UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

____________________________________________________________________

FORM 10-K

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF

THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended June 26, 2013 | Commission File No. 1-10275 | |

____________________________________________________________________

BRINKER INTERNATIONAL, INC.

(Exact name of registrant as specified in its charter)

DELAWARE | 75-1914582 | |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |

6820 LBJ Freeway, Dallas, Texas | 75240 | |

(Address of principal executive offices) | (Zip Code) | |

(972) 980-9917 | ||

(Registrant’s telephone number, including area code) | ||

Securities registered pursuant to Section 12(b) of the Act:

Title of Each Class

Common Stock, $0.10 par value

Securities registered pursuant to Section 12(g) of the Act: None

____________________________________________________________________

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes x No o

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No x

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No o

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (229.405 of this chapter) is not contained herein, and will not be contained, to the best of the registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See definition of “accelerated filer” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer | x | Accelerated filer | o | |

Non-accelerated filer | o | (Do not check if a smaller reporting company) | Smaller reporting company | o |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes o No x

State the aggregate market value of the voting and non-voting common equity held by non-affiliates computed by reference to the price at which the common equity was last sold, or the average bid and asked price of such common equity, as of the last business day of the registrant’s most recently completed second fiscal quarter. $1,999,440,915.

Indicate the number of shares outstanding of each of the registrant’s classes of common stock, as of the latest practicable date.

Class | Outstanding at August 12, 2013 |

Common Stock, $0.10 par value | 66,224,836 shares |

DOCUMENTS INCORPORATED BY REFERENCE

We have incorporated portions of our Annual Report to Shareholders for the fiscal year ended June 26, 2013 into Part II hereof, to the extent indicated herein. We have also incorporated by reference portions of our Proxy Statement for our annual meeting of shareholders on November 7, 2013, to be dated on or about September 17, 2013, into Part III hereof, to the extent indicated herein.

PART I

Item 1. | BUSINESS. |

General

References to “Brinker,” “the Company,” “we,” “us,” and “our” in this Form 10-K are references to Brinker International, Inc. and its subsidiaries and any predecessor companies of Brinker International, Inc.

We own, develop, operate and franchise the Chili’s Grill & Bar (“Chili’s”) and Maggiano’s Little Italy (“Maggiano’s”) restaurant brands. The Company was organized under the laws of the State of Delaware in September 1983 to succeed to the business operated by Chili’s, Inc., a Texas corporation, which was organized in August 1977. We completed the acquisition of Maggiano’s in August 1995.

Restaurant Brands

Chili’s Grill & Bar

Chili’s, a recognized leader in the Bar & Grill category of casual dining, has been operating restaurants for 38 years. Chili’s also enjoys a global presence with locations in 32 foreign countries and two U.S. territories around the world. Consistent in all locations, whether domestic or international and company-owned or franchised, Chili’s passion is making our guests feel special. Our Team Members, referred to as ChiliHeads, take special pride in proudly serving America’s Favorites Like No Place Else.

Chili’s varied menu features America’s favorites boldly flavored and freshly prepared, including several signature items such as Baby Back Ribs smoked in-house, Big Mouth Burgers, Sizzling Fajitas, hand-battered Chicken Crispers and house-made Chips and Salsa. Chili's has also introduced new pizzas and flatbreads. The all-day menu offers our guests a generous selection of appetizers, entrees and desserts at affordable prices. A special lunch section is available on weekdays. In addition to our flavorful food options, Chili’s offers a full selection of alcoholic beverages available from the bar, with Margaritas and draft beer being favorites of our guests. For guests seeking convenience, Chili’s offers To Go service that can be ordered by calling the restaurant or on-line or via mobile app, and most Chili’s offer a separate To Go entrance for service.

During the year ending June 26, 2013, at our company-owned restaurants, entrée selections ranged in menu price from $6.00 to $17.69. The average revenue per meal, including alcoholic beverages, was approximately $13.99 per person. During this same year, food and non-alcoholic beverage sales constituted approximately 86.1% of Chili’s total restaurant revenues, with alcoholic beverage sales accounting for the remaining 13.9%. Our average annual sales volume per Chili’s restaurant during this same year was $3.0 million.

Maggiano’s Little Italy

Maggiano’s is a full-service, national, casual dining Italian restaurant brand with a passion for making people feel special. The exterior of each Maggiano’s restaurant varies to reflect local architecture; however, the interior of all locations transport our guests back to a classic Italian-American restaurant in the style of New York’s Little Italy in the 1940s. Our Maggiano’s restaurants feature individual and family-style menus, and our restaurants also have extensive banquet facilities designed to host large party business or social events. We have a full lunch and dinner menu offering chef-prepared, classic Italian-American fare in the form of appetizers, entrées with bountiful portions of pasta, chicken, seafood, veal and prime steaks, and desserts. Our Maggiano’s restaurants also offer a full range of alcoholic beverages, including a selection of Handcrafted Classic Cocktails and premium wines. In addition, Maggiano’s offers a full carryout menu as well as local delivery services.

During the year ending June 26, 2013, entrée selections ranged in menu price from $12.95 to $42.50. The average revenue per meal, including alcoholic beverages, was approximately $26.72 per person. During this same year, food and non-alcoholic beverage sales constituted approximately 83.0% of Maggiano’s total restaurant revenues, with alcoholic beverage sales accounting for the remaining 17.0%. Sales from events at our banquet facilities made up 19.4% of our total restaurant revenues for the year. Our average annual sales volume per Maggiano’s restaurant during this same year was $8.81 million.

2

Business Strategy

We are committed to strategies and initiatives that are centered on long-term sales and profit growth, enhancing the guest experience and team member engagement. These strategies are intended to differentiate our brands from the competition, reduce the costs associated with managing our restaurants allowing us to reinvest back into the guest experience and value proposition, and establish a strong presence for our brands in key markets around the world. We will continue to maintain a strong balance sheet and financial flexibility to support our strategic initiatives and to provide stability in all operating environments.

Overall economic growth continues to be tepid providing a challenging operating environment for the casual dining industry as a whole. Growth in key economic factors such as total employment, consumer confidence and personal disposable income levels has been slight this year suggesting consumers remain cautious as the economy slowly rebounds. Consumer optimism now appears focused more on housing and large purchases such as cars in light of continued low interest rates. We anticipate market conditions will continue to challenge the industry; however, we believe our strategies and initiatives will provide a solid foundation for earnings growth going forward and are appropriate for all operating conditions.

Our current initiatives are designed to drive profitable sales growth and improve the guest experience in our restaurants. We are investing in new kitchen equipment, operations software and remodel initiatives as the core pieces of our current strategy. We have now completed the installation of new kitchen equipment in both our company-owned Chili's restaurants and our domestic franchise restaurants. We anticipate that the upgraded equipment will consistently provide a high quality product at a faster pace, enhancing both profitability and guest satisfaction. Based on our robust testing process, we believe the usability and efficiency of the equipment results in significant labor savings over time. Also, the flexibility of our equipment allows for the development of new menu categories that we believe results in increased sales and guest traffic.

All company-owned Chili's restaurants are now operating with an integrated point of sale and back office software system that was designed to enhance the efficiency of our restaurant operations and reporting capabilities. Timely and more detailed reporting in our restaurants will result in improved inventory and labor management while reducing software maintenance costs. Additionally, our management team will have timely visibility into operating performance and trends which will enhance decision making and improve profitability. We expect to complete the system installation in Maggiano's restaurants by the end of the calendar year.

