UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-Q

For the Quarterly Period Ended June 30, 2024

For the Transition Period From to

_________________________________________

Commission File Number 001-03157

(Exact name of registrant as specified in its charter)

(State or other jurisdiction of incorporation) | (I.R.S. Employer Identification No.) | ||||

(Address of Principal Executive Offices) | (Zip Code) | ||||

Registrant’s telephone number, including area code: (901 ) 419-9000

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||||||

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ¨

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (paragraph 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and "emerging growth company" in Rule 12b-2 of the Exchange Act.

| ☒ | Accelerated filer | ☐ | |||||||||

| Non-accelerated filer | ☐ | Smaller reporting company | |||||||||

| Emerging growth company | |||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13 (a) of the Exchange

Act. ¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

The number of shares outstanding of the registrant’s common stock, par value $1.00 per share, as of July 19, 2024 was 347,369,739 .

INDEX

| PAGE NO. | ||||||||

| Condensed Consolidated Statement of Operations - Six Months Ended June 30, 2024 and 2023 | ||||||||

| Condensed Consolidated Statement of Comprehensive Income - Six Months Ended June 30, 2024 and 2023 | ||||||||

| Condensed Consolidated Balance Sheet - June 30, 2024 and December 31, 2023 | ||||||||

| Condensed Consolidated Statement of Cash Flows - Six Months Ended June 30, 2024 and 2023 | ||||||||

ITEM 1.FINANCIAL STATEMENTS

INTERNATIONAL PAPER COMPANY

(Unaudited)

(In millions, except per share amounts)

| Three Months Ended June 30, | Six Months Ended June 30, | |||||||||||||||||||||||||

| 2024 | 2023 | 2024 | 2023 | |||||||||||||||||||||||

| Net Sales | $ | $ | $ | $ | ||||||||||||||||||||||

| Costs and Expenses | ||||||||||||||||||||||||||

| Cost of products sold | ||||||||||||||||||||||||||

| Selling and administrative expenses | ||||||||||||||||||||||||||

| Depreciation and amortization | ||||||||||||||||||||||||||

| Distribution expenses | ||||||||||||||||||||||||||

| Taxes other than payroll and income taxes | ||||||||||||||||||||||||||

| Restructuring and other charges, net | ||||||||||||||||||||||||||

| Net (gains) losses on sales of fixed assets | ( | |||||||||||||||||||||||||

| Interest expense, net | ||||||||||||||||||||||||||

| Non-operating pension expense (income) | ( | ( | ||||||||||||||||||||||||

| Earnings (Loss) From Continuing Operations Before Income Taxes and Equity Earnings (Loss) | ||||||||||||||||||||||||||

| Income tax provision (benefit) | ( | ( | ||||||||||||||||||||||||

| Equity earnings (loss), net of taxes | ( | ( | ( | |||||||||||||||||||||||

| Earnings (Loss) From Continuing Operations | ||||||||||||||||||||||||||

| Discontinued operations, net of taxes | ||||||||||||||||||||||||||

| Net Earnings (Loss) | $ | $ | $ | $ | ||||||||||||||||||||||

| Basic Earnings (Loss) Per Share | ||||||||||||||||||||||||||

| Earnings (loss) from continuing operations | $ | $ | $ | $ | ||||||||||||||||||||||

| Discontinued operations, net of taxes | ||||||||||||||||||||||||||

| Net earnings (loss) | $ | $ | $ | $ | ||||||||||||||||||||||

| Diluted Earnings (Loss) Per Share | ||||||||||||||||||||||||||

| Earnings (loss) from continuing operations | $ | $ | $ | $ | ||||||||||||||||||||||

| Discontinued operations, net of taxes | ||||||||||||||||||||||||||

| Net earnings (loss) | $ | $ | $ | $ | ||||||||||||||||||||||

| Average Shares of Common Stock Outstanding – assuming dilution | ||||||||||||||||||||||||||

The accompanying notes are an integral part of these condensed financial statements.

1

INTERNATIONAL PAPER COMPANY

(Unaudited)

(In millions)

| Three Months Ended June 30, | Six Months Ended June 30, | ||||||||||||||||||||||

| 2024 | 2023 | 2024 | 2023 | ||||||||||||||||||||

| Net Earnings (Loss) | $ | $ | $ | $ | |||||||||||||||||||

| Other Comprehensive Income (Loss), Net of Tax: | |||||||||||||||||||||||

| Amortization of pension and post-retirement prior service costs and net loss: | |||||||||||||||||||||||

| U.S. plans | |||||||||||||||||||||||

| Change in cumulative foreign currency translation adjustment | ( | ( | ( | ( | |||||||||||||||||||

| Total Other Comprehensive Income (Loss), Net of Tax | ( | ( | ( | ||||||||||||||||||||

| Comprehensive Income (Loss) | $ | $ | $ | $ | |||||||||||||||||||

The accompanying notes are an integral part of these condensed financial statements.

2

INTERNATIONAL PAPER COMPANY

(In millions)

| June 30, 2024 | December 31, 2023 | ||||||||||

| (unaudited) | |||||||||||

| Assets | |||||||||||

| Current Assets | |||||||||||

| Cash and temporary investments | $ | $ | |||||||||

| Accounts and notes receivable, net | |||||||||||

| Contract assets | |||||||||||

| Inventories | |||||||||||

| Other current assets | |||||||||||

| Total Current Assets | |||||||||||

| Plants, Properties and Equipment, net | |||||||||||

| Investments | |||||||||||

| Long-Term Financial Assets of Variable Interest Entities (Note 15) | |||||||||||

| Goodwill | |||||||||||

| Overfunded Pension Plan Assets | |||||||||||

| Right of Use Assets | |||||||||||

| Deferred Charges and Other Assets | |||||||||||

| Total Assets | $ | $ | |||||||||

| Liabilities and Equity | |||||||||||

| Current Liabilities | |||||||||||

| Notes payable and current maturities of long-term debt | $ | $ | |||||||||

| Accounts payable | |||||||||||

| Accrued payroll and benefits | |||||||||||

| Other current liabilities | |||||||||||

| Total Current Liabilities | |||||||||||

| Long-Term Debt | |||||||||||

| Long-Term Nonrecourse Financial Liabilities of Variable Interest Entities (Note 15) | |||||||||||

| Deferred Income Taxes | |||||||||||

| Underfunded Pension Benefit Obligation | |||||||||||

| Postretirement and Postemployment Benefit Obligation | |||||||||||

| Long-Term Lease Obligations | |||||||||||

| Other Liabilities | |||||||||||

| Equity | |||||||||||

Common stock, $ | |||||||||||

| Paid-in capital | |||||||||||

| Retained earnings | |||||||||||

| Accumulated other comprehensive loss | ( | ( | |||||||||

Less: Common stock held in treasury, at cost, 2024 – | |||||||||||

| Total Equity | |||||||||||

| Total Liabilities and Equity | $ | $ | |||||||||

The accompanying notes are an integral part of these condensed financial statements.

3

INTERNATIONAL PAPER COMPANY

(Unaudited)

(In millions)

| Six Months Ended June 30, | |||||||||||

| 2024 | 2023 | ||||||||||

| Operating Activities | |||||||||||

| Net earnings (loss) | $ | $ | |||||||||

| Depreciation and amortization | |||||||||||

| Deferred income tax provision (benefit), net | ( | ( | |||||||||

| Restructuring and other charges, net | |||||||||||

| Net (gains) losses on sales and impairments of equity method investments | |||||||||||

| Equity method dividends received | |||||||||||

| Equity (earnings) losses, net of taxes | ( | ||||||||||

| Periodic pension (income) expense, net | ( | ||||||||||

| Other, net | |||||||||||

| Changes in current assets and liabilities | |||||||||||

| Accounts and notes receivable | ( | ||||||||||

| Contract assets | ( | ( | |||||||||

| Inventories | |||||||||||

| Accounts payable and accrued liabilities | ( | ||||||||||

| Interest payable | ( | ||||||||||

| Other | ( | ( | |||||||||

| Cash Provided By (Used For) Operations | |||||||||||

| Investment Activities | |||||||||||

| Invested in capital projects | ( | ( | |||||||||

| Proceeds from sale of fixed assets | |||||||||||

| Other | ( | ||||||||||

| Cash Provided By (Used For) Investment Activities | ( | ( | |||||||||

| Financing Activities | |||||||||||

| Repurchases of common stock and payments of restricted stock tax withholding | ( | ( | |||||||||

| Issuance of debt | |||||||||||

| Reduction of debt | ( | ( | |||||||||

| Change in book overdrafts | ( | ( | |||||||||

| Dividends paid | ( | ( | |||||||||

| Other | ( | ||||||||||

| Cash Provided By (Used For) Financing Activities | ( | ( | |||||||||

| Effect of Exchange Rate Changes on Cash and Temporary Investments | ( | ||||||||||

| Change in Cash and Temporary Investments | ( | ( | |||||||||

| Cash and Temporary Investments | |||||||||||

| Beginning of period | |||||||||||

| End of period | $ | $ | |||||||||

The accompanying notes are an integral part of these condensed financial statements.

