UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

|

[X]

|

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

For the fiscal year ended June 30, 2015

or

|

[ ]

|

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

001-34941

(Commission file number)

PARK CITY GROUP, INC.

(Exact name of registrant as specified in its charter)

|

Nevada

|

37-1454128

|

|

|

State or other jurisdiction of incorporation

|

(IRS Employer Identification No.)

|

|

|

299 South Main Street, Suite 2370

Salt Lake City, Utah 84111

|

(435) 645-2000

|

|

|

(Address of principal executive offices)

|

(Registrant's telephone number, including area code)

|

Securities registered pursuant to Section 12(b) of the Act: None

|

Title of each Class

|

Name of each exchange on which registered

|

|

|

Common Stock, $0.01 Par Value

|

NASDAQ Capital Market

|

Securities registered pursuant to Section 12(g) of the Act: Common Stock, $0.01 par value per share

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. [ ] Yes [X] No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. [ ] Yes [X] No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. [X] Yes [ ] No

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 229.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). [X] Yes [ ] No

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. [ ]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

|

Large accelerated filer

|

[ ]

|

Accelerated filer

|

[X]

|

|

Non-accelerated filer

(Do not check if a smaller reporting company)

|

[ ]

|

Smaller reporting company

|

[ ]

|

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act).

[ ] Yes [X] No

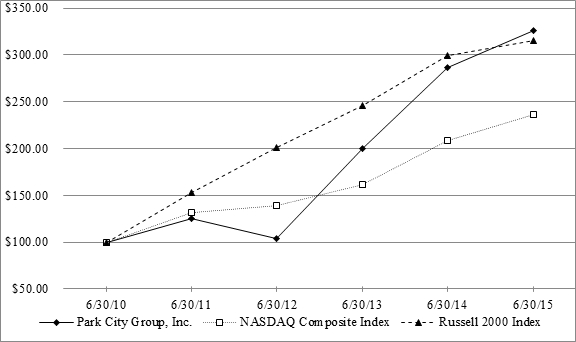

The aggregate market value of the voting and non-voting common stock held by non-affiliates of the issuer as of December 31, 2014, which is the last business day of the registrant’s most recently completed second fiscal quarter, was approximately $114,182,000 (at a closing price of $9.02 per share).

As of September 11, 2015, 19,064,108 shares of the Company’s $0.01 par value common stock were outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Items 10, 11, 12, 13 and 14 of Part III incorporate by reference certain information from Park City Group, Inc.’s definitive proxy statement, to be filed with the Securities and Exchange Commission on or before October 28, 2015.

TABLE OF CONTENTS TO ANNUAL REPORT

ON FORM 10-K

YEAR ENDED JUNE 30, 2015

|

PART I

|

||

|

1

|

||

|

9

|

||

|

16

|

||

|

16

|

||

|

16

|

||

| PART II | ||

|

17

|

||

|

18

|

||

|

18

|

||

|

28

|

||

|

29

|

||

|

29

|

||

|

29

|

||

|

29

|

||

| PART III | ||

|

30

|

||

|

30

|

||

|

30

|

||

|

30

|

||

|

30

|

||

| PART IV | ||

|

31

|

||

|

32

|

||

|

F-1

|

||

|

F-2

|

||

|

F-3

|

||

|

F-4

|

||

|

F-6

|

||

|

F-8

|

||

FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K contains forward-looking statements. The words or phrases “would be,” “will allow,” “intends to,” “will likely result,” “are expected to,” “will continue,” “is anticipated,” “estimate,” “project,” or similar expressions are intended to identify “forward-looking statements.” Actual results could differ materially from those projected in the forward looking statements as a result of a number of risks and uncertainties, including the risk factors set forth below and elsewhere in this Report. See “Risk Factors” and “Management's Discussion and Analysis of Financial Condition and Results of Operations.” Statements made herein are as of the date of the filing of this Form 10-K with the Securities and Exchange Commission and should not be relied upon as of any subsequent date. Unless otherwise required by applicable law, we do not undertake, and specifically disclaim any obligation, to update any forward-looking statements to reflect occurrences, developments, unanticipated events or circumstances after the date of such statement.

PART I

|

ITEM I.

|

BUSINESS

|

Overview

Park City Group, Inc. (the “Company”) is a Software-as-a-Service (“SaaS”) provider that brings unique visibility to the consumer goods supply chain, delivering actionable information that ensures product is on the shelf when the consumer expects it. Our service increases our customers’ sales and profitability while enabling lower inventory levels for both retailers and their suppliers.

Our services are delivered principally though proprietary software products designed, developed, marketed and supported by the Company. These products are designed to facilitate improved business processes among all key constituents in the supply chain, starting with the retailer and moving back to suppliers and eventually raw material providers. In addition, the Company has built a consulting practice for business process improvement that centers around the Company’s proprietary software products and through establishment of a neutral and “trusted” third party relationship between retailers and suppliers. The principal markets for the Company's products are multi-store retail and convenience store chains, branded food manufacturers, suppliers and distributors and manufacturing companies.

Historically, the Company offered applications and related maintenance contracts to new customers for a one-time, non-recurring up front license fee. Although not completely abandoning the license fee and maintenance model, since the acquisition of Prescient Applied Intelligence, Inc. (“Prescient”) in January 2009, the Company has focused its strategic initiatives and resources to marketing and selling prospective customers a subscription for its product offerings. In support of this strategic shift toward a subscription-based model, the Company has scaled its contracting process, streamlined its customer on-boarding and implemented a financial package that integrates multiple systems in an automated fashion. As a result, subscription based revenue has grown from $203,000 for the 2008 fiscal year to approximately $10.9 million in the year ended June 30, 2015. During that same period our revenue has transitioned from 6% subscription revenue and 94% license and other revenue, to 80% subscription revenue and 20% license and other revenue.

The Company is incorporated in the state of Nevada. The Company has three subsidiaries: PC Group, Inc. (formerly, Park City Group, Inc.), a Utah corporation (98.76% owned), Park City Group, Inc. (formerly, Prescient Applied Intelligence, Inc.), a Delaware corporation (100% owned) and ReposiTrak, Inc., a Utah corporation (100% owned). All intercompany transactions and balances have been eliminated in consolidation.

Our principal executive offices of the Company are located at 299 South Main Street, Suite 2370, Salt Lake City, Utah 84111. Our telephone number is (435) 645-2000. Our website address is http://www.parkcitygroup.com.

Recent Developments

Acquisition of ReposiTrak

During the year ended June 30, 2015, the Company entered into agreements with each of the stockholders of ReposiTrak, Inc. (“ReposiTrak”), including Leavitt Partners, LP and LP Special Asset 4, LLC, to acquire all of the outstanding capital stock of ReposiTrak (the “ReposiTrak Shares”) in exchange for shares of the Company’s common stock (the “ReposiTrak Acquisition”). On June 30, 2015, the Company completed the ReposiTrak Acquisition and issued an aggregate total of 873,438 shares of its common stock in exchange for the ReposiTrak Shares. Immediately following the completion of the ReposiTrak Acquisition, ReposiTrak became a wholly owned subsidiary of the Company.

Registered Direct Offering

On April 15, 2015, the Company offered and sold 572,500 shares of its common stock in a registered direct offering at a price of $12.50 per share. The Company received total net proceeds from the registered direct offering of approximately $6.7 million after deducting placement agent fees and other offering expenses.

Creation of Series B-1 Preferred

On March 31, 2015, the Company filed with the Nevada Secretary of State the Certificate of Designation of the Relative Rights, Powers and Preferences of the Series B-1 Preferred Stock (the “Series B-1 Certificate of Designation”) in order to designate 300,000 shares of the Company’s preferred stock as non-voting, non-convertible shares of Series B-1 Preferred Stock (“Series B-1 Preferred”). Each share of Series B-1 Preferred accrued dividends at a rate of 7% per annum if paid by the Company in cash, and 9% per annum if paid by the Company in additional shares of Series B-1 Preferred.

Series B Restructuring

On February 4, 2015, holders of the Company’s Series B Convertible Preferred Stock (“Series B Preferred”), consisting of the Company’s Chief Executive Officer, his spouse, and a director (the “Holders”), entered into a restructuring agreement (the “Restructuring Agreement”), pursuant to which the Holders consented to the filing of an amendment (the “Series B Amendment”) to the Certificate of Designation of the Relative Rights, Powers and Preference of the Series B Preferred (the “Series B Certificate of Designation”), pursuant to which (i) the rate at which the Series B Preferred accrues dividends was lowered to 7% per annum if paid by the Company in cash, or 9% if paid by the Company in PIK Shares (as defined below), (ii) the Company may now elect to pay accrued dividends on outstanding shares of Series B Preferred in either cash or by the issuance of additional shares of Series B Preferred (“PIK Shares”), (iii) the conversion feature of the Series B Preferred was eliminated, and (iv) the number of shares of the Company's preferred stock designated as Series B Preferred was increased from 600,000 to 900,000 shares (the “Series B Restructuring”). In consideration for the Series B Restructuring, the Company issued to the Holders: (y) an aggregate of 214,198 additional shares of Series B Preferred, which shares had a stated value equal to the amount that, but for the Series B Restructuring, would have been paid to the Holders as dividends over the next five years (“Additional Shares”), and (z) five-year warrants to purchase an aggregate of 1,085,068 shares of common stock for $4.00 per share (“Series B Warrants”), an amount and per share purchase price equal to what the Holders would otherwise be entitled to receive upon conversion of their shares of Series B Preferred (“Warrant Shares”).

The terms of the Series B Restructuring were amended on March 31, 2015 as follows: (i) the Series B Certificate of Designation was further amended (the “Second Series B Amendment”) to (x) reduce the number of shares of the Company’s preferred stock designated thereunder from 900,000 to 600,000, which number was subsequently increased to 700,000, (y) require that, should the Company pay dividends on the Series B Preferred in PIK Shares, shares Series B-1 Preferred will be issued, rather than shares of Series B Preferred, and (z) in the event any Holder elects to exercise a Series B Warrant, one share of Series B Preferred will be automatically converted into one share of Series B-1 Preferred for every 2.5 Warrant Shares received by such Holder; and (ii) the Restructuring Agreement was amended to substitute the Additional Shares for shares of Series B-1 Preferred. The Second Series B Amendment was filed with the Nevada Secretary of State on March 31, 2015.

Private Placement

On January 26, 2015, we accepted subscription agreements from certain accredited investors, including certain members of the Company's Board of Directors, to purchase an aggregate total of 95,302 shares of the Company's common stock for $9.48 per share, and five year warrants to purchase an aggregate total of 23,737 shares of common stock for $10.00 per share. The Company received gross proceeds of approximately $900,000 from this private placement.

Company History

The Company’s technology has its genesis in the operations of Mrs. Fields Cookies co-founded by Randall K. Fields, the Company’s Chief Executive Officer. The Company began operations utilizing patented computer software and profit optimization consulting services to help its retail clients reduce their inventory and labor cost - the two largest controllable expenses in the retail industry. Because the product concepts originated in the environment of actual multi-unit retail chain ownership, the products are strongly oriented to an operation’s bottom line results.

The Company was incorporated in the State of Delaware on December 8, 1964 as Infotec, Inc. From June 20, 1999 to approximately June 12, 2001, it was known as Amerinet Group.com, Inc. In 2001, the name was changed from Amerinet Group.com to Fields Technologies, Inc. On June 13, 2001, the Company entered into a “Reorganization Agreement” with Randall K. Fields and Riverview Financial Corporation whereby it acquired substantially all of the outstanding stock of Park City Group, Inc., a Delaware corporation, which became a 98.67% owned subsidiary.

On July 25, 2002, Fields Technologies, Inc. changed its name from Fields Technologies, Inc. to Park City Group, Inc. through a merger with Park City Group, Inc., a Nevada corporation, which was organized for that purpose and was also the surviving entity in the merger. As a result, both the parent-holding company (Nevada) and its operating subsidiary (Delaware) were named Park City Group, Inc. In February 2014, Park City Group, Inc. (Delaware) was domesticated in Utah and changed its name to PC Group, Inc. Park City Group, Inc. (Nevada) has no business operations separate from the operations conducted through its subsidiaries, including ReposiTrak, Inc. and Park City Group, Inc., a Delaware corporation, (formerly Prescient Applied Intelligence, Inc. (“Prescient”)).

On January 13, 2009, the Company acquired 100% of Prescient, a leading provider of on-demand solutions for the retail marketplace, including both retailers and suppliers. Its solutions capture information at the point of sale, provide greater visibility into real-time demand and turn data into actionable information across the entire supply chain. In February 2014, Prescient changed its name to Park City Group, Inc. The Company’s condensed consolidated financial statements contain the results of operations of Park City Group, Inc. (Delaware). Operations are conducted through this subsidiary.

ReposiTrak, Inc. was founded by Leavitt Partners. It was originally incorporated as Global Supply Chain Systems, Inc. on May 17, 2012 and on November 8, 2012 changed its name to ReposiTrak, Inc. (“ReposiTrak”). ReposiTrak provides food retailers and suppliers with a robust solution to help protect their brands and remain in compliance with rapidly evolving regulations in the Food Safety Modernization Act. Powered by Park City Group’s technology, this internet-based solution, also called ReposiTrakTM, enables all participants in the farm-to-table supply chain to easily manage records management and regulatory compliance. Additionally, ReposiTrak enables traceability as products and their ingredients move between trading partners. ReposiTrak, Inc. became a wholly owned subsidiary of Park City Group, Inc. on June 30, 2015.

Software-as-a-Service Delivery Model

Historically, the Company offered applications and related maintenance contracts to new customers for a one-time, non-recurring up front license fee and provided an option for annually renewing their maintenance agreements. As a result of the Prescient merger and Prescient’s reliance on subscription based revenue, and the Company began shifting away from offering its solutions for a one-time licensing fee and now principally offers prospective customers monthly subscription based licensing of its products. Although not completely abandoning the license fee and maintenance model, the Company continues to focus its strategic initiatives on increasing the number of retailers, suppliers and manufacturers that use its software on a subscription basis.

Our on-demand, software-as-a-service delivery model enables our proprietary software solutions to be implemented, accessed and used by our customers remotely. Our solutions are hosted and maintained by us, thus significantly reducing costs by eliminating for our customers the time, risk and headcount associated with installing and maintaining applications within their own information technology infrastructures. As a result, we believe our solutions require significantly less capital to build and require less initial investment in third-party software, hardware and implementation services, and have lower ongoing support costs versus traditional enterprise software. The software-as-a-service ("SaaS") model also allows for advanced information technology infrastructure management, security, disaster recovery and other best practices. Since we manage updates and upgrades to our solution on behalf of our customers, we are able to implement improvements to our solutions in a more rapid and uniform way, enabling us to take advantage of operational efficiencies.

Target Industries Overview

The Company develops and offers its software to supermarkets, convenience stores and other retailers. As a result of the acquisition of Prescient, we have expanded our offerings to include supply chain solutions focused on large manufacturers, distributors and suppliers in the consumer products industry. The Company also provides professional consulting services targeting implementation, assessments, profit optimization and support functions for its application and related products.

Supermarkets

The supermarket industry is under increased competitive pressure from mass market retailers such as Wal-Mart, Costco, Target, and other channels, including extreme value (dollar stores), limited assortment (ALDI/Save-a-lot), and convenience (Sheetz, 7/11) stores. One of the strategies traditional supermarkets are implementing is to improve the demographic “mix” of products to match the unique needs of those consumers who shop at individual stores. Mix is most difficult to manage for those products that are delivered by Direct Store Delivery (“DSD”) suppliers such as carbonated beverages, bread, dairy, greeting cards, magazines and salty snacks. The Company’s software provides newfound visibility to the retailer as to specific item deliveries and in-stock status with item and category productivity. In addition, supermarkets are growing sales and consumer loyalty by developing and distributing their own brand or private label for all key categories within their stores. This proliferation of new items is creating a new set of challenges for both retailers and suppliers as they battle to find space to accommodate the new private label items at the expense of the incumbent or national brand supplier. The Company’s software and consulting services provide visibility tools to facilitate the decision making process by providing a shared and trusted view to information that helps the parties optimize item selection and shelf presence. Furthermore, supermarkets are under pressure to increase the quantity and quality of their perishable offerings. Perishable departments, such as bakery, meat and seafood, dairy, and deli historically are loosely managed, but now are a focus for profitability improvement. The Company’s software and consulting services and change management resources are designed to address this specific business problem, increasing the profitability of perishable products at the department and store level.

Convenience Stores

For convenience stores, recent trends of contracting gasoline sales margins and declining tobacco sales further increases the need for improved cost controls, focus on product mix and better decision support. To intensify the focus on these issues, other industry segments such as value retailers and grocery stores are cutting into the convenience store stronghold by offering gasoline, a product that once was almost solely offered by convenience store retailers. In response to declining gasoline sales and profits, the convenience store industry is pushing into fresh food as an avenue of increasing sales and profitability. Only the most progressive convenience store operations have automated systems to help store managers, leaving the majority of the operators without any technology to ease their administrative and operational burdens.

Suppliers

As stated above, supermarkets and convenience stores are increasingly focused on product and margin mix, improving sales through reduced out of stocks and increasing collaboration with their suppliers. Suppliers are increasingly pressured by retailers to provide consumer insights and innovative products that differentiate both the supplier and retailer while providing economic incentives or assistance. The Company’s solutions enable suppliers to work with their retail partners to align their objectives of increasing sales through expanded distribution of their product offering and the objectives of the retailer to increase sales, reduce inventory carrying risk and minimizing out of stocks. Additionally, the Company is able to share the retailer scan sales data with the supplier to assist them in improving forecasts and production planning by leveraging the most reliable demand signal in daily sales by store and item.

Specialty Retailers

Specialty retailers and their suppliers are faced with many of the same replenishment and forecasting challenges as other retailers, with the added complexity of managing an ever increasing imported versus domestic manufacturing model. The added manufacturing and transportation lead-time puts an increased premium on both accurate and timely forecasting. The Company has developed a suite of applications to facilitate collaborative analysis and forecasting. The specialty retailers are faced with strong competition for qualified managers and staff. Managers are time-constrained due to increased labor and inventory demands, margins are increasingly tight due to higher labor and lease costs and customer satisfaction demands are higher than ever before. The Company has developed a range of applications that enable managers in specialty retail to improve their labor scheduling efficiency and reduce their total paperwork and administrative workload.

Benefits of our Solutions and Services

Our Supply Chain services bring unique visibility to the consumer goods supply chain, delivering actionable information that ensures product is on the shelf when the consumer expects it. Our service increases our customers’ sales and profitability while enabling lower inventory levels for both retailers and their suppliers.

Key advantages of our solutions include:

|

●

|

synchronizing retailers and suppliers so they can actually exchange information;

|

|

●

|

aligning their financial interests with payment and invoicing protocols and systems;

|

|

●

|

enlisting brain power of suppliers to help retailers manage complex businesses;

|

|

●

|

providing information to each side to identify and fix out of stocks and overstocks;

|

|

●

|

providing forecasting technology to improve store orders;

|

|

●

|

providing forecasting to help suppliers replenish retailer warehouses;

|

|

●

|

providing systems for suppliers to actually manage inventory flow to retailers; and

|

|

●

|

helping suppliers with overall demand planning and line sequencing.

|

Ultimately, the Company’s products and services come together to create a true partnership between retailers and suppliers.

Solutions and Services

Solutions

The Company’s primary solutions are Scan Based Trading, ScoreTracker, Vendor Managed Inventory, Store Level Replenishment, Enterprise Supply Chain Planning Suite, Fresh Market Manager and ActionManager®, all of which are designed to aid the retailer and supplier with managing inventory, product mix and labor while improving sales through reduced out of stocks by improving visibility and forecasting.

Scan Based Trading (“SBT”). Our SBT solution eliminates supply chain inefficiencies and helps retailers and suppliers get product to the store shelves more quickly, efficiently and profitably. SBT is an advanced commerce practice where the supplier retains ownership of the inventory until it scans at the cash register. Once the retailer and supplier have agreed to begin an SBT relationship, the first step is item and price authorization. This process matches retailer and supplier product data to eliminate invoice discrepancies at the point of sale. Our SBT system receives the scan sales data and maintains it in a repository to ensure that product movement data is available to all members of the trading community. Implementation creates increased demand visibility and improved forecast accuracy. Our SBT solution is offered as a hosted service, so implementation is immediate and always available.

ScoreTracker. Our ScoreTracker solution gives retailers and suppliers a clear view into critical aspects of their supply chain operations so that they can better serve the consumer. This visibility solution provides analysis of scan sales data by store, by day and by category. Retailers and suppliers better understand what is selling, the velocity at which a product is moving and how profitable it is. In addition, our solution helps analyze shrink and how to use that information to prevent out of stocks. This tool is provided to retailers and suppliers who provide additional data inputs valuable to operating their business such as routes, returns and credits. The ScoreTracker solution enables a true collaborative view to the Key Performance Indicators (“KPI’s”) for both retailers and suppliers. The Company is a neutral third party between the trading partners and the retailer and ScoreTracker delivers a trusted view to performance and actionable insights with respect to improving sales and item performance and reducing operational and shrink costs.

Vendor-Managed Inventory (“VMI”). VMI programs are gaining in popularity because suppliers have come to realize that VMI offers the opportunity to better align themselves with their trading partners and add value to those relationships. Our VMI solution provides collaborative tools that increase supply chain efficiencies, lower inventory and enhance trading partner relationships. The solution is pre-mapped to the specific requirements of each trading partner for the transfer of electronic data directly into our system. This enables suppliers to analyze retailer-supplied demand information, automatically generate orders for each customer, set inventory policy at the retailer’s distribution center and monitor on-going inventory levels, determine which items need to be replenished, and how to ship them most cost-effectively. Our VMI suite has the flexibility and functionality to scale to accommodate new trading partners. Our solution delivers real value for suppliers through fewer out-of-stocks, increased inventory turns, and increased customer satisfaction and loyalty.

Store Level Replenishment (“SLR”). Many retailers are shifting the responsibility of replenishing product at the store shelf onto the suppliers who bring that product into the store. Avoiding overstocks and understocks, particularly with highly promoted products such as ice cream or bread, has been a challenge for DSD suppliers. Our on-demand SLR solution provides these suppliers visibility into store level movement and activity, and generates replenishment orders based on point of sale data. Suppliers using this solution are able to optimize store-level demand forecasting and replenishment, resulting in fewer out of stocks and lost sales. Retailers benefit by having product on the shelf.

Enterprise Supply Chain Planning Suite (“ESCP”). Our ESCP suite includes a solution to help users analyze point of service data and other demand signals to gain insight into customer demand. Suppliers have visibility into historical data – seasonal events, promotions and buying trends – to facilitate accurate forecasting. Our software assesses how inventory will be impacted, then calculates recommended stocking levels, considers service level goals and develops a time-phased replenishment plan. The solution brings demand data into one place where users can easily manage the complex sets of data and parameters that impact their businesses, including seasonal builds, desired service levels, and manufacturing constraints. ESCP considers consumption rates and inventory levels and automatically calculates time-phase safety stocks and replenishment quantities while being extremely flexible and can be configured to meet the needs of any company’s supply chain processes.

The Company also offers a variety of other solutions that address the unique needs of its customers.

Fresh Market Manager. Addressing the inventory issues that plague today’s retailers, Fresh Market Manager is a suite of software product applications designed to help manage perishable food departments including bakery, deli, seafood, produce, meat, home meal replacement, dairy, frozen food, and floral. Fresh Market Manager helps identify true cost of goods and provides accurate and actionable profitability data on a corporate, regional, store-by-store and/or item-by-item basis. Fresh Market Manager also produces hour-by-hour forecasts, production plans, perpetual inventory and placed/received orders. Fresh Market Manager automates the majority of the planning, forecasting, ordering and administrative functions associated with fresh merchandise or products.

ActionManager®. The second most important cost element typically facing today’s retailers is labor. ActionManager® addresses labor needs by providing a suite of solutions that forecast labor demand, schedules staff resources and provides store managers with the necessary tools to keep labor costs under control while improving customer service, satisfaction, and sales. ActionManager® applications provide an automated method for managers to plan, schedule and administer many administrative tasks including new hire, time and attendance paperwork. In addition to automating most administrative processes, ActionManager® provides the local manager with a “dashboard” view of the business. ActionManager® also has extensive reporting capabilities for corporate, field and store-level management to enable improved decision support.

ReposiTrak™. ReposiTrak provides a document management service that provides visibility to insurance and indemnification documents, reports, audits, etc. for every facility in the connected supply chain, all in a single location through its web-based application. It also provides a targeted solution for improving supply chain visibility for food and drug safety. ResposiTrak’s solution, similarly called ReposiTrak™, is powered by the Company’s technology and was developed in response to the passage of the Food Safety and Modernization Act in January of 2012. ReposiTrak™ enables grocery, supermarkets, packaged goods manufacturers, food processing facilities, drug stores and drug manufacturers, as well as logistics partners, to track and trace products and components to products throughout the food, drug and dietary supplement supply chains. In the event of a product recall, the solution quickly identifies the supply chain path taken by the recalled product or product component, and allows for the removal of affected products in a matter of minutes, rather than weeks. Additionally, ReposiTrak™ reduces risk of further contamination in the supply chain by identifying backward chaining sources and forward chaining recipients of affected products in near real time.

Services

Business Analytics. Park City Group’s Business Analytics Group offers business-consulting services to suppliers and retailers in the grocery, convenience store and specialty retail industries. The Business Analytics Group mines store-level scan data to develop item-specific recommendations to improve customer satisfaction and profitability.

Professional Services. Our Professional Services Group provides consulting services to ensure that our solutions are seamlessly integrated into our customers’ business processes as quickly and efficiently as possible. In addition to implementation of our solutions, we have developed a portfolio of service offerings designed to deliver unparalleled performance throughout the lifecycle of the customer’s solution. Specific services are tailored to each customer and include the following: implementation, business optimization, technical services, education, business process outsourcing and advisory services. The intent of such services is to support our clients’ business operations by enabling them to maximize the speed, effectiveness and overall value of our offerings. We believe the ability to create value for our customers is critical to our long-term success.

Technology, Development and Operations

Product Development

The products sold by the Company are subject to rapid and continual technological change. Products available from the Company, as well as from its competitors, increasingly offer a wider range of features and capabilities. The Company believes that in order to compete effectively in its selected markets, it must provide compatible systems incorporating new technologies at competitive prices. In order to achieve this, the Company has made a substantial commitment to on-going development.

Our product development strategy is focused on creating common technology elements that can be leveraged in applications across our core markets. Except for its supply chain application, which is based on a proprietary architecture, the Company’s software architecture is based on open platforms and is modular, thereby allowing it to be phased into a customer’s operations. In order to remain competitive, we are currently designing, coding and testing a number of new products and developing expanded functionality of our current products.

Operations

We currently serve our customers from a third-party data center hosting facility. Along with the Company’s Statement on Standards for Attestation Engagements (“SSAE”) No. 16 certification Service Organization Control (“SOC2”), the third-party facility is also a SSAE No. 16 – SOC2 certified location and is secured by around-the-clock guards, biometric screening and escort-controlled access, and is supported by on-site backup generators in the event of a power failure. As part of our current disaster recovery arrangements, all of our customers’ data is currently backed-up in near real-time. This strategy is designed to protect our customers’ data and ensure service continuity in the event of a major disaster. Even with the disaster recovery arrangements, our service could be interrupted.

Customers

We sell to business of all sizes. Our customers primarily include food related consumer goods retailers, suppliers and manufacturers. However, the Company is opportunistic and will offer its supply chain solutions to non-food consumer goods related companies as well. None of our retailing or supplier customers accounted for more than 10% percent of our revenue in fiscal 2015 or 2014. Prior to the ReposiTrak Acquisition, our contractual relationship with ReposiTrak generated approximately $3.0 million in subscription and management fees during 2015, which amount constituted approximately 21% of the Company’s total revenue in 2015.

Sales, Marketing and Customer Support

Sales and Marketing

Through a focused and dedicated sales effort designed to address the requirements of each of its software and service solutions, we believe our sales force is positioned to understand our customers’ businesses, trends in the marketplace, competitive products and opportunities for new product development. Our deep industry knowledge enables the Company to take a consultative approach in working with our prospects and customers. Our sales personnel focus on selling our technology solutions to major customers, both domestically and internationally.

To date, our primary marketing objectives have been to increase awareness of our technology solutions, generate sales leads and develop new customer relationships. In addition, the sales effort has been directed toward developing existing customers by cross-selling Prescient solutions to legacy Park City Group accounts as well as introducing Park City Group solutions to legacy Prescient customers. To this end, we attend industry trade shows, conduct direct marketing programs, publish industry trade articles and white papers, participate in interviews and selectively advertise in industry publications.

Customer Support

Our global customer support group responds to both business and technical inquiries from our customers relating to how to use our products and is available to customers by telephone and email. Basic customer support during business hours is available at no charge to customers who purchase certain Company solutions. Premier customer support includes extended availability and additional services, such as an assigned support representative and/or administrator. Premier customer support is available for an additional fee. Additional support services include developer support and partner support.

Competition

The market for the Company’s products and services is very competitive. We believe the principal competitive factors include product quality, reliability, performance, price, vendor and product reputation, financial stability, features and functions, ease of use, quality of support and degree of integration effort required with other systems. While our competitors are often considerably larger companies in size with larger sales forces and marketing budgets, we believe that our deep industry knowledge and the breadth and depth of our offerings give us a competitive advantage. Our ability to continually improve our products, processes and services, as well as our ability to develop new products, enables the Company to meet evolving customer requirements. We compete with large enterprise-wide software vendors, developers and integrators, business-to-business exchanges, consulting firms, focused solution providers, and business intelligence technology platforms. Our supply chain solution competitors include supply chain vendors, major enterprise resource planning (“ERP”) software vendors, mid-market ERP vendors and niche players for VMI and SLR.

Patents and Proprietary Rights

The Company relies on a combination of trademark, copyright, trade secret and patent laws in the United States and other jurisdictions as well as confidentiality procedures and contractual provisions to protect our proprietary technology and our name. We also enter into confidentiality agreements with our employees, consultants and other third parties and control access to software, documentation and other proprietary information.

The Company has been awarded nine U.S. patents, eight U.S. registered trademarks and has 37 U.S. copyrights relating to its software technology and solutions. The Company’s patent portfolio has been transferred to an unrelated third party, although the Company retains the right to use the licensed patents in connection with its business. However, Company policy is to continue to seek patent protection for all developments, inventions and improvements that are patentable and have potential value to the Company and to protect its trade secrets and other confidential and proprietary information. The Company intends to vigorously defend its intellectual property rights to the extent its resources permit.

The Company is not aware of any patent infringement claims against it; however, there are no assurances that litigation to enforce patents issued to the Company to protect proprietary information, or to defend against the Company’s alleged infringement of the rights of others will not occur. Should any such litigation occur, the Company may incur significant litigation costs, Company resources may be diverted from other planned activities, and while the outcome of any litigation is inherently uncertain, any litigation result may cause a materially adverse effect on the Company’s operations and financial condition. Any intellectual property claims, with or without merit, could be time-consuming and expensive to resolve, could divert management attention from executing our business plan and could require us to alter our technology, change our business methods and/or pay monetary damages or enter into licensing agreements.

Employees

As of June 30, 2015, the Company employed a total of 68 employees, including 10 software developers and programmers, 19 sales, marketing and account management employees, 19 software service and support employees, 3 network operations employees and 7 accounting and administrative employees. During 2015, the Company contracted with 8 programmers and 2 business analysts overseas. The Company plans to continue expanding its offshore workforce to augment its analytics services offerings, expand its professional services and to provide additional programming resources. The employees are not represented by any labor union.

Reports to Security Holders

The Company is subject to the informational requirements of the Securities Exchange Act of 1934. Accordingly, it files annual, quarterly and other reports and information with the Securities and Exchange Commission. You may read and copy these reports and other information at the Securities and Exchange Commission's public reference rooms in Washington, D.C. and Chicago, Illinois. The Company’s filings are also available to the public from commercial document retrieval services and the website maintained by the Securities and Exchange Commission at http://www.sec.gov.

Government Regulation and Approval

Like all businesses, the Company is subject to numerous federal, state and local laws and regulations, including regulations relating to patent, copyright, and trademark law matters.

Cost of Compliance with Environmental Laws

The Company currently has no costs associated with compliance with environmental regulations, and does not anticipate any future costs associated with environmental compliance; however, there can be no assurance that it will not incur such costs in the future.

|

ITEM 1A.

|

RISK FACTORS

|

An investment in our common stock is subject to many risks. You should carefully consider the risks described below, together with all of the other information included in this Annual Report on Form 10-K, including the financial statements and the related notes, before you decide whether to invest in our common stock. Our business, operating results and financial condition could be harmed by any of the following risks. The trading price of our common stock could decline due to any of these risks, and you could lose all or part of your investment.

Risks Related to the Company

The Company has incurred losses in the past and there can be no assurance that the Company will operate profitably in the future.

The Company’s marketing strategy emphasizes sales of subscription-based services, instead of annual licenses, and contracting with suppliers (“spokes”) to connect to our clients (“hubs”). This strategy has resulted in the development of a foundation of hubs to which suppliers can be “connected”, thereby accelerating future growth. If, however, this marketing strategy fails, revenue and operations will be negatively affected.

The Company had a net loss of $3,849,773 for the year ended June 30, 2015, compared to a net loss of $2,490,145 for the year ended June 30, 2014. There can be no assurance that the Company will achieve profitability in future periods. If the Company does not operate profitably in the future, the Company’s current cash resources will be used to fund the Company’s operating losses. Continued losses would have an adverse effect on the long-term value of the Company’s common stock and any investment in the Company. The Company cannot give any assurance that the Company will continue to generate revenue or have sustainable profits.

Although the Company’s cash resources are currently sufficient, the Company’s long-term liquidity and capital requirements may be difficult to predict, which may adversely affect the Company’s long-term cash position.

Historically, the Company has been successful in raising capital when necessary, including private placements, a registered direct offering, and stock issuances from its officers and directors, including its Chief Executive Officer and majority stockholder, in order to pay its indebtedness and fund its operations, in addition to cash flow from operations. As a result of the consummation of the registered direct offering on April 15, 2015, resulting in net proceeds of approximately $6.7 million, the Company anticipates that it will have adequate cash resources to fund its operations and satisfy its debt obligations for at least the next 12 months.

If the Company is required to seek additional financing in the future in order to fund its operations, retire its indebtedness and otherwise carry out its business plan, there can be no assurance that such financing will be available on acceptable terms, or at all, and there can be no assurance that any such arrangement, if required or otherwise sought, would be available on terms deemed to be commercially acceptable and in the Company’s best interests.

Quarterly and annual operating results may fluctuate, which makes it difficult to predict future performance.

Management expects a significant portion of the Company’s revenue stream to come from the sale of subscriptions, and to a lesser extent, license sales, maintenance and services charged to new customers. These amounts will fluctuate because predicting future sales is difficult and involves speculation. In addition, the Company may potentially experience significant fluctuations in future operating results caused by a variety of factors, many of which are outside of its control, including:

|

●

|

our ability to retain and increase sales to existing customers, attract new customers and satisfy our customers' requirements;

|

|

●

|

the renewal rates for our service;

|

|

●

|

the amount and timing of operating costs and capital expenditures related to the operations and expansion of our business;

|

|

●

|

changes in our pricing policies whether initiated by us or as a result of competition;

|

|

●

|

the cost, timing and management effort for the introduction of new features to our service;

|

|

●

|

the rate of expansion and productivity of our sales force;

|

|

●

|

new product and service introductions by our competitors;

|

|

●

|

variations in the revenue mix of editions or versions of our service;

|

|

●

|

technical difficulties or interruptions in our service;

|

|

●

|

general economic conditions that may adversely affect either our customers' ability or willingness to purchase additional subscriptions or upgrade their service, or delay a prospective customers' purchasing decision, or reduce the value of new subscription contracts or affect renewal rates;

|

|

●

|

timing of additional investments in our enterprise cloud computing application and platform services and in our consulting service;

|

|

●

|

regulatory compliance costs;

|

|

●

|

the timing of customer payments and payment defaults by customers;

|

|

●

|

extraordinary expenses such as litigation or other dispute-related settlement payments;

|

|

●

|

the impact of new accounting pronouncements; and

|

|

●

|

the timing of stock awards to employees and the related financial statement impact.

|

Future operating results may fluctuate because of the foregoing factors, making it difficult to predict operating results. Period-to-period comparisons of operating results are not necessarily meaningful and should not be relied upon as an indicator of future performance. In addition, a relatively large portion of the Company’s expenses will be fixed in the short-term, particularly with respect to facilities and personnel. Therefore, future operating results will be particularly sensitive to fluctuations in revenue because of these and other short-term fixed costs.

The Company will need to effectively manage its growth in order to achieve and sustain profitability. The Company’s failure to manage growth effectively could reduce its sales growth and result in continued net losses.

To achieve continual and consistent profitable operations on a fiscal year on-going basis, the Company must have significant growth in its revenue from its products and services, specifically subscription-based services. If the Company is able to achieve significant growth in future subscription sales, and expands the scope of its operations, the Company’s management, financial condition, operational capabilities, and procedures and controls could be strained. The Company cannot be certain that its existing or any additional capabilities, procedures, systems, or controls will be adequate to support the Company’s operations. The Company may not be able to design, implement or improve its capabilities, procedures, systems or controls in a timely and cost-effective manner. Failure to implement, improve and expand the Company’s capabilities, procedures, systems or controls in an efficient and timely manner could reduce the Company’s sales growth and result in a reduction of profitability or increase of net losses.

The Company’s officers and directors have significant control over it, which may lead to conflicts with other stockholders over corporate governance.

The Company’s officers and directors, including our Chief Executive Officer, Randall K. Fields, control approximately 37.8% of the Company’s common stock. Mr. Fields, individually, controls 30.4% of the Company’s common stock. Consequently, Mr. Fields individually, and the Company’s officers and directors, as stockholders acting together, are able to significantly influence all matters requiring approval by the Company’s stockholders, including the election of directors and significant corporate transactions, such as mergers or other business combination transactions.

The Company’s corporate charter contains authorized, unissued “blank check” preferred stock issuable without stockholder approval with the effect of diluting then current stockholder interests.

The Company’s certificate of incorporation currently authorizes the issuance of up to 30,000,000 shares of ‘blank check’ preferred stock with designations, rights, and preferences as may be determined from time to time by the Company’s Board of Directors, of which 700,000 shares are currently designated as Series B Preferred and 300,000 shares are designated as Series B-1 Preferred. As of June 30, 2015, a total of 625,375 shares of Series B Preferred and 74,200 shares of Series B-1 Preferred were issued and outstanding. The Company’s board of directors is empowered, without stockholder approval, to issue one or more additional series of preferred stock with dividend, liquidation, conversion, voting, or other rights that could dilute the interest of, or impair the voting power of, the Company’s common stockholders. The issuance of an additional series of preferred stock could be used as a method of discouraging, delaying or preventing a change in control.

Because the Company has never paid dividends on its common stock, investors should exercise caution before making an investment in the Company.

The Company has never paid dividends on its common stock and does not anticipate the declaration of any dividends pertaining to its common stock in the foreseeable future. The Company intends to retain earnings, if any, to finance the development and expansion of the Company’s business. The Company’s board of directors will determine future dividend policy at their sole discretion and future dividends will be contingent upon future earnings, if any, obligations of the stock issued, the Company’s financial condition, capital requirements, general business conditions and other factors. Future dividends may also be affected by covenants contained in loan or other financing documents, which may be executed by the Company in the future. Therefore, there can be no assurance that dividends will ever be paid on its common stock.

The Company’s business is dependent upon the continued services of the Company’s founder and Chief Executive Officer, Randall K. Fields; should the Company lose the services of Mr. Fields, the Company’s operations will be negatively impacted.

The Company’s business is dependent upon the expertise of its founder and Chief Executive Officer, Randall K. Fields. Mr. Fields is essential to the Company’s operations. Accordingly, an investor must rely on Mr. Fields’ management decisions that will continue to control the Company’s business affairs. The Company currently maintains key man insurance on Mr. Fields’ life in the amount of $5,000,000; however, that coverage would be inadequate to compensate for the loss of his services. The loss of the services of Mr. Fields would have a materially adverse effect upon the Company’s business.

If the Company is unable to attract and retain qualified personnel, the Company may be unable to develop, retain or expand the staff necessary to support its operational business needs.

The Company’s current and future success depends on its ability to identify, attract, hire, train, retain and motivate various employees, including skilled software development, technical, managerial, sales, marketing and customer service personnel. Competition for such employees is intense and the Company may be unable to attract or retain such professionals. If the Company fails to attract and retain these professionals, the Company’s revenue and expansion plans may be negatively impacted.

The Company’s officers and directors have limited liability and indemnification rights under the Company’s organizational documents, which may impact its results.

The Company’s officers and directors are required to exercise good faith and high integrity in the management of the Company’s affairs. The Company’s certificate of incorporation and bylaws, however, provide, that the officers and directors shall have no liability to the stockholders for losses sustained or liabilities incurred which arise from any transaction in their respective managerial capacities unless they violated their duty of loyalty, did not act in good faith, engaged in intentional misconduct or knowingly violated the law, approved an improper dividend or stock repurchase or derived an improper benefit from the transaction. As a result, an investor may have a more limited right to action than he would have had if such a provision were not present. The Company’s certificate of incorporation and bylaws also require it to indemnify the Company’s officers and directors against any losses or liabilities they may incur as a result of the manner in which they operate the Company’s business or conduct the Company’s internal affairs, provided that the officers and directors reasonably believe such actions to be in, or not opposed to, the Company’s best interests, and their conduct does not constitute gross negligence, misconduct or breach of fiduciary obligations.

