Table of Contents

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

| þ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2011

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission File Number 1-4858

INTERNATIONAL FLAVORS & FRAGRANCES INC.

(Exact name of registrant as specified in its charter)

| NEW YORK | 13-1432060 | |

| (State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification No.) | |

| 521 WEST 57TH STREET, NEW YORK, N.Y. | 10019 | |

| (Address of principal executive offices) | (Zip Code) | |

Registrant’s telephone number, including area code (212) 765-5500

SECURITIES REGISTERED PURSUANT TO SECTION 12(b) OF THE ACT:

| Title of Each Class |

Name of Each Exchange on Which Registered | |

| Common Stock, par value | New York Stock Exchange | |

| 12 1/2¢ per share |

SECURITIES REGISTERED PURSUANT TO SECTION 12(g) OF THE ACT:

None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes þ No ¨

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No þ

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes þ No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes þ No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendments to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer þ | Accelerated filer ¨ | Non-accelerated filer ¨ | Smaller reporting company ¨ |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No þ

For the purpose of reporting the following market value of registrant’s outstanding common stock, the term “affiliate” refers to persons, entities or groups which directly or indirectly control, are controlled by, or are under common control with the registrant and does not include individual executive officers, directors or less than 10% shareholders. The aggregate market value of registrant’s common stock not held by affiliates as of June 30, 2011 was $5,192,991,749.

As of February 13, 2012, there were 80,927,390 shares of the registrant’s common stock, par value 12 1/2¢ per share, outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant’s proxy statement for the 2012 Annual Meeting of Shareholders (the “IFF 2012 Proxy Statement”) are incorporated by reference in Part III of this Form 10-K.

Table of Contents

INTERNATIONAL FLAVORS & FRAGRANCES INC.

2

Table of Contents

PART I

| ITEM 1. | BUSINESS. |

When used in this report, the terms “IFF”, “the Company”, “we”, “us” and “our”, mean International Flavors & Fragrances Inc., and its subsidiaries. We create, manufacture and supply flavors and fragrances for the food, beverage, personal care and household products industries. Our flavors and fragrances are individual ingredients or compounds of a large number of ingredients that are blended, mixed or reacted together to produce proprietary formulas created by our perfumers and flavorists. Utilizing our capabilities in consumer insight, in research and product development (“R&D”), and in creative expertise, we collaborate with our customers to drive consumer preference for our customers’ brands. This collaboration in turn helps bolster our customers’ market share and grow equity in their brand portfolio.

The global market for flavors and fragrances has expanded consistently, primarily as a result of an increase in demand for, as well as an increase in the variety of, consumer products containing flavors and fragrances. The flavors and fragrances market is part of a larger market which supplies a variety of ingredients and components that consumer products companies utilize in their products. The broader market includes large multinational companies or smaller regional and local participants which supply products such as seasonings, texturizers, spices, enzymes, certain food related commodities, fortified products and cosmetic ingredients.

In 2011, we achieved sales of approximately $2.8 billion, making us one of the top four companies in the global flavors and fragrances sub-segment of the broader market. Within this sub-segment of the broader market, the top four companies comprise approximately 70% of the total estimated sales. We believe that our broad geographic coverage and our diversified portfolio position us to achieve significant growth as the flavors and fragrances markets expand.

With operations in 32 different countries worldwide and more than 5,600 employees, we collaborate with our customers to serve consumers in more than 100 countries. We operate in two business segments, Flavors and Fragrances, in four regions. Our largest region is Europe, Africa and the Middle East, which accounted for 34% of our sales in 2011. Greater Asia is our second largest region, accounting for 27% of our sales in 2011, while North America represented 24% of our sales and Latin America represented 15% of our sales during 2011. Importantly, the fast growing emerging markets, including countries in Asia, Latin America, Africa, the Middle East and Eastern Europe, contributed approximately 46% of 2011 sales. As our customers in emerging markets grow their business, they will have the ability to leverage our long-standing presence and our extensive market knowledge to help drive their brands.

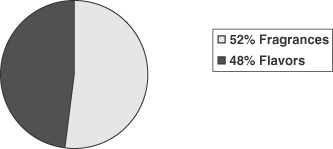

In addition to our geographic diversity, we believe we have a diversified product portfolio which helps to provide us stability in challenging economic environments. In 2011, our Flavors business represented 48% of our sales while our Fragrances business represented 52% of sales.

For financial information about our operating segments and the geographic areas in which we do business, please see Note 12 of our Consolidated Financial Statements included in this Form 10-K.

Core Competencies

We focus on five core competencies that we believe enable us to (i) successfully provide our customers with superior products, (ii) drive productivity and efficiency gains, and (iii) improve our margins and our cash flow. In that regard, we strive to:

| Ÿ | Develop a deep understanding of consumers’ preferences and values. Through our Consumer Insights program, we have dedicated professionals working to understand consumer trends all around the globe. Our consumer and our marketing teams interpret consumer trends, monitor product launches, analyze quantitative market data and conduct a few hundred thousand consumer interviews annually. Our sensory experts explore flavor and fragrance performance, the psychophysics of sensory perception (including |

3

Table of Contents

| chemesthetic properties such as warming, cooling and tingling), the genetic basis for flavor and fragrance preference, and the effects of tastes and aromas on mood, performance, health and well-being. Utilizing our proprietary statistical programs, we use this information to enable us to understand the emotional connections between a prospective product and the consumer. The ability to pinpoint the likelihood of a product’s success translates into stronger brand equity, helping to produce increased returns and greater market share gains for our customers and us. |

| Ÿ | Utilize technology to create innovative solutions that drive brand success. We spend approximately 8% of our sales on the development and implementation of new molecules, compounds and technologies that help our customers respond to changing consumer preference. As a result of this investment, we have been granted over 200 patents in the United States since 2000 and we have developed many unique molecules and delivery systems for our customers that are used as the foundations of successful flavors and fragrances around the world. |

| Ÿ | Cultivate our creative expertise in collaboration with our customers. We have a network of creative centers around the world where we create or adapt the basic flavors or fragrances that we have developed in the R&D process to commercialize for use in our customers’ consumer products. Our global creative teams consist of perfumers, fragrance evaluators and flavorists, as well as marketing, consumer insight, and technical application experts, from a wide range of cultures and nationalities. In close partnership with our customers’ product development groups, our creative teams create the scents or tastes that our customers are seeking in order to satisfy consumer demands in each of their markets. |

| Ÿ | Understand our customer specific knowledge. We believe that understanding our customers’ brands and their goals by supplying them with superior products accurately and on time, and our ability to be named a “core list supplier,” are key drivers of our future growth. |

| Ÿ | Drive efficiency in all that we do. We focus on integrating our consumer insight, technology and creative expertise in a manner that we believe drives the necessary productivity and efficiency to improve profitability on a long-term basis. We believe that discipline in driving efficiencies is a significant factor in our ability simultaneously to enhance margins and cash flows while continuing to invest in our key growth initiatives. |