4

INTERNATIONAL PAPER COMPANY

(Unaudited)

The accompanying unaudited condensed consolidated financial statements have been prepared in conformity with accounting principles generally accepted in the United States and in accordance with the instructions to Form 10-Q and, in the opinion of management, include all adjustments that are necessary for the fair presentation of International Paper Company’s ("International Paper's," "the Company’s," "IP's" or "our") financial position, results of operations, and cash flows for the interim periods presented. Except as disclosed herein, such adjustments are of a normal, recurring nature. Results for the first six months of the year may not necessarily be indicative of full year results. You should read these unaudited condensed financial statements in conjunction with the audited financial statements and the notes thereto included in the Company’s Annual Report on Form 10-K for the year ended December 31, 2023 (the "Annual Report"), which have previously been filed with the U.S. Securities and Exchange Commission ("SEC").

These unaudited condensed consolidated financial statements have been prepared in conformity with accounting principles generally accepted in the United States that require the use of management’s estimates. Actual results could differ from management’s estimates.

Recently Adopted Accounting Pronouncements

Reference Rate Reform

In March 2020, the Financial Accounting Standards Board ("FASB") issued Accounting Standard Update ("ASU") 2020-04, "Reference Rate Reform (Topic 848): Facilitation of the Effects of Reference Rate Reform on Financial Reporting." This guidance provides companies with optional guidance to ease the potential accounting burden associated with transitioning away from reference rates that are expected to be discontinued. This guidance is effective upon issuance and generally can be applied through December 31, 2024. The Company has applied and will continue to apply this guidance to account for contract modifications due to changes in reference rates as those modifications occur. We do not expect this guidance to have a material impact on our consolidated financial statements and related disclosures.

Segment Reporting

In November 2023, the FASB issued ASU 2023-07, "Segment Reporting (Topic 280): Improvements to Reportable Segment Disclosures." This guidance requires companies to disclose incremental segment information on an annual and interim basis. This guidance is effective for annual reporting periods beginning after December 15, 2023 and interim periods within those years beginning after December 15, 2024. Early adoption of these amendments is permitted and amendments are required to be applied retrospectively to all prior periods presented in the financial statements. The Company adopted this guidance as of January 1, 2024 and will update disclosures within the Company's 2024 annual filing.

Recently Issued Accounting Pronouncements Not Yet Adopted

Income Taxes

In December 2023, the FASB issued ASU 2023-09, "Income Taxes (Topic 740): Improvements to Income Tax Disclosures." This guidance requires companies to enhance income tax disclosures, particularly around rate reconciliations and income taxes paid information. This guidance is effective for annual reporting periods beginning after December 15, 2024. Early adoption of these amendments is permitted and amendments should be applied prospectively. The Company plans to adopt this guidance as of January 1, 2025 and will update disclosures within the Company's 2025 annual filing.

5

Generally, the Company recognizes revenue on a point-in-time basis when the customer takes title to the goods and assumes the risks and rewards for the goods. For customized goods where the Company has a legally enforceable right to payment for the goods, the Company recognizes revenue over time which, generally, is as the goods are produced.

Disaggregated Revenue

| Three Months Ended June 30, 2024 | ||||||||||||||||||||||||||

| In millions | Industrial Packaging | Global Cellulose Fibers | Corporate & Intersegment | Total | ||||||||||||||||||||||

| Primary Geographical Markets (a) | ||||||||||||||||||||||||||

| United States | $ | $ | $ | $ | ||||||||||||||||||||||

| Europe, Middle East & Africa ("EMEA") | ||||||||||||||||||||||||||

| Pacific Rim and Asia | ||||||||||||||||||||||||||

| Americas, other than U.S. | ||||||||||||||||||||||||||

| Total | $ | $ | $ | $ | ||||||||||||||||||||||

| Operating Segments | ||||||||||||||||||||||||||

| North American Industrial Packaging | $ | $ | — | $ | — | $ | ||||||||||||||||||||

| EMEA Industrial Packaging | — | — | ||||||||||||||||||||||||

| Global Cellulose Fibers | — | — | ||||||||||||||||||||||||

| Intrasegment Eliminations | ( | — | — | ( | ||||||||||||||||||||||

| Corporate & Intersegment Sales | — | — | ||||||||||||||||||||||||

| Total | $ | $ | $ | $ | ||||||||||||||||||||||

(a) Net sales are attributed to countries based on the location of the seller.

| Six Months Ended June 30, 2024 | ||||||||||||||||||||||||||

| In millions | Industrial Packaging | Global Cellulose Fibers | Corporate & Intersegment | Total | ||||||||||||||||||||||

| Primary Geographical Markets (a) | ||||||||||||||||||||||||||

| United States | $ | $ | $ | $ | ||||||||||||||||||||||

| EMEA | ||||||||||||||||||||||||||

| Pacific Rim and Asia | ||||||||||||||||||||||||||

| Americas, other than U.S. | ||||||||||||||||||||||||||

| Total | $ | $ | $ | $ | ||||||||||||||||||||||

| Operating Segments | ||||||||||||||||||||||||||

| North American Industrial Packaging | $ | $ | — | $ | — | $ | ||||||||||||||||||||

| EMEA Industrial Packaging | — | — | ||||||||||||||||||||||||

| Global Cellulose Fibers | — | — | ||||||||||||||||||||||||

| Intrasegment Eliminations | ( | — | — | ( | ||||||||||||||||||||||

| Corporate & Intersegment Sales | — | — | ||||||||||||||||||||||||

| Total | $ | $ | $ | $ | ||||||||||||||||||||||

(a) Net sales are attributed to countries based on the location of the seller.

6

| Three Months Ended June 30, 2023 | ||||||||||||||||||||||||||

| In millions | Industrial Packaging | Global Cellulose Fibers | Corporate & Intersegment | Total | ||||||||||||||||||||||

| Primary Geographical Markets (a) | ||||||||||||||||||||||||||

| United States | $ | $ | $ | $ | ||||||||||||||||||||||

| EMEA | ||||||||||||||||||||||||||

| Pacific Rim and Asia | ||||||||||||||||||||||||||

| Americas, other than U.S. | ||||||||||||||||||||||||||

| Total | $ | $ | $ | $ | ||||||||||||||||||||||

| Operating Segments | ||||||||||||||||||||||||||

| North American Industrial Packaging | $ | $ | — | $ | — | $ | ||||||||||||||||||||

| EMEA Industrial Packaging | — | — | ||||||||||||||||||||||||

| Global Cellulose Fibers | — | — | ||||||||||||||||||||||||

| Intrasegment Eliminations | ( | — | — | ( | ||||||||||||||||||||||

| Corporate & Intersegment Sales | — | — | ||||||||||||||||||||||||

| Total | $ | $ | $ | $ | ||||||||||||||||||||||

(a) Net sales are attributed to countries based on the location of the seller.

| Six Months Ended June 30, 2023 | ||||||||||||||||||||||||||

| In millions | Industrial Packaging | Global Cellulose Fibers | Corporate & Intersegment | Total | ||||||||||||||||||||||

| Primary Geographical Markets (a) | ||||||||||||||||||||||||||

| United States | $ | $ | $ | $ | ||||||||||||||||||||||

| EMEA | ||||||||||||||||||||||||||

| Pacific Rim and Asia | ||||||||||||||||||||||||||

| Americas, other than U.S. | ||||||||||||||||||||||||||

| Total | $ | $ | $ | $ | ||||||||||||||||||||||

| Operating Segments | ||||||||||||||||||||||||||

| North American Industrial Packaging | $ | $ | — | $ | — | $ | ||||||||||||||||||||

| EMEA Industrial Packaging | — | — | ||||||||||||||||||||||||

| Global Cellulose Fibers | — | — | ||||||||||||||||||||||||

| Intrasegment Eliminations | ( | — | — | ( | ||||||||||||||||||||||

| Corporate & Intersegment Sales | — | — | ||||||||||||||||||||||||

| Total | $ | $ | $ | $ | ||||||||||||||||||||||

(a) Net sales are attributed to countries based on the location of the seller.

7

Revenue Contract Balances

A contract asset is created when the Company recognizes revenue on its customized products prior to having an unconditional right to payment from the customer, which generally does not occur until goods are transferred to the customer.

A contract liability is created when customers prepay for goods prior to the Company transferring those goods to the customer. The contract liability is reduced once control of the goods is transferred to the customer. The majority of our customer prepayments are received during the fourth quarter each year for goods that will be transferred to customers over the following twelve months. Contract liabilities of $17 million and $32 million are included in Other current liabilities in the accompanying condensed consolidated balance sheet as of June 30, 2024 and December 31, 2023, respectively. The Company also recorded a contract liability of $115 million related to a previous acquisition. The balance of this contract liability was $88 million and $92 million at June 30, 2024 and December 31, 2023, respectively, and is recorded in Other current liabilities and Other Liabilities in the accompanying condensed consolidated balance sheet.

The difference between the opening and closing balances of the Company's contract assets and contract liabilities primarily results from the difference between the price and quantity at comparable points in time for goods for which we have an unconditional right to payment or receive prepayment from the customer, respectively.

