UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

| ý | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the quarterly period ended January 31, 2013

OR

| o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from _______________ to _______________

Commission file number: 0-17085

PEREGRINE PHARMACEUTICALS, INC.

(Exact name of Registrant as specified in its charter)

| Delaware | 95-3698422 | |

| (State or other jurisdiction of | (I.R.S. Employer | |

| incorporation or organization) | Identification No.) |

| 14282 Franklin Avenue, Tustin, California | 92780-7017 | ||

| (Address of principal executive offices) | (Zip Code) |

(714) 508-6000

(Registrant’s telephone number, including area code)

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes ý No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

Yes ý No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one)

| Large Accelerated Filer | o | Accelerated Filer | ý | |

| Non- Accelerated Filer | o | Smaller reporting company | o |

(Do not check if a smaller reporting company)

Indicate by checkmark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Yes o No ý

As of March 11, 2013, there were 137,110,758 shares of common stock, $0.001 par value, outstanding.

PEREGRINE PHARMACEUTICALS, INC.

TABLE OF CONTENTS

| Page | ||

| No. | ||

| PART I - FINANCIAL INFORMATION | 1 | |

| Item 1. | Consolidated Financial Statements. | 1 |

| Item 2. | Management’s Discussion and Analysis of Financial Condition And Results of Operations. | 15 |

| Item 3. | Quantitative and Qualitative Disclosures About Market Risk. | 24 |

| Item 4. | Controls and Procedures. | 24 |

| PART II - OTHER INFORMATION | 25 | |

| Item 1. | Legal Proceedings. | 25 |

| Item 1A. | Risk Factors. | 25 |

| Item 2. | Unregistered Sales of Equity Securities and Use of Proceeds. | 39 |

| Item 3. | Defaults Upon Senior Securities. | 39 |

| Item 4. | Mine Safety Disclosures. | 39 |

| Item 5. | Other Information. | 39 |

| Item 6. | Exhibits. | 40 |

| SIGNATURES | 41 | |

The terms “we,” “us,” “our,” “the Company,” and “Peregrine,” as used in this Report on Form 10-Q refers to Peregrine Pharmaceuticals, Inc. and its wholly-owned subsidiary, Avid Bioservices, Inc.

| i |

PART I - FINANCIAL INFORMATION

Item 1. Consolidated Financial Statements.

PEREGRINE PHARMACEUTICALS, INC.

CONDENSED CONSOLIDATED BALANCE SHEETS

| JANUARY 31, 2013 | APRIL 30, 2012 | |||||||

| Unaudited | ||||||||

| ASSETS | ||||||||

| CURRENT ASSETS: | ||||||||

| Cash and cash equivalents | $ | 26,255,000 | $ | 18,033,000 | ||||

| Trade and other receivables, net | 1,983,000 | 2,353,000 | ||||||

| Inventories, net | 4,635,000 | 3,611,000 | ||||||

| Prepaid expenses and other current assets, net | 878,000 | 795,000 | ||||||

| Total current assets | 33,751,000 | 24,792,000 | ||||||

| Property, net | 2,783,000 | 2,900,000 | ||||||

| Other assets | 623,000 | 570,000 | ||||||

| TOTAL ASSETS | $ | 37,157,000 | $ | 28,262,000 | ||||

| LIABILITIES AND STOCKHOLDERS’ EQUITY | ||||||||

| CURRENT LIABILITIES: | ||||||||

| Accounts payable | $ | 1,620,000 | $ | 3,492,000 | ||||

| Accrued clinical trial and related fees | 1,478,000 | 2,111,000 | ||||||

| Accrued payroll and related costs | 2,949,000 | 2,468,000 | ||||||

| Deferred revenue | 5,061,000 | 3,651,000 | ||||||

| Customer deposits | 6,729,000 | 4,865,000 | ||||||

| Other current liabilities | 930,000 | 1,052,000 | ||||||

| Total current liabilities | 18,767,000 | 17,639,000 | ||||||

| Deferred revenue | 292,000 | 361,000 | ||||||

| Other long-term liabilities | 699,000 | 779,000 | ||||||

| Commitments and contingencies | ||||||||

| STOCKHOLDERS' EQUITY: | ||||||||

| Preferred stock-$0.001 par value; authorized 5,000,000 shares; non-voting; nil shares outstanding | – | – | ||||||

| Common stock-$0.001 par value; authorized 325,000,000 shares; outstanding – 133,770,614 and 101,421,365, respectively | 134,000 | 101,000 | ||||||

| Additional paid-in capital | 376,720,000 | 347,506,000 | ||||||

| Accumulated deficit | (359,455,000 | ) | (338,124,000 | ) | ||||

| Total stockholders’ equity | 17,399,000 | 9,483,000 | ||||||

| TOTAL LIABILITIES AND STOCKHOLDERS' EQUITY | $ | 37,157,000 | $ | 28,262,000 | ||||

See accompanying notes to condensed consolidated financial statements.

| 1 |

PEREGRINE PHARMACEUTICALS, INC.

CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS AND COMPREHENSIVE LOSS

| THREE MONTHS ENDED JANUARY 31, | NINE MONTHS ENDED JANUARY 31, | |||||||||||||||

| 2013 | 2012 | 2013 | 2012 | |||||||||||||

| Unaudited | Unaudited | Unaudited | Unaudited | |||||||||||||

| REVENUES: | ||||||||||||||||

| Contract manufacturing revenue | $ | 6,961,000 | $ | 3,203,000 | $ | 17,157,000 | $ | 12,796,000 | ||||||||

| License revenue | 78,000 | 78,000 | 272,000 | 372,000 | ||||||||||||

| Total revenues | 7,039,000 | 3,281,000 | 17,429,000 | 13,168,000 | ||||||||||||

| COSTS AND EXPENSES: | ||||||||||||||||

| Cost of contract manufacturing | 3,651,000 | 2,484,000 | 9,378,000 | 9,219,000 | ||||||||||||

| Research and development | 5,437,000 | 9,180,000 | 18,471,000 | 26,758,000 | ||||||||||||

| Selling, general and administrative | 3,112,000 | 2,710,000 | 9,469,000 | 8,371,000 | ||||||||||||

| Total costs and expenses | 12,200,000 | 14,374,000 | 37,318,000 | 44,348,000 | ||||||||||||

| LOSS FROM OPERATIONS | (5,161,000 | ) | (11,093,000 | ) | (19,889,000 | ) | (31,180,000 | ) | ||||||||

| OTHER INCOME (EXPENSE): | ||||||||||||||||

| Interest and other income | 255,000 | 9,000 | 307,000 | 31,000 | ||||||||||||

| Interest and other expense | (8,000 | ) | (6,000 | ) | (53,000 | ) | (88,000 | ) | ||||||||

| Loss on early extinguishment of debt | – | – | (1,696,000 | ) | – | |||||||||||

| NET LOSS | $ | (4,914,000 | ) | $ | (11,090,000 | ) | $ | (21,331,000 | ) | $ | (31,237,000 | ) | ||||

| WEIGHTED AVERAGE COMMON SHARES OUTSTANDING: | ||||||||||||||||

| Basic and Diluted | 131,489,994 | 87,149,770 | 114,726,569 | 78,443,114 | ||||||||||||

| BASIC AND DILUTED LOSS PER COMMON SHARE | $ | (0.04 | ) | $ | (0.13 | ) | $ | (0.19 | ) | $ | (0.40 | ) | ||||

| COMPREHENSIVE LOSS | $ | (4,914,000 | ) | $ | (11,090,000 | ) | $ | (21,331,000 | ) | $ | (31,237,000 | ) | ||||

See accompanying notes to condensed consolidated financial statements.

| 2 |

PEREGRINE PHARMACEUTICALS, INC.

CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS

| NINE MONTHS ENDED JANUARY 31, | ||||||||

| 2013 | 2012 | |||||||

| Unaudited | Unaudited | |||||||

| CASH FLOWS FROM OPERATING ACTIVITIES: | ||||||||

| Net loss | $ | (21,331,000 | ) | $ | (31,237,000 | ) | ||

| Adjustments to reconcile net loss to net cash used in operating activities: | ||||||||

| Share-based compensation | 2,320,000 | 2,438,000 | ||||||

| Depreciation and amortization | 806,000 | 664,000 | ||||||

| Amortization of discount on notes payable and debt issuance costs | – | 33,000 | ||||||

| Loss on early extinguishment of debt | 1,696,000 | – | ||||||

| Loss on disposal of property | 8,000 | 2,000 | ||||||

| Changes in operating assets and liabilities: | ||||||||

| Trade and other receivables, net | 370,000 | (596,000 | ) | |||||

| Inventories, net | (1,024,000 | ) | 2,540,000 | |||||

| Prepaid expenses and other current assets, net | (83,000 | ) | (285,000 | ) | ||||

| Other non-current assets | 2,000 | 748,000 | ||||||

| Accounts payable | (1,883,000 | ) | (119,000 | ) | ||||

| Accrued clinical trial and related fees | (633,000 | ) | 750,000 | |||||

| Accrued payroll and related expenses | 481,000 | 643,000 | ||||||

| Deferred revenue | 1,341,000 | (3,174,000 | ) | |||||

| Customer deposits | 1,864,000 | 704,000 | ||||||

| Other current liabilities | (64,000 | ) | (29,000 | ) | ||||

| Other long-term liabilities | (80,000 | ) | (224,000 | ) | ||||

| Net cash used in operating activities | (16,210,000 | ) | (27,142,000 | ) | ||||

| CASH FLOWS FROM INVESTING ACTIVITIES: | ||||||||

| Property acquisitions | (686,000 | ) | (1,103,000 | ) | ||||

| (Increase) decrease in other assets | (55,000 | ) | 34,000 | |||||

| Net cash used in investing activities | (741,000 | ) | (1,069,000 | ) | ||||

| CASH FLOWS FROM FINANCING ACTIVITIES: | ||||||||

| Proceeds from issuance of common stock, net of issuance costs of $885,000 and $1,007,000, respectively | 26,166,000 | 26,190,000 | ||||||

| Proceeds from issuance of notes payable, net of issuance costs of $251,000 | 14,749,000 | – | ||||||

| Proceeds from exercise of stock options and under Employee Stock Purchase Plan | 291,000 | 96,000 | ||||||

| Principal payments on notes payable | (15,000,000 | ) | (1,333,000 | ) | ||||

| Payment of final fee on notes payable | (975,000 | ) | – | |||||

| Principal payments on capital leases | (58,000 | ) | (56,000 | ) | ||||

| Net cash provided by financing activities | 25,173,000 | 24,897,000 | ||||||

| NET INCREASE (DECREASE) IN CASH AND CASH EQUIVALENTS | 8,222,000 | (3,314,000 | ) | |||||

| CASH AND CASH EQUIVALENTS, beginning of period | 18,033,000 | 23,075,000 | ||||||

| CASH AND CASH EQUIVALENTS, end of period | $ | 26,255,000 | $ | 19,761,000 | ||||

| Schedule of non-cash investing and financing activities: | ||||||||

| Accounts payable for purchase of property | $ | 11,000 | $ | 13,000 | ||||

| Fair market value of warrants issued in connection with notes payable | $ | 470,000 | $ | – | ||||

See accompanying notes to condensed consolidated financial statements.

| 3 |

PEREGRINE PHARMACEUTICALS, INC.

NOTES

TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

FOR THE NINE MONTHS ENDED JANUARY 31, 2013 (unaudited)

| 1. | ORGANIZATION AND BUSINESS |

Peregrine Pharmaceuticals, Inc. (“Peregrine” or “Company”) is a biopharmaceutical company developing first-in-class monoclonal antibodies focused on the treatment and diagnosis of cancer. We are advancing two oncology programs with our lead product candidates, bavituximab and Cotara, for the treatment of various cancers. In addition, we are advancing our lead molecular imaging agent, 124I-PGN650, in an exploratory clinical trial for the imaging of multiple solid tumor types. Peregrine also has in-house manufacturing capabilities through its wholly-owned subsidiary Avid Bioservices, Inc. (“Avid”), a contract manufacturing organization that provides development and biomanufacturing services for Peregrine and its third-party clients.

| 2. | BASIS OF PRESENTATION |

The accompanying interim unaudited condensed consolidated financial statements have been prepared in accordance with United States generally accepted accounting principles (“U.S. GAAP”) and with the rules and regulations of the U.S. Securities and Exchange Commission (“SEC”) related to quarterly reports on Form 10-Q. Accordingly, they do not include all of the information and disclosures required by U.S. GAAP for a complete set of financial statements. These interim unaudited condensed consolidated financial statements and notes thereto should be read in conjunction with the audited consolidated financial statements and notes thereto included in the Company’s Annual Report on Form 10-K for the year ended April 30, 2012. The condensed consolidated balance sheet at April 30, 2012 has been derived from audited financial statements at that date. The unaudited financial information for the interim periods presented herein reflects all adjustments which, in the opinion of management, are necessary for a fair presentation of the financial condition and results of operations for the periods presented, with such adjustments consisting only of normal recurring adjustments. Results of operations for interim periods covered by this quarterly report on Form 10-Q may not necessarily be indicative of results of operations for the full fiscal year.

The interim unaudited condensed consolidated financial statements include the accounts of Peregrine Pharmaceuticals, Inc., and its wholly-owned subsidiary, Avid Bioservices, Inc. All intercompany accounts and transactions have been eliminated in the interim unaudited condensed consolidated financial statements.

The preparation of financial statements in conformity with U.S. GAAP requires management to make estimates and assumptions that affect the reported amounts, as well as disclosures of commitments and contingencies in the financial statements and accompanying notes. Actual results could differ from those estimates.

Going Concern

Our interim unaudited condensed consolidated financial statements have been prepared on a going concern basis, which contemplates the realization of assets and the satisfaction of liabilities in the normal course of business. The financial statements do not include any adjustments relating to the recoverability of the recorded assets or the classification of liabilities that may be necessary should it be determined that we are unable to continue as a going concern.

At January 31, 2013, we had $26,255,000 in cash and cash equivalents. We have expended substantial funds on the research and development of our product candidates, and funding the operations of Avid. As a result, we have historically experienced negative cash flows from operations since our inception and we expect the negative cash flows from operations to continue for the foreseeable future. Our net loss incurred during the nine-month period ended January 31, 2013 amounted to $21,331,000 and our net losses incurred during the past three fiscal years ended April 30, 2012, 2011 and 2010, amounted to $42,119,000, $34,151,000, and $14,494,000, respectively. Therefore, unless and until we are able to generate sufficient revenues from Avid’s contract manufacturing services and/or from the sale and/or licensing of our products under development, we expect such losses to continue for the foreseeable future.

Therefore, our ability to continue to fund our clinical trials and development efforts is highly dependent on the amount of cash and cash equivalents on hand combined with our ability to raise additional capital to support our future operations through one or more methods, including but not limited to, issuing additional equity or debt.

| 4 |

PEREGRINE PHARMACEUTICALS, INC.

NOTES

TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

FOR THE NINE MONTHS ENDED JANUARY 31, 2013 (unaudited) (continued)

Historically, we have funded a significant portion of our operations through the issuance of equity. During the nine months ended January 31, 2013, we raised $27,051,000 in gross proceeds under an At Market Sales Issuance Agreement (Note 8), of which $25,555,000 was raised subsequent to September 25, 2012, primarily to replace the $15,000,000 of initial funding we repaid on September 25, 2012 under an earlier loan facility we entered into on August 30, 2012 (Note 7). Subsequent to January 31, 2013 and through March 12, 2013, we raised an additional $4,805,000 in aggregate gross proceeds under two separate At Market Sales Issuance Agreements (Note 8).

With respect to our ability to raise additional capital from the issuance of equity, as of March 12, 2013, we have an effective shelf registration statement on Form S-3, under which we may issue, from time to time, in one or more offerings, shares of our common stock for gross proceeds of up to $145,525,000. However, our ability to raise additional capital in the equity markets is dependent on a number of factors, including, but not limited to, the market demand for our common stock. The market demand or liquidity of our common stock is subject to a number of risks and uncertainties, including but not limited to, negative economic conditions, adverse market conditions, adverse clinical trials results, and significant delays in one or more clinical trials. If our ability to access the capital markets becomes severely restricted, it could have a negative impact on our business plans, including our clinical trial programs and other research and development activities. In addition, even if we are able to raise additional capital, it may not be at a price or on terms that are favorable to us.

