UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

Annual

Report Pursuant to Section 13 or 15(d)

of the Securities Exchange Act of 1934

|

For the fiscal year ended |

|

Commission File |

|

December 31, 2005 |

|

Number 1-7107 |

Louisiana-Pacific Corporation

(Exact name of registrant as specified in its charter)

|

Delaware |

93-0609074 |

|

(State of Incorporation) |

(I.R.S. Employer Identification No.) |

|

414 Union Street, Suite 2000 Nashville, TN 37219 |

Registrant’s telephone number (including area code) |

|

(Address of principal executive offices) |

615-986-5600 |

Securities registered pursuant to Section 12(b) of the Act:

|

Title of Each Class |

|

Name of Each Exchange on Which Registered |

|

Common Stock, $1 par value |

|

New York Stock Exchange |

|

Preferred Stock Purchase Rights |

|

New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer as defined in Rule 405 of the Securities Act. Yes x No o

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. o

Indicate by check mark if the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See definition of “accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act (Check one):

|

Large accelerated filer x |

Accelerated filer o |

Non-accelerated filer o |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act): Yes o No x

State the aggregate market value of the voting and non-voting common equity held by non-affiliates computed by reference to the price at which the common equity was sold, or the average bid and asked price of such common equity, as of the last business day of the registrant’s most recently completed second fiscal quarter: $2,653,100,000

Indicate the number of shares outstanding of each of the registrant’s classes of common stock as of the latest practicable date: 106,034,834 of Common Stock, $1 par value, outstanding as of March 6, 2006.

Documents Incorporated by

Reference

Definitive Proxy Statement for 2006 Annual Meeting: Part III

Except as otherwise specified and unless the context otherwise requires, references to “LP”, the “Company”, “we”, “us”, and “our” refer to Louisiana-Pacific Corporation and its subsidiaries.

ABOUT FORWARD-LOOKING STATEMENTS

Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934 provide a “safe harbor” for forward-looking statements to encourage companies to provide prospective information about their businesses and other matters as long as those statements are identified as forward-looking and are accompanied by meaningful cautionary statements identifying important factors that could cause actual results to differ materially from those discussed in the statements. This report contains, and other reports and documents filed by us with the Securities and Exchange Commission may contain, forward-looking statements. These statements are or will be based upon the beliefs and assumptions of, and on information available to, our management.

The following statements are or may constitute forward-looking statements: (1) statements preceded by, followed by or that include words like “may,” “will,” “could,” “should,” “believe,” “expect,” “anticipate,” “intend,” “plan,” “estimate,” “potential,” “continue” or “future” or the negative or other variations thereof and (2) other statements regarding matters that are not historical facts, including without limitation, plans for product development, forecasts of future costs and expenditures, possible outcomes of legal proceedings, capacity expansion and other growth initatives and the adequacy of reserves for loss contingencies.

Factors that could cause actual results to differ materially from those expressed or implied by the forward-looking statements include, but are not limited to the following:

· changes in general economic conditions;

· changes in the cost and availability of capital;

· changes in the level of home construction activity;

· changes in competitive conditions and prices for our products;

· changes in the relationship between supply of and demand for building products, including the effects of industry-wide increases in manufacturing capacity;

· changes in the relationship between supply of and demand for raw materials, including wood fiber and resins, used in manufacturing our products;

· changes in tax laws, and interpretations thereof;

· changes in the cost of and availability of energy, primarily natural gas, electricity and diesel fuel;

· changes in other significant operating expenses;

· changes in exchange rates between the U.S. dollar and other currencies, particularly the Canadian dollar, EURO and the Chilean peso;

· changes in general and industry-specific environmental laws and regulations;

· changes in circumstances giving rise to environmental liabilities or expenditures;

· the resolution of product-related litigation and other legal proceedings; and

· acts of God or public authorities, war, civil unrest, fire, floods, earthquakes and other matters beyond our control.

In addition to the foregoing and any risks and uncertainties specifically identified in the text surrounding forward-looking statements, any statements in the reports and other documents filed by us with the Commission that warn of risks or uncertainties associated with future results, events or

2

circumstances identify important factors that could cause actual results, events and circumstances to differ materially from those reflected in the forward-looking statements.

In this report, we rely on and refer to information regarding industry data obtained from market research, publicly available information, industry publications, U.S. government sources and other third parties. Although we believe the information is reliable, we cannot guarantee the accuracy or completeness of the information and have not independently verified it.

3

Our company, headquartered in Nashville, TN, is a leading manufacturer and distributor of building products. As of December 31, 2005, we had approximately 5,600 employees and operated 29 facilities in the U.S. and Canada and one facility in Chile. Our focus is on delivering innovative, high-quality commodity and specialty building products to retail, wholesale, home building and industrial customers. Our products are used primarily in new home construction, repair and remodeling, and manufactured housing.

Business Segments

We operate in three segments: Oriented Strand Board (OSB); Siding; and Engineered Wood Products (EWP). In general, our businesses are affected by the level of housing starts; the level of home repairs; the availability and cost of financing; changes in industry capacity; changes in the prices we pay for raw materials and energy; changes in foreign exchange rates, primarily the Canadian dollar; and other operating costs.

Our OSB segment manufactures and distributes OSB structural panel products.

OSB is an innovative, affordable and environmentally smart product made from wood strands arranged in layers and bonded with resin. OSB serves many of the same uses as unsanded plywood, including roof decking, sidewall sheathing and floor underlayment, but can be produced at a significantly lower cost. In the past decade, land use regulations, endangered species and environmental concerns have resulted in reduced supplies and higher costs for domestic timber, causing many plywood mills to close or divert their production to other uses. OSB has replaced most of the volume lost from these mills. It is estimated that OSB accounts for approximately 58% of the structural panel consumption with plywood accounting for the remainder. We estimate that the overall North American structural panel market is 45 billion square feet with the OSB market comprising an estimated 27 billion square feet of this market. Based upon our production capacity of 5.6 billion square feet, we account for 21% of the OSB market and 12% of the overall North American structural panel market. We believe we are the largest and one of the most efficient producers of OSB in North America.

Our siding offerings fall into two categories: SmartSide® siding products and related accessories; and hardboard siding and accessory products.

The SmartSide® Products Our SmartSide® products consist of a full line of OSB-based sidings, trim, soffit and fascia. These products have quality and performance characteristics similar to solid wood at more attractive prices due to lower raw material and production costs.

Hardboard Siding Products Our hardboard siding product offerings include a number of lap and panel products in a variety of patterns and textures.

Additionally, as market demand warrants, commodity OSB is produced and sold in this segment.

Our Engineered Wood Products (EWP) segment manufactures and distributes I-joists and laminated veneer lumber (LVL) and other related products. We believe that in North America we are one of the top

4

three producers of I-joists and LVL. A plywood mill associated with our LVL operations in British Columbia is also included in this segment.

We believe that our engineered I-joists, which are used primarily in residential and commercial flooring and roofing systems and other structural applications, are stronger, lighter and straighter than conventional lumber joists. Our LVL is a high-grade, value-added structural product used in applications where extra strength is required, such as headers and beams. It is also used, together with OSB and lumber, in the manufacture of engineered I-joists.

Our other products category includes our composite decking, decorative moulding and Chilean OSB operations and our joint venture that produces cellulose insulation. Additionally, our other products category includes our remaining timber and timberlands, and other minor products, services and closed operations.