We have remodeled a significant number of our company-owned Chili's restaurants and plan to continue the initiative at a brisk pace. The remodel design in intended to revitalize Chili's in a way which enhances the relevance of the brand and raises guest expectations regarding the quality of the experience. The design is contemporary while staying true to the Chili's brand heritage. We believe that these updates will positively impact the guest perception of the restaurant in both the dining room and bar areas and provide a long-term positive impact to traffic and sales.

We continually evaluate our menu at Chili's to improve quality, freshness and value by introducing new items and improving existing favorites. This year, Chili's has introduced new menu innovations including several pizza and flatbread choices and lighter entree selections like Mango Chile Chicken and Mango Chile Tilapia. The dessert and appetizer sections of the menu have also been enhanced with a new freshly baked skillet cookie, soft pretzel sticks and sweet potato fries. Our two for twenty dollars and lunch combo offerings have been refreshed with new menu items including pizzas, flatbreads and Southwestern Mac 'n' Cheese with Grilled Chicken. Our new steak selection introduced last year also continues to have a high guest preference and has been enhanced with steak topper add-ons. An emphasis on new products, training and our reimaged bar also resulted in improved bar sales over last year. We believe these changes as well as our ability to develop new and innovative items will further enhance sales and drive incremental traffic. We are committed to offering a compelling everyday menu that provides items our guests prefer at a solid value.

Improvements at Chili’s are expected to have the most significant impact on the business; however, our results are also expected to benefit through additional contributions from Maggiano’s and our global business. Maggiano’s sales trends and traffic continue to improve, driven by offering guests a great value with Classic Pastas, Marco’s Meal offering, new food and beverage options and direct marketing. Additionally, Maggiano’s has implemented initiatives around kitchen efficiency and inventory control contributing to increased financial results. We believe our authentic Italian-American cuisine and signature drinks, improved service and updated atmospheres will result in stronger brands and sustainable sales and profit growth through increased guest loyalty and traffic.

Global expansion allows further diversification which will enable us to build strength in a variety of markets and economic conditions. This expansion will come through acquisitions, franchise relationships, joint venture arrangements and equity investments, taking advantage of demographic and food trends that will accelerate in the international market over the next decade. Our growing percentage of franchise operations, both domestically and internationally, allow us to improve margins as royalty payments impact the bottom line.

3

The casual dining industry is a competitive business which is sensitive to changes in economic conditions, trends in lifestyles and fluctuating costs. Our priority remains increasing profitable growth over time in all operating environments. We have designed both operational and financial strategies to achieve this goal and in our opinion, improve shareholder value. Success with our initiatives to improve sales trends and operational effectiveness will enhance the profitability of our restaurants and strengthen our competitive position. The effective execution of our financial strategies, including repurchasing shares of our common stock, payment of quarterly dividends, disciplined use of capital and efficient management of operating expenses, will increase our profitability and return value to our shareholders. We remain confident in the financial health of our company, the long-term prospects of the industry as well as our ability to perform effectively in a competitive marketplace and a variety of economic environments.

Company Development

In fulfilling our long-term vision, over the past fiscal year we continued the expansion of our restaurant brands domestically through new company-owned restaurants and the development of a select number of company-owned restaurants in strategically desirable markets. We will concentrate on the development of certain identified markets to achieve the necessary levels to improve our competitive position, marketing potential, profitability and return on invested capital. Our domestic expansion efforts focus not only on major metropolitan areas in the United States but also on smaller market areas and non-traditional locations (such as airports and universities) that can adequately support our restaurant brands.

The restaurant site selection process is critical and we devote significant effort to the investigation of new locations utilizing a variety of sophisticated analytical techniques. Our process evaluates a variety of factors, including: trade area demographics, such as target population density and household income levels, physical site characteristics, such as visibility, accessibility and traffic volume; relative proximity to activity centers, such as shopping centers, hotel and entertainment complexes and office buildings; supply and demand trends, such as proposed infrastructure improvements, new developments and existing and potential competition. Members of each brand’s executive team inspect, review and approve each restaurant site prior to its acquisition for that brand.

The specific rate at which we are able to open new restaurants is determined, in part, by our success in locating satisfactory sites, negotiating acceptable lease or purchase terms, securing appropriate local governmental permits and approvals, and by our capacity to supervise construction and recruit and train management and hourly team members.

The following table illustrates the system-wide restaurants opened in fiscal 2013 and the planned openings in fiscal 2014:

Fiscal 2013 Openings(1) | Fiscal 2014 Projected Openings(1) | ||||

Chili’s: | |||||

Company-owned | 3 | 11-12 | |||

Franchise(2) | 2 | 4-6 | |||

Maggiano’s | — | 2-3 | |||

International: | |||||

Company-owned(3) | — | 2 | |||

Franchise(3) | 33 | 31-35 | |||

Total | 38 | 50-58 | |||

____________________________________________________________________

(1) | The numbers in this column are the total of new restaurant openings and openings of relocated restaurants during fiscal 2013. |

(2) | The numbers on this line for fiscal 2014 are projected domestic franchise openings. |

(3) | The numbers on this line are for Chili’s. |

4

We periodically re-evaluate company-owned restaurant sites to ensure attributes have not deteriorated below our minimum standards. In the event site deterioration occurs, each brand makes a concerted effort to improve the restaurant’s performance by providing physical, operating and marketing enhancements unique to each restaurant’s situation. If efforts to restore the restaurant’s performance to acceptable minimum standards are unsuccessful, the brand considers relocation to a proximate, more desirable site, or evaluates closing the restaurant if the brand’s measurement criteria, such as return on investment and area demographic trends, do not support relocation. We closed three company-owned restaurants in fiscal 2013. We perform a comprehensive analysis that examines restaurants not performing at a required rate of return. These closed restaurants were generally performing below our standards or were near or at the expiration of their lease term. Our strategic plan is targeted to support our long-term growth objectives, with a focus on continued development of those restaurant locations that have the greatest return potential for the Company and our shareholders.

Franchise Development

In addition to our development of company-owned restaurants, our restaurant brands will maintain expansion through our franchisees and joint venture partners.

As part of our strategy to expand through our franchisees, our franchise operations (domestically and internationally) increased in fiscal 2013. The following table illustrates the percentages of franchise operations as of June 26, 2013 for the Company and by restaurant brand, respectively:

Percentage of Franchise Operated Restaurants | ||||||||

Domestic(1) | International(2) | Overall(3) | ||||||

Brinker | 34 | % | 96 | % | 45 | % | ||

Chili’s | 35 | % | 96 | % | 46 | % | ||

Maggiano’s | — | % | — | % | — | % | ||

____________________________________________________________________

(1) | The percentages in this column are based on number of domestic franchised restaurants versus total domestic restaurants. |

(2) | The percentages in this column are based on number of international franchised restaurants versus total international restaurants. |

(3) | The percentages in this column are based on the total number of franchised restaurants (domestic and international) versus total system-wide number of restaurants. |

Domestic

Domestic expansion is also focused on growing our number of franchised restaurants. We are accomplishing this through existing, new or renewed development obligations with new or existing franchisees. In addition, we have from time to time also sold and may sell company-owned restaurants to our franchisees (new or existing). As of June 26, 2013, eight total domestic development arrangements existed including a new development agreement for three restaurants in the State of Alaska. A typical domestic franchise development agreement provides for payment of development and initial franchise fees in addition to subsequent royalty and advertising fees based on the gross sales of each restaurant. We expect future domestic franchise development agreements to remain limited to enterprises having significant experience as restaurant operators and proven financial ability to support and develop multi-unit operations.