Our Product Offerings

Flavors

Flavors are the key building blocks that impart taste in processed food and beverage products and, as such, play a significant role in determining consumer preference of the end products in which they are used. While we are a global leader, our Flavors business is regional in nature, with different formulas that reflect local taste and ingredients preferences. As a leading creator of flavors, we help our customers deliver on the promise of delicious and healthy foods and drinks that appeal to consumers. Our Flavors business includes four categories of products: (1) Savory, (2) Beverages, (3) Sweet, pharmaceutical and oral care (“Sweet”), and (4) Dairy. We create our flavors in our regional creative and technical centers that allow us to satisfy local taste preferences, while helping to ensure regulatory compliance and production standards. We also manufacture a limited amount of flavor ingredients for our use in developing flavor compounds.

| Ÿ | Savory — We produce flavors which are used in soups, sauces, condiments, prepared meals, meat and poultry, and potato chips and other savory snacks. |

| Ÿ | Beverages — We create flavors for juice drinks, carbonated beverages, flavored waters and spirits and have creative expertise dedicated to beverage flavor systems. |

| Ÿ | Sweet — We create innovative flavor concepts and heat-stable flavors for bakery products, as well as candy, chewing gum and cereal which each have distinctive sweet tastes. For pharmaceutical and oral care products, we produce flavors for products such as toothpaste and mouthwash and have the expertise to create flavors that work well while masking the active ingredients that make these products effective. |

4

Table of Contents

| Ÿ | Dairy — We offer a complete range of value-added compounded flavors for all dairy applications, including yogurt, ice cream, cheese, cream and butter flavor. We also offer a wide range of quality vanilla extracts and a variety of flavor solutions that build on our understanding of vanilla. |

We develop thousands of different flavors for our customers, most of which are tailor-made, and we continuously develop new formulas in order to meet changing consumer preferences and customer needs. Consumers, especially those in developed markets such as the United States and Europe, are increasingly seeking to focus on products which promote health and wellness. They want food and beverage products that are good for them, but which taste good. Our objective is to capture a significant share of this shift in consumer demand by capitalizing on the ability of our naturals and proprietary ingredients and taste modulation technology to provide consumers with healthier solutions without changing the taste experience of the food or beverage. For example, our sweetness modulation technology, combined with our blend of natural sweeteners, allows products to have a reduced sugar content without affecting taste. Our sodium modulation technology seeks to reduce the content of salt in consumer products while at the same time maximizing taste by enhancing the flavors of other ingredients.

We are also developing sophisticated flavor profiles in our CulinEssence™ program to bring authentic culinary flavors to our customers. The success of our recent launches of new culinary chicken and beef flavors was a direct result of this program.

Fragrances

We are a global leader in the creation of fragrances. Our fragrances are a key component in the world’s finest perfumes and best-known consumer brands, including beauty care, fabric care, personal wash and home care products. Our Fragrances business consists of three categories of products: (1) Fine Fragrance and Beauty Care, (2) Functional Fragrances and (3) Fragrance Ingredients.

| Ÿ | Fine Fragrance and Beauty Care — We have created some of the industry-leading fragrance classics as well as cutting-edge niche fragrances, as evidenced by our number of top sellers and the success of our new launches. Within our Beauty Care product line, we provide our customers innovation in the hair care, deodorant and skincare categories to create new fragrance experiences for the consumer and increased brand loyalty for our customers. |

| Ÿ | Functional Fragrances — We have three subcategories of products in which our fragrances are included: (1) Fabric Care, including laundry detergents, fabric softeners and specialty laundry products; (2) Personal Wash, including bar soap and shower gel; and (3) Home Care, including household cleaners, dishwashing detergents and air fresheners. |

| Ÿ | Fragrance Ingredients — We manufacture innovative, high-quality and cost-effective fragrance ingredients for internal use by our perfumers in our Fragrances business and for external use by our customers and other third parties, including our competitors. With over 1,300 separate fragrance ingredients, we believe that we lead the industry with the breadth of our product portfolio. We manufacture our ingredients through our global network of production facilities. We believe that this network gives us the flexibility to make products in different locations while maintaining the same high and consistent standards of product quality. |

Our perfumers have access to our large portfolio of innovative ingredients to support their creativity, which in turn provides our customers with a unique identity for their brands. We also create innovative delivery systems, including our (i) proprietary encapsulation technology, which consists of individual fragrance droplets which are coated with a protective polymetric shell to deliver superior fragrance performance throughout a product’s lifecycle, and (ii) our exclusive polymer delivery system, PolyIFF, which is a “solid fragrance” technology that allows us to add scent to functional or molded plastic.

We believe that our in-house naturals facilities, led by Laboratoire Monique Rémy (LMR) in Grasse, France, is the industry standard for quality natural materials, offering decades of experience understanding natural products and perfecting the process of transforming naturals, such as narcissus, jasmine and blackcurrant bud, into pure absolutes that retain the unique fragrance of their origin.

5

Table of Contents

We also collaborate with the leading art and fashion schools in the world to tap into the creative minds of the future leaders of fashion and design. We collaborate with writers, artists, film-makers and scientists to expose our perfumers to new and constantly evolving creative territories.

Research and Product Development

We consider our research and product development infrastructure to be one of our key competencies and we focus and invest substantial resources in the research and development of new and innovative compounds, formulas and technologies and the application of these to our customers’ products. Using the knowledge gained from our Consumer Insights program, we strategically focus our resources to formulate the two main components of a flavor or fragrance: (1) innovative materials (taste and scent building blocks) and (2) delivery systems (taste and scent releases). We maintain four research and development centers around the world, at which we employ scientists and application engineers to support (i) the discovery of new materials, (ii) the development of new technologies, such as our delivery systems, (iii) the creation of new compounds and (iv) the enhancement of existing ingredients and compounds.

In our 17 creative centers around the world, including our newest facilities in Shanghai, Sao Paulo, Mumbai and Moscow, teams of flavorists and perfumers work with our customers’ product development groups to create the exact scent or taste they are seeking. In 2011, we employed about 1,175 employees in research and product development activities. We spent $220 million, $219 million and $185 million, or approximately 8% of our sales, in 2011, 2010 and 2009, respectively, on R&D and product development activities.

Our ingredients research program discovers molecules found in natural substances and creates new molecules that are subsequently tested for their fragrance or flavor value. To broaden our offering of natural, innovative and unique products, we seek out collaborations with research institutions and other companies throughout the world. We have created a number of such collaborations that strengthen and broaden the pipeline of new and innovative products we intend to launch in the coming years.

The development of new and customized flavor and fragrance products is a complex process calling upon the combined knowledge of our scientists, flavorists and perfumers. Scientists from various disciplines work in project teams with the flavorists and perfumers to develop flavor and fragrance products with consumer preferred performance characteristics. The development of new flavor and fragrance compounds requires (i) in-depth knowledge of the flavor and fragrance characteristics of the various ingredients we use, (ii) an understanding of how the many ingredients in a consumer product interact and (iii) the creation of controlled release and delivery systems to enhance flavor and fragrance performance. To facilitate this process, in 2011, we formed a scientific advisory board comprising of five expert scientists to provide external perspectives on our research and development programs.

Development of new flavors and fragrances is driven by a variety of sources including requests from our customers, who are in need of a specific flavor or fragrance for use in a new or modified consumer product, or as a result of internal initiatives stemming from our Consumer Insights program. Our product development team works in partnership with our scientists and researchers to optimize the consumer appeal of the flavor or fragrance. It then becomes a collaborative process between our researchers, our product development team and our customers to perfect the flavor or fragrance so that it is ready to be included in the final consumer product.

