UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

_________________________________________________________________

FORM 10-K

(Mark One)

For the fiscal year ended October 1, 2021

OR

For the transition period from ____ to ____

Commission File No. 1-7463

_________________________________________________________________

| (State or other jurisdiction of incorporation or organization) | (IRS Employer identification number) | |||||||||||||

| (Address of principal executive offices) | (Zip Code) | |||||||||||||

(214 ) 583 – 8500

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

_________________________________________________________________

| Title of Each Class | Trading Symbol(s) | Name of Each Exchange on Which Registered | |||||||||

| $1 par value | |||||||||||

Securities registered pursuant to Section 12(g) of the Act: None

_________________________________________________________________

Indicate by check-mark if the Registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act: ☒ Yes ☐ No

Indicate by check-mark if the Registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. ☐ Yes ☒ No

Indicate by check-mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. ☒ Yes ☐ No

Indicate by check-mark whether the Registrant: has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the Registrant was required to submit such files). ☒ Yes ☐ No

Indicate by check-mark whether the Registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See the definitions of “large accelerated filer”, “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| ☒ | Accelerated filer | ☐ | ||||||||||||||||||

| Non-accelerated filer | ☐ | Smaller reporting company | ||||||||||||||||||

| Emerging growth company | ||||||||||||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management's assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☒

Indicate by check-mark whether the Registrant is a shell company (as defined in Rule 12b-2 of the Act) ☐ Yes ☒ No

There were 128,948,685 shares of common stock outstanding as of November 12, 2021. The aggregate market value of the Registrant’s common equity held by non-affiliates was approximately $16.9 billion as of April 2, 2021, based upon the last reported sales price on the New York Stock Exchange on that date.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the Registrant’s definitive proxy statement to be issued in connection with its 2022 annual meeting of shareholders are incorporated by reference into Part III of this Annual Report on Form 10-K where indicated.

JACOBS ENGINEERING GROUP INC.

Fiscal 2021 Annual Report on Form 10-K

Table of Contents

| Item | Page No. | |||||||||||||||||||

| Item 1. | Page 3 | |||||||||||||||||||

| Item 1A. | Page 21 | |||||||||||||||||||

| Item 1B. | Page 46 | |||||||||||||||||||

| Item 2. | Page 46 | |||||||||||||||||||

| Item 3. | Page 46 | |||||||||||||||||||

| Item 4. | Page 46 | |||||||||||||||||||

| Item 5. | Page 47 | |||||||||||||||||||

| Item 6. | Page 48 | |||||||||||||||||||

| Item 7. | Page 48 | |||||||||||||||||||

| Item 7A. | Page 64 | |||||||||||||||||||

| Item 8. | Page 64 | |||||||||||||||||||

| Item 9. | Page 64 | |||||||||||||||||||

| Item 9A. | Page 64 | |||||||||||||||||||

| Item 9B. | Page 66 | |||||||||||||||||||

| Item 10. | Page 67 | |||||||||||||||||||

| Item 11. | Page 67 | |||||||||||||||||||

| Item 12. | Page 67 | |||||||||||||||||||

| Item 13. | Page 67 | |||||||||||||||||||

| Item 14. | Page 67 | |||||||||||||||||||

| Item 15. | Page 68 | |||||||||||||||||||

Page 71 | ||||||||||||||||||||

Page 2

PART I

FORWARD-LOOKING STATEMENTS

In addition to historical information, this Annual Report on Form 10-K contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. Forward-looking statements are statements that do not directly relate to any historical or current fact. When used herein, words such as "expects," "anticipates," "believes," "seeks," "estimates," "plans," "intends," “future,” “will,” “would,” “could,” “can,” “may,” and similar words are intended to identify forward-looking statements. Examples of forward-looking statements include, but are not limited to, statements we make concerning the potential continued effects of the COVID-19 pandemic on our business, financial condition and results of operations and our expectations as to our future growth, prospects, financial outlook and business strategy for fiscal 2022 or future fiscal years and the anticipated benefits of the strategic investment in PA Consulting. You should not place undue reliance on these forward-looking statements. Although such statements are based on management’s current estimates and expectations and/or currently available competitive, financial, and economic data, forward-looking statements are inherently uncertain and you should not place undue reliance on such statements as actual results may differ materially. We caution the reader that there are a variety of risks, uncertainties and other factors that could cause actual results to differ materially from what is contained, projected or implied by our forward-looking statements.. Such factors include the magnitude, timing, duration and ultimate impact of the COVID-19 pandemic, including the emergence and spread of variants of COVID-19 and any resulting economic downturn on our results, prospects and opportunities;, measures or restrictions imposed by governments and health officials in response to the pandemic, including the requirement for vaccination of our workforce, or if such orders, measures or restrictions are re-imposed after being lifted or eased, including as a result of increases in cases of COVID-19; the effectiveness and distribution of vaccines or treatments for COVID-19, the timing and scope of any government stimulus programs enacted in response to the impacts of the COVID-19 pandemic, including, but not limited to, any additional infrastructure-related stimulus programs, and the timing of the award of projects and funding under the Infrastructure Investment and Jobs Act signed into law by President Biden on November 15, 2021. The impact of such matters includes, but is not limited to, the possible reduction in demand for certain of our services and the delay or abandonment of ongoing or anticipated projects due to the financial condition of our clients and suppliers or to governmental budget constraints or changes to governmental budgetary priorities; the inability of our clients to meet their payment obligations in a timely manner or at all; potential issues and risks related to a significant portion of our employees working remotely; illness, travel restrictions and other workforce disruptions that have, and could continue to, negatively affect our supply chain and our ability to timely and satisfactorily complete our clients’ projects; difficulties associated with hiring of additional employees; and the inability of governments in certain of the countries in which we operate to effectively mitigate the financial or other impacts of the COVID-19 pandemic on their economies and workforces and our operations therein. The foregoing factors and potential future developments are inherently uncertain, unpredictable and, in many cases, beyond our control. For a description of these and additional factors that may occur that could cause actual results to differ from our forward-looking statements, see Item 1A— Risk Factors below. We undertake no obligation to release publicly any revisions or updates to any forward-looking statements. We encourage you to read carefully the risk factors described herein and in other documents we file from time to time with the United States Securities and Exchange Commission (the "SEC").

Unless the context otherwise requires, all references herein to "Jacobs" or the "Registrant" are to Jacobs Engineering Group Inc. and its predecessors, and references to the "Company", "we", "us" or "our" are to Jacobs Engineering Group Inc. and its consolidated subsidiaries.

Item 1. BUSINESS

At Jacobs, we’re challenging today to reinvent tomorrow by solving the world’s most critical problems for thriving cities, resilient environments, mission-critical outcomes, operational advancement, scientific discovery and cutting-edge manufacturing, turning abstract ideas into realities that transform the world for good. Leveraging a talent force of approximately 55,000, Jacobs provides a full spectrum of professional services including consulting, technical, scientific and project delivery for the government and private sector.

Our deep global domain knowledge – applied together with the latest advances in technology – are why customers large and small choose to partner with Jacobs. We operate in two lines of business areas: Critical Mission Solutions and People & Places Solutions, as well as a third business segment as a result of our majority investment in PA Consulting Group Limited ("PA Consulting").

Page 3

Our three-year accelerated profitable growth strategy launched at our Investor Day in February 2019 focused on innovation and continued transformation to build upon our position as the leading solutions provider for our clients. Setting the wheels in motion for our current path, this transformation most recently included acquiring a 65% stake in PA Consulting. Recent acquisitions of John Wood Group’s nuclear business and The Buffalo Group ("Buffalo Group") further position us as a leader in high-value government services and technology-enabled solutions.

We are now focused on broadening our leadership in sustainable, high growth sectors. As part of our strategy, our new brand promise: Challenging today. Reinventing tomorrow. signals our transition to a global technology-forward solutions company. We began trading as “J” on the New York Stock Exchange in December 2019, and in March 2021 our Global Industry Classifications Standard (GICS®) code changed to Research & Consulting Services. Our Focus 2023 Transformation Office is charged with driving further innovation, delivering value-creating solutions for our clients and leveraging an integrated digital and technology strategy to improve our efficiency and effectiveness, ultimately freeing up valuable time and resources for reinvestment in our people.

