UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

|

|

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended

OR

|

|

TRANSITION REPORT PURSUANT TO SECTION 13 or 15 (d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from _________ to _________

Commission file number

(Exact name of Registrant as specified in its charter)

|

|

|

|

(State or other jurisdiction of |

(I.R.S. Employer |

|

|

|

|

(Address of principal executive offices) |

(Zip Code) |

Registrant’s telephone number, including area code: (

Securities registered pursuant to Section 12(b) of the Act:

|

Title of each class |

Trading Symbol |

Name of each exchange on which registered |

||

|

|

|

|

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the Registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐

F

Indicate by check mark if the Registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Indicate by check mark whether the Registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

Indicate by check mark whether the Registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

|

Large accelerated filer ☐ |

|

Non-accelerated filer ☐ |

Smaller reporting company |

|

Emerging growth company |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the Registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report.

if securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark whether the Registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes

The aggregate market value of the common shares, without par value, of The Gorman-Rupp Company held by non-affiliates based on the closing sales price as of June 30, 2022 was approximately $

On March 8, 2023, there were

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the Notice of 2023 Annual Meeting of Shareholders and related Proxy Statement are incorporated by reference into Part III (Items 10-14).

|

The Gorman-Rupp Company and Subsidiaries

Annual Report on Form 10-K For the Year Ended December 31, 2022

|

||

|

PART I |

Page |

|

|

ITEM 1. |

Business |

3 |

|

ITEM 1A. |

Risk Factors |

6 |

|

ITEM 1B. |

Unresolved Staff Comments |

11 |

|

ITEM 2. |

Properties |

11 |

|

ITEM 3. |

Legal Proceedings |

12 |

|

ITEM 4. |

Mine Safety Disclosure |

12 |

|

* |

Information about our Executive Officers |

12 |

|

PART II |

||

|

ITEM 5. |

Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities |

13 |

|

ITEM 6. |

[Reserved] |

14 |

|

ITEM 7. |

Management’s Discussion and Analysis of Financial Condition and Results of Operations |

15 |

|

ITEM 7A. |

Quantitative and Qualitative Disclosures about Market Risk |

24 |

|

ITEM 8. |

Financial Statements and Supplementary Data |

25 |

|

ITEM 9. |

Changes in and Disagreements with Accountants on Accounting and Financial Disclosure |

54 |

|

ITEM 9A. |

Controls and Procedures |

54 |

|

ITEM 9B. |

Other Information |

57 |

| ITEM 9C. | Disclosure Regarding Foreign Jurisdictions that Prevent Inspections | 57 |

|

PART III |

||

|

ITEM 10. |

Directors, Executive Officers and Corporate Governance |

57 |

|

ITEM 11. |

Executive Compensation |

57 |

|

ITEM 12. |

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters |

57 |

|

ITEM 13. |

Certain Relationships and Related Transactions, and Director Independence |

58 |

|

ITEM 14. |

Principal Accounting Fees and Services |

58 |

|

PART IV |

||

|

ITEM 15. |

Exhibits and Financial Statement Schedules |

58 |

|

Exhibit Index |

59 |

|

|

ITEM 16. |

Form 10-K Summary |

60 |

|

Signatures |

61 |

|

|

* |

Included pursuant to the instructions to Item 401 of Regulation S-K. |

|

PART I

Cautionary Note Regarding Forward-Looking Statements

In connection with the “safe harbor” provisions of the Private Securities Litigation Reform Act of 1995, The Gorman-Rupp Company provides the following cautionary statement: This Annual Report on Form 10-K contains various forward-looking statements based on assumptions concerning The Gorman-Rupp Company’s operations, future results and prospects. These forward-looking statements are based on current expectations about important economic, political, and technological factors, among others, and are subject to risks and uncertainties, which could cause the actual results or events to differ materially from those set forth in or implied by the forward-looking statements and related assumptions.

Such uncertainties include, but are not limited to, our estimates of future earnings and cash flows, general economic conditions and supply chain conditions and any related impact on costs and availability of materials, integration of the Fill-Rite business in a timely and cost effective manner, retention of supplier and customer relationships and key employees, the ability to achieve synergies and cost savings in the amounts and within the time frames currently anticipated and the ability to service and repay indebtedness incurred in connection with the transaction. Other factors include, but are not limited to: company specific risk factors including (1) loss of key personnel; (2) intellectual property security; (3) acquisition performance and integration; (4) the Company’s indebtedness and how it may impact the Company’s financial condition and the way it operates its business; (5) general risks associated with acquisitions; (6) the anticipated benefits from the Fill-Rite transaction may not be realized; (7) impairment in the value of intangible assets, including goodwill; (8) defined benefit pension plan settlement expense; (9) LIFO inventory method, and (10) family ownership of common equity; and general risk factors including (11) continuation of the current and projected future business environment; (12) highly competitive markets; (13) availability and costs of raw materials and labor; (14) cyber security threats; (15) compliance with, and costs related to, a variety of import and export laws and regulations; (16) environmental compliance costs and liabilities; (17) exposure to fluctuations in foreign currency exchange rates; (18) conditions in foreign countries in which The Gorman-Rupp Company conducts business; (19) changes in our tax rates and exposure to additional income tax liabilities; and (20) risks described from time to time in our reports filed with the Securities and Exchange Commission. Except to the extent required by law, we do not undertake and specifically decline any obligation to review or update any forward-looking statements or to publicly announce the results of any revisions to any of such statements to reflect future events or developments or otherwise.

|

ITEM 1. |

BUSINESS |

The Gorman-Rupp Company (“Registrant”, “Gorman-Rupp”, the “Company”, “we” or “our”) was incorporated in Ohio in 1934. The Company designs, manufactures and globally sells pumps and pump systems for use in water, wastewater, construction, dewatering, industrial, petroleum, original equipment, agriculture, fire supression, heating, ventilating and air conditioning (“HVAC”), military and other liquid-handling applications.

On May 31, 2022, the Company acquired the assets of Fill-Rite and Sotera (“Fill-Rite”), a division of Tuthill Corporation, for $528.0 million. The Company funded the transaction with cash on-hand and new debt. The results of operations for Fill-Rite from the acquisition date are included in the Company’s Consolidated Statements of Income for the year ended December 31, 2022.

PRODUCTS

The Company operates in one business segment, the manufacture and sale of pumps and pump systems. The following table sets forth, for the years 2020 through 2022, the total net sales, income before income taxes and year-end total assets of the Company.

|

(Dollars in thousands) |

||||||||||||

|

2022 |

2021 |

2020 |

||||||||||

|

Net sales |

$ | 521,027 | $ | 378,316 | $ | 348,967 | ||||||

|

Income before taxes |

13,872 | 37,248 | 31,246 | |||||||||

|

Total assets |

872,830 | 420,754 | 394,457 | |||||||||

The Company’s product line consists of pump models ranging in size from 1/4” to nearly 15 feet and ranging in rated capacity from less than one gallon per minute to nearly one million gallons per minute. The types of pumps which the Company produces include self-priming centrifugal, standard centrifugal, magnetic drive centrifugal, axial and mixed-flow, vertical turbine line shaft, submersible, high-pressure booster, rotary gear, rotary vein, diaphragm, bellows and oscillating.

The pumps have drives that range from 1/35 horsepower electric motors up to much larger electric motors or internal combustion engines capable of producing several thousand horsepower. Many of the larger units comprise encased, fully-integrated water and wastewater pumping stations. In certain cases, units are designed for the inclusion of customer-supplied drives.

The Company’s larger pumps are sold principally for use in the construction, industrial, water and wastewater handling fields; for flood control; for boosting low residential water pressure; for pumping refined petroleum products, including the ground refueling of aircraft; for fluid control in HVAC applications; and for various agricultural purposes.

