Table of Contents

2017

United States

Securities and Exchange Commission

Washington, D.C. 20549

Form 40-F

| ☐ | Registration Statement pursuant to section 12 of the Securities Exchange Act of 1934 |

| ☒ | Annual report pursuant to section 13(a) or 15(d) of the Securities Exchange Act of 1934 |

For the fiscal year ended December 31, 2017

Commission File Number: 001-04307

Husky Energy Inc.

(Exact name of Registrant as specified in its charter)

| Alberta, Canada | 1311 | Not Applicable | ||

| (Province or other jurisdiction of incorporation or organization) |

(Primary Standard Industrial Classification Code Number (if applicable)) |

(I.R.S. Employer Identification Number (if applicable)) |

707-8th Avenue S.W. Calgary, Alberta, Canada T2P 1H5

(403) 298-6111

(Address and telephone number of Registrant’s principal executive office)

CT Corporation System, 111 Eighth Avenue, New York, New York 10011

(877) 467-3525

(Name, address (including zip code) and telephone number (including area code) of agent for service in the United States)

Securities registered or to be registered pursuant to Section 12(b) of the Act:

Title of Class: None

Securities registered or to be registered pursuant to Section 12(g) of the Act:

Title of Class: None

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act:

Title of Class: Common Shares

For annual reports, indicate by check mark the information filed with this Form:

| ☒ Annual information form | ☒ Audited annual financial statements |

Number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period

covered by the annual report:

1,005,120,012 Common Shares outstanding as of December 31, 2017

10,435,932 Cumulative Redeemable Preferred Shares, Series 1 outstanding as of December 31, 2017

1,564,068 Cumulative Redeemable Preferred Shares, Series 2 outstanding as of December 31, 2017

10,000,000 Cumulative Redeemable Preferred Shares, Series 3 outstanding as of December 31, 2017

8,000,000 Cumulative Redeemable Preferred Shares, Series 5 outstanding as of December 31, 2017

6,000,000 Cumulative Redeemable Preferred Shares, Series 7 outstanding as of December 31, 2017

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Exchange Act during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports) and (2) has been subject to such filing requirements for the past 90 days.

Yes ☒ No ☐

Indicate by check mark whether the Registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (s.232.405 of this chapter) during the preceding 12 months (or for such shorter period that the Registrant was required to submit and post such files).

Yes ☒ No ☐

Indicate by check mark whether the registrant is an emerging growth company as defined in Rule 12b-2 of the Exchange Act.

Emerging growth company ☐

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards† provided pursuant to Section 13(a) of the Exchange Act. ☐

This Annual Report on Form 40-F shall be incorporated by reference into or as an exhibit to, as applicable, the Registrant’s Registration Statement under the Securities Act of 1933: Form F-10 (File No. 333-222652); Form S-8 (File No. 333-187135).

| † | The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012. |

Table of Contents

Principal Documents

The following documents have been filed as part of this Annual Report on Form 40-F:

A. Annual Information Form

The Annual Information Form (“AIF”) of Husky Energy Inc. (“Husky” or the “Company”) for the year ended December 31, 2017 is included as Document A of this Annual Report on Form 40-F.

B. Audited Annual Financial Statements

Husky’s audited consolidated financial statements for the years ended December 31, 2017 and December 31, 2016, including the auditors’ report with respect thereto, are included as Document B of this Annual Report on Form 40-F.

C. Management’s Discussion and Analysis

Husky’s Management’s Discussion and Analysis for the year ended December 31, 2017 is included as Document C of this Annual Report on Form 40-F.

Certifications

See Exhibits 31.1, 31.2, 32.1 and 32.2, which are included as Exhibits to this Annual Report on Form 40-F.

Supplemental Reserves Information

See Exhibit 99.1 for the Supplemental Reserves Information, which is included as an Exhibit to this Annual Report on Form 40-F.

Disclosure Controls and Procedures

See the section “Disclosure Controls and Procedures” in Husky’s Management’s Discussion and Analysis for the year ended December 31, 2017, which is included as Document C of this Annual Report on Form 40-F.

Management’s Annual Report on Internal Control Over Financial Reporting

See the section “Disclosure Controls and Procedures” in Husky’s Management’s Discussion and Analysis for the year ended December 31, 2017, which is included as Document C of this Annual Report on Form 40-F.

Attestation Report of the Independent Registered Public Accounting Firm

See the “Report of Independent Registered Public Accounting Firm” that accompanies Husky’s audited consolidated financial statements for the years ended December 31, 2017 and 2016, which is included as Document B of this Annual Report on Form 40-F.

Changes in Internal Control Over Financial Reporting

See the section “Disclosure Controls and Procedures” in Husky’s Management’s Discussion and Analysis for the year ended December 31, 2017, which is included as Document C of this Annual Report on Form 40-F.

Notice Pursuant to Regulation BTR

Not Applicable.

Table of Contents

Audit Committee Financial Expert

The Board of Directors of Husky has determined that William Shurniak is an “audit committee financial expert” (as defined in paragraph 8(b) of General Instruction B to Form 40-F) serving on its Audit Committee. Pursuant to paragraph 8(a)(2) of General Instruction B to Form 40-F, the Board has applied the definition of independence applicable to the audit committee members of New York Stock Exchange listed companies, although the Company’s securities are not listed on a U.S. stock exchange. Mr. Shurniak is a corporate director and is independent under the New York Stock Exchange standards. For a description of Mr. Shurniak’s relevant experience in financial matters, see Mr. Shurniak’s history in the section “Directors and Officers” and in the section “Audit Committee” in Husky’s AIF for the year ended December 31, 2017, which is included as Document A of this Annual Report on Form 40-F.

Code of Business Conduct and Ethics

Husky’s Code of Ethics is disclosed in its Code of Business Conduct, which is applicable to its principal executive officer, principal financial officer, principal accounting officer or controller or persons performing similar functions and to all of its other employees, and is posted on its website at www.huskyenergy.com. On February 23, 2017, Husky amended its Code of Business Conduct effective as of February 24, 2017, and a copy of this new amended Code of Business Conduct is included as Exhibit 99.2 to this Annual Report on Form 40-F for the fiscal year ended December 31, 2017. A copy of such amended Code of Business Conduct was posted on Husky’s website (together with a disclosure of the nature of the amendment) promptly after the amendment became effective. In the fiscal year ended December 31, 2017, Husky has not granted a waiver, including an implicit waiver, from a provision of its Code of Ethics to any of its principal executive officer, principal financial officer, principal accounting officer or controller or persons performing similar functions that relates to one or more of the items set forth in paragraph (9)(b) of General Instruction B to Form 40-F. In the event that, during Husky’s ensuing fiscal year, Husky:

| i. | amends any provision of its Code of Business Conduct that applies to its principal executive officer, principal financial officer, principal accounting officer or controller or persons performing similar functions that relates to any element of the code of ethics definition enumerated in paragraph (9)(b) of General Instruction B to Form 40-F; or |

| ii. | grants a waiver, including an implicit waiver, from a provision of its Code of Business Conduct to any of its principal executive officer, principal financial officer, principal accounting officer or controller or persons performing similar functions that relates to one or more of the items set forth in paragraph (9)(b) of General Instruction B to Form 40-F; |

Husky will promptly disclose such occurrences on its website following the date that such amendment or waiver is granted and will specifically describe the nature of any amendment or waiver, and in the case of a waiver, name the person to whom the waiver was granted and the date of the waiver, in each case as further described in paragraph (9) of General Instruction B to Form 40-F.

Principal Accountant Fees and Services

See the section “External Auditor Service Fees” in Husky’s AIF for the year ended December 31, 2017, which is included as Document A of this Annual Report on Form 40-F.

Off-Balance Sheet Arrangements

See the section “Contractual Obligations, Commitments and Off-Balance Sheet Arrangements” in Husky’s Management’s Discussion and Analysis for the year ended December 31, 2017, which is included as Document C of this Annual Report on Form 40-F.

Tabular Disclosure of Contractual Obligations

See the section “Contractual Obligations, Commitments and Off-Balance Sheet Arrangements” in Husky’s Management’s Discussion and Analysis for the year ended December 31, 2017, which is included as Document C of this Annual Report on Form 40-F.

Interactive Data File

See Exhibit 101 to this Annual Report on Form 40-F for the fiscal year ended December 31, 2017.