Sales, Marketing and Distribution

Our sales and marketing efforts are primarily focused on traditional two-step distribution, professional building products dealers, home centers, third-party wholesale buying groups and other retailers. The wholesale distribution channel includes a variety of specialized and broad-line wholesale distributors and dealers focused primarily on the supply of products for use by professional builders and contractors. The retail distribution channel includes large retail chains catering to the do-it-yourself (DIY) and repair and remodeling markets as well as smaller independent retailers.

Customers

We seek to maintain a broad customer base and a balanced approach to national distribution through both wholesale and retail channels. In 2005, our top 10 customers accounted for approximately 42% of our continuing sales, with the largest customer accounting for no more than 7% of our revenues. Because a significant portion of our sales are from OSB that is a commodity product sold primarily on the basis of price and availability, we are not dependent on any one customer. Our principal customers include the following:

· Wholesale distribution companies, which supply building materials to retailers on a regional, state or local basis;

· Two-step distributors, who provide building materials to smaller retailers, contractors and others;

· Building materials professional dealers, that specialize in sales to professional builders, remodeling firms and trade contractors that are involved in residential home construction and light commercial building;

· Retail home centers, that provide access to consumer markets with a broad selection of home improvement materials and increasingly serve professional builders, remodelers and trade contractors; and

· Manufactured housing producers, who design, construct and distribute prefabricated residential and light commercial structures, including fully manufactured, modular and panelized structures, for consumer and professional markets.

Seasonality

Our business is subject to seasonal variances, with demand for many of our products tending to be greater during the building season in the second and third quarters. From time to time, we engage in

5

promotional activities designed to stimulate demand for our products, such as reducing our selling prices and providing extended payment terms, particularly at times when demand is otherwise relatively soft. We do this in an effort to better balance supply with demand, manage our inventory levels, manage the logistics of our product shipments, allow our production facilities to run efficiently, meet the terms offered by our competitors, and/or obtain initial orders from customers.

Competitors

The building products industry is highly competitive. We compete internationally with several thousand forest and building products firms, ranging from very large, fully integrated firms to smaller enterprises that may manufacture only one or a few items. We also compete less directly with firms that manufacture substitutes for wood building products. Some competitors have substantially greater financial and other resources than we do that could, in some instances, give them a competitive advantage over us.

Raw Materials

Wood fiber is the primary raw material used in most of our operations, and the primary source of wood fiber is timber. The primary end-markets for timber harvested in the U.S. are manufacturers who supply: (1) the housing market, where it is used in the construction of new housing and the repair and remodeling of existing housing; (2) the pulp and paper market; and (3) export markets. The supply of timber is limited by access to timber and by the availability of timberlands. The availability of timberlands, in turn, is limited by several factors, including forest management policies, alternate uses of land, and loss to urban or suburban real estate development.

During 2003, we sold our remaining fee timberland. This wood fiber largely supplied our plywood business that we divested in 2002. In Canada, we harvest enough timber annually under long-term harvest rights with various Canadian governments and other third parties to support our Canadian production facilities. The average remaining life of our Canadian timber rights is 20 years with provisions for regular renewal.

We purchase approximately 59% of our wood fiber requirements on the open market, through either private cutting contracts or purchased wood arrangements. Our remaining wood fiber requirements (41%) are fulfilled through government contracts, principally in Canada. Because wood fiber is subject to commodity pricing, the cost of various types of timber that we purchase in the market has at times fluctuated greatly due to weather, governmental, economic or other industry conditions. However, our mills are generally located in areas that are in close proximity to large and diverse supplies of timber. Our mills generally have the ability to procure wood fiber at competitive prices from third-party sources.

In addition to wood fiber, we use a significant quantity of various resins in our manufacturing processes. Resin product costs are influenced by changes in the prices of raw materials used to produce resin, primarily petroleum products, as well as demand for resin products.

While the majority of our energy requirements are generated at our plants through the conversion of wood waste, we also purchase substantial amounts of energy in our operations, primarily electricity and natural gas. Energy prices have experienced significant volatility in recent years, particularly in deregulated markets. We attempt to control our exposure to energy price changes through the use of long-term supply agreements.

Environmental Compliance

Our operations are subject to many environmental laws and regulations governing, among other things, discharges of pollutants and other emissions on or into land, water and air, the disposal of hazardous substances or other contaminants, the remediation of contamination and the restoration and

6

reforestation of timberlands. In addition, certain environmental laws and regulations impose liability and responsibility on present and former owners, operators or users of facilities and sites for contamination at such facilities and sites without regard to causation or knowledge of contamination. Compliance with environmental laws and regulations can significantly increase the costs of our operations and otherwise result in significant costs and expenses. In some cases, plant closures can result in more onerous compliance requirements becoming applicable to a facility or a site. Violations of environmental laws and regulations can subject us to additional costs and expenses, including defense costs and expenses and civil and criminal penalties. We cannot assure you that the environmental laws and regulations to which we are subject will not become more stringent, or be more stringently implemented or enforced, in the future.

Our policy is to comply fully with all applicable environmental laws and regulations. In recent years, we have devoted increasing management attention to achieving this goal. In addition, from time to time, we undertake construction projects for environmental control equipment or incur other environmental costs that extend an asset’s useful life, improve its efficiency or improve the marketability of certain properties.

The U.S. government has enacted regulations related to Maximum Achievable Control Technology (MACT). MACT regulations govern the manner in which we measure and control the emissions from our manufacturing facilities into the air. We anticipate, based upon our current facilities, that we will be required to spend between $7 million and $10 million over the next several years to comply with these regulations.

Additional information concerning environmental matters is set forth under Item 3, Legal Proceedings, and in Note 18 of the Notes to the financial statements included in item 8 of this report.

Employees

We employ approximately 5,600 people, approximately 1,500 of whom are members of unions. We consider our relationship with our employees generally to be good. From May 2002 through June 2003, a work stoppage occurred at our Chambord, Quebec OSB facility. There can be no assurance that additional work stoppages will not occur. During 2006, one union contract relating to a manufacturing facility in Canada will expire.

Available Information

We file annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, proxy statements and other information with the Securities and Exchange Commission (“SEC”). Our SEC filings are available to the public over the Internet at the SEC’s website at http://www.sec.gov. You may also read and copy any document we file at the SEC’s public reference room at 450 Fifth Street, N.W., Washington, D.C. 20549. You may obtain information on the operation of the SEC’s public reference room in Washington, D.C. by calling the SEC at 1-800-SEC-0330.

In addition, we will make available our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Exchange Act free of charge through our internet website at http://www.lpcorp.com as soon as reasonably practicable after we electronically file such material with, or furnish it to, the SEC.

Segment and Price Trend Data

The following table sets forth, for each of the last three years: (1) production volumes; (2) the average wholesale price of OSB sold in the United States; and (3) logs procured by source. In addition, information concerning our: (1) consolidated net sales by business segment; (2) consolidated profit (loss) by business

7

segment; (3) identifiable assets by segment; (4) depreciation, amortization and cost of timber harvested; (5) capital expenditures; and (6) geographic segment information is included at Note 24 of the Notes to the financial statements included in item 8 of this report and information concerning our sales by product line is included in item 7 of this report.