Domestic expansion efforts continue to focus not only on major metropolitan areas in the United States but also on smaller market areas and non-traditional locations (such as airports, college campuses and food courts) that can adequately support our restaurant brands.

During the year ended June 26, 2013, our domestic franchisees opened two Chili’s restaurants. Additionally, we acquired one Chili’s restaurant from a franchisee in the Miami, Florida metropolitan area.

International

We continue our international growth through development agreements with new and existing franchisees and joint venture partners, as well as introducing Chili’s to new countries and expanding the brand within our existing markets. As of June 26, 2013, we had 20 total development arrangements. During fiscal year 2013, our international franchisees and joint venture partners opened 33 Chili’s restaurants. In the same year, we entered into a new development agreement with one franchisee for the development of 25 Chili’s restaurants. The area of development for these locations includes south and west India.

5

As we develop Chili’s internationally, we will selectively pursue expansion through various means, including franchising and joint ventures. Similar to our domestic franchise agreements, a typical international franchise development agreement provides the vehicle for payment of development fees and franchise fees in addition to subsequent royalty fees based on the gross sales of each restaurant. We expect future development agreements to remain limited to enterprises who demonstrate a proven track record as a restaurant operator and showcase financial strength that can support a multi-unit development agreement, as well as, in some instances, multi-brand operations.

During the year ended June 26, 2013, we acquired 11 Chili's restaurants from one of our franchisees in Alberta, Canada.

Restaurant Management

Our Chili’s and Maggiano’s brands have separate designated teams who support each brand including operations, finance, franchise, marketing, peopleworks and culinary. We believe these strategic, brand-focused teams foster the identities of the individual and uniquely positioned brands. To maximize efficiencies, brands continue to utilize common and shared infrastructure, including, among other services, accounting, information technology, purchasing, legal and restaurant development.

At the restaurant level, management structure varies by brand. A typical restaurant is led by a management team including a general manager, two to six additional managers, and for Maggiano’s, an additional three to four chefs. The level of restaurant supervision depends upon the operating complexity and sales volume of individual locations.

We believe there is a high correlation between the quality of restaurant management and the long-term success of a brand. In that regard, we encourage increased experience at all management positions through various short and long-term incentive programs, which may include equity ownership. These programs, coupled with a general management philosophy emphasizing quality of life, have enabled us to attract and retain key team members.

We ensure consistent quality standards in all brands through the issuance of operations manuals covering all elements of operations and food and beverage manuals, which provide guidance for preparation of brand-formulated recipes. Routine visitation to the restaurants by all levels of supervision enforces strict adherence to our overall brand standards and operating procedures. Each brand is responsible for maintaining their operational training program. The training program typically includes a two to four-month training period for restaurant management trainees. We also provide reoccurring management training for managers and supervisors to improve effectiveness or prepare them for more responsibility.

Supply Chain

Our ability to maintain consistent quality throughout each restaurant brand depends upon acquiring products from reliable sources. Our pre-approved suppliers and our restaurants are required to adhere to strict product and safety specifications established through our quality assurance and culinary programs. These requirements ensure high quality products are served in each of our restaurants. We strategically negotiate directly with major suppliers to obtain competitive prices. We also use purchase commitment contracts when appropriate to stabilize the potentially volatile pricing associated with certain commodity items. All essential products are available from pre-qualified distributors to be delivered to our restaurant brands. Additionally, as a purchaser of a variety of protein products, we do require our suppliers to adhere to humane processing standards for their respective industries and encourage them to evaluate new technologies for food safety and humane processing improvements. Due to the relatively rapid turnover of perishable food products, inventories in the restaurants, which consists primarily of food, beverages and supplies, have a modest aggregate dollar value in relation to revenues. Internationally, our franchisees and joint venture operations may encounter cultural and regulatory differences resulting in variances with product specifications for international restaurant locations.

Advertising and Marketing

Our brands generally target the 26 to 54 year-old age group, which constitutes approximately 41 percent of the United States population. It is our belief these consumers value the benefits of the casual dining category for multiple meal occasions. In choosing not to cook, these consumers want the higher food quality, the opportunity to connect with family and friends and the enhanced dining experience our restaurant brands offer. To reach this target group, we use a mix of television, radio, print, outdoor or online advertising, as well as mail (direct and electronic) and social media, with each of our restaurant brands utilizing one or more of these mediums to meet their communication strategy and budget. Our brands have also leveraged extensive consumer marketing research to monitor brand health, guest satisfaction and emerging trends, as well as validate menu development and creative campaigns.

Our franchise agreements generally require advertising contributions to us by the franchisees. We use these contributions, in conjunction with company funds, for the purpose of retaining agencies, obtaining consumer insights, developing and producing brand-specific creative materials and purchasing national or regional media to meet the brand’s strategy. Some franchisees also spend additional amounts on local advertising. Any such local advertising must first be approved by us.

6

Team Members

As of June 26, 2013, we employed approximately 54,653 team members, of which 644 were restaurant support center personnel in Dallas, and 3,974 were restaurant area directors, managers, or trainees. The remaining 50,035 were employed in non-management restaurant positions. Our executive officers have an average of 20 years of experience in the restaurant industry.

We have a positive team member relations outlook and continue to focus on improving our team member turnover rate. We have a variety of tools and strong resources in place to help us recruit and retain the best talent to work in our restaurants.

The majority of our team members, outside of restaurant management and restaurant support center personnel, are paid on an hourly basis. We stand firm in the belief that we provide competitive working conditions and wages favorable with other companies in our industry. Our team members are not covered by any collective bargaining agreements.

Trademarks

We have registered and/or have pending, among other marks, “Brinker International”, “Chili’s”, “Chili’s Bar & Bites”, “Chili's Express”, “Chili’s Margarita Bar”, “Chili’s Southwest Grill & Bar”, “Chili’s Too”, “Maggiano’s”, and “Maggiano’s Little Italy”, as trademarks with the United States Patent and Trademark Office.

Available Information

We maintain an internet website with the address of http://www.brinker.com. You may obtain, free of charge, at our website, copies of our reports filed with, or furnished to, the Securities and Exchange Commission (the “SEC”) on Forms 10-K, 10-Q and 8-K. Any amendments to such reports are also available for viewing and copying at our internet website. These reports will be available as soon as reasonably practicable after filing such material with, or furnishing it to, the SEC. In addition, you may view and obtain, free of charge, at our website, copies of our corporate governance materials, including, Corporate Governance Guidelines, Governance and Nominating Committee Charter, Audit Committee Charter, Compensation Committee Charter, Executive Committee Charter, Code of Conduct and Ethical Business Policy, and Problem Resolution Procedure/Whistle Blower Policy.

Item 1A. | RISK FACTORS. |

We wish to caution you that our business and operations are subject to a number of risks and uncertainties. The factors listed below are important because they could cause actual results to differ materially from our historical results and from those projected in forward-looking statements contained in this report, in our other filings with the SEC, in our news releases, written or electronic communications, and verbal statements by our representatives.

You should be aware that forward-looking statements involve risks and uncertainties. These risks and uncertainties may cause our or our industry’s actual results, performance or achievements to be materially different from any future results, performances or achievements contained in or implied by these forward-looking statements. Forward-looking statements are generally accompanied by words like “believes,” “anticipates,” “estimates,” “predicts,” “expects,” and other similar expressions that convey uncertainty about future events or outcomes. We expressly disclaim any obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise.

