Table of Contents

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

| [X] | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES |

EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2010

OR

| [ ] | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES |

EXCHANGE ACT OF 1934

For the transition period from to

Commission file number 1-3671

GENERAL DYNAMICS CORPORATION

(Exact name of registrant as specified in its charter)

| Delaware |

13-1673581 | |||

| State or other jurisdiction of incorporation or organization |

IRS Employer Identification No. | |||

| 2941 Fairview Park Drive, Suite 100, Falls Church, Virginia |

22042-4513 | |||

| Address of principal executive offices | Zip code | |||

Registrant’s telephone number, including area code:

(703) 876-3000

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class |

Name of exchange on which registered | |||

| Common stock, par value $1 per share | New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act:

None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ü No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes No ü

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the

Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to

file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ü No

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every

Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during

the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ü No

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and

will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by

reference in Part III of this Form 10-K or any amendment of this Form 10-K.

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller

reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in

Rule 12b-2 of the Exchange Act.

Large Accelerated Filer ü Accelerated Filer Non-Accelerated Filer Smaller Reporting Company

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes No ü

The aggregate market value of the voting common equity held by non-affiliates of the registrant was $21,219,557,495 as of July 4, 2010

(based on the closing price of the shares on the New York Stock Exchange).

372,704,788 shares of the registrant’s common stock were outstanding on January 30, 2011.

DOCUMENTS INCORPORATED BY REFERENCE:

Part III incorporates by reference information from certain portions of the registrant’s definitive proxy statement for the 2011 annual

meeting of shareholders to be filed with the Securities and Exchange Commission within 120 days after the close of the fiscal year.

Table of Contents

2 General Dynamics Annual Report Ÿ 2010

Table of Contents

(Dollars in millions, unless otherwise noted)

PART I

BUSINESS OVERVIEW

General Dynamics offers a broad portfolio of products and services in business aviation; combat vehicles, weapons systems and munitions; military and commercial shipbuilding; and communications and information technology. Incorporated in Delaware, we employ approximately 90,000 people and have a global presence.

We are dedicated to delivering consistently superior shareholder returns. Shareholder value is created through disciplined program execution, organic growth, margin improvement, efficient cash-flow conversion and prudent capital deployment. To drive growth, we pursue innovative product development and fast currents in our core markets as well as new customers and attractive opportunities in adjacent markets. To enhance margins, we seek to manage overhead costs, incentivize continuous-improvement initiatives and collaborate across our commercial and defense businesses. Our balanced capital deployment approach includes: acquisitions and divestitures, dividends, internal investment and, when appropriate, the repurchase of company shares on the open market.

In creating shareholder value and delivering the highest-quality products and services, we foster a culture centered on ethical behavior and integrity. This culture is evident in how we interact with shareholders, employees, customers, suppliers, partners and the communities in which we operate.

Formed in 1952 through the combination of Electric Boat Company, Consolidated Vultee (CONVAIR) and other companies, General Dynamics grew organically and through acquisitions until the early 1990s, when we sold nearly all of our divisions except Electric Boat and Land Systems. Beginning in 1995, we expanded those two core defense businesses by acquiring additional shipyards and combat vehicle-related businesses. In 1997, to reach a new, expanding market, we began acquiring companies with expertise in information technology products and services. In 1999, we purchased Gulfstream Aerospace Corporation, a business-jet aircraft and aviation support-services company. Since 1995, we have acquired and integrated 57 businesses, including three in 2010.

General Dynamics operates through four business groups: Aerospace, Combat Systems, Marine Systems and Information Systems and Technology. For selected financial information regarding each of our business groups, see Note Q to the Consolidated Financial Statements contained in Part II, Item 8, of this Annual Report on Form 10-K.

AEROSPACE

Our Aerospace group designs, manufactures and outfits a comprehensive family of mid- and large-cabin business-jet aircraft, and provides maintenance, refurbishment, outfitting and aircraft services for a variety of business-jet, narrow-body and wide-body aircraft customers globally. With more than 50 years of experience at the forefront of the business-jet aviation market, the Aerospace group is noted for:

| • | superior aircraft design, quality, safety and reliability; |

| • | technologically advanced cockpit and cabin systems and |

| • | industry-leading product service and support. |

The group’s Gulfstream products include eight aircraft across a spectrum of price and performance options. The varying ranges, speeds and cabin dimensions are well-suited to the transportation needs of an increasingly diverse global customer base. The large-cabin models are

General Dynamics Annual Report Ÿ 2010 3

Table of Contents

manufactured at Gulfstream’s headquarters in Savannah, Georgia, and outfitted at one of the group’s U.S. completion facilities. The mid-cabin models are constructed by a key supplier and outfitted by Gulfstream in one of the group’s U.S. completion centers.

While the installed base of aircraft is predominately in North America, international customers represent nearly 60 percent of the group’s backlog, with growing order interest from emerging markets including the Asia-Pacific region. Private companies and individual customers collectively represent approximately two-thirds of the group’s total orders. Gulfstream remains a leading provider of aircraft for government and military service around the world, with aircraft operated by nearly 40 nations. These government aircraft are used for head-of-state/executive transportation and a variety of special-mission applications, including aerial reconnaissance, maritime surveillance, weather research and astronaut training.

To maximize profitability, management has adjusted aircraft production rates, invested in innovative product development and facilities, and enhanced the group’s global service network. For example, prior to the recent economic downturn, Gulfstream amassed a multi-year large-cabin backlog by making measured increases in aircraft production that consciously lagged growing international customer demand. This backlog provided Gulfstream increased flexibility when global economic turmoil began to negatively impact the business-jet market in late 2008. In response to this sudden market deterioration, we quickly and aggressively cut 2009 production levels to stabilize the backlog. We also reduced employment, cut overhead costs and introduced a multi-week summer furlough to adjust the group’s manufacturing operations. Improved new order activity and lower customer default levels enabled us to maintain large-cabin production in 2010 while modestly increasing mid-cabin production.

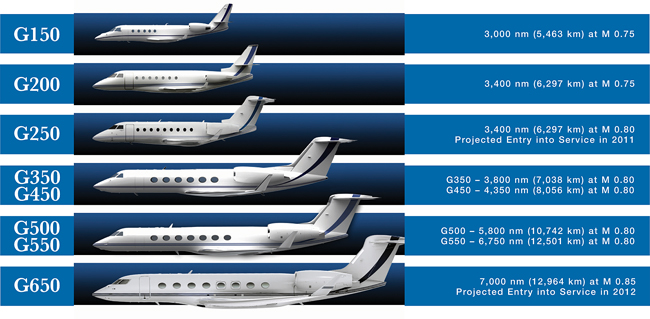

The Aerospace group continuously invests in research and development (R&D) over the course of each aircraft model’s lifecycle to introduce new products and first-to-market enhancements that broaden customer choice, improve aircraft performance and set new standards for customer safety, comfort and in-flight productivity. The two newest aircraft to join the Gulfstream family, the super-mid-size G250 and the ultra-large-cabin, ultra-high-speed G650, demonstrate this innovation. The G250, which will replace the G200, offers the largest cabin and the longest range at the fastest speed in its class. The G650 has the longest range, fastest speed, largest cabin and most advanced cockpit in the Gulfstream fleet and defines a completely new segment at the top of the business-jet market. Scheduled to enter service in late 2011 and mid-2012, respectively, both aircraft continue to perform well in flight testing, and they each remain on track for aircraft certification in 2011. Gulfstream’s new and upgraded aircraft models are designed to minimize lifecycle costs while maximizing the commonality of parts among the various models.

Current product-enhancement and development efforts include initiatives in advanced avionics, composites, flight-control systems, acoustics, cabin technologies and enhanced vision systems. Recent innovations include the second-generation Enhanced Vision System (EVS II) and the Synthetic Vision-Primary Flight Display (SV-PFD), both of which assist the pilot during low-visibility conditions. EVS II is a specially designed, forward-looking infrared (FLIR) camera that projects a real-world infrared image on the pilot's head-up display (HUD), while Synthetic Vision provides three-dimensional images of the terrain, runway environment and obstacles on the pilot’s primary head-down display. These products work in tandem to provide pilots with unparalleled situational awareness regardless of weather, terrain or landing-field conditions.

In November 2010, we announced a $500 seven-year facilities expansion project at Gulfstream’s Savannah campus designed to ensure the group is well-positioned to meet future demand for business-jet aircraft and support services. This investment plan includes constructing new facilities, renovating existing infrastructure and expanding the group’s R&D center. The new effort follows a recently completed $400 multi-year project in Savannah that established a purpose-built G650 manufacturing facility, increased aircraft-service capacity, improved the group’s customer sales and design center and created a state-of-the-art paint facility. This expansion initiative has paid immediate dividends. For example, the new manufacturing facility, designed for lean manufacturing and precision assembly, has successfully produced the five G650 test aircraft that are being used to meet the program’s certification testing schedule. Further, the newly expanded service center helped accommodate the significant recovery in customer demand in 2010.

In addition to the increased service capacity in Savannah, Gulfstream’s service network continues to evolve to address the demands of the growing international installed base. In 2010, we focused on increasing the group’s international parts and materials inventory, adding key personnel in fast-growing markets including Asia and South America, and realigning our existing North American service organization. In the western hemisphere, Gulfstream’s product support team continues to deploy a team of technicians in support of urgent customer-service requirements. We have also leveraged our 2008 acquisition of Jet Aviation, a maintenance and repair services provider with aircraft service centers in more than 20 locations worldwide, to provide customers around the world first-in-class service and support 24 hours a day.

Jet Aviation also expanded the Aerospace group’s portfolio to include premium aircraft-outfitting operations for airframes produced by other original equipment manufacturers (OEMs). Jet Aviation performs aircraft completions and refurbishments for business jets and narrow- and wide-body commercial aircraft at locations in Europe and the United States. As a trusted provider of turnkey aircraft management and fixed-base operations (FBO) services to a broad global customer base, Jet Aviation supports the continued growth and diversification of the Aerospace portfolio.

4 General Dynamics Annual Report Ÿ 2010

Table of Contents

A market leader in the business-aviation industry, the Aerospace group remains focused on:

| • | continuously investing in innovative first-to-market technologies and products; |

| • | providing exemplary and timely service support to customers around the world and |

| • | driving efficiencies into, and taking cost out of, the aircraft production, outfitting and service processes. |

Revenues for the Aerospace group were 19 percent of our consolidated revenues in 2008 and 16 percent in both 2009 and 2010. Revenues by major products and services were as follows:

| Year Ended December 31 | 2008 | 2009 | 2010 | |||||||||||

| Aircraft manufacturing and outfitting |

$ | 4,678 | $ | 3,893 | $ 3,869 | |||||||||

| Aircraft services |

816 | 1,154 | 1,323 | |||||||||||

| Pre-owned aircraft |

18 | 124 | 107 | |||||||||||

| Total Aerospace |

$ | 5,512 | $ | 5,171 | $ 5,299 | |||||||||

COMBAT SYSTEMS

Our Combat Systems group is a global leader in the design, development, production, support and enhancement of tracked and wheeled military vehicles, weapons systems and munitions for the United States and its allies. The group’s product lines include:

| • | wheeled combat and tactical vehicles, |

| • | main battle tanks and tracked infantry vehicles, |

| • | munitions and propellant, |

| • | rockets and gun systems and |

| • | drivetrain components and aftermarket parts. |

Combat Systems has a strong foundation of programs that deliver core capabilities to customers across the military-vehicle, weapons-system and munitions markets. These long-term production programs enable the group to pursue continuous process and productivity improvements, reduce product costs and improve the group’s financial performance. The group also applies its design and engineering expertise to develop product improvements that advance the utility and performance of these systems and increase warfighter safety and effectiveness, while identifying and positioning itself for new opportunities.

Combat Systems’ primary military-vehicle platforms consist of a variety of wheeled combat vehicles and main battle tanks. At the heart of these programs are the Stryker wheeled combat vehicle and the Abrams main battle tank – two of the key ground-force assets for our customers. Both of these vehicles remain elemental to the military’s force structure and offer continuing opportunities for modernization and enhancements to meet the warfighter’s evolving requirements.

The Stryker has proven itself as a versatile combat vehicle, supporting numerous missions with 10 variants: infantry carrier; command and control; medical evacuation; fire support; engineering; anti-tank; mortar carrier; reconnaissance; mobile gun system (MGS); and nuclear, biological and chemical reconnaissance vehicle (NBCRV). In addition to ongoing production of these vehicles, Combat Systems continues to work with the Army to ensure the Stryker remains relevant, affordable and capable of addressing a dynamic threat environment. For example, we are in the process of developing, testing and deploying in a period of just 18 months double-V-hulled vehicles that are designed to protect the crew from improvised explosive devices (IEDs). The group was authorized to begin production of these upgraded vehicles in 2010, with initial deliveries expected in early 2011.

Combat Systems continues to support the Army’s evolving needs for main battle tanks with technology upgrades to the Abrams, such as the System Enhancement Package (SEP). The SEP-configured tank is a digital platform with an enhanced command-and-control system, second-generation thermal sights and improved armor. We are also engaged in ongoing development efforts that can provide additional upgrade work while increasing the efficiency and capability of the tank.

Complementing these combat-vehicle programs are Combat Systems’ weapons-systems and munitions programs. For ground forces, the group manufactures vehicle armor, M2 heavy machine guns and MK19 and MK47 grenade launchers. For airborne platforms, Combat Systems produces weapons for most U.S. fighter aircraft, including all high-speed Gatling guns for fixed-wing aircraft and the Hydra-70 family of rockets. Combat Systems is also a global manufacturer and supplier of highly engineered axles, suspensions, brakes and aftermarket parts for heavy-payload vehicles for a variety of military and commercial customers.

The group holds leading or sole-source munitions supply positions for products such as:

| • | the 120mm mortar and the 155mm and 105mm artillery projectile for the U.S. government, |

| • | conventional bomb structures for the U.S. government, |

| • | mortar systems and large-caliber ammunition for the Canadian Department of National Defence and |

| • | military propellant for the North American market. |

In addition, Combat Systems is the principal second source for the U.S. military’s small-caliber ammunition needs.

Beyond these long-term platform and supply programs, Combat Systems provides logistics support in the United States’ ongoing operations in Iraq and Afghanistan. The group has opportunities associated with the

General Dynamics Annual Report Ÿ 2010 5

Table of Contents

refurbishment of battle-damaged vehicles, the replacement of equipment that has reached the end of its service life and the replenishment of ammunition and other supplies for the U.S. armed forces. As the sole provider of Abrams tanks and Stryker vehicles, Combat Systems is the primary contractor for the maintenance, repair and reset of these vehicles. The group is also a provider for the upgrade of Mine-Resistant, Ambush-Protected (MRAP) vehicles.

With the expertise from our incumbency on current production programs, the Combat Systems group is well-positioned to participate in future U.S. vehicle development programs. We are competing to lead the design and development of the Army’s next-generation armored personnel carrier, the Ground Combat Vehicle (GCV). The group is developing the Expeditionary Fighting Vehicle (EFV), a mission-critical combat platform designed to address the U.S. Marine Corps' amphibious assault requirement. As part of a system design and development contract, we have delivered seven new prototypes, which have performed well in customer reliability testing. The group is also a member of one of three teams awarded technology demonstration contracts for the Joint Light Tactical Vehicle (JLTV), which is intended to replace a portion of the U.S. fleet of High Mobility Multi-purpose Wheeled Vehicles (HMMWV).

Combat Systems has a significant presence internationally and is a recognized military-vehicle integrator and leading defense-materiel provider worldwide. The group has manufacturing facilities in Australia, Austria, Brazil, Canada, France, Germany, Spain and Switzerland. These operations are a key part of the defense industrial base of their home countries and have an extended customer base in more than 30 countries. The group’s European business offers a broad range of products, including light- and medium-weight tracked and wheeled tactical vehicles, amphibious bridge systems, artillery systems, light weapons, ammunition and propellants. Key platforms and their customers include the Leopard 2E tank and the Pizarro tracked infantry vehicle, produced for the Spanish army; the EAGLE wheeled vehicle for Germany; and the Piranha and Pandur wheeled armored vehicles, which the group produces for several European and Middle Eastern countries.

Combat Systems is experiencing strong international demand as a result of the demonstrated success of its fielded products. The group’s U.S. export activities include Abrams tanks and light armored vehicles (LAVs) for U.S. allies in the Middle East. Additionally, in 2010, the group was selected to manufacture tracked combat vehicle hulls for the Israeli Ministry of Defense. Combat Systems is also leveraging the strong customer relationships developed through its in-country operations. For example, Combat Systems continues work on Canada’s next-generation LAV at its Ontario facility and expects to transition from development to production in 2011. Through a contract awarded in 2010 to the United Kingdom operations of the company’s Information Systems and Technology group (see pg. 8), we will co-produce with a U.K.-based partner the Specialist Vehicle for the U.K. Ministry of Defence. The Specialist Vehicle is based on one of the group’s proven platforms. The program is envisioned to field up to 1,200 vehicles of different variants.

The Combat Systems group continues to emphasize operational execution across the business to drive cost reductions and margin improvement as the group delivers on its substantial backlog. In an environment of dynamic threats and evolving customer needs, the group remains focused on innovation, affordability and speed-to-market to secure new opportunities.

Revenues for the Combat Systems group were 28 percent of our consolidated revenues in 2008, 30 percent in 2009 and 27 percent in 2010. Revenues by major products and services were as follows:

| Year Ended December 31 | 2008 | 2009 | 2010 | |||||||||||||

| Wheeled combat vehicles |

$ | 3,475 | $ | 4,017 | $ | 3,916 | ||||||||||

| Munitions and propellant |

1,470 | 1,541 | 1,612 | |||||||||||||

| Tanks and tracked vehicles |

1,563 | 1,670 | 1,567 | |||||||||||||

| Rockets and gun systems |

512 | 595 | 616 | |||||||||||||

| Engineering and development |

673 | 960 | 372 | |||||||||||||

| Drivetrain components and other |

501 | 862 | 795 | |||||||||||||

| Total Combat Systems |

$ | 8,194 | $ | 9,645 | $ | 8,878 | ||||||||||

MARINE SYSTEMS

Our Marine Systems group designs, builds and supports submarines and surface ships for the U.S. Navy and Jones Act ships for commercial customers. The group is one of two primary shipbuilders for the Navy. The group’s diverse portfolio of platforms and capabilities includes:

| • | nuclear-powered submarines (Virginia Class), |

| • | surface combatants (DDG-51, DDG-1000, Littoral Combat Ship), |

| • | auxiliary and combat-logistics ships (T-AKE), |

| • | commercial ships (Jones Act ships), |

| • | design and engineering support (SSBN) and |

| • | overhaul, repair and lifecycle support services. |

The substantial majority of Marine Systems’ workload supports the U.S. Navy. These efforts include the construction of new ships, and the design and development of next-generation platforms to help the customer meet evolving missions and maintain its desired fleet size. The group also provides maintenance and repair services to help maximize the life and effectiveness of in-service ships and maintain their relevance to the Navy’s current requirements. This business consists primarily of major ship-construction programs awarded under large, multi-ship contracts that span several years. The group’s three mature Navy construction programs are the fast-attack Virginia-class nuclear-powered submarine, the Arleigh Burke-class (DDG-51) guided-missile destroyer and the Lewis and Clark-class (T-AKE) dry cargo/ammunition combat-logistics ship.

The Virginia-class submarine is the first U.S. submarine designed to address post-Cold War threats, including capabilities tailored for both

6 General Dynamics Annual Report Ÿ 2010

Table of Contents

open-ocean and littoral missions. These stealthy ships are well-suited for a variety of global assignments, including intelligence gathering, special-operations missions and sea-based missile launch. The Virginia-class program includes 30 submarines, which the customer is procuring in multi-ship blocks. The group has delivered the first seven of 18 boats under contract in conjunction with an industry partner that shares in the construction of these vessels. In 2010, Marine Systems delivered the seventh boat in a record 65 months, five months faster than any of the previous boats in the program. The remaining 11 boats under contract extend deliveries through 2018. As a result of U.S. combatant-commander requirements for the versatile capabilities of the Virginia-class submarine, strong customer and congressional support, innovative cost-saving design and production efforts, and successful program performance, the group is scheduled to start construction of two submarines per year beginning in 2011. The group has been working toward this increased submarine production workload for several years.

Marine Systems also is the lead designer and producer of Arleigh Burke destroyers, the only active destroyer in the Navy’s global surface fleet. In 2010, we delivered USS Jason Dunham, the 32nd of 34 DDG-51 ships the Navy has contracted with us to build. The two remaining ships are scheduled for delivery in 2011 and 2012, respectively. DDG-51s are multi-mission combatants that offer excellent defense against a wide range of threats, including ballistic missile defense. The Navy plans to continue the DDG-51 program given the proven capabilities of this destroyer. The group expects to receive an award in 2011 for an additional DDG-51 ship associated with the continuation of this program. Marine Systems remains the lead DDG-51 design and planning shipyard, managing the design, modernization and lifecycle support of these ships.

The group’s T-AKE combat-logistics ship supports multiple missions for the Navy, including replenishment at sea for U.S. and NATO operating forces around the world. T-AKE is the first Navy ship to incorporate proven commercial marine technologies such as integrated electric-drive propulsion. These technologies are designed to minimize T-AKE operations and maintenance costs over an expected 40-year life. In 2010, we received construction contracts for the final two ships under the 14-ship program. The group has delivered the first 10 of these ships, including two in 2010. Work is underway on the remaining four ships, with two deliveries scheduled in 2011 and two in 2012.

The group is also developing technologies and naval platforms for the future. These design and engineering efforts include initial concept studies for the development of the next-generation ballistic-missile submarine (SSBN), which is expected to replace the current Ohio Class of ballistic missile submarines. The group is also participating in the design of the SSBN Common Missile Compartment under development for the U.S. Navy and the Royal Navy of the United Kingdom.

Marine Systems participates in a number of programs in support of the Navy’s efforts to renew its surface fleet. The group has completed the detailed design of the next-generation guided-missile destroyer, the DDG-1000 Zumwalt Class, and is currently building the first ship at its Bath, Maine, shipyard. In 2010, the group was awarded a contract for continued engineering and support services for the program, and long-lead construction and material for the second and third ships. We expect to be awarded construction contracts for the second and third ships in 2011.

In 2010, the group was awarded a contract for long-lead material and advanced design efforts for the first ship of the Mobile Landing Platform (MLP) program. The MLP is an auxiliary support ship intended to serve as a floating transfer station, improving the Navy’s ability to deliver equipment and cargo to areas without adequate port access in support of a variety of missions. The Navy plans to build three MLP ships, and the contract for construction of the first ship is scheduled to be awarded in 2011.

In addition to these design and construction programs, Marine Systems provides comprehensive ship and submarine overhaul, repair and lifecycle support services to extend the service life of these vessels and maximize the value of these ships to the customer. The group operates the only full-service maintenance and repair shipyard on the West Coast, positioning us to support the Navy’s rebalancing of its surface force toward the Pacific Fleet. The group also provides international allies with program management, planning, engineering and design support for submarine and surface-ship construction programs.

Beyond its Navy programs, Marine Systems designs and produces ships for commercial customers to meet the Jones Act requirement that ships carrying cargo between U.S. ports be built in U.S. shipyards. In 2010, the group completed a contract to build five product-carrier ships. Given the group’s proven success on this program, the age of the fleet of Jones Act ships and environmental regulations that require double-hull tankers and impose emission control limits, we anticipate additional commercial shipbuilding opportunities to materialize as the economy recovers.

To further the group’s goals of efficiency, affordability for the customer and continuous improvement, we make strategic investments in our business, often in cooperation with the Navy and local governments. In addition, Marine Systems leverages its design and engineering expertise across its business to improve program execution and generate cost savings. This knowledge sharing enables the group to use resources more efficiently and drive process improvements. The group is well-positioned to effectively fulfill the ship-construction and support requirements of its Navy and commercial customers.

Revenues for the Marine Systems group were 19 percent of our consolidated revenues in 2008, 20 percent in 2009 and 21 percent in 2010. Revenues by major products and services were as follows:

| Year Ended December 31 | 2008 | 2009 | 2010 | |||||||||||||

| Nuclear-powered submarines |

$ | 2,579 | $ | 3,173 | $ | 3,587 | ||||||||||

| Surface combatants |

1,195 | 1,278 | 1,360 | |||||||||||||

| Auxiliary and commercial ships |

1,192 | 1,179 | 961 | |||||||||||||

| Repair and other services |

590 | 733 | 769 | |||||||||||||

| Total Marine Systems |

$ | 5,556 | $ | 6,363 | $ | 6,677 | ||||||||||

General Dynamics Annual Report Ÿ 2010 7

Table of Contents

INFORMATION SYSTEMS AND TECHNOLOGY

Our Information Systems and Technology group provides critical technologies, products and services that support a wide range of government and commercial communication and information-sharing needs. The group consists of a three-part portfolio centered on tactical communication systems, information technology services, and intelligence, surveillance and reconnaissance systems.

Tactical communication systems – The group designs, manufactures and delivers trusted and secure communications systems, command-and-control systems and operational hardware to customers within the U.S. Department of Defense, the intelligence community and federal civilian agencies, and to international customers. Our leadership in this market results from decades of experience with previous systems, incumbency on today’s programs and an ongoing record of innovation that encompasses key technologies at the center of our customers’ missions. These include:

| • | ruggedized mobile computing solutions with embedded wireless capability; |

| • | information assurance and encryption technologies, products, systems and services that ensure the security and integrity of digital communications worldwide; |

| • | digital switching, broadband networking and automated network management; |

| • | battlespace command-and-control systems and |

| • | fixed and mobile radio and satellite communications systems and antenna technologies. |

This market is characterized by programs that enhance warfighters’ ability to communicate, collaborate and access vital information through Internet-like networks on the battlefield. Key programs include the U.S. Army’s Warfighter Information Network-Tactical (WIN-T) and the Joint Tactical Radio System (JTRS).

WIN-T is the Army’s primary battlefield communications network. As the prime contractor, we are responsible for the design, engineering, integration, production, program management and support of the network. Using ground and satellite communications links, WIN-T provides commanders with the digital communications services they need to access intelligence information, initiate battle plans, collaborate with other military elements, issue orders and monitor the status of their forces. The group has deployed the first increment of WIN-T around the world to more than half of the U.S. Army. The group is transitioning into the second increment of the program, which adds on-the-move command and control and expands the capability to additional soldiers. The third increment of the program is designed to provide enhanced network reliability and capacity and smaller, more-tightly integrated communications and networking gear.

The JTRS program will provide communications among all branches of the U.S. military on multi-channel, software-defined radios. We are developing the JTRS Handheld, Manpack, Small Form Fit (HMS) network radios to connect soldiers, sensors and robotic platforms. These small radios will enhance dismounted soldiers’ situational awareness and combat effectiveness by giving them greater communications capabilities and access to intelligence data in the field. This critical networking capability was successfully demonstrated by the Army during extensive testing exercises in 2010 that connected command posts, on-the-move forces and dismounted soldiers. These exercises also demonstrated how WIN-T and JTRS enable key battle command applications to increase force effectiveness across a variety of missions and terrain.

Information Systems and Technology delivers the same type of modern communications and information-sharing benefits to many civilian customers, including the U.S. Department of Homeland Security and other federal civilian agencies. For example, we are the prime contractor for the U.S. Coast Guard’s Rescue 21 system, which provides enhanced search-and-rescue capabilities as well as state-of-the-art command-and-control capabilities to assist the Coast Guard in effectively deploying available assets on all maritime missions.

We also provide many of these capabilities to non-U.S. customers, including the U.K. Ministry of Defence and the Canadian Department of National Defence. Most recently, the U.K. Ministry of Defence awarded the group a contract for the demonstration phase of its Specialist Vehicle program. In this phase, the group will manage the design, integration and production of seven prototypes. The Specialist Vehicle’s open electronic architecture will make the fleet easier to maintain and reduce product lifecycle costs. Work under the contract will be shared with the Combat Systems group, including a significant portion of the future production effort.

Information technology services – The group provides mission-critical information technology (IT) and highly specialized mission-support services to the U.S. defense and intelligence communities, the Department of Homeland Security and other federal civilian agencies, and commercial and international customers. The group specializes in:

| • | design, development, integration, maintenance and security of wireless and wire-line networks and enterprise infrastructure; |

| • | mission-operations simulation and training systems and services; |

| • | large-scale data center consolidation and modernization and |

| • | healthcare technology solutions and services. |

In this market, Information Systems and Technology has a long-standing reputation for excellence in providing technical-support personnel and domain specialists who enable customers to execute their missions effectively. For many customers, the group’s employees are the on-call staff that provide technical support for both commercial desktop technology and mission-specific hardware. Our employees also develop, install and operate mission systems on a day-to-day basis. In Fort Huachuca, Arizona, for example, Information Systems and Technology employees

8 General Dynamics Annual Report Ÿ 2010

Table of Contents

provide training and IT support services for critical Army intelligence operations, including unmanned aircraft systems training units. We integrate and operate systems that create lifelike training scenarios, helping operators improve their proficiency at a fraction of the cost of live-action exercises.

Information Systems and Technology also supplies network-modernization and IT infrastructure services to U.S. government customers. As one of the U.S. Air Force’s leading partners for network modernization, the group has provided IT support services to more than 75 Air Force bases, and it currently supports the Air Force’s main operating bases. The group also has provided continuous enterprise-wide IT services and support to the U.S. Senate for more than five years.

In addition, we are a leading provider of healthcare technology solutions that meet the fast-growing needs for technology modernization of government and commercial healthcare organizations. Our offerings include data management, analytics, fraud prevention and detection software, decision support and process automation solutions. In Afghanistan and Iraq, the group supports the Army’s military healthcare IT mission, helping ensure continuity of care for injured soldiers by providing accurate and timely information to medical staff both in the field and at treatment facilities. For the Centers for Medicare & Medicaid Services, we are supporting the government’s implementation of healthcare reform and medical benefits programs, including facilitating a program to provide retirees with prescription health coverage.

Intelligence, surveillance and reconnaissance systems – We also provide mission-related systems development, integration and operations support to customers in the U.S. defense, intelligence and homeland security communities, and to U.S. allies. These offerings include:

| • | open-architecture mission systems; |

| • | signals and information collection, processing and distribution systems; |

| • | design, development and integration of imagery solutions; |

| • | sensors and cameras; |

| • | special-purpose computing and |

| • | cyber security services and products. |

We have a 50-year legacy of providing advanced fire control systems for Navy submarine programs, and currently are developing and integrating commercial-off-the-shelf (COTS) software and hardware upgrades to improve the tactical control capabilities for multiple submarine classes. This initiative leads the implementation of the Navy's open architecture and open business model approach on submarines with a design that emphasizes shared standards, providing greater interoperability, scalability and supplier independence. Capitalizing on this expertise and open architecture approach, the group developed the core mission system for the Navy’s Independence Class of Littoral Combat Ships (LCS), and it is the ship mission systems integrator on the Joint High Speed Vessel (JHSV) program for the Army and the Navy.

Information Systems and Technology continues to expand its imagery offerings. For example, the group recently integrated cameras and optics with algorithms and sensors to enhance customers’ ability to gather and interpret visual data. This group also produces the Defense Department’s most-widely used imagery-analysis software suite. This software is currently providing actionable information derived from raw intelligence and archived imagery to more than 10,000 intelligence and tactical users.

Information Systems and Technology’s contracts in securing and protecting organizations from network attacks have resulted in a market-leading position in cyber security. The group performs data recovery, forensic examinations and diagnostics as a prime contractor for the DoD Cyber Crime Center (DC3), the world’s largest accredited cyber crime laboratory. It is also the principal support contractor for the Department of Homeland Security’s U.S. Computer Emergency Readiness Team (US-CERT), which provides response support to and defense against cyber attacks for U.S. executive branch agencies, and information sharing and collaboration with state and local government, industry and international partners.

The group’s diverse customer base has stimulated strong growth opportunities in each of its three principal markets, including:

| • | the warfighter’s need for improved tactical communications and real-time intelligence; |

| • | IT network and business system consolidation and modernization, and military and federal requirements for healthcare IT services and |

| • | the growing requirements for cyber security services among homeland security, defense, intelligence and commercial customers. |

Revenues for the Information Systems and Technology group were 34 percent of our consolidated revenues in 2008 and 2009 and 36 percent in 2010. Revenues by major products and services were as follows:

| Year Ended December 31 | 2008 | 2009 | 2010 | |||||||||||||

| Tactical communication systems |

$ | 4,455 | $ | 4,713 | $ | 5,134 | ||||||||||

| Information technology services |

3,536 | 3,920 | 4,262 | |||||||||||||

| Intelligence, surveillance and reconnaissance systems |

2,047 | 2,169 | 2,216 | |||||||||||||

| Total Information Systems and Technology |

$ | 10,038 | $ | 10,802 | $ | 11,612 | ||||||||||

General Dynamics Annual Report Ÿ 2010 9

Table of Contents

CUSTOMERS

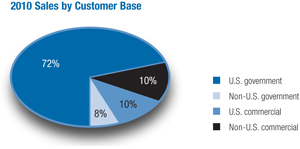

In 2010, 72 percent of our revenues were from the U.S. government; 10 percent were from U.S. commercial customers; 8 percent were directly from international defense customers; and the remaining 10 percent were from international commercial customers.

U.S. GOVERNMENT

Our primary customers are the U.S. Department of Defense and the U.S. intelligence community. We have also developed relationships with other U.S. government customers, including the Department of Homeland Security, Centers for Medicare & Medicaid Services, National Aeronautics and Space Administration and several first-responder agencies. Our revenues from the U.S. government were as follows:

| Year Ended December 31 | 2008 | 2009 | 2010 | |||||||||

| Direct |

||||||||||||

| Department of Defense (DoD) |

$ | 18,442 | $ | 20,344 | $ | 20,446 | ||||||

| Non-DoD |

1,422 | 1,899 | 1,941 | |||||||||

| Foreign Military Sales* |

282 | 478 | 876 | |||||||||

| Total U.S. government |

$ | 20,146 | $ | 22,721 | $ | 23,263 | ||||||

| Percent of total revenues |

69% | 71% | 72% | |||||||||

| * | In addition to our direct international sales, we sell to foreign governments through the Foreign Military Sales (FMS) program. Under the FMS program, we contract with and are paid by the U.S. government, and the U.S. government assumes the risk of collection from the foreign government customer. |

We perform our U.S. government business under fixed-price, cost-reimbursement and time-and-materials contracts. Our production contracts are primarily fixed-price. Under these contracts, we agree to perform a specific scope of work for a fixed amount. Contracts for research, engineering, prototypes, repair and maintenance are typically cost-reimbursement or time-and-materials. Under cost-reimbursement contracts, the customer reimburses us for allowable costs and pays a fixed fee or an incentive- or award-based fee. These fees are determined by our ability to achieve targets set in the contract, such as cost, quality, schedule and performance. Under time-and-materials contracts, the customer pays a fixed hourly rate for direct labor and reimburses us for materials costs.

Fixed-price contracts accounted for approximately 55 percent of our U.S. government business in both 2009 and 2010; cost-reimbursement contracts accounted for approximately 38 percent in 2009 and 39 percent in 2010; and time-and-materials contracts accounted for approximately 7 percent in 2009 and 6 percent in 2010.

Each of these contract types presents advantages and disadvantages. Fixed-price contracts typically have higher fee levels as we are required to absorb cost overruns, should they occur. Therefore, these types of contracts offer us additional profits if we can complete the work for less than the contract amount. Cost-reimbursement contracts generally subject us to lower risk. They also can include fee schedules that allow the customer to make additional payments when we satisfy certain performance criteria. However, not all costs are reimbursed under these types of contracts, and the government carefully reviews the costs we charge. In addition, the negotiated base fees associated with cost-reimbursement contracts are generally lower, consistent with our lower risk. Under time-and-materials contracts, our profit may vary if actual labor-hour costs vary significantly from the negotiated rates. Additionally, because we often charge materials costs with little or no fee, the content mix can impact the profit margins associated with these contracts.

U.S. COMMERCIAL

Our U.S. commercial revenues were $4.1 billion in 2008, $3.3 billion in 2009 and $3.2 billion in 2010. This represented approximately 14 percent of our consolidated revenues in 2008 and 10 percent in both 2009 and 2010. The majority of these revenues are for business-jet aircraft where our customer base consists of individuals and public and privately held companies representing a wide range of industries. Other commercial products include drivetrain components and aftermarket parts in our Combat Systems group, Jones Act ships in our Marine Systems group and ruggedized mobile computing solutions in our Information Systems and Technology group.

INTERNATIONAL

Our direct revenues from government and commercial customers outside the United States were $5.1 billion in 2008 and $6 billion in both 2009 and 2010. This represented approximately 17 percent of our consolidated revenues in 2008, 19 percent in 2009 and 18 percent in 2010.

We conduct business with government customers around the world with primary subsidiary operations in Australia, Austria, Brazil, Canada, France, Germany, Italy, Mexico, Spain, Switzerland and the United Kingdom. Our non-U.S. defense subsidiaries are committed to developing long-term relationships with their respective governments and have distinguished themselves as principal regional suppliers and employers.

Our international commercial business consists primarily of business-jet aircraft exports and worldwide aircraft services. The market for business-jet aircraft and related services outside North America has expanded significantly in recent years, particularly in emerging markets, including the Asia-Pacific region. While the United States continues to be our largest market for business aircraft, orders from customers outside North America represent a growing segment of our aircraft business, approximately 60 percent of total orders and backlog in 2010.

10 General Dynamics Annual Report Ÿ 2010

Table of Contents

For a discussion of the risks associated with conducting business in international locations, see Risk Factors contained in Part I, Item 1A, of this Annual Report on Form 10-K. For information regarding sales and assets by geographic region, see Note Q to the Consolidated Financial Statements contained in Part II, Item 8, of this Annual Report on Form 10-K.

COMPETITION

Several factors determine our ability to compete successfully in both the defense and business-jet aircraft markets. While customers’ evaluation criteria vary, the principal competitive elements include:

| • | the technical excellence, reliability and cost competitiveness of our products and services; |

| • | our ability to innovate and develop new products and technology that improve mission performance; |

| • | successful program execution and on-time delivery of complex, integrated systems; |

| • | our global footprint and accessibility to customers; |

| • | our indigenous presence in the countries of several key customers; |

| • | the reputation and customer confidence derived from our past performance and |

| • | the successful management of our businesses and customer relationships. |

DEFENSE MARKET

The U.S. government contracts with numerous domestic and foreign companies for products and services. We compete against other large platform and system-integration contractors, as well as smaller companies that specialize in a particular technology or capability. Internationally, we compete with global defense contractors’ exports and the offerings of private and state-owned defense manufacturers based in the countries where we operate. Our Combat Systems group competes with a large number of domestic and foreign businesses. Our Marine Systems group has one primary competitor, Northrop Grumman Corporation, with which it also partners or subcontracts on several programs, including the Virginia-class submarine. Our Information Systems and Technology group competes with many companies, from large defense companies to small niche competitors with specialized technologies. The operating cycle of many of our major platform programs can result in sustained periods of program continuity when we perform successfully.

We also are involved in teaming and subcontracting relationships with some of our competitors. Competitions for major defense programs often require companies to form teams to bring together broad capabilities to meet the customer’s requirements. Opportunities associated with these programs include roles as the program’s integrator, overseeing and coordinating the efforts of all participants in the team, or as a provider of a specific hardware, such as military vehicles provided by Combat Systems, or a subsystem element, such as core mission systems provided by Information Systems and Technology.

Another competitive factor in the defense market is the U.S. government’s use of multiple-award indefinite delivery, indefinite quantity (IDIQ) contracts to provide customers with flexible procurement options. IDIQ contracts allow the government to select a group of eligible contractors for a program and establish an overall spending limit. When the government awards IDIQ contracts to multiple bidders under the same program, we must compete to be selected as a participant in the program and subsequently compete for individual delivery orders. This contracting model is most common among our Information Systems and Technology group’s customers but is also being used in programs for which our Combat Systems group competes.

BUSINESS-JET AIRCRAFT MARKET

The business-jet aircraft manufacturing market is divided into segments based on aircraft range, price and cabin size. Gulfstream has several competitors for each of its products, with more competitors for the shorter-range aircraft. Key competitive factors include aircraft safety, reliability and performance; comfort and in-flight productivity; service quality, global footprint and timeliness; technological and new-product innovation; and price. We believe Gulfstream competes effectively in all of these areas.

The Aerospace group competes worldwide in its business-jet aircraft services business primarily on the basis of price, service quality and timeliness. In its maintenance, repair and overhaul (MRO) and fixed-base operations (FBO) business, the group competes with several other large companies, as well as a number of smaller companies, particularly in the maintenance business. In its completions business, the group competes with original equipment manufacturers (OEMs), as well as other third-party providers.

General Dynamics Annual Report Ÿ 2010 11

Table of Contents

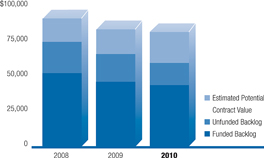

BACKLOG

Our total backlog represents the estimated remaining sales value of work to be performed under firm contracts and includes funded and unfunded portions. For additional discussion of backlog, see Management’s Discussion and Analysis of Financial Condition and Results of Operations contained in Part II, Item 7, of this Annual Report on Form 10-K.

Summary backlog information for each of our business groups follows:

| 2010 Total Backlog Not Expected to be Completed in |

||||||||||||||||||||||||||||

| December 31 | 2009 | 2010 | 2011 | |||||||||||||||||||||||||

| Funded | Unfunded | Total | Funded | Unfunded | Total | |||||||||||||||||||||||

| Aerospace |

$ | 18,891 | $ | 433 | $ | 19,324 | $ | 17,443 | $ | 378 | $ | 17,821 | $ | 13,781 | ||||||||||||||

| Combat Systems |

11,431 | 1,985 | 13,416 | 10,908 | 892 | 11,800 | 4,486 | |||||||||||||||||||||

| Marine Systems |

7,111 | 15,362 | 22,473 | 7,050 | 13,069 | 20,119 | 14,398 | |||||||||||||||||||||

| Information Systems and Technology |

8,423 | 1,909 | 10,332 | 7,978 | 1,843 | 9,821 | 2,980 | |||||||||||||||||||||

| Total backlog |

$ | 45,856 | $ | 19,689 | $ | 65,545 | $ | 43,379 | $ | 16,182 | $ | 59,561 | $ | 35,645 | ||||||||||||||

RESEARCH AND DEVELOPMENT

To foster innovative product development and evolution, we conduct sustained R&D activities as part of our normal business operations. In the commercial sector, most of our Aerospace group’s R&D activities support Gulfstream’s product enhancement and development programs. In our defense businesses, we conduct both customer-sponsored R&D activities under U.S. government contracts and company-sponsored R&D. In accordance with government regulations, we recover a significant portion of company-sponsored R&D expenditures through overhead charges to U.S. government contracts. For more information on our R&D activities, including our expenditures for the past three years, see Note A to the Consolidated Financial Statements contained in Part II, Item 8, of this Annual Report on Form 10-K.

INTELLECTUAL PROPERTY

We develop technology, manufacturing processes and systems-integration practices. In addition to owning a large portfolio of proprietary intellectual property, we license some intellectual property rights to and from others. The U.S. government holds licenses to our patents developed in the performance of U.S. government contracts, and it may use or authorize others to use the inventions covered by our patents. Although these intellectual property rights are important to the operation of our business, no existing patent, license or other intellectual property right is of such importance that its loss or termination would, in our opinion, have a material impact on our business.

EMPLOYEES

On December 31, 2010, we had approximately 90,000 employees, one-fifth of whom work under collective agreements with various labor unions and worker representatives. Agreements covering approximately 3 percent of total employees are due to expire during 2011. Historically, we have renegotiated labor agreements without any significant disruption of operating activities.

RAW MATERIALS, SUPPLIERS AND SEASONALITY

We depend on suppliers and subcontractors for raw materials and components. These supply networks can experience price fluctuations and capacity constraints, which can put pressure on pricing. Effective management and oversight of suppliers and subcontractors is an important element of our successful performance. We attempt to mitigate these risks through long-term agreements with our suppliers, by negotiating flexible pricing terms in our customer contracts and by procuring from our suppliers jointly across our business groups to achieve economies of scale. We have not experienced, and do not foresee, significant difficulties in obtaining the materials, components or supplies necessary for our business operations.

Our business is not generally seasonal in nature. The timing of contract awards, the availability of funding from the customer, the incurrence of contract costs and unit deliveries are the primary drivers of our revenue recognition. In the United States, these factors are influenced by the federal government’s October-to-September fiscal year. This process has historically resulted in higher revenues in the latter half of the year. Internationally, many of our government customers schedule deliveries toward the end of the calendar year, resulting in increasing revenues and earnings over the course of the year.

12 General Dynamics Annual Report Ÿ 2010

Table of Contents

REGULATORY MATTERS

U.S. GOVERNMENT CONTRACTS

U.S. government contracts are subject to procurement laws and regulations. The Federal Acquisition Regulation (FAR) and the Cost Accounting Standards (CAS) govern the majority of our contracts. The FAR mandates uniform policies and procedures for U.S. government acquisitions and purchased services. Also, individual agencies can have acquisition regulations that provide implementing language for the FAR or that supplement the FAR. For example, the Department of Defense implements the FAR through the Defense Federal Acquisition Regulation supplement (DFARs). For all federal government entities, the FAR regulates the phases of any product or service acquisition, including:

| • | acquisition planning, |

| • | competition requirements, |

| • | contractor qualifications, |

| • | protection of source selection and vendor information and |

| • | acquisition procedures. |

In addition, the FAR addresses the allowability of our costs, while the CAS address how those costs can be allocated to contracts. The FAR also subjects us to audits and other government reviews covering issues such as cost, performance and accounting practices relating to our contracts.

INTERNATIONAL

Our international sales are subject to the applicable foreign government regulations and procurement policies and practices, as well as certain U.S. policies and regulations, including the Foreign Corrupt Practices Act (FCPA). We are also subject to regulations governing investments, exchange controls, repatriation of earnings and import-export control, including the International Traffic in Arms Regulations (ITAR).

BUSINESS-JET AIRCRAFT

The Aerospace group is subject to Federal Aviation Administration (FAA) regulation in the United States and other similar aviation regulatory authorities internationally, including the European Aviation Safety Agency (EASA). For an aircraft to be manufactured and sold, the model must receive a type certificate from the appropriate aviation authority, and each aircraft must receive a certificate of airworthiness. Aircraft completions also require approval by the appropriate aviation authority, which often is accomplished through a supplemental type certificate. Aviation authorities can require changes to a specific aircraft or model type for safety reasons if they believe the aircraft does not meet their standards. Maintenance facilities and charter operations must be licensed by aviation authorities as well.

ENVIRONMENTAL

We are subject to a variety of federal, state, local and foreign environmental laws and regulations. These laws and regulations cover the discharge, treatment, storage, disposal, investigation and remediation of some materials, substances and wastes. We are directly or indirectly involved in environmental investigations or remediation at some of our current and former facilities and at third-party sites that we do not own but where we have been designated a Potentially Responsible Party (PRP) by the U.S. Environmental Protection Agency or a state environmