UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

For the fiscal year ended October 3 , 2020

or

For the transition period from _____________ to ______________

Commission File No. 0-02382

(Exact name of registrant as specified in its charter)

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | ||||||||||

| (Address of principal executive offices) | (Zip Code) | ||||||||||

Registrant's telephone number, including area code: (952 ) 937-4000

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||||||

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined by Rule 405 of the Securities Act. Yes o No ý

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No ý

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ý No o

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ý No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of "large accelerated filer," "accelerated filer," "smaller reporting company," and "emerging growth company" in Rule 12b-2 of the Exchange Act.

Large accelerated filer o Accelerated filer ý Non-accelerated filer o

Smaller reporting company ☐ Emerging growth company ☐

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. o

Indicate by check mark whether the registrant has filed a report on and attestation to its management's assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☒

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ý

The aggregate market value of the voting and non-voting common stock held by non-affiliates of the registrant as of March 28, 2020 was approximately $400.0 million based on the closing price of $21.74 as of March 27, 2020 as reported by The Nasdaq Stock Market LLC.

As of December 10, 2020, there were 19,314,226 shares of common stock outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Certain information required by Part III of this Annual Report on Form 10-K will either be incorporated into this Annual Report on Form 10-K by reference to MTS Systems Corporation's Definitive Proxy Statement for its 2021 Annual Meeting of Shareholders, or will be included in an amendment to this Annual Report on Form 10-K filed within 120 days of October 3, 2020.

MTS Systems Corporation

Annual Report on Form 10-K

For the Year Ended October 3, 2020

| Table of Contents | ||||||||

PART I

ITEM 1. BUSINESS

Business Overview

MTS Systems Corporation is a leading global supplier of advanced test systems, motion simulators and precision sensors that was incorporated under Minnesota law in 1966. Our operations are organized and managed in two reportable segments, Test & Simulation and Sensors, based on global similarities within their markets, products, operations and distribution. The Test & Simulation and Sensors segments represented 59% and 41% of our revenue, respectively, for the fiscal year ended October 3, 2020.

Terms

The terms "MTS," "we," "us," the "Company" or "our" in this Annual Report on Form 10-K, unless the context otherwise requires, refer to MTS Systems Corporation and its wholly owned subsidiaries.

Fiscal year 2020 refers to the fiscal year ended October 3, 2020, fiscal year 2019 refers to the fiscal year ended September 28, 2019, and fiscal year 2018 refers to the fiscal year ended September 29, 2018. Fiscal year 2020 includes 53 weeks, while fiscal years 2019 and 2018 include 52 weeks. All dollar amounts and shares are in thousands unless otherwise noted.

Products and Markets

Test & Simulation

Our Test & Simulation segment (Test & Simulation) provides testing and simulation solutions including hardware, software and services that are used by customers in product development to characterize a product's mechanical properties along with simulation systems for human response features. Our solutions simulate forces and motions that customers expect their products to encounter in use. Mechanical simulation testing in a lab setting is an accepted method to accelerate product development compared to reliance on full physical prototypes in real-world settings, proving ground testing, and virtual testing because it provides more controlled simulation and accurate measurement. The need for mechanical simulation increases in proportion to the cost of a product, the range and complexity of the physical environment in which the product will be used, expected warranty or recall risk and expense, governmental regulation and potential legal liability. A significant portion of Test & Simulation products are considered by our customers to be capital expenditures. The timing of purchases of our products may be impacted by interest rates, general economic conditions, product development cycles and new product initiatives.

A typical Test & Simulation system includes a reaction frame to hold the prototype specimen; a hydraulic pump or electro-mechanical power source; actuators to create the force or motion; and a computer controller with specialized software to coordinate the actuator movement, and to measure, record, analyze and manipulate results. Lower force and less dynamic testing can usually be accomplished with electro-mechanical power sources, which are generally less expensive than hydraulic systems. In addition to these basic components, we sell a variety of accessories and spare parts.

We provide Test & Simulation customers across all sectors with a spectrum of services to maximize product performance. Our service offerings include installation, product life cycle management, professional training, calibration and metrology, technical consulting and onsite and factory repair and maintenance.

On December 31, 2019, we acquired all ownership interests of R&D, including R&D Test Systems, R&D Engineering, R&D Steel, R&D Prague, RGDK Engineering Private Limited and R&D Tools and Structures (collectively, "R&D"), a manufacturer of test systems that accurately simulate the extreme operating environments often encountered by large, rotating structures, such as wind turbines and aircraft engine propulsion systems. The acquisition of R&D expands our technology base and market presence for wind energy and aerospace markets globally. R&D is included in our Test & Simulation structures sector.

Test & Simulation serves a diverse spectrum of customers by industry and geography. Regionally, the Americas, Europe and Asia represented 29%, 30% and 41% of revenue for fiscal year 2020, respectively, based on customer location.

Test & Simulation products, service and customers are grouped into the following three global sectors:

•Ground Vehicles (approximately 40% of Test & Simulation revenue for fiscal year 2020)

This sector consists of automobile, truck, motorcycle, motorsports vehicles, construction equipment, agricultural equipment, rail and off-road vehicle manufacturers and their suppliers. Customers include original equipment manufacturers (OEMs), universities, government research and development institutes, motorsports teams and contract test facilities. Our products are used to measure and simulate solutions to assess durability, vehicle dynamics and aerodynamics of vehicles, sub-systems and components. Our products include:

1

◦Road simulators and component test systems for durability testing;

◦Vehicle performance test systems that evaluate ride handling, ride comfort and noise;

◦Vehicle dynamics simulators to test conceptual vehicle designs in advance of physical prototypes;

◦High-performance electrical motors and energy recovery systems for high-end automotive and aerospace applications;

◦Tire performance and rolling resistance measurement systems; and

◦Moving ground-plane systems and balances for vehicle aerodynamic measurements in wind tunnels.

•Materials (approximately 30% of Test & Simulation revenue for fiscal year 2020)

This sector covers a diverse range of applications, spanning many different industries, including power generation, aerospace, vehicles and biomedical. Our solutions deliver the reliable, innovative technologies required to satisfy every material evaluation needed from single-axle tension / compression testing to complex fracture mechanics and multi-axial fatigue testing. Our products and services support customers in the research and development of products through the physical characterization of material properties, such as metals, composites and ceramics to polymers, textiles, concrete, geomaterials and many others. Our biomedical applications include systems to test durability and performance of implants, prostheses and other medical and dental materials and devices.

•Structures (approximately 30% of Test & Simulation revenue for fiscal year 2020)

This sector serves the structural testing and simulation needs and services of our customers in the fields of aerospace, structural engineering, oil and gas, wind energy, amusement parks, flight simulation and others. The aerospace structural testing market consists of manufacturers of commercial, military and private aircraft and their suppliers that use our products, systems and software to perform static and fatigue testing of aircraft. Systems for structural engineering include high force static and dynamic testing, as well as seismic simulation tables used around the world to test the design of structures, such as bridges and buildings, and to help governments establish building codes. Structural engineering customers include construction companies, government agencies, universities and building materials manufacturers. The wind energy market consists of wind turbine manufacturers and their component suppliers that use our products to reduce cost and improve reliability of blades, bearings and entire wind turbines. We provide high-quality, durable motion systems servicing human-rated entertainment and training simulation markets. Key product applications include high-technology motion simulators for the amusement park industry and flight simulators for certified pilot training.

