Table of Contents

As filed with the U.S. Securities and Exchange Commission on October 5, 2020

Registration No. 333-238072

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

Amendment No. 4

to

FORM S-4

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

INTERNATIONAL FLAVORS & FRAGRANCES INC.

(Exact name of registrant as specified in its charter)

| New York | 2860 | 13-1432060 | ||

| (State or other jurisdiction of incorporation or organization) |

(Primary Standard Industrial Classification Code Number) |

(I.R.S. Employer Identification Number) |

521 West 57th Street

New York, NY 10019-2960

(212) 765-5500

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

Anne Chwat

Executive Vice President, General Counsel and Corporate Secretary

International Flavors & Fragrances Inc.

521 West 57th Street

New York, New York 10019

(212) 765-5500

(Name, address, including zip code, and telephone number, including area code, of agent for service)

With copies to:

| Christopher E. Austin Cleary Gottlieb Steen & Hamilton LLP One Liberty Plaza New York, NY 10006 (212) 225-2000 |

Erik T. Hoover Senior Vice President and General Counsel DuPont de Nemours, Inc. 974 Centre Road, Building 730 Wilmington, DE 19805 (302) 774-3034 |

Brandon Van Dyke Skadden, Arps, Slate, Meagher & Flom LLP One Manhattan West New York, NY 10001 (212) 735-3000 |

Approximate date of commencement of the proposed sale of the securities to the public: As soon as possible following the effective date of this registration statement and satisfaction or waiver of all other conditions to the consummation of the Exchange Offer and Merger described herein.

Table of Contents

If the securities being registered on this Form are being offered in connection with the formation of a holding company and there is compliance with General Instruction G, check the following box. ☐

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☒ | Accelerated filer | ☐ | |||

| Non-accelerated filer | ☐ | Smaller reporting company | ☐ | |||

| Emerging growth company | ☐ | |||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided to Section 7(a)(2)(B) of the Securities Act. ☐

If applicable, place an X in the box to designate the appropriate rule provision relied upon in conducting this transaction:

| Exchange Act Rule 13e-4(i) (Cross-Border Issuer Tender Offer) |

☐ | |||

| Exchange Act Rule 14d-1(d) (Cross-Border Third-Party Tender Offer) |

☐ |

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended, or until this registration statement shall become effective on such date as the U.S. Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

Table of Contents

EXPLANATORY NOTE

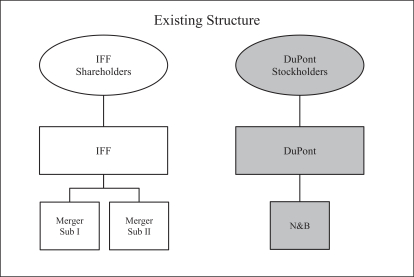

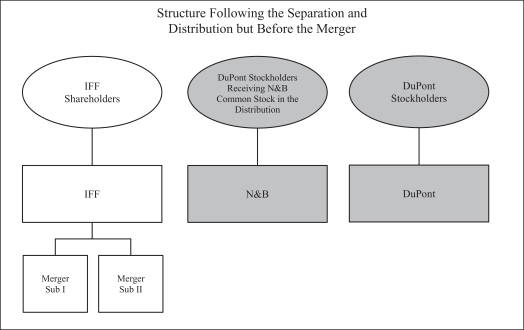

International Flavors & Fragrances Inc. (“IFF”) is filing this registration statement on Form S-4 (Registration No. 333-238072) to register the shares of its common stock, par value $0.125 per share (“IFF common stock”), that will be issued in the merger of Neptune Merger Sub I Inc., a Delaware corporation (“Merger Sub I”), which is a wholly owned subsidiary of IFF, with and into Nutrition & Biosciences, Inc., a Delaware corporation (“N&B”), which is a wholly owned subsidiary of DuPont de Nemours, Inc., a Delaware corporation (“DuPont”), whereby the separate corporate existence of Merger Sub I will cease and N&B will continue as the surviving company and a wholly owned subsidiary of IFF (the “Merger”). Prior to the Merger, subject to the terms of the Separation Agreement (as defined below), DuPont will transfer certain assets, liabilities and entities comprising its nutrition and biosciences business (such business to be transferred, the “N&B Business”) to N&B or its subsidiaries. In exchange therefor, DuPont will receive shares of N&B common stock, as well as the Special Cash Payment (as defined below), and the shares of N&B common stock will be distributed to DuPont stockholders as provided below. As a result of the Merger, the existing shares of N&B common stock will be automatically converted into the right to receive shares of IFF common stock. No fewer than 30 days (and in some circumstances 15 days) after the Merger, N&B will merge with and into Neptune Merger Sub II LLC, a Delaware limited liability company (“Merger Sub II”), which is a wholly owned subsidiary of IFF, with Merger Sub II surviving as a wholly owned subsidiary of IFF (the “Second Merger,” and together with the Merger, the “Mergers”).

N&B is a newly formed, wholly owned subsidiary of DuPont that was organized specifically for the purpose of effecting the Separation (as defined below). N&B has engaged in no business activities to date and it has no material assets or liabilities of any kind, other than those incident to its formation and those incurred in connection with the Transactions (as defined below). The shares of N&B common stock will be immediately converted into shares of IFF common stock upon completion of the Merger. IFF filed a proxy statement that relates to the special meeting of shareholders of IFF to approve the issuance of shares of IFF common stock in the Merger. In addition, N&B filed a registration statement on Form S-4 and Form S-1 (Registration No. 333-238089) to register the offer of shares of N&B common stock, which shares will be distributed to DuPont stockholders.

Based on market conditions prior to the closing of the Merger, DuPont will determine whether the shares of N&B common stock will be distributed to DuPont stockholders in a spin-off or a split-off exchange offer and if conducted as an exchange offer, the terms thereof (including whether to offer any discount for shares of N&B common stock). In a spin-off, all DuPont stockholders would receive a pro rata number of shares of N&B common stock. In a split-off exchange offer, DuPont would offer its stockholders the option to exchange their shares of DuPont common stock for shares of N&B common stock, which would be converted automatically into shares of IFF common stock in the Merger. As a result, there would be a reduction in DuPont’s outstanding shares. If the exchange offer is not fully subscribed because the number of shares of DuPont common stock tendered results in fewer than all of the shares of N&B common stock being exchanged, then DuPont would conduct a clean-up spin-off. In the clean-up spin-off, DuPont would distribute the remaining shares of N&B common stock on a pro rata basis to DuPont stockholders whose shares of DuPont common stock remain outstanding after the consummation of the exchange offer. If DuPont decides to undertake a split-off exchange offer, DuPont presently expects that a clean-up spin-off will be necessary following the exchange offer.

IFF and N&B are filing this registration statement under the assumption that the shares of N&B common stock will be distributed to DuPont stockholders pursuant to an exchange offer with a clean-up spin-off to distribute any additional shares of N&B common stock not exchanged in the exchange offer. However, no final decision has been made about whether the shares will be distributed by way of an exchange offer or a spin-off or the final terms of any potential exchange offer (including whether to offer any discount for shares of N&B common stock). Once a final decision is made regarding the manner of distribution of the shares, this registration statement on Form S-4 (Registration No. 333-238072) will be amended to reflect that decision, if necessary. It is not expected that DuPont’s decision to effect the distribution of N&B common stock solely through a spin-off instead of a split-off exchange offer would have a material impact on the combined company or on IFF’s shareholders.

Table of Contents

The information in this prospectus is not complete and may change. The Exchange Offer and issuance of securities being registered pursuant to the registration statement of which this prospectus forms a part may not be completed until the registration statement is effective. This prospectus is not an offer to sell these securities, and it is not soliciting an offer to buy these securities, in any jurisdiction where such offer or sale is not permitted.

SUBJECT TO COMPLETION, DATED OCTOBER 5, 2020

PRELIMINARY PROSPECTUS—OFFER TO EXCHANGE

DuPont de Nemours, Inc.

Offer to Exchange Shares of Common Stock of

NUTRITION & BIOSCIENCES, INC.

which are owned by DuPont de Nemours, Inc.

and will be converted into Shares of Common Stock of

INTERNATIONAL FLAVORS & FRAGRANCES INC.

for

Shares of Common Stock of DuPont de Nemours, Inc.