In addition to financing our operations through the issuance of equity, we may also secure additional funding through the issuance of debt, licensing or partnering our products in development, or increasing revenue from our wholly-owned subsidiary, Avid. While we will continue to explore these potential opportunities, there can be no assurances that we will be successful in securing debt financing, licensing or partnering our products in development, or generating additional revenue from Avid to complete the research, development, and clinical testing of our product candidates.

| 3. | SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES |

Adoption of Recent Accounting Pronouncements

Effective May 1, 2012, we adopted Financial Accounting Standards Board’s (“FASB”) Accounting Standards Update (“ASU”) No. 2011-05, Comprehensive Income (Topic 220): Presentation of Comprehensive Income and ASU No. 2011-12, Comprehensive Income (Topic 220): Deferral of the Effective Date for Amendments to the Presentation of Reclassifications of Items Out of Accumulated Other Comprehensive Income in ASU No. 2011-5. In these updates, an entity has the option to present the total of comprehensive income, the components of net income, and the components of other comprehensive income either in a single continuous statement of comprehensive income or in two separate but consecutive statements. In both choices, an entity is required to present each component of net income along with total net income, each component of other comprehensive income along with a total for other comprehensive income, and a total amount for comprehensive income. ASU No. 2011-05 eliminates the option to present the components of other comprehensive income as part of the statement of changes in stockholders’ equity. The amendments in ASU No. 2011-05 do not change the items that must be reported in other comprehensive income or when an item of other comprehensive income must be reclassified to net income. The adoption of ASU Nos. 2011-05 and 2011-12 did not have a material impact on our consolidated financial statements. We have presented comprehensive loss in the accompanying interim unaudited condensed consolidated statements of operations and comprehensive loss.

Pending Adoption of Recent Accounting Pronouncements

In February 2013, the FASB issued ASU No. 2013-02, Other Comprehensive Income (Topic 220): Reporting of Amounts Reclassified Out of Accumulated Other Comprehensive Income. ASU No. 2013-02 does not change the current requirements for reporting net income or other comprehensive income in financial statements, however, it does require an entity to report the effect of significant reclassifications out of accumulated other comprehensive income on the respective line items in net income if the amounts are required to be reclassified in their entirety to net income. For other amounts that are not required to be reclassified in their entirety to net income in the same reporting period, an entity is required to cross-reference to other disclosures that provide additional detail about those amounts. This guidance will be effective for reporting periods beginning after December 15, 2012, which will be our fiscal year 2014 (or May 1, 2013). We do not expect the adoption of this guidance to have a material impact on our consolidated financial statements.

| 5 |

PEREGRINE PHARMACEUTICALS, INC.

NOTES

TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

FOR THE NINE MONTHS ENDED JANUARY 31, 2013 (unaudited) (continued)

Revenue Recognition

We currently derive revenue from two sources: (i) contract manufacturing services provided by Avid, and (ii) licensing revenue related to agreements associated with Peregrine’s technologies under development.

We recognize revenue in accordance with the authoritative guidance for revenue recognition. We recognize revenue when all of the following criteria are met: (i) persuasive evidence of an arrangement exists, (ii) delivery (or passage of title) has occurred or services have been rendered, (iii) the seller’s price to the buyer is fixed or determinable, and (iv) collectability is reasonably assured. We also comply with the authoritative guidance for revenue recognition regarding arrangements with multiple deliverables.

Contract Manufacturing Revenue

Revenue associated with contract manufacturing services provided by Avid is recognized once the service has been rendered and/or upon shipment (or passage of title) of the product to the customer. On occasion, we recognize revenue on a “bill-and-hold” basis in accordance with the authoritative guidance. Under “bill-and-hold” arrangements, revenue is recognized once the product is complete and ready for shipment, title and risk of loss has passed to the customer, management receives a written request from the customer for “bill-and-hold” treatment, the product is segregated from other inventory, and no further performance obligations exist.

In addition, we also follow the authoritative guidance when reporting revenue as gross when we act as a principal versus reporting revenue as net when we act as an agent. For transactions in which we act as a principal, have discretion to choose suppliers, bear credit risk and perform a substantive part of the services, revenue is recorded at the gross amount billed to a customer and costs associated with these reimbursements are reflected as a component of cost of sales for contract manufacturing services.

Any amounts received prior to satisfying our revenue recognition criteria are recorded as deferred revenue in the accompanying interim unaudited condensed consolidated financial statements. We also record a provision for estimated contract losses, if any, in the period in which they are determined.

License Revenue

Revenue associated with licensing agreements primarily consists of non-refundable upfront license fees, non-refundable annual license fees and milestone payments. Non-refundable upfront license fees received under license agreements, whereby continued performance or future obligations are considered inconsequential to the relevant license technology, are recognized as revenue upon delivery of the technology. If a licensing agreement has multiple elements, we analyze each element of our licensing agreements and consider a variety of factors in determining the appropriate method of revenue recognition of each element.

Multiple Element Arrangements. Prior to the adoption of ASU No. 2009-13 on May 1, 2011, if a license agreement has multiple element arrangements, we analyze and determine whether the deliverables, which often include performance obligations, can be separated or whether they must be accounted for as a single unit of accounting in accordance with the authoritative guidance. Under multiple element arrangements, we recognize revenue for delivered elements only when the delivered element has stand-alone value and we have objective and reliable evidence of fair value for each undelivered element. If the fair value of any undelivered element included in a multiple element arrangement cannot be objectively determined, the arrangement would be accounted for as a single unit of accounting, and revenue is recognized over the estimated period of when the performance obligation(s) are performed.

In addition, under certain circumstances, when there is objective and reliable evidence of the fair value of the undelivered items in an arrangement, but no such evidence for the delivered items, we utilize the residual method to allocate the consideration received under the arrangement. Under the residual method, the amount of consideration allocated to delivered items equals the total arrangement consideration less the aggregate fair value of the undelivered items, and revenue is recognized upon delivery of the undelivered items based on the relative fair value of the undelivered items.

For new licensing agreements or material modifications of existing licensing agreements entered into after May 1, 2011, we follow the provisions of ASU No. 2009-13. If a licensing agreement includes multiple elements, we identify which deliverables represent separate units of accounting, and then determine how the arrangement consideration should be allocated among the separate units of accounting, which may require the use of significant judgment.

| 6 |

PEREGRINE PHARMACEUTICALS, INC.

NOTES

TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

FOR THE NINE MONTHS ENDED JANUARY 31, 2013 (unaudited) (continued)

If a licensing agreement includes multiple elements, a delivered item is considered a separate unit of accounting if both of the following criteria are met:

| 1. | The delivered item has value to the licensing partner on a standalone basis based on the consideration of the relevant facts and circumstances for each agreement; |

| 2. | If the arrangement includes a general right of return relative to the delivered item, delivery or performance of the undelivered item is considered probable and substantially in the Company’s control. |

Arrangement consideration is allocated at the inception of the agreement to all identified units of accounting based on their relative selling price. The relative selling price for each deliverable is determined using vendor specific objective evidence (“VSOE”), of selling price or third-party evidence of selling price if VSOE does not exist. If neither VSOE nor third-party evidence of selling price exists, we use our best estimate of the selling price for the deliverable. The amount of allocable arrangement consideration is limited to amounts that are fixed or determinable. The consideration received is allocated among the separate units of accounting, and the applicable revenue recognition criteria are applied to each of the separate units. Changes in the allocation of the sales price between delivered and undelivered elements can impact revenue recognition but do not change the total revenue recognized under any agreement.

Milestone Payments. Prior to the adoption of ASU No. 2010-17 on May 1, 2011, milestone payments were recognized as revenue upon the achievement of the specified milestone, provided that (i) the milestone event was substantive in nature and the achievement of the milestone was not reasonably assured at the inception of the agreement, (ii) the fees were non-refundable, and (iii) there was no continuing performance obligations associated with the milestone payment.

Effective May 1, 2011, we adopted on a prospective basis the Milestone Method under ASU No. 2010-17 for new licensing agreements or material modifications of existing licensing agreements entered into after May 1, 2011. Under the Milestone Method, we recognize consideration that is contingent upon the achievement of a milestone in its entirety as revenue in the period in which the milestone is achieved only if the milestone is substantive in its entirety. A milestone is considered substantive when it meets all of the following criteria:

| 1. | The consideration is commensurate with either the entity’s performance to achieve the milestone or the enhancement of the value of the delivered item(s) as a result of a specific outcome resulting from the entity’s performance to achieve the milestone; |

| 2. | The consideration relates solely to past performance; and |

| 3. | The consideration is reasonable relative to all of the deliverables and payment terms within the arrangement. |

A milestone is defined as an event (i) that can only be achieved based in whole or in part on either the entity’s performance or on the occurrence of a specific outcome resulting from the entity’s performance, (ii) for which there is substantive uncertainty at the date the arrangement is entered into that the event will be achieved and (iii) that would result in additional payments being due to the Company.

