UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

| FORM | |||||

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the fiscal year ended May 31 , 2021

OR

| TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the transition period from to

Commission File Number: 1-7102

__________________________

(Exact name of registrant as specified in its charter)

__________________________

| (State or other jurisdiction of incorporation or organization) | (I.R.S. employer identification no.) | |||||||

| (Address of principal executive offices) (Zip Code) | |||||||||||

Registrant’s telephone number, including area code: (703) 467-1800

__________________________

Securities registered pursuant to Section 12(b) of the Act:

| Title of Each Class | Trading Symbol(s) | Name of Each Exchange on Which Registered | ||||||

| | ||||||||

Securities Registered Pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes x No ¨

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes x No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer ¨ Accelerated filer ¨ Non-accelerated filer x Smaller reporting company ¨ Emerging growth company ¨

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transaction period for complying with any new or revised financial accounting standards provided pursuant to Section13(a) of the Exchange Act. ¨

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C.7262(b)) by the registered public accounting firm that prepared or issued its audit report. ¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

The Registrant is a tax-exempt cooperative and therefore does not issue capital stock.

TABLE OF CONTENTS

| Page | ||||||||||||||

i

| Page | ||||||||||||||

ii

CROSS REFERENCE INDEX OF MD&A TABLES

| Table | Description | Page | ||||||||||||

| 1 | Summary of Selected Financial Data | 23 | ||||||||||||

| 2 | Average Balances, Interest Income/Interest Expense and Average Yield/Cost | 35 | ||||||||||||

| 3 | Rate/Volume Analysis of Changes in Interest Income/Interest Expense | 37 | ||||||||||||

| 4 | Non-Interest Income | 39 | ||||||||||||

| 5 | Derivative Gains (Losses) | 40 | ||||||||||||

| 6 | Derivatives—Average Notional Amounts and Interest Rates | 41 | ||||||||||||

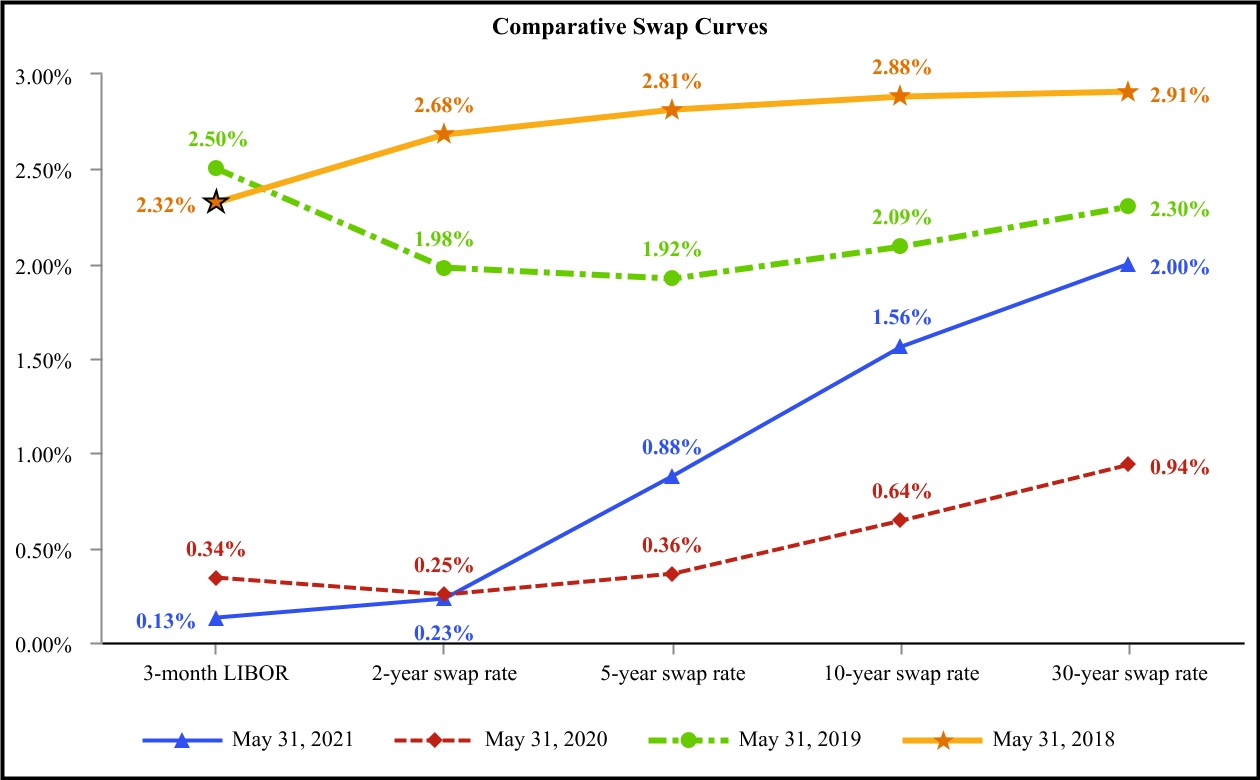

| 7 | Comparative Swap Curves | 41 | ||||||||||||

| 8 | Non-Interest Expense | 42 | ||||||||||||

| 9 | Loans—Outstanding Amount by Member Class and Loan Type | 43 | ||||||||||||

| 10 | Loans—Historical Retention Rate and Repricing Selection | 44 | ||||||||||||

| 11 | Debt—Debt Product Types | 45 | ||||||||||||

| 12 | Total Debt Outstanding and Weighted-Average Interest Rates | 46 | ||||||||||||

| 13 | Member Investments | 47 | ||||||||||||

| 14 | Equity | 48 | ||||||||||||

| 15 | Loan Portfolio Security Profile | 52 | ||||||||||||

| 16 | Loan Geographic Concentration | 54 | ||||||||||||

| 17 | Loan Exposure to 20 Largest Borrowers | 55 | ||||||||||||

| 18 | Troubled Debt Restructured Loans | 56 | ||||||||||||

| 19 | Nonperforming Loans | 56 | ||||||||||||

| 20 | Allowance for Credit Losses by Borrower Member Class and Evaluation Methodology | 59 | ||||||||||||

| 21 | Rating Triggers for Derivatives | 61 | ||||||||||||

| 22 | Available Liquidity | 62 | ||||||||||||

| 23 | Committed Bank Revolving Line of Credit Agreements | 64 | ||||||||||||

| 24 | Short-Term Borrowings—Outstanding Amount and Weighted-Average Interest Rates | 66 | ||||||||||||

| 25 | Short-Term Borrowings—Funding Sources | 66 | ||||||||||||

| 26 | Long-Term and Subordinated Debt Issuances and Repayments | 67 | ||||||||||||

| 27 | Collateral Pledged | 68 | ||||||||||||

| 28 | Unencumbered Loans | 68 | ||||||||||||

| 29 | Loans—Maturities of Scheduled Principal Payments | 69 | ||||||||||||

| 30 | Contractual Obligations | 70 | ||||||||||||

| 31 | Projected Sources and Uses of Liquidity from Debt and Investment Activity | 71 | ||||||||||||

| 32 | Credit Ratings | 72 | ||||||||||||

| 33 | Interest Rate Sensitivity Analysis | 74 | ||||||||||||

| 34 | LIBOR-Indexed Financial Instruments | 75 | ||||||||||||

| 35 | Selected Quarterly Financial Data | 77 | ||||||||||||

| 36 | Adjusted Financial Measures—Income Statement | 79 | ||||||||||||

| 37 | TIER and Adjusted TIER | 80 | ||||||||||||

| 38 | Adjusted Financial Measures—Balance Sheet | 81 | ||||||||||||

| 39 | Debt-to-Equity Ratio and Adjusted Debt-to-Equity Ratio | 82 | ||||||||||||

