Exhibit 13

ANNUAL REPORT OF THE TRUSTEES OF

MESABI TRUST

For The Fiscal Year Ended January 31, 2024

ADDRESS

Mesabi Trust

c/o Deutsche Bank Trust Company Americas

Trust & Agency Services

1 Columbus Circle, 17th Floor

Mail Stop: NYC01-1710

New York, NY 10019

(904) 271-2520 (telephone)

www.mesabi-trust.com

REGISTRAR AND TRANSFER AGENT

Deutsche Bank Trust Company Americas

LEGAL COUNSEL

Fox Rothschild LLP

REGISTRANT INFORMATION

Mesabi Trust maintains a website that provides access to its annual, quarterly, and other reports it files with the Securities and Exchange Commission. Such reports can be accessed at www.mesabi-trust.com. Mesabi Trust will provide, upon the written request of any Unitholder addressed to the Trustees at the above address and without charge to such Unitholder, (i) a paper copy of Mesabi Trust’s Annual Report on Form 10-K for the fiscal year ended January 31, 2024 (the “Annual Report”) as filed with the Securities and Exchange Commission pursuant to the Securities Exchange Act of 1934, as amended, and (ii) the Trustees’ Code of Ethics.

Table of Contents

Special Note Regarding Forward-Looking Statements

This report contains certain forward-looking statements with respect to iron ore pellet production, iron ore pricing and adjustments to pricing, shipments by Northshore Mining Company (“Northshore”) during 2024, royalty (including bonus royalty) amounts, and other matters, which statements are intended to be made under the safe harbor protections of the Private Securities Litigation Reform Act of 1995, as amended. Actual production, prices, price adjustments, and shipments of iron ore pellets, as well as actual royalty payments (including bonus royalties) could differ materially from current expectations due to inherent risks and uncertainties such as general adverse business and industry economic trends, uncertainties arising from war, terrorist events, the impact of the coronavirus (COVID-19) pandemic and other global events, higher or lower customer demand for steel and iron ore, decisions by mine operators regarding curtailments or idling production lines or entire plants, environmental compliance uncertainties, difficulties in obtaining and renewing necessary operating permits, higher imports of steel and iron ore substitutes, processing difficulties, consolidation and restructuring in the domestic steel market, market inputs tied to indexed price adjustment factors found in some pellet supply agreements between Cleveland-Cliffs Inc. (“Cliffs”) and its customers (“Cliffs Customer Contracts”) resulting in future adjustments to royalties payable to Mesabi Trust and other factors. Further, historically some of the royalties earned by Mesabi Trust have been based on estimated prices that are subject to interim and final adjustments, which can be positive or negative, and are dependent in part on multiple price and inflation index factors under agreements to which Mesabi Trust was not a party and that were not known until after the end of a contract year. Although the Mesabi Trustees believe that any such forward-looking statements are based on reasonable assumptions, such statements are subject to risks and uncertainties, which could cause actual results to differ materially. Additional information concerning these and other risks and uncertainties is contained under the caption “Risk Factors” in Mesabi Trust’s filings with the Securities and Exchange Commission, including this Annual Report. Mesabi Trust undertakes no obligation to publicly update or revise any of the forward-looking statements made herein to reflect events or circumstances after the date hereof.

Mesabi Trust qualifies as a “Small Reporting Company” under Item 10(f)(1) of Regulation S-K. Therefore, Mesabi Trust has determined to comply with the disclosure requirements applicable to Smaller Reporting Companies in this Annual Report on Form 10-K. Mesabi Trust has elected to voluntarily include certain disclosures not required by a Smaller Reporting Company.

OVERVIEW

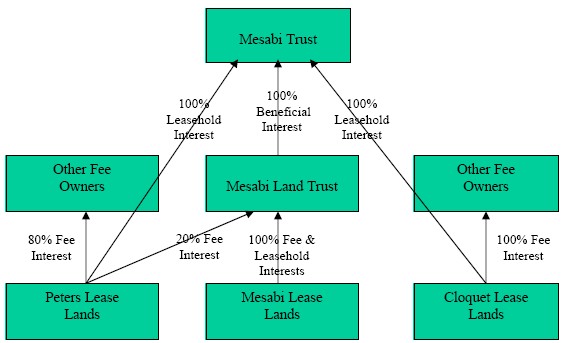

Mesabi Trust (“Mesabi Trust” or the “Trust”), formed pursuant to an Agreement of Trust dated July 18, 1961, as amended by the Amendment to the Agreement of Trust dated as of October 25, 1982 (the “Agreement of Trust”), is a trust organized under the laws of the State of New York. Mesabi Trust holds all of the interests formerly owned by Mesabi Iron Company (“MIC”), including all right, title and interest in the Amendment of Assignment, Assumption and Further Assignment of Peters Lease dated August 17, 1989 among the trustees of Mesabi Trust, Bruce D. Sherling, as Trustee in Bankruptcy for the Estate of Reserve Mining Company, and Cypress Northshore Mining Corporation, predecessor to Northshore (referred to as the “Amended Assignment of Peters Lease” or the “Royalty Agreement”), the Amendment of Assignment, Assumption and Further Assignment of Cloquet Lease dated August 17, 1989 among the trustees of Mesabi Trust, Bruce D. Sherling, as Trustee in Bankruptcy for the Estate of Reserve Mining Company, and Cypress Northshore mining corporation (referred to as the “Amended Assignment of Cloquet Lease” and together with the Amended Assignment of Peters Lease, the “Amended Assignment Agreements”), the beneficial interest in a trust organized under the laws of the State of Minnesota to administer the Mesabi Fee Lands (as defined below) as the trust corpus in compliance with the laws of the State of Minnesota on July 18, 1961 (the “Mesabi Land Trust”) and all other assets and property identified in the Agreement of Trust. The Amended Assignment of Peters Lease relates to an Indenture made as of April 30, 1915 among East Mesaba Iron Company (“East Mesaba”), Dunka River Iron Company (“Dunka River”) and Claude W. Peters (the “Peters

1

Lease”) and the Amended Assignment of Cloquet Lease relates to an Indenture made May 1, 1916 between Cloquet Lumber Company and Claude W. Peters (the “Cloquet Lease”).

A pass-through trust with certificates of beneficial interest in the trust traded on the New York Stock Exchange

Pursuant to a ruling from the Internal Revenue Service, which ruling was based on the terms of the Agreement of Trust including the prohibition against conducting any business, the Trust is not taxable as a corporation for federal income tax purposes. Instead, the holders of Certificates of Beneficial Interest in Mesabi Trust (“Unitholders”) are considered “owners” of the Trust and the Trust’s income is taxable directly to the Unitholders. The Certificates of Beneficial Interest in Mesabi Trust are listed on the New York Stock Exchange (“NYSE”) and is therefore subject to extensive regulation under, among others, the Securities Act of 1933, the Securities Exchange Act of 1934, the Sarbanes-Oxley Act of 2002 (“Sarbanes-Oxley”), each as amended, and the rules and regulations of the NYSE.

Limited authorities and responsibilities of the Trustees

The Agreement of Trust specifically prohibits the Trustees of Mesabi Trust (the “Trustees”) from entering into or engaging in any business. This prohibition seemingly applies even to business activities the Trustees may deem necessary or proper for the preservation and protection of the Trust Estate (as defined on page 31 of this Annual Report). Accordingly, the Trustees’ activities in connection with the administration of Trust assets are limited to collecting income, paying expenses and liabilities, distributing net income to the Unitholders after the payment of, or provision for, such expenses and liabilities, and protecting and conserving the assets held by the Trust.