Sensors

Our Sensors segment (Sensors) is a global leader in sensing technologies and solutions used worldwide by design engineers and predictive maintenance professionals, serving customers with a focus on total customer satisfaction, and offering regional support to provide innovative and reliable sensing solutions. Our high-performance sensors provide measurements of vibration, pressure, position, force and sound in a variety of applications. Our products and solutions are used to enable automation, enhance precision and safety, and lower our customers' production costs by improving performance and reducing downtime. Revenue is fueled by our customers' spending on research and development activities and industrial capacity utilization. Sensors products and solutions serve the automotive, aerospace, industrial, defense, and research and development markets, as well as many other markets. Sensors manufactures products utilizing piezoelectric and magnetostriction technology, both of which provide highly accurate, reliable and durable sensors ideal for use in harsh operating environments.

Sensors serves a diverse spectrum of customers by industry and geography. Regionally, the Americas, Europe and Asia represented 53%, 27% and 20% of revenue for fiscal year 2020, respectively, based on customer location.

Sensors products and customers are grouped into the following four global sectors:

•Test Sensors (approximately 45% of Sensors revenue for fiscal year 2020)

This sector covers diverse industries, including test and measurement, automotive, rail, aerospace and defense. These sensors are used in a variety of applications including research and development and testing for use in harsh environments; structural monitoring; ground testing of aircraft and vehicles; impact sensors for shock and vibration testing; component and system performance; ride and handling; durability testing; and noise, vibration, and harshness testing. These sensors provide engineers and scientists with precise and accurate measurements to accelerate technology advancement and reduce new product development cycle time.

•Position Sensors (approximately 30% of Sensors revenue for fiscal year 2020)

This sector consists of a wide range of industrial machinery OEMs and their end use customers with applications in all areas of manufacturing including plastics, steel, construction, agriculture, wood and mining, as well as other factory automation applications. These sensors provide positional feedback for motion control systems, improve productivity by enabling high levels of automation, reduce maintenance costs and enhance safety of machine operations.

2

•Industrial Sensors (approximately 15% of Sensors revenue for fiscal year 2020)

This sector consists of sensors used in heavy industrial markets and energy and power generation. Sensors used in heavy industrial markets are primarily used to monitor the vibration and pressure in a wide spectrum of applications including motors, pumps, paper machines and steel rollers. These sensors provide valuable feedback on equipment performance, reducing downtime and maximizing safety and productivity. Sensors used in the energy and power generation markets are equipped to address hazardous and inaccessible locations and serve gas and wind turbines, oil and gas refineries, and nuclear power instrumentation, as well as other critical energy infrastructure providers.

•Systems Sensors (approximately 10% of Sensors revenue for fiscal year 2020)

This sector consists of dynamic test, measurement and sensing systems primarily used to test, model and monitor the behavior of structures and processes, as well as to ensure safety and compliance from exposure to noise and vibration. This sector also includes the calibration systems used with a variety of sensors, our comprehensive rental offering of both transactional sensor products, and consultative systems that serve a broad range of testing and industrial customers.

Financial and geographical information about our segments is included in Item 7 and Item 8 of Part II of this Annual Report on Form 10-K.

Sales and Service

Test & Simulation

Test & Simulation products are sold worldwide through a direct field sales and service organization, independent representatives and distributors and, to a much lesser extent, through other means (e.g., catalogs, internet, etc.) for standard products and accessories. Direct field sales and service personnel are compensated through salary and order incentive programs. Independent representatives and distributors are either compensated through commissions based upon orders or discounts off list prices.

In addition to direct field sales and service personnel throughout the U.S., we have sales and service subsidiaries in Toronto, Canada; Berlin, Germany; Paris, France; Amsterdam, Netherlands; Guildford, United Kingdom; Turin, Italy; Gothenburg, Sweden; Aarhus, Denmark; Tokyo and Nagoya, Japan; Seoul, South Korea; Moscow, Russia; Bangalore, India; and Beijing, Shanghai and Shenzhen, China.

The timing and volume of large orders (valued at $5,000 or greater on a U.S. dollar-equivalent basis) may produce volatility in backlog and quarterly operating results. Most customer orders are based on fixed-price quotations and typically have an average sales cycle of three to nine months due to the technical nature of the test systems and customer capital expenditure approval processes. The sales cycle for larger, more complex test systems may be several years.

Sensors

Sensors products are sold worldwide through a direct sales and service organization as well as through independent distributors. The direct sales and service organization is compensated through salary and commissions based upon revenue. The independent distributors purchase our products at wholesale pricing and resell the products to their customers.

In addition to direct field sales and service personnel throughout the U.S., we have sales subsidiaries in Treviolo, Italy; Stevenage, United Kingdom; Aubervilliers, France; Huckelhoven and Dresden, Germany; Beijing and Shanghai, China; Vandreuil, Canada; and Zaventem, Belgium.

The average sales cycle for Sensors products ranges from approximately one week to one month for existing customers purchasing standard products. The average sales cycle for a new account can range from approximately two weeks to two years depending on customer testing and specification requirements.

Manufacturing and Engineering

Test & Simulation

Test & Simulation systems are largely built to order and primarily engineered and assembled at our headquarters in Eden Prairie, Minnesota. We assemble certain smaller systems at our locations in Berlin, Germany and Seoul, South Korea. We also operate system assembly facilities in Amsterdam and Mijdrect, Netherlands for electrical motion platforms and in Aarhus, Denmark for wind power energy test systems; however, the majority of the wind energy test systems are constructed at the customer site. Test & Simulation also has engineering operations in Amsterdam, Netherlands; Aarhus, Denmark and Prague, Czech Republic. Certain materials testing products are produced by a contract manufacturer in Shanghai and Hangzhou, China.

Installation of systems, training and services are primarily delivered at customer sites. The engineering and assembly cycle for a typical test system ranges from one to 12 months, depending on the complexity of the system and the availability of components. The engineering and assembly cycle for larger, more complex systems may be several years.

3

Sensors

Sensors are engineered and assembled regionally at facilities located in Depew, New York; Halifax and Cary, North Carolina; Sunnyvale, California; Farmington Hills, Michigan; Provo, Utah; Cincinnati, Ohio; and Lüdenscheid, Germany. Assembly cycles generally vary from several days to several weeks, depending on the degree of product customization, the size of the order and manufacturing capacity.

Sources and Availability of Raw Materials and Components

Test & Simulation

A significant portion of our test systems consist of materials and component parts purchased from independent vendors. We are dependent, in certain situations, on a limited number of vendors to provide raw materials and components. As Test & Simulation generally sells products and services based on fixed-price contracts, fluctuations in the cost of materials and components between the date of the order and the delivery date may impact the expected profitability. Material and component cost variability is considered in the estimation and customer negotiation process.

Sensors

A significant portion of Sensors products consists of materials and component parts purchased from independent vendors. We are dependent, in certain situations, on a limited number of vendors to provide raw materials and components, such as mechanical and electronic components. As Sensors generally sells products and services based on fixed-price contracts and the products are manufactured and delivered within days to months from the time of order, fluctuations in the cost of materials and components between the date of the order and the delivery date are not likely to materially impact the expected profitability.

Patents and Trademarks

We rely on a combination of patents, copyrights, trademarks and proprietary trade secrets to protect our proprietary technology, some of which are material to our segments. We have obtained numerous patents and trademarks worldwide and actively file and renew patents and trademarks on a global basis to establish and protect our proprietary technology. We are also party to exclusive and non-exclusive license and confidentiality agreements relating to our own and third-party technologies. We aggressively protect certain of our processes, products and strategies as proprietary trade secrets. Our efforts to protect intellectual property and avoid disputes over proprietary rights include ongoing review of third-party patents and patent applications.