Risks Related to Our Business

Competition may adversely affect our operations and financial results.

The restaurant business is highly competitive as to price, service, restaurant location, nutritional and dietary trends and food quality, and is often affected by changes in consumer tastes, economic conditions, population and traffic patterns. We compete within each market with locally-owned restaurants as well as national and regional restaurant chains, some of which operate more restaurants and have greater financial resources and longer operating histories than ours. Despite a weak U.S. employment market, there is active competition for quality management personnel and hourly team members. We continue to face competition as a result of several factors, including quick service and fast casual restaurants also offering high quality food and beverage offerings, the convergence in grocery, deli and restaurant services, including the grocery industry offering of convenient meals in the form of improved entrees and side dishes. We compete primarily on the quality, variety and value perception of menu items, as well as the quality and efficiency of service, the attractiveness of facilities and the effectiveness of advertising and marketing programs.

Our restaurants also face competition from the introduction of new products and menu items by competitors, as well as substantial price discounting among other offers, and are likely to continue to face such future competition in light of the slow

7

paced economic recovery. Although we may implement a number of business strategies, the success of new products, initiatives and overall strategies is highly difficult to predict and will be influenced by competitive product offerings, pricing and promotions offered by competitors. Our ability to differentiate our brands from their competitors, which is in part limited by the advertising spend available to us and by consumer perception, cannot be assured. These factors could reduce the gross sales or profitability at our restaurants, which would decrease revenues generated by company-owned restaurants and royalty payments from franchisees.

Changing health or dietary preferences may cause consumers to avoid our products in favor of alternative foods. The foodservice industry as a whole rests on consumer preferences and demographic trends at the local, regional, national and international levels, including the impact on consumer eating habits of new information regarding diet, nutrition, health and health insurance. We and our franchisees depend on the sustained demand for our products, which may be affected by factors outside of our control. Changes in nutritional or health insurance guidelines issued by federal or local government agencies, issuance of similar guidelines or statistical information by other federal, state or local municipalities, academic studies, or advocacy organizations among other things, may impact consumer choice and cause consumers to select foods other than those that are offered by our restaurants. We may not be able to adequately adapt our menu offerings to keep pace with developments in current consumer preferences, which may result in reductions to the revenues generated by our company-owned restaurants and the payments we receive from franchisees.

The weak global economic recovery continues to impact consumer discretionary spending and a prolonged economic recovery could result in declines in consumer discretionary spending materially affecting our financial performance in the future.

The restaurant industry is dependent upon consumer discretionary spending. Consumer confidence has not fully recovered from recent lows impacting the public’s ability and/or desire to spend discretionary dollars as a result of significantly limited job availability, slow recovering home values, limited investment gains in the financial markets and continued reduced access to credit. Current international fiscal concerns continue to impact the slow U.S. economic recovery. While sales and traffic gains were made by the restaurant industry and our brands in the prior fiscal year, economic headwinds were encountered in fiscal 2013, including increased personal income taxes and payroll taxes. Economic improvement in the restaurant industry continues to come from cost savings initiatives as well as our success to improve the guest experience within our existing restaurant locations. If this current slow economic recovery continues for a prolonged period of time and/or deepens in magnitude returning to the negative trends of the prior years, our business, results of operations and ability to comply with the covenants under our credit facility could be materially affected. Leading economic indicators such as employment and consumer confidence remain challenged and did not show meaningful improvement in fiscal 2013. Deterioration in guest traffic and/or a reduction in the average amount guests spend in our restaurants will negatively impact our revenues. This will also result in lower royalties collected, sales deleverage, spreading fixed costs across a lower level of sales, and in turn, cause downward pressure on our profitability. The result could be further reductions in staff levels, asset impairment charges and potential restaurant closures.

Future slower global economic recovery or recessionary effects on us are unknown at this time and could have a potential material adverse affect on our financial position and results of operations. There is no assurance that the government’s plan to restore fiscal responsibility or future plans to stimulate the economy will revive consumer confidence, stabilize the financial markets, increase liquidity and the availability of credit, or result in lower unemployment, which continues to remain stubbornly high at the present time.

The current slow economic recovery could have a material adverse impact on our landlords or other tenants in retail centers in which we or our franchisees are located, which in turn could negatively affect our financial results.

If the slow economic recovery continues or returns to recessionary levels, our landlords may be unable to obtain financing or remain in good standing under their existing financing arrangements, resulting in failures to pay required construction contributions or satisfy other lease covenants to us. In addition, other tenants at retail centers in which we or our franchisees are located or have executed leases, may fail to open or may cease operations. If our landlords fail to satisfy required co-tenancies, this may result in us or our franchisees terminating leases or delaying openings in these locations. Also, decreases in total tenant occupancy in retail centers in which we are located may affect guest traffic at our restaurants. All of these factors could have a material adverse impact on our operations.

Inflation may increase our operating expenses.

We have experienced impact from inflation. Inflation has caused added food, labor and benefits costs and increased our operating expenses. As operating expenses rise, we, to the extent permitted by competition, recover costs by raising menu

8

prices, or by reviewing, then implementing, alternative products or processes, or other cost reduction procedures. We cannot ensure, however, we will be able to continue to recover increases in operating expenses due to inflation in this manner.

Changes in governmental regulation may adversely affect our ability to maintain our existing and future operations and to open new restaurants.

We are subject to the Fair Labor Standards Act (which governs such matters as minimum wages, overtime and other working conditions), along with the Americans with Disabilities Act, the Immigration Reform and Control Act of 1986, various family leave mandates and a variety of other laws enacted, or rules and regulations promulgated by federal, state and local governmental authorities that govern these and other employment matters, including, tip credits, working conditions, safety standards and immigration status. We expect adjustments in payroll expenses as a result of federal and state mandated increases in the minimum wage, and although such increases are not expected to be material, we cannot be certain there will be no material increases in the future. Enactment and enforcement of various federal, state and local laws, rules and regulations on immigration and labor organizations may adversely impact the availability and costs of labor for our restaurants in a particular area or across the United States. Other labor shortages or increased team member turnover could also increase labor costs. In addition, our suppliers may be affected by higher minimum wage standards or availability of labor, which may increase the price of goods and services they supply to us. We continue to review the health care reform law enacted by Congress in March of 2010 and regulations issued related to the law to evaluate the potential impact of this new law on our business, and to accommodate various parts of the law as they take effect. There are no assurances that a combination of cost management and price increases can accommodate all of the costs associated with compliance.

We are subject to laws and regulations, which vary from jurisdiction to jurisdiction, relating to nutritional content and menu labeling. Compliance with these laws and regulations may lead to increased costs and operational complexity, changes in sales mix and profitability, and increased exposure to governmental investigations or litigation. We do not expect to incur material costs from compliance with the provision of the new health care law requiring disclosure of calories on the menus, but cannot reliably anticipate any changes in guest behavior resulting from implementation of this portion of the law, which could have adverse effects on our sales or results of operations.

Each of our company-owned and our franchisees’ restaurants is also subject to licensing and regulation by alcoholic beverage control, health, sanitation, safety and fire agencies in the state, county and/or municipality where the restaurant is located. We generally have not encountered any material difficulties or failures in obtaining and maintaining the required licenses and approvals that could impact the continuing operations of an existing restaurant, or delay or prevent the opening of a new restaurant. Although we do not, at this time, anticipate any occurring in the future, we cannot be certain that we, or our franchisees, will not experience material difficulties or failures that could impact the continuing operations of an existing restaurant, or delay the opening of restaurants in the future.