Jacobs is poised to launch a new three-year strategy that builds on our success over the past three years and takes advantage of a new lens crafted from the incredible pace of change in the world and in our markets. Our new strategy will be driven by our values and reflective of our vision of becoming a company like no other.

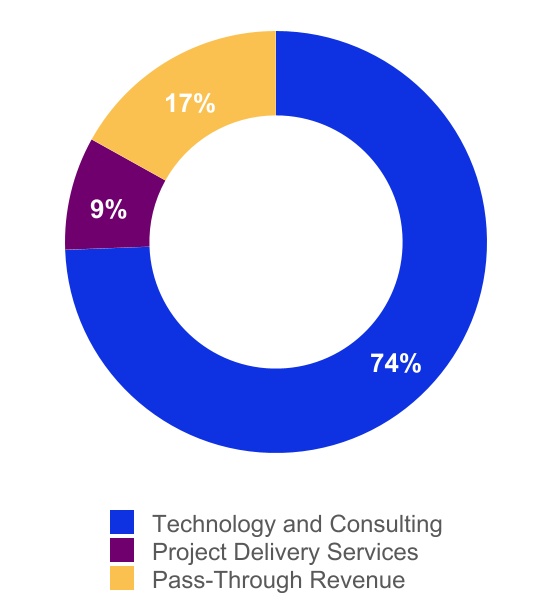

Revenue by Type (Fiscal Year 2021)

Technology and Consulting includes engineering and design, cybersecurity, data analytics, systems and software application integration services and consulting, enterprise and mission IT services, nuclear services, enterprise level operations and maintenance and other highly technical consulting solutions within Critical Mission Solutions (CMS) and data analytics, artificial intelligence and automation, software development as well as digitally-driven engineering and design, consulting, planning and architecture, program management and other highly technical consulting solutions within People & Places Solutions (P&PS). PA Consulting (PA), in which Jacobs has invested a 65% stake, offers end-to-end innovation, accelerating new growth ideas from concept, through design, development, and to commercial success and revitalizing organizations, building the leadership, culture, systems and processes to make innovation a reality.

Project Delivery Services includes management and execution of wind-tunnel design-build projects in CMS and progressive design-build for water and construction management for our Advanced Facilities business in P&PS. We believe these services are lower risk.

Pass-through Revenue includes P&PS procurement activities and revenue where we are acting as principal for subcontract labor or third-party materials and equipment and are consequently reflected in both revenues and costs.

Page 4

Challenging today. Reinventing tomorrow

Our values continue to guide our behaviors, relationships and outcomes - allowing us to act as one company and unify us worldwide when interacting with our clients, employees, communities and shareholders.

•We do things right. We always act with integrity – taking responsibility for our work, caring for our people and staying focused on safety and sustainability. We make investments in our clients, people and communities, so we can grow together.

•We challenge the accepted. We know that to create a better future, we must ask the difficult questions. We always stay curious and are not afraid to try new things.

•We aim higher. We do not settle – always looking beyond to raise the bar and deliver with excellence. We are committed to our clients by bringing innovative solutions that lead to profitable growth and shared success.

•We live inclusion. We put people at the heart of our business. We have an unparalleled focus on inclusion, with a diverse team of visionaries, thinkers and doers. We embrace all perspectives, collaborating to make a positive impact.

These values underpin our three-pillar strategy to become the employer of choice, deliver connected and sustainable solutions, and leverage technology-enabled execution.

Page 5

We do things right

From the way we operate our business, to the work we perform with clients and other organizations, we look at ways we can make a positive environmental, societal and economic difference for our people, businesses, governments and communities around the world.

PlanBeyondSM 2.0 is our enhanced sustainable business strategy that propels the integration of sustainability throughout our operations and client solutions in alignment with the United Nations Sustainable Development Goals (UN SDGs).

Leadership on climate response and social value

Detailed in our Carbon Neutrality Commitment, we became carbon neutral for our operations and business travel in 2020, and we are now focused on fulfilling our science-based carbon-reduction targets for our direct and indirect emissions.

Our ESG Disclosures Report shares our Environmental, Social and Governance (ESG) performance, reported in alignment with the Sustainability Accounting Standards Board (SASB) framework.

Our partnership with Simetrica (a U.K.-based organization that specializes in social value measurement and well-being analysis) enables us to help clients understand how they can transform local, city and regional decision-making – identifying innovative, inclusive and ethical investments that will drive social change, spread prosperity and meet the growing challenges facing communities.

Jacobs. A world where you can

We put people at the heart of our business: we are a merit-based organization that is inclusive and diverse; we aim to continually recruit and develop the best talent.

We are building an inclusive and diverse culture to provide a solid foundation for selecting, developing and retaining the best and brightest minds at Jacobs. Our eight Jacobs Employee Networks (JENs) play a critical role in attracting new talent into our business, helping to shape our recruiting strategies, our science, technology, engineering, arts and math (STEAM) programs, and our accessibility practices.

Conducting our business with integrity

Jacobs' ethics and Code of Conduct are rooted in our values and provide the standards and support to help us successfully navigate issues, make the right decisions and conduct our business with the integrity that reflects our heritage and ethical reputation. We hold our suppliers and business partners to the same standards.

Our culture of caring

As global challenges to our security, well-being and ability to operate evolve, our BeyondZero® strategy continues to drive a safer, more secure, healthier, and more resilient future for our Jacobs family. We stay focused on managing HSE and security risks effectively and leveraging our Culture of Caring℠ to deliver the best outcomes for our people, the environment, our clients, our communities and our shareholders. And through our mental health matters program, we empower our workforce, so they know they work in an environment where their mental health and well-being is the top priority and where everyone can "bring their best whole self to work."

Supporting our communities

We focus on putting our values into practice. Around the world, our people craft solutions that affect the way people live; helping to improve social, environmental and economic resiliency. As part of our PlanBeyond 2.0 sustainability strategy, the Collectively℠ program (our Global Giving and Volunteering program) governs and centralizes our giving strategy and budget and provides a user-friendly way for employees to donate and volunteer.

Page 6

We challenge the accepted

To us, everything we do – whether tackling water scarcity, aging infrastructure, access to life-saving therapies or sophisticated cyberattacks – is more than a job. We work every day to make the world better for all.

For us, innovation means creating and delivering value and Beyond IfSM is our award-winning global innovation program instilling and sustaining our innovation culture. It represents our creativity and agility to challenge the accepted, with the domain expertise to push beyond our boundaries and deliver for today and into tomorrow. We act to turn ideas into reality and create outcomes that deliver value for our clients and society at large.

We aim higher

We take on some of the world’s biggest challenges, bringing a different way of thinking to everything we do, challenging the status quo and questioning what others might accept. We craft solutions that affect the way people live. From first-of-its-kind environmental cleanup efforts, helping communities adapt and thrive to retrofitting vaccine facilities to protect public health, we solve for better, never losing sight of our responsibility to each other.

The table below highlights key focus areas where we combine our deep domain knowledge with the latest advances in technology to deliver solutions to solve our customer's most complex challenges.

BeyondExcellence℠ is our global program focused on quality, performance excellence, continual improvement and recognizing those who set the new standard through our awards program. Our BeyondExcellence Awards celebrate those who raise the bar and deliver the extraordinary with excellence.

We live inclusion

At Jacobs, we understand that inclusion means going beyond statements, commitments and initiatives to take tangible action that drives meaningful, measurable change both in our company and in the communities that we serve. It means

Page 7

creating a workplace where our differences are not just accepted but are celebrated and harnessed to bring the innovative, extraordinary solutions to life that our clients demand from us. It means creating a culture of belonging where everyone can thrive — a culture that we call TogetherBeyond℠.

Our eight Jacobs Employee Networks (JENs) promote inclusion and equality, not only within Jacobs but with our clients, potential recruits and within the communities that we serve. The JENs are employee-led and organized, partnering with leadership to shape an inclusive organization and ensure everyone feels that they belong.