Product

Information Summary

For Years Ended December 31

(Dollar amounts in millions, except per unit)

|

|

|

2005 |

|

2004 |

|

2003 |

|

|||

|

PRODUCTION VOLUMES |

|

|

|

|

|

|

|

|||

|

OSB, 3¤8” basis, million square feet |

|

5,603 |

|

5,547 |

|

5,526 |

|

|||

|

Wood-based siding, 3¤8” basis, million square feet |

|

963 |

|

1,033 |

|

871 |

|

|||

|

Engineered I-joists, million lineal feet |

|

92 |

|

89 |

|

91 |

|

|||

|

Laminated veneer lumber, thousand cubic feet |

|

11,184 |

|

11,860 |

|

10,070 |

|

|||

|

Composite decking, thousand lineal feet |

|

46,117 |

|

40,044 |

|

32,119 |

|

|||

|

INDUSTRY PRODUCT PRICE TRENDS(1) |

|

|

|

|

|

|

|

|||

|

OSB, MSF, 7¤16” - 24¤16” span rating (North Central price) |

|

$ |

320 |

|

$ |

370 |

|

$ |

293 |

|

|

% LOGS BY SOURCES(2) |

|

|

|

|

|

|

|

|||

|

Fee owned lands |

|

— |

|

— |

|

5 |

|

|||

|

Private cutting contracts |

|

14 |

|

11 |

|

18 |

|

|||

|

Government contracts |

|

41 |

|

31 |

|

22 |

|

|||

|

Purchased logs |

|

45 |

|

58 |

|

55 |

|

|||

|

Total volumes—million board feet |

|

2,774 |

|

2,367 |

|

2,490 |

|

|||

(1) Prices represent yearly averages stated in dollars per thousand square feet (MSF). Source: Random Lengths.

(2) Stated as a percentage of total log volume.

8

You should be aware that the occurrence of any of the events described in this Risk Factors section and elsewhere in this report or in any other of our filings with the SEC could have a material adverse effect on our business, financial position, results of operations and cash flows. In evaluating us, you should consider carefully, among other things, the risks described below and the matters described in “About Forward-Looking Statements.”

Cyclical industry conditions and commodity pricing have and may continue to adversely affect our financial conditions and results of operations. Our operating results reflect the general cyclical pattern of the building products industry. Demand for our products correlates to a significant degree to the level of residential construction activity in North America, which historically has been characterized by significant cyclicality. This cyclicality is influenced by a number of factors, including longer-term interest rates, which in recent years have been at relatively low levels. A significant increase in longer-term interest rates, or the occurrence of other events that reduce levels of residential construction activity, could have a material adverse effect on our financial condition, results of operations and cash flows. Our primary product, OSB, and a significant portion of our raw materials are globally traded commodity products. In addition, our products are subject to competition from manufacturers worldwide. Historical prices for our products have been volatile, and we, like other participants in the building products industry, have limited influence over the timing and extent of price changes for our products. Product pricing is significantly affected by the relationship between supply and demand in the building products industry. Product supply is influenced primarily by fluctuations in available manufacturing capacity. Demand is affected by the state of the economy in general and a variety of other factors. The level of new residential construction activity and home repair and remodeling activity primarily affects the demand for our building products. Demand is also subject to fluctuations due to changes in economic conditions, interest rates, population growth, weather conditions and other factors. We are not able to predict with certainty market conditions and selling prices for our products. We cannot assure you that prices for our products will not decline from current levels. A prolonged and severe weakness in the markets for one or more of our principal products, particularly OSB, could seriously harm our financial condition and results of operations and our ability to satisfy our cash requirements, including the payment of interest and principal on our debt.

We have a high degree of product concentration. OSB accounted for about 60% of our sales in 2005 and 64% in 2004 and we expect OSB sales to continue to account for a substantial portion of our revenues and profits in the future. Concentration of our business in the OSB market further increases our sensitivity to commodity pricing and price volatility. We cannot assure you that pricing for OSB or our other products will not decline from current levels.

Increased industry production capacity for OSB could constrain our operating margins for the foreseeable future. According to Resource Information Systems, Inc. (RISI), an industry market research organization, total North American OSB annual production capacity increased by about 7 billion square feet from 2000 to 2005 on a 3¤8 -inch equivalent basis and is projected to increase by approximately 8 billion square feet in the 2006 to 2010 period. RISI has projected that total North American demand for OSB will increase by about 8 billion square feet during the same 2006 to 2010 period. If increases in OSB production capacity exceed increases in OSB demand, OSB could have constrained operating margins in the foreseeable future.

Intense competition in the building products industry could prevent us from increasing or sustaining our net sales and from sustaining profitability. The markets for our products are highly competitive. Our competitors range from very large, fully integrated forest and building products firms to smaller firms that may manufacture only one or a few types of products. We also compete less directly with firms that manufacture substitutes for wood building products. Many of our competitors have greater financial and other resources than we do, and certain of the mills operated by our competitors may be lower-cost producers than the mills operated by us.

9

Our results of operations may be harmed by potential shortages of raw materials and increases in raw material costs. The most significant raw material used in our operations is wood fiber. We currently obtain about 59% of our wood fiber requirements in the open market. Wood fiber is subject to commodity pricing, which fluctuates on the basis of market factors over which we have no control. In addition, the cost of various types of wood fiber that we purchase in the market has at times fluctuated greatly because of governmental, economic or industry conditions. In addition to wood fiber, we also use a significant quantity of various resins in our manufacturing processes. Resin product costs are influenced by changes in the prices or availability of raw materials used to produce resins, primarily petroleum products, as well as demand for and availability of resin products. Selling prices of our products have not always increased in response to raw material cost increases. We are unable to determine to what extent, if any, we will be able to pass any future raw material cost increases through to our customers through product price increases. Our inability to pass increased costs through to our customers could have a material adverse effect on our financial condition, results of operations and cash flows.

Many of the Canadian forestlands also are subject to the constitutionally protected treaty or common-law rights of the aboriginal peoples of Canada. Most of B.C. is not covered by treaties and, as a result, the claims of B.C.’s aboriginal peoples relating to forest resources are largely unresolved, although many aboriginal groups are actively engaged in treaty discussions with the governments of B.C. and Canada. Final or interim resolution of claims brought by aboriginal groups are expected to result in additional restrictions on the sale or harvest of timber and may increase operating costs and affect timber supply and prices in Canada. It is possible that, over the long term, such claims could have an adverse effect on LP’s business and results of operations.

Our operations require substantial capital. Capital expenditures for expansion or replacement of existing facilities or equipment or to comply with future changes in environmental laws and regulations may be substantial. Although we maintain our production equipment with regular periodic and scheduled maintenance, we cannot assure you that key pieces of equipment in our various production processes will not need to be repaired or replaced or that we will not incur significant additional costs associated with environmental compliance. The costs of repairing or replacing such equipment and the associated downtime of the affected production line could have a material adverse effect on our financial condition, results of operations and cash flow. Based on our current operations, we believe our cash flow from operations and other capital resources will be adequate to meet our operating needs, capital expenditures and other cash requirements for the foreseeable future. If for any reason we are unable to provide for our operating needs, capital expenditures and other cash requirements on economic terms, we could experience a material adverse effect on our business, financial condition, results of operations and cash flows.

We are subject to significant environmental regulation and environmental compliance expenditures and liabilities. Our businesses are subject to many environmental laws and regulations, particularly with respect to discharges of pollutants and other emissions on or into land, water and air, and the disposal, remediation of hazardous substances or other contaminants and, in the past, the restoration and reforestation of timberlands. Compliance with these laws and regulations is a significant factor in our business. We have incurred and expect to continue to incur significant expenditures to comply with applicable environmental laws and regulations. Moreover, some or all of the environmental laws and regulations to which we are subject could become more stringent in the future. Our failure to comply with applicable environmental laws and regulations and permit requirements could result in civil or criminal fines or penalties or enforcement actions, including regulatory or judicial orders enjoining or curtailing operations or requiring corrective measures, installation of pollution control equipment or remedial actions.