DuPont de Nemours, Inc. (“DuPont”) is offering to exchange all shares of common stock (“N&B common stock”) of Nutrition & Biosciences, Inc. (“N&B”) owned by DuPont for shares of common stock of DuPont (“DuPont common stock”) that are validly tendered and not properly withdrawn. The number of shares of DuPont common stock that will be accepted if the Exchange Offer (as defined below) is completed will depend on the final exchange ratio and the number of shares of DuPont common stock tendered. The terms and conditions of the Exchange Offer are described in this prospectus, which you should read carefully. None of DuPont, N&B, any of their respective directors or officers nor any of their respective representatives makes any recommendation as to whether you should participate in the Exchange Offer. You must make your own decision after reading this prospectus and consulting with your advisors. The Exchange Offer is voluntary. If you would like to keep all of your shares of DuPont common stock, you do not need to take any action.

DuPont’s obligation to exchange shares of N&B common stock for shares of DuPont common stock is subject to the satisfaction of certain conditions, including conditions to the consummation of the Transactions (as defined below), which include approval by the shareholders of International Flavors & Fragrances Inc. (“IFF”) of the issuance of shares of common stock of IFF (“IFF common stock”) in the Merger (as defined below) (IFF’s shareholders approved the issuance of shares of IFF common stock in the Merger at a special meeting on August 27, 2020).

The Transactions are being undertaken to transfer the N&B Business (as defined below) from DuPont to IFF. The aggregate value of the consideration to be paid to DuPont stockholders with respect to the N&B Business in the Transactions is estimated to be approximately $ billion in value of IFF common stock (calculated based on the closing price on the New York Stock Exchange (the “NYSE”) of IFF common stock as of , 2020) issuable to DuPont stockholders that participate in the Exchange Offer or receive shares in the Clean-Up Spin-Off (as defined below) if the Exchange Offer is not fully subscribed because the number of shares of DuPont common stock tendered results in fewer than all shares of N&B common stock being exchanged. This stock consideration combined with the Special Cash Payment (as defined below) would result in an overall value of approximately $ billion received by DuPont and DuPont stockholders in connection with the Transactions.

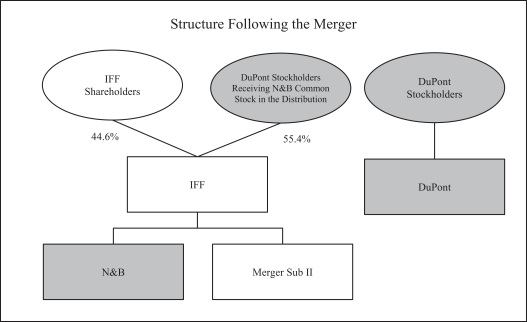

Immediately following the distribution of shares of N&B common stock to DuPont stockholders (the “Distribution”), a wholly owned subsidiary of IFF named Neptune Merger Sub I Inc., a Delaware corporation (“Merger Sub I”), will be merged with and into N&B, whereby the separate corporate existence of Merger Sub I will cease and N&B will continue as the surviving company and a wholly owned subsidiary of IFF (the “Merger”). In the Merger, each outstanding share of N&B common stock (except for shares of N&B common stock held by N&B as treasury stock or by DuPont, which will be automatically cancelled) will be automatically converted into the right to receive a number of shares of IFF common stock equal to the exchange ratio set forth in the Merger Agreement. The aggregate number of shares of IFF common stock to be issued in the Merger by IFF is expected to result in pre-Merger holders of shares of N&B common stock collectively owning approximately 55.4% of the issued and outstanding shares of IFF common stock on a fully diluted basis after giving effect to the Merger and IFF’s existing shareholders collectively owning approximately 44.6% of the issued and outstanding shares of IFF common stock on a fully diluted basis (in each case, excluding any overlaps in the pre-Merger stockholder bases). N&B common stock will not be transferred to participants in the Exchange Offer; such participants will instead receive shares of IFF common stock in the Merger. No trading market currently exists for N&B common stock. You will not be able to trade shares of N&B common stock before they are converted into shares of IFF common stock in the Merger. In addition, there can be no assurance that shares of IFF common stock, when issued in the Merger, will trade at the same prices that shares of IFF common stock are traded at prior to the Merger.

The value of DuPont common stock and N&B common stock will be determined by DuPont by reference to the simple arithmetic average of the daily volume-weighted average prices (“VWAP”) on each of the Valuation Dates (as defined below) of DuPont common stock on the NYSE and IFF common stock on the NYSE on each of the last full three trading days ending on and including the second trading day preceding the expiration date of the Exchange Offer period (“Valuation Dates”), as it may be voluntarily extended. Based on an expiration date of , 2020, the Valuation Dates are expected to be , 2020, , 2020 and , 2020. See “The Exchange Offer—Terms of the Exchange Offer.”

The Exchange Offer is designed to permit you to exchange your shares of DuPont common stock for shares of N&B common stock at a % discount to the per-share value of IFF common stock, calculated as set forth in this prospectus, subject to the upper limit described below. For each $100 of DuPont common stock accepted in the Exchange Offer, you will receive approximately $ of N&B common stock, subject to an upper limit of shares of N&B common stock per share of DuPont common stock. The Exchange Offer does not provide for a minimum exchange ratio. See “The Exchange Offer—Terms of the Exchange Offer.” If the upper limit is in effect, then the exchange ratio will be fixed at that limit. IF THE UPPER LIMIT IS IN EFFECT, AND UNLESS YOU PROPERLY WITHDRAW YOUR SHARES, YOU WILL RECEIVE LESS THAN $ OF N&B COMMON STOCK FOR EACH $100 OF DUPONT COMMON STOCK THAT YOU TENDER, AND YOU COULD RECEIVE MUCH LESS.

Table of Contents

The indicative exchange ratio that would have been in effect following the official close of trading on the NYSE on , 2020 (the second to last trading day before the date of this prospectus), based on the daily VWAPs of DuPont common stock and IFF common stock on , 2020, , 2020 and , 2020 would have provided for shares of N&B common stock to be exchanged for every share of DuPont common stock accepted. The value of N&B common stock received and, following the Merger, the value of IFF common stock received may not remain above the value of DuPont common stock tendered following the expiration of the Exchange Offer.

THE EXCHANGE OFFER AND WITHDRAWAL RIGHTS WILL EXPIRE AT P.M., NEW YORK CITY TIME, ON , 2020 UNLESS THE OFFER IS EXTENDED OR TERMINATED. SHARES OF DUPONT COMMON STOCK TENDERED PURSUANT TO THE EXCHANGE OFFER MAY BE WITHDRAWN AT ANY TIME PRIOR TO THE EXPIRATION OF THE EXCHANGE OFFER.

In reviewing this prospectus, you should carefully consider the risk factors beginning on page 65 of this prospectus.

We Are Not Asking You for a Proxy and You are Requested Not To Send Us a Proxy.

Neither the U.S. Securities and Exchange Commission (the “SEC”) nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

The date of this prospectus is , 2020.

The final exchange ratio used to determine the number of shares of N&B common stock that you will receive for each share of DuPont common stock accepted in the Exchange Offer will be announced by press release no later than 11:59 p.m., New York City time, at the end of the second trading day immediately preceding the expiration date. At such time, the final exchange ratio will be available at https:// and from the information agent at the toll-free number provided on the back cover of this prospectus. DuPont will announce whether the upper limit on the number of shares that can be received for each share of DuPont common stock tendered will be in effect, through https:// and by press release, no later than 11:59 p.m., New York City time, at the end of the second trading day immediately preceding the expiration date. Starting at the end of the third trading day of the Exchange Offer, indicative exchange ratios (calculated in the manner described in this prospectus) will also be available on that website and from the information agent at the toll-free number provided on the back cover of this prospectus.

This prospectus provides information regarding DuPont, N&B, IFF, the Exchange Offer, the Clean-Up Spin-Off and the Merger. DuPont stock is listed on the NYSE under the symbol “DD.” IFF common stock is listed on the NYSE, Euronext Paris and the Tel Aviv Stock Exchange (“TASE”) under the symbol “IFF.” On , 2020, the last reported sale price of DuPont common stock on the NYSE was $ per share, and the last reported sale price of IFF common stock on the NYSE was $ per share. The market prices of DuPont common stock and of IFF common stock will fluctuate prior to the completion of the Exchange Offer and thereafter and may be higher or lower at the expiration date than the prices set forth above. No trading market currently exists for N&B common stock. N&B has not applied for listing of N&B common stock on any exchange.

