Supplemental Package

Exhibit 99.3

Supplemental Information

Second Quarter 2011

This information is preliminary and based on company data available

at the time of the earnings presentation. It speaks only as of the particular date or dates included in the accompanying pages. Bank of America does not undertake an obligation to, and disclaims any duty to, update any of the information provided.

Any forward-looking statements in this information are subject to the forward-looking language contained in Bank of America’s reports filed with the SEC pursuant to the Securities Exchange Act of 1934, which are available at the SEC’s

website (www.sec.gov) or at Bank of America’s website (www.bankofamerica.com). Bank of America’s future financial performance is subject to risks and uncertainties as described in its SEC filings.

|

|

|

|

|

| Bank of America Corporation and Subsidiaries |

|

|

|

|

| Table of Contents |

|

|

Page |

|

| |

|

|

|

| Consolidated Financial Highlights |

|

|

2 |

|

| Supplemental Financial Data |

|

|

3 |

|

| Consolidated Statement of Income |

|

|

4 |

|

| Consolidated Balance Sheet |

|

|

5,6 |

|

| Capital Management |

|

|

7 |

|

| Core Net Interest Income |

|

|

8 |

|

| Quarterly Average Balances and Interest Rates |

|

|

9,10 |

|

| Year-to-Date Average Balances and Interest Rates |

|

|

11,12 |

|

| Debt Securities and Available-for-Sale Marketable Equity Securities |

|

|

13 |

|

| Quarterly Results by Business Segment |

|

|

14 |

|

| Year-to-Date Results by Business Segment |

|

|

15 |

|

| Deposits |

|

|

|

|

| Total Segment Results |

|

|

16 |

|

| Key Indicators |

|

|

17 |

|

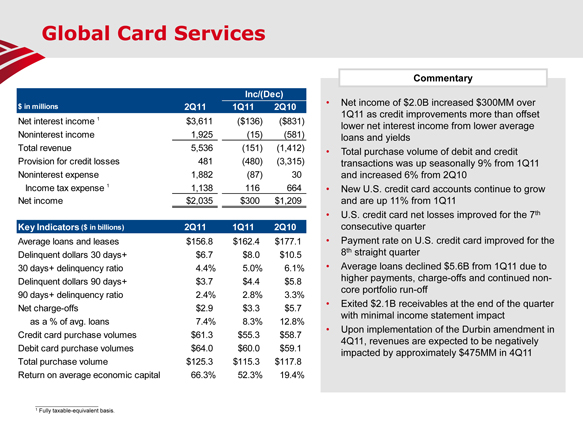

| Global Card Services |

|

|

|

|

| Total Segment Results |

|

|

18 |

|

| Key Indicators |

|

|

19 |

|

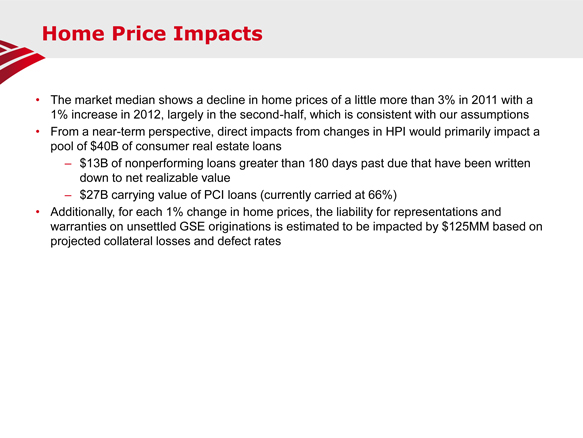

| Consumer Real Estate Services |

|

|

|

|

| Total Segment Results |

|

|

20 |

|

| Quarterly and Year-to-Date Results |

|

|

21 |

|

| Key Indicators |

|

|

22 |

|

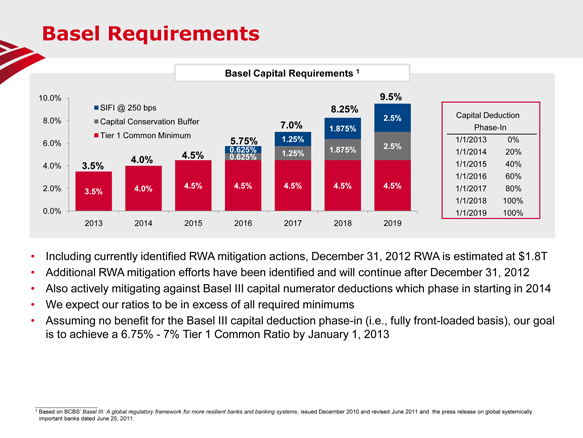

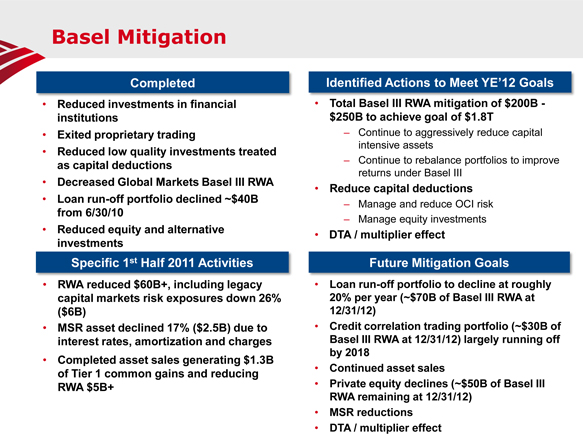

| Global Commercial Banking |

|

|

|

|

| Total Segment Results |

|

|

23 |

|

| Key Indicators |

|

|

24 |

|

| Global Banking & Markets |

|

|

|

|

| Total Segment Results |

|

|

25 |

|

| Key Indicators |

|

|

26 |

|

| Credit Default Swaps with Monoline Financial Guarantors |

|

|

27 |

|

| Investment Banking Product Rankings |

|

|

28 |

|

| Global Wealth & Investment Management |

|

|

|

|

| Total Segment Results |

|

|

29 |

|

| Key Indicators |

|

|

30 |

|

| All Other |

|

|

|

|

| Total Segment Results |

|

|

31 |

|

| Equity Investments |

|

|

32 |

|

| Outstanding Loans and Leases |

|

|

33 |

|

| Quarterly Average Loans and Leases by Business Segment |

|

|

34 |

|

| Commercial Credit Exposure by Industry |

|

|

35 |

|

| Net Credit Default Protection by Maturity Profile and Credit Exposure Debt Rating |

