Table of Contents

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

| þ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES |

EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2011

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission File Number 1-1023

(Exact name of registrant as specified in its charter)

| New York | 13-1026995 | |

| (State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification No.) |

| 1221 Avenue of the Americas, New York, New York | 10020 | |

| (Address of principal executive offices) |

(Zip Code) |

Registrant’s telephone number, including area code: 212-512-2000

| Title of each class | Name of exchange on which registered | |

| Common Stock — $1 par value |

New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the Registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

YES þ NO ¨

Indicate by check mark if the Registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

YES ¨ NO þ

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15 (d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

YES þ NO ¨

Indicate by check mark whether the Registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Date File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the Registrant was required to submit and post such files).

YES þ NO ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of Registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. þ

Indicate by check mark whether the Registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “small reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

| þ Large accelerated filer | ¨ Accelerated filer | ¨ Non-accelerated filer | ¨ Smaller reporting company | |||

| . | (Do not check if a smaller reporting company) | |||||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

YES ¨ NO þ

The aggregate market value of voting stock held by non-affiliates of the Registrant as of the last business day of the second fiscal quarter ended June 30, 2011, was $12.6 billion, based on the closing price of the common stock as reported on the New York Stock Exchange of $41.91 per common share. For purposes of this calculation, it is assumed that directors, executive officers and beneficial owners of more than 10% of the registrant outstanding stock are affiliates. The number of shares of common stock of the Registrant outstanding as of January 20, 2012 was 278 million shares.

Part III incorporates information by reference from the definitive proxy statement for the 2012 annual meeting of shareholders.

Table of Contents

Table of Contents

FORWARD-LOOKING STATEMENTS

This report contains forward-looking statements, including without limitation statements relating to our businesses and our prospects, new products, sales, expenses, tax rates, cash flows, prepublication investments and operating and capital requirements that are made pursuant to the safe harbor provisions of the Private Securities Litigation Reform Act of 1995. These forward-looking statements are intended to provide management’s current expectations or plans for our future operating and financial performance and are based on assumptions management believes are reasonable at the time they are made.

Forward-looking statements can be identified by the use of words such as “believe,” “expect,” “plan,” “estimate,” “project,” “target,” “anticipate,” “intend,” “may,” “will,” “continue” and other words of similar meaning in connection with a discussion of future operating or financial performance. These statements are not guarantees of future performance and involve certain risks, uncertainties and assumptions that are difficult to predict; therefore, actual outcomes and results could differ materially from what is expected or forecasted. These risks and uncertainties include, among others:

| • | worldwide economic, financial, political and regulatory conditions; |

| • | currency and foreign exchange volatility; |

| • | the effect of competitive products and pricing; |

| • | the level of success of new product development and global expansion; |

| • | the level of future cash flows; |

| • | the levels of capital and prepublication investments; |

| • | income tax rates; |

| • | restructuring charges; |

| • | the health of debt and equity markets, including credit quality and spreads, the level of liquidity and future debt issuances; |

| • | the level of interest rates and the strength of the capital markets in the U.S. and abroad; |

| • | the demand and market for debt ratings, including collateralized debt obligations, residential and commercial mortgage and asset-backed securities and related asset classes; |

| • | the state of the credit markets and their impact on Standard & Poor’s Ratings and the economy in general; |

| • | the regulatory environment affecting Standard & Poor’s Ratings; |

| • | the level of merger and acquisition activity in the U.S. and abroad; |

| • | the level of funding in the education market; |

| • | School Education Group’s level of success in adoptions and open territories; |

| • | enrollment and demographic trends; |

| • | the strength of School Education Group’s testing market, Higher Education, Professional and International’s publishing markets and the impact of technology on them; |

| • | continued investment by the construction, automotive, computer and aviation industries; |

| • | the strength of the domestic and international advertising markets; |

| • | the strength and performance of the domestic and international automotive markets; |

| • | the volatility of the energy marketplace; |

| • | and the contract value of public works, manufacturing and single-family unit construction. |

In addition, there are certain risks and uncertainties relating to our previously announced Growth and Value Plan which contemplates a tax-free spin-off of our education business, including, but not limited to, the impact and possible disruption to our operations, the timing and certainty of completing the transaction, unanticipated developments that may delay or negatively impact the spin-off, and the ability of each business to operate as an independent entity upon completion of the spin-off. We caution readers not to place undue reliance on forward-looking statements.

2

Table of Contents

Overview

The McGraw-Hill Companies, Inc. (together with its consolidated subsidiaries, the “Company,” the “Registrant,” “we,” “us” or “our”) is a leading global information services provider serving the financial, education, commercial and commodities markets with the information they need to succeed in the “Knowledge Economy”. We serve our global customers through a broad range of products, services and distribution channels, including digital data and information, integrated digital platforms, online via Internet Websites as well as with printed books, magazines and newsletters, and conferences and trade shows.

On September 12, 2011, we announced that our Board of Directors unanimously approved a comprehensive Growth and Value Plan as the culmination of a portfolio review begun in late 2010. One of the primary features of this plan is the separation of the enterprise into two public companies: McGraw-Hill Financial, focused on content and analytics for financial markets, and McGraw-Hill Education, focused on education services and digital learning. On December 7, 2011, management provided an update on our Growth and Value Plan, discussing new actions that will facilitate the separation into two independent companies. Highlighted actions included:

| • | Reporting results for 2012 in five lines of business for the new McGraw-Hill Financial (S&P Ratings, S&P Capital IQ, S&P Indices, Commodities Markets, and Commercial Markets). |

| • | Reducing the McGraw-Hill Education workforce by 10% to create a flatter and more agile organization. |

| • | Freezing our U.S. defined-benefit pension plan as of April 1, 2012 and focusing our retirement program on market-competitive offerings. |

| • | Repurchasing additional shares through a $500 million accelerated share repurchase transaction. |

Further information regarding these actions can be found in our Notes to the Consolidated Financial Statements under Item 8, Consolidated Financial Statements and Supplementary Data, in this report.

We expect to complete the separation by the end of 2012 through a tax-free spin-off of the education business to the Company’s shareholders, subject to various conditions and regulatory approvals including final Board approval and a tax ruling from the Internal Revenue Service.

Furthermore, on October 3, 2011, we entered into a definitive agreement with The E.W. Scripps Company to sell the Broadcasting Group. The sale was completed on December 30, 2011, when we received net proceeds of approximately $216 million. The divestiture of our Broadcasting Group, previously included in our Commodities & Commercial segment (previously named the McGraw-Hill Information & Media segment), was carried out pursuant to our Growth and Value Plan discussed in further detail below. As a result of the sale, the results of operations for all periods presented have been reclassified to reflect the Broadcasting Group as a discontinued operation and the assets and liabilities of the business have been removed from the Consolidated Balance Sheet as of December 31, 2011 and reclassified as held for sale as of December 31, 2010.

Our Businesses

We have four operating segments which have historically been named: Standard & Poor’s (“S&P”), McGraw-Hill Financial, McGraw-Hill Information & Media and McGraw-Hill Education (“MHE”). As part of our Growth and Value Plan we have changed the names of our four operating segments to align with how we plan on referring to the businesses going forward. S&P has changed to S&P Ratings, McGraw-Hill Financial has been changed to S&P Capital IQ / S&P Indices, McGraw-Hill Information & Media has changed to Commodities & Commercial (“C&C”) and MHE has remained the same. Going forward, the new McGraw-Hill Financial will include S&P Ratings, S&P Capital IQ / S&P Indices and C&C.