| 40 | Members’ Equity | 82 | ||||||||||||

iii

FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K for the fiscal year ended May 31, 2021 (“this Report” or “2021 Form 10-K”) contains certain statements that are considered “forward-looking statements” as defined in and within the meaning of the safe-harbor provisions of the Private Securities Litigation Reform Act of 1995. Forward-looking statements do not represent historical facts or statements of current conditions. Instead, forward-looking statements represent management’s current beliefs and expectations, based on certain assumptions and estimates made by, and information available to, management at the time the statements are made, regarding our future plans, strategies, operations, financial results or other events and developments, many of which, by their nature, are inherently uncertain and outside our control. Forward-looking statements are generally identified by the use of words such as “intend,” “plan,” “may,” “should,” “will,” “project,” “estimate,” “anticipate,” “believe,” “expect,” “continue,” “potential,” “opportunity” and similar expressions, whether in the negative or affirmative. All statements about future expectations or projections, including statements about loan volume, the adequacy of the allowance for credit losses, operating income and expenses, leverage and debt-to-equity ratios, borrower financial performance, impaired loans, and sources and uses of liquidity, are forward-looking statements. Although we believe the expectations reflected in our forward-looking statements are based on reasonable assumptions, actual results and performance may differ materially from our forward-looking statements. Therefore, you should not place undue reliance on any forward-looking statement and should consider the risks and uncertainties that could cause our current expectations to vary from our forward-looking statements, including, but not limited to, legislative changes that could affect our tax status and other matters, demand for our loan products, lending competition, changes in the quality or composition of our loan portfolio, changes in our ability to access external financing, changes in the credit ratings on our debt, valuation of collateral supporting impaired loans, charges associated with our operation or disposition of foreclosed assets, nonperformance of counterparties to our derivative agreements, economic conditions and regulatory or technological changes within the rural electric industry, the costs and impact of legal or governmental proceedings involving us or our members, general economic conditions, governmental monetary and fiscal policies, the occurrence and effect of natural disasters, including severe weather events or public health emergencies, such as the emergence in 2019 and spread of a novel coronavirus that causes coronavirus disease 2019 (“COVID-19”) and the factors listed and described under “Item 1A. Risk Factors” in this Report. Forward-looking statements speak only as of the date they are made, and, except as required by law, we undertake no obligation to update any forward-looking statement to reflect the impact of events, circumstances or changes in expectations that arise after the date any forward-looking statement is made.

PART I

Item 1. Business

| OVERVIEW | ||

Our financial statements include the consolidated accounts of National Rural Utilities Cooperative Finance Corporation (“CFC”), National Cooperative Services Corporation (“NCSC”), Rural Telephone Finance Cooperative (“RTFC”) and subsidiaries created and controlled by CFC to hold foreclosed assets resulting from defaulted loans or bankruptcy. CFC and its consolidated entities have not held any foreclosed assets since the fiscal year ended May 31, 2017. Our principal operations are currently organized for management reporting purposes into three business segments, which are based on the accounts of each of the legal entities included in our consolidated financial statements and discussed below.

The business affairs of CFC, NCSC and RTFC are governed by separate boards of directors for each entity. We provide information on CFC’s corporate governance in “Item 10. Directors, Executive Officers and Corporate Governance.” We provide information on the members of each of these entities below in “Item 1. Business—Members” and describe the financing products offered to members by each entity under “Item 1. Business—Loan and Guarantee Programs.” Information on the financial performance of our business segments is disclosed in “Note 16—Business Segments.” Unless stated otherwise, references to “we,” “our” or “us” relate to CFC and its consolidated entities. All references to members within this document include members, associates and affiliates of CFC and its consolidated entities, except where indicated otherwise.

1

CFC

CFC is a member-owned, nonprofit finance cooperative association incorporated under the laws of the District of Columbia in April 1969. CFC’s principal purpose is to provide its members with financing to supplement the loan programs of the Rural Utilities Service (“RUS”) of the United States Department of Agriculture (“USDA”). CFC extends loans to its rural electric members for construction, acquisitions, system and facility repairs and maintenance, enhancements and ongoing operations to support the goal of electric distribution and generation and transmission (“power supply”) systems of providing reliable, affordable power to the customers they service. CFC also provides its members with credit enhancements in the form of letters of credit and guarantees of debt obligations. As a cooperative, CFC is owned by and exclusively serves its membership, which consists of not-for-profit entities or subsidiaries or affiliates of not-for-profit entities. CFC is exempt from federal income taxes under Section 501(c)(4) of the Internal Revenue Code. As a member-owned cooperative, CFC’s objective is not to maximize profit, but rather to offer members cost-based financial products and services. As described below under “Allocation and Retirement of Patronage Capital,” CFC annually allocates its net earnings, which consist of net income excluding the effect of certain noncash accounting entries, to: (i) a cooperative educational fund; (ii) a general reserve, if necessary; (iii) members based on each member’s patronage of CFC’s loan programs during the year; and (iv) a members’ capital reserve. CFC funds its activities primarily through a combination of public and private issuances of debt securities, member investments and retained equity. As a Section 501(c)(4) tax-exempt, member-owned cooperative, CFC cannot issue equity securities.

NCSC

NCSC is a taxable cooperative incorporated in 1981 in the District of Columbia as a member-owned cooperative association. The principal purpose of NCSC is to provide financing to its members, entities eligible to be members of CFC and the for-profit and not-for-profit entities that are owned, operated or controlled by, or provide significant benefit to Class A, B and C members of CFC. See “Members” below for a description of our member classes. NCSC’s membership consists of distribution systems, power supply systems and statewide and regional associations that were members of CFC as of May 31, 2021. CFC, which is the primary source of funding for NCSC, manages NCSC’s business operations under a management agreement that is automatically renewable on an annual basis unless terminated by either party. NCSC pays CFC a fee and, in exchange, CFC reimburses NCSC for loan losses under a guarantee agreement. As a taxable cooperative, NCSC pays income tax based on its reported taxable income and deductions. NCSC is headquartered with CFC in Dulles, Virginia.

RTFC

RTFC is a taxable Subchapter T cooperative association originally incorporated in South Dakota in 1987 and reincorporated as a member-owned cooperative association in the District of Columbia in 2005. RTFC’s principal purpose is to provide financing for its rural telecommunications members and their affiliates. RTFC’s membership consists of a combination of not-for-profit and for-profit entities. CFC is the sole lender to and manages RTFC’s business operations through a management agreement that is automatically renewable on an annual basis unless terminated by either party. RTFC pays CFC a fee and, in exchange, CFC reimburses RTFC for loan losses under a guarantee agreement. As permitted under Subchapter T of the Internal Revenue Code, RTFC pays income tax based on its taxable income, excluding patronage-sourced earnings allocated to its patrons. RTFC is headquartered with CFC in Dulles, Virginia.

| OUR BUSINESS | ||

CFC was established by and for the rural electric cooperative network to provide affordable financing alternatives to electric cooperatives. While our business strategy and policies are set by CFC’s board of directors and may be amended or revised from time to time, the fundamental goal of our overall business model is to work with our members to ensure that CFC is able to meet their financing needs, as well as provide industry expertise and strategic services to aid them in delivering affordable and reliable essential services to their communities.

2

Focus on Electric Lending

As a member-owned, nonprofit finance cooperative, our primary objective is to provide our members with the credit products they need to fund their operations. As such, we primarily focus on lending to electric systems and securing access to capital through diverse funding sources at rates that allow us to offer cost-based credit products to our members. Rural electric cooperatives, most of which are not-for-profit entities, were established to provide electricity in rural areas historically deemed too costly to be served by investor-owned utilities. As such, our electric cooperative members experience limited competition because they generally operate in exclusive territories, the majority of which are not rate regulated. Loans to electric utility organizations accounted for approximately 99% of our total loans outstanding as of both May 31, 2021 and 2020. Substantially all of our electric cooperative borrowers continued to demonstrate stable operating performance and strong financial ratios as of May 31, 2021.