The provisions of ASU No. 2010-17 do not apply to contingent consideration for which payment is either contingent solely upon the passage of time or the result of a counterparty’s performance. We will assess the nature of, and appropriate accounting for, these payments on a case-by-case basis in accordance with the applicable authoritative guidance for revenue recognition.

Any amounts received prior to satisfying our revenue recognition criteria are recorded as deferred revenue in the accompanying interim unaudited condensed consolidated financial statements.

Fair Value Measurements

We determine fair value measurements in accordance with the authoritative guidance for fair value measurements and disclosures for all assets and liabilities within the scope of this guidance. This guidance, which among other things, defines fair value, establishes a consistent framework for measuring fair value and expands disclosure for each major asset and liability category measured at fair value on either a recurring or nonrecurring basis. Fair value is defined as the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date. The guidance prioritizes the inputs used in measuring fair value into the following hierarchy:

| 7 |

PEREGRINE PHARMACEUTICALS, INC.

NOTES

TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

FOR THE NINE MONTHS ENDED JANUARY 31, 2013 (unaudited) (continued)

| · | Level 1 – Quoted prices in active markets for identical assets or liabilities. |

| · | Level 2 – Observable inputs other than quoted prices included in Level 1, such as assets or liabilities whose values are based on quoted market prices in markets where trading occurs infrequently or whose values are based on quoted prices of instruments with similar attributes in active markets. |

| · | Level 3 – Unobservable inputs that are supported by little or no market activity and significant to the overall fair value measurement. |

As of January 31, 2013 and April 30, 2012, we do not have any Level 2 or Level 3 financial assets or liabilities and our cash and cash equivalents are carried at fair value based on quoted market prices for identical securities (Level 1 input).

Customer Deposits

Customer deposits primarily represent advance billings and/or payments received from Avid’s third-party customers prior to the initiation of contract manufacturing services.

Research and Development Expenses

Research and development costs are charged to expense when incurred in accordance with the authoritative guidance for research and development costs. Research and development expenses primarily include (i) payroll and related costs associated with research and development personnel, (ii) costs related to clinical and preclinical testing of our technologies under development, (iii) costs to develop and manufacture the product candidates, including raw materials and supplies, product testing, depreciation, and facility related expenses, (iv) expenses for research services provided by universities and contract laboratories, including sponsored research funding, and (v) other research and development expenses.

Accrued Clinical Trial and Related Fees

We accrue clinical trial and related fees based on work performed in connection with advancing our clinical trials, which relies on estimates and/or representations from clinical research organizations (“CRO”), hospitals, consultants, and other clinical trial related vendors. We maintain regular communication with our vendors, including our CRO vendors, and gauge the reasonableness of estimates provided. However, actual clinical trial costs may differ from estimated clinical trial costs and are adjusted for in the period in which they become known. There were no material adjustments for a change in estimate to research and development expenses in the accompanying interim unaudited condensed consolidated financial statements for the three and nine months ended January 31, 2013 and 2012.

Share-based Compensation

We account for stock options and other share-based awards granted under our equity compensation plans in accordance with the authoritative guidance for share-based compensation. The estimated fair value of share-based payments to employees in exchange for services is measured at the grant date, using a fair value based method, and is recognized as expense on a straight-line basis over the requisite service periods. Share-based compensation expense recognized during the period is based on the value of the portion of the share-based payment that is ultimately expected to vest during the period.

In addition, we periodically grant stock options and other share-based awards to non-employee consultants, which we account for in accordance with the authoritative guidance for share-based compensation. The cost of non-employee services received in exchange for share-based awards are measured based on either the fair value of the consideration received or the fair value of the share-based award issued, whichever is more reliably measurable. In addition, guidance requires share-based compensation related to unvested options and awards issued to non-employees to be recalculated at the end of each reporting period based upon the fair market value on that date until the share-based award has vested, and any adjustment to share-based compensation resulting from the remeasurement is recognized in the current period. See Note 9 for further discussion regarding share-based compensation.

Basic and Dilutive Net Loss Per Common Share

Basic net loss per common share is computed by dividing our net loss by the weighted average number of common shares outstanding during the period excluding the dilutive effects of stock options, common shares expected to be issued under our employee stock purchase plan, and warrants in accordance with the authoritative guidance. Diluted net loss per common share is computed by dividing the net loss by the sum of the weighted average number of common shares outstanding during the period plus the potential dilutive effects of stock options, common shares expected to be issued under our employee stock purchase plan, and warrants outstanding during the period calculated in accordance with the treasury stock method, but are excluded if their effect is anti-dilutive. Because the impact of options, awards and warrants are anti-dilutive during periods of net loss, there was no difference between basic and diluted loss per share amounts for the three and nine months ended January 31, 2013 and 2012.

| 8 |

PEREGRINE PHARMACEUTICALS, INC.

NOTES

TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

FOR THE NINE MONTHS ENDED JANUARY 31, 2013 (unaudited) (continued)

The calculation of weighted average diluted shares outstanding excludes the dilutive effect of outstanding stock options, common shares expected to be issued under our employee stock purchase plan, and warrants, to purchase up to an aggregate of 3,387,483 and 3,500,609 shares of common stock for the three months and nine months ended January 31, 2013, respectively, and 50,577 and 87,083 shares of common stock for the three and nine months ended January 31, 2012, respectively, since their impact are anti-dilutive during periods of net loss.

The calculation of weighted average diluted shares outstanding also excludes weighted average outstanding stock options and warrants to purchase up to an aggregate of 6,053,421 and 6,044,158 shares of common stock for the three and nine months ended January 31, 2013, respectively, and 5,971,867 and 6,046,536 shares of common stock for the three and nine months ended January 31, 2012, respectively, as their exercise prices were greater than the average market price of our common stock during the respective periods, resulting in an anti-dilutive effect.

Subsequent to January 31, 2013 and through March 12, 2013, we issued an aggregate of 3,333,556 shares of our common stock (Note 8), which are not included in the calculation of basic and dilutive net loss per common share for the three and nine months ended January 31, 2013.

| 4. | TRADE AND OTHER RECEIVABLES |

Trade and other receivables are recorded at the invoiced amount net of an allowance for doubtful accounts, if necessary. Trade and other receivables, net, consist of the following at January 31, 2013 and April 30, 2012:

| January 31, 2013 | April 30, 2012 | |||||||

| Trade receivables(1) | $ | 1,964,000 | $ | 2,264,000 | ||||

| Other receivables, net | 19,000 | 89,000 | ||||||

| Trade and other receivables, net | $ | 1,983,000 | $ | 2,353,000 | ||||

______________

| (1) | Represents amounts billed for contract manufacturing services provided by Avid. |

We continually monitor our allowance for doubtful accounts for all receivables. We apply judgment in assessing the ultimate realization of our receivables and we estimate an allowance for doubtful accounts based on various factors, such as, the aging of accounts receivable balances, historical experience, and the financial condition of our customers. Based on our analysis, an allowance for doubtful accounts amounted to $19,000 as of January 31, 2013 and April 30, 2012.

| 9 |

PEREGRINE PHARMACEUTICALS, INC.

NOTES

TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

FOR THE NINE MONTHS ENDED JANUARY 31, 2013 (unaudited) (continued)

| 5. | PROPERTY |

Property, net consists of the following at January 31, 2013 and April 30, 2012:

| January 31, 2013 | April 30, 2012 | |||||||

| Leasehold improvements | $ | 1,383,000 | $ | 1,383,000 | ||||

| Laboratory equipment | 5,339,000 | 4,967,000 | ||||||

| Furniture, fixtures, office equipment and software | 2,553,000 | 2,287,000 | ||||||

| 9,275,000 | 8,637,000 | |||||||

| Less accumulated depreciation and amortization | (6,492,000 | ) | (5,737,000 | ) | ||||

| Property, net | $ | 2,783,000 | $ | 2,900,000 | ||||

Depreciation and amortization expense for three and nine months ended January 31, 2013 was $280,000 and $806,000, respectively, and $238,000 and $664,000 for the three and nine months ended January 31, 2012, respectively.

| 6. | INVENTORIES |

Inventories are stated at the lower of cost or market and primarily include raw materials, direct labor and overhead costs (work-in-process) associated with our wholly-owned subsidiary, Avid. Cost is determined by the first-in, first-out method. Inventories consist of the following at January 31, 2013 and April 30, 2012:

| January 31, 2013 | April 30, 2012 | |||||||

| Raw materials, net | $ | 2,125,000 | $ | 1,966,000 | ||||

| Work-in-process | 2,510,000 | 1,645,000 | ||||||

| Total inventories, net | $ | 4,635,000 | $ | 3,611,000 | ||||

| 7. | NOTE PAYABLE |

On August 30, 2012, we entered into a loan and security agreement (the “Loan Agreement”) with Oxford Finance LLC, MidCap Financial SBIC LP, and Silicon Valley Bank (collectively, the “Lenders”) for up to $30,000,000 in total funding available in two $15,000,000 tranches. The Loan Agreement was secured by a first-priority security interest in substantially all of our assets, excluding our intellectual property and our rights under license agreements granting us rights to intellectual property. On August 30, 2012, we received initial funding of $15,000,000 under the Loan Agreement, excluding debt issuance costs of $251,000.