S&P Ratings

S&P Ratings is the world's foremost provider of credit ratings. Credit ratings are one of several tools that investors can use when making decisions about purchasing bonds and other fixed income investments. They are opinions about credit risk and our ratings express our opinion about the ability and willingness of an issuer, such as a corporation or state or city government, to meet its financial obligations in full and on time. Our credit ratings can also speak to the credit quality of an individual debt issue, such as a corporate or municipal bond, and the relative likelihood that the issue may default.

With offices in over 20 countries around the world, S&P Ratings is an important part of the world's financial infrastructure and has played a leading role for over 150 years in providing investors with information and independent benchmarks for their investment and financial decisions and access to the financial markets. The key constituents S&P Ratings serves are investors; corporations; governments; municipalities; commercial and investment banks; insurance companies; asset managers; and other debt issuers.

3

Table of Contents

S&P Ratings differentiates its revenue between transactional and non-transactional. Transaction revenue primarily includes fees associated with:

| • | ratings related to new issuance of corporate and government debt instruments, and structured finance debt instruments; |

| • | bank loan ratings; and |

| • | corporate credit estimates, which are intended, based on an abbreviated analysis, to provide an indication of our opinion regarding creditworthiness of a company which does not currently have an S&P Ratings credit rating. |

Non-transaction revenue primarily includes fees for surveillance of a credit rating, annual fees for customer relationship-based pricing programs and fees for entity credit ratings.

Global markets have begun to recover and some are expanding rapidly, particularly those in emerging economies such as China and India, and raising capital is essential for growth. Though some uncertainties do remain, individuals, countries, and corporations will continue to require access to world capital markets, and investors will demand the diversification they offer. The primary risk point in the financial markets has moved to Europe. New financial legislation around the world will help improve investor confidence and market stability.

S&P Capital IQ / S&P Indices

S&P Capital IQ / S&P Indices is a leading global provider of digital and traditional research and analytical tools for investment advisors, wealth managers and institutional investors. It deploys the latest innovative technology driven strategies to deliver to customers an integrated portfolio of cross-asset analytics, desktop services, valuation and index benchmarks and investment recommendations in the rapidly growing financial information, data and analytics market. The key constituents S&P Capital IQ / S&P Indices serves are asset managers; investment banks; investors; brokers; financial advisors; investment sponsors; and companies’ back-office functions, including compliance, operations, risk, clearance, and settlement.

S&P Capital IQ / S&P Indices differentiates its revenue between subscription and non-subscription. Subscription revenue primarily includes:

| • | products in our Integrated Desktop Solutions Group, which include the following content: Capital IQ – a product suite that provides data and analytics for global financial professionals, Global Credit Portal – a web-based solution that provides real-time credit research, market information and risk analytics, and TheMarkets.com – a real-time research offering featuring content from the world’s leading brokers and independent research providers; |

| • | products in our Enterprise Solutions group, such as Global Data Solutions, which combines high-quality, multi-asset class and market data to help investors meet the new analytical, risk management, regulatory and front-to-back office operations requirements; |

| • | investment research products in our Research & Analytics group; |

| • | and other data subscriptions. |

Non-subscription revenue is generated primarily from products in our S&P Indices group, specifically through fees based on assets underlying exchange-traded funds; as well as certain advisory, pricing and analytical services in our Integrated Desktop Solutions group.

The increasing interconnections among the world economies and financial markets underpin the need for financial information. The retirement of the baby boomers in developed countries as well as the emergence of a vast new middle class in developing countries will also increase the need for financial services.

Commodities & Commercial

C&C consists of business-to-business companies specializing in the commercial and commodities markets, each an expert in its industry, that deliver their customers access to actionable pricing benchmarks, data and analytics. C&C includes such brands as Platts, J.D. Power and Associates, McGraw-Hill Construction and Aviation Week. The Broadcasting Group has historically been part of the C&C segment and was sold on December 30, 2011. In accordance with the presentation of the Broadcasting Group as discontinued operations, the results of operations for all periods presented have been reclassified to reflect this change.

Key markets served by C&C include professionals and corporate executives in automotive, aerospace and defense, construction, and energy; and global business and financial professionals, traders, investors, marketers, advertisers, and consumers worldwide.

The global business is driven by the need for information and transparency in a variety of industries, and to a lesser extent, by advertising revenue. C&C delivers critical information, largely through digital channels, for the energy, construction, aerospace and defense, automotive, and general business markets. The recent recession has adversely affected the construction and automobile industries. These sectors are beginning to stabilize, but the rate of recovery is still unknown. Information is the main currency of the new industrial age. Global information coverage and the interconnections in global trade and finance demand faster and more accurate information flows.

4

Table of Contents

McGraw-Hill Education

MHE is one of the premier global educational publishers and consists of two operating groups: the School Education Group (“SEG”), serving the elementary and high school (“el-hi”) markets, and the Higher Education, Professional and International Group (“HPI”), serving the college and university, professional, international and adult education markets. As world economies become increasingly centered on the service sector and technology and as the global population continues to rise, education is more than ever the key to growth.

The el-hi market is changing with digital capabilities becoming increasingly critical. SEG sells textbooks and supplemental materials (in print, digital, and hybrid versions) and provides online and traditional assessment and reporting services. The key markets are pre-kindergarten, elementary, secondary, testing, supplemental, vocational, and post-secondary fields in the United States. The market for textbooks consists of adoption states, which are states that provide educational funding to school districts for specific programs based on adoption calendars, and open territory states, which are states that do not follow adoption calendars. This market is influenced strongly by the size and timing of state adoption opportunities and the availability of funds in adoption states and in the open territory. Federal support has eased some of the pressure on state and local finances, which has helped to mitigate the cutbacks in K-12 education.

In the college and university market, and the international market, we sell integrated digital e-learning platforms, textbooks and other instructional resources for the broad range of higher education disciplines. Key markets for higher education products are domestic and international colleges, universities, post-graduate institutions and English as a Second Language (ESL) programs. For the professional market, both in the United States and internationally, we offer digital and print products in medicine, healthcare, engineering, science, computer technology, business, education and general reference.

The college and university market is affected by enrollments, higher education funding and the number of courses available to students. Enrollments in degree-granting higher education institutions are projected to rise by 13% to 20.6 million by 2018, according to the National Center for Educational Statistics. College enrollments are rising as more high school graduates perceive the need to bridge skills gaps with college-educated workers. Continuing education is becoming more common, as workers may need to change careers several times over the course of a working lifetime. Reflecting these trends, online enrollments have continued to grow more rapidly than the total higher education population. Internationally, postsecondary enrollments are also increasing in many regions, notably in India, China and other emerging economies.

Our Strategy

As discussed above, on September 12, 2011 we announced our Growth and Value Plan which includes the creation of two independent companies: McGraw-Hill Financial, a world leader in content and analytics for financial and commodities markets, and McGraw-Hill Education, a global leader in education services and digital learning. This transaction is expected to be completed by the end of 2012.