8

A summary of the changes in equity for the three months and six months ended June 30, 2024 and 2023 is provided below:

| Three Months Ended June 30, 2024 | |||||||||||||||||||||||||||||||||||

| In millions, except per share amounts | Common Stock Issued | Paid-in Capital | Retained Earnings | Accumulated Other Comprehensive Income (Loss) | Common Stock Held In Treasury, At Cost | Total Equity | |||||||||||||||||||||||||||||

| Balance, April 1 | $ | $ | $ | $ | ( | $ | $ | ||||||||||||||||||||||||||||

| Issuance of stock for various plans, net | — | — | — | ( | |||||||||||||||||||||||||||||||

Common stock dividends ($ | — | — | ( | — | — | ( | |||||||||||||||||||||||||||||

| Comprehensive income (loss) | — | — | ( | — | |||||||||||||||||||||||||||||||

| Ending Balance, June 30 | $ | $ | $ | $ | ( | $ | $ | ||||||||||||||||||||||||||||

| Six Months Ended June 30, 2024 | |||||||||||||||||||||||||||||||||||

| In millions, except per share amounts | Common Stock Issued | Paid-in Capital | Retained Earnings | Accumulated Other Comprehensive Income (Loss) | Common Stock Held In Treasury, At Cost | Total Equity | |||||||||||||||||||||||||||||

| Balance, January 1 | $ | $ | $ | $ | ( | $ | $ | ||||||||||||||||||||||||||||

| Issuance of stock for various plans, net | — | ( | — | — | ( | ||||||||||||||||||||||||||||||

| Repurchase of stock | — | — | — | — | ( | ||||||||||||||||||||||||||||||

Common stock dividends ($ | — | — | ( | — | — | ( | |||||||||||||||||||||||||||||

| Comprehensive income (loss) | — | — | ( | — | |||||||||||||||||||||||||||||||

| Ending Balance, June 30 | $ | $ | $ | $ | ( | $ | $ | ||||||||||||||||||||||||||||

| Three Months Ended June 30, 2023 | |||||||||||||||||||||||||||||||||||

| In millions, except per share amounts | Common Stock Issued | Paid-in Capital | Retained Earnings | Accumulated Other Comprehensive Income (Loss) | Common Stock Held In Treasury, At Cost | Total Equity | |||||||||||||||||||||||||||||

| Balance, April 1 | $ | $ | $ | $ | ( | $ | $ | ||||||||||||||||||||||||||||

| Issuance of stock for various plans, net | — | ( | — | — | ( | ( | |||||||||||||||||||||||||||||

| Repurchase of stock | — | — | — | — | ( | ||||||||||||||||||||||||||||||

Common stock dividends ($ | — | — | ( | — | — | ( | |||||||||||||||||||||||||||||

| Comprehensive income (loss) | — | — | ( | — | |||||||||||||||||||||||||||||||

| Ending Balance, June 30 | $ | $ | $ | $ | ( | $ | $ | ||||||||||||||||||||||||||||

| Six Months Ended June 30, 2023 | ||||||||||||||||||||||||||||||||

| In millions, except per share amounts | Common Stock Issued | Paid-in Capital | Retained Earnings | Accumulated Other Comprehensive Income (Loss) | Common Stock Held In Treasury, At Cost | Total Equity | ||||||||||||||||||||||||||

| Balance, January 1 | $ | $ | $ | $ | ( | $ | $ | |||||||||||||||||||||||||

| Issuance of stock for various plans, net | — | ( | — | — | ( | |||||||||||||||||||||||||||

| Repurchase of stock | — | — | — | — | ( | |||||||||||||||||||||||||||

Common stock dividends ($ | — | — | ( | — | — | ( | ||||||||||||||||||||||||||

| Comprehensive income (loss) | — | — | — | |||||||||||||||||||||||||||||

| Ending Balance, June 30 | $ | $ | $ | $ | ( | $ | $ | |||||||||||||||||||||||||

9

The following table presents changes in Accumulated Other Comprehensive Income (Loss) ("AOCI"), net of tax, for the three months and six months ended June 30, 2024 and 2023:

| Three Months Ended June 30, | Six Months Ended June 30, | ||||||||||||||||||||||

| In millions | 2024 | 2023 | 2024 | 2023 | |||||||||||||||||||

| Defined Benefit Pension and Postretirement Adjustments | |||||||||||||||||||||||

| Balance at beginning of period | $ | ( | $ | ( | $ | ( | $ | ( | |||||||||||||||

| Amounts reclassified from accumulated other comprehensive income | |||||||||||||||||||||||

| Balance at end of period | ( | ( | ( | ( | |||||||||||||||||||

| Change in Cumulative Foreign Currency Translation Adjustments | |||||||||||||||||||||||

| Balance at beginning of period | ( | ( | ( | ( | |||||||||||||||||||

| Other comprehensive income (loss) before reclassifications | ( | ( | ( | ( | |||||||||||||||||||

| Balance at end of period | ( | ( | ( | ( | |||||||||||||||||||

| Net Gains and Losses on Cash Flow Hedging Derivatives | |||||||||||||||||||||||

| Balance at beginning of period | ( | ( | ( | ( | |||||||||||||||||||

| Balance at end of period | ( | ( | ( | ( | |||||||||||||||||||

| Total Accumulated Other Comprehensive Income (Loss) at End of Period | $ | ( | $ | ( | $ | ( | $ | ( | |||||||||||||||

The following table presents details of the reclassifications out of AOCI for the three months and six months ended June 30, 2024 and 2023:

| In millions: | Amount Reclassified from Accumulated Other Comprehensive Income | Location of Amount Reclassified from AOCI | |||||||||||||||||||||||||||

| Three Months Ended June 30, | Six Months Ended June 30, | ||||||||||||||||||||||||||||

| 2024 | 2023 | 2024 | 2023 | ||||||||||||||||||||||||||

| Defined benefit pension and postretirement items: | |||||||||||||||||||||||||||||

| Prior-service costs | $ | ( | $ | ( | $ | ( | $ | ( | (a) | Non-operating pension expense (income) | |||||||||||||||||||

| Actuarial gains (losses) | ( | ( | ( | ( | (a) | Non-operating pension expense (income) | |||||||||||||||||||||||

| Total pre-tax amount | ( | ( | ( | ( | |||||||||||||||||||||||||

| Tax (expense) benefit | |||||||||||||||||||||||||||||

| Net of tax | ( | ( | ( | ( | |||||||||||||||||||||||||

| Total reclassifications for the period | $ | ( | $ | ( | $ | ( | $ | ( | |||||||||||||||||||||

(a)These accumulated other comprehensive income components are included in the computation of net periodic pension cost (see Note 17 for additional details).

10

Basic earnings per share is computed by dividing earnings by the weighted average number of common shares outstanding. Diluted earnings per share is computed assuming that all potentially dilutive securities were converted into common shares. There are no adjustments required to be made to net income for purposes of computing basic and diluted earnings per share. A reconciliation of the amounts included in the computation of basic earnings (loss) per share from continuing operations and diluted earnings (loss) per share from continuing operations is as follows:

| Three Months Ended June 30, | Six Months Ended June 30, | ||||||||||||||||||||||

| In millions, except per share amounts | 2024 | 2023 | 2024 | 2023 | |||||||||||||||||||

| Earnings (loss) from continuing operations | $ | $ | $ | $ | |||||||||||||||||||

| Weighted average common shares outstanding | |||||||||||||||||||||||

| Effect of dilutive securities | |||||||||||||||||||||||

| Restricted performance share plan | |||||||||||||||||||||||

| Weighted average common shares outstanding – assuming dilution | |||||||||||||||||||||||

| Basic earnings (loss) per share from continuing operations | $ | $ | $ | $ | |||||||||||||||||||

| Diluted earnings (loss) per share from continuing operations | $ | $ | $ | $ | |||||||||||||||||||

2024: There were no restructuring and other charges recorded during the three months ended June 30, 2024.

During the three months ended March 31, 2024, the Company recorded restructuring and other charges of $3 million for costs associated with the permanent closure of our containerboard mill in Orange, Texas and the permanent shutdown of pulp machines at our Riegelwood, North Carolina and Pensacola, Florida mills.

2023: There were no restructuring and other charges recorded during the three months and six months ended June 30, 2023.

11

Temporary Investments

Temporary investments with an original maturity of three months or less and money market funds with greater than three month maturities but with the right to redeem without notices are treated as cash equivalents and stated at cost. Temporary investments totaled $862 million and $950 million at June 30, 2024 and December 31, 2023, respectively.

Accounts and Notes Receivable

| In millions | June 30, 2024 | December 31, 2023 | |||||||||

| Accounts and notes receivable, net: | |||||||||||

Trade (less allowances of $ | $ | $ | |||||||||

| Other | |||||||||||

| Total | $ | $ | |||||||||

Inventories

| In millions | June 30, 2024 | December 31, 2023 | |||||||||

| Raw materials | $ | $ | |||||||||

| Finished pulp, paper and packaging | |||||||||||

| Operating supplies | |||||||||||

| Other | |||||||||||

| Total | $ | $ | |||||||||

Plants, Properties and Equipment

Accumulated depreciation was $19.9 billion and $19.6 billion at June 30, 2024 and December 31, 2023, respectively. Depreciation expense was $251 million and $235 million for the three months ended June 30, 2024 and 2023, respectively, and $519 million and $467 million for the six months ended June 30, 2024 and 2023, respectively.

Non-cash additions to plants, properties and equipment included within accounts payable were $63 million and $141 million at June 30, 2024 and December 31, 2023, respectively.

Accounts Payable

Under a supplier finance program, International Paper agrees to pay a bank the stated amount of confirmed invoices from its designated suppliers on the original maturity dates of the invoices. International Paper or the bank may terminate the agreement upon at least 90 days’ notice. The supplier invoices that have been confirmed as valid under the program require payment in full on the due date with no terms exceeding 180 days. The accounts payable balance included $110 million and $122 million of supplier finance program liabilities as of June 30, 2024 and December 31, 2023, respectively.