The Company’s pumps are also utilized for dewatering purposes. Additionally, pumps manufactured for fire suppression are used for sprinkler back-up systems, fire hydrants, stand pipes, fog systems and deluge systems at hotels, banks, factories, airports, schools, public buildings and hundreds of other types of facilities throughout the world.

Many of the Company’s smallest pumps are sold to customers for incorporation into such products as food processing, chemical processing, medical applications, waste treatment, HVAC equipment, appliances and solar heating.

MARKETING

The Company’s pumps are marketed in the United States and worldwide through a broad network of distributors, through manufacturers’ representatives (for sales to many original equipment manufacturers), through third-party distributor catalogs, direct sales, and commerce. The Company regularly seeks alliances with distributors and other partners to further enhance marketing opportunities. Export sales are made primarily through foreign distributors and representatives. The Company has long-standing relationships with many of the leading independent distributors in the markets it serves and provides specialized training programs to distributors on a regular basis with a focus on meeting the world’s water and wastewater pumping needs.

During 2022, 2021 and 2020, there were no shipments to any single customer that exceeded 10% of total net sales. Gorman-Rupp continued to actively pursue international business opportunities and, in 2022, shipped its pumps to approximately 130 countries around the world. No sales made to customers in any one foreign country amounted to more than 10% of total net sales for 2022, 2021 or 2020.

COMPETITION

The pump industry is highly fragmented and therefore Gorman-Rupp competes with a large number of businesses. Numerous pump competitors exist as subsidiaries, divisions or departments within significantly larger corporations. The Company also faces increased competition from foreign-sourced pumps in most of the Company’s domestic markets.

Most commercial and industrial pumps are specifically designed and engineered for a particular customer’s application. The Company believes that proper application, product performance, and quality of delivery and service are its principal methods of competition, and attributes its success to its continued emphasis in these areas. In the sale of products and services, the Company benefits from its large base of previously installed products, which periodically require replacement parts due to the critical application and nature of the products and the conditions under which they operate.

PURCHASING AND PRODUCTION

Substantially all of the materials, supplies, components and accessories used by the Company in the fabrication of its products, including all castings (for which most patterns are made and owned by the Company), structural steel, bar stock, motors, solenoids, engines, seals, and plastic and elastomeric components are purchased by the Company from other suppliers and manufacturers. The Company does not purchase materials under long-term contracts and is not dependent upon a single source for any materials, supplies, components or accessories which are of material importance to its business.

The Company purchases motor components for its large submersible pumps, and motors and engines for its pump systems, from a limited number of suppliers, while motors for its polypropylene bellows pumps and magnetic drive pumps are purchased from several alternative vendors. Products requiring small motors are also sourced from alternative suppliers.

The other production operations of the Company consist of the machining of castings, the cutting, shaping and welding of bar stock and structural members, the design and assembly of electrical control panels, the manufacture of some small motors and a few minor components, and the assembling, painting and testing of its products. Substantially all of the Company’s products are tested prior to shipment.

HUMAN CAPITAL

As of December 31, 2022, the Company employed approximately 1,420 persons, of whom approximately 800 were hourly employees. The majority of the Company’s manufacturing operations take place in the United States, as evidenced by 88% of its employees being in the Company’s U.S. locations and 12% of its employees being in its international locations.

Our approach is to develop talent from within and supplement with external hires. We invest resources to develop the talent needed to remain a leading designer and manufacturer of pumps and pump systems. We provide our employees with training opportunities and educational benefits to assist in the expansion of their careers and skills. This approach has resulted in a deep understanding among our employee base of our business, products, and customers. We believe that our average tenure of 10 years, as of the end of 2022, reflects both the strong engagement of our employees and our positive workplace culture. Approximately 8% of our employees operate under a collective bargaining agreement. The Company has never experienced a work stoppage.

We provide competitive compensation and benefits programs to help meet the needs of our employees. In addition to salaries, these programs (which vary by country and region) include profit sharing, a 401(k) plan, medical insurance and benefits, health savings accounts, paid time off, and tuition assistance, among others. Certain domestic employees hired prior to January 1, 2008, and certain union employees, participate in defined benefit plans. Non-union employees hired after this date, in eligible locations, participate in an enhanced 401(k) plan instead of the defined benefit plan. To create performance incentives and to encourage share ownership by our employees, we have implemented an employee stock purchase plan, which enables eligible employees worldwide to purchase the Company’s common shares at a discount through payroll contributions. Because our business involves the manufacturing of products, many of our employees are unable to work from home. For certain positions, we do provide hybrid work from home options.

The health and safety of our workforce is fundamental to the success of our business. We provide our employees upfront and ongoing safety training to ensure that safety policies and procedures are effectively communicated and implemented. We also provide personal protective equipment to those employees who need it to perform their job functions safely. We have experienced personnel on-site at each of our manufacturing locations who are tasked with environmental, health and personal safety education and compliance, and in certain locations we have an on-site nurse available to our employees for medical needs.

We are committed to upholding fundamental human rights and believe that all human beings should be treated with dignity, fairness and respect. This commitment is outlined in our Human Rights Policy which applies to all employees worldwide including part time and temporary workers. We communicated our expectation that suppliers also adhere to our Human Rights Policy through our Supplier Code of Conduct. We strive to promote inclusion and diversity in the workplace, engage with our communities, and encourage our suppliers to treat their employees in a manner that respects human rights. We utilize an on-line platform to provide training to all employees worldwide in key areas such as harassment and discrimination prevention, human rights, and our code of conduct. We also internally publicize the availability of an anonymous ethics hotline through which any employee may report any ethics, safety or other employment concerns.

OTHER ASPECTS

Although the Company owns a number of patents, several of which are important to its business, the Company does not consider its business to be materially dependent upon any one or more patents. The Company’s patents, trademarks and other intellectual property are adequate for its business purposes.

AVAILABLE INFORMATION

The Company maintains a website accessible through its internet address of www.gormanrupp.com. Gorman-Rupp makes available free of charge on or through www.gormanrupp.com its Annual Report to Shareholders, its annual Proxy Statement, its annual report on Form 10-K, its quarterly reports on Form 10-Q, and its current reports on Form 8-K, and any amendments to those reports, as soon as reasonably practicable after those reports (and any amendments) are electronically filed with or furnished to the Securities and Exchange Commission (“Commission”). However, the information contained on the Company’s website is not a part of this Form 10-K or any other report filed with or furnished to the Commission.

A paper copy of the Company’s Form 10-K is also available free of charge upon written request to the Company’s Corporate Secretary.

|

ITEM 1A. |

RISK FACTORS |

Gorman-Rupp’s business and financial performance are subject to various risks and uncertainties, some of which are beyond its control. In addition to the risks discussed elsewhere in this Form 10-K, the following risks and uncertainties could materially adversely affect the Company’s business, prospects, financial condition, results of operations, liquidity and access to capital markets. These risks could cause the Company’s actual results to differ materially from its historical experience and from expected results discussed in forward-looking statements made by the Company related to conditions or events that it anticipates may occur in the future.

COMPANY SPECIFIC RISK FACTORS

Loss of key personnel

The Company’s success depends to a significant extent on the continued service of its executive management team and the ability to recruit, hire and retain other key management personnel to support the Company’s growth and operational initiatives and replace executives who retire or resign. Failure to retain key management personnel and attract and retain other highly-skilled personnel could limit the Company’s global growth and ability to execute operational initiatives, or may result in inefficient and ineffective management and operations, which could harm the Company’s revenues, operations and product development efforts and could eventually result in a decrease in profitability.