In addition to creating new flavors and fragrances, our researchers and product development teams advise customers on ways to improve their existing products by adjusting or substituting current ingredients with more readily accessible or less expensive materials or modifying the current ingredients to produce an enhanced yield. Often this results in creating a better value proposition for the consumer.

Our flavor and fragrance formulas are treated as trade secrets and remain our proprietary asset. Our business is not materially dependent upon any individual patent, trademark or license.

6

Table of Contents

Supply Chain

We have an integrated supply chain from raw material sourcing through manufacturing, quality assurance, regulatory compliance and distribution, which permits us to provide our customers with consistent quality products on a timely and cost-effective basis.

Procurement. The ingredients that we use in our compounds are both natural and synthetic. We purchase approximately 9,000 different raw materials from about 2,200 domestic and international suppliers. Approximately half of the materials we purchase are naturals or crop related items and the other half are synthetics and chemicals. Natural ingredients are derived from flowers, fruits and other botanical products as well as from animal products. They contain varying numbers of organic chemicals, which are responsible for the fragrance or flavor of the natural product. The natural products are purchased in processed or semi-processed form. Some are used in compounds in the state in which they are purchased and others after further processing. Natural products, together with various chemicals, are also used as raw materials for the manufacture of synthetic ingredients by chemical processes. Our flavor products also include extracts and seasonings derived from various fruits, vegetables, nuts, herbs and spices as well as microbiologically-derived ingredients. We manufacture most of our synthetic ingredients for use in our fragrance compounds as well as for sale to others.

While we purchase a diverse portfolio of raw materials, about 80% of our spending is focused on approximately 1,000 materials, which allows us to leverage our buying power with suppliers. In order to ensure our supply of raw materials, achieve favorable pricing, and provide timely transparency regarding inflationary trends to our customers, we continue to be focused on (i) implementing a forward buy strategy, (ii) entering into supplier relationships to gain access to supplies that we do not have, (iii) implementing indexed pricing, (iv) reducing the complexity of our formulations, and (v) evaluating whether it is more profitable to buy or make an ingredient. We are also concentrating on local country sourcing with our own procurement professionals.

Manufacturing and Distribution. We have 29 manufacturing sites around the world that support more than 36,000 products. Our major manufacturing facilities are located in the United States, the Netherlands, Spain, Great Britain, Argentina, Brazil, Mexico, Australia, China, India, Indonesia, Japan and Singapore. Our supply chain initiatives in developing markets are focused on increasing capacity and investments in key technologies, while we focus on consolidation and cost optimization in mature markets. In addition to our own manufacturing facilities, we develop relationships with third parties that permit us to expand the technologies, capabilities and capacity that we can access to serve our customers.

Based on the regional nature of the Flavors business, and the concerns regarding the transportability of raw materials, we have established smaller manufacturing facilities in our local markets that are focused on local needs. Products within the Fragrances business are typically composed of compounds that are more stable and more transportable around the world. Consequently, we have fewer manufacturing facilities within our Fragrances business, which produce compounds and ingredients for global distribution.

During 2011, our 25 largest customers accounted for 53% of our sales. Sales to the largest customer accounted for 11%, 10% and 11% of our sales in 2011, 2010 and 2009, respectively. These sales were largely in our Fragrances business.

Governmental Regulation

We develop, produce and market our products in a number of jurisdictions throughout the world and are subject to federal, regional and local legislation and regulations in each of the various countries. Our flavor and many of our fragrance products are intended for the food, beverage and pharmaceutical industries, which are subject to strict quality and regulatory standards. As a result, we are required to meet these strict standards which, in recent years, have become increasingly stringent.

In addition, we are subject to various rules relating to health, work safety and environment at the local and international levels in the various countries in which we operate. Our manufacturing facilities throughout the

7

Table of Contents

world are subject to environmental standards relating to air emissions, sewage discharges, the use of hazardous materials, waste disposal practices and clean up of existing environmental contamination. In recent years, there has been a significant increase in the stringency of environmental regulation and enforcement of environmental standards, and the costs of compliance have risen significantly. We expect that the trend of increased regulation and disclosure will continue in the future.

Our products and operations are subject to regulation by governmental agencies in each of the markets in which we operate; these agencies include (1) the Food and Drug Administration and equivalent international agencies that regulate the flavors and other ingredients in consumer products, (2) the Environmental Protection Agency and equivalent international agencies that regulate our fragrance compounds, (3) the Occupational Safety and Health Administration and equivalent international agencies that regulate the working conditions in our manufacturing, research laboratories and creative centers, (4) local and international agencies that regulate trade and customs and (5) the Drug Enforcement Administration and other international agencies that regulate controlled chemicals that we use in our operations. For example, in the continuing implementation of the EU REACH (Registration, Evaluation, Authorization and Restriction of Chemical Substances) regulations, we will be registering a number of chemical substances in advance of the next registration deadline of May, 2013.

Strategic Priorities

We are focused on generating sustainable profitable growth in our business and positioning our portfolio for long-term growth. In 2010, we performed an in-depth strategic review of our company, evaluating the economic profitability of each of our product categories, our regions and our customers. As a result, we believe we can improve our long-term business performance and increase shareholder value by leveraging our geographic reach, strengthening our innovation platform and maximizing our portfolio. The key elements of these strategic priorities are the following:

| Ÿ | Leverage geographic reach: The expansion of our geographic reach to capture the attractive population growth and wealth creation in emerging markets is a key component in our growth plan. In emerging markets, strong GDP growth and a significant expansion of the middle-class consumer are expanding the demand for better-flavored and fragranced consumer products. As a result of this trend, we have made significant investments in emerging markets. Since 2008, we have opened four state-of-the-art creative centers in Shanghai, Sao Paulo, Moscow and Mumbai, and in 2011 we announced the construction of two manufacturing sites in China and Singapore. We expect that the emerging markets will represent a greater percentage of our sales than the developed markets by 2015, as we estimate that growth potential in these markets is approximately three to four times greater than growth in the developed markets. |

| Ÿ | Strengthen innovation platform: We continue to focus on creating innovative and distinctive products that drive consumer preference to our customers’ brands. We have been strengthening our innovation platforms by reinforcing them with technological developments and external collaborations. We anticipate that this renewed focus will be instrumental in driving customer growth, as our consumer-centric innovation will allow our customers to win in the marketplace and drive market share gains. To capture these opportunities in Flavors, we are focusing on key taste modulation technology to provide consumers with healthier solutions without a change in the taste quality. In Fragrances, we are focusing on ingredients, including our naturals portfolio and delivery systems. |

| Ÿ | Maximize portfolio: We have identified opportunities where we can accelerate our performance by further leveraging our advantaged portfolio and implementing solutions to fix less attractive areas. These solutions include appropriate pricing actions, greater efficiency in our supply chain, aligning resources behind our advantaged portfolio, and, in some cases, phasing out some low margin businesses. |

Competition

The market for flavors and fragrances is highly competitive. Based on annual sales, our main competitors consist of (1) the three other large global flavor and fragrance manufacturers, Givaudan, Firmenich and Symrise,

8

Table of Contents

(2) mid-sized companies, (3) numerous small and local manufacturers with more limited research and development capabilities who focus on narrow market segments and local customers and (4) consumer product companies who may develop their own flavors or fragrances. The flavors and fragrances market is part of a larger market which supplies a variety of ingredients and components that consumer products companies utilize in their products. The broader market includes large multinational companies or smaller regional and local participants which supply products such as seasonings, texturizers, spices, enzymes, certain food related commodities, fortified products and cosmetic ingredients. We, together with the other top three companies, represent approximately 70% of the total estimated sales in the global flavors and fragrances sub-segment of the broader market. Over the last five years, there has been a trend towards consolidation.