Interest

Interest payments made during the six months ended June 30, 2024 and 2023 were $222 million and $240 million, respectively.

Amounts related to interest were as follows:

| Three Months Ended June 30, | Six Months Ended June 30, | ||||||||||||||||||||||

| In millions | 2024 | 2023 | 2024 | 2023 | |||||||||||||||||||

| Interest expense | $ | $ | $ | $ | |||||||||||||||||||

| Interest income | |||||||||||||||||||||||

| Capitalized interest costs | |||||||||||||||||||||||

12

Asset Retirement Obligations

The Company recorded liabilities in Other Liabilities in the accompanying condensed consolidated balance sheet of $104 million and $103 million related to asset retirement obligations at June 30, 2024 and December 31, 2023, respectively.

International Paper leases various real estate, including certain operating facilities, warehouses, office space and land. The Company also leases material handling equipment, vehicles, and certain other equipment. The Company's leases have a remaining lease term of up to 29 years. Total lease costs were $79 million and $73 million for the three months ended June 30, 2024 and 2023, respectively, and $158 million and $148 million for the six months ended June 30, 2024 and 2023, respectively.

Supplemental Balance Sheet Information Related to Leases

| In millions | Classification | June 30, 2024 | December 31, 2023 | |||||||||||||||||

| Assets | ||||||||||||||||||||

| Operating lease assets | Right-of-use assets | $ | $ | |||||||||||||||||

| Finance lease assets | Plants, properties and equipment, net (a) | |||||||||||||||||||

| Total leased assets | $ | $ | ||||||||||||||||||

| Liabilities | ||||||||||||||||||||

| Current | ||||||||||||||||||||

| Operating | Other current liabilities | $ | $ | |||||||||||||||||

| Finance | Notes payable and current maturities of long-term debt | |||||||||||||||||||

| Noncurrent | ||||||||||||||||||||

| Operating | Long-term lease obligations | |||||||||||||||||||

| Finance | Long-term debt | |||||||||||||||||||

| Total lease liabilities | $ | $ | ||||||||||||||||||

(a)Finance leases are recorded net of accumulated amortization of $70 million and $67 million as of June 30, 2024 and December 31, 2023, respectively.

Ilim S.A.

On September 18, 2023, pursuant to a previously announced agreement, the Company completed the sale of its 50 % equity interest in Ilim S.A. ("Ilim"), which was a joint venture that operated a pulp and paper business in Russia and has subsidiaries including Ilim Group, to its joint venture partners for $484 million in cash. The Company also completed the sale of all of its Ilim Group shares (constituting a 2.39 % stake) for $24 million, and divested other non-material residual interests associated with Ilim, to its joint venture partners. Following the completed sales, the Company no longer has an interest in Ilim or any of its subsidiaries. Additionally, we incurred transaction fees of $36 million in the third quarter of 2023 in connection with the sale of our investment. The Company reclassified currency translation adjustments in AOCI of $517 million to the investment at the completion of the transaction.

All historical results of the Ilim investment are presented as Discontinued Operations, net of taxes in the condensed consolidated statement of operations.

The following summarizes the items comprising Equity Earnings, Impairment Charges, Tax Expense (Benefit), Discontinued Operations and Dividends related to the sale of our equity interest in Ilim:

13

| In millions | Equity Earnings | Impairment Charges | Tax Expense (Benefit) | Discontinued Operations, net of tax (a) | Dividends | ||||||||||||||||||||||||

| 2023 First Quarter | |||||||||||||||||||||||||||||

| 2023 Second Quarter | |||||||||||||||||||||||||||||

| 2023 Third Quarter | ( | ( | |||||||||||||||||||||||||||

| Six Months Ended June 30, 2023 | |||||||||||||||||||||||||||||

(a) Discontinued operations, net of tax is Equity Earnings less Impairment Charges and Tax Expense (Benefit)

Goodwill

The following table presents changes in goodwill balances as allocated to each business segment for the six months ended June 30, 2024:

| In millions | Industrial Packaging | Global Cellulose Fibers | Total | ||||||||||||||

| Balance as of January 1, 2024 | |||||||||||||||||

| Goodwill | $ | $ | $ | ||||||||||||||

| Accumulated impairment losses | ( | ( | ( | ||||||||||||||

| Total | |||||||||||||||||

| Currency translation and other | ( | ( | |||||||||||||||

| Accumulated impairment loss additions / reductions | — | — | — | ||||||||||||||

| Balance as of June 30, 2024 | |||||||||||||||||

| Goodwill | |||||||||||||||||

| Accumulated impairment losses | ( | ( | ( | ||||||||||||||

| Total | $ | $ | $ | ||||||||||||||

Other Intangibles

Identifiable intangible assets are recorded in Deferred Charges and Other Assets in the accompanying condensed consolidated balance sheet and comprised the following:

| June 30, 2024 | December 31, 2023 | ||||||||||||||||||||||||||||||||||

| In millions | Gross Carrying Amount | Accumulated Amortization | Net Intangible Assets | Gross Carrying Amount | Accumulated Amortization | Net Intangible Assets | |||||||||||||||||||||||||||||

| Customer relationships and lists | $ | $ | $ | $ | $ | $ | |||||||||||||||||||||||||||||

| Tradenames, patents and trademarks, and developed technology | |||||||||||||||||||||||||||||||||||

| Land and water rights | |||||||||||||||||||||||||||||||||||

| Other | |||||||||||||||||||||||||||||||||||

| Total | $ | $ | $ | $ | $ | $ | |||||||||||||||||||||||||||||

The Company recognized the following amounts as amortization expense related to intangible assets:

| Three Months Ended June 30, | Six Months Ended June 30, | ||||||||||||||||||||||

| In millions | 2024 | 2023 | 2024 | 2023 | |||||||||||||||||||

| Amortization expense related to intangible assets | $ | $ | $ | $ | |||||||||||||||||||

14

International Paper made income tax payments, net of refunds, of $153 million and $215 million for the six months ended June 30, 2024 and 2023, respectively.

The Company currently estimates that, as a result of ongoing discussions, pending tax settlements and expirations of statutes of limitations, the amount of unrecognized tax benefits could be reduced by approximately $4 million during the next 12 months.

The Organization for Economic Cooperation and Development has proposed a 15% global minimum tax applied on a country-by-country basis (the "Pillar Two rule"), and many countries, including countries in which we operate, have enacted or begun the process of enacting laws adopting the Pillar Two rule. The first component of the Pillar Two rule became effective as of January 1, 2024 and did not have a material impact on the Company’s effective tax rate. The second component is expected to go into effect in 2025.

During the second quarter, the Company completed an internal legal entity restructuring for which a capital loss was recognized for U.S. federal and state income tax purposes. The Company intends to use this capital loss to offset capital gains, and, as such, recorded a deferred tax asset and a deferred tax benefit of approximately $338 million in the second quarter, which impacted the effective income tax rate for the three months and six months ended June 30, 2024.

General

The Company is involved in various inquiries, administrative proceedings and litigation relating to environmental and safety matters, personal injury, product liability, labor and employment, contracts, sales of property, intellectual property, tax, and other matters, that arise in the normal course of business. These matters may raise difficult and complicated legal issues and may be subject to many uncertainties and complexities. Moreover, some of these matters allege substantial or indeterminate monetary damages.

International Paper reviews inquiries, administrative proceedings and litigation, including with respect to environmental matters, on an ongoing basis and establishes an estimated liability for specific legal proceedings and other loss contingencies when it determines that the likelihood of an unfavorable outcome is probable, and the amount of the loss can be reasonably estimated. In addition, if the likelihood of an unfavorable outcome with respect to material loss contingencies is reasonably possible and International Paper is able to determine an estimate of the possible loss or range of loss, whether in excess of a related accrued liability of where there is no accrued liability, International Paper will disclose the estimate of the possible loss or range of loss. When no amount in a range of loss is more likely than any other amount in the range, the low end of the range is used as the estimate of the possible loss. International Paper’s assessment of whether a loss is probable is based on management’s assessment of the ultimate outcome of the matter.

Assessments of lawsuits and claims and the estimates reflected herein, are subject to significant judgments about future events, rely heavily on estimates and assumptions, and are otherwise subject to significant known and unknown uncertainties. The matters underlying such estimates may change from time to time and actual losses may vary significantly from current estimates. Additionally, the estimated liability for loss contingencies does not include matters or losses for which an estimate is not reasonably estimable and probable.

Based on information currently known to International Paper, management believes that loss contingencies arising from pending matters, including the matters described herein, will not have a material adverse effect on the consolidated financial position or liquidity of the Company. However, in light of the inherent uncertainties involved in such matters, some of which are beyond the Company's control, and the large or indeterminate damages sought in some of these matters, a future adverse ruling, settlement, unfavorable development, or increase in accruals with respect to these matters could result in future charges that could be materially adverse to the Company's results of operations or cash flows in any particular reporting period.

Environmental

The Company has been named as a potentially responsible party ("PRP") in environmental remediation actions under various federal and state laws, including the Comprehensive Environmental Response, Compensation and Liability Act of 1980, as amended ("CERCLA"). Many of these proceedings involve the cleanup of hazardous substances at large commercial landfills that received waste from many different sources. While joint and several liability is authorized under CERCLA and equivalent state laws, as a practical matter, liability for CERCLA cleanups is typically allocated among the many PRPs. There are other

15

remediation costs typically associated with the cleanup of hazardous substances at the Company’s current, closed and formerly-owned facilities, and recorded as liabilities in the balance sheet.