Mine Safety Disclosure

Not applicable.

Table of Contents

Undertaking and Consent to Service of Process

Undertaking

Husky undertakes to make available, in person or by telephone, representatives to respond to inquiries made by the Commission staff, and to furnish promptly, when requested to do so by the Commission staff, information relating to: the securities in relation to which the obligation to file an annual report on Form 40-F arises; or transactions in said securities.

Consent to Service of Process

A Form F-X signed by Husky and its agent for service of process has been filed with the Commission together with Form F-10 (File No. 333-222652) in connection with its securities registered on such form.

Any change to the name or address of the agent for service of process of Husky shall be communicated promptly to the Commission by an amendment to the Form F-X referencing the file number of Husky.

Signatures

Pursuant to the requirements of the Exchange Act, Husky Energy Inc. certifies that it meets all of the requirements for filing on Form 40-F and has duly caused this Annual Report to be signed on its behalf by the undersigned, thereto duly authorized.

Dated this 1st day of March, 2018

| Husky Energy Inc.

| ||

| By: |

/s/ Robert J. Peabody | |

| Name: Robert J. Peabody | ||

| Title: President & Chief Executive Officer

| ||

| By: |

/s/ James D. Girgulis | |

| Name: James D. Girgulis | ||

| Title: Senior Vice President, General Counsel & | ||

| Secretary |

Table of Contents

Document A

Form 40-F

Annual Information Form

For the Year Ended December 31, 2017

Table of Contents

ANNUAL INFORMATION FORM

FOR THE YEAR ENDED DECEMBER 31, 2017

MARCH 1, 2018

Table of Contents

| 1 | ||||

| 1 | ||||

| 6 | ||||

| 6 | ||||

| 7 | ||||

| 10 | ||||

| STATEMENT OF RESERVES DATA AND OTHER OIL AND GAS INFORMATION |

21 | |||

| 43 | ||||

| 46 | ||||

| 56 | ||||

| 63 | ||||

| 63 | ||||

| 65 | ||||

| 68 | ||||

| 71 | ||||

| 79 | ||||

| 79 | ||||

| 79 | ||||

| 79 | ||||

| 79 | ||||

| 80 | ||||

| 84 | ||||

| APPENDIX B - REPORT ON RESERVES DATA BY INTERNAL QUALIFIED RESERVES EVALUATOR |

88 | |||

| APPENDIX C - REPORT OF MANAGEMENT AND DIRECTORS ON OIL AND GAS DISCLOSURE |

89 | |||

| 91 |

Table of Contents

Unless otherwise indicated, in this Annual Information Form (“AIF”), the terms “Husky” and the “Company” mean Husky Energy Inc. and its subsidiaries and partnership interests on a consolidated basis, including information with respect to predecessor corporations.

Unless otherwise indicated, the information contained in this AIF is presented as at or for the year ended December 31, 2017, and all financial information included and incorporated by reference in this AIF is determined using International Financial Reporting Standards (“IFRS”), as issued by the International Accounting Standards Board.

Except where otherwise indicated, all dollar amounts stated in this AIF are in Canadian dollars.

See also “Reader Advisories” on page 80 of this AIF.

ABBREVIATIONS AND GLOSSARY OF TERMS

When used in this AIF, the following terms have the meanings indicated:

| Units of Measure |

||

| bbl |

barrel | |

| bbls |

barrels | |

| bbls/day |

barrels per calendar day | |

| bcf |

billion cubic feet | |

| boe |

barrels of oil equivalent | |

| boe/day |

barrels of oil equivalent per calendar day | |

| GJ |

gigajoule | |

| kt |

kilotonne | |

| long tons/day |

imperial measurement of a metric tonne per calendar day | |

| m3 |

cubic metres | |

| mbbls |

thousand barrels | |

| mbbls/day |

thousand barrels per calendar day | |

| mboe |

thousand barrels of oil equivalent | |

| mboe/day |

thousand barrels of oil equivalent per calendar day | |

| mcf |

thousand cubic feet | |

| mmbbls |

million barrels | |

| mmboe |

million barrels of oil equivalent | |

| mmbtu |

million British thermal units | |

| mmcf |

million cubic feet | |

| mmcf/day |

million cubic feet per calendar day | |

| tcf |

trillion cubic feet | |

| tCO2e |

tonnes of carbon dioxide equivalent |

abandonment and reclamation costs

All costs associated with the process of restoring Husky’s properties that have been disturbed by oil and gas activities to a standard imposed by applicable government or regulatory authorities, including costs associated with the retirement of upstream and downstream assets which consist primarily of plugging and abandoning wells, abandoning surface and subsea plant, equipment and facilities, and restoring land.

API gravity

Measure of oil density or specific gravity used in the petroleum industry. The API scale expresses density such that the greater the density of the petroleum, the lower the degree of API gravity.

barrel

A unit of volume equal to 42 U.S. gallons.

Husky Energy Inc. | Annual Information Form 2017 | 1

Table of Contents

bitumen

Bitumen is a naturally occurring solid or semi-solid hydrocarbon consisting mainly of heavier hydrocarbons with a viscosity greater than 10,000 millipascal-seconds or 10,000 centipoise measured at the hydrocarbon’s original temperature in the reservoir and at atmospheric pressure on a gas-free basis, and that is not primarily recoverable at economic rates through a well without the implementation of enhanced recovery methods.

BP-Husky Toledo Refinery

The crude oil refinery owned 50 percent by the Company and 50 percent by BP Corporation North America Inc. and located in Toledo, Ohio.

CO2e

Carbon dioxide equivalent.

development well

A well drilled within the proved area of an oil and gas reservoir to the depth of a stratigraphic horizon known to be productive.

diluent

A lighter gravity liquid hydrocarbon, usually condensate or synthetic oil, added to heavy oil and bitumen to facilitate the transmissibility of the oil through a pipeline.

enhanced oil recovery

The increased recovery from a crude oil pool achieved by artificial means or by the application of energy extrinsic to the pool. An artificial means or application includes pressuring, cycling, pressure maintenance or injection to the pool of a substance or form of energy but does not include the injection in a well of a substance or form of energy for the sole purpose of aiding in the lifting of fluids in the well, or stimulation of the reservoir at or near the well by mechanical, chemical, thermal or explosive means.

exploration licence

A licence with respect to the Canadian offshore or the Northwest Territories conferring the right to explore for, and the exclusive right to drill and test for, hydrocarbons and petroleum, the exclusive right to develop the applicable area in order to produce petroleum and, subject to satisfying the requirements for issuance of a production licence and compliance with the terms of the licence and other provisions of the relevant legislation, the exclusive right to obtain a production licence.

exploration well

A well drilled to find a new field or to find a new reservoir in a field previously found to be productive of oil or gas. Generally, an exploration well is any well that is not a development well, a service well, an extension well, which is a well drilled to extend the limits of a known reservoir, or a stratigraphic test well as those terms are defined herein.

feedstock

Raw materials which are processed into petroleum products.

field

An area consisting of a single reservoir or multiple reservoirs all grouped on or related to the same individual geological structural feature and/or stratigraphic condition. There may be two or more reservoirs in a field which are separated vertically by intervening impervious strata, or laterally by local geologic barriers, or by both.

gross/net acres and gross/net wells

Gross refers to the total number of acres or wells, as the context requires, in which a working interest is owned. Net refers to the sum of the fractional working interests owned by a company.

gross reserves and gross production

A company’s working interest share of reserves or production, as the context requires, before deduction of royalties.

heavy crude oil

Crude oil with a relative density greater than 10 degrees API gravity and less than or equal to 22.3 degrees API gravity.

high-TAN

A measure of acidity. Crude oils with a high content of naphthenic acids are referred to as high total acid number (“TAN”) crude oils or high acid crude oil. The TAN value is defined as the milligrams of Potassium Hydroxide required to neutralize the acidic group of one gram of the oil sample. Crude oils in the industry with a TAN value greater than one are referred to as high-TAN crudes.

light crude oil

Crude oil with a relative density greater than 31.1 degrees API gravity.

