Exhibit 1

INCORPORATION OF DOCUMENTS BY REFERENCE

This document is the Republic of Italy’s Annual Report on Form 18-K (“Annual Report”) under the U.S. Securities Exchange Act of 1934 for the fiscal year ended December 31, 2012. All amendments to the Annual Report filed by the Republic of Italy on Form 18-K following the date hereof shall be incorporated by reference into this document. Any statement contained herein, or deemed to be incorporated by reference herein, shall be deemed to be modified or superseded for purposes of this document to the extent that a statement contained herein or in any other subsequently filed document that also is or is deemed to be incorporated by reference herein modifies or supersedes such statement. Any statement so modified or superseded shall not be deemed, except as so modified or superseded, to constitute a part of this document.

FORWARD-LOOKING STATEMENTS

As required by Form 18-K, the Republic of Italy’s most recent budget is filed as an exhibit to this Annual Report. In addition, other Italian Government budgetary papers may from time to time be filed as exhibits to amendments to this Annual Report. This Annual Report, any amendments hereto and exhibits hereto contain or may contain budgetary papers or other forward-looking statements that are not historical facts, including statements about the Italian Government’s beliefs and expectations for the forthcoming budget period. Forward-looking statements can generally be identified by the use of terms such as “will”, “may”, “could”, “should”, “would”, “expect”, “intend”, “estimate”, “anticipate”, “believe”, “continue”, “project” or other similar terms. Those statements are or will be based on plans, estimates and projections that are current only as of the original date of release by the Italian Government of those budgetary papers and speak only as of the date they are so made. The information included in those budgetary papers may also have changed since that date. In addition, these budgets are prepared for government planning purposes, not as future predictions, and actual results may differ and have in fact differed, in some cases materially, from results contemplated by the budgets or other forward-looking statements. Therefore, you should not rely on the information in those budgetary papers or forward-looking statements. If the information included or incorporated by reference in this Annual Report differs from the information in those budgetary papers or forward-looking statements, you should consider only the most current information included in this Annual Report, any amendments hereto and exhibits hereto. Certain figures regarding prior fiscal years have been updated to reflect more recent data that were not previously available. You should read all the information in this Annual Report.

v

TABLE OF CONTENTS

| Summary Information |

1 | |||

| Republic of Italy |

4 | |||

| Area and Population |

4 | |||

| Government and Political Parties |

6 | |||

| The European Union |

7 | |||

| Membership of International Organizations |

9 | |||

| The Italian Economy |

10 | |||

| General |

10 | |||

| Measures to Address the Global Financial and Economic Crisis |

12 | |||

| EU Measures to Address the Eurocrisis |

14 | |||

| Gross Domestic Product |

17 | |||

| Principal Sectors of the Economy |

19 | |||

| Role of the Government in the Economy |

19 | |||

| Services |

19 | |||

| Employment and Labor |

23 | |||

| Prices and Wages |

24 | |||

| Monetary System |

27 | |||

| Monetary Policy |

27 | |||

| Exchange Rate Policy |

30 | |||

| Banking Regulation |

30 | |||

| Measures to assess the robustness of Italian Banking System |

35 | |||

| Credit Allocation |

35 | |||

| Exchange Controls |

35 | |||

| The External Sector of the Economy |

37 | |||

| Foreign Trade |

37 | |||

| Geographic Distribution of Trade |

39 | |||

| Balance of Payments |

40 | |||

| Reserves and Exchange Rates |

43 | |||

| Public Finance |

45 | |||

| The Budget Process |

45 | |||

| European Economic and Monetary Union |

45 | |||

| Accounting Methodology |

47 | |||

| Measures of Fiscal Balance |

47 | |||

| The 2012 Economic and Financial Document |

49 | |||

| The Update of the 2012 Economic and Financial Document |

51 | |||

| The 2013 Economic and Financial Document |

53 | |||

| The Update of the 2013 Economic and Financial Document |

55 | |||

| Revenues and Expenditures |

56 | |||

| Expenditures |

58 | |||

| Revenues |

58 | |||

| Government Enterprises |

60 | |||

| Public Debt |

61 | |||

| General |

61 | |||

| Summary of Internal Debt |

64 | |||

| Summary of External Debt |

65 | |||

| Debt Record |

66 | |||

| Tables and Supplementary Information |

67 | |||

vi

Except as otherwise specified, all amounts are expressed in euro (“euro” or “€”). With the implementation of the third stage of European Economic and Monetary Union on January 1, 1999, the exchange rate between the euro and Italian lire (“lira” or “lire”) was irrevocably fixed at Lit. 1,936.27 per €1.00. The euro was introduced as a physical currency on January 1, 2002 and on February 28, 2002 the lira ceased to be legal tender in Italy and was withdrawn from the financial system. For additional information concerning the exchange rate of the euro against the U.S. dollar and certain other currencies, see “External Sector of the Economy—Reserves and Exchange Rates—U.S. Dollar/Euro Exchange Rate”. We make no representation that the euro amounts referred to in this Annual Report could have been converted into U.S. dollars at any particular rate.

vii

Defined Terms and Conventions

We use terms in this Annual Report that may not be familiar to you. These terms are commonly used to refer to economic concepts that are discussed in this Annual Report. Set forth below are some of the terms used in this Annual Report.

| • | Gross domestic product, or GDP, means the total value of products and services produced inside a country during the relevant period. |

| • | Gross national product, or GNP, means GDP plus income earned by a country’s nationals from products produced, services rendered and capital invested outside the home country, less income earned inside the home country by non-nationals. |

| • | Imports and Exports. Imports are goods brought into a country from a foreign country for trade or sale. Exports are goods taken out of a country for trade or sale abroad. Data on imports and exports included in this Annual Report are derived from customs documents for non-European Union countries and data supplied by other Member States of the European Union. |

| • | The unemployment rate is calculated as the ratio of the members of the labor force who register with local employment agencies as being unemployed to the total labor force. “Labor force” means people employed and people over the age of 15 looking for a job. The reference population used to calculate the Italian labor force in this Annual Report consists of all household members present and resident in Italy and registered with local authorities. |

| • | The inflation rate is measured by the year-on-year percentage change in the general retail price index, unless otherwise specified. The European Union harmonized consumer price index (“HICP”) is calculated on the basis of a weighted basket of goods and services taking into account all families resident in a given territory. Year-on-year rates are calculated by comparing the average of the twelve monthly indices for the later period against the average of the twelve monthly indices for the prior period. |

| • | Net borrowing, or government deficit, is consolidated revenues minus consolidated expenditures of the general government. This is the principal measure of fiscal balance for countries participating in the European Economic and Monetary Union and is calculated in accordance with the EU Protocol on Excessive Deficit Procedure, which implements the European System of Accounts (“ESA95”). |

| • | Net borrowing-to-GDP or deficit-to-GDP means the ratio of net borrowing or government deficit to nominal GDP. |

| • | Debt-to-GDP means the ratio of public debt to nominal GDP. Public debt includes debt incurred by the central government (including Treasury securities and borrowings), regional and other local government, public social security agencies and other public agencies. |

| • | Primary balance is net borrowing less interest payments and other borrowing costs of the general government. The primary balance is used to measure the effect of discretionary actions taken to control expenditures and increase revenues. |

Unless otherwise indicated, we have expressed:

| • | all annual rates of growth as average annual compounded rates; |

| • | all rates of growth or percentage changes in financial data in constant prices adjusted for inflation; and |

| • | all financial data in current prices. |

Amounts included in this Annual Report are normally rounded. In particular, amounts stated as a percentage are normally rounded to the first decimal place. Totals in certain tables in this Annual Report may differ from the sum of the individual items in such tables due to rounding.