Remediation costs are recorded in the consolidated financial statements when they become probable and reasonably estimable. International Paper has estimated the probable liability associated with these environmental remediation matters, including those described herein, to be approximately $270 million and $251 million in the aggregate as of June 30, 2024 and December 31, 2023, respectively. Other than as described below, completion of required environmental remedial actions ("RAs") is not expected to have a material effect on our consolidated financial statements.

Cass Lake: One of the matters included above arises out of a closed wood-treatment facility located in Cass Lake, Minnesota. In June 2011, the U.S. Environmental Protection Agency ("EPA") selected and published a proposed soil remedy at the site with an estimated cost of $46 million. In April 2020, the EPA issued a final plan concerning clean-up standards at a portion of the site, the estimated cost of which is included within the soil remedy referenced above. The estimated liability for the Cass Lake superfund site was $45 million and $46 million as of June 30, 2024 and December 31, 2023, respectively.

Kalamazoo River: The Company is a PRP with respect to the Allied Paper, Inc./Portage Creek/Kalamazoo River Superfund Site in Michigan. The EPA asserts that the site is contaminated by polychlorinated biphenyls primarily as a result of discharges from various paper mills located along the Kalamazoo River, including a paper mill formerly owned by St. Regis Paper Company ("St. Regis"). The Company is a successor in interest to St. Regis.

•Operable Unit 5, Area 1: In March 2016, the Company and other PRPs received a special notice letter from the EPA (i) inviting participation in implementing a remedy for a portion of the site known as Operable Unit 5, Area 1, and (ii) demanding reimbursement of EPA past costs totaling $37 million, including $19 million in past costs previously demanded by the EPA. The Company responded to the special notice letter. In December 2016, the EPA issued a unilateral administrative order to the Company and other PRPs to perform the remedy. The Company responded to the unilateral administrative order, agreeing to comply with the order subject to its sufficient cause defenses.

•Operable Unit 1: In October 2016, the Company and another PRP received a special notice letter from the EPA inviting participation in the remedial design ("RD") component of the landfill remedy for the Allied Paper Mill, which is also known as Operable Unit 1. A Record of Decision ("ROD") establishing the final landfill remedy for the Allied Paper Mill was issued by the EPA in September 2016. The Company responded to the Allied Paper Mill special notice letter in December 2016. In February 2017, the EPA informed the Company that it would make other arrangements for the performance of the RD. In the summer 2021, the EPA initiated RA activities. In October 2022, the Company received a unilateral administrative order to perform the RA. As a result, the Company increased its estimated liability by $27 million in the fourth quarter of 2022.

The total estimated liability for the Kalamazoo River superfund site was $20 million and $27 million as of June 30, 2024 and December 31, 2023, respectively.

In addition, in December 2020, the U.S. District for the Western District of Michigan ("District Court") approved a Consent Decree among the United States, NCR Corporation (one of the parties to the allocation/apportionment litigation described below), the State of Michigan and natural resource trustees. Under the Consent Decree NCR agreed to make payments of more than $100 million and perform work in Operable Unit 5, Areas 2, 3, and 4 at an estimated cost of $136 million.

The Company’s CERCLA liability has not been finally determined with respect to these or any other portions of the site, and except as noted above, the Company has declined to perform any work or reimburse the EPA at this time. As noted below, the Company is involved in allocation/apportionment litigation with regard to the site. Accordingly, it is premature to predict the outcome or estimate our maximum reasonably possible loss or range of loss with respect to this site. We have recorded a liability for future remediation costs at the site that are probable and presently reasonably estimable, and it remains reasonably possible that additional losses in excess of this recorded liability could be material; however, we are unable to estimate any possible loss or range of loss in excess of such recorded liability.

The Company was named as a defendant by Georgia-Pacific Consumer Products LP, Fort James Corporation and Georgia Pacific LLC (collectively, "GP") in a contribution and cost recovery action for alleged pollution at the site related to the Company's potential CERCLA liability. NCR Corporation and Weyerhaeuser Company were also named as defendants. The lawsuit seeks contribution under CERCLA for costs purportedly expended by plaintiffs ($79 million as of the filing of the complaint) and for future remediation costs. In June 2018, the District Court issued its Final Judgment and Order, which fixed the past cost amount at approximately $50 million (plus interest to be determined) and allocated to the Company a 15 % share of responsibility for those past costs. The District Court did not address responsibility for future costs in its decision. In July 2018,

16

the Company and each of the other parties filed notices appealing the Final Judgment and prior orders incorporated into the Final Judgment. In April 2022, the Sixth Circuit Court of Appeals (the "Sixth Circuit") reversed the Judgment of the Court, finding that the lawsuit against the Company was time-barred by the applicable statute of limitations. In May 2022, GP filed a petition for rehearing with the Sixth Circuit, which was denied in July 2022. In November 2022, GP filed a petition for writ of certiorari with the U.S. Supreme Court. In October 2023, the U.S. Supreme Court denied GP's writ petition, thus rendering final the Sixth Circuit's decision that GP's lawsuit against the Company was time-barred. In January 2024 GP requested that the District Court’s final order declare that each party is jointly and severally liable for future costs, arguing that the Sixth Circuit decision only applies to past costs. On April 9, 2024, the District Court entered Final Judgment After Remand, declaring, consistent with the Sixth Circuit's decision, that GP’s past costs are time-barred by the applicable statute of limitations. The District Court also entered Final Judgment on Remand that all three parties, including the Company, are jointly and severally liable for future response costs at the site. The Company believes the District Court’s Final Judgment on Remand regarding liability for future costs is in error and is appealing the Final Judgment on Remand on future costs liability to the Sixth Circuit.

Harris County: International Paper and McGinnis Industrial Maintenance Corporation ("MIMC"), a subsidiary of Waste Management, Inc. ("WMI"), are PRPs at the San Jacinto River Waste Pits Superfund Site in Harris County, Texas. The PRPs have been actively participating in the activities at the site and share the costs of these activities.

In October 2017, the EPA issued a ROD selecting the final remedy for the site: removal and relocation of the waste material from both the northern and southern impoundments. The EPA did not specify the methods or practices needed to perform this work. The EPA’s selected remedy was accompanied by a cost estimate of approximately $115 million ($105 million for the northern impoundment, and $10 million for the southern impoundment). Subsequent to the issuance of the ROD, there have been numerous meetings between the EPA and the PRPs, and the Company continues to work with the EPA and MIMC/WMI to develop the RD.

To this end, in April 2018, the PRPs entered into an Administrative Order on Consent ("AOC") with the EPA, agreeing to work together to develop the RD for the northern impoundment. That RD work is ongoing. The AOC does not include any agreement to perform waste removal or other construction activity at the site. Rather, it involves adaptive management techniques and a pre-design investigation, the objectives of which include filling data gaps (including but not limited to post-Hurricane Harvey technical data generated prior to the ROD and not incorporated into the selected remedy), refining areas and volumes of materials to be addressed, determining if an excavation remedy is able to be implemented in a manner protective of human health and the environment, and investigating potential impacts of remediation activities to infrastructure in the vicinity.

During the first quarter of 2020, through a series of meetings among the Company, MIMC/WMI, our consultants, the EPA and the Texas Commission on Environmental Quality, progress was made to resolve key technical issues previously preventing the Company from determining the manner in which the selected remedy for the northern impoundment would be feasibly implemented. As a result of these developments, the Company reserved the following estimated liability amounts in relation to remediation at this site: (a) $10 million for the southern impoundment; and (b) $55 million for the northern impoundment, which represents the Company's 50 % share of our estimate of the low end of the range of probable remediation costs.

We submitted the Final Design Package for the southern impoundment to the EPA, and the EPA approved this plan in May 2021. The EPA issued a Unilateral Administrative Order for RA of the southern impoundment in August 2021. An addendum to the Final 100 % RD (Amended April 2021) was submitted to the EPA for the southern impoundment in June 2022. This addendum incorporated additional data collected to date which indicated that additional waste material removal will be required, lengthening the time to complete RA.

With respect to the northern impoundment, the PRPs submitted the final component of the 90 % to the EPA in November 2022. Upon submittal of the final component, an updated engineering estimate was developed, and the Company increased the estimated liability amount by approximately $21 million, which represents the Company's 50 % share of our estimate of the low end of the range of probable remediation costs. On January 5, 2024, the PRPs received comments from the EPA on the November 2022 90 % RD submittal. The PRPs responded to the EPA comments in late January 2024. In April 2024, the EPA responded to the submitted plans and requested a 100 % RD by July 17, 2024, which was timely submitted by the PRPs. Among other things, the revised RD proposes design changes that include modification of the wastewater treatment facilities, changes to outer walls, and the addition of scour and barge protection systems. To account for the design changes and the updated estimate of costs from the site engineer, the Company increased the estimated liability amount by approximately $25 million as of June 30, 2024. This amount represents the Company’s 50 % share of the low end of the range of estimated remediation costs. While several key technical issues have been resolved, respondents still face significant challenges remediating this area in a cost-efficient manner that will not result in a release of contaminated materials to the environment during the excavation, removal and transport of the materials. Our discussions with the EPA on the best approach to remediation will continue. Because of ongoing questions regarding cost effectiveness, timing and gathering other technical data, additional losses in excess

17

of our recorded liability are possible. The total estimated liability for the southern and northern impoundment was $98 million and $83 million as of June 30, 2024 and December 31, 2023, respectively.

