Filed by: International Paper Company

Pursuant to Rule 425 under the Securities Act of 1933

Subject Company: Smurfit Kappa Group Plc

Subject Company Commission File No.: 333-178633

Date: March 26, 2018

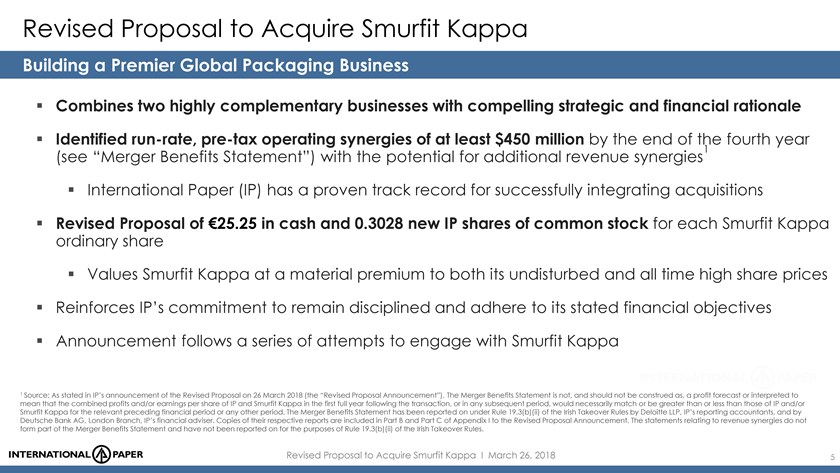

Building a Premier Global Packaging Business

Revised Proposal to Acquire Smurfit Kappa I March 26, 2018

No offer or solicitation

This presentation is provided for informational purposes only and is not intended to and does not constitute an offer to subscribe for or purchase nor a

solicitation of an offer to sell or the solicitation of any vote or approval in any jurisdiction in respect of, shares of International Paper Company (“International Paper“ or “IP”) or Smurfit Kappa Group plc (“Smurfit

Kappa”). Further to the announcement by IP on 6 March 2018 of its possible offer to acquire the entire issued and to be issued share capital of Smurfit Kappa (the “Possible Offer”): (i) any offer for Smurfit Kappa would, if it is

proposed to implement the offer by way of a scheme of arrangement, be made pursuant to the terms of a circular to be issued by Smurfit Kappa to its shareholders in due course setting out the terms and conditions of the offer, including details of

how to vote in respect of the offer (“Circular”) or, in the event that IP determines to conduct the acquisition pursuant to a takeover offer, be made pursuant to the terms of a takeover offer document to be despatched by IP to Smurfit

Kappa shareholders in due course setting out the terms and conditions of the offer, including details of how to accept the offer (“Takeover Offer Document”); and (ii) if an offer is made, IP may, to the extent required, publish a

prospectus for the purposes of EU Directive 2003/71/EC (together with any applicable implementing measures in any Member State, the “Prospectus Directive”) in relation to shares which will be issued by it in connection with the offer

(“Prospectus”). Any decision in respect of, or in response to, the Possible Offer or any subsequent offer should be made only on the basis of the information in a Circular (or Takeover Offer Document, if appropriate) and Prospectus issued

for the purpose of such offer. Investors are advised to read any such Circular (or Takeover Offer Document, if appropriate) and Prospectus carefully.

This

presentation is not intended to and does not constitute a prospectus for the purposes of the Prospectus Directive. Accordingly, investors should not subscribe for, or purchase, any securities referred to in this presentation except on the basis of

the information to be contained in the Prospectus, which, if published, will be prepared in accordance with the Prospectus Directive. Copies of the Prospectus, if published, will be available from IP’s website at

(http://investor.internationalpaper.com/investor-relations/Smurfit-Kappa-Proposal/).

Restrictions on certain information under the Irish Takeover Rules

Smurfit Kappa is a company subject to the jurisdiction of the Irish Takeover Panel Act, 1997, Takeover Rules 2013 (“Irish Takeover Rules”). Under the Irish Takeover

Rules, IP management is prohibited from discussing any material information or significant new opinions which have not been publicly announced. Any person interested in securities of Smurfit Kappa or IP is encouraged to consult their professional

advisers.

Statements required by the Irish Takeover Rules

The directors of IP

accept responsibility for the information contained in this presentation, save that the only responsibility accepted by the Directors of IP in respect of the information in this presentation relating to Smurfit Kappa, the Smurfit Kappa group, the

Smurfit Kappa board and persons connected with them, which has been compiled from published sources, has been to ensure that such information has been correctly and fairly reproduced or presented (and no steps have been taken by the Directors of IP

to verify such information). To the best of their knowledge and belief (having taken all reasonable care to ensure that such is the case), the information contained in this presentation for which they accept responsibility is in accordance with the

facts and does not omit anything likely to affect the import of such information.

Disclosure requirements of the Irish Takeover Rules

Under the provisions of Rule 8.3 of the Irish Takeover Rules, if any person is, or becomes, “interested” (directly or indirectly) in, 1% or more of any class of

“relevant securities” of Smurfit Kappa or IP, all “dealings” in any “relevant securities” of Smurfit Kappa or IP (including by means of an option in respect of, or a derivative referenced to, any such “relevant

securities”) must be publicly disclosed by no later than 3.30pm (Irish/UK time) in respect of “relevant securities” of Smurfit Kappa and 3.30pm (New York time) in respect of “relevant securities” of IP on the

“business” day following the date of the relevant transaction. This requirement will continue until the “offer period” ends. If two or more persons co-operate on the basis of any agreement,

either express or tacit, either oral or written, to acquire an “interest” in “relevant securities” of Smurfit Kappa or IP, they will be deemed to be a single person for the purposes of Rule 8.3 of the Irish Takeover Rules.

Under the provisions of Rule 8.1 of the Irish Takeover Rules, all “dealings” in “relevant securities” of Smurfit Kappa by IP or “relevant

securities” of IP by Smurfit Kappa, or by any party “acting in concert” with either of them, must also be disclosed by no later than 12 noon (Irish/UK time) in respect of “relevant securities” of Smurfit Kappa and 12 noon

(New York time) in respect of “relevant securities” of IP on the “business” day following the date of the relevant transaction. A disclosure table, giving details of the companies in whose “relevant securities”

“dealings” should be disclosed, can be found on the Irish Takeover Panel’s website at www.irishtakeoverpanel.ie.