Intellectual property security

The Company possesses a wide array of intellectual property rights, including patents, trademarks, copyrights, and applications for the above, as well as other proprietary information. There is a risk that third parties would attempt to copy, in full or in part, the Company’s products, technologies or industrial designs, or to obtain unauthorized access and use of Company technological know-how or other protected intellectual property rights. Also, other companies could successfully develop technologies, products or industrial designs similar to the Company’s, and thus potentially compete with the Company. From time to time, the Company has been faced with instances where competitors have infringed or unfairly used its intellectual property or taken advantage of its design and development efforts. The ability to protect and enforce intellectual property rights varies across jurisdictions. Competitors who attempt to copy the Company’s products, technologies or industrial designs are becoming more prevalent, particularly in Asia. If the Company is unable to adequately enforce and protect its intellectual property rights, it could adversely affect its revenues and profits and hamper its ability to grow.

Competitors and others may also challenge the validity of the Company’s intellectual property or allege that it has infringed their intellectual property, including through litigation. The Company may be required to pay substantial damages if it is determined its products infringe the intellectual property of others. The Company may also be required to develop an alternative, non-infringing product that could be costly and time-consuming, or acquire a license (if available) on terms that are not favorable to it. Regardless of whether infringement claims against the Company are successful, defending against such claims could significantly increase the Company’s costs, divert management’s time and attention away from other business matters, and otherwise adversely affect the Company’s results of operations and financial condition.

Acquisition performance and integration

The Company’s historical growth has depended, and its future growth is likely to continue to depend, in part on its acquisition strategy and the successful integration of acquired businesses into existing operations. The Company intends to continue to seek additional domestic and international acquisition opportunities that have the potential to support and strengthen its operations. The Company cannot assure it will be able to successfully identify suitable acquisition opportunities, prevail against competing potential acquirers, negotiate appropriate acquisition terms, obtain financing that may be needed to consummate such acquisitions, complete proposed acquisitions, successfully integrate acquired businesses into existing operations or expand into new markets. In addition, the Company cannot assure that any acquisition, even if successfully integrated, will perform as planned, be accretive to earnings, or prove to be beneficial to the Company’s operations and cash flows.

The Company incurred substantial indebtedness, which may impact the Company’s financial condition and the way it operates its business

In connection with the Company’s acquisition of the assets of Fill-Rite, the Company incurred substantial indebtedness. Such indebtedness includes senior secured first lien credit facilities comprised of a $350 million term loan facility and a $100 million revolving credit facility, and an unsecured senior subordinated term loan facility in an aggregate principal amount of $90 million. The indebtedness could have important negative consequences, including:

|

● |

higher borrowing costs resulting from fluctuations in our variable benchmark borrowing rates that have adversely affected, and could in the future adversely affect, our interest rates; |

|

● |

reduced availability of cash for the Company’s operations and other business activities after satisfying interest payments and other requirements under the terms of its debt instruments; |

|

● |

less flexibility to plan for or react to competitive challenges, and a competitive disadvantage relative to competitors that do not have as much indebtedness; |

|

● |

difficulty in obtaining additional financing in the future; |

|

● |

inability to comply with covenants in, and potential for default under, the Company’s debt instruments; |

|

● |

inability to operate our business or to take advantage of business opportunities due to restrictions created from the debt covenants; and |

|

● |

challenges to repaying or refinancing any of the Company’s debt. |

The Company’s ability to satisfy its debt and other obligations will depend principally upon its future operating performance. As a result, prevailing economic conditions and financial, business, legal and regulatory and other factors, many of which are beyond the Company’s control, may affect its ability to make payments on its debt and other obligations.

The Company’s operations are subject to the general risks associated with acquisitions

The Company has historically made strategic acquisitions of businesses, such as Fill-Rite, and may do so in the future in support of its strategy. The success of past and future acquisitions is dependent on the Company’s ability to successfully integrate acquired and existing operations. If the Company is unable to integrate acquisitions successfully, its financial results could suffer. Additional potential risks associated with acquisitions are the diversion of management’s attention from other business concerns, additional debt leverage, the loss of key employees and customers of the acquired business, the assumption of unknown liabilities, disputes with sellers, and the inherent risk associated with the Company entering new lines of business.

The anticipated benefits from the Fill-Rite transaction may not be realized

The Company may not realize the full benefits of the increased sales volume and other benefits that are currently expected to result from the Fill-Rite transaction, or realize these benefits within the time frame that is currently expected. In addition, the benefits of the Fill-Rite transaction may be offset by operating losses relating to changes in material or energy prices, inflationary economic conditions, increased competition, or by other risks and uncertainties. If the Company fails to realize the benefits it anticipates from the Fill-Rite transaction, the Company’s results of operations may be adversely affected.

Impairment in the value of intangible assets, including goodwill

The Company’s total assets reflect goodwill from acquisitions, representing the excess cost over the fair value of the identifiable net assets acquired, including other indefinite-lived and finite-lived intangible assets. Goodwill and other indefinite-lived intangible assets are not amortized but are reviewed annually for impairment as of October 1 or whenever events or changes in circumstances indicate there may be a possible permanent loss of value using either a quantitative or qualitative analysis. Finite-lived assets are reviewed for impairment whenever events or changes in circumstances indicate the carrying amount may not be recovered through future net cash flows generated by the assets. If future operating performance at one or more of the Company’s reporting units were to fall significantly below forecast levels or if market conditions for one or more of its acquired businesses were to decline, the Company could be required to incur a non-cash charge to operating income for impairment. Any impairment in the value of these assets could have an adverse non-cash impact on the Company’s reported results of operations.

Defined benefit pension plan settlement expense

The Company sponsors a defined benefit pension plan (“GR Plan”) covering certain domestic employees and accrues amounts for funding of its obligations under the plan. The GR Plan allows eligible retiring employees to receive a lump-sum distribution for benefits earned in lieu of annual payments and most of the Company’s retirees historically have elected this option. Under applicable accounting rules, if the lump-sum distributions made for a plan year exceed an actuarially-determined threshold of the total of the service cost and interest cost for the plan year, the Company at such point would be required to recognize for that year’s results of operations settlement expense for the resulting unrecognized actuarial loss. The Company has been required to make such adjustments, and, if such non-cash adjustments are necessary in future periods, they may negatively impact the Company’s operating results.

In 2022, 2021, and 2020, the Company recorded pre-tax non-cash pension settlement charges of $6.4 million, $2.3 million, and $4.6 million, respectively, driven by lump-sum distributions discussed above. See Note 10 to the Consolidated Financial Statements, Pensions and Other Postretirement Benefits.

LIFO inventory method

The majority of the Company’s inventories are valued on the last-in, first-out (LIFO) method and stated at the lower of cost or market. Current cost approximates replacement cost, or market, and LIFO cost is determined at the end of each fiscal year based on inventory levels on-hand at current replacement cost and a LIFO reserve. The Company uses the simplified LIFO method, under which the LIFO reserve is determined utilizing the inflation factor specified in the Producer Price Index for Machinery and Equipment – Pumps, Compressors and Equipment, as published by the U.S. Bureau of Labor Statistics. Interim LIFO calculations are based on management’s estimate of the expected year-end inflation index and, as such, are subject to adjustment each quarter including the fourth quarter when the inflation index for the year is finalized. If inflation causes the Producer Price Index for Machinery and Equipment – Pumps, Compressors and Equipment to increase in future periods, the LIFO reserve will increase with a corresponding increase to non-cash LIFO expense which may negatively impact the Company’s operating results.

In 2022, 2021, and 2020, the Company recorded pre-tax non-cash LIFO expense of $18.0 million, $6.7 million, and $1.0 million, respectively. See Note 5 to the Consolidated Financial Statements, Inventories.