Information Sources

The source for most of the financial and demographic statistics for Italy included in this Annual Report is data prepared by Istituto Nazionale di Statistica, or ISTAT, an independent Italian public agency that produces statistical information regarding Italy (including GDP data), in particular financial and demographic statistics for Italy published in the Annual Report of ISTAT dated May 22, 2013 and appendices thereto (together the “2013 ISTAT Annual Report”) and elaborations on such data and other data published in the Annual Report of the Bank of Italy (Banca d’Italia, Italy’s central bank) dated May 31, 2013 and appendices thereto (together the “2013 Bank of Italy Annual Report”). We also include in this Annual Report information published by the Statistical Office of the European Communities or Eurostat.

viii

Certain other financial and statistical information contained in this Annual Report has been derived from other Italian Government sources, including the economic and financial document of 2013 (Documento di Economia e Finanza 2012), dated April 10, 2013 (the “2013 Economic and Financial Document”), which includes the 2013 stability programme (the “2013 Stability Programme”) attached as Exhibit 2 to this Annual Report and the 2013 national reform programme (the “2013 National Reform Programme”) attached as Exhibit 3 to this Annual Report, and the update of the economic and financial document of 2013 (Nota di Aggiornamento del Documento di Economia e Finanza 2013), dated September 20, 2013 (the “Update of the 2013 Economic and Financial Document”) attached as Exhibit 4 to this Annual Report.

Revised National Accounts

In 1999, ISTAT introduced a new system of national accounts in accordance with the new European System of Accounts (ESA95) as set forth in European Union Regulation 2223/1996. This system was intended to contribute to the harmonization of the accounting framework, concepts and definitions within the European Union. Under ESA95, all European Union countries apply a uniform methodology and present their results on a common calendar. Both state sector accounting and public sector accounting transactions are recorded on an accrual basis. Since introducing the ESA95 accounting system, ISTAT has published revisions to the national system of accounts, including replacing its methodology for calculating real growth, which had been based on a fixed base index, with a methodology linking real growth between consecutive time periods, or a chain-linked index. As a result of this change in methodology, all “real” revenue and expenditure figures included in this document differ from and are not comparable to data published in earlier documents filed by Italy with the United States Securities and Exchange Commission, or SEC, prior to March 12, 2007. In addition, certain data relating to the years 2000-2010 which was previously presented at purchasing power parity with 2000 prices have been restated and are now presented at purchasing power parity with 2005 prices. For additional information regarding the restatement of data from previous fiscal years, see “Public Finance—Accounting Methodology”.

The general government revenues and expenditure figures in this Annual Report reflect consolidated revenues and expenditures for the public sector, which is the broadest aggregate for which data is available.

All references herein to “Italy,” the “State” or the “Republic” are to the Republic of Italy, all references herein to the “Government” are to the central government of the Republic of Italy and all references to the “general government” are collectively to the central government and local government sectors and social security funds (those institutions whose principal activity is to provide social benefits), but exclude government owned corporations. In addition, all references herein to the “Ministry of Economy and Finance”, to the “MEF” and to the “Treasury” are interchangeable and refer to the Ministry of Economy and Finance.

ix

SUMMARY INFORMATION

The following summary is qualified in its entirety by, and should be read in conjunction with, the more detailed information appearing elsewhere in this Annual Report, any amendments hereto and annexes hereto.

Gross Domestic Product: According to International Monetary Fund estimates, the economy of Italy, as measured by 2012 GDP (at current prices in U.S. dollars), is the eighth largest in the world. In 2012, Italy’s real GDP decreased by 2.4 per cent, compared to a 0.4 per cent increase in 2011. In the last ten years, Italy’s GDP growth rate has generally been lower than the average GDP growth rate of the euro area. The growth gap between other euro area countries and Italy in the past decade reflects the persistence of several medium and long-term factors, including the difficulties in fully integrating southern Italian regions into the more dynamic economy of northern and central Italy, unfavorable export specialization in traditional goods, inadequate infrastructure, the incomplete liberalization process and insufficient flexibility of national markets. For additional information with respect to Italy’s GDP, see “The Italian Economy—Gross Domestic Product”. In order to address the financial and economic crisis, from 2008 up to 2013, the Government enacted legislation providing for measures aimed at stimulating the economy and stabilizing the Italian financial system. For additional information on the measures enacted by the Government to stimulate the economy and stabilize the Italian financial system, see “The Italian Economy”, Exhibit 2—2013 Stability Programme and Exhibit 4—Update of the 2013 Economic and Financial Document.

The European Economic and Monetary Union: Italy is a signatory of the Treaty on European Union of 1992, also known as the “Maastricht Treaty,” which established the European Economic and Monetary Union, or EMU, culminating in the introduction of a single currency. Eleven member countries, including Italy, met the government deficit, inflation, exchange rate and interest rate requirements of the Maastricht Treaty and were included in the first group of countries to join the EMU on January 1, 1999. On that date, conversion from each EMU member’s old national currency into the euro was irrevocably fixed and the euro became legal tender. The euro was introduced in physical form in the countries participating in the EMU on January 1, 2002 and replaced national notes and coins entirely on February 28, 2002. On January 4, 1999, the noon buying rate for the euro as reported by the European Central Bank (the “Noon Buying Rate”) was €1 for US$1.1812. On September 30, 2013, the European Central Bank (“ECB”) exchange reference rate was €1 for $1.3505. For additional information regarding the historic dollar/euro exchange rate, see “The External Sector of the Economy—Reserves and Exchange Rates”.

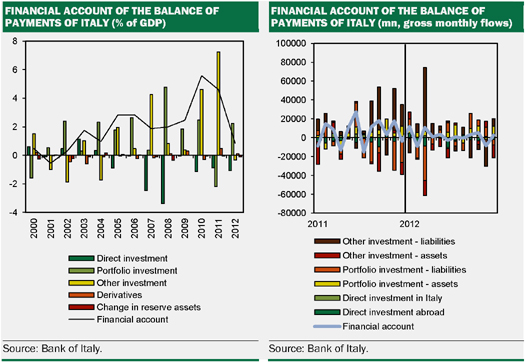

Foreign Trade: Over half of Italy’s exports and imports involve other European Union countries. Italy’s main exports are manufactured goods, including industrial machinery, office machinery, automobiles, clothing, shoes and textiles. Since 2004, Italy’s balance of payments has recorded current account deficits. The deficit on Italy’s external current account in 2012 was €8.4 billion or 0.5 per cent of GDP, the lowest level since 2004, compared to €48.3 billion or 3.1 per cent of GDP in 2011.

Inflation: In 2012, consumer prices in Italy increased at an annual rate of 3.3 per cent measured by the harmonized EU consumer price index (HICP), compared to 2.9 per cent in 2011.

Public Finance: Italy has historically experienced substantial government deficits and high public debt. Countries participating in the EMU are required to reduce “excessive deficits”, adopting budgetary balance as a medium-term objective, and to reduce public debt. Italy recorded net borrowing amounts as a percentage of GDP higher than the 3.0 per cent ratio imposed by the Maastricht Treaty in 2001 and each year during 2003-2006 and 2009-2011. As set out in the Update of the 2013 Economic and Financial Document, Italy’s deficit-to-GDP ratio was 3.0 per cent in 2012 and its debt-to-GDP ratio (gross of euro area financial support) was 127.0 per cent in 2012. For additional information with respect to Italy’s debt-to-GDP, see “The Italian Economy”, “Public Finance”, Exhibit 2—2013 Stability Programme and Exhibit 4—Update of the 2013 Economic and Financial Document.

Eurocrisis: The global financial system began showing signs of disruption in the summer of 2007 and its condition quickly deteriorated following the bankruptcies of several major international financial institutions in the summer of 2008. Its condition continued to deteriorate and caused major disruptions in global financial markets, including unsustainably low levels of liquidity and funding sources (which resulted in high funding costs, historically high credit spreads, volatile and unsustainable capital markets and declining asset values). Many countries acted to combat deteriorating economic conditions, including borrowing in order to support troubled financial and other institutions and adopting other measures to stimulate their economies, which actions led to the credit ratings of various countries to be reduced. The first to be directly affected was Iceland in 2008, followed by Greece, Ireland and Portugal in 2010 and Spain and Italy in 2011. Such reductions to sovereign credit ratings, compounded by the existing recessionary global economy, made it difficult, or in

1

certain instances impossible, for many European countries to access the capital markets to satisfy their funding needs. Such difficulties led to further reductions in sovereign credit ratings and the need for such countries to receive financial support from third parties, including from other countries and the financial support mechanisms adopted by the European Union. In particular, beginning in 2010, Greece, Ireland and Portugal began receiving financial assistance in the form of direct and indirect loans from EU member states. Such conditions have persisted through the date of this Annual Report. For additional information on the measures that the European Union and Italy have taken to address the Eurocrisis, see “The Italian Economy”, Exhibit 2—2013 Stability Programme and Exhibit 3—2013 National Reform Programme.