Some environmental laws and regulations impose liability and responsibility on present and former owners, operators or users of facilities and sites for contamination at such facilities and sites without regard to causation or knowledge of contamination. In addition, we occasionally evaluate various alternatives with respect to our facilities, including possible dispositions or closures. Investigations undertaken in connection

10

with these activities may lead to discoveries of contamination that must be remediated, and closures of facilities may trigger compliance requirements that are not applicable to operating facilities. Consequently, we cannot assure you that existing or future circumstances or developments with respect to contamination will not require significant expenditures by us.

We are involved in various

environmental matters and legal proceedings. The outcome of these matters and

proceedings and the magnitude of related costs and liabilities are subject to

uncertainties. The

conduct of our business involves the use of hazardous substances and the

generation of contaminants and pollutants. In addition, the end-users of many

of our products are members of the general public. We currently are and from

time to time in the future will be involved in a number of environmental

matters and legal proceedings, including legal proceedings involving warranty

or non-warranty product liability claims and other claims, including claims for

wrongful death, personal injury and property damage alleged to have arisen out of

the use or release by us or our predecessors of hazardous substances.

Environmental matters and legal matters and proceedings, including class action

settlements relating to certain of our products, have in the past caused and in

the future may cause us to incur substantial costs. We have established

contingency reserves in our consolidated financial statements with respect to

the estimated costs of existing environmental matters and legal proceedings to

the extent that our management has determined that such costs are both probable

and reasonably estimable as to amount. However, such reserves are based upon

various estimates and assumptions relating to future events and circumstances,

all of which are the subject of inherent uncertainties. We regularly monitor

our estimated exposure to environmental and litigation loss contingencies and,

as additional information becomes known, may change our estimates significantly.

However, no estimate of the range of any such change can be made at this time. We

may incur costs in respect of existing and future environmental matters and

legal proceedings as to which no contingency reserves have been established. We

cannot assure you that we will have sufficient resources available to satisfy

the related costs and expenses associated

with these matters and proceedings.

Settlements of tax exposures may exceed the amounts we have established for known estimated tax exposures. We maintain reserves for known estimated tax exposures in federal, state and international jurisdictions. Significant income tax exposures may include potential challenges to intercompany pricing, the treatment of financing, acquisition and disposition transactions, the use of hybrid entities, the use of the installment sale method of accounting for tax purposes and other matters. These exposures are settled primarily through the closure of audits with the taxing jurisdictions and, on occasion, through the judicial process, either of which may produce a result inconsistent with past estimates. We believe that we have appropriate liabilities established for known estimated exposures, however, if actual results differ materially from our estimates we could experience a material adverse affect on our financial condition, results of operations and cash flows.

Fluctuations in foreign currency exchange rates could result in currency exchange losses. A significant portion of our operations are conducted through foreign subsidiaries. The functional currency for our Canadian subsidiary is the U.S. dollar. The financial statements of this foreign subsidiary are remeasured into U.S. dollars using the historical exchange rate for property, plant and equipment, timber and timberlands, goodwill, equity and certain other non-monetary assets and liabilities and related depreciation and amortization on these assets and liabilities. These transaction gains or losses are recorded in foreign exchange gains (losses) in the income statement. The functional currency of our Chilean subsidiary is the Chilean Peso. Translation adjustments, which are based upon the exchange rate at the balance sheet date for assets and liabilities and the weighted average rate for the income statement, are recorded in the Accumulated Comprehensive Income (Loss) section of Stockholders’ Equity. Therefore, a strengthening of the Canadian dollar or the Chilean Peso relative to the U.S. dollar may have a material adverse affect on our financial condition and results of operations.

ITEM 1B. Unresolved Staff Comments

None.

11

Information regarding our principal properties and facilities is set forth in the following tables. Information regarding production capacities is based on normal operating rates and normal production mixes under current market conditions, taking into account known constraints such as log supply. Market conditions, fluctuations in log supply, and the nature of current orders may cause actual production rates and mixes to vary significantly from the production rates and mixes shown.

|

ORIENTED STRAND BOARD |

|

|

|

|

Oriented Strand Board Panel Plants(1) |

|

|

|

|

13 plants—5,635 million square feet |

|

|

|

|

annual capacity, 3¤8”basis |

|

Square feet |

|

|

3 shifts per day, 7 days per week |

|

in millions |

|

|

Athens, GA |

|

375 |

|

|

Carthage, TX |

|

450 |

|

|

Chambord, Quebec, Canada |

|

470 |

|

|

Dawson Creek, BC, Canada(2) |

|

390 |

|

|

Hanceville, AL |

|

375 |

|

|

Houlton, ME |

|

280 |

|

|

Jasper, TX |

|

450 |

|

|

Maniwaki, Quebec, Canada |

|

625 |

|

|

Roxboro, NC |

|

470 |

|

|

Sagola, MI |

|

400 |

|

|

Silsbee, TX |

|

330 |

|

|

St. Michel, Quebec, Canada |

|

500 |

|

|

Swan Valley, Manitoba, Canada |

|

520 |

|

|

SIDING |

|

|

|

|

Oriented Strand Board Siding and Specialty |

|

|

|

|

Plants |

|

|

|

|

4 plants—895 million square feet annual |

|

|

|

|

capacity, 3¤8” basis |

|

Square feet |

|

|

3 shifts per day, 7 days per week |

|

in millions |

|

|

Newberry, MI |

|

135 |

|

|

Hayward, WI(3) |

|

475 |

|

|

Tomahawk, WI |

|

135 |

|

|

Two Harbors, MN |

|

150 |

|

|

Hardboard plants |

|

|

|

|

2 plants—550 million square feet capacity, |

|

|

|

|

surface measure |

|

Square feet |

|

|

3 shifts per day, 7 days per week |

|

in millions |

|

|

Roaring River, NC |

|

250 |

|

|

East River, Nova Scotia, |

|

300 |

|

|

ENGINEERED WOOD PRODUCTS |

|

|

|

|

I-joist Plants(5) |

|

|

|

|

1 plant—80 million lineal feet |

|

|

|

|

annual capacity |

|

Lineal feet |

|

|

1 to 3 shifts per day, 5 days per week |

|

in millions |

|

|

Red Bluff, CA |

|

80 |

|

|

LVL Plants |

|

|

|

|

3 plants—12,100 thousand cubic feet |

|

|

|

|

annual capacity |

|

Cubic feet |

|

|

1 to 3 shifts per day, 5 days per week |

|

in thousands |

|

|

Hines, OR |

|

4,000 |

|

|

Golden, BC, Canada |

|

3,500 |

|

|

Wilmington, NC |

|

4,600 |

|

|

OTHER(6) |

|

|

|

|

Plastic Mouldings Plant |

|

|

|

|

1 plant—300 million lineal feet |

|

|

|

|

annual capacity |

|

Lineal feet |

|

|

3 shifts per day, 7 days per week |

|

in millions |

|

|

Middlebury, IN |

|

300 |

|

|

Wood Composite Decking |

|

|

|

|

2 plants—81 million lineal feet capacity |

|

Lineal feet |

|

|

1 shift per day, 7 days per week |

|

in millions |

|

|

Meridian, ID |

|

37 |

|

|

Selma, AL |

|

44 |

|

|

OSB |

|

Panguipulli, Chile |

|

|

Plywood |

|

Golden, BC, Canada |

|

|

Lumber |

|

St. Michel, Quebec, Canada |

|

(1) In addition to the plants described, our 50/50 joint venture with Canfor Corporation owns and operates a plant in Peace Valley, British Columbia, Canada, that has an annual production capacity of 820 million square feet of OSB. The land upon which this plant is located is leased from a third party.