As of December 31, 2022 we had a LIFO reserve of $88.2 million, which at the current U.S. Corporate tax rate, represents approximately $18.5 million of income taxes, payment of which is delayed to future dates based upon changes in inventory costs. From time-to-time, discussions regarding changes in U.S. tax laws have included the potential of LIFO being repealed. Should LIFO be repealed, the $18.5 million of postponed taxes, plus any future benefit realized prior to the date of repeal, would likely have to be repaid over some period of time. Repayment of these postponed taxes will reduce the amount of cash that we would have available to fund our operations, working capital, capital expenditures, acquisitions, or general corporate or other business activities. This could materially and adversely affect our business, financial condition and results of operations,

Family ownership of common equity

A substantial percentage of the Company’s common shares is held by various members of the Gorman family and their respective affiliates. Because of this concentrated ownership relative to many other publicly-traded companies, the market price of the Company’s common shares may be influenced by lower trading volume and therefore more susceptible to price fluctuations than many other companies’ shares. If any one or more of the Company’s significant shareholders were to sell all or a portion of their holdings of Company common shares at once or within short periods of time, or there was an expectation that such a sale was imminent, then the market price of the Company’s common shares could be negatively affected.

GENERAL RISK FACTORS

Continuation of current and projected future business environment

The overall pump industry is cyclical in nature, and some of its business activity is related to general business conditions in the durable goods and capital equipment markets. Demand for most of the Company’s products and services is affected by the level of new capital investment and planned maintenance expenditures by its customers. The level of such investment and expenditures by our customers depends, in turn, on factors such as general economic conditions, availability of credit, economic conditions within their respective industries and expectations of future market behavior. Volatility or sustained increases in prices of commodities such as oil and agricultural products can negatively affect the levels of investment and expenditures of certain customers and result in postponement of capital investment decisions or the delay or cancellation of existing orders. Inflationary economic conditions may further increase prices and exacerbate these risks. Any of these developments may negatively impact the Company’s sales.

Highly competitive markets

Gorman-Rupp sells its products in highly competitive markets. Maintaining and improving the Company’s competitive position requires periodic investment in manufacturing, engineering, quality standards, marketing, customer service and support, and distribution networks. Even with such investment, the Company may not be successful in maintaining its competitive position. The Company’s competitors may develop products that are superior to its products, or may develop methods of more efficiently and effectively providing products and services, or may adapt more quickly to new technologies or evolving customer requirements. Pricing pressures may require the Company to adjust the prices of its products downward to stay competitive. The Company may not be able to compete successfully with its existing competitors or with new competitors. Failure to compete successfully could negatively impact the Company’s sales, operating margins and overall financial performance.

Availability and costs of raw materials and labor

The Company could be adversely affected by raw material price volatility or an inability of its suppliers to meet quality and delivery requirements. We are required to maintain sufficient inventories to accommodate the needs of our customers, often with short lead times. Our business could be adversely affected if we fail to source and maintain adequate inventory levels. Raw material and energy expenses are substantial drivers of costs in the manufacture of pumps and changes in these costs are often unpredictable. While the Company manufactures certain parts and components used in its products, the Company’s business requires substantial amounts of raw materials, parts and components to be purchased from suppliers. The availability and prices of raw materials, parts and components purchased from the Company’s suppliers may be subject to curtailment or change due to, among other things, suppliers’ allocations to other purchasers, interruptions in production or deliveries by suppliers, changes in exchange rates, tariffs, changes in duty rates and changes in other trade barriers and import and export licensing requirements.

The Company's business depends, in part, upon the adequate recruitment and retention, and continued service of, key managerial, engineering, marketing, sales and technical and operational personnel. Economic conditions may cause an increasingly competitive labor market, which could lead to labor shortages or increased turnover rates within, or increased labor costs to maintain, the Company’s employee base.

These considerations may also impact the operations of the Company’s suppliers, who may seek to pass along any increased costs to the Company. Inflationary economic conditions may further increase these various costs. The Company may not be able to pass along any increased material or labor costs to customers for competitive or other reasons. A change in the availability of, or increases in the costs associated with raw materials, parts and components or labor and workforce could affect our ability to fulfill our customer backlog and materially affect our business, financial condition, results of operations or cash flows.

Cyber security threats

Increased global information technology security threats and more sophisticated and targeted computer crime pose a risk to the security of Gorman-Rupp’s systems and networks and to the confidentiality, availability, and integrity of its data. While the Company attempts to mitigate these risks by employing a number of measures, including employee training, comprehensive monitoring of its networks and systems, and the deployment of backup and protective systems, the Company’s systems, networks, proprietary information, products, solutions and services remain potentially vulnerable to advanced persistent threats. Depending on their nature and scope, such threats could potentially lead to liability for damages or the loss of confidential information including as a result of, but not limited to, the compromising of confidential information relating to customer, supplier, or employee data, improper use of the Company’s systems and networks, manipulation and destruction of data, defective products, production downtimes and operational disruptions which, in turn, could adversely affect Gorman-Rupp’s reputation, competitiveness and results of operations.

Compliance with, and costs related to, a variety of import and export laws and regulations

The Company is subject to a variety of laws and regulations regarding international operations, including regulations issued by the U.S. Department of Commerce Bureau of Industry and Security and various other domestic and foreign governmental agencies. Actual or alleged violations of import-export laws could result in enforcement actions and/or financial penalties. The Company cannot predict the nature, scope or effect of future regulatory requirements to which our international operations and trading practices might be subject or the manner in which existing laws or regulations might be administered or interpreted. Future legislation or regulations could limit the countries in which certain of our products may be manufactured or sold or could restrict our access to, and increase the cost of obtaining, products from foreign sources.

Environmental compliance costs and liabilities

The Company’s operations and properties are subject to numerous domestic and foreign environmental laws and regulations which can impose operating and/or financial sanctions for violations. Moreover, environmental and sustainability initiatives, practices, rules and regulations are under increasing scrutiny of both governmental and non-governmental bodies and may require changes to the Company’s operational practices, standards and expectations and, in turn, increase the Company’s compliance costs. Periodically, the Company has incurred, and it expects to continue to incur, operating and capital costs to comply with environmental requirements. The Company monitors its environmental responsibilities, together with trends in the related laws, and believes it is in substantial compliance with current regulations. If the Company is required to incur increased compliance costs or violates environmental laws or regulations, future environmental compliance expenditures or liabilities could have a material adverse effect on our financial condition, results of operations or cash flows.

Exposure to fluctuations in foreign currency exchange rates

The Company is exposed to fluctuations in foreign currency exchange rates, particularly with respect to the Euro, Canadian Dollar, South African Rand and British Pound. Any significant change in the value of these currencies could affect the Company’s ability to sell products competitively and control its cost structure, which could have a material effect on its financial condition, results of operations or cash flows.

Conditions in foreign countries in which the Company conducts business

In 2022, 27% of the Company’s net sales were to customers outside the United States. The Company expects its international and export sales to continue to be a significant portion of its revenue. The Company’s sales from international operations and export sales are subject, in varying degrees, to risks inherent to doing business outside the United States. These risks include, but are not limited to, the following, some of which are further addressed in our other Risk Factors:

|

● |

Possibility of unfavorable circumstances arising from host country laws or regulations; |

|

● |

Currency exchange rate fluctuations and restrictions on currency repatriation; |

|

● |

Potential negative consequences from changes to taxation policies; |

|

● |

Disruption of operations from labor or political disturbances, or public health crises; |

|

● |

Changes in tariffs, duty rates, and other trade barriers and import and export licensing requirements; |

|

● |

Increased costs and risks of developing, staffing and simultaneously managing a number of global operations as a result of distance as well as language and cultural differences; and |

|

● |

Insurrections, armed conflicts, terrorism or war. |

Any of these events could have an adverse impact on the Company’s business and operations.

