPF&S has advised us that the hedging arrangements will include a hedging related charge of approximately $7.50 per unit, reflecting an estimated profit to be credited to MLPF&S from these transactions. Since hedging entails risk and may be influenced by unpredictable market forces, actual profits or losses from these hedging arrangements may be realized by MLPF&S or any third party hedge providers.

The economic terms of the notes depend in part on the terms of these hedging arrangements. Furthermore, the public offering price you pay for the notes includes, in addition to the underwriting commission described above, costs associated with these hedging arrangements. All such fees and costs reduce the economic terms of the notes to you.

MLPF&S may repurchase and resell the notes, with repurchases and resales being made at prices related to then-prevailing market prices or at negotiated prices, and these will include MLPF&S’s trading commissions and mark-ups. MLPF&S may act as principal or agent in these market-making transactions; however it is not obligated to engage in any such transactions.

VALIDITY OF THE NOTES

In the opinion of McGuireWoods LLP, as counsel to BAC, when the trustee has made an appropriate entry on Schedule 1 to the Master Registered Global Senior Note, dated March 30, 2012 (the “Master Note”) identifying the notes offered hereby as supplemental obligations thereunder in accordance with the instructions of BAC, and the notes have been delivered against payment therefor as contemplated in this Note Prospectus, all in accordance with the provisions of the Senior Indenture, such notes will be legal, valid and binding obligations of BAC, subject to applicable bankruptcy, reorganization, insolvency, moratorium, fraudulent conveyance or other similar laws affecting the rights of creditors now or hereafter in effect, and to equitable principles that may limit the right to specific enforcement of remedies, and further subject to 12 U.S.C. §1818(b)(6)(D) (or any successor statute) and any bank regulatory powers now or hereafter in effect and to the application of principles of public policy. This opinion is given as of the date hereof and is limited to the federal laws of the United States, the laws of the State of New York and the Delaware General Corporation Law (including the statutory provisions, all applicable provisions of the Delaware Constitution and reported judicial decisions interpreting the foregoing). In addition, this opinion is subject to the assumption that the trustee’s certificate of authentication of the Master Note has been manually signed by one of the trustee’s authorized officers and to customary assumptions about the trustee’s authorization, execution and delivery of the Senior Indenture, the validity, binding nature and enforceability of the Senior Indenture with respect to the trustee, the legal capacity of natural persons, the genuineness of signatures, the authenticity of all documents submitted to McGuireWoods LLP as originals, the conformity to original documents of all documents submitted to McGuireWoods LLP as photocopies thereof, the authenticity of the originals of such copies and certain factual matters, all as stated in the letter of McGuireWoods LLP dated March 30, 2012, which has been filed as an exhibit to BAC’s Registration Statement relating to the notes filed with the SEC on March 30, 2012.

TS-7

U.S. FEDERAL INCOME TAX SUMMARY

The following summary of the material U.S. federal income tax considerations of the acquisition, ownership, and disposition of the notes is based upon the advice of Morrison & Foerster LLP, our tax counsel. The following discussion supplements the discussions under “U.S. Federal Income Tax Considerations” in the accompanying prospectus and under “U.S. Federal Income Tax Considerations” in the accompanying prospectus supplement and is not exhaustive of all possible tax considerations. This summary is based upon the Internal Revenue Code of 1986, as amended (the “Code”), regulations promulgated under the Code by the U.S. Treasury Department (“Treasury”) (including proposed and temporary regulations), rulings, current administrative interpretations and official pronouncements of the Internal Revenue Service (“IRS”), and judicial decisions, all as currently in effect and all of which are subject to differing interpretations or to change, possibly with retroactive effect. No assurance can be given that the IRS would not assert, or that a court would not sustain, a position contrary to any of the tax consequences described below. This summary does not include any description of the tax laws of any state or local governments, or of any foreign government, that may be applicable to a particular holder.

This summary is directed solely to U.S. Holders and Non-U.S. Holders that, except as otherwise specifically noted, will purchase the notes upon original issuance and will hold the notes as capital assets within the meaning of Section 1221 of the Code, which generally means property held for investment, and that are not excluded from the discussion under “U.S. Federal Income Tax Considerations” in the accompanying prospectus. This summary assumes that the issue price of the notes, as determined for U.S. federal income tax purposes, equals the principal amount thereof.

You should consult your own tax advisor concerning the U.S. federal income tax consequences to you of acquiring, owning, and disposing of the notes, as well as any tax consequences arising under the laws of any state, local, foreign, or other tax jurisdiction and the possible effects of changes in U.S. federal or other tax laws.