We are also subject to federal and state environmental regulations, and although these have not had a material negative affect on our operations, we cannot ensure this will not occur in the future. In particular, the U.S. and other foreign governments have increased focus on environmental matters such as climate change, greenhouse gases and water conservation. This may lead to new initiatives directed at regulating an as-yet-unspecified array of environmental matters. These efforts could result in increased taxation or in future restrictions on or increases in costs associated with food and other restaurant supplies, transportation costs and utility costs, any of which could decrease our operating profits and/or necessitate future investments in our restaurant facilities and equipment to achieve compliance. Further, more stringent and varied requirements of local and state governmental bodies with respect to zoning, land use and environmental factors could delay, prevent or make cost prohibitive the continuing operations of an existing restaurant or the development of new restaurants in particular locations.

Due to our international franchising, we are also subject to governmental regulations throughout the world impacting the way we do business with our international franchisees and joint venture partners. These include antitrust and tax requirements, anti-boycott regulations, import/export/customs and other international trade regulations, the USA Patriot Act and The Foreign Corrupt Practices Act. Failure to comply with any such legal requirements could subject us to monetary liabilities and other sanctions, which could adversely impact our business and financial performance.

The impact of current laws and regulations, the effect of future changes in laws or regulations that impose additional requirements and the consequences of litigation relating to current or future laws and regulations, or our inability to respond effectively to significant regulatory or public policy issues, could increase our compliance and other costs of doing business and therefore have an adverse affect on our results of operations. Failure to comply with the laws and regulatory requirements of federal, state and local authorities could result in, among other things, revocation of required licenses, administrative enforcement actions, fines and civil and criminal liability. Compliance with these laws and regulations can be costly and can increase our exposure to litigation or governmental investigations or proceedings.

9

Our profitability may be adversely affected by increases in energy costs.

Our success depends in part on our ability to absorb increases in utility costs, in particular, electricity and natural gas. Various regions of the United States in which we operate multiple restaurants have experienced volatility in utility prices. This has affected costs in the past and if they occur again, it would have possible adverse effects on our profitability to the extent not otherwise recoverable through price increases or alternative products, processes or cost reduction procedures. Further, higher prices for petroleum-based fuels may be passed on to us by suppliers putting further pressure on margins as well as impact our guests discretionary funds and ability to patron our restaurants or their menu choices.

Shortages or interruptions in the availability and delivery of food and other products may increase costs or reduce revenues.

Possible shortages or interruptions in the supply of food items and other products to our restaurants caused by inclement weather, natural disasters such as floods, drought and hurricanes; the inability of our suppliers to obtain credit in a tightened credit market; food safety warnings or advisories or the prospect of such pronouncements; or other conditions beyond our control, could adversely affect the availability, quality and cost of items we buy and the operations of our restaurants. Our inability to effectively manage supply chain risk could increase our costs and limit the availability of products critical to our restaurant operations.

Successful strategic transactions are important to our future growth and profitability.

We evaluate potential franchisees of new and existing restaurants and joint venture investments, as well as mergers, acquisitions and divestitures, as part of our strategic planning initiative. These transactions involve various inherent risks, including accurately assessing:

• | the value, future growth potential, strengths, weaknesses, contingent and other liabilities and potential profitability of franchise and joint venture partner candidates; |

• | our ability to achieve projected economic and operating synergies; and |

• | unanticipated changes in business and economic conditions affecting an acquired business or the completion of a divestiture. |

If we are unable to meet our business strategy plan, our profitability in the future may be adversely affected.

Our ability to meet our business strategy plan is dependent upon, among other things, our and our franchisees’ ability to:

• | increase gross sales and operating profits at existing restaurants with food and beverage options and high quality service desired by our guests through successful implementation of strategic initiatives; |

• | identify adequate sources of capital to fund and finance strategic initiatives, including remodeling of existing restaurants and new restaurant development; |

• | identify available, suitable and economically viable locations for new restaurants; |

• | obtain all required governmental permits (including zoning approvals and liquor licenses) on a timely basis; |

• | hire all necessary contractors and subcontractors, obtain construction materials at suitable prices, and maintain construction schedules; and |

• | hire and train or retain qualified managers and team members for existing and new restaurants. |

The success of our franchisees is important to our future growth.

We have significantly increased the percentage of restaurants owned and operated by our franchisees. While our franchise agreements are designed to maintain brand consistency, this increase reduces our direct day-to-day control over these restaurants and may expose us to risks not otherwise encountered if we maintained ownership and control of same. These risks include franchisee defaults in their obligations to us arising from financial or other difficulties encountered by them, such as payments to us or maintenance and improvements obligations; limitations on enforcement of franchise obligations due to bankruptcy or insolvency proceedings; inability to participate in business strategy changes due to financial constraints; inability to meet rent obligations on leases on which we retain contingent liability; and failure to comply with food quality and preparation requirements subjecting us to litigation even when we are not legally liable for a franchisee’s actions or failure to act.

10

Additionally our international franchisees and joint venture partners are subject to risks not encountered by our domestic franchisees. These risks include:

• | difficulties in achieving consistency of product quality and service as compared to U.S. operations; |

• | changes to recipes and menu offerings to meet cultural norms; |

• | challenges to obtain adequate and reliable supplies necessary to provide menu items and maintain food quality; and |

• | differences, changes or uncertainties in economic, regulatory, legal, social and political conditions. |

Our sales volumes generally decrease in winter months in North America.

Our sales volumes fluctuate seasonally and are generally higher in the summer months and lower in the winter months, which may cause seasonal fluctuations in our operating results.

Unfavorable publicity relating to one or more of our restaurants in a particular brand may taint public perception of the brand.

Multi-unit restaurant businesses can be adversely affected by publicity resulting from poor food quality, illness or health concerns or operating issues stemming from one or a limited number of restaurants. In particular, since we depend heavily on the Chili’s brand for a majority of our revenues, unfavorable publicity relating to one or more Chili’s restaurants could have a material adverse effect on the Chili’s brand, and consequently on our business, financial condition and results of operations. The speed at which negative publicity (whether or not accurate) can be disseminated has increased dramatically with the capabilities of electronic communication, including social media. If we are unable to quickly and effectively respond to such reports, we may suffer declines in guest traffic which could materially impact our financial performance.

Litigation could have a material adverse impact on our business and our financial performance.

We are subject to lawsuits, administrative proceedings and claims that arise in the regular course of business. These matters typically involve claims by guests, team members and others regarding issues such as food borne illness, food safety, premises liability, compliance with wage and hour requirements, work-related injuries, discrimination, harassment, disability and other operational issues common to the foodservice industry, as well as contract disputes and intellectual property infringement matters. We could be adversely affected by negative publicity and litigation costs resulting from these claims, regardless of their validity. Significant legal fees and costs in complex class action litigation or an adverse judgment or settlement that is not insured or is in excess of insurance coverage could have a material adverse effect on our financial position and results of operations.

We are dependent on information technology and any material failure of that technology or our ability to execute a comprehensive business continuity plan could impair our ability to efficiently operate our business.

We rely on information systems across our operations, including, for example, point-of-sale processing in our restaurants, management of our supply chain, collection of cash, payment of obligations and various other processes and procedures. Our ability to efficiently manage our business depends significantly on the reliability and capacity of these systems. The failure of these systems to operate effectively, problems with maintenance, upgrading or transitioning to replacement systems, or a breach in security of these systems could cause delays in customer service and reduce efficiency in our operations. Significant capital investments might be required to remediate any problems.