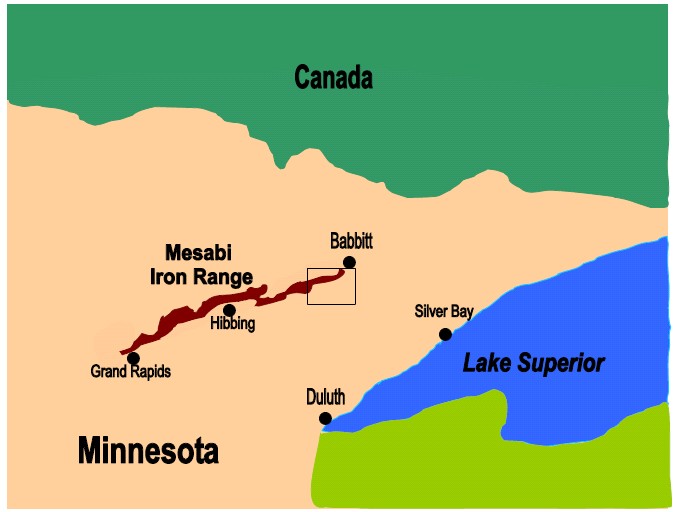

The Trustees do not intend to expand their responsibilities beyond those permitted or required by the Agreement of Trust, the Amendment to the Agreement of Trust dated October 25, 1982 (the “Amendment”), and those required under applicable law. The Trust has no employees, but it engages consultants to assist the Trustees in, among other things, monitoring the volume and sales prices of iron ore products shipped from Silver Bay, Minnesota, based on information supplied to the Trustees by Northshore, the lessee/operator of the lands leased under the Peters Lease and Cloquet Lease (the “Peters Lease Lands” and “Cloquet Lease Lands,” respectively, as further described on page 33 of this Annual Report) and the 20% fee interest of certain lands that are particularly described in, and subject to a mining lease under, the Peters Lease (the “Mesabi Fee Lands,” and together with the Peters Lease Lands and Cloquet Lease Lands, “Mesabi Trust Lands”), and Northshore’s parent company, Cliffs. References to Northshore in this Annual Report, unless the context requires otherwise, are applicable to Cliffs as well.

The information regarding amounts and sales prices of shipped iron ore products is used to compute the royalties payable to the Trust by Northshore. The Trustees request material information, from time to time, for use in the Trust’s periodic reports and as part of their evaluation of the Trust’s disclosure controls and procedures. The Trustees rely on Northshore to provide accurate and timely information for use in the Trust’s periodic and current reports filed with the Securities and Exchange Commission (the “SEC”).

Duration and Termination of the Trust

The Trust is governed by New York trust and estate law, which prohibits creation of any trust estate that suspends the power of alienation by a condition or limitation for a period longer than lives in being at the time of the creation of such trust estate, plus a term of twenty-one years. Pursuant to a ruling from the Internal Revenue Service, which ruling was based on the terms of the Agreement of Trust including the prohibition against entering into any business, the Trust is not taxable as a corporation for federal income tax purposes.

2

Instead, the Unitholders are considered “owners” of the Trust and the Trust’s income is taxable directly to the Unitholders. In accordance with the Agreement of Trust, the Trust may continue to remain in force and effect until twenty-one years after the death of the last survivor of twenty-five persons named in an exhibit to the Agreement of Trust. Based upon the results of research conducted by the Trust’s outside legal counsel, as of February 2024, the Trustees believed that there are a number of individuals named in the Agreement of Trust who were alive as of February 2024, the youngest of whom is believed to be 63 years old.

The Trust may be terminated earlier at any time by the action of Unitholders holding 75% of the total Units of Beneficial Interest of the Trust as evidenced by any instrument executed by such Unitholders or by such Unitholders’ voting in favor of the termination of the Trust at a duly called and held meeting of the Unitholders.

References in the Annual Report

All references in this discussion and in this Annual Report on Form 10-K to iron ore products “shipped” shall include iron ore products that are actually shipped from Silver Bay, Minnesota and/or stockpiled for intercompany use that Cliffs has deemed shipped, as referenced by the parties to, and in accordance with, the Amended Assignment of Peters Lease. Similarly, all references in this discussion and in this Annual Report on Form 10-K to “shipments” shall include actual shipments of iron ore products and/or iron ore products stockpiled for intercompany sale that Cliffs has deemed shipped, as referenced by the parties to, and in accordance with, the Amended Assignment of Peters Lease. After the start of the 2019 arbitration and Cliffs’ change in practices, Cliffs accrues royalty payment to the Trust upon production to stockpile for DR pellets to be sold for internal use at facilities owned by Cliffs or its subsidiaries. Following the outcome of the 2019 arbitration, Cliffs began accruing royalty payments to the Trust for both DR pellets and standard pellets to be sold for internal use at facilities owned by Cliffs or its subsidiaries. As a result, the Trust recognizes revenue for internal use pellets upon production of those pellets, regardless of pellet grade. Pellets produced by Northshore that are not designated for internal use by Cliffs, or its subsidiaries, and instead are intended for sale to third parties in arms’-length sales, continue to be recognized as revenue upon shipment from Silver Bay, Minnesota.

3

RISK FACTORS

The results of operations and financial condition of the Trust are subject to various risks. Some of these risks are described below, and you should take such risks into account in evaluating the Trust or any investment decision involving the Trust. This section does not describe all risks that may be applicable to the Trust and it is intended only as a summary of certain material risk factors. More detailed information concerning the risk factors described below may also be contained in other sections of this Annual Report.

Risks Related to Pass-Through Trust Structure of Mesabi Trust

The Trustees have no control over the operations, sales and marketing efforts or other activities of Cliffs or Northshore.

Except within the framework of the Royalty Agreement and the enforcement of rights thereunder, neither the Trust nor the Trustees have any control over the operations, decisions to reduce or idle operations, sales and marketing efforts or other activities of Cliffs or its wholly-owned subsidiary, Northshore. Accordingly, the royalty income of the Trust is highly dependent upon the activities, investments and operational decisions of Cliffs and Northshore, including temporary or permanent reduction or idling of operations, the supply and demand of suppliers and customers in the iron ore and steel industry in the U.S. and internationally, and the terms and conditions of the Amended Assignment of Peters Lease. Northshore, together with Cliffs, without any input or influence from the Trust or the Trustees (except within the framework of the Royalty Agreement), control: (i) current operating plans, including iron ore production volumes, decisions to reduce or idle Northshore plant and mining operations, marketing of iron ore products, operating and capital expenditures as they relate to Northshore, environmental and other liabilities and the effects of regulatory changes; (ii) plans for Northshore’s future production, operations and capital expenditures, if any; (iii) geological data relating to iron ore reserve estimates; (iv) sales and marketing efforts, and shipments of iron ore products to customers of Cliffs and the extent to which sales of iron ore products are marketed and sold directly to independent third parties; (v) the terms and conditions, especially related to pricing, price adjustment mechanisms and delivery terms, of the sale of all iron ore products to Cliffs’ customers, including the Cliffs’ Customer Contracts; and (vi) the proportion of iron ore mined from the Mesabi Trust Lands that Cliffs sells to Cliffs’ corporate affiliates versus the proportion Cliffs sells to third parties in arms’-length transactions. Any substantial change in Cliffs’ financial condition or business, or the operations, production and shipments of iron ore products by Northshore, including production curtailments, temporary idling or permanent idling of Northshore operations, about which the Trust may have little or no prior notice, could adversely affect the royalty income of the Trust, as well as the resulting cash available for distribution by the Trust to Unitholders. Further, such developments could have a material adverse impact on the market price of the Trust’s Units.

Cliffs’ announced intentions to shift DR-grade pellet production away from Northshore, use Northshore as a swing operation and idle Northshore operations from time to time, including from May 2022 through April 2023, would reduce or potentially eliminate funds available for distribution to unit holders.

On October 22, 2021, Cliffs, the parent of Northshore, the lessee/operator of the leased lands upon which Mesabi Trust is dependent for its royalties, held a conference call to discuss its third-quarter 2021 earnings. During the call, Lourenco Goncalves, Chairman, President, Chief Executive Officer of Cliffs, disclosed “…we will soon be shifting our DR-grade pellet production away from Northshore and into Minorca, where we will not have to deal with the unreasonable royalty structure at Northshore.” Mr. Goncalves also indicated that “As we plan to no longer sell pellets to third parties in the coming years, Northshore will become a swing operation, which we will keep idle every time we decided to do so. In any event, we will continue to be able to feed our Toledo plant with a consistent feed of DR-grade pellets but from Minorca and not from Northshore.”