“Interests in securities”

arise, in summary, when a person has a long economic exposure, whether conditional or absolute, to changes in the price of securities. In particular, a person will be treated as having an “interest” by virtue of the ownership or control of

securities, or by virtue off any option in respect of, or derivative referenced to, securities.

Terms in quotation marks are defined in the Irish Takeover Rules,

which can also be found on the Irish Takeover Panel’s website. If you are in any doubt as to whether or not you are required to disclose dealings under Rule 8, please consult with the Irish Takeover Panel’s website at

www.irishtakeoverpanel.ie or contact the Irish Takeover Panel by telephone on +353 1 678 9020.

Revised Proposal to Acquire Smurfit Kappa I March 26, 2018

No profit forecast / asset valuations

No statement in this presentation is intended to constitute a profit forecast for any period nor should any statements be interpreted to mean that profits and/or or earnings per

share will necessarily be greater or lesser than those for the relevant preceding financial periods for IP or Smurfit Kappa as appropriate. No statement in this presentation constitutes an asset valuation.

The statements that the Revised Proposal meets IP’s objectives for the combined company of earnings per share accretion in the first full year, free cash flow enhancement in

the first full year and return on invested capital exceeding IP’s weighted average cost of capital by the third year are not, nor should they be construed as, profit forecasts for the purposes of the Irish Takeover Rules and should not be

interpreted to mean that profits and/or earnings per share will necessarily be greater or lesser than those for the relevant preceding financial periods. The statements are not, nor should they be construed as, estimates of the anticipated financial

effects of the Revised Proposal, if completed, and accordingly have not been reported on for the purposes of Rule 19.3(b)(ii) of the Irish Takeover Rules. No quantification of the level of accretion, free cash flow enhancement, return on invested

capital or weighted average cost of capital has been provided by IP, nor has any base figure against which such accretion, free cash flow enhancement, return on invested capital or weighted average cost of capital may be determined been provided.

Forward-looking statements

Certain statements in this presentation may be

considered forward-looking statements. Words such as “expects”, “anticipates”, “estimates” and similar expressions identify forward-looking statements. The forward-looking statements include, but are not limited to,

information regarding the ability of IP to complete the transaction, the estimated and anticipated impact of the transaction on IP’s future results of operations (including earnings per share, free cash flow), return on investment, cost of

capital, estimated synergies, credit ratings, costs, opportunity for growth, nature of the combined company, leverage ratios, and dividends. These statements reflect management’s current views and are subject to risks and uncertainties that

could cause actual results to differ materially from those expressed or implied in these statements. Factors which could cause actual results to differ include but are not limited to: (i) the level of indebtedness and changes in interest rates;

(ii) industry conditions, including but not limited to changes in the cost or availability of raw materials, energy and transportation costs, competition faced, cyclicality and changes in consumer preferences, demand and pricing for IP

products; (iii) global economic conditions and political changes, including but not limited to the impairment of financial institutions, changes in currency exchange rates, credit ratings issued by recognized credit rating organizations, the

amount of future pension funding obligation, changes in tax laws and pension and health care costs; (iv) unanticipated expenditures related to the cost of compliance with existing and new environmental and other governmental regulations and to

actual or potential litigation; (v) whether IP experiences a material disruption at one of its manufacturing facilities; (vi) risks inherent in conducting business through joint ventures; (vii) ability to achieve the benefits expected

from strategic acquisitions, divestitures and restructurings; (viii) the outcome of consultations with employees required by applicable law; and (ix) other factors that can be found in IP’s press releases and U.S. Securities and

Exchange Commission (the “SEC”) filings. These and other factors that could cause or contribute to actual results differing materially from such forward-looking statements are discussed in greater detail in IP’s SEC filings. IP

undertakes no obligation to publicly update any forward-looking statements, whether as a result of new information, future events or otherwise.

Merger benefit

statement

There are various material assumptions underlying the statement that IP expects that the acquisition of Smurfit Kappa will result in total run-rate pre-tax operating synergies of at least $450 million by the end of the fourth year following completion (the “Merger Benefits Statement”), which may

result in the value of the Merger Benefits Statement being materially greater or less than estimated. The Merger Benefits Statement should therefore be read in conjunction with the key assumptions underlying the statement which are set out in Part A

of Appendix I to IP’s announcement pursuant to Rule 2.4 of the Irish Takeover Rules on 26 March 2018 (the “Revised Proposal Announcement”).

The

Merger Benefits Statement is not, and should not be construed as, a profit forecast or interpreted to mean that the combined profits and/or earnings per share of IP and Smurfit Kappa in in the first full year following the transaction, or in any

subsequent period would necessarily match or be greater than or less than those of IP and/or Smurfit Kappa for the relevant preceding financial period or any other period.

The Merger Benefits Statement has been reported on for the purposes of Rule 19.3(b)(ii) of the Irish Takeover Rules by Deloitte LLP, IP’s reporting accountants, and by

Deutsche Bank AG, London Branch, IP’s financial adviser. Copies of their respective reports are included in Part B and Part C of Appendix I of the Revised Proposal Announcement.

Publication on website

Pursuant to Rule 19.9 of the Irish Takeover Rules, this presentation

will be made available (including to IP’s employees) on IP’s website (http://investor.internationalpaper.com/investor-relations/Smurfit-Kappa-Proposal). Neither the contents of IP’s website, nor the contents of any other website

accessible from hyperlinks on such websites, is incorporated herein or forms part of this presentation.

Statements Relating to

Non-GAAP Measures

During the course of this presentation, certain non U.S. GAAP financial measures will be presented, such

as Adjusted Operating EPS, Adjusted EBIT, Adjusted EBITDA, Adjusted EBITDA Margin, Free Cash Flow and Adjusted ROIC. A reconciliation of all presented non-GAAP measures (and their components) to U.S. GAAP

financial measures is available on the company’s website at internationalpaper.com under Performance/Investors.

Revised Proposal to Acquire Smurfit Kappa I

March 26, 2018

Employee consultation

No

potential options, proposals, analysis and costings in this presentation are, or should be deemed to be, an indication that any decision has been made to implement any course of action that could affect employees. No final decisions will be made

until legally required employee consultation has concluded.