Our global Action Plan for Advancing Justice and Equality sets out actionable initiatives and measurable objectives to address racial inequalities both within Jacobs and in communities across the world. The plan is about achieving true equality for all our employees current and future, with a focus on empowering our Black employees to advance and achieve at Jacobs. It's about doing our part as a global leader to educate and change the culture in our communities — reaching future talent early to highlight and celebrate their potential.

We maintain agile and disciplined capital deployment

M&A and Divestitures

Consistent with our profitable growth strategy, Jacobs pursues acquisitions, divestitures, strategic investments and other transactions to maximize long-term value by continuing to reshape its portfolio to higher value solutions and accelerating its profitable growth strategy. The company has made the following recent acquisitions, strategic investments and divestitures:

Page 8

•On November 19, 2021, Jacobs consummated its previously announced acquisition of BlackLynx ("BlackLynx"). Pursuant to and subject to the terms and conditions of Agreement and Plan of Merger (the “Merger Agreement”), Jacobs acquired all of BlackLynx's outstanding shares of common stock, in a transaction valued at up to $257.5 million, on a cash-free, debt-free basis, including base consideration of $250 million, and a potential earn-out payment of up to $7.5 million. The amount of any earnout payment will depend on BlackLynx achieving certain revenue and gross margin thresholds in calendar year 2022. The purchase price was paid in cash and is subject to customary post-closing adjustments.

•On March 2, 2021, Jacobs completed the strategic investment of a 65% interest in PA Consulting, a UK-based leading innovation and transformation consulting firm. The total consideration paid by the Company was $1.7 billion, funded through cash on hand, a new term loan and draws on the Company's existing revolver. The remaining 35% interest is held by PA Consulting employees.

•On November 24, 2020, Jacobs completed the acquisition of Buffalo Group, a leader in advanced cyber and intelligence solutions.

•On March 6, 2020, Jacobs acquired the nuclear consulting, remediation and program management business of John Wood Group ("John Wood Group" or "Wood Group"), a U.K.-based energy services company.

•On June 12, 2019, Jacobs acquired The KeyW Holding Corporation (“KeyW”), a U.S.-based national security technology solutions provider to the intelligence, cyber, and counterterrorism communities.

•On April 26, 2019, Jacobs completed the sale of its Energy, Chemicals and Resources ("ECR") business to Worley Limited, a company incorporated in Australia ("Worley"), for a purchase price of $3.4 billion consisting of (i) $2.8 billion in cash plus (ii) 58.2 million ordinary shares of Worley, subject to adjustments for changes in working capital and certain other items (the “ECR sale”). ECR provided engineering and construction services mainly for energy, chemicals and resources sectors. With the sale of ECR, the Company has exited direct hire construction and fixed price lump sum energy-related construction.

•On December 15, 2017, Jacobs acquired CH2M, a provider of consulting and other services in the water, environmental, transportation and nuclear remediation sectors.

Share Repurchases

During fiscal 2021, the Company repurchased $274.9 million in shares.

Shareholder Dividends

During fiscal 2021, the Company paid dividends of $.19 per share in the first quarter and $.21 per share in the second, third and fourth quarters.

Impact of COVID-19 on Our Business

In fiscal 2021, demand for certain of our services, including those supporting health care relief efforts relating to COVID-19, increased as a result of COVID-19. Notwithstanding our continuing critical operations, COVID-19 negatively impacted parts of our business, and may have further adverse impacts on our continued operations, including those listed and discussed in Item 1A, Risk Factors included in this Annual Report on Form 10-K. Looking ahead, we have developed contingency plans to reduce costs further if the situation further deteriorates or lasts longer than current expectations. We continue to actively monitor the situation and may take further actions that alter our business operations as may be necessary or appropriate for the health and safety of employees, contractors, customers, suppliers or others or as required by international, federal, state or local authorities.

Based on current estimates, we expect the impact of COVID-19 to continue through fiscal 2022, although to a lesser degree than what was seen in fiscal 2021 and 2020. Although this business disruption is expected to be temporary, significant uncertainty exists concerning the magnitude, duration and impacts of the COVID-19 pandemic, including with regard to the effects on our customers, customer demand for our services and supply chain. Accordingly, actual results for future fiscal periods could differ materially versus current expectations and current results and financial condition discussed herein may not be indicative of future operating results and trends.

Looking forward to the future of work, we are embracing and rethinking how we will work differently - honing our capabilities to better help our clients adjust, innovate and implement. Our reimagined solutions drive resilient outcomes now through the pandemic to what comes next as the world changes and we face other unprecedented challenges.

Page 9

For a discussion of risks and uncertainties related to COVID-19, including the potential impacts on our business, financial condition and results of operations, see Item 1A - Risk Factors.

Page 10

Lines of Business

The services we provide fall into the following two lines of business (LOB): Critical Mission Solutions (CMS), People & Places Solutions (P&PS) and a majority investment in PA Consulting (PA), which are also the Company’s reportable segments. For additional information regarding our segments, including information about our financial results by segment and financial results by geography, see Note 20 - Segment Information of Notes to Consolidated Financial Statements beginning on page F-1 of this Annual Report on Form 10-K.

Critical Mission Solutions (CMS)

Our Critical Mission Solutions line of business provides a full spectrum of cyber, data analytics, systems and software application integration services and consulting, enterprise level operations and maintenance and mission IT, engineering and design, enterprise operations and maintenance, program management, and other highly technical consulting solutions to government agencies as well as commercial customers and international markets. Our representative clients include the U.S. Department of Defense (DoD), the Combatant Commands, the U.S. Intelligence Community, NASA, the U.S. Department of Energy (DoE), U.K. Ministry of Defence, the U.K. Nuclear Decommissioning Authority (NDA), and the Australian Department of Defence, as well as private sector customers mainly in the aerospace, automotive, energy and telecom sectors.

Serving mission-critical end markets

Critical Mission Solutions serves broad sectors, including U.S. government services, cyber, nuclear, commercial and international sectors.

Fiscal Year 2021

The U.S. Government is the world’s largest buyer of technical services, and in fiscal 2021, approximately 74% of CMS’s revenue was earned from serving the DoD, Intelligence Community and Federal Civilian governmental entities.

Trends affecting our government clients include information warfare, cyber, IT modernization, space exploration and intelligence, defense systems and intelligent asset management, which are driving demand for our highly technical solutions.

Page 11

Another trend we are witnessing is an increase in the capabilities of unmanned aircraft and hypersonic weapons, which is impacting both offensive and defensive spending priorities among our clients and is a driver for next generation solutions such as C5ISR (command, control, communications, computer, combat systems, intelligence, surveillance and reconnaissance) and advanced aeronautical testing, respectively. We are also seeing an increase in space exploration initiatives both from the U.S. government, such as NASA’s Artemis program to return to the moon in 2024, as well as the commercial sector.

Within the nuclear sector, our customers have decades-long initiatives to manage, upgrade, decommission and remediate existing energy infrastructure and nuclear defense facilities.

Our international customers, which accounted for 18% of fiscal 2021 revenue, have also increased demand for our IT and cybersecurity solutions and nuclear projects, and the U.K. Ministry of Defence continues to focus on accelerating its strategic innovative and technology focused initiatives.

Leveraging our base market of offering valued technical services to U.S. government customers, CMS also serves commercial markets. In fiscal 2021, approximately 8% of CMS’s revenue was from various U.S. commercial sectors, including the telecommunications sector, which anticipates a large cellular infrastructure build-out from 4G to 5G technology. And like our government facility-based clients, our commercial manufacturing clients are seeking ways to reduce maintenance costs and optimize their facilities with network connected facilities and equipment to optimize operational systems, which we refer to as Intelligent Asset Management.

Page 12

People & Places Solutions (P&PS)

Jacobs' People & Places Solutions line of business provides end-to-end solutions for our clients’ most complex challenges – whether climate change, energy transition, connected mobility, integrated water management, smart cities or vaccine manufacturing. In doing so, we incorporate the full spectrum of data science and technology-enabled toolsets within a people-centric solution development and delivery framework. We embrace inclusive engagement of partners and stakeholders and generate enduring social equity/value through consulting, planning, architecture, design and engineering project outcomes, as well as long-term operation of facilities and infrastructure. Solutions may be delivered as standalone engagements or through comprehensive program management that integrates disparate workstreams to yield additional benefits not attainable through project-by-project implementation. We also provide progressive design-build and construction management at-risk delivery solutions in targeted markets.

