UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

SCHEDULE 14A

Proxy Statement Pursuant to Section 14(a) of the

Securities Exchange Act of 1934

(Amendment No. )

Filed by the Registrant þ Filed by a Party other than the Registrant ¨

Check the appropriate box:

| ¨ | Preliminary Proxy Statement | |||

| ¨ | Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) | |||

| ¨ | Definitive Proxy Statement | |||

| þ | Definitive Additional Materials | |||

| ¨ | Soliciting Material Pursuant to § 240.14a-12 | |||

MENTOR GRAPHICS CORPORATION | ||||

| (Name of Registrant as Specified In Its Charter) | ||||

| N/A | ||||

| (Name of Person(s) Filing Proxy Statement, if other than the Registrant) | ||||

| Payment of Filing Fee (Check the appropriate box): | ||||

| þ | No fee required. | |||

| ¨ | Fee computed on table below per Exchange Act Rules 14a-6(i)(1) and 0-11. | |||

| (1) | Title of each class of securities to which transaction applies:

| |||

| (2) | Aggregate number of securities to which transaction applies:

| |||

| (3) | Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (set forth the amount on which the filing fee is calculated and state how it was determined):

| |||

| (4) | Proposed maximum aggregate value of transaction:

| |||

| (5) | Total fee paid: | |||

| ¨ | Fee paid previously with preliminary materials: | |||

| ¨ | Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the form or schedule and the date of its filing. | |||

| (1) | Amount previously paid:

| |||

| (2) | Form, Schedule or Registration Statement No.:

| |||

| (3) | Filing Party:

| |||

| (4) | Date Filed:

| |||

Convertible

Debenture Analysis

April 2011 |

Important

Information On March 31, 2011, the company filed a definitive proxy statement

with the Securities and Exchange Commission (the “SEC”) in

connection with the company’s upcoming 2011 annual meeting of

shareholders. Shareholders are advised to read the company’s

definitive proxy statement, and any other relevant documents filed by

the company with the SEC, before making any voting or investment

decision because they contain important information. The definitive

proxy statement is, and any other relevant documents and other

material filed with the SEC concerning the company will be, when

filed,

available

free

of

charge

at

http://www.sec.gov

and

http://www.mentor.com/company/investor_relations. In addition, copies

of the proxy materials may be requested from the company’s proxy solicitor,

MacKenzie Partners, Inc., by telephone at 1-800-322- 2885

or

by

email

at

proxy@mackenziepartners.com. |

Forward-Looking

Statements This presentation and commentary may contain “forward-looking”

statements based on current expectations within the meaning of the Securities Exchange

Act of 1934. Such forward-looking statements involve known and unknown risks,

uncertainties and other factors that may cause the actual results, performance or

achievements of the Company or industry results to be materially different from any

results, performance or achievements expressed or implied by such forward-looking

statements. Such factors include, among others, the following: (i) weakness or recession

in the US, EU, Japan or other economies; (ii) the Company’s ability to successfully

offer products and services that compete in the highly competitive EDA industry; (iii)

product bundling or discounting of products and services by competitors, which could

force the Company to lower its prices or offer other more favorable terms to customers; (iv)

possible delayed or canceled customer orders, a loss of key personnel or other consequences

resulting from the business disruption and uncertainty of prolonged proxy fights, offers

to purchase the Company’s securities or other actions of activist shareholders; (v)

effects of the increasing volatility of foreign currency fluctuations on the

Company’s business and operating results; (vi) changes in accounting or reporting rules

or interpretations; (vii) the impact of tax audits by the IRS or other taxing authorities, or

changes in the tax laws, regulations or enforcement practices where the Company does

business; (viii) effects of unanticipated shifts in product mix on gross margin; and