Important Additional Information

In connection with a potential acquisition by IP of Smurfit Kappa that is carried out by way of a scheme of arrangement (“Scheme”), the new IP shares to be issued to

Smurfit Kappa shareholders under the terms of the Scheme have not been, and will not be, registered under the U.S. Securities Act of 1933 or under the securities laws of any state, district or other jurisdiction of the United States. It is expected

that the new IP shares would be issued in reliance upon the exemption from the registration requirements of the U.S. Securities Act of 1933 provided by Section 3(a)(10) thereof. Nothing in this presentation should be construed as meaning that

the potential acquisition will be carried out by a scheme of arrangement, or at all.

In the event that a Scheme does not qualify (or IP otherwise elects pursuant

to its right to proceed with the transaction in a manner that does not qualify) for an exemption from the registration requirements of the U.S. Securities Act of 1933, IP would expect to register the offer and sale of the securities it would issue

to Smurfit Kappa’s shareholders by filing with the SEC a registration statement on Form S-4 (the “Registration Statement”), which would contain the Prospectus, as well as other relevant

materials (the “Tender Offer Documents”). No such materials have yet been filed. This communication is not a substitute for any Registration Statement or Prospectus that IP may file with the SEC. INVESTORS AND SECURITY HOLDERS ARE URGED TO

READ THE TENDER OFFER DOCUMENTS AND ALL OTHER RELEVANT DOCUMENTS THAT IP OR SMURFIT KAPPA HAS FILED OR MAY FILE WITH THE SEC WHEN THEY BECOME AVAILABLE BECAUSE THEY CONTAIN OR WILL CONTAIN IMPORTANT INFORMATION THAT INVESTORS AND SECURITY HOLDERS

SHOULD CONSIDER BEFORE MAKING ANY DECISION REGARDING THE PROPOSED ACQUISITION.

The information contained in this document must not be published, released or

distributed, directly or indirectly, in any jurisdiction where the publication, release or distribution of such information is restricted by laws or regulations. Therefore, persons in such jurisdictions into which these materials are published,

released or distributed must inform themselves about and comply with such laws or regulations. IP does not accept any responsibility for any violation by any person of any such restrictions. The Tender Offer Documents and other documents referred to

above, if filed or furnished by IP with the SEC, as applicable, will be available free of charge at the SEC’s website (www.sec.gov) or by writing to IP, 6400 Poplar Ave Memphis, TN 38197, United States.

Revised Proposal to Acquire Smurfit Kappa

Building a Premier Global Packaging Business

Combines two highly complementary businesses with

compelling strategic and financial rationale Identified run-rate, pre-tax operating synergies of at least $450 million by the end of the fourth year

(see “Merger Benefits Statement”) with the potential for additional revenue synergies1

International Paper (IP) has a proven track record for successfully integrating acquisitions

Revised Proposal of €25.25 in cash and 0.3028 new IP shares of common stock for each Smurfit Kappa ordinary share

Values Smurfit Kappa at a material premium to both its undisturbed and all time high share prices

Reinforces IP’s commitment to remain disciplined and adhere to its stated financial objectives Announcement follows a series of attempts to engage with Smurfit Kappa

1 Source: As stated in IP’s announcement of the Revised Proposal on 26 March 2018 (the “Revised Proposal Announcement”). The Merger Benefits

Statement is not, and should not be construed as, a profit forecast or interpreted to mean that the combined profits and/or earnings per share of IP and Smurfit Kappa in the first full year following the transaction, or in any subsequent period,

would necessarily match or be greater than or less than those of IP and/or Smurfit Kappa for the relevant preceding financial period or any other period. The Merger Benefits Statement has been reported on under Rule 19.3(b)(ii) of the Irish Takeover

Rules by Deloitte LLP, IP’s reporting accountants, and by Deutsche Bank AG, London Branch, IP’s financial adviser. Copies of their respective reports are included in Part B and Part C of Appendix I to the Revised Proposal Announcement. The

statements relating to revenue synergies do not form part of the Merger Benefits Statement and have not been reported on for the purposes of Rule 19.3(b)(ii) of the Irish Takeover Rules.

Revised Proposal to Acquire Smurfit Kappa I March 26, 2018 5

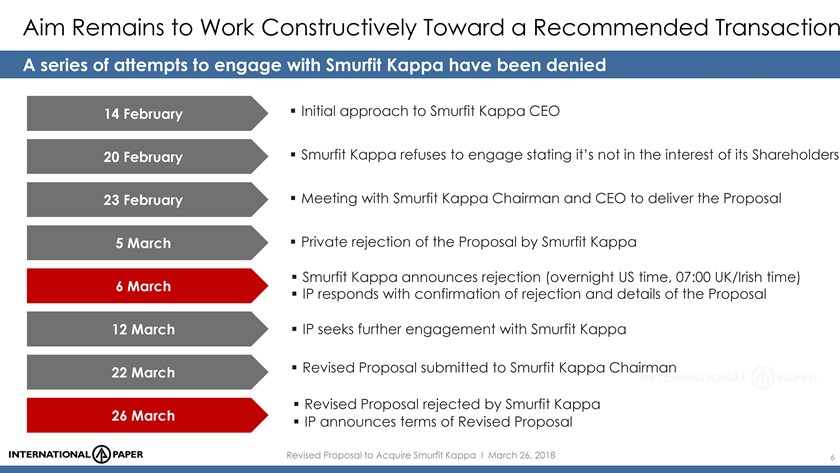

Aim Remains to Work Constructively Toward a Recommended Transaction

A series of attempts to engage with Smurfit Kappa have been denied

14 February Initial

approach to Smurfit Kappa CEO

20 February Smurfit Kappa refuses to engage stating it’s not in the interest of its Shareholders

23 February Meeting with Smurfit Kappa Chairman and CEO to deliver the Proposal

5 March Private rejection of the Proposal by Smurfit Kappa

Smurfit Kappa

announces rejection (overnight US time, 07:00 UK/Irish time)

6 March

IP

responds with confirmation of rejection and details of the Proposal

12 March IP seeks further engagement with Smurfit Kappa

22 March Revised Proposal submitted to Smurfit Kappa Chairman Revised Proposal rejected by Smurfit Kappa

26 March IP announces terms of Revised Proposal

Revised Proposal to Acquire Smurfit Kappa

I March 26, 2018 6

Building a Premier Global Packaging Business

Combination is highly complementary and offers compelling strategic and financial rationale

Global platform well positioned to capture growth in expanding containerboard and Improves access to attractive markets in corrugated packaging markets the most

profitable geographies Delivers enhanced supply chain

Creates a

global leader wit solutions to benefit both local, advantaged assets and a regional and global customers to low cost virgin and recovered fiber Brings together two highly Complementary fit facilitates capable teams with shared improved vertical

integration core values

Accelerates capture of secula s two world

class package by e-commerce, consumer fresh food consumption design innovators with the commercial and corrugated packaging as a sustainable solution expertise to deliver superior customer solutions

Revised Proposal to Acquire Smurfit Kappa I March 26, 2018

Creating a Global Containerboard Leader

Combined system capacity of 19MM tonnes of kraftliner and recycled containerboard

Europe

Ilim JV 1MM

Americas Kraftliner tonnes

30% kraftliner

~

Recycled

~40% IP

Smurfit 5.0MM

Kappa Tonnes

Recycled

~70% IP

14.0MM Smurfit

Tonnes Kappa

Kraftliner

~60% ~185 Box Plants

~215 Box Plants

Note: Please refer to the Annex to this presentation for the sources and bases

of calculation for figures presented

Revised Proposal to Acquire Smurfit Kappa I March 26, 2018

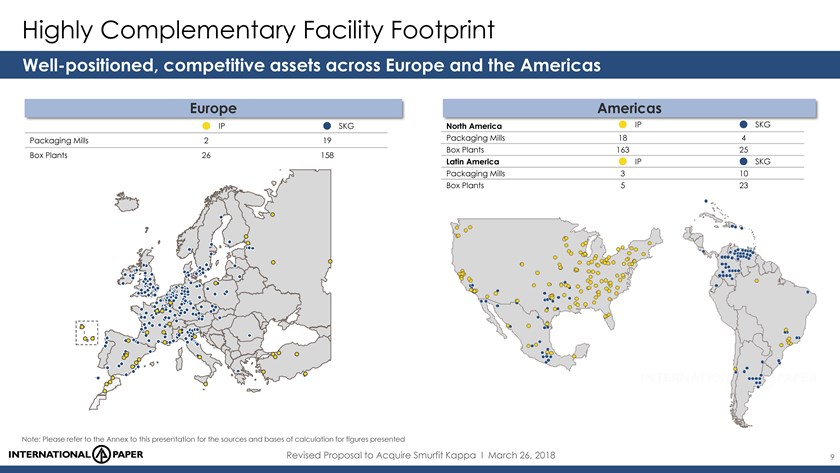

Highly Complementary Facility Footprint

Well-positioned, competitive assets across Europe and the Americas

Europe Americas

IP SKG North America IP SKG Packaging Mills 2 19 Packaging Mills 18 4 Box Plants 163 25 Box Plants 26 158

Latin America IP SKG Packaging Mills 3 10 Box Plants 5 23

Note: Please refer to the Annex to

this presentation for the sources and bases of calculation for figures presented

Revised Proposal to Acquire Smurfit Kappa I March 26, 2018 9

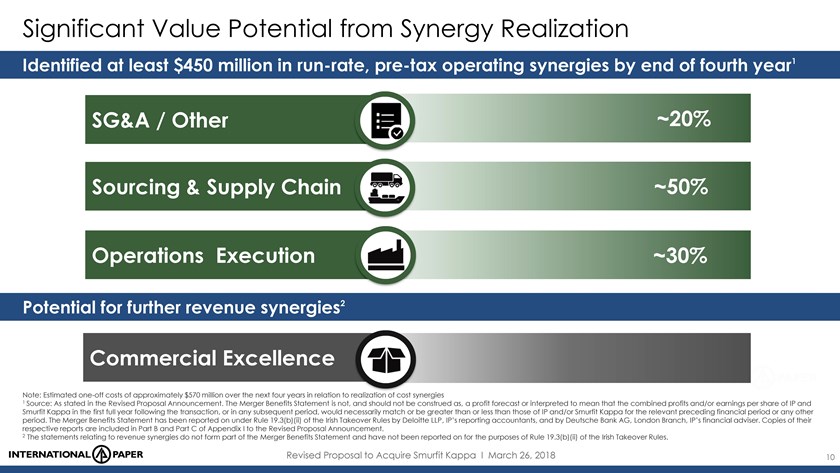

Significant Value Potential from Synergy Realization

Identified at least $450 million in run-rate, pre-tax operating synergies by end of fourth

year1

SG&A / Other ~20%

Sourcing & Supply Chain ~50%

Operations Execution ~30%

Potential for further revenue synergies2

Commercial Excellence

Note: Estimated one-off costs of

approximately $570 million over the next four years in relation to realization of cost synergies

1 Source: As stated in the Revised Proposal Announcement. The

Merger Benefits Statement is not, and should not be construed as, a profit forecast or interpreted to mean that the combined profits and/or earnings per share of IP and Smurfit Kappa in the first full year following the transaction, or in any

subsequent period, would necessarily match or be greater than or less than those of IP and/or Smurfit Kappa for the relevant preceding financial period or any other period. The Merger Benefits Statement has been reported on under Rule 19.3(b)(ii) of

the Irish Takeover Rules by Deloitte LLP, IP’s reporting accountants, and by Deutsche Bank AG, London Branch, IP’s financial adviser. Copies of their respective reports are included in Part B and Part C of Appendix I to the Revised

Proposal Announcement.

2 The statements relating to revenue synergies do not form part of the Merger Benefits Statement and have not been reported on for the

purposes of Rule 19.3(b)(ii) of the Irish Takeover Rules.