Subsequently, on September 24, 2012, we received a written notice of default (“Notice of Default”) from the Lenders, with respect to the Loan Agreement. The Notice of Default was triggered by a material adverse change under the Loan Agreement due to our discovery of major discrepancies in treatment group coding by an independent third-party vendor responsible for distribution of blinded investigational product used in our bavituximab Phase II second-line non-small cell lung cancer clinical trial. Pursuant to the terms of the Notice of Default, all amounts due under the Loan Agreement were declared immediately due and payable by the Lenders. On September 25, 2012, we paid the Lenders all obligations declared due and payable under the Loan Agreement, including outstanding principal of $15,000,000, accrued interest thereon at the Loan Agreement’s applicable fixed rate of 7.95% per annum, plus a final payment fee equal to 6.5% of the principal amount funded (or $975,000), upon which, the Loan Agreement was terminated.

In addition, under the Loan Agreement, we issued to the Lenders six-year warrants to purchase shares of our common stock upon the funding of each tranche in an amount equal to 4.50% of the amount of such tranche divided by the exercise price, which is the lower of the average closing price of our common stock for the 10 business days immediately prior to the funding date for such tranche or the closing price on the day prior to such funding date. Therefore, upon the initial funding under the Loan Agreement, we issued the Lenders warrants to purchase an aggregate of 273,280 shares of our common stock at a per share price of $2.47, which are exercisable on a cash or cashless basis, and will expire on August 30, 2018. The fair value of the warrants issued was $470,000 and was calculated using a Black-Scholes valuation model with the following assumptions: risk-free interest rate of 0.87%; expected volatility of 80.20%; expected term of six years; and a dividend yield of 0%. The fair value of the warrants issued was initially recorded as a debt discount with a corresponding increase to additional paid-in capital. As of January 31, 2013, the warrants issued under the Loan Agreement were outstanding and exercisable (Note 10).

| 10 |

PEREGRINE PHARMACEUTICALS, INC.

NOTES

TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

FOR THE NINE MONTHS ENDED JANUARY 31, 2013 (unaudited) (continued)

Upon the termination of the Loan Agreement, we recorded a loss on the early extinguishment of debt of $1,696,000, which consisted of the final payment fee of $975,000, the unamortized debt discount associated with the fair value of the warrants issued to the Lenders of $470,000, and the unamortized aggregate debt issuance costs of $251,000. The loss on the early extinguishment of debt is included in the accompanying interim unaudited condensed consolidated statements of operations and comprehensive loss for the nine months ended January 31, 2013.

| 8. | STOCKHOLDERS’ EQUITY |

December 2010 AMI Agreement.

On December 29, 2010, we entered into an At Market Sales Issuance Agreement (the “December 2010 AMI Agreement”) with McNicoll, Lewis & Vlak LLC (now known as MLV & Co. LLC, “MLV”), pursuant to which we may sell shares of our common stock at market prices through MLV, as agent, in registered transactions from the Company’s shelf registration statement on Form S-3 (File No. 333-171252) filed with the SEC on December 29, 2010, for aggregate gross proceeds of up to $75,000,000.

During the nine months ended January 31, 2013, we sold 31,662,214 shares of common stock at varying market prices under the December 2010 AMI Agreement for aggregate gross proceeds of $27,051,000 before deducting commissions and other issuance costs of $885,000. As of January 31, 2013, aggregate gross proceeds of up to $330,000 remained available under the December 2010 AMI Agreement.

Subsequent to January 31, 2013 and through March 12, 2013, we sold 201,154 shares of common stock at market prices under the December 2010 AMI Agreement for aggregate gross proceeds of $330,000. As of March 12, 2013, we had raised the full amount of gross proceeds available under the December 2010 AMI Agreement.

December 2012 AMI Agreement

On December 27, 2012, we entered into an At Market Sales Issuance Agreement (the “December 2012 AMI Agreement”) with MLV, pursuant to which we may sell shares of our common stock at market prices through MLV, as agent, for aggregate gross proceeds of up to $75,000,000, in registered transactions from the Company’s shelf registration statement on Form S-3 (File No. 333-180028), filed with the SEC on March 9, 2012. As of January 31, 2013, we had not sold any shares of common stock under the December 2012 AMI Agreement.

Subsequent to January 31, 2013 and through March 12, 2013, we sold 3,132,402 shares of common stock at market prices under the December 2012 AMI Agreement for aggregate gross proceeds of $4,475,000. As of March 12, 2013, aggregate gross proceeds of up to $70,525,000 remained available under the December 2012 AMI Agreement.

Shares of Common Stock Authorized And Reserved For Future Issuance

As of January 31, 2013, we had reserved 24,414,094 additional shares of our common stock, which may be issued under our equity compensation plans and outstanding warrant agreements, excluding shares of common stock that could potentially be issued under our current effective shelf registration statements, as further described in the following table:

| Number of Shares Reserved | ||||

| Common shares reserved for issuance under outstanding option grants and available for issuance under our stock incentive plans | 20,150,287 | |||

| Common shares reserved for and available for issuance under our Employee Stock Purchase Plan | 3,889,004 | |||

| Common shares issuable upon exercise of outstanding warrants | 374,803 | |||

| Total shares of common stock reserved for issuance | 24,414,094 | |||

| 11 |

PEREGRINE PHARMACEUTICALS, INC.

NOTES

TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

FOR THE NINE MONTHS ENDED JANUARY 31, 2013 (unaudited) (continued)

| 9. | EQUITY COMPENSATION PLANS |

Stock Incentive Plans

We currently maintain seven stock incentive plans referred to as the 2011 Plan, the 2010 Plan, the 2009 Plan, the 2005 Plan, the 2003 Plan, the 2002 Plan, and the 1996 Plan (collectively referred to as the “Stock Plans”). On October 18, 2012, our stockholders approved an amendment to our 2011 Plan to increase the number of shares of our common stock reserved for issuance from 3,500,000 to 11,500,000 shares.

As of January 31, 2013, we had an aggregate of 20,150,287 shares of common stock reserved for issuance under the Stock Plans, of which, 15,487,701 shares were subject to outstanding options and 4,662,586 shares were available for future grants of share-based awards.

The following summarizes our stock option transaction activity for the nine months ended January 31, 2013:

| Stock Options | Shares | Weighted Average Exercisable Price | ||||||

| Outstanding, May 1, 2012 | 7,531,651 | $ | 2.90 | |||||

| Granted | 8,556,862 | $ | 0.87 | |||||

| Exercised | (92,497 | ) | $ | 0.86 | ||||

| Canceled or expired | (508,315 | ) | $ | 1.70 | ||||

| Outstanding, January 31, 2013 | 15,487,701 | $ | 1.83 | |||||

Employee Stock Purchase Plan

We have reserved a total of 5,000,000 shares of common stock to be purchased under our 2010 Employee Stock Purchase Plan (the “2010 ESPP”), of which 3,889,004 shares of common stock remain available for purchase as of January 31, 2013. Under the 2010 ESPP, we will sell shares to participants at a price equal to the lesser of 85% of the fair market value of stock at the (i) beginning of a six-month offering period or (ii) at the end of the six-month offering period. The 2010 ESPP provides for two six-month offering periods each year; the first offering period will begin on the first trading day on or after each November 1; the second offering period will begin on the first trading day on or after each May 1. During the nine months ended January 31, 2013, 548,111 shares of common stock were purchased under the 2010 ESPP at a purchase price per share of $0.39.