Following the Exchange Offer, the remaining shares of N&B common stock held by DuPont (if the Exchange Offer is not fully subscribed because the number of shares of DuPont common stock that have been tendered results in fewer than all outstanding shares of N&B common stock being exchanged), will be distributed to DuPont stockholders whose shares of DuPont common stock remain outstanding after the consummation of the Exchange Offer pursuant to a pro rata distribution in the Clean-Up Spin-Off. Any DuPont stockholder who validly tenders (and does not properly withdraw) shares of DuPont common stock for shares of N&B common stock and whose shares are accepted in the Exchange Offer will waive their rights with respect to such shares to receive, and forfeit any rights to, shares of N&B common stock distributed on a pro rata basis to DuPont stockholders in the Clean-Up Spin-Off. This prospectus covers all shares of N&B common stock offered by DuPont in the Exchange Offer and all shares of N&B common stock that may be distributed by DuPont in the Clean-Up Spin-Off (or, if the Exchange Offer is terminated by DuPont, the Spin-Off (as defined below)) to holders of shares of DuPont common stock. If the Exchange Offer is terminated by DuPont without the exchange of shares (but the conditions to consummation of the Transactions have otherwise been satisfied), all shares of N&B common stock owned by DuPont will be distributed in a spin-off on a pro rata basis to holders of DuPont common stock, with a record date to be announced by DuPont (the “Spin-Off”). See “The Exchange Offer—Distribution of N&B Common Stock Remaining After the Exchange Offer.”

Following the consummation of the Distribution, in the Merger, Merger Sub I will be merged with and into N&B, whereby the separate corporate existence of Merger Sub I will cease and N&B will continue as the surviving company. In the Merger, each outstanding share of N&B common stock (except for shares of N&B common stock held by N&B as treasury stock or by DuPont, which will be cancelled) will be automatically converted into the right to receive a number of shares of IFF common stock equal to the exchange ratio set forth in the Merger Agreement. The aggregate number of shares of IFF common stock to be issued in the Merger by IFF is expected to result in pre-Merger holders of shares of N&B common stock collectively owning approximately 55.4% of the issued and outstanding shares of IFF common stock on a fully diluted basis after giving effect to the Merger and IFF’s existing shareholders collectively owning approximately 44.6% of the issued and outstanding shares of IFF common stock on a fully diluted basis (in each case, excluding any overlaps in the pre-Merger shareholder bases).

No fewer than 30 days (and in some circumstances 15 days) following the Merger, N&B will be merged with and into Neptune Merger Sub II LLC, a Delaware limited liability company (“Merger Sub II”), which is a wholly owned subsidiary of IFF, whereby the separate corporate existence of N&B will cease and Merger Sub II will continue as the surviving company (such merger, the “Second Merger” and together with the Merger, the “Mergers”).

DuPont’s obligation to exchange shares of N&B common stock for IFF common stock is subject to the conditions listed under “The Exchange Offer—Conditions to Consummation of the Exchange Offer,” including the satisfaction of conditions to the Merger.

Table of Contents

i

Table of Contents

| 132 | ||||

| 134 | ||||

| 134 | ||||

| 134 | ||||

| 135 | ||||

| 135 | ||||

| 135 | ||||

| 136 | ||||

| 136 | ||||

| 136 | ||||

| 137 | ||||

| 137 | ||||

| 137 | ||||

| 138 | ||||

| 138 | ||||

| 138 | ||||

| 139 | ||||

| 139 | ||||

| 139 | ||||

| 139 | ||||

| 140 | ||||

| 140 | ||||

| Selected Historical Combined Financial Data of the N&B Business |

140 | |||

| 141 | ||||

| 143 | ||||

| DUPONT’S UNAUDITED PRO FORMA CONSOLIDATED FINANCIAL STATEMENTS |

145 | |||

| UNAUDITED CONDENSED COMBINED PRO FORMA INFORMATION OF IFF AND THE N&B BUSINESS |

156 | |||

| 179 | ||||

| 182 | ||||

| 183 | ||||

| 197 | ||||

| 203 | ||||

| 203 | ||||

| 204 | ||||

| 207 | ||||

| 208 | ||||

| 209 | ||||

| 222 | ||||

| 225 | ||||

| 235 | ||||

| 244 | ||||

| 248 | ||||

| 250 | ||||

| 253 | ||||

ii

Table of Contents

| Board of Directors and Management of IFF Following the Transactions |

254 | |||

| Interests of DuPont’s and N&B’s Directors and Executive Officers in the Transactions |

254 | |||

| Interests of IFF’s Directors and Executive Officers in the Transactions |

255 | |||

| Effects of the Distribution and the Merger on DuPont Equity Awards |

261 | |||

| 262 | ||||

| 262 | ||||

| 263 | ||||

| 265 | ||||

| 265 | ||||

| 265 | ||||

| 265 | ||||

| 266 | ||||

| Distributions With Respect to Shares of IFF Common Stock after the Effective Time of the Merger |

266 | |||

| 267 | ||||

| 267 | ||||

| 267 | ||||

| 268 | ||||

| 270 | ||||

| 276 | ||||

| 276 | ||||

| 276 | ||||

| 280 | ||||

| 281 | ||||

| 283 | ||||

| 283 | ||||

| 285 | ||||

| Termination Fees and Expenses Payable in Certain Circumstances |

288 | |||

| 289 | ||||

| 289 | ||||

| 289 | ||||

| 290 | ||||

| 290 | ||||

| 298 | ||||

| 298 | ||||

| 299 | ||||

| 299 | ||||

| 299 | ||||

| 301 | ||||

| 301 | ||||

| 301 | ||||

| 302 | ||||

| 302 | ||||

| 302 | ||||

| 303 | ||||

| 303 | ||||

iii

Table of Contents

| 306 | ||||

| 306 | ||||

| 309 | ||||

| 310 | ||||

| 312 | ||||

| 312 | ||||

| 312 | ||||

| 313 | ||||

| 313 | ||||

| 313 | ||||

| 314 | ||||

| 314 | ||||

| 314 | ||||

| 314 | ||||

| DESCRIPTION OF CAPITAL STOCK OF IFF AND THE COMBINED COMPANY |

315 | |||

| 315 | ||||

| 315 | ||||

| Certain Anti-Takeover Effects of Provisions of the IFF Charter and the IFF Bylaws |

316 | |||

| 317 | ||||

| 317 | ||||

| 318 | ||||

| 318 | ||||

| 319 | ||||

| COMPARISON OF RIGHTS OF HOLDERS OF DUPONT COMMON STOCK AND IFF COMMON STOCK |

320 | |||

| 320 | ||||

| Certain Anti-Takeover Effects of Provisions of the IFF Charter, the IFF Bylaws and New York Law |

334 | |||

| 335 | ||||

| 335 | ||||

| 337 | ||||

| 339 | ||||

| 342 | ||||

| 344 | ||||

| 344 | ||||

| 344 | ||||

| 345 | ||||

| WHERE YOU CAN FIND MORE INFORMATION; INCORPORATION BY REFERENCE |

345 | |||

| 346 | ||||

| 347 | ||||

| F-1 | ||||

| A-1 | ||||

| B-1 | ||||

iv

Table of Contents

This prospectus incorporates by reference important business and financial information about DuPont and IFF from documents filed with the SEC that have not been included in or delivered with this prospectus. This information is available without charge at the website that the SEC maintains at www.sec.gov, as well as from other sources. See “Where You Can Find More Information; Incorporation By Reference.” You also may ask any questions about the Exchange Offer or request copies of the Exchange Offer documents and the other information incorporated by reference in this prospectus, without charge, upon written or oral request to DuPont’s information agent, , located at , at the telephone number or at the email address . In order to receive timely delivery of the documents, you must make your requests no later than , 2021.

All information contained or incorporated by reference in this prospectus with respect to IFF, Merger Sub I, Merger Sub II and their respective subsidiaries, as well as information on IFF after the consummation of the Transactions, has been provided by IFF. All other information contained or incorporated by reference in this prospectus with respect to DuPont, N&B or their respective subsidiaries, or the N&B Business, and with respect to the terms and conditions of the Exchange Offer, has been provided by DuPont.