During 2012, several measures have been adopted to relieve the eurocrisis. In February 2012, EU Member States established the European Stability Mechanism (ESM), which has a large lending capacity, to help preserve the financial stability of Europe’s Monetary Union by providing assistance to Eurozone countries. See “The Italian Economy—EU Measures to Address the Eurocrisis—The ESM”. In September 2012, the ECB stated that investors’ fears over the reversibility of the Euro are unfounded because the ECB is strongly committed to maintaining the singleness of the monetary policy among Eurozone countries, including through Outright Monetary Transactions, in order to address severe distortions in government bond markets. The ECB stated that these steps have been and will continue to be taken within the ECB mandate to maintain price stability over the medium term.

If the eurocrisis were to deepen or extend, the EU Member States may determine further reforms in order to manage the crisis. A prolonged crisis in Europe or a new crisis in Italy could make the refinancing of debt by Italy more expensive.

The Italian Political System: Italy is a democratic republic. Italy is a civil law jurisdiction, with judicial power vested in ordinary courts, administrative courts and courts of accounts. The Government operates under a Constitution that provides for a division of powers among Parliament, the executive branch and the judiciary. Parliament comprises a Senate and a Chamber of Deputies. The executive branch consists of a Council of Ministers selected and headed by a Prime Minister. The Prime Minister is appointed by the President of the Republic and the Prime Minister’s government is confirmed by Parliament. The general Parliamentary elections held on February 24 and 25, 2013 resulted in no party or coalition having a majority of both the Chamber of Deputies and the Senate. The center-left coalition, led by Mr. Pier Luigi Bersani, obtained the highest number of votes on a national level for the elections of the Chamber of Deputies and therefore was awarded with the majority of seats in the Chamber of Deputies. No political party or coalition obtained an absolute majority of seats in the Senate. On April 24, 2013, Mr. Enrico Letta, a representative of the center-left coalition, was appointed to form a new government, which was sworn in on April 28, 2013. On April 29 and 30, 2013, Prime Minister Letta’s government received the confidence vote of the Parliament.

2013 Developments: Law decree n. 35/2013 (converted into law on June 6, 2013) enacted a series of measures aimed at allowing the public administration to accelerate the payments of certain trade payables (overdue as of December 31, 2012) in order to stimulate economic growth. The decree authorized payments due to enterprises, cooperatives and professionals for a total of up to €40 billion, which has been subsequently increased by additional €7.2 billion through Law decree 102/2013. The injection of liquidity achieved through such acceleration is intended to have a positive effect on GDP growth, consumption and investments. For additional information on these measures, see Exhibit 2—2013 Stability Programme, Exhibit 3—2013 National Reform Programme and Exhibit 4—Update of the 2013 Economic and Financial Document.

Law decree n. 69/2013 (Decreto del Fare) (converted into law on August 9, 2013) enacted a new package of urgent measures aimed at stimulating the Italian economy, including, among other things, provisions aimed at facilitating access to credit by small and medium sized companies, measures aimed at developing infrastructure (such as the “European corridors” and certain railway services for approximately €2 billion), rules aimed at bureaucracy and tax simplification, rules aimed at enhancing the efficiency of the justice system, rules aimed at enhancing the digitalization of the public administration (the “Italian Digital Agenda”) and measures concerning education.

In October 2013, the Government approved the draft stability law for 2014 and the draft budget law for 2014/2016. These bills (disegni di legge) have been submitted to the Italian Parliament for discussion and approval. In particular, the draft stability law for 2014 includes measures aimed at sustaining economic growth and increasing employment through, inter alia, a decrease of taxes applicable to individuals and enterprises (including taxes on labor cost), the allocation of financial resources for certain strategic investments (mainly infrastructural) and the reduction of public expenditure.

In addition, the draft stability law for 2014 proposes the introduction of a new service tax to cover costs of services provided by local administrations (including waste management) to be levied by municipalities against real estate properties located in Italy which, with respect to primary residences (prima casa), shall replace the current real property tax (Imposta Municipale Unitaria or IMU)

2

Ratings of the Republic of Italy’s Indebtedness: As of the date hereof, the Republic of Italy’s long-term credit is rated BBB with negative outlook by Standard & Poor’s, BBB+ with negative outlook by Fitch Ratings and Baa2 with negative outlook by Moody’s.

3

REPUBLIC OF ITALY

Area and Population

Geography. The Republic of Italy is situated in south central Europe on a peninsula approximately 1,120 kilometers (696 miles) long and includes the islands of Sicily and Sardinia in the Mediterranean Sea and numerous smaller islands. To the north, Italy borders on France, Switzerland, Austria and Slovenia along the Alps, and to the east, west and south it is surrounded by the Mediterranean Sea. Italy’s total area is approximately 301,300 square kilometers (116,336 square miles), and it has 7,375 kilometers (4,582 miles) of coastline. The independent States of San Marino and Vatican City, whose combined area is approximately 61 square kilometers (24 square miles), are located within the same geographic area. The Apennine Mountains running along the peninsula and the Alps north of the peninsula give much of Italy a rugged terrain.

The following is a map of the European Union and the countries, including Italy, within the Euro area.

4

The following is a map of Italy.

Population. According to ISTAT data, as of December 31, 2012, Italy’s resident population was estimated to be approximately 59.685 million, accounting for approximately 12.1 per cent of the EU population. Italy is the fourth most populated country in the EU after Germany, France and the United Kingdom. According to ISTAT data, as of December 31, 2012, the six regions in the southern part of the peninsula together with Sicily and Sardinia, known as the Mezzogiorno, had a population of approximately 20.6 million. As of the same date, northern and central Italy had a population of approximately 27.3 million and 11.6 million, respectively.

As of January 1, 2012, the breakdown of the resident population by age group was as follows:

| • | under 20 | 17.9 | % | |||

| • | 20 to 39 | 24.9 | % | |||

| • | 40 to 59 | 29.4 | % | |||

| • | 60 and over | 27.8 | % |

Source: ISTAT

Italy’s fertility rate is one of the lowest in the world, while life expectancy for Italians is among the highest in the world. Because population growth has been low in recent years, the average age of the population is increasing.

Rome, the capital of Italy and its largest city, is situated near the western coast approximately halfway down the peninsula, and had a population of approximately 2.6 million as of December 31, 2011. The next largest cities are Milan, with a population of approximately 1.2 million, Naples, with approximately 0.95 million, and Turin, with approximately 0.9 million. In 2011, approximately 68.0 per cent of Italy’s population lived in urban areas. Based on ISTAT data, as of December 31, 2011, population density is approximately 197.4 persons per square kilometer.

Like other EU countries, Italy has experienced significant immigration in recent years, particularly from North Africa and Eastern European countries. According to ISTAT data, in 2012, there were approximately 4.3 million foreigners holding permits to live in Italy, an 8.3 per cent increase from the previous year. Immigration legislation has been the subject of intense political debate since the early 1990s. Italy has tightened its immigration laws in the past decade and initiated bilateral agreements with several countries for

5

cooperation in identifying illegal immigrants. In addition to measures aimed at controlling illegal immigration, the Government has also introduced measures aimed at regularizing the position of illegal immigrants. While these legislative efforts have resulted in the regularization of large numbers of illegal immigrants, Italy continues to have high numbers of foreigners living in Italy illegally.

Government and Political Parties

Italy was originally a loose-knit collection of city-states, most of which united into one kingdom in 1861. It has been a democratic republic since 1946. The Government operates under a Constitution, originally adopted in 1948, that provides for a division of powers among the legislative, executive and judicial branches.