Seasonality

There is no significant seasonality in Test & Simulation or Sensors.

Working Capital

Test & Simulation

Test & Simulation does not have significant finished product inventory, but maintains inventories of materials and components to facilitate on-time product delivery. Test & Simulation may have varying levels of work-in-process projects that are classified as inventories, net or unbilled accounts receivable, net in our Consolidated Balance Sheets, depending upon the manufacturing cycle, timing of orders, project revenue recognition and shipments to customers.

Payments are often received from Test & Simulation customers upon order or at milestones during the fulfillment of the order depending on the size and customization of the system. These payments are recorded as advance payments from customers in our Consolidated Balance Sheets and reduced as revenue is recognized. Conversely, if revenue is recognized on a project prior to customer billing, this revenue is recorded as unbilled accounts receivable, net in our Consolidated Balance Sheets until the customer has been billed. Upon billing, it is recorded as accounts receivable, net in our Consolidated Balance Sheets. Changes in the average size, payment terms and revenue recognition for orders in Test & Simulation may have a significant impact on accounts receivable, net; unbilled accounts receivable, net; advance payments from customers; and inventories, net. It has not been our practice to provide rights of return for our products. Payment terms vary and are subject to negotiation.

Sensors

Sensors has finished product inventory, as well as inventories of materials and components to facilitate rapid delivery of product to exceed customer expectations on delivery time. The type and amount of finished goods on hand are targeted based on historical and anticipated customer demands for high-volume products. Payment terms vary and are subject to negotiation. Revenue is primarily recognized when products are shipped.

Customers

We do not have a significant concentration of sales with any individual customer within Test & Simulation, Sensors or total MTS. Therefore, the loss of any one customer would not have a material impact on our results.

4

Backlog

Most of our products are built to order. Our backlog of orders, defined as firm orders from customers that remain unfulfilled, totaled approximately $457,586, $420,115 and $415,155 as of October 3, 2020, September 28, 2019 and September 29, 2018, respectively. Test & Simulation backlog was $385,905, $342,652 and $346,006 as of October 3, 2020, September 28, 2019 and September 29, 2018, respectively. Sensors backlog was $71,681, $77,463 and $69,149 as of October 3, 2020, September 28, 2019 and September 29, 2018, respectively. Based on anticipated manufacturing schedules, we expect approximately 68% of the backlog as of October 3, 2020 will be converted to revenue in fiscal year 2021. Delays may occur in the conversion of backlog into revenue as a result of export licensing compliance, technical difficulties, specification changes, manufacturing capacity, supplier issues or access to the customer site for installation. While certain contracts within backlog are subject to order cancellation, we have not historically experienced a significant number of order cancellations. Refer to Item 7 of Part II of this Annual Report on Form 10-K for further discussion of order cancellations.

Government Contracts

Revenue from U.S. government contracts varies by year. A portion of our government business is subject to renegotiation of profits or termination of contracts or subcontracts at the election of the U.S. government. In addition to contract terms, we must comply with procurement laws and regulations relating to the formation, administration and performance of U.S. government contracts. Failure to comply with these laws and regulations could lead to the termination of contracts at the election of the U.S. government or the suspension or debarment from U.S. government contracting or subcontracting. U.S. government revenue as a percentage of our total revenue was 11%, 6% and 4% for fiscal years 2020, 2019 and 2018, respectively.

Competition

Test & Simulation

For relatively simple and inexpensive mechanical testing applications, customers may satisfy their needs internally by building their own test systems or using competitors who compete on price, performance, quality and service. For larger and more complex mechanical test systems, we compete directly with several companies worldwide based upon customer value including application knowledge, engineering capabilities, technical features, price, quality and service.

Sensors

We primarily compete on factors that include technical performance, price and customer service in new applications or in situations in which other sensing technologies have been used. Sensors competitors are typically larger companies that carry multiple sensors product lines; larger diverse companies with only a small portion of business in the sensors market; or smaller, privately held companies throughout the world.

Environmental Compliance

We believe our operations are in compliance with all applicable material environmental regulations within the jurisdictions in which we operate. Capital expenditures for environmental compliance were not material in fiscal year 2020, 2019 and 2018, and we do not expect such expenditures will be material in fiscal year 2021.

Employees

Our employees are vital to MTS' success in providing advanced test systems, motion simulators and precision sensors. We depend on our highly skilled engineering, sales and service, and manufacturing teams to develop and deliver products to our customers. MTS has approximately 3,600 employees as of October 3, 2020.

MTS services customers around the world with a diverse, geographical footprint of office locations. Employees span the Americas, Europe and Asia with approximately 1,250 employees located outside of the U.S. as of October 3, 2020. This global representation promotes diversity of thought, experiences, cultures and backgrounds that enhances our ability to innovate, solve global challenges, and drive long-term value for MTS.

MTS' talent strategy is led by our Chief Human Resources Officer and governed by the Compensation and Leadership Development Committee of our Board of Directors. Talent management activities support employees in their growth and development throughout their time at MTS. These programs include activities for acquiring strategic talent, training and developing our teams to build key capabilities and skills, and engaging, motivating and retaining our employees to do their best work. To drive long term value and address evolving business strategies, we prioritize activities for strategic workforce planning and succession planning, as well as perform an ongoing evaluation of our organizational design, culture and values.

MTS offers comprehensive compensation and benefits packages to attract and retain a talented and experienced workforce. The Compensation and Leadership Development Committee oversees the design of our executive compensation programs and any risks associated with our overall compensation practices. MTS regularly reviews its global compensation and benefit plans to ensure they are competitive, align to MTS’s strategic priorities, and support company values.

5

MTS is committed to employee engagement by regularly soliciting feedback through surveys and other mechanisms to gain insights into workplace experiences and what motivates employees to do their best work. Employees are provided opportunities to raise suggestions and collaborate with leadership to implement actions for ongoing improvements.

Information about our Executive Officers

The names, ages and positions of our executive officers are presented below.

| Name | Age | Position | ||||||

| Randy J. Martinez | 65 | Director, Interim President and Chief Executive Officer | ||||||

| Steven B. Harrison | 54 | Executive Vice President and President, Test & Simulation | ||||||

| David T. Hore | 55 | Executive Vice President and President, Sensors | ||||||

| Brian T. Ross | 44 | Executive Vice President and Chief Financial Officer | ||||||

| Todd J. Klemmensen | 47 | Senior Vice President, General Counsel and Corporate Secretary | ||||||

Randy J. Martinez - Director of MTS since March 2014 and Interim President and Chief Executive Officer since May 2020. Prior to joining MTS, Mr. Martinez served in several leadership roles at AAR Corporation from 2009 to 2017, a provider of aviation services to the worldwide commercial aviation and aerospace & defense industries, most notably President & CEO of the Airlift Group and Group Vice President, Aviation Services. Before joining AAR, Mr. Martinez was the CEO at World Air Holdings, Inc. As a graduate of the United States Air Force Academy, Mr. Martinez served with distinction in the U.S. Air Force for 21 years, retiring as a Colonel and Command Pilot and having held a wide variety of leadership roles, including command and senior staff positions.

