Exhibit 99.1

KINROSS GOLD CORPORATION

ANNUAL INFORMATION FORM

FOR THE YEAR ENDED DECEMBER 31, 2011

Dated March 29, 2012

TABLE OF CONTENTS

|

|

Page |

|

CAUTIONARY STATEMENT |

3 |

|

CORPORATE STRUCTURE |

4 |

|

GENERAL DEVELOPMENT OF THE BUSINESS |

6 |

|

DESCRIPTION OF THE BUSINESS |

8 |

|

Employees |

8 |

|

Competitive Conditions |

9 |

|

Environmental Protection |

9 |

|

Operations |

10 |

|

Gold Equivalent Production (Ounces) and Sales |

11 |

|

Marketing |

12 |

|

Kinross Mineral Reserves and Mineral Resources |

13 |

|

Kinross Material Properties |

22 |

|

Fort Knox and Area, Alaska, United States |

22 |

|

Paracatu, Brazil |

28 |

|

Kupol mine, Russian Federation |

34 |

|

Tasiast, Mauritania |

41 |

|

Other Kinross Properties |

47 |

|

RISK FACTORS |

56 |

|

DIVIDEND POLICY |

68 |

|

LEGAL PROCEEDINGS AND REGULATORY ACTIONS |

68 |

|

DESCRIPTION OF CAPITAL STRUCTURE |

69 |

|

MARKET PRICE FOR KINROSS SECURITIES |

70 |

|

DIRECTORS AND OFFICERS |

71 |

|

CEASE TRADE ORDERS, BANKRUPTCIES, PENALTIES OR SANCTIONS |

76 |

|

CONFLICT OF INTEREST |

76 |

|

INTEREST OF MANAGEMENT AND OTHERS IN MATERIAL TRANSACTIONS |

77 |

|

TRANSFER AGENT AND REGISTRAR |

77 |

|

MATERIAL CONTRACTS |

77 |

|

INTERESTS OF EXPERTS |

77 |

|

AUDIT AND RISK COMMITTEE |

78 |

|

ADDITIONAL INFORMATION |

79 |

|

GLOSSARY OF TECHNICAL TERMS |

80 |

|

SCHEDULE “A” - CHARTER OF THE AUDIT AND RISK COMMITTEE |

A-1 |

|

SCHEDULE “I” — INDEPENDENCE REQUIREMENT OF NATIONAL INSTRUMENT 52-110 |

I-1 |

IMPORTANT NOTICE

ABOUT INFORMATION IN THIS ANNUAL INFORMATION FORM

Unless specifically stated otherwise in this Annual Information Form:

· all dollar amounts are in United States dollars;

· information is presented as at December 31, 2011; and

· references to “Kinross”, the “Company”, “its”, “our” and “we”, or related terms, refer to Kinross Gold Corporation and its subsidiaries.

CAUTIONARY STATEMENT

All statements, other than statements of historical fact, contained or incorporated by reference in this Annual Information Form including, but not limited to, any information as to the future financial or operating performance of Kinross, constitute “forward-looking information” or “forward-looking statements” within the meaning of certain securities laws, including the provisions of the Securities Act (Ontario) and the provisions for “safe harbour” under the United States Private Securities Litigation Reform Act of 1995 and are based on expectations, estimates and projections as of the date of this Annual Information Form. Forward-looking statements include, without limitation, possible events, statements with respect to possible events, the future price of gold and silver, the estimation of mineral reserves and mineral resources, the realization of mineral reserve and resource estimates, the timing and amount of estimated future production, costs of production, expected capital expenditures, costs and timing of the development of new deposits, success of exploration, development and mining activities, permitting time lines, currency fluctuations, requirements for additional capital, government regulation of mining operations, environmental risks, unanticipated reclamation expenses, title disputes or claims and limitations on insurance coverage. The words “plans”, “expects” or “does not expect”, “is expected”, “budget”, “scheduled”, “estimates”, “targets”, “forecasts”, “intends”, “anticipates”, or “does not anticipate”, or “believes”, or variations of such words and phrases or statements that certain actions, events or results “may”, “could”, “would”, “should”, “might”, or “will be taken”, “occur” or “be achieved” and similar expressions identify forward-looking statements. Forward-looking statements are necessarily based upon a number of estimates and assumptions that, while considered reasonable by Kinross as of the date of such statements, are inherently subject to significant business, economic and competitive uncertainties and contingencies. The estimates, models and assumptions of Kinross referenced, contained or incorporated by reference in this Annual Information Form, which may prove to be incorrect, include, but are not limited to, the various assumptions set forth herein and in our most recently filed Management’s Discussion and Analysis, as well as: (1) there being no significant disruptions affecting the operations of the Company or any entity in which it now or hereafter directly or indirectly holds an investment, whether due to labour disruptions, supply disruptions, power disruptions, damage to equipment or otherwise; (2) permitting, development, operations, expansion and acquisitions at Paracatu (including, without limitation, land acquisitions and permitting for the construction and operation of the new tailings facility) being consistent with our current expectations; (3) development of and production from the Phase 7 pit expansion and heap leach project at Fort Knox continuing on a basis consistent with Kinross’ current expectations; (4) the viability, permitting and development of the Fruta del Norte deposit, and its continuing ownership by the Company, being consistent with Kinross’ current expectations; (5) political and legal developments in any jurisdiction in which the Company, or any entity in which it now or hereafter directly or indirectly holds an investment, operates being consistent with its current expectations including, without limitation, the implementation of Ecuador’s new mining and investment laws and related regulations and policies, and negotiation of an exploitation agreement and investment protection agreement with the government (on terms satisfactory to Kinross), being consistent with Kinross’ current expectations; (6) permitting, construction, development and production at Cerro Casale being consistent with the Company’s current expectations; (7) the viability, permitting and development of the Lobo-Marte project, including, without limitation, the metallurgy and processing of its ore, being consistent with our current expectations; (8) the exchange rate between the Canadian dollar, Brazilian real, Chilean peso, Russian rouble, Mauritanian ouguiya, Ghanaian cedi and the U.S. dollar being approximately consistent with current levels; (9) certain price assumptions for gold and silver; (10) prices for natural gas, fuel oil, electricity and other key supplies being approximately consistent with current levels; (11) production and cost of sales forecasts for the Company, and entities in which it now or hereafter directly or indirectly holds an investment, meeting expectations; (12) the accuracy of the current mineral reserve and mineral resource estimates of the Company and any entity in which it now or hereafter directly or indirectly holds an investment; (13) labour and materials costs increasing on a basis consistent with Kinross’ current expectations; (14) the development of the Dvoinoye and Vodorazdelnaya deposits being consistent with Kinross’ expectations; (15) the viability of the Tasiast and Chirano mines, and the permitting, development and expansion of the Tasiast and Chirano mines on a basis consistent with

