UNITED

STATES

SECURITIES

AND EXCHANGE COMMISSION

WASHINGTON,

D. C. 20549

FORM

10-K

|

x

|

ANNUAL

REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF

1934

|

For

the fiscal year ended June 30, 2008

OR

|

o

|

TRANSITION

REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF

1934

|

For the

transition period from________ to _________

Commission

file number 1-44

ARCHER-DANIELS-MIDLAND

COMPANY

(Exact

name of registrant as specified in its charter)

|

Delaware

|

41-0129150

|

|

(State

or other jurisdiction of

|

(I.

R. S. Employer

|

|

incorporation

or organization)

|

Identification

No.)

|

|

4666

Faries Parkway Box 1470 Decatur,

Illinois

|

62525

|

|

(Address

of principal executive offices)

|

(Zip

Code)

|

|

217-424-5200

|

|

|

(Registrant's

telephone number, including area code)

|

|

|

Securities

registered pursuant to Section 12(b) of the Act:

|

|

|

Title of each

class

|

Name of each exchange

on which registered

|

|

Common

Stock, no par value

|

New

York Stock Exchange

|

|

Frankfurt

Stock Exchange

|

|

Securities

registered pursuant to Section 12(g) of the Act:

None

Indicate

by check mark if the registrant is a well-known seasoned issuer, as defined in

Rule 405 of the Securities Act. Yes x No

¨

Indicate

by check mark if the registrant is not required to file reports pursuant to

Section 13 or 15(d) of the Act.

Yes ¨ No x

Indicate

by check mark whether the registrant (1) has filed all reports required to be

filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the

preceding 12 months (or for such shorter period that the registrant was required

to file such reports), and (2) has been subject to such filing requirements for

the past 90 days.

Yes x No ¨

Indicate

by check mark if disclosure of delinquent filers pursuant to Item 405 of

Regulation S-K is not contained herein, and will not be contained, to the best

of registrant’s knowledge, in definitive proxy or information statements

incorporated by reference in Part III of this Form 10-K or any amendment to this

Form 10-K. o

Indicate

by check mark whether the registrant is a large accelerated filer, an

accelerated filer, a non-accelerated filer, or a smaller reporting

company. See definition of “large accelerated filer”, “accelerated

filer” and “smaller reporting company” in Rule 12b-2 of the Exchange

Act.

Large

Accelerated Filer x Accelerated

Filer o

Non-accelerated

Filer o Smaller

Reporting Company o

Indicate

by check mark whether the registrant is a shell company (as defined in Rule

12b-2 of the Exchange Act).

Yes o No x

State the

aggregate market value of the voting and non-voting common equity held by

non-affiliates computed by reference to the price at which the common equity was

last sold, or the average bid and asked price of such common equity, as of the

last business day of the registrant’s most recently completed second fiscal

quarter.

Common

Stock, no par value--$29.2 billion

(Based on

the closing sale price of Common Stock as reported on the New York Stock

Exchange

as of

December 31, 2007)

Indicate

the number of shares outstanding of each of the registrant’s classes of common

stock, as of the latest practicable date.

Common

Stock, no par value—644,267,509 shares

(July 31,

2008)

DOCUMENTS

INCORPORATED BY REFERENCE

Portions

of the proxy statement for the annual meeting of stockholders to be held

November 6, 2008, are incorporated by reference into Part III.

SAFE

HARBOR STATEMENT

This Form

10-K contains forward-looking information that is subject to certain risks and

uncertainties that could cause actual results to differ materially from those

projected, expressed, or implied by such forward-looking

information. In some cases, you can identify forward-looking

statements by our use of words such as “may, will, should, anticipates,

believes, expects, plans, future, intends, could, estimate, predict, potential

or contingent,” the negative of these terms or other similar

expressions. The Company’s actual results could differ materially

from those discussed or implied herein. Factors that could cause or

contribute to such differences include, but are not limited to, those discussed

in this Form 10-K for the fiscal year ended June 30, 2008. Among

these risks are legislative acts; changes in the prices of food, feed, and other

commodities, including gasoline; and macroeconomic conditions in various parts

of the world. To the extent permitted under applicable law, the

Company assumes no obligation to update any forward-looking statements as a

result of new information or future events.

Table of

Contents

|

Item

No.

|

Description

|

Page

No.

|

|

Part

I

|

||

|

1.

|

Business

|

4

|

|

1A.

|

Risk

Factors

|

10

|

|

1B.

|

Unresolved

Staff Comments

|

12

|

|

2.

|

Properties

|

13

|

|

3.

|

Legal

Proceedings

|

15

|

|

4.

|

Submission

of Matters to a Vote of Security Holders

|

15

|

|

|

||

|

Part

II

|

||

|

5.

|

Market

for Registrant’s Common Equity, Related Stockholder Matters,

and

Issuer Purchases of Equity Securities

|

16

|

|

6.

|

Selected

Financial Data

|

19

|

|

7.

|

Management’s

Discussion and Analysis of Financial Condition and

Results

of Operations

|

20

|

|

7A.

|

Quantitative

and Qualitative Disclosures About Market Risk

|

34

|

|

8.

|

Financial

Statements and Supplementary Data

|

36

|

|

9.

|

Changes

in and Disagreements With Accountants on Accounting

and

Financial Disclosure

|

75

|

|

9A.

|

Controls

and Procedures

|

75

|

|

9B.

|

Other

Information

|

75

|

|

Part

III

|

||

|

10.

|

Directors,

Executive Officers and Corporate Governance

|

76

|

|

11.

|

Executive

Compensation

|

78

|

|

12.

|

Security

Ownership of Certain Beneficial Owners and Management

and

Related Stockholder Matters

|

79

|

|

13.

|

Certain

Relationships and Related Transactions, and Director

Independence

|

79

|

|

14.

|

Principal

Accounting Fees and Services

|

79

|

|

Part

IV

|

||

|

15.

|

Exhibits

and Financial Statement Schedules

|

79

|

|

Signatures

|

84

|

|

PART

I

|

Item

1.

|

BUSINESS

|

Company

Overview

Archer

Daniels Midland Company (the Company) was incorporated in Delaware in 1923,

successor to the Daniels Linseed Co. founded in 1902. The Company is

one of the world’s largest processors of oilseeds, corn, wheat, cocoa, and other

feedstuffs and is a leading manufacturer of soybean oil and protein meal, corn

sweeteners, flour, biodiesel, ethanol, and other value-added food and

feed ingredients. The Company also has an extensive grain elevator

and transportation network to procure, store, clean, and transport agricultural

commodities, such as oilseeds, corn, wheat, milo, oats, and barley.

During

the past five years, the Company has experienced significant growth, spending

approximately $5.3 billion for construction of new plants, maintenance and

expansions of existing plants, and the acquisitions of plants and transportation

equipment. The Company is constructing two dry corn milling plants

which will increase the Company’s annual ethanol production capacity by 550

million gallons to 1.7 billion gallons. In addition, the Company is

currently constructing a polyhydroxy alkanoate (PHA) natural plastics production

facility, a propylene/ethylene glycol production facility, two cocoa processing

facilities, and two coal cogeneration facilities. Construction of

these plants is expected to be completed during the next two fiscal

years. The Company expects to spend approximately $2.5 billion to

complete construction of these facilities and other approved capital projects

over the next five years. There have been no significant dispositions

during the last five years.

Segment

Descriptions

The

Company’s operations are classified into three reportable business segments:

Oilseeds Processing, Corn Processing, and Agricultural Services. Each

of these segments is organized based upon the nature of products and services

offered. The Company’s remaining operations are aggregated and

classified as Other. Financial information with respect to the

Company’s reportable business segments is set forth in “Note 14 of Notes to

Consolidated Financial Statements” included in Item 8 herein, “Financial

Statements and Supplementary Data.”