Changes in our tax rates and exposure to additional income tax liabilities

Gorman-Rupp is subject to income and other taxes in the United States federal jurisdiction and various local, state and foreign jurisdictions. The Company’s future effective income tax rates could be unfavorably affected by various factors, including changes in the tax rates as well as rules and regulations in relevant jurisdictions. In addition, the amount of income taxes paid is subject to ongoing audits by U.S. federal, state and local tax authorities and by non-U.S. authorities. If these audits result in assessments different from amounts recorded, the Company’s future financial results may include unfavorable adjustments.

|

ITEM 1B. |

UNRESOLVED STAFF COMMENTS |

None.

|

ITEM 2. |

PROPERTIES |

The Company’s corporate headquarters are located in Mansfield, Ohio. The production operations of the Company are conducted at several locations throughout the United States and other countries as set forth below. The Company is a lessee under a number of operating leases for certain real properties, none of which is material to its operations.

The Company’s principal production operations are:

|

United States |

||||

|

Mansfield (two) and Bellville, Ohio |

Royersford, Pennsylvania (two) |

Olive Branch, Mississippi |

||

|

Toccoa, Georgia |

Glendale, Arizona |

Lubbock, Texas |

||

|

Fort Wayne, Indiana |

Lenexa, Kansas |

|||

|

Other Countries |

||||

|

St. Thomas, Ontario, Canada |

County Westmeath, Ireland |

Waardenburg, The Netherlands |

||

|

Johannesburg, South Africa |

Namur, Belgium |

|||

The Company owns a facility in Dallas, Texas comprising a training center and warehouse.

Gorman-Rupp considers its plants, machinery and equipment to be well maintained, in good operating condition and adequate for the present uses and business requirements of the Company.

|

ITEM 3. |

LEGAL PROCEEDINGS |

For over twenty years, numerous business entities in the pump and fluid-handling industries, as well as a multitude of companies in many other industries, have been targeted in a series of lawsuits in several jurisdictions by various individuals seeking redress to claimed injury as a result of the entities’ alleged use of asbestos in their products. Since 2001, the Company and some of its subsidiaries have been involved in this mass-scaled litigation, typically as one of many co-defendants in a particular proceeding. The allegations in the lawsuits involving the Company and/or its subsidiaries have been vague, general and speculative. Most of these lawsuits have been dismissed without advancing beyond the early stage of discovery, some as a result of nominal monetary settlements recommended for payment by the Company's insurers. The claims and related legal expenses generally have been covered by the Company's insurance, subject to applicable deductibles and limitations. Accordingly, this series of lawsuits has not, cumulatively or individually, had a material adverse impact on the Company's consolidated results of operations, liquidity or financial condition, nor is it expected to have any such impact in the future, based on the current knowledge of the Company.

In addition, the Company and/or its subsidiaries are parties in a small number of legal proceedings arising in the ordinary course of business. Management does not currently believe that these proceedings will materially impact the Company’s consolidated results of operations, liquidity or financial condition.

|

ITEM 4. |

MINE SAFETY DISCLOSURE |

Not applicable.

INFORMATION ABOUT OUR EXECUTIVE OFFICERS

The following table sets forth certain information with respect to the executive officers of the Company as of January 31, 2023:

|

Name |

Age |

Office |

Date Elected to Executive Office Position |

|||

|

Jeffrey S. Gorman |

70 |

Executive Chairman |

1998 |

|||

|

Scott A. King |

48 |

President and Chief Executive Officer |

2019 |

|||

|

James C. Kerr |

60 |

Executive Vice President and Chief Financial Officer |

2017 |

|||

|

Brigette A. Burnell |

47 |

Executive Vice President, General Counsel and Corporate Secretary |

2014 |

Mr. Gorman was elected Executive Chairman effective January 1, 2022 after previously serving as Chairman of the Board since April 25, 2019, Chief Executive Officer from May 1, 1998 to December 31, 2021 and as President from 1998 to 2020 after having served as Senior Vice President since 1996. Mr. Gorman also held the position of General Manager of the Gorman-Rupp Pumps USA division from 1989 through 2005. He served as Assistant General Manager from 1986 to 1988; and he held the office of Corporate Secretary from 1982 to 1990. He has served as a Director of the Company continuously since 1989.

Mr. King was elected Chief Executive Officer effective January 1, 2022 in addition to his role as President. Mr. King served as President and Chief Operating Officer since January 1, 2021 after previously serving as Vice President and Chief Operating Officer since April 25, 2019. Mr. King also previously served as Vice President of Operations effective March 1, 2018 and as Vice President from April 1, 2017 to February 28, 2018. Mr. King previously held positions with the Gorman-Rupp Pumps USA division of the Company as Vice President and General Manager from January 1, 2014 until March 31, 2017, Vice President of Operations from June 1, 2010 until December 31, 2013, Director of Manufacturing from July 1, 2007 until May 31, 2010 and Manufacturing Manager from November 1, 2004 until June 30, 2007. He has served as a Director of the Company continuously since 2021.

Mr. Kerr was elected Executive Vice President and Chief Financial Officer effective January 1, 2021 after previously serving as Vice President and Chief Financial Officer since March 1, 2018. Mr. Kerr previously served as Chief Financial Officer effective January 1, 2017 and as Vice President of Finance from July 18, 2016 to December 31, 2016. Prior to 2016, Mr. Kerr served as both Executive Vice President and Chief Financial Officer of Jo-Ann Stores from 2006 to 2015 and as Vice President, Controller of Jo-Ann Stores from 1998 to 2006.

Ms. Burnell was elected Executive Vice President, General Counsel and Corporate Secretary effective March 1, 2022 after previously serving as Senior Vice President, General Counsel and Corporate Secretary since January 1, 2021. Ms. Burnell previously served as Vice President, General Counsel and Corporate Secretary effective March 1, 2018, General Counsel effective May 1, 2015, and as Corporate Secretary effective May 1, 2014. Ms. Burnell previously served as Corporate Counsel effective May 1, 2014. Ms. Burnell joined the Company as Corporate Attorney on January 2, 2014. Prior to 2014, Ms. Burnell served as Corporate Counsel of Red Capital Group from 2011 to 2013 and as an Associate at Jones Day from 2002 to 2011.

PART II

|

ITEM 5. |

MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES |

The Company’s Common Stock is listed on the New York Stock Exchange under the ticker symbol “GRC”. On February 1, 2023, there were 1,570 registered holders of the Company’s common shares.

The Company currently expects to continue its exceptional history of paying regular quarterly dividends, and increased annual dividends. However, any future dividends will be reviewed individually and declared by our Board of Directors at its discretion, dependent on an assessment of the Company’s financial condition and business outlook at the applicable time.

PERFORMANCE GRAPH

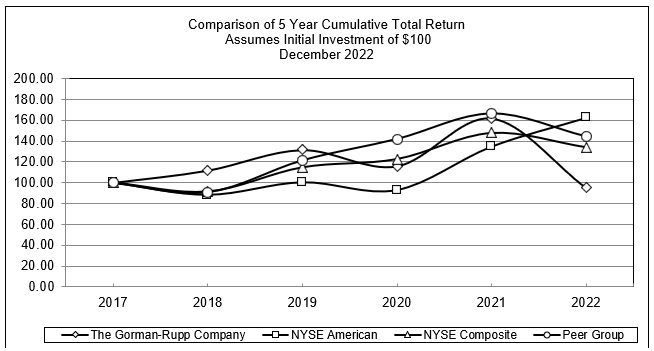

The following stock price performance graph and related table compares the cumulative total returns (assuming reinvestment of dividends) on $100 invested on December 31, 2017 through December 31, 2022 in the Company’s common shares, the NYSE Composite Index, the NYSE American Index and a peer group of companies in the SIC Code 3561 Index — Pumps and Pumping Equipment. The stock price performance graph and related table is not necessarily indicative of future investment performance. This graph is not deemed to be “soliciting material” or “filed” with the SEC or subject to the liabilities of Section 18 of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), and the graph shall not be deemed to be incorporated by reference into any prior or subsequent filing by us under the Securities Act of 1933, as amended, or the Exchange Act.

|

2017 |

2018 |

2019 |

2020 |

2021 |

2022 |

|||||||||||||||||||

|

The Gorman-Rupp Company |

100.00 | 111.78 | 131.52 | 115.91 | 161.92 | 95.23 | ||||||||||||||||||

|

NYSE Composite |

100.00 | 91.20 | 114.67 | 122.69 | 148.06 | 134.22 | ||||||||||||||||||

|

NYSE American |

100.00 | 88.23 | 100.34 | 92.80 | 134.71 | 162.54 | ||||||||||||||||||

|

SIC Code 3561 |

100.00 | 91.06 | 121.51 | 141.94 | 166.38 | 144.49 | ||||||||||||||||||

PURCHASES OF EQUITY SECURITIES

(Amounts in tables in thousands of dollars, except share and per share data)

On October 29, 2021, the Company announced a share repurchase program of up to $50.0 million of the Company’s common shares. Shares may be repurchased from time to time by the Company through a variety of methods, which may include open-market transactions, pre-set trading plans designed in accordance with Rule 10b5-1, privately negotiated transactions, accelerated share repurchase transactions, or any combination of such methods. The actual number of shares repurchased will depend on prevailing market conditions, alternative uses of capital and other factors, and will be determined at management’s discretion. The Company is not obligated to make any purchases under the program, and the program may be suspended or discontinued at any time. The program does not have an expiration date.

|

Period |

Total number of shares purchased |

Average price paid per share |

Total number of shares purchased as part of publicly announced program |

Approximate dollar value of shares that may yet be purchased under the program |

||||||||||||

|

October 1 to October 31, 2022 |

- | - | - | $ | 48,067 | |||||||||||

|

November 1 to November 30, 2022 |

- | - | - | 48,067 | ||||||||||||

|

December 1 to December 31, 2022 |

- | - | - | 48,067 | ||||||||||||

|

Total |

- | - | - | $ | 48,067 | |||||||||||

|

ITEM 6. |

RESERVED |

|

ITEM 7. |

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

(Amounts in tables in thousands of dollars, except for per share data)

Executive Overview

On May 31, 2022, the Company acquired the assets of Fill-Rite and Sotera (“Fill-Rite”), a division of Tuthill Corporation, for $528.0 million. When adjusted for approximately $80.0 million in expected tax benefits, the net transaction value is approximately $448.0 million. The Company funded the transaction with cash on-hand and new debt. The Company incurred $7.1 million of one-time acquisition costs during the year ended December 31, 2022 and does not expect to incur material acquisition costs in connection with the transaction going forward. The results of operations for Fill-Rite from the acquisition date are included in the Company’s Consolidated Statements of Income for the year ended December 31, 2022.

The following discussion of Results of Operations includes certain non-GAAP financial data and measures such as adjusted earnings per share and adjusted earnings before interest, taxes, depreciation and amortization. Adjusted earnings per share is earnings per share excluding non-cash pension settlement charges per share, one-time acquisition costs per share, amortization of step up in value of acquired inventories per share, and amortization of customer backlog per share. Adjusted earnings before interest, taxes, depreciation and amortization is net income (loss) excluding interest, taxes, depreciation and amortization, adjusted to exclude non-cash pension settlement charges, one-time acquisition costs, amortization of step up in value of acquired inventories, amortization of customer backlog, and non-cash LIFO expense. Management utilizes these adjusted financial data and measures to assess comparative operations against those of prior periods without the distortion of non-comparable factors. The inclusion of these adjusted measures should not be construed as an indication that the Company’s future results will be unaffected by unusual or infrequent items or that the items for which the Company has made adjustments are unusual or infrequent or will not recur. Further, the impact of the LIFO inventory costing method can cause results to vary substantially from company to company depending upon whether they elect to utilize LIFO and depending upon which method they may elect. The Gorman-Rupp Company believes that these non-GAAP financial data and measures also will be useful to investors in assessing the strength of the Company’s underlying operations from period to period. These non-GAAP financial measures are not intended to replace GAAP financial measures, and they are not necessarily standardized or comparable to similarly titled measures used by other companies. Provided below is a reconciliation of adjusted earnings per share and adjusted earnings before interest, taxes, depreciation and amortization.

|

2022 |

2021 |

2020 |

||||||||||

|

Adjusted earnings per share: |

||||||||||||

|

Reported earnings per share – GAAP basis |

$ | 0.43 | $ | 1.14 | $ | 0.97 | ||||||

|

Plus pension settlement charge |

0.20 | 0.07 | 0.14 | |||||||||

|

Plus one-time acquisition costs |

0.22 | - | - | |||||||||

|

Plus amortization of step up in value of acquired inventories |

0.04 | - | - | |||||||||

|

Plus amortization of acquired customer backlog |

0.05 | - | - | |||||||||

|

Non-GAAP adjusted earnings per share |

$ | 0.94 | $ | 1.21 | $ | 1.11 | ||||||

|

Adjusted earnings before interest, taxes, depreciation and amortization: |

||||||||||||

|

Reported net income – GAAP basis |

$ | 11,195 | $ | 29,851 | $ | 25,188 | ||||||

|

Plus interest expense |

19,240 | 1 | 18 | |||||||||

|

Plus provision for income taxes |

2,677 | 7,397 | 6,058 | |||||||||

|

Plus depreciation and amortization |

21,158 | 11,914 | 12,692 | |||||||||

|

Non-GAAP earnings before interest, taxes, depreciation and amortization |

54,270 | 49,163 | 43,956 | |||||||||

|

Plus pension settlement charge |

6,427 | 2,304 | 4,583 | |||||||||

|

Plus one-time acquisition costs |

7,088 | - | - | |||||||||

|

Plus amortization of step up in value of acquired inventories |

1,406 | - | - | |||||||||

|

Plus amortization of acquired customer backlog |

1,517 | - | - | |||||||||

|

Plus non-cash LIFO expense |

18,041 | 6,669 | 969 | |||||||||

|

Non-GAAP adjusted earnings before interest, taxes, depreciation and amortization |

$ | 88,749 | $ | 58,136 | $ | 49,508 | ||||||

The Gorman-Rupp Company (“we”, “our”, “Gorman-Rupp” or the “Company”) is a leading designer, manufacturer and international marketer of pumps and pump systems for use in diverse water, wastewater, construction, dewatering, industrial, petroleum, original equipment, agriculture, fire suppression, heating, ventilating and air conditioning (HVAC), military and other liquid-handling applications. The Company attributes its success to long-term product quality, applications and performance combined with timely delivery and service, and continually seeks to develop initiatives to improve performance in these key areas.

We regularly invest in training for our employees, in new product development and in modern manufacturing equipment, technology and facilities all designed to increase production efficiency and capacity and drive growth by delivering innovative solutions to our customers. We believe that the diversity of our markets is a major contributor to the generally stable financial growth we have produced historically.

As a result of the Fill-Rite acquisition, the Company’s cash position decreased $118.4 million during the year ended December 31, 2022 to $6.8 million. The Company generated $88.7 million in adjusted earnings before interest, taxes, depreciation and amortization during the same period. From these earnings, the Company invested $18.0 million primarily in buildings, machinery and equipment and returned $17.9 million in dividends to shareholders.

Capital expenditures in 2022 were $18.0 million and consisted primarily of machinery and equipment and building improvements. Capital expenditures for the full-year 2023 are presently planned to be in the range of $18-$20 million primarily for machinery and equipment purchases, and are expected to be financed through internally-generated funds.

The Company’s backlog of orders was $267.4 million at December 31, 2022 compared to $186.0 million at December 31, 2021, an increase of 43.8%. Fill-Rite added $13.0 million to the backlog at December 31, 2022. The increase in backlog for the year ending December 31, 2022 was primarily driven by strong incoming orders during the year, large municipal orders which are longer term in nature, and the acquisition of Fill-Rite. The backlog aging was consistent with historical levels. Approximately 89% of the Company’s backlog of unfilled orders is scheduled to be shipped during 2023, with the remainder principally during the first half of 2024.

Incoming orders increased 30.6% for the year ending December 31, 2022 compared to the same period in 2021, and 11.2% excluding Fill-Rite.

On January 26, 2023, the Board of Directors authorized the payment of a quarterly dividend of $0.175 per share, representing the 292nd consecutive quarterly dividend to be paid by the Company. During 2022, the Company again paid increased dividends and thereby attained its 50th consecutive year of increased dividends. These consecutive years of increases continue to position Gorman-Rupp in the top 50 of all U.S. public companies with respect to number of years of increased dividend payments. The regular dividend yield at December 31, 2022 was 2.7%.

The Company currently expects to continue its exceptional history of paying regular quarterly dividends and increased annual dividends. However, any future dividends will be reviewed individually and declared by our Board of Directors at its discretion, dependent on our assessment of the Company’s financial condition and business outlook at the applicable time.

Outlook

As we begin our 90th year, our outlook remains positive. We enter 2023 with record backlog and believe the majority of our markets will continue to show growth, particularly those related to infrastructure. We expect our 2023 gross margin to benefit as the pricing actions we have taken throughout 2022 are fully realized and the impact of LIFO and related expense returns to more normal levels. In addition to pursuing earnings growth, we continue to focus on cash flow by improving on our working capital through inventory management without diminishing customer service.

Results of Operations – 2022 Compared to 2021:

Net Sales

|

Year Ended |

||||||||||||||||

|

December 31, |

||||||||||||||||

|

2022 |

2021 |

$ Change |

% Change |

|||||||||||||

|

Net sales |

$ | 521,027 | $ | 378,316 | $ | 142,711 | 37.7 | % | ||||||||

Net sales for 2022 were $521.0 million compared to net sales of $378.3 million for 2021, an increase of 37.7% or $142.7 million. Domestic sales of $381.3 million increased 46.3%, or $120.6 million, and international sales of $139.7 million increased 18.8%, or $22.1 million, compared to 2021. Fill-Rite sales, which are primarily domestic, were $87.4 million from the acquisition date of May 31, 2022 to December 31, 2022.

Excluding Fill-Rite, sales in our water markets increased 15.9% or $42.5 million in 2022 compared to 2021. Sales increased $17.3 million in the fire market, $14.8 million in the municipal market, $6.4 million in the repair market, and $5.1 million in the construction market. Partially offsetting these increases was a decrease of $1.1 million in the agriculture market.

Excluding Fill-Rite, sales in our non-water markets increased 11.7% or $12.8 million in 2022 compared to 2021. Sales increased $13.5 million in the industrial market and $1.9 million in the OEM market. Partially offsetting these increases was a decrease of $2.6 million in the petroleum market.

Cost of Products Sold and Gross Profit

|

Year Ended |

||||||||||||||||

|

December 31, |

||||||||||||||||

|

2022 |

2021 |

$ Change |

% Change |

|||||||||||||

|

Cost of products sold |

$ | 390,090 | $ | 282,419 | $ | 107,671 | 38.1 | % | ||||||||

|

% of Net sales |

74.9 | % | 74.7 | % | ||||||||||||

|

Gross margin |

25.1 | % | 25.3 | % | ||||||||||||

Gross profit was $130.9 million in 2022, resulting in gross margin of 25.1%, compared to gross profit of $95.9 million and gross margin of 25.3% in 2021. The 20 basis point decrease in gross margin was driven by a 280 basis point increase in cost of material, which included an unfavorable LIFO impact of 170 basis points, an unfavorable impact of 30 basis points related to Fill-Rite inventory recorded at fair value and recognized during the second quarter of 2022, and an unfavorable impact of 30 basis points related to the amortization of acquired Fill-Rite customer backlog. The full amount of the step up to record Fill-Rite inventory at fair value was recognized during the second quarter of 2022 and will not recur, while the acquired Fill-Rite customer backlog will be fully amortized within the next two quarters. The increase in cost of material was partially offset by a 260 basis point improvement from labor and overhead leverage due to increased sales volume.

For further discussion on the LIFO inventory costing method, see Note 1 “Summary of Significant Accounting Policies” and Note 5 “Inventories” in the Notes to our Consolidated Financial Statements.

Selling, General and Administrative (SG&A) Expenses

|

Year Ended |

||||||||||||||||

|

December 31, |

||||||||||||||||

|

2022 |

2021 |

$ Change |

% Change |

|||||||||||||

|

Selling, general and administrative expenses |

$ | 83,117 | $ | 56,004 | $ | 27,113 | 48.4 | % | ||||||||

|

% of Net sales |

16.0 | % | 14.8 | % | ||||||||||||

Selling, general and administrative (“SG&A”) expenses were $83.1 million in 2022, which included $7.1 million of one-time acquisition costs. Excluding acquisition costs, SG&A expenses were $76.0 million and 14.6% of net sales in 2022 compared to $56.0 million and 14.8% of net sales in 2021. The decrease in SG&A expenses as a percentage of sales, excluding acquisition costs, was primarily due to leverage from increased sales volume.

Amortization Expense

|

Year Ended |

||||||||||||||||

|

December 31, |

||||||||||||||||

|

2022 |

2021 |

$ Change |

% Change |

|||||||||||||

|

Amortization expense |

$ | 7,637 | $ | 537 | $ | 7,100 | 1,322.2 | % | ||||||||

|

% of Net sales |

1.5 | % | 0.1 | % | ||||||||||||

Amortization expense was $7.6 million in 2022 compared to $0.5 million in 2021. The increase in amortization expense was due to $7.0 million in amortization attributable to the Fill-Rite acquisition.

Operating Income

|

Year Ended |

||||||||||||||||

|

December 31, |

||||||||||||||||

|

2022 |

2021 |

$ Change |

% Change |

|||||||||||||

|

Operating income |

$ | 40,183 | $ | 39,356 | $ | 827 | 2.1 | % | ||||||||

|

% of Net sales |

7.7 | % | 10.4 | % | ||||||||||||

Operating income was $40.2 million in 2022, which included $7.1 million in one-time acquisition costs, $1.4 million of inventory step up amortization, and $1.5 million of acquired customer backlog amortization. Excluding acquisition costs, inventory step up and backlog amortization, operating income was $50.2 million in 2022, resulting in an operating margin of 9.6%, compared to operating income of $39.4 million and operating margin of 10.4% in 2021. The decrease of 80 basis points in operating margin was primarily the result of an unfavorable LIFO impact.