Kinross’ current expectations, including but not limited to the terms and conditions of the legal and fiscal stability agreements for these operations being interpreted and applied in a manner consistent with their intent and Kinross’ expectations; and (16) access to capital markets, including but not limited to securing project financing for Dvoinoye, Fruta del Norte and the Tasiast expansion projects, being consistent with the Company’s current expectations. Known and unknown factors could cause actual results to differ materially from those projected in the forward-looking statements. Such factors include, but are not limited to: fluctuations in the currency markets; fluctuations in the spot and forward price of gold or certain other commodities (such as diesel fuel and electricity); changes in interest rates or gold or silver lease rates that could impact the mark-to-market value of outstanding derivative instruments and ongoing payments/receipts under any interest rate swaps and variable rate debt obligations; risks arising from holding derivative instruments (such as credit risk, market liquidity risk and mark-to-market risk); changes in national and local government legislation, taxation, (including but not limited to income tax, advance income tax, stamp withholding tax, capital tax, tariffs, value-added or sales tax, capital outflow tax, capital gains tax, windfall or windfall profits tax, royalty, excise tax, customs/import or export duties, asset taxes, asset transfer tax, property use or other real estate tax, together with any related fine, penalty, surcharge, or interest imposed in connection with such taxes, controls, policies and regulations), the security of personnel and assets and political or economic developments in Canada, the United States, Chile, Brazil, Russia, Ecuador, Mauritania, Ghana or other countries in which Kinross, or entities in which it now or hereafter directly or indirectly holds an investment do business or may carry on business in the future; business opportunities that may be presented to, or pursued by, us; our ability to successfully integrate acquisitions and complete divestitures; operating or technical difficulties in connection with mining or development activities; employee relations; commencement of litigation against the Company, including but not limited to, securities class action in Canada and/or the US; the speculative nature of gold exploration and development, including the risks of obtaining necessary licenses and permits; diminishing quantities or grades of reserves; adverse changes in our credit rating; and contests over title to properties, particularly title to undeveloped properties. In addition, there are risks and hazards associated with the business of gold exploration, development and mining, including environmental hazards, industrial accidents, unusual or unexpected formations, pressures, cave-ins, flooding and gold bullion losses (and the risk of inadequate insurance, or the inability to obtain insurance, to cover these risks). Many of these uncertainties and contingencies can directly or indirectly affect, and could cause, Kinross’ actual results to differ materially from those expressed or implied in any forward-looking statements made by, or on behalf of, Kinross. There can be no assurance that forward-looking statements will prove to be accurate, as actual results and future events could differ materially from those anticipated in such statements. Forward-looking statements are provided for the purpose of providing information about management’s expectations and plans relating to the future. All of the forward-looking statements made in this Annual Information Form are qualified by these cautionary statements and those made in our other filings with the securities regulators of Canada and the United States including, but not limited to, the cautionary statements made in the “Risk Analysis” section of our most recently filed Management’s Discussion and Analysis. These factors are not intended to represent a complete list of the factors that could affect Kinross. Kinross disclaims any intention or obligation to update or revise any forward-looking statements or to explain any material difference between subsequent actual events and such forward-looking statements, except to the extent required by applicable law.

CORPORATE STRUCTURE

Kinross Gold Corporation was initially created in May 1993 by the amalgamation of CMP Resources Ltd., Plexus Resources Corporation, and 1021105 Ontario Corp. In December 2000, Kinross amalgamated with LT Acquisition Inc.; in January 2005, Kinross amalgamated with its wholly-owned subsidiary, TVX Gold Inc. (“TVX”); in January 2006, it amalgamated with its wholly-owned subsidiary, Echo Bay Mines Ltd. (“Echo Bay”); and in January 2011, it amalgamated with Underworld Resources Inc. (“Underworld”). Kinross is the continuing entity resulting from these amalgamations. Kinross is governed by the Business Corporations Act (Ontario) and its registered and principal offices are located at 25 York Street, 17th Floor, Toronto, Ontario, M5J 2V5.

Each of Kinross’ mining operations is a separate business unit managed by its Vice-President and General Manager, who in turn, reports to a Regional Vice-President, who then reports to the Chief Operating Officer. Exploration strategies, corporate financing, tax planning, additional technical support services, hedging and acquisition strategies are managed centrally. Execution of site/regional exploration strategies is managed locally. Kinross’ risk management programs are subject to overview by its Audit and Risk Committee and the Board of Directors.

A significant portion of Kinross’ business is carried on through subsidiaries. A chart showing the names of the significant subsidiaries of Kinross and their respective jurisdictions of incorporation, is set out below as of December 31, 2011. All subsidiaries are 100% owned unless otherwise noted.

GENERAL DEVELOPMENT OF THE BUSINESS

Overview

Kinross is principally engaged in the mining and processing of gold and, as a by-product, silver ore and the exploration for, and the acquisition of, gold bearing properties in the Americas, the Russian Federation, West Africa and worldwide. The principal products of Kinross are gold and silver produced in the form of doré that is shipped to refineries for final processing.

Kinross’ strategy is to increase shareholder value through increases in precious metal reserves, net asset value, production, long-term cash flow and earnings per share. Kinross’ strategy also consists of optimizing the performance, and therefore, the value, of existing operations, investing in quality exploration and development projects and acquiring new potentially accretive properties and projects.

Kinross’ operations and mineral reserves are impacted by, among other things, changes in metal prices. The average gold price during 2011 was approximately $1570 ($1225 during 2010). Kinross used a gold price of $1200 per ounce at the end of 2011 to estimate mineral reserves.

Kinross’ share of proven and probable mineral reserves as at December 31, 2011, was 62.6 million ounces of gold, 84.9 million ounces of silver and 1.4 billion pounds of copper.

Three Year History

The acquisition of 100% of the outstanding shares of Aurelian Resources Inc. (“Aurelian”) was completed on September 30, 2008 for aggregate consideration consisting of approximately 43.7 million common shares of Kinross and approximately 19.7 million warrants, each warrant being exercisable for one Kinross common share at an exercise price of $32.00. As a result of the acquisition, Kinross acquired a 100% interest in the Fruta del Norte (“FDN”) and Condor deposits in Ecuador as well as substantial exploration ground.

On December 16, 2008, Kinross completed the acquisition of a 40% interest in Minera Santa Rose SCM (“Minera”) from certain subsidiaries of Anglo American Plc (“Anglo”), and on January 8, 2009 Kinross acquired the remaining 60% interest in Minera from a subsidiary of Teck Cominco Limited (“Teck”). Kinross holds a 100% interest in the Lobo-Marte gold project in Chile. The aggregate purchase price for the acquisition of Minera consisted of $180 million in cash and approximately $70 million in Kinross common shares, plus a royalty on future production payable to Teck.

On February 5, 2009, Kinross completed the sale of 24,035,000 common shares at a price of $17.25 per common share. Kinross sold the common shares to certain underwriters pursuant to an underwriting agreement dated January 22, 2009. Kinross received net proceeds of approximately $396 million, which are being used to enhance the Company’s capital position following the funding of the approximately $180 million cash portion of the purchase price for acquisitions made in 2008 and 2009, with the balance being used for general corporate purposes.

On March 19, 2009 Kinross entered into a subscription agreement with Harry Winston Diamond Corporation (“Harry Winston”) pursuant to which, subject to certain terms and conditions, Kinross agreed to make a net investment of $150 million in exchange for a 22.5% minority interest in the partnership that holds Harry Winston’s 40% interest in the Diavik Diamond Mine joint venture and a 19.9% equity interest in Harry Winston. The transaction was completed on March 31, 2009.

In September 2009, Kinross and Barrick Gold Corporation (“Barrick”) entered into a joint venture agreement in respect of the Cerro Casale property, pursuant to which the parties restructured their shareholdings in the joint venture company so that each of Barrick and Kinross held a 50% interest.

On December 2, 2009 Companhia Nacional De Mineração (“CNM”), a subsidiary of Kinross, closed a sale to Jaguar Mining Inc. (“Jaguar”) pursuant to which Jaguar purchased all of the shares held by CNM in MCT Mineração Ltda. (“MCT”, which holds the Gurupi project located in Brazil) for a purchase price of $42.5 million, which was paid through the issuance of 3,377,354 Jaguar common shares.