Steven B. Harrison - Executive Vice President and President, Test & Simulation. Prior to joining MTS in 2017, Mr. Harrison served as President, AAR Airlift Group, Inc., as well as President and CEO, National Air Cargo, Inc. During a distinguished 22-year career in the United States Air Force, Mr. Harrison commanded at the wing, group, and squadron level, including three deployed commands. He also held senior staff positions at Headquarters US Air Force, the Joint Staff and US Transportation Command. Mr. Harrison is a command pilot with more than 3,400 flight hours in the C-32A, C-5B, C-17A, KC-10A, T-38A, and T-37B. A Rhodes Scholar, he holds Masters Degrees in Engineering Science as well as Politics, Philosophy, and Economics, from Oxford University, England. He also earned a Bachelor of Science in Aeronautical Engineering from the United States Air Force Academy and a Masters of National Security Strategy from the United States Air War College.

David T. Hore - Executive Vice President and President, Sensors since July 2016. Mr. Hore joined MTS through the acquisition of PCB Group, Inc. (PCB). Mr. Hore initially led PCB as its Co-President and later its President, from 2003-2016. Prior to joining PCB, Mr. Hore was Founder and Managing Partner of the CPA firm Tronconi Segarra & Hore LLP, where he served as strategic consultant and outsourced CFO for PCB from 1995-2003. Prior to that, Mr. Hore was a CPA at Price Waterhouse from 1987-1994. Mr. Hore holds a bachelor’s degree in business administration with a concentration in accounting from the State University of New York at Buffalo.

Brian T. Ross - Executive Vice President and Chief Financial Officer since May 2017. Prior to joining MTS as Corporate Controller in 2014, Mr. Ross was the Director of Financial Planning and Analysis at Digi International Inc. (NASDAQ: DGII), where he gained valuable global experience ranging from strategic planning and acquisitions to operational execution and internal control. Earlier in his career, Mr. Ross served as Controller at Restore Medical, following a seven-year tenure at PricewaterhouseCoopers LLP. Mr. Ross holds a BA in Accounting from the University of Northern Iowa and is a licensed CPA (inactive) in Minnesota.

Todd J. Klemmensen - Senior Vice President, General Counsel and Secretary since July 2018. Mr. Klemmensen directs MTS's global legal affairs, including corporate governance, commercial and strategic agreements, U.S. Government contracting, litigation, and intellectual property. Previously, Mr. Klemmensen served within MTS as Acting General Counsel (April 2017 - July 2018), Associate General Counsel (November 2015 - March 2017) and Director of Contracts & Senior Counsel (January 2012 - October 2015). Mr. Klemmensen served in various roles at Alliant Techsystems, Inc. (ATK), including Sr. Manager - Contracts and providing legal counsel within its Armament Systems Group. Prior to transitioning into industry, Mr. Klemmensen practiced business and corporate law in Minneapolis, MN. He holds a Bachelor of Arts degree from Gustavus Adolphus College and a Juris Doctor degree from Hamline University School of Law. Mr. Klemmensen is a former board member of the National Contract Management Association (NCMA) Twin Cities Chapter and a graduate of the NCMA - Leadership Development Program.

6

Available Information

The U.S. Securities and Exchange Commission (SEC) maintains a website that contains reports, proxy and information statements and other information regarding issuers, including us, that file with the SEC. The public can obtain any documents that we file with the SEC at http://www.sec.gov. We file annual reports, quarterly reports, current reports, proxy statements and other documents with the SEC under the Securities Exchange Act of 1934, as amended (the Exchange Act).

We also make available free of charge on or through the "Investor Relations" pages of our corporate website (www.mts.com) our Annual Report on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K, and, if applicable, amendments to those reports filed or furnished pursuant to the Exchange Act as soon as reasonably practicable after we file such material with, or furnish it to, the SEC. Our Code of Conduct (the Code); any waivers from or amendments to the Code; our Corporate Governance Guidelines, Articles of Incorporation and Bylaws; and the Charters for the Audit, Compensation and Leadership Development, and Nominating and Governance Committees of our Board of Directors are also available free of charge on the "Investor Relations" pages of our corporate website (www.mts.com). We are not including the information on our corporate website as a part of or incorporating it by reference into this Annual Report on Form 10-K.

ITEM 1A. RISK FACTORS

Our business involves risks. The following summarizes what we believe to be the most important risks facing us that could adversely impact our business, financial condition or operating results. The information about these risks should be considered carefully together with the other information contained in this Annual Report on Form 10-K. Additional risks not currently known to us or that we currently deem to be immaterial may also adversely affect our business, financial condition or results of operations in future periods.

Risks Relating to our Business and Operations

The extent to which the outbreak of COVID-19 and measures taken to contain the outbreak will negatively affect our financial condition and results of operations is highly uncertain and cannot be predicted.

Our global operations expose us to risks associated with public health crises and pandemics, such as the outbreak of COVID-19. Attempts to slow the spread of COVID-19 implemented by governments across the globe, including travel bans, restrictions on gatherings, shutdowns of business and government facilities, shelter in place orders, and quarantines, have impacted and will continue to impact our workforce and operations, the operations of our customers, and the operations of our vendors and suppliers.

We have significant manufacturing operations in North America, Europe and Asia, and each of the countries in which we operate has been affected by the outbreak and taken measures in an attempt to contain it. There is considerable uncertainty about the magnitude and duration of future containment measures and the impact on our operations and the operations of our suppliers and customers. The number of jurisdictions in which we operate add complexity to our efforts to operate under current and future restrictions. We also operate with a global supply chain, and both restrictions on the operations of our suppliers and regulation of the international movement of goods may prevent us from timely completing customer orders.

If the COVID-19 outbreak continues and conditions worsen, we may continue to experience a decline in sales activities and delays in customer orders. It remains uncertain what impact these declines will have on future sales and customer orders once conditions begin to improve. Many of our customer orders are part of large capital expenditures and the financial uncertainty resulting from COVID-19 and its market impacts may cause customers to delay planned capital expenditures.

The extent to which the COVID-19 outbreak impacts our business, results of operations and financial condition will depend on future developments, which are highly uncertain and cannot be predicted, including, but not limited to, the duration and spread of the outbreak, the severity of the outbreak, the actions of governments and private sectors to slow the spread of the outbreak, the effect of passed and potential future fiscal stimulus measures, and how quickly and to what extent normal economic and operating conditions can resume. We do not yet know the full extent of the impact on our business, our operations or the global economy as a whole. However, the effects could have a material impact on our results of operations, and we will continue to monitor the COVID-19 situation closely.

Our business is significantly international in scope, which subjects us to the political, economic and other risks that are inherent in operating in foreign countries, and addressing these risks may be costly or may otherwise impact our financial position or results of operations.

We have manufacturing facilities in North America, Europe and Asia. Over the past 15 years, approximately 70% of our revenue has been derived from customers outside of the U.S. Although our financial results are reported in U.S. dollars, a large portion of our sales and operating costs are transacted in Euros, Chinese yuan, Japanese yen and other foreign currencies.