Husky Energy Inc. | Annual Information Form 2017 | 2

Table of Contents

Lima Refinery

The crude oil refinery owned by the Company and located in Lima, Ohio.

liquefied petroleum gas

Liquefied propanes and butanes, separately or in mixtures.

medium crude oil

Crude oil with a relative density greater than 22.3 degrees API gravity and less than or equal to 31.1 degrees API gravity.

natural gas

Natural gas is a naturally occurring hydrocarbon gas mixture consisting primarily of methane, but commonly including varying amounts of other higher alkanes, and sometimes a small percentage of carbon dioxide, nitrogen and/or hydrogen sulfide.

natural gas liquids

Those hydrocarbon components recovered from raw natural gas as liquids by processing through extraction plants, or recovered from field separators, scrubbers or other gathering facilities. These liquids include the hydrocarbon components ethane, propane and butane and condensates and combinations thereof.

net revenue

Gross revenues less royalties.

oil sands

Sands and other rock materials that contain bitumen and all other mineral substances in association therewith.

operating netback

Gross revenue less production, operating and transportation costs and royalties on a per unit basis.

petroleum coke

A carbonaceous solid delivered from oil refinery coker units or other cracking processes.

Plan of Development

As it relates to the Company’s operations in Indonesia, a Plan of Development represents development planning on one or more oil and gas fields in an integrated and optimal plan for the production of hydrocarbon reserves considering technical, economical and environmental aspects. An initial Plan of Development in a development area needs both SKK Migas and the Minister of Energy and Mineral Resources approvals. Subsequent Plans of Development in the same development area only need SKK Migas approval.

Prince George Refinery

The light oil refinery owned by the Company and located in Prince George, British Columbia.

production licence

Confers, with respect to the portions of the offshore area to which the licence applies, the right to explore for, and the exclusive right to drill and test for, petroleum, the exclusive right to develop those portions of the offshore area in order to produce petroleum, the exclusive right to produce petroleum from those portions of the offshore area and title to the petroleum produced.

production sharing contract

A contract for the development of resources under which the contractor’s costs (investment) are recoverable each year out of the production but with a maximum amount of production that can be applied to the cost recovery in any year.

Scope 1 emissions

Direct emissions from sources that are owned or controlled by the Company, as prescribed by the U.S. Environmental Protection Agency.

Scope 2 emissions

Indirect emissions from sources that are owned or controlled by the Company, as prescribed by the U.S. Environmental Protection Agency.

secondary recovery

Oil or gas recovered by injecting water or gas into the reservoir to force additional oil or gas to the producing wells. Usually, but not necessarily, this is done after the primary recovery phase has passed.

seismic survey

A method by which the physical attributes in the outer rock shell of the earth are determined by measuring, with a seismograph, the rate of transmission of shock waves through the various rock formations.

Husky Energy Inc. | Annual Information Form 2017 | 3

Table of Contents

service well

A well drilled or completed for the purpose of supporting production in an existing field. Specific purposes of service wells include gas injection, water injection, steam injection, air injection, saltwater disposal, water supply for injection, observation or injection for in-situ combustion.

significant discovery declaration

A discovery indicated by the first well on a geological feature that demonstrates by flow testing the existence of hydrocarbons in that feature and, having regard to geological and engineering factors, suggests the existence of an accumulation of hydrocarbons that has potential for sustained production.

significant discovery licence

The document of “title” by which an interest owner can continue to hold rights to a discovery area while the extent of that discovery is determined and, if it has potential to be brought into commercial production in the future, until commercial development becomes viable. A significant discovery licence is effective from the application date and remains in force for so long as the relevant declaration of significant discovery is in force, or until a production licence is issued for the relevant lands.

spot price

The price for a one-time open market transaction for immediate delivery of a specific quantity of product at a specific location where the commodity is purchased “on the spot” at current market rates.

steam-assisted gravity drainage

An enhanced oil recovery method used to produce heavy crude oil and bitumen in-situ. Steam is injected via a horizontal well along a producing formation. The temperature in the formation increases and lowers the viscosity of the crude oil allowing it to fall into a horizontal production well beneath the steam injection well.

stratigraphic test well

A hole drilled to delineate or derisk the geology, and may include the cutting of cores, to aid in exploring and developing for oil and gas and usually drilled without the intent of being completed for production.

sulphur

An element that occurs in natural gas and petroleum.

Superior Refinery

The crude oil refinery owned by the Company and located in Superior, Wisconsin.

synthetic oil

A mixture of hydrocarbons derived by upgrading heavy crude oils, including bitumen, through a process that reduces the carbon content and increases the hydrogen content.

thermal

Use of steam injection into the reservoir in order to enable the heavy oil and bitumen to flow to the well bore.

turnaround

Performance of plant or facility maintenance.

Upgrader

The heavy oil upgrading facility owned and operated by the Company and located in Lloydminster, Saskatchewan.

waterflood

One method of secondary recovery in which water is injected into an oil reservoir for the purpose of forcing oil out of the reservoir and into the bore of a producing well.

wellhead

The structure, sometimes called the “Christmas tree”,that is positioned on the surface over a well and used to control the flow of oil or gas as it emerges from the subsurface casing head.

working interest

A percentage of ownership in an oil and gas lease granting its owners the right to explore, drill and produce oil and gas from a property.

2-D seismic survey

Two-dimensional seismic imaging uses seismic wave data recorded on one receiver line on the ground, to output a single cross-section of seismic data that is used to detect geologic variations in the subsurface.

Husky Energy Inc. | Annual Information Form 2017 | 4

Table of Contents

3-D seismic survey

Three-dimensional seismic imaging uses seismic wave data recorded simultaneously on a series of parallel receiver lines on the ground, to output a three-dimensional volume of seismic data that is used to detect geologic variations in the subsurface.

2015 Canadian Shelf Prospectus

The universal short form base shelf prospectus filed by the Company on February 23, 2015 with applicable securities regulators in each of the provinces of Canada.

Husky Energy Inc. | Annual Information Form 2017 | 5

Table of Contents

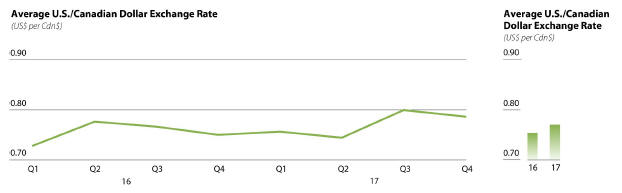

The following table discloses various indicators of the Canadian dollar/U.S. dollar rate of exchange or the cost of a U.S. dollar in Canadian currency for the three years indicated.

| Year ended December 31, | ||||||||||||

| Exchange Rate Information (Cdn$ per US$) |

2017 | 2016 | 2015 | |||||||||

| Year-end(1) |

1.252 | 1.343 | 1.384 | |||||||||

| Low |

1.213 | 1.254 | 1.173 | |||||||||

| High |

1.374 | 1.459 | 1.399 | |||||||||

| Average |

1.298 | 1.325 | 1.279 | |||||||||

| (1) | The year-end exchange rate for 2017 was quoted by the Thomson Reuters WM/R for the noon rate at the last day of the relevant period. The year-end exchange rates for 2016 and 2015 were as quoted by the Bank of Canada for the noon buying rate as at the last day of the relevant period. The Bank of Canada discontinued the publication of the noon buying rates during 2017. The high, low and average rates were either quoted or calculated within each of the relevant periods. |

Incorporation and Organization

Husky Energy Inc. was incorporated under the Business Corporations Act (Alberta) on June 21, 2000. The Company’s Articles were amended effective February 28, 2011 to permit the issuance of common shares as payment of stock dividends on the common shares and to authorize preferred shares to be issued in one or more series. The Company’s Articles were amended: effective March 11, 2011, to create Cumulative Redeemable Preferred Shares, Series 1 (the “Series 1 Preferred Shares”) and Cumulative Redeemable Preferred Shares, Series 2 (the “Series 2 Preferred Shares”); effective December 4, 2014, to create Cumulative Redeemable Preferred Shares, Series 3 (the “Series 3 Preferred Shares”) and Cumulative Redeemable Preferred Shares, Series 4 (the “Series 4 Preferred Shares”); effective March 9, 2015, to create Cumulative Redeemable Preferred Shares, Series 5 (the“Series 5 Preferred Shares”) and Cumulative Redeemable Preferred Shares, Series 6 (the “Series 6 Preferred Shares”); and effective June 15, 2015, to create Cumulative Redeemable Preferred Shares, Series 7 (the “Series 7 Preferred Shares”) and Cumulative Redeemable Preferred Shares, Series 8 (the “Series 8 Preferred Shares”).