4

On February 11, 2022, Cliffs held a conference call to discuss Cliffs’ full year and fourth-quarter 2021 earnings. During the call, Mr. Goncalves disclosed “…with the use of additional scrap in our BOF’s [basic oxygen furnaces], our iron ore needs are not as high as before, and we no longer need to run our mines full out. When determining where to adjust production, our first look is at our cost structure. Because we are now able to produce DR-grade pellets at Minorca, and mainly due to the ridiculous royalty structure we have in place with the Mesabi Trust, we will be idling all production at our Northshore mine, starting in the Spring, carrying through at least to the Fall period, and maybe beyond. At Northshore, no production, no shipments, no royalty payments. We also acknowledge that our strategy to stretch hot metal, by adding increased amounts of scrap to the BOF’s is working extremely well. With more scrap in the BOF’s, we need fewer tons of hot metal to produce the same tonnage of liquid steel. As a consequence, the Northshore idle could go longer than currently planned.”

During Cliffs’ February 11, 2022 earnings call, Mr. Goncalves also said that, “Going forward, [Cliffs] will be limiting the tonnage of iron ore pellets we sell to third parties.”

On July 22, 2022, Cliffs held a conference call to discuss Cliffs’ second-quarter 2022 earnings. During the call, Mr. Goncalves disclosed “… we are now extending the ongoing idle at our Northshore swing facility to at least April of next year. With the increased use of scrap company-wide in our steel making operations made possible by the acquisition of FPT last year, the pellets from Northshore are not needed at this time. Rather than deplete this finite resource for the benefit of the Mesabi Trust and its so-called unit holders, we will keep Northshore idle until we decide otherwise.”

During Cliffs earnings conference call on April 24, 2023, Mr. Goncalves announced: “Our higher levels of steel production have led to the partial restart of some operations at our iron ore mining and pelletizing swing facility at Northshore earlier this month. As you may recall, Northshore has been totally idle since the spring of last year. We will continue to treat that facility as our swing operation. And at this time, we still do not expect to operate Northshore in full any time this year.” The Trustees of Mesabi Trust have not been provided with any additional information regarding the anticipated volume of production, stockpiling or shipping of iron ore products at the Northshore operations in Babbitt and Silver Bay, Minnesota for the remainder of calendar year 2024.

Cliffs had not previously notified the Trust of any of the aforementioned operational changes. Pursuant to the Agreement of Trust, any change to the royalty structure would require an amendment to the royalty agreement, which would require the approval of the Trustees as well as approval of 66 2/3% in interest of the Trust Certificate Holders.

Under the Royalty Agreement, Northshore’s obligation to pay base overriding royalties and royalty bonuses with respect to the sale or use of iron ore products generally accrues upon production or shipment of those products from Silver Bay. However, regardless of whether any shipment has occurred, Northshore is obligated to pay to Mesabi Trust a minimum advance royalty. Each year, the amount of the minimum advance royalty is adjusted (but not below $500,000 per annum) for inflation and deflation. The minimum advance royalty was $1,034,237 for calendar year 2022, $1,100,498 for calendar year 2023 and is $1,129,615 for calendar year 2024.

Operational decisions about when, how often and for how long to idle Northshore operations are solely in the control of Cliffs and Northshore. The Trustees are not notified in advance of such decisions to idle, or to restart, Northshore operations, and the Trustees cannot predict the frequency or duration of such idling events.

Accordingly, these plans, if and when implemented by Cliffs, could have a material adverse effect on Mesabi Trust’s future royalty revenue and could materially reduce or potentially eliminate funds available for distribution. In addition, the market price of the Trust’s Units, which are listed for trading on the NYSE,

5

could be negatively impacted, and the Trust’s ability to continue to meet the continued listing criteria of the NYSE could be compromised, and could result in delisting of our Units.

The limited or lack of arms’-length third-party sales of iron ore products (processed at Northshore using Mesabi Trust iron ore) by Cliffs could lead to uncertainty under the Royalty Agreement with respect to the calculation of royalties, which could in turn result in potential disputes regarding the amount of royalties owed to the Trust.

In order to calculate the royalties owed by Northshore to the Trust, the 1989 Royalty Agreement requires that Northshore make sales of iron ore products to third parties on an arms’-length basis without regard to any other business relationship between Northshore and the third-party buyer of the iron ore products. In order to calculate royalties on less than arms’-length sales (including sales from Northshore to Cliffs’ corporate affiliates), the Royalty Agreement requires reference to the highest contract price obtained by Northshore in the preceding four calendar quarters in a sale to a buyer not affiliated with Northshore and made on an arms’-length basis. Since Cliffs’ acquisition of ArcelorMittal USA in late-2020, and accelerating after Cliffs’ Toledo HBI plant came online in mid-2021, Northshore has increased the proportion of iron ore mined from the Mesabi Trust Lands that it sells to Cliffs’ corporate affiliates and decreased the proportion of such iron ore that it sells to third parties in arms’-length transactions. Cliffs’ public statements beginning in October 2021 indicated that Cliffs will be limiting the tonnage of iron ore pellets that it sells to third parties from all of its mines, and particularly Northshore, which Cliffs idled from May 2022 to April 2023. Cliffs also said it will continue to run Northshore as a swing operation. For the twelve month period ended December 31, 2023, Cliffs has reported to the Trust two low volume shipments of iron ore pellets (produced with iron ore principally mined from Mesabi Trust Lands) to a single third-party customer, which shipments together are much less than one typical boatload of iron ore normally shipped from Silver Bay in arms’-length third-party sale transactions. Cliffs’ quarterly royalty report used the highest price from those two transactions to set the price for royalty purposes for subsequent shipments intended for Cliffs’ affiliates’ internal consumption beginning in July 2023, subject to any newly reported arms’-length third-party customer sale transaction thereafter. The Trust is continuing to evaluate whether such transactions meet the requirements of the Royalty Agreement. Without consistent arms’-length sales from Northshore to third parties, the calculation of royalties on iron ore Northshore ships to Cliffs’ affiliates could be uncertain under the Royalty Agreement, which could in turn result in potential disputes regarding the amount of royalties owed to the Trust.

Cliffs’ Annual Report has cited certain economic and market risks, including risks related to the volatility of commodity prices, uncertainty or weakness in global economic conditions, reduced economic growth in China and oversupply of iron ore and excess steel or imported products, any of which could adversely affect Cliffs’ ability to generate revenue, maintain stable cash flows and fund its operations, which in turn could adversely affect Northshore operations and could adversely affect royalties payable to the Trust.

In Cliffs’ Annual Report, Cliffs disclosed that, as a mining company, Cliffs’ profitability is dependent upon the price of the steel, iron ore and scrap metal, and that the price of steel, iron ore and scrap metal has fluctuated significantly in the recent past and is affected by factors beyond its control including: international demand for, and the impact of higher inflation on, raw materials used in steel production; availability of scrap metal substitutes such as pig iron; commodity prices speculation; rates of global economic growth, especially construction and infrastructure activity that requires significant amounts of steel; changes in the levels of economic activity in the U.S., China, India, Europe and other industrialized or developing economies, including as a result of geopolitical conflicts or otherwise; changes in China’s emissions policies and environmental compliance enforcement practices; changes in the production capacity, production rate and inventory levels of other steel producers, distributors, iron ore suppliers and scrap metal processors and traders; changes in trade laws; volumes of unfairly traded imports; imposition or termination of duties, tariffs, import and export controls and other trade barriers impacting the steel and iron ore markets; climate change

6

and other weather-related disruptions, infectious disease outbreaks, such as the COVID-19 pandemic, or natural disasters that may impact the global supply of steel, iron ore or scrap metal; and the proximity, capacity and cost of infrastructure and transportation. Further, Cliffs stated that its revenues vary in accordance with the prices of the products it sells. During 2023, for example, Cliffs indicated it experienced lower average selling prices for its steel products as compared to 2022 due to the impact from lower index pricing, which resulted in lower revenues despite increased sale volumes. To the extent that commodity prices, including the HRC price, coated and other specialty steel prices, international steel prices and scrap metal prices, significantly decline for an extended period, Cliffs may have to revise its operating plans, including curtailing production, reducing operating costs and deferring capital expenditures. Cliffs also disclosed that it may have to record impairments on its goodwill, intangible assets, long-lived assets and/or inventory. Sustained lower prices also could cause Cliffs to reduce existing reserves if certain reserves can no longer be economically mined or processed at prevailing prices. Particularly during periods of increased inflation resulting in higher input costs, Cliffs may be unable to decrease its costs in an amount sufficient to offset reductions in revenues and may incur losses. These events could have a material adverse effect on Cliffs and, in certain circumstances, could potentially adversely affect Northshore, which in turn, could have a material adverse effect on Cliffs’ ability to pay future royalties owed to the Trust.