7

Accordingly, our business is subject to the political, economic and other risks that are inherent in operating in foreign countries. These risks include, but are not limited to:

•exposure to the risk of foreign currency fluctuations, where payment for products is denominated in a currency other than U.S. dollars;

•variability in the U.S. dollar value of foreign currency-denominated assets, earnings and cash flows;

•difficulty enforcing agreements, including patents and trademarks, and collecting receivables through foreign legal systems;

•trade protection measures and import or export licensing requirements;

•tax rates in certain foreign countries that exceed those in the U.S., the imposition of withholding requirements on foreign earnings and restrictions on repatriation of foreign earnings;

•elevated risk of terrorist activity, war or civil unrest;

•the impact of global pandemics;

•imposition of tariffs, exchange controls or other restrictions, including tariffs imposed by the U.S. and responsive tariffs imposed by China and the European Union;

•difficulty in staffing and managing global operations;

•required compliance with a variety of existing and emerging foreign laws and regulations and U.S. laws and regulations, such as the Foreign Corrupt Practices Act, applicable to our international operations, and significant compliance costs and penalties for failure to comply with any of these laws and regulations; and

•changes in general economic and political conditions in countries where we operate, including emerging markets, continued volatility in currency exchange rates and uncertainties caused by the United Kingdom's exit from the European Union.

These risks could have an adverse effect on our financial position, results of operations or cash flows. In addition, foreign currency fluctuations could also make our products more expensive than competitors' products not subject to these fluctuations, which could adversely affect our revenues and profitability in international markets. As further described in Item 7 of Part II of this Annual Report on Form 10-K, revenue for fiscal year 2020 was unfavorably impacted by currency translation.

Our business is subject to competition, which could cause us to have to adjust our product pricing or otherwise adjust our operations in order to remain competitive, and any of these changes could impact our operations and financial condition.

Our products are sold in competitive markets throughout the world. Competition is based on application knowledge, product features and design, brand recognition, reliability, technology, breadth of product offerings, price, delivery, customer relationships and after-market support. If we are not perceived as competitive in overall value as measured by these criteria, our customers would likely choose solutions offered by our competitors or developed internally. In order to remain competitive, we may have to adjust our product pricing or otherwise make changes to our operations, which could potentially impact our financial condition.

Our business is subject to customer demand cycles, and changes in those cycles may impact customer demand for our products, which could cause us to fail to meet our expectations as to revenue.

For many of our products, orders are subject to customers' procurement cycles and their willingness and ability to invest in capital, especially in the cyclical automotive, aircraft, entertainment and machine tool industries. Any event that adversely impacts those customers' new product development activities may reduce their demand for our products, which in turn will impact our revenue.

We may experience difficulty obtaining materials or components for our products, or the cost of materials or components may increase, which could adversely impact our production cycle and our margins.

We purchase materials and components from third-party suppliers, some of whom may be competitors. Other materials and components may be provided by a limited number of suppliers or by sole sources and could only be replaced with difficulty or at significant added cost. Additionally, some materials or components may become scarce or difficult to obtain in the market or they may increase in price. This could adversely affect the lead time within which we receive the materials or components, and in turn affect our commitments to our customers, or could adversely affect the cost or quality of materials. Our intention is to partner with suppliers who engage in supply chain transparency and responsible sourcing and who support human rights.

If we fail to achieve our long-term growth plans for the expansion of the business, our business and financial condition could be negatively impacted.

In addition to market penetration, our long-term success depends on our ability to expand our business through (a) new product development and service offerings; (b) mergers and acquisitions; and/or (c) geographic expansion.

8

New product development and service offerings require that we maintain our ability to improve existing products, continue to bring innovative products and services to market in a timely fashion, and address changing global trends, to meet the needs and standards of current and potential customers. Our products and services may become less competitive or eclipsed by technologies to which we do not have access, or which render our solutions obsolete.

Mergers and acquisitions will be accompanied by risks that may include:

•failure to achieve, or delays in achieving, the financial and strategic goals, including growth opportunities and cost synergies, for the acquired and combined businesses;

•difficulty integrating the operations and personnel of the acquired businesses, including the inability to eliminate duplicative costs or the substantial expenses that may be incurred in connection with integration;

•disruption of ongoing business and acquired business and distraction of management from the operation of both businesses;

•dilution of existing shareholders and earnings per share;

•unanticipated, undisclosed or inaccurately assessed liabilities, legal risks and costs;

•reputation risk associated with any pre-existing legal matters resulting from the acquired business;

•legal and regulatory requirements if the acquired business was not formerly a public company; and

•difficulties retaining the key vendors, customers or employees of the acquired business.

Acquisitions of businesses having a significant presence outside the U.S. will increase our exposure to the risks of international operations discussed in the risks relating to our business and operations.

Geographic expansion may be outside of the U.S., and hence will be disproportionately subject to the risks of international operations discussed in the risks relating to our business and operations.

For further information on our business acquisitions, see Note 18 to the Consolidated Financial Statements included in Item 8 of Part II of this Annual Report on Form 10-K.

We initiated several restructuring actions during fiscal year 2020 and if these actions do not provide the results we expect or the cost of such actions is greater than our estimates, our financial condition and results of operations could be negatively impacted.

During fiscal year 2020, we initiated several restructuring actions through a series of global workforce reductions and facility closures, including the reorganization of our European operations within Test & Simulation intended to increase organizational effectiveness, gain operational efficiencies and provide cost savings that can be reinvested in our growth initiatives, a workforce reduction within Test & Simulation to reduce the overall cost structure in response to COVID-19, and a product rationalization of certain product lines in China designed to increase organizational effectiveness, gain operational efficiencies, improve profitability and provide permanent cost savings. We can make no assurances that our current estimates of costs and timing of these restructuring actions will be accurate or that additional costs will not be incurred as we continue the restructuring actions. Any differences from our current estimates could be material and could adversely impact our business, financial condition and results of operations through delays in our timeline or increased costs. Additionally, if these actions fail to provide the operational efficiencies and cost savings that we expect, our financial condition and results of operations could be materially impacted.

Certain Test & Simulation production operations in China are performed by our contract manufacturing partner and may be subject to delays, increased costs or other unanticipated consequences.

We partner with a contract manufacturer in China to provide organizational effectiveness and gain efficiencies in production processes for test systems manufactured in China. While we believe our China contract manufacturing partner to be qualified to manufacture our Test & Simulation segment products, we may need to address quality and delivery issues due to manufacturing performed outside of our control. Significant quality or delivery schedule concerns and unforeseen costs may adversely affect our relationships with customers and our overall business, financial condition or results of operations.

We design and manufacture first-of-a-kind products, and our inability to accurately plan for these new products may result in higher-than-expected costs or damage to our reputation with our customers.

We design and build systems that are unique and innovative and, in some cases, the first created to address complex and unresolved issues. The design, manufacture and support of these systems may involve higher than planned costs. If we are unable to meet our customers' expectations, our reputation and ability to further utilize our expertise will likely be damaged.

9

Backlog, sales, delivery and acceptance cycle for many of our products is irregular and may not develop as anticipated, which could require us to incur increased expenses or otherwise result in fluctuations in our periodic financial results.

Many of our products have long sales, delivery and acceptance cycles. In addition, certain contracts within our backlog are subject to order cancellations. If an order is canceled, we typically would only be entitled to receive reimbursement from the customer for actual costs incurred under the arrangement plus a reasonable margin. Events may cause recognition of orders, backlog and results of operations to be irregular over shorter periods of time. These factors include the timing of individual large orders which may be impacted by interest rates, customer capital spending and product development cycles, design and manufacturing problems, capacity constraints, delays in product readiness, damage or delays in transit, problems in achieving technical performance requirements, and various customer-initiated delays. Any such delay or any cancellations may cause fluctuations in our reported periodic financial results and may cause our stated backlog conversion to revenue to be inaccurate.

We may be subject to product liability or other commercial litigation, which could be expensive, damage our reputation, or otherwise require significant management time and attention, each of which could adversely impact our business.