Share-Based Compensation

Total share-based compensation expense for the three and nine-month periods ended January 31, 2013 and 2012 are included in the accompanying interim unaudited condensed consolidated statements of operations and comprehensive loss as follows:

| Three Months Ended January 31, | Nine Months Ended January 31, | |||||||||||||||

| 2013 | 2012 | 2013 | 2012 | |||||||||||||

| Cost of contract manufacturing | $ | 37,000 | $ | 5,000 | $ | 55,000 | $ | 10,000 | ||||||||

| Research and development | 539,000 | 299,000 | 1,151,000 | 920,000 | ||||||||||||

| Selling, general and administrative | 453,000 | 455,000 | 1,114,000 | 1,508,000 | ||||||||||||

| Total | $ | 1,029,000 | $ | 759,000 | $ | 2,320,000 | $ | 2,438,000 | ||||||||

| Share-based compensation from: | ||||||||||||||||

| Stock options | $ | 870,000 | $ | 720,000 | $ | 2,069,000 | $ | 2,356,000 | ||||||||

| Employee stock purchase plan | 159,000 | 39,000 | 251,000 | 82,000 | ||||||||||||

| $ | 1,029,000 | $ | 759,000 | $ | 2,320,000 | $ | 2,438,000 | |||||||||

As of January 31, 2013, the total estimated unrecognized compensation cost related to non-vested stock options was $6,045,000. This cost is expected to be recognized over a weighted average vesting period of 1.64 years based on current assumptions.

| 12 |

PEREGRINE PHARMACEUTICALS, INC.

NOTES

TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

FOR THE NINE MONTHS ENDED JANUARY 31, 2013 (unaudited) (continued)

| 10. | WARRANTS |

During the quarter ended January 31, 2013, 118,444 warrants were exercised on a cashless basis in exchange for 46,427 shares of our common stock. The warrants were issued in December 2008 in connection with a three-year term loan we entered into during fiscal year 2009.

As of January 31, 2013, the following warrants to purchase an aggregate of 374,803 shares of our common stock were outstanding:

| Date Issued | Warrants Outstanding | Exercise Price Per Share | Expiration Date | |||

| December 19, 2008 | 101,523 | $1.4775 | December 19, 2013 | |||

| August 30, 2012 (Note 7) | 273,280 | $2.4700 | August 30, 2018 | |||

| Total Warrants Outstanding | 374,803 |

| 11. | SEGMENT REPORTING |

Our business is organized into two reportable operating segments and both operate in the U.S. Peregrine is engaged in the research and development of monoclonal antibodies for the treatment and diagnosis of cancer. Avid is engaged in providing contract manufacturing services for Peregrine, and third-party customers on a fee-for-service basis.

The accounting policies of the operating segments are the same as those described in Note 3. We evaluate the performance of our contract manufacturing services segment based on gross profit or loss from third-party customers. However, our products in the research and development segment are not evaluated based on gross profit or loss, but rather based on scientific progress of the technologies. As such, gross profit or loss is only provided for our contract manufacturing services segment in the below table. All revenues shown below are derived from transactions with third-party customers.

Segment information for the three and nine-month periods is summarized as follows:

| Three Months Ended January 31, | Nine Months Ended January 31, | |||||||||||||||

| 2013 | 2012 | 2013 | 2012 | |||||||||||||

| Contract manufacturing services revenue | $ | 6,961,000 | $ | 3,203,000 | $ | 17,157,000 | $ | 12,796,000 | ||||||||

| Cost of contract manufacturing services | 3,651,000 | 2,484,000 | 9,378,000 | 9,219,000 | ||||||||||||

| Gross profit | 3,310,000 | 719,000 | 7,779,000 | 3,577,000 | ||||||||||||

| Revenue from products in research and development | 78,000 | 78,000 | 272,000 | 372,000 | ||||||||||||

| Research and development expense | (5,437,000 | ) | (9,180,000 | ) | (18,471,000 | ) | (26,758,000 | ) | ||||||||

| Selling, general and administrative expense | (3,112,000 | ) | (2,710,000 | ) | (9,469,000 | ) | (8,371,000 | ) | ||||||||

| Other income (expense), net | 247,000 | 3,000 | 254,000 | (57,000 | ) | |||||||||||

| Loss on early extinguishment of debt | – | – | (1,696,000 | ) | – | |||||||||||

| Net loss | $ | (4,914,000 | ) | $ | (11,090,000 | ) | $ | (21,331,000 | ) | $ | (31,237,000 | ) | ||||

| 13 |

PEREGRINE PHARMACEUTICALS, INC.

NOTES

TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

FOR THE NINE MONTHS ENDED JANUARY 31, 2013 (unaudited) (continued)

Revenues generated from our contract manufacturing services segment were derived from a limited number of customers. The percentages below represent revenue derived from each customer as a percentage of total contract manufacturing services revenue:

| Three Months Ended January 31, | Nine Months Ended January 31, | |||||||||||||||

| 2013 | 2012 | 2013 | 2012 | |||||||||||||

| United States (customer A) | 60% | 58% | 78% | 36% | ||||||||||||

| United States (customer B) | 37 | – | 20 | – | ||||||||||||

| United States (customer C) | – | 31 | – | 8 | ||||||||||||

| Germany (one customer) | – | 5 | – | 20 | ||||||||||||

| Denmark (one customer) | – | 4 | – | 28 | ||||||||||||

| Other customers | 3 | 2 | 2 | 8 | ||||||||||||

| Total | 100% | 100% | 100% | 100% | ||||||||||||

Revenue generated from our products in our research and development segment during the three and nine months ended January 31, 2013 and 2012, is directly related to license revenue recognized under licensing agreements with unrelated entities.

| 12. | COMMITMENTS AND CONTINGENCIES |

In the ordinary course of business, we are at times subject to various legal proceedings and disputes. Except as set forth below, we currently are not aware of any material litigation or other dispute nor, to management’s knowledge, is any litigation or other proceeding threatened against us that collectively is expected to have a material adverse effect on our consolidated cash flows, financial condition or results of operations.

Securities Related Class Action Lawsuits

On September 28, 2012, three complaints were filed in the U.S. District Court for the Central District of California (the “Court”) against us and certain of our executive officers and one consultant (collectively, the “Individual Defendants”) on behalf of certain purchasers of our common stock. The complaints have been brought as purported stockholder class actions, and, in general, include allegations that we and the Individual Defendants violated (i) Section 10(b) of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), and Rule 10b-5 promulgated thereunder and (ii) Section 20(a) of the Exchange Act, by making materially false and misleading statements regarding the interim median overall survival results of our bavituximab Phase II second-line non-small cell lung cancer trial, thereby artificially inflating the price of our common stock. The plaintiffs are seeking unspecified monetary damages and other relief. On November 27, 2012, four prospective lead plaintiffs filed motions to consolidate, appoint a lead plaintiff, and appoint lead counsel. On February 5, 2013, the court appointed James T. Fahey as lead plaintiff in the action. The lead plaintiff has until April 8, 2013 to file an amended consolidated complaint against us. We believe that the various shareholder lawsuits are without merit, and we intend to vigorously defend the various actions and to seek dismissal of these complaints. Due to the early stage of these proceedings, we believe that the probability of an unfavorable outcome or loss related to these proceedings and an estimate of the amount or range of loss related to these claims, if any, from an unfavorable outcome are not determinable at this time.

Other Legal Matters

On September 24, 2012, we filed a lawsuit against Clinical Supplies Management, Inc. (“CSM”), in the U.S. District Court for the Central District of California (the “Court”). We had contracted with CSM in 2010 as our third-party vendor responsible for distribution of the blinded investigational product used in our bavituximab Phase II second-line non-small cell lung cancer trial. As part of the routine collection of data in advance of an end-of-Phase II meeting with regulatory authorities, we discovered major discrepancies between some patient sample test results and patient treatment code assignments. Consequently, we filed this lawsuit against CSM alleging breach of contract, negligence and negligence per se arising from CSM’s performance of its contracted services. We are seeking monetary damages. On March 7, 2013, we and CSM submitted to the Court a proposed stipulation pursuant to which the lawsuit would be stayed for up to 120 days during which time we and CSM would participate in an alternative dispute resolution process, pursuant to our contract with CSM. The proposed stipulation was approved by the Court on March 8, 2013.

| 14 |

| Item 2. | Management’s Discussion and Analysis of Financial Condition And Results of Operations. |

This Quarterly Report on Form 10-Q contains “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended, which represent our projections, estimates, expectations or beliefs concerning among other things, financial items that relate to management’s future plans or objectives or to our future economic and financial performance. In some cases, you can identify these statements by terminology such as “may”, “should”, “plans”, “believe”, “will”, “anticipate”, “estimate”, “expect” “project”, or “intend”, including their opposites or similar phrases or expressions. You should be aware that these statements are projections or estimates as to future events and are subject to a number of factors that may tend to influence the accuracy of the statements. These forward-looking statements should not be regarded as a representation by the Company or any other person that the events or plans of the Company will be achieved. You should not unduly rely on these forward-looking statements, which speak only as of the date of this Quarterly Report. We undertake no obligation to publicly revise any forward-looking statement to reflect circumstances or events after the date of this Quarterly Report or to reflect the occurrence of unanticipated events. You should, however, review the factors and risks we describe in the reports we file from time to time with the Securities and Exchange Commission (“SEC”) after the date of this Quarterly Report. Actual results may differ materially from any forward-looking statement.