The Legislative Branch. Parliament consists of a Chamber of Deputies, with 630 elected members, and a Senate, with 315 elected members and a small number of life Senators, consisting of former Presidents of the Republic and prominent individuals appointed by the President. The Chamber of Deputies and the Senate share equally and have substantially the same legislative power. Any statute must be approved by both assemblies before being enacted. Except for life Senators, members of Parliament are elected for five years by direct universal adult suffrage, although elections have been held more frequently in the past because the instability of multi-party coalitions has led to premature dissolutions of Parliament.

The Executive Branch. The head of State is the President, elected for a seven-year term by an electoral college that includes the members of Parliament and 58 regional delegates. The current President, Giorgio Napolitano, was originally elected in 2006 and re-elected for a second term. The next presidential election will occur in the spring of 2020. The President has the power to appoint the Prime Minister and to dissolve Parliament. The Constitution also grants the President the power to appoint one-third of the members of the Constitutional Court, to call general elections and to command the armed forces. The President nominates and Parliament confirms the Prime Minister, who is the effective head of Government. The Council of Ministers is appointed by the President on the Prime Minister’s advice. The Prime Minister and Council of Ministers answer to both houses of Parliament and must resign if one of the houses of Parliament passes a vote of no confidence in the administration.

The Judicial Branch. Italy is a civil law jurisdiction. Judicial power is vested in ordinary courts, administrative courts and courts of accounts. The highest ordinary court is the Corte di Cassazione in Rome, where judgments of lower courts of local jurisdiction may be appealed. The highest of the administrative courts, which hear claims against the State and local entities, is the Consiglio di Stato in Rome. The Corte dei Conti in Rome supervises the preparation of, and adjudicates, the State budget of Italy. There is also a Constitutional Court (Corte Costituzionale) that does not exercise general judicial powers, but adjudicates conflicts among the other branches of government and determines the constitutionality of statutes. Criminal matters are within the jurisdiction of the criminal law divisions of ordinary courts, which consist of magistrates who either act as judges in criminal trials or are responsible for investigating and prosecuting criminal cases.

Political Parties. The main political parties are grouped into four coalitions: (i) a center-right coalition led by Il Popolo delle Libertá (in the person of Mr. Silvio Berlusconi), (ii) a center-left coalition led by the Partito Democratico (in the person of Mr. Guglielmo Epifani), (iii) a center coalition led by Scelta Civica con Monti per l’Italia (in the person of Mr. Mario Monti) and (iv) the non-aligned party named Movimento 5 Stelle Beppegrillo.It (in the person of Mr. Giuseppe Piero Grillo).

The general Parliamentary elections held in February 2013 resulted in no party or coalition having a majority of both the Chamber of Deputies and the Senate. The center-left coalition, led by Mr. Pier Luigi Bersani, obtained the highest number of votes on a national level for the elections of the Chamber of Deputies and therefore was awarded the majority of seats in the Chamber of Deputies. No political party or coalition obtained an absolute majority of seats in the Senate.

On April 24, 2013, President Napolitano appointed Mr. Enrico Letta, a member of the center-left coalition, to form a new government and Mr. Letta was sworn in as Prime Minister on April 28, 2013. The new government is composed of members from and supported by the center-left coalition, the center-right coalition and the center coalition. On April 29 and 30, 2013, Prime Minister Letta’s government received the confidence vote of the Parliament

Elections. Except for a brief period, since Italy became a democratic republic in 1946 no one party has been able to command an overall majority in Parliament, and, as a result, Italy has a long history of weak coalition governments. In 1993, Parliament adopted a partial “first past the post” voting system for the election of 75 per cent of the members of both the Senate and the Chamber of Deputies. Under this system, the candidate receiving the largest number of votes in a single district wins. The remaining 25 per cent are elected through a proportional representation system. In the Chamber of Deputies, only parties that receive 4 per cent

6

of the total vote on a nationwide basis are eligible for the seats elected by proportional representation. These modifications of the voting system have resulted in a significantly smaller number of Parliamentary seats held by parties with relatively small shares of the popular vote. Historically, however, government stability has depended on the larger parties’ coalitions with smaller parties.

In December 2005, a new law was enacted modifying the voting system for the Chamber of Deputies and the Senate. In the Chamber of Deputies and in the Senate, the electorate votes for lists of candidates presented by the multiparty coalitions and individual parties. Seats in the Chamber of Deputies are awarded based on the number of votes obtained by each list, provided that multiparty coalitions and individual parties are not eligible for any seat unless they attain at least 10 per cent and 4 per cent of the total votes, respectively. Seats in the Senate are also awarded based on the number of votes obtained by each list, but the minimum per cent of the total votes to be attained by multiparty coalitions and individual parties are determined on a regional basis. In order to ensure government stability, if the winning coalition does not obtain at least 340 seats in the Chamber of Deputies, it is automatically awarded as many seats as it needs to reach 340 seats. In the Senate, the award for the winning coalition is determined on a regional basis. This modified voting system was utilized for the first time in the general elections in April 2006.

Regional and Local Governments. Italy is divided into 20 regions containing 110 provinces. The Italian Constitution reserves certain functions, including police services, education and other local services, for the regional and local governments. Following a Constitutional reform passed by Parliament in 2001, additional legislative and executive powers were transferred to the regions. Legislative competence that historically had belonged exclusively to Parliament was transferred in certain areas (including foreign trade, health and safety, ports and airports, transport network and energy production and distribution) to a regime of shared responsibility whereby the national government promulgates legislation defining fundamental principles and the regions promulgate implementing legislation. Furthermore, as to all areas that are neither subject to the exclusive competence of Parliament nor in a regime of shared responsibility between Parliament and the regions, exclusive regional competence is conferred to a region upon its request, subject to Parliamentary approval. In 2009, Italy adopted legislation that is designed to increase the fiscal autonomy of regional and local governments. The reform is expected to come fully into effect by 2016. Under the new system, lower levels of government will be able to levy their own taxes and will have a share in central tax revenues, including income tax and value added tax. Under the new system, a “standard cost” for public services such as health, education, welfare and public transport will be determined to set budgets for local governments. A fund will be made available to local governments that incur government deficits and convergence plans will be set up for local governments that record significant government deficits in consecutive years.

The Italian Constitution grants special status to five regions (Sicily, Sardinia, Trentino-Alto Adige, Friuli-Venezia Giulia and Valle d’Aosta) providing them with additional legislative and executive powers.

Referenda. An important feature of Italy’s Constitution is the right to hold a referendum to abrogate laws passed by Parliament. Upon approval, a referendum has the legal effect of annulling legislation to which it relates. A referendum can be held at the request of 500,000 signatories or five regional councils but cannot be held on matters relating to taxation, the State budget, the ratification of international treaties or judicial amnesties. In order for a referendum to be approved, a majority of the Italian voting population must vote in the referendum and a majority of such voters must vote in favor of the referendum.

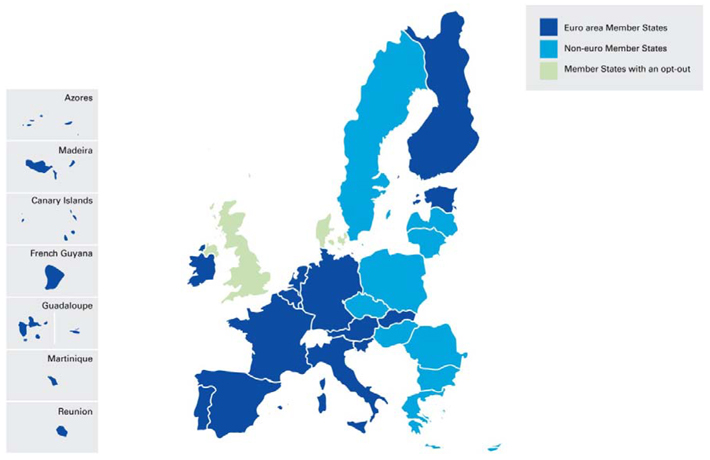

The European Union

Italy is a founding member of the European Economic Community, which now forms part of the European Union. Italy is one of the 28 current members of the EU together with Austria, Belgium, Bulgaria, Croatia, Cyprus, the Czech Republic, Denmark, Estonia, Finland, France, Germany, Greece, Hungary, Ireland, Latvia, Lithuania, Luxembourg, Malta, The Netherlands, Poland, Portugal, Romania, Slovakia, Slovenia, Spain, Sweden and the United Kingdom. The EU had an estimated population of approximately 506.8 million as of January 1, 2012.