Husky’s registered office and head and principal office are located at 707 - 8th Avenue S.W., Calgary, Alberta, T2P 1H5.

Intercorporate Relationships

The following table lists Husky’s significant subsidiaries and jointly-controlled entities and their respective places of incorporation, continuance or organization, as the case may be, as at December 31, 2017. (1) All of the entities listed below, except as otherwise indicated, are 100 percent beneficially owned, or controlled or directed, directly or indirectly, by Husky.

| Significant Subsidiaries and Joint Operations | Jurisdiction | |

| Husky Oil Operations Limited |

Alberta | |

| Husky Energy International Corporation |

Alberta | |

| Lima Refining Company |

Delaware | |

| Husky Marketing and Supply Company |

Delaware | |

| Husky Oil Limited Partnership |

Alberta | |

| Husky Terra Nova Partnership |

Alberta | |

| Husky Downstream General Partnership |

Alberta | |

| Husky Energy Marketing Partnership |

Alberta | |

| Sunrise Oil Sands Partnership (50 percent) |

Alberta | |

| BP-Husky Refining LLC (50 percent) |

Delaware |

| (1) | Principal operating subsidiaries exclusive of intercorporate relationships due to financing related receivables and financing investments. |

Husky Energy Inc. | Annual Information Form 2017 | 6

Table of Contents

Three-year History of Husky

The following is a description of how Husky’s business has developed over the last three completed financial years.

2015

On February 23, 2015, the Company filed the 2015 Canadian Shelf Prospectus, which enabled the Company to offer up to $3.0 billion of common shares, preferred shares, debt securities, subscription receipts, warrants and other units in Canada up to and including March 23, 2017.

On March 11, 2015, the Company announced that it had started oil production at the Sunrise Energy Project in northern Alberta.The project is being developed in multiple phases with Phase 1 consisting of two 30,000 bbls/day bitumen plants (Plants 1A and 1B).

On March 12, 2015, the Company issued $750 million of 3.55 percent notes due March 12, 2025 by way of a prospectus supplement dated March 9, 2015 to the 2015 Canadian Shelf Prospectus. The notes are redeemable at the option of the Company at any time, subject to a make whole premium unless the notes are redeemed in the three-month period prior to maturity. Interest is payable semi-annually on March 12 and September 12 of each year, beginning September 12, 2015. The notes are unsecured and unsubordinated and rank equally with all of the Company’s other unsecured and unsubordinated indebtedness.

On March 12, 2015, the Company issued 8 million Series 5 Preferred Shares at a price of $25.00 per share, for aggregate gross proceeds of $200 million, by way of a prospectus supplement dated March 5, 2015 to the 2015 Canadian Shelf Prospectus. Holders of the Series 5 Preferred Shares are entitled to receive a cumulative quarterly fixed dividend yielding 4.50 percent annually for the initial period ending March 31, 2020 as declared by the Board of Directors. See “Dividends – Dividend Policy and Restrictions – Series 5 Preferred Share Dividends”.

On June 17, 2015, the Company issued 6 million Series 7 Preferred Shares at a price of $25.00 per share, for aggregate gross proceeds of $150 million, by way of a prospectus supplement dated June 10, 2015 to the 2015 Canadian Shelf Prospectus. Holders of the Series 7 Preferred Shares are entitled to receive a cumulative fixed dividend yielding 4.60 percent annually for the initial period ending June 30, 2020 as declared by the Board of Directors. See “Dividends – Dividend Policy and Restrictions – Series 7 Preferred Share Dividends”.

On June 29, 2015, the Company announced that it had started production from the South White Rose project in the Jeanne d’Arc Basin offshore Newfoundland and Labrador (“NL”).

On July 16, 2015, the Company announced that it had started production at the 10,000 bbls/day Rush Lake Thermal Project in Saskatchewan.

On September 8, 2015, the Company announced that it had commenced production from a second oil well at the South White Rose project in the Jeanne d’Arc Basin offshore NL.

On October 6, 2015, the Company announced that it had entered into an agreement with Imperial Oil to create a single expanded truck transport network of approximately 160 sites in Canada.

On October 30, 2015, the Board of Directors approved an amendment to the Company’s dividend policy and the Company announced that the third quarter 2015 dividend would be paid in the form of common shares as an interim measure in lieu of paying a cash dividend. Given the persistent downward pressure on oil prices and the extended lower for longer outlook, the Board of Directors subsequently suspended the quarterly dividend. No cash or share dividend was issued for the fourth quarter of 2015.

On November 9, 2015, the Company announced the sanctioning of the development of the MDA, MBH and MDK gas fields. The Company had secured the gas sales agreement (“GSA”) for the first tranche of gas from the MDA-MBH fields development.

On December 3, 2015, the Company announced the signing of a production sharing contract (“PSC”) for Block 15/33 in the Pearl River Mouth Basin in the South China Sea. Under the PSC, Husky has an obligation to drill two exploration wells within the first three years.

During 2015, the Company acquired 2-D and 3-D seismic survey data on the Anugerah contract area.

Husky Energy Inc. | Annual Information Form 2017 | 7

Table of Contents

2016

On March 9, 2016, the maturity date for one of the Company’s $2.0 billion revolving syndicated credit facilities, previously set to expire on December 14, 2016, was extended to March 9, 2020. In addition, the Company’s leverage covenant was modified to a debt-to-capital covenant.

On March 31, 2016, the Company announced that holders of 1,564,068 Series 1 Preferred Shares exercised their option to convert their shares, on a one-for-one basis, to Series 2 Preferred Shares and receive a floating rate quarterly dividend.

On April 18, 2016, the Company announced that it had commenced production at the 10,000 bbls/day Edam East Thermal Project in Saskatchewan.

On April 19, 2016, the Company commenced production from the Colony formation at the Tucker Thermal Project in the Cold Lake region of Alberta.

On May 25, 2016, the Company completed the sale of Western Canada royalty interests to a third party for gross proceeds of $165 million.

On June 16, 2016, the Company announced that it had commenced production at the 10,000 bbls/day Vawn Thermal Project in Saskatchewan.

Production from the Sunrise Energy Project was temporarily impacted by wildfires in the Fort McMurray region of Alberta in the second quarter of 2016. Operations were successfully restarted in the same quarter with all 55 well pairs back online and the plant being fully operational.

On July 15, 2016, the Company completed the sale of 65 percent of its ownership interest in select midstream assets in the Lloydminster region of Alberta and Saskatchewan for gross proceeds of $1.69 billion in cash. The assets include approximately 1,900 kilometres of pipeline in the Lloydminster region, 4.1 mmbbls of storage capacity at Hardisty and Lloydminster and other ancillary assets. The assets are held by a newly formed limited partnership, Husky Midstream Limited Partnership (“HMLP”), of which Husky owns 35 percent, Power Assets Holdings Limited (“PAH”)owns 48.75 percent and CK Infrastructure Holdings Limited (“CKI”) owns 16.25 percent. Proceeds from the transaction were received in the third quarter of 2016.

On August 2, 2016, the Company announced that its China subsidiary had signed a Heads of Agreement (“HOA”) with China National Offshore Oil Corporation (“CNOOC”) and relevant companies for the price adjustment of natural gas from the Liwan 3-1 and Liuhua 34-2 fields with the revised price set at Cdn$12.50-Cdn$15.00 per mcf. The price adjustment under the HOA was effective as of November 20, 2015, and the settlement of outstanding payment was calculated from that date.

On August 29, 2016, the Company commenced production at the 4,500 bbls/day Edam West Thermal Project in Saskatchewan.

On September 15, 2016, the Company commenced production at the North Amethyst Hibernia formation well offshore NL.

On October 27, 2016, the Company announced that at the Liwan Gas Project, the second 22-inch subsea pipeline connecting the deepwater pipeline to the central platform was completed, tested and placed in service. This pipeline provides operating flexibility for the deepwater infrastructure and completes the Liwan facilities to their full design specification.

On November 9, 2016, the Canada-Newfoundland and Labrador Offshore Petroleum Board (“C-NLOPB”) announced that the Company was the successful bidder on two parcels of land in its 2016 land sale. The lands cover an area of 211,574 hectares and brought the Company’s exploration licences (“ELs”) in the region to eight. The southwest parcel is adjacent to the White Rose field and satellite extensions, while the other is northeast of the field and adjacent to other Husky operated ELs in the Jeanne d’Arc Basin.