Risks Related to the ReposiTrak

The Company faces risks associated with new product introductions of ReposiTrak™.

The first installations of ReposiTrak™ began in August 2012, and market and product data related to these implementations is still being analyzed. The Company also continually receives and analyzes market and product data on other products, and the Company may endeavor to develop and commercialize new product offerings based on this data. The following risks apply to ReposiTrak™ and other potential new product offerings:

|

●

|

it may be difficult for the Company to predict the amount of service and technological resources that will be needed by customers of ReposiTrak™ or other new offerings, and if the Company underestimates the necessary resources, the quality of its service will be negatively impacted thereby undermining the value of the product to the customer;

|

|

●

|

the Company lacks experience with ReposiTrak™ and the market acceptance to accurately predict if it will be a profitable product;

|

|

●

|

technological issues between the Company and customers may be experienced in capturing data, and these technological issues may result in unforeseen conflicts or technological setbacks when implementing additional installations of ReposiTrak™. This may result in material delays and even result in a termination of the ReposiTrak™ engagement;

|

|

●

|

the customer’s experience with ReposiTrak™ and other new offerings, if negative, may prevent the Company from having an opportunity to sell additional products and services to that customer;

|

|

●

|

if customers do not use ReposiTrak™ as the Company recommends and fails to implement any needed corrective action(s), it is unlikely that customers will experience the business benefits from the software service and may therefore be hesitant to continue the engagement as well as acquire any additional software services from the Company; and

|

|

●

|

delays in proceeding with the implementation of ReposiTrak™ or other new products for a new customer will negatively affect the Company’s cash flow and its ability to predict cash flow.

|

Approximately 21% of our total revenue during 2015 was attributable to ReposiTrak. In the event the market for ReposiTrak’s services fails to develop as anticipated, or ReposiTrak is otherwise unable to execute its business plan, our financial condition and results of operations may be materially and adversely affected.

The Company recognized approximately $3.0 million in subscription and management fees during the year ended June 30, 2015 from its contractual relationship with ReposiTrak prior to the ReposiTrak Acquisition, which amount constituted approximately 21% of the Company’s total revenue in 2015. Approximately $2.3 million net was advanced to ReposiTrak for working capital purposes during the year ended June 30, 2015, which amount was evidenced by the issuance of promissory notes by ReposiTrak to the Company. The notes were eliminated in connection with the consolidation of ReposiTrak following the ReposiTrak Acquisition. In the event the market for ReposiTrak’s services fails to develop as anticipated, or ReposiTrak is otherwise unable to execute its business plan, the Company’s financial results, including its financial condition, may be adversely and materially affected.

If our products do not perform as expected, whether as a result of operator error or otherwise, it would impair our operating results and reputation.

Our success depends on the food safety market’s confidence that we can provide reliable, high-quality reporting for our customers. We believe that our customers are likely to be particularly sensitive to product defects and operator errors, including if our systems fail to accurately report issues that could reduce the liability of our clients in the event of a product recall. In addition, our reputation and the reputation of our products can be adversely affected if our systems fail to perform as expected.

However, if our customers or potential customers fail to implement and use our systems as suggested by us, they may not be in a position to deal with a recall as effectively as they could have. As a result, the failure or perceived failure of our products to perform as expected, could have a material adverse effect on our revenue, results of operations and business.

If a customer is sued because of a recalled product we could be joined in that suit, the defense of which would impair our operating results.

A customer which is a defendant in a product liability case could claim that had our services performed as represented the extent of potential liability would have been minimized and therefore the Company should have some contributory liability in the case. Defending such a claim could have a material adverse effect on our revenue, results of operations and business.

Business Operations Risks

If the Company’s marketing strategy fails, its revenue and operations will be negatively affected.

The Company plans to concentrate its future sales efforts towards marketing the Company’s applications and services, and specifically to contract with suppliers (“spokes”) to connect to our existing retail customers (“hubs”) previously signed up by the Company. These applications and services are designed to be highly flexible so that they can work in multiple retail and supplier environments such as grocery stores, convenience stores, specialty retail and route-based delivery environments. There is no assurance that the public will accept the Company’s applications and services in proportion to the Company’s increased marketing of this product line, or that the Company will be able to successfully leverage its hubs to increase revenue by connecting suppliers. The Company may face significant competition that may negatively affect demand for its applications and services, including the public’s preference for the Company’s competitors’ new product releases or updates over the Company’s releases or updates. If the Company’s applications and services marketing strategies fail, the Company will need to refocus its marketing strategy toward other product offerings, which could lead to increased development and marketing costs, delayed revenue streams, and otherwise negatively affect the Company’s operations.

Because the Company’s emphasis is on the sale of subscription based services, rather than annual license fees, the Company’s revenue may be negatively affected.

Historically, the Company offered applications and related maintenance contracts to new customers for a one-time, non-recurring up front license fee and provided an option for annually renewing their maintenance agreements. The Company is now principally offering prospective customers monthly subscription based licensing of its products. The Company’s customers may now choose to acquire a license to use the software on an Application Solution Provider basis (also referred to as “ASP”) resulting in monthly charges for use of the Company’s software products and maintenance fees. The Company’s conversion from a strategy of one-time, non-recurring licensing based model to a monthly recurring fees based approach is subject to the following risks:

|

●

|

the Company’s customers may prefer one-time fees rather than monthly fees; and

|

|

●

|

there may be a threshold level (number of locations) at which the monthly based fee structure may not be economical to the customer, and a request to convert from monthly fees to an annual fee could occur.

|

The Company faces threats from competing and emerging technologies that may affect its profitability.

Markets for the Company’s type of software products and that of its competitors are characterized by:

|

●

|

development of new software, software solutions or enhancements that are subject to constant change;

|

|

●

|

rapidly evolving technological change; and

|

|

●

|

unanticipated changes in customer needs.

|

Because these markets are subject to such rapid change, the life cycle of the Company’s products is difficult to predict. As a result, the Company is subject to the following risks:

|

●

|

whether or how the Company will respond to technological changes in a timely or cost-effective manner;

|

|

●

|

whether the products or technologies developed by the Company’s competitors will render the Company’s products and services obsolete or shorten the life cycle of the Company’s products and services; and

|

|

●

|

whether the Company’s products and services will achieve market acceptance.

|

Interruptions or delays in service from our third-party data center hosting facility could impair the delivery of our service and harm our business.

We currently serve our customers from a third-party data center hosting facility located in the United States. Any damage to, or failure of, our systems generally could result in interruptions in our service. As we continue to add capacity, we may move or transfer our data and our customers' data. Despite precautions taken during this process, any unsuccessful data transfers may impair the delivery of our service. Further, any damage to, or failure of, our systems generally could result in interruptions in our service. Interruptions in our service may reduce our revenue, cause us to issue credits or pay penalties, cause customers to terminate their subscriptions and adversely affect our renewal rates and our ability to attract new customers. Our business will also be harmed if our customers and potential customers believe our service is unreliable.