This prospectus is not an offer to sell or exchange and it is not a solicitation of an offer to buy any shares of DuPont common stock, N&B common stock or IFF common stock in any jurisdiction in which the offer, sale or exchange is not permitted. Non-U.S. stockholders should consult their advisors in considering whether they may participate in the Exchange Offer in accordance with the laws of their home countries and, if they do participate, whether there are any restrictions or limitations on transactions in the shares of N&B common stock that may apply in their home countries. DuPont, N&B and IFF cannot provide any assurance about whether such limitations may exist. See “The Exchange Offer—Certain Matters Relating to Non-U.S. Jurisdictions” for additional information about limitations on the Exchange Offer outside the United States.

v

Table of Contents

Certain abbreviations and terms used in the text and notes are defined below:

| Abbreviation/Term |

Description | |

| Ancillary Agreements |

The Tax Matters Agreement, the Employee Matters Agreement, the Intellectual Property Cross-License Agreement, the Trademark Cross-License Agreement, the Regulatory Cross-License Agreement, the Umbrella Secrecy Agreement, the Regulatory Transfer and Support Agreement, TMODS License Agreement, Transition Services Agreements, Supply Agreement, Space Leases and the other agreements set forth in the Separation Agreement and any other agreements to be entered into by and between any member of the N&B Group and any member of the DuPont Group, at, prior to or after the Distribution in connection with the Distribution (to the extent consented to by IFF), N&B and IFF, but shall exclude any conveyancing and assumption instruments and the Merger Agreement | |

| Benefit Plan |

All employee or director compensation and benefit plans, programs, agreements, policies or arrangements, including any employment, severance, welfare (including medical, dental, vision and life insurance), cafeteria, retirement, savings and other deferred compensation plans, programs, agreements, policies or arrangements | |

| Clean-Up Spin-Off |

The distribution by DuPont following the consummation of the Exchange Offer, if the Exchange Offer is not fully subscribed, of the remaining shares of N&B common stock owned by DuPont on a pro rata basis to DuPont stockholders whose shares of DuPont common stock remain outstanding after consummation of the Exchange Offer | |

| Code |

The Internal Revenue Code of 1986, as amended | |

| Collective Bargaining Agreement |

A collective bargaining agreement, labor agreement or similar written contract with a labor union, labor organization or other employee representative body and each written contract with a works council | |

| DGCL |

General Corporation Law of the State of Delaware | |

| Distribution |

The distribution by DuPont, pursuant to the Separation Agreement, of 100% of the shares of N&B common stock to DuPont’s stockholders in the Exchange Offer with the Clean-Up Spin-Off to the extent required, or the Spin-Off | |

1

Table of Contents

| Abbreviation/Term |

Description | |

| Distribution Date |

The date, as shall be determined by the board of DuPont, on which DuPont distributes all of the issued and outstanding shares of N&B common stock to the holders of DuPont common stock | |

| DuPont |

Depending on context, either DuPont de Nemours, Inc. or DuPont de Nemours, Inc. and its consolidated subsidiaries | |

| DuPont Benefit Plan |

Any Benefit Plan sponsored or maintained by DuPont or any member of the DuPont Group | |

| DuPont Bylaws |

DuPont’s Fourth Amended and Restated Bylaws, effective June 1, 2019 (as they may be amended) | |

| DuPont Charter |

DuPont’s Second Amended and Restated Certificate of Incorporation, effective June 1, 2019 (as it may be amended) | |

| DuPont common stock |

The common stock, par value $0.01 per share, of DuPont | |

| DuPont Equity Award |

Any outstanding DuPont Option, DuPont Stock Appreciation Right, DuPont RSU Award, DuPont Restricted Stock Award, DuPont PSU Award and other equity incentive compensation award that was granted under the DuPont Incentive Plan | |

| DuPont Group |

DuPont and each of its subsidiaries and any legal predecessors thereto, but excluding any member of the N&B Group | |

| DuPont Incentive Plan |

DuPont’s Omnibus Incentive Plan and any other equity compensation plan or arrangement maintained by DuPont | |

| DuPont Option |

Each option to purchase shares of DuPont common stock from DuPont, whether granted by DuPont pursuant to the DuPont Incentive Plan, assumed by DuPont in connection with any merger, acquisition or similar transaction or otherwise issued or granted and whether vested or unvested | |

| DuPont PSU Award |

Each stock unit representing the right to be issued shares of DuPont common stock by DuPont upon the satisfaction of a performance-based vesting requirement, whether granted by DuPont pursuant to the DuPont Incentive Plan, assumed by DuPont in connection with any merger, acquisition or similar transaction or otherwise issued or granted and whether vested or unvested | |

| DuPont Restricted Stock Award |

Each restricted stock award in respect of shares of DuPont common stock, whether granted by DuPont pursuant to the DuPont Incentive Plan, assumed by DuPont in connection with any merger, acquisition or similar transaction or otherwise issued or granted and whether vested or unvested | |

2

Table of Contents

| Abbreviation/Term |

Description | |

| DuPont RSP |

The DuPont Retirement Savings Plan | |

| DuPont RSU Award |

Each restricted stock unit representing the right to vest in and be issued shares of DuPont common stock by DuPont, whether granted by DuPont pursuant to a DuPont Incentive Plan, assumed by DuPont in connection with any merger, acquisition or similar transaction or otherwise issued or granted and whether vested or unvested | |

| DuPont Stock Appreciation Right |

Each stock appreciation right in respect of DuPont common stock, whether granted by DuPont pursuant to the DuPont Incentive Plan, assumed by DuPont in connection with any merger, acquisition or similar transaction or otherwise issued or granted and whether vested or unvested | |

| Employee Matters Agreement |

The Employee Matters Agreement, dated as of December 15, 2019, by and among DuPont, N&B and IFF | |

| Exchange Act |

The Securities Exchange Act of 1934, as amended | |

| Exchange Offer |

The exchange offer to which this prospectus relates, whereby DuPont is offering to its stockholders the ability to exchange all or a portion of their shares of DuPont common stock for shares of N&B common stock, which N&B common stock will be immediately exchanged for IFF common stock in the Merger | |

| GAAP |

Generally accepted accounting principles in the United States | |

| HSR Act |

The Hart-Scott-Rodino Antitrust Improvements Act of 1976, as amended | |

| IFF |

International Flavors & Fragrances Inc. | |

| IFF Bylaws |

IFF’s Bylaws (as they may be amended) | |

| IFF Charter |

IFF’s Restated Certificate of Incorporation (as it may be amended) | |

| IFF common stock |

The common stock, par value $0.125 per share, of IFF | |

| IFF Companies |

IFF and each of IFF’s subsidiaries, including Merger Sub I and Merger Sub II | |

| IFF Equity Awards |

Any outstanding LTIP Award, IFF Option, IFF PRSU, IFF RSU, IFF SSAR and other equity incentive compensation award that was granted under the IFF Incentive Plan | |

| IFF Form S-4 Registration Statement |

IFF’s registration statement on Form S-4 filed with the SEC in connection with the issuance of IFF common stock pursuant to the Merger, as such registration statement may be amended prior to the time it becomes effective under the Securities Act | |

3

Table of Contents

| Abbreviation/Term |

Description | |

| IFF Incentive Plan |

IFF’s 2015 Stock Award and Incentive Plan and any other equity compensation plan or arrangement maintained by IFF | |

| IFF Option |

Each option to purchase shares of IFF common stock from IFF, whether granted by IFF pursuant to the IFF Incentive Plan, assumed by IFF in connection with any merger, acquisition or similar transaction or otherwise issued or granted and whether vested or unvested | |

| IFF PRSU |

Each purchased restricted stock unit representing the right to vest in and be issued shares of IFF common stock by IFF, purchased pursuant to the IFF Incentive Plan | |

| IFF RSU |

Each restricted stock unit representing the right to vest in and be issued shares of IFF common stock by IFF, whether granted by IFF pursuant to the IFF Incentive Plan, assumed by IFF in connection with any merger, acquisition or similar transaction or otherwise issued or granted and whether vested or unvested | |

| IFF SSAR |

Each stock-settled appreciation right in respect of IFF common stock, whether granted by IFF pursuant to the IFF Incentive Plan, assumed by IFF in connection with any merger, acquisition or similar transaction or otherwise issued or granted and whether vested or unvested | |

| Indenture |

The indenture, dated September 16, 2020, between N&B and U.S. Bank National Association, as trustee | |

| Intellectual Property Cross-License Agreement |

The Intellectual Property Cross-License Agreement substantially in the form attached as Exhibit 10.4 hereto and to be entered into at or prior to the Distribution Date | |

| Internal Reorganization |

The transfer and/or assignment and assumption of certain N&B Assets, N&B Liabilities, Excluded Assets and Excluded Liabilities in furtherance of the Separation and the Parent Contribution | |

| LTIP Award |

Each performance cash and share in the form of long-term incentive plan awards granted by IFF pursuant to the IFF Incentive Plan | |

| Merger |

The merger of Merger Sub I with and into N&B, with N&B surviving the merger as a wholly owned subsidiary of IFF, as contemplated by the Merger Agreement | |

| Merger Agreement |

The Agreement and Plan of Merger, dated as of December 15, 2019, by and among DuPont, IFF, N&B and Merger Sub I (as it may be amended from time to time) | |