|

|

36 |

|

| Selected Emerging Markets |

|

|

37 |

|

| Selected European Countries |

|

|

38 |

|

| Nonperforming Loans, Leases and Foreclosed Properties |

|

|

39 |

|

| Nonperforming Loans, Leases and Foreclosed Properties Activity |

|

|

40 |

|

| Quarterly Net Charge-offs and Net Charge-off Ratios |

|

|

41 |

|

| Year-to-Date Net Charge-offs and Net Charge-off Ratios |

|

|

42 |

|

| Allocation of the Allowance for Credit Losses by Product Type |

|

|

43 |

|

|

|

| Exhibit A: Non-GAAP Reconciliations |

|

|

44,45 |

|

|

|

| Appendix: Selected Slides from the Second Quarter 2011 Earnings Release Presentation |

|

|

46 |

|

1

Bank of America Corporation and Subsidiaries

Consolidated Financial Highlights

(Dollars in millions, except per share information; shares in thousands)

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

Six Months Ended

June 30 |

|

|

|

|

|

|

Second

Quarter

2011 |

|

|

First

Quarter

2011 |

|

|

Fourth

Quarter

2010 |

|

|

Third

Quarter

2010 |

|

|

Second

Quarter

2010 |

|

| |

|

2011 |

|

|

2010 |

|

|

|

|

|

|

|

|

|

|

| Income statement |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Net interest income |

|

$ |

23,425 |

|

|

$ |

26,649 |

|

|

|

|

|

|

$ |

11,246 |

|

|

$ |

12,179 |

|

|

$ |

12,439 |

|

|

$ |

12,435 |

|

|

$ |

12,900 |

|

| Noninterest income |

|

|

16,688 |

|

|

|

34,473 |

|

|

|

|

|

|

|

1,990 |

|

|

|

14,698 |

|

|

|

9,959 |

|

|

|

14,265 |

|

|

|

16,253 |

|

| Total revenue, net of interest expense |

|

|

40,113 |

|

|

|

61,122 |

|

|

|

|

|

|

|

13,236 |

|

|

|

26,877 |

|

|

|

22,398 |

|

|

|

26,700 |

|

|

|

29,153 |

|

| Provision for credit losses |

|

|

7,069 |

|

|

|

17,910 |

|

|

|

|

|

|

|

3,255 |

|

|

|

3,814 |

|

|

|

5,129 |

|

|

|

5,396 |

|

|

|

8,105 |

|

| Goodwill impairment |

|

|

2,603 |

|

|

|

— |

|

|

|

|

|

|

|

2,603 |

|

|

|

— |

|

|

|

2,000 |

|

|

|

10,400 |

|

|

|

— |

|

| Merger and restructuring charges |

|

|

361 |

|

|

|

1,029 |

|

|

|

|

|

|

|

159 |

|

|

|

202 |

|

|

|

370 |

|

|

|

421 |

|

|

|

508 |

|

| All other noninterest expense (1) |

|

|

40,175 |

|

|

|

33,999 |

|

|

|

|

|

|

|

20,094 |

|

|

|

20,081 |

|

|

|

18,494 |

|

|

|

16,395 |

|

|

|

16,745 |

|

| Income tax expense (benefit) |

|

|

(3,318 |

) |

|

|

1,879 |

|

|

|

|

|

|

|

(4,049 |

) |

|

|

731 |

|

|

|

(2,351 |

) |

|

|

1,387 |

|

|

|

672 |

|

| Net income (loss) |

|

|

(6,777 |

) |

|

|

6,305 |

|

|

|

|

|

|

|

(8,826 |

) |

|

|

2,049 |

|

|

|

(1,244 |

) |

|

|

(7,299 |

) |

|

|

3,123 |

|

| Preferred stock dividends |

|

|

611 |

|

|

|

688 |

|

|

|

|

|

|

|

301 |

|

|

|

310 |

|

|

|

321 |

|

|

|

348 |

|

|

|

340 |

|

| Net income (loss) applicable to common shareholders |

|

|

(7,388 |

) |

|

|

5,617 |

|

|

|

|

|

|

|

(9,127 |

) |

|

|

1,739 |

|

|

|

(1,565 |

) |

|

|

(7,647 |

) |

|

|

2,783 |

|

| Diluted earnings (loss) per common share

(2) |

|

|

(0.73 |

) |

|

|

0.55 |

|

|

|

|

|

|

|

(0.90 |

) |

|

|

0.17 |

|

|

|

(0.16 |

) |

|

|

(0.77 |

) |

|

|

0.27 |

|

| Average diluted common shares issued and outstanding

(2) |

|

|

10,085,479 |

|

|

|

10,020,926 |

|

|

|

|

|

|

|

10,094,928 |

|

|

|

10,181,351 |

|

|

|

10,036,575 |

|

|

|

9,976,351 |

|

|

|

10,029,776 |

|

| Dividends paid per common share |

|

$ |

0.02 |

|

|

$ |

0.02 |

|

|

|

|

|

|

$ |

0.01 |

|

|

$ |

0.01 |

|

|

$ |

0.01 |

|

|

$ |

0.01 |

|

|

$ |

0.01 |

|

|

|

|

|

|

|

|

|

|

|

| Performance ratios |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Return on average assets |

|

|

n/m |

|

|

|

0.51 |

% |

|

|

|

|

|

|

n/m |

|

|

|

0.36 |

% |

|

|

n/m |

|

|

|

n/m |

|

|

|

0.50 |

% |

| Return on average common shareholders’ equity |

|

|

n/m |

|

|

|

5.45 |

|

|

|

|

|

|

|

n/m |

|

|

|

3.29 |

|

|

|

n/m |

|

|

|

n/m |

|

|

|

5.18 |

|

| Return on average tangible common shareholders’ equity

(3) |

|

|

n/m |

|

|

|

9.48 |

|

|

|

|

|

|

|

n/m |

|

|

|

5.28 |

|

|

|

n/m |

|

|

|

n/m |

|

|

|

9.19 |

|

| Return on average tangible shareholders’ equity (3) |

|

|

n/m |

|

|

|

9.26 |

|

|

|

|

|

|

|

n/m |

|

|

|

5.54 |

|

|

|

n/m |

|

|

|

n/m |

|

|

|

8.98 |

|

| At period end |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Book value per share of common stock |