Revised Proposal to Acquire Smurfit Kappa I March 26, 2018 10

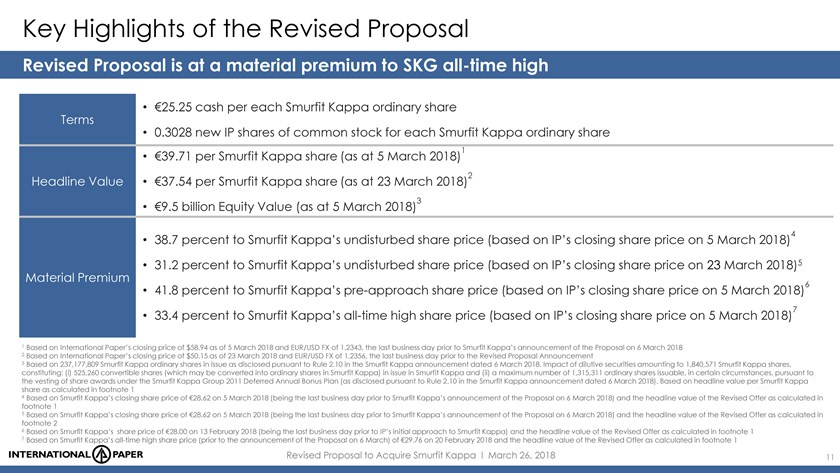

Key Highlights of the Revised Proposal

Revised Proposal is at a material premium to SKG all-time high

€25.25 cash per each Smurfit Kappa ordinary share Terms

0.3028 new IP shares of common

stock for each Smurfit Kappa ordinary share (as 2018)1

€39.71 per Smurfit Kappa share at 5 March

Value 2 Headline €37.54 per Smurfit Kappa share (as at 23 March 2018) €9.5 billion Equity Value 3

(as at 5 March 2018)

2018)4

38.7 percent to Smurfit Kappa’s undisturbed share price (based on IP’s closing share price on 5 March

31.2 percent to Smurfit Kappa’s undisturbed share price (based on IP’s closing share price on 23 March 2018)5

Material Premium

6

41.8 percent to Smurfit Kappa’s pre-approach share price (based on IP’s closing share price on 5 March 2018)

33.4 percent to Smurfit Kappa’s all-time high share price (based on IP’s closing share price on 5 March 2018)7

1 Based on International Paper’s closing price of $58.94 as of 5 March 2018 and EUR/USD FX of 1.2343, the last business day prior to Smurfit Kappa’s announcement of

the Proposal on 6 March 2018

2 Based on International Paper’s closing price of $50.15 as of 23 March 2018 and EUR/USD FX of 1.2356, the last

business day prior to the Revised Proposal Announcement

3 Based on 237,177,809 Smurfit Kappa ordinary shares in issue as disclosed pursuant to Rule 2.10 in the

Smurfit Kappa announcement dated 6 March 2018. Impact of dilutive securities amounting to 1,840,571 Smurfit Kappa shares, constituting: (i) 525,260 convertible shares (which may be converted into ordinary shares in Smurfit Kappa) in issue in

Smurfit Kappa and (ii) a maximum number of 1,315,311 ordinary shares issuable, in certain circumstances, pursuant to the vesting of share awards under the Smurfit Kappa Group 2011 Deferred Annual Bonus Plan (as disclosed pursuant to Rule 2.10

in the Smurfit Kappa announcement dated 6 March 2018). Based on headline value per Smurfit Kappa share as calculated in footnote 1

4 Based on Smurfit

Kappa’s closing share price of €28.62 on 5 March 2018 (being the last business day prior to Smurfit Kappa’s announcement of the Proposal on 6 March 2018) and the headline value of the Revised Offer as calculated in footnote

1

5 Based on Smurfit Kappa’s closing share price of €28.62 on 5 March 2018 (being the last business day prior to Smurfit Kappa’s announcement

of the Proposal on 6 March 2018) and the headline value of the Revised Offer as calculated in footnote 2

6 Based on Smurfit Kappa’s share price of

€28.00 on 13 February 2018 (being the last business day prior to IP’s initial approach to Smurfit Kappa) and the headline value of the Revised Offer as calculated in footnote 1

7 Based on Smurfit Kappa’s all-time high share price (prior to the announcement of the Proposal on 6 March) of €29.76 on

20 February 2018 and the headline value of the Revised Offer as calculated in footnote 1

Revised Proposal to Acquire Smurfit Kappa I March 26, 2018 11

Firm Commitment to Financial Objectives and Value Creation

Proposal aligns with International Paper’s disciplined approach to capital allocation

 EPS accretive in the first full year



Free Cash Flow enhancement in the first full year ROIC > WACC by the third year  Continued alignment with current Dividend Policy

 Continued commitment to strong Balance Sheet

Strong FCF generation enables

rapid deleveraging post completion Investment grade credit rating

1 The statements that the Revised Proposal meets IP’s objectives for the combined company of

earnings per share accretion in the first full year, free cash flow enhancement in the first full year and return on invested capital exceeding IP’s weighted average cost of capital by the third year are not, nor should they be construed as,

profit forecasts for the purposes of the Irish Takeover Rules and should not be interpreted to mean that profits and/or earnings per share will necessarily be greater or lesser than those for the relevant preceding financial periods. The statements

are not, nor should they be construed as, estimates of the anticipated financial effects of the Revised Proposal, if completed, and accordingly have not been reported on for the purposes of Rule 19.3(b)(ii) of the Irish Takeover Rules. No

quantification of the level of accretion, free cash flow enhancement, return on invested capital or weighted average cost of capital has been provided by IP, nor has any base figure against which such accretion, free cash flow enhancement, return on

invested capital or weighted average cost of capital may be determined been provided.

Revised Proposal to Acquire Smurfit Kappa I March 26, 2018 12

Full Alignment with International Paper’s Framework for Value Creation

Disciplined approach to acquisitions with clearly defined strategic and financial objectives

Fiber-based Packaging, Pulp and Paper

Advantaged Positions Attractive Markets

Shareholder Value

Low cost, competitive assets Good market growth rates Delivers strong and sustainable free cash flows

Operational excellence Customers and markets that value our products and innovations Increases intrinsic value with Availability and access to low return spreads above our cost

cost, sustainable fiber Strong growing supply positions of capital (ROIC > WACC) Capability to provide both Access to the best global Supports policies to return differentiated and innovative customers and segments capital to shareholders value

propositions Strong balance sheet Opportunity for optimization and productivity gains