Oilseeds

Processing

The

Company is engaged in processing oilseeds such as soybeans, cottonseed,

sunflower seeds, canola, peanuts, and flaxseed into vegetable oils and protein

meals in North America, Europe, South America and Asia principally for the food

and feed industries. Crude vegetable oil is sold “as is” or is

further processed by refining, bleaching, and deodorizing into salad

oils. Salad oils can be further processed by hydrogenating and/or

interesterifying into margarine, shortening, and other food

products. Partially refined oil is sold for use in chemicals, paints

and other industrial products. Refined oil can be further processed

for use in the production of biodiesel. Oilseed meals are primary

ingredients used in the manufacture of commercial livestock and poultry

feeds. Cottonseed flour is produced and sold primarily to the

pharmaceutical industry. Cotton cellulose pulp is manufactured and

sold to the chemical, paper, and filter markets. Lecithin, an

emulsifier produced in the vegetable oil refining process, is marketed as a food

and animal feed ingredient.

The

Company produces a wide range of edible soy protein products including soy

flour, soy grits, soy protein concentrates and soy isolates that are used in

processed meats, baked foods, nutritional products, snacks, and dairy and meat

analogs.

The

Company produces natural source vitamin E, tocopherol antioxidants and

phytosterols from co-products of oilseeds which are marketed to the dietary

supplement and food industry. The Company produces soy isoflavones, a

dietary supplement, from a co-product of edible soy processing.

In South

America, the Company is also a supplier of fertilizer products.

|

Item

1.

|

BUSINESS

(Continued)

|

Golden

Peanut Company LLC, a joint venture between the Company and Alimenta (U.S.A.),

Inc., is a major supplier of peanuts to both the domestic and export

markets. The Company has a 50% ownership interest in this joint

venture.

The

Company has a 16.1% ownership interest in Wilmar International Limited, a

Singapore publicly-listed company. Wilmar International Limited is

the largest agricultural processing business in Asia and operates palm

plantations; soybean, rapeseed, cottonseed, sunflower seed, peanut, palm kernel,

and sesame seed crushing facilities and related vegetable oil refineries and

packaging facilities; an oleochemical plant that produces fatty acids, glycerin,

and soap noodles; a soy protein plant; wheat flour mills; rice mills; feed

mills; fertilizer operations; and related silos and storage

facilities.

Corn

Processing

The

Company is engaged in wet milling and dry milling corn operations primarily in

the United States. Products produced for use in the food and beverage

industry include syrup, starch, glucose, dextrose, and

sweeteners. Dextrose is also produced for use by the Company as a

feedstock for its bioproducts operations. Corn gluten feed and meal

as well as distillers grains are produced for use as animal feed

ingredients. Corn germ, a by-product of the wet milling process, is

further processed as an oilseed into vegetable oil and protein

meal.

By

fermentation of dextrose, the Company produces alcohol, amino acids, and other

specialty food and animal feed ingredients. Ethyl alcohol is produced

to beverage grade or for industrial use as ethanol. In gasoline,

ethanol increases octane and is used as an extender and

oxygenate. Amino acids, such as lysine and threonine, are vital

compounds used in swine feeds to produce leaner animals and in poultry feeds to

enhance the speed and efficiency of poultry production. The Company

also produces, by fermentation, astaxanthin, a product used in aquaculture to

enhance flesh coloration. The Company produces citric and lactic

acids, lactates, sorbitol and xanthan gum which are used in various food and

industrial products.

Almidones

Mexicanos S.A., in which the Company has a 50% interest, operates a wet corn

milling plant in Mexico.

Eaststarch

C.V. (Netherlands), in which the Company has a 50% interest, owns interests in

companies that operate wet corn milling plants in Bulgaria, Hungary, Romania,

Slovakia, and Turkey.

The

Company has a 50% interest in Telles, LLC (Telles), a joint venture formed

between the Company and Metabolix to market and sell PHA, which will be produced

in a facility being constructed by the Company which is expected to be completed

during fiscal 2009.

Red Star

Yeast Company, LLC produces and sells fresh and dry yeast in the United States

and Canada. The Company has a 40% ownership interest in this joint

venture.

Agricultural

Services

The

Agricultural Services segment utilizes the Company’s extensive grain elevator

and transportation network in the United States to buy, store, clean, and

transport agricultural commodities, such as oilseeds, corn, wheat, milo, oats,

and barley, and resells these commodities primarily as animal feed ingredients

and as raw materials for the agricultural processing

industry. Agricultural Services’ grain sourcing and transportation

network provides reliable and efficient services to the Company’s agricultural

processing operations. Agricultural Services’ transportation network

capabilities include ground, river, rail, and ocean services which provide the

flexibility to transport agricultural commodities timely and efficiently to the

end consumer or the Company’s agricultural processing operations.

|

Item

1.

|

BUSINESS

(Continued)

|

The

Company processes and distributes edible beans in the United States for use as a

food ingredient. The Company produces and distributes formula feeds

and animal health and nutrition products to the livestock, dairy, poultry, and

pet food industries.

A.C.

Toepfer International (Toepfer), in which the Company has an 80% interest, is a

global merchandiser of agricultural commodities and processed

products. Toepfer has 38 sales offices worldwide and operates export,

river, and country elevators in Argentina, Romania, Ukraine, and the United

States.

The

Company has a 45% interest in Kalama Export Company, a grain export elevator in

Washington.

Other

The

Company is engaged in milling wheat, corn, and milo into flour in the United

States, Canada, the Caribbean, and the United Kingdom. Wheat flour is

sold primarily to commercial bakeries, food companies, food service companies,

and retailers. Bulgur, a gelatinized wheat food, is sold to both the

export and the domestic food markets. Corn meal and flour is sold

primarily to the cereal, snack, and bakery mix markets. The Company

produces bakery products and mixes, wheat starch, and gluten which are sold to

the baking industry. The Company also mills milo to produce

industrial flour used in the manufacturing of wallboard for the building

industry.

Gruma

S.A. de C.V.(Gruma), in which the Company has a 23% interest, is the world’s

largest producer and marketer of corn flour and tortillas with operations in the

United States, Mexico, Central America, South America, and

Europe. Additionally, the Company has a 20% share, through a joint

venture with Gruma, in six U.S. corn flour mills. The Company

also has a 40% share, through a joint venture with Gruma, in nine Mexican-based

wheat flour mills.

The

Company processes cocoa beans and produces cocoa liquor, cocoa butter, cocoa

powder, chocolate, and various compounds in North America, South America,

Europe, Asia, and Africa for the food processing industry.

The

Company sold its interest in International Malting Company (IMC), a wholly-owned

subsidiary of the Company, which operated malting barley plants in the United

States, Australia, New Zealand, and Canada on July 31, 2008.

Hickory

Point Bank and Trust Company, fsb, a wholly-owned subsidiary of the Company,

furnishes public banking and trust services, as well as cash management,

transfer agency, and securities safekeeping services, for the

Company.

ADM

Investor Services, Inc., a wholly-owned subsidiary of the Company, is a

registered futures commission merchant and a clearing member of all principal

commodities exchanges. ADM Investor Services International, Ltd.,

ADMIS Hong Kong Limited, and ADM Investor Services Taiwan are wholly-owned

subsidiaries of the Company offering broker services in Europe and

Asia. ADM Derivatives, Inc. offers foreign exchange services to

institutional and retail clients.