|

$ |

20.29 |

|

|

$ |

21.45 |

|

|

|

|

|

|

$ |

20.29 |

|

|

$ |

21.15 |

|

|

$ |

20.99 |

|

|

$ |

21.17 |

|

|

$ |

21.45 |

|

| Tangible book value per share of common

stock (3) |

|

|

12.65 |

|

|

|

12.14 |

|

|

|

|

|

|

|

12.65 |

|

|

|

13.21 |

|

|

|

12.98 |

|

|

|

12.91 |

|

|

|

12.14 |

|

| Market price per share of common stock: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Closing price |

|

$ |

10.96 |

|

|

$ |

14.37 |

|

|

|

|

|

|

$ |

10.96 |

|

|

$ |

13.33 |

|

|

$ |

13.34 |

|

|

$ |

13.10 |

|

|

$ |

14.37 |

|

| High closing price for the period |

|

|

15.25 |

|

|

|

19.48 |

|

|

|

|

|

|

|

13.72 |

|

|

|

15.25 |

|

|

|

13.56 |

|

|

|

15.67 |

|

|

|

19.48 |

|

| Low closing price for the period |

|

|

10.50 |

|

|

|

14.37 |

|

|

|

|

|

|

|

10.50 |

|

|

|

13.33 |

|

|

|

10.95 |

|

|

|

12.32 |

|

|

|

14.37 |

|

| Market capitalization |

|

|

111,060 |

|

|

|

144,174 |

|

|

|

|

|

|

|

111,060 |

|

|

|

135,057 |

|

|

|

134,536 |

|

|

|

131,442 |

|

|

|

144,174 |

|

|

|

|

|

|

|

|

|

|

|

| Number of banking centers - U.S. |

|

|

5,742 |

|

|

|

5,900 |

|

|

|

|

|

|

|

5,742 |

|

|

|

5,805 |

|

|

|

5,856 |

|

|

|

5,879 |

|

|

|

5,900 |

|

| Number of branded ATMs - U.S. |

|

|

17,817 |

|

|

|

18,078 |

|

|

|

|

|

|

|

17,817 |

|

|

|

17,886 |

|

|

|

17,926 |

|

|

|

17,929 |

|

|

|

18,078 |

|

| Full-time equivalent employees |

|

|

287,839 |

|

|

|

284,628 |

|

|

|

|

|

|

|

287,839 |

|

|

|

288,062 |

|

|

|

288,471 |

|

|

|

287,293 |

|

|

|

284,628 |

|

| (1) |

Excludes merger and restructuring charges and goodwill impairment charge. |

| (2) |

Due to a net loss applicable to common shareholders for the second quarter of 2011 and the fourth and third quarters of 2010, no dilutive potential common shares

were included in the calculations of diluted earnings per share and average diluted common shares because they were antidilutive. |

| (3) |

Tangible equity ratios and tangible book value per share of common stock are non-GAAP measures. We believe the use of these non-GAAP measures provides additional

clarity in assessing the results of the Corporation. (See Exhibit A: Non-GAAP Reconciliations - Reconciliations to GAAP Financial Measures on pages 44-45.) |

Certain prior period amounts have been reclassified to conform to current period presentation.

|

|

|

| This information is preliminary and based on company data available at the time of the presentation. |

|

2 |

Bank of America Corporation and Subsidiaries

Supplemental Financial Data

(Dollars in millions, except per share information)

Fully taxable-equivalent basis data (1)

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

Six Months

Ended

June 30 |

|

|

|

|

|

|

|

|

|

Second

Quarter

2011 |

|

|

|

|

|

First

Quarter

2011 |

|

|

|

|

|

Fourth

Quarter

2010 |

|

|

|

|

|

Third

Quarter

2010 |

|

|

|

|

|

Second

Quarter

2010 |

|

|

|

|

| |

|

2011 |

|

|

|

|

|

2010 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Net interest income |

|

$ |

23,890 |

|

|

|

|

|

|

$ |

27,267 |

|

|

|

|

|

|

|

|

|

|

$ |

11,493 |

|

|

|

|

|

|

$ |

12,397 |

|

|

|

|

|

|

$ |

12,709 |

|

|

|

|

|

|

$ |

12,717 |

|

|

|

|

|

|

$ |

13,197 |

|

|

|

|

|

| Total revenue, net of interest expense |

|

|

40,578 |

|

|

|

|

|

|

|

61,740 |

|

|

|

|

|

|

|

|

|

|

|

13,483 |

|

|

|

|

|

|

|

27,095 |

|

|

|

|

|

|

|

22,668 |

|

|

|

|

|

|

|

26,982 |

|

|

|

|

|

|

|

29,450 |

|

|

|

|

|

| Net interest yield (2) |

|

|

2.58 |

|

|

|

% |

|

|

|

2.85 |

|

|

|

% |

|

|

|

|

|

|

|

2.50 |

|

|

|

% |

|

|

|

2.67 |

|

|

|

% |

|

|

|

2.69 |

|

|

|

% |

|

|

|

2.72 |

|

|

|

% |

|

|

|

2.77 |

|

|

|

% |

|

| Efficiency ratio |

|

|

n/m |

|

|

|

|

|

|

|

56.73 |

|

|

|

|

|

|

|

|

|

|

|

n/m |

|

|

|

|

|

|

|

74.86 |

|

|

|

|

|

|

|

92.04 |

|

|

|

|

|

|

|

100.87 |

|

|

|

|

|

|

|

58.58 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Performance ratios, excluding goodwill impairment charges (3) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