Renewable Natural Resources

Revised Proposal to Acquire Smurfit Kappa I March 26, 2018 13

Appendix

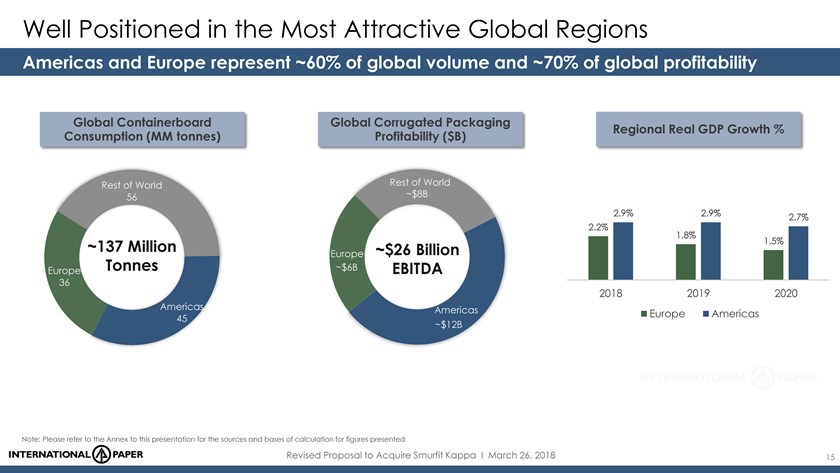

Well Positioned in the Most Attractive Global Regions

Americas and Europe represent ~60% of global volume and ~70% of global profitability

Global

Containerboard Global Corrugated Packaging

Regional Real GDP Growth % Consumption (MM tonnes) Profitability ($B)

Rest of World Rest of World

56 ~$8B

2.9% 2.9% 2.7% 2.2% 1.8%

~137 Million ~$26 Billion 1.5%

Europe

Europe Tonnes ~$6B EBITDA 36

2018 2019 2020

Americas Americas

45 Europe Americas

~$12B

~$12B

Note: Please refer to the Annex to this presentation for the sources and bases of

calculation for figures presented

Revised Proposal to Acquire Smurfit Kappa I March 26, 2018 15

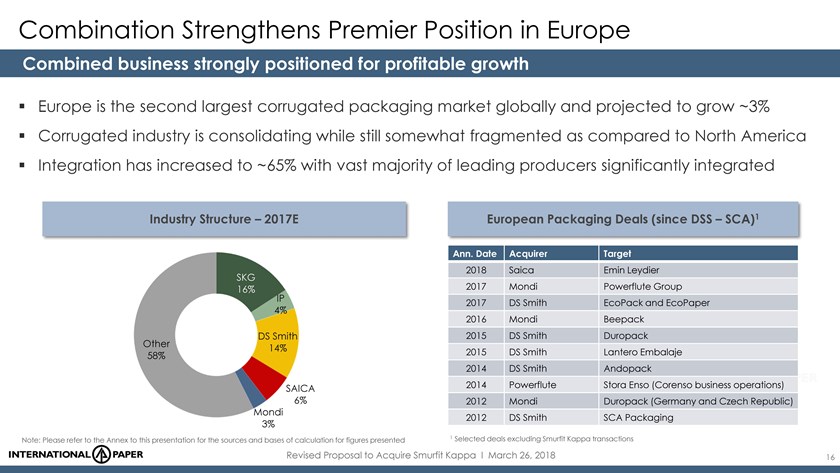

Combination Strengthens Premier Position in Europe

Combined business strongly positioned for profitable growth

Europe is the second largest

corrugated packaging market globally and projected to grow ~3% Corrugated industry is consolidating while still somewhat fragmented as compared to North America Integration has increased to ~65% with vast majority of leading producers significantly

integrated

Industry Structure – 2017E European Packaging Deals (since DSS – SCA)1

Ann. Date Acquirer Target

2018 Saica Emin Leydier SKG 2017 Mondi Powerflute Group

16% IP

2017 DS Smith EcoPack and EcoPaper

4% 2016 Mondi Beepack DS Smith 2015 DS Smith Duropack

Other 14%

58% 2015 DS Smith Lantero Embalaje 2014 DS Smith Andopack

SAICA 2014 Powerflute Stora Enso

(Corenso business operations)

6% 2012 Mondi Duropack (Germany and Czech Republic)

Mondi

2012 DS Smith SCA Packaging

3%

Note: Please refer to the Annex to this presentation for the sources and bases of

calculation for figures presented 1 Selected deals excluding Smurfit Kappa transactions

Revised Proposal to Acquire Smurfit Kappa I March 26, 2018 16

Leading Pan-regional Supplier of Corrugated Latin America

Combination increases exposure to the best markets in Latin America

Sizeable and populous

region

Regional corrugated consumption of ~13 million tonnes Growth prospects across region are >3%

International Paper Position Smurfit Kappa Position Combined Business

Venezuela Venezuela

9% 6%

Brazil, Brazil, Brazil, Argentina, Argentina, Mexico Argentina,

0.6MM Chile 1.7MM 47% Chile 2.3MM Mexico Chile 21% 27% 49%

Tonnes Mexico

Tonnes Tonnes

45%

55%

Colombia, Colombia, Caribbean Caribbean 23% 17%

Note: Please refer to the Annex to this

presentation for the sources and bases of calculation for figures presented

Revised Proposal to Acquire Smurfit Kappa I March 26, 2018 17

Combined Business Positioned for Profitable Growth

Combination enhances capability for differentiated and innovative value propositions

Secular

Growth Drivers E-commerce / Distribution

E-commerce as key retail channel Consumer

consumption trends, preferences & convenience Corrugated as sustainable solution

Key Corrugated Segments Shelf-Ready Retail Fresh Food

E-commerce

Fresh Food – Protein and

Fruits & Vegetables Shelf-ready retail

Revised Proposal to Acquire Smurfit Kappa I March 26, 2018 18

Proven Track Record of Successful Integration

Exceeded synergy commitments, more and faster, in prior transactions

Weyerhaeuser Temple

Inland Weyerhaeuser

Cellulose Fibers (2016) Smurfit Kappa Packaging (2008) Packaging (2012)

15% of sales

12% of sales

End of

9% 10% of sales Year 1 of sales

4 Years

8% of sales 8% of sales

End of End of Year 1 Year 1

3 Years 2 Years 2 Years 2

5% of sales $400 $490 $300 $400 $175 $205 4 Years million in million in million in million in million in million in synergies synergies synergies synergies 1 synergies synergies

$450 million in synergies

Commitment Achieved Commitment Achieved Commitment Achieved Commitment

Note: Please refer to the Annex to this presentation for the sources and bases of calculation for figures presented

1 Source: As stated in the Revised Proposal Announcement. Estimated run-rate pre-tax operating

synergies of $450 million by end of year four. The Merger Benefits Statement is not, and should not be construed as, a profit forecast or interpreted to mean that the combined profits and/or earnings per share of IP and Smurfit Kappa in the

first full year following the transaction, or in any subsequent period, would necessarily match or be greater than or less than those of IP and/or Smurfit Kappa for the relevant preceding financial period or any other period. The Merger Benefits

Statement has been reported on under Rule 19.3(b)(ii) of the Irish Takeover Rules by Deloitte LLP, IP’s reporting accountants, and by Deutsche Bank AG, London Branch, IP’s financial adviser. Copies of their respective reports are included

in Part B and Part C of Appendix I to the Revised Proposal Announcement.