Our clients include national, state and local government in the U.S., Europe, U.K., Middle East, Australia, New Zealand and Asia, as well as multinational private sector clients throughout the world.

Fiscal Year 2021

Serving broad industry sectors that support people and places

Aging infrastructure; climate action; urbanization; water, food and energy security; global supply chains; pandemic preparedness and response; environmental, social, and corporate governance (ESG); and digital transformation are driving new challenges and opportunities for our clients. These drivers are highlighting the need for holistic, integrated technology solutions that draw on the domain knowledge in the multidisciplinary consulting and delivery expertise of our global workforce. For example, an airport is no longer simply aviation infrastructure but is now a smart city with extensive operational, cybersecurity and autonomous mobility requirements, as well as the contactless travel requirements necessary to best manage COVID-19. Master planning for a city now requires advanced analytics to plan for climate adaption and next-generation mobility as well as revenue generating fiber infrastructure. The future of nearly all water infrastructure will be highly technology-enabled, leveraging solutions with digital twins, predictive analytics and smart metering technology to ensure we're giving communities, industries and regions the secure water resource they need to flourish and expand.

Page 13

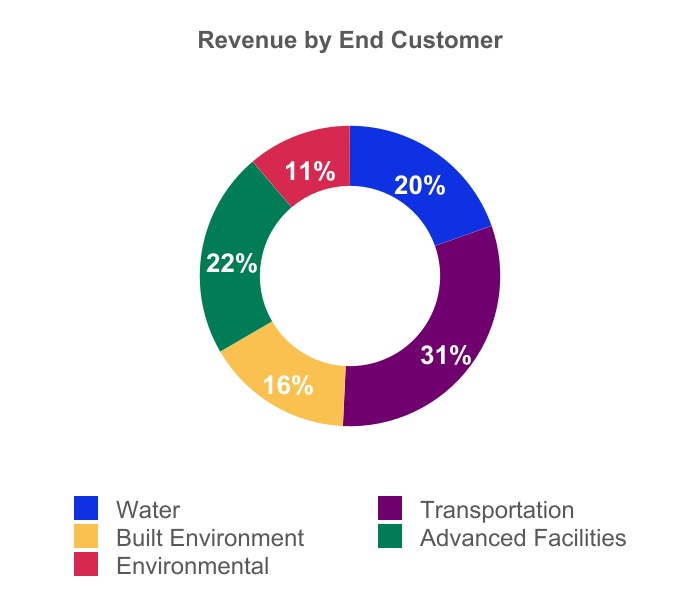

This increase in technology requirements is a key factor in our organic growth strategy as well as our recent acquisitions, strategic investments and divestitures. Our business model is evolving to provide a broader spectrum of digital- and technology-enabled solutions to address our infrastructure clients' challenges with less exposure to craft construction services. Our focus on the five core sectors of Transportation, Water, Built Environment, Environmental and Advanced Facilities provides us with the ability to leverage our expansive domain expertise across all global markets, enabling truly end-to-end connected solutions for our clients' most complex major projects and programs, including Expo 2020 Dubai, the Thames Estuary Asset Management (TEAM 2100) and the LaGuardia Airport Redevelopment.

A strong foundation of data-rich innovative solutions is woven into every project that we deliver. This may include Jacobs-developed proprietary software that employs an array of technical expertise to enable the most efficient, effective and predictable solutions for our clients.

PA Consulting (PA)

Jacobs invested in a 65% stake in PA, the consultancy that is Bringing Ingenuity to Life. Its diverse teams of experts combine innovative thinking and breakthrough use of technologies to progress further, faster. PA’s clients adapt and transform and achieve enduring results. An innovation and transformation consultancy, PA's roughly 3,300 employees work across seven sectors: consumer and manufacturing, defense and security, energy and utilities, financial services, government, health and life sciences, and transport. PA people are strategists, innovators, designers, consultants, digital experts, scientists, engineers and technologists. The team operates globally from offices across the U.K., U.S., Nordics and the Netherlands.

PA offers end-to-end innovation, accelerating new growth ideas from concept, through design, development, and to commercial success, and revitalizing organizations, building the leadership, culture, systems and processes to make innovation a reality. The company has a diverse mix of private and public sector clients, from global household names to start-ups, to national and local public services.

Jacobs and PA recognize that unprecedented changes in society and technology are creating new opportunities to make a positive impact, and together, the companies are supporting clients to address five key trends: product and service innovation; the future of work; sustainability and climate change; the quest to lead healthier lives; and the challenges of keeping people (and the organizations they work for) safe. PA’s distinct brand, market positioning and competitive differentiation positions the company well to help clients respond and seize new opportunities.

PA led the efforts to design, manufacture and distribute thousands of lifesaving ventilators as part of the U.K. Ventilator Challenge, and has continued to support the U.K. Government’s COVID-19 response throughout 2021. Other work during 2021 includes re-designing the U.K. Army’s Operating Model, working as the Home Office’s Software Engineering partner for border safety, and working with the U.K. MOD’s Defence Science & Technology Laboratory and the Danish National Genome Center.

Page 14

Recently, PA has been appointed by the U.K. Government to design an iconic electric vehicle charge point to accelerate the transition to electric vehicles. And PA and Jacobs together announced a joint framework win, with the U.K.’s Department for Environment, Food & Rural Affairs, for business transformation and delivery.

PA has seen growth projects across key industries within the private sector, including Consumer & Manufacturing, Health & Life Sciences, Transportation and Financial Services.

Energy, Chemicals and Resources (ECR)

ECR Disposition

On April 26, 2019, Jacobs completed the sale of its Energy, Chemicals and Resources (ECR) business to Worley Limited, a company incorporated in Australia (Worley), for a purchase price of $3.4 billion consisting of (i) $2.8 billion in cash plus (ii) 58.2 million ordinary shares of Worley, subject to adjustments for changes in working capital and certain other items (the ECR sale).

As a result of the ECR sale, substantially all ECR-related assets and liabilities were sold (the "Disposal Group"). We determined that the disposal group should be reported as discontinued operations in accordance with ASC 210-05, Discontinued Operations because their disposal represents a strategic shift that had a major effect on our operations and financial results. As such, the financial results of the ECR business are reflected in our Consolidated Statements of Earnings as discontinued operations for all periods presented. Additionally, assets and liabilities of the ECR business were reflected as held-for-sale in the Consolidated Balance Sheets through September 27, 2019. As of the year ended October 2, 2020, all of the ECR business to be sold under the terms of the sale has been conveyed to Worley and as such, no amounts remained held for sale. For further discussion, see Note 16- Sale of Energy, Chemicals and Resources ("ECR") Business to the consolidated financial statements.

Significant Customers

The following table sets forth the percentage of total revenues earned directly or indirectly from agencies of the U.S. federal government for each of the last three fiscal years:

| 2021 | 2020 | 2019 | ||||||||||||

| 33% | 33% | 27% | ||||||||||||

Given the percentage of total revenue derived directly from the U.S. federal government, the loss of U.S. federal government agencies as customers could have a material adverse effect on the Company. In addition, any or all of our government contracts could be terminated, we could be suspended or debarred from all government contract work, or payment of our costs could be disallowed. Approximately 83% of revenue derived directly from the U.S. federal government is in the CMS segment. For more information on risks relating to our government contracts, see Item 1A - Risk Factors.