Overview

We are a biopharmaceutical company developing first-in-class monoclonal antibodies focused on the treatment and diagnosis of cancer. We are advancing two oncology programs with our lead product candidates, bavituximab and Cotara, for the treatment of various cancers. In addition, we are advancing our lead imaging agent, 124I-PGN650, in an exploratory clinical trial for the imaging of multiple solid tumor types.

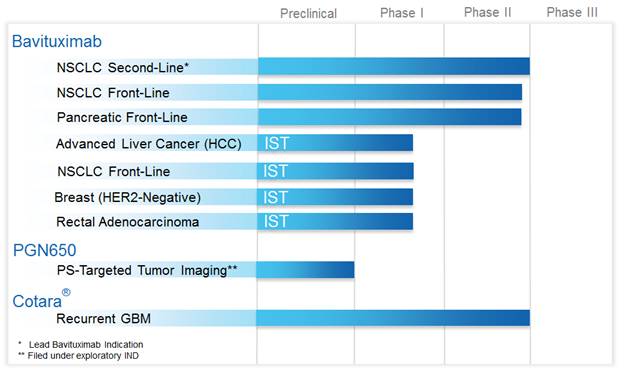

The following product pipeline reflects our current clinical trials focused on oncology, as further discussed below:

| 15 |

Bavituximab for the Treatment of Solid Tumors

Bavituximab is our lead phosphatidylserine (“PS”)-targeting antibody that has demonstrated broad therapeutic potential in combination with chemotherapy across multiple oncology indications and represents a new approach to treating cancer. PS is a highly immunosuppressive molecule usually located inside the membrane surface of healthy cells, but “flips” and becomes exposed on the outside of cells that line tumor blood vessels, creating a specific target for anti-cancer treatments. PS-targeting antibodies target and bind to PS and block this immunosuppressive signal, thereby enabling the immune system to recognize and fight the tumor.

As reflected in the above product pipeline, bavituximab’s therapeutic potential is currently being evaluated in three company-sponsored Phase II randomized trials in second-line non-small cell lung cancer (“NSCLC”), front-line NSCLC, and front-line pancreatic cancer, as well as in several investigator-sponsored trials (“IST”) in additional oncology indications. The following represents the current status of each of these clinical trials:

Phase IIb Trial – Bavituximab Plus Docetaxel in Second-Line NSCLC

We conducted a randomized, double-blind, placebo-controlled Phase IIb second-line NSCLC trial evaluating two dose levels of bavituximab plus docetaxel (“bavituximab-containing arms”) versus docetaxel plus placebo (“control arm”) as second-line treatment in 121 patients with Stage IIIb or Stage IV NSCLC. The trial was designed to evaluate overall response rate (“ORR”) measured in accordance with Response Evaluation Criteria In Solid Tumors (“RECIST”) criteria, progression-free survival (“PFS”), duration of response, overall survival (“OS”), and safety.

On September 24, 2012, we announced that during the course of preparing for an end-of-Phase II meeting with regulatory authorities and following the data announcement on September 7, 2012 from this Phase IIb trial, we discovered major discrepancies between some patient sample test results and patient treatment code assignments. As a result of these discrepancies, the data that we disclosed on or before September 7, 2012 should not be relied upon.

Upon discovery of the discrepancies, we initiated an internal review of this Phase IIb trial, which included the testing of investigational product, patient samples, reviewing the operations of multiple vendors, among other activities. The initial results of this internal review were announced on January 7, 2013 and indicated that discrepancies were isolated to the control arm and 1mg/kg bavituximab-containing treatment arms of the trial and that there was no evidence of discrepancies in the 3mg/kg bavituximab-containing treatment arm of the trial. Based on the results of our internal review, we took a conservative approach toward analyzing the results from the trial, which included combining the control arm and 1mg/kg bavituximab-containing arm into one treatment arm (“combined control arm”), and comparing those results to the 3mg/kg bavituximab-containing treatment arm.

On February 19, 2013, we reported updated top-line data from this trial based upon the completion of the aforementioned internal review of discrepancies in the trial and updated patient survival data from the trial. Updated top-line data from this Phase IIb trial indicate a meaningful improvement in median OS of 11.7 months in the 3mg/kg bavituximab-containing arm compared to 7.3 months in the combined control arm. In addition, these results also demonstrated that bavituximab was well-tolerated with no significant differences in adverse events between the trial arms. We believe these updated top-line data support advancing the 3mg/kg bavituximab dose into Phase III development in second-line NSCLC, and therefore, we are actively preparing for an end-of-Phase II meeting with the United States Food and Drug Administration (“FDA”) which we planning to have by the end of the first half of calendar year 2013.

Phase IIb Trial – Bavituximab Plus Paclitaxel/Carboplatin in Front-Line NSCLC

Our randomized Phase II trial is designed to evaluate bavituximab plus carboplatin and paclitaxel versus carboplatin and paclitaxel alone as front-line therapy in 86 patients with Stage IIIb or Stage IV NSCLC. In March 2012, we announced top-line ORR, a primary endpoint, and current median PFS, a secondary endpoint, from this trial from 83 evaluable patients. Initial ORR and median PFS data from this study were deemed inconclusive and therefore, we believe median OS, another secondary endpoint, will be an important data point from this study and instrumental in determining our next steps in advancing bavituximab in front-line NSCLC in combination with carboplatin and paclitaxel. We anticipate announcing median OS from this trial in the first half of calendar year 2013.

| 16 |

Phase II Trial – Bavituximab Plus Gemcitabine in Pancreatic Cancer

In June 2012, we announced the completion of patient enrollment in our Phase II randomized trial evaluating bavituximab in combination with gemcitabine versus gemcitabine alone in 70 patients with previously untreated pancreatic cancer patients. The primary endpoint from this trial is median OS and the secondary endpoints are ORR and median PFS. On February 13, 2013, we announced top-line results from this trial showing that the combination of bavituximab and gemcitabine resulted in more than a doubling of ORR and an improvement in OS when compared to gemcitabine alone (“control arm”). In the trial, patients treated with a combination of bavituximab and gemcitabine had a 28% tumor response rate as compared to 13% in the control arm. In addition, we saw a modest improvement in median OS, the primary endpoint of the trial, which was 5.6 months for the bavituximab plus gemcitabine arm and 5.2 months for the control arm.

Based on these data, as well as other recent developments in the treatment of pancreatic cancer, we are actively evaluating the next steps for advancing our bavituximab pancreatic program.

Investigator-Sponsored Trials (“IST”)

With respect to our ISTs, our clinical collaborators are evaluating bavituximab with additional drug combinations and additional oncology indications. Enrollment is ongoing in each of the following ISTs:

| (i) | a Phase I/II trial evaluating bavituximab combined with sorafenib in patients with advanced hepatocellular carcinoma (“HCC”), or liver cancer; |

| (ii) | a Phase Ib trial evaluating bavituximab combined with pemetrexed and carboplatin in patients with front-line NSCLC; |

| (iii) | a Phase I trial evaluating bavituximab combined with paclitaxel in patients with HER2-negative metastatic breast cancer; and |

| (iv) | a Phase I trial evaluating bavituximab combined with capecitabine and radiation in patients with stage II or III rectal adenocarcinoma. |

In addition, we periodically evaluate our IST program based on a number of factors, including enrollment and changes in the standard of care of patients for each of our ongoing IST’s. As a result of our recent evaluation, during March 2013, we discontinued a Phase I/II IST evaluating bavituximab combined with cabazitaxel in patients with second-line castration resistant prostate cancer due to slow enrollment in the trial which we believe will continue due to two new oral drugs that had been approved for the same indication following the inception of this IST. We will continue to monitor our IST program as we look to evaluate new indications and combinations based on the broad therapeutic potential of bavituximab.