Four key trends are increasing the need for content and analytics in the financial, commercial and commodities markets:

| • | The globalization of the capital markets: the global demand for capital and commodities markets trading and liquidity is expanding rapidly in both developed and emerging markets |

| • | The need for data-driven decision making tools: developments in technology, communications and data processing have increased the demand for time-critical, multi-asset class data and solutions |

| • | Systemic regulatory change: new global legislation (e.g. Dodd-Frank, U.S. Commodity Futures Trading Commission and Basel III) is creating new and complex operating and capital models for banks and market participants |

| • | Increased volatility and risk: there is amplified uncertainty and market volatility around short-term events are driving the need for new methodologies to measure risk, return and profitability |

McGraw-Hill Financial

In 2012, we plan to focus on the following strategies for our financial information businesses to capitalize on the above four trends:

| • | Integrated Solutions: providing integrated solutions within and across market segments that fill evolving customer needs |

| • | Distribution: capturing additional revenue by leveraging and expanding our strong channel relationships |

| • | Geographic Penetration: using our vast global footprint to capitalize on opportunities in mature and growth markets |

| • | Scalable Capabilities: creating and leveraging efficiency and effectiveness through common platforms, processes and standards |

| • | Continuing to pursue targeted acquisitions and alliances |

| • | Continuing cost-reduction initiatives |

5

Table of Contents

Integrated Solutions: providing integrated solutions within and across market segments that fill evolving customer needs

We will build economies of scale that allow us to leverage and maximize the value of content and analytics across all of our different businesses. This will result in the creation of innovative new solutions that help investors face the evolving challenges of today’s volatile and changing market landscape. The growing need for investors to be able to track price movements across all asset classes creates an existing and fast growing opportunity for us to deliver integrated solutions on commodities, fixed income, equity, credit, and funds that inform strategy and trade ideas on cash, derivatives and volatility indices.

Distribution: capturing additional revenue by leveraging and expanding our strong channel relationships

We will capture additional revenue by leveraging and expanding on our multi-channel distribution capabilities. We have varied distribution channels which enable us to reach many different customers in many different ways with essential, high-value content. Our strategy is to own and commercialize high-quality brands and content and then distribute it to clients in any fashion they wish.

Geographic Penetration: using our vast global footprint to capitalize on opportunities in mature and growth markets

We will increase our global footprint and revenues by expanding upon and fully exploiting the many operational and strategic synergies that exist among our brands, including overlapping customer bases, shared technology platforms, optimized access to global capital markets, and an international employee base active in growth markets. Our scale and leadership positions will also enable us to capitalize on growth trends and extend our position in fast-developing emerging markets.

Scalable Capabilities: creating and leveraging efficiency and effectiveness through common platforms, processes and standards

We will maximize the capabilities of our entire portfolio of assets through an operating model that allows us to leverage infrastructure, and more quickly and effectively combine assets to create new solutions. This will allow us to create solutions that offer high-value, differentiated offerings.

Continuing to pursue targeted acquisitions and alliances

We will continue to pursue acquisitions and alliances that will expand our business and accelerate growth.

| • | In November 2011, we announced an agreement with CME Group to establish a new joint venture in the rapidly growing index business. Under this agreement, we will contribute our S&P Indices business and the CME Group/Dow Jones joint venture will contribute the Dow Jones Indices business to create S&P/Dow Jones Indices, a global leader in index services. S&P/Dow Jones Indices is expected to close by the end of the second quarter of 2012, subject to regulatory approval and customary closing conditions. |

| • | In July 2011, we acquired the issued and outstanding shares of Steel Business Briefing Group (the “SBB Group”), a privately held U.K. company and leading provider of news, pricing and analytics to the global steel market. The SBB Group provides subscription-based, electronic products to the steel industry and its participants through two principal businesses, Steel Business Briefing and The Steel Index. The SBB Group is included within Platts, part of our C&C segment. |

| • | In January 2011, we acquired all of the issued and outstanding membership interest units of Bentek Energy LLC (“Bentek”), which is included as part of our C&C segment. Bentek offers its customers a comprehensive portfolio of data, information and analytics products in the natural gas and liquids sector. The primary purpose of the acquisition was to acquire Bentek’s knowledge, skill and expertise in gathering high-quality detailed data and their ability to identify key relationships within the data critical to industry participants. |

Continuing cost-reduction initiatives

We have made significant progress in 2011 towards our cost reduction goals to ensure that we will have appropriate cost structures to drive margin expansion and invest selectively in attractive growth opportunities. We reduced C&C’s workforce by approximately 100 positions and Standard & Poor’s workforce by approximately 30 positions in 2011. We will continue to look to extend outsourcing efforts to enhance cost synergies and realign administrative support for a leaner overall cost structure.

McGraw-Hill Education

In 2012, we plan to focus on the following strategies for our education business:

| • | Continuing to accelerate growth by aligning McGraw-Hill Education’s key strengths with market forces |

| • | Continue to optimize resource allocation for long-term value |

6

Table of Contents

Continuing to accelerate growth by aligning McGraw-Hill Education’s key strengths with market forces

We will continue to accelerate growth by capitalizing on digital transformation, maintaining and growing our leadership position in individualized learning; expanding international presence to meet the rising demand for education in global growth markets; enhancing capabilities to drive expansion in education services, digital delivery and global growth; and supporting growth through acquisitions or partnerships. We will continue to reinvest resources into the creation of education services and digital products and solutions to better capitalize on growth opportunities in the education market. In November 2011, we announced an agreement with New Oriental Education & Technology Group to form a joint venture company which will provide critical 21st century skills to students across China. The planned formation highlights McGraw-Hill Education’s global expansion in the English-language skills development and college and career readiness services market, as well as its highly advanced digital capabilities.

Optimize resource allocation for long-term value

We will continue to optimize resource allocation to create long-term value. This means deploying capital as appropriate to support our growth strategy, developing an integrated and focused organizational structure, and rationalizing the cost structure to enhance efficiency. We reduced McGraw-Hill Education’s workforce by approximately 540 positions in 2011 to create a flatter more agile organization. We will continue to reduce costs and streamline McGraw-Hill Education’s operational structure which will enable it to aggressively pursue a strategy that focuses on high-growth opportunities in digital learning and education services.

Uncertainties

There can be no assurance that we will achieve success in implementing any one or more of these strategies. The following factors could unfavorably impact operating results in 2012:

| • | Prolonged difficulties in the credit markets |

| • | A change in the regulatory environment affecting our businesses |

| • | Lower educational funding as a result of state budget concerns |

| • | A change in educational spending |

| • | Unanticipated problems in executing our Growth and Value Plan |

Segment and Geographic Data

The relative contribution of our operating segments to operating revenue, operating profit, long-lived assets and geographic area for the three years ended December 31, 2011 is included in Note 12 – Segment and Geographic Information to the Consolidated Financial Statements under Item 8, Consolidated Financial Statements and Supplementary Data, in this Form 10-K.

Our Personnel

As of December 31, 2011, we have approximately 22,700 employees located worldwide, of which approximately 11,600 were employed in the United States.

Available Information

We have an investor kit available online and in print that includes the current (and prior years’) Annual Report, Proxy Statement, Form 10-Qs, Form 10-K, all filings through EDGAR with the Securities and Exchange Commission, and the current earnings release. For online access go to www.mcgraw-hill.com/investor_relations and click on Digital Investor Kit. Requests for printed copies, free of charge, can be e-mailed to investor_relations@mcgraw-hill.com or mailed to Investor Relations, The McGraw-Hill Companies, Inc., 1221 Avenue of the Americas, New York, NY 10020-1095. You can call Investor Relations toll free at 866-436-8502 (domestic callers) or 212-512-2192 (international callers).

You may also read and copy materials that we have filed with the Securities and Exchange Commission (“SEC”) at the SEC’s public reference room located at 450 Fifth Street, N.W., Room 1024, Washington, D.C. 20549. Please call the Commission at 1-800-SEC-0330 for further information on the public reference room. In addition, our filings with the Commission are available to the public on the Commission’s Web site at www.sec.gov. Several years of SEC filings are also available on our Investor Relations Web site. Go to www.mcgraw-hill.com/investor_relations and click on the SEC Filings link.

7

Table of Contents

We are providing the following cautionary statements which identify all known material risks, uncertainties and other factors that could cause our actual results to differ materially from historical and expected results.