Cliffs sells a significant portion of its steel products to the automotive market, and fluctuations or changes in the automotive market could adversely affect Cliffs’ business operations and financial performance, which in turn could adversely affect the royalties payable to the Trust.

Cliffs’ Annual Report indicated that the largest end user of Cliffs’ steel products is the automotive industry in North America. Beyond these direct sales to the automotive industry, Cliffs makes additional sales to distributors and converters, which may ultimately resell some of that volume to the automotive market. In addition to the magnitude of Cliffs’ exposure to the automotive industry, Cliffs faces risks arising from Cliffs’ relative concentration of sales to certain specific automotive manufacturers, and its sales volumes and revenues may be adversely affected if it is unable to renew its fixed-price contracts with one or more significant automotive customers or if those customers choose to move certain portions of their parts business to alternate suppliers. In addition, automotive production and sales are cyclical and sensitive to general economic conditions and other factors, including interest rates, consumer credit, spending and preferences, and supply chain disruptions. If automotive production and sales decline, whether due to consumers facing reduced purchasing power caused by inflation, higher interest rates or otherwise, Cliffs’ sales and shipments to the automotive market are likely to decline in a corresponding manner. Adverse impacts that Cliffs may sustain as a result include, without limitation, lower margins because of the need to sell steel to less profitable customers and markets, higher fixed costs from lower steel production if Cliffs is unable to sell the same amount of steel to other customers and markets, and lower sales, shipments, pricing and margins generally as Cliffs’ competitors face similar challenges and compete vigorously in other markets that Cliffs serves. These adverse impacts would negatively affect Cliffs’ revenues, financial results and cash flows.

Moreover, despite Cliffs’ position as the largest flat-rolled steel producer in North America, competition for automotive business has intensified in recent years, as steel producers and companies producing alternative materials have focused their efforts on capturing and/or expanding their market share of automotive business because of less favorable conditions in other markets for steel and other metals, including commodity products. As a result, the potential exists that Cliffs may lose market share to existing or new entrants or that automotive manufacturers will take advantage of the intense competition among potential suppliers during periodic contract renewal negotiations to pressure Cliffs’ pricing and margins in order to maintain or expand market share with them, which could negatively affect Cliffs’ revenue, financial results and cash flows.

These events could have a material adverse effect on Cliffs and, in certain circumstances, could potentially adversely affect Northshore, which in turn, could have a material adverse effect on Cliffs’ ability to pay future royalties owed to the Trust.

7

Severe financial hardship or bankruptcy of one or more of Cliffs’ major customers or key vendors could adversely affect Cliffs’ business operations and financial performance, which in turn could adversely affect Cliffs’ ability to pay royalties owed to the Trust.

Sales and operations for a majority of Cliffs’ customers are sensitive to general economic conditions in the North American automotive, housing, construction, appliance, energy, defense and other industries. Some of Cliffs’ customers are highly leveraged. If there is a significant weakening of current economic conditions, whether because of operational, cyclical, supply chain or other issues, including inflationary pressures, higher interest rates or an infectious disease outbreak, it could cause customers to reduce, delay or cancel their orders, impact significantly the creditworthiness of Cliffs’ customers and lead to other financial difficulties or even bankruptcy filings by Cliffs’ customers. Failure to receive payment for products that Cliffs has delivered could adversely affect Cliffs’ results of operations, financial condition and liquidity. The concentration of customers in a specific industry, such as the automotive industry, may increase Cliffs’ risk because of the likelihood that circumstances may affect multiple customers at the same time. Such events could cause Cliffs to experience lost sales or losses associated with the potential inability to collect all outstanding accounts receivable as well as reduced liquidity. Similarly, if Cliffs’ key vendors face financial hardship or need to operate in bankruptcy, as Cliffs experienced with one of its major steel mill slag services providers during 2022-2023, such vendors could suffer operational disruption or even face liquidation, which could result in such vendor defaulting on its obligations to Cliffs or Cliffs’ inability to secure replacement materials or services on a timely basis, or at all, or cause Cliffs to incur increased costs to do so. Such events could adversely impact Cliffs’ continuity of operations, financial results and cash flows, which in turn could adversely affect Cliffs’ ability to pay royalties owed to the Trust.

U.S. government actions regarding its trade policies may have a material adverse impact on Cliffs’ business, which could adversely affect Cliffs’ ability to generate revenue, which in turn could adversely affect royalties payable to the Trust.

In recent years, the U.S. government has altered its approach to international trade policy, both generally and with respect to matters directly and indirectly affecting the steel industry, including by undertaking certain unilateral actions affecting trade, renegotiating existing bilateral or multilateral trade agreements, and entering into new agreements or treaties with foreign countries. For example, in March 2018, the U.S. government issued a proclamation pursuant to Section 232 imposing a 25% tariff on imported steel. These Section 232 tariffs were imposed on national security grounds and addressed imported steel that was being unfairly traded by certain foreign competitors at artificially low prices. In retaliation against the Section 232 tariffs, the European Union subsequently imposed its own tariffs against certain steel products and other goods imported from the U.S. Following the November 2020 U.S. presidential election, negotiations between the U.S. government and other governments have resulted in revisions to these measures. For example, the U.S. government agreed to modified tariff rate quota systems with each of the European Union, Japan and the United Kingdom that allow more imports from those trading partners to enter the U.S. market free of Section 232 tariffs. The U.S. government may also negotiate reductions or eliminations of Section 232 duties with other trading partners. If the Section 232 measures are further removed or substantially lessened, whether through legal challenge, legislation, executive action or otherwise, imports of foreign steel would likely increase and steel prices in the U.S. would likely fall, which could materially adversely affect Cliffs’ revenues, financial results and cash flows.

In addition, during 2020, the United States-Mexico-Canada Agreement (“USMCA”) was implemented among the U.S., Mexico and Canada in place of the North American Free Trade Agreement. Because all of Cliffs’ steel manufacturing facilities are located in North America and one of Cliffs’ principal markets is automotive manufacturing in North America, Cliffs believes that the USMCA has the potential to positively impact its business by incentivizing automakers and other manufacturers to increase manufacturing production in North America and to use North American steel. However, it is difficult to predict the short- and long-term implications of changes in trade policy and, therefore, whether the USMCA or other new or

8

renegotiated trade agreements, treaties, laws, regulations or policies that may be implemented by the U.S. government, or otherwise, will have a beneficial or detrimental impact on Cliffs’ business and its customers’ and suppliers’ businesses. Adverse effects could occur directly from a disruption to trade and commercial transactions and/or indirectly by adversely affecting the U.S. economy or certain sectors of the economy, impacting demand for Cliffs’ customers’ products and, in turn, negatively affecting demand for Cliffs’ products. According to Cliffs’ disclosures, important links of the supply chain for some of Cliffs’ key customers, including automotive manufacturers, could be negatively impacted by the USMCA or other new or renegotiated trade agreements, treaties, laws, regulations or policies.

While Cliffs may currently benefit from certain antidumping and countervailing duty orders, any such relief is subject to periodic reviews and challenges, which can result in revocation or modification of the orders or reduction of the duties. During 2022 and 2023, the U.S. International Trade Commission reviewed and continued antidumping and countervailing duty orders covering imports from several major trading partners of some of its key products, including corrosion-resistant steel, cold-rolled steel, hot-rolled steel and cut-to-length plate. However, previously granted petitions for trade relief may not be successful or fully effective at preventing harm from dumped and subsidized imports. Any of these actions and their direct and indirect impacts could materially adversely affect Cliffs’ revenues, financial results and cash flows.