Six Months

Ended

June 30

2011 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Second

Quarter

2011 |

|

|

|

|

|

|

|

|

|

|

|

Fourth

Quarter

2010 |

|

|

|

|

|

Third

Quarter

2010 |

|

|

|

|

|

|

|

|

|

|

| Per common share information |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Earnings (loss) |

|

$ |

(0.48 |

) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

$ |

(0.65 |

) |

|

|

|

|

|

|

|

|

|

|

|

|

|

$ |

0.04 |

|

|

|

|

|

|

$ |

0.27 |

|

|

|

|

|

|

|

|

|

|

|

|

|

| Diluted earnings (loss) |

|

|

(0.48 |

) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(0.65 |

) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

0.04 |

|

|

|

|

|

|

|

0.27 |

|

|

|

|

|

|

|

|

|

|

|

|

|

| Efficiency ratio (1) |

|

|

n/m |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

n/m |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

83.22 |

|

|

|

% |

|

|

|

62.33 |

|

|

|

% |

|

|

|

|

|

|

|

|

|

| Return on average assets |

|

|

n/m |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

n/m |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

0.13 |

|

|

|

|

|

|

|

0.52 |

|

|

|

|

|

|

|

|

|

|

|

|

|

| Return on average common shareholders’ equity |

|

|

n/m |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

n/m |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

0.79 |

|

|

|

|

|

|

|

5.06 |

|

|

|

|

|

|

|

|

|

|

|

|

|

| Return on average tangible common shareholders’ equity (3) |

|

|

n/m |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

n/m |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1.27 |

|

|

|

|

|

|

|

8.67 |

|

|

|

|

|

|

|

|

|

|

|

|

|

| Return on average tangible shareholders’ equity

(3) |

|

|

n/m |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

n/m |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1.96 |

|

|

|

|

|

|

|

8.54 |

|

|

|

|

|

|

|

|

|

|

|

|

|

| (1) |

Fully taxable-equivalent basis is a non-GAAP measure. Fully taxable-equivalent basis is a performance measure used by management in operating the business that

management believes provides investors with a more accurate picture of the interest margin for comparative purposes. (See Exhibit A: Non-GAAP Reconciliations - Reconciliations to GAAP Financial Measures on pages 44-45). |

| (2) |

Calculation includes fees earned on overnight deposits placed with the Federal Reserve of $112 million and $198 million for the six months ended June 30, 2011

and 2010; $49 million and $63 million for the second and first quarters of 2011, and $63 million, $107 million and $106 million for the fourth, third and second quarters of 2010, respectively. For more information see Quarterly and Year-to-Date

Average Balances and Interest Rates - Fully Taxable-equivalent Basis on pages 9-10 and 11-12. |

| (3) |

Total noninterest expense, excluding goodwill impairment charges, net income, excluding goodwill impairment charges and net income applicable to common shareholders,

excluding goodwill impairment charges and tangible equity ratios are non-GAAP measures. We believe the use of these non-GAAP measures provides additional clarity in assessing the results of the Corporation. (See Exhibit A: Non-GAAP Reconciliations -

Reconciliations to GAAP Financial Measures on pages 44-45). |

| Certain |

prior period amounts have been reclassified to conform to current period presentation. |

|

|

|

| This information is preliminary and based on company data available at the time of the presentation. |

|

3 |

Bank of America Corporation and Subsidiaries

Consolidated Statement of Income

(Dollars in millions, except per share information; shares in thousands)

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

Six Months

Ended

June 30 |

|

|

|

|

Second Quarter |

|

|

First Quarter |

|

|

Fourth Quarter |

|

|

Third Quarter |

|

|

Second Quarter |

|

| |

|

2011 |

|

|

2010 |

|

|

|

|

2011 |

|

|

2011 |

|

|

2010 |

|

|

2010 |

|

|

2010 |

|

| Interest income |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Loans and leases |

|

$ |

23,249 |

|

|

$ |

26,362 |

|

|

|

|

$ |

11,320 |

|

|

$ |

11,929 |

|

|

$ |

12,149 |

|

|

$ |

12,485 |

|

|

$ |

12,887 |

|

| Debt securities |

|

|

5,557 |

|

|

|

6,033 |

|

|

|

|

|

2,675 |

|

|

|

2,882 |

|

|

|

3,029 |

|

|

|

2,605 |

|

|

|

2,917 |

|

| Federal funds sold and securities borrowed or purchased under agreements to resell |

|

|

1,114 |

|

|

|

905 |

|

|

|

|

|

597 |

|

|

|

517 |

|

|

|

486 |

|

|

|

441 |

|

|

|

457 |

|

| Trading account assets |

|

|

3,164 |

|

|

|

3,539 |

|

|

|

|

|

1,538 |

|

|

|

1,626 |

|

|

|

1,661 |

|

|

|

1,641 |

|

|

|

1,796 |

|

| Other interest income |

|

|

1,886 |

|

|

|

2,159 |

|

|

|

|

|

918 |

|

|

|

968 |

|

|

|

965 |

|

|

|

1,037 |

|

|

|

1,062 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Total interest income |

|

|

34,970 |

|

|

|

38,998 |

|

|

|

|

|

17,048 |

|

|

|

17,922 |

|

|

|

18,290 |

|

|

|

18,209 |

|

|

|

19,119 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Interest expense |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Deposits |

|

|

1,682 |

|

|

|

2,153 |

|

|

|

|

|

843 |

|

|

|

839 |

|

|

|

894 |

|

|

|

950 |

|

|

|

1,031 |

|

| Short-term borrowings |

|

|

2,525 |

|

|

|

1,709 |

|

|

|

|

|

1,341 |

|

|

|

1,184 |

|

|

|

1,142 |

|

|

|

848 |

|

|

|

891 |

|

| Trading account liabilities |

|

|

1,254 |

|

|

|

1,375 |

|

|

|

|

|

627 |

|

|

|

627 |

|

|

|

561 |

|

|

|

635 |

|

|

|

715 |

|

| Long-term debt |

|

|

6,084 |

|

|

|

7,112 |

|

|

|

|

|

2,991 |

|

|

|

3,093 |

|

|

|

3,254 |

|

|

|

3,341 |

|

|

|

3,582 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Total interest expense |

|

|

11,545 |

|

|

|

12,349 |

|

|

|

|

|

5,802 |

|

|

|

5,743 |

|

|

|

5,851 |

|

|

|

5,774 |

|

|

|

6,219 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Net interest income |

|

|

23,425 |

|

|

|

26,649 |

|

|

|

|

|

11,246 |

|

|

|

12,179 |

|

|

|

12,439 |

|

|

|

12,435 |

|

|

|

12,900 |

|

|

|

|

|

|

|

|

|

|

| Noninterest income |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Card income |

