UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

FORM 10-K

FOR THE FISCAL YEAR ENDED DECEMBER 31 , 2022

Commission File Number 1-2958

(Exact name of registrant as specified in its charter)

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |||||||

| (Address of principal executive offices) | (Zip Code) | |||||||

| (Registrant's telephone number, including area code) | ||||||||

| SECURITIES REGISTERED PURSUANT TO SECTION 12(b) OF THE ACT: | ||||||||

| Title of each Class | Trading Symbol(s) | Name of Exchange on which Registered | ||||||

| | ||||||||

| SECURITIES REGISTERED PURSUANT TO SECTION 12(g) OF THE ACT: | ||||||||

| NONE | ||||||||

| Indicate by check mark | ||||||||||||||||||||||||||

• | if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. | ☑ | No | ☐ | ||||||||||||||||||||||

• | if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934. | Yes | ☐ | ☑ | ||||||||||||||||||||||

• | whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such report), and (2) has been subject to such filing requirements for the past 90 days. | ☑ | No | ☐ | ||||||||||||||||||||||

• | whether the registrant has submitted electronically every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). | ☑ | No | ☐ | ||||||||||||||||||||||

• | whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer”, “smaller reporting company” and "emerging growth company" in Rule 12b-2 of the Exchange Act. | |||||||||||||||||||||||||

| ☑ | Accelerated filer ☐ | Non-accelerated filer ☐ | Smaller reporting company | |||||||||||||||||||||||

| Emerging growth company | If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standard provided pursuant to Section 13(a) of the Exchange Act. ☐ | |||||||||||||||||||||||||

• | whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. | |||||||||||||||||||||||||

• | whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements.(1) | ☐ | ||||||||||||||||||||||||

• | whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b).(1) | ☐ | ||||||||||||||||||||||||

•whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). | Yes | ☐ | No | |||||||||||||||||||||||

(1) Per SEC guidance, this blank checkbox is included on this cover page but no disclosure with respect thereto shall be made until the adoption and effectiveness of related stock exchange listing standards.

The aggregate market value of the voting and non-voting stock held by non-affiliates of the registrant as of June 30, 2022 was $9,535,164,630 *. The number of shares outstanding of Hubbell Common Stock as of February 3, 2023 is 53,600,592 .

DOCUMENTS INCORPORATED BY REFERENCE

*Calculated by excluding all shares held by Executive Officers and Directors of registrant without conceding that all such persons or entities are “affiliates” of registrant for purpose of the Federal Securities Laws.

| Table of contents | ||||||||

| Reserved | ||||||||

2 | HUBBELL INCORPORATED - Form 10-K | ||||

| PART I | ||

ITEM 1 Business

Hubbell Incorporated (herein referred to as “Hubbell”, the “Company”, the “registrant”, “we”, “our” or “us”, which references shall include its divisions and subsidiaries as the context may require) was founded as a proprietorship in 1888, and was incorporated in Connecticut in 1905. Recognized for our innovation, quality, and deep commitment to serving our customers for over 130 years, Hubbell is a world-class manufacturer of electrical and utility solutions, with more than 75 brands used around the world. We provide utility and electrical solutions that enable our customers to operate critical infrastructure reliably and efficiently, and we empower and energize communities through innovative solutions supporting energy infrastructure In Front of the Meter, on The Edge, and Behind the Meter. In Front of the Meter is where utilities transmit and distribute energy to their customers. The Edge connects utilities with owner/operators and allows energy and data to be distributed back and forth. Behind the Meter is where owners and operators of building and other critical infrastructure consume energy.

Our products are either sourced complete, manufactured or assembled by subsidiaries in the United States, Canada, Puerto Rico, Mexico, the People’s Republic of China (“China”), the United Kingdom (“UK”), Brazil, Australia, Spain and Ireland. Hubbell also participates in joint ventures in Hong Kong and the Philippines, and maintains offices in Singapore, Italy, China, India, Mexico, South Korea, Chile, and countries in the Middle East.

The Company’s reporting segments consist of the Utility Solutions segment and the Electrical Solutions segment.

The Company’s annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and all amendments to those reports are made available free of charge through the Investor Relations section of the Company’s website at http://www.hubbell.com as soon as practicable after such material is electronically filed with, or furnished to, the SEC. The information contained on the Company’s website or connected to our website is not incorporated by reference into this Annual Report on Form 10-K and should not be considered part of this report.

Utility Solutions Segment

Hubbell Utility Solutions has leading positions In Front of the Meter and at The Edge. The Utility Solutions segment (58% of consolidated revenues in 2022, 56% in 2021 and 56% in 2020) consists of businesses that design, manufacture, and sell a wide variety of electrical distribution, transmission, substation, and telecommunications products, which support applications In Front of the Meter. This includes utility transmission & distribution (T&D) components such as arresters, insulators, connectors, anchors, bushings, enclosures, cutoffs and switches. The Utility Solutions segment also offers solutions that serve The Edge of the utility infrastructure, including smart meters, communications systems, and protection and control devices. Hubbell Utility Solutions supports the electrical distribution, electrical transmission, water, gas distribution, telecommunications, and solar and wind markets. While Hubbell believes its sales in this area are not materially dependent upon any customer or group of customers, a substantial variability in purchases by electrical utilities would affect this segment.

Products of the Utility Solutions segment are sold under the following brands and/or trademarks:

| • | Aclara® | • | Chance® | • | Anderson® | • | PenCell® | ||||||||||||||||

| • | Fargo® | • | Hubbell® | • | Polycast® | • | Opti-loop Design® | ||||||||||||||||

| • | Quazite® | • | Quadri*sil® | • | Trinetics® | • | Reuel® | ||||||||||||||||

| • | Electro Composites® | • | USCO™ | • | CDR™ | • | RFL Design® | ||||||||||||||||

| • | Hot Box® | • | PCORE® | • | Delmar™ | • | Turner Electric® | ||||||||||||||||

| • | EMC™ | • | Longbow™ | • | Ohio Brass® | • | Meramec® | ||||||||||||||||

| • | Reliaguard® | • | Greenjacket® | • | Armorcast® | • | Beckwith Electric™ | ||||||||||||||||

| • | Continental® | • | R.W. Lyall™ | • | Gas Breaker® | • | AEC™ | ||||||||||||||||

| • | Ripley® | ||||||||||||||||||||||

HUBBELL INCORPORATED - Form 10-K | 3 | ||||

Electrical Solutions Segment

Hubbell Electrical Solutions is positioned Behind the Meter, providing key components to building operators and industrial customers that enable them to manage their energy and operate critical infrastructure more efficiently and effectively. The Electrical Solutions segment (42% of consolidated revenues in 2022, 44% in 2021 and 44% in 2020) comprises businesses that sell stock and custom products including standard and special application wiring device products, rough-in electrical products, connector and grounding products, and lighting fixtures, as well as other electrical equipment.

Products of the Electrical Solutions segment have applications in the light industrial, non-residential, wireless communications, transportation, data center, and heavy industrial markets. Electrical Solutions segment products are typically used in and around industrial, commercial and institutional facilities by electrical contractors, maintenance personnel, electricians, utilities, and telecommunications companies. In addition, certain of our businesses design and manufacture industrial controls and communication systems used in the non-residential and industrial markets. Many of these products are designed such that they can also be used in harsh and hazardous locations where a potential for fire and explosion exists due to the presence of flammable gasses and vapors. Harsh and hazardous products are primarily used in the oil and gas (onshore and offshore) and mining industries. We also offer a variety of lighting fixtures, wiring devices and electrical products that have residential and utility applications, including residential products with Internet-of-Things ("IoT") enabled technologies.