As a result, certain events could have a material adverse effect on Cliffs and, in certain circumstances, could potentially adversely affect Northshore, which in turn, could have a material adverse effect on Cliffs’ and Northshore’s ability to pay future royalties owed to the Trust, and the Trustees are not able to predict the impact that changing U.S. trade policy, or its results and/or consequences, will have on future royalties payable to the Trust.

Global steelmaking overcapacity, steel imports and oversupply of iron ore could lead to lower or more volatile global steel and iron ore prices, directly or indirectly impacting Cliffs’ profitability, which in turn could adversely affect royalties payable to the Trust.

Significant existing global steel capacity and new or expanded production capacity in recent years could potentially cause capacity to exceed demand globally. Although certain of Cliffs’ U.S. competitors have shut down production capacity, certain of Cliffs’ competitors have announced and are moving ahead with plans to develop new steelmaking capacity in the near term. In addition, certain foreign competitors, which may have cost advantages due to being owned, controlled or subsidized by foreign governments, have substantially increased their steel production capacity in the last few years and in some instances appear to have targeted the U.S. market for imports. The risk of even greater levels of imports may continue, depending upon foreign market and economic conditions, changes in trade agreements and treaties, laws, regulations or government policies affecting trade, the ability of foreign producers to circumvent U.S. trade sanctions and policy (including in the markets for tin mill products and electrical steels), the value of the U.S. dollar relative to other currencies and other variables beyond Cliffs’ control. In addition, higher sustained market prices of steel and iron ore products could cause new producers to enter the market or existing producers to further expand productive capacity, which could in turn lead to lower steel prices and increasing prices of steel making inputs, such as scrap metal. Excess steel and iron ore supply combined with reduced global steel demand and increased imports, also could lead to lower steel and iron ore prices. Downward pressure on steel and/or iron ore prices could have an adverse effect on Cliffs’ results of operations, financial condition and profitability, which in turn could adversely affect Cliffs’ ability to pay royalties owed to the Trust.

9

Due to the lack of industry and geographic diversification, adverse developments in the iron ore mining industry could adversely impact the Trust’s financial condition and reduce its ability to make distributions to the Trust’s Unitholders.

Substantially all of the revenue, operating profits and assets of the Trust relate to one business segment—iron ore mining. In addition, the principal assets of the Trust consist of two different interests in certain properties in the Mesabi Iron Range located in northern Minnesota. This concentration could disproportionally expose the Trust’s interests to operational and regulatory risks in that area. Due to the lack of diversification in industry type and location of the Trust’s interests, adverse developments in the iron ore markets or at the location of the Trust’s real estate interests could have a significantly greater impact on the Trust’s financial condition, results of operations and royalty revenues than if the Trust’s interests were more diversified.

Royalties received by the Trust, and distributions paid to Unitholders, in any particular quarter or year are highly variable and are not necessarily indicative of royalties or distributions that will be paid in any subsequent quarter or in any full year. Idling of Northshore plant and mining operations exacerbate this volatility.

Although Cliffs’ obligation to pay royalties has never been dependent on Cliffs’ revenue receipts, and under the Royalty Agreement Mesabi Trust does not bear collection risk from Cliff's’ customers, royalties received by the Trust typically do fluctuate significantly from quarter to quarter and year to year based upon market prices for iron ore products, the level of orders for iron ore products from Cliffs’ customers, the sales and marketing efforts of Cliffs, the consumption of inventory by Cliffs’ customers, and production decisions made by Northshore, including, as discussed above, decisions to reduce or idle Northshore plant and mining operations. For example, Cliffs elected to idle Northshore operations from May 2022 until April 2023, which resulted in no royalty payments to the Trust for a period of time. Moreover, because some of the royalties paid to the Trust in any particular quarter (other than the minimum advance royalty) include payments made with respect to pellets shipped and sold at estimated prices that, under some Cliffs Customer Contracts, may be subject to future interim and final multi-year adjustments in accordance with such supply agreements, a downward trend in demand and market prices for iron and steel products could result in negative adjustments to royalties in future quarters, some of which may be significant. These negative price adjustments could have a material adverse effect on the Trust’s royalty income, which in time could result in lower quarterly distributions paid by the Trust to Unitholders, and possibly reduce or even eliminate funds available for distribution in any quarter and in some quarters may completely offset royalties otherwise payable to the Trust.

Due to the factors described above, royalties paid to the Trust in future quarters for iron ore products shipped earlier during a year could materially increase or decrease, and in case of decrease, such decrease could result in little or no cash being available for distribution to Unitholders. As a result, distributions that may be declared and paid to Unitholders, in any particular quarter, are not necessarily indicative of royalties that will be received, or distributions that will be paid, in any subsequent quarter or in any full year. Based on the foregoing and the current uncertainty in the economic environment, the Trust cannot ensure that there will be adequate cash available to make a distribution to Unitholders in any particular quarter.

Cliffs’ Annual Report has disclosed certain financial risks, including risks related to Cliffs’ existing and future level of indebtedness, risks related to potential limitations on its ability to invest in the ongoing needs of its business, risks concerning its ability to generate sufficient cash flow to service all of its debt, and risks related to adverse changes in credit ratings, which may adversely affect its cost of financing.

Cliffs’ Annual Report has disclosed that (i) a portion of its cash flow from operations is used to service debt, reducing the availability of its cash to fund capital expenditures, acquisitions or other strategic

10

development initiatives and other general corporate purposes or to return capital to shareholders, including via share repurchases, (ii) if it is unable to service its debt service obligations, it may face substantial liquidity problems and may be forced to reduce or delay investments, capital expenditures and share repurchases, or to sell assets, seek additional capital, including additional secured or unsecured debt, or restructure or refinance its debt, and (iii) the cost of financing or refinancing, access to the capital markets, and the terms under which it purchases goods and services if credit rating agencies could downgrade Cliffs’ ratings, whether due to factors specific to its business or debt profile, a prolonged cyclical downturn in the steel, scrap metal and mining industry or macroeconomic trends (such as global or regional recessions), increases in pension and OPEB obligations, adverse impacts of inflation and higher interest rates, or trends in credit and capital markets more generally.

Cliffs’ Annual Report also disclosed that if it is unable to service its debt obligations, it could face substantial liquidity problems and may be forced to reduce or delay investments, capital expenditures and share repurchases, or to sell assets, seek additional capital, including additional secured or unsecured debt, or restructure or finance its debt, and may be unable to continue as a going concern.

These potential circumstances, if they become real developments, could have a material adverse effect on Cliffs and Northshore, which in turn, could have a material adverse effect on royalties paid to the Trust in the future.

Equipment failures and other unexpected events at Northshore may lead to production curtailments, idling or shutdown.

Interruptions in production capabilities at the mine operated by Northshore may have an adverse impact on the royalties payable to the Trust. In addition to planned production shutdowns, idling or curtailments and equipment failures, the Northshore facilities are also subject to the risk of loss due to unanticipated events such as fires, explosions or extreme weather conditions due to climate change or otherwise and natural and human-caused disasters, terrorist events, lack of energy or other supplies, and infectious disease outbreaks. For example, the temporary production shutdowns in the automotive industry during 2020 as a result of the COVID-19 pandemic and associated reduction in demand for Cliffs’ products led to Cliffs’ decision to temporarily idle certain steelmaking facilities and iron ore mines. The manufacturing processes that take place in Northshore’s mining operations, as well as in Northshore’s crushing, concentrating and pelletizing facilities, depend on critical pieces of equipment, such as drilling and blasting equipment, crushers, grinding mills, pebble mills, thickeners, separators, filters, mixers, furnaces, kilns and rolling equipment, as well as electrical equipment, such as transformers. It is possible that this equipment may, on occasion, be out of service because of unanticipated failures or unforeseeable acts of vandalism or terrorism. In addition, because the Northshore processing facilities have been in operation for several decades, some of the equipment may be aged. A shutdown or reduction in capacity may come with little or no advance warning. The remediation of any interruption in production capability at Northshore could require Cliffs to make large capital expenditures which may take place over an extended period of time. According to Cliffs’ Annual Report, if Cliffs’ cash flows and capital resources are insufficient to fund its debt service obligations, it may be forced to reduce or delay investments and capital expenditures. Any additional idling, shutdown, reduction in operations, or production curtailment at Northshore would likely adversely affect the royalties payable to the Trust.