Maintain Diversified Funding Sources

We strive to maintain diversified funding sources beyond capital market offerings of debt securities. We offer various short- and long-term unsecured investment products to our members and affiliates, including commercial paper, select notes, daily liquidity fund notes, medium-term notes and subordinated certificates. We continue to issue debt securities, such as secured collateral trust bonds, unsecured medium-term notes and dealer commercial paper, in the capital markets. We also have access to funds through bank revolving line of credit arrangements, government-guaranteed programs such as funding from the Federal Financing Bank that is guaranteed by RUS through the Guaranteed Underwriter Program of the USDA (the “Guaranteed Underwriter Program”), as well as private placement note purchase agreements with the Federal Agricultural Mortgage Corporation (“Farmer Mac”). We provide additional information on our funding sources in “Item 7. MD&A—Consolidated Balance Sheet Analysis,” “Item 7. MD&A—Liquidity Risk,” “Note 6—Short-Term Borrowings,” “Note 7—Long-Term Debt,” “Note 8—Subordinated Deferrable Debt” and “Note 9—Members’ Subordinated Certificates.”

| MEMBERS | ||

Our consolidated membership, after taking into consideration entities that are members of both CFC and NCSC and eliminating overlapping members between CFC, NCSC and RTFC, totaled 1,424 members and 246 associates as of May 31, 2021, compared with 1,439 members and 232 associates as of May 31, 2020.

CFC

CFC lends to its members and associates and also provides credit enhancements in the form of guarantees of debt obligations and letters of credit. Membership in CFC is limited to cooperative or not-for-profit rural electric systems that are eligible to borrow from RUS under its Electric Loan Program and affiliates of these entities. CFC categorizes its members, all of which are not-for-profit entities or subsidiaries or affiliates of not-for-profit entities, into classes based on member type because the demands and needs of each member class differs. Affiliates represent holding companies, subsidiaries and other entities that are owned, controlled or operated by members. Members are not required to have outstanding loans from RUS as a condition of borrowing from CFC. CFC membership consists of members in 49 states and three U.S. territories. In addition to members, CFC has associates that are nonprofit groups or entities organized on a cooperative basis that are owned, controlled or operated by members and are engaged in or plan to engage in furnishing non-electric services primarily for the benefit of the ultimate consumers of CFC members. Associates are not eligible to vote on matters put to a vote of the membership. CFC’s members, by member class, and associates were as follows as of May 31, 2021.

3

| CFC Member | ||||||||||||||

| Member Type | Class | May 31, 2021 | ||||||||||||

| Distribution systems | A | 842 | ||||||||||||

| Power supply systems | B | 67 | ||||||||||||

| Statewide and regional associations, including NCSC | C | 62 | ||||||||||||

National association of cooperatives(1) | D | 1 | ||||||||||||

| Total CFC members | 972 | |||||||||||||

| Associates, including RTFC | 46 | |||||||||||||

| Total CFC members and associates | 1,018 | |||||||||||||

____________________________

(1) National Rural Electric Cooperative Association is our sole class D member.

NCSC

Membership in NCSC includes organizations that are Class A, B and C members of CFC, or eligible for such membership and are approved for membership by the NCSC Board of Directors. In addition to members, NCSC has associates that may include members of CFC, entities eligible to be members of CFC and for-profit and not-for-profit entities owned, controlled or operated by, or provide significant benefit to, Class A, B, and C members of CFC. All of NCSC’s members also were CFC members as of May 31, 2021. CFC is not, however, a member of NCSC. NCSC’s members and associates were as follows as of May 31, 2021.

| CFC Member | ||||||||||||||

| Member Type | Class | May 31, 2021 | ||||||||||||

| Distribution systems | A | 447 | ||||||||||||

| Power supply systems | B | 3 | ||||||||||||

| Statewide associations | C | 6 | ||||||||||||

| Total NCSC members | 456 | |||||||||||||

| Associates | 195 | |||||||||||||

| Total NCSC members and associates | 651 | |||||||||||||

RTFC

Membership in RTFC is limited to cooperative corporations, nonprofit corporations, private corporations, public corporations, utility districts and other public bodies that are approved by the RTFC Board of Directors and are actively borrowing or are eligible to borrow from RUS’s traditional infrastructure loan program. These companies must be engaged directly or indirectly in furnishing telephone services as the licensed incumbent carrier. Holding companies, subsidiaries and other organizations that are owned, controlled or operated by members, which are referred to as affiliates, are eligible to borrow from RTFC. Associates are organizations that provide non-telephone or non-telecommunications services to rural telecommunications companies that are approved by the RTFC Board of Directors. Neither affiliates nor associates are eligible to vote on matters put to a vote of the membership. CFC and NCSC are not members of RTFC. RTFC’s members and associates were as follows as of May 31, 2021.

| Member Type | May 31, 2021 | |||||||

| Members | 453 | |||||||

| Associates | 6 | |||||||

| Total RTFC members and associates | 459 | |||||||

4

| LOAN AND GUARANTEE PROGRAMS | ||

CFC lends to its members and associates and also provides credit enhancements in the form of guarantees of debt obligations and letters of credit. NCSC and RTFC also lend and provide credit enhancements to their members and associates. For information on the membership of CFC, NCSC and RTFC, see “Item 1. Business—Members.”

CFC, NCSC and RTFC loan commitments generally contain provisions that restrict further borrower advances or trigger an event of default if there is any material adverse change in the business or condition, financial or otherwise, of the borrower. Below is additional information on the loan and guarantee programs offered by CFC, NCSC and RTFC.

CFC Loan Programs

Long-Term Loans

CFC’s long-term loans generally have the following characteristics:

•terms of up to 35 years on a senior secured basis and terms of up to five years on an unsecured basis;

•amortizing, bullet maturity or serial payment structures;

•the property, plant and equipment financed by and securing the long-term loan has a useful life generally equal to or in excess of the loan maturity;

•flexibility for the borrower to select a fixed interest rate for periods of one to 35 years or a variable interest rate; and

•the ability for the borrower to select various tranches with either a fixed or variable interest rate for each tranche.

Borrowers typically have the option of selecting a fixed or variable interest rate at the time of each advance on long-term loan facilities. When selecting a fixed rate, the borrower has the option to choose a fixed rate for a term of one year through the final maturity of the loan. When the selected fixed interest rate term expires, the borrower may select another fixed rate for a term of one year through the remaining loan maturity or the current variable rate.

To be in compliance with the covenants in the loan agreement and eligible for loan advances, distribution systems generally must maintain an average modified debt service coverage ratio, as defined in the loan agreement, of 1.35 or greater. CFC may make long-term loans to distribution systems, on a case-by-case basis, that do not meet this general criterion. Power supply systems generally are required: (i) to maintain an average modified debt service coverage ratio, as defined in the loan agreement, of 1.00 or greater; (ii) to establish and collect rates and other revenue in an amount to yield margins for interest, as defined in an indenture, in each fiscal year sufficient to equal at least 1.00; or (iii) both. CFC may make long-term loans to power supply systems, on a case-by-case basis, that may include other requirements, such as maintenance of a minimum equity level.

Line of Credit Loans

Line of credit loans are designed primarily to assist borrowers with liquidity and cash management and are generally advanced at variable interest rates. Line of credit loans are typically revolving facilities. Certain line of credit loans require the borrower to pay off the principal balance for at least five consecutive business days at least once during each 12-month period. Line of credit loans are generally unsecured and may be conditional or unconditional facilities.

Line of credit loans can be made on an emergency basis when financing is needed quickly to address weather-related or other unexpected events and can also be made available as interim financing when a member either receives RUS approval to obtain a loan and is awaiting its initial advance of funds or submits a loan application that is pending approval from RUS (sometimes referred to as “bridge loans”). In these cases, when the borrower receives the RUS loan advance, the funds must be used to repay the bridge loans.