(ix) effects of customer seasonal purchasing patterns and the timing of significant

orders, which may negatively or positively impact the Company’s quarterly results

of operations, all as may be discussed in more detail under the heading “Risk Factors” in

the Company’s most recent Form 10-K or Form 10-Q. Given these uncertainties,

prospective investors are cautioned not to place undue reliance on such

forward-looking statements. In addition, statements regarding guidance do not

reflect potential impacts of mergers or acquisitions that have not been announced or

closed as of the time the statements are made. The Company disclaims any obligation to

update any such factors or to publicly announce the results of any revisions to any of the

forward-looking statements to reflect future events or developments.

|

Mentor

Graphics’ new 4.00% debentures are favorable relative to the old 6.25%

debentures The make whole provision is consistent with market practice and the 6.25%

debentures, and will not be a material impediment to any premium transaction

– in fact, at Icahn’s $17 per share proposal, the make

whole would only reduce transaction value to shareholders by 1.24%

Mentor Graphics eliminated the proxy fight change-in-control put provision that is

common in many convertible debt issues, including our old 6.25% debentures

Mentor Graphics’

Board took the course of action that it determined was in the best interests of all

shareholders by pursuing a prudent refinancing

The proceeds from the new 4.00% debentures will be used to refinance the old 6.25% debentures,

to repurchase $25MM of outstanding common stock at $14.67, the closing price on

29-Mar-2011, and to repay $18.5MM of term loan due 2013

Mentor Graphics’

New Convertible Debt is an

Improvement Over the Outstanding Debt

1

New

Debentures

Old

Debentures

Which is

Better?

Size (Principal, $MM)

$

253

$ 196 (1)

Seniority

Subordinated

Subordinated

Same

Coupon

4.00%

6.25%

New

Conversion Price

$

20.54

$

17.97

New

Illustrative Shares Underlying (2) -- Net of Repurchase (MM) (3)

10.613

10.907

New

Put Date

April 2018

March 2013

New

Proxy Fight Change-in-Control Put

No

Yes

New

Stock Change-of-Control Make Whole

No

No

Same

Cash Change-of-Control Make Whole

Yes

Yes (but lapsed in 2011)

Old

Source: Mentor Graphics 10-K dated 31-Jan-2011, Mentor Graphics indentures for

Convertible Subordinated Debentures due 2026 and 2031, Mentor Graphics management (1) Does

not include $18.5MM of term loan that will be retired with net proceeds from the sale of the 4.00% debentures

(2) For comparative purposes only, the share amounts in the table above assume physical

settlement of the debentures. However, if the 6.25% Debentures or 4.00% Debentures were to be converted, they will be settled by “net share” settlement,

i.e. the first $1,000 of conversion value will be paid in cash, with the remaining conversion

value to be paid, at the election of Mentor Graphics, in cash or shares of common stock. For example, if Mentor Graphics’ common stock price was $25.00 at

the time of conversion, (a) the conversion of $253 million of 4.00% Debentures would be settled

with $253 million in cash and, assuming Mentor Graphics elected to repay the remaining conversion value in shares of common stock, approximately

2.676 million shares, and (b) the conversion of $196.5 million of 6.25% Debentures would be

settled with $196.5 million in cash, and assuming Mentor Graphics elected to repay the remaining conversion value in shares of common stock,

approximately 4.280 million shares.

(3) The underlying shares for the 4.00% Debentures reflects a repurchase of approximately 1.7

million shares of common stock with $25.0 million of the net proceeds from the sale of the 4.00% Debentures. |

Acquisition make

whole shares compensate investors for the lost coupons and option value that they paid

for when buying a convertible bond A make whole is only triggered by a cash

acquisition: A make

whole

provision

is

market

for

convertible

debt

–

all

convertible

debt

issued

by

U.S. public companies in the last twelve months has included make whole provisions