The mining operations of Northshore are subject to extensive governmental regulations and Northshore is subject to risks related to its compliance with federal and state environmental regulations.

Northshore, as the operator of the mine on Mesabi Trust Lands, is subject to various international, foreign, federal, state and local laws and regulations relating to protection of the environment and human health and safety, including those relating to air quality, water quality and conservation, plant, wetlands, natural resources and wildlife protection (including endangered and threatened species), reclamation,

11

remediation and restoration of properties and related surety bonds or other financial assurances, land use, the discharge of materials into the environment, and the effects that industrial operations and mining has on groundwater quality and availability, the management of electrical equipment containing polychlorinated biphenyls, and other related matters. Northshore is required to maintain numerous permits and approvals issued by federal and state regulatory agencies and its mining operations are subject to inspection and regulation by the Mine Safety and Health Administration of the United States Department of Labor (“MSHA”) under the provisions of the Mine Safety and Health Act of 1977. The Occupational Safety and Health Administration (“OSHA”) has jurisdiction over safety and health standards not covered by MSHA and the Minnesota Pollution Control Agency (“MPCA”) regulates various aspects of Northshore’s operations. Northshore may from time to time be involved in disputes or litigation with the regulatory agencies over certain aspects of its operations and the Trustees cannot predict the potential impact of these proceedings. Moreover, Northshore is solely responsible for its compliance with all laws, regulations or permits applicable to Northshore’s operations and Northshore may at times fail to operate in compliance with such laws, regulations and permits. The Trust has limited ability to control or determine whether Northshore has been or will in the future operate in compliance with such laws and regulations. If Northshore fails to comply with these laws, regulations or permits, it could be subject to fines or other sanctions, any of which could have an adverse effect on its operations and its ability to ship iron ore products from Silver Bay, Minnesota, which could, in turn, have a material adverse effect on the royalties paid to the Trust.

TMDL (a regulatory term describing a value of the maximum amount of a pollutant that a body of water can receive while still meeting water quality standards under the Clean Water Act) regulations are contained in the Clean Water Act and, as a part of Minnesota’s Mercury TMDL Implementation Plan, in cooperation with the MPCA, the taconite industry developed a Taconite Mercury Reduction Strategy and signed a voluntary agreement to effectuate its terms. The strategy includes a 72% target reduction of mercury air emissions from Minnesota pellet plants collectively by 2025. For Cliffs, the requirements in the voluntary agreement do not apply to Northshore. Late in 2013, however, Minnesota published a draft mercury control rule that would require annual mercury emissions reporting and could require installation of mercury emission control equipment on all Cliffs’ Minnesota facilities including those of Northshore. On September 22, 2014, Minnesota promulgated the Mercury Air Emissions Reporting and Reduction Rule mandating mercury air emissions reporting and reduction. The adopted rule expanded applicability to all of Cliffs’ Minnesota operations and required (i) a 70% reduction of mercury emissions from Northshore’s industrial boilers by January 1, 2018, and (ii) by the end of 2018, the submission of a plan to reduce mercury emissions by 72% from all of Cliffs’ Minnesota taconite furnaces, with such plan implementation requirements to become effective on January 1, 2025. Cliffs expressed its concerns about the technical and economic feasibility to reduce taconite mercury emissions by 72% and conducted detailed engineering analyses to determine the impact of the regulations on each unique iron ore indurating furnace affected by the Mercury Air Emissions Reporting and Reduction Rule. Cliffs’ Annual Report states that one of the main tenets agreed upon for evaluating potential mercury reduction technologies during TMDL implementation and the 2014 rule development proceedings was that the selected technology must meet the following “Adaptive Management Criteria”: the technology (i) must be technically feasible; (ii) must be economically feasible; (iii) must not impact pellet quality; and (iv) must not cause excessive corrosion in the indurating furnaces or air pollution control equipment. According to Cliffs’ Annual Report, there is currently no proven technology to cost-effectively reduce mercury emissions from taconite furnaces to the target level of 72% that would meet all four Adaptive Management Criteria. Cliffs submitted its mercury reduction plans for its Minnesota facilities to the MPCA in December 2018. The plans determined that there are currently no proven technologies to cost effectively reduce mercury emissions from taconite furnaces to achieve the targeted 72% reduction rate, while satisfying all Adaptive Management Criteria. According to Cliffs, this determination was based on detailed engineering analysis and research testing. In January 2023, the MPCA responded that certain technologies may be appropriate, and the MPCA requested submission of revised Mercury Reduction Plans from the facilities. Potential impacts to Cliffs are not estimable at this time because the revised Mercury Reduction Plans remain under development.

12

The Trustees are unable to predict what impact, if any, the Mercury Air Emissions Reporting and Reduction Rule will have on production and shipments of iron ore products from Northshore or future royalties payable to the Trust.

The Trust does not control the portion of Northshore’s shipments that will come from iron ore mined from Mesabi Trust Lands.

The Trustees do not exert any influence over mining operational decisions at Northshore and Northshore alone determines whether to mine from Mesabi Trust Lands or state-owned lands, based on its current production estimates and engineering plan. Northshore’s mining operations include Mesabi Trust Lands and mineral-producing land owned by the State of Minnesota and others. Iron ore mined by Northshore from lands other than Mesabi Trust Lands is processed, along with iron ore mined from Mesabi Trust Lands, in Northshore-owned crushing, concentrating and pelletizing facilities and is separately accounted for on a periodic basis. Northshore also has the ability to process and ship iron ore products from lands other than Mesabi Trust Lands. In certain circumstances, the Trust may be entitled to royalties on those other shipments, but not in all cases. In general, the Trust will receive higher royalties (assuming all other factors are equal) if a higher percentage of shipments is from Mesabi Trust Lands. The percentages of shipments from Mesabi Trust Lands were 90.0%, 99.7% and 91.3% in calendar years 2023, 2022 and 2021, respectively. If Northshore decides to materially reduce the percentage of iron ore mined, or pellets shipped, from Mesabi Trust Lands, the income of the Trust could be materially adversely affected.

The Trust relies on Cliffs’ estimates of recoverable reserves, and if those estimates are inaccurate, the total potential future royalty stream to the Trust and distributions payable to Unitholders may be materially adversely affected.

The Trustees do not participate in preparing the recoverable iron ore reserve estimates reported by Cliffs. According to Cliffs’ Annual Report, Cliffs regularly evaluates its iron ore reserves based on revenues and costs and updates them as required in accordance with SEC regulations. In 2018, the Trustees engaged an independent firm of geological experts to evaluate the process Cliffs uses to estimate the recoverable iron ore reserves at the Peter Mitchell Mine. Additionally, according to Cliffs’ Annual Report, Cliffs updates its iron ore reserve estimates to comply with Final Rule 13-10570, Modernization of Property Disclosures for Mining Registrants. Still, there are numerous uncertainties inherent in estimating quantities of reserves of mineral producing lands and such estimates necessarily depend upon a number of variable factors and assumptions, such as production capacity, effects of regulations by governmental agencies, future prices for iron ore, future industry conditions and operating costs, severance and excise taxes, development costs and costs of extraction and reclamation costs. All of these factors are outside of the control and influence of the Trustees. Actual reserves will likely vary from estimates, and if such variances are negative and material, the expected royalties payable to the Trust could be materially adversely affected and the value of the Trust’s Units could decline.

Cliffs has disclosed certain operational risks, including risks that could arise related to substantial costs from idled production capacity, announced and potential mine closures and risks related to its ability to transport its products to customers at competitive rates and in a timely manner.