We operate in the financial, education, commercial and commodities markets. The commercial markets include automotive, construction, aerospace and defense, and marketing/research information services, while the commodities market includes energy. Certain risk factors are applicable to individual markets while other risk factors are applicable company-wide.

Company-Wide Risk Factors

Our ability to grow is dependent on a number of factors including the following:

Introduction of new products, services or technologies could impact our profitability

| • | We operate in highly competitive markets that continue to change to adapt to customer needs. In order to maintain a competitive position, we must continue to invest in new offerings and new ways to deliver our products and services. |

| ¡ | These investments may not be profitable or may be less profitable than what we have experienced historically. |

| • | We could experience threats to our existing businesses from the rise of new competitors due to the rapidly changing environment within which we operate. |

| • | We rely on our information technology environment and certain critical databases, systems and applications to support key product and service offerings. We believe we have appropriate policies, processes and internal controls to ensure the stability of our information technology, provide security from unauthorized access to our systems and maintain business continuity, but our business could be subject to significant disruption and our operating results may be adversely impacted by unanticipated system failures, data corruption or unauthorized access to our systems. |

| • | We are in the process of migrating certain of our financial processing systems to an enterprise-wide systems solution. There can be no certainty that these initiatives will deliver the expected benefits. The failure to migrate successfully may impact our ability to process transactions accurately and efficiently. In addition, the failure to either deliver the application on time, or anticipate the necessary readiness and training needs, could lead to business disruption. |

A significant increase in operating costs and expenses could have a material adverse effect on our profitability

| • | Our major expenses include employee compensation and printing, paper, and distribution costs for product-related manufacturing. |

| ¡ | We offer competitive salary and benefit packages in order to attract and retain the quality employees required to grow and expand our businesses. Compensation costs are influenced by general economic factors, including those affecting the cost of health insurance and postretirement benefits, and any trends specific to the employee skill sets we require. |

| ¡ | We could experience changes in pension costs and funding requirements due to poor investment returns and/or changes in pension assumptions. |

| ¡ | Paper prices fluctuate based on the worldwide demand and supply for paper in general and for the specific types of paper used by us. Our overall paper price increase is currently limited due to negotiated price reductions, long-term agreements, and short-term price caps for a portion of paper purchases that are not protected by long-term agreements. |

| ¡ | Our books and magazines are printed by third parties and we typically have multi-year service contracts for the printing of books and magazines in order to reduce price fluctuations over the contract term. |

| ¡ | We make significant investments in information technology data centers and other technology initiatives as well as significant investments in the development of programs for the el-hi market place. Although we believe we are prudent in our investment strategies and execution of our implementation plans, there is no assurance as to the ultimate recoverability of these investments. |

Our ability to protect our intellectual property rights could impact our competitive position

| • | Our products contain intellectual property delivered through a variety of media, including print and digital. Our ability to achieve anticipated results depends in part on our ability to defend our intellectual property against infringement. Our operating results may be adversely affected by inadequate or changing legal and technological protections for intellectual property and proprietary rights in some jurisdictions and markets. |

Exposure to litigation could have a material effect on our financial position and results of operations

| • | We are involved in legal actions and claims arising from our business practices, as discussed under Item 7, Management’s Discussion and Analysis of Financial Condition and Results of Operations, in this Form 10-K and in Note 13 – Commitments and Contingencies to the Consolidated Financial Statements under Item 8, Consolidated Financial Statements and |

8

Table of Contents

| Supplementary Data, in this Form 10-K, and face the risk that additional actions and claims will be filed in the future. Due to the inherent uncertainty of the litigation process, the resolution of any particular legal proceeding or change in applicable legal standards could have a material effect on our financial position and results of operations. |

Risk of doing business abroad

| • | As we continue to expand our operations overseas, we face the increased risks of doing business abroad, including inflation, fluctuation in interest rates and currency exchange rates, changes in applicable laws and regulatory requirements, export and import restrictions, tariffs, nationalization, expropriation, limits on repatriation of funds, civil unrest, terrorism, unstable governments and legal systems, and other factors. Adverse developments in any of these areas could cause actual results to differ materially from historical and/or expected operating results. |

Risks associated with the proposed spin-off transaction

| • | Our previously announced tax-free spin-off is complex in nature and subject to various regulatory approvals, including a favorable letter ruling from the Internal Revenue Service, and may be affected by unanticipated developments or changes in market conditions. These factors could prevent the completion of or otherwise adversely affect or delay the proposed spin-off. |

| • | Completion of the spin-off requires significant time, effort, and expense. Any delays in the anticipated completion of the spin-off may increase the expenses which we incur to complete the transaction. The separated businesses could also face unanticipated problems in operating independently, and thus may not achieve the anticipated benefits of the separation. |

| • | If consummated, the spin-off will result in two separate independent public companies each of which will be a smaller, less diversified company than we currently are with a narrower business focus than we currently have. In addition, diversification of revenues, costs, and cash flows may diminish. As such, it is possible that our results of operations, cash flows, working capital and financing requirements may be subject to increased volatility. |

| • | The spin-off transaction requires us to hire, retain and develop our senior management and a highly skilled workforce for two separate businesses. Any unplanned turnover or our failure to develop current leadership positions or to hire and retain a skilled workforce could affect our institutional knowledge base and our competitive advantage. Our employees may also be distracted due to uncertainty about their future roles with each of the separate companies pending the completion of the spin-off transaction. In addition, our operating results could be adversely affected by increased costs due to increased competition for employees and higher employee turnover. |

| • | In addition, we plan to outsource certain support functions to third-party service providers in the future to achieve cost savings and efficiencies. If the service providers that we outsource these functions to do not perform effectively, we may not be able to achieve the expected cost savings and depending on the function involved, we may experience business disruption, processing inefficiencies, the loss of or damage to intellectual property through security breach, or harm employee morale. |

Risk Factors Specific to S&P Ratings

Changes in the volume of debt securities issued in domestic and/or global capital markets and changes in interest rates and other volatility in the financial markets could have a material impact on our results of operations

| • | Unfavorable financial or economic conditions that either reduce investor demand for debt securities or reduce issuers’ willingness or ability to issue such securities could reduce the number and dollar volume of debt issuance for which S&P Ratings provides credit ratings. |

| • | Increases in interest rates or credit spreads, volatility in financial markets or the interest rate environment, significant political or economic events, defaults of significant issuers and other market and economic factors may negatively impact the general level of debt issuance, the debt issuance plans of certain categories of borrowers, and/or the types of credit-sensitive products being offered. |

| • | A sustained period of market decline or weakness could have a material adverse effect on us. |

| • | Our results could be adversely affected because of public statements or actions by market participants, government officials and others who may be advocates of increased regulation, regulatory scrutiny or litigation. |

Increased competition or regulation could result in a loss of market share or revenue

| • | The markets for credit ratings are competitive. S&P Ratings competes domestically and internationally on the basis of a number of factors, including the quality of its ratings, client service, reputation, price, geographic scope, range of products and technological innovation. |

| • | In addition, in some of the countries in which S&P Ratings competes, governments may provide financial or other support to locally-based rating agencies and may from time to time establish official credit rating agencies, credit ratings criteria or procedures for evaluating local issuers. |