Additionally, our corporate systems and processes and corporate support for our restaurant operations are handled primarily at our restaurant support center. We have disaster recovery procedures and business continuity plans in place to address most events of a crisis nature, including tornadoes and other natural disasters, and back up and off-site locations for recovery of electronic and other forms of data and information. However, if we are unable to fully implement our disaster recovery plans, we may experience delays in recovery of data, inability to perform vital corporate functions, tardiness in required reporting and compliance, failures to adequately support field operations and other breakdowns in normal communication and operating procedures that could have a material adverse effect on our financial condition, results of operation and exposure to administrative and other legal claims.

11

We outsource certain business processes to third-party vendors that subject us to risks, including disruptions in business and increased costs.

Some business processes are currently outsourced to third parties. Such processes include gift card tracking and authorization, credit card authorization and processing, insurance claims processing, certain payroll processing, tax filings and other accounting processes. We also continue to evaluate our other business processes to determine if additional outsourcing is a viable option to accomplish our goals. We make a diligent effort to ensure that all providers of outsourced services are observing proper internal control practices, such as redundant processing facilities; however, there are no guarantees that failures will not occur. Failure of third parties to provide adequate services could have an adverse effect on our results of operations, financial condition or ability to accomplish our financial and management reporting.

Disruptions in the global financial markets may adversely impact the availability and cost of credit and consumer spending patterns.

The disruptions to the global financial markets and continuing slow economic recovery have adversely impacted the availability of credit already arranged and the availability and cost of credit in the future. The disruptions in the financial markets also had an adverse effect on the U.S. and world economy, which has negatively impacted consumer spending patterns. There can be no assurance that various U.S. and world government present and future responses to the disruptions in the financial markets will restore consumer confidence, stabilize the markets or increase liquidity or the availability of credit.

Failure to protect the integrity and security of individually identifiable data of our guests and teammates could expose us to litigation and damage our reputation.

We receive and maintain certain personal information about our guests and teammates. The use of this information by us is regulated at the federal and state levels, as well as by certain third party contracts. If our security and information systems are compromised or our business associates fail to comply with these laws and regulations and this information is obtained by unauthorized persons or used inappropriately, it could adversely affect our reputation, as well as operations, results of operations and financial condition, and could result in litigation against us or the imposition of penalties. As privacy and information security laws and regulations change, we may incur additional costs to ensure it remains in compliance.

Declines in the market price of our common stock or changes in other circumstances that may indicate an impairment of goodwill could adversely affect our financial position and results of operations.

We perform our annual goodwill impairment test in the second quarter of each fiscal year. Interim goodwill impairment tests are also required when events or circumstances change between annual tests that would more likely than not reduce the fair value of our reporting units below their carrying value. It is possible that a change in circumstances such as the decline in the market price of our common stock or changes in consumer spending levels, or in the numerous variables associated with the judgments, assumptions and estimates made in assessing the appropriate valuation of our goodwill, could negatively impact the valuation of our brands and create the potential for a non-cash charge to recognize impairment losses on some or all of our goodwill. If we were required to write down a portion of our goodwill and record related non-cash impairment charges, our financial position and results of operations would be adversely affected.

Changes to estimates related to our property and equipment, or operating results that are lower than our current estimates at certain restaurant locations, may cause us to incur impairment charges on certain long-lived assets.

We make certain estimates and projections with regards to individual restaurant operations, as well as our overall performance in connection with our impairment analyses for long-lived assets. An impairment charge is required when the carrying value of the asset exceeds the estimated fair value or undiscounted future cash flows of the asset. The projection of future cash flows used in this analysis requires the use of judgment and a number of estimates and projections of future operating results. If actual results differ from our estimates, additional charges for asset impairments may be required in the future. If impairment charges are significant, our results of operations could be adversely affected.

Identification of material weakness in internal control may adversely affect our financial results.

We are subject to the ongoing internal control provisions of Section 404 of the Sarbanes-Oxley Act of 2002. Those provisions provide for the identification of material weaknesses in internal control. If such a material weakness is identified, it could indicate a lack of adequate controls to generate accurate financial statements. We routinely assess our internal controls, but we cannot assure you that we will be able to timely remediate any material weaknesses that may be identified in future periods, or maintain all of the controls necessary for continued compliance. Likewise, we cannot assure you that we will be able to retain sufficient skilled finance and accounting team members, especially in light of the increased demand for such individuals among publicly traded companies.

12

Other risk factors may adversely affect our financial performance.

Other risk factors that could cause our actual results to differ materially from those indicated in the forward-looking statements by affecting, among many things, pricing, consumer spending and consumer confidence, include, without limitation, changes in economic conditions and financial and credit markets (including rising interest rates and costs for consumers and reduced disposable income); credit availability; increased costs of food commodities; increased fuel costs and availability for our team members, customers and suppliers; increased health care costs; health epidemics or pandemics or the prospects of these events; consumer perceptions of food safety; changes in consumer tastes and behaviors; governmental monetary policies; changes in demographic trends; availability of employees; terrorist acts; energy shortages and rolling blackouts; and weather (including, major hurricanes and regional winter storms) and other acts of God.

Item 1B. | UNRESOLVED STAFF COMMENTS. |

None.

Item 2. | PROPERTIES. |

Restaurant Locations

At June 26, 2013, our system of company-owned and franchised restaurants included 1,591 restaurants located in 50 states and Washington, D.C. We also have restaurants in the U.S. territories of Guam and Puerto Rico and the countries of Bahrain, Brazil, Canada, Columbia, Costa Rica, Dominican Republic, Ecuador, Egypt, El Salvador, Germany, Guatemala, Honduras, India, Indonesia, Japan, Jordan, Kuwait, Lebanon, Malaysia, Mexico, Oman, Peru, Philippines, Qatar, Russia, Saudi Arabia, Singapore, South Korea, Syria, Taiwan, United Arab Emirates and Venezuela. We have provided you a breakdown of our portfolio of restaurants in the two tables below:

Table 1: Company-owned vs. franchise (by brand) as of June 26, 2013:

Chili’s | ||

Company-owned (domestic) | 822 | |

Company-owned (international) | 11 | |

Franchise | 714 | |

Maggiano’s | ||

Company-owned | 44 | |

Total | 1,591 | |

Table 2: Domestic vs. foreign locations (by brand) as of June 26, 2013 (company-owned and franchised):

Domestic (No. of States) | Foreign (No. of countries and territories) | |||

Chili’s | 1,265(50) | 282(34) | ||

Maggiano’s | 44 | — | ||

Restaurant Property Information

The following table illustrates the approximate average dining capacity for each current prototypical restaurant in our restaurant brands:

Chili’s | Maggiano’s | ||

Square Feet | 3,930-6,000 | 7,700-24,000 | |

Dining Seats | 150-252 | 200-700 | |

Dining Tables | 35-54 | 35-150 | |

13

The leases typically provide for a fixed rental plus percentage rentals based on sales volume. At June 26, 2013, we owned the land and building for 189 of our 877 company-owned restaurant locations. For these 189 restaurant locations, the net book value for the land was $142 million and for the buildings was $118 million. For the remaining 688 restaurant locations leased by us, the net book value of the buildings and leasehold improvements was $537 million. The 688 leased restaurant locations can be categorized as follows: 541 are ground leases (where we lease land only, but own the building) and 147 are retail leases (where we lease the land/retail space and building). We believe that our properties are suitable, adequate, well-maintained and sufficient for the operations contemplated. Some of our leased restaurants are leased for an initial lease term of 5 to 30 years, with renewal terms of 1 to 35 years.