|

|

3,795 |

|

|

|

3,999 |

|

|

|

|

|

1,967 |

|

|

|

1,828 |

|

|

|

2,127 |

|

|

|

1,982 |

|

|

|

2,023 |

|

| Service charges |

|

|

4,044 |

|

|

|

5,142 |

|

|

|

|

|

2,012 |

|

|

|

2,032 |

|

|

|

2,036 |

|

|

|

2,212 |

|

|

|

2,576 |

|

| Investment and brokerage services |

|

|

6,110 |

|

|

|

6,019 |

|

|

|

|

|

3,009 |

|

|

|

3,101 |

|

|

|

2,879 |

|

|

|

2,724 |

|

|

|

2,994 |

|

| Investment banking income |

|

|

3,262 |

|

|

|

2,559 |

|

|

|

|

|

1,684 |

|

|

|

1,578 |

|

|

|

1,590 |

|

|

|

1,371 |

|

|

|

1,319 |

|

| Equity investment income |

|

|

2,687 |

|

|

|

3,391 |

|

|

|

|

|

1,212 |

|

|

|

1,475 |

|

|

|

1,512 |

|

|

|

357 |

|

|

|

2,766 |

|

| Trading account profits |

|

|

4,813 |

|

|

|

6,463 |

|

|

|

|

|

2,091 |

|

|

|

2,722 |

|

|

|

995 |

|

|

|

2,596 |

|

|

|

1,227 |

|

| Mortgage banking income (loss) |

|

|

(12,566 |

) |

|

|

2,398 |

|

|

|

|

|

(13,196 |

) |

|

|

630 |

|

|

|

(1,419 |

) |

|

|

1,755 |

|

|

|

898 |

|

| Insurance income |

|

|

1,013 |

|

|

|

1,393 |

|

|

|

|

|

400 |

|

|

|

613 |

|

|

|

598 |

|

|

|

75 |

|

|

|

678 |

|

| Gains on sales of debt securities |

|

|

1,445 |

|

|

|

771 |

|

|

|

|

|

899 |

|

|

|

546 |

|

|

|

872 |

|

|

|

883 |

|

|

|

37 |

|

| Other income (loss) |

|

|

2,218 |

|

|

|

3,065 |

|

|

|

|

|

1,957 |

|

|

|

261 |

|

|

|

(1,114 |

) |

|

|

433 |

|

|

|

1,861 |

|

| Other-than-temporary impairment losses on available-for-sale debt securities: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Total other-than-temporary impairment losses |

|

|

(157 |

) |

|

|

(1,783 |

) |

|

|

|

|

(63 |

) |

|

|

(111 |

) |

|

|

(612 |

) |

|

|

(156 |

) |

|

|

(462 |

) |

| Less: Portion of other-than-temporary impairment losses recognized in other comprehensive income |

|

|

24 |

|

|

|

1,056 |

|

|

|

|

|

18 |

|

|

|

23 |

|

|

|

495 |

|

|

|

33 |

|

|

|

336 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Net impairment losses recognized in earnings on available-for-sale debt securities |

|

|

(133 |

) |

|

|

(727 |

) |

|

|

|

|

(45 |

) |

|

|

(88 |

) |

|

|

(117 |

) |

|

|

(123 |

) |

|

|

(126 |

) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Total noninterest income |

|

|

16,688 |

|

|

|

34,473 |

|

|

|

|

|

1,990 |

|

|

|

14,698 |

|

|

|

9,959 |

|

|

|

14,265 |

|

|

|

16,253 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Total revenue, net of interest expense |

|

|

40,113 |

|

|

|

61,122 |

|

|

|

|

|

13,236 |

|

|

|

26,877 |

|

|

|

22,398 |

|

|

|

26,700 |

|

|

|

29,153 |

|

|

|

|

|

|

|

|

|

|

| Provision for credit losses |

|

|

7,069 |

|

|

|

17,910 |

|

|

|

|

|

3,255 |

|

|

|

3,814 |

|

|

|

5,129 |

|

|

|

5,396 |

|

|

|

8,105 |

|

|

|

|

|

|

|

|

|

|

| Noninterest expense |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Personnel |

|

|

19,339 |

|

|

|

17,947 |

|

|

|

|

|

9,171 |

|

|

|

10,168 |

|

|

|

8,800 |

|

|

|

8,402 |

|

|

|

8,789 |

|

| Occupancy |

|

|

2,434 |

|

|

|

2,354 |

|

|

|

|

|

1,245 |

|

|

|

1,189 |

|

|

|

1,212 |

|

|

|

1,150 |

|

|

|

1,182 |

|

| Equipment |

|

|

1,199 |

|

|

|

1,226 |

|

|

|

|

|

593 |

|

|

|

606 |

|

|

|

607 |

|

|

|

619 |

|

|

|

613 |

|

| Marketing |

|

|

1,124 |

|

|

|

982 |

|

|

|

|

|

560 |

|

|

|

564 |

|

|

|

484 |

|

|

|

497 |

|

|

|

495 |

|

| Professional fees |

|

|

1,412 |

|

|

|

1,161 |

|

|

|

|

|

766 |

|

|

|

646 |

|

|

|

883 |

|

|

|

651 |

|

|

|

644 |

|

| Amortization of intangibles |

|

|

767 |

|

|

|

885 |

|

|

|

|

|

382 |

|

|

|

385 |

|

|

|

420 |

|

|

|

426 |

|

|

|

439 |

|

| Data processing |

|

|

1,338 |

|

|

|

1,280 |

|

|

|

|

|

643 |

|

|

|

695 |

|

|

|

662 |

|

|

|

602 |

|

|

|

632 |

|

| Telecommunications |

|

|

762 |

|

|

|

689 |

|

|

|

|

|

391 |

|

|

|

371 |

|

|

|

366 |

|

|

|

361 |

|

|

|

359 |

|

| Other general operating |

|

|

11,800 |

|

|

|

7,475 |

|

|

|

|

|

6,343 |

|

|

|

5,457 |

|

|

|

5,060 |

|

|

|

3,687 |

|

|

|

3,592 |

|

| Goodwill impairment |

|

|

2,603 |

|

|

|

— |

|

|

|

|

|

2,603 |

|

|

|

— |

|

|

|

2,000 |

|

|

|

10,400 |

|

|

|

— |

|

| Merger and restructuring charges |

|

|

361 |

|

|

|

1,029 |

|

|

|

|

|

159 |

|

|

|

202 |

|

|

|

370 |

|

|

|

421 |

|

|

|

508 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Total noninterest expense |