We believe that our ability to compete successfully in the flavors and fragrance market is based on (1) our understanding of consumers, (2) innovation, arising from the creative skills of our perfumers and flavorists and the technological advances resulting from our research and development activities, (3) our ability to develop products which are tailor made for our customers’ needs, (4) the quality, reliability and cost effectiveness of our products, (5) the quality of our customer service, (6) the support provided by our marketing and application groups and (7) an understanding of the regulatory requirements in the markets in which our customers operate.

Large multinational customers, and increasingly, mid-sized customers, may limit the number of their suppliers, placing some on “core lists,” giving them priority for development and production of their new or modified products. To compete more successfully in this environment, we must make continued investments in customer relationships and tailor product research and development in order to anticipate customers’ needs, provide effective service and secure and maintain inclusion on certain “core lists.”

Employee Relations

At December 31, 2011, we had approximately 5,600 employees worldwide, of whom approximately 1,400 are employed in the United States. We believe that relations with our employees are good.

Availability of Reports

We make available free of charge on or through the Investor Relations link on our website, www.iff.com, all materials that we file electronically with the Securities and Exchange Commission (“SEC”), including our annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and amendments to those reports, filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934, as amended, as soon as reasonably practicable after electronically filing such materials with, or furnishing them to, the SEC. During the period covered by this Form 10-K, we made all such materials available through our website as soon as reasonably practicable after filing such materials with the SEC.

You may also read and copy any materials filed by us with the SEC at the SEC’s Public Reference Room at 100 F Street, N.E., Washington, D.C. 20549, and you may obtain information on the operation of the Public Reference Room by calling the SEC in the U.S. at 1-800-SEC-0330. In addition, the SEC maintains an Internet website, www.sec.gov, that contains reports, proxy and information statements and other information that we file electronically with the SEC.

A copy of our Corporate Governance Guidelines, Code of Business Conduct and Ethics, and the charters of the Audit Committee, Compensation Committee, and Nominating and Governance Committee of the Board of Directors are posted on the Investor Relations section of our website, www.iff.com.

Our principal executive offices are located at 521 West 57th Street, New York, New York 10019 (212-765-5500).

9

Table of Contents

Executive Officers of Registrant

The current executive officers of the Company, as of February 28, 2012, are listed below.

| Douglas D. Tough |

62 | Chairman of the Board and Chief Executive Officer | ||||

| Kevin C. Berryman |

53 | Executive Vice President and Chief Financial Officer | ||||

| Nicolas Mirzayantz |

49 | Group President, Fragrances | ||||

| Hernan Vaisman |

53 | Group President, Flavors | ||||

| Ahmet Baydar |

59 | Senior Vice President, Research and Development | ||||

| Angelica T. Cantlon |

60 | Senior Vice President, Human Resources | ||||

| Anne Chwat |

52 | Senior Vice President, General Counsel and Corporate Secretary | ||||

| Francisco Fortanet |

43 | Senior Vice President, Operations | ||||

| Richard A. O’Leary |

51 | Vice President and Controller |

Douglas D. Tough has served as IFF’s Chairman and Chief Executive Officer since March 2010. Previously, he served as Chief Executive Officer and Managing Director of Ansell Limited, a global leader in healthcare barrier protection, from 2004 until March 2010. Mr. Tough joined the IFF Board in 2008 and served as its non-Executive Chairman from October 2009 until he became our CEO.

Kevin C. Berryman has served as our Executive Vice President and Chief Financial Officer since May 2009, and also served as a member of our Temporary Office of the Chief Executive Officer from October 1, 2009 until February 2010. Prior to joining us, Mr. Berryman served as Chief Financial Officer of Nestle Professional, Americas, a global foodservice manufacturer, from October 2008 to May 2009, and Senior Vice President, Group Controller of Nestle S.A., an international food and beverage company, from June 2006 to September 2008. Mr. Berryman was also Chief Financial Officer of Nestle Purina PetCare, a pet care company, from December 2001 to May 2006.

Nicolas Mirzayantz has served as our Group President, Fragrances since January 2007, and also served as a member of our Temporary Office of the Chief Executive Officer from October 1, 2009 until February 2010. Mr. Mirzayantz has also served as our Senior Vice President, Fine Fragrance and Beauty Care and Regional Manager North America, from March 2005 to December 2006, our Senior Vice President, Fine Fragrance and Beauty Care from October 2004 to February 2005, and our Vice President Global Fragrance Business Development from February 2002 to September 2004.

Hernan Vaisman has served as our Group President, Flavors since January 2007, and also served as a member of our Temporary Office of the Chief Executive Officer from October 1, 2009 until February 2010. From October 2004 to December 2006, Mr. Vaisman served as our Vice President, Latin America, and from January 2003 to September 2004, Mr. Vaisman served as our Regional Finance Director, Latin America Region.

Ahmet Baydar has served as our Senior Vice President, Research and Development since September 2010, and as our Vice President, Global Fragrance Research from February 2009 to August 2010. Prior to joining us, Dr. Baydar served as a Director of Shave Care and Integrated Shaving Systems at The Procter & Gamble Company, a branded consumer packed goods company, from January 2006 to October 2007, and Vice President of R&D-Personal Care at The Gillette Company, a personal care products company, from August 2000 to January 2006.

Angelica T. Cantlon has served as our Senior Vice President, Human Resources since August 2009. Prior to joining us, Ms. Cantlon served as Senior Vice President-International Chief Administrative Officer of MetLife, Inc., an insurance and financial services company, from June 2005 to August 2009, and Senior Vice President-Human Resources Business Leader, of Metlife from September 1999 to June 2005.

Anne Chwat has served as our Senior Vice President, General Counsel and Corporate Secretary since April 2011. Prior to joining us, Ms. Chwat served as Executive Vice President and General Counsel of Burger King

10

Table of Contents

Holdings, Inc., a fast food hamburger restaurant company, from September 2004 to April 2011. From September 2000 to September 2004, Ms. Chwat served in various positions at BMG Music (now SonyBMG Music Entertainment), including as Senior Vice President, General Counsel and Chief Ethics and Compliance Officer.

Francisco Fortanet has served as Senior Vice President, Operations since February 27, 2012 and as our Vice President, Global Manufacturing Compounding from January 2007 to February 2012. Mr. Fortanet has also served as our Vice President, Global Manufacturing from January 2006 to January 2007, our Regional Director of North America Operations from December 2003 to January 2005, the Project Manager of a Special Project in IFF Ireland from May 2003 to December 2003 and as our Plant Manager in Hazlet, New Jersey from October 1999 to May 2003.