These products are sold under various brands and/or trademarks and are primarily sold through electrical and industrial distributors, home centers, retail and hardware outlets, lighting showrooms and residential product oriented internet sites. Special application products are primarily sold through wholesale distributors to contractors, industrial customers and original equipment manufacturers (“OEMs”). Brands and/or trademarks of products of the Electrical Solutions segment include:

| • | Hubbell® | • | Bell® | • | Raco® | • | Gleason Reel® | • | ACME Electric® | ||||||||||||||||||||

| • | Kellems® | • | TayMac® | • | Hipotronics® | • | Powerohm® | • | EC&M Design® | ||||||||||||||||||||

| • | Bryant® | • | Wiegmann® | • | AccelTex Solutions™ | • | iDevices® | • | Progress Lighting Design® | ||||||||||||||||||||

| • | Burndy® | • | Killark® | • | GAI-Tronics® | • | Connector Products™ | • | Austdac™ | ||||||||||||||||||||

| • | CMC® | • | Hawke™ | • | Chalmit™ | • | PCX™ | ||||||||||||||||||||||

4 | HUBBELL INCORPORATED - Form 10-K | ||||

Information Applicable to Our Business

International Operations

The Company has several operations located outside of the United States. These operations manufacture, assemble and/or procure and market Hubbell products and services for both the Utility Solutions and Electrical Solutions segments.

See Note 21 — Industry Segments and Geographic Area Information in the Notes to Consolidated Financial Statements and Item 1A. Risk Factors relating to manufacturing in and sourcing from foreign countries.

Customers

We have an extensive customer base of distributors, wholesalers, electric utilities, OEMs, electrical contractors, telecommunications companies and retail and hardware outlets. We are not dependent on a single customer, however, our top ten customers account for approximately 43% of our Net sales.

Raw Materials

Raw materials used in the manufacture of Hubbell products primarily include steel, aluminum, brass, copper, bronze, zinc, nickel, plastics, phenolics, elastomers and petrochemicals. Hubbell also purchases certain electrical and electronic components, including solenoids, lighting ballasts, printed circuit boards, integrated circuit chips and cord sets, from a number of suppliers. Hubbell is not materially dependent upon any one supplier for raw materials used in the manufacture of its products and equipment however the cost and supply of these materials may be affected by disruptions in availability of raw materials, components or sourced finished goods. See also Item 7A. Quantitative and Qualitative Disclosures about Market Risk.

Patents

Hubbell has approximately 3,000 active United States and foreign patents covering a portion of its products, which expire at various times. While Hubbell deems these patents to be of value, it does not consider its business to be dependent upon patent protection. Hubbell also licenses products under patents owned by others, as necessary, and grants licenses under certain of its patents.

Working Capital

Inventory, accounts receivable and accounts payable levels, payment terms and, where applicable, return policies are in accordance with the general practices of the electrical products industry and standard business procedures. See also Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations.

Backlog

Substantially all of the backlog existing at December 31, 2022 in the Electrical Solutions segment is expected to be shipped to customers in 2023. In the Utility Solutions segment, the backlog existing at December 31, 2022 includes backlog expected to be shipped during 2023, along with $320 million of backlog of contracts that span multiple years, primarily related to long-term contracts of the Aclara business to deliver and install meters and grid monitoring sensor technology. The backlog of orders believed to be firm at December 31, 2022 was $2,463.4 million compared to $1,848.0 million at December 31, 2021. Although this backlog is important, the majority of Hubbell’s revenues result from sales of inventoried products or products that have short periods of manufacture.

Competition

Hubbell experiences substantial competition in all categories of its business, but does not compete with the same companies in all of its product categories. The number and size of competitors vary considerably depending on the product line. Hubbell cannot specify with precision the number of competitors in each product category or their relative market position. However, some of its competitors are larger companies with substantial financial and other resources. Hubbell considers product performance, reliability, quality and technological innovation as important factors relevant to all areas of its business and considers its reputation as a manufacturer of quality products to be an important factor in its business. In addition, product price, service levels and other factors can affect Hubbell’s ability to compete.

HUBBELL INCORPORATED - Form 10-K | 5 | ||||

Environment

The Company is subject to various federal, state and local government requirements relating to the protection of employee health and safety and the environment. The Company believes that, as a general matter, its policies, practices and procedures are properly designed to prevent unreasonable risk of environmental damage and personal injury to its employees and its customers’ employees and that the handling, manufacture, use and disposal of hazardous or toxic substances are in accordance with environmental laws and regulations.

Like other companies engaged in similar businesses, the Company has incurred or acquired through business combinations, remedial response and voluntary cleanup costs for site contamination, and is a party to product liability and other lawsuits and claims associated with environmental matters, including past production of products containing toxic substances. Additional lawsuits, claims and costs involving environmental matters are likely to continue to arise in the future. However, considering past experience and reserves, the Company does not anticipate that these matters will have a material adverse effect on earnings, capital expenditures, financial condition or competitive position. See also Item 1A. Risk Factors and Note 16 — Commitments and Contingencies in the Notes to Consolidated Financial Statements.

Human Capital

Our commitment to developing our employees is one of four pillars that guide Hubbell as a company. We recruit, hire, and develop talent that meets and anticipates the ever-changing needs of our enterprise, while fostering an inclusive and diverse workplace. Hubbell provides market competitive compensation, health and well-being programs, and retirement benefits based on the countries and markets in which we operate to motivate market-leading performance.

As of December 31, 2022, Hubbell had approximately 16,300 salaried and hourly employees of whom approximately 9,800, or 60% are located in the United States. Approximately 1,800 of these U.S. employees are represented by 8 labor unions. Hubbell considers its labor relations to be satisfactory and regularly engages with its labor unions.

Hubbell is committed to fostering an environment that respects and encourages individual differences, diversity of thought, and talent. We strive to create a workplace where employees feel that their contributions are welcomed and valued, allowing them to fully engage their talents and training in their work, while generating personal satisfaction in their role within Hubbell. Hubbell has created a multi-year, enterprise-wide strategy dedicated to evolving our inclusive culture while addressing underrepresentation where it exists across our company. As of December 31, 2022, 32% of our employees identify as female, and within the United States, 30% identify as female and 45% are racially diverse.

Across the enterprise, there are a variety of ways we invest in our people to learn - on the job, in the classroom, through self-directed learning, or through leadership programs. We have expanded our learning management system (known as Hubbell University) to make new content and training available to our employees. The Company has also expanded leadership development programs to provide career development to employees at all levels and continues to expand its Campus Programs to foster a pipeline of early career talent at Hubbell.

The Company also fosters and encourages its employees to give back to their communities. The Company supports employees’ spirit of volunteerism in their communities throughout the year with its Volunteer Paid Time Off policy, which provides all employees with up to 8 hours of paid time off a year to volunteer with an eligible 501(c)(3) charity of their choice.

As a manufacturing company we focus on protecting the health and safety of our employees. We dedicate resources to track and monitor safety and recordable incidents using an enterprise-wide data management system. Through the Company’s myLife program, the Company provides comprehensive, competitive benefits that retain and support our employees supporting their health, wealth and peace of mind.

In October 2022, as a showing of appreciation to our employees continued excellence, the Company provided all employees globally with a Global Recharge Day. This paid day off provided all employees an opportunity to relax, refresh and recharge.

In 2022, Hubbell conducted an enterprise-wide employee survey, the Elevate Employee Experience Survey to better understand the voices of our employees worldwide. Elevate was the largest survey conducted by the Company and over 80% of Hubbell’s employees responded, providing insights that the Company is translating into action plans.