Agrinational

Insurance Company, a wholly-owned subsidiary of the Company, provides insurance

coverage for certain property, casualty, marine, and other miscellaneous risks

of the Company and participates in certain third-party reinsurance

arrangements.

The

Company is a limited partner in various private equity funds which invest

primarily in emerging markets.

|

Item

1.

|

BUSINESS

(Continued)

|

Corporate

Compagnie

Industrielle et Financiere des produits Amylaces SA (Luxembourg) and affiliates,

of which the Company has a 41.5% interest, is a joint venture which targets

investments in food, feed ingredients and bioenergy businesses.

Methods

of Distribution

Since the

Company’s customers are principally other manufacturers and processors, the

Company’s products are distributed mainly in bulk from processing plants or

storage facilities directly to the customers’ facilities. The Company

has developed a comprehensive transportation system utilizing trucks, railcars,

river barges, and ocean-going vessels to efficiently move both commodities and

processed products virtually anywhere in the world. The Company owns

or leases large numbers of the trucks, trailers, railroad tank and hopper cars,

river barges, and towboats used in this transportation system.

Concentration

of Sales by Product

The

following products account for 10% or more of net sales and other operating

income for the last three fiscal years:

| % of Net Sales and Other Operating Income | ||||||||||||

|

2008

|

2007

|

2006

|

||||||||||

|

Soybeans

|

16%

|

12%

|

14%

|

|||||||||

|

Corn

|

14%

|

15%

|

12%

|

|||||||||

|

Soybean

Meal

|

11%

|

12%

|

13%

|

|||||||||

|

Wheat

|

10%

|

8%

|

8%

|

|||||||||

Status

of New Products

The

Company continues to expand its business through the development of new products

to meet the growing demands for food, animal feed, chemicals and

energy.

The

Company’s researchers continue to develop custom low-trans fats and oils for

bakery and quick-service restaurants that utilize the Company’s Novalipid

portfolio of low-trans fats and oils. These products have enabled

customers to comply with various municipal trans fat bans.

The

Company’s cooked, dried edible bean products are finding a number of new

applications due to the increased interest among our customers in improving

nutrition, especially in the area of foods designed for children.

The

Company’s alliance with Metabolix for production of PHA, a biodegradable

plastic, is proceeding. Semi-works production of PHA is being used

for market development by Telles, a joint-venture company between the Company

and Metabolix. The construction of the Company’s 50,000 metric ton per year

commercial manufacturing facility is scheduled for completion in fiscal

2009.

The

Company is proceeding with construction of a 100,000 metric ton per year

commercial propylene/ethylene glycol facility. These products are

principally used in industrial applications such as antifreeze and coolants, the

manufacture of certain plastics, and paints and coatings.

The

Company has entered into a joint development agreement with ConocoPhillips that

will develop renewable transportation fuels from agriculture, forestry, and

crops grown specifically for energy. This development effort is focused on the

production of bio-crude oil that can be used by conventional petroleum

refineries to produce transportation fuels.

|

Item

1.

|

BUSINESS

(Continued)

|

Source

and Availability of Raw Materials

Substantially

all of the Company’s raw materials are agricultural commodities. In

any single year, the availability and price of these commodities are subject to

unpredictable factors such as weather, plantings, government programs

and policies, changes in global demand created by population growth and changes

in standards of living, and global production of similar and competitive

crops. The Company’s raw materials are procured from thousands of

growers, grain elevators, and wholesale merchants, principally in North America,

South America, and Europe, pursuant to short-term agreements (less than one

year) or on a spot basis. The Company is not dependent upon any

particular grower, elevator, or merchant as a source for its raw

materials.

Patents,

Trademarks, and Licenses

The

Company owns several valuable patents, trademarks, and licenses but does not

consider any segment of its business dependent upon any single or group of

patents, trademarks or licenses.

Seasonality,

Working Capital Needs, and Significant Customers

Since the

Company is so widely diversified in global agribusiness markets, there are no

material seasonal fluctuations in the manufacture, sale, and distribution of its

products and services. There is a degree of seasonality in the

growing cycles, procurement, and transportation of the Company’s principal raw

materials: oilseeds, corn, wheat, cocoa beans, and other

grains. However, the physical movement of the millions of bushels of

these crops through the Company’s processing facilities is reasonably constant

throughout the year.

Price

variations and availability of raw agricultural commodities may cause

fluctuations in the Company’s working capital levels. No material

part of the Company’s business in any segment is dependent upon a single

customer or very few customers.

Competition

The

Company has significant competition in the markets in which it operates based

principally on price, quality, products and alternative products, some of which

are made from different raw materials than those utilized by the

Company. Given the commodity-based nature of many of its businesses,

the Company, on an ongoing basis, focuses on managing unit

costs and improving efficiency through technology improvements, productivity

enhancements, and regular evaluation of the Company’s asset

portfolio.

Research

and Development Expenditures

The

Company’s research and development expenditures are focused on developing food,

animal feed, chemical, and energy products from renewable agricultural

crops.

The

Company maintains a research laboratory in Decatur, Illinois, where product and

process development activities are conducted. Activities include the

development of new bioproducts and the improvement of existing bioproducts, by

utilizing new microbial strains that are developed using classical mutation and

genetic engineering. Protein and vegetable oil research is also

conducted in Decatur where bakery, meat and dairy pilot plants support food

ingredient research. Vegetable oil research is also conducted in

Hamburg, Germany; Erith, UK; and Arras, France. Research in Hamburg,

Germany was expanded this year to include capabilities for biodiesel and

oleochemicals. Research to support sales and development of flour and

bakery products is conducted at a newly-constructed laboratory in Overland Park,

Kansas. Sales and development support for cocoa and chocolate

products is performed in Milwaukee, Wisconsin, and the

Netherlands. Research and technical support for industrial and food

wheat starch applications is conducted in Montreal, Canada. The

Company has consolidated its research facilities by closing the Clinton, Iowa

and Decatur, Indiana research locations and relocating staff to the research

center in Decatur, Illinois.

|

Item

1.

|

BUSINESS

(Continued)

|

The

Company uses technical services representatives to interact with customers to

understand the customers’ product needs. These technical service

representatives then interact with researchers who are familiar with the

Company’s wide range of products as well as applications

technology. These individuals form quick-acting teams to develop

solutions to customer needs.

The

Company has entered into a new cooperative research and development agreement

with Pacific Northwest National Laboratory which is focused on hydrothermal

liquefaction of biomass to biocrude oils. This agreement is part of

the effort being undertaken to support a joint development project with

ConocoPhillips.

The

Company has begun research related to the recently awarded funding from the

Department of Energy to develop yeasts capable of fermenting 5-carbon sugars,

which is a key technology for producing ethanol from lignocellulosic

biomass. The Company is partnered with Purdue University on this

project.

The

amounts spent during the three years ended June 30, 2008, 2007 and 2006 for such

technical efforts were approximately $49 million, $45 million, and $45 million,

respectively.

Environmental

Compliance

During

the year ended June 30, 2008, $125 million was spent for equipment, facilities,

and programs for pollution control and compliance with the requirements of

various environmental agencies.

There

have been no material effects upon the earnings and competitive position of the

Company resulting from compliance with federal, state, and local laws or

regulations enacted or adopted relating to the protection of the

environment.

Number

of Employees

The

number of persons employed by the Company was approximately 27,600 at June 30,

2008.

Financial

Information About Foreign and Domestic Operations

Item 1A,

“Risk Factors,” and Item 2, “Properties,” includes information relating to the

Company’s foreign operations. Geographic financial information is set

forth in “Note 14 of Notes to Consolidated Financial Statements” included in

Item 8 herein, “Financial Statements and Supplementary Data”.