Syndicated Line of Credit Loans

A syndicated line of credit loan is typically a large financing offered by a group of lenders that work together to provide funds for a single borrower. Syndicated loans are generally unsecured, floating-rate loans that can be provided on a

5

revolving or term basis for tenors that range from several months to five years. Syndicated financings are arranged for borrowers on a case-by-case basis. CFC may act as lead lender, arranger and/or administrative agent for the syndicated facilities. CFC will syndicate these line of credit facilities on a best effort basis.

NCSC Loan Programs

NCSC makes loans to electric cooperatives and their subsidiaries that provide non-electric services in the energy and telecommunication industries as well as to entities that provide substantial benefit to CFC members, including eligible solar energy providers and investor-owned utilities. Loans to NCSC associates may require a guarantee of repayment to NCSC from the CFC member cooperative with which it is affiliated.

Long-Term Loans

NCSC’s long-term loans generally have the following characteristics:

•terms from 7 to up to 30 years on a senior secured basis and terms of up to five years on an unsecured basis;

•amortizing, balloon, bullet maturity or serial payment structures;

•the property, plant and equipment financed by and securing the long-term loan has a useful life equal to or in excess of the loan maturity;

•flexibility for the borrower to select a fixed interest rate for periods of one to 30 years or a variable interest rate; and

•the ability for the borrower to select various tranches with either a fixed or variable interest rate for each tranche.

NCSC allows borrowers to select a fixed interest rate or a variable interest rate at the time of each advance on long-term loan facilities. When selecting a fixed rate, the borrower has the option to choose a fixed rate for a term of one year through the final maturity of the loan. When the selected fixed interest rate term expires, the borrower may select another fixed rate for a term of one year through the remaining loan maturity or the current variable rate. The fixed rate on a loan generally is determined on the day the loan is advanced or repriced based on the term selected.

Line of Credit Loans

NCSC also provides revolving line of credit loans to assist borrowers with liquidity and cash management on terms similar to those provided by CFC as described herein.

RTFC Loan Programs

RTFC primarily makes long-term loans to rural local exchange carriers or holding companies of rural local exchange carriers for debt refinancing, construction or upgrades of infrastructure, acquisitions and other corporate purposes. Most of these rural telecommunications companies have diversified their operations and also provide broadband services.

Long-Term Loans

RTFC’s long-term loans generally have the following characteristics:

•terms not exceeding 10 years on a senior secured basis and terms of up to five years on an unsecured basis;

•amortizing or bullet maturity payment structures;

•the property, plant and equipment financed by and securing the long-term loan has a useful life generally equal to or in excess of the loan maturity;

•flexibility for the borrower to select a fixed interest rate for periods from one year to the final loan maturity or a variable interest rate; and

•the ability for the borrower to select various tranches with either a fixed or variable interest rate for each tranche.

When a selected fixed interest rate term expires, generally the borrower may select another fixed-rate term or the current variable rate. The fixed rate on a loan is generally determined on the day the loan is advanced or converted to a fixed rate based on the term selected.

6

To borrow from RTFC, a rural telecommunication system generally must be able to demonstrate the ability to achieve and maintain an annual debt service coverage ratio of 1.25. RTFC may make long-term loans to rural telecommunication systems, on a case-by-case basis, that do not meet this general criterion.

Line of Credit Loans

RTFC also provides revolving line of credit loans to assist borrowers with liquidity and cash management on terms similar to those provided by CFC as described herein.

Loan Features and Options

Interest Rates

As a member-owned cooperative finance organization, CFC is a cost-based lender. As such, our interest rates are set based on a yield that we believe will generate a reasonable level of earnings to cover our cost of funding, general and administrative expenses and provision for credit losses. Long-term fixed rates are set daily for new loan advances and loans that reprice. The fixed rate on each loan is generally determined on the day the loan is advanced or repriced based on the term selected. The variable rate is established monthly. Various standardized discounts may reduce the stated interest rates for borrowers meeting certain criteria related to performance, volume, collateral and equity requirements.

Conversion Option

Generally, a borrower may convert a long-term loan from a variable interest rate to a fixed interest rate at any time without a fee and convert a long-term loan from a fixed rate to another fixed rate or to a variable rate at any time generally subject to a make-whole premium fee.

Prepayment Option

Generally, borrowers may prepay long-term fixed-rate loans at any time, subject to payment of an administrative fee and a make-whole premium, and prepay long-term variable-rate loans at any time, subject to payment of an administrative fee. Line of credit loans may be prepaid at any time without a fee.

Loan Security

Long-term loans made by CFC typically are senior secured on parity with other secured lenders (primarily RUS), if any, by all assets and revenue of the borrower, subject to standard liens typical in utility mortgages such as those related to taxes, worker’s compensation awards, mechanics’ and similar liens, rights-of-way and governmental rights. We are able to obtain liens on parity with liens for the benefit of RUS because RUS’ form of mortgage expressly provides for other lenders such as CFC to have a parity lien position if the borrower satisfies certain conditions or obtains a written lien accommodation from RUS. When we make loans to borrowers that have existing loans from RUS, we generally require those borrowers to either obtain such a lien accommodation or satisfy the conditions necessary for our loan to be secured on parity under the mortgage with the loan from RUS. As noted above, CFC line of credit loans generally are unsecured.

We provide additional information on our loan programs in the sections “Item 7. MD&A—Consolidated Balance Sheet Analysis,” and “Item 7. MD&A—Credit Risk.”

Guarantee Programs

When we guarantee our members’ debt obligations, we use the same credit policies and monitoring procedures for guarantees as for loans. If a member system defaults in its obligation to pay debt service, then we are obligated to pay any required amounts under our guarantees. Meeting our guarantee obligations satisfies the underlying obligation of our member systems and prevents the exercise of remedies by the guarantee beneficiary based upon a payment default by a member system. The member system is required to repay any amount advanced by us with interest pursuant to the documents evidencing the member system’s reimbursement obligation.

7

Guarantees of Long-Term Tax-Exempt Bonds

We guarantee debt issued for our members’ construction or acquisition of pollution control, solid waste disposal, industrial development and electric distribution facilities. Governmental authorities issue such debt on a nonrecourse basis and the interest thereon is exempt from federal taxation. The proceeds of the offering are made available to the member system, which in turn is obligated to pay the governmental authority amounts sufficient to service the debt.

If a system defaults for failure to make the debt payments and any available debt service reserve funds have been exhausted, we are obligated to pay scheduled debt service under our guarantee. Such payment will prevent the occurrence of an event of payment default that would otherwise permit acceleration of the bond issue. The system is required to repay any amount that we advance pursuant to our guarantee plus interest on that advance. This repayment obligation, together with the interest thereon, is typically senior secured on parity with other lenders (including, in most cases, RUS), by a lien on substantially all of the system’s assets. If the security instrument is a common mortgage with RUS, then in general, we may not exercise remedies for up to two years following default. However, if the debt is accelerated under the common mortgage because of a determination that the related interest is not tax-exempt, the system’s obligation to reimburse us for any guarantee payments will be treated as a long-term loan. The system is required to pay us initial and/or ongoing guarantee fees in connection with these transactions.

Certain guaranteed long-term debt bears interest at variable rates that are adjusted at intervals of one to 270 days including weekly, every five weeks or semi-annually to a level favorable to their resale or auction at par. If funding sources are available, the member that issued the debt may choose a fixed interest rate on the debt. When the variable rate is reset, holders of variable-rate debt have the right to tender the debt for purchase at par. In some transactions, we have committed to purchase this debt as liquidity provider if it cannot otherwise be re-marketed. If we hold the securities, the member cooperative pays us the interest earned on the bonds or interest calculated based on our short-term variable interest rate, whichever is greater. The system is required to pay us stand-by liquidity fees in connection with these transactions.

Letters of Credit

In exchange for a fee, we issue irrevocable letters of credit to support members’ obligations to energy marketers, other third parties and to the USDA Rural Business-Cooperative Service. Each letter of credit is supported by a reimbursement agreement with the member on whose behalf the letter of credit was issued. In the event a beneficiary draws on a letter of credit, the agreement generally requires the member to reimburse us within one year from the date of the draw, with interest accruing from the draw date at our line of credit variable interest rate.