6 | HUBBELL INCORPORATED - Form 10-K | ||||

Information about our Executive Officers

Name (1) | Age | Present Position | Business Experience | ||||||||

| Gerben W. Bakker | 58 | Chairman of the Board, President and Chief Executive Officer | Present position since May 4, 2021; previously President and Chief Executive Officer since October 1, 2020; previously, President and Chief Operating Officer June 6, 2019 to October 1, 2020; Group President, Power Systems February 1, 2014 to June 6, 2019; Division Vice President, Hubbell Power Systems, Inc. (“HPS”) August 2009 - February 2014; President, HPS Brazil June 2005 - July 2009; Vice President, Sourcing, HPS March 2004 - May 2005. | ||||||||

| William R. Sperry | 60 | Executive Vice President, Chief Financial Officer | Present position since May 5, 2020; previously, Executive Vice President, Chief Financial Officer and Treasurer June 6, 2019 to May 2020; Senior Vice President and Chief Financial Officer June 6, 2012 to June 6, 2019; Vice President, Corporate Strategy and Development August 15, 2008 to June 6, 2012; Managing Director, Lehman Brothers August 2006 to April 2008; various positions, including Managing Director, of J.P. Morgan and its predecessor institutions, 1994-2006; also a member of the board of directors of MSA Safety Incorporated since February 2019. | ||||||||

| Jonathan M. Del Nero | 51 | Vice President, Controller | Present position since January 15, 2021; previously, Assistant Controller June 14, 2014, to January 15, 2021; Executive Director, Financial Reporting, Aetna June 2011 to June 2014; Senior Manager, Technical Accounting, Stanley Black and Decker June 2009 to June 2011; Manager of Accounting Policy, The Hartford September 2008 to June 2009; various positions at CIGNA March 2003 to September 2008. | ||||||||

| Allan J. Connolly | 55 | President, Utility Solutions Segment | Present position since July 1, 2019 (the Utility Solutions Segment was formerly known as the Power Systems Group); previously, President, Aclara February 2018 to June 28, 2019; President and Chief Executive Officer of Aclara May 2014 to February 2018; Chief Operating Officer of Culligan International July 2012 to January 2014; Executive Vice President of Operations, Engineering and N.A. Industrial of Culligan International November 2006 to July 2012; Vice President of Research, Development & Engineering of Culligan International April 2006 to November 2006; General Manager Technology; GE Power & Water March 2003 to April 2006. | ||||||||

| Alyssa R. Flynn | 51 | Chief Human Resources Officer | Present position since February 15, 2022; previously Vice President, Compensation, Benefits & HR Systems from February 2014 to February 2022; Chief of Staff to the Chief Executive Officer from June 2021 to February 2022; various positions, including Vice President, Human Resources, at PepsiCo from 1996 to 2014. | ||||||||

| Katherine A. Lane | 45 | Senior Vice President, General Counsel and Secretary | Present position since May 4, 2021; previously Vice President, General Counsel and Secretary since June 6, 2019; previously, Vice President, Acting General Counsel and Secretary March 2019 to June 6, 2019; Vice President, Associate General Counsel June 2017 to March 2019; Vice President, Legal, Hubbell Commercial & Industrial September 2015 to June 2017; Senior Counsel, Hubbell Electrical Systems May 2014 to September 2015; Corporate General Attorney August 2010 to May 2014. Previously, various positions in private practice in law firms based in Massachusetts and Connecticut. | ||||||||

(1)As of February 9, 2023, there are no family relationships among any of the above executive officers and any of our directors. For information related to our Board of Directors, refer to Item 10. Directors, Executive Officers and Corporate Governance.

HUBBELL INCORPORATED - Form 10-K | 7 | ||||

ITEM 1A Risk Factors

Our business, operating results, financial condition, and cash flows may be affected by a number of factors including, but not limited to those set forth below. Any one of these factors could cause our actual results to vary materially from recent results or future anticipated results. See also Item 7. Management’s Discussion and Analysis — “Executive Overview of the Business” and “Results of Operations”.

COVID-19 Pandemic Risks

Our business and operations, and the operations of our suppliers, have been, and may in the future be adversely affected by epidemics or pandemics such as the COVID-19 pandemic outbreak.

We may face risks related to health epidemics and pandemics or other outbreaks of communicable diseases.

A public health epidemic or pandemic, such as the COVID-19 pandemic, poses the risk that our employees, contractors, suppliers, customers and other business partners may be prevented from conducting business activities for an indefinite period of time, including due to shutdowns that may be requested or mandated by governmental authorities, or that such epidemic may otherwise interrupt or impair business activities.

The COVID-19 pandemic continues to cause disruption to the global economy, including in all of the regions in which we, our suppliers, distributors, business partners, and customers do business. We continue to monitor the pandemic, and while periodic local increases and decreases in COVID-19 cases are likely, generally the restrictions due to and in response to the pandemic continue to relax in most locations. However, the COVID-19 pandemic and efforts to manage it, including those by governmental authorities, have had, and could continue to have, an adverse effect on the economy and our business in many ways. This includes, but is not limited to, global supply chain shortages for materials and component parts used in our products and associated escalating prices. In addition to supply shortages, constrained transportation capacities have led to significant price increases in transportation costs. We expect to continue to be affected by supply chain issues due to factors largely beyond our control, including, a global shortage of semi-conductors, chips and components used in our products, a strain on raw materials and cost inflation, all of which could escalate in future quarters.

Although economic conditions have generally improved since the height of the pandemic, the strength of the economic recovery is uncertain and may vary across industries, customers and from country to country. The ultimate extent and robustness of any economic recovery from the impact of the pandemic imposes a significant degree of uncertainty and complexity, and may adversely affect our operations, customer demand and our costs of production. Failure of economic recovery to continue and adverse or weakening economic conditions may also result in deterioration in the collection of customer accounts receivable, as well as a reduction in sales.

Industry and Economic Risks

Inflation and other adverse conditions may adversely affect our business results of operations and financial condition.

Our operating results can be sensitive to changes in general economic conditions, inflation, economic slowdowns, stagflation and recessions. Our sales are subject to market conditions that may cause customer demand for our products to be volatile and unpredictable, particularly in our Electrical Solutions segment. Product demand can be affected by fluctuations in domestic and international economic conditions, as well as currency fluctuations, commodity costs, and a variety of other factors.

We have recently experienced significant inflationary pressure across much of our business. Global supply chains continue to struggle to keep up with increasing demand due to the lingering impact of the COVID-19 pandemic. The resulting supply chain issues and increased demand have also led to increased freight, labor and commodity costs. In addition, various factors, including the level of economic activity in China and the conflict in Ukraine, has added to the volatility in energy costs. We have had to take various pricing actions to cover the higher costs and protect our margin profile. There can be no assurance that we will be able to maintain our margins in response to further changes in inflationary pressures.

In addition, macroeconomic effects such as increases in interest rates and other measures taken by central banks and other policy makers could have a negative effect on overall economic activity that could reduce our customers’ demand for our products. Adverse changes in demand could impact our business, collection of accounts receivable and our expected cash flow generation from current and acquired businesses, which may adversely impact our financial condition and results of operations.

We operate in markets that are subject to competitive pressures that could affect selling prices or demand for our products.

We compete on the basis of product performance, quality, service and/or price. Competitors' behavior related to these areas could potentially have significant impacts on our financial results. Our competitive strategy is to design and manufacture high quality products at the lowest possible cost. Our strategy is to also increase selling prices to offset rising costs of raw materials and components. Competitive pricing pressures may not allow us to offset some or all of our increased costs through pricing actions. Alternatively, if raw material and component costs decline, the Company may not be able to maintain current pricing levels. Competition could also affect future selling prices or demand for our products which could have an adverse impact on our results of operations, financial condition and cash flows.

8 | HUBBELL INCORPORATED - Form 10-K | ||||

Volatility in currency exchange rates may adversely affect our financial condition, results of operations and cash flows.

Our international operations accounted for approximately 8% of our Net sales in 2022. We are exposed to the effects (both positive and negative) that fluctuating exchange rates have on translating the financial statements of our international operations, most of which are denominated in local currencies, into the U.S. dollar. Fluctuations in exchange rates may affect product demand and reported profits in our international operations. In addition, currency fluctuations may affect the prices we pay suppliers for materials used in our products, along with other local costs incurred in foreign countries for foreign entities with U.S. dollar functional currency. As a result, fluctuating exchange rates may adversely impact our results of operations and cash flows.