The European Union is currently negotiating the terms and conditions of accession to the EU of the following candidate countries: the Former Yugoslav Republic of Macedonia, Montenegro, Iceland and Turkey.

The EU Member States have agreed to delegate sovereignty for certain matters to independent institutions that represent the interests of the union as a whole, its Member States and its citizens. Set forth below is a summary description of the main EU institutions and their role in the European Union.

The Council of the EU. The Council of the EU (the “EU Council”), is the EU’s main decision-making body. It meets in different compositions by bringing together, on a regular basis, ministers of

7

the Member States to decide on matters such as foreign affairs, finance, education and telecommunications. When the EU Council meets to address economic and financial affairs, it is referred to as ECOFIN (“ECOFIN”). The EU Council mainly exercises, together with the European Parliament, the European Union’s legislative function and promulgates:

| • | regulations, which are EU laws directly applicable in Member States; |

| • | directives, which set forth guidelines that Member States are required to enact by promulgating national laws; and |

| • | decisions, through which the EU Council implements EU policies. |

The EU Council also coordinates the broad economic policies of the Member States and concludes, on behalf of the EU, international agreements with one or more Member States or international organizations. In addition, the EU Council:

| • | shares budgetary authority with the European Parliament; |

| • | makes the decisions necessary for framing and implementing a common foreign and security policy; and |

| • | coordinates the activities of Member States and adopts measures in the field of police and judicial cooperation in criminal matters. |

Decisions of the EU Council are made by vote. Each Member State’s voting power is largely based on the size of its population. The following are the number of votes each Member State can cast:

| • | Germany, France, Italy and the United Kingdom each have 29 votes; |

| • | Spain and Poland each have 27 votes; |

| • | Romania has 14 votes; |

| • | the Netherlands has 13 votes; |

| • | Belgium, the Czech Republic, Greece, Hungary and Portugal each have 12 votes; |

| • | Austria, Bulgaria and Sweden each have 10 votes; |

| • | Denmark, Croatia, Ireland, Lithuania, Slovakia and Finland each have 7 votes; |

| • | Cyprus, Estonia, Latvia, Luxembourg and Slovenia each have 4 votes; and |

| • | Malta has 3 votes. |

Generally, decisions of the EU Council are made by qualified majority, which is achieved if:

| • | a majority of Member States (in certain cases, a two-thirds majority of Member States) approves the decision; |

| • | a number of votes representing at least 73.9 per cent of all votes is cast in favor of the decision; and |

| • | a Member State may ask for confirmation that the votes in favor represent at least 62 per cent of the total population of the European Union. |

Commencing on October 1, 2014, pursuant to changes enacted by the Treaty of Lisbon, the voting rules for the EU Council will change, increasing the required majority to 55 per cent of Member States (72 per cent in certain cases) and 65 per cent of the population, and permitting four Member States to block a proposal.

The European Parliament. The European Parliament is elected every five years by direct universal suffrage. The European Parliament has three essential functions:

| • | it shares with the EU Council the power to adopt directives, regulations and decisions; |

| • | it shares budgetary authority with the EU Council and can therefore influence EU spending; and |

| • | it approves the nomination of Commissioners, has the right to censure the Commission and exercises political supervision over all the EU institutions. |

8

Following the election held in 2009 and the accession of Croatia in July 2013, each Member State was allocated the following number of seats in Parliament:

The European Commission. The European Commission (the “Commission”), upholds the interests of the EU as a whole and has the right to initiate draft legislation by presenting legislative proposals to the European Parliament and Council. Currently, the European Commission consists of 28 members, one appointed by each Member State for five-year terms.

Court of Justice. The Court of Justice ensures that community law is uniformly interpreted and effectively applied. It has jurisdiction in disputes involving Member States, EU institutions, businesses and individuals. A Court of First Instance has been attached to it since 1989.

Other Institutions. Other institutions that play a significant role in the European Union are:

| • | the European Central Bank, which is responsible for defining and implementing a single monetary policy in the euro area; |

| • | the Court of Auditors, which checks that all the European Union’s revenue has been received and that all its expenditures have been incurred in a lawful and regular manner and oversees the financial management of the EU budget; and |

| • | the European Investment Bank, which is the European Union’s financial institution, supporting EU objectives by providing long-term financing for specific capital projects. |

Membership of International Organizations

Italy is also a member of the North Atlantic Treaty Organization (NATO), as well as many other regional and international organizations, including the United Nations and many of its affiliated agencies. Italy is one of the Group of Eight (G-8) industrialized nations, together with the United States, Japan, Germany, France, the United Kingdom, Canada and Russia, and a member of the Organization for Economic Co-operation and Development (OECD), the World Trade Organization (WTO), the International Monetary Fund (IMF), the International Bank for Reconstruction and Development (World Bank), the European Bank for Reconstruction and Development (EBRD) and other regional development banks.

9

THE ITALIAN ECONOMY

General

According to IMF data, the Italian economy, as measured by 2012 GDP (at current prices in U.S. dollars), is the eighth largest in the world after the United States, Japan, Germany, the People’s Republic of China, the United Kingdom, France and Brazil.

The Italian economy developed rapidly in the period following World War II as large-scale, technologically advanced industries flourished along with more traditional agricultural and industrial enterprises. Between 1960 and 1974, Italian GDP, adjusted for changes in prices, or “real GDP,” grew by an average of 5.2 per cent per year. As a result of the 1973-74 oil price shocks and the accompanying worldwide recession, output declined by 2.1 per cent in 1975, but between 1976 and 1980 real GDP again grew by an average rate of approximately 4 per cent per year. During this period, however, the economy experienced higher inflation, driven in part by wage inflation and high levels of borrowing by the Government. For the 1980s as a whole, real GDP growth in Italy averaged 2.4 per cent per year.

Italy’s economic growth slowed down substantially in the 1990s. Tighter fiscal policy, which followed the lira’s suspension from the Exchange Rate Mechanism in September 1992, led Italy’s economy into recession in 1993. The economy recovered in 1994; however, Italy’s GDP grew at a modest pace, an average of 1.6 per cent per year from 1996 through 1999, lagging behind those of other major European countries. The growth gap between other EMU countries and Italy since the mid-1990s reflects the persistence of several medium and long-term factors, including the difficulties in fully integrating southern Italian regions into the more dynamic economy of northern and central Italy, unfavorable export specialization in traditional goods, inadequate infrastructure, the incomplete liberalization process and insufficient flexibility of national markets, the slowness of the recovery in economic activity is due to shortcomings in the Italian productive economy that make it fragile in the new competitive environment. These deficiencies depend both on factors internal to firms, such as small size and the limitations of exclusive family control and on external factors, such as insufficient infrastructure, high tax rates combined with widespread tax evasion, an uncertain and complex regulatory framework and long administrative procedures. Some lack of competition is adversely affecting the service sector in particular.

Over the seven-year period from 2000 to 2007, average annual GDP growth in Italy equaled 1.5 per cent compared to the average annual GDP growth of the euro area of 2.5 per cent.

The table below shows the annual percentage change in real GDP growth for Italy and the EU, including Italy, for the period 2000 through 2007.

Annual Per Cent Change in Real GDP (2000-2007)

| 2000 | 2001 | 2002 | 2003 | 2004 | 2005 | 2006 | 2007 | |||||||||||||||||||||||||

| Italy |

3.7 | 1.9 | 0.5 | 0.0 | 1.7 | 0.9 | 2.2 | 1.7 | ||||||||||||||||||||||||

| EU area(1) |

3.9 | 2.1 | 1.3 | 1.5 | 2.6 | 2.2 | 3.4 | 3.2 | ||||||||||||||||||||||||

| (1) | The EU area represents the 28 countries participating in the European Union. |

Source: Eurostat.