On January 20, 2010, Kinross entered into an agreement to acquire the Dvoinoye deposit and the Vodorazdelnaya property, both located approximately 90 kilometres north of Kinross’ Kupol operation in the Chukotka region of the Russian Far East, from Northern Gold LLC and Regionruda LLC. The purchase price for the transaction was $346.8 million, comprising $167 million in cash and approximately 10.6 million Kinross shares, which were issued from treasury. The transaction was completed on August 27, 2010.

On February 17, 2010, Kinross entered into an agreement with Barrick to sell one-half of its 50% interest in the Cerro Casale project in Chile to Barrick for a total value of $474.3 million, comprising $454.3 million in cash, plus the assumption by Barrick of a $20 million contingent obligation. The transaction was completed on March 31, 2010.

On March 15, 2010, Kinross entered into a support agreement with Underworld whereby Kinross agreed to make an offer to purchase all of the outstanding common shares of Underworld, other than common shares of Underworld held directly or indirectly by Kinross, on the basis of 0.141 of a common share of Kinross, plus Cdn.$0.01 per Underworld common share, and Underworld agreed to support the offer. The transaction was completed on June 30, 2010.

On May 7, 2010, Kinross closed a CAD $600 million private placement into Red Back Mining Inc. (“Red Back”). As a result of the transaction, Kinross held 24 million common shares of Red Back, representing approximately 9.4% of Red Back’s issued and outstanding common shares.

On July 23, 2010, Kinross entered into an agreement with a group of financial institutions to sell its approximate 19.9% equity interest in Harry Winston, consisting of 15.2 million Harry Winston common shares, on an underwritten block trade basis, for net proceeds of $185.6 million. The sale was completed on July 28, 2010.

On August 25, 2010, Kinross completed the sale of its 22.5% interest in the partnership holding Harry Winston’s 40% interest in the Diavik Diamond Mines joint venture to Harry Winston for final net proceeds of $190 million. The purchase price was comprised of $50 million cash, approximately 7.1 million Harry Winston common shares (with a value of $69.7 million at the time that the transaction closed), and a note receivable in the amount of $70 million maturing 12 months from the transaction date. The note bore interest at a rate of 5% per annum and was repaid in cash by Harry Winston to Kinross on August 25, 2011. On March 23, 2011, Kinross entered into an agreement with a group of financial institutions to sell its approximate 8.5% equity interest in Harry Winston, consisting of approximately 7.1 million common shares, on an underwritten block trade basis for net proceeds of approximately $100.6 million.

On August 27, 2010, Kinross completed the acquisition of B2Gold Corporation’s (“B2Gold”) right to an interest in the Kupol East and Kupol West exploration licence areas. Under the terms of a previous agreement, Kinross had undertaken to secure a 37.5% joint venture interest for B2Gold in the Kupol East and Kupol West exploration licence areas. According to the new agreement, Kinross is no longer obligated to enter into joint venture arrangements with B2Gold in respect of Kinross’ 75% interest in these licence areas. In exchange, Kinross paid B2Gold $33 million in cash on closing and agreed to contingent payments based on National Instrument 43-101 qualified proven and probable gold reserves at the subject properties, should such gold reserves be declared in future and payments based on 1.5% net smelter returns of from any future production at the properties.

On September 17, 2010, Kinross completed the acquisition of all of the issued and outstanding common shares of Red Back for total consideration of approximately $8.7 billion, including the cost of a previously owned interest. In accordance with the arrangement agreement, former Red Back shareholders received 1.778 Kinross common shares plus 0.11 of a Kinross common share purchase warrant for each common share of Red Back. Each whole warrant is exercisable for a period of four years at an exercise price of $21.30 per Kinross common share.

On March 31, 2011, Kinross amended its unsecured revolving credit facility. The changes to the facility included an increase of available credit from $600 million to $1.2 billion. The facility will expire on March 31, 2015.

On April 27, 2011, Kinross entered into a Share Purchase Agreement with the State Unitary Enterprise of the Chukotka Autonomous Okrug or “CUE”, to repurchase the 2,292,348 shares of CMGC held by CUE, representing 25.01% of CMGC’s outstanding share capital, for an approximate consideration of $335 million, including transaction costs. As a result Kinross owns 100% of CMGC, which in turn, holds both the Kupol mine and the Kupol East-West exploration licences in the Chukotka region of the Russian Federation.

On August 22, 2011, Kinross completed a $1 billion offering of debt securities, consisting of $250 million principal amount of its 3.625% Senior Notes due 2016, $500 million principal amount of its 5.125% Senior Notes due 2021 and $250 million principal amount of its 6.875% Senior Notes due 2041 (collectively, the “notes”). The notes are unsecured, senior obligations of Kinross and are wholly and unconditionally guaranteed by certain of Kinross’ wholly-owned subsidiaries that are also guarantors under Kinross’ senior unsecured credit agreement.

On December 22, 2011, Kinross announced that it had completed a $200 million non-recourse loan issued to CMGC by a group of international financial institutions. The non-recourse loan carries a term of five years, with annual interest of London Inter Bank Offered Rate plus 2.5%.

On February 15, 2012, Kinross announced an update regarding its previously announced capital and project optimization process. As a result of that process, Kinross confirmed that the Tasiast and then Dvoinoye projects remained the key development priorities, and the expected development timelines for the Fruta Del Norte and Lobo-Marte projects would be extended.

DESCRIPTION OF THE BUSINESS

Kinross is principally engaged in the exploration for, and acquisition, development and operation of, gold-bearing properties. The material properties of Kinross as of December 31, 2011 were as follows:

|

Property (1) |

|

Location |

|

Property |

|

|

Fort Knox |

|

Alaska, United States |

|

100 |

% |

|

Paracatu |

|

Minas Gerais, Brazil |

|

100 |

% |

|

Kupol |

|

Russian Federation |

|

100 |

%(2) |

|

Tasiast |

|

Mauritania |

|

100 |

% |

(1) The Fort Knox, Paracatu and Tasiast properties are subject to various royalties (See “Kinross Material Properties” — “Fort Knox and Area, Alaska, United States” and “Paracatu, Brazil” and “Tasiast, Mauritania”).

(2) On April 27, 2011, Kinross acquired the 25% of Kupol it did not already own through its subsidiary, Chukotka Mining and Geological Company (“CMGC”), giving Kinross 100% ownership of the Kupol mine.

In addition, as of December 31, 2011, Kinross held a 50% interest in the Crixas mine, situated in Brazil, a 100% interest in the Kettle River property in Washington, United States, which includes the Kettle River mill and the Buckhorn mine, a 50% interest in the Round Mountain mine in Nevada, United States, a 100% interest in the La Coipa mine in Chile, a 90% interest in the Chirano mine in Ghana, a 100% interest in the Lobo-Marte property in Chile, a 25% interest in the Cerro Casale property in Chile, a 100% interest in the Maricunga mine in Chile, a 100% interest in the FDN project in Ecuador and other mining properties in various stages of exploration, development, reclamation, and closure. The Company’s principal product is gold and it also produces silver as a byproduct.

Employees

At December 31, 2011 Kinross and its subsidiaries employed approximately 8,230 persons. Kinross’ employees in the United States, Canada and Russia are non-unionized. In Chile, both of La Coipa’s collective agreements were successfully negotiated and will extend until July 31, 2014. Maricunga has three collective agreements in place, two of which expire on February 28, 2014 (relating to operations employees) and one of which expires on December 31, 2012

(relating to a supervisory employee). In Ecuador, the employees at Fruta del Norte are represented by an employee association. Paracatu, Brazil has an annual collective bargaining process, with the agreement having an annual expiry date of January 31st. In West Africa, employees at both the Chirano and Tasiast mines are represented by unions. Chirano’s agreements with its union and association expire at the end of August 2012. At Tasiast, a new delegation of union representatives will be elected by the employees in April 2012 following which it is expected that a multi-year collective agreement will be negotiated. Kinross considers the status of its employee relations to be very positive.