Our products or services may be claimed to cause or contribute to personal injury or property damage to our customers' facilities, which could damage our reputation or necessitate a product recall. Additionally, we are, at times, involved in commercial disputes with third parties, such as customers, vendors and others. The ensuing claims may arise singularly, in groups of related claims or in class actions involving multiple claimants. Such claims, litigation and product recalls may be expensive and time consuming to resolve and may result in substantial liability to us, and any liability and related costs and expenses may not be recoverable through insurance or other forms of reimbursement.

We may experience difficulties obtaining and retaining the services of skilled employees, which could require us to incur additional costs to fill such positions or retain such employees, which may then require us to delay planned investments in our business.

We rely on knowledgeable, experienced and skilled technical personnel, particularly engineers, sales management and service personnel, to design, assemble, sell and service our products. We may be unable to attract, retain and motivate a sufficient number of such people, which could require us to incur additional costs to fill such positions or retain such employees, which could then adversely affect our business by delaying our ability to make other investments or changes as planned. The inability to transfer knowledge and transition between roles within these teams could also adversely affect our business by delaying or impacting our ability to fulfill customers' orders.

Risks Relating to our Indebtedness and Financial Position

We have recently recognized impairment charges for goodwill, indefinite-lived intangibles and long-lived assets, and we may need to recognize further impairments in the future, which could adversely impact our financial condition and results of operations.

As of October 3, 2020, the net carrying value of goodwill, indefinite-lived intangible and long-lived assets (property and equipment, net and intangible assets, net) totaled $618,845. We periodically assess the value of these assets for impairment in accordance with U.S. generally accepted accounting principles (GAAP). Significant negative industry or economic trends, disruptions to our businesses, significant unexpected or planned changes in use of the assets, divestitures and market capitalization declines may result in impairments to goodwill and other long-lived assets.

As discussed in Note 1 to the Consolidated Financial Statements included in Item 8 of Part II of this Annual Report on Form 10-K, for fiscal year 2020 we recorded an impairment charge to goodwill and long-lived assets of approximately $291,389, which reflects impairments to each of the Test & Simulation excluding E2M and R&D (Legacy Test), E2M and PCB reporting units. This impairment was generally driven by a decline in market conditions, including a sustained decrease in our stock price, and the current outlook for sales and projected profitability in the impacted reporting units. These impairment charges negatively impacted our results of operations for fiscal year 2020 and future impairment charges could have a further adverse effect on our results of operations.

The level and terms of our indebtedness may limit our ability to operate our business as we desire and may require the use of our available cash resources to meet repayment obligations, which could reduce the cash available for other purposes and could adversely affect our business and results of operations.

We have a senior secured credit facility that provides for a $200,000 revolving credit facility (the Revolving Credit Facility) and a $460,000 tranche B term loan facility (the Term Facility), both of which require that we pay a variable interest rate on outstanding borrowings, as well as $350,000 in aggregate principal amount of 5.750% senior unsecured notes due 2027. The debt under the tranche B term loan facility amortizes in equal quarterly installments in an aggregate annual amount equal to 1% of the original principal amount and matures on July 5, 2023.

10

As of October 3, 2020, we had $244,671 outstanding under our senior secured credit facilities, consisting of $169,095 on our tranche B term loan facility and $75,576 drawn under our revolving credit facility, and we had $350,000 in aggregate principal amount of senior unsecured notes outstanding. We may, at times, use debt under the revolving credit facility to continue to finance the growth of the business through acquisitions, finance working capital needs or purchase shares of our common stock.

Our substantial debt could have important consequences to us, including:

•increasing our vulnerability to general economic and industry conditions;

•requiring a substantial portion of our cash flow used in operations to be dedicated to the payment of principal and interest on our indebtedness, which would reduce our liquidity and our ability to use our cash flow to fund our operations, capital expenditures and future business opportunities;

•exposing us to the risk of increased interest rates, and corresponding increased interest expense, because future borrowings under our senior secured credit facilities would be at variable rates of interest;

•reducing funds available for working capital, capital expenditures, acquisitions and other general corporate purposes due to the costs and expenses associated with such debt;

•limiting our ability to obtain additional financing for working capital, capital expenditures, debt service requirements, acquisitions, and general corporate or other purposes;

•limiting our ability to adjust to changing marketplace conditions and placing us at a competitive disadvantage compared to our competitors who may have less debt; and

•potentially causing us to fail to comply with the financial and other restrictive covenants in our debt instruments, which, among other things, require us to maintain specified financial ratios, which failure could, if not cured or waived, have a material adverse effect on our ability to fulfill our obligations under our senior secured credit facilities and the senior unsecured notes and on our business and prospects generally.

In addition, the credit agreement that governs our senior secured credit facilities and the indenture that governs the senior unsecured notes impose significant operating and financial restrictions on us, including limitations on our ability to, among other things, incur additional indebtedness (including guarantee obligations); incur liens; engage in mergers, consolidations and certain other fundamental changes; dispose of assets; make advances, investments and loans; engage in certain sale and leaseback transactions; engage in certain transactions with affiliates; pay dividends, distributions and other payments in respect of capital stock; repurchase or retire capital stock, warrants or options; and engage in other actions that we may believe are advisable or necessary for our business. As a result of these restrictions, we are limited as to how we conduct our business and we may be unable to raise additional debt or equity financing to compete effectively or to capitalize on available business opportunities. Further, our tranche B term loan facility is also subject to mandatory prepayments in certain circumstances and requires a prepayment of a certain percentage of our excess cash flow. Any future mandatory prepayments will reduce our cash available for other purposes and could impact our ability to reinvest in other areas of our business. We do not anticipate an excess cash flow payment will be required in the first quarter of fiscal year 2021.

We can provide no assurances that we will maintain a level of liquidity sufficient to permit us to pay the principal, premium and interest on our indebtedness. If our cash flows and capital resources are insufficient to fund our debt service obligations, we may be forced to reduce or delay capital expenditures, sell assets, seek additional capital, or restructure or refinance our indebtedness. These alternative measures may not be successful and may not permit us to meet our scheduled debt service obligations, which could cause us to default on our debt obligations and impair our liquidity. In the event of a default under any of our indebtedness, the holders of the defaulted debt could elect to declare all the funds borrowed to be due and payable, together with accrued and unpaid interest, which in turn could result in cross-defaults under our other indebtedness. The lenders under our senior secured credit facilities could also elect to terminate their commitments thereunder and cease making further loans, and such lenders could institute foreclosure proceedings against their collateral, and we could be forced into bankruptcy or liquidation.

For further information on our financing arrangements, see Note 9 to the Consolidated Financial Statements included in Item 8 of Part II of this Annual Report on Form 10-K.

Our variable rate indebtedness subjects us to interest rate risk, which could cause our debt service obligations to increase significantly.

Our senior secured credit facilities bear, and other indebtedness we may incur in the future may bear, interest at a variable rate. As a result, at any given time interest rates on the senior secured credit facilities and any other variable rate debt could be higher or lower than current levels. If interest rates increase, our debt service obligations on our variable rate indebtedness will increase even though the amount borrowed remains the same, and therefore net income and associated cash flows, including cash available for servicing our indebtedness, will correspondingly decrease.

11

Increases in interest rates may directly impact the amount of interest we are required to pay and reduce earnings accordingly. In addition, developments in tax policy as a part of the Tax Act, such as the disallowance of tax deductions for a portion of the interest paid on outstanding indebtedness, could have a material adverse effect on our financial condition and results of operations.