Uncertainty about the future of the London Interbank Offer Rate ("LIBOR") may adversely affect our business and financial results.

Our 2021 Credit Facility uses LIBOR as a reference rate, such that the interest due pursuant to such borrowings may be calculated using LIBOR plus an applicable margin (determined by reference to a ratings based grid) or the alternate base rate. In March 2021, the UK’s Financial Conduct Authority, which regulates LIBOR, announced that for most tenors of the USD LIBOR, rates would cease to be published after June 30, 2023, and one-week and two-month LIBOR ceased being published as of December 31, 2021. It is not possible to predict the effect of this announcement, including what alternative reference rates may replace LIBOR in use going forward, and how LIBOR will be determined for purposes of loans, securities and derivative instruments currently referencing it when it ceases to exist. Once LIBOR is no longer available, if lenders have increased costs due to such changes, we may suffer from potential increases in interest rates on our floating rate debt. These uncertainties or their resolution also could negatively impact our funding costs, loan and other asset values, asset-liability management strategies, and other aspects of our business and financial results.

Business and Operational Risks

Our ability to effectively develop and introduce new products could adversely affect our ability to compete.

New product introductions and enhancement of existing products and services are key to the Company’s competitive strategy. The success of new product introductions is dependent on a number of factors, including, but not limited to, timely and successful development of new products, including software development, market acceptance of these products and the Company’s ability to manage the risks associated with these introductions. These risks include development and production capabilities, management of inventory levels to support anticipated demand, the risk that new products may have quality defects in the early stages of introduction, and obsolescence risk of existing products. The Company cannot predict with certainty the ultimate impact new product introductions could have on our results of operations, financial condition or cash flows.

We manufacture and source products and materials from various countries throughout the world. A disruption in the availability, price or quality of these products or materials could adversely affect our operating results.

Our business is subject to risks associated with global manufacturing and sourcing. We use a variety of raw materials in the production of our products including steel, aluminum, brass, copper, bronze, zinc, nickel, plastics, phenolics, elastomers and petrochemicals. We also purchase certain electrical and electronic components, including solenoids, lighting ballasts, printed circuit boards, integrated circuit chips and cord sets from a number of suppliers. Significant shortages in the availability of these materials or significant price increases could increase our operating costs and adversely impact the competitive positions of our products, which could adversely impact our results of operations. See also Risk Factor, “Significant developments from the recent and potential changes in U.S. trade policies could have a material adverse effect on us.”

We rely on materials, components and finished goods that are sourced from or manufactured in foreign countries including Mexico, China, and other international countries. Political instability in any country where we do business could have an adverse impact on our results of operations.

We rely on our suppliers to produce high quality materials, components and finished goods according to our specifications, including timely delivery. There is a risk that products may not meet our quality control procedure specifications which could adversely affect our ability to ship quality products to our customers on a timely basis and, could adversely affect our results of operations.

We may be required to recognize impairment charges for our goodwill and other intangible assets.

As of December 31, 2022, the net carrying value of our goodwill and other intangible assets totaled approximately $2,640.4 million. As required by generally accepted accounting principles, we periodically assess these assets to determine if they are impaired. Impairment of intangible assets may be triggered by developments both within and outside the Company’s control. Deteriorating economic conditions, technological changes, disruptions to our business, inability to effectively integrate acquired businesses, unexpected significant changes or planned changes in use of the assets, intensified competition, divestitures, market capitalization declines and other factors may impair our goodwill and other intangible assets. Any charges relating to such impairments could adversely affect our results of operations in the periods an impairment is recognized.

HUBBELL INCORPORATED - Form 10-K | 9 | ||||

We engage in acquisitions and strategic investments and may encounter difficulty in obtaining appropriate acquisitions and in integrating these businesses.

Part of the Company’s growth strategy involves acquisitions. We have pursued and will continue to seek acquisitions and other strategic investments to complement and expand our existing businesses. The rate and extent to which acquisitions become available may affect our growth rate. The success of these transactions will depend on our ability to integrate these businesses into our operations and realize the planned synergies. We may encounter difficulties in integrating acquisitions into our operations and in managing strategic investments and foreign acquisitions and joint ventures may also present additional risk related to the integration of operations across different cultures and languages. Failure to effectively complete or manage acquisitions may adversely affect our existing businesses as well as our results of operations, financial condition and cash flows.

We may not be able to successfully implement initiatives, including our restructuring activities that improve productivity and streamline operations to control or reduce costs.

Achieving our long-term profitability goals depends significantly on our ability to control or reduce our operating costs. Because many of our costs are affected by factors completely, or substantially outside our control, we generally must seek to control or reduce costs through productivity initiatives. If we are not able to identify and implement initiatives that control or reduce costs and increase operating efficiency, or if the cost savings initiatives we have implemented to date do not generate expected cost savings, our financial results could be adversely affected. Our efforts to control or reduce costs may include restructuring activities involving workforce reductions, facility consolidations and other cost reduction initiatives. If we do not successfully manage our current restructuring activities, or any other restructuring activities that we may undertake in the future, expected efficiencies and benefits may be delayed or not realized, and our operations and business could be disrupted, which could have an adverse effect on our results of operations, financial condition and cash flows.

We are subject to risks surrounding our information technology systems failures, network disruptions, breaches in data security and compliance with data privacy laws or regulations.

We are highly dependent on various software and information technology systems to record and process operational, human resources and financial transactions. The proper functioning of Hubbell’s information technology systems is critical to the successful operation of our business. Our information technology systems are susceptible to cyber threats, malware, phishing attacks, break-ins and similar events, breaches of physical security or tampering and manipulation of these systems by employees or unauthorized third parties. Information security risks also exist with respect to the use of portable electronic devices, such as smartphones and laptops, which are particularly vulnerable to loss and theft. Hubbell may also be subject to disruptions of any of our systems and our vendor's systems arising from events that are wholly or partially beyond our control, such as natural disasters, acts of terrorism, cyber-attacks, computer viruses, and electrical/telecommunications outages or failures. All of these risks are also applicable where Hubbell relies on outside vendors to provide services, which may operate in an online, or “cloud,” environment. A failure of our information technology systems could adversely affect our ability to process orders, maintain proper levels of inventory, collect accounts receivable and pay expenses; all of which could have an adverse effect on our results of operations, financial condition and cash flows. In addition, security breaches could result in unauthorized disclosure of confidential information that may result in financial or reputational damage to the Company, as well as expose the Company to litigation and regulatory enforcement actions.

Hubbell also provides customers with solutions that include software components that allow for the control and/or the communication of data from those solutions to Hubbell or customer systems. In addition to the risks noted above, there are other risks associated with these solutions. For example, control and/or data from these solutions may be integral to a customer's operations. A failure of our technology to operate as designed or as a result of cyber threats could impact those operations, including by loss or destruction of data. Likewise, a customer’s failure to properly configure its own network are outside of the Company’s control and could result in a failure in functionality or security of our technology.

10 | HUBBELL INCORPORATED - Form 10-K | ||||

Hubbell is also subject to an increasing number of evolving data privacy and security laws and regulations that impose requirements on the Company and our technology prior to certain use or transfer, storing, processing, disclosure, and protection of data and prior to sale or use of certain technologies. Failure to comply with such laws and regulations could result in the imposition of fines, penalties and other costs. For example, the European Union’s implementation of the General Data Protection Regulation in 2018, the European Union’s pending ePrivacy Regulation and the implementation of the ePrivacy Directive by the various European Union member states, and California’s implementation of its Consumer Privacy Act of 2018 and Connected Device Privacy Act of 2018, as well as data privacy statutes implemented by other states, could all disrupt our ability to sell products and solutions or use and transfer data because such activities may not be in compliance with applicable law in certain jurisdictions.