Competitive Conditions

The precious metal mineral exploration and mining business is a competitive business. Kinross competes with numerous other companies and individuals in the search for and the acquisition of attractive precious metal mineral properties. The ability of Kinross to replace or increase its mineral reserves and mineral resources in the future will depend not only on its ability to develop its present properties, but also on its ability to select and acquire suitable producing properties or prospects for precious metal development or mineral exploration.

Environmental Protection

Kinross’ exploration activities and mining and processing operations are subject to the federal, state, provincial, regional and local environmental laws and regulations in the jurisdictions in which Kinross’ activities and facilities are located. For example, in the United States, Kinross is subject to a number of such laws and regulations including, without limitation: the Clean Air Act; the Clean Water Act; the Comprehensive Environmental Response, Compensation and Liability Act; the Emergency Planning and Community Right to Know Act; the Endangered Species Act; the Federal Land Policy and Management Act; the National Environmental Policy Act; the Resource Conservation and Recovery Act; and related state laws.

Kinross is subject to similar laws in other jurisdictions in which it operates. In all jurisdictions in which Kinross operates, environmental licenses, permits and other regulatory approvals are required in order to engage in exploration, mining and processing, and mine closure activities. Regulatory approval of a detailed plan of operations and a comprehensive environmental impact assessment is required prior to initiating mining or processing activities or for any substantive change to previously approved plans. In all jurisdictions in which Kinross operates, specific statutory and regulatory requirements and standards must be met throughout the life of the mining or processing operations in regard to air quality, water quality, fisheries, wildlife and biodiversity protection, archaeological and cultural resources, solid and hazardous waste management and disposal, the management and transportation of hazardous chemicals, toxic substances, noise, community right-to-know, land use, and reclamation. Except as may be otherwise disclosed herein, Kinross is currently in compliance, in all material respects, with all material applicable environmental laws and regulations. Details and quantification of the Company’s reclamation and remediation obligations are set out in Note 14 to the audited Consolidated Financial Statements of the Company for the year ended December 31, 2011.

At Kinross, a strong environmental ethic and sound environmental management program have been integrated with core business functions at all levels, and at all locations throughout the organization.

As part of Kinross’ Corporate Responsibility Management System, corporate environmental governance programs that Kinross has implemented include:

STANDARDS — Corporate environmental management standards provide a clear bottom line for all Kinross activities in all jurisdictions in which we carry on business. Where legal requirements are unclear, Kinross’ environmental management standards provide clear direction regarding performance expectations and minimum design and operating requirements.

An example of this is Kinross’ decision to adopt the standards that comprise the International Cyanide Management Code for the Manufacture, Transport and Use of cyanide in the Production of Gold (the “Cyanide Code”). Kinross is a signatory to the Cyanide Code, which is administered by the International Cyanide Management Institute (the “ICMI”). The ICMI is an independent body that was established by a multi-stakeholder group under the guidance of the United Nations Environmental Program. The ICMI established operating standards for cyanide manufacturers, transporters and mines and provides for third party certification of facilities’ compliance

with the Cyanide Code. All Kinross operations have either already been certified as compliant with the Cyanide Code or are preparing to be certified.

AUDITS - Comprehensive environmental compliance audits are conducted at all operations and at selected residual properties on a biennial basis. The audit program assesses compliance with applicable legal requirements, measures effectiveness of management systems, and includes procedures to ensure timely follow-up on audit findings.

METRICS - Kinross has identified operational parameters that are key indicators of environmental performance, and measures these indicators on a regular basis. The Company tracks an index of these key performance indicators and sets performance targets to encourage continuous environmental improvement.

ENGINEERING - To effectively manage environmental risk, a program is in place to assess the management and stability of tailings and heap leach facilities. It includes a detailed water balance accounting, to assure sufficient storage capacity, and a review of operational procedures. Every Kinross operation has a tailings or heap management plan in place. In addition, Kinross performs periodic assessments of engineered systems to assure adequate secondary systems are in place to minimize or eliminate environmental risks.

RECLAMATION - Kinross recognizes its responsibility to manage the environmental change associated with its operations, and requires all material sites to develop and maintain reclamation and closure plans to address the Company’s reclamation and closure obligations in a way that demonstrates excellence and establishes industry-wide leadership through example.

The results of these programs have been recognized by others within and outside the mining industry. Examples of significant recognition of Kinross’ efforts are listed on Kinross’ website at www.kinross.com.

Operations

Kinross’ production in 2011 was derived from the mines in North America (25%), South America (36%), West Africa (17%) and the Russian Federation (22%). The following shows the location of Kinross’ properties as of the date hereof.

Gold Equivalent Production and Sales

The following table summarizes attributable production and sales by Kinross in the last three years:

|

|

|

Years ended December 31, |

| ||||

|

|

|

2011 |

|

2010 |

|

2009 |

|

|

|

|

|

|

|

|

|

|

|

Gold equivalent production — ounces |

|

2,610,373 |

|

2,334,104 |

|

2,238,665 |

|

|

|

|

|

|

|

|

|

|

|

Gold equivalent sales - ounces |

|

2,611,287 |

|

2,343,505 |

|

2,251,189 |

|

Included in gold equivalent production and sales is silver production and sales, as applicable, converted into gold production using a ratio of the average spot market prices of gold and silver for the three comparative years. The ratios were 44.65:1 in 2011, 60.87:1 in 2010 and 66.97:1 in 2009.

The following table sets forth the attributable gold equivalent production (in ounces) reflective of Kinross’ interest in each of its operating assets during the last three years:

|

|

|

2011 |

|

2010 |

|

2009 |

|

|

North America: |

|

|

|

|

|

|

|

|

Fort Knox |

|

289,794 |

|

349,729 |

|

263,260 |

|

|

Round Mountain (1) |

|

187,444 |

|

184,554 |

|

213,916 |

|

|

Kettle River-Buckhorn |

|

175,292 |

|

198,810 |

|

173,555 |

|

|

Total |

|

652,530 |

|

733,093 |

|

650,731 |

|

|

|

|

|

|

|

|

|

|

|

South America: |

|

|

|

|

|

|

|

|

Paracatu |

|

453,396 |

|

482,397 |

|

354,396 |

|

|

Maricunga |

|

236,249 |

|

156,590 |

|

233,585 |

|

|

La Coipa |

|

178,287 |

|

196,330 |

|

231,169 |

|

|

Crixas (1) |

|

66,583 |

|

74,777 |

|

74,654 |

|

|

Total |

|

934,515 |

|

910,094 |

|

893,804 |

|

|

|

|

|

|

|

|

|

|

|

West Africa |

|

|

|

|

|

|

|

|

Tasiast(2) |

|

200,619 |

|

56,611 |

|

N/A |

|

|

Chirano(2)(3) |

|

235,661 |

|

80,298 |

|

N/A |

|

|

Total |

|

436,280 |

|

136,909 |

|

|

|

|

|

|

|

|

|

|

|

|

|

Russian Federation: |

|

|

|

|

|

|

|

|

Kupol(4) |

|

587,048 |

|

554,008 |

|

694,130 |

|

(1) Represents Kinross’ 50% ownership interest.