Versailles Pond: The Company is a responsible party for the investigation and remediation of Versailles Pond, a 57-acre dammed river impoundment that historically received paperboard mill wastewater in Sprague, Connecticut. A comprehensive investigation has determined that Versailles Pond is contaminated with polychlorinated biphenyls, mercury, and metals. A preliminary remediation plan was prepared in the third quarter of 2023. Negotiations with state and federal governmental officials are ongoing regarding the scope and timing of the remediation. The total estimated liability for Versailles Pond was $30

Asbestos-Related Matters

We have been named as a defendant in various asbestos-related personal injury litigation, in both state and federal court, primarily in relation to the prior operations of certain companies previously acquired by the Company. The Company's total recorded liability with respect to pending and future asbestos-related claims was $112 million and $97 million as of June 30, 2024 and December 31, 2023, respectively, both net of estimated insurance recoveries. While it is reasonably possible that the Company may incur losses in excess of its recorded liability with respect to asbestos-related matters, we are unable to estimate any loss or range of loss in excess of such liability, and do not believe additional material losses are probable.

Antitrust

In March 2017, the Italian Competition Authority ("ICA") commenced an investigation into the Italian packaging industry to determine whether producers of corrugated sheets and boxes violated the applicable European competition law. In April 2019, the ICA concluded its investigation and issued initial findings alleging that over 30 producers, including our Italian packaging subsidiary ("IP Italy"), improperly coordinated the production and sale of corrugated sheets and boxes. In August 2019, the ICA issued its decision and assessed IP Italy a fine of €29 million (approximately $31 million at the then-current exchange rates) which was recorded in the third quarter of 2019. We appealed the ICA decision and our appeal was denied in May 2021. We further appealed the decision to the Italian Council of State ("Council of State"), and in March 2023 the Council of State largely upheld the ICA’s findings, but referred the calculation of IP Italy’s fine back to the ICA, finding that it was disproportionately high based on the conduct found. We further appealed the Council of State decision to uphold the ICA’s findings, and in March 2024, the Council of State published its decision holding that its earlier decision should be interpreted as accepting many of IP Italy’s earlier arguments and that the ICA should reduce IP Italy’s fine accordingly. Notwithstanding these decisions by the Council of State, in March 2024 the ICA served IP Italy with its redetermination decision leaving IP Italy’s fine unchanged. IP Italy does not believe the ICA's redetermination decision is consistent with the Council of State's March 2024 decision or its March 2023 referral back to the ICA, and has further appealed the amount of its fine. The Company and other producers also have been named in lawsuits, and we have received other claims, by a number of customers in Italy for damages associated with the alleged anticompetitive conduct. We do not believe material losses arising from such private lawsuits and claims are probable.

Guarantees

In connection with sales of businesses, property, equipment, forestlands and other assets, International Paper commonly makes representations and warranties relating to such businesses or assets, and may agree to indemnify buyers with respect to tax and environmental liabilities, breaches of representations and warranties, and other matters. Where liabilities for such matters are determined to be probable and reasonably estimable, accrued liabilities are recorded at the time of sale as a cost of the transaction.

Brazil Goodwill Tax Matter: The Brazilian Federal Revenue Service has challenged the deductibility of goodwill amortization generated in a 2007 acquisition by Sylvamo do Brasil Ltda. ("Sylvamo Brazil"), which was a wholly-owned subsidiary of the Company, until the October 1, 2021 spin-off of the Printing Papers business, after which it became a subsidiary of Sylvamo Corporation ("Sylvamo"). Sylvamo Brazil received assessments for the tax years 2007-2015 totaling approximately $105 million (adjusted for variation in currency exchange rates) in tax, plus interest, penalties and fees. The interest, penalties and fees currently total approximately $249 million (adjusted for variation in currency exchange rates). Accordingly, the assessments currently total approximately $354 million (adjusted for variation in currency exchange rates). After an initial favorable ruling challenging the basis for these assessments, Sylvamo Brazil received subsequent unfavorable decisions from the Brazilian Administrative Council of Tax Appeals. Sylvamo Brazil has appealed these decisions and intends to appeal any future unfavorable administrative judgments to the Brazilian federal courts; however, this tax litigation matter may take many years to resolve. Sylvamo Brazil and International Paper believe the transaction underlying these assessments was appropriately evaluated, and that Sylvamo Brazil's tax position should be sustained, based on Brazilian tax law.

18

This matter pertains to a business that was conveyed to Sylvamo on October 1, 2021, as part of our spin-off transaction. Pursuant to the terms of the tax matters agreement entered into between the Company and Sylvamo, the Company will pay 60 % and Sylvamo will pay 40 %, on up to $300 million of any assessment related to this matter, and the Company will pay all amounts of the assessment over $300 million. Under the terms of the tax matters agreement, decisions concerning the conduct of the litigation related to this matter, including strategy, settlement, pursuit and abandonment, will be made by the Company. Sylvamo thus has no control over any decision related to this ongoing litigation. The Company intends to vigorously defend this historical tax position against the current assessments and any similar assessments that may be issued for tax years subsequent to 2015. The Brazilian government may enact a tax amnesty program that would allow Sylvamo Brazil to resolve this dispute for less than the assessed amount. As of October 1, 2021, in connection with the recording of the distribution of assets and liabilities resulting from the spin-off transaction, the Company established a liability representing the initial fair value of the contingent liability under the tax matters agreement. The contingent liability was determined in accordance with ASC 460 "Guarantees" based on the probability weighting of various possible outcomes. The initial fair value estimate and recorded liability as of December 31, 2021 was $48

Variable Interest Entities

As of June 30, 2024, the fair value of the Timber Notes and Extension Loans for the 2007 Financing Entities was $2.4 billion and $2.1 billion, respectively. The Timber Notes and Extension Loans are classified as Level 2 within the fair value hierarchy, which is further defined in Note 1 in the Company’s Annual Report.

The Timber Notes of $2.4 billion and the Extension Loans of $2.1 billion both mature in 2027 and are shown in Long-term nonrecourse financial assets of variable interest entities and Long-term nonrecourse financial liabilities of variable interest entities, respectively, on the accompanying condensed consolidated balance sheet.

Activity between the Company and the 2007 Financing Entities was as follows:

| Three Months Ended June 30, | Six Months Ended June 30, | ||||||||||||||||||||||

| In millions | 2024 | 2023 | 2024 | 2023 | |||||||||||||||||||

| Revenue (a) | $ | $ | $ | $ | |||||||||||||||||||

| Expense (b) | |||||||||||||||||||||||

| Cash receipts (c) | |||||||||||||||||||||||

| Cash payments (d) | |||||||||||||||||||||||

(a)The revenue is included in interest expense, net in the accompanying statement of operations and includes approximately $4 9

(b)The expense is included in interest expense, net in the accompanying statement of operations and includes approximately $1 3

(c)The cash receipts are interest received on the Long-term financial assets of variable interest entities.

19

The borrowing capacity of the Company's commercial paper program is $1.0 billion supported by its $1.4 billion credit agreement. Under the terms of the program, individual maturities on borrowings may vary, but not exceed one year from the date of issue. Interest bearing notes may be issued either as fixed or floating rate notes. As of June 30, 2024, the Company had no borrowings outstanding under the program.

At June 30, 2024, International Paper’s credit facilities totaled $1.9 billion. The credit facilities generally provide for interest rates at a floating rate index plus a pre-determined margin dependent upon International Paper’s credit rating. The credit facilities previously included a $1.5 billion contractually committed bank facility with a maturity date of June 2026. In June 2023, the Company amended and restated its credit agreement to, among other things, (i) reduce the size of the contractually committed bank facility from $1.5 billion to $1.4 billion, (ii) extend the maturity date from June 2026 to June 2028, and (iii) replace the LIBOR-based rate with a SOFR-based rate. The liquidity facilities also includes up to $500 million of uncommitted financings based on eligible receivables balances under a receivables securitization program that expires in June 2025. At June 30, 2024, the Company had no borrowings outstanding under the receivables securitization program.

During the first quarter of 2024, the Company had debt reductions of $3 million related to decreases in the amount of capital leases.

During the second quarter of 2024, the Company had debt reductions of $5 million related to decreases in the amount of capital leases.

The Company’s financial covenants require the maintenance of a minimum net worth, as defined in our debt agreements, of $9 billion and a total debt-to-capital ratio of less than 60 %. Net worth is defined as the sum of common stock, paid-in capital and retained earnings, less treasury stock plus any cumulative goodwill impairment charges. The calculation also excludes accumulated other comprehensive income/loss and both the current and long-term Nonrecourse Financial Liabilities of Variable Interest Entities. The total debt-to-capital ratio is defined as total debt divided by the sum of total debt plus net worth. As of June 30, 2024, we were in compliance with our debt covenants.

At June 30, 2024, the fair value of International Paper’s $5.6 billion of debt was approximately $5.2 billion. The fair value of the Company’s long-term debt is estimated based on the quoted market prices for the same or similar issues. International Paper’s long-term debt is classified as Level 2 within the fair value hierarchy, which is further defined in Note 1 in the Company’s Annual Report.

International Paper sponsors and maintains the Retirement Plan of International Paper Company (the "Pension Plan"), a tax-qualified defined benefit pension plan that provides retirement benefits to substantially all hourly and union employees who work at a participating business unit. The Pension Plan was frozen as of January 1, 2019 for salaried participants.