9

Table of Contents

Increased domestic and foreign regulation of the credit rating industry may adversely impact S&P Rating’s business

| • | The financial services industry is subject to the potential for increasing regulation in the United States and abroad. The businesses conducted by S&P Ratings are in certain cases regulated under the U.S. Credit Rating Agency Reform Act of 2006, the U.S. Securities Exchange Act of 1934, and/or the laws of the states or other jurisdictions in which they conduct business. |

| ¡ | In the past several years the U.S. Congress, the SEC, the European Commission, through regulators including the International Organization of Securities Commissions and the European Securities and Markets Authority, have been reviewing the role of rating agencies and their processes and the need for greater oversight or regulations concerning the issuance of credit ratings or the activities of credit rating agencies. |

| ¡ | Local, national and multinational bodies have considered and adopted other legislation and regulations relating to credit rating agencies from time to time. |

| ¡ | We do not believe that any such laws, regulations or rules will have a material adverse effect on our financial condition or results of operations. |

| ¡ | Other laws, regulations and rules relating to credit rating agencies are being considered by local, national, foreign and multinational bodies and are likely to continue to be considered in the future, including provisions seeking to reduce regulatory and investor reliance on credit ratings, rotation of credit rating agencies and liability standards applicable to credit rating agencies. The impact on us of the adoption of any such laws, regulations or rules remains uncertain, but could increase the costs and legal risks relating to S&P Rating’s rating activities. |

| ¡ | Additional information regarding rating agencies is provided under Item 7, Management’s Discussion and Analysis of Financial Condition and Results of Operations, in this Form 10-K. |

Risk Factors Specific to S&P Capital IQ / S&P Indices

Increased competition or regulation could result in a loss of market share or revenue

| • | The markets for financial research, investment and advisory services are very competitive. S&P Capital IQ / S&P Indices competes domestically and internationally on the basis of a number of factors, including the quality of its research and advisory services, client service, reputation, price, geographic scope, range of products and services, and technological innovation. |

| • | The financial services industry is subject to the potential for increasing regulation in the United States and abroad. The businesses conducted by S&P Capital IQ / S&P Indices are in certain cases regulated under the U.S. Investment Advisers Act of 1940, the U.S. Securities Exchange Act of 1934, and/or the laws of the states or other jurisdictions in which they conduct business. |

| ¡ | We do not believe that any such laws, regulations or rules will have a material adverse effect on our financial condition or results of operations. |

| ¡ | In the future, other laws, regulations and rules relating to financial information may be considered by local, national, foreign and multinational bodies. |

| ¡ | Additional information regarding S&P Capital IQ / S&P Indices is provided under Item 7, Management’s Discussion and Analysis of Financial Condition and Results of Operations, in this Form 10-K. |

Consolidation of customers could impact our available markets and revenue growth

| • | Our businesses within S&P Capital IQ / S&P Indices have a customer base which is largely comprised of members from the financial services industry. The current challenging business environment and the consolidation of customers resulting from mergers and acquisitions in the financial services industry can result in reductions in the number of firms and workforce which can impact the size of our customer base. |

Risk Factors Specific to Commodities & Commercial

Increased domestic or foreign regulation of the oil price reporting industry may adversely impact Platts’ business

| • | In the fall of 2011, the G20 Cannes Final Summit Declaration called upon the International Organization of Securities Commissions (IOSCO), International Energy Forum, International Energy Agency and the Organization of Petroleum Exporting Countries to prepare recommendations to improve the functioning and oversight of price reporting companies by mid-2012. |

| • | In a meeting with representatives of IOSCO in January 2012, principals at IOSCO advised Platts management that among the recommendations the regulatory group is considering is establishment of formal oversight of price reporting organizations and their processes, or a self-regulatory oversight regime. |

| • | In addition, new rules that are expected to be adopted by the U.S. Commodity Futures Trading Commission (CFTC) in 2012 affecting transactions in oil derivatives may implicate Platts in relation to its administration of the Platts electronic window (eWindow) as a means of determining price assessments in oil. Similar new rules and regulations in Europe are currently under consideration, albeit on a slower time frame. |

10

Table of Contents

| • | We do not believe that any new regulatory or self-regulatory oversight regime, or any such new CFTC or other regulations or rules, would have a material adverse effect on our financial condition or results of operations. |

Changes in the global automotive markets

| • | Declines in the global automotive industry impacts our ability to sustain or grow our revenue streams associated with business intelligence to that market. |

Risk Factors Specific to McGraw-Hill Education Segment

Changes in educational funding could materially affect our education businesses

| • | Our U.S. educational materials and testing businesses may be adversely affected by changes in state educational funding as a result of changes in federal or state legislation, changes in the state procurement processes and/or changes in the condition of the local, state or U.S. economy. |

| • | Although the elementary and high school education market has benefited over the last several years from programs funded under the No Child Left Behind Act of 2002 and, more recently, from additional programs funded under the American Recovery and Reinvestment Act of 2009, future changes in federal funding and/or state or local tax bases could create an unfavorable environment for education budgets, resulting in a decrease in educational spending. |

Our education businesses operate in a cyclical environment

| • | A significant portion of our sales are to customers in educational markets. Our School Education Group and the industry it serves are influenced strongly by the magnitude and timing of state adoption opportunities. Approximately 20 states currently conduct a state-level adoption process to review instructional materials, creating approved lists from which local school districts may select. In the remaining states, known as “open territories,” instructional materials are selected and purchased independently by local districts or individual schools. There is no guarantee that our materials will be successful in the state new adoption market or in open territories. |

Item 1b. Unresolved Staff Comments

None.

Our corporate headquarters are located in leased premises located at 1221 Avenue of the Americas, New York, NY 10020. We lease office facilities at 172 locations; 68 are in the United States. In addition, we own real property at 14 locations, of which 6 are in the United States. The number of overall locations decreased from 2010 primarily due to the divestiture of our Broadcasting Group, which resulted in the loss of owned buildings and leased tower sites. See Note 2 — Acquisitions, Divestitures and Other Significant Events under Item 8, Consolidated Financial Statements and Supplementary Data, in this Form 10-K for further detail. Our properties consist primarily of office space used by each of our segments. Our MHE segment also utilizes warehouse space and book distribution centers. We believe that all of our facilities are well maintained and are suitable and adequate for our current needs.

Information on our legal proceedings in Note 13 — Commitments and Contingencies under Item 8, Consolidated Financial Statements and Supplementary Data, in this Form 10-K.

Item 4. (Removed and Reserved)

11

Table of Contents

Executive Officers of the Registrant

| Name |

Age | Position | ||||

| Harold McGraw III |

63 | Chairman of the Board, President and Chief Executive Officer | ||||

| Jack F. Callahan, Jr. |

53 | Executive Vice President and Chief Financial Officer | ||||

| John L. Berisford |

48 | Executive Vice President, Human Resources | ||||

| D. Edward Smyth |

62 | Executive Vice President, Corporate Affairs and Executive Assistant | ||||

| to the Chairman, President and Chief Executive Officer | ||||||

| Charles L. Teschner, Jr. |

51 | Executive Vice President, Global Strategy | ||||

| Kenneth M. Vittor |

62 | Executive Vice President and General Counsel | ||||

The following executive officers have been full-time employees and officers for less than five years: Mr. Callahan, Mr. Berisford, Mr. Smyth and Mr. Teschner.

Mr. Callahan, prior to becoming an officer on December 6, 2010, was Chief Financial Officer of Dean Foods. Prior to that, Mr. Callahan held senior management positions at PepsiCo, including Chief Financial Officer of Frito-Lay International.

Mr. Berisford, prior to becoming an officer on January 3, 2011, was Senior Vice President, Human Resources, for Pepsi Beverages Company. Prior to that, he held senior Human Resources positions with Pepsi Bottling Group.

Mr. Smyth, prior to becoming an officer on February 17, 2009, served as Chief Administrative Officer and Senior Vice President of Corporate and Government Affairs for H.J. Heinz Company. Prior to that, Mr. Smyth spent fifteen years as a senior Irish diplomat.