Richard A. O’Leary has served as our Vice President and Controller since June 2009, our Interim Chief Financial Officer from July 2008 to May 2009 and our Vice President, Corporate Development from July 2007 to May 2009. Prior to joining us, Mr. O’Leary served in various positions since 1986 at International Paper Co., a paper and packaging company, including, most recently, as Chief Financial Officer of International Paper Company (Brazil) from June 2004 to June 2007.

| ITEM 1A. | RISK FACTORS. |

We routinely encounter and address risks in conducting our business. Some of these risks may cause our future results to be different — sometimes materially different — than we presently anticipate. Below are certain important operational and strategic risks that could adversely affect our business. How we react to material future developments, as well as how our competitors react to those developments, could also affect our future results.

Volatility and increases in the price of raw materials, energy and transportation could harm our profits.

We use many different raw materials for our business, including essential oils, extracts and concentrates derived from fruits, vegetables, flowers, woods and other botanicals, animal products, raw fruits, organic chemicals and petroleum-based chemicals. During 2011, the cost of raw materials exceeded our initial estimates and we anticipate modest inflation in commodity and other raw material prices in 2012. Historically, we have experienced the greatest amount of price volatility in natural products that represent approximately half of our raw material purchases. Availability and pricing of these natural products, such as citrus and vanilla, can be impacted by crop size and quality, weather or alternative land use which we cannot control.

If we are unable to increase the prices to our customers of our fragrance or flavor products to cover raw material and other input cost increases or if we are unable to achieve cost savings to offset such cost increases, our profits and operating results will be adversely affected. Increases in prices of our products to customers may lead to declines in volume, and we may not be able to accurately predict the volume impact of price increases, which could adversely affect our financial condition and results of operations. In addition, we source many of our raw materials globally to help ensure quality control. If the cost of energy, shipping and transportation increases and we are unable to pass along these costs to our customers, our profit margins would be adversely affected. Furthermore, increasing our prices to our customers could result in long-term sales declines or loss of market share if our customers find alternative suppliers or choose to reformulate their consumer products to use fewer ingredients, which could have a long-term impact on our results of operations.

To mitigate our sourcing risk, we maintain strategic stock levels for critical items. However, if we do not accurately estimate the amount of raw materials that will be used or the geographic region in which we will need these materials our margins could be adversely affected.

The current volatility in the global economy may adversely affect consumer spending and may negatively impact our business and operating results.

Our flavors and fragrances are components of a wide assortment of global consumer products throughout the world. Since mid-2008, the global economy has experienced significant recessionary pressures and declines

11

Table of Contents

in consumer confidence and economic growth. These conditions led to economic contractions in the developed economies and reduced growth rates in the emerging markets. While some segments of the global economy appear to be recovering, the ongoing debt crisis in Europe and the austerity plans being adopted in many countries has, and may in the near future, increase unemployment and underemployment, decrease salaries and wage rates, increase energy prices and inflation or result in other market-wide cost pressures that will adversely affect demand for consumer products in both developed and emerging markets. Reduced consumer spending may cause changes in our customer orders including reduced demand for our flavors and fragrances, increased pressure to reduce the price of our flavors and fragrances and/or order cancellations. To the extent that the volatility in global economic conditions continue, our sales, profitability and overall operating results could be adversely affected.

We may not successfully develop and introduce new products that appeal to our customers or our customers may not accurately anticipate and respond to global consumer market trends.

Our growth and performance largely depends on our ability to successfully develop and introduce new products and product improvements that appeal to our customers, and ultimately to global consumers. We must continually anticipate and react to, in a timely and cost-efficient manner, changes in consumer preferences and demands. We cannot be certain that we will successfully achieve our innovation goals. We currently spend approximately 8% of our sales on research and development; however, such investments may only generate future revenues to the extent that we are able to successfully develop products that meet our customers’ specifications, that can be delivered at an acceptable price and that are accepted by the targeted consumer market. Furthermore, there may be significant lag times from the time we incur R&D costs to the time that these R&D costs may result in increased revenue. Consequently, even when we have “won” a project, our ability to generate revenues as a result of these investments is subject to numerous economic and other risks that are outside of our control, including delays by our customers in the launch of a new product, insufficient resources allocated by our customers to promoting the new product, anticipated sales by our customers not being realized or changes in market preferences or demands.

Failure to maintain the integrity of our raw materials, supply chain and finished goods may adversely impact sales and our results of operations, litigation costs and our reputation.

The manufacture and sale of our products are subject to various regulatory requirements in each of the countries in which our products are manufactured and sold. In addition, we are subject to product safety and compliance requirements established by the industry or similar oversight bodies. We use a variety of strategies, methodologies and tools to (i) identify current product standards, (ii) assess relative risks in our supply chain that can impact product integrity, (iii) monitor internal and external performance and (iv) test raw materials and finished goods to minimize the likelihood of product or process non-compliance.

If a product non-compliance event were to go undetected, we could be subject to customer claims, recalls, penalties, litigation costs and/or settlements, remediation costs or loss of sales. These consequences would be exacerbated if our customer did not identify the defect and there was a resulting impact at the consumer level. This could lead to potentially large scale adverse publicity, recalls and potential consumer litigation. Furthermore, adverse publicity about our products, including concerns about product safety or similar issues, whether real or perceived, could harm our reputation and result in an immediate adverse effect on our sales, as well as require us to utilize significant resources to rebuild our reputation.

The increase in demand for consumer products using flavors and fragrances has been driven by factors outside of our control, and if these factors do not persist our future growth could be adversely affected.

Demand for consumer products using flavors and fragrances has been stimulated and broadened by changing social habits and economic growth, especially in emerging markets. Nearly 46% of our 2011 sales were generated in emerging markets and we expect emerging markets to significantly contribute to our future growth. Increasing consumer demand for products using flavors and fragrances is dependent on factors such as increases

12

Table of Contents

in personal income, dual-earner households, teenage population, leisure time, health concerns and urbanization and by the continued growth in world population, all of which are outside of our control. Changes in any number of external economic factors, or changes in social or consumer preferences, could materially adversely impact our results of operations. Accordingly, our future growth will depend upon the continued economic growth and development of consumer spending on products for which we supply the flavor or fragrance in these global markets.

Our international operations are subject to economic, political and other risks that could materially and adversely affect our revenues or financial position.