The table below shows the annual percentage change in real GDP growth for Italy and the countries participating in the EU and in the EMU, including Italy, for the period 2008 through 2011.

Annual Per Cent Change in Real GDP (2008-2012)

| 2008 | 2009 | 2010 | 2011 | 2012 | ||||||||||||||||

| Italy |

(1.2 | ) | (5.5 | ) | 1.7 | 0.4 | (2.4 | ) | ||||||||||||

| EU area(1) |

0.4 | (4.5 | ) | 2.1 | 1.6 | (0.4 | ) | |||||||||||||

| Euro area(2) |

0.4 | (4.4 | ) | 2.0 | 1.4 | (0.6 | ) | |||||||||||||

| (1) | The EU area represents the 28 countries participating in the European Union. |

| (2) | The Euro area represents the 17 countries participating in the European Monetary Union. |

Source: Bank of Italy and Eurostat.

In 2008, as a result of the global financial and economic crisis, Italy’s real GDP decreased by 1.2 per cent mainly as a result of a steep decline in exports. Italy also recorded a decrease in domestic private consumption, largely attributable to the stagnation of Italian families’ purchasing power (the rise in nominal salaries was offset by inflation) and increasing propensity to save, and a decrease in gross fixed investments, especially in machinery and equipment and real estate. The uncertainty resulting from the financial crisis and its long-term effects seriously affected consumer and business confidence and played a major role in the reduction of spending and investment.

10

In 2009, Italy’s real GDP decreased by 5.5 per cent. A moderate recovery began in the second half of the year, mainly because of improved exports. In the same period, the industrial sector returned to moderate growth and the decline in the services sector came to a halt, but the decline in the construction sector continued. Domestic demand remained weak. Spending on capital goods, although increasing slightly in the second half of 2009 in response to tax incentives for purchases of machinery and equipment, was dampened by spare capacity and uncertainty about growth. The decline in consumer spending generally worsened, despite the measures introduced to support purchases of certain durable goods. Signs of an easing in the decline of the real property market appeared towards the end of 2009.

In 2010, the Italian economy grew and real GDP increased by 1.7 per cent compared to 2009. Domestic demand sustained the recovery. Private consumption contributed to the GDP growth by approximately 0.6 per cent, fixed investment contributed to the GDP growth by approximately 0.5 per cent and an increase in inventories contributed to the GDP growth by approximately 0.7 per cent. Net exports provided a negative contribution to GDP growth by approximately 0.4 per cent. The deterioration reflects the position on merchandise trade, which turned negative last year after being broadly in balance in 2009. It was largely due to only two sectors: energy raw materials, whose deficit grew mainly because of the rise in oil prices, and electronic apparatus, where the major factor was the significant increase in imports of photovoltaic cells.

In 2011, Italy’s real GDP grew by 0.4 per cent compared to 2010. Private consumption contributed to GDP growth by 0.1 per cent and net exports contributed to GDP growth by 1.4 per cent while fixed investment negatively contributed to GDP growth by 0.4 per cent. The growth in merchandise exports in 2011 was mainly due to sales to non-EU countries, particularly sales of machinery and equipment, basic metals and other metal products. Good export performances were also recorded by traditional products, pharmaceuticals and electronic products.

In 2012, Italy’s GDP decreased by 2.4 per cent compared to 2011. The decrease in real GDP in 2012 was due to an 8.0 per cent decrease in gross fixed investment, a 3.9 per cent decrease in total consumption and a 7.7 per cent decrease in imports, partly offset by a 2.3 per cent increase in exports.

The Government has historically experienced substantial government deficits. Among other factors, this is largely attributable to high levels of social spending and the fact that social services and other non-market activities of the central and local governments account for a relatively significant percentage of total employment as well as high interest expense resulting from the size of Italy’s public debt. Countries participating in the European Economic and Monetary Union are required to reduce “excessive deficits” and adopt budgetary balance as a medium-term objective. For additional information on the budget and financial planning process, see “Public Finance—Measures of Fiscal Balance” and “Public Finance—Revenues and Expenditures”.

A longstanding objective of the Government has been to control Italy’s debt-to-GDP ratio. Italy’s debt-to-GDP ratio increased in 2012 to 124.3 per cent net of euro area financial support and 127.0 per cent gross of euro area financial support, reflecting the gap of 6.5 per cent between the average cost of debt and the expansion of nominal GDP and to the financial support provided to EMU countries, only partly offset by the primary surplus of 2.5 per cent. The debt-to-GDP ratio in 2012 was above the forecasts indicated in the September 20, 2012 update of the 2012 Economic and Financial Document. Compared to the forecast, the negative difference of 0.6 per cent was mainly due to an increased public sector borrowing requirement, which was €12 billion higher than the forecast made in September. According to Italy’s most recent projections, Italy’s debt-to-GDP ratio (gross of euro area financial support and of the effects of the acceleration of payments due by the public administration) is expected to be 133.0 per cent in 2013, 133.2 per cent in 2014, 130.5 per cent in 2015 and 127.1 per cent in 2016. For additional information on Italy’s forecasts for its debt-to-GDP ratio, see “Public Finance—The 2013 Economic and Financial Document”, Exhibit 2—2013 Stability Programme and Exhibit 4—Update of the 2013 Economic and Financial Document.

Historically, Italy has had a high but declining savings rate, calculated as a percentage of gross national disposable income, which measures aggregate income of a country’s citizens after providing for capital consumption (the replacement value of capital used up in the process of production). Private sector savings as a percentage of gross national disposable income averaged 19.6 per cent in the period from 1999 to 2008. Private sector savings as a percentage of gross national disposable income was 12.0 per cent in 2011 and decreased to 11.4 per cent in 2012. Because of the historically high savings rate, the Government has been able to raise large amounts of funds through issuances of Treasury securities in the domestic market, with limited recourse to external financing. As at December 31, 2012, the internal debt and the external debt were 96.32 per cent and 3.68 per cent, respectively, of the total debt.

11

The Italian economy is characterized by significant regional disparities, with the level of economic development of southern Italy well below that of northern and central Italy. The per capita GDP of southern Italy, also known as the Mezzogiorno, is significantly lower than that of the rest of Italy. The marked regional divide in Italy is also evidenced by significantly higher unemployment in the Mezzogiorno. For additional information on Italian employment, see “—Employment and Labor”.

Inflation, as measured by the European Union harmonized consumer price index (HICP) was 3.3 per cent in 2012. For additional information on inflation, see “—Prices and Wages”.

Measures to Address the Global Financial and Economic Crisis

In each of 2009, 2010, 2011 and 2012, the Government acted to limit the effects of the global crisis, support the economy and facilitate its recovery. The Government also injected significant liquidity into the financial system by accelerating payment of past debts and reducing the accrual of tax refunds.

Measures adopted in 2009, 2010 and 2011

During the years 2009, 2010 and 2011, the Government adopted a series of measures aimed at increasing Government revenues, reducing Government spending, fighting tax evasion, sustaining the economic and financial growth of Italy, achieving the financing targets adopted by the EU and balancing the general government’s budget. The main reforms adopted by the Government in those years were introduced by (i) Law No. 102 of August 3, 2009, (ii) Law No. 122 of July 31, 2010, (iii) Law No. 111 of July 15, 2011 and (iv) Law No. 148 of September 14, 2011. For additional information on these measures, see Exhibit 2—2013 Stability Programme and Exhibit 3—2013 National Reform Programme.