4

Table of Contents

| Abbreviation/Term |

Description | |

| Merger Sub I |

Neptune Merger Sub I Inc., a wholly owned subsidiary of IFF | |

| Merger Sub II |

Neptune Merger Sub II LLC, a wholly owned subsidiary of IFF | |

| N&B |

Nutrition & Biosciences, Inc., a Delaware corporation and currently a wholly owned subsidiary of DuPont | |

| N&B Assets |

The assets allocated to N&B and the members of the N&B Group described in the section of this document entitled “The Separation Agreement—The Separation—Transfer of Assets” | |

| N&B Benefit Plan |

Any Benefit Plan sponsored or maintained by N&B or any member of the N&B Group that is in place immediately prior to the Distribution | |

| N&B Business |

The nutrition and biosciences business of DuPont | |

| N&B Bylaws |

The Bylaws of N&B, dated as of October 30, 2019 (as they may be amended) | |

| N&B Certificate of Incorporation |

The Certificate of Incorporation of N&B, dated as of October 30, 2019 (as it may be amended) | |

| N&B common stock |

The common stock, par value $0.01 per share, of N&B | |

| N&B Companies |

N&B and its subsidiaries, after giving effect to the Separation and the Parent Contribution | |

| N&B Debt Financing |

The indebtedness to be incurred by N&B under the Commitment Letter and/or the Permanent Financing in connection with the transactions contemplated by the Separation Agreement and the Merger Agreement, as described in the section of this document entitled “Debt Financing” | |

| N&B Dedicated Employee |

Each individual described in Section 1.01(a)(i) of the Employee Matters Agreement (and, for the avoidance of doubt, not including any individual in a shared corporate or functional role to be identified pursuant to Section 1.01(a)(ii) of the Employee Matters Agreement) | |

| N&B Employee |

Each employee who is employed as of the Separation Date and is: (i) an N&B Dedicated Employee, (ii) identified through a process for talent selection to fill a shared corporate or functional department listed in Schedule 1.01(a)(ii) of the Employee Matters Agreement, (iii) hired by DuPont prior to the Distribution, as permitted under the Merger Agreement, (iv) by operation of law or the terms of the N&B Labor Agreement, without the taking of any action by DuPont or any of its affiliates, automatically transferred to the N&B Group on or before the Distribution Date or (v) mutually identified by N&B, DuPont and IFF, in each case, exclusive of Non-Consenting Employees or any individual, as determined and agreed upon by DuPont and IFF in | |

5

Table of Contents

| Abbreviation/Term |

Description | |

| good faith, was inappropriately identified for employment with a member of the N&B Group | ||

| N&B Group |

N&B, and each person that is a direct or indirect affiliate of N&B immediately following the Distribution, and each person that becomes a subsidiary of N&B after the Distribution | |

| N&B Indemnitees |

N&B, each other member of the N&B Group, and each of their affiliates from and after the Distribution, including IFF and each of IFF’s affiliates, and all persons who are or have been directors, officers, employees and of any member of the N&B Group (in each case, in their respective capacities as such), and their respective heirs, executors, successors and assigns | |

| N&B Key Executive Role |

The position of a principal executive officer of N&B or his or her direct reports | |

| N&B Liabilities |

The liabilities allocated to N&B and the members of the N&B Group described in the section of this document entitled “The Separation Agreement—The Separation—Assumption of Liabilities” | |

| New York City time |

Local time in the City of New York, New York | |

| Non-Consenting Employees |

Each individual who otherwise would be an N&B Employee pursuant to Section 1.01(a) of the Employee Matters Agreement, who has the right under applicable law or applicable N&B Labor Agreement to object to, opt out of, refuse to consent to, or otherwise fail to acquiesce to, and who has (a) validly objected to, opted out of, refused to consent to, or otherwise failed to acquiesce to, the automatic transfer of their employment to N&B Group by operation of applicable law, in cases where such employee is subject to automatic transfer by operation of applicable law, (b) validly refused to consent to, refused to accept the offer to, refused to execute a tripartite agreement or otherwise failed to acquiesce to, become an employee of N&B Group, or (c) validly objected to, opted out of, refused to consent to, or otherwise failed to acquiesce to, changes in his or her compensation or employee benefits by validly resigning or terminating his or her employment with, validly withdrawing his or her consent to employment with or validly rejecting his or her transfer to, N&B Group, in accordance with and to the extent permitted by applicable law or an applicable N&B Labor Agreement | |

| NYSE |

The New York Stock Exchange | |

| Parent Contribution |

The conveyance by DuPont to N&B of certain assets and liabilities constituting the N&B Business | |

6

Table of Contents

| Abbreviation/Term |

Description | |

| record date |

The record date to be established for any pro rata distribution of shares | |

| SEC |

The United States Securities and Exchange Commission | |

| Securities Act |

The Securities Act of 1933, as amended | |

| Separation |

The transfer of the N&B Assets that are not already owned by members of the N&B Group to members of the N&B Group and the assumption of the N&B Liabilities that are not already directly owed by or otherwise directly the responsibility of members of the N&B Group by members of the N&B Group, and the transfer of Excluded Assets that are not already directly owned by members of the DuPont Group to members of the DuPont Group and the Assumption of the Excluded Liabilities that are not already directly owed by or otherwise the responsibility of members of the DuPont Group by the DuPont Group, including the steps contemplated by the Internal Reorganization | |

| Separation Agreement |

The Separation and Distribution Agreement, dated as of December 15, 2019, by and among DuPont, IFF and N&B (as it may be amended from time to time) | |

| Separation Date |

The effective date of the Separation | |

| Separation Plan |

DuPont’s plan with respect to the Internal Reorganization, as further described in the Separation Agreement | |

| Share Issuance |

The issuance of shares of IFF common stock to the stockholders of N&B in the Merger | |

| Special Cash Payment |

A special cash payment from N&B to DuPont in an amount equal to $7.306 billion, subject to certain adjustments as described in “The Separation Agreement—The Separation—Special Cash Payment and Post-Closing Adjustments” | |

| Spin-Off |

If the Exchange Offer is terminated by DuPont without the exchange of shares (but the conditions to consummation of the Transactions have otherwise been satisfied), the distribution of all shares of N&B common stock on a pro rata basis to holders of DuPont common stock, with a record date to be announced by DuPont | |

| Tax Matters Agreement |

The Tax Matters Agreement substantially in the form attached as Exhibit 10.3 hereto and to be entered into immediately prior to the Distribution | |

| Termination Fee |

The termination fee of $521.5 million payable by IFF to DuPont upon termination of the Merger Agreement under circumstances as described in the section of this document entitled “The Merger Agreement— | |

7

Table of Contents

| Abbreviation/Term |

Description | |

| Termination Fees and Expenses Payable in Certain Circumstances” | ||

| Transaction Documents |

The Merger Agreement, the Separation Agreement and the Ancillary Agreements | |

| Transactions |

The transactions contemplated by the Transaction Documents, which provide for, among other things, the Separation, the Distribution and the Merger, as described in “The Transactions” | |

| Transition Services Agreements |

The Transition Services Agreement (DuPont (or certain of its affiliates) to N&B (or certain of its affiliates)) and the Transition Services Agreement (N&B (or certain of its affiliates) to DuPont (or certain of its affiliates)), each as contemplated by the Merger Agreement | |

| Valuation Dates |

The last three full trading days ending on and including the second trading day preceding the expiration date of the Exchange Offer period, as it may be voluntarily extended | |

| Voting Agreement |

The Voting Agreement, dated as of December 15, 2019, by and between DuPont and Winder Investment Pte. Ltd. | |

| VWAP |

Volume-weighted average price | |

8

Table of Contents

QUESTIONS AND ANSWERS ABOUT THE EXCHANGE OFFER AND THE TRANSACTIONS

The following are some of the questions that DuPont stockholders may have, and answers to those questions. These questions and answers, as well as the following summary, are not meant to be a substitute for the information contained in the remainder of this prospectus, and this information is qualified in its entirety by the more detailed descriptions and explanations contained elsewhere in this prospectus. You are urged to read this prospectus in its entirety prior to making any decision.