PS-Targeting Molecular Imaging Program (PGN650)

In addition to bavituximab’s therapeutic potential to treat multiple solid tumors, we believe these PS-targeting antibodies may have broad potential for the imaging and diagnosis of multiple diseases, including cancer. In April 2012, we filed an exploratory Investigational New Drug Application with the FDA to advance our lead molecular imaging agent, 124I-PGN650 (“PGN650”), into clinical development for the imaging of multiple solid tumor types. Our initial goal for the PGN650 program is to further validate the broad nature of the PS-targeting platform. The current trial will enroll up to 12 patients and results from this study may provide new insight into new indications and potential applications, including development of antibody drug conjugates, the ability of PGN650 to monitor the effectiveness of current standard cancer treatments, and the ability to potentially select patients that may benefit from bavituximab-based treatment.

Cotara for the Treatment of Brain Cancer

Cotara is a monoclonal antibody linked to a radioisotope that is administered as a single one-time infusion, directly into the tumor, destroying the tumor from the inside out, with minimal exposure to healthy tissue. In calendar year 2011, we reported what we believe to be promising median OS of 9.3 months in patients with glioblastoma multiforme (“GBM”) at first relapse following a single dose of Cotara in a Phase II clinical trial. Based on these data and data from earlier clinical studies, we have reached an agreement with the FDA on the design of a single pivotal trial to potentially support product registration for Cotara in the treatment of recurrent GBM. We are actively seeking potential partners as we look to further advance Cotara into Phase III development. Cotara has been granted orphan drug status and fast track designation for the treatment of GBM and anaplastic astrocytoma by the FDA.

Integrated Biomanufacturing Subsidiary

In addition to our clinical research and development efforts, we operate a wholly-owned cGMP (current Good Manufacturing Practices) contract manufacturing subsidiary, Avid Bioservices, Inc. (“Avid”). Avid is a Contract Manufacturing Organization that provides fully integrated services from cell line development to commercial cGMP biomanufacturing for Peregrine and Avid’s third-party clients. In addition to generating revenue from providing a broad range of biomanufacturing services to third-party clients, Avid is strategically integrated with Peregrine to manufacture all clinical products to support our clinical trials while also preparing for Phase III and potential commercial launch.

| 17 |

Going Concern

Our interim unaudited condensed consolidated financial statements have been prepared on a going concern basis, which contemplates the realization of assets and the satisfaction of liabilities in the normal course of business. The financial statements do not include any adjustments relating to the recoverability of the recorded assets or the classification of liabilities that may be necessary should it be determined that we are unable to continue as a going concern.

At January 31, 2013, we had $26,255,000 in cash and cash equivalents. We have expended substantial funds on the research and development of our product candidates, and funding the operations of Avid. As a result, we have historically experienced negative cash flows from operations since our inception and we expect the negative cash flows from operations to continue for the foreseeable future. Our net loss incurred during the nine-month period ended January 31, 2013 amounted to $21,331,000 and our net losses incurred during the past three fiscal years ended April 30, 2012, 2011 and 2010, amounted to $42,119,000, $34,151,000, and $14,494,000, respectively. Therefore, unless and until we are able to generate sufficient revenues from Avid’s contract manufacturing services and/or from the sale and/or licensing of our products under development, we expect such losses to continue for the foreseeable future.

Therefore, our ability to continue to fund our clinical trials and development efforts is highly dependent on the amount of cash and cash equivalents on hand combined with our ability to raise additional capital to support our future operations through one or more methods, including but not limited to, issuing additional equity or debt.

Historically, we have funded a significant portion of our operations through the issuance of equity. During the nine months ended January 31, 2013, we raised $27,051,000 in gross proceeds under an At Market Sales Issuance Agreement, of which $25,555,000 was raised subsequent to September 25, 2012, primarily to replace the $15,000,000 of initial funding we repaid on September 25, 2012 under an earlier loan facility we entered into on August 30, 2012. Subsequent to January 31, 2013 and through March 12, 2013, we raised an additional $4,805,000 in aggregate gross proceeds under two separate At Market Sales Issuance Agreements.

With respect to our ability to raise additional capital from the issuance of equity, as of March 12, 2013, we have an effective shelf registration statement on Form S-3, under which we may issue, from time to time, in one or more offerings, shares of our common stock for gross proceeds of up to $145,525,000. However, our ability to raise additional capital in the equity markets is dependent on a number of factors, including, but not limited to, the market demand for our common stock. The market demand or liquidity of our common stock is subject to a number of risks and uncertainties, including but not limited to, negative economic conditions, adverse market conditions, adverse clinical trials results, and significant delays in one or more clinical trials. If our ability to access the capital markets becomes severely restricted, it could have a negative impact on our business plans, including our clinical trial programs and other research and development activities. In addition, even if we are able to raise additional capital, it may not be at a price or on terms that are favorable to us.

In addition to financing our operations through the issuance of equity, we may also secure additional funding through the issuance of debt, licensing or partnering our products in development, or increasing revenue from our wholly-owned subsidiary, Avid. While we will continue to explore these potential opportunities, there can be no assurances that we will be successful in securing debt financing, licensing or partnering our products in development, or generating additional revenue from Avid to complete the research, development, and clinical testing of our product candidates.

Based on our current projections, which include projected cash inflows under signed contracts with existing customers of Avid, assuming we raise no additional capital from the capital markets or other potential sources, and excluding any third-party Phase III development costs, we believe we will have sufficient cash on hand to meet our obligations as they become due through at least the third quarter of our fiscal year 2014 ending January 31, 2014. There are a number of uncertainties associated with our financial projections, including but not limited to, termination of third party contracts, technical challenges, and regulatory decisions affecting bavituximab, any of which could reduce, delay or accelerate our future projected cash inflows and outflows. In addition, in the event our projected cash-inflows are reduced or delayed we might not have sufficient capital to operate our business beyond the third quarter of our fiscal year 2014. The uncertainties surrounding our future cash inflows have raised substantial doubt regarding our ability to continue as a going concern.

| 18 |

Results of Operations

The following table compares the interim unaudited condensed consolidated statements of operations for the three and nine-month periods ended January 31, 2013 and 2012. This table provides you with an overview of the changes in the condensed consolidated statements of operations for the comparative periods, which are further discussed below.

| Three Months Ended January 31, | Nine Months Ended January 31, | |||||||||||||||||||||||

| 2013 | 2012 | $ Change | 2013 | 2012 | $ Change | |||||||||||||||||||

| REVENUES: | ||||||||||||||||||||||||

| Contract manufacturing revenue | $ | 6,961,000 | $ | 3,203,000 | $ | 3,758,000 | $ | 17,157,000 | $ | 12,796,000 | $ | 4,361,000 | ||||||||||||

| License revenue | 78,000 | 78,000 | – | 272,000 | 372,000 | (100,000 | ) | |||||||||||||||||

| Total revenues | 7,039,000 | 3,281,000 | 3,758,000 | 17,429,000 | 13,168,000 | 4,261,000 | ||||||||||||||||||

| COSTS AND EXPENSES: | ||||||||||||||||||||||||

| Cost of contract manufacturing | 3,651,000 | 2,484,000 | 1,167,000 | 9,378,000 | 9,219,000 | 159,000 | ||||||||||||||||||

| Research and development | 5,437,000 | 9,180,000 | (3,743,000 | ) | 18,471,000 | 26,758,000 | (8,287,000 | ) | ||||||||||||||||

| Selling, general & administrative | 3,112,000 | 2,710,000 | 402,000 | 9,469,000 | 8,371,000 | 1,098,000 | ||||||||||||||||||

| Total costs and expenses | 12,200,000 | 14,374,000 | (2,174,000 | ) | 37,318,000 | 44,348,000 | (7,030,000 | ) | ||||||||||||||||

| LOSS FROM OPERATIONS | (5,161,000 | ) | (11,093,000 | ) | 5,932,000 | (19,889,000 | ) | (31,180,000 | ) | 11,291,000 | ||||||||||||||

| OTHER INCOME (EXPENSE): | ||||||||||||||||||||||||

| Interest and other income | 255,000 | 9,000 | 246,000 | 307,000 | 31,000 | 276,000 | ||||||||||||||||||

| Interest and other expense | (8,000 | ) | (6,000 | ) | (2,000 | ) | (53,000 | ) | (88,000 | ) | 35,000 | |||||||||||||

| Loss on the early extinguishment of debt | – | – | – | (1,696,000 | ) | – | (1,696,000 | ) | ||||||||||||||||

| NET LOSS | $ | (4,914,000 | ) | $ | (11,090,000 | ) | $ | 6,176,000 | $ | (21,331,000 | ) | $ | (31,237,000 | ) | $ | 9,906,000 | ||||||||

Results of operations for interim periods covered by this quarterly report on Form 10-Q may not necessarily be indicative of results of operations for the full fiscal year.

Total Revenues