We have continued to work on improving our utilization of our enterprise resource planning system, expanding standardization of business processes and performing implementations at our remaining businesses, as well as acquired businesses. We expect to incur additional costs related to future implementations, process reengineering efforts as well as enhancements and upgrades to the system. These system modifications and implementations could result in operating inefficiencies which could adversely impact our operating results and/or our ability to perform necessary business transactions.

System failures, ineffective system implementation or disruptions, failure to comply with data privacy and security laws or regulations, IT system risk arising from the Company's acquisition activity or the compromise of security with respect to internal or external systems or portable electronic devices could damage the Company’s systems or infrastructure, subject us to liability claims, or regulatory fines, penalties, or intervention, harm our reputation, interrupt our operations, disrupt customer operations, and adversely affect the Company’s internal control over financial reporting, business, financial condition, results of operations, or cash flows.

Our ability to access capital markets or failure to maintain our credit ratings may adversely affect our business.

Our ability to invest in our business and make strategic acquisitions may require access to the capital markets. If general economic and capital market conditions deteriorate significantly, it could impact our ability to access capital. Failure to maintain our credit ratings could also impact our ability to access credit markets and could increase our cost of borrowing. The capital and credit markets could deteriorate and market conditions could make it more difficult for us to access capital to finance our investments and acquisitions, which could adversely affect our results of operations, financial condition and cash flows.

Deterioration in the credit quality of our customers could have a material adverse effect on our operating results and financial condition.

We have an extensive customer base of distributors, wholesalers, electric utilities, OEMs, electrical contractors, telecommunications companies and retail and hardware outlets. We are not dependent on a single customer, however, our top ten customers account for approximately 43% of our Net sales. Deterioration in the credit quality of several major customers could adversely affect our results of operations, financial condition and cash flows.

We have outstanding indebtedness; our indebtedness will increase if we incur additional indebtedness in the future and do not retire existing indebtedness.

We have outstanding indebtedness and other financial obligations and significant unused borrowing capacity. Our indebtedness level and related debt service obligations could have negative consequences, including (i) requiring us to dedicate significant cash flow from operations to the payment of principal and interest on our indebtedness, which would reduce the funds we have available for other purposes, (ii) reducing our flexibility in planning for or reacting to changes in our business and market conditions and (iii) exposing us to interest rate risk since a portion of our debt obligations are at variable rates.

We may incur significantly more indebtedness in the future. If we add new indebtedness and do not retire existing indebtedness, the risks described above could increase.

If the underlying investments of our defined benefit plans do not perform as expected, we may have to make additional contributions to these plans.

We sponsor certain pension and other postretirement defined benefit plans. The performance of the financial markets and interest rates impact these plan expenses and funding obligations. Significant changes in market interest rates, investment losses on plan assets and reductions in discount rates may increase our funding obligations and could adversely impact our results of operations, cash flows, and financial condition. Furthermore, there can be no assurance that the value of the defined benefit plan assets will be sufficient to meet future funding requirements.

HUBBELL INCORPORATED - Form 10-K | 11 | ||||

Legal, Tax and Regulatory Risks

Changes in tax law relating to multinational corporations could adversely affect our tax position.

Government agencies, and the Organisation for Economic Co-operation and Development (“OECD”) have focused on issues related to the taxation of multinational corporations. One example is in the area of “base erosion and profit shifting,” for which the OECD has released several components of its comprehensive plan that have been adopted and expanded by many taxing authorities to address perceived tax abuse and inconsistencies between tax jurisdictions. As a result, the tax laws in countries in which we do business could change on a prospective or retroactive basis, and any such changes could adversely affect our business and financial statements.

Because tax laws and regulations are subject to interpretation and uncertainty, tax payments may ultimately differ from amounts currently recorded by the Company.

We are subject to income taxes as well as non-income based taxes, in both the United States and numerous foreign jurisdictions. The determination of the Company's worldwide provision for income taxes and other tax liabilities requires judgment and is based on diverse legislative and regulatory structures that exist in the various jurisdictions where the company operates. The ultimate tax outcome may differ from the amounts recorded in the Company's financial statements and may adversely affect the Company's financial results for the period when such determination is made. We are subject to ongoing tax audits in various jurisdictions. Tax authorities may disagree with certain positions we have taken and assess additional taxes. We regularly assess the likely outcomes of these audits in order to determine the appropriateness of our tax provisions. However, there can be no assurance that we will accurately predict the outcomes of these audits, and the future outcomes of these audits could adversely affect our results of operations, financial condition and cash flows.

Significant developments from the recent and potential changes in U.S. trade policies could have a material adverse effect on us.

Over the last five years, the U.S. government has announced and, in some cases, implemented a new approach to trade policy, including renegotiating, or potentially terminating, certain existing bilateral or multi-lateral trade agreements, such as the North American Free Trade Agreement ("NAFTA"), which was replaced by the U.S.-Mexico-Canada Agreement, on July 1, 2020, and proposed trade agreements, like the Trans-Pacific Partnership ("TPP"), from which the United States has formally withdrawn, as well as implementing the imposition of additional tariffs on certain foreign goods, including finished products and raw materials such as steel and aluminum. Changes in the U.S. trade policy, U.S. social, political, regulatory and economic conditions or in laws and policies governing foreign trade, manufacturing, development and investment in the territories and countries where we currently manufacture and sell products, and any resulting negative sentiments towards the United States as a result of such changes, could have an adverse effect on our business. In addition, we cannot predict what changes to trade policy will be made by the current presidential administration and Congress, including whether existing tariff policies will be maintained or modified or whether the entry into new bilateral or multilateral trade agreements will occur, nor can we predict the effects that any conceivable changes would have on our business.

We rely on materials, components and finished goods, such as steel and aluminum, that are sourced from or manufactured in foreign countries, including China and Mexico. Import tariffs and potential import tariffs have resulted or may result in increased prices for these imported goods and materials and, in some cases, may result or have resulted in price increases for domestically sourced goods and materials. Changes in U.S. trade policy have resulted and could result in additional reactions from U.S. trading partners, including adopting responsive trade policies making it more difficult or costly for us to export our products or import goods and materials from those countries. These measures could also result in increased costs for goods imported into the U.S. or may cause us to adjust our worldwide supply chain. Either of these could require us to increase prices to our customers which may reduce demand, or, if we are unable to increase prices, result in lowering our margin on products sold.

In recent years, various countries, and regions, including, without limitation, China, Mexico, Canada and Europe, have announced plans or intentions to impose or have imposed tariffs on a wide range of U.S. products in retaliation for new U.S. tariffs. These actions could, in turn, result in additional tariffs being adopted by the U.S. These conditions and future actions could have a significant adverse effect on world trade and the world economy. To the extent that trade tariffs and other restrictions imposed by the United States increase the price of, or limit the amount of, raw materials and finished goods imported into the United States, the costs of our raw materials may be adversely affected and the demand from our customers for products and services may be diminished, which could adversely affect our revenues and profitability.

12 | HUBBELL INCORPORATED - Form 10-K | ||||

We cannot predict future trade policy or the terms of any renegotiated trade agreements and their impacts on our business. The adoption and expansion of trade restrictions, the occurrence of a trade war, or other governmental action related to tariffs or trade agreements or policies has the potential to adversely impact demand for our products, our costs, our customers, our suppliers, and the U.S. economy, which in turn could adversely impact our business, financial condition and results of operations.

Our business and results of operations may be materially adversely effected by compliance with import and export laws.

We must comply with various laws and regulations relating to the import and export of products, services and technology from the U.S. and other countries having jurisdiction over our operations, which may affect our transactions with certain customers, business partners and other persons. In certain circumstances, export control and economic sanctions regulations may prohibit the export of certain products, services and technologies and in other circumstances, we may be required to obtain an export license before exporting a controlled item. The length of time required by the licensing processes can vary, potentially delaying the shipment of products or performance of services and the recognition of the corresponding revenue. In addition, failure to comply with any of these regulations could result in civil and criminal, monetary and non-monetary penalties, disruptions to our business, limitations on our ability to import and export products and services and damage to our reputation. Moreover, any changes in export control or sanctions regulations may further restrict the export of our products or services, and the possibility of such changes requires constant monitoring to ensure we remain compliant. Any restrictions on the export of our products or product lines could have a material adverse effect on our competitive position, results of operations, cash flows or financial condition.