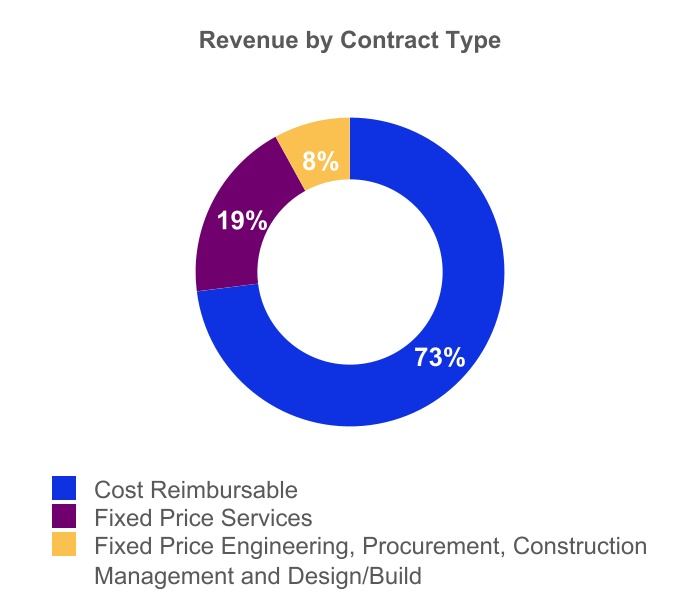

Contracts

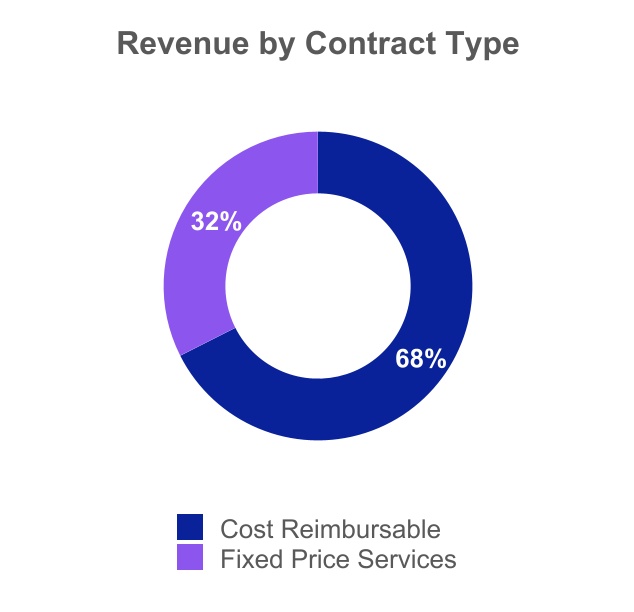

While there is considerable variation in the pricing provisions of the contracts we undertake, our contracts generally fall into two broad categories: cost-reimbursable and fixed-price. The following table sets forth the percentages of total revenues represented by these types of contracts for each of the last three fiscal years:

| 2021 | 2020 | 2019 | |||||||||||||||

| Cost-reimbursable | 76% | 76% | 76% | ||||||||||||||

| Fixed-price, limited risk | 18% | 17% | 18% | ||||||||||||||

| Fixed-price, at risk | 6% | 7% | 6% | ||||||||||||||

In accordance with industry practice, most of our contracts (including those with the U.S. federal government) are subject to termination at the discretion of the client, which is discussed in greater detail in Item 1A - Risk Factors. In such situations, our contracts typically provide for reimbursement of costs incurred and payment of fees earned through the date of termination.

Page 15

Cost-Reimbursable Contracts

Cost-reimbursable contracts generally provide for reimbursement of costs incurred plus an amount of profit. The profit element may be in the form of a simple mark-up applied to the labor costs incurred or it may be in the form of a fee, or a combination of a mark-up and a fee. The fee element can also take several forms. The fee may be a fixed amount; it may be an amount based on a percentage of the costs incurred; or it may be an incentive fee based on targets, milestones, or performance factors defined in the contract.

Fixed-Price Contracts

Fixed-price contracts include both “lump sum bid” contracts and “negotiated fixed-price” contracts. Under lump sum bid contracts, we typically bid against competitors based on client-furnished specifications. This type of pricing presents certain inherent risks, including the possibility of ambiguities in the specifications received, problems with new technologies, and economic and other changes that may occur over the contract period. Additionally, it is not unusual for lump sum bid contracts to lead to an adversarial relationship with clients, which is contrary to our relationship-based business model. Accordingly, lump sum bid contracts are not our preferred form of contract. In contrast, under a negotiated fixed-price contract, we are selected as the contractor first and then we negotiate a price with our client. Negotiated fixed-price contracts frequently exist in single-responsibility arrangements where we perform some portion of the work before negotiating the total price of the project. Thus, although both types of contracts involve a firm price for the client, the lump sum bid contract provides the greater degree of risk to us in our services contracts as well as construction. However, because of economies that may be realized during the contract term, both negotiated fixed-price and lump sum bid contracts may offer greater profit potential than other types of contracts. The Company carefully manages the risk inherent in these types of contracts. In recent years, most of our fixed-price work has been either negotiated fixed-price contracts or lump sum bid contracts for design and/or project services, rather than turnkey construction.

Competition

We compete with a large number of companies across the world including technology consulting, federal IT services, aerospace, defense and engineering firms. Typically, no single company or companies dominate the markets in which we provide services and in many cases we partner with our competitors or other companies to jointly pursue projects. AECOM, Booz Allen, CACI, KBR, Leidos, Parsons, SAIC, Tetra Tech, WSP, General Dynamics, Northrop Grumman, Accenture, Stantec, Montrose, Capgemini, Cognizant, DXC Technology, Fluor, 3LHarris, Quanta Services, SNC-Lavalin, IBM, Infosys, Deloitte, KPMG, PwC, ICF International and Huron are some of our competitors. We compete based on the following factors, among others: technical capabilities, reputation for quality, price of services, safety record, availability of qualified personnel, and ability to timely perform work and contract terms.

Human Capital Management

At Jacobs, our people are the heart of our business. With our culture of caring and inclusion as our foundation, we celebrate the differences that drive our collective strength and encourage our employees that there is no limit to who they can be and what we can achieve. Together we deliver extraordinary solutions for a better tomorrow and live by our employee value statement: Jacobs. A world where you can.

As of October 1, 2021, we had a workforce of approximately 55,000 people worldwide, including a contingent workforce of approximately 3,000 people. The breakdown of our employees by region is as follows:

| Region | Percentage of Global Workforce(1) | |||||||

| Americas | 61 | % | ||||||

| Europe (including U.K) | 23 | % | ||||||

| Asia Pacific (including India) | 13 | % | ||||||

| Middle East and Africa | 3 | % | ||||||

| (1) Excludes contingent workforce | ||||||||

Attracting, Engaging and Developing our Workforce

The success of Jacobs is dependent on our ability to hire, retain, engage and leverage highly qualified employees, across the full spectrum of technical, professional, scientific and consulting disciplines. We put the spotlight on ensuring that Jacobs is an employer of choice in every way: we are a merit-based organization that is inclusive and diverse; we are

Page 16

building an inclusive culture where all employees feel they belong. Our culture is the foundation for selecting, developing and retaining the best and brightest minds at Jacobs. Our eight Jacobs Employee Networks play a critical role in attracting new talent into our business, helping to shape our recruiting strategies and policies, our science, technology, engineering, arts and math (STEAM) programs, and our accessibility practices. In fiscal 2021, more than1,900 graduates, interns and apprentices were welcomed to our global team; making a total of approximately 3,500 early career talent working with us.

In fiscal year 2021, our people took the time to share honest, unfiltered feedback in our confidential culture survey. The results were overwhelmingly positive, with the majority of respondents feeling connected to our values, inspired by our culture of integrity, safety, and inclusion — and proud to be part of Jacobs. We shared six priority areas, along with a set of dynamic dashboards, enabling all employees to see survey data relevant to them.

Our unique employee experience platform – e3: engage. excel. elevate. – is not just a system but a mindset for developing our employees through continuous feedback and celebrations, aligning priorities, learning new skills and upskilling knowledge. To date, 97% of our employees have participated in their current annual conversation about their priorities and accomplishments. In fiscal year 2021, we launched 1,696 new courses across ten learning spaces, including our new Advocate & Ally development program. In partnership with the Royal Scottish Geographical Society, we launched the Climate Solutions Accelerator online course to employees to help them understand the role they can play in climate change action and continue to develop the critical green skills and solutions needed for our continually evolving world. We expanded our Executive Leadership Program, developed by Jacobs in partnership with Duke Corporate Education, with 224 of our next level leaders participating in our Amplif(i)3 Program. We accelerated talent development in creating sustainable solutions through our participation in the UN Global Compact Young SDG Innovators program. And, we published our No Harassment, Discrimination, Bullying and Violence Policy on our external Jacobs website.