Despite our current level of indebtedness, the terms of our existing indebtedness allow us, under certain circumstances, to incur substantially more debt, incur substantial ordinary course operating obligations, and enter into other transactions, which would increase our leverage and further exacerbate the risks to our financial condition described above.

We may be able to incur additional indebtedness in the future. Although the credit agreement that governs our senior secured credit facilities and the indenture that governs the senior unsecured notes contain restrictions on incurring additional indebtedness and entering into certain types of other transactions, these restrictions are subject to a number of qualifications and exceptions. Additional indebtedness incurred in compliance with these restrictions could be substantial. In addition, these restrictions do not prevent us from incurring obligations, such as certain trade payables, that do not constitute indebtedness as defined under our debt instruments. To the extent we incur additional indebtedness or other obligations, the risks described above may increase.

Risks Relating to Government Regulation, Intellectual Property, Information Security and Other Policies

Our failure to comply with laws and regulations regarding government contracts could adversely impact our ability to continue to do business with the government, which could lead to a decline in revenue and future business opportunities.

Government business is important to us and is expected to increase in the future. Revenue from U.S. government related contracts varies by year. Such revenue as a percent of our total revenue was 11%, 6% and 4% for fiscal years 2020, 2019 and 2018, respectively.

We must comply with procurement laws and regulations relating to the formation, administration and performance of U.S. government contracts. Failure to comply with these laws and regulations could lead to suspension or debarment from U.S. government contracting or subcontracting and result in administrative, civil or criminal penalties. Failure to comply could also have a material adverse effect on our reputation, our ability to secure future U.S. government contracts and export control licenses, and our results of operations or financial condition. These laws and regulations also create compliance risks and affect how we do business with federal agency clients. U.S. government contracts, as well as contracts with certain foreign governments with which we do business, are also subject to modification or termination by the government, either for the convenience of the government or for default as a result of our failure to perform under the applicable contract. Further, any investigation relating to, or suspension or debarment from, U.S. government contracting could have a material impact on our results of operations as, during the duration of any suspension or debarment, we would be prohibited or otherwise limited in our ability to enter into prime contracts or subcontracts with U.S. government agencies, certain entities that receive U.S. government funds or that are otherwise subject to the Federal Acquisition Regulations, and certain state government or commercial customers who decline to contract with suspended or debarred entities. A federal suspension could also impact our ability to obtain export control licenses which are materially important to our business.

Compliance with government regulations and policies imposes costs and other constraints, which may impact our financial condition or ability to do business in certain jurisdictions.

Our manufacturing operations and past and present ownership and operation of real property subject us to extensive and changing federal, state, local and foreign laws and regulations, including laws and regulations pertaining to regulatory compliance, such as environmental, health and safety, employee benefits, import and export compliance, intellectual property, product liability, tax matters and securities regulation. We expect to continue to incur costs to comply with these laws and may incur penalties for any failure to do so.

In particular, some of our export sales require approval from the U.S. government. Recent changes in policy may increase the number of our export sales that require licenses, in particular for certain sales to customers located in China, which would increase both our costs to make such sales and the time to do so. Depending on how these changes in policy are interpreted, this could limit our ability in certain cases to recognize these sales orders at all. Moreover, changes in political relations between the U.S. and foreign countries and/or specific potential customers for which export licenses may be required may cause a license application to be delayed or denied, or a previously issued license withdrawn, rendering us unable to complete a sale or vulnerable to competitors who do not operate under such restrictions.

In addition, the U.S. government has imposed tariffs on certain products imported from China as well as steel and aluminum imported from the European Union, Mexico and Canada. China and the European Union have imposed tariffs on U.S. products in response. These tariffs could force our customers or us to consider various strategic options including, but not limited to, looking for different suppliers, shifting production to facilities in different geographic regions, absorbing the additional costs or

12

passing the cost on to customers. Moreover, any retaliatory actions by other countries where we operate could also negatively impact our financial performance.

We may fail to protect our intellectual property effectively or may infringe upon the intellectual property of others, which could result in increased costs to defend our intellectual property rights or could cause us to be unable to pursue new business opportunities.

We have developed significant proprietary technology and other rights that are used in our businesses. We rely on trade secret, copyright, trademark and patent laws and contractual provisions to protect our intellectual property. While we take enforcement of these rights seriously, other companies such as competitors or others in markets in which we do not participate may attempt to copy or use our intellectual property for their own benefit.

The intellectual property of others also has an impact on our ability to offer some of our products and services for specific uses or at competitive prices. Competitors' patents or other intellectual property may limit our ability to offer products and services to our customers. Any infringement on the intellectual property rights of others could result in litigation and adversely affect our ability to continue to provide, or could increase the cost of providing, our products and services.

Intellectual property litigation can be very costly and could result in substantial expense and diversion of our resources, both of which could adversely affect our business, financial condition and results of operations. In addition, there may be no effective legal recourse against infringement of our intellectual property by third parties, whether due to limitations on enforcement of rights in foreign jurisdictions or as a result of other factors.

If we are unable to protect our information systems against misappropriation of data or breaches of security or we are unable to comply, or are perceived as being unable to comply, with evolving regulations and legal obligations related to data privacy, data protection and information security, our business, financial condition or results of operations may be adversely impacted due to costs we may have to incur to correct such issues or the reputational harm we may face.

Information security risks have generally increased in recent years because of the proliferation of new technologies and the increased sophistication of cyber-attacks. Although we strive to have appropriate security controls in place, prevention of security breaches cannot be assured, particularly as cyber threats continue to evolve. As further discussed in Item 7 of Part II of this Annual Report on Form 10-K, in November 2020, we were the victim of a ransomware incident that impacted operations. We have incurred expenses to-date to investigate and resolve the issues resulting from this incident, but as we continue our investigation into this incident, we may also be required to expend additional resources to continue to enhance our privacy and security measures or to resolve any vulnerabilities. The financial and reputational consequences of this incident and these risks could adversely impact our business, financial condition or results of operations.

In addition, our handling of certain data is subject to a variety of existing and emerging laws and regulations, designed by various federal, state and foreign governments to regulate the collection, distribution, use and storage of personal information. Several foreign countries in which we conduct business, including the European Economic Area (EEA), currently have in place, or have recently proposed, laws or regulations concerning privacy, data protection and information security, which are more restrictive than those imposed in the U.S. Some of these laws are in the early stages and we cannot yet determine the impact these laws and regulations, if implemented, may have on our business. However, any failure or perceived failure by us to comply with these privacy laws, regulations, policies or obligations or any security incident that results in the unauthorized release or transfer of personally identifiable information or other customer data in our possession, could result in government enforcement actions, regulatory investigations, litigation, fines and penalties and/or adverse publicity, all of which could require us to change the way we collect and use personal and customer data and/or have an adverse effect on our reputation and business.

We are required to conduct a good faith reasonable country of origin analysis on our use of conflict minerals, which has imposed and may impose additional costs on us and could raise reputational and other risks.

The SEC has promulgated final rules in connection with the Dodd-Frank Wall Street Reform and Consumer Protection Act regarding disclosure of the use of certain minerals, known as conflict minerals, mined from the Democratic Republic of the Congo and adjoining countries. We have incurred and will continue to incur costs associated with complying with these disclosure requirements, including costs to determine the source of any conflict minerals used in our products. We have adopted a policy relating to conflict minerals, incorporating the standards set forth in the Organisation for Economic Co-operation and Development Due Diligence Guidance, which affects the sourcing, supply, and pricing of materials used in our products. As we continue our due diligence, we may face reputational challenges if we are unable to verify the origins for all metals used in our products through the procedures we have and may continue to implement. We may also encounter challenges in our efforts to satisfy customers that may require all of the components of products purchased to be certified as conflict-free. If we are not able to meet customer requirements, customers may choose to disqualify us as a supplier.