On November 29, 2016, the Company commenced production from a third well at the South White Rose project in the Jeanne d’Arc Basin offshore NL.

In late 2016, the Company sanctioned three new Lloyd thermal projects with total design capacity of 30,000 bbls/day at Dee Valley, Spruce Lake North and Spruce Lake Central.

Also during 2016, the Company completed the sale of approximately 30,200 boe/day of legacy crude oil and gas assets in Western Canada for gross proceeds of $1.12 billion.

Husky Energy Inc. | Annual Information Form 2017 | 8

Table of Contents

2017

On March 10, 2017, the Company issued $750 million of 3.60 percent notes due March 10, 2027 by way of a prospectus supplement dated March 7, 2017, to the 2015 Canadian Shelf Prospectus. The notes are redeemable at the option of the Company at any time, subject to a make whole premium unless the notes are redeemed in the three-month period prior to maturity. Interest is payable semi-annually on March 10 and September 10 of each year, beginning September 10, 2017. The notes are unsecured and unsubordinated and rank equally with all of the Company’s other unsecured and unsubordinated indebtedness.

On April 13, 2017, the Company announced that it had signed a PSC for Block 16/25 in the Pearl River Mouth Basin in the South China Sea. Under the PSC, Husky has an obligation to drill two exploration wells within the first three years.

On May 5, 2017, the Company announced that, during the first quarter of 2017, it had commenced production from a new eight-well pad at the Tucker Thermal Project in the Cold Lake region of Alberta and from a new infill well at North Amethyst offshore NL.

On May 29, 2017, the Company announced that, together with its partners, it would be moving forward with the West White Rose Project in the Jeanne d’Arc Basin offshore NL, using a fixed wellhead platform tied back to the SeaRose FPSO, which would enable the Company and its partners to maximize resource recovery.

Also in May 2017, the Company announced a new discovery at Northwest White Rose. The White Rose A-78 well was drilled approximately 11 kilometres northwest of the SeaRose FPSO in the first quarter of 2017 and delineated a light oil column of more than 100 metres (gross). The Company has a 93.23 percent working interest in the well.

On July 21, 2017, the Company announced that the construction and installation of the shallow water jackets and subsea pipelines for the MDA-MBH fields in the Madura Strait were completed. The contract for a leased floating production unit was signed, and planning for the build commenced.

On September 15, 2017, the Company repaid the maturing 6.20 percent notes issued under a trust indenture dated September 11, 2007. The amount paid to note holders was $365 million, including $11 million of interest.

On October 26, 2017, the Company announced that, during the third quarter of 2017, gas production from the BD Project commenced and was sold from the onshore gas distribution facility in East Java under a fixed price GSA.

Also in October 2017, the Company announced that the GSA for future gas production from Liuhua 29-1, the third deepwater gas field at the Liwan Gas Project, was signed. The project was sanctioned in the fourth quarter of 2017.

On November 8, 2017, the Company completed the purchase of the Superior Refinery, a 50,000 bbls/day permitted capacity facility located in Superior, Wisconsin, U.S., from Calumet Specialty Products Partners, L.P. (“Calumet”) for $670 million (US$527 million) in cash, which includes $108 million (US$85 million) of working capital, subject to final adjustments. The acquisition included the Superior Refinery’s associated logistics, including two asphalt terminals, 3.6 mmbbls of crude and product storage and a fuels and asphalt marketing business. See “Description of Husky’s Business – Downstream Operations – U.S. Refining and Marketing – Superior Refinery”.

In November 2017, the Company sanctioned two new 10,000 bbls/day thermal projects at Westhazel and Edam Central.

In November 2017, the C-NLOPB announced that the Company was the successful bidder on a parcel of land in its 2017 land sale (50 percent Husky working interest). The lands cover an area of 121,453 hectares in the Jeanne d’Arc Basin. The lands are adjacent to the Company’s other ELs in the basin.

Also in November 2017, the Company’s participation in the Wenchang oilfields petroleum contract expired, and the Company will not be entitled to any further production rights.

During 2017, the Company completed the sale of select assets in Western Canada, representing approximately 20,200 boe/day for gross proceeds of approximately $185 million.

Also during 2017, regulatory approval was received for the three Lloyd thermal projects sanctioned in late 2016, Dee Valley, Spruce Lake North and Spruce Lake Central.

Also during 2017, the Company and Imperial Oil closed their previously announced transaction to create a single expanded truck transport network of approximately 160 sites.

Husky Energy Inc. | Annual Information Form 2017 | 9

Table of Contents

DESCRIPTION OF HUSKY’S BUSINESS

Overview

Husky is a publicly traded international integrated energy company headquartered in Calgary, Alberta, Canada.

Management has identified segments for the Company’s business based on differences in products, services and management responsibility. The Company’s business is conducted predominantly through two major business segments: Upstream and Downstream.

Upstream operations include exploration for, and development and production of, crude oil, bitumen, natural gas and natural gas liquids (“NGL“) (“Exploration and Production”) and marketing of the Company’s and other producers’ crude oil, natural gas, NGLs, sulphur and petroleum coke, pipeline transportation, the blending of crude oil and natural gas, and storage of crude oil, diluent and natural gas (“Infrastructure and Marketing”). Infrastructure and Marketing markets and distributes products to customers on behalf of Exploration and Production and is grouped in the Upstream business segment based on the nature of its interconnected operations. The Company’s Upstream operations are located primarily in Alberta, Saskatchewan and British Columbia (“Western Canada”), offshore the east coast of Canada (“Atlantic”) and offshore China and offshore Indonesia (“Asia Pacific”).

Downstream operations include upgrading of heavy crude oil feedstock into synthetic crude oil in Canada (“Upgrading”), refining crude oil in Canada, marketing of refined petroleum products including gasoline, diesel, ethanol blended fuels, asphalt and ancillary products and production of ethanol (“Canadian Refined Products”). It also includes refining in the U.S. of primarily crude oil to produce and market asphalt, gasoline, jet fuel and diesel fuels that meet U.S. clean fuels standards (“U.S. Refining and Marketing”). Upgrading, Canadian Refined Products and U.S. Refining and Marketing all process and refine natural resources into marketable products and are grouped together as the Downstream business segment due to the similar nature of their products and services.

Corporate Strategy

The Company’s business strategy is to focus on returns from investment in a deep portfolio of opportunities that can generate increased funds from operations and free cash flow. The Company has two main businesses: (i) an integrated Canada-U.S. Upstream and Downstream corridor ( “Integrated Corridor”); and (ii) production located offshore Atlantic and Asia Pacific ( “Offshore”).

The Company’s business in the Integrated Corridor includes crude oil, bitumen, natural gas and NGL production from Western Canada, the Lloydminster upgrading and asphalt refining complex, the Prince George Refinery, HMLP (35 percent working interest and operatorship), and the Lima, Toledo and Superior refineries in the U.S. midwest. Natural gas production from the Western Canada portfolio is closely aligned with the Company’s energy requirements for refining and thermal bitumen production and acts as a natural hedge.

The Company’s Offshore business includes operations, development and exploration in Asia Pacific and Atlantic. Each area generates high-netback production, with near and long-term investment potential.

Husky Energy Inc. | Annual Information Form 2017 | 10

Table of Contents

Upstream Operations

Integrated Corridor

Thermal and Non-Thermal Developments

Heavy Oil

The majority of the Company’s heavy oil assets are located in the Lloydminister region of Alberta and Saskatchewan, with lands consisting of approximately two million acres. This extensive land position spans most of the productive oil fields in the area, all within 100 kilometres of the City of Lloydminister.The majority of the Company’s operations are 100 percent working interest. The Company’s operations are supported by a network of Company-owned treating facilities and operated pipelines that transport heavy crude oil from the field locations to the Husky Lloydminister Asphalt Refinery, the Husky Lloydminister Upgrader and third-party pipeline systems at Hardisty, Alberta, providing full integration with the Company’s Upstream Infrastructure and Marketing and its Downstream business segments.

Production of heavy crude oil from the Lloydminister area uses a variety of technologies, including Cold Heavy Oil Production with Sand (“CHOPS”), horizontal wells, waterflooded fields and non-thermal enhanced oil recovery (“EOR”).