The uncertainty surrounding the implementation and effect of Brexit and related negative developments in the European Union and elsewhere could adversely affect our business, financial condition and results of operations.

In 2020, the United Kingdom exited the European Union (“EU”) (commonly referred to as “Brexit”). The long-term effects of Brexit, including the UK's relationship with the EU and other countries, including the U.S., remains unclear. We conduct business in both the UK and EU and shipments from our UK subsidiaries represented 3% of our total Net sales in both 2022 and 2021. Brexit could adversely affect European or worldwide political, regulatory, economic or market conditions and could contribute to instability in political institutions and regulatory agencies. Brexit could also have the effect of disrupting the free movement of goods, services, and people between the UK, the EU and elsewhere. There can be no assurance that any or all of these events, or others that we cannot anticipate at this time, will not have a material adverse effect on our business, financial condition and results of operations.

We could incur significant and/or unexpected costs in our efforts to successfully avoid, manage, defend and litigate intellectual property matters.

The Company relies on certain patents, trademarks, copyrights, trade secrets and other intellectual property of which the Company cannot be certain that others have not and will not infringe upon. Intellectual property litigation could be costly and time consuming and the Company could incur significant legal expenses pursuing these claims against others.

From time to time, we receive notices from third parties alleging intellectual property infringement. Any dispute or litigation involving intellectual property could be costly and time-consuming due to the complexity and the uncertainty of intellectual property litigation. Our intellectual property portfolio may not be useful in asserting a counterclaim, or negotiating a license, in response to a claim of infringement or misappropriation. In addition, as a result of such claims, the Company may lose its rights to utilize critical technology or may be required to pay substantial damages or license fees with respect to the infringed rights or be required to redesign our products at a substantial cost, any of which could negatively impact our operating results. Even if we successfully defend against claims of infringement, we may incur significant costs that could adversely affect our results of operations, financial condition and cash flow. See Item 3 “Legal Proceedings” for a discussion of our legal proceedings.

We are subject to litigation and environmental regulations that may adversely impact our operating results.

We are a party to a number of legal proceedings and claims, including those involving product liability, intellectual property and environmental matters, which could be significant. It is not possible to predict with certainty the outcome of every claim and lawsuit. In the future, we could incur judgments or enter into settlements of lawsuits and claims that could have a materially adverse effect on our results of operations, cash flows, and financial condition. In addition, we maintain insurance coverage with respect to certain claims, which insurance may not provide adequate coverage against such claims. We establish reserves based on our assessment of contingencies, including contingencies related to legal claims asserted against us. Subsequent developments in legal proceedings may affect our assessment and estimates of the loss contingency recorded as a reserve and require us to make additional payments, which could have a materially adverse effect on our results of operations, financial condition and cash flow.

We are also subject to various laws and regulations relating to environmental protection and the discharge of materials into the environment, and we could incur substantial costs as a result of the noncompliance with or liability for clean up or other costs or damages under environmental laws. In addition, we could be affected by future laws or regulations, including those imposed in response to climate change concerns. Environmental laws and regulations have generally become stricter in recent years. Compliance with any future laws and regulations could result in a materially adverse effect on our business and financial results. See Item 3 “Legal Proceedings” for a discussion of our legal proceedings.

HUBBELL INCORPORATED - Form 10-K | 13 | ||||

Our reputation and our ability to conduct business may be impaired by improper conduct by any of our employees, agents or business partners.

We cannot provide absolute assurance that our internal controls and compliance systems will always protect us from acts committed by our employees, agents or business partners that would violate U.S. and/or non-U.S. laws, including the laws governing payments to government officials, bribery, fraud, anti-kickback and false claims rules, competition, export and import compliance, money laundering and data privacy. In particular, the U.S. Foreign Corrupt Practices Act, the U.K. Bribery Act, and similar anti-bribery laws in other jurisdictions generally prohibit companies and their intermediaries from making improper payments to government officials for the purpose of obtaining or retaining business, and we operate in parts of the world that have experienced governmental corruption to some degree. Despite meaningful measures that we undertake to facilitate lawful conduct, which include training and internal control policies, these measures may not always prevent reckless or criminal acts by our employees or agents. Any such improper actions could damage our reputation and subject us to civil or criminal investigation in the United States and in other jurisdictions, could lead to substantial civil and criminal, monetary and non-monetary penalties and could cause us to incur significant legal and investigative fees.

Regulations related to conflict-free minerals may cause us to incur additional expenses and may create challenges with our customers.

The Dodd-Frank Wall Street Reform and Consumer Protection Act contains provisions to improve transparency and accountability regarding the use of “conflict” minerals mined from the Democratic Republic of Congo and adjoining countries (“DRC”). The SEC has established annual disclosure and reporting requirements for those companies who use “conflict” minerals sourced from the DRC in their products. These new requirements could limit the pool of suppliers who can provide conflict-free minerals and as a result, we cannot ensure that we will be able to obtain these conflict-free minerals at competitive prices. Compliance with these new requirements may also increase our costs. In addition, we may face challenges with our customers if we are unable to sufficiently verify the origins of the minerals used in our products.

General Risk Factors

We face the potential harms of natural disasters, terrorism, acts of war, international conflicts or other disruptions to our operations.

Natural disasters, the economic uncertainty resulting from the spread of global pandemics, acts or threats of war or terrorism, international conflicts, and the actions taken by the United States and other governments in response to such events could cause damage to or disrupt our business operations, our suppliers or our customers, and could create political or economic instability, any of which could have an adverse effect on our business. For example, increases in energy demand and supply disruptions caused by the conflict in Ukraine have resulted in significantly higher energy prices, particularly in Europe. Persistent high energy prices and the potential for further supply disruptions, may have an adverse impact on our business. Although it is not possible to predict such events or their consequences, these events could decrease demand for our products, make it difficult or impossible for us to deliver products, or disrupt our supply chain.

Global economic uncertainty could adversely affect us.

During periods of prolonged slow growth, or a downturn in conditions in the worldwide or domestic economies, we could experience reduced orders, payment delays, supply chain disruptions or other factors caused by economic challenges faced by our customers, prospective customers and suppliers. Depending upon their severity and duration, these conditions could have an adverse impact on our results of operations, financial condition and cash flows.

Our success depends on attracting and retaining qualified personnel.

Our ability to sustain and grow our business requires us to hire, retain and develop a highly skilled and diverse management team and workforce. Failure to ensure that we have the depth and breadth of personnel with the necessary skill set and experience, or the loss of key employees, could impede our ability to deliver our growth objectives and execute our strategy.

14 | HUBBELL INCORPORATED - Form 10-K | ||||

ITEM 1B Unresolved Staff Comments

None.

ITEM 2 Properties

As of December 31, 2022, Hubbell’s global headquarters are located in leased office space in Shelton, Connecticut. Other principal administrative offices are in Greenville, South Carolina, Manchester, New Hampshire and St. Louis, Missouri. The Utility Solutions segment operates 3 warehouse facilities and 23 manufacturing facilities globally, totaling approximately 4.4 million square feet. The Electrical Solutions segment operates 7 warehouse facilities and 25 manufacturing facilities globally totaling approximately 5.1 million square feet. The Company believes its manufacturing and warehousing facilities are adequate to carry on its business activities.

HUBBELL INCORPORATED - Form 10-K | 15 | ||||

ITEM 3 Legal Proceedings

Information required by this item is incorporated herein by reference to the section captioned “Notes to Consolidated Financial Statements, Note 16 — Commitments and Contingencies” of this Form 10-K.

ITEM 4 Mine Safety Disclosures

Not applicable.