13

If we fail to maintain effective processes and controls relative to adherence to our Code of Conduct and related company policies, we may incur costs to remedy these violations and may suffer reputational harm, either of which could adversely affect our business, financial condition or results of operations.

Our Code of Conduct and related company policies, which cover topics such as human and labor rights, anti-bribery, product quality and safety, privacy, security and environmental compliance, promote both a culture of ethical business practices and compliance with legal and regulatory requirements. However, there can be no assurance that all of our employees or agents will refrain from acting in violation of such policies and procedures or that our processes and controls will be sufficient to detect any such violations. The investigation into potential violations of these policies, or even allegations of such violations, and the related evaluation of our internal controls, could disrupt our operations, involve significant management distraction, and lead to significant costs and expenses, including legal and accounting fees, and such expenses may have a material adverse effect on our financial results. Further, if our employees or agents violate such policies and procedures, such actions could result in non-compliance with our internal control over financial reporting. If we, or our employees or agents acting on our behalf, are found to have engaged in practices that violate these policies and/or applicable law, we could suffer severe fines and penalties, repayment of ill-gotten gains, injunctions on future conduct, securities litigation, material weaknesses in our internal control over financial reporting, delayed regulatory filings and other consequences that may have a material adverse effect on our business, financial condition or results of operations. In addition, our reputation, sales activities or stock price could be adversely affected if we become the subject of any negative publicity related to actual or potential violations of applicable laws and regulations.

Changing environmental regulations and industry standards, as well as the potential physical risks of climate change, create uncertainty and the costs of compliance with such regulations and standards could impact our results of operations and financial position.

Increased public awareness and concern regarding environmental risks, including global climate change, may result in more international, regional, and/or federal requirements or industry standards to reduce or mitigate global warming and other environmental risks. These regulations or standards could be more restrictive than those currently in place. Moreover, there continues to be a lack of consistent climate legislation, which creates economic and regulatory uncertainty. In addition, the physical risks of climate change may impact the availability and cost of materials and natural resources, sources and supply of energy, product demand and manufacturing. While no one product line puts us at substantial risk of climate change, our global operations require us to be cognizant of risks that span the globe and could impact our business as a whole. If the changing environmental laws or regulations or industry standards impose significant operational restrictions and compliance requirements upon us or our products, or our operations are disrupted due to physical impacts of climate change, our business, capital expenditures, results of operations, financial condition and competitive position could be negatively impacted.

ITEM 1B. UNRESOLVED STAFF COMMENTS

None.

ITEM 2. PROPERTIES

Our properties consist of owned and leased facilities for manufacturing, engineering, sales, service administration, research and warehouse space. We own our corporate headquarters, located in Eden Prairie, Minnesota, which is also the primary location for Test & Simulation manufacturing and research. We own facilities in Depew, New York and Cary, North Carolina, which are the primary manufacturing and research locations for Sensors. In addition, we own manufacturing, engineering, sales and service administration facilities in the U.S., Germany and China. We lease space in the U.S., Europe and Asia for manufacturing, engineering, sales, service administration, research and warehouse space. We consider our current facilities suitable for their purpose and adequate to support our business.

Additional information relative to lease obligations is included in Item 7 of Part II of this Annual Report on Form 10-K.

ITEM 3. LEGAL PROCEEDINGS

Discussion of legal matters is incorporated by reference from Note 19 to the Consolidated Financial Statements included in Item 8 of Part II of this Annual Report on Form 10-K and should be considered an integral part of Item 3 of Part I of this Annual Report on Form 10-K.

ITEM 4. MINE SAFETY DISCLOSURES

Not applicable.

14

PART II

ITEM 5. MARKET FOR REGISTRANT'S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES

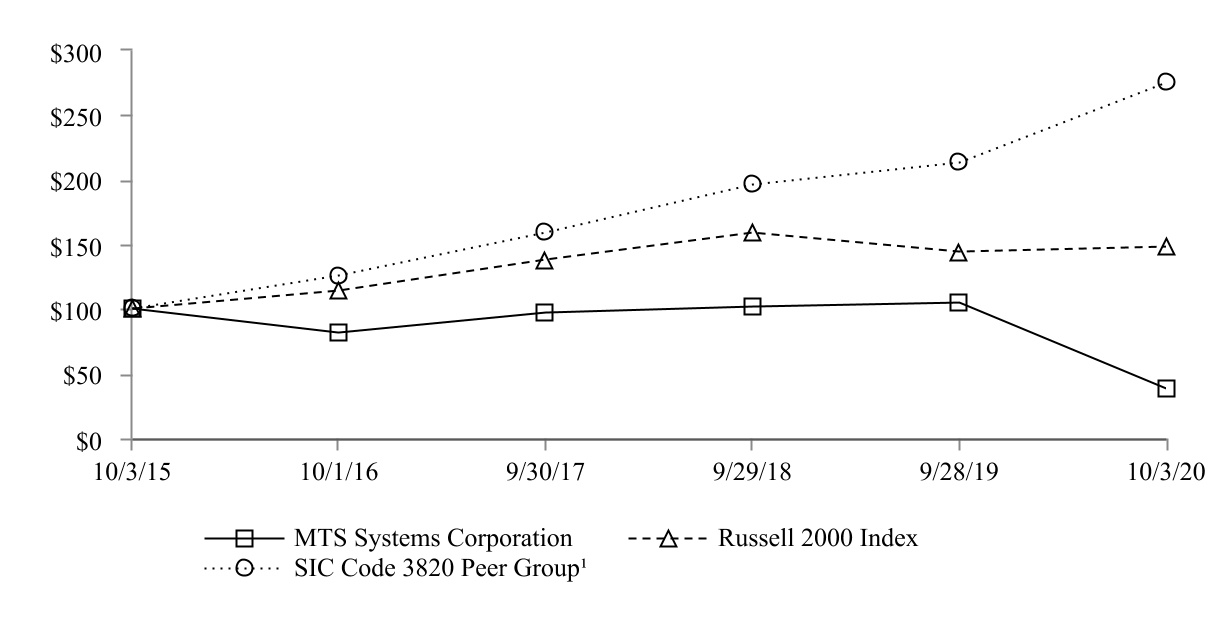

Shares of our common stock are traded on the Nasdaq Global Select Market under the trading symbol MTSC. The number of record holders of our common stock, par value $0.25 per share, as of December 10, 2020 was 610. This number does not reflect shareholders who hold their shares in the name of broker-dealers or other nominees.

Issuer Purchases of Equity Securities

| Total Number of Shares Purchased | Average Price Paid per Share | Total Number of Shares Purchased As Part of Publicly Announced Plans or Programs | Maximum Number of Shares that May Yet be Purchased As Part of Publicly Announced Plans or Programs | |||||||||||||||||||||||

| June 28, 2020 – August 1, 2020 | — | $ | — | — | 438 | |||||||||||||||||||||

| August 2, 2020 – August 29, 2020 | — | $ | — | — | 438 | |||||||||||||||||||||

| August 30, 2020 – October 3, 2020 | — | $ | — | — | 438 | |||||||||||||||||||||