Available

Information

The

Company’s Internet address is http://www.admworld.com. The Company

makes available, free of charge, through its Internet site, the Company’s annual

reports on Form 10-K; quarterly reports on Form 10-Q; current reports on Form

8-K; Directors and Officers Forms 3, 4, and 5; and amendments to those reports,

as soon as reasonably practicable after electronically filing such materials

with, or furnishing them to, the Securities and Exchange Commission

(SEC).

In

addition, the Company makes available, through its Internet site, the Company’s

Business Code of Conduct and Ethics, Corporate Governance Guidelines, and the

written charters of the Audit, Compensation/Succession, Nominating/Corporate

Governance, and Executive Committees.

References

to our website addressed in this report are provided as a convenience and do not

constitute, or should not be viewed as, an incorporation by reference of the

information contained on, or available through, the

website. Therefore, such information should not be considered part of

this report.

|

Item

1.

|

BUSINESS

(Continued)

|

The

public may read and copy any materials filed by the Company with the SEC at the

SEC’s Public Reference Room at 100 F Street, N.E., Washington, D.C.

20549. The public may obtain information on the operation of the

Public Reference Room by calling the SEC at 1-800-SEC-0330. The SEC

maintains an Internet site which contains reports, proxy and information

statements, and other information regarding issuers that file information

electronically with the SEC. The SEC’s Internet address is

http://www.sec.gov.

|

Item

1A.

|

RISK

FACTORS

|

The

availability and price of the agricultural commodities and agricultural

commodity products the Company produces and merchandises can be affected by

weather, disease, government programs, competition, and various other factors

beyond the Company’s control and could adversely affect the Company’s operating

results.

The

availability and price of agricultural commodities are subject to wide

fluctuations due to unpredictable factors such as weather, plantings, government

programs and policies, changes in global demand resulting from population growth

and changes in standards of living, and global production of similar and

competitive crops. These factors have historically caused volatility

in the agricultural commodities industry and, consequently, in the Company’s

operating results. Reduced supply of agricultural commodities due to

weather-related factors or other reasons could adversely affect the Company’s

profitability by increasing the cost of raw materials used in the Company’s

agricultural processing operations. Reduced supplies of agricultural

commodities could also limit the Company’s ability to procure, transport, store,

process, and merchandise agricultural commodities in an efficient manner which

could adversely affect the Company’s profitability. In addition, the

availability and price of agricultural commodities can be affected by other

factors, such as plant disease, which can result in crop failures and reduced

harvests.

Also,

with respect to prices, to the extent production capacity is added within the

agricultural processing industry, the disruption to the balance of supply and

demand may result in increased raw material costs and/or downward pressure on

the relevant product selling prices, thereby adversely affecting revenues and

operating results.

Fluctuations

in energy prices could adversely affect the Company’s operating

results.

The

Company’s operating costs and the selling prices of certain finished products

are sensitive to changes in energy prices. The Company’s processing

plants are powered principally by electricity, natural gas, and

coal. The Company’s transportation operations are dependent upon

diesel fuel and other petroleum products. Significant increases in

the cost of these items could adversely affect the Company’s production costs

and operating results.

The

Company has certain finished products, such as ethanol and biodiesel, which are

closely related to, or may be substituted for, petroleum

products. Therefore, the selling prices of ethanol and biodiesel can

be impacted by the selling prices of gasoline and diesel fuel. A

significant decrease in the price of gasoline or diesel fuel could result in a

significant decrease in the selling price of the Company’s ethanol and biodiesel

and could adversely affect the Company’s revenues and operating

results.

The

Company is subject to economic downturns, political instability and other risks

of doing business globally which could adversely affect the Company’s operating

results.

The

Company conducts its business and has substantial assets located in many

countries and geographic areas. The Company’s operations are principally in the

United States and developed countries in Western Europe and South

America, but the Company also operates in, or plans to expand or develop its

business in, emerging market areas such as Asia, Eastern Europe, and Africa.

Both developed and emerging market areas are subject to economic downturns and

emerging market areas could be subject to more volatile economic, political and

market conditions. Such economic downturns and volatile conditions may have a

negative impact on the Company’s ability to execute its business strategies and

on its operating results.

|

Item

1A.

|

RISK

FACTORS (Continued)

|

The

Company’s operating results could be affected by changes in trade, monetary and

fiscal policies, laws and regulations, and other activities of governments,

agencies, and similar organizations. These conditions include but are

not limited to changes in a country’s or region’s economic or political

conditions, trade regulations affecting production, pricing and marketing of

products, local labor conditions and regulations, reduced protection of

intellectual property rights, changes in the regulatory or legal environment,

restrictions on currency exchange activities, currency exchange fluctuations,

burdensome taxes and tariffs, enforceability of legal agreements and judgments,

and other trade barriers. International risks and uncertainties,

including changing social and economic conditions as well as terrorism,

political hostilities, and war, could limit the Company’s ability to transact

business in these markets and could adversely affect the Company’s revenues and

operating results.

Government

policies and regulations, in general, and specifically affecting the

agricultural sector and related industries, could adversely affect the

Company’s operating results.

Agricultural

production and trade flows are subject to government policies and regulations.

Governmental policies affecting the agricultural industry, such as taxes,

tariffs, duties, subsidies, incentives, and import and export restrictions on

agricultural commodities and commodity products, can influence the planting of

certain crops, the location and size of crop production, whether unprocessed or

processed commodity products are traded, the volume and types of imports and

exports, the availability and competitiveness of feedstocks as raw materials,

and industry profitability. In addition, international trade disputes can

adversely affect agricultural commodity trade flows by limiting or disrupting

trade between countries or regions. Future government policies may adversely

affect the supply of, demand for, and prices of the Company’s products, restrict

the Company’s ability to do business in its existing and target markets, and

could negatively impact revenues and operating results.

The Company is subject to industry -

specific risks which could adversely affect the Company’s operating

results.

The

Company is subject to risks which include, but are not limited to, product

quality or contamination, shifting consumer preferences, federal, state, and

local food processing regulations, and customer product liability

claims. The liability which could result from these risks may not

always be covered by, or could exceed liability insurance related to product

liability and food safety matters maintained by the Company. The

occurrence of any of the matters described above could adversely affect the

Company’s revenues and operating results.

Certain

of the Company’s merchandised commodities and finished products are used as

ingredients in livestock and poultry feed. The Company is subject to

risks associated with the outbreak of disease in livestock and poultry,

including, but not limited to, mad-cow disease and avian

influenza. The outbreak of disease could adversely affect demand for

the Company’s products used as ingredients in livestock and poultry

feed. A decrease in demand for these products could adversely affect

the Company’s revenues and operating results.

The

Company is subject to numerous laws and regulations globally which could

adversely affect the Company’s operating results.

The

Company is required to comply with the numerous and broad reaching laws and

regulations administered by United States federal, state, local, and foreign

governmental agencies relating to, but not limited to, the sourcing,

transporting, storing, and processing of agricultural raw materials as well as

the transporting, storing and distributing of related agricultural products

including commercial activities conducted by Company employees and third parties

globally. Any failure to comply with applicable laws and regulations

could subject the Company to administrative penalties and injunctive relief,

civil remedies, including fines, injunctions, and recalls of its

products.

The

production of the Company’s products requires the use of materials which can

create emissions of certain regulated substances. Although the

Company has programs in place throughout the organization globally to guard

against non-compliance, failure to comply with these regulations can have

serious consequences, including civil and administrative penalties as well as a

negative impact on the Company’s reputation.

|

Item

1A.

|

RISK

FACTORS (Continued)

|

In

addition, changes to regulations may require the Company to modify existing

processing facilities and/or processes which could significantly increase

operating costs and negatively impact operating results.