Mr. Teschner, prior to becoming an officer on March 23, 2009, served as Lead Partner and senior client officer at the consulting firm of Booz Allen Hamilton, where he lived or worked in more than 20 countries and served on various management committees.

12

Table of Contents

Item 5. Market for the Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities

Price Range of Common Stock

On January 20, 2012, the closing price of our common stock was $46.26 per share as reported on the New York Stock Exchange (“NYSE”) under the ticker symbol “MHP”. The approximate number of record holders of our common stock as of January 20, 2012 was 4,134. The high and low sales prices of the McGraw-Hill Companies’ common stock on the NYSE for the past three fiscal years are as follows:

| 2011 | 2010 | 2009 | ||||

| First Quarter |

$40.56 - $36.20 | $36.67 - $32.68 | $25.89 - $17.22 | |||

| Second Quarter |

43.50 - 38.09 | 36.94 - 26.95 | 34.09 - 22.46 | |||

| Third Quarter |

46.99 - 34.95 | 33.80 - 27.08 | 34.10 - 23.55 | |||

| Fourth Quarter |

45.77 - 38.68 | 39.45 - 32.70 | 35.24 - 24.46 | |||

| Year |

46.99 - 34.95 | 39.45 - 26.95 | 35.24 - 17.22 |

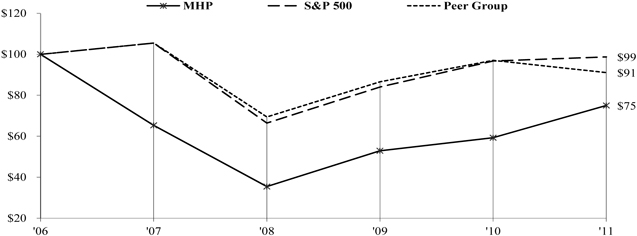

The performance graph below compares our cumulative total shareholder return during the previous five years with a performance indicator of the overall market (i.e., S&P 500), and our peer group. The Peer Group consists of the following companies: Dow Jones & Company (through 2007), Thomson Reuters Corporation, Thomson Reuters PLC (through September 2009), Reed Elsevier NV, Reed Elsevier PLC, Pearson PLC, Moody’s Corporation and Wolters Kluwer. Prior to 2008, the Peer Group also included Thomson Corporation and Reuters Group PLC (which are now included as Thomson Reuters) and Dow Jones & Company, Inc. (which has been acquired by News Corporation). Returns assume $100 invested on December 31, 2006 and total return includes reinvestment of dividends through December 31, 2011.

Dividend Policy

We expect to continue our policy of paying regular cash dividends, although there is no assurance as to future dividend payments because they depend on future earnings, capital requirements and our financial condition. Dividends per share of our common stock for 2011 and 2010 were as follows:

| 2011 | 2010 | |||||||

| $0.250 per quarter in 2011 |

$ | 1.00 | ||||||

| $0.235 per quarter in 2010 |

$ | 0.94 | ||||||

Transfer Agent and Registrar for Common Stock

BNY Mellon Shareowner Services1 is the transfer agent for The McGraw-Hill Companies. BNY Mellon maintains the records for our registered shareholders and can assist with a variety of shareholder related services.

BNY Mellon Shareowner Services

P.O. Box 358015

Pittsburgh PA 15252-8015

13

Table of Contents

View and manage account online at: www.bnymellon.com/shareowner/equityaccess

For shareholder assistance:

| In the U.S. and Canada: |

(888) 201-5538 | |

| Outside the U.S. and Canada: |

(201) 680-6578 | |

| TDD for the hearing impaired: |

(800) 231-5469 | |

| TDD outside the U.S. and Canada: |

(201) 680-6610 | |

| E-mail address: |

shrrelations@bnymellon.com |

| 1 | The Bank of New York Mellon's Shareowner Services business was acquired by Computershare on December 31, 2011. Shareholders should continue to contact BNY Mellon as noted. |

Repurchase of Equity Securities

On January 31, 2007, the Board of Directors approved a stock repurchase program authorizing the purchase of up to 45 million shares of the Company’s common stock (the “2007 Repurchase Program”), which was approximately 13% of the total shares of our outstanding common stock at that time. During the third quarter of 2011, we completed the repurchase of such shares.

On June 29, 2011, the Board of Directors approved a new stock repurchase program authorizing the purchase of up to 50 million shares (the “2011 Repurchase Program”), which was approximately 17% of the total shares of our outstanding common stock at that time. During the fourth quarter of 2011, we repurchased 18 million shares and, as of December 30, 2011, 24 million shares remained available under the 2011 Repurchase Program. The repurchased shares may be used for general corporate purposes, including the issuance of shares for stock compensation plans and to offset the dilutive effect of the exercise of employee stock options. The 2011 Repurchase Program has no expiration date and purchases under this program may be made from time to time on the open market and in private transactions, depending on market conditions.

On December 7, 2011 we entered into two separate accelerated share repurchase agreements (“ASR Agreements”) with a financial institution to initiate share repurchases, aggregating $500 million. The first ASR Agreement was structured as an uncollared ASR Agreement in which we paid $250 million on December 12, 2011 and received an initial delivery of approximately 5 million shares subject to a 20%, or $50 million, holdback. The second ASR Agreement was structured as a capped ASR Agreement in which we paid $250 million and received approximately 5 million shares representing the minimum number of common shares to be repurchased based on a calculation using a specific capped price per share. Further discussion relating to our ASR Agreements can be found in Note 9 – Equity to our Consolidated Financial Statements.

The following table provides information on our purchases of our outstanding common stock during the fourth quarter of 2011 pursuant to the 2011 Repurchase Program (column c). In addition to these purchases, the number of shares in column (a) include: 1) shares of common stock that are tendered to us to satisfy our employees’ tax withholding obligations in connection with the vesting of awards of restricted shares (we repurchase such shares based on their fair market value on the vesting date), and 2) our shares deemed surrendered to us to pay the exercise price and to satisfy our employees’ tax withholding obligations in connection with the exercise of employee stock options. There were no other share repurchases during the quarter outside the repurchases noted below.

| (amounts in millions, except average price paid per share) | ||||||||||||||||

| Period |

(a) Total Number of Shares Purchased |

(b) Average Price Paid per Share |

(c) Total Number of Shares Purchased as Part of Publicly Announced Programs |

(d) Maximum Number of Shares that may yet be Purchased Under the Programs |

||||||||||||

| (Oct. 1 – Oct. 31, 2011) |

2 | $ | 43.99 | 2 | 40 | |||||||||||

| (Nov. 1 – Nov. 30, 2011) |

6 | $ | 42.80 | 6 | 34 | |||||||||||

| (Dec. 1 – Dec. 31, 2011) |

10 | — | 1 | 10 | 24 | |||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total – Qtr |

18 | $ | 43.14 | 2 | 18 | 24 | ||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| 1 | Average price not available for the ASR transactions. |

| 2 | Average price per share information does not include the ASR transactions. |