|

|

43,139 |

|

|

|

35,028 |

|

|

|

|

|

22,856 |

|

|

|

20,283 |

|

|

|

20,864 |

|

|

|

27,216 |

|

|

|

17,253 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Income (loss) before income taxes |

|

|

(10,095 |

) |

|

|

8,184 |

|

|

|

|

|

(12,875 |

) |

|

|

2,780 |

|

|

|

(3,595 |

) |

|

|

(5,912 |

) |

|

|

3,795 |

|

| Income tax expense (benefit) |

|

|

(3,318 |

) |

|

|

1,879 |

|

|

|

|

|

(4,049 |

) |

|

|

731 |

|

|

|

(2,351 |

) |

|

|

1,387 |

|

|

|

672 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Net income (loss) |

|

$ |

(6,777 |

) |

|

$ |

6,305 |

|

|

|

|

$ |

(8,826 |

) |

|

$ |

2,049 |

|

|

$ |

(1,244 |

) |

|

$ |

(7,299 |

) |

|

$ |

3,123 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Preferred stock dividends |

|

|

611 |

|

|

|

688 |

|

|

|

|

|

301 |

|

|

|

310 |

|

|

|

321 |

|

|

|

348 |

|

|

|

340 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Net income (loss) applicable to common shareholders |

|

$ |

(7,388 |

) |

|

$ |

5,617 |

|

|

|

|

$ |

(9,127 |

) |

|

$ |

1,739 |

|

|

$ |

(1,565 |

) |

|

$ |

(7,647 |

) |

|

$ |

2,783 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Per common share information |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Earnings (loss) |

|

$ |

(0.73 |

) |

|

$ |

0.56 |

|

|

|

|

$ |

(0.90 |

) |

|

$ |

0.17 |

|

|

$ |

(0.16 |

) |

|

$ |

(0.77 |

) |

|

$ |

0.28 |

|

| Diluted earnings (loss) (1) |

|

|

(0.73 |

) |

|

|

0.55 |

|

|

|

|

|

(0.90 |

) |

|

|

0.17 |

|

|

|

(0.16 |

) |

|

|

(0.77 |

) |

|

|

0.27 |

|

| Dividends paid |

|

|

0.02 |

|

|

|

0.02 |

|

|

|

|

|

0.01 |

|

|

|

0.01 |

|

|

|

0.01 |

|

|

|

0.01 |

|

|

|

0.01 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Average common shares issued and outstanding |

|

|

10,085,479 |

|

|

|

9,570,166 |

|

|

|

|

|

10,094,928 |

|

|

|

10,075,875 |

|

|

|

10,036,575 |

|

|

|

9,976,351 |

|

|

|

9,956,773 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Average diluted common shares issued and

outstanding (1) |

|

|

10,085,479 |

|

|

|

10,020,926 |

|

|

|

|

|

10,094,928 |

|

|

|

10,181,351 |

|

|

|

10,036,575 |

|

|

|

9,976,351 |

|

|

|

10,029,776 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| (1) |

Due to a net loss applicable to common shareholders for the second quarter of 2011 and for the fourth and third quarters of 2010, the impact of antidilutive equity

instruments was excluded from diluted earnings per share and average diluted common shares. |

Certain prior period amounts

have been reclassified to conform to current period presentation.

|

|

|

| This information is preliminary and based on company data available at the time of the presentation. |

|

4 |

Bank of America Corporation and Subsidiaries

Consolidated Balance Sheet

(Dollars in millions)

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

June 30

2011 |

|

|

March 31

2011 |

|

|

June 30

2010 |

|

| Assets |

|

|

|

|

|

|

|

|

|

|

|

|

| Cash and cash equivalents |

|

$ |

119,527 |

|

|

$ |

97,542 |

|

|

$ |

151,034 |

|

| Time deposits placed and other short-term investments |

|

|

20,291 |

|

|

|

23,707 |

|

|

|

20,718 |

|

| Federal funds sold and securities borrowed or purchased under agreements to resell |

|

|

235,181 |

|

|

|

234,056 |

|

|

|

247,667 |

|

| Trading account assets |

|

|

196,939 |

|

|

|

208,761 |

|

|

|

197,376 |

|

| Derivative assets |

|

|

66,598 |

|

|

|

65,334 |

|

|

|

87,839 |

|

| Debt securities: |

|

|

|

|

|

|

|

|

|

|

|

|

| Available-for-sale |

|

|

330,871 |

|

|

|

330,345 |

|

|

|

314,765 |

|

| Held-to-maturity, at cost |

|

|

181 |

|

|

|

431 |

|

|

|

435 |

|

| Total debt securities |

|

|

331,052 |

|

|

|

330,776 |

|

|

|

315,200 |

|

| Loans and leases |

|

|

941,257 |

|

|

|

932,425 |

|

|

|

956,177 |

|

| Allowance for loan and lease losses |

|

|

(37,312 |

) |

|

|

(39,843 |

) |

|

|

(45,255 |

) |

| Loans and leases, net of allowance |

|

|

903,945 |

|

|

|

892,582 |

|

|

|

910,922 |

|

| Premises and equipment, net |

|

|

13,793 |

|

|

|

14,151 |

|

|

|

14,536 |

|

| Mortgage servicing rights (includes $12,372, $15,282 and $14,745 measured at fair value) |

|

|

12,642 |

|

|

|

15,560 |

|

|

|

15,041 |

|

| Goodwill |

|

|

71,074 |

|

|

|

73,869 |

|

|

|

85,801 |

|

| Intangible assets |

|

|

9,176 |

|

|

|

9,560 |

|

|

|

10,796 |

|

| Loans held-for-sale |

|

|

20,092 |

|

|

|

25,003 |

|

|

|

38,046 |

|

| Customer and other receivables |

|

|

86,550 |

|

|

|

97,318 |

|

|

|

86,466 |

|

| Other assets |

|

|

174,459 |

|

|

|

186,313 |

|

|

|

186,942 |

|

| Total assets |

|

$ |

2,261,319 |

|

|

$ |

2,274,532 |

|

|

$ |

2,368,384 |

|

|

|

|

|

| Assets of consolidated VIEs included in total assets above (substantially all pledged