Other Properties

We own an office building containing approximately 108,000 square feet which we use for part of our corporate headquarters and menu development activities. We lease an additional office complex containing approximately 198,000 square feet for the remainder of our corporate headquarters which is currently utilized by us, reserved for future expansion of our headquarters, or sublet to third parties. Because of our operations throughout the United States, we also lease office space in California, Colorado, Florida, New Jersey and Texas for use as regional operation offices. The size of these office leases range from approximately 100 square feet to approximately 4,000 square feet.

Item 3. | LEGAL PROCEEDINGS. |

In August 2004, certain current and former hourly restaurant team members filed a putative class action lawsuit against us in California Superior Court alleging violations of California labor laws with respect to meal periods and rest breaks. The lawsuit sought penalties and attorney’s fees and was certified as a class action by the trial court in July 2006. In July 2008, the California Court of Appeal decertified the class action on all claims with prejudice. In October 2008, the California Supreme Court granted a writ to review the decision of the Court of Appeal and oral arguments were heard by the California Supreme Court on November 8, 2011. On April 12, 2012, the California Supreme Court issued an opinion affirming in part, reversing in part, and remanding in part for further proceedings. The California Supreme Court’s opinion resolved many of the legal standards for meal periods and rest breaks in our California restaurants and we intend to vigorously defend our position on the remaining issues upon remand to the trial court. It is not possible at this time to reasonably estimate the possible loss or range of loss, if any.

We are engaged in various other legal proceedings and have certain unresolved claims pending. Reserves have been established based on our best estimates of our potential liability in certain of these matters. Based upon consultation with legal counsel, Management is of the opinion that there are no matters pending or threatened which are expected to have a material adverse effect, individually or in the aggregate, on our consolidated financial condition or results of operations.

Item 4. | MINE SAFETY DISCLOSURES. |

Not applicable.

14

PART II

Item 5. | MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES. |

Our common stock is traded on the New York Stock Exchange (“NYSE”) under the symbol “EAT”. Bid prices quoted represent interdealer prices without adjustment for retail markup, markdown and/or commissions, and may not necessarily represent actual transactions. The following table sets forth the quarterly high and low closing sales prices of the common stock, as reported by the NYSE.

Fiscal year ended June 26, 2013:

High | Low | ||||||

First Quarter | $ | 35.98 | $ | 30.62 | |||

Second Quarter | $ | 35.30 | $ | 28.71 | |||

Third Quarter | $ | 37.07 | $ | 30.39 | |||

Fourth Quarter | $ | 41.60 | $ | 37.25 | |||

Fiscal year ended June 27, 2012:

High | Low | ||||||

First Quarter | $ | 26.57 | $ | 20.01 | |||

Second Quarter | $ | 27.07 | $ | 20.07 | |||

Third Quarter | $ | 28.98 | $ | 25.66 | |||

Fourth Quarter | $ | 32.69 | $ | 26.65 | |||

As of August 12, 2013, there were 587 holders of record of our common stock.

During the fiscal year ended June 26, 2013, we continued to declare quarterly cash dividends for our shareholders. We have set forth the dividends declared for the fiscal year in the following table on the specified dates:

Dividend Per Share of Common Stock | Declaration Date | Record Date | Payment Date | |||

$0.20 | August 23, 2012 | September 10, 2012 | September 27, 2012 | |||

$0.20 | November 8, 2012 | December 7, 2012 | December 27, 2012 | |||

$0.20 | February 7, 2013 | March 8, 2013 | March 28, 2013 | |||

$0.20 | May 30, 2013 | June 14, 2013 | June 27, 2013 | |||

15

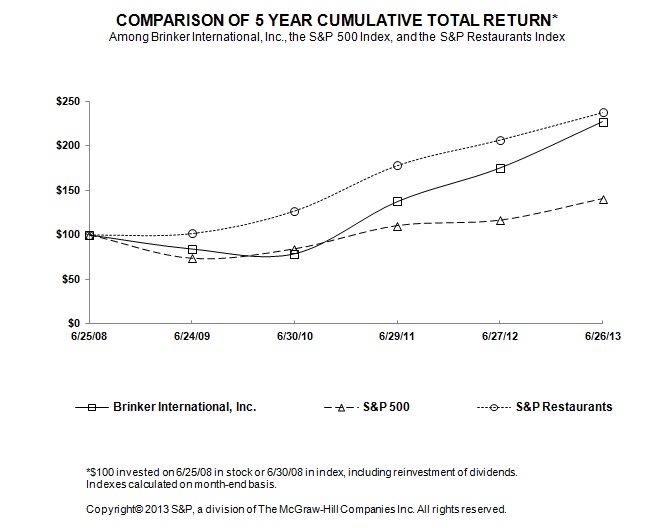

The following graph compares the cumulative five-year total return provided shareholders on Brinker International, Inc.’s common stock relative to the cumulative total returns of the S&P 500 Index and the S&P Restaurants Index.

The graph assumes a $100 initial investment and the reinvestment of dividends in our stock and each of the indexes on June 25, 2008 and its relative performance is tracked through June 26, 2013. The values shown are neither indicative nor determinative of future performance.

2008 | 2009 | 2010 | 2011 | 2012 | 2013 | ||||||||||||||||||

Brinker International | $ | 100.00 | $ | 84.22 | $ | 78.95 | $ | 137.37 | $ | 175.08 | $ | 227.02 | |||||||||||

S&P 500 | $ | 100.00 | $ | 73.79 | $ | 84.43 | $ | 110.35 | $ | 116.36 | $ | 140.32 | |||||||||||

S&P Restaurants(1) | $ | 100.00 | $ | 101.52 | $ | 127.02 | $ | 177.98 | $ | 206.64 | $ | 237.49 | |||||||||||

____________________________________________________________________

(1) | The S&P Restaurants Index is comprised of Chipotle Mexican Grill, Inc., Darden Restaurants, Inc., McDonald’s Corp., Starbucks Corporation and Yum! Brands Inc. |

In May 2013, the Company issued $250.0 million in the aggregate principal amount at maturity of 2.600% Notes due 2018 (the "2018 Notes") and $300.0 million in the aggregate principal amount at maturity of 3.875% Notes due 2023 (the "2023 Notes", and together with the 2018 Notes, the "Notes"). J.P. Morgan Securities LLC and Merrill Lynch, Pierce, Fenner & Smith Incorporated served as the joint book-running managers for the offering. The Notes were issued in a public offering pursuant to a registration statement on Form S-3, File No. 333-188252, and are freely tradeable. The Notes are redeemable at the Company's option at any time, in whole or in part. The proceeds of the offering were and will be used for general corporate purposes, including the redemption of the 5.75% notes due June 2014, pay down of the revolver and the repurchase of the Company's common stock pursuant to its share repurchase program.

16

Except as described in the immediately preceding paragraphs, during the three-year period ended on August 12, 2013, we issued no securities which were not registered under the Securities Act of 1933, as amended.

We continue to maintain our share repurchase program; on August 22, 2013, our Board of Directors increased our share repurchase authorization by $200 million, bringing the total authorization to $3,585 million. During the fourth quarter, we repurchased shares as follows (in thousands, except share and per share amounts):

Total Number of Shares Purchased(a) | Average Price Paid per Share | Total Number of Shares Purchased as Part of Publicly Announced Program | Approximate Dollar Value that May Yet be Purchased Under the Program(b) | ||||||||||

March 28, 2013 through May 1, 2013 | 420,874 | $ | 38.09 | 420,000 | $ | 458,134 | |||||||

May 2, 2013 through May 29, 2013 | 1,375,000 | $ | 40.91 | 1,375,000 | $ | 401,856 | |||||||

May 30, 2013 through June 26, 2013 | 1,721,019 | $ | 40.23 | 1,720,400 | $ | 332,610 | |||||||

Total | 3,516,893 | $ | 40.24 | 3,515,400 | |||||||||

____________________________________________________________________

(a) | These amounts include shares purchased as part of our publicly announced programs and shares owned and tendered by team members to satisfy tax withholding obligations on the vesting of restricted share awards, which are not deducted from shares available to be purchased under publicly announced programs. Unless otherwise indicated, shares owned and tendered by team members to satisfy tax withholding obligations were purchased at the average of the high and low prices of the Company’s shares on the date of vesting. During the fourth quarter of fiscal 2013, 1,493 shares were tendered by team members at an average price of $37.66. |

(b) | The final amount shown is as of June 26, 2013. |

Item 6. | SELECTED FINANCIAL DATA. |

The information set forth in that section entitled “Selected Financial Data” in our 2013 Annual Report to Shareholders is presented on page F-1 of Exhibit 13 to this document. We incorporate that information in this document by reference.

Item 7. | MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS. |

The information set forth in that section entitled “Management’s Discussion and Analysis of Financial Condition and Results of Operations” in our 2013 Annual Report to Shareholders is presented on pages F-2 through F-11 of Exhibit 13 to this document. We incorporate that information in this document by reference.

Item 7A. | QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK. |

The information set forth in that section entitled “Quantitative and Qualitative Disclosures About Market Risk” contained within “Management’s Discussion and Analysis of Financial Condition and Results of Operations” is in our 2013 Annual Report to Shareholders presented on page F-11 of Exhibit 13 to this document. We incorporate that information in this document by reference.

Item 8. | FINANCIAL STATEMENTS AND SUPPLEMENTARY DATA. |

We refer you to the Index to Financial Statements attached hereto on page 23 for a listing of all financial statements in our 2013 Annual Report to Shareholders. This report is attached as part of Exhibit 13 to this document. We incorporate those financial statements in this document by reference.

Item 9. | CHANGES IN AND DISAGREEMENTS WITH ACCOUNTANTS ON ACCOUNTING AND FINANCIAL DISCLOSURE. |

None.

17

Item 9A. | CONTROLS AND PROCEDURES. |

Disclosure Controls and Procedures

Based on their evaluation of our disclosure controls and procedures (as defined in Rules 13a-15 and 15d-15 under the Securities Exchange Act of 1934 [the “Exchange Act”]), as of the end of the period covered by this Annual Report on Form 10-K, our principal executive officer and principal financial officer have concluded that our disclosure controls and procedures were effective.

Management’s Report on Internal Control over Financial Reporting

“Management’s Report on Internal Control over Financial Reporting” and the attestation report of the independent registered public accounting firm of KPMG, LLP on internal control over financial reporting are in our 2013 Annual Report to Shareholders and are presented on pages F-30 through F-32 of Exhibit 13 to this document. We incorporate these reports in this document by reference.

Internal Control over Financial Reporting

There were no changes in our internal control over financial reporting during our fourth quarter ended June 26, 2013, that have materially affected or are reasonably likely to materially affect, our internal control over financial reporting.

Item 9B. | OTHER INFORMATION. |

None.

PART III

Item 10. | DIRECTORS, EXECUTIVE OFFICERS AND CORPORATE GOVERNANCE. |

If you would like information about:

• | our executive officers, |

• | our Board of Directors, including its committees, and |

• | our Section 16(a) reporting compliance, |

you should read the sections entitled “Election of Directors—Information About Nominees”, “Committees of the Board of Directors”, “Executive Officers”, and “Section 16(a) Beneficial Ownership Reporting Compliance” in our Proxy Statement to be dated on or about September 17, 2013, for the annual meeting of shareholders on November 7, 2013. We incorporate that information in this document by reference.

The Board of Directors has adopted a code of ethics that applies to all of the members of Board of Directors and all of our team members, including, the principal executive officer, principal financial officer, principal accounting officer or controller, or persons performing similar functions. A copy of the code is posted on our internet website at the internet address: http://www.brinker.com/corp_gov/ethical_business_ policy.asp. You may obtain free of charge copies of the code from our website at the above internet address. Any amendment of, or waiver from, our code of ethics will be posted on our website within four business days of such amendment or waiver.

Item 11. | EXECUTIVE COMPENSATION. |

If you would like information about our executive compensation, you should read the section entitled “Executive Compensation—Compensation Discussion and Analysis” in our Proxy Statement to be dated on or about September 17, 2013, for the annual meeting of shareholders on November 7, 2013. We incorporate that information in this document by reference.

Item 12. | SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND MANAGEMENT AND RELATED STOCKHOLDER MATTERS. |

If you would like information about our security ownership of certain beneficial owners and management and related stockholder matters, you should read the sections entitled “Director Compensation for Fiscal 2013”, “Compensation Discussion and Analysis”, and “Stock Ownership of Certain Persons” in our Proxy Statement to be dated on or about September 17, 2013, for the annual meeting of shareholders on November 7, 2013. We incorporate that information in this document by reference.

18

Item 13. | CERTAIN RELATIONSHIPS AND RELATED TRANSACTIONS, AND DIRECTOR INDEPENDENCE. |

If you would like information about certain relationships and related transactions, you should read the section entitled “Compensation Committee Interlocks and Insider Participation” in our Proxy Statement to be dated on or about September 17, 2013, for the annual meeting of shareholders on November 7, 2013. We incorporate that information in this document by reference.

If you would like information about the independence of our non-management directors and the composition of the Audit Committee, Compensation Committee and Governance and Nominating Committee, you should read the sections entitled “Director Independence” and “Committees of the Board of Directors” in our Proxy Statement to be dated on or about September 17, 2013, for the annual meeting of shareholders on November 7, 2013. We incorporate that information in this document by reference.

Item 14. | PRINCIPAL ACCOUNTANT FEES AND SERVICES. |

If you would like information about principal accountant fees and services, you should read the section entitled “Ratification of Independent Auditors” in our Proxy Statement to be dated on or about September 17, 2013, for the annual meeting of shareholders on November 7, 2013. We incorporate that information in this document by reference.

19

PART IV

Item 15. | EXHIBITS AND FINANCIAL STATEMENT SCHEDULES. |

(a)(1) Financial Statements.

We make reference to the Index to Financial Statements attached to this document on page 23 for a listing of all financial statements attached as Exhibit 13 to this document.

(a)(2) Financial Statement Schedules.

None.

(a)(3) Exhibits.

We make reference to the Index to Exhibits preceding the exhibits attached hereto on pages E-1 and E-2 for a list of all exhibits filed as a part of this document.

20

SIGNATURES

Pursuant to the requirements of Section 13 or 15(d) of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned, thereunto duly authorized.

BRINKER INTERNATIONAL, INC., a Delaware corporation | |||

By: | /S/ GUY J. CONSTANT | ||

Guy J. Constant, Executive Vice President, Chief Financial Officer and President of Global Business Development | |||

Dated: August 26, 2013