According to Cliffs’ Annual Report, Cliffs indicated that its decisions concerning which facilities to operate and at what production levels are made based in part upon its customers’ orders for products, as well as the quality, performance capabilities and production cost of its operations. During depressed market conditions, Cliffs may concentrate production at certain facilities and not operate others in response to customer demand or other reasons, and as a result Cliffs would incur idle costs that could offset its anticipated savings from not operating the idled facility. For example, focusing on the magnitude and structure of the Mesabi royalty, Cliffs temporary idled Northshore operations from May 2022 until April 2023. As a result of Cliffs’ idling of the Northshore operations, Cliffs made no quarterly royalty payments to the Trust for

13

October 2022, January 2023 and April 2023, and Cliffs incurred fixed costs during the idle period. When Cliffs restarts idled facilities, it incurs certain costs to replenish inventories, prepare the previously idled facilities for operation, perform the required repair and maintenance activities, and prepare employees to return to work safely and resume production responsibilities. The amount of any such costs can be material, depending on a variety of factors, such as the period of idle time, necessary repairs and available employees, and is difficult to project.

Cliffs also disclosed that in its iron ore operations, disruption of the rail, trucking, lake or other waterway transportation services due to weather-related problems, climate change, strikes, lock-outs, driver shortages and other disruptions in the trucking industry, train crew shortages or other rail network constraints, infectious disease outbreaks or other events and lack of alternative transportation sources could impair Cliffs’ ability to move products internally around its facilities and to supply products to its customers at competitive rates or in a timely manner, and thus, could adversely affect its operations, revenues, margins and profitability.

These events could have a material adverse effect on Cliffs and potentially Northshore, which in turn, could have a material adverse effect on royalties paid to the Trust in the future.

Certain risk factors affecting Cliffs’ North American iron ore business generally, and Northshore operations in particular, could have a material adverse effect on the royalties payable to the Trust.

Because substantially all of the Trust’s revenue is derived from iron ore products shipped by Northshore from Silver Bay, Northshore’s iron ore pellet processing and shipping activities directly impact the Trust’s revenues in each quarter and each year. According to Cliffs’ Annual Report, a number of risk factors affect Cliffs’ operations and could impact Northshore’s production and shipment volume. Cliffs’ Annual Report identified the following seven categories of risk to which Cliffs is subject: (i) economic and market, (ii) regulatory, (iii) financial, (iv) operational, (v) sustainability and development, and (vi) human capital. These risk factors include, among others, the volatility of commodity prices, concentration of business in the automotive market, global steelmaking overcapacity, severe financial hardship or bankruptcy of major customers or key vendors, U.S. government trade policies, extensive governmental regulations relating to the environment and human health and the costs and risks related thereto, use of hazardous materials, inability to obtain, maintain or renew operational permits and licenses, financial risks associated with existing and future indebtedness, dependence on certain raw materials and energy sources, the cost or time to implement strategic capital projects, natural or human-caused disasters, weather conditions, disruptions or failures of its IT systems, costs associated with the idling or closures of an operating facility or mine, lack of appropriate insurance coverage, pressures to reduce carbon footprint, risks associated with maintaining social license, assumptions regarding recoverable mineral reserves, defects in title to any leasehold interests, dependence on senior management team and key employees, labor relations, pension costs and labor shortages. Specifically, if any portion of Northshore’s pelletizing lines becomes idle for any reason, production, shipments and, consequently, the royalties payable to the Trust could be materially adversely affected.

Furthermore, other events such as terrorist acts, conflicts, wars and geopolitical uncertainties, whether or not occurring in or involving, directly or indirectly, the United States, may cause serious harm to Cliffs’ and/or Northshore’s business, operations and revenue. The potential for the occurrence of any of these types of events has created global and domestic economic and political uncertainties. As disclosed by Cliffs, if any of these types of events were to occur, the results would be unpredictable, but may include decreases in demand for iron ore, difficulties related to shipping of iron ore products to Cliffs’ customers, and delays and inefficiencies in Cliffs’ supply chain. The Trust is uninsured, and cannot obtain insurance, for losses and interruptions caused by any of these types of events.

14

We are dependent upon third-party information technology systems, which are subject to cyber threats, disruption, damage and failure.

We are dependent upon third-party information systems and other technologies, including those related to our financial and operational management and those related to Cliffs’ and Northshore’s financial and operational management. Network and information systems-related events, such as computer hackings, cyber-attacks, ransomware, computer viruses, worms or other destructive or disruptive software, process breakdowns, denial of service attacks, malicious social engineering or other malicious activities, or any combination of the foregoing, or power outages, natural disasters, terrorist attacks or other similar events, could result in damage to our information and data that is stored or transmitted by our third-party vendors. Any security breaches, such as computer viruses and more sophisticated and targeted cyber-related attacks, as well as misappropriation, misuse, leakage, falsification or accidental release or loss of information maintained in these information technology systems could result in significant losses and damage to our reputation, and require us to expend significant capital and other resources to remedy any such security breach. There can be no assurance that these events and security breaches will not occur in the future or not ultimately have an adverse effect on the royalties payable to the Trust.

Risks Related to Human Capital

The Trustees are not subject to annual election and, as a result, the ability of the holders of Trust Certificates to influence the policies of the Trust may be limited.

Directors of a corporation are generally subject to election at each annual meeting of shareholders or, in the case of staggered boards, at regular intervals. However, under the Agreement of Trust, the Trust is not required to hold annual meetings of holders of Trust Certificates to elect Trustees and Trustees generally hold office until their death, resignation or disqualification. As a result, the ability of holders of Trust Certificates to effect changes in the composition of those serving as Trustees and the policies of the Trust is significantly more limited than that of the shareholders of a corporation.

Royalties payable to the Trust could be materially adversely affected by the failure of the Trust’s independent consultants to competently perform.

As permitted by the terms of the Agreement of Trust, the Trustees are authorized to, and in fact do, rely upon certain independent consultants to assist the Trustees in carrying out and fulfilling their obligations as Trustees. Independent consultants perform a variety of services for the Trust, render advice and produce reports with respect to monthly production and shipments, which include figures on crude iron ore production, iron ore pellet production, iron ore pellet shipments, and discussions concerning the condition and accuracy of the scales used to weigh iron ore pellets produced at Northshore’s facilities. The Trustees have also retained an accounting firm to provide non-audit services, including preparing financial statements, reviewing financial data related to shipping and sales reports provided by Northshore and reviewing the schedule of leasehold and fee royalties payable to the Trust. The Trustees believe that the independent consultants engaged by the Trust are qualified to perform the services and functions assigned to them. Nevertheless, any negligence or the failure of any such independent consultants to competently perform could materially adversely affect the royalties to be received by the Trust.

General Risk Factors

The Trust is subject to disputes from time to time that could result in litigation, arbitration or other administrative proceedings that could adversely affect the Trust’s operating results and financial condition and the market value of Mesabi Trust Units.

The Trust may become involved in litigation, arbitration or other administrative proceedings from time to time. These proceedings can be costly, and the results and other consequences of such proceedings

15

are often difficult to predict. The Trust may not have adequate insurance coverage or contractual protection to cover costs and liability in the event we are sued, and to the extent we resort to litigation, arbitration or other administrative proceedings to enforce our rights, we may incur significant costs and ultimately be unsuccessful or unable to recover amounts we believe are owed to us or unable to resolve the matter on favorable terms.

More specifically on December 9, 2019, the Trust initiated arbitration with the American Arbitration Association (“AAA”) against Northshore, the lessee/operator of the leased lands, and its parent, Cliffs. The Trust asserted claims concerning the calculation of royalties related to the production, shipment and sale of iron ore, including DR-grade pellets. The arbitration was completed before a panel of three arbitrators in July 2021 under the commercial rules of the AAA. The Trust received the AAA final award on October 1, 2021, which awarded the Trust damages in the amount of $2,312,106 for the resolution of royalties on DR grade pellets in 2019 and 2020 and interest in the amount of $430,710, calculated through June 30, 2021, and continuing to accrue until paid. Pursuant to the award, Cliffs paid the damages award to the Trust on October 29, 2021. The Tribunal granted the Trust’s request for a declaration that “for purposes of calculating royalties on intercompany sales, Northshore shall reference all third-party pellet sales, regardless of grade, and select the highest price arm’s length pellet sale from the preceding four quarters.” The Tribunal denied the Trust’s request for declaratory relief regarding access to certain information.