2 Based on $450 million estimated run-rate pre-tax operating synergies by end of year four divided by Smurfit Kappa revenue of €8,562m, extracted from Smurfit Kappa’s Fourth Quarter and Full Year 2017 Results published on 7 February 2018

(converted at a €:$ exchange rate of €1 = $1.1300, the average exchange rate for 2017, sourced from Bloomberg)

Revised Proposal to Acquire Smurfit Kappa

I March 26, 2018 19

Proven Track Record of Deleveraging

Rapid deleveraging post completion in prior transactions

2008 -2010 2012-2013 2016-2017 WY

Packaging TIN Packaging WY Pulp

5.5

2.2 5.0 $2.0 2.1 2.0 4.5 1.8 1.8 1.9 $ B

1.7 1.7 $1.5 1.7 1.6 4.0 (x)

Flow 3.5 Cash $1.0 3.0

Free 0.6 2.5 Leverage

$0.5 2.0 1.5 $0.0 1.0

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Net Debt Leverage Moody’s Adj. Debt to EBITDA

Note: Please refer to the

Annex to this presentation for sources and bases of the calculation for figures presented

Revised Proposal to Acquire Smurfit Kappa I March 26, 2018 20

Investor Relations Contacts

Guillermo Gutierrez +1-901-419-1731 Michele

Vargas +1-901-419-7287

Media Contact

Tom Ryan +1-901-419-4333

Annex

Slide 8

The statement that the combined business would be a leading producer of 19 million tonnes of kraftliner and recycled containerboard in the Americas and Europe is based on a

combination of: a. Smurfit Kappa’s production disclosed in Smurfit Kappa’s Annual Report 2016 (pages 22-23 for Europe and Americas, respectively) ; and b. IP’s internal capacity information

disclosed in IP’s Annual Report 2016 (Appendix II, A-4). Europe includes mill in Morocco and start-up mill in Madrid, Spain.

IP estimates of percentages for kraftliner vs. recycled are derived from IP internal estimates. Smurfit Kappa estimates for kraftliner vs. recycled are extracted from disclosure

relating to Europe in Smurfit Kappa’s Annual Report 2016 (graph of Kraftliner vs. Recycled on page 10) as well as confirmation from European Paper Packaging Capacity report (Jan 10, 2018). The Americas portion is extracted from World

Containerboard Capacity report (May 17, 2017). Ilim data obtained from IP internal reporting (IR Roadshow Handout February 28, 2018 page 58).

Number of box

plants was obtained from Smurfit Kappa’s Annual Report 2016 (pages 22-23 and includes corrugated and sheet plants) and IP’s Annual Report 2016 (2016 List of Facilities beginning on A-1). Europe includes IP locations in Morocco and Turkey.

Slide 9

Maps of Americas and Europe were extracted from Smurfit Kappa’s Capital Markets Day Presentation (June 3, 2016) overlaid with IP locations.

SKG North America and Latin America: Number of box plants and mills were extracted from Smurfit Kappa’s Annual Report 2016 (page 23) in conjunction with the “See our

locations” feature on Smurfit Kappa’s website https://www.smurfitkappa.com/vHome/com/Locations. Smurfit Kappa’s North America locations filtered on Smurfit Kappa’s website for corrugated packaging, corrugated sheets, and paper

mills in Mexico, US, and Canada.

Packaging Mills include those mills that produce containerboard, solidboard and boxboard.

SKG Europe: Number of box plants and mills were extracted from Smurfit Kappa’s Annual Report 2016 (page 22) (21 total mills: 15 produce containerboard, 1 sack kraft mill, 1

mill producing machine-glaze paper, and 4 other mills producing solidboard and boxboard). Packaging Mills include those mills that produce containerboard, solidboard and boxboard.

IP locations extracted from IP’s Annual Report 2016 (2016 List of Facilities beginning on A-1). IP Mills for North America and Europe

include announced conversion of Riverdale 15 (US) and Holmen Mill in Madrid, Spain (Europe), respectively. IP Europe includes locations in Morocco and Turkey.

Appendix Slide 15

Chart (Far Left)

Global Containerboard Consumption chart is based on apparent consumption of containerboard extracted from the following reports:

RISI Latin America Pulp and Paper Forecast – 5 Year (Sept 12, 2017);

RISI Asian Paper

Packaging Forecast – 5 Year (Aug 18, 2017);

RISI North American Paper Packaging Forecast – 5 Year (Aug 11, 2017);

RISI European Paper Packaging Forecast – 5 Year (Aug 25, 2017); and

World Containerboard

Forecast – (Nov 7, 2017).

Europe is Eurozone and includes Western Europe and Eastern Europe (which includes Central, Eastern and Southeastern Europe and

Russia). Americas includes North America and Latin America, Rest of World includes China, Africa and India.