The U.S. Federal Communications Commission (“FCC”) has designated CFC as an acceptable source for letters of credit in support of USDA and FCC programs that encourage deployment of high-speed broadband services throughout rural America. The designation allows CFC to provide credit support for rural electric cooperatives and telecommunication providers that participate in programs designed to increase deployment of broadband services to underserved rural areas.

Other Guarantees

We may provide other guarantees as requested by our members. Other guarantees are generally unsecured with guarantee fees payable to us.

We provide additional information on our guarantee programs and outstanding guarantee amounts as of May 31, 2021 and 2020 in “Note 13—Guarantees.”

8

| INVESTMENT POLICY | ||

We invest funds in accordance with policies adopted by our board of directors. Pursuant to our current investment policy, an Investment Management Committee was established to oversee and administer our investments with the objective of seeking returns consistent with the preservation of principal and maintenance of adequate liquidity. The Investment Management Committee may direct funds to be invested in direct obligations of, or obligations guaranteed by, the United States (“U.S.”) or agencies thereof and investments in government-sponsored enterprises, certain financial institutions in the form of overnight investment products and Eurodollar deposits, bankers’ acceptances, certificates of deposit, working capital acceptances or other deposits. Other permitted investments include highly rated obligations, such as commercial paper, certain obligations of foreign governments, municipal securities, asset-backed securities, mortgage-backed securities and certain corporate bonds. In addition, we may invest in overnight or term repurchase agreements. Investments are denominated in U.S. dollars exclusively. All of these investments are subject to requirements and limitations set forth in our investment policy.

| INDUSTRY | ||

Overview

Our rural electric cooperative members operate in the energy sector, which is one of 16 critical infrastructure sectors identified by the U.S. government because the services provided by each sector, all of which have an impact on other sectors, are deemed as essential in supporting and maintaining the overall functioning of the U.S. economy. Rural electric cooperatives are an integral part of the U.S. electric utility industry, a sub-sector of the energy sector, serving as power providers for approximately 1 in 8 individuals in the U.S., totaling approximately 42 million people, including over 20 million businesses, homes, schools, churches, farms, irrigation systems and other establishments across the U.S. Based on the latest annual data reported by the U.S. Energy Information Administration, a statistical and analytical agency within the U.S. Department of Energy, the electric utility industry had revenue of approximately $402 billion in 2019, of which approximately 12% was generated by electric cooperatives. For more than 75 years, electric cooperatives have powered local economies across approximately 56% of the nation’s land mass.

CFC was established by electric utility cooperatives to serve as a supplemental financing source to RUS loan programs and to mitigate uncertainty related to government funding. CFC aggregates the combined strength of its rural electric member cooperatives to access the public capital markets and other funding sources. CFC works cooperatively with RUS; however, CFC is not a federal agency or a government-sponsored enterprise. CFC meets the financial needs of its rural electric members by:

•providing financing to RUS-eligible rural electric utility systems for infrastructure, including for those facilities that are not eligible for financing from RUS;

•providing bridge loans required by borrowers in anticipation of receiving RUS funding;

•providing financial products not otherwise available from RUS, including lines of credit, letters of credit, guarantees on tax-exempt financing, weather-related emergency lines of credit, unsecured loans and investment products such as commercial paper, select notes, medium-term notes and member capital securities; and

•meeting the financing needs of those rural electric systems that repay or prepay their RUS loans and replace the government loans with private capital.

Electric Member Operating Environment

In general, electric cooperatives have not been significantly impacted by the effects of retail deregulation. There were 19 states that had adopted programs that allow consumers to choose their supplier of electricity as of May 31, 2021. Depending on the state, the choices can range from being limited to commercial and industrial consumers to “retail choice” for all consumers. In most states, cooperatives have been exempted from or have been allowed to opt out of the regulations allowing for competition. In states offering retail competition, it is important to note that while consumers may be able to

9

choose their energy supplier, the electric utility still receives compensation for the necessary service of delivering electricity to consumers through its utility transmission and distribution plant.

The electric utility industry is facing a potential decrease to kilowatt-hour sales due to technology advances that increase energy efficiency of all appliances and devices used in the home and in businesses as well as from distributed generation in the form of rooftop solar and home generators (“behind-the-meter generation”). Electric cooperatives are facing the same issues, but in general to a lesser extent than investor-owned power systems. To date, we have not seen negative impacts in the electric cooperative financial results due to behind-the-meter generation.

Electric cooperatives have options to mitigate the impact of such issues, such as rate structures to ensure that costs are appropriately recovered for grid and other necessary ancillary services and the use of electricity for end-uses that would otherwise be powered by fossil fuels where doing so reduces emissions and saves consumers money (“beneficial electrification”). The push away from fossil fuel use may continue the trend toward beneficial electrification such as the adoption of electric vehicles, which may increase kilowatt-hour sales to many utilities. Beneficial electrification may also improve the utilities’ ability to balance load profiles by leveraging and balancing consumer and system assets such as electric vehicles and battery storage.

Facilitation of Rural Broadband Expansion by Electric Cooperatives

Many electric cooperatives are making investments in fiber to support core electric plant communications. Some of these electric cooperatives are leveraging these fiber assets to offer broadband services, either directly or through partnering with local telecommunication companies and others. Over 30 electric cooperatives were awarded approximately $250 million in federal funding through the Connect America Fund Phase II auction (“CAF II”) process by the FCC that was held in 2018. The awarded funds are being distributed over a 10-year period. More than 190 electric cooperatives, many of which are already offering or building out projects, were awarded approximately $1.6 billion though the FCC’s Rural Development Opportunity Fund (“RDOF”). Those funds also will be distributed over a 10-year period. As federal and state governments increase funding opportunities for electric cooperatives in order to offer broadband services, we will continue to increase our credit support, which may include loans and/or letters of credit, to borrowers who participate in CAF II, RDOF and other programs designed to increase broadband services in rural areas. Loans outstanding to our members related to the construction and operation of broadband services totaled approximately $854 million as of May 31, 2021.

Regulatory Oversight of Electric Cooperatives

There are 11 states in which some or all electric cooperatives are subject to state regulatory oversight of their rates and tariffs by state utility commissions and do not have a right to opt out of regulation. Those states are Arizona, Arkansas, Hawaii, Kentucky, Louisiana, Maine, Maryland, New Mexico, Vermont, Virginia and West Virginia. Regulatory jurisdiction by state commissions generally includes rate and tariff regulation, the issuance of securities and the enforcement of service territory as provided for by state law.

The Federal Energy Regulatory Commission (“FERC”) has regulatory authority over three aspects of electric power, as provided for under Parts II and III of the Federal Power Act (“FPA”):

•the transmission of electric energy in interstate commerce;

•the sale of electric energy at wholesale in interstate commerce; and

•the approval and enforcement of reliability standards affecting all users, owners and operators of the bulk power system.

In addition, FERC regulates the issuance of securities by public utilities under the FPA in the event the applicable state commission does not.

Our electric distribution and power supply members are subject to regulation by various federal, regional, state and local authorities with respect to the environmental effects of their operations. At the federal level, the U.S. Environmental Protection Agency (“EPA”) from time to time proposes rulemakings that could force the electric utility industry to incur capital costs to comply with potential new regulations and possibly retire coal-fired generating capacity. Since there are only 11 states in which some or all electric cooperatives are subject to state regulatory oversight of their rates and tariffs, in most cases any associated costs of compliance can be passed on to cooperative consumers without additional regulatory approval.