We operate on a global basis, with manufacturing and sales facilities in the United States, Europe, Africa and the Middle East, Latin America, and Greater Asia. During 2011, the majority of our net sales were generated outside the United States and we intend to continue expansion of our international operations. As a result, our business is increasingly exposed to risks inherent in international operations. These risks, which can vary substantially by market, are described in many of the risk factors in this section and include the following:

| Ÿ | governmental laws, regulations and policies adopted to manage national economic conditions, such as increases in taxes, austerity measures that impact consumer spending, monetary policies that may impact inflation rates and currency fluctuations; |

| Ÿ | the effects of legal and regulatory changes and the burdens and costs of our compliance with a variety of foreign laws and regulations; |

| Ÿ | the imposition of tariffs, quotas, trade barriers, other trade protection measures and import or export licensing requirements, which could adversely affect our cost or ability to import raw materials or export our flavors or fragrances to surrounding markets; |

| Ÿ | our ability to anticipate and adapt our flavors and fragrances to local preferences; |

| Ÿ | risks and costs arising from language and cultural differences; |

| Ÿ | changes in the laws and policies that govern foreign investment in the countries in which we operate, including the risk of expropriation or nationalization, and the costs and ability to repatriate the revenue that we generate in these countries; |

| Ÿ | risks and costs associated with political and economic instability, corruption, and social and ethnic unrest in the countries in which we operate; |

| Ÿ | difficulty in recruiting and retaining trained personnel; |

| Ÿ | risks and costs associated with health or similar issues, such as a pandemic or epidemic; |

| Ÿ | the risks of operating in developing or emerging markets in which there are significant uncertainties regarding the interpretation, application and enforceability of laws and regulations and the enforceability of contract rights and intellectual property rights. |

These factors may increase in importance as we expand our operations in emerging markets as part of our growth strategy.

In addition, there is a risk of potentially higher incidence of fraud or corruption in certain foreign jurisdictions or increased risk of internal control issues. As needed, we conduct internal investigations, control testing and compliance reviews to help ensure that we are in compliance with applicable laws and regulations. Additionally, we could be subject to inquiries or investigations by government and other regulatory bodies. Any determination that our operations or activities are not in compliance with U.S. laws, including the Foreign Corrupt Practices Act, or international laws and regulations could expose us to significant fines, penalties or other sanctions that may harm our business and reputation.

13

Table of Contents

Our ability to compete effectively depends on our ability to protect our intellectual property rights

We rely on patents and trade secrets to protect our intellectual property rights. As part of our strategy to protect our intellectual property rights, we often rely on trade secrets to protect our proprietary fragrance and flavor formulations, as this does not require us to publicly file information regarding our intellectual property. If a third party infringes upon our intellectual property, or if a third party claims that we have infringed upon their intellectual property rights, we could incur significant costs in connection with legal actions to assert our intellectual property rights or to defend ourselves from assertions of invalidity, infringement or misappropriation. For those intellectual property rights that are protected by way of trade secrets, this litigation could result in even higher costs, and potentially the loss of certain rights, as we would not have a perfected intellectual property right that precludes others from making, using or selling our products or processes.

For intellectual property rights that we seek to protect through patents, we cannot be certain that these rights, if obtained, will not later be opposed, invalidated, or circumvented. In addition, even if such rights are obtained in the United States, the laws of some of the other countries in which our products are or may be sold do not protect intellectual property rights to the same extent as the laws of the United States. If other parties were to infringe on our intellectual property rights, or if a third party successfully asserted that we had infringed on their intellectual property rights, it could materially and adversely affect our future results of operations by (i) reducing the price that we could obtain in the marketplace for products which are based on such rights, (ii) increasing the royalty or other fees that we may be required to pay in connection with such rights or (iii) limiting the volume, if any, of such products that we can sell.

Our business is highly competitive, and if we are unable to compete effectively our sales and results of operations will suffer.

The market for flavors and fragrances is highly competitive. We face vigorous competition from companies throughout the world, including multinational and specialized flavor and fragrance companies, as well as consumer product companies who may develop their own flavors or fragrances. Some of our competitors specialize in one or more of our product segments, while others participate in many of our product segments. In addition, some of our global competitors may have greater resources than we do or may have proprietary products that could permit them to respond to changing business and economic conditions more effectively than we can. Consolidation of our competitors may exacerbate these risks.

Competition in our business is based on innovation, product quality, pricing, quality of our customer service, the support provided by our marketing and application groups, and our understanding of consumers. It is difficult for us to predict the timing and scale of our competitors’ actions in these areas. The discovery and development of new flavor and fragrance materials, protection of the Company’s intellectual property and development and retention of key employees are important issues in our ability to compete in our businesses. Increased competition by existing or future competitors, including aggressive price competition, could result in the potential loss of substantial sales or create the need for us to reduce prices or increase spending and this could have an impact on sales and profitability.

Large multinational customers, and increasingly, mid-sized customers, may limit the number of their suppliers, giving those that remain on “core lists” priority for new or modified products. To compete more successfully in this environment, we must continue to make investments in customer relationships and tailor product research and development in order to anticipate customers’ needs, provide effective service and secure and maintain inclusion on certain “core lists.” If we are unable to do so, it could adversely impact our future results of operations.

Our success depends on attracting and retaining talented people within our business. Significant shortfalls in recruitment or retention could adversely affect our ability to compete and achieve our strategic goals.

Attracting, developing, and retaining talented employees, including our perfumers and flavorists, is essential to the successful delivery of our products and success in the marketplace. Competition for these employees can

14

Table of Contents

be intense. The ability to attract and retain talented employees is critical in the development of new products and technologies which is an integral component of our growth strategy. However, we may not be able to attract and retain such employees in the future. If we experience significant shortfalls in recruitment or retention, our ability to effectively compete with our competitors and to grow our business could be adversely affected.

Our reliance on a limited base of suppliers may result in a disruption to our business.

For certain raw materials, we rely on a limited number of suppliers and we may not have readily available alternatives. If we are unable to maintain our supplier arrangements and relationships and are unable to obtain the quantity, quality and price levels needed for our business, or if any of our key suppliers becomes insolvent or experiences other financial distress, we could experience disruptions in production and our financial results could be adversely affected.

A disruption in operations or our supply chain could adversely affect our business and financial results.

As a company engaged in development, manufacturing and distribution on a global scale, we are subject to the risks inherent in such activities, including industrial accidents, environmental events, strikes and other labor disputes, disruptions in supply chain or information systems, loss or impairment of key manufacturing sites, product quality control, safety, licensing requirements and other regulatory issues, as well as natural disasters and other external factors over which we have no control. If any of these events were to occur, it could have an adverse effect on our business and financial results. In addition, while we have manufacturing facilities throughout the world, certain of our facilities are the sole manufacturer of a specific ingredient. If the manufacture of that ingredient were disrupted, the cost of relocating or replacing the production of an ingredient or reformulating a product may be substantial, which could have an adverse effect on our operating results.

Our results may be negatively impacted by the outcome of uncertainties related to litigation.

We are involved in a number of legal claims and litigation, including claims related to indirect taxes. We cannot predict the ultimate outcome of such litigation. In addition, we cannot provide assurance that future events will not result in an increase in the number of claims or require an increase in the amount accrued for any such claims, or require accrual for one or more claims that has not been previously accrued.

Our future success depends on our ability to achieve our long-term strategy.

Achieving our long-term objectives will require investment in product innovation and expanding our presence in emerging markets. These investments may result in short-term costs without any current revenues and, therefore, may be dilutive to our earnings, at least in the short term. In addition, as part of our strategy to maximize the economic profitability of our product portfolio, we may employ various strategies, including increasing pricing, implementing cost reduction or containment measures or phasing out low margin products. We may not realize, in full or in part, the anticipated benefits of our strategy, and we may incur costs or special charges related to our strategy. The failure to realize benefits, which may be due to our inability to execute plans, global or local economic conditions, competition, changes in our industry and the other risks described herein, could have a material adverse effect on our business, financial condition and results of operations.