A make

whole

provision

does

not

prevent

a

change

in

control

–

it

will

not

impact

a

stock

transaction

and

it

will

only

slightly

reduce

the

premium

that

an

acquiror

is

willing

to

pay

in a cash transaction

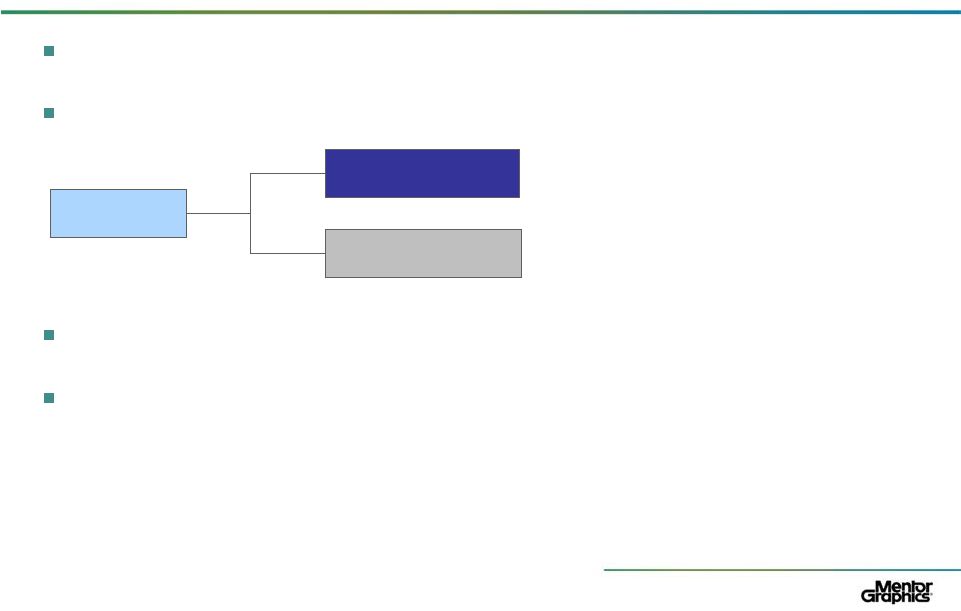

Appendix: Overview of Make Whole

Provisions

Acquisition

Conversion Rate Adjustment

Convertible into New Shares

Cash Acquisition

Stock Acquisition

No Put; No Make Whole Adjustment

Put at 100% or Conversion with

Make Whole Adjustment

2 |

Appendix:

Illustrative Impact of 4.00% Debentures’

Make Whole Provision

MENT

4.00%

Debentures

Change

of

Control

Make

Whole:

Adjustment

to

the

Conversion

Rate

3

For illustrative purposes, assuming Icahn’s $17 per share all cash acquisition proposal

and a closing date of April 4, 2011, the impact would be a 9.33% premium on the bonds

and a reduction in the price paid to shareholders of only $0.21 (1.24%)

Illustrative Acquisition Price

$

17.00

Make Whole Premium Calculation Per Bond

Theoretical Impact to Offer Price Calculation

Shares Underlying Bonds --

No Make Whole

48.6902

Mentor Basic Shares (PF for repurchase, no make whole)

110.653

112.357 basic -1.704 repurchase

Make Whole Shares

15.6236

(17.2990 + 13.9481)

2

x Illustrative Acquisition Price

$

17.00

Shares Underlying Bonds --

With Make Whole

64.3138

Implied Equity Value

$

1,881

+ 4.00% Debentures (1)

253

Par Value of Bond

$

1,000.00

-

Cash & Equivalents

133

Value of Bond at Acquisition Price

1,093.33

64.314 x $17.00

Implied Enterprise Value

$

2,001

% Premium Over Face Value

9.33%

-

4.00% Debentures (assuming conversion, net share settled) (1)

253

Repaid at par $1,000 + net shares

+ Cash & Equivalents

133

Implied Equity Value

$

1,881

Mentor Basic Shares (pro forma for repurchase)

110.653

Mentor Shares from Convert (net share settled)