(2) A portion of this facility is located on leased land.

(3) The Hayward, WI OSB siding facility produces both commodity OSB and OSB siding. Only one of the two production lines has the capability of producing OSB siding.

(4) The East River, Nova Scotia, Canada plant produces both hardboard panel products and hardboard siding products.

(5) In addition to the plant described, our 50/50 joint venture with Abitibi-Consolidated owns and operates a plant in St. Prime, Quebec, Canada and a plant in La Rouche, Quebec, Canada The annual production capacity of these facilities is 140 million lineal feet.

(6) The above table does not reflect the 12 cellulose insulation facilities that are operated by LP’s 50/50 joint venture with Casella Waste Systems, U.S. GreenFiber, LLC.

12

|

CANADIAN TIMBERLAND LICENSE AGREEMENTS |

|

|

|

|

|

|

Location |

|

|

|

Acres |

|

|

British Columbia |

|

7,900,000 |

|

||

|

Manitoba |

|

6,300,000 |

|

||

|

Nova Scotia |

|

900,000 |

|

||

|

Quebec |

|

33,600,000 |

|

||

|

Total timberlands under license agreements in Canada |

|

48,700,000 |

|

||

We also have timber-cutting rights under long-term contracts (five years or longer) on approximately 31,000 acres and approximately 30,000 acres on short-term contracts (less than one year), on government and privately owned timberlands in the U.S.

Our Canadian subsidiary has arrangements with four Canadian provincial governments which give our subsidiary the right to harvest a volume of wood off public land from defined forest areas under supply and forest management agreements, long-term pulpwood agreements, and various other timber licenses. The acreage noted above is the gross amount of the licenses and is not reflective of the amount of timber acreage that we currently manage. We also obtain wood from private parties in certain cases where the provincial governments require us to obtain logs from private parties prior to harvesting from the licenses to meet our raw materials needs. The timberland licenses above do not include the timber we have under license associated with our joint venture OSB mill with Canfor Corporation located in British Columbia.

Certain environmental matters and legal proceedings are discussed below.

We are involved in a number of environmental proceedings and activities, and may be wholly or partially responsible for known or unknown contamination existing at a number of other sites at which we have conducted operations or disposed of wastes. Based on the information currently available, management believes that any fines, penalties or other costs or losses resulting from these matters will not have a material adverse effect on our financial position, results of operations, cash flows or liquidity.

Settlement agreements relating to a nationwide class action suit involving OSB Siding manufactured by us and installed prior to January 1, 1996, a related class action in Florida and a nationwide class action suit involving hardboard siding manufactured or sold by corporations acquired by us in 1999 and installed prior to May 15, 2000, were approved by the applicable courts in 1996, 1995 and 2000, respectively. We continue to have payment and other obligations related to the hardboard siding settlement, but have satisfied all of our obligations under the nationwide and Florida OSB siding settlements.

To all persons who filed a timely and valid claim in the In re Louisiana-Pacific Inner-Seal Siding Litigation class action settlement in the United States District Court for the District of Oregon, Case no. 96-879-JO-LEAD: if you filed a timely and valid claim approved by the independent claims administrator but did not receive payment or cash your check, you may be entitled to receive a reissued check provided that you make your request and submit the required documentation postmarked no later than December 31, 2006. For more information or to receive a Settlement Check Reissuance Request Form and Affidavit, please call (877) 677-6722 or write LP Corp, Attention: Claims Department, 805 SW Broadway, Suite 740, Portland, OR 97205-3303.

Additional information regarding these matters is set forth in Note 18 of the Notes to the financial statements included in item 8 of this report.

13

On October 15, 2002, a jury returned a verdict of $29.6 million against us in a Minnesota State Court action entitled Lester Building Systems, a division of Butler Manufacturing Company, and Lester’s of Minnesota, Inc., v. Louisiana-Pacific Corporation and Canton Lumber Company. On December 13, 2002, the District of Oregon, which maintains jurisdiction over the nationwide OSB class action, permanently enjoined the Minnesota state trial court from entering judgment against us with respect to $11.2 million of the verdict that related to siding that was subject to the nationwide OSB siding settlement. Lester’s had appealed this injunction to the Ninth Circuit Court of Appeals. Subsequently, on January 27, 2003, the Minnesota state trial court entered judgment against us in the amount of $20.1 million, representing the verdict amount plus costs and interest less the enjoined amount. That judgment became final and we satisfied that judgment during the second quarter of 2004. The enjoined amount was not paid as part of that satisfaction of judgment because the injunction remains in place pending the appeal by Lester’s. Lester’s appealed the District Court’s injunction to the Ninth Circuit Court of Appeals and on October 24, 2005, the Court of Appeals decided in a 2 to 1 decision to vacate the District Court’s injunction. We requested an En Banc hearing at the Ninth Circuit Court of Appeals, which was denied. We are petitioning the United States Supreme Court to accept this case for review. If the Supreme Court refuses to hear the case or ultimately decides that the injunction was not proper, then the state court judgment of $11.2 million will be entered and our time to appeal that judgment will begin to run. Based upon the information currently available, we believe that any further liability related to this case is remote and will not have a material adverse effect on our financial position, results of operations, cash flows or liquidity.

NATURE GUARD CEMENT SHAKES MATTERS

We are a defendant in a class action lawsuit, captioned as Nature Guard Cement Roofing Shingle Cases, that is pending in the Superior Court for Stanislaus County, California. The plaintiffs in this action are a class of persons owning structures on which Nature Guard Fiber Cement Shakes were installed as roofing. The complaint in this action asserts claims for breach of express and implied warranties, unfair business practices, and violation of the Consumer Legal Remedies Act and seeks general, compensatory, special and punitive damages, disgorgement of profits and the establishment of a fund to provide restitution to the purported class members.

We no longer manufacture or sell fiber cement shakes. The dollar amount of the referenced claims cannot presently be determined. The complaint in this action does not quantify the relief sought by the plaintiffs individually or on behalf of the class. Counsel for the plaintiffs in this action has stated that the plaintiffs “seek as damages the cost of replacing all of the roofs, estimated to be approximately $100 million, plus punitive damages.” In addition to denying liability for the replacement of the affected roofs, we believe that the foregoing estimate of related cost is significantly overstated. We believe that we have substantial defenses to this action and we believe that the resolution of such proceedings will not have a material adverse effect on our financial position, results of operations, cash flows or liquidity.