The Company operated five carbon dioxide (“CO2”) injection EOR pilot projects in 2017 and a CO2 capture and liquefaction plant at the Lloydminster Ethanol Plant. The liquefied CO2 is used in the ongoing EOR piloting program. The Company is also piloting several types of CO2 capture technology at its Lashburn facility in Saskatchewan.

Lloydminster Thermal Projects

Lloydminster bitumen production consists of nine thermal plants located in the Lloydminster region of Saskatchewan: Bolney/Celtic, Edam East, Edam West, Paradise Hill, Pikes Peak, Pikes Peak South, Rush Lake, Sandall and Vawn. Each plant has a number of production pads and utilizes Steam-Assisted Gravity Drainage (“SAGD”) technology. 2017 production from Lloyd thermal projects averaged 77,100 bbls/day.

In 2017, work continued on the 10,000 bbls/day Rush Lake 2 thermal development, with the central facility 65 percent complete as of the end of 2017, and with first bitumen expected in the first quarter of 2019.

Regulatory approval has also been secured for the next three new Lloyd thermal projects at Dee Valley, Spruce Lake North and Spruce Lake Central with a total design capacity of about 30,000 bbls/day. Site clearing was completed at Dee Valley in the fourth quarter of 2017 and construction will commence in 2018. Site clearing and construction will start at Spruce Lake Central in 2018, and at Spruce Lake North site clearing will start in 2018 with construction commencing in 2019. First production for all three projects is expected in 2020.

In November 2017, the Company sanctioned the next two 10,000 bbls/day thermal developments at Edam Central and Westhazel respectively. First production is expected in the second half of 2021.

All of the Company’s six new sanctioned 10,000 bbls/day thermal developments represent long life assets, using repeatable modular designs, with low sustaining capital requirements.

Tucker Thermal Project

The Tucker Thermal Project is a SAGD oil sands project located 30 kilometres northwest of Cold Lake, Alberta. It commenced bitumen production at the end of 2006.

In 2017, bitumen production averaged 21,900 bbls/day, with daily peak rates exceeding 24,000 bbls/day. Production is expected to reach 30,000 bbls/day by the end of 2018 through further development and optimization.

Sunrise Energy Project

On March 31, 2008, Husky and BP Corporation North America Inc. (“BP”) completed a transaction that created integrated North American oil sands and refining businesses. The businesses are comprised of a 50/50 partnership to develop the Sunrise Energy Project, operated by Husky, and a 50/50 limited liability company for the BP-Husky Toledo Refinery, operated by BP.

The Sunrise Energy Project is a SAGD oil sands project located in the Athabasca region of northern Alberta. At the end of 2017, there were 69 producing well pairs. In 2017, bitumen production averaged approximately 40,200 bbls/day (20,100 bbls/day Husky working interest). The project is expected to reach its 60,000 bbls/day nameplate capacity by the end of 2018.

Husky Energy Inc. | Annual Information Form 2017 | 11

Table of Contents

Western Canada

Foothills Operations

The Company’s Foothills operations are located primarily in western Alberta. Primary areas of operations consist of Rocky Mountain House, Edson and Grande Prairie. Foothills operations are centered on a gas resource growth strategy.

Within its Foothills operations, production in 2017 consisted of approximately 1,700 bbls/day of light and medium crude oil, 6,000 bbls/day of NGL and 252.5 mmcf/day of natural gas. The area is heavily weighted towards natural gas production at approximately 81 percent. The Company is pursuing liquids-rich natural gas development opportunities within the existing asset portfolio primarily in the Ansell and Kakwa areas.

The Kakwa Spirit River liquids-rich gas resource play, in which 2017 production averaged 3,500 boe/day, is located south of Grande Prairie. The Company initiated an operated drilling program with four wells drilled in the fourth quarter of 2017, and one well was put on production before the end of 2017. The remaining three wells are expected to come on production in the first quarter of 2018.

Edson operations are located primarily in northern Alberta and consist of the Ansell and Galloway areas. The Ansell liquids-rich natural gas resource play is located in the deep basin Cretaceous formations of west-central Alberta, with the Company holding an average 95 percent working interest in approximately 173 net sections of contiguous lands. The Company has been actively developing the Spirit River formations since 2012 using multi-stage fractured horizontal wells. Production from the Ansell and Galloway areas has doubled since 2012 and in 2017 averaged 2,100 bbls/day of NGL and 120 mmcf/day of natural gas. The Company operates over 400 producing wells at Ansell including 51 Spirit River horizontal wells and 20 Cardium horizontal wells. In 2017, the Company drilled 17 horizontal wells and completed 12 horizontal wells with nine wells on production at the end of 2017.

In the Wembley and Karr areas of Alberta, the Company has drilled five wells in the liquids-rich Montney formation. At Wembley, three wells have been drilled with one currently on production and two expected to be on production in 2018. At Karr, two wells were drilled and on production before the end of 2017.

Resource oil development is focused on the Cardium oil play in the Wapiti area south of the city of Grand Prairie, Alberta, utilizing horizontal well and multi-stage fracturing technology to unlock crude oil reserves. During 2017, production from the Cardium play averaged 2,500 boe/day. A four well drilling program was completed in the fourth quarter of 2017 with all four wells expected to be completed and put on production in the first quarter of 2018.

Plans in 2018 for Foothills include an 18-well development program targeting the Spirit River formation and an eight- well development program targeting the Montney formation.

Plains Operations

The Company’s Plains operations are located in central Alberta, northern Alberta and southwest Saskatchewan. As at December 31, 2017, the Company operated one crude oil and four natural gas facilities with approximately 400 active wells throughout the area. Production in 2017 averaged 3,900 bbls/day of crude oil, 400 bbls/day of NGL and 28.5 mmcf/day of natural gas.

Rainbow Lake Development

Rainbow Lake, located approximately 900 kilometres northwest of Edmonton, Alberta, is the site of the Company’s largest light oil production operation in Western Canada. Production during 2017 from the Rainbow Lake Development operations averaged 5,300 bbls/day of light crude oil, 4,100 bbls/day of NGL and 72.6 mmcf/day of natural gas. NGL and natural gas production ramped up in 2017 with the sale of additional volumes which are no longer required for injection into EOR operations, which was enabled by the completion and start-up of a 4,000 bbls/day NGL processing and truck loading facility in the second quarter of 2017.

The Company holds a 50 percent interest in a 90 megawatt natural gas fired cogeneration facility adjacent to its Rainbow Lake processing plant. The cogeneration facility produces electricity and thermal energy, or steam, for the Rainbow Lake processing plant. Additional electricity is also generated for the Power Pool of Alberta.

Northwest Territories

The Company holds two ELs acquired in 2011 in the Northwest Territories at the Slater River Canol shale play, which were consolidated as one EL in 2015 and cover 483,000 gross acres (466,000 net acres). Two vertical pilot wells were drilled, completed and flow tested in 2012. These wells satisfied the requirements to extend the term of both the ELs to the full nine-year term. The Company acquired a 220-square kilometre multi-component 3-D seismic survey in 2012, and construction of an all-season access road was completed in 2014. In 2016, the Company was awarded a significant discovery declaration on 545 sections (150,000 hectares) of land north of the Gambill Fault. Additionally, five sections of land were granted significant discovery licence (“SDL”) status earlier in 2016 based on the MGM East MacKay I-78 well south of the Gambill Fault. The Company engaged in no activity in the Northwest Territories in 2017, and no activity is planned for 2018.

Husky Energy Inc. | Annual Information Form 2017 | 12

Table of Contents

Offshore

Asia Pacific

China

Liwan Gas Project

The Liwan Gas Project includes the natural gas discoveries at the Liwan 3-1, Liuhua 34-2 and Liuhua 29-1 fields within the Contract Area 29/26 exploration block located in the Pearl River Mouth Basin of the South China Sea, approximately 300 kilometres southeast of the Hong Kong Special Administrative Region.

The Company has a 49 percent working interest in the project, and CNOOC has a 51 percent working interest. The initial development project of the Liwan 3-1 and Liuhua 34-2 fields was separated into deepwater and shallow water development projects, with the Company acting as deepwater operator and CNOOC acting as shallow water operator. The deepwater infrastructure includes production wells and trees, subsea pipelines and manifolds that produce to twin 22-inch deepwater pipelines running approximately 78 kilometres to a shallow water central platform. The shallow water infrastructure includes the central platform standing in approximately 120 metres of water, a 261-kilometre shallow water pipeline running from the central platform to the onshore Gaolan Gas Plant and the onshore gas plant with liquids separation facilities, 10 spherical NGL storage tanks, an export jetty, control facilities as well as administrative and accommodation buildings.