Revised Proposal to Acquire Smurfit Kappa I

March 26, 2018 22

Annex

Appendix Slide 15

(continued)

Chart (Middle) a. Global Corrugated Packaging Profitability chart is based on apparent consumption of containerboard extracted from the same reports

above. Apparent consumption was then adjusted for imports/exports. b. Proxies for EBITDA margins derived from the publicly available filings of and sources relating to the peer companies identified below and then applied to internal regional

assumptions on box pricing (with the exception of China, where RISI pricing for containerboard was used as a proxy for box pricing). a. In China, an average EBITDA margin was derived from: a. 9 Dragons’ Full Company EBITDA margin obtained from

FactSet for Year End June 2017 (21.7%); b. Lee & Man’s Full Company EBITDA margin obtained from FactSet for Year End December 2017 (24.8%) b. In North America, an average EBITDA margin was derived from: a. IP’s Fourth Quarter and

Full Year 2017 Results, published on February 1, 2018 using North America Industrial Packaging Trailing Twelve Months (TTM) margin (21.5%); b. PCA’s Fourth Quarter 2017 Results press release, published on January 30, 2018; PCA’s

Third Quarter 2017 Results press release, published on October 25, 2017; PCA’s Second Quarter 2017 Results press release, published on July 26, 2017; and PCA’s First Quarter 2017 Results press release, published on April 26,

2017 using the Packaging segment’s TTM EBITDA margin before special items (adjusted for 80% corporate items) (22.6%); c. Westrock’s First Quarter 2018 Earnings Presentation, published on January 29, 2018; Westrock’s Fourth

Quarter 2017 Earnings Presentation, published on November 2, 2017; Westrock’s Third Quarter 2017 Earnings Presentation, published on August 3, 2017; Westrock’s Second Quarter 2017 Earnings Presentation, published on

April 26, 2017 using the North American Corrugated Packaging segment’s TTM EBITDA margin before special items (18.9%) c. In Latin America, EBITDA margin was derived from Klabin’s 2017 Annual Financial Statements, published on

January 31, 2018; page 74 “Consolidated Information about Operating Segments” for Paper; add back

Depreciation and Amortization to operating results

before finance costs (27.0%) d. In Western Europe, EBITDA margin was derived from Smurfit Kappa’s Full Year 2017 Results presentation page 5, published on February 7, 2018, using 2017 EBITDA margin for Europe (14.9%). e. In Eastern Europe,

an average EBITDA margin was derived from: a. DS Smith’s 2017/18 Half Year Results page 9, published on December 7, 2017, Central Europe and Italy segment’s return on sales for half year ended on October 31, 2017 (9.0%); b. Mondi

Group Full Year 2017 Results press announcement published on March 2, 2018; underlying Paper Packaging EBITDA on page 3 (27.4%) c. This combination of sources and analysis provides the basis for the estimate of global corrugated packaging

profitability d. Europe is Eurozone and includes Western Europe and Eastern Europe (which includes Central, Eastern and Southeastern Europe and Russia). Americas includes North America and Latin America, Rest of World includes China, Africa and

India.

Chart (Far right)

Real GDP growth estimates obtained from Oxford

Economics Assumptions (Jan 31, 2018). a. Americas consists of average estimates among North America and Latin America (North America: US, Canada and Mexico). b. Latin America: Argentina, Brazil, Chile, Colombia, Dominican Republic and El Salvador.

c. Europe is the Eurozone.

Revised Proposal to Acquire Smurfit Kappa I March 26, 2018 23

Annex

Appendix Slide 16

The European Containerboard Supply Positions 2017E were extracted from FEFCO and supplemental IP intelligence. For 2017E, adjustments were made for IP FY17 actual

and SAICA acquisition of Emin Leydier

Level of integration for Europe was obtained from FEFCO, RISI European Paper Packaging Capacity Report (Jan 10, 2018) and

supplemental IP intelligence. Adjusted for IP Madrid Mill full capacity, SAICA acquisition of Emin Leydier and Mondi acquisition of Powerflute.

Growth rates

obtained from RISI European Paper Packaging Forecast – 5 Year (updated February 21, 2018) apparent consumption (CAGR 2018-2021)

Appendix Slide 17

IP chart: IP internally reported volumes for respective regions

Smurfit Kappa

chart: market share for respective regions publicly disclosed in Smurfit Kappa’s Capital Markets Day Presentation (June 3, 2016) multiplied by RISI 2016 Containerboard apparent consumption for respective regions from the World Containerboard

Forecast (Dec 2017). Smurfit Kappa did not report a market share for Chile or Caribbean (it was assumed these market shares were negligible and were not considered for the analysis) Combined Chart: Based on a combination of the above analysis Growth

rates and the statement that the region is ~13 million tonnes obtained from RISI Latin America Paper Packaging Forecast – 5 Year (updated February 15, 2018) apparent consumption (CAGR 2018-2021)

Appendix Slide 19

Weyerhaeuser Packaging (2008): Press Release “IP Agrees to Purchase

Weyerhaeuser’s Packaging Business” (March 17, 2008) and presentation titled “Strengthening our North American Industrial Packaging Business” (March 17, 2008); Final Results reported in IP’s Second Quarter 2009 Earnings

Presentation.

Temple Inland Packaging (2012): Press Release “IP Announces Definitive Agreement to Acquire Temple-Inland for $32.00 Per Share in Cash”

(Sept 6, 2011) and presentation titled “Acquisition of Temple-Inland” (September 2011); Final Results reported in IP’s First Quarter 2013 Earnings Presentation.

Weyerhaeuser Cellulose Fibers (2016): Investor Webcast (May 2, 2016) and presentation titled “Strengthening IP’s North American Pulp Business”; Final results

reported in IP’s Fourth Quarter 2017 and Full Year 2017 Earnings Presentation.

Appendix Slide 20

Free Cash Flow, a non U.S. GAAP measure, reflects cash provided by continuing operations for 2005 – 2011, based on data in the 10-K for

each year at the time of filing. Free Cash Flow reflects cash provided by operations for 2012 onwards. Excludes net cash pension contributions impacting 2006, 2010, 2011, 2013, 2014, 2015, 2016 & 2017, cash flows under European accounts

receivable securitization beginning in 2009 and ending in 2011, and cash received from Black Liquor Tax Credits in 2009 and 2010. 2012 excludes $120MM cash paid for Temple-Inland

change-in-control agreements, $251MM cash received from unwinding a timber monetization, $44MM cash paid for Temple-Inland pension plan contribution, and $80MM cash paid

for Guaranty Bank settlement. 2013 excludes $30MM cash received from Guaranty Bank insurance reimbursements.

Leverage ratios provided by IP Treasury. Moody’s

methodology adjusts for debt to include pension gap + operating leases in addition to balance sheet debt. EBITDA incorporates interest income, pension and lease expense adjustments.

Revised Proposal to Acquire Smurfit Kappa I March 26, 2018 24