U.S. Holders

The notes will be treated as variable rate debt instruments providing for stated interest at a single fixed rate and one or more qualified floating rates. Under Treasury regulations applicable to such instruments, you generally will be required to account for interest on the notes as described below. You will be required to construct an “equivalent fixed rate debt instrument” for the notes and apply the general rules applicable to debt instruments described under the section of the prospectus entitled “U.S. Federal Income Tax Considerations—Taxation of Debt Securities.” The applicable rules require (i) replacing the initial fixed rate by a “qualified floating rate” that would preserve the fair market value of the notes, and (ii) determining the fixed rate substitute for each floating rate. The fixed rate substitute for each qualified floating rate is the value of the rate on the issue date of the notes. The equivalent fixed rate debt instrument is the hypothetical instrument that has terms that are identical to those of the notes, except that the equivalent fixed rate debt instrument provides for the fixed rate substitutes in lieu of the rates on the notes. Under these rules, the equivalent fixed rate debt instrument will have stated interest equal to the fixed rate substitutes. The amount of OID is determined for the equivalent fixed rate debt instrument under the rules applicable to fixed rate debt instruments and is taken into account as if the holder held the equivalent fixed rate debt instrument. Please see the discussion in the prospectus under the section entitled “U.S. Federal Income Tax Considerations—Taxation of Debt Securities—Consequences to U.S. Holders—Original Issue Discount” for a discussion of these rules. Under these rules, based on the rates in effect as of the date of this pricing supplement, we expect that the notes will be issued with no more than de minimis OID. Qualified stated interest and OID, if any, allocable to an accrual period must be increased (or decreased) if the interest actually accrued or paid during an accrual period exceeds (or is less than) the interest assumed to be accrued or paid during the accrual period under the equivalent fixed rate debt instrument. This increase or decrease is an adjustment to qualified stated interest for the accrual period if the equivalent fixed rate debt instrument provides for qualified stated interest and the increase or decrease is reflected in the amount actually paid during the accrual period. Otherwise, this increase or decrease is an adjustment to OID, if any, for the accrual period.

Upon the sale, exchange, retirement, or other disposition of a note, a U.S. Holder will recognize gain or loss equal to the difference between the amount realized upon the sale, exchange, retirement, or other disposition (less an amount equal to any accrued interest not previously included in income if the note is disposed of between interest payment dates, which will be included in income as interest income for U.S. federal income tax purposes) and the U.S. Holder’s adjusted tax basis in the note. A U.S. Holder’s adjusted tax basis in a note generally will be the cost of the note to such U.S. Holder, increased by any OID previously

TS-8

included in income with respect to the note, and decreased by the amount of any payment (other than a payment of qualified stated interest) received in respect of the note. Any gain or loss realized on the sale, exchange, retirement, or other disposition of a note generally will be capital gain or loss and will be long-term capital gain or loss if the note has been held for more than one year. The ability of U.S. Holders to deduct capital losses is subject to limitations under the Code.

Non-U.S. Holders

Please see the discussion under “U.S. Federal Income Tax Considerations—Taxation of Debt Securities—Consequences to Non-U.S. Holders” in the accompanying prospectus for the material U.S. federal income tax consequences that will apply to Non-U.S. Holders of the notes.

Backup Withholding and Information Reporting

Please see the discussion under “U.S. Federal Income Tax Considerations—Taxation of Debt Securities—Backup Withholding and Information Reporting” in the accompanying prospectus for a description of the applicability of the backup withholding and information reporting rules to payments made on the notes.

Foreign Account Tax Compliance Act

Withholding and reporting requirements under the legislation enacted on March 18, 2010 (as discussed beginning on page 85 of the prospectus), will generally apply to payments made after December 31, 2013. However, this withholding tax will not be imposed on payments pursuant to obligations outstanding on January 1, 2014. Holders are urged to consult with their own tax advisors regarding the possible implications of this recently enacted legislation on their investment in the notes.

You should consult your own tax advisor concerning the U.S. federal income tax consequences to you of acquiring, owning, and disposing of the notes, as well as any tax consequences arising under the laws of any state, local, foreign, or other tax jurisdiction and the possible effects of changes in U.S. federal or other tax laws.

WHERE YOU CAN FIND MORE INFORMATION

We have filed a registration statement (including a prospectus supplement and a prospectus) with the SEC for the offering to which this term sheet relates. Before you invest, you should read the prospectus supplement and the prospectus in that registration statement, and the other documents relating to this offering that we have filed with the SEC for more complete information about us and this offering. You may get these documents without cost by visiting EDGAR on the SEC Website at www.sec.gov. Alternatively, we, any agent, or any dealer participating in this offering will arrange to send you these documents if you so request by calling MLPF&S toll-free at 1-866-500-5408.

TS-9