The

Company is exposed to potential business disruption, including but not limited

to transportation services, and other serious adverse impacts resulting from

acts of terrorism or war, natural disasters and severe weather conditions, and

accidents which could adversely affect the Company’s operating

results.

The

assets and operations of the Company are subject to damage and disruption from

various events which include, but are not limited to, acts of terrorism or war,

natural disasters and severe weather conditions, accidents, explosions, and

fires.

The

potential effects of the conditions cited above include, but are not limited to,

extensive property damage, extended business interruption, personal injuries,

and damage to the environment. The Company’s operations also rely on

dependable and efficient transportation services. A disruption in

transportation services could result in supply problems at the Company’s

facilities and impair the Company’s ability to deliver products to its customers

in a timely manner.

The

Company’s business is capital intensive in nature and the Company relies on cash

generated from its operations and external financing to fund its growth and

ongoing capital needs. Limitations on access to external financing could

adversely affect the Company’s operating results.

The

Company requires significant capital to operate its current business and fund

its growth strategy. The Company’s working capital requirements are

directly affected by the price of agricultural commodities, which may fluctuate

significantly and change quickly. The Company also requires

substantial capital to maintain and upgrade its extensive network of storage

facilities, processing plants, refineries, mills, ports, transportation assets

and other facilities to keep pace with competitive developments, technological

advances, regulations and changing safety standards in the industry.

Moreover, the expansion of the Company’s business and pursuit of acquisitions or

other business opportunities may require significant amounts of

capital. If the Company is unable to generate sufficient cash flows

or raise adequate external financing, it may restrict the Company’s current

operations and its growth opportunities which could adversely affect the

Company’s operating results

The

Company’s risk management strategies may not be effective.

The

Company’s business is affected by fluctuations in agricultural commodity prices,

transportation costs, energy prices, interest rates, and foreign currency

exchange rates. We engage in hedging transactions to manage these

risks. However, our hedging strategies may not be successful in

mitigating our exposure to these fluctuations. See “Item 7A.

Quantitative and Qualitative Disclosures About Market Risk.”

|

Item

1B.

|

UNRESOLVED

STAFF COMMENTS

|

The

Company has no unresolved staff comments.

|

Item

2.

|

PROPERTIES

|

|

The

Company owns or leases the following processing plants and procurement

facilities:

|

|

Processing

Plants

|

Procurement

Facilities

|

|||||||||||||||||||||||

|

United

|

International

|

Total

|

United

|

International

|

Total

|

|||||||||||||||||||

|

States

|

States

|

|||||||||||||||||||||||

|

Owned

|

131 | 97 | 228 | 176 | 104 | 280 | ||||||||||||||||||

|

Leased

|

2 | 2 | 4 | 19 | 29 | 48 | ||||||||||||||||||

| 133 | 99 | 232 | 195 | 133 | 328 | |||||||||||||||||||

|

The

Company’s operations are such that most products are efficiently processed

near the source of raw materials. Consequently, the Company has

many plants strategically located in agricultural commodity producing

areas. The annual volume of commodities processed will vary

depending upon availability of raw materials and demand for finished

products.

To

enhance the efficiency of transporting large quantities of raw materials

and finished products between the Company’s procurement facilities and

processing plants and also the final delivery of products to our customers

around the world, the Company owns or leases over 2,200 barges, 23,700

rail cars, 800 trucks, and 2,100

trailers.

|

|

Oilseeds

Processing

|

|

Processing

Plants

|

Procurement

Facilities

|

|||||||||||||||||||||||

|

United

States

|

International

|

Total

|

United

States

|

International

|

Total

|

|||||||||||||||||||

|

Owned

|

53 | 56 | 109 | 15 | 80 | 95 | ||||||||||||||||||

|

Leased

|

– | – | – | – | 20 | 20 | ||||||||||||||||||

| 53 | 56 | 109 | 15 | 100 | 115 | |||||||||||||||||||

|

The

Company operates twenty-three domestic and eighteen international oilseed

crushing plants with a daily processing capacity of approximately 91,000

metric tons (3.4 million bushels). The domestic plants are

located in Georgia, Illinois, Indiana, Iowa, Kansas, Minnesota, Missouri,

Nebraska, North Dakota, Ohio, South Carolina, Tennessee, and

Texas. The international plants are located in Bolivia, Brazil,

Canada, England, Germany, India, Mexico, the Netherlands, Poland, and

Ukraine.

The

Company operates thirteen domestic oilseed refineries in Georgia,

Illinois, Indiana, Iowa, Minnesota, Missouri, Nebraska, North Dakota, and

Tennessee, as well as seventeen international refineries in Bolivia,

Brazil, Canada, England, Germany, India, the Netherlands, and

Poland. The Company packages oils at five domestic plants

located in California, Georgia, and Illinois, as well as at seven

international plants located in Bolivia, Brazil, England, Poland and

Germany. The Company operates one domestic and six

international biodiesel plants located in North Dakota, Brazil, Germany,

and India. In addition, the Company operates two fertilizer

blending plants in Brazil.

The

Oilseeds Processing segment operates fifteen domestic country grain

elevators as adjuncts to its processing plants. These

elevators, with an aggregate storage capacity of eight million bushels,

are located in Illinois, Missouri, North Carolina, and Ohio.

This

segment also operates one hundred international elevators, including port

facilities, in Bolivia, Brazil, Canada, Germany, the Netherlands,

Paraguay, and Poland as adjuncts to its processing

plants. These facilities have a storage capacity of 125 million

bushels.

|

The

Company operates two soy protein specialty plants in Illinois and one plant in

the Netherlands. Lecithin products are produced at six domestic and

four international plants in Illinois, Iowa, Nebraska, Canada, Germany, and

the Netherlands. The Company produces soy-based foods at a plant in

North Dakota and vitamin E, sterols, and isoflavones at plants in

Illinois. The Company also operates a specialty oils and

fats plant in France that produces various value-added products for the

pharmaceutical, cosmetic and food industries.

|

Item

2.

|

PROPERTIES

(Continued)

|

|

Corn

Processing

|

|

Processing

Plants

|

Procurement

Facilities

|

|||||||||||||||||||||||

|

United

States

|

International

|

Total

|

United

States

|

International

|

Total

|

|||||||||||||||||||

|

Owned

|

13 | – | 13 | 5 | – | 5 | ||||||||||||||||||

|

The

Company operates five wet corn milling plants and two dry corn milling

plants with a daily grind capacity of approximately 50,000 metric tons

(2.0 million bushels). The Company also operates corn germ extraction

plants, sweeteners and starches production facilities, and bioproducts

production facilities in Illinois, Iowa, Minnesota, Nebraska, North

Carolina, and North Dakota. The Corn Processing segment also

operates five domestic grain terminal elevators as adjuncts to its

processing plants. These elevators, with an aggregate storage

capacity of 13 million bushels, are located in Minnesota.

|

|

Agricultural

Services

|

|

Processing

Plants

|

Procurement

Facilities

|

|||||||||||||||||||||||

|

United

States

|

International

|

Total

|

United

States

|

International

|

Total

|

|||||||||||||||||||

|

Owned

|

29 | 6 | 35 | 156 | 18 | 174 | ||||||||||||||||||

|

Leased

|

2 | 1 | 3 | 19 | 7 | 26 | ||||||||||||||||||

| 31 | 7 | 38 | 175 | 25 | 200 | |||||||||||||||||||

|

The

Company operates one hundred fifty-two domestic terminal, sub-terminal,

country, and river elevators covering the major grain producing states,

including sixty-four country elevators, eighty sub-terminal, terminal and

river loading facilities, and eight grain export elevators in Florida,

Louisiana, Ohio, and Texas. Elevators are located in Arkansas,

Illinois, Indiana, Iowa, Kansas, Kentucky, Michigan, Minnesota, Missouri,

Montana, Nebraska, North Dakota, Ohio, Oklahoma, Tennessee, and

Texas. These elevators have an aggregate storage capacity of

approximately 356 million bushels. The Company has five grain

export elevators in Argentina, Mexico, and Ukraine that have an aggregate

storage capacity of approximately 29 million bushels. The

Company has thirteen country elevators located in the Dominican Republic,

Romania, and Ukraine. In addition, the Company has seven

river elevators located in Romania and Ukraine.