as collateral) |

|

|

|

|

|

|

|

|

|

|

|

|

| Trading account assets |

|

$ |

10,746 |

|

|

$ |

12,012 |

|

|

$ |

10,675 |

|

| Derivative assets |

|

|

2,293 |

|

|

|

2,280 |

|

|

|

2,094 |

|

| Available-for-sale debt securities |

|

|

251 |

|

|

|

2,104 |

|

|

|

9,493 |

|

| Loans and leases |

|

|

151,928 |

|

|

|

146,309 |

|

|

|

134,143 |

|

| Allowance for loan and lease losses |

|

|

(7,792 |

) |

|

|

(8,335 |

) |

|

|

(10,585 |

) |

| Loans and leases, net of allowance |

|

|

144,136 |

|

|

|

137,974 |

|

|

|

123,558 |

|

| Loans held-for-sale |

|

|

1,561 |

|

|

|

1,605 |

|

|

|

3,371 |

|

| All other assets |

|

|

7,115 |

|

|

|

4,883 |

|

|

|

9,190 |

|

| Total assets of consolidated VIEs |

|

$ |

166,102 |

|

|

$ |

160,858 |

|

|

$ |

158,381 |

|

Certain prior period amounts have been reclassified to conform to current period presentation.

|

|

|

| This information is preliminary and based on company data available at the time of the presentation. |

|

5 |

Bank of America Corporation and Subsidiaries

Consolidated Balance Sheet (continued)

(Dollars in millions)

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

June 30

2011 |

|

|

March 31

2011 |

|

|

June 30

2010 |

|

| Liabilities |

|

|

|

|

|

|

|

|

|

|

|

|

| Deposits in U.S. offices: |

|

|

|

|

|

|

|

|

|

|

|

|

| Noninterest-bearing |

|

$ |

301,558 |

|

|

$ |

286,357 |

|

|

$ |

258,988 |

|

| Interest-bearing |

|

|

647,480 |

|

|

|

652,096 |

|

|

|

640,807 |

|

| Deposits in non-U.S. offices: |

|

|

|

|

|

|

|

|

|

|

|

|

| Noninterest-bearing |

|

|

6,555 |

|

|

|

7,894 |

|

|

|

5,791 |

|

| Interest-bearing |

|

|

82,815 |

|

|

|

73,828 |

|

|

|

68,881 |

|

| Total deposits |

|

|

1,038,408 |

|

|

|

1,020,175 |

|

|

|

974,467 |

|

| Federal funds purchased and securities loaned or sold under agreements to repurchase |

|

|

239,521 |

|

|

|

260,521 |

|

|

|

307,211 |

|

| Trading account liabilities |

|

|

74,989 |

|

|

|

88,478 |

|

|

|

89,982 |

|

| Derivative liabilities |

|

|

54,414 |

|

|

|

53,501 |

|

|

|

67,297 |

|

| Commercial paper and other short-term borrowings |

|

|

50,632 |

|

|

|

58,324 |

|

|

|

73,358 |

|

| Accrued expenses and other liabilities (includes $897, $961 and $1,413 of reserve for unfunded lending

commitments) |

|

|

154,520 |

|

|

|

128,221 |

|

|

|

132,812 |

|

| Long-term debt |

|

|

426,659 |

|

|

|

434,436 |

|

|

|

490,083 |

|

| Total liabilities |

|

|

2,039,143 |

|

|

|

2,043,656 |

|

|

|

2,135,210 |

|

| Shareholders’ equity |

|

|

|

|

|

|

|

|

|

|

|

|

| Preferred stock, $0.01 par value; authorized -100,000,000 shares; issued and outstanding - 3,943,660, 3,943,660 and

3,960,660 shares |

|

|

16,562 |

|

|

|

16,562 |

|

|

|

17,993 |

|

| Common stock and additional paid-in capital, $0.01 par value; authorized - 12,800,000,000, 12,800,000,000 and

12,800,000,000 shares; issued and outstanding - 10,133,189,501, 10,131,803,417 and 10,033,016,719 shares |

|

|

151,567 |

|

|

|

151,379 |

|

|

|

149,175 |

|

| Retained earnings |

|

|

53,254 |

|

|

|

62,483 |

|

|

|

70,497 |

|

| Accumulated other comprehensive income (loss) |

|

|

793 |

|

|

|

463 |

|

|

|

(4,447 |

) |

| Other |

|

|

— |

|

|

|

(11 |

) |

|

|

(44 |

) |

| Total shareholders’ equity |

|

|

222,176 |

|

|

|

230,876 |

|

|

|

233,174 |

|

| Total liabilities and shareholders’ equity |

|

$ |

2,261,319 |

|

|

$ |

2,274,532 |

|

|

$ |

2,368,384 |

|

|

|

|

|

| Liabilities of consolidated VIEs included in total liabilities

above |

|

|

|

|

|

|

|

|

|

|

|

|

| Commercial paper and other short-term borrowings |

|

$ |

5,421 |

|

|

$ |

6,954 |

|

|

$ |

17,848 |

|

| Long-term debt |

|

|

64,745 |

|

|

|

65,197 |

|

|

|

85,186 |

|

| All other liabilities |

|

|

1,127 |

|

|

|

1,240 |

|

|

|

2,535 |

|

| Total liabilities of consolidated

VIEs |

|

$ |

71,293 |

|

|

$ |

73,391 |

|

|

$ |

105,569 |

|

Certain prior period amounts have been reclassified to conform to current period presentation.

|

|

|

| This information is preliminary and based on company data available at the time of the presentation. |

|

6 |

Bank of America Corporation and Subsidiaries

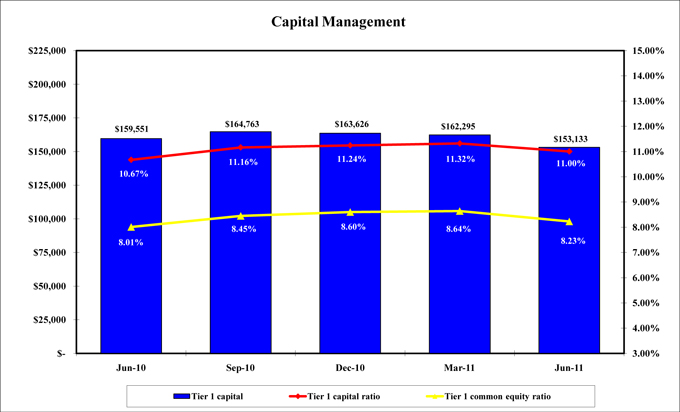

Capital Management

(Dollars in millions)