The measures adopted by the Government in 2009, 2010 and 2011 consisted of, inter alia:

| • | tax measures, including an increase of the ordinary value-added tax (“VAT”) rate from 20 per cent to 21 per cent, an increase of the capital gains tax rate on financial instruments from 12.5 per cent to 20 per cent, with the exception of public debt instruments, which remain subject to a capital gains tax of 12.5 per cent and an additional 3 per cent tax on income exceeding €300,000; |

| • | reforms intended to reduce government spending, including Government expenditure cuts, simplifying general governmental structures, implementing a public spending review, reforming the tax and welfare systems and commencing the process to amend the Constitution to introduce a balanced budget rule; |

| • | measures to fight tax evasion, including a limit to the permissible amount of cash transactions to €2,500 or less and imposing harsher penalties for the payment of professional services without proper invoicing; and |

| • | reforms to enhance potential growth, including a reduction of bureaucratic obstacles for business organizations and the allowance of more flexible labor contracts. |

In November 2011, the Italian Parliament adopted the stability law for 2012 through Law No. 183 of November 12, 2011 and the budget law for 2012/2014 through Law No. 184 of November 12, 2011. These laws implemented several of the austerity measures previously adopted, including, among other things, reduced funding for Ministries, rules for disposing of public real estate and other measures to incentivize financial and economic growth and public deficit reduction. For additional information on the Italian budget and financial planning process, see “Public Finance—The Budget Process”.

In December 2011, the Government enacted additional measures through Law No. 214 of December 22, 2011, which consisted of, inter alia:

| • | tax measures, including a new real property tax (Imposta Municipale Unitaria or IMU) on real estate located in Italy, which will also be levied against primary residences (prima casa), further increases and adjustments to VAT rates and an increase of excise taxes on fuels; |

| • | reforms intended to reduce government spending, including changes to retirement eligibility requirements intended to align the retirement eligibility age with the average projected life span of the population and gradually equalize the retirement eligibility ages of both males and females; |

| • | measures to fight tax evasion, including strengthened investigative powers of tax authorities, new rules requiring financial intermediaries to transmit certain information with respect to customer accounts to the tax authorities and a further reduction of the permissible amount of cash transactions to €1,000 or less; and |

12

| • | reforms to enhance potential growth, including the introduction of new incentives such as an economic growth aid (ACE) that provides for a reduction of income taxes that is proportionate to the notional yield of new capital invested in a business, a reduction of labor taxes (particularly with respect to women and young workers), the establishment of policies intended to increase the employment of women and young workers and the introduction of regulations aimed at liberalizing commerce. |

Measures adopted in 2012

The Government continued adopting measures to address the global financial and economic crisis in 2012. In April 2012, Italy amended its Constitution to include a balanced budget requirement, pursuant to which the general government will be required to operate under balanced budgets beginning in fiscal year 2014. In addition, in September 2012, Italy announced its commitment to reach, within 2013, a balanced budget and reduce its public debt by increasing the primary surplus.

The main measures adopted by the Government in 2012 were introduced through (i) Law No. 27 of March 24, 2012; (ii) Law No. 35 of April 4, 2012; (iii) Law No. 92 of June 28, 2012; (iv) Law No. 134 of August 7, 2012; (v) Law No. 135 of August 7, 2012 and (vi) Law Decree No. 179 of October 18, 2012, the latter of which has been submitted to the Italian Parliament for conversion into law. For additional information on these reforms, see Exhibit 2—2013 Stability Programme and Exhibit 3—2013 National Reform Programme.

The measures adopted by the Government in 2012 consisted of, inter alia:

| • | tax measures, including a deferral of the scheduled increase of the VAT rate; |

| • | reforms intended to reduce government spending, including reduced funding to political groups and political appointees at the regional level, a reduction of the number of regional counselors, increased financial controls, various measures intended to rationalize and streamline bureaucratic processes and administrative structures and the strengthening of centralized purchasing systems; and |

| • | reforms to enhance potential growth, including measures to foster the development and growth of companies engaged in the construction and management of infrastructure and other public works, eliminate bureaucratic obstacles for professionals and entrepreneurs, facilitate access to capital markets for non-listed companies, amendments to bankruptcy laws and civil procedure, new rules and incentives for start-up companies and measures aimed at reducing labor costs and attracting increased foreign direct investment. |

On December 24, 2012, the Italian Parliament approved the stability law for 2013 through Law No. 228 of December 24, 2012 and approved the budget law for 2013/2015 through Law No. 229 of December 24, 2012, which includes measures aimed at achieving a structurally balanced budget in 2013 while increasing productivity, reducing public expenditure and intervening on certain tax regimes applicable to personal income and financial instruments. In addition, on the same date, the Italian Parliament enacted a law to implement the Constitutional balanced budget requirement through Law No. 243 of December 24, 2012 (“Law No. 243”). Law No. 243 will enter into force starting from fiscal year 2014.

Measures adopted in 2013

Law decree n. 35/2013 (converted into law on June 6, 2013) enacted a series of measures aimed at allowing the public administration to accelerate the payments of certain trade payables (overdue as of December 31, 2012) in order to stimulate economic growth. The decree authorized payments due to enterprises, cooperatives and professionals for a total of up to €40 billion, which has been subsequently increased by additional €7.2 billion through Law decree 102/2013. The injection of liquidity achieved through such acceleration is intended to have a positive effect on GDP growth, consumption and investments. For additional information on these measures, see Exhibit 2—2013 Stability Programme, Exhibit 3—2013 National Reform Programme and Exhibit 4—Update of the 2013 Economic and Financial Document.

Law decree n. 69/2013 (Decreto del Fare) (converted into law on August 9, 2013) enacted a new package of urgent measures aimed at stimulating the Italian economy, including, among other things, provisions aimed at facilitating access to credit by small and medium sized companies, measures aimed at developing infrastructure (such as the “European corridors” and certain railway services for approximately €2 billion), rules aimed at bureaucracy and tax simplification, rules aimed at enhancing the efficiency of the justice system, rules aimed at enhancing the digitalization of the public administration (the “Italian Digital Agenda”) and measures concerning education.

13

As a consequence of the fiscal measures adopted in 2012, on October 1, 2013, the VAT rate increased from 21 per cent to 22 per cent.

In October 2013, the Government approved the draft stability law for 2014 and the draft budget law for 2014/2016. These bills (disegni di legge) have been submitted to the Italian Parliament for discussion and approval. In particular, the draft stability law for 2014 includes measures aimed at sustaining economic growth and increasing employment through, inter alia, a decrease of taxes applicable to individuals and enterprises (including taxes on labor cost), the allocation of financial resources for certain strategic investments (mainly infrastructural) and the reduction of public expenditure.

In addition, the draft stability law for 2014 proposes the introduction of a new service tax to cover costs of services provided by local administrations (including waste management) to be levied by municipalities against real estate properties located in Italy which, with respect to primary residences (prima casa), shall replace the current real property tax (Imposta Municipale Unitaria or IMU).

EU Measures to Address the Eurocrisis

The global financial system began showing signs of disruption in the summer of 2007 and its condition quickly deteriorated following the bankruptcies of several major international financial institutions in the summer of 2008. Its condition continued to deteriorate and caused major disruptions in global financial markets, including unsustainably low levels of liquidity and funding sources (which resulted in high funding costs, historically high credit spreads, volatile and unsustainable capital markets and declining asset values). Many countries acted to combat deteriorating economic conditions, including borrowing in order to support troubled financial and other institutions and adopting other measures to stimulate their economies, which actions led to the credit ratings of various countries to be reduced. The first to be directly affected was Iceland in 2008 followed by Greece, Ireland and Portugal in 2010 and Spain and Italy in 2011. Such reductions to sovereign credit ratings, compounded by the existing recessionary global economy, made it difficult, or in certain instances impossible, for many European countries to access the capital markets to satisfy their funding needs. Such difficulties led to further reductions in sovereign credit ratings and the need for such countries to receive financial support from third parties, including from other countries and the financial support mechanisms adopted by the European Union. In particular, beginning in 2010, Greece, Ireland and Portugal began receiving financial assistance in the form of direct and indirect loans from EU member states. Such conditions have persisted through the date of this Annual Report. For additional information on the measures that the European Union have taken to address the Eurocrisis, see Exhibit 2—2013 Stability Programme.

The Stability and Growth Pact and the Euro Plus Pact. In March 2011, the EU Council adopted measures to respond to the economic crisis, requiring all Member States to include a multi-annual consolidation plan including specific deficit, revenue and expenditure targets and an implementation strategy and timeline in their stability or convergence programmes prepared pursuant to their existing responsibilities under the Stability and Growth Pact of 1998. For additional information on the Stability and Growth Pact of 1998, see “Public Finance—European Economic and Monetary Union”. Member States were also required to include structural reforms in their national reform programmes prepared in connection with the European Semester. For additional information on national reform programmes and the European Semester, see “Public Finance—The Budget Process”.