10

On June 19, 2019, the EPA issued the final Affordable Clean Energy (“ACE”) rule. Falling under Section 111(d) of the Federal Clean Air Act, the ACE rule addresses existing sources of emissions and sets a framework under which states should develop plans establishing standards of performance for their existing emissions sources and then submit those plans to the EPA for approval. States will have three years from the date of the final rule to prepare and submit a plan that establishes a standard of performance. A coalition of 23 states, several local governments and several environmental organizations filed a lawsuit against the EPA challenging the ACE rule in the U.S. Court of Appeals for the D.C. Circuit. On January 19, 2021, the court vacated the ACE rule and directed the EPA to consider the greenhouse gas standards. A petition for certiorari has been filed with the U.S. Supreme Court.

| LENDING COMPETITION | ||

Overview

RUS is the largest lender to electric cooperatives, providing them with long-term secured loans. CFC provides financial products and services to its members, primarily in the form of long-term secured and short-term unsecured loans, to supplement RUS financing, to provide loans to members that have elected not to borrow from RUS, and to bridge long-term financing provided by RUS. We also offer other financing options, such as credit support in the form of letters of credit and guarantees, loan syndications and loan participations. Our credit products are tailored to meet the specific needs of each borrower, and we often offer specific transaction structures that our competitors do not provide. CFC also offers certain risk-mitigation products and interest rate discounts on secured, long-term loans for its members that meet performance, volume, collateral and equity requirements.

Primary Lending Competitors

CFC’s primary competitor is CoBank, ACB a federally chartered instrumentality of the U.S. that is a member of the Farm Credit System. CFC also competes with banks, other financial institutions and the capital markets to provide loans and other financial products to our members. As a result, we are competing with the customer service, pricing and funding options our members are able to obtain from these sources. We attempt to minimize the effect of competition by offering a variety of loan options and value-added services and by leveraging the working relationships developed with the majority of our members over the past 52 years. Further, on an annual basis, we allocate substantially all net earnings to members (i) in the form of patronage capital, which reduces our members’ effective cost of borrowing, and (ii) through the members’ capital reserve. The value-added services that we provide include, but are not limited to, benchmarking tools, financial models, publications and various conferences, meetings and training workshops.

We are not able to specifically identify the amount of debt our members have outstanding to CoBank, ACB from either the annual financial and statistical reports our members file with us or from CoBank, ACB’s public disclosure; however, we believe CoBank, ACB is the additional lender, along with CFC and RUS, with significant long-term debt outstanding to rural electric cooperatives.

Rural Electric Lending Market

Most of our rural electric borrowers are non-for-profit, private companies owned by the members they serve. As such, there is limited publicly available information to accurately determine the overall size of the rural electric lending market. We utilize the annual financial and statistical reports submitted to us by our members to estimate the overall size of the rural electric lending market. The substantial majority of our members have a fiscal year-end that corresponds with the calendar year-end. Therefore, the annual information we use to estimate the size of the rural electric market is typically based on the calendar year-end rather than CFC’s fiscal year-end.

Based on financial data submitted to us by our electric utility members, we present the long-term debt outstanding to CFC by member class, RUS and other lenders in the electric cooperative industry as of December 31, 2020 and 2019 in the table below. The data presented as of December 31, 2020, were based on information reported by 811 distribution systems and 52 power supply systems. The data presented as of December 31, 2019, were based on information reported by 800 distribution systems and 53 power supply systems.

11

| December 31, | ||||||||||||||||||||||||||

| 2020 | 2019 | |||||||||||||||||||||||||

| (Dollars in thousands) | Debt Outstanding | % of Total | Debt Outstanding | % of Total | ||||||||||||||||||||||

Total long-term debt reported by members:(1) | ||||||||||||||||||||||||||

| Distribution | $ | 52,274,309 | $ | 49,976,016 | ||||||||||||||||||||||

| Power supply | 44,830,704 | 43,958,889 | ||||||||||||||||||||||||

| Less: Long-term debt funded by RUS | (39,660,041) | (39,214,146) | ||||||||||||||||||||||||

| Members’ non-RUS long-term debt | $ | 57,444,972 | $ | 54,720,759 | ||||||||||||||||||||||

| Funding sources of members’ long-term debt: | ||||||||||||||||||||||||||

| Long-term debt funded by CFC by member class: | ||||||||||||||||||||||||||

| Distribution | $ | 20,382,616 | 36 | % | $ | 19,540,233 | 36 | % | ||||||||||||||||||

| Power supply | 4,723,956 | 8 | 4,398,516 | 8 | ||||||||||||||||||||||

| Long-term debt funded by CFC | 25,106,572 | 44 | 23,938,749 | 44 | ||||||||||||||||||||||

| Long-term debt funded by other lenders | 32,338,400 | 56 | 30,782,010 | 56 | ||||||||||||||||||||||

| Members’ non-RUS long-term debt | $ | 57,444,972 | 100 | % | $ | 54,720,759 | 100 | % | ||||||||||||||||||

____________________________

(1) Reported amounts are based on member-provided financial information, which may not have been subject to audit by an independent accounting firm.

While we believe our estimates of the overall size of the rural electric lending market serve as a useful tool in gauging the size of this lending sector, they should be viewed as estimates rather than precise measures as there are certain limitations in our estimation methodology, including, but not limited to, the following:

•Although certain underlying data included in the financial and statistical reports provided to us by members may have been audited by an independent accounting firm, our accumulation of the data from these reports has not been subject to a review for accuracy by an independent accounting firm.

•The data presented is not necessarily inclusive of all members because in some cases our receipt of annual member financial and statistical reports may be delayed and not received in a timely manner to incorporate into our market estimates.

•The financial and statistical reports submitted by members include information on indebtedness to RUS, but the reports do not include comprehensive data on indebtedness to other lenders and are not on a consolidated basis.

| REGULATION | ||

General

CFC, NCSC and RTFC are not subject to direct federal regulatory oversight or supervision with regard to lending. CFC, NCSC and RTFC are subject to state and local jurisdiction commercial lending and tax laws that pertain to business conducted in each state, including but not limited to lending laws, usury laws and laws governing mortgages. These state and local laws regulate the manner in which we make loans and conduct other types of transactions. The statutes, regulations and policies to which the companies are subject may change at any time. In addition, the interpretation and application by regulators of the laws and regulations to which we are subject may change from time to time. Certain of our contractual arrangements, such as those pertaining to funding obtained through the Guaranteed Underwriter Program, provide for the Federal Financing Bank and RUS to periodically review and assess CFC’s compliance with program terms and conditions.

Derivatives Regulation

CFC engages in over-the-counter (“OTC”) derivative transactions to manage interest rate risk. As an end user of derivative financial instruments, CFC is subject to regulations that apply to derivatives generally. The Dodd-Frank Act (“DFA”), enacted July 2010, resulted in, among other things, comprehensive regulation of the OTC derivatives market. The DFA

12

provides for an extensive framework for the regulation of OTC derivatives, including mandatory clearing, exchange trading and transaction reporting of certain OTC derivatives. Subsequent to the enactment of the DFA, the U.S. Commodity Futures Trading Commission (“CFTC”) issued a final rule, “Clearing Exemption for Certain Swaps Entered into by Cooperatives,” which created an exemption from mandatory clearing for cooperatives. The CFTC’s final rule, “Margin Requirements for Uncleared Swaps for Swap Dealers and Major Swap Participants,” includes an exemption from margin requirements for uncleared swaps for cooperatives that are financial end users. CFC is an exempt cooperative end user of derivative financial instruments and does not participate in the derivatives markets for speculative, trading or investing purposes and does not make a market in derivatives.

| HUMAN CAPITAL MANAGEMENT | ||

CFC’s success in providing industry expertise and responsive service to meet the needs of our members across the U.S. is dependent on the quality of service provided by our employees and their relationships with our members. We therefore strive to align our human resource policies and staffing strategy with our member-focused mission and core values of service, integrity and excellence. Our staffing objectives are (i) to attract, develop and retain a highly qualified workforce, with diverse backgrounds and experience in multiple areas whose skills and strengths are consistent with CFC’s mission, and (ii) to create an engaged, inclusive and collaborative work culture, which we believe are both critical in delivering exceptional service to our members. Because much of our business operations involves significant member-facing interaction with a relatively stable base of long-standing member borrowers, we place a priority on the retention of high-performing employees who have extensive, in-depth experience serving the needs of our members. Over the last four fiscal years, our voluntary turnover rate has remained at or below 10%, which is lower than the annual voluntary separation rates reported by the U.S. Bureau of Labor Statistics for the financial activities industry sector for this period. We had 248 and 253 employees as of May 31, 2021 and 2020, respectively, all of which were located in the U.S. The slight decrease in the number of employees during fiscal year 2021 was primarily due to natural attrition.