(2) Kinross acquired Tasiast and Chirano on September 17, 2010 in the acquisition of Red Back.

(3) Represents Kinross’ 90% ownership interest.

(4) On April 27, 2011, Kinross acquired the remaining 25% of CMGC, and thereby obtained 100% ownership of Kupol. As such, the results up to April 27, 2011 reflect 75% and results thereafter reflect 100%.

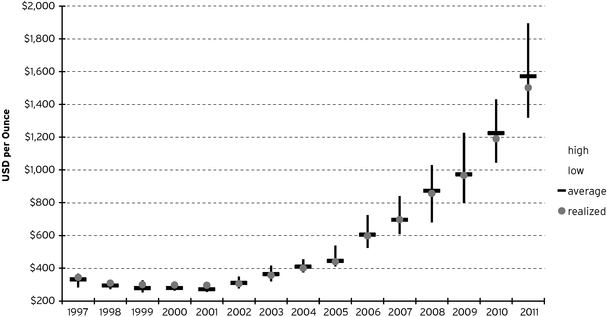

Marketing

Gold is a metal that is traded on world markets, with benchmark prices generally based on the London market. Gold has two principal uses: product fabrication and bullion investment. Fabricated gold has a wide variety of end uses, including jewellery manufacture (the largest fabrication component), electronics, dentistry, industrial and decorative uses, medals, medallions, and official coins. Gold bullion is held primarily as a store of value and a safeguard against devaluation of paper assets denominated in fiat currencies. Kinross sells all of its refined gold to banks, bullion dealers, and refiners. In 2011, sales to its top two customers totalled $1,421.3 million and $521.9 million, respectively, for an aggregate of $1,943.2 million. In 2010, sales to three customers totalled $1,152.7 million, $353.4 million and $353.1 million, respectively, for an aggregate of $1,859.2 million. Due to the size of the bullion market and the above ground inventory of bullion, activities by Kinross will generally not influence gold prices. Kinross believes that the loss of any of these customers would have no material adverse impact on Kinross because of the active worldwide market for gold.

The following table sets forth for the years indicated the high and low London Bullion Market afternoon fix prices for gold:

|

Year |

|

High |

|

Low |

|

Average |

| |||

|

2002 |

|

$ |

349.30 |

|

$ |

277.75 |

|

$ |

309.68 |

|

|

2003 |

|

$ |

416.25 |

|

$ |

319.90 |

|

$ |

363.32 |

|

|

2004 |

|

$ |

454.20 |

|

$ |

375.00 |

|

$ |

409.17 |

|

|

2005 |

|

$ |

536.50 |

|

$ |

411.10 |

|

$ |

444.45 |

|

|

2006 |

|

$ |

725.00 |

|

$ |

524.25 |

|

$ |

603.77 |

|

|

2007 |

|

$ |

841.10 |

|

$ |

608.40 |

|

$ |

695.39 |

|

|

2008 |

|

$ |

1,011.25 |

|

$ |

712.50 |

|

$ |

871.96 |

|

|

2009 |

|

$ |

1,212.50 |

|

$ |

810.00 |

|

$ |

972.35 |

|

|

2010 |

|

$ |

1,421.00 |

|

$ |

1,058.00 |

|

$ |

1,224.52 |

|

|

2011 |

|

$ |

1,895.00 |

|

$ |

1,319.00 |

|

$ |

1,570.25 |

|

Kinross Mineral Reserves and Mineral Resources

Definitions

The estimated mineral reserves and mineral resources for Kinross’ properties have been calculated in accordance with the Canadian Institute of Mining, Metallurgy and Petroleum (“CIM”) — Definitions Adopted by CIM Council on November 27, 2010 (the “CIM Standards”) which were adopted by the Canadian Securities Administrators’ National Instrument 43-101 Standards of Disclosure for Mineral Projects (the “Instrument”). The following definitions are reproduced from the CIM Standards:

A Mineral Resource is a concentration or occurrence of diamonds, natural solid inorganic material, or natural solid fossilized organic material including base and precious metals, coal, and industrial minerals in or on the Earth’s crust in such form and quantity and of such a grade or quality that it has reasonable prospects for economic extraction. The location, quantity, grade, geological characteristics and continuity of a Mineral Resource are known, estimated or interpreted from specific geological evidence and knowledge.

An Inferred Mineral Resource is that part of a Mineral Resource for which quantity and grade or quality can be estimated on the basis of geological evidence and limited sampling and reasonably assumed, but not verified, geological and grade continuity. The estimate is based on limited information and sampling gathered through appropriate techniques from locations such as outcrops, trenches, pits, workings and drill holes.

An Indicated Mineral Resource is that part of a Mineral Resource for which quantity, grade or quality, densities, shape and physical characteristics, can be estimated with a level of confidence sufficient to allow the appropriate application of technical and economic parameters, to support mine planning and evaluation of the economic viability of the deposit. The estimate is based on detailed and reliable exploration and testing information gathered through appropriate techniques from locations such as outcrops, trenches, pits, workings and drill holes that are spaced closely enough for geological and grade continuity to be reasonably assumed.

A Measured Mineral Resource is that part of a Mineral Resource for which quantity, grade or quality, densities, shape, and physical characteristics are so well established that they can be estimated with confidence sufficient to allow the appropriate application of technical and economic parameters, to support production planning and evaluation of the economic viability of the deposit. The estimate is based on detailed and reliable exploration, sampling and testing information gathered through appropriate techniques from locations such as outcrops, trenches, pits, workings and drill holes that are spaced closely enough to confirm both geological and grade continuity.

A Mineral Reserve is the economically mineable part of a Measured or Indicated Mineral Resource demonstrated by at least a Preliminary Feasibility Study. This Study must include adequate information on mining, processing, metallurgical, economic and other relevant factors that demonstrate, at the time of reporting, that economic extraction can be justified. A Mineral Reserve includes diluting materials and allowances for losses that may occur when the material is mined.

A Probable Mineral Reserve is the economically mineable part of an Indicated and, in some circumstances, a Measured Mineral Resource demonstrated by at least a Preliminary Feasibility Study. This Study must include adequate information on mining, processing, metallurgical, economic, and other relevant factors that demonstrate, at the time of reporting, that economic extraction can be justified.

A Proven Mineral Reserve is the economically mineable part of a Measured Mineral Resource demonstrated by at least a Preliminary Feasibility Study. This Study must include adequate information on mining, processing, metallurgical, economic, and other relevant factors that demonstrate, at the time of reporting, that economic extraction is justified.