During the third quarter of 2004, we received a letter from a law firm purporting to represent more than 1,400 potential plaintiffs who allegedly experienced various personal injuries and property damages as a result of the alleged release of chemical substances from our wood treatment facility in Lockhart, Alabama during the period from 1953 to 1998. The letter is characterized as a “pre-litigation settlement demand” to us and Pactiv Corporation, from whom we acquired the facility in 1983. We and the potential plaintiffs agreed to refrain from commencing any legal proceedings in respect of the potential plaintiffs’ allegations and to the tolling of applicable statutes of limitations. The parties further agreed to exchange information and enter into non-binding mediation. In this process and in response to a request by the mediator, the representatives of the potential plaintiffs indicated that they were seeking damages in the amount of $183 million. These agreements terminated in January 2006 after non-binding mediation with

14

plaintiffs counsel failed to resolve any issue. Subsequent to the termination of the agreements, 19 individuals, in 10 separate lawsuits (four in Federal District Court and six in Alabama State Court), filed claims against us seeking compensatory and punitive damages for alleged wrongful death, personal injuries and property damage. These lawsuits are as follows: Melanie Chambers v. TMA Forest Products Group, A division of Tennessee River Pulp and Paper Company, a Subsidiary of Packaging Corporation of America and Louisiana-Pacific Corporation; Lillian Edwards v. TMA Forest Products Group, A division of Tennessee River Pulp and Paper Company, a Subsidiary of Packaging Corporation of America and Louisiana-Pacific Corporation; Rickey Phillips v. TMA Forest Products Group, A division of Tennessee River Pulp and Paper Company, a Subsidiary of Packaging Corporation of America and Louisiana-Pacific Corporation filed in the Federal District Court of Alabama and Thomas Douglas v. TMA Forest Products Group, A division of Tennessee River Pulp and Paper Company, a Subsidiary of Packaging Corporation of America and Louisiana-Pacific Corporation; Stanton Kelley v. TMA Forest Products Group, A division of Tennessee River Pulp and Paper Company, a Subsidiary of Packaging Corporation of America and Louisiana-Pacific Corporation; Sherri Davis, et al. v. TMA Forest Products Group, A division of Tennessee River Pulp and Paper Company, a Subsidiary of Packaging Corporation of America and Louisiana-Pacific Corporation; Lorrine Thompson v. TMA Forest Products Group, A division of Tennessee River Pulp and Paper Company, a Subsidiary of Packaging Corporation of America and Louisiana-Pacific Corporation; Janice Madden v. TMA Forest Products Group, A division of Tennessee River Pulp and Paper Company, a Subsidiary of Packaging Corporation of America and Louisiana-Pacific Corporation; Ginger Cravey v. TMA Forest Products Group, A division of Tennessee River Pulp and Paper Company, a Subsidiary of Packaging Corporation of America and Louisiana-Pacific Corporation filed in the Alabama State Court. Due to numerous uncertainties associated with the matters alleged in the letter and subsequent lawsuits, including uncertainties regarding the existence, nature, magnitude and causation of the alleged wrongful death, injuries and property damage, responsibility therefore and defenses thereto, we are not presently able to quantify our financial exposure, if any, relating to such matters. LP intends to defend these suits vigorously.

We have been named as one of seven named defendants in multiple complaints filed on or about February 26, 2006 in the United States District Court for the Eastern District of Pennsylvania: Sawbell Lumber Co. v. Louisiana-Pacific Corporation, Georgia-Pacific Corporation, Weyerhaeuser Company, Potlatch Corporation, Ainsworth Lumber Co. Ltd., Norbord, Inc., J.M. Huber Corporation; and Columbare Inc. v. Louisiana-Pacific Corporation, Georgia-Pacific Corporation, Weyerhaeuser Company, Potlatch Corporation, Ainsworth Lumber Co. Ltd., Norbord, Inc., J.M. Huber Corporation; and Frontier Lumber Co. Inc. v. Louisiana-Pacific Corporation, Georgia-Pacific Corporation, Weyerhaeuser Company, Potlatch Corporation, Ainsworth Lumber Co. Ltd., Norbord, Inc., J.M. Huber Corporation; and West Lumber Co., Inc. v. Louisiana-Pacific Corporation, Georgia-Pacific Corporation, Weyerhaeuser Company, Potlatch Corporation, Ainsworth Lumber Co. Ltd., Norbord, Inc., J.M. Huber Corporation; and Norword Sash & Door Manufacturing Co.. v. Louisiana-Pacific Corporation, Georgia-Pacific Corporation, Weyerhaeuser Company, Potlatch Corporation, Ainsworth Lumber Co. Ltd., Norbord, Inc., J.M. Huber Corporation. The plaintiffs seek to certify a class consisting of persons and entities who purchased OSB from the defendants from June 1, 2002 through the date the applicable complaint was filed. Plaintiffs seek treble damages in an unspecified amount alleged to have resulted from a conspiracy among the defendants to curtail OSB production in order to fix, raise, maintain and stabilize the prices at which OSB is sold in the United States, in violation of Section 1 of the Sherman Act, 15 U.S.C. §1. We believe that the claims asserted are without merit, and intend to defend this matter vigorously. We are unable to predict whether the court will declare these actions to be class actions, and likewise are unable to predict the potential financial impact of these actions.

We are parties to other legal proceedings. Based on the information currently available, we believe that the resolution of such proceedings will not have a material adverse effect on our financial position, results of operations, cash flows or liquidity.

15

We maintain reserves for the estimated cost of the legal and environmental matters referred to above. However, as with any estimate, there is uncertainty of predicting the outcomes of claims and litigation and environmental investigations and remediation efforts that could cause actual costs to vary materially from current estimates. Due to various uncertainties, we cannot predict to what degree actual payments will exceed the recorded liabilities related to these matters. However, it is possible that, in either the near term or the longer term, revised estimates or actual payments will significantly exceed the recorded liabilities.

For information regarding our financial statement reserves for the estimated costs of the environmental and legal matters referred to above, see Note 18 of the Notes to financial statements included in item 8 in this report.

ITEM 4. Submission of Matters to a Vote of Security Holders

No matter was submitted to a vote of LP’s security holders during the fourth quarter of 2005.

16

PART II

ITEM 5. Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities

The common stock of LP is listed on the New York Stock Exchange with the ticker symbol “LPX.” The Dow-Jones newspaper quotations symbol for the common stock is “LaPac.” Information regarding the high and low sales prices for the common stock for each quarter of the last two years is as follows:

|

HIGH AND LOW STOCK PRICES |

|

|

|

1ST QTR |

|

2ND QTR |

|

3RD QTR |

|

4TH QTR |

|

||||||||||||

|

2005 High |

|

|

$ |

28.73 |

|

|

|

$ |

26.26 |

|

|

|

$ |

27.80 |

|

|

|

$ |

28.69 |

|

|

||

|

Low |

|

|

24.31 |

|

|

|

22.06 |

|

|

|

23.78 |

|

|

|

24.61 |

|

|

||||||

|

2004 High |

|

|

$ |

25.92 |

|

|

|

$ |

26.93 |

|

|

|

$ |

26.71 |

|

|

|

$ |

28.31 |

|

|

||

|

Low |

|

|

17.96 |

|

|

|

21.25 |

|

|

|

21.05 |

|

|

|

23.34 |

|

|

||||||

As of March 6, 2006, there were approximately 10,824 holders of record of our common stock. In February 2004, LP’s Board of Director’s reinstated a quarterly dividend. For the year ended December 31, 2004, LP paid cash dividends of $0.30 per share. For the year ended December 31, 2005, LP paid cash dividends of $0.475 per share. We currently have no restrictions as to the payment of dividends.

ISSUER PURCHASES OF EQUITY SECURITIES

On November 1, 2003, the Board of Directors authorized our management to purchase from time to time up to 20,000,000 shares of its outstanding stock in the open market or in privately negotiated transactions. As of December 31, 2005, the remaining open authorization is 14,431,000 shares. During the third quarter of 2005, we repurchased 5.4 million shares in connection with an accelerated stock buyback program with a financial intermediary for an aggregate purchase price of $151 million (including fees). Under the terms of the program, the financial intermediary delivered to LP the initial number of shares of common stock during LP’s third quarter. On February 9, 2006, LP received the final 166,880 shares under this program. The total shares purchased were 5,589,297 shares at an average price per share (including fees) of $26.95.