Because attracting, developing and retaining high-level talent is a key component of our human capital objectives, we seek to provide competitive compensation and benefits packages. In establishing base salary amounts, we take into account market and industry competitive data. We encourage regular, ongoing employee performance feedback and conduct annual performance reviews of each employee, which are intended to evaluate individual performance, achievements and contributions to the company, identify development opportunities and serve as a basis for awarding annual merit increases. In addition to base salary amounts, we offer annual incentive bonus plan opportunities that are based on attainment of a scorecard of targeted corporate goals established at the beginning of each fiscal year. Attainment of each of the annual scorecard goals requires the collective engagement and effort of employees across the company, which we believe incentivizes employees to work together across teams and fosters an overall collaborative working environment.

We place a high priority on the health and wellness of our employees. We therefore offer various programs intended to promote the physical, mental and financial well-being of employees. Our benefits offerings include vacation and leave programs; health, dental, vision, life and disability insurance coverage; and flexible spending and health savings plans, most of which are funded in whole or in part by CFC. We make investments in the future financial security of our employees by offering retirement plans that consist of a 401(k) plan with a company match component and an employer-funded defined benefit retirement plan in which CFC makes an annual contribution in an amount that approximates 17% of each employee’s base salary, which we believe helps in our efforts to engage employees, retain high-performing employees and reduce turnover. We also offer programs and resources intended to promote work-life balance, assist in navigating life events and improve employee well-being, such as flexible work schedules, remote work options, an employee assistance program, legal insurance and identity theft coverage services.

As part of our efforts to promote an engaged, inclusive and collaborative workplace culture, we encourage employees to expand their capabilities and enhance their career potential through employer-funded onsite training, external training, tuition assistance and professional events. In fiscal year 2021, CFC employees completed more than 3,632 training hours through our internal corporate training classes and resources as well as through our support of employees’ enrollment in external professional training opportunities. We seek to tailor our training programs to evolving events and employee interests. Examples of training programs offered in the reporting period include Unconscious Bias & Allyship, Inclusive Leadership, Leading Virtual Teams, Personal Finance and Adapting to Change. We also support employee development

13

though a company-sponsored Toastmasters chapter, guest speakers from cooperative partners and staff trips to local electric cooperatives to allow new employees to learn first-hand how their efforts contribute to our members’ success.

The onset of the COVID-19 pandemic in March 2020 introduced numerous, unprecedented challenges. Our priorities during the COVID-19 pandemic, which continues to persist, have been to protect the health and safety of our employees while also ensuring that we are able to meet the needs of our electric cooperative borrowers as they operate in a sector that provides an essential service to residential and commercial customers. We responded promptly to these challenges, taking a number of precautionary steps to safeguard our business operations and employees, including, but not limited to, implementing remote work arrangements, limiting employee travel and in-person meetings, providing flexible work schedules to accommodate school and childcare challenges and offering training to help our employees adapt to the changes in our work environment.

In July 2021, following the expiration on June 30, 2021 of the state of emergency declared in March 2020 by Virginia’s governor in response to the pandemic and the lifting of all COVID-19 restrictions in Virginia, subject to certain exceptions, we brought 100% of our staff back to CFC’s corporate headquarters building, which continues to adhere to the COVID-19 workplace safety and health standards established by Virginia and guidance provided by the CDC. While we have been able to maintain business continuity throughout the pandemic and experienced no pandemic-related employee furloughs or layoffs, we believe we can provide the highest quality of service and deliver more effectively on our member-focused mission, which requires a significant number of member-facing staff working collaboratively with other staff, by resuming full-time, in-office work.

| AVAILABLE INFORMATION | ||

Our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and any amendments to these reports, are available for free at www.nrucfc.coop as soon as reasonably practicable after they are electronically filed with or furnished to the U.S. Securities and Exchange Commission (“SEC”). These reports also are available for free on the SEC’s website at www.sec.gov. Information posted on our website is not incorporated by reference into this Form 10-K.

Item 1A. Risk Factors

Our financial condition, results of operations and liquidity are subject to various risks and uncertainties, some of which are inherent in the financial services industry and others of which are more specific to our own business. The discussion below addresses the most significant risks, of which we are currently aware, that could have a material adverse impact on our business, financial condition, results of operations or liquidity. However, other risks and uncertainties, including those not currently known to us, could also negatively impact our business, financial condition, results of operations and liquidity. Therefore, the following should not be considered a complete discussion of all the risks and uncertainties we may face. For information on how we manage our key risks, see “Item 7. MD&A—Risk Management.” You should consider the following risks together with all of the other information in this report.

| RISK FACTORS | ||

Credit Risks

We are subject to credit risk that a borrower or other counterparty may not be able to meet its contractual obligations in accordance with agreed-upon terms, which could have a material adverse effect on our financial condition, results of operations and liquidity. Because we lend primarily to U.S. rural electric utility systems, we also are inherently subject to single-industry and single-obligor concentration risks.

As a lender, our primary credit risk arises from the extension of credit to borrowers. Our loan portfolio, which represents the largest component of assets on our balance sheet, accounts for the substantial majority of our credit risk exposure. Loans outstanding to electric utility organizations represented approximately 99% of our total loans outstanding as of May 31, 2021. We had 892 borrowers with loans outstanding as of May 31, 2021, and our 20 largest borrowers accounted for 22% of total loans outstanding as of May 31, 2021. The largest total exposure to a single borrower or controlled group represented less than 2% of total loans outstanding as of May 31, 2021. Texas historically has had the largest number of borrowers with

14

loans outstanding and the largest loan concentration in any one state. Loans outstanding to Texas borrowers represented 17% of total loans outstanding as of May 31, 2021.

We face the risk that the principal of, or interest on, a loan will not be paid timely or at all or that the value of any underlying collateral securing a loan will be insufficient to cover our outstanding exposure. A deterioration in the financial condition of a borrower or underlying collateral could impair the ability of a borrower to repay a loan or our ability to recover unpaid amounts from the underlying collateral. We maintain an internal risk rating system in which we assign a rating to each borrower and credit facility that are intended to reflect the ability of a borrower to repay its obligations and assess the probability of default. Unforeseen events and developments that affect specific borrowers or that occur in a region where we have a high concentration of credit risk, such as the February 2021 polar vortex, may result in significant risk rating downgrades. Such an event may result in an increase in delinquent, nonperforming and criticized loans and net charge-offs and an increase in our credit risk.

We establish an allowance for credit losses for estimated expected credit losses in our loan portfolio. Because the process for determining our allowance for credit losses requires significant, complex judgments about the ability of borrowers to repay their loans, we identified the estimation of our allowance for credit losses as a critical accounting policy. Our borrower risk ratings are a key input in establishing our allowance for credit losses. Therefore, the deterioration in the financial condition of a borrower may result in a significant increase in our allowance for credit losses and provision for credit losses and may have a material adverse impact on our results of operations, financial condition and liquidity. In addition, we might underestimate expected credit losses and have credit losses in excess of the established allowance for credit losses if we fail to timely identify a deterioration in a borrower’s financial condition or due to other factors, such as if the methodology and process we use in assigning risk ratings and making judgments in extending credit to our borrowers does not accurately capture the level of our credit risk exposure or our historical loss experience proves to be not indicative of our expected future losses.

Adverse changes, developments or uncertainties in the rural electric utility industry could adversely impact the operations or financial performance of our member electric cooperatives, which, in turn, could have an adverse impact on our financial results.