Questions and Answers about the Exchange Offer

| Q: | Who may participate in the Exchange Offer? |

| A: | Any U.S. holders of DuPont common stock in the United States during the Exchange Offer period may participate in the Exchange Offer. Although DuPont has mailed this document to its stockholders to the extent required by U.S. law, including stockholders located outside the United States, this document is not an offer to buy, sell or exchange and it is not a solicitation of an offer to buy, sell or exchange any shares of DuPont common stock, shares of IFF common stock or shares of N&B common stock in any jurisdiction in which such offer, sale or exchange is not permitted. |

Countries outside the United States generally have their own legal requirements that govern securities offerings made to persons resident in those countries and often impose stringent requirements about the form and content of offers made to the general public. None of DuPont, N&B or IFF has taken any action under non-U.S. laws or regulations to facilitate a public offer to exchange shares of DuPont common stock, shares of N&B common stock or shares of IFF common stock outside the United States. Accordingly, the ability of any non-U.S. person and any U.S. person residing outside of the United States to tender shares of DuPont common stock in the Exchange Offer will depend on whether there is an exemption available under the laws of such person’s home country that would permit such person to participate in the Exchange Offer without the need for DuPont, N&B or IFF to take any action to facilitate a public offering in that country or otherwise. For example, some countries exempt transactions from the rules governing public offerings if they involve persons who meet certain eligibility requirements relating to their status as sophisticated or professional investors.

Non-U.S. stockholders and U.S. stockholders residing outside of the United States should consult their advisors in considering whether they may participate in the Exchange Offer in accordance with the laws of their home countries or countries of residence, as applicable, and, if they do participate, whether there are any restrictions or limitations on transactions in the shares of DuPont common stock, N&B common stock or IFF common stock that may apply in such countries. None of DuPont, IFF or N&B can provide any assurance about whether such limitations may exist. See “The Exchange Offer—Certain Matters Relating to Non-U.S. Jurisdictions” for additional information about limitations on the Exchange Offer outside the United States.

| Q: | How many shares of N&B common stock will I receive for each share of DuPont common stock that I tender? |

| A: | The Exchange Offer is designed to permit you to exchange your shares of DuPont common stock for shares of N&B common stock at a price per share equal to a % discount to the per-share value of IFF common stock, calculated as set forth in this prospectus. Stated another way, for each $100 of your DuPont common stock accepted in the Exchange Offer, you will receive approximately $ of N&B common stock. The value of the DuPont common stock will be based on the calculated per-share value for the DuPont common stock on the NYSE and the value of the N&B common stock will be based on the calculated per-share value for IFF common stock on the NYSE, in each case determined by reference to the simple arithmetic average of the daily VWAP of DuPont common stock and IFF common stock on the NYSE on each of the Valuation Dates. The last day on which tenders will be accepted, whether on , 2021 or any later date to |

9

Table of Contents

| which the Exchange Offer is extended, is referred to in this document as the “expiration date.” Please note, however, that: |

| • | The number of shares you can receive is subject to an upper limit of shares of N&B common stock for each share of DuPont common stock accepted in the Exchange Offer. The next question and answer below describes how this limit may impact the value you receive. |

| • | The Exchange Offer does not provide for a minimum exchange ratio. See “The Exchange Offer—Terms of the Exchange Offer.” |

| • | If the number of shares of DuPont common stock that have been tendered results in fewer than all shares of N&B common stock being exchanged in the Exchange Offer, then such remaining shares of N&B common stock will be distributed pro rata to DuPont stockholders in the Clean-Up Spin-Off. DuPont currently expects that a portion of the shares of N&B common stock will be distributed to DuPont stockholders in the Clean-Up Spin-Off. |

| • | Because the Exchange Offer is subject to proration in the event of oversubscription, DuPont may accept for exchange only a portion of the DuPont common stock tendered by you. Any proration of the number of shares accepted in the Exchange Offer will be determined on the basis of the proration mechanics described under “The Exchange Offer—Terms of the Exchange Offer—Proration; Tenders for Exchange by Holders of Fewer than 100 Shares of DuPont Common Stock.” While proration is possible, DuPont does not expect proration to occur because DuPont currently expects that the number of shares of DuPont common stock tendered in the Exchange Offer will result in fewer than all of the shares of N&B common stock being subscribed for, and that shares of N&B common stock will remain to be distributed following the completion of the Exchange Offer. |

For more information on the terms of the Exchanger Offer see “The Exchange Offer—Terms of the Exchange Offer.”

| Q: | Is there a limit on the number of shares of N&B common stock I can receive for each share of DuPont common stock that I tender? |

| A: | The number of shares you can receive is subject to an upper limit of shares of N&B common stock for each share of DuPont common stock accepted in the Exchange Offer. If the upper limit is in effect, you will receive less than $ of N&B common stock for each $100 of DuPont common stock that you tender, and you could receive much less. For example, if the calculated per-share value of DuPont common stock was $ ( % above the highest closing price for DuPont common stock on the NYSE during the three-month period prior to commencement of the Exchange Offer) and the calculated per-share value of N&B common stock was $ (the lowest closing price for IFF common stock on the NYSE during that three-month period), the value of N&B common stock, based on the IFF common stock price, received for shares of DuPont common stock accepted for exchange would be approximately $ for each $100 of DuPont common stock accepted for exchange. |

The upper limit would represent a % discount for N&B common stock based on the average of the daily VWAPs of DuPont common stock and IFF common stock on the NYSE on , 2020, , 2020 and , 2020 (the last three full trading days ending on the second to last full trading day prior to commencement of the Exchange Offer). DuPont set this upper limit to ensure that an unusual or unexpected drop in the trading price of IFF common stock, relative to the trading price of DuPont common stock, would not result in an unduly high number of shares of N&B common stock being exchanged for shares of DuPont common stock accepted in the Exchange Offer.

In addition, depending on the number of the shares of DuPont common stock validly tendered in the Exchange Offer and the final exchange ratio, the Exchange Offer could become oversubscribed. In the event of such an oversubscription, DuPont would have to limit the number of shares of DuPont common stock that it accepts in the Exchange Offer through a proration process. Any proration of the number of shares

10

Table of Contents

accepted in the Exchange Offer will be determined on the basis of the proration mechanics described under “The Exchange Offer—Terms of the Exchange Offer—Proration; Tenders for Exchange by Holders of Fewer than 100 Shares of DuPont Common Stock.” While proration is possible, DuPont does not expect proration to occur because DuPont currently expects that the number of shares of DuPont common stock tendered in the Exchange Offer will result in fewer than all of the shares of N&B common stock being subscribed for, and that shares of N&B common stock will remain to be distributed following the completion of the Exchange Offer.