As part of our current disaster recovery arrangements, our production environment and all of our customers' data is currently replicated in near real-time in a separate facility physically located in a different geographic region of the United States. Companies and products added through acquisition may be temporarily served through an alternate facility. We do not control the operation of these facilities, and they are vulnerable to damage or interruption from earthquakes, floods, fires, power loss, telecommunications failures and similar events. They may also be subject to break-ins, sabotage, intentional acts of vandalism and similar misconduct. Despite precautions taken at these facilities, the occurrence of a natural disaster or an act of terrorism, a decision to close the facilities without adequate notice or other unanticipated problems at these facilities could result in lengthy interruptions in our service. Even with the disaster recovery arrangements, our service could be interrupted.

If our security measures are breached and unauthorized access is obtained to a customer's data, our data or our information technology systems, our service may be perceived as not being secure, customers may curtail or stop using our service and we may incur significant legal and financial exposure and liabilities.

Our service involves the storage and transmission of customers' proprietary information, and security breaches could expose us to a risk of loss of this information, litigation and possible liability. These security measures may be breached as a result of third-party action, including intentional misconduct by computer hackers, employee error, malfeasance or otherwise during transfer of data to additional data centers or at any time, and result in someone obtaining unauthorized access to our customers' data or our data, including our intellectual property and other confidential business information, or our information technology systems. Additionally, third parties may attempt to fraudulently induce employees or customers into disclosing sensitive information such as user names, passwords or other information in order to gain access to our customers' data or our data, including our intellectual property and other confidential business information, or our information technology systems. Because the techniques used to obtain unauthorized access, or to sabotage systems, change frequently and generally are not recognized until launched against a target, we may be unable to anticipate these techniques or to implement adequate preventative measures. Any security breach could result in a loss of confidence in the security of our service, damage our reputation, disrupt our business, lead to legal liability and negatively impact our future sales.

We cannot accurately predict subscription renewal or upgrade rates and the impact these rates may have on our future revenue and operating results.

Our customers have no obligation to renew their subscriptions for our service after the expiration of their initial subscription period. Our renewal rates may decline or fluctuate as a result of a number of factors, including customer dissatisfaction with our service, customers' ability to continue their operations and spending levels, and deteriorating general economic conditions. If our customers do not renew their subscriptions for our service or reduce the level of service at the time of renewal, our revenue will decline and our business will suffer.

Our future success also depends in part on our ability to sell additional features and services, more subscriptions or enhanced editions of our service to our current customers. This may also require increasingly sophisticated and costly sales efforts that are targeted at senior management. Similarly, the rate at which our customers purchase new or enhanced services depends on a number of factors, including general economic conditions. If our efforts to upsell to our customers are not successful, our business may suffer.

Weakened global economic conditions may adversely affect our industry, business and results of operations.

Our overall performance depends in part on worldwide economic conditions. The United States and other key international economies have experienced in the past a downturn in which economic activity was impacted by falling demand for a variety of goods and services, restricted credit, poor liquidity, reduced corporate profitability, volatility in credit, equity and foreign exchange markets, bankruptcies and overall uncertainty with respect to the economy. These conditions affect the rate of information technology spending and could adversely affect our customers' ability or willingness to purchase our enterprise cloud computing services, delay prospective customers' purchasing decisions, reduce the value or duration of their subscription contracts or affect renewal rates, all of which could adversely affect our operating results.

If the Company is unable to adapt to constantly changing markets and to continue to develop new products and technologies to meet the customers’ needs, the Company’s revenue and profitability will be negatively affected.

The Company’s future revenue is dependent upon the successful and timely development and licensing of new and enhanced versions of its products and potential product offerings suitable to the customer’s needs. If the Company fails to successfully upgrade existing products and develop new products, and those new products do not achieve market acceptance, the Company’s revenue will be negatively impacted.

The Company faces risks associated with the loss of maintenance and other revenue.

The Company has historically experienced the loss of long-term maintenance customers as a result of the reliability of some of its products. Some customers may not see the value in continuing to pay for maintenance that they do not need or use, and in some cases, customers have decided to replace the Company’s applications or maintain the system on their own. The Company continues to focus on these maintenance clients by providing new functionality and enhancements to meet their business needs. The Company also may lose some maintenance revenue due to consolidation of industries, macroeconomic conditions or customer operational difficulties that lead to their reduction of size. In addition, future revenue will be negatively impacted if the Company fails to add new maintenance customers that will make additional purchases of the Company’s products and services.

The Company faces risks associated with proprietary protection of the Company’s software.

The Company’s success depends on the Company’s ability to develop and protect existing and new proprietary technology and intellectual property rights. The Company seeks to protect its software, documentation and other written materials primarily through a combination of patents, trademarks, and copyright laws, trade secret laws, confidentiality procedures and contractual provisions. While the Company has attempted to safeguard and maintain the Company’s proprietary rights, there are no assurances that the Company will be successful in doing so. The Company’s competitors may independently develop or patent technologies that are substantially equivalent or superior to the Company’s.

Despite the Company’s efforts to protect its proprietary rights, unauthorized parties may attempt to copy aspects of the Company’s products or obtain and use information that the Company regards as proprietary. In some types of situations, the Company may rely in part on ‘shrink wrap’ or ‘point and click’ licenses that are not signed by the end user and, therefore, may be unenforceable under the laws of certain jurisdictions. Policing unauthorized use of the Company’s products is difficult. While the Company is unable to determine the extent to which piracy of the Company’s software exists, software piracy can be expected to be a persistent problem, particularly in foreign countries where the laws may not protect proprietary rights as fully as the United States. The Company can offer no assurance that the Company’s means of protecting its proprietary rights will be adequate or that the Company’s competitors will not reverse engineer or independently develop similar technology.

The Company may discover software errors in its products that may result in a loss of revenue, injury to the Company’s reputation or subject us to substantial liability.

Non-conformities or bugs (“errors”) may be found from time to time in the Company’s existing, new or enhanced products after commencement of commercial shipments, resulting in loss of revenue or injury to the Company’s reputation. In the past, the Company has discovered errors in its products and as a result, has experienced delays in the shipment of products. Errors in the Company’s products may be caused by defects in third-party software incorporated into the Company’s products. If so, the Company may not be able to fix these defects without the cooperation of these software providers. Since these defects may not be as significant to the software provider as they are to us, the Company may not receive the rapid cooperation that may be required. The Company may not have the contractual right to access the source code of third-party software, and even if the Company does have access to the code, the Company may not be able to fix the defect. In addition, our customers may use our service in unanticipated ways that may cause a disruption in service for other customers attempting to access their data. Since the Company’s customers use the Company’s products for critical business applications, any errors, defects or other performance problems could hurt the Company’s reputation and may result in damage to the Company’s customers’ business. If that occurs, customers could elect not to renew, delay or withhold payment to us, we could lose future sales or customers may make warranty or other claims against us, which could result in an increase in our provision for doubtful accounts, an increase in collection cycles for accounts receivable or the expense and risk of litigation. These potential scenarios, successful or otherwise, would likely be time consuming and costly.

Some competitors are larger and have greater financial and operational resources that may give them an advantage in the market.