On October 14, 2022, the Trust initiated arbitration against Northshore and its parent, Cliffs. The arbitration proceeding was commenced with the AAA. The Trust seeks an award of damages relating to the underpayment of royalties in 2020, 2021, and 2022 by virtue of the failure to use the highest price arm’s length iron ore pellet sale from the preceding four quarters in pricing internal production during the fourth quarter of 2020 through 2022. The Trust also seeks declaratory relief related to the Trust’s entitlement to certain documentation and to the time the Operator’s royalty obligation accrues. The AAA evidentiary hearing took place in March 2024. Post-hearing briefs will be exchanged in May 2024, and post-hearing oral argument, if any, will take place in June 2024.

Any arbitration, legal or administrative proceedings to which the Mesabi Trust is subject could require the significant involvement of Trustees and the professional advisors and consultants to the Trust, and may divert attention from the Trustees’ other roles and responsibilities. In addition, it is difficult to foresee the results of legal actions, arbitration matters and other proceedings currently involving the Mesabi Trust or of those which may arise in the future, and an adverse result in these matters could have a material adverse effect on the market value of Mesabi Trust units and on Mesabi Trust’s asset value, royalty income, results of operations and financial condition.

We are subject to the continued listing criteria of the NYSE, and our failure to satisfy these criteria may result in delisting of our Units.

Our Units are currently listed for trading on the NYSE. In order to maintain the listing, we must maintain certain objective standards such as Unit prices and a minimum number of public Unitholders. In addition to objective standards, the NYSE may delist the securities of any issuer using subjective standards such as, if in the NYSE’s opinion, the issuer’s financial condition and/or operating results appear unsatisfactory or if any event occurs or any condition exists which makes continued listing on the NYSE inadvisable.

If the NYSE delists our Units, Unitholders may face material adverse consequences, including, but not limited to, a lack of trading market for our Units and reduced liquidity.

16

The Trust faces risks from cybersecurity threats that could have a material adverse effect on its financial condition, financial record keeping, investment management, reporting, results of operations, cash flows or reputation.

The Trust is exposed to potential harm from cybersecurity events that may affect the operations of the Corporate Trustee and other third parties such as Cliffs and Northshore, and the Trust’s consultants, experts and agents (“Trust Third Parties”) who provide the Trust and Trustees with professional services including legal, accounting, on-site inspection and investment management. The Corporate Trustee or the Trust Third Parties maintain robust cybersecurity protocols. However, if the measures taken by the Corporate Trustee and the Trust Third Parties to protect against cybersecurity disruptions, whether from internal or external actors, prove to be insufficient or if confidential or proprietary data of the Trust is otherwise not protected, the Trust could be adversely affected. A breach of cybersecurity protections or a cyber-attack on the Corporate Trustee or the Trust Third Parties could potentially jeopardize the confidential, proprietary, and other information of the Trust that is processed, stored in, and transmitted through the computer systems and networks of these parties. Cybersecurity disruptions could cause physical harm to people or the environment, damage or destroy assets; compromise business systems; result in proprietary information being altered, lost, or stolen; result in the Trust’s or third-party information being compromised; or otherwise disrupt business operations of the Corporate Trustee or the Trust Third Parties. The Trust could incur significant costs to remedy the effects of a major cybersecurity disruption in addition to costs in connection with any resulting regulatory actions, litigation or reputational harm. Although the Corporate Trustee and the Trust Third Parties take steps to prevent and detect such attacks, it is possible that a cyber incident will not be discovered for some time after it occurs, which could increase exposure to these consequences.

OVERVIEW OF TRUST’S ROYALTY STRUCTURE

Leasehold royalty income constitutes the principal source of the Trust’s revenue. The income of the Trust is highly dependent upon the activities and operations of Northshore. Royalty rates and the resulting royalty payments received by the Trust are determined in accordance with the terms of the Trust’s leases and assignments of leases.

Three types of royalties, as well as royalty bonuses, comprise the Trust’s leasehold royalty income:

| ● | Base overriding royalties. Base overriding royalties have historically constituted the majority of the Trust’s royalty income. Base overriding royalties are determined by both the volume and selling price of iron ore products shipped. Northshore is obligated to pay the Trust base overriding royalties in varying amounts, based on the volume of iron ore products shipped. Base overriding royalties are calculated as a percentage of the gross proceeds of iron ore products produced at Mesabi Trust Lands (and to a limited extent other lands) and shipped from Silver Bay, Minnesota. The percentage ranges from 2-1/2% of the gross proceeds for the first one million tons of iron ore products shipped annually to 6% of the gross proceeds for all iron ore products in excess of four million tons so shipped annually. Base overriding royalties are subject to interim and final price adjustments under the Cliffs Customer Contracts and, as described elsewhere in this Annual Report, such adjustments may be positive or negative. |

| ● | Royalty bonuses. The Trust earns royalty bonuses when iron ore products shipped from Silver Bay are sold at prices above a threshold price per ton. The royalty bonus is based on a percentage of the gross proceeds of product shipped from Silver Bay. The threshold price is adjusted (but not below $30.00 per ton) on an annual basis for inflation and deflation (the “Adjusted Threshold Price”). The Adjusted Threshold Price was $62.03 per ton for calendar year 2022 and $66.00 per ton for calendar year 2023, and is $67.75 per ton for calendar year 2024. The royalty bonus percentage ranges from 1/2 of 1% of the gross proceeds (on all tonnage shipped for sale at prices |

17

| between the Adjusted Threshold Price and $2.00 above the Adjusted Threshold Price) to 3% of the gross proceeds (on all tonnage shipped for sale at prices $10.00 or more above the Adjusted Threshold Price). Royalty bonuses are subject to price adjustments under the Cliffs Customer Contracts (and, as described elsewhere in this Annual Report); such adjustments may be positive or negative. See the section entitled “Comparison of Financial Results for Fiscal Years ended January 31, 2024 and January 31, 2023” in this Annual Report for more information. |

| ● | Fee royalties. Fee royalties have historically constituted a smaller component of the Trust’s total royalty income. Fee royalties are payable to the Mesabi Land Trust, a Minnesota land trust, which holds a 20% interest as fee owner in the Amended Assignment of Peters Lease. Mesabi Trust holds the entire beneficial interest in the Mesabi Land Trust for which U.S. Bank N.A. acts as the corporate trustee. Mesabi Trust receives the net income of the Mesabi Land Trust, which is generated from royalties on the amount of crude ore mined after the payment of expenses to U.S. Bank N.A. for its services as the corporate trustee. Crude ore is the source of iron oxides used to make iron ore pellets and other products. The fee royalty on crude ore is based on an agreed price per ton, subject to certain indexing. |

| ● | Minimum advance royalties. Northshore’s obligation to pay base overriding royalties and royalty bonuses with respect to the sale of iron ore products generally accrues upon the shipment of those products from Silver Bay. However, regardless of whether any shipment has occurred, Northshore is obligated to pay to Mesabi Trust a minimum advance royalty. Each year, the amount of the minimum advance royalty is adjusted (but not below $500,000 per annum) for inflation and deflation. The minimum advance royalty was $1,034,237 for calendar year 2022 and $1,100,498 for calendar year 2023, and is $1,129,615 for calendar year 2024. Until overriding royalties (and royalty bonuses, if any) for a particular year equal or exceed the minimum advance royalty for the year, Northshore must make quarterly payments of up to 25% of the minimum advance royalty for the year. Because minimum advance royalties are essentially prepayments of base overriding royalties and royalty bonuses earned each year, any minimum advance royalties paid in a fiscal quarter are recouped by credits against base overriding royalties and royalty bonuses earned in later fiscal quarters during the year. |

The current royalty rate schedule became effective on August 17, 1989 pursuant to the Amended Assignment of Peters Lease, which the Trust entered into with Cyprus Northshore Mining Corporation (“Cyprus NMC”). Pursuant to the Amended Assignment of Peters Lease, overriding royalties are determined by both the volume and selling price of iron ore products shipped. In 1994, Cyprus NMC was sold by its parent corporation to Cliffs and renamed Northshore Mining Company. Cliffs now operates Northshore as a wholly-owned subsidiary.