Our focus as a member-owned finance cooperative is on lending to our rural member electric utility cooperatives, which is the primary source of our revenue. As a result of lending primarily to our members, we have a loan portfolio with single-industry concentration. Loans to rural electric utility cooperatives accounted for approximately 99% of our total loans outstanding as of May 31, 2021. While we historically have experienced limited defaults and very low credit losses in our electric utility loan portfolio, factors that may have a negative impact on the operations of our member rural electric cooperatives include but are not limited to, the price and availability of distributed energy resources, regulatory or compliance factors related to managing greenhouse gas emissions (including the potential for stranded assets) and extreme weather conditions related to climate change. The factors listed above, individually or in combination, could result in declining sales or increased power supply and operating costs and could potentially cause a deterioration in the financial performance of our members and the value of the collateral securing their loans. This could impair their ability to repay us in accordance with the terms of their loans. In such case, it may be necessary to increase our allowance for credit losses, which would result in an increase in the provision for credit losses and a decrease in our net income.

Advances in technology may change the way electricity is generated and transmitted, which could adversely affect the business operations of our members and negatively impact the credit quality of our loan portfolio and financial results.

Advances in technology could reduce demand for power supply systems and distribution services. The development of alternative technologies that produce electricity, including solar cells, wind power and microturbines, has expanded and could ultimately provide affordable alternative sources of electricity and permit end users to adopt distributed generation systems that would allow them to generate electricity for their own use. As these and other technologies, including energy conservation measures, are created, developed and improved, the quantity and frequency of electricity usage by rural customers could decline. Advances in technology and conservation that cause our electric system members’ power supply, transmission and/or distribution facilities to become obsolete prior to the maturity of loans secured by these assets could have an adverse impact on the ability of our members to repay such loans, which could result in an increase in nonperforming or restructured loans. These conditions could negatively impact the credit quality of our loan portfolio and financial results.

15

We may obtain entities or other assets through foreclosure, which would subject us to the same performance and financial risks as any other owner or operator of similar businesses or assets.

As a financial institution, from time to time we may obtain entities and assets of borrowers in default through foreclosure proceedings. If we become the owner and operator of entities or assets obtained through foreclosure, we are subject to the same performance and financial risks as any other owner or operator of similar assets or entities. In particular, the value of the foreclosed assets or entities may deteriorate and have a negative impact on our results of operations. We assess foreclosed assets, if any, for impairment periodically as required under generally accepted accounting principles in the U.S. (“U.S. GAAP.”) Impairment charges, if required, represent a reduction to earnings in the period of the charge. There may be substantial judgment used in the determination of whether such assets are impaired and in the calculation of the amount of the impairment. In addition, when foreclosed assets are sold to a third party, the sale price we receive may be below the amount previously recorded in our financial statements, which will result in a loss being recorded in the period of the sale.

The nonperformance of our derivative counterparties could impair our financial results.

We use interest rate swaps to manage our interest rate risk. There is a risk that the counterparties to these agreements will not perform as agreed, which could adversely affect our results of operations. The nonperformance of a counterparty on an agreement would result in the derivative no longer being an effective risk-management tool, which could negatively affect our overall interest rate risk position. In addition, if a counterparty fails to perform on our derivative obligation, we could incur a financial loss to replace the derivative with another counterparty and/or a loss through the failure of the counterparty to pay us amounts owed. We were in a net payable position for all of our interest rate swaps, after taking into consideration master netting agreements, of $464 million as of May 31, 2021.

A decline in our credit rating could trigger payments under our derivative agreements, which could impair our financial results.

We have certain interest rate swaps that contain credit risk-related contingent features referred to as rating triggers. Under certain rating triggers, if the credit rating for either counterparty falls to the level specified in the agreement, the other counterparty may, but is not obligated to, terminate the agreement. If either counterparty terminates the agreement, a net payment may be due from one counterparty to the other based on the prevailing fair value, excluding credit risk, of the underlying derivative instrument. These rating triggers are based on our senior unsecured credit ratings by Moody’s Investors Service (“Moody’s”) and S&P Global Inc. (“S&P”). Based on our interest rate swap agreements subject to rating triggers, if all agreements for which we owe amounts were terminated as of May 31, 2021 and our senior unsecured ratings fell below Baa2 by Moody’s or below BBB by S&P, we would have been required to make a payment of up to $328 million as of that date. In addition, if our senior unsecured ratings fell below Baa3 by Moody’s, below BBB- by S&P or below BBB- by Fitch Ratings Inc. (“Fitch”), we would have been required to make a payment of up to $22 million as of that date. In calculating the required payments, we only consider agreements that, when netted for each counterparty pursuant to a master netting agreement, would require a payment upon termination. In the event that we are required to make a payment as a result of a rating trigger, it could have a material adverse impact on our financial results.

Liquidity Risks

If we are unable to access the capital markets or other external sources for funding, our liquidity position may be negatively affected and we may not have sufficient funds to meet all of our financial obligations as they become due.

We depend on access to the capital markets and other sources of financing, such as our investment portfolio, repurchase agreements, bank revolving credit agreements, investments from our members, private debt issuances through Farmer Mac and through the Guaranteed Underwriter Program, to fund new loan advances and refinance our long- and short-term debt and, if necessary, to fulfill our obligations under our guarantee and repurchase agreements. Market disruptions, downgrades to our long-term and/or short-term debt ratings, adverse changes in our business or performance, downturns in the electric industry and other events over which we have no control may deny or limit our access to the capital markets and/or subject us to higher costs for such funding. Our access to other sources of funding also could be limited by the same factors, by adverse changes in the business or performance of our members, by the banks committed to our revolving credit agreements or Farmer Mac, or by changes in federal law or the Guaranteed Underwriter Program. Our funding needs are determined primarily by scheduled short- and long-term debt maturities and the amount of our loan advances to our borrowers relative to the scheduled payment amortization of loans previously made by us. If we are unable to timely issue debt into the capital markets or obtain funding from other sources, we may not have the funds to meet all of our obligations as they become due.

16

A reduction in the credit ratings for our debt could adversely affect our liquidity and/or cost of debt.

Our credit ratings are important to maintaining our liquidity position. We currently contract with three nationally recognized statistical rating organizations to receive ratings for our secured and unsecured debt and our commercial paper. In order to access the commercial paper markets at current levels, we believe that we need to maintain our current ratings for commercial paper of P-1 from Moody’s, A-2 from S&P and F1 from Fitch. Changes in rating agencies’ rating methodology, actions by governmental entities or others, losses from individually evaluated loans and other factors could adversely affect the credit ratings on our debt. A reduction in our credit ratings could adversely affect our liquidity and competitive position, increase our borrowing costs or limit our access to the capital markets and the sources of financing available to us. A significant increase in our cost of borrowings and interest expense could cause us to sustain losses or impair our liquidity by requiring us to seek other sources of financing, which may be difficult to obtain.

Our ability to maintain compliance with the covenants related to our revolving credit agreements, collateral trust bond and medium-term note indentures and debt agreements could affect our ability to retire patronage capital, result in the acceleration of the repayment of certain debt obligations, adversely impact our credit ratings and hinder our ability to obtain financing.

We must maintain compliance with all covenants and conditions related to our revolving credit agreements and debt indentures. We are required to maintain a minimum average adjusted times interest earned ratio (“adjusted TIER”) for the six most recent fiscal quarters of 1.025 and an adjusted leverage ratio of no more than 10-to-1. In addition, we must maintain loans pledged as collateral for various debt issuances at or below 150% of the related secured debt outstanding as a condition to borrowing under our revolving credit agreements. If we were unable to borrow under the revolving credit agreements, our short-term debt ratings would likely decline, and our ability to issue commercial paper could become significantly impaired. Our revolving credit agreements also require that we earn a minimum annual adjusted TIER of 1.05 in order to retire patronage capital to members. See “Item 7. MD&A—Non-GAAP Financial Measures” for additional information on our adjusted measures and a reconciliation to the most comparable U.S. GAAP measures.