The level of returns on pension and postretirement plan assets and the actuarial assumptions used for valuation purposes could affect our earnings and cash flows in future periods. Changes in government regulations could also affect our pension and postretirement plan expenses and funding requirements.

The funding obligations for our pension plans are impacted by the performance of the financial markets, particularly the equity markets, and interest rates. Funding obligations are determined under government regulations and are measured each year based on the value of assets and liabilities on a specific date. If the financial markets do not provide the long-term returns that are expected under the governmental funding calculations, we could be required to make larger contributions. The equity markets can be, and recently have been, very volatile, and therefore our estimate of future contribution requirements can change dramatically in

15

Table of Contents

relatively short periods of time. Similarly, changes in interest rates and legislation enacted by governmental authorities can impact the timing and amounts of contribution requirements. An adverse change in the funded status of the plans could significantly increase our required contributions in the future and adversely impact our liquidity.

Assumptions used in determining projected benefit obligations and the fair value of plan assets for our pension and other postretirement benefit plans are determined by us in consultation with outside consultants and advisors. In the event that we determine that changes are warranted in the assumptions used, such as the discount rate, expected long-term rate of return on assets, or expected health care costs, our future pension and postretirement benefit expenses could increase or decrease. Due to changing market conditions or changes in the participant population, the assumptions that we use may differ from actual results, which could have a significant impact on our pension and postretirement liabilities and related costs and funding requirements.

Impairment charges on our long-lived assets could have a material adverse effect on our financial results.

Future events may occur that would adversely affect the reported value of our long-lived assets and require impairment charges. Such events may include, but are not limited to, strategic decisions made in response to changes in economic and competitive conditions, the impact of the economic environment on our sales and our relationship with significant customers or business partners, or a sustained decline in our stock price. We continue to evaluate the impact of economic and other developments on our business to assess whether impairment indicators are present. Accordingly, we may perform impairment tests more frequently than annually required, based on changes in the economic environment and other factors, and these tests could result in impairment charges in the future.

Our financial results may be adversely impacted by the failure to successfully execute acquisitions, collaborations and joint ventures.

From time to time, we may evaluate potential acquisitions, collaborations or joint ventures that align with our strategic objectives. The success of such activity depends, in part, upon our ability to identify suitable buyers or partners; perform effective assessments prior to contract execution; negotiate contract terms; and, if applicable, obtain government approval. These activities may present certain financial, managerial and operational risks, including diversion of management’s attention from existing core businesses; difficulties integrating or separating businesses from existing operations, including employee integration; and challenges presented by acquisitions, collaborations or joint ventures which may not achieve sales levels and profitability that justify the investments made. If the acquisitions, collaborations or joint ventures are not successfully implemented or completed, there could be a negative impact on our results of operations, financial condition and cash flows.

Our results of operations may be negatively affected by the impact of currency fluctuation or devaluation in the international markets in which we operate.

Our operations are conducted in many countries, the results of which are reported in the local currency and then translated into U.S. dollars at applicable exchange rates. The exchange rates between these currencies and the U.S. dollar have fluctuated and will continue to do so in the future. Volatility in currency exchange rates may materially adversely impact our reported results of operations, financial condition or liquidity. We employ a variety of techniques to reduce the impact of exchange rate fluctuations, including sourcing strategies and a limited number of foreign currency hedging activities. However, if our hedging and risk management strategies are not effective, our results of operations could be adversely affected.

Changes in our tax rates, the adoption of new U.S. or international tax legislation or exposure to additional tax liabilities could affect our future results.

We are subject to taxes in the United States and numerous foreign jurisdictions. Our future effective tax rates could be affected by changes in the mix of earnings in countries with differing statutory tax rates, changes

16

Table of Contents

in the valuation of deferred tax assets and liabilities, changes in liabilities for uncertain tax positions, cost of repatriations or changes in tax laws or their interpretation. In addition, the current administration and Congress have announced proposals for new U.S. tax legislation that, if adopted, could adversely affect our tax rate. Any of these changes could have a material adverse effect on our profitability. We are also subject to the continual examination of our income tax returns by the Internal Revenue Service and foreign tax authorities in those countries in which we operate. In particular, we are currently involved in tax disputes with the Spanish tax authorities regarding certain tax positions taken in our Spanish subsidiaries’ tax returns and anticipate that we will receive additional assessments for matters similar to those under appeal. We are disputing the pending tax assessments and intend to dispute any future tax assessment that challenges these same tax positions. The final determination of tax audits and any related litigation could be materially different from our historical income tax provisions and accruals. The results of a tax audit or related litigation could have a material effect on our income tax provision, net income or cash flows in the period or periods in which that determination is made.

Our operations may be affected by greenhouse emissions and climate change and related regulations.

The availability of raw materials and energy supplies fluctuate in markets throughout the world. Climate change may also affect the availability and price of key raw materials, including natural products used in the manufacture of our products. In order to mitigate the risk of price increases and shortages, our purchasers have developed various sourcing strategies, including multiple suppliers, inventory management systems, various geographic suppliers and long-term agreements to mitigate risk.

In addition to market forces, there are various regulatory efforts relating to climate change that may increase the cost of raw materials, particularly energy used to operate our facilities, that could materially impact our financial condition, results of operations and cash flows.

Information technology system failures or interruptions or breaches of our network security may interrupt our operations, subject us to increased operating costs and expose us to litigation.

We have information systems that support our business processes, including product formulas, product development, sales, order processing, production, distribution, finance and intra-company communications throughout the world. These systems may be susceptible to outages due to fire, floods, power loss, telecommunications failures, break-ins and similar events. In addition, our systems may be vulnerable to computer viruses, computer hacking and similar disruptions from unauthorized tampering. The occurrence of these or other events could interrupt our operations, subject us to increased operating costs and expose us to litigation.

| ITEM 1B. | UNRESOLVED STAFF COMMENTS. |

None.

| ITEM 2. | PROPERTIES. |

Our principal properties are as follows:

| Location |

Operation | |

| United States |

||

| Augusta, GA |

Production of fragrance ingredients. | |

| Carrollton, TX(1) |

Production of flavor compounds; flavor laboratories. | |

| Hazlet, NJ(1) |

Production of fragrance compounds; fragrance laboratories. | |

| Jacksonville, FL |

Production of fragrance ingredients. | |

| New York, NY(1) |

Fragrance laboratories; corporate headquarters. | |

| South Brunswick, NJ(1) |

Production of flavor compounds and ingredients; flavor laboratories. | |

| Union Beach, NJ |

Research and development center. |

17

Table of Contents

| Location |

Operation | |

| France |

||

| Neuilly(1) |

Fragrance laboratories. | |

| Grasse |

Production of flavor and fragrance ingredients; fragrance laboratories. | |

| Great Britain |

||

| Haverhill |

Production of flavor compounds and ingredients, and fragrance ingredients; flavor laboratories. | |

| Netherlands |

||

| Hilversum |

Flavor and fragrance laboratories. | |

| Tilburg |

Production of flavor compounds and ingredients, and fragrance compounds. | |

| Spain |

||

| Benicarlo |

Production of fragrance ingredients. | |

| Argentina |

||

| Garin |

Production of flavor compounds and ingredients, and fragrance compounds; flavor laboratories. | |