17

ITEM 6. Selected Financial Data

Dollar amounts in millions, except per share

|

Year ended December 31 |

|

|

|

2005(3) |

|

2004 |

|

2003(2) |

|

2002(1) |

|

2001 |

|

|||||

|

SUMMARY INCOME STATEMENT DATA |

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

Net sales |

|

$ |

2,598.9 |

|

$ |

2,730.7 |

|

$ |

2,168.7 |

|

$ |

1,482.5 |

|

$ |

1,497.5 |

|

||

|

Income (loss) from continuing operations before cumulative effect of change in accounting principle |

|

475.8 |

|

420.2 |

|

280.7 |

|

(9.3 |

) |

(134.3 |

) |

|||||||

|

Income (loss) from discontinued operations |

|

(19.2 |

) |

0.5 |

|

(8.3 |

) |

(48.9 |

) |

(37.3 |

) |

|||||||

|

Net income (loss) |

|

455.5 |

|

420.7 |

|

272.5 |

|

(62.0 |

) |

(171.6 |

) |

|||||||

|

Income (loss) from continuing operations before cumulative effect of change in accounting principle per share—basic |

|

$ |

4.37 |

|

$ |

3.88 |

|

$ |

2.66 |

|

$ |

(0.09 |

) |

$ |

(1.29 |

) |

||

|

Net income (loss) per share—basic |

|

$ |

4.18 |

|

$ |

3.88 |

|

$ |

2.58 |

|

$ |

(0.59 |

) |

$ |

(1.64 |

) |

||

|

Income (loss) from continuing operations before cumulative effect of change in accounting principle per share—diluted |

|

$ |

4.34 |

|

$ |

3.84 |

|

$ |

2.64 |

|

$ |

(0.09 |

) |

$ |

(1.29 |

) |

||

|

Net income (loss) per share—diluted |

|

$ |

4.15 |

|

$ |

3.84 |

|

$ |

2.56 |

|

$ |

(0.59 |

) |

$ |

(1.64 |

) |

||

|

Average shares of common stock outstanding (millions) |

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

Basic |

|

109.0 |

|

108.3 |

|

105.5 |

|

104.6 |

|

104.4 |

|

|||||||

|

Diluted |

|

109.7 |

|

109.6 |

|

106.5 |

|

104.6 |

|

104.4 |

|

|||||||

|

Cash dividends paid |

|

$ |

0.475 |

|

$ |

0.30 |

|

— |

|

— |

|

$ |

0.24 |

|

||||

|

SUMMARY BALANCE SHEET INFORMATION |

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

Total assets |

|

$ |

3,598.0 |

|

$ |

3,450.6 |

|

$ |

3,204.4 |

|

$ |

2,780.0 |

|

$ |

3,014.0 |

|

||

|

Long-term debt, excluding current portion |

|

$ |

734.8 |

|

$ |

622.5 |

|

$ |

1,020.7 |

|

$ |

1,077.0 |

|

$ |

1,152.0 |

|

||

|

Contingency reserves, excluding current portion |

|

$ |

31.4 |

|

$ |

42.1 |

|

$ |

55.6 |

|

$ |

106.1 |

|

$ |

135.1 |

|

||

|

Stockholders’ equity |

|

$ |

2,042.9 |

|

$ |

1,767.8 |

|

$ |

1,310.9 |

|

$ |

1,006.2 |

|

$ |

1,080.9 |

|

||

(1) As of January 1, 2002, LP adopted the Statement of Financial Accounting Standards (SFAS) No. 142, “Goodwill and Other Intangible Assets”. See Note 1 of the Notes to the financial statements included in item 8 of this report for further information.

(2) As of January 1, 2003, LP adopted SFAS No. 143, “Asset Retirement Obligations”. See Note 1 of the Notes to the financial statements included in item 8 of this report for further information.

(3) As of December 31, 2005, LP adopted FASB Interpretation (FIN) No. 47, “Accounting for Conditional Asset Retirement Obligations—An Interpretation of FASB Statement No. 143”. See Note 1 of the Notes to the financial statements included in item 8 of this report for further information.

18

ITEM 7. Management’s Discussion and Analysis of Financial Conditions and Results of Operations

Our products are used primarily in new home construction, repair and remodeling, and manufactured housing. We also market and sell our products in light industrial and commercial construction and have a modest export business for some of our specialty building products. Our manufacturing facilities are primarily located in the U.S. and Canada, but we also operate a facility in Chile.

To serve these markets, we operate in three segments: Oriented Strand Board (OSB); Siding; and Engineered Wood Products (EWP). OSB is the most significant segment, accounting for 60% of continuing sales in 2005, 64% in 2004 and 62% in 2003.

Over the last several years, we adopted and implemented plans to sell selected businesses and assets in order to improve our operating results, reduce our debt and increase our financial flexibility. The plans involved divesting LP’s plywood, industrial panel, vinyl siding and lumber businesses, fee timber and timberlands, a wholesale operation and our distribution business. We believe that these divestitures, which had been substantially completed at December 31, 2005, enable us to focus our attention exclusively on our retained businesses, and to develop strategies to make them stronger through cost reductions, increased efficiencies and appropriate capacity expansions. Our retained businesses have several common characteristics that include significant scale in the categories in which they compete, strong growth potential in the future and competitive cost structures.

Our most significant product, OSB, is sold as a commodity for which sales prices fluctuate daily based on market factors over which we have little or no control. We cannot predict whether the prices of our products will remain at current levels, increase or decrease in the future. During 2005, commodity OSB prices moderated compared to 2004 but nonetheless remained at relatively high cyclical levels. We saw significant increases in the cost of petroleum-based raw materials, energy and wood (including log delivery costs) throughout our businesses. In our non-commodity based businesses, we were able to implement price increases to partially mitigate these cost increases. We expect the costs of these inputs to remain at relatively high levels, and possibly to increase further, in the foreseeable future.

We derive our revenues from sales of our products. The unit volumes of products sold and the prices at which sales are made determine the amount of our revenues. These volumes and prices are affected by the overall level of demand for, and supply of, products of the type we sell and comparable or substitute products, and by competitive conditions in our industry.

Our operating results reflect the relationship between the amount of our revenues and our costs of production and other operating costs and expenses. Our costs of production are affected by, among other factors, costs of raw materials (primarily wood fiber and various petroleum-based resins) and energy costs, which in turn are affected by the overall market supply of and demand for these manufacturing inputs. The Canadian dollar strengthened significantly against the U.S. dollar in 2005, causing our costs, as reported in U.S. dollars, to rise.

Demand for our products correlates to a significant degree to the level of residential construction activity in North America, which historically has been characterized by significant cyclicality. This activity

19

can be further delineated into three areas: (1) new home construction; (2) repair and remodeling; and (3) manufactured housing.

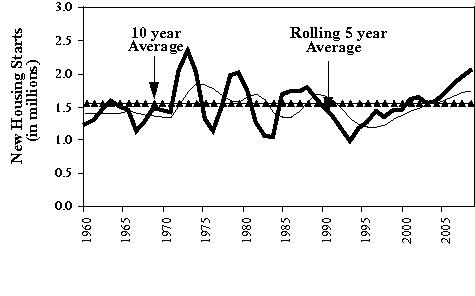

New Home Construction. During the last three years, there has been increased housing activity driven by a combination of higher demand due to the demographics of the U.S. population and a low interest rate environment. The chart below provides a graphical summary of new housing starts in the U.S. since 1960. The level of volatility in housing starts has moderated in recent years. We believe that this is largely due to the continued consolidation among the big homebuilders, shortage of construction laborers and lengthier processes to obtain appropriate zoning. The chart below depicts actual, rolling five and ten year average housing starts.