The Liwan 3-1 field commenced production at the end of March 2014. The gas field is currently producing from nine wells. The single production well in the Liuhua 34-2 field was tied into the deepwater facilities of the Liwan 3-1 field and commenced production in December 2014.

In 2017, gross gas sales from Liwan 3-1 and Liuhua 34-2 averaged 283 mmcf/day and 29 mmcf/day, respectively. In 2017, the Company’s working interest share of production from the two fields was 153 mmcf/day of conventional natural gas and 6,900 bbls/day of NGL.

The Liuhua 29-1 field is planned to be developed in a second project phase. The Company, acting as deepwater operator, plans to complete production wells and lay deepwater pipelines to tie into the existing Liuhua 34-2 field production manifold to share the existing Liwan Gas Project subsea infrastructure and the onshore Gaolan Gas Plant. In 2017, a gas sales agreement (“GSA”) was reached for future gas production from the field and the Board sanctioned the Liuhua 29-1 project for development. Construction is anticipated to begin in 2018, followed by first production in 2021.

Wenchang

The Wenchang field is located in the western Pearl River Mouth Basin, approximately 400 kilometres south of the Hong Kong Special Administrative Region and 100 kilometres east of Hainan Island. The Company held a 40 percent working interest in two oil fields, which commenced production in July 2002. The Wenchang 13-1 and 13-2 oil fields produced from 32 wells in 100 metres of water into an FPSO stationed between fixed platforms located in each of the two fields. In 2016, the PSC was extended for 130 days corresponding to the duration of production suspension for FPSO maintenance experienced in 2014. The PSC expired in November 2017, and the Company will not be entitled to any further production rights. The Company’s share of production averaged 5,400 bbls/day of light crude oil and NGL during 2017.

Block 15/33

The Company executed a PSC in December 2015 for an exploration block offshore China. Block 15/33 is located in the Pearl River Mouth Basin in the South China Sea, about 140 kilometres southeast of the Hong Kong Special Administrative Region and covers an area of 155 square kilometres in water depths of approximately 80 100 metres. The Company is the operator of the block during the exploration phase, with a working interest of 100 percent. In the event of a commercial discovery, its partner CNOOC may assume a working interest of up to 51 percent during the development and production phase. Under the PSC, the corresponding CNOOC share of exploration costs is to be recovered from production allocated to the Company. The Company expects to drill two exploration wells in the 2018 timeframe.

Block 16/25

The Company executed a PSC in April 2017 for an exploration block offshore China. Block 16/25 is located in the Pearl River Mouth Basin in the South China Sea, about 150 kilometres southeast of the Hong Kong Special Administrative Region and approximately 72 kilometres northeast of Block 15/33. The block covers an area of 44 square kilometres in water depths of approximately 85 100 metres. The Company is the operator of the block during the exploration phase, with a working interest of 100 percent. In the event of a commercial discovery, its partner CNOOC may assume a working interest of up to 51 percent during the development and production phase. Under the PSC, the corresponding CNOOC share of exploration costs is to be recovered from production allocated to the Company. The Company expects to drill two exploration wells in the 2018 timeframe in conjunction with the drilling on Block 15/33.

Husky Energy Inc. | Annual Information Form 2017 | 13

Table of Contents

Taiwan

In December 2012, the Company signed a joint venture agreement with CPC Corporation. The Company and CPC Corporation have rights to an exploration block in the South China Sea covering approximately 7,700 square kilometres located southwest of the island of Taiwan. The Company holds a 75 percent working interest during exploration, while CPC Corporation has the right to participate in the development program up to a 50 percent interest.

The acquisition of 2-D seismic survey data was completed in 2014, and the acquisition of 3-D seismic survey data was completed in 2017. The Company is analyzing the 3-D seismic survey data to identify potential drilling prospects.

Indonesia

Madura Strait

The Company has a 40 percent interest in approximately 622,000 acres (2,516 square kilometres) of the Madura Strait, located offshore East Java, in Indonesia. The Company’s two partners are CNOOC, which is the operator and has a 40 percent working interest, and Samudra Energy Ltd., which holds the remaining 20 percent interest through its affiliate, SMS Development Ltd. The Madura Strait includes the operating BD field and developments at the MDA, MBH, MDK and MAC fields and three additional discoveries.

In 2017 at the liquids-rich BD field, testing and commissioning of the shallow water production platform, FPSO, subsea pipeline to shore and onshore gas metering station were completed and first sales production was achieved mid-year. Gas sales to a second customer commenced in December. Gross gas sales are expected to ramp up to the full sales production target of 100 mmcf/day of gas and 6,000 bbls/day of associated liquids in 2018. Gross BD field sales averaged 20 mmcf/day of gas and 1,600 bbls/day of associated liquids in 2017. The Company’s working interest share of production was 8 mmcf/day and and 600 bbls/day, respectively.

At the MDA and MBH fields, facilities construction is ongoing. The platforms and in-field and tie-in production pipelines have been installed. A contract for the lease of a floating production unit vessel was signed in July 2017. Drilling of five MDA field production wells and two MBH field production wells is planned for the first half of 2018. Production from the MDA, MBH and MDK fields is expected in the 2019 timeframe with the additional MDK shallow water field expected to be tied in during the same period. Combined working interest sales volumes from the BD, MDA, MBH and MDK fields are expected to be approximately 100 mmcf/day of natural gas and 2,400 bbls/day of associated NGL once production is fully ramped up. Pre-engineering activities progressed at the MAC field, where an approved Plan of Development is in place. Additional discoveries in the region are being evaluated for potential development.

Anugerah

The Company executed a PSC in February 2014 with the Government of Indonesia for the Anugerah contract area. The Company holds a 100 percent interest in the Anugerah Block, which is located in the East Java Basin approximately 150 kilometres east of the Madura Strait. The block covers an area of 2,030,000 acres (8,215 square kilometres) with potential drilling opportunities in water depths of 800 to 1,300 metres. The PSC requires the acquisition of 2-D and 3-D seismic data during the first three years of the contract. In 2015 and 2016, a seismic acquisition program was carried out, and the results from the seismic surveys’ data continue to be evaluated to determine the potential for future drilling opportunities.

Atlantic

Overview

The Company’s Atlantic exploration and development program is focused in the Jeanne d’Arc Basin and the Flemish Pass. The Jeanne d’Arc Basin contains the Hibernia, Terra Nova and Hebron fields, as well as the White Rose field and satellite extensions, including North Amethyst, West White Rose and South White Rose. In the Flemish Pass Basin, the Company holds a 35 percent non-operated working interest in each of the Bay du Nord, Bay de Verde, Baccalieu, Harpoon and Mizzen discoveries. The Company is the operator of the White Rose field and satellite extensions and holds an ownership interest in the Terra Nova field, as well as a number of smaller undeveloped fields. The Company also holds significant exploration acreage offshore NL.

White Rose Field and Satellite Extensions

The White Rose field is located 354 kilometres off the coast of NL and is approximately 48 kilometres east of the Hibernia field on the eastern flank of the Jeanne d’Arc Basin. The Company is the operator of the main White Rose field and satellite tiebacks, including the North Amethyst, West White Rose and South White Rose extensions. The Company has a 72.5 percent working interest in the main field and a 68.875 percent working interest in the satellite extensions. To date, production has been facilitated via subsea tie-ins with wells drilled independently through drill centres and connected via flowlines to the SeaRose FPSO.

First oil was achieved at White Rose in November 2005. The White Rose field currently has 10 production wells, 10 water injection wells and three gas injection wells. During 2017, the Company’s light crude oil production from the White Rose field was 11,000 bbls/ day (Husky working interest).

Husky Energy Inc. | Annual Information Form 2017 | 14

Table of Contents

On May 31, 2010, first oil was achieved from North Amethyst, the first satellite extension at the White Rose field. The field is located approximately six kilometres southwest of the SeaRose FPSO. Production flows from North Amethyst to the SeaRose FPSO through a series of subsea flow lines. In September 2016, the Company began production from the deeper Hibernia formation at North Amethyst utilizing existing infrastructure. As of December 31, 2017, the field had seven production wells and four water injection wells. During 2017, the Company’s light crude oil production from North Amethyst was 10,000 bbls/day (Husky working interest).