Interest Expense

|

Year Ended |

||||||||||||||||

|

December 31, |

||||||||||||||||

|

2022 |

2021 |

$ Change |

% Change |

|||||||||||||

|

Interest Expense |

$ | 19,240 | $ | - | $ | 19,240 | 100.0 | % | ||||||||

|

% of Net sales |

3.7 | % | - | % | ||||||||||||

Interest expense was $19.2 million in 2022. No interest expense was recorded in 2021. The interest expense was due to debt financing attributable to the Fill-Rite acquisition.

Net Income

|

Year Ended |

||||||||||||||||

|

December 31, |

||||||||||||||||

|

2022 |

2021 |

$ Change |

% Change |

|||||||||||||

|

Income before income taxes |

$ | 13,872 | $ | 37,248 | $ | (23,376 | ) | (62.8 | )% | |||||||

|

% of Net sales |

2.7 | % | 9.8 | % | ||||||||||||

|

Income taxes |

$ | 2,677 | $ | 7,397 | $ | (4,720 | ) | (63.8 | )% | |||||||

|

Effective tax rate |

19.3 | % | 19.9 | % | ||||||||||||

|

Net income |

$ | 11,195 | $ | 29,851 | $ | (18,656 | ) | (62.5 | )% | |||||||

|

% of Net sales |

2.1 | % | 7.9 | % | ||||||||||||

|

Earnings per share |

$ | 0.43 | $ | 1.14 | $ | (0.71 | ) | (62.3 | )% | |||||||

Net income was $11.2 million, or $0.43 per share, in 2022 compared to $29.9 million, or $1.14 per share, in 2021. Adjusted earnings per share in 2022 were $0.94 per share compared to $1.21 per share in 2021. Adjusted earnings per share in 2022 included an unfavorable LIFO impact of $0.56 per share compared to an unfavorable LIFO impact of $0.20 per share in 2021.

The Company’s effective tax rate was 19.3% for 2022 compared to 19.9% for 2021. The effective tax rate for 2022 was impacted by similar benefits from credits and permanent items as the prior year on lower pretax income. We expect our effective tax rate for 2023 to be between 20.0% and 22.0%.

Results of Operations – 2021 Compared to 2020:

Information pertaining to fiscal year 2020 was included in the Company’s Annual Report on Form 10-K for the year ended December 31, 2020 beginning on page 15 under Item 7, “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” which was filed with the SEC on March 1, 2021.

Liquidity and Capital Resources

Our primary sources of liquidity are cash generated from operations and borrowings under our Credit Facility. Cash and cash equivalents totaled $6.8 million at December 31, 2022. The Company had an additional $78.5 million available under the revolving credit facility after deducting $17.0 million drawn and $1.5 million in outstanding letters of credit primarily related to customer orders. During 2022, our debt obligations increased as a result of the Senior Term Loan Facility, revolving Credit Facility and Subordinated Credit Facility entered into in connection with the Fill-Rite transaction. See Note 6 “Financing Arrangements” in the Notes to our Consolidated Financial Statements.

Capital expenditures for 2023, which are expected to consist principally of machinery and equipment purchases, are estimated to be in the range of $18 - $20 million and are expected to be financed through internally generated funds. During 2022, 2021 and 2020, the Company financed its capital improvements and working capital requirements principally through internally generated funds.

The Company contributed $2.3 million to its defined benefit pension plans in 2022 and expects to contribute up to $2.3 million to its defined benefit pension plans in 2023.

Free cash flow, a non-GAAP measure for reporting cash flow, is defined by the Company as adjusted earnings before interest, income taxes and depreciation and amortization, less capital expenditures and dividends. The Company believes free cash flow provides investors with an important perspective on cash available for investments, acquisitions and working capital requirements.

The following table reconciles adjusted earnings before interest, income taxes and depreciation and amortization as reconciled above to free cash flow:

|

2022 |

2021 |

2020 |

||||||||||

|

Non-GAAP adjusted earnings before interest, taxes, depreciation and amortization |

$ | 88,749 | $ | 58,136 | $ | 49,508 | ||||||

|

Less capital expenditures |

(17,986 | ) | (9,751 | ) | (7,999 | ) | ||||||

|

Less cash dividends |

(17,872 | ) | (16,586 | ) | (15,394 | ) | ||||||

|

Non-GAAP free cash flow |

$ | 52,891 | $ | 31,799 | $ | 26,115 | ||||||

Financial Cash Flow

|

Year Ended |

||||||||||||

|

December 31, |

||||||||||||

|

2022 |

2021 |

2020 |

||||||||||

|

Beginning of period cash and cash equivalents |

$ | 125,194 | $ | 108,203 | $ | 80,555 | ||||||

|

Net cash provided by operating activities |

13,685 | 45,438 | 51,162 | |||||||||

|

Net cash used for investing activities |

(545,673 | ) | (9,169 | ) | (7,704 | ) | ||||||

|

Net cash received from (used for) financing activities |

414,113 | (18,553 | ) | (16,136 | ) | |||||||

|

Effect of exchange rate changes on cash |

(536 | ) | (725 | ) | 326 | |||||||

|

Net increase (decrease) in cash and cash equivalents |

(118,411 | ) | 16,991 | 27,648 | ||||||||

|

End of period cash and cash equivalents |

$ | 6,783 | $ | 125,194 | $ | 108,203 | ||||||

The decrease in cash provided by operating activities in 2022 compared to 2021 was primarily due to interest expense of $19.2 million and acquisition costs of $7.1 million as well as increases in accounts receivable and inventory as the result of increased sales and backlog. In addition, cash flow from accounts payable decreased $11.0 million from 2021 to 2022 and deferred revenue and customer deposits have decreased in the current year compared to an increase in the prior year.

During 2022, investing activities of $545.7 million consisted of $528.0 million for the acquisition of Fill-Rite and $18.0 million for capital expenditures primarily for machinery and equipment. During 2021, investing activities of $9.2 million consisted of capital expenditures primarily for machinery and equipment of $9.8 million.

Net cash received of $414.1 million from financing activities for 2022 consisted of proceeds from the Senior Secured Term Loan Facility of $350.0 million, $90.0 million from the unsecured Subordinated Credit Facility, and $17.0 million from the revolving Credit Facility. Partially offsetting these proceeds were debt issuance fees paid of $15.2 million, dividend payments of $17.9 million, payments on borrowings of $8.9 million and share repurchases of $0.9 million during 2022. During 2021, net cash used for financing activities of $18.6 million consisted primarily of dividend payments of $16.6 million and open market share repurchases of $1.2 million. See Note 6 “Financing Arrangements” in the Notes to our Consolidated Financial Statements.

Maturities of long-term debt in the next five fiscal years, and the remaining years thereafter, are as follows:

|

2023 |

2024 |

2025 |

2026 |

2027 |

Total |

|||||||||||||||||

| $ | 17,500 | $ | 21,875 | $ | 30,625 | $ | 35,000 | $ | 343,250 | $ | 448,250 | |||||||||||

The Company was in compliance with its debt covenants, including limits on additional borrowings and maintenance of certain operating and financial ratios at December 31, 2022 and December 31, 2021. We believe we have adequate liquidity from funds on hand and borrowing capacity to execute our financial and operating strategy, as well as comply with debt obligation and financial covenants for at least the next 12 months.

The Company currently expects to continue its exceptional history of paying regular quarterly dividends and increased annual dividends. However, any future dividends will be reviewed individually and declared by our Board of Directors at its discretion, dependent on our assessment of the Company’s financial condition and business outlook at the applicable time.

The Board of Directors has authorized a share repurchase program of up to $50.0 million of the Company’s common shares, of which approximately $48.1 million has yet to be repurchased. The actual number of shares repurchased will depend on prevailing market conditions, alternative uses of capital and other factors, and will be determined at management’s discretion. The Company is not obligated to make any purchases under the program, and the program may be suspended or discontinued at any time.

Contractual Obligations