In addition, an agreement named the Euro Plus Pact (the “Pact”) was agreed to by the heads of government of the euro area and joined by Bulgaria, Denmark, Latvia, Lithuania, Poland and Romania (and remains open for other EU Member States to join). The Pact aimed at a closer coordination of policies for economic convergence and requires the heads of government to set common objectives in each chosen policy area and to make annual concrete national commitments. More specific objectives of the Pact are to stimulate competitiveness and employment, to enhance the sustainability of public finances and to reinforce financial stability. Italy has committed together with the other EU Member States to confirm and develop its economic policy based on the Pact and to conform and articulate its national political documentation and process based on the Pact. For additional information on Italy’s budget and financial planning process, see “Public Finance—The Budget Process”.

Financial Assistance to EU Member States. In early 2010, the EU member states began to take steps to provide financial assistance to troubled European Member States. As Greece slipped into a deep recession and came close to defaulting on financial obligations, in May of 2010 the EU provided, on a coordinated bilateral basis, a first round of loans to Greece through a three-year plan (2010 to 2013) for a total commitment of €80 billion. Italy’s portion of the total commitment equaled €14.7 billion. Of the €80 billion, €21 billion was disbursed in 2010 and €31.9 billion in 2011. At the same time the International Monetary Fund (the “IMF”) undertook to provide Greece with an additional €30 billion in loans, €10.5 billion of which was lent in 2010 and €9.6 billion in 2011. As of December 31, 2011, Italy’s exposure to Greece through direct loans was just over €10 billion.

14

The EFSF. In June 2010, the EU member states created the European Financial Stability Facility (the “EFSF”) whose objective is to “preserve financial stability of Europe’s monetary union by providing temporary assistance to euro area Member States”. In order to fund any such assistance the EFSF has the capacity to issue bonds or other debt instruments in the financial markets. Such debt is guaranteed by each Member State on a several basis based on each Member State’s participation in the ECB’s share capital. Initially the extent of the guarantees (and therefore of the facility itself) was capped at €440 billion. Italy’s participation in the EFSF is approximately 18 per cent. Pursuant to a ruling of Eurostat, financings granted by the EFSF cause an increase of public debt of the countries participating in the financing, based on their participation in the ECB’s share capital.

The EFSF financings are combined with those from the European Financial Stabilization Mechanism (the “EFSM”), a €60 billion facility organized by the European Commission, and additional financings from the IMF. The EFSM allows the European Commission to borrow in financial markets on behalf of the Union and then lend the proceeds to the beneficiary Member State. All interest and loan principal is repaid by the beneficiary Member State via the European Commission. The EU budget guarantees the repayment of the bonds in case of the default by the borrower. The EFSF, EFSM and IMF can only act after a request for support is made by a euro area Member State and a country program has been negotiated with the European Commission and the IMF. As a result, any financial assistance by the EFSF, EFSM and IMF to a country in need is linked to strict policy conditions. The EFSF and EFSM may only grant new financings until June 2013; after this date, only existing financings may be administered. During 2011, the EFSM began issuing bonds backed by EU budgetary resources in order to finance the loan package agreed in November 2010 in favor of Ireland and the loan package agreed in May 2011 in favor of Portugal. The EFSM issued approximately €28 billion in bonds in 2011 in order to provide loans of 13.9 billion to Ireland and €14.1 billion to Portugal. Also during 2011, the EFSF issued approximately €18 billion of securities in order to grant loans of €7.6 billion to Ireland and €6.9 billion to Portugal. In addition to the loans provided by the EFSM and the EFSF, the IMF made loans of €12.5 billion to Ireland and €13 billion to Portugal.

A set of measures designed to increase the EFSF’s capacity were approved during the course of 2011: (a) the guarantees provided by the euro area countries were raised from €440 billion to €780 billion; (b) the facility was authorized to make purchases of Member States’ government bonds in the primary and secondary markets; (c) it was authorized to take action under precautionary programmes and to finance the recapitalization of financial institutions; and (d) it will be allowed to use the leverage options offered by granting partial risk protection on new government bond issues by euro area countries and/or by setting up one or more vehicles to raise funds from investors and financial institutions. In early 2012, Greece, having enacted the budget and other reform measures required by the EU, reached a further agreement with the European Commission, the ECB and IMF for a second round of financial support, which consisted of €138 billion in loans from the IMF and the EFSF over the period 2012 to 2016. This second round of financial support differed from the package Greece received in May 2010, in that it received loans directly from the EFSF rather than directly from Member States. In May 2012, Greece had received approximately €72.9 billion from the EFSF. Greece also received an additional €1.7 billion from the IMF.

Also in 2012, the EFSF provided financial support for Ireland and Portugal. Ireland received €13.8 billion, of which €4.6 billion came from the EFSF while the EFSM provided €4.5 billion and the IMF provided €3.6 billion. Ireland also received bilateral loans directly from the United Kingdom and Denmark for a further €1 billion. Portugal received €14.3 billion, of which €6 billion came from the EFSM, €2.7 billion from the EFSF and €5.6 billion from the IMF.

The ESM. From July 2013, the European Stability Mechanism (“ESM”), a facility with lending capacity of €500 billion, will assume the role of the EFSF and the EFSM. The ESM will have a subscribed capital of €700 billion, of which €80 billion will be paid-in capital provided by the euro area Member States and €620 billion will be committed callable capital and guarantees from euro area Member States, who will commit to maintain a minimum 15 per cent ratio of paid-in capital to outstanding amount of ESM issuances in the transitional phase from 2013 to 2017. Italy’s maximum commitment to the ESM will be approximately €125.3 billion. The ESM will grant financings to requesting countries in the euro area under strict conditions and following a debt sustainability analysis.

On February 2, 2012, a number of revisions were made to the treaty instituting the ESM. Its entry into force was brought forward by one year, to July 2012, and the voting rules were amended to allow decisions to be taken by a qualified majority of 85 per cent in certain circumstances. This majority rule can be invoked in

15

place of the requirement of unanimous decisions if the European Commission and the ECB determine that financial assistance measures need to be taken urgently and in the interests of the euro area’s financial and economic stability. Furthermore, as in the case of the EFSF, the ESM has additional means available to it to support countries in difficulty: it can purchase member countries’ government bonds, both directly or on the secondary market, and is allowed greater flexibility in its direct purchases of government bonds; it can take action under precautionary programmes; and it can finance the recapitalization of financial institutions. Finally, in order to strengthen investors’ confidence in the new arrangements, on March 30, 2012 the EU announced that the ESM’s endowment capital would be paid up by 2014 instead of 2017 as originally planned. Payment will be made in five installments, two in 2012, two in 2013 and the last in the first half of 2014. It was also agreed that as of July 2012 the ESM will become the main instrument for financing new support packages. The EFSF will continue to operate until existing financing arrangements terminate and it will be allowed to finance new projects until halfway through next year. From the middle of 2014, the ESM will have a total lending capacity of €500 billion. While the EU had anticipated that the ESM would be operational in July 2012, complications in the ratification of the treaty establishing the ESM led to delays. In particular, Germany’s Federal Constitutional Court took into consideration whether Germany could ratify the treaty in compliance with its constitution. On September 12, 2012, the German Federal Constitutional Court ruled that Germany could ratify the treaty, so long as the treaty was amended slightly to make it clear that the contribution of a Member State could not be increased “without the prior agreement of each Member State and with due regard to national procedures”. The EU finance ministers agreed to an “interpretive declaration” to this effect on September 27, 2012. The Board of Governors of the ESM met for the first time on October 8, 2012 and has become the main European instrument for financing new support programmes.

Collective Action Clauses. Following recommendations of the International Monetary Fund and the release of a draft model form of collective action clause, Italy introduced a form of collective action clause into the documentation of all of its New York law governed bonds issued since June 16, 2003.