Source: Resource International Systems, Inc. (RISI)

Repair and Remodeling. Demand for building materials to support home improvement projects is largely tied to the size and age of the existing housing stock in North America. As can be seen from the chart above, the 1970s and 1980s had some of the highest levels of building activity. This puts these homes at an age of 25-35 years, which has been shown to be consistent with the highest per home expenditure rate on repair and remodeling. With the rise in the number and scale of home improvement stores in North America, individuals now have ready and convenient access to obtain the building materials needed for repair and remodeling, as well as increased access to installation services. We believe that the growth rate over the last three years has been in the 4-6% range, and has been driven by increased store-to-store sales and the addition of new stores.

Manufactured Housing. While new home construction activity has been robust in the last three years, manufactured housing has suffered. There are several factors that have led to the decline in the number of manufactured housing units produced, including a lack of available financing, increased ability of potential customers to purchase site-built starter homes and financial difficulties at some of the larger manufactured housing producers.

OSB is a commodity product, and all of our products are subject to competition from manufacturers worldwide. Product supply is influenced primarily by fluctuations in available manufacturing capacity.

20

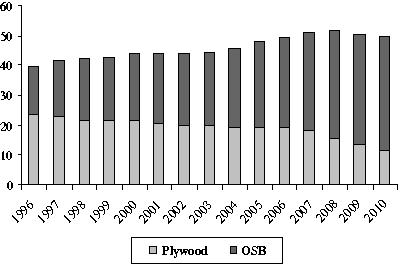

According to Resource International Systems Inc. (RISI), an economic consulting firm, total North American OSB annual production is projected to increase by approximately 8.0 billion square feet in the period from 2006 to 2010 while plywood production is projected to decline by 7.8 billion square feet for the same period. The chart below depicts the North America structural wood market in billions of square feet.

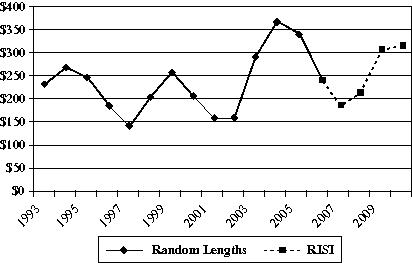

Historical prices for our products have been volatile, and we, like other participants in the building products industry, have limited influence over the timing and extent of price changes for our products. According to Random Lengths, an industry publication, the average North Central wholesale price for OSB (per thousand square feet 7/16” basis) from 1993 through 2005 is presented below. Additionally, according to RISI (as of December 2005), the forecast for average North Central wholesale price for OSB (per thousand square feet 7/16” basis) through 2010 is also included.

21

Presented in Note 1 of the Notes to the financial statements in item 8 of this report is a discussion of our significant accounting policies. The discussion of each of the policies outlines the specific accounting treatment related to each of these accounting areas. While all of these are important to understand when reading our financial statements, there are several policies that we have adopted and implemented from among acceptable alternatives that could lead to different financial results had another policy been chosen:

Inventory valuation. We use the LIFO (last-in, first-out) method for some of our log inventories with the remaining inventories valued at FIFO (first-in, first-out) or average cost. Our inventories would have been approximately $3.9 million higher if the LIFO inventories were valued at average cost as of December 31, 2005.

Property, plant and equipment. We principally use the units of production method of depreciation for machinery and equipment. This method amortizes the cost of machinery and equipment over the estimated units that will be produced during its estimated useful life.

Stock options. We have chosen to report our stock based compensation using the intrinsic value method prescribed by Accounting Principles Board (APB) Opinion No. 25, “Accounting for Stock Issued to Employees” under which no compensation cost for stock options is recognized for stock options granted at or above fair market value. As permitted through 2005, we have applied only the disclosure provisions of Statement of Financial Accounting Standards (SFAS) No. 123, “Accounting for Stock-Based Compensation” which established a fair value approach to measuring compensation expense related to employee stock compensation plans. Had compensation expense for our stock-based compensation plans been determined based upon the fair value at the grant dates under those plans consistent with SFAS No. 123, our net income would have been lower. For 2005, had we recorded this compensation expense, our net income would have been lower by $1.9 million. In 2004, the FASB issued SFAS No. 123R, which will require us to use the fair value method beginning in 2006. The impact of the adoption of SFAS No.123R is discussed further in Note 1 of the Notes to the financial statements included in item 8 of this report.

SIGNIFICANT ACCOUNTING ESTIMATES AND JUDGMENTS

Throughout the preparation of the financial statements, we employ significant judgments in the application of accounting principles and methods. These judgments are primarily related to the assumptions used to arrive at various estimates. For 2005, these significant accounting estimates and judgments include:

Legal Contingencies. Our estimates of loss contingencies for legal proceedings are based on various judgments and assumptions regarding the potential resolution or disposition of the underlying claims and associated costs. In making judgments and assumptions regarding legal contingencies for ongoing class action settlements, we consider, among other things, discernible trends in the rate of claims asserted and related damage estimates and information obtained through consultation with statisticians and economists, including statistical analyses of potential outcomes based on experience to date and the experience of third parties who have been subject to product-related claims judged to be comparable. Due to the numerous variables associated with these judgments and assumptions, both the precision and reliability of the resulting estimates of the related loss contingencies are subject to substantial uncertainties. We regularly monitor our estimated exposure to these contingencies and, as additional information becomes known, may change our estimates significantly.

Workers’ Compensation Self-Insurance Liabilities. We are self-insured for workers’ compensation in most U.S. states. The liability recorded in our financial statements for self-insured workers’ compensation claims is based on the estimates of a third party administrator of the future liability based on the specific

22

facts and circumstances of each specific claim at any point in time. We do not use actuarial data from our past workers’ compensation claims history or general industry experience to project the growth of workers’ compensation claims over time. Had we done so, our workers’ compensation liabilities might have been higher than the amount we currently have recorded, although we cannot presently estimate by how much.

Environmental Contingencies. Our estimates of loss contingencies for environmental matters are based on various judgments and assumptions. These estimates typically reflect judgments and assumptions relating to the probable nature, magnitude and timing of required investigation, remediation and/or monitoring activities and the probable cost of these activities, and in some cases reflect judgments and assumptions relating to the obligation or willingness and ability of third parties to bear a proportionate or allocated share of the cost of these activities, including third parties who purchased assets from us subject to environmental liabilities. We consider the ability of third parties to pay their apportioned cost when developing our estimates. In making these judgments and assumptions related to the development of our loss contingencies, we consider, among other things, the activity to date at particular sites, information obtained through consultation with applicable regulatory authorities and third-party consultants and contractors and our historical experience at other sites that are judged to be comparable. Due to the numerous variables associated with these judgments and assumptions, and the effects of changes in governmental regulation and environmental technologies, both the precision and reliability of the resulting estimates of the related contingencies are subject to substantial uncertainties. We regularly monitor our estimated exposure to environmental loss contingencies and, as additional information becomes known, may change our estimates significantly. At December 31, 2005, we excluded from our estimates approximately $1.6 million of potential environmental liabilities that we estimate will be allocated to third parties pursuant to existing and anticipated future cost sharing arrangements.