14

Table of Contents

Item 6. Selected Financial Data

(Dollars in millions, except per share amounts or as noted)

| 2011 | 2010 | 2009 | 2008 | 2007 | ||||||||||||||||

| Income statement data: |

||||||||||||||||||||

| Revenue |

$ | 6,246 | $ | 6,072 | $ | 5,870 | $ | 6,248 | $ | 6,669 | ||||||||||

| Segment operating income |

1,622 | 1,593 | 1,386 | 1,465 | 1,821 | |||||||||||||||

| Income from continuing operations before taxes on income |

1,347 | 1 | 1,331 | 3 | 1,182 | 4 | 1,280 | 5 | 1,620 | 6 | ||||||||||

| Provision for taxes on income |

489 | 483 | 429 | 473 | 603 | |||||||||||||||

| Net income attributable to The McGraw-Hill Companies, Inc. |

911 | 2 | 828 | 731 | 800 | 1,014 | ||||||||||||||

| Earnings per common share: |

||||||||||||||||||||

| Basic |

3.05 | 2 | 2.68 | 2.34 | 2.53 | 3.01 | ||||||||||||||

| Diluted |

3.00 | 2 | 2.65 | 2.33 | 2.51 | 2.94 | ||||||||||||||

| Dividends per share |

1.00 | 0.94 | 0.90 | 0.88 | 0.82 | |||||||||||||||

| Operating statistics: |

||||||||||||||||||||

| Return on average equity |

48.2 | % | 40.4 | % | 45.7 | % | 54.1 | % | 46.6 | % | ||||||||||

| Income from continuing operations before taxes on income as a percent of revenue |

21.6 | % | 21.9 | % | 20.1 | % | 20.5 | % | 24.3 | % | ||||||||||

| Net income as a percent of revenue |

15.0 | % | 14.0 | % | 12.8 | % | 13.1 | % | 15.4 | % | ||||||||||

| Balance sheet data: |

||||||||||||||||||||

| Working capital |

$ | (451 | ) | $ | 694 | $ | 474 | $ | (231 | ) | $ | (307 | ) | |||||||

| Total assets |

6,427 | 7,047 | 6,475 | 6,080 | 6,391 | |||||||||||||||

| Total debt |

1,198 | 1,198 | 1,198 | 1,268 | 1,197 | |||||||||||||||

| Equity |

1,584 | 2,292 | 1,929 | 1,353 | 1,678 | |||||||||||||||

| Number of employees |

22,660 | 20,755 | 21,077 | 21,649 | 21,171 | |||||||||||||||

| 1 | Includes the impact of the following items: a $66 million pre-tax restructuring charge and a $10 million pre-tax charge for Growth and Value Plan costs. |

| 2 | Includes a $74 million gain from the sale of our Broadcasting Group, net of taxes of $48 million. |

| 3 | Includes the impact of the following items: a $16 million pre-tax charge for subleasing excess space in our New York facilities, an $11 million pre-tax restructuring charge, a $7 million pre-tax gain on the sale of certain equity interests at Standard & Poor’s Ratings and a $4 million pre-tax gain on the sale of McGraw-Hill Education’s Australian secondary education business. |

| 4 | Includes the impact of the following items: a $15 million net pre-tax restructuring charge, a $14 million pre-tax loss on the sale of Vista Research, Inc. and an $11 million pre-tax gain on the sale of BusinessWeek. |

| 5 | Includes a $73 million pre-tax restructuring charge. |

| 6 | Includes the impact of the following items: a $44 million pre-tax restructuring charge and a $17 million pre-tax gain on the sale of our mutual fund data business. |

15

Table of Contents

Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations

(Dollars in millions, except per share amounts or as noted)

The following Management Discussion and Analysis (“MD&A”) provides a narrative of the results of operations and financial condition of The McGraw-Hill Companies, Inc. (together with its consolidated subsidiaries, the “Company,” “we,” “us” or “our”) for the years ended December 31, 2011 and 2010, respectively. The MD&A should be read in conjunction with the Consolidated Financial Statements and accompanying notes included in this Form 10-K for the year ended December 31, 2011, which have been prepared in accordance with accounting principles generally accepted in the United States of America (“U.S. GAAP”). The MD&A includes the following sections:

| • | Overview |

| • | Results of Operations |

| • | Liquidity and Capital Resources |

| • | Reconciliation of Non-GAAP Financial Information |

| • | Critical Accounting Estimates |

| • | Recently Issued or Adopted Accounting Standards |

Certain of the statements below are forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. In addition, any projections of future results of operations and cash flows are subject to substantial uncertainty. See Forward-Looking Statements on page 2 of this report.

OVERVIEW

We are a leading global information services provider serving the financial services, education, commercial and commodities markets with the information they need to succeed in the “Knowledge Economy”. The commercial markets include automotive, construction, aerospace and defense, and marketing/research information services, while the commodities market includes energy.

Our operations consist of four operating segments which have historically been named: Standard & Poor’s (“S&P”), McGraw-Hill Financial, McGraw-Hill Information & Media and McGraw-Hill Education (“MHE”). As part of our Growth and Value Plan we have changed the names of our four operating segments to align with how we plan on referring to the businesses going forward. S&P has changed to S&P Ratings, McGraw-Hill Financial has been changed to S&P Capital IQ / S&P Indices, McGraw-Hill Information & Media has changed to Commodities & Commercial (“C&C”) and MHE has remained the same. Going forward, the new McGraw-Hill Financial will include S&P Ratings, S&P Capital IQ / S&P Indices and C&C.

| • | S&P Ratings is the world's foremost provider of credit ratings providing investors with information and independent ratings benchmarks for their investment and financial decisions. |

| • | S&P Capital IQ / S&P Indices is a leading global provider of digital and traditional research and analytical tools which integrate cross-asset analytics, desktop services, and valuation and index benchmarks for investment advisors, wealth managers and institutional investors. |

| • | C&C consists of business-to-business companies specializing in commercial and commodities markets, each an expert in its industry, that deliver their customers access to actionable data and analytics. |

| • | MHE is a leading global provider of educational materials, information and solutions serving the elementary and high school, college and university, professional, international and adult education markets. |

On October 3, 2011, we entered into a definitive agreement with The E.W. Scripps Company to sell the Broadcasting Group. The sale was completed on December 30, 2011, when we received net proceeds of approximately $216 million. The divestiture of our Broadcasting Group, previously included in our C&C segment, was carried out pursuant to our Growth and Value Plan discussed in further detail below. As a result of the sale, the results of operations for all periods presented have been reclassified to reflect the Broadcasting Group as a discontinued operation and the assets and liabilities of the business have been removed from the Consolidated Balance Sheet as of December 31, 2011 and reclassified as held for sale as of December 31, 2010.

On September 12, 2011, we announced that our Board of Directors unanimously approved a comprehensive Growth and Value Plan that includes separation into two public companies: McGraw-Hill Financial, focused on content and analytics for financial markets, and McGraw-Hill Education, focused on education services and digital learning. On December 7, 2011, management provided an update on our Growth and Value Plan discussing new actions that will facilitate the separation into two independent companies. Highlighted actions included:

| • | Reporting results for 2012 in five lines of business for the new McGraw-Hill Financial (S&P Ratings, S&P Capital IQ, S&P Indices, Commodities Markets and Commercial Markets). |

| • | Reducing the McGraw-Hill Education workforce by 10% to create a flatter and more agile organization, see Note 11 – Restructuring to the Consolidated Financial Statements for further detail. |

16

Table of Contents

| • | Freezing our U.S. defined-benefit pension plan as of April 1, 2012 and focusing our retirement program on market-competitive offerings, see Note 7 – Employee Benefits to the Consolidated Financial Statements for further detail. |

| • | Repurchasing additional shares through a $500 million accelerated share repurchase transaction, see Note 9 – Equity to the Consolidated Financial Statements for further detail. |

We expect to complete the separation by the end of 2012 through a tax-free spin-off of the education business to the Company’s shareholders, subject to various conditions and regulatory approvals including final Board approval and a tax ruling from the Internal Revenue Service. Professional fees associated with the Growth and Value Plan recorded during the fourth quarter of 2011 were approximately $10 million.