1.389

Net shares of $93 per bond

Mentor Diluted Shares

112.042

Implied Value per Share

$16.79

$ Difference

$0.21

% Difference

1.24%

Source: Make Whole data from Indenture for 4.00% Subordinated Convertible Debentures due 2031,

Mentor Graphics 10-K dated 31-Jan-2011, Bloomberg (1) Debt pro forma for

redemption / retirement of extant 6.25% debentures and repayment of amounts outstanding on current term loan

Effective

Stock Price

Date

$14.67

$16.00

$18.00

$20.00

$25.00

$30.00

$35.00

$40.00

$45.00

$60.00

$80.00

$100.00

April 4, 2011

19.4761

17.2990

13.9481

11.5561

7.9359

6.0016

4.8248

4.0337

3.4731

2.4171

1.6540

1.2010

April 1, 2012

19.4761

16.6147

13.0468

10.5478

6.9108

5.0903

4.0421

3.3633

2.8912

2.0156

1.3847

1.0097

April 1, 2013

19.4761

15.8645

12.0083

9.3637

5.7036

4.0347

3.1515

2.6108

2.2442

1.5706

1.0836

0.7927

April 1, 2014

19.4761

15.1086

10.8191

7.9467

4.2499

2.8084

2.1511

1.7827

1.5377

1.0837

0.7506

0.5509

April 1, 2015

19.4761

14.2999

9.3043

6.0394

2.3740

1.3892

1.0692

0.9039

0.7873

0.5592

0.3884

0.2858

April 5, 2016

19.4761

13.9556

8.2314

3.4939

0.0002

—

—

—

—

—

—

—

|

Effective

Stock Price

Date

11.23

$

16.00

$

20.00

$

24.00

$

30.00

$

35.00

$

March 3, 2006

33.39

19.16

13.89

11.00

8.45

7.15

March 1, 2007

33.39

17.13

12.08

9.33

7.08

5.97

March 1, 2008

33.39

14.90

9.88

7.42

5.54

4.66

March 1, 2009

33.39

12.51

7.45

5.28

3.85

3.23

March 1, 2010

33.39

9.95

4.55

2.79

1.97

1.67

March 1, 2011

33.39

-

-

-

-

-

Appendix: Mentor’s 4.00% and 6.25% Make

Whole Provisions Are Substantially Similar

The make whole provision for each series of debentures was calculated in the same

manner

The biggest difference is that the base stock price at the time of the 6.25% debentures

was $11.23 versus a stock price of $14.67 at the time of the 4.00% debentures

Compare an approximate 40% premium on both tables: $16 on Table 1 and $20 on

Table 2

To use these tables, add the base conversion rate to the table entry and then multiply

by the stock price. For example:

Table 1: 6.25% Debentures

Table 2: 4.00% Debentures

4

Premium Value of

Bond

(Par = $1,000)

Conversion

Rate

Make Whole

Adjustment

Acquisition

Stock Price

6.25%

Debentures

$1,197

=

(55.6545

+

19.16)

x

$16

4.00%

Debentures

$1,205

=

(48.6902

+

11.5561)

x

$20

Source: Indenture for 6.25% Subordinated Convertible Debentures due 2026 and Indenture for

4.00% Subordinated Convertible Debentures due 2031

Effective

Stock Price

Date

$14.67

$16.00

$18.00

$20.00

$25.00

$30.00

$35.00

April 4, 2011

19.4761

17.2990

13.9481

11.5561

7.9359

6.0016

4.8248

April 1, 2012

19.4761

16.6147

13.0468

10.5478

6.9108

5.0903

4.0421

April 1, 2013

19.4761

15.8645

12.0083

9.3637

5.7036

4.0347

3.1515

April 1, 2014

19.4761

15.1086

10.8191

7.9467

4.2499

2.8084

2.1511

April 1, 2015

19.4761

14.2999

9.3043

6.0394

2.3740

1.3892

1.0692

April 5, 2016

19.4761

13.9556

8.2314

3.4939

0.0002

—

—

|