The Pension Plan provides defined pension benefits based on years of credited service and either final average earnings (salaried employees and hourly employees receiving salaried benefits), hourly job rates or specified benefit rates (hourly and union employees).

Net periodic pension expense (income) for our qualified and nonqualified U.S. defined benefit plans comprised the following:

| Three Months Ended June 30, | Six Months Ended June 30, | ||||||||||||||||||||||

| In millions | 2024 | 2023 | 2024 | 2023 | |||||||||||||||||||

| Service cost | $ | $ | $ | $ | |||||||||||||||||||

| Interest cost | |||||||||||||||||||||||

| Expected return on plan assets | ( | ( | ( | ( | |||||||||||||||||||

| Actuarial loss | |||||||||||||||||||||||

| Amortization of prior service cost | |||||||||||||||||||||||

| Net periodic pension expense (income) | $ | $ | $ | ( | $ | ||||||||||||||||||

The components of net periodic pension expense (income) other than the Service cost component are included in Non-operating pension expense (income) in the condensed consolidated statement of operations.

20

The Company’s funding policy for our pension plans is to contribute amounts sufficient to meet legal funding requirements, plus any additional amounts that the Company may determine to be appropriate considering the funded status of the plan, tax deductibility, the cash flows generated by the Company, and other factors. The Company made no 11 million for the six months ended June 30, 2024.

On February 13, 2024, the Company's Board of Directors, upon recommendation of the Management Development and Compensation Committee (the "Committee"), authorized adoption of a 2024 Long-Term Incentive Compensation Plan (the "2024 LTICP") to replace the 2009 Amended and Restated Incentive Compensation Plan (the "2009 Plan"), subject to shareowner approval at the Company's annual meeting of shareowners held on May 13, 2024. The 2024 LTICP became effective following approval by shareowners at the May 13, 2024 annual meeting and replaced the 2009 Plan. The 2024 LTICP authorized up to 9,250,000 shares of our Class A common stock, par value $1.00 per share, available for future grants in the form of restricted stock, restricted or deferred stock units, performance awards payable in cash or stock upon the attainment of specified performance goals, dividend equivalents, options, stock appreciation rights, other stock-based awards and cash-based awards at the discretion of the Committee. The LTICP is administered by the Committee. As of June 30, 2024, 9.2 million shares were available for grant under the 2024 LTICP.

Stock-based compensation expense and related income tax benefits were as follows:

| Three Months Ended June 30, | Six Months Ended June 30, | ||||||||||||||||||||||

| In millions | 2024 | 2023 | 2024 | 2023 | |||||||||||||||||||

| Total stock-based compensation expense (selling and administrative) | $ | $ | ( | $ | $ | ||||||||||||||||||

| Income tax benefits related to stock-based compensation | |||||||||||||||||||||||

At June 30, 2024, $103 million, net of estimated forfeitures, of compensation cost related to time-based and performance-based shares and restricted stock attributable to future service had not yet been recognized. This amount will be recognized in expense over a weighted-average period of 1.6 years.

Long-Term Incentive Plan

During the first sixth months of 2024, the Company granted 2.0 million performance units at an average grant date fair value of $35.25 and 1.4 million time-based units at an average grant date fair value of $36.15 .

International Paper’s business segments, Industrial Packaging and Global Cellulose Fibers, are consistent with the internal structure used to manage these businesses. Both segments are differentiated on a common product, common customer basis consistent with the business segmentation generally used in the Forest Products industry.

Business segment operating profits (losses) are used by International Paper's management to measure the earnings performance of its businesses. Management believes that this measure allows a better understanding of trends in costs, operating efficiencies, prices and volumes. Business segment operating profits (losses) are defined as earnings (loss) from continuing operations before income taxes and equity earnings, but including the impact of less than wholly owned subsidiaries, and excluding interest expense, net, corporate expenses, net, corporate net special items, business net special items and non-operating pension expense.

21

Net sales by business segment for the three months and six months ended June 30, 2024 and 2023 were as follows:

| Three Months Ended June 30, | Six Months Ended June 30, | ||||||||||||||||||||||

| In millions | 2024 | 2023 | 2024 | 2023 | |||||||||||||||||||

| Industrial Packaging | $ | $ | $ | $ | |||||||||||||||||||

| Global Cellulose Fibers | |||||||||||||||||||||||

| Corporate and Intersegment Sales | |||||||||||||||||||||||

| Net Sales | $ | $ | $ | $ | |||||||||||||||||||

Operating profit (loss) by business segment for the three months and six months ended June 30, 2024 and 2023 were as follows:

| Three Months Ended June 30, | Six Months Ended June 30, | ||||||||||||||||||||||

| In millions | 2024 | 2023 | 2024 | 2023 | |||||||||||||||||||

| Industrial Packaging | $ | $ | $ | $ | |||||||||||||||||||

| Global Cellulose Fibers | ( | ||||||||||||||||||||||

| Business Segment Operating Profit (Loss) | $ | $ | $ | $ | |||||||||||||||||||

| Net Earnings (Loss) From Continuing Operations | $ | $ | $ | $ | |||||||||||||||||||

| Add back (deduct): | |||||||||||||||||||||||

| Income tax provision (benefit) | ( | ( | |||||||||||||||||||||

| Equity (earnings) loss, net of taxes | |||||||||||||||||||||||

| Earnings (loss) from continuing operations before income taxes and equity earnings | |||||||||||||||||||||||

| Interest expense, net | |||||||||||||||||||||||

| Adjustment for less than wholly owned subsidiaries | ( | ( | |||||||||||||||||||||

| Corporate expenses, net | |||||||||||||||||||||||

| Corporate net special items | |||||||||||||||||||||||

| Business net special items | ( | ||||||||||||||||||||||

| Non-operating pension expense (income) | ( | ( | |||||||||||||||||||||

| Business Segment Operating Profit (Loss) | $ | $ | $ | $ | |||||||||||||||||||

22

The following discussion and analysis of our financial condition and results of operations should be read in conjunction with our unaudited condensed consolidated financial statements and related notes included in "Financial Statements and Supplementary Data" of this Quarterly Report on Form 10-Q (this "Form 10-Q") and the Company's Annual Report on Form 10-K for the year ended December 31, 2023 (our "Annual Report"). In addition to historical consolidated financial information, the following discussion contains forward-looking statements that reflect our plans, estimates, and beliefs that involve significant risks and uncertainties. Our actual results could differ materially from those discussed in the forward-looking statements. Factors that could cause or contribute to those differences include those discussed below and in our Annual Report, particularly under "Risk Factors" and "Forward-Looking Statements" of this Form 10-Q and our Annual Report. Please see our "Cautionary Statement Regarding Forward-Looking Statements" below.