The

Company operates twenty-three domestic edible bean procurement facilities

with an aggregate storage capacity of approximately 11 million bushels,

located in Colorado, Idaho, Michigan, Minnesota, North Dakota, and

Wyoming.

The

Company operates a rice mill located in California, an animal feed

facility in Illinois, and an edible bean plant in North

Dakota. The Company also operates twenty-eight domestic and

seven international formula feed and animal health and nutrition

plants. The domestic plants are located in Georgia, Illinois,

Indiana, Iowa, Kansas, Kentucky, Michigan, Minnesota, Missouri, Nebraska,

Ohio, Pennsylvania, Texas, Washington, and Wisconsin. The

foreign plants are located in Canada, China, Puerto Rico, and Trinidad

& Tobago.

|

|

Item

2.

|

PROPERTIES

(Continued)

|

Other

|

Processing

Plants

|

Procurement

Facilities

|

|||||||||||||||||||||||

|

United

States

|

International

|

Total

|

United

States

|

International

|

Total

|

|||||||||||||||||||

|

Owned

|

36

|

35

|

71

|

–

|

6

|

6

|

||||||||||||||||||

|

Leased

|

–

|

1

|

1

|

–

|

2

|

2

|

||||||||||||||||||

|

36

|

36

|

72

|

–

|

8

|

8

|

|||||||||||||||||||

The

Company operates twenty-three domestic wheat flour mills, a domestic bulgur

plant, two domestic corn flour mills, two domestic milo mills, and twenty

international flour mills with a total daily milling capacity of approximately

27,000 metric tons (1.0 million bushels). The Company also operates

six bakery mix plants. These plants and related properties are

located in California, Illinois, Indiana, Kansas, Minnesota, Missouri, Nebraska,

New York, North Carolina, Oklahoma, Pennsylvania, Tennessee, Texas, Washington,

Barbados, Belize, Canada, England, Grenada, and Jamaica. The Company

operates two formula feed plants as adjuncts to the wheat flour mills in Belize

and Grenada, a rice milling plant in Jamaica, and a starch and gluten

plant in Iowa and one in Canada. The Company also operates a honey

drying operation in Wisconsin.

The

Company operates three domestic and nine international chocolate and cocoa bean

processing plants with a total daily grind capacity of approximately 2,200

metric tons. The domestic plants are located in Massachusetts, New

Jersey, and Wisconsin, and the international plants are located in Brazil,

Canada, England, Ivory Coast, the Netherlands, and Singapore. The

Company operates eight cocoa bean procurement and handling facilities/port sites

in Brazil, Indonesia, Ivory Coast, and Malaysia.

|

Item

3.

|

LEGAL

PROCEEDINGS

|

Environmental

Matters

The

United States Environmental Protection Agency and the Missouri Department of

Natural Resources have initiated a criminal investigation of the wastewater

discharge practices at one of the Company’s barge facilities in

Missouri. Since February 2008, several employees at the facility have

received grand jury subpoenas relating to wastewater discharges from the

facility. The Company has been cooperating with the

investigation. The Company has also undertaken an internal

investigation of those discharge practices and does not believe that the filing

of any criminal action would be appropriate. The Company does not yet have

enough information to reasonably estimate any penalty that may be imposed if any

enforcement action is brought.

The

Company is involved in approximately twenty administrative and judicial

proceedings in which it has been identified as a potentially responsible party

(PRP) under the federal Superfund law and its state analogs for the study and

cleanup of sites contaminated by material discharged into the

environment. In all of these matters there are numerous

PRPs. Due to various factors, such as the required level of

remediation and participation in the cleanup effort by others, the Company’s

future cleanup costs at these sites cannot be reasonably estimated.

In

management’s opinion, these proceedings will not, either individually or in the

aggregate, have a material adverse affect on the Company’s financial condition

or results of operations.

|

Item

4.

|

SUBMISSION

OF MATTERS TO A VOTE OF SECURITY

HOLDERS

|

None.

PART

II

|

Item

5.

|

MARKET

FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS, AND ISSUER

PURCHASES OF EQUITY SECURITIES

|

Common

Stock Market Prices and Dividends

The

Company’s common stock is listed and traded on the New York Stock Exchange and

the Frankfurt Stock Exchange. The following table sets forth, for the periods

indicated, the high and low market prices of the common stock as reported on the

New York Stock Exchange and common stock cash dividends declared per

share.

|

Cash

|

||||||||||||

|

Market

Price

|

Dividends

|

|||||||||||

|

High

|

Low

|

Per

Share

|

||||||||||

|

Fiscal

2008-Quarter Ended

|

||||||||||||

|

June

30

|

$ | 48.95 | $ | 31.65 | $ | 0.130 | ||||||

|

March

31

|

47.18 | 38.11 | 0.130 | |||||||||

|

December

31

|

47.33 | 32.43 | 0.115 | |||||||||

|

September

30

|

37.02 | 31.28 | 0.115 | |||||||||

|

Fiscal

2007-Quarter Ended

|

||||||||||||

|

June

30

|

$ | 39.65 | $ | 32.05 | $ | 0.115 | ||||||

|

March

31

|

37.84 | 30.20 | 0.115 | |||||||||

|

December

31

|

40.00 | 31.20 | 0.100 | |||||||||

|

September

30

|

45.05 | 36.44 | 0.100 | |||||||||

The

number of registered shareholders of the Company’s common stock at June 30,

2008, was 17,330. The Company expects to continue its policy of

paying regular cash dividends, although there is no assurance as to future

dividends because they are dependent on future earnings, capital requirements,

and financial condition.

|

Item

5.

|

MARKET

FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS, AND ISSUER

PURCHASES OF EQUITY SECURITIES

(Continued)

|

Issuer

Purchases of Equity Securities

|

Total

Number of

|

Number

of Shares

|

|||||||||||||||

|

Total

Number

|

Average

|

Shares

Purchased as

|

Remaining

to be

|

|||||||||||||

|

of

Shares

|

Price

Paid

|

Part

of Publicly

|

Purchased

Under the

|

|||||||||||||

|

Period

|

Purchased

(1)

|

per

Share

|

Announced

Program (2)

|

Program (2)

|

||||||||||||

|

April

1, 2008 to

April

30, 2008

|

1,799 | $ | 47.13 | 307 | 75,630,561 | |||||||||||

|

May

1, 2008 to

May

31, 2008

|

9,061 | 43.99 | 154 | 75,630,407 | ||||||||||||

|

June

1, 2008 to

June

30, 2008

|

118 | 41.80 | 118 | 75,630,289 | ||||||||||||

|

Total

|

10,978 | $ | 44.48 | 579 | 75,630,289 | |||||||||||

|

(1) Total

shares purchased represents those shares purchased as part of the

Company’s publicly announced share repurchase program described below and

shares received as payment of the exercise price for stock option

exercises. During the three-month period ended June 30, 2008,

the Company received 10,399 shares as payment of the exercise price for

stock option exercises.