| Q: | Are there possible adverse effects on the value of IFF common stock ultimately to be received by DuPont stockholders who participate in the Exchange Offer? |

| A: | The factors associated with the Transactions are described in more detail in the section of this document entitled “Risk Factors.” You should carefully consider the risk factors set forth in that section. |

| Q: | How and when will I know the final exchange ratio and whether the upper limit is in effect? |

| A: | DuPont will announce the final exchange ratio used to determine the number of shares that can be received for each share of DuPont common stock accepted in the Exchange Offer by press release, and it will be available on the website , in each case by 11:59 p.m., New York City time, at the end of the second trading day (currently expected to be , 2021) immediately preceding the expiration date of the Exchange Offer (currently expected to be , 2021), unless the Exchange Offer is extended or terminated. At such time, the final exchange ratio will also be available from the information agent at the toll-free number provided on the back cover of this document. DuPont will also announce at that time whether the upper limit on the number of shares that can be received for each share of DuPont common stock tendered will be in effect. Therefore, the timing of such announcement will provide each holder of DuPont common stock with two full business days after knowing the final exchange ratio and whether the upper limit is in effect during which to decide whether to tender or withdraw their shares in the Exchange Offer. |

| Q: | How are the calculated per-share values of DuPont common stock and IFF common stock determined for purposes of calculating the number of shares of N&B common stock to be received in the Exchange Offer? |

| A: | The calculated per-share value of DuPont common stock and IFF common stock for purposes of the Exchange Offer will equal the simple arithmetic average of the daily VWAP of DuPont common stock and IFF common stock, as the case may be, on the NYSE on each of the Valuation Dates. The daily VWAP will be as reported by Bloomberg L.P. as displayed under the heading Bloomberg VWAP on the Bloomberg pages “ ” with respect to DuPont common stock and “ ” with respect to N&B common stock (or any other recognized quotation source selected by DuPont in its sole discretion if such pages are not available or are manifestly erroneous). The daily VWAPs of DuPont common stock and IFF common stock obtained from Bloomberg L.P. may be different from other sources of volume-weighted average prices or investors’ or other security holders’ own calculations. DuPont will determine the simple arithmetic average of the VWAPs of each stock based on prices provided by Bloomberg L.P., and such determination will be final. For more information on the terms of the Exchange Offer, see “The Exchange Offer—Terms of the Exchange Offer.” |

| Q: | What is the “daily volume-weighted average price” or “daily VWAP?” |

| A: | The “daily volume-weighted average price” for DuPont common stock and IFF common stock will be the volume-weighted average price of DuPont common stock and IFF common stock on the NYSE during the period beginning at 9:30 a.m., New York City time (or such other time as is the official open of trading on the NYSE), and ending at 4:00 p.m., New York City time (or such other time as is the official close of |

11

Table of Contents

| trading on the NYSE) except that such data will only take into account adjustments made to reported trades included by 4:10 p.m., New York City time, as reported to DuPont by Bloomberg L.P. for the equity ticker pages of DuPont, in the case of DuPont common stock, and IFF, in the case of IFF common stock. The daily VWAPs obtained from Bloomberg L.P. may be different from other sources of volume-weighted average prices or investors’ or other security holders’ own calculations. DuPont will determine the simple arithmetic average of the VWAPs of each stock based on prices provided by Bloomberg L.P., and such determination will be final. |

| Q: | Where can I find the daily VWAP of DuPont common stock and IFF common stock during the Exchange Offer period? |

| A: | DuPont will maintain a website at that provides the daily VWAP of both DuPont common stock and IFF common stock, together with indicative exchange ratios, which will be made available commencing at the end of the third trading day of the Exchange Offer and until the first Valuation Date. On the first two Valuation Dates, when the values of DuPont common stock and IFF common stock are calculated for the purposes of the Exchange Offer, the website will show the indicative exchange ratios based on indicative calculated per-share values calculated by DuPont, which will equal: (i) on the first Valuation Date, the daily VWAP of DuPont common stock and the IFF common stock for that day; and (ii) on the second Valuation Date, the simple arithmetic average of the daily VWAPs of DuPont common stock and IFF common stock for the first and second Valuation Dates. The website will not provide an indicative exchange ratio on the third Valuation Date. The final exchange ratio (as well as whether the upper limit on the number of shares that can be received for each share of DuPont common stock tendered will be in effect) will be announced by press release and be available on the website, in each case by 11:59 p.m., New York City time, at the end of the second trading day (currently expected to be , 2021) immediately preceding the expiration date of the Exchange Offer (currently expected to be , 2021). DuPont will determine the simple arithmetic average of the VWAPs based on data provided by Bloomberg L.P., and such determinations will be final. |

| Q: | Why is the calculated per-share value for N&B common stock based on the trading prices for IFF common stock? |

| A: | There is currently no trading market for N&B common stock. DuPont believes, however, that the trading prices for IFF common stock are an appropriate proxy for the trading prices of N&B common stock because (i) in the Merger, each outstanding share of N&B common stock (except for shares of N&B common stock held by N&B as treasury stock or by DuPont, which will be canceled and cease to exist and no consideration will be delivered in exchange therefor) will be automatically converted into the right to receive a number of shares of IFF common stock such that immediately after the Merger such DuPont stockholders will collectively own approximately 55.4% of IFF common stock on a fully diluted basis, and IFF shareholders will collectively own approximately 44.6% of IFF common stock on a fully diluted basis, in each case excluding any overlaps in the pre-transaction stockholder bases (calculated as further described in “The Merger Agreement – Merger Consideration”), (ii) prior to the consummation of the Exchange Offer, N&B will issue to DuPont a number of shares of N&B common stock such that the number of shares of N&B common stock issued and outstanding at the time of the Distribution is equal to the number of shares to be issued in the Share Issuance and the exchange ratio in the Merger is equal to approximately one and, as a result, each share of N&B common stock (except for shares of N&B common stock held by N&B as treasury stock or by DuPont, which will be canceled and cease to exist and no consideration will be delivered in exchange therefor) will be converted into approximately one share of IFF common stock in the Merger, and (iii) at the Valuation Dates, it is expected that all the major conditions to the consummation of the Merger will have been satisfied or, if permitted by the Merger Agreement, waived (except for those conditions that by their nature are satisfied at the closing of the Merger), and the Merger will be expected to be consummated shortly, such that investors should be expected to be valuing IFF common stock based on the expected value of such IFF common stock immediately after the Merger. There can be no assurance, |

12

Table of Contents

| however, that IFF common stock after the Merger will trade on the same basis as IFF common stock trades prior to the Merger. See “Risk Factors—Risks Related to the Exchange Offer—The trading prices of IFF common stock may not be an appropriate proxy for the prices of N&B common stock.” |

| Q: | How and when will I know the final exchange ratio? |

| A: | DuPont will announce the final exchange ratio used to determine the number of shares that can be received for each share of DuPont common stock accepted in the Exchange Offer by press release, and it will be available on the website , in each case by 11:59 p.m., New York City time, at the end of the second trading day (currently expected to be , 2021) immediately preceding the expiration date of the Exchange Offer (currently expected to be , 2021), unless the Exchange Offer is extended or terminated. At such time, the final exchange ratio will also be available from the information agent at the toll-free number provided on the back cover of this document. DuPont will also announce at that time whether the upper limit on the number of shares that can be received for each share of DuPont common stock tendered will be in effect. Therefore, the timing of such announcement will provide each holder of DuPont common stock with two full business days after knowing the final exchange ratio and whether the upper limit is in effect during which to decide whether to tender or withdraw their shares in the Exchange Offer. |

| Q: | Will indicative exchange ratios be provided during the Exchange Offer period? |

| A: | Yes. Prior to the Valuation Dates and commencing at the end of the third trading day of the Exchange Offer, indicative exchange ratios will be available by contacting the information agent at the toll-free number provided on the back cover of this prospectus and at , calculated as though that day were the last of the three Valuation Dates for the Exchange Offer. The indicative exchange ratio will also reflect whether the upper limit on the exchange ratio, described above, would have been in effect. In other words, assuming that a given day is a trading day, the indicative exchange ratio will be calculated based on the simple arithmetic average of the daily VWAPs of DuPont common stock and IFF common stock for that day and the two immediately preceding trading days. On the first two Valuation Dates, when the values of DuPont common stock and IFF common stock are calculated for the purposes of the Exchange Offer, the website will show the indicative exchange ratios based on indicative calculated per-share values calculated by DuPont, which will equal: (i) on the first Valuation Date, the daily VWAP of DuPont common stock and the IFF common stock for that day; and (ii) on the second Valuation Date, the simple arithmetic mean of the daily VWAPs of DuPont common stock and IFF common stock for the first and second Valuation Dates. The website will not provide an indicative exchange ratio on the third Valuation Date. The final exchange ratio (as well as whether the upper limit on the number of shares that can be received for each share of DuPont common stock tendered will be in effect) will be announced by press release and be available on the website, in each case by 11:59 p.m., New York City time, at the end of the second trading day (currently expected to be , 2021) immediately preceding the expiration date of the Exchange Offer (currently expected to be , 2021). |