Mineral Reserve and Mineral Resource Estimates

The following tables set forth the estimated mineral reserves and mineral resources attributable to interests held by Kinross for each of its properties:

|

MINERAL RESERVE AND MINERAL RESOURCE STATEMENT |

|

GOLD |

|

PROVEN AND PROBABLE MINERAL RESERVES (1),(3),(6),(7),(14) |

|

|

|

Kinross Gold Corporation’s Share at December 31, 2011 |

|

|

|

|

|

|

|

Kinross |

|

Proven |

|

Probable |

|

Proven and Probable |

| ||||||||||||

|

|

|

|

|

Interest |

|

Tonnes |

|

Grade |

|

Ounces |

|

Tonnes |

|

Grade |

|

Ounces |

|

Tonnes |

|

Grade |

|

Ounces |

|

|

Property |

|

Location |

|

(%) |

|

(kt) |

|

(g/t) |

|

(koz) |

|

(kt) |

|

(g/t) |

|

(koz) |

|

(kt) |

|

(g/t) |

|

(koz) |

|

|

NORTH AMERICA |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Fort Knox Area |

|

USA |

|

100.0 |

% |

141,633 |

|

0.39 |

|

1,763 |

|

173,036 |

|

0.46 |

|

2,540 |

|

314,669 |

|

0.43 |

|

4,303 |

|

|

Kettle River |

|

USA |

|

100.0 |

% |

— |

|

— |

|

— |

|

1,082 |

|

10.96 |

|

381 |

|

1,082 |

|

10.96 |

|

381 |

|

|

Round Mountain Area |

|

USA |

|

50.0 |

% |

24,968 |

|

0.70 |

|

563 |

|

50,048 |

|

0.53 |

|

849 |

|

75,016 |

|

0.59 |

|

1,412 |

|

|

SUBTOTAL |

|

|

|

|

|

166,601 |

|

0.43 |

|

2,326 |

|

224,166 |

|

0.52 |

|

3,770 |

|

390,767 |

|

0.49 |

|

6,096 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

SOUTH AMERICA |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Cerro Casale |

(10) |

Chile |

|

25.0 |

% |

57,425 |

|

0.65 |

|

1,195 |

|

241,975 |

|

0.59 |

|

4,616 |

|

299,400 |

|

0.60 |

|

5,811 |

|

|

Crixas |

(9) |

Brazil |

|

50.0 |

% |

1,859 |

|

3.35 |

|

200 |

|

1,458 |

|

3.73 |

|

175 |

|

3,317 |

|

3.52 |

|

375 |

|

|

Fruta del Norte |

|

Ecuador |

|

100.0 |

% |

— |

|

— |

|

— |

|

25,440 |

|

8.21 |

|

6,715 |

|

25,440 |

|

8.21 |

|

6,715 |

|

|

La Coipa |

(11) |

Chile |

|

100.0 |

% |

12,435 |

|

1.36 |

|

544 |

|

2,828 |

|

1.33 |

|

121 |

|

15,263 |

|

1.36 |

|

665 |

|

|

Lobo Marte |

(13) |

Chile |

|

100.0 |

% |

— |

|

— |

|

— |

|

164,230 |

|

1.14 |

|

6,028 |

|

164,230 |

|

1.14 |

|

6,028 |

|

|

Maricunga Area |

|

Chile |

|

100.0 |

% |

126,709 |

|

0.74 |

|

3,000 |

|

145,472 |

|

0.63 |

|

2,948 |

|

272,181 |

|

0.68 |

|

5,948 |

|

|

Paracatu |

|

Brazil |

|

100.0 |

% |

682,118 |

|

0.40 |

|

8,670 |

|

640,113 |

|

0.42 |

|

8,715 |

|

1,322,231 |

|

0.41 |

|

17,385 |

|

|

SUBTOTAL |

|

|

|

|

|

880,546 |

|

0.48 |

|

13,609 |

|

1,221,516 |

|

0.75 |

|

29,318 |

|

2,102,062 |

|

0.64 |

|

42,927 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

AFRICA |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Chirano |

|

Ghana |

|

90.0 |

% |

8,135 |

|

1.46 |

|

381 |

|

14,505 |

|

3.43 |

|

1,599 |

|

22,640 |

|

2.72 |

|

1,980 |

|

|

Tasiast |

|

Mauritania |

|

100.0 |

% |

88,808 |

|

1.75 |

|

4,990 |

|

40,075 |

|

1.92 |

|

2,467 |

|

128,883 |

|

1.80 |

|

7,457 |

|

|

SUBTOTAL |

|

|

|

|

|

96,943 |

|

1.72 |

|

5,371 |

|

54,580 |

|

2.32 |

|

4,066 |

|

151,523 |

|

1.94 |

|

9,437 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

RUSSIA |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Dvoinoye |

|

Russia |

|

100.0 |

% |

— |

|

— |

|

— |

|

1,950 |

|

17.80 |

|

1,116 |

|

1,950 |

|

17.80 |

|

1,116 |

|

|

Kupol |

|

Russia |

|

100.0 |

% |

2,073 |

|

10.09 |

|

673 |

|

7,488 |

|

9.63 |

|

2,319 |

|

9,561 |

|

9.73 |

|

2,992 |

|

|

SUBTOTAL |

|

|

|

|

|

2,073 |

|

10.09 |

|

673 |

|

9,438 |

|

11.32 |

|

3,435 |

|

11,511 |

|

10.66 |

|

4,108 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

TOTAL GOLD |

|

|

|

|

|

1,146,163 |

|

0.60 |

|

21,979 |

|

1,509,700 |

|

0.84 |

|

40,589 |

|

2,655,863 |

|

0.73 |

|

62,568 |

|

|

MINERAL RESERVE AND MINERAL RESOURCE STATEMENT |

|

SILVER |

|

PROVEN AND PROBABLE MINERAL RESERVES (1),(3),(6),(7) |

|

|

|

Kinross Gold Corporation’s Share at December 31, 2011 |

|

|

|

|

|

|

|

Kinross |

|

Proven |

|

Probable |

|

Proven and Probable |

| ||||||||||||

|

|

|

|

|

Interest |

|

Tonnes |

|

Grade |

|

Ounces |

|

Tonnes |

|

Grade |

|

Ounces |

|

Tonnes |

|

Grade |

|

Ounces |

|

|

Property |

|

Location |

|

(%) |

|

(kt) |

|

(g/t) |

|

(koz) |

|

(kt) |

|

(g/t) |

|

(koz) |

|

(kt) |

|

(g/t) |

|

(koz) |

|

|

NORTH AMERICA |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Round Mountain Area |

|

USA |

|

50.0 |

% |

110 |

|

7.8 |

|

28 |

|

11,492 |

|

7.1 |

|

2,616 |

|

11,602 |

|

7.1 |

|

2,644 |

|

|

SUBTOTAL |

|

|

|

|

|

110 |

|

7.8 |

|

28 |

|

11,492 |

|

7.1 |

|

2,616 |

|

11,602 |

|

7.1 |

|

2,644 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

SOUTH AMERICA |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Cerro Casale |