(2) On

November 4, 2004, the Company’s Board of Directors approved a stock

repurchase program authorizing the Company to repurchase up to 100,000,000

shares of the Company’s common stock during the period commencing January

1, 2005 and ending December 31,

2009.

|

|

Item

5.

|

MARKET

FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS, AND ISSUER

PURCHASES OF EQUITY SECURITIES

(Continued)

|

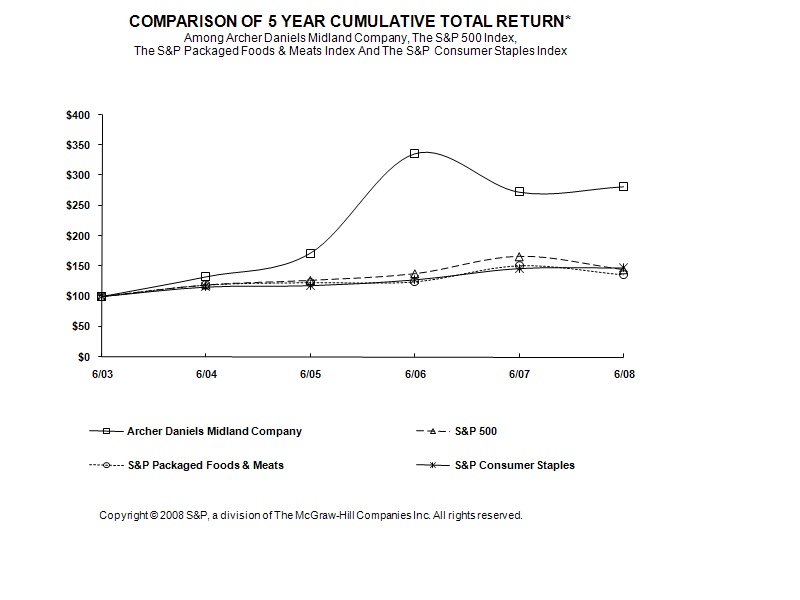

Performance

Graph

The graph

below compares five-year returns of the Company’s common stock with those of the

S&P 500 Index, the S&P Packaged Foods and Meats Index, and the S&P

Consumer Staples Index which the Company today considers a more relevant

line-of-business index. The graph assumes all dividends have been

reinvested and assumes an initial investment of $100 on June 30,

2003. Information in the graph is presented on a June 30 fiscal year

basis.

Graph

produced by Research Data Group, Inc.

|

Item

6.

|

SELECTED

FINANCIAL DATA

|

Selected

Financial Data

(In

millions, except ratio and per share data)

|

2008

|

2007

|

2006

|

2005

|

2004

|

||||||||||||||||

|

Net

sales and other operating income

|

$ | 69,816 | $ | 44,018 | $ | 36,596 | $ | 35,943 | $ | 36,151 | ||||||||||

|

Depreciation

|

721 | 701 | 657 | 665 | 686 | |||||||||||||||

|

Net

earnings

|

1,802 | 2,162 | 1,312 | 1,044 | 495 | |||||||||||||||

|

Basic

earnings per common share

|

2.80 | 3.32 | 2.01 | 1.60 | 0.76 | |||||||||||||||

|

Diluted

earnings per common share

|

2.79 | 3.30 | 2.00 | 1.59 | 0.76 | |||||||||||||||

|

Cash

dividends

|

316 | 281 | 242 | 209 | 174 | |||||||||||||||

|

Per

common share

|

0.49 | 0.43 | 0.37 | 0.32 | 0.27 | |||||||||||||||

|

Working

capital

|

$ | 10,834 | $ | 7,254 | $ | 5,661 | $ | 4,344 | $ | 3,589 | ||||||||||

|

Current

ratio

|

1.7 | 1.9 | 1.9 | 1.8 | 1.5 | |||||||||||||||

|

Inventories

|

10,160 | 6,060 | 4,677 | 3,907 | 4,592 | |||||||||||||||

|

Net

property, plant, and equipment

|

7,125 | 6,010 | 5,293 | 5,184 | 5,255 | |||||||||||||||

|

Gross

additions to property, plant, and

equipment

|

1,789 | 1,404 | 841 | 647 | 621 | |||||||||||||||

|

Total

assets

|

37,056 | 25,118 | 21,269 | 18,598 | 19,369 | |||||||||||||||

|

Long-term

debt

|

7,690 | 4,752 | 4,050 | 3,530 | 3,740 | |||||||||||||||

|

Shareholders’

equity

|

13,490 | 11,253 | 9,807 | 8,435 | 7,698 | |||||||||||||||

|

Per

common share

|

20.95 | 17.50 | 14.95 | 12.96 | 11.83 | |||||||||||||||

|

Weighted

average shares

outstanding-basic

|

644 | 651 | 654 | 654 | 648 | |||||||||||||||

|

Weighted

average shares

outstanding-diluted

|

646 | 656 | 656 | 656 | 650 | |||||||||||||||

Significant

items affecting the comparability of the financial data shown above are as

follows.

|

·

|

Net

earnings for 2007 include a gain of $440 million ($286 million after tax,

equal to $0.44 per share) related to the exchange of the Company’s

interests in certain Asian joint ventures for shares of Wilmar

International Limited, realized securities gains of $357 million ($225

million after tax, equal to $0.34 per share) related to the Company’s sale

of equity securities of Tyson Foods Inc. and Overseas Shipholding Group

Inc. and a $209 million gain ($132 million after tax, equal to $0.20 per

share) related to the sale of

businesses.

|

|

·

|

Net

earnings for 2005 include a gain of $159 million ($119 million after tax,

equal to $0.18 per share) related to the sale of the Company’s interest in

Tate & Lyle PLC.

|

|

·

|

Net

earnings for 2004 include a $400 million charge ($252 million after tax,

equal to $0.39 per share) related to the settlement of fructose

litigation.

|

|

Item

7.

|

MANAGEMENT’S

DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF

OPERATIONS

|

Company

Overview

The

Company is principally engaged in procuring, transporting, storing, processing,

and merchandising agricultural commodities and products. Beginning in

fiscal 2008, the Company has reclassified

certain operations within its reportable segments

to reflect how the Company now manages its businesses following a realignment of

the organizational structure of the Company and to reflect the activities of the Company

as viewed by the Company’s chief operating decision maker. Prior period

segment information has been reclassified to conform to the new

presentation. The

Company’s operations are classified into three reportable business segments:

Oilseeds Processing, Corn Processing and Agricultural Services. Each

of these segments is organized based upon the nature of products and services

offered. The Company’s remaining operations are aggregated and

classified as Other.

The

Oilseeds Processing segment includes activities related to the origination and

crushing of oilseeds such as soybeans, cottonseed, sunflower seeds, canola,

peanuts, and flaxseed into vegetable oils and protein meals principally for the

food and feed industries. In addition, oilseeds and oilseed products

may be processed internally or resold into the marketplace as raw materials for

other processing. Crude vegetable oil is sold "as is" or is further

processed by refining, bleaching, and deodorizing into salad

oils. Salad oils can be further processed by hydrogenating and/or

interesterifying into margarine, shortening, and other food products. Partially

refined oil is sold for use in chemicals, paints, and other industrial

products. Refined oil can be further processed for use in the

production of biodiesel. Oilseed protein meals are primary

ingredients used in the manufacture of commercial livestock and poultry

feeds. Oilseeds Processing includes activities related to the

production of natural health and nutrition products and the production of other

specialty food and feed ingredients. This segment also includes

activities related to the Company’s interests in unconsolidated affiliates in

Asia, principally Wilmar International Limited.