EXECUTIVE SUMMARY

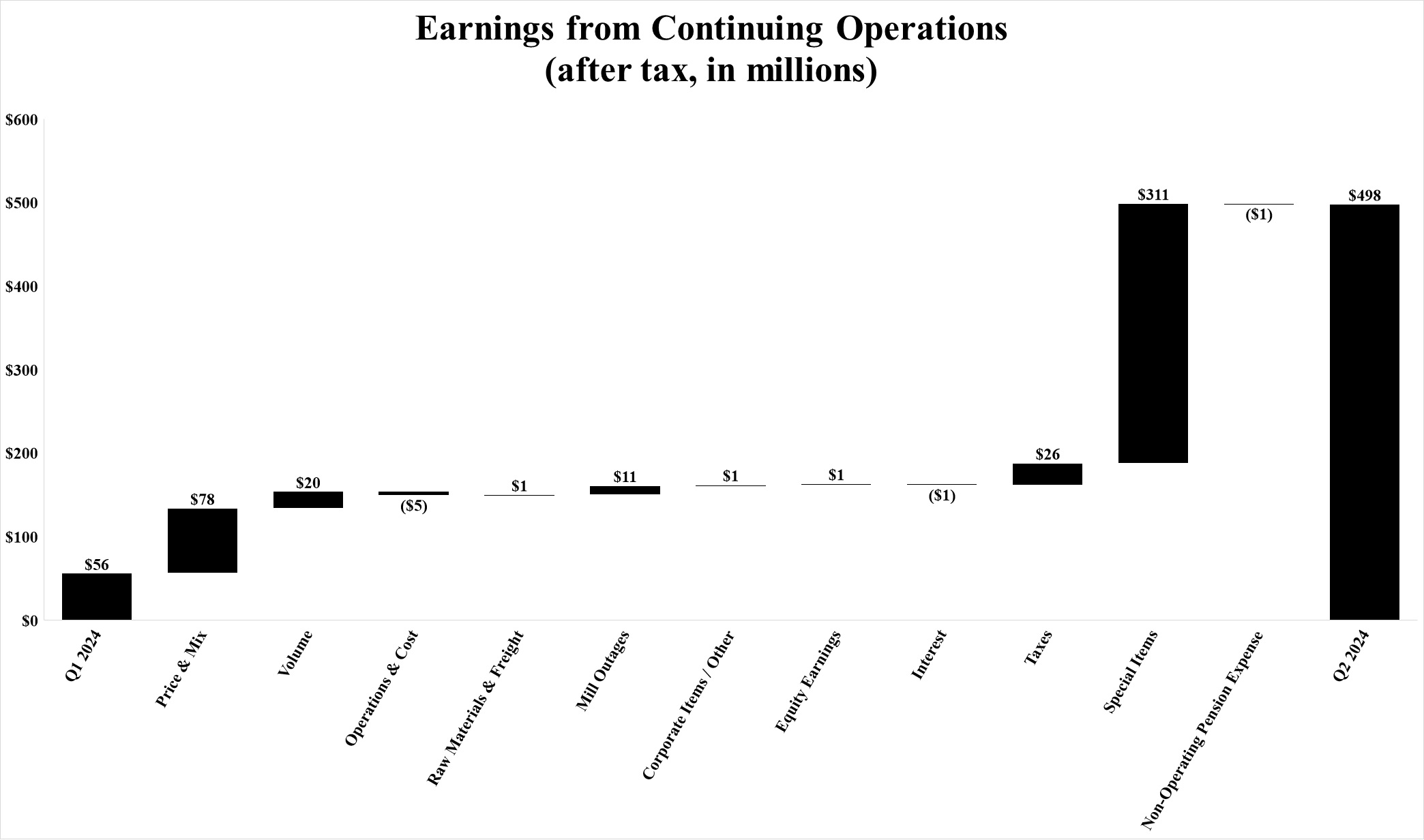

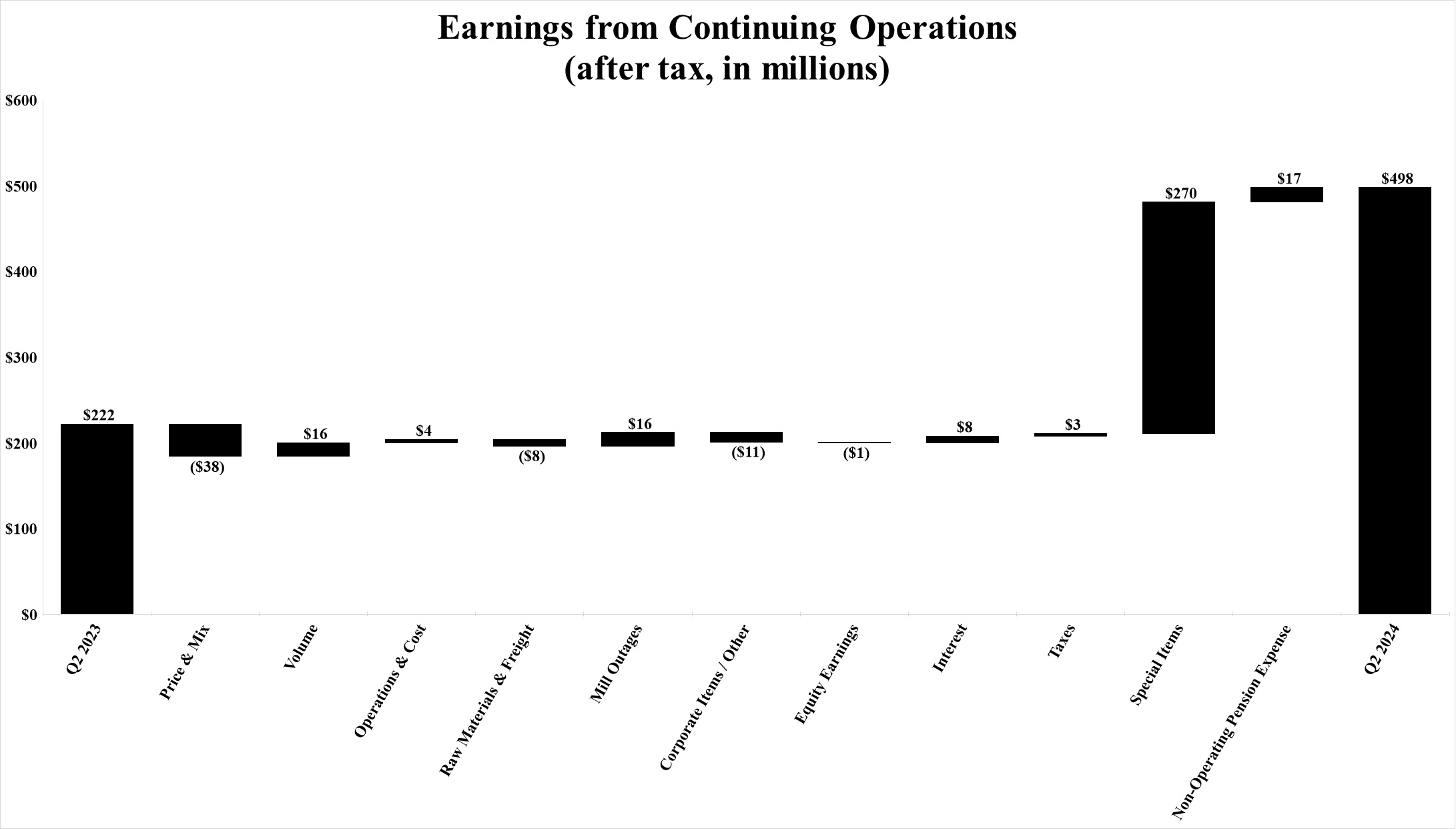

Net earnings (loss) were $498 million ($1.41 per diluted share) in the second quarter of 2024, compared with $56 million ($0.16 per diluted share) in the first quarter of 2024 and $235 million ($0.68 per diluted share) in the second quarter of 2023. The Company generated Adjusted operating earnings (a non-GAAP measure defined below) of $193 million ($0.55 per diluted share) in the second quarter of 2024, compared with $61 million ($0.17 per diluted share) in the first quarter of 2024 and $204 million ($0.59 per diluted share) in the second quarter of 2023.

International Paper delivered improved earnings in the second quarter of 2024 on higher sales prices across the portfolio along with higher volumes on improved box demand. We were encouraged to see stable to moderately improved industry demand across various customer markets we serve. Even with the stable demand environment positively impacting volumes, our Industrial Packaging volumes performance came in below expectations and continued to lag the overall packaging market. We realized some additional benefits from our Box Go-to-Market strategy, but we believe that the second quarter performance also reflects the lagging residual effect of under investing in certain areas where, as a result, there have been ongoing reliability and capacity issues. Over the past year, we have been investing more in our box system and we are seeing improvement in key metrics such as customer on-time delivery and machine productivity. Fixing these issues continues to be a particular focus in future periods but in the near term, specifically the third quarter 2024, earnings are expected to be negatively impacted by this reset along with higher maintenance outage expense and seasonally lower sales volumes. In order to accelerate improvement, we are deploying an 80/20 strategic approach. We intend to make the changes needed to focus our portfolio, become excellent with our customers and optimize our costs to deliver profitable growth. In North America, our investments will center on providing customers with the most reliable and innovative packaging solutions.

Comparing our performance in the second quarter of 2024 to the first quarter of 2024, price and mix in our Industrial Packaging business was higher due to the realization of benefits from prior index movements. We believe that the improved price and mix also reflects the benefits from our Box Go-to-Market Strategy along with higher export pricing and mix. Price and mix in our Global Cellulose Fibers business was higher due to prior index movement and the GCF optimization strategy driving benefits from higher absorbent pulp mix, and a reduction in commodity grades. Volume in our Industrial Packaging business was higher in the second quarter on a stable to improving demand trend. However, our Box Go-to-Market Strategy is about making choices that are expected to adversely impact our volume in the near term but are intended to allow us to improve our margins and mix over the long term. Although we expect to trail the industry for the next few quarters in unit volume growth, we expect the volume impacts to be temporary, as we continue to transition toward our target mix of customers and invest in the business to maximize profitability. Volume in our Global Cellulose Fibers business was sequentially flat overall, as improved demand for absorbent pulp was offset by lower sales of commodity grades, as we continued to focus on strategically aligning our business with the most attractive customers and end markets. Operations and costs were sequentially higher in our Industrial Packaging business due to the impacts of inflation, seasonally higher selling and administration costs and higher spending to improve reliability. Operations and costs in our Global Cellulose Fibers business were lower due in large part to lower fixed costs resulting from the closure of the pulp machine at our Riegelwood, North Carolina mill. Planned maintenance outages were marginally higher in our Industrial Packaging business while lower in our Global Cellulose Fibers business. Input costs were flat in our Industrial Packaging business as lower energy costs offset higher recovered fiber costs. Input costs in our Global Cellulose Fibers business were slightly higher, primarily driven by higher chemical and wood costs partially offset by lower energy costs.

Looking ahead to the third quarter of 2024, as compared to the second quarter of 2024, in our Industrial Packaging business, we expect price and mix to improve earnings from prior index movements in North America and higher export prices to date. We also expect incremental benefit from continued progress with our Box Go-to-Market strategy. Volume is expected to be lower in North America on one less shipping day versus the second quarter of 2024 along with seasonally lower daily demand.

23

Operations and costs are expected to be higher on increased reliability spending, labor and benefits costs during the summer months, timing of maintenance spend, and higher unabsorbed fixed costs. Maintenance outage expense is expected to be higher in the third quarter of 2024 while input costs are also expected to be higher on increased energy costs. In our Global Cellulose Fibers business, we expect price and mix to increase earnings on prior index movements. Volume is expected to be lower on seasonally lower demand. Operations and costs are expected to be higher due to higher distribution costs, timing of maintenance spend, as well as higher unabsorbed fixed costs. Maintenance outage expense is expected to be lower while input costs are expected to be stable relative to the second quarter of 2024.