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

Second

Quarter

2011 |

|

|

|

|

First

Quarter

2011 |

|

|

|

|

Fourth

Quarter

2010 |

|

|

|

|

Third

Quarter

2010 |

|

|

|

|

Second

Quarter

2010 |

|

|

|

| Risk-based capital (1): |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Tier 1 common |

|

$ |

114,684 |

|

|

|

|

$ |

123,882 |

|

|

|

|

$ |

125,139 |

|

|

|

|

$ |

124,756 |

|

|

|

|

$ |

119,716 |

|

|

|

| Tier 1 capital |

|

|

153,133 |

|

|

|

|

|

162,295 |

|

|

|

|

|

163,626 |

|

|

|

|

|

164,763 |

|

|

|

|

|

159,551 |

|

|

|

| Total capital |

|

|

217,986 |

|

|

|

|

|

229,094 |

|

|

|

|

|

229,594 |

|

|

|

|

|

231,120 |

|

|

|

|

|

220,827 |

|

|

|

| Risk-weighted assets |

|

|

1,392,747 |

|

|

|

|

|

1,433,377 |

|

|

|

|

|

1,455,951 |

|

|

|

|

|

1,476,774 |

|

|

|

|

|

1,494,990 |

|

|

|

| Tier 1 common equity ratio (2) |

|

|

8.23 |

|

|

% |

|

|

8.64 |

|

|

% |

|

|

8.60 |

|

|

% |

|

|

8.45 |

|

|

% |

|

|

8.01 |

|

|

% |

| Tier 1 capital ratio |

|

|

11.00 |

|

|

|

|

|

11.32 |

|

|

|

|

|

11.24 |

|

|

|

|

|

11.16 |

|

|

|

|

|

10.67 |

|

|

|

| Total capital ratio |

|

|

15.65 |

|

|

|

|

|

15.98 |

|

|

|

|

|

15.77 |

|

|

|

|

|

15.65 |

|

|

|

|

|

14.77 |

|

|

|

| Tier 1 leverage ratio |

|

|

6.86 |

|

|

|

|

|

7.25 |

|

|

|

|

|

7.21 |

|

|

|

|

|

7.21 |

|

|

|

|

|

6.68 |

|

|

|

| Tangible equity ratio (3) |

|

|

6.63 |

|

|

|

|

|

6.85 |

|

|

|

|

|

6.75 |

|

|

|

|

|

6.54 |

|

|

|

|

|

6.14 |

|

|

|

| Tangible common equity ratio (3) |

|

|

5.87 |

|

|

|

|

|

6.10 |

|

|

|

|

|

5.99 |

|

|

|

|

|

5.74 |

|

|

|

|

|

5.35 |

|

|

|

| (1) |

Reflects preliminary data for current period risk-based capital. |

| (2) |

Tier 1 common equity ratio equals Tier 1 capital excluding preferred stock, trust preferred securities, hybrid securities and minority interest divided by

risk-weighted assets. |

| (3) |

Tangible equity ratio equals period end tangible shareholders’ equity divided by period end tangible assets. Tangible common equity equals period end tangible

common shareholders’ equity divided by period end tangible assets. Tangible shareholders’ equity and tangible assets are non-GAAP measures. We believe the use of these non-GAAP measures provide additional clarity in assessing the results

of the Corporation. (See Exhibit A: Non-GAAP Reconciliations - Reconciliation to GAAP Financial Measures on pages 44-45). |

| * |

Preliminary data on risk-based capital |

Outstanding Common Stock

No common shares were repurchased in the second

quarter of 2011.

There is no existing Board authorized share repurchase program.

Certain prior period amounts have been reclassified to conform to current period presentation.

|

|

|

| This information is preliminary and based on company data available at the time of the presentation. |

|

7 |

Bank of America Corporation and Subsidiaries

Core Net Interest Income

(Dollars in millions)

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

Six Months

Ended

June 30 |

|

|

|

|

|

|

Second

Quarter |

|

|

|

|

|

First Quarter |

|

|

|

|

|

Fourth Quarter |

|

|

|

|

|

Third Quarter |

|

|

|

|

|

Second

Quarter |

|

|

|

|

| |

|

2011 |

|

|

|

|

|

2010 |

|

|

|

|

|

|

2011 |

|

|

|

|

|

2011 |

|

|

|

|

|

2010 |

|

|

|

|

|

2010 |

|

|

|

|

|

2010 |

|

|

|

|

| Net interest income (1) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| As reported (2) |

|

$ |

23,890 |

|

|

|

|

|

|

$ |

27,267 |

|

|

|

|

|

|

$ |

11,493 |

|

|

|

|

|

|

$ |

12,397 |

|

|

|

|

|

|

$ |

12,709 |

|

|

|

|

|

|

$ |

12,717 |

|

|

|

|

|

|

$ |

13,197 |

|

|

|

|

|

| Impact of market-based net

interest

income (3) |

|

|

(1,965 |

) |

|

|

|

|

|

|

(2,235 |

) |

|

|

|

|

|

|

(914 |

) |

|

|

|

|

|

|

(1,051 |

) |

|

|

|

|

|

|

(1,150 |

) |

|

|

|

|

|

|

(1,045 |

) |

|

|

|

|

|

|

(1,049 |

) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Core net interest income |

|

$ |

21,925 |

|

|

|

|

|

|

$ |

25,032 |

|

|

|

|

|

|

$ |

10,579 |

|

|

|

|

|

|

$ |

11,346 |

|

|

|

|

|

|

$ |

11,559 |

|

|

|

|

|

|

$ |

11,672 |

|

|

|

|

|

|

$ |

12,148 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Average earning assets (4) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| As reported |

|

$ |

1,857,124 |

|

|

|

|

|

|

$ |

1,921,864 |

|

|

|

|

|

|

$ |

1,844,525 |

|

|

|

|

|

|

$ |

1,869,863 |

|

|

|

|

|

|

$ |

1,883,539 |