16 | HUBBELL INCORPORATED - Form 10-K | ||||

| PART II | ||

ITEM 5 Market for the Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities

The Company's Common Stock trades on the New York Stock Exchange under the symbol, "HUBB".

The number of common shareholders of record on February 3, 2023 was 1,205.

Our dividends are declared at the discretion of our Board of Directors. In October 2022, the Company’s Board of Directors approved an increase in the common stock dividend rate from $1.05 to $1.12 per share per quarter. The increased quarterly dividend payment commenced with the December 15, 2022 payment made to the shareholders of record on November 30, 2022.

The information required by Item 5 with respect to securities authorized for issuance under equity compensation plans is incorporated herein by reference to Part III, Item 12 of this Form 10-K.

Purchases of Equity Securities

On October 23, 2020 the Board of Directors approved a stock repurchase program (the "October 2020 program") that authorized the repurchase of up to $300 million of common stock and expires in October 2023. At December 31, 2022 our remaining share repurchase authorization under the October 2020 program is $106.7 million. On October 21, 2022 the Board of Directors approved a new stock repurchase program (the "October 2022 program") that authorized the repurchase of up to $300 million of common stock and expires in October 2025. There have been no repurchases under the October 2022 program. The Company repurchased $182.0 million and $11.2 million of shares of Common Stock, in 2022 and 2021, respectively. When combined with the $106.7 million of remaining share repurchase authorization under the October 2020 program, we have a total share repurchase authorization of approximately $406.7 million. Subject to numerous factors, including market conditions and alternative uses of cash, we may conduct discretionary repurchases through open market or privately negotiated transactions, which may include repurchases under plans complying with Rules 10b5-1 and 10b-18 under the Securities Exchange Act of 1934, as amended.

The following table summarizes the Company's repurchase activity of common stock during the quarter ended December 31, 2022:

| Period | Total Number of Shares of Common Stock Purchased (a) (000s) | Average Price Paid per share of Common Stock | Approximate Value of Shares that May Yet be Purchased Under the plans (b) (in millions) | Total number of shares purchased as part of the plans (000s) | ||||||||||

| BALANCE AS OF SEPTEMBER 30, 2022 | $ | 138.8 | 888 | |||||||||||

| October 1, 2022 - October 31, 2022 | — | — | $ | 438.8 | 888 | |||||||||

| November 1, 2022 - November 30, 2022 | 133 | $ | 240.14 | $ | 406.7 | 1,021 | ||||||||

| December 1, 2022 - December 31, 2022 | — | — | $ | 406.7 | 1,021 | |||||||||

TOTAL FOR THE QUARTER ENDED DECEMBER 31, 2022(a) | 133 | $ | 240.14 | |||||||||||

(a) Purchased under our October 2020 share repurchase program authorizing the repurchase of up to $300 million shares of common stock, which was publicly announced on October 23, 2020 and expires in October 2023.

(b) As of December 31, 2022, the remaining amount available for share repurchases includes $106.7 million under our October 2020 program and the full amount under our October 2022 program authorizing the repurchase of up to $300 million shares of common stock, which was publicly announced on October 21, 2022 and expires in October 2025.

HUBBELL INCORPORATED - Form 10-K | 17 | ||||

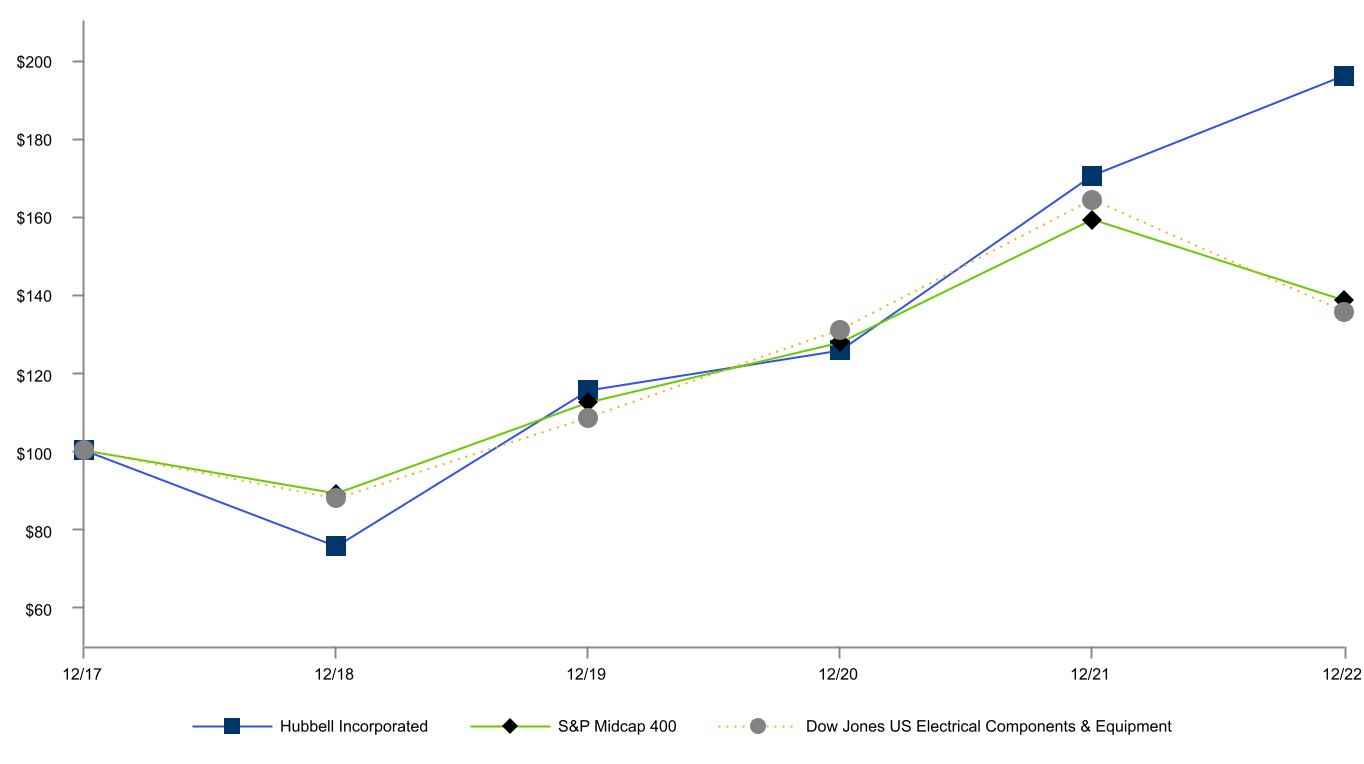

Corporate Performance Graph

The following graph compares the total return to shareholders on the Company’s common stock during the five years ended December 31, 2022, with a cumulative total return on the (i) Standard & Poor’s MidCap 400 (“S&P MidCap 400”) and (ii) the Dow Jones U.S. Electrical Components & Equipment Index (“DJUSEC”). The Company is a member of the S&P MidCap 400. The comparison assumes $100 was invested on December 31, 2017 in the Company’s Common Stock and in each of the foregoing indices and assumes reinvestment of dividends.

COMPARISON OF 5 YEAR CUMULATIVE TOTAL RETURN

Among Hubbell Incorporated, the S&P MidCap 400 Index

and the Dow Jones US Electrical Components & Equipment Index

| 12/17 | 12/18 | 12/19 | 12/20 | 12/21 | 12/22 | |||||||||||||||

| Hubbell, Inc. | 100.00 | 75.39 | 115.22 | 125.48 | 170.14 | 195.74 | ||||||||||||||

| S&P Midcap 400 | 100.00 | 88.92 | 112.21 | 127.54 | 159.12 | 138.34 | ||||||||||||||

| Dow Jones US Electrical Components & Equipment | 100.00 | 87.73 | 108.51 | 131.02 | 164.23 | 135.50 | ||||||||||||||

18 | HUBBELL INCORPORATED - Form 10-K | ||||

ITEM 6 [Reserved]

HUBBELL INCORPORATED - Form 10-K | 19 | ||||

ITEM 7 Management’s Discussion and Analysis of Financial Condition and Results of Operations

The following discussion should be read in conjunction with the consolidated financial statements and accompanying notes included in Part II, Item 8 of this Annual Report on Form 10-K. This section of this Form 10-K generally discusses 2022 and 2021 items and year-to-year comparisons between 2022 and 2021. Discussions of 2020 items and year-to-year comparisons between 2021 and 2020 are not included in this Form 10-K and can be found in "Management's Discussion and Analysis of Financial Condition and Results of Operations" in Part II, Item 7 of the Company's Annual Report on Form-10-K for the fiscal year ended December 31, 2021 filed with the Securities and Exchange Commission on February 11, 2022.

Executive Overview of the Business

Hubbell is a global manufacturer of quality electrical products and utility solutions for a broad range of customer and end market applications. We provide utility and electrical solutions that enable our customers to operate critical infrastructure reliably and efficiently, and we empower and energize communities through innovative solutions supporting energy infrastructure In Front of the Meter, on The Edge, and Behind the Meter. In Front of the Meter is where utilities transmit and distribute energy to their customers. The Edge connects utilities with owner/operators and allows energy and data to be distributed back and forth. Behind the Meter is where owners and operators of buildings, industrial facilities and other critical infrastructure consume energy. Products are either sourced complete, manufactured or assembled by subsidiaries in the United States, Canada, Puerto Rico, Mexico, China, the UK, Brazil, Australia, Spain and Ireland. The Company also participates in joint ventures in Hong Kong and the Philippines, and maintains offices in Singapore, Italy, China, India, Mexico, South Korea, Chile, and countries in the Middle East. The Company employed approximately 16,300 individuals worldwide as of December 31, 2022.

Our reporting segments consist of the Utility Solutions segment, that has leading position in Front of the Meter and at The Edge and the Electrical Solutions segment that is positioned Behind the Meter.

Our long-term strategy is to serve our customers with reliable and innovative electrical and related infrastructure solutions with desired brands and high-quality service, delivered through a competitive cost structure; to complement organic revenue growth with acquisitions that enhance its product offerings; and to allocate capital effectively to create shareholder value.

Our strategy to complement organic revenue growth with acquisitions is focused on acquiring assets that extend our capabilities, expand our product offerings, and present opportunities to compete in core, adjacent or complementary markets. Our acquisition strategy also provides the opportunity to advance our revenue growth objectives during periods of weakness or inconsistency in our end-markets.

Our strategy to deliver products through a competitive cost structure has resulted in past and ongoing restructuring and related activities. Our restructuring and related efforts include the consolidation of manufacturing and distribution facilities, and workforce actions, as well as streamlining and consolidating our back-office functions. The primary objectives of our restructuring and related activities are to optimize our manufacturing footprint, cost structure, effectiveness and efficiency of our workforce.

Productivity improvement also continues to be a key area of focus for the Company and efforts to drive productivity complement our restructuring and related activities to minimize the impact of rising material costs and other administrative cost inflation. Because material costs are approximately two thirds of our cost of goods sold, volatility in this area can significantly impact profitability. Our goal is to have pricing and productivity programs that offset material and other inflationary cost increases as well as pay for investments in key growth areas.

Productivity programs affect virtually all functional areas within the Company by reducing or eliminating waste and improving processes. We continue to expand our efforts related to global product and component sourcing and supplier cost reduction programs. Value engineering efforts, product transfers and the use of lean process improvement techniques are expected to continue to increase manufacturing efficiency. In addition, we continue to build upon the benefits of our enterprise resource planning system across all functions.

20 | HUBBELL INCORPORATED - Form 10-K | ||||

Our sales are also subject to market conditions that may cause customer demand for our products to be volatile and unpredictable, particularly in our Electrical Solutions segment. Product demand can be affected by fluctuations in domestic and international economic conditions, as well as currency fluctuations, commodity costs, and a variety of other factors. We have recently experienced significant inflationary pressure across much of our business. We have had to take various pricing actions to cover the higher costs and protect our margin profile. Because we expect inflation to remain a factor for the foreseeable future, we expect to continue these pricing actions subject, however, to demand and market conditions. Accordingly, there can be no assurance that we will be able to maintain our margins in response to the continuation or worsening of inflationary pressures. In addition, macroeconomic effects such as increases in interest rates and other measures taken by central banks and other policy makers could have a negative effect on overall economic activity that could reduce our customers’ demand for our products.

Discontinued Operations

On February 1, 2022, the Company completed the sale of the Commercial and Industrial Lighting business (the "C&I Lighting business") to GE Current, a Daintree Company. The disposal of the C&I Lighting business met the criteria set forth in ASC 205-20 to be presented as a discontinued operation. The C&I Lighting businesses' results of operations and the related cash flows have been reclassified to income from discontinued operations in the Consolidated Statements of Income and cash flows from discontinued operations in the Consolidated Statement of Cash Flows, respectively, for all periods presented. For additional information regarding this transaction and its effect on our financial reporting, see Note 2 – Discontinued Operations, in the accompanying Consolidated Financial Statements, which note is incorporated herein by reference.

Impact of the COVID-19 Pandemic

Notwithstanding a general improvement in conditions and reduction of adverse effects from the COVID-19 pandemic that began in the first quarter of 2020, as of December 31, 2022 there continues to be significant uncertainty around the scope, severity, and duration of the pandemic, as well as the breadth and duration of business disruptions related to it and the overall impact on the U.S., global economies, and our operating results in future periods.

Additionally, as economies have re-opened, global supply chains have struggled to keep up with increasing demand, and the resulting supply chain disruptions have, in certain cases, affected our ability to ship finished products in a timely manner. These supply chain disruptions and the increase in demand have also led to increased freight, labor and commodity costs, which are expected to persist into 2023.

HUBBELL INCORPORATED - Form 10-K | 21 | ||||

Results of Operations

Our operations are classified into two reportable segments: Utility Solutions and Electrical Solutions. For a complete description of the Company’s segments, see Part I, Item 1 of this Annual Report on Form 10-K. Within these segments, Hubbell serves customers in five primary end markets: utility T&D components, utility communications and controls, non-residential, residential, and industrial.

In 2022, Net sales increased by 18.0% or $754 million and organic Net sales(1) increased by 17.5% or $732 million on favorable price realization along with higher volumes, as further discussed in segment results below. Operating margin increased in 2022, by 160 basis points and adjusted operating margin(1) increased by 140 basis points, driven by price realization that exceeded material cost inflation, higher unit volume and savings from our restructuring and related actions, partially offset by higher freight, logistics and manufacturing costs, as well as other inflationary cost increases in excess of productivity and increased investment in our business. Net income from Continuing Operations attributable to Hubbell increased by 40.1% in 2022 compared to the prior year and diluted earnings per share from Continuing Operations increased by 41.6%. Adjusted net income from continuing operations attributable to Hubbell(1) increased by 30.3% in 2022 compared to the prior year and adjusted diluted earnings per share from continuing operations(1) increased by 31.9% in 2022.

Free cash flow(2) was higher in 2022 at $506.9 million as compared to $423.5 million in the prior year. In 2022 we paid $229.6 million in shareholder dividends, an increase of 5.9% as compared to the prior year, while also repurchasing $182 million of shares in 2022.

(1) Organic Net sales, adjusted operating margin, adjusted net income from continuing operations attributable to Hubbell and adjusted diluted earnings per share from continuing operations are non-GAAP financial measures. See "Adjusted Operating Measures" below for a reconciliation to the comparable GAAP financial measures.

(2) Free cash flow is a non-GAAP financial measure. See "Adjusted Operating Measures" and "Financial Condition, Liquidity and Capital Resources - Cash Flow" below for a reconciliation to the comparable GAAP financial measure.