Q2 2011 Conference Call

1

ITW Conference Call

Second Quarter

2011

Exhibit 99.2

Q2 2011 Conference Call

2

ITW

Agenda

Agenda

1. Introduction…………………...….. John Brooklier/David Speer

2. Financial Overview…………..….. Ron Kropp

3. Reporting Segments………....…. John Brooklier

4. 2011 Forecasts…..……….….…… Ron Kropp

5. Q & A………………......……...…... John Brooklier/Ron Kropp/David Speer

Q2 2011 Conference Call

3

ITW

Forward - Looking Statements

Forward - Looking Statements

This conference call contains forward-looking statements

within the meaning of the Private Securities Litigation

Reform Act of 1995 including, without limitation, statements

regarding operating performance, revenue growth, diluted

net income per share, restructuring expenses and related

benefits, tax rates, end market conditions, and the

Company’s related 2011 forecasts. These statements are

subject to certain risks, uncertainties, and other factors

which could cause actual results to differ materially from

those anticipated. Important risks that could cause actual

results to differ materially from the Company’s

expectations are detailed in ITW’s Form 10-K for 2010.

within the meaning of the Private Securities Litigation

Reform Act of 1995 including, without limitation, statements

regarding operating performance, revenue growth, diluted

net income per share, restructuring expenses and related

benefits, tax rates, end market conditions, and the

Company’s related 2011 forecasts. These statements are

subject to certain risks, uncertainties, and other factors

which could cause actual results to differ materially from

those anticipated. Important risks that could cause actual

results to differ materially from the Company’s

expectations are detailed in ITW’s Form 10-K for 2010.