(10) |

Chile |

|

25.0 |

% |

57,425 |

|

1.9 |

|

3,522 |

|

241,975 |

|

1.4 |

|

11,150 |

|

299,400 |

|

1.5 |

|

14,672 |

|

|

Fruta del Norte |

|

Ecuador |

|

100.0 |

% |

— |

|

— |

|

— |

|

25,440 |

|

11.0 |

|

9,004 |

|

25,440 |

|

11.0 |

|

9,004 |

|

|

La Coipa |

(11) |

Chile |

|

100.0 |

% |

12,435 |

|

41.6 |

|

16,639 |

|

2,828 |

|

37.5 |

|

3,406 |

|

15,263 |

|

40.8 |

|

20,045 |

|

|

SUBTOTAL |

|

|

|

|

|

69,860 |

|

9.0 |

|

20,161 |

|

270,243 |

|

2.7 |

|

23,560 |

|

340,103 |

|

4.0 |

|

43,721 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

RUSSIA |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Dvoinoye |

|

Russia |

|

100.0 |

% |

— |

|

— |

|

— |

|

1,950 |

|

21.8 |

|

1,370 |

|

1,950 |

|

21.8 |

|

1,370 |

|

|

Kupol |

|

Russia |

|

100.0 |

% |

2,073 |

|

143.2 |

|

9,548 |

|

7,488 |

|

114.6 |

|

27,589 |

|

9,561 |

|

120.8 |

|

37,137 |

|

|

SUBTOTAL |

|

|

|

|

|

2,073 |

|

143.2 |

|

9,548 |

|

9,438 |

|

119.1 |

|

28,959 |

|

11,511 |

|

104.0 |

|

38,507 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

TOTAL SILVER |

|

|

|

|

|

72,043 |

|

12.8 |

|

29,737 |

|

291,173 |

|

5.9 |

|

55,135 |

|

363,216 |

|

7.3 |

|

84,872 |

|

|

MINERAL RESERVE AND MINERAL RESOURCE STATEMENT |

|

COPPER |

|

PROVEN AND PROBABLE MINERAL RESERVES (3),(6),(7) |

|

|

|

Kinross Gold Corporation’s Share at December 31, 2011 |

|

|

|

|

|

|

|

Kinross |

|

Proven |

|

Probable |

|

Proven and Probable |

| ||||||||||||

|

|

|

|

|

Interest |

|

Tonnes |

|

Grade |

|

Pounds |

|

Tonnes |

|

Grade |

|

Pounds |

|

Tonnes |

|

Grade |

|

Pounds |

|

|

Property |

|

Location |

|

(%) |

|

(kt) |

|

(%) |

|

(Mlb) |

|

(kt) |

|

(%) |

|

(Mlb) |

|

(kt) |

|

(%) |

|

(Mlb) |

|

|

SOUTH AMERICA |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Cerro Casale |

(10) |

Chile |

|

25.0 |

% |

57,425 |

|

0.19 |

|

240 |

|

241,975 |

|

0.23 |

|

1,204 |

|

299,400 |

|

0.22 |

|

1,444 |

|

|

SUBTOTAL |

|

|

|

|

|

57,425 |

|

0.19 |

|

240 |

|

241,975 |

|

0.23 |

|

1,204 |

|

299,400 |

|

0.22 |

|

1,444 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

TOTAL COPPER |

|

|

|

|

|

57,425 |

|

0.19 |

|

240 |

|

241,975 |

|

0.23 |

|

1,204 |

|

299,400 |

|

0.22 |

|

1,444 |

|

Measured and Indicated Mineral Resources

Cautionary Note to United States Investors Concerning Estimates of Measured and Indicated Mineral Resources

This section uses the terms “Measured” and “Indicated” mineral resources. United States investors are advised that while those terms are recognized and required by Canadian regulations, the United States Securities and Exchange Commission does not recognize them. United States investors are cautioned not to assume that all or any part of mineral deposits in these categories will ever be converted into proven and probable mineral reserves or recovered.

|

MINERAL RESERVE AND MINERAL RESOURCE STATEMENT |

|

GOLD |

|

MEASURED AND INDICATED MINERAL RESOURCES (EXCLUDES PROVEN AND PROBABLE MINERAL RESERVES) (2),(3),(4),(6),(7),(8) |

|

|

|

Kinross Gold Corporation’s Share at December 31, 2011 |

|

|

|

|

|

|

|

Kinross |

|

Measured |

|

Indicated |

|

Measured and Indicated |

| ||||||||||||

|

|

|

|

|

Interest |

|

Tonnes |

|

Grade |

|

Ounces |

|

Tonnes |

|

Grade |

|

Ounces |

|

Tonnes |

|

Grade |

|

Ounces |

|

|

Property |

|

Location |

|

(%) |

|

(kt) |

|

(g/t) |

|

(koz) |

|

(kt) |

|

(g/t) |

|

(koz) |

|

(kt) |

|

(g/t) |

|

(koz) |

|

|

NORTH AMERICA |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Fort Knox Area |

|

USA |

|

100.0 |

% |

7,638 |

|

0.33 |

|

81 |

|

104,460 |

|

0.40 |

|

1,345 |

|

112,098 |

|

0.40 |

|

1,426 |

|

|

Round Mountain Area |

|

USA |

|

50.0 |

% |

16,143 |

|

0.77 |

|

400 |

|

59,535 |

|

0.49 |

|

938 |

|

75,678 |

|

0.55 |

|

1,338 |

|

|

White Gold Area |

(12) |

Yukon |

|

100.0 |

% |

— |

|

— |

|

— |

|

9,797 |

|

3.19 |

|

1,005 |

|

9,797 |

|

3.19 |

|

1,005 |

|

|

SUBTOTAL |

|

|

|

|

|

23,781 |

|

0.63 |

|

481 |

|

173,792 |

|

0.59 |

|

3,288 |

|

197,573 |

|

0.59 |

|

3,769 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

SOUTH AMERICA |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Cerro Casale |