Initial production from West White Rose was achieved in September 2011 through a two-well pilot project. The pilot wells have helped provide further information on the reservoir to refine development plans for the full West White Rose field. During 2017, the Company’s share of light crude oil production from this satellite field was 2,000 bbls/day (Husky working interest).

In May 2017, the Company and its co-venturers announced plans to proceed with full field development at West White Rose using a fixed drilling platform. First oil is forecasted for 2022, with the West White Rose Project expected to ramp up to peak production of 52,500 bbls/day (Husky working interest) in 2025 as development wells are brought online. Costs are estimated at $2.2 billion (Husky working interest) to first oil. Like the other White Rose tiebacks, the platform will leverage existing offshore infrastructure including the SeaRose FPSO.

Production commenced from the South White Rose Extension in 2015 with production wells supported by both gas flood and water injection. The South White Rose Extension was developed in phases, with gas injection equipment installed in 2013 and oil production equipment installed in 2014. As at December 31, 2017, the project had four production wells, one water injection well and one gas injection well. During 2017, the Company’s working interest share of light crude oil production from the South White Rose Extension was 7,000 bbls/day.

Terra Nova Field

The Terra Nova field is located approximately 350 kilometres southeast of St. John’s, NL. The Terra Nova field is divided into three distinct areas, known as the Graben, the East Flank and the Far East. Production at Terra Nova commenced in January 2002. The Company’s working interest in the field increased to 13 percent effective December 1, 2010.

As at December 31, 2017, there were 14 development wells drilled in the Graben area, consisting of eight production wells, four water injection wells and two gas injection wells. In the East Flank area, there were 14 development wells, consisting of eight production wells and six water injection wells. The Far East has one extended reach producer and an extended reach water injection well. The operator continues to progress delineation and development opportunities at Terra Nova.

Light crude oil production during 2017 from the Terra Nova field was 4,000 bbls/day (Husky working interest).

East Coast Exploration

The Company holds working interests ranging from 5.8 percent to 100 percent in 24 Significant Discovery Areas in the Jeanne d’Arc Basin and Flemish Pass Basin, offshore NL and Baffin Island.

In May 2017, the Company announced a near-field oil discovery at Northwest White Rose. The White Rose A-78 well was drilled approximately 11 kilometres northwest of the SeaRose FPSO in the first quarter of 2017 and delineated a light oil column of more than 100 metres. The discovery continues to be assessed. Husky has a 93.232 percent ownership interest. A potential development could leverage the SeaRose FPSO, existing subsea infrastructure and the future West White Rose wellhead platform.

In June 2016, the Company and its partner announced two oil discoveries at the Bay de Verde and Baccalieu prospects in the Flemish Pass Basin, which add to the resource base for a potential development at the Bay du Nord discovery.The Company holds a 35 percent non-operated working interest in each of the Bay du Nord, Bay de Verde, Baccalieu, Harpoon and Mizzen discoveries. The C-NLOPB issued an SDL for Bay du Nord in November 2017. The SDL 1055 covers an area of 13,149 hectares. The Company and its partner continue to assess the commercial potential of these discoveries.

In November 2017, the C-NLOPB announced that the Company was the successful bidder on a parcel of land in its 2017 land sale. The lands cover an area of 121,453 hectares in the Jeanne d’Arc Basin. The lands are adjacent to other Husky ELs in the basin, and bring the Company’s ELs in the region to nine.

Infrastructure and Marketing

Overview

The Company is engaged in the marketing of both its own and other producers’ crude oil, natural gas, NGL, sulphur and petroleum coke production. The Infrastructure and Marketing business manages the sale and transportation of the Company’s Upstream and Downstream production and third-party commodity trading volumes through access to capacity on third-party pipelines and storage facilities in both Canada and the U.S. The Company is able to capture differences between the two markets by utilizing infrastructure capacity to deliver feedstock acquired in Canada to the U.S. market.

Husky Energy Inc. | Annual Information Form 2017 | 15

Table of Contents

Husky Midstream Limited Partnership

HMLP was created in July 2016 with the sale of selected pipeline gathering systems in Alberta and Saskatchewan and the Lloydminster and Hardisty terminals. CKI owns 16.25 percent, PAH owns 48.75 percent, and Husky owns 35 percent of HMLP and remains the operator. The entity has approximately 1,900 kilometres of pipeline in the Lloydminster region, 4.1 mmbbls of storage capacity at Hardisty and Lloydminster and other ancillary assets. The Lloydminster Terminal, with a total storage capacity of 1.0 mmbbls, serves as a hub for the gathering systems. The pipeline systems transport blended heavy crude oil to Lloydminster,accessing markets through Husky’s Upgrader and Asphalt Refinery in Lloydminster. Blended heavy crude oil and bitumen from the field and synthetic crude oil from the upgrading operations are transported south to Hardisty, Alberta to a connection with the major export trunk pipelines. The Hardisty Terminal, with a total storage capacity of 3.1 mmbbls, acts as the exclusive blending hub for Western Canada Select (“WCS”), the largest heavy oil benchmark pricing point in North America.

HMLP has a separate Board of Directors from Husky and independent financing that supports both significant growth projects that are under construction and forecasted future expansions. Approximately $800 million in growth projects are underway. HMLP is in the process of diversifying its operations beyond the Lloydminster and Hardisty area and has commercial support to enter the natural gas processing segment.

In 2018, HMLP expects to commission a 150-kilometre pipeline system in Alberta to allow for third-party and Husky production growth in both Alberta and Saskatchewan. A second major pipeline project is underway in Saskatchewan to provide transportation for the anticipated increase in the Company’s bitumen production. The Hardisty terminal is also expanding to provide additional pipeline connectivity and crude oil storage for customers. The assets will play an integral and valuable role in the successful transportation of heavy oil and bitumen production to end markets by providing connections to the Husky Lloydminster Upgrader and Asphalt Refinery, third-party terminals and pipelines through strategic hubs such as the Hardisty Terminal.

Third-Party Pipeline Commitments

In 2010, the Company commenced its pipeline commitment on the Keystone pipeline system, which ships Canadian crude oil from Hardisty, Alberta to Patoka, Illinois. This commitment was part of a strategy, commenced in 2006, to expand the market for the Company’s crude oil into the midwest U.S. This strategy was further supported through the acquisition of the Lima Refinery in 2007, which now enables the Company’s Canadian synthetic and bitumen production along with additional third-party purchases to be processed at the refinery. The Company has the ability to utilize the portion of the Keystone pipeline system that continues to Cushing, Oklahoma, and the Company holds long-term firm capacity on the Enbridge Flanagan South pipeline and Southern Access Extension pipeline which connect Enbridge’s Mainline to the U.S. Gulf Coast and Patoka markets.

Due to the Company’s ongoing Keystone pipeline commitment, the Lima Refinery has the option to access a significant amount of Canadian crude oil as part of its crude feedstock requirements. The Keystone pipeline has enabled the Company to sell bitumen through interconnecting pipeline systems to the Lima Refinery and into Cushing, Oklahoma.

Since 2012, the pipeline systems leaving Canada have at times been subject to significant apportionment, affecting both Canadian export volumes and crude oil prices in Western Canada. The Company has mitigated these effects through the reliability of its proprietary pipeline system, its firm capacity on export pipelines and the Company’s demand for Canadian crude oil feedstock for its Canadian upgrading and refining assets. In 2017, the Company further enhanced this integration when it purchased a 50,000 bbls/ day refinery at Superior, Wisconsin which runs a combination of heavy Canadian crude and light crudes from Canada and the U.S. The Superior Refinery is located on the Enbridge Mainline crude system. As a seller and buyer of crude oils, the Company has a relatively balanced exposure to many location and grade differentials.

The Company has been monitoring opportunities to participate in growing crude oil markets accessed by rail, which have developed due to refiners’ desire for inland crude oil which has at times been priced at significant discounts to ocean imports. The Company has made crude oil deliveries to rail-loading facilities via trucks, where netbacks can be increased relative to pipeline alternatives. While the Company’s primary focus is on low-cost pipeline transportation options, it has developed the capability to employ rail transport to a variety of crude oil markets.

Natural Gas Storage Facilities

The Company has operated a 25 bcf natural gas storage facility at Hussar, Alberta since 2000.

Commodity Marketing