The Corn

Processing segment includes activities related to the production of sweeteners,

starches, dextrose, and syrups primarily for the food and beverage industry as

well as activities related to the production, by fermentation, of bioproducts

such as ethanol, amino acids, and other food, feed and industrial

products.

The

Agricultural Services segment utilizes the Company’s extensive grain elevator

and transportation network to buy, store, clean, and transport agricultural

commodities, such as oilseeds, corn, wheat, milo, oats, barley, and edible

beans, and resells or processes these commodities primarily as food and feed

ingredients for the agricultural processing industry. Agricultural

Services’ grain sourcing and transportation network provides reliable and

efficient services to the Company’s agricultural processing operations. Also

included in Agricultural Services are the activities of A.C. Toepfer

International, a global merchant of agricultural commodities and processed

products.

Other

includes the Company’s remaining processing operations, consisting of activities

related to processing agricultural commodities into food ingredient products

such as wheat into wheat flour, cocoa into chocolate and cocoa products, and

barley into malt. Other also includes financial activities related to banking,

captive insurance, private equity fund investments, and futures commission

merchant activities.

Operating

Performance Indicators

The

Company’s Oilseeds Processing, Agricultural Services, and wheat processing

operations are principally agricultural commodity-based businesses where changes

in selling prices move in relationship to changes in prices of the

commodity-based agricultural raw materials. Therefore, changes in

agricultural commodity prices have relatively equal impacts on both net sales

and cost of products sold and minimal impact on the gross profit of underlying

transactions. As a result, changes in gross profit of these businesses

do not necessarily correspond to the changes in net sales amounts.

|

Item

7.

|

MANAGEMENT’S

DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

(Continued)

|

The

Company’s Corn Processing operations and certain other food and animal feed

processing operations also utilize agricultural commodities (or products derived

from agricultural commodities) as raw materials. In these operations,

agricultural commodity market price changes can result in significant

fluctuations in cost of products sold, and such price changes cannot necessarily

be passed directly through to the selling price of the finished

products.

The

Company conducts its business in many countries. For the majority of

the Company’s subsidiaries located outside the United States, the local currency

is the functional currency. Revenues and expenses denominated in

foreign currencies are translated into U.S. dollars at the weighted average

exchange rates for the applicable periods. Fluctuations in the

exchange rates of foreign currencies, primarily the Euro, British pound, and

Canadian dollar, as compared to the U.S. dollar will result in corresponding

fluctuations in the U.S. dollar value of revenues and expenses reported by the

Company. The impact of these currency exchange rate changes, where

significant, is discussed below.

The

Company measures the performance of its business segments using key operating

statistics such as segment operating profit, return on fixed capital investment,

return on equity, return on net assets, and cost per metric ton

produced. The Company’s operating results can vary significantly due

to changes in unpredictable factors such as fluctuations in energy prices,

weather conditions, crop plantings, government programs and policies,

changes in global demand resulting from population growth and changes in

standards of living, and global production of similar and competitive

crops. Due to these unpredictable factors, the Company does not

provide forward-looking information in “Management’s Discussion and Analysis of

Financial Condition and Results of Operations.”

2008

Compared to 2007

As an

agricultural-based commodity business, the Company is subject to a variety of

market factors which affect the Company’s operating

results. Strong demand for agricultural commodities and

processed products has challenged the global supply chain and provided

exceptional margin opportunities in 2008. Strong global demand for

protein meal and vegetable oil and strong fertilizer demand in South America

positively impacted Oilseeds Processing results. The market price of

corn rose due to increased demand, resulting in higher raw material costs for

Corn Processing which were only partially passed on in the form of increased

selling prices for sweeteners and starches. Average ethanol selling

prices decreased due to additional supply entering the market. Large

North American crops combined with global wheat shortages created favorable

conditions in agricultural merchandising and handling

operations. Increased commodity costs resulted in larger LIFO

inventory valuation reserves.

Earnings

before income taxes decreased due principally to gains totaling $1.0 billion

before income tax on business disposals recorded in 2007 including $440 million

related to the exchange of the Company’s interest in certain Asian joint

ventures for shares of Wilmar International Limited (the Wilmar gain), a $357

million realized securities gain from sales of the Company’s equity securities

of Tyson Foods, Inc. and Overseas Shipholding Group, Inc., a gain of $153

million from the sale of the Company’s interest in Agricore United, and a $53

million gain from the sale of the Company’s Arkady food ingredient

business.

Earnings

before income taxes for 2008 include a charge of $569 million from the effect of

changing commodity prices on LIFO inventory valuations, compared to a charge of

$207 million in 2007. Earnings before income taxes for 2008 also include a $32

million charge related to abandonment and write-down of long-lived assets, a $38

million gain on sales of securities, and a $21 million gain on the disposal of

long-lived assets. Earnings before income taxes for 2007 include

charges of $46 million related to the repurchase of $400 million of the

Company’s outstanding debentures and $21 million related to abandonment and

write-down of long-lived assets.

|

Item

7.

|

MANAGEMENT’S

DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

(Continued)

|

Analysis

of Statements of Earnings

Net sales

and other operating income increased 59% to $69.8

billion. Increased selling prices of agricultural commodities

and oilseed processing products and, to a lesser extent, corn processing

products and wheat flour accounted for 85% of the increase and higher sales

volumes, principally of agricultural commodities, ethanol, and biodiesel, also

contributed to the increase in net sales. In addition, net sales and

other operating income increased $1.83 billion, or 4%, due to currency rate

fluctuations.

Net sales

and other operating income by segment are as follows:

|

2008

|

2007

|

Change | ||||||||||

|

(In

millions)

|

||||||||||||

|

Oilseeds

Processing

|

||||||||||||

|

Crushing

& Origination

|

$ | 14,477 | $ | 8,036 | $ | 6,441 | ||||||

|

Refining,

Packaging, Biodiesel & Other

|

8,588 | 5,758 | 2,830 | |||||||||

|

Asia

|

214 | 149 | 65 | |||||||||

|

Total

Oilseeds Processing

|

23,279 | 13,943 | 9,336 | |||||||||

|

Corn

Processing

|

||||||||||||

|

Sweeteners

& Starches

|

3,546 | 2,761 | 785 | |||||||||

|

Bioproducts

|

3,591 | 3,064 | 527 | |||||||||

|

Total

Corn Processing

|

7,137 | 5,825 | 1,312 | |||||||||

|

Agricultural

Services

|

||||||||||||

|

Merchandising

& Handling

|

33,749 | 20,222 | 13,527 | |||||||||

|

Transportation

|

219 | 197 | 22 | |||||||||

|

Total

Agricultural Services

|

33,968 | 20,419 | 13,549 | |||||||||

|

Other

|

||||||||||||

|

Wheat,

Cocoa, & Malt

|

5,335 | 3,738 | 1,597 | |||||||||

|

Financial

|

97 | 93 | 4 | |||||||||

|

Total

Other

|

5,432 | 3,831 | 1,601 | |||||||||

|

Total

|

$ | 69,816 | $ | 44,018 | $ | 25,798 | ||||||

Oilseeds

Processing sales increased 67% to $23.3 billion due principally to increased

average selling prices resulting primarily from increases in underlying

commodity costs and from continuing strong demand for vegetable oil, biodiesel

and protein meal. Sales volumes of vegetable oil, protein meal and

biodiesel also increased. Corn Processing sales increased 23% to $7.1

billion. Good demand for sweeteners and starches resulted in higher

average selling prices. Bioproducts sales increased primarily as a