Key results for the years ended December 31 are as follows:

| Years ended December 31, | % Change | |||||||||||||||||||

| 2011 | 2010 | 2009 | ’11 vs ’10 | ’10 vs ’09 | ||||||||||||||||

| Revenue |

$ | 6,246 | $ | 6,072 | $ | 5,870 | 3 | % | 3 | % | ||||||||||

| Operating income |

$ | 1,422 | $ | 1,413 | $ | 1,259 | 1 | % | 12 | % | ||||||||||

| % Operating margin |

23 | % | 23 | % | 21 | % | ||||||||||||||

| Diluted EPS |

$ | 3.00 | $ | 2.65 | $ | 2.33 | 13 | % | 14 | % | ||||||||||

As the customers of our businesses vary, we manage and assess the performance of our business based on the performance of our segments and use operating income as a key measure. Based on this approach and the nature of our operations, the discussion of results generally focuses around our four business segments and their related operating groups versus distinguishing between products and services.

2011

Revenue increased at our S&P Ratings, S&P Capital IQ / S&P Indices and C&C segments and declined at our MHE segment. Operating income improved at our S&P Capital IQ / S&P Indices and C&C segments and declined at our S&P Ratings and MHE segments.

| • | S&P Ratings revenue increased 4% and operating income declined 6%. Revenue growth was driven by an increase in non-transaction revenues due to growth in non-issuance related revenue at corporate ratings and increases at CRISIL, our majority owned Indian credit rating agency, partially offset by declines in structured finance. The decline in operating income was driven by an increase in expenses resulting from staff increases and incremental compliance and regulatory costs as well as a decline in transaction revenue. |

| • | S&P Capital IQ / S&P Indices revenue and operating income increased 14% and 28%, respectively. Increases were primarily driven by Integrated Desktop Solutions due to growth at Capital IQ, revenue from TheMarkets.com acquired in September 2010 and our subscription base for the Global Credit Portal, which includes RatingsDirect; S&P Indices due to growth in our exchange-traded fund products; and increases at Enterprise Solutions driven by growth at Global Data Solutions, which includes RatingsXpress. Also impacting operating income were higher expenses from personnel costs and additional costs to further develop infrastructure. |

| • | C&C revenue and operating income increased 10% and 18%, primarily driven by strong demand for Platt’s’ proprietary content and growth in our syndicated studies and consulting services in the automotive and non-automotive sectors, partially offset by decreases in our construction business. |

| • | MHE revenue and operating income declined 6% and 12%, respectively, primarily due to decreases in the adoption states as well as open territory sales at School Education Group. Also impacting operating income were increased costs due to technology requirements and the continuing investment in digital product development. |

2010

Revenue increased at our S&P Ratings, S&P Capital IQ / S&P Indices and MHE segments and declined at our C&C segment. Operating income improved at all four of our segments.

| • | S&P Ratings revenue and operating income increased 10% and 7%, respectively. Increases were largely due to growth in transaction revenues driven by high-yield corporate bond issuance. These increases were partially offset by declines in structured finance. |

| • | S&P Capital IQ / S&P Indices revenue and operating income increased 6% and 4%, respectively. Increases were largely due to growth in S&P Indices, RatingsXpress and RatingsDirect as compared to the prior year. Additional growth occurred at Capital IQ. These increases were partially offset by declines in investment research products. |

| • | C&C revenue declined 7% and operating income improved significantly compared to the prior year, primarily driven by the divestiture of BusinessWeek in the fourth quarter of 2009. Offsetting this revenue decline was continued growth in our global commodities information products related to oil and natural gas, increases in both political and base advertising and growth at JDPA, primarily due to syndicated research sales. |

17

Table of Contents

| • | MHE revenue and operating income improved 2% and 32%, respectively, primarily due to increases at Higher Education for both print and digital product and SEG in the adoption states. The increases were partially offset by declines in SEG related to open territory sales and custom testing revenue due to the discontinuation of several contracts. |

Outlook

As discussed above, on September 12, 2011, we announced our Growth and Value Plan that includes separation into two public companies: McGraw-Hill Financial and McGraw-Hill Education. This transaction is expected to be completed by the end of 2012.

Four key trends are increasing the need for content and analytics in the financial, commercial and commodities markets:

| • | The globalization of the capital markets: the global demand for capital and commodities markets trading and liquidity is expanding rapidly in both developed and emerging markets |

| • | The need for data-driven decision making tools: developments in technology, communications and data processing have increased the demand for time-critical, multi-asset class data and solutions |

| • | Systemic regulatory change: new global legislation (e.g. Dodd-Frank, U.S. Commodity Futures Trading Commission and Basel III) is creating new and complex operating and capital models for banks and market participants |

| • | Increased volatility and risk: there is amplified uncertainty and market volatility around short-term events are driving the need for new methodologies to measure risk, return and profitability |

McGraw-Hill Financial

In 2012, we plan to focus on the following strategies for our financial information businesses to capitalize on the above four trends:

| • | Integrated Solutions: providing integrated solutions within and across market segments that fill evolving customer needs |

| • | Distribution: capturing additional revenue by leveraging and expanding our strong channel relationships |

| • | Geographic Penetration: using our vast global footprint to capitalize on opportunities in mature and growth markets |

| • | Scalable Capabilities: creating and leveraging efficiency and effectiveness through common platforms, processes and standards |

| • | Continuing to pursue targeted acquisitions and alliances |

| • | Continuing cost-reduction initiatives |

McGraw-Hill Education

In 2012, we plan to focus on the following strategies for our education business:

| • | Continuing to accelerate growth by aligning McGraw-Hill Education’s key strengths with market forces |

| • | Continue to optimize resource allocation for long-term value |

Uncertainties

There can be no assurance that we will achieve success in implementing any one or more of these strategies. The following factors could unfavorably impact operating results in 2012:

| • | Prolonged difficulties in the credit markets |

| • | A change in the regulatory environment affecting our businesses |

| • | Lower educational funding as a result of state budget concerns |

| • | A change in educational spending |

| • | Unanticipated problems in executing our Growth and Value Plan |

Further projections and discussion on our 2012 outlook for our segments can be found within “Results of Operations”.

18

Table of Contents

RESULTS OF OPERATIONS

Consolidated Review

| Years ended December 31, | % Change | |||||||||||||||||||

| 2011 | 2010 | 2009 | '11 vs '10 | '10 vs '09 | ||||||||||||||||

| Revenue |

||||||||||||||||||||

| Product |

$ | 2,275 | $ | 2,411 | $ | 2,362 | (6 | %) | 2 | % | ||||||||||

| Service |

3,971 | 3,661 | 3,508 | 8 | % | 4 | % | |||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Operating-related expenses |

||||||||||||||||||||

| Product |

1,008 | 1,080 | 1,132 | (7 | %) | (5 | %) | |||||||||||||

| Service |

1,392 | 1,215 | 1,207 | 15 | % | 1 | % | |||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Selling and general expenses |

2,281 | 2,234 | 2,113 | 2 | % | 6 | % | |||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total expenses |

4,837 | 4,670 | 4,608 | 4 | % | 1 | % | |||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Interest expense, net |

75 | 82 | 77 | (9 | %) | 6 | % | |||||||||||||

| Net income attributable to The McGraw-Hill Companies, Inc. |

911 | 828 | 731 | 10 | % | 13 | % | |||||||||||||

Product revenue and expenses consist of educational and information products, primarily books, magazine circulations and syndicated study programs in our MHE and C&C segments. Service revenue and expenses consist of our S&P Ratings and S&P Capital IQ / S&P Indices segments, service assessment contracts in our MHE segment and information-related services and advertising in our C&C segment.

Revenue

2011