| Brazil |

||

| Rio de Janeiro |

Production of fragrance compounds. | |

| São Paulo |

Flavor and fragrance laboratories. | |

| Taubate |

Production of flavor compounds and ingredients. | |

| Mexico |

||

| Tlalnepantla |

Production of flavor and fragrance compounds; flavor and fragrance laboratories. | |

| India |

||

| Mumbai(2) |

Flavor and fragrance laboratories. | |

| Chennai(2) |

Production of flavor compounds and ingredients, and fragrance compounds; flavor laboratories. | |

| Australia |

||

| Dandenong |

Production of flavor compounds and flavor ingredients. | |

| China |

||

| Guangzhou(4) |

Production of flavor and fragrance compounds. | |

| Shanghai(6) |

Flavor and fragrance laboratories. | |

| Xin’anjiang(5) |

Production of fragrance ingredients. | |

| Zhejiang(4) |

Production of fragrance ingredients. | |

| Indonesia |

||

| Jakarta(3) |

Production of flavor compounds and ingredients, and fragrance compounds and ingredients; flavor and fragrance laboratories. | |

| Japan |

||

| Gotemba |

Production of flavor compounds. | |

| Tokyo |

Flavor and fragrance laboratories. | |

| Singapore |

||

| Jurong (6) |

Production of flavor and fragrance compounds. | |

| Science Park(1) |

Flavor and fragrance laboratories. | |

| (1) | Leased. |

| (2) | We have a 93.4% interest in the subsidiary company that owns this facility. |

| (3) | Land is leased and building is partially leased and partially owned. |

| (4) | Land is leased and building and machinery and equipment are owned. |

| (5) | We have a 90% interest in the subsidiary company that leases the land and owns the buildings and machinery. |

| (6) | Building is leased and machinery and equipment are owned. |

18

Table of Contents

Our principal executive offices and New York laboratory facilities are located at 521 West 57th Street, New York City.

| ITEM 3. | LEGAL PROCEEDINGS. |

Patent Claims

In May 2006, Mane Fils S.A. filed a complaint against the Company in the U.S. District Court for the District of New Jersey alleging that the Company infringed U.S. Patent Nos. 5,725,856 and 5,843,466 that relate to a cooling additive in food and beverage products. The complaint was subsequently amended to also assert claims for violations of the Lanham Act, tortious interference and unfair competition. The Company answered both the original complaint and the amended complaint by denying liability and asserting that both patents were invalid and various other defenses. In connection with the claims, the plaintiff sought (i) monetary damages, (ii) punitive damages, (iii) injunctive relief (with respect to the patent claims) and (iv) fees, costs and interest. On December 29, 2011, the Company settled all patent and non-patent claims. Pursuant to the terms of the settlement agreement, the Company paid Mane a one-time royalty of approximately $40 million. In addition, the Company agreed to cease making or selling Cooler 1 products and to ensure that the Monomenthyl Succinate (MMS) content of its Cooler 2® products going forward is at a level that has been agreed upon by both parties.

Tax Claims

The Company is currently involved in administrative and legal proceedings that relate to tax deductions taken in its Spanish subsidiaries’ tax returns which are being challenged by the Spanish tax authorities. As a result of tax audits, the Spanish tax authorities imposed tax assessments on the Company’s Spanish subsidiaries in the amounts of Euro 23.1 ($29.9) million for fiscal years 2002-2003 and Euro 61.6 ($79.6) million for fiscal years 2004-2006. In addition to the disallowance of tax deductions, the tax authorities are also asserting tax avoidance arising from the same facts. During 2007 and 2008, we filed appeals against the 2002-2003 tax assessments and related tax avoidance claim with the Central Economic-Administrative Tribunal (“TEAC”) in Spain. In March 2010, the TEAC affirmed the 2002-2003 tax assessments and related claim and, in January 2011, the Company filed an appeal for judicial review with the Spanish National Appellate Court. During 2011, we filed appeals with the TEAC against the 2004-2006 tax assessment and related tax avoidance claim. The TEAC has not yet ruled on such appeals. In January 2012, the Spanish tax authorities notified the Company of their intent to audit the 2007-2010 tax returns of our Spanish subsidiaries. The tax positions that have previously been challenged by the Spanish tax authorities were consistently taken in our Spanish subsidiaries’ tax returns from 2002 through the end of 2011. Consequently, the Company anticipates that it will receive an assessment for matters similar to those under appeal, for the fiscal years 2007-2011. In 2012, the Company has reorganized its business operations in Spain and the Netherlands, and, therefore, the Company anticipates that substantially all of the challenged tax deductions previously taken will no longer be applicable in future tax returns of its Spanish subsidiaries. The Company continues to dispute the pending tax assessments and intends to dispute any future tax assessment that challenges these same tax positions.

In addition to the above, the Company is also a party to four dividend withholding tax controversies in Spain, alleging that the Company’s Spanish subsidiaries underpaid withholding taxes, which are at different stages of administrative and judicial review, spanning fiscal years 1995-2001, in the aggregate amount of Euro 18.1 million ($23.4 million). The Company expects that two of these cases, aggregating Euro 12.3 ($15.9 million), will be decided by the Spanish Supreme Court during the first half of 2012. The Company obtained a favorable ruling at the lower court in one of these cases and the Spanish tax authorities have appealed to the Spanish Supreme Court. The Company has appealed the other case to the Spanish Supreme Court, as it obtained an unfavorable ruling at the lower court.

If the aforementioned tax assessments are ultimately resolved against the Company, the resulting increase in its liability for uncertain tax positions could have a material effect on the Company’s results of operations and cash flows in a particular period.

19

Table of Contents

Environmental

Over the past 20 years, various federal and state authorities and private parties have claimed that the Company is a Potentially Responsible Party (“PRP”) as a generator of waste materials for alleged pollution at a number of waste sites operated by third parties located principally in New Jersey and have sought to recover costs incurred and to be incurred to clean up the sites.

The Company has been identified as a PRP at ten facilities operated by third parties at which investigation and/or remediation activities may be ongoing. The Company analyzes its liability on at least a quarterly basis. The Company accrues for environmental liabilities when they are probable and estimable. The Company estimates its share of the total future cost for these sites to be less than $5 million.

While joint and several liability is authorized under federal and state environmental laws, the Company believes the amounts it has paid and anticipates paying in the future for clean-up costs and damages at all sites are not and will not have a material adverse effect on our financial condition, results of operations or liquidity. This assessment is based upon, among other things, the involvement of other PRPs at most sites, the status of the proceedings, including various settlement agreements and consent decrees, the extended time period over which payments will likely be made and an agreement reached in July 1994 with three of the Company’s liability insurers pursuant to which defense costs and indemnity amounts payable by the Company in respect of the sites will be shared by the insurers up to an agreed amount. There can be no assurance, however, that future events will not require us to materially increase the amounts we anticipate paying for clean-up costs and damages at these sites.

Other

The Company is also a party to other litigation arising in the ordinary course of business. The Company does not expect the outcome of these cases, singly or in the aggregate, to have a material effect on its financial condition, results of operations or liquidity.

| ITEM 4. | MINE SAFETY DISCLOSURES. |

Not applicable.

20

Table of Contents

PART II

| ITEM 5. | MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES. |

Market Information.