Q2 2011 Conference Call

4

Conference Call Playback

Replay number: 402-220-9704

No pass code necessary

Telephone replay available through midnight of

August 9, 2011

August 9, 2011

Webcast / PowerPoint replay available at

www.itw.com

www.itw.com

Q2 2011 Conference Call

ITW

Quarterly Highlights

Quarterly Highlights

Q2 2011 Conference Call

6

ITW

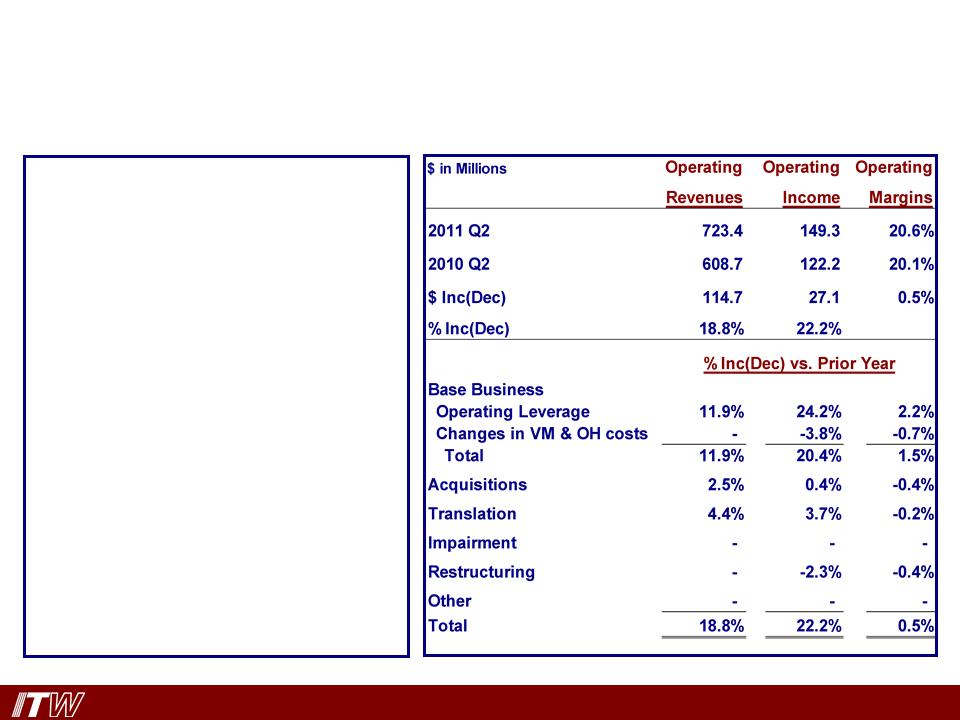

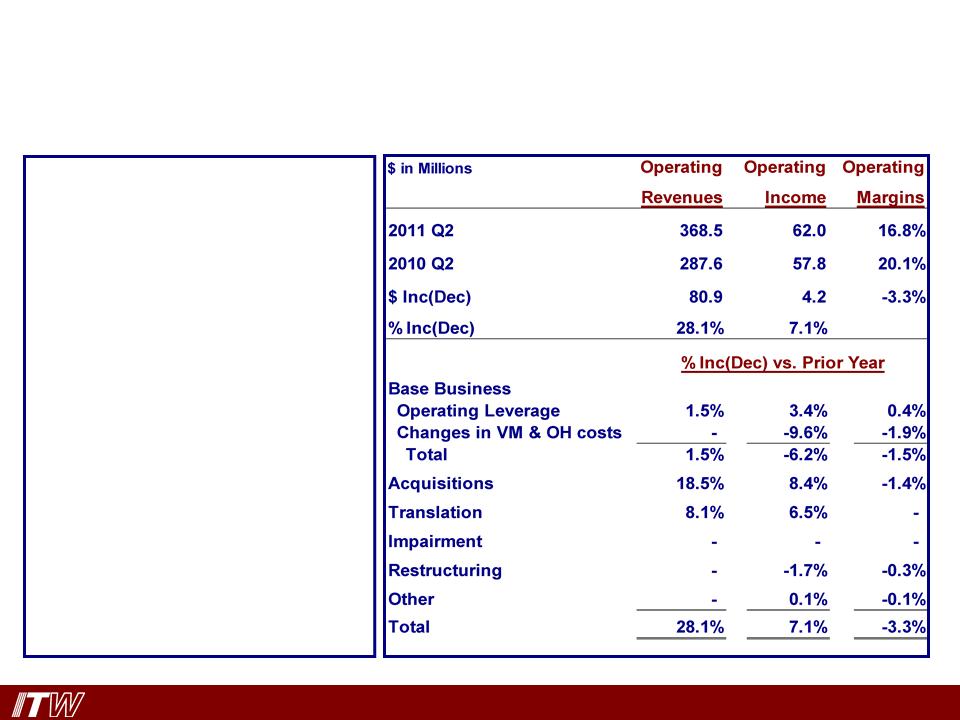

Quarterly Operating Analysis

Quarterly Operating Analysis

Q2 2011 Conference Call

7

ITW

Non Operating & Taxes

Non Operating & Taxes

Q2 2011 Conference Call

8

ITW

Invested Capital

Invested Capital

Q2 2011 Conference Call

9

ITW

Debt & Equity

Debt & Equity

Q2 2011 Conference Call

10

ITW

Cash Flow

Cash Flow

Q2 2011 Conference Call

11

ITW

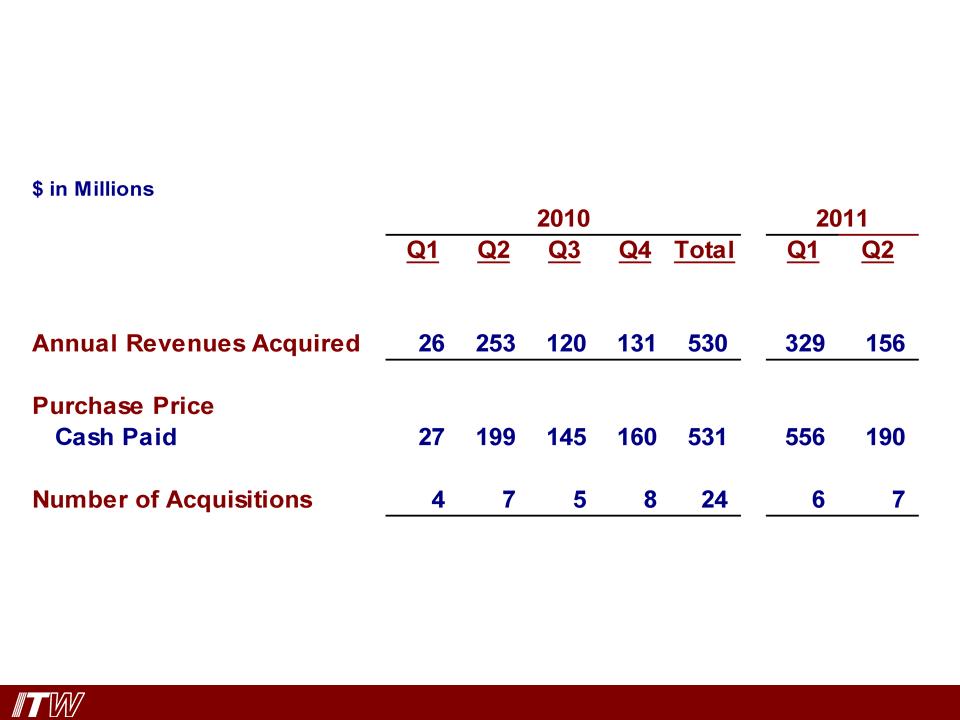

Acquisitions

Acquisitions

Q2 2011 Conference Call

12

Transportation

Quarterly Analysis

Q2 2011

Quarterly Analysis

Q2 2011

Key Points (Q2’11 vs Q2’10)

• Segment organic revenues: +7.4%

• Auto OEM/Tiers: Worldwide base

revenue growth of 7.5%; impacted

modestly by Japan disaster

revenue growth of 7.5%; impacted

modestly by Japan disaster

– North American base revenues:

+6.6% vs. 1% growth in North

America auto builds

+6.6% vs. 1% growth in North

America auto builds

– International base revenues: +8.2%

vs. 4% growth in European auto

builds

vs. 4% growth in European auto

builds

– 2011 full year auto build forecast:

• North America: 12.9 - 13.1 million units

• Europe: 19.8 - 20.0 million units

• Auto aftermarket worldwide base

revenues: modest 1.3% growth due

to rise in gas prices and lower miles

driven

revenues: modest 1.3% growth due

to rise in gas prices and lower miles

driven

Q2 2011 Conference Call

13

Industrial Packaging

Quarterly Analysis

Q2 2011

Quarterly Analysis

Q2 2011

Key Points (Q2’11 vs. Q2’10)

• Segment organic revenues: +9.6%

reflected solid industrial production

activity worldwide

reflected solid industrial production

activity worldwide

– Total North American industrial

packaging base revenues: +11.2%

packaging base revenues: +11.2%

– Total international industrial

packaging base revenues: +7.6%

packaging base revenues: +7.6%

• Worldwide strapping and related

equipment base revenues: +8.8%

equipment base revenues: +8.8%

– North America: +12.9%

– International: +6.2%

• Protective packaging base revenues:

+11.3%

+11.3%

Q2 2011 Conference Call

14

Power Systems and Electronics

Quarterly Analysis

Q2 2011

Quarterly Analysis

Q2 2011

Key Points (Q2’11 vs. Q2’10)

• Segment organic revenues: +11.9%

due to strong contributions from

welding and PC board fabrication

businesses

due to strong contributions from

welding and PC board fabrication

businesses

• Worldwide welding base revenues:

+18.2%

+18.2%

– North America welding base

revenues: +19.9% due to heavy

equipment OEMs and manufacturers

revenues: +19.9% due to heavy

equipment OEMs and manufacturers

– International welding base revenues:

+14.1% as Europe and Asia Pacific

both contributed to organic growth

+14.1% as Europe and Asia Pacific

both contributed to organic growth

• Electronics: +4.1% largely due to

contribution from PC board

fabrication businesses

contribution from PC board

fabrication businesses

Q2 2011 Conference Call

15

Food Equipment

Quarterly Analysis

Q2 2011

Quarterly Analysis

Q2 2011

Key Points (Q2’11 vs. Q2’10)

• Segment organic revenues: +1.9%

as equipment sales moderated

internationally

as equipment sales moderated

internationally

• Total North America base revenues:

+4.2%

+4.2%

– Equipment base revenues: +6.2%

– Service base revenues: +3.0%

• International base revenues:

-0.4%

-0.4%

– Equipment base revenues: -2.8%

– Service base revenues: +2.1%

Q2 2011 Conference Call

16

Construction Products

Quarterly Analysis

Q2 2011

Quarterly Analysis

Q2 2011

Key Points (Q2’11 vs. Q2’10)

• Segment organic revenues: -2.2%

as European growth moderates

and North America remains weak

as European growth moderates

and North America remains weak

• International construction base

revenues: +2.1%

revenues: +2.1%

– Europe base revenues: +6.1%

– Asia Pacific base revenues: -2.8%

• North America construction base

revenues: -10.7%

revenues: -10.7%

– Residential base revenues: -8.1%

– Commercial base revenues: -24.0%

but -5.3% excluding one-time

revenue gain in Q2’10

but -5.3% excluding one-time

revenue gain in Q2’10

– Renovation base revenues: -3.1%

Q2 2011 Conference Call

17

Polymers and Fluids

Quarterly Analysis

Q2 2011

Quarterly Analysis

Q2 2011

Key Points (Q2’11 vs Q2’10)

• Segment organic revenues:

+1.5% reflected moderated

industrial demand for polymer

products in North American and

international end markets; fluid

demand stronger

+1.5% reflected moderated

industrial demand for polymer

products in North American and

international end markets; fluid

demand stronger

• Worldwide polymers: Flat

• Worldwide fluids: +5.6%

Q2 2011 Conference Call

18

Decorative Surfaces

Quarterly Analysis

Q2 2011

Quarterly Analysis

Q2 2011

Key Points (Q2’11 vs. Q2’10)

• Segment organic revenues: +6.5%

• North America laminate base

revenues: +4.9% due to ongoing

product innovation and

penetration in commercial

construction

revenues: +4.9% due to ongoing

product innovation and

penetration in commercial

construction

• International base revenues:

+8.3% due to increased activity in

Asia Pacific (China) and Europe

+8.3% due to increased activity in

Asia Pacific (China) and Europe

Q2 2011 Conference Call

19

All Other

Quarterly Analysis

Q2 2011

Quarterly Analysis

Q2 2011

Key Points (Q2’11 vs. Q2’10)

• Segment organic revenues:

+8.1%

+8.1%

• Worldwide test and

measurement base revenues:

+17.0% as equipment orders

improved in Asia Pacific

(China) and Europe

measurement base revenues:

+17.0% as equipment orders

improved in Asia Pacific

(China) and Europe

• Worldwide consumer

packaging base revenues:

+5.7% due to strength in the

decorating and consumer

packaging businesses

packaging base revenues:

+5.7% due to strength in the

decorating and consumer

packaging businesses

• Worldwide industrial/appliance

base revenues: -0.5% due to

weakness in appliance sector

base revenues: -0.5% due to

weakness in appliance sector

Q2 2011 Conference Call

20

ITW

2011 Forecast

2011 Forecast

Q2 2011 Conference Call

21

ITW 2011 Forecast

Key Assumptions

Key Assumptions

• Exchange rates hold at current levels

• Acquired revenues in the $800 million to $1 billion range

for the year

for the year

• Restructuring costs of $40 to $50 million for the full year

• Tax rate range of 28.5% to 29.5% for Q3 and full year

(excludes the impact of the Q1 Australian tax case)

(excludes the impact of the Q1 Australian tax case)

Q2 2011 Conference Call

22

ITW Conference Call

Q & A

Q & A

Second Quarter

2011