In addition, for purposes of illustration, a table that indicates the number of shares of N&B common stock that you would receive per share of DuPont common stock, calculated on the basis described above and taking into account the upper limit, assuming a range of averages of the daily VWAP of DuPont common stock and IFF common stock on the Valuation Dates, is provided under “The Exchange Offer—Terms of the Exchange Offer.”

| Q: | What if DuPont common stock or IFF common stock does not trade on any of the Valuation Dates? |

| A: | If a market disruption event, as defined below, occurs with respect to DuPont common stock or IFF common stock on any of the Valuation Dates, the calculated per-share value of DuPont common stock and per-share value of N&B common stock will be determined using the daily VWAP of shares of DuPont |

13

Table of Contents

| common stock and shares of IFF common stock on the preceding full trading day or days, as the case may be, on which no market disruption event occurred with respect to either DuPont common stock and IFF common stock. If, however, a market disruption event occurs as specified above, DuPont may terminate or extend the Exchange Offer if, in its reasonable judgment, the market disruption event has impaired the benefits of the Exchange Offer to DuPont. If DuPont decides to extend the Exchange Offer period following a market disruption event, the Valuation Dates will be reset, as with any extension of the Exchange Offer, to the period of three consecutive trading days ending on and including the second trading day preceding the expiration date, as may be extended. Therefore, the timing of such announcement will provide each holder of DuPont common stock with two full business days after knowing the final exchange ratio and whether the upper limit is in effect during which to decide whether to tender or withdraw their shares in the Exchange Offer. For specific information as to what would constitute a market disruption event, see “The Exchange Offer—Conditions to Consummation of the Exchange Offer.” |

| Q: | Are there circumstances under which I would receive fewer shares of N&B common stock than I would have received if the exchange ratio were determined using the closing prices of DuPont common stock and IFF common stock on the expiration date of the Exchange Offer? |

| A: | Yes. The exchange ratio is calculated based on an average of the daily VWAP of shares of DuPont common stock and shares of IFF common stock on the Valuation Dates and not using the closing prices of DuPont common stock and IFF common stock on the expiration date of the Exchange Offer, such that you could receive fewer shares of N&B common stock than you would have received if the exchange ratio were determined using the closing prices of DuPont common stock and IFF common stock on the expiration date of the Exchange Offer. For example, if the trading price of DuPont common stock were to increase during the last two full trading days of the Exchange Offer, the average DuPont stock price used to calculate the exchange ratio would likely be lower than the closing price of shares of DuPont common stock on the expiration date of the Exchange Offer. As a result, you would receive fewer shares of N&B common stock, and therefore effectively fewer shares of IFF common stock, for each $100 of shares of DuPont common stock than you would have if the average DuPont stock price were calculated on the basis of the closing price of shares of DuPont common stock on the expiration date of the Exchange Offer or on the basis of an averaging period that includes the last two full trading days prior to the expiration of the Exchange Offer period. Similarly, if the trading price of IFF common stock were to decrease during the last two full trading days prior to the expiration of the Exchange Offer period, the average IFF stock price used to calculate the exchange ratio would likely be higher than the closing price of IFF common stock on the last full trading day prior to the expiration date. This could also result in your receiving fewer shares of N&B common stock, and therefore effectively fewer shares of IFF common stock, for each $100 of DuPont common stock than you would otherwise receive if the average IFF common stock price were calculated on the basis of the closing price of IFF common stock on the last full trading day prior to the expiration date or on the basis of an averaging period that included the last two full trading days prior to the expiration of the Exchange Offer period. See “The Exchange Offer—Terms of the Exchange Offer.” |

| Q: | Will fractional shares of IFF common stock be distributed? |

| A: | No fractional shares will be issued in the Merger, as described in this document. The Exchange Offer Agent will hold shares of N&B common stock in trust for the holders of DuPont common stock who validly tendered their shares in the Exchange Offer or are entitled to receive shares in the Clean-Up Spin-Off. Immediately following the consummation of the Exchange Offer and the expected Clean-Up Spin-Off, and by means of the Merger, each outstanding share of N&B common stock will be converted into the right to receive an equal number of shares of IFF common stock (because, prior to the consummation of the Exchange Offer, N&B will issue to DuPont a number of shares of N&B common stock such that the number of shares of N&B common stock issued and outstanding at the time of the Distribution is equal to the number of shares to be issued in the Share Issuance and the exchange ratio in the Merger is equal to approximately one). In the Merger, no fractional shares of IFF common stock will be delivered to holders of |

14

Table of Contents

| N&B common stock. All fractional shares of IFF common stock that a holder of shares of N&B common stock would otherwise be entitled to receive as a result of the Merger will be aggregated by the Exchange Agent. The Exchange Agent will cause the whole shares obtained thereby to be sold on behalf of such holders of shares of N&B common stock that would otherwise be entitled to receive such fractional shares of IFF common stock pursuant to the Merger, in the open market. The Exchange Agent will make available the net proceeds thereof, after deducting any required withholding taxes and brokerage charges, commissions and conveyance and similar taxes, on a pro rata basis, without interest, as soon as practicable to the holders of N&B common stock that would otherwise be entitled to receive such fractional shares of IFF common stock in the Merger. See “The Exchange Offer—Terms of the Exchange Offer.” |

| Q: | What is the aggregate number of shares of N&B common stock being offered in the Exchange Offer? |

| A: | In the Exchange Offer, DuPont is offering to exchange all of the shares of N&B common stock held by it. In addition, N&B will issue to DuPont a number of shares of N&B common stock such that the number of shares of N&B common stock issued and outstanding at the time of the Distribution is equal to the number of shares to be issued in the Share Issuance and the exchange ratio in the Merger is equal to approximately one. DuPont currently expects that approximately million shares of N&B common stock will be available in the Exchange Offer. See “The Exchange Offer—Terms of the Exchange Offer.” |

| Q: | What happens if not enough shares of DuPont common stock are tendered to allow DuPont to exchange all of the shares of N&B common stock DuPont holds? |

| A: | If the Exchange Offer is consummated but less than all of the shares of N&B common stock being offered in the Exchange Offer are exchanged because the Exchange Offer is not fully subscribed, the additional shares of N&B common stock owned by DuPont will be distributed on a pro rata basis to the holders of shares of DuPont common stock whose shares of DuPont common stock remain outstanding after the consummation of the Exchange Offer in the Clean-Up Spin-Off. Any DuPont stockholder who validly tenders (and does not properly withdraw) shares of DuPont common stock for shares of N&B common stock and whose shares are accepted in the Exchange Offer will waive their rights with respect to such shares to receive, and forfeit any rights to, shares of N&B common stock distributed on a pro rata basis to DuPont stockholders in the Clean-Up Spin-Off. See “The Exchange Offer—Distribution of N&B Common Stock Remaining After the Exchange Offer.” |

| Q: | What happens if DuPont declares a quarterly dividend during the Exchange Offer? |

| A: | If DuPont declares a quarterly dividend and the record date for that dividend occurs during the Exchange Offer period, you will be eligible to receive that dividend if you continue to own your shares of DuPont common stock as of that record date. |

| Q: | Will tendering my shares affect my ability to receive the DuPont quarterly dividend? |

| A: | No. If a dividend is declared by DuPont with a record date before the completion of the Exchange Offer, you will be entitled to that dividend even if you tendered your shares of DuPont common stock. Tendering your shares of DuPont common stock in the Exchange Offer is not a sale or transfer of those shares until they are accepted for exchange upon completion of the Exchange Offer. |

| Q: | Will all shares of DuPont common stock that I tender be accepted in the Exchange Offer? |

| A: | Not necessarily. Depending on the number of shares of DuPont common stock validly tendered in the Exchange Offer and not properly withdrawn, the calculated per-share value of DuPont common stock and the per-share value of N&B common stock determined as described above, DuPont may have to limit the number of shares of DuPont common stock that it accepts in the Exchange Offer through a proration |

15

Table of Contents

| process. Any proration of the number of shares accepted in the Exchange Offer will be determined on the basis of the proration mechanics described under “The Exchange Offer—Terms of the Exchange Offer—Proration; Tenders for Exchange by Holders of Fewer than 100 Shares of DuPont Common Stock.” |