(10) |

Chile |

|

25.0 |

% |

5,853 |

|

0.29 |

|

55 |

|

68,534 |

|

0.35 |

|

777 |

|

74,387 |

|

0.35 |

|

832 |

|

|

Crixas |

(9) |

Brazil |

|

50.0 |

% |

238 |

|

4.87 |

|

37 |

|

283 |

|

3.70 |

|

34 |

|

521 |

|

4.23 |

|

71 |

|

|

Fruta del Norte |

|

Ecuador |

|

100.0 |

% |

— |

|

— |

|

— |

|

4,266 |

|

4.89 |

|

671 |

|

4,266 |

|

4.89 |

|

671 |

|

|

La Coipa |

(11) |

Chile |

|

100.0 |

% |

12,041 |

|

1.09 |

|

422 |

|

4,785 |

|

1.02 |

|

157 |

|

16,826 |

|

1.07 |

|

579 |

|

|

Lobo Marte |

(13) |

Chile |

|

100.0 |

% |

— |

|

— |

|

— |

|

34,052 |

|

0.83 |

|

908 |

|

34,052 |

|

0.83 |

|

908 |

|

|

Maricunga Area |

|

Chile |

|

100.0 |

% |

20,056 |

|

0.64 |

|

413 |

|

182,061 |

|

0.58 |

|

3,374 |

|

202,117 |

|

0.58 |

|

3,787 |

|

|

Paracatu |

|

Brazil |

|

100.0 |

% |

44,937 |

|

0.29 |

|

415 |

|

262,709 |

|

0.34 |

|

2,876 |

|

307,646 |

|

0.33 |

|

3,291 |

|

|

SUBTOTAL |

|

|

|

|

|

83,125 |

|

0.50 |

|

1,342 |

|

556,690 |

|

0.49 |

|

8,797 |

|

639,815 |

|

0.49 |

|

10,139 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

AFRICA |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Chirano |

|

Ghana |

|

90.0 |

% |

1,031 |

|

1.57 |

|

52 |

|

2,276 |

|

2.25 |

|

164 |

|

3,307 |

|

2.04 |

|

216 |

|

|

Tasiast |

|

Mauritania |

|

100.0 |

% |

119,307 |

|

0.62 |

|

2,367 |

|

283,909 |

|

0.96 |

|

8,738 |

|

403,216 |

|

0.86 |

|

11,105 |

|

|

SUBTOTAL |

|

|

|

|

|

120,338 |

|

0.63 |

|

2,419 |

|

286,185 |

|

0.97 |

|

8,902 |

|

406,523 |

|

0.87 |

|

11,321 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

RUSSIA |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Dvoinoye |

|

Russia |

|

100.0 |

% |

— |

|

— |

|

— |

|

243 |

|

17.79 |

|

139 |

|

243 |

|

17.79 |

|

139 |

|

|

SUBTOTAL |

|

|

|

|

|

— |

|

— |

|

— |

|

243 |

|

17.79 |

|

139 |

|

243 |

|

17.79 |

|

139 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

TOTAL GOLD |

|

|

|

|

|

227,244 |

|

0.58 |

|

4,242 |

|

1,016,910 |

|

0.65 |

|

21,126 |

|

1,244,154 |

|

0.63 |

|

25,368 |

|

|

MINERAL RESERVE AND MINERAL RESOURCE STATEMENT |

|

SILVER |

|

MEASURED AND INDICATED MINERAL RESOURCES (EXCLUDES PROVEN AND PROBABLE MINERAL RESERVES) (2),(3),(4),(6),(7),(8) |

|

|

|

Kinross Gold Corporation’s Share at December 31, 2011 |

|

|

|

|

|

|

|

Kinross |

|

Measured |

|

Indicated |

|

Measured and Indicated |

| ||||||||||||

|

|

|

|

|

Interest |

|

Tonnes |

|

Grade |

|

Ounces |

|

Tonnes |

|

Grade |

|

Ounces |

|

Tonnes |

|

Grade |

|

Ounces |

|

|

Property |

|

Location |

|

(%) |

|

(kt) |

|

(g/t) |

|

(koz) |

|

(kt) |

|

(g/t) |

|

(koz) |

|

(kt) |

|

(g/t) |

|

(koz) |

|

|

NORTH AMERICA |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Round Mountain Area |

|

USA |

|

50.0 |

% |

35 |

|

7.7 |

|

9 |

|

5,088 |

|

6.5 |

|

1,058 |

|

5,123 |

|

6.5 |

|

1,067 |

|

|

SUBTOTAL |

|

|

|

|

|

35 |

|

7.7 |

|

9 |

|

5,088 |

|

6.5 |

|

1,058 |

|

5,123 |

|

6.5 |

|

1,067 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

SOUTH AMERICA |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Cerro Casale |

(10) |

Chile |

|

25.0 |

% |

5,853 |

|

1.3 |

|

240 |

|

68,534 |

|

1.1 |

|

2,419 |

|

74,387 |

|

1.1 |

|

2,659 |

|

|

Fruta del Norte |

|

Ecuador |

|

100.0 |

% |

— |

|

— |

|

— |

|

4,266 |

|

10.3 |

|

1,412 |

|

4,266 |

|

10.3 |

|

1,412 |

|

|

La Coipa |

(11) |

Chile |

|

100.0 |

% |

12,041 |

|

39.3 |

|

15,224 |

|

4,785 |

|

20.1 |

|

3,093 |

|

16,826 |

|

33.9 |

|

18,317 |

|

|

SUBTOTAL |

|

|

|

|

|

17,894 |

|

26.9 |

|

15,464 |

|

77,585 |

|

2.8 |

|

6,924 |

|

95,479 |

|

7.3 |

|

22,388 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

RUSSIA |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Dvoinoye |

|

Russia |

|

100.0 |

% |

— |

|

— |

|

— |

|

243 |

|

12.3 |

|

96 |

|

243 |

|

12.3 |

|

96 |

|

|

SUBTOTAL |

|

|

|

|

|

— |

|

— |

|

— |

|

243 |

|

12.3 |

|

96 |

|

243 |

|

12.3 |

|

96 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

TOTAL SILVER |

|

|

|

|

|

17,929 |

|

26.8 |

|

15,473 |

|

82,916 |

|

3.0 |

|

8,078 |

|

100,845 |

|

7.3 |

|

23,551 |

|

|

MINERAL RESERVE AND MINERAL RESOURCE STATEMENT |

|

COPPER |

|

MEASURED AND INDICATED MINERAL RESOURCES (EXCLUDES PROVEN AND PROBABLE MINERAL RESERVES) (3),(4),(7),(8) |

|

|

|

Kinross Gold Corporation’s Share at December 31, 2011 |

|

|

|

|

|

|

|

Kinross |

|

Measured |

|

Indicated |

|

Measured and Indicated |

| ||||||||||||

|

|

|

|

|

Interest |

|

Tonnes |

|

Grade |

|

Pounds |

|

Tonnes |

|

Grade |

|

Pounds |

|

Tonnes |

|

Grade |

|

Pounds |

|

|

Property |

|

Location |

|

(%) |

|

(kt) |

|

(%) |

|

(Mlb) |

|

(kt) |

|

(%) |

|

(Mlb) |

|

(kt) |

|

(%) |

|

(Mlb) |

|

|

SOUTH AMERICA |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Cerro Casale |

(10) |

Chile |

|

25.0 |

% |

5,853 |

|

0.13 |

|

16 |

|

68,534 |

|

0.16 |

|

243 |

|

74,387 |

|

0.16 |

|

259 |

|

|

SUBTOTAL |

|

|

|

|

|

5,853 |

|

0.13 |

|

16 |

|

68,534 |

|

0.16 |

|

243 |

|

74,387 |

|

0.16 |

|

259 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

TOTAL COPPER |

|

|

|

|

|

5,853 |

|

0.13 |

|

16 |

|

68,534 |

|

0.16 |

|

243 |

|

74,387 |

|

0.16 |

|

259 |

|

Inferred Mineral Resources

Cautionary Note to United States Investors Concerning Estimates of Inferred Mineral Resources

This section uses the terms “Inferred” mineral resources. United States investors are advised that while those terms are recognized and required by Canadian regulations, the United States Securities and Exchange Commission does not recognize them. United States investors are cautioned not to assume that all or any part of mineral deposits in these categories will ever be converted into proven and probable mineral reserves or recovered.

|

MINERAL RESERVE AND MINERAL RESOURCE STATEMENT |

|

GOLD |

|

INFERRED MINERAL RESOURCES (2),(3),(4),(6),(7),(8) |

|

|

|

Kinross Gold Corporation’s Share at December 31, 2011 |

|

|

|

|

|

|

|

Kinross |

|

Inferred |

| ||||

|

|

|

|

|

Interest |

|

Tonnes |

|

Grade |

|

Ounces |

|

|

Property |

|

Location |

|

(%) |

|

(kt) |

|

(g/t) |

|

(koz) |

|

|

NORTH AMERICA |

|

|

|

|

|

|

|

|

|

|

|

|

Fort Knox Area |

|

USA |

|

100.0 |

% |

22,180 |

|

0.41 |

|

295 |

|

|

Kettle River |

(5) |

USA |

|

100.0 |

% |

255 |

|

10.39 |

|

85 |

|

|

Round Mountain Area |

|

USA |

|

50.0 |

% |

35,242 |

|

0.41 |

|

464 |

|

|

White Gold Area |

(12) |

Yukon |

|

100.0 |

% |

9,391 |

|

1.91 |

|

578 |

|

|

SUBTOTAL |

|

|

|

|

|

67,068 |

|

0.66 |

|

1,422 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

SOUTH AMERICA |

|

|

|

|

|

|

|

|

|

|

|

|

Cerro Casale |

(10) |

Chile |

|

25.0 |

% |

124,894 |

|

0.37 |

|

1,504 |

|

|

Crixas |

(9) |

Brazil |

|

50.0 |

% |

3,405 |

|

4.67 |

|

511 |

|

|

Fruta del Norte |

|

Ecuador |

|

100.0 |

% |

22,093 |

|

5.13 |

|

3,645 |

|

|

La Coipa |

(11) |

Chile |

|

100.0 |

% |

4,508 |

|

2.07 |

|

300 |

|

|

Lobo Marte |

(13) |

Chile |

|

100.0 |

% |

112,767 |

|

0.78 |

|

2,834 |

|

|

Maricunga Area |

|

Chile |

|

100.0 |

% |

377,609 |

|

0.47 |

|

5,651 |