Focus on Inclusion and Diversity

At Jacobs we have an unparalleled focus on inclusion, with a diverse team of visionaries, thinkers and doers. We embrace all perspectives, collaborating to make a positive impact. Joining, belonging and thriving are Jacobs’ key elements in retaining talent and developing a culture where people want to stay – and a place where you can bring your best, whole self to work.

TogetherBeyond℠ is our approach to living inclusion every day and enabling diversity and equity globally – it is not just about numbers and statistics, but about every one of our people and the collective strength we take from their unique perspectives and ambitions.

Operationalizing TogetherBeyond is supported by the strength of tangible leadership commitment and accountability at Jacobs. Our Board of Directors is now 55% diverse, (race and gender) and our Executive Leadership Team is 67% diverse.

Having a culture of belonging where everyone can join in and thrive allows us to recruit and retain the best global talent and drive innovative solutions for our business, clients and communities. Through TogetherBeyond, we tackle topics that are important to our employees such as equality, unconscious bias and allyship. While providing training and resources to our people is important – over 97% of them have completed our Advocate & Ally inclusion learning program – equally effective are the regular authentic and courageous conversations our grassroots employee networks are creating around these topics.

We are committed to holding all leaders accountable to making sure that broad based diversity is reflected in their own teams, using data analytics to measure our progress with the same rigor and transparency as our financial performance metrics. Inclusive behaviors are now a key formal component of all our leaders’ performance and salary reviews, and all leaders at Vice President level and above are required to mentor two or more junior members of staff, at least one of whom must have different lived a experience from themselves (i.e. on the basis of ethnicity, gender, race, geography, disability, sexuality or veteran status). This framework supports our Global Action Plan for Advancing Justice and Equality and our 2025 aspirational 40:40:20 goal (40% men, 40% women and 20% any gender) — and ensures that we are propelling a new generation of diverse visionary thinkers throughout our company.

Page 17

As of October 1, 2021, our U.S. employees had the following race and ethnicity demographics:

October 1, 2021 | ||||||||

| All U.S. Employees (1) | ||||||||

| White | 70.0 | % | ||||||

| Hispanic / Latinx | 9.3 | % | ||||||

| Black | 8.6 | % | ||||||

| Asian | 7.1 | % | ||||||

| Multiracial | 2.3 | % | ||||||

| American Indian or Alaska Native | 0.5 | % | ||||||

| Native Hawaiian / Other Pacific Islander | 0.4 | % | ||||||

| Not provided | 1.8 | % | ||||||

| (1) Includes U.S. employee population only (excluding approximately 2,000 craft employees) | ||||||||

Our focus on creating equal opportunities within Jacobs, including as to historically underrepresented groups, continues to increase as we deliver on the promises laid out in our Global Action Plan for Advancing Justice and Equality launched in fiscal year 2020.

In partnership with McKinsey, nearly 300 talented employees are participating in their Connected Leaders Academy programs, which seek to create a unique learning environment and safe space for sharing common experiences, helping promising Black, Latinx and Asian employees build their network and become part of a new wave of Jacobs leaders.

Our Black and Latinx employee networks, Harambee and Enlace, continue to lead STEAM outreach efforts in the communities that we serve and are working to bring a new generation of diverse visionaries from underrepresented and underserved groups into the industry.

As of October 1, 2021, our global employees had the following gender demographics:

October 1, 2021 | |||||||||||

| Women | Men | ||||||||||

| All employees | 30.0% | 70.0% | |||||||||

U.S. combined diverse talent (ethnicity & female) was 47.4%. In partnership with our Women’s Network, we launched gender-balanced interview teams, provided flexible working arrangements, improved caregiver leave, rolled out our first domestic violence policy in Australia/NZ, piloted a “Male Champions of Change” allyship program and created “Bridge the Gap”, a program that actively support parents returning to work.

We are taking action in connection with our Prism network to ensure that our LGBTQ+ family can truly “bring their whole best self to work”, establishing gender-neutral restrooms, training HR specialists on transgender guidelines and ensuring U.S. healthcare plans are inclusive.

Through VetNet, our employee network for veterans, their families and current military reserve members, we continue to work to recruit, develop and retain the best military and veteran talent, partnering with key organizations like Hiring Our Heroes, Boots2Roots and HirePurpose. We were proud to receive the HIRE Vets Gold Medallion for Veteran Recruiting.

Our One World employee network continues to celebrate cultures around the globe and to foster global connectivity, nurturing and supporting our diverse employees and clients across all ethnicities and cultures.

Our ACE employee network connects and empowers members living with disability, health challenges or neurodiversity, and those who provide care to others. ACE embraces the social model of disability which aims to identify and remove the social, digital, and physical barriers that create exclusion in the workplace and society in general.

Page 18

Through our Jacobs Careers Network (JCN), we empower every employee to maximize their potential and make Jacobs the industry leader and workplace of choice. JCN organizes and supports career-enriching development and networking opportunities in all our geographies.

Looking ahead, we will continue to focus on inclusion, belonging and diversity by:

•Continuing action through our global Action Plan for Advancing Justice and Equality

•Striving to achieve our aspirational goals of creating a more gender-balanced and a more racially/ethnically diverse workforce around the globe to more appropriately reflect the labor markets and communities in which we live and serve

•Amplifying our culture of belonging and helping all employees see the various communities they can engage with at Jacobs so that everyone has a sense of belonging

•Following through on our six priority areas identified through our global culture survey

•Identifying, developing and promoting allies across Jacobs

Our Employees’ Safety and Well-being

As global challenges to our security, well-being and ability to operate evolve, we stay focused on managing HSE and security risks effectively and leveraging our Culture of Caring℠ to deliver the best outcomes for our people, the environment and our company. Our new BeyondZero® strategy continues to drive a safer, more secure, healthier, and more resilient future for our Jacobs family, our communities and the environment. We are maturing our business continuity program to assure business delivery and resilience in an ever-changing operational environment.

We also continue to demonstrate safety excellence with another year of zero employee fatalities at work and a total recordable incident rate1 of 0.21, compared to the North American Industry Classification System’s most recently reported2 aggregate rate of 0.70.

Our new global well-being strategy integrates physical, mental, financial, social and workplace well-being for Jacobs employees and their families. The strategy includes Jacobs’ One Million Lives, developed in collaboration with global mental health professionals, to provide a free mental health check-in tool with a resources website that enable users to check their own mental health and access proactive strategies for personal mental health development. Over 14,000 One Million Lives check-ins were completed between December 2020 launch and our fiscal year end 2021.

In fiscal 2021, all vice presidents acknowledged and made a commitment to become BeyondZero Ambassadors and establish priorities to deliver the greatest impact through our BeyondZero strategy. More than 2,500 Positive Mental Health Champions (a 35% increase from fiscal year 2020) are now trained to support the mental well-being of our employees and one in every 21 employees is trained as a Positive Mental Health Champion. In addition, we launched Suicide Awareness Training through our e3 Learning.

We are committed to continue our work to create an inclusive and innovative organization and taking action to ensure Jacobs is, and remains, an employer of choice.

1 As at October 15, 2021 and recorded in accordance with OSHA record keeping requirements, but subject to change thereafter due to possible injury/illness classification changes.

2 Cited on October 5th, 2021 via U.S. Bureau of Labor Statistics - Incidence rates of non-fatal occupational injuries and illnesses by industry and case types, 2019 for NAICS code 5413XXX.

Information About Our Executive Officers

The information required by Paragraph (a), and Paragraphs (c) through (g) of Item 401 of Regulation S-K (except for information required by Paragraph (e) of that Item to the extent the required information pertains to our executive officers) and Item 405 of Regulation S-K is set forth under the caption “Members of the Board of Directors” in our definitive proxy statement to be filed with the SEC pursuant to Regulation 14A within 120 days after the close of our fiscal year and is incorporated herein by reference.

Page 19

The following table presents the information required by Paragraph (b) of Item 401 of Regulation S-K.

| Name | Age | Position with the Company | Year Joined the Company | |||||||||||||||||

| Steven J. Demetriou | 63 | Chair and Chief Executive Officer | 2015 | |||||||||||||||||

| Kevin C. Berryman | 62 | President and Chief Financial Officer | 2014 | |||||||||||||||||

| Robert V. Pragada | 53 | President and Chief Operating Officer | 2016 | |||||||||||||||||

| Dawne S. Hickton | 64 | Executive Vice President and President, Critical Mission Solutions | 2019 | |||||||||||||||||

| Patrick X. Hill | 48 | Executive Vice President and President, People & Places Solutions | 1998 | |||||||||||||||||

| Joanne E. Caruso | 61 | Executive Vice President, Chief Legal and Administrative Officer | 2012 | |||||||||||||||||

| William B. Allen, Jr. | 57 | Senior Vice President, Chief Accounting Officer | 2016 | |||||||||||||||||

All of the officers listed in the preceding table serve in their respective capacities at the pleasure of the Board of Directors of the Company.

Mr. Demetriou joined the Company in August 2015. Mr. Demetriou served as Chairman and CEO of Aleris Corporation for 14 years, a global downstream aluminum producer based in Cleveland, Ohio. Over the course of his career, he has gained broad experience with companies in a range of industries including metals, specialty chemicals, oil & gas, manufacturing and fertilizers.

Mr. Berryman joined the Company in December 2014. Mr. Berryman served as EVP and CFO for five years at International Flavors and Fragrances Inc., an S&P 500 company and leading global creator of flavors and fragrances used in a wide variety of consumer products. Prior to that, he spent 25 years at Nestlé in a number of finance roles including treasury, mergers & acquisitions, strategic planning and control.

Mr. Pragada rejoined the Company in February 2016 after serving as President and Chief Executive Officer of The Brock Group since August 2014. From March 2006 to August 2014 Mr. Pragada served in executive and senior leadership capacities with the Company.

Ms. Hickton joined the Company in 2019. Previously, Ms. Hickton served as a member of the Board of Directors of the Company and was the Vice Chair and Chief Executive Officer for eight years at RTI International Metals, Inc., a global supplier of advanced titanium products and services in commercial aerospace, defense, propulsion, medical device and energy markets.

Mr. Hill joined the Company through the SKM acquisition, where he started in 1998. Mr. Hill has served in a number of senior leadership positions crossing multiple sectors and operations throughout Australia, New Zealand, Asia, Europe, the Middle East and the United States. Prior to his appointment as President – People & Places Solutions, Mr. Hill jointly led People & Places Solutions with day-to-day responsibilities for Jacobs' Buildings and Infrastructure global operations outside of North America.

Ms. Caruso joined the Company in 2012. Prior to becoming Executive Vice President, Chief Legal and Administrative Officer, Ms. Caruso was Senior Vice President, Chief Administrative Officer, and previously held the positions of Senior Vice President, Global Human Resources and Vice President, Global Litigation. Prior to joining the Company, Ms. Caruso was a partner in two international law firms, Howrey LLP and Baker & Hostetler LLP.

Mr. Allen joined the Company in October 2016. Mr. Allen served as Vice President, Finance and Principal Accounting Officer at LyondellBasell Industries, N.V. from 2013 to 2016. Prior to that, he was with Albemarle Corporation, where he served as Vice President, Corporate Controller and Chief Accounting Officer from 2009 to 2013 after serving in CFO roles for their Catalysts and Fine Chemistry businesses from 2005 to 2009.

Additional Information

Jacobs was founded in 1947 and incorporated as a Delaware corporation in 1987. We are headquartered in Dallas, Texas, USA. The SEC maintains a site on the Internet that contains reports, proxy and information statements, and other information regarding issuers that file electronically with the SEC. The SEC’s website is http://www.sec.gov. You may also read and download the various reports we file with, or furnish to, the SEC free of charge from our website at www.jacobs.com.

Page 20

Item 1A. RISK FACTORS

We operate in a changing global environment that involves numerous known and unknown risks and uncertainties that could materially adversely affect our business, financial condition and results of operations. The risks described below highlight some of the factors that have affected and could affect us in the future. We may also be affected by unknown risks or risks that we currently think are immaterial. If any such events actually occur, our business, financial condition and results of operations could be materially adversely affected.

Summary Risk Factors

The following is a summary of some of the risks and uncertainties that could materially adversely affect our business, financial condition and results of operations. You should read this summary together with the more detailed description of each risk factor contained below.

Risks Related to Our Operations

•The COVID-19 pandemic, including the measures that international, federal, state and local public health and other governmental authorities implement to address it, have adversely affected, and may continue to adversely affect, our business, financial condition and results of operations.

•Project sites are inherently dangerous workplaces. Failure to maintain safe work sites by us, the owner or others working at the project site can lead to our employees or others becoming injured, disabled or even losing their lives, and exposes us to significant financial losses and reputational harm, as well as civil and criminal liabilities.

•Our results of operations depend on the award of new contracts and the timing of the performance of these contracts.

•We engage in a highly competitive business. If we are unable to compete effectively, we could lose market share and our business and results of operations could be negatively impacted.

•The nature of our contracts, particularly those that are fixed-price, subjects us to risks of cost overruns. We may experience reduced profits or, in some cases, losses if costs increase above budgets or estimates or if the project experiences schedule delays.

•The contracts in our backlog may be adjusted, canceled or suspended by our clients and, therefore, our backlog is not necessarily indicative of our future revenues or earnings. Additionally, even if fully performed, our backlog is not a good indicator of our future gross margins.

•Contracts with the U.S. federal government and other governments and their agencies pose additional risks relating to future funding and compliance.

•Our project execution activities may result in liability for faulty services.

•The outcome of pending and future claims and litigation could have a material adverse impact on our business, financial condition, and results of operations and damage our reputation.

•Our use of joint ventures, partnerships and strategic investments in entities exposes us to risks and uncertainties, many of which are outside of our control

•Employee, agent or partner misconduct, or our overall failure to comply with laws or regulations, could weaken our ability to win contracts, which could result in reduced revenues and profits.

•Our international operations are exposed to additional risks and uncertainties, including unfavorable political developments and weak foreign economies.

•Cyber security or privacy breaches, or systems and information technology interruption or failure could adversely impact our ability to operate or expose us to significant financial losses and reputational harm.

•We are subject to professional standards, duties and statutory obligations on professional reports and opinions we issue, which could subject us to monetary damages.

•If we do not have adequate indemnification for our nuclear services, it could adversely affect our business, financial condition and results of operations.

•Our actual results could differ from the estimates and assumptions used to prepare our financial statements.

•An impairment charge on our goodwill could have a material adverse impact on our financial position and results of operations.

Page 21

•We may be required to contribute additional cash to meet any underfunded benefit obligations associated with retirement and post-retirement benefit plans we manage or for which we have contribution and/or funding obligations.

•Demand for our services is cyclical as the sectors and industries in which our clients operate are impacted by economic downturns, reductions in government or private spending and times of political uncertainty.

•Rising inflation, interest rates, and/or construction costs could reduce the demand for our services as well as decrease our profit on our existing contracts, in particular with respect to our fixed-price contracts.

•Our global presence could give rise to material fluctuations in our income tax rates.

•Our businesses could be materially and adversely affected by events outside of our control.

•Our continued success is dependent upon our ability to hire, retain, and utilize qualified personnel.

•Our business strategy relies in part on acquisitions and strategic investments to sustain our growth. These transactions present certain risks and uncertainties.

•Our professional reputation and relationships with U.S. government agencies are critical to our business, and any harm to our reputation or relationships could decrease the amount of business the U.S. government does with us, which could have a material adverse effect on our business, financial condition and results of operations.

•Our focus on new growth areas for our business entails risks, including those associated with new relationships, clients, talent needs, capabilities, service offerings, and maintaining our collaborative culture and core values.

Risks Related to Regulatory Compliance

•Past and future environmental, health, and safety laws could impose significant additional costs and liabilities.

•If we fail to comply with federal, state, local or foreign governmental requirements, our business may be adversely affected.

•We could be adversely affected by violations of the U.S. Foreign Corrupt Practices Act and similar worldwide anti-bribery laws.

Risks Related to Climate Change

•Climate change and related environmental issues could have a material adverse impact on our business, financial condition and results of operations.

•We may be affected by market or regulatory responses to climate change.

•We may be unable to achieve our climate commitments and targets.

Risks Related to Our Indebtedness

•We rely on cash provided by operations and liquidity under our credit facilities to fund our business. Negative conditions in the credit and financial markets and delays in receiving client payments could adversely affect our cost of borrowing and our business.

•Maintaining adequate bonding and letter of credit capacity is necessary for us to successfully bid on and win some contracts.

Risks Related to Our Common Stock

•Our quarterly results may fluctuate significantly, which could have a material negative effect on the price of our common stock.

•There can be no assurance that we will pay dividends on our common stock.

•In the event we issue stock as consideration for certain acquisitions we may make, we could dilute share ownership, and if we receive stock in connection with a divestiture, the value of stock is subject to fluctuation.

Page 22

Risks Related to Our Operations

The COVID-19 pandemic, including the measures that international, federal, state and local public health and other governmental authorities implement to address it, have adversely affected, and may continue to adversely affect, our business, financial condition and results of operations.

Despite the availability of vaccines in some geographies, COVID-19 continues to spread throughout the United States and globally, including in regions where we have significant operations and personnel, and uncertainties exist as to the efficacy of vaccines against new variants or mutations of COVID-19. To attempt to mitigate the spread of the pandemic, there have been extraordinary and wide-ranging actions taken by international, federal, state and local public health and governmental authorities to contain and combat the outbreak of COVID-19 in regions across the United States and around the world. These actions include quarantines and “stay-at-home” or “shelter-in-place” orders, social distancing measures, travel restrictions, school closures and similar mandates for many individuals in order to substantially restrict daily activities and orders for many businesses to curtail or cease normal operations unless their work is critical, essential or life-sustaining and to require their employees to be vaccinated against COVID-19 as a condition for continued employment. Although there has been an easing of restrictions in certain jurisdictions, some of these restrictions have been reinstated in other jurisdictions, or could be reinstated in the future, to manage a resurgence or new outbreak of COVID-19, including in connection with new variants or mutations of the virus. In addition, the reopening of businesses and economies in certain countries is creating a variety of new challenges, including, for example, higher prices for goods and services, limited availability of products, and disruptions to supply chains. As such, the duration, severity of its effects and ultimate impact to the world’s population and the global economy are still unknown.

The COVID-19 pandemic has adversely affected, and may continue to adversely affect, certain elements of our business, including, but not limited to, the following:

•We have experienced, and may continue to experience, reductions in demand for certain of our services and the delay or abandonment of ongoing or anticipated projects due to our clients’, suppliers’ and other third parties’ diminished financial conditions or financial distress, as well as governmental budget constraints. These impacts are expected to continue or worsen if “stay-at-home”, “shelter-in-place”, social distancing, travel restrictions and other similar orders, measures or restrictions remain in place for an extended period of time or are re-imposed after being lifted or eased. Although we have experienced, and may continue to experience, an increase in demand for certain of our services as a result of new projects that have arisen in response to the COVID-19 pandemic, there can be no assurance that any such increased demand would be sufficient to offset lost or delayed demand.

•Government-sponsored stimulus or assistance programs enacted to-date in the United States and in the foreign countries in which we operate in response to the COVID-19 pandemic have only been available to us or our customers or suppliers on a limited basis and are insufficient to address the full impact of the COVID-19 pandemic. These and other government-sponsored assistance and stimulus programs are subject to renewal, modification or termination by the applicable governing bodies. If any government-sponsored program from which we receive benefits is modified or terminated, our benefits thereunder could decline or cease altogether, which could have a material adverse effect on our business, financial position, results of operations, and/or cash flows.

•Our clients may be unable to meet their payment obligations to us in a timely manner, including as a result of deteriorating financial condition or bankruptcy resulting from the COVID-19 pandemic and resulting economic impacts. Further, other third parties, such as suppliers, subcontractors, joint venture partners and other outside business partners, may experience significant disruptions in their ability to satisfy their obligations with respect to us, or they may be unable to do so altogether.

•While we have begun voluntary phased re-openings in our offices in accordance with guidance provided by government agencies, the majority of our employees are currently still working remotely. Although many of our employees can effectively perform their responsibilities while working remotely, some work is not well-suited for remote work, and that work may not be completed as efficiently as if it were performed on site. Additionally, we may be exposed to unexpected cybersecurity risks and additional information technology-related expenses as a result of these remote working requirements. In addition, our management team has spent, and will likely continue to spend, significant time, attention and resources monitoring the COVID-19 pandemic and seeking to manage its effects on our business and workforce.. A long-term continuation of these restrictions could, among other things, negatively impact employee morale and productivity. Any failure to

Page 23

preserve our culture could harm our future success, including our ability to retain and recruit personnel, innovate and operate effectively and execute on our business strategy.

•Consistent with public health guidance and Executive Order 14042 mandating COVID-19 vaccination for employees of businesses servicing federal contracts, we have announced a Company policy requiring full COVID-19 vaccinations of all employees in the United States and Canada, except for employees who qualify for medical or religious exemptions. This policy, along with the federal vaccine mandate, may result in employee attrition and difficulty securing future labor needs, and could impair our ability to perform certain contractual services, to retain such contracts, and to win new business, all of which could have an adverse effect on our business, results of operations and/or cash flows.

•Illness, travel restrictions or other workforce disruptions could adversely affect our supply chain, our ability to timely and satisfactorily complete our clients’ projects, our ability to provide services to our clients or our other business processes. Even after the COVID-19 pandemic subsides, we could experience a longer-term impact on our operating expenses, including, for example, the need for enhanced health and hygiene requirements or the periodic revival of social distancing or other measures in one or more regions in attempts to counteract future outbreaks.

•We may experience difficulties associated with hiring additional employees or replacing employees, in particular with respect to roles that require security clearances or other special qualifications that may be limited or difficult to obtain, as well as with effectively training and integrating new employees, and in the short term, to do so remotely during the COVID-19 pandemic. Increased turnover rates of our employees could increase operating costs and create challenges for us in maintaining high levels of employee awareness of, and compliance with, our internal procedures and external regulatory compliance requirements, in addition to increasing our recruiting, training and supervisory costs.

•In addition to existing travel restrictions implemented in response to the COVID-19 pandemic, jurisdictions may continue to close borders, impose prolonged quarantines and further restrict travel and business activity, which could materially impair our ability to support our operations and clients (both domestic and international), to source supplies through the global supply chain and to identify, pursue and capture new business opportunities, and which could continue to restrict the ability of our employees to access their workplaces. We also face the possibility of increased overhead or other expenses resulting from compliance with any current and future government orders or other measures enacted in response to the COVID-19 pandemic.

•We operate in many countries around the world, and certain of those countries’ governments may be unable to effectively mitigate the financial or other impacts of the COVID-19 pandemic on their economies and workforces and our operations therein.

The continued global spread of the COVID-19 pandemic and the responses thereto are complex and rapidly evolving, and the extent to which the pandemic impacts our business, financial condition and results of operations, including the duration and magnitude of such impacts, will depend on numerous evolving factors that we may not be able to accurately predict or assess. COVID-19, and the volatile regional and global economic conditions stemming from the pandemic, as well as reactions to future pandemics or resurgences of COVID-19, could also precipitate or aggravate the other risk factors that we identify in this Annual Report on Form 10-K, which in turn could materially adversely affect our business, financial condition and results of operations. There may be other adverse consequences to our business, financial condition and results of operations from the spread of COVID-19 that we have not considered or have not become apparent. As a result, we cannot assure you that if COVID-19 continues to spread, it would not have a further adverse impact on our business, financial condition and results of operations.

Project sites are inherently dangerous workplaces. Failure to maintain safe work sites by us, the owner or others working at the project site can lead to our employees or others becoming injured, disabled or even losing their lives, and exposes us to significant financial losses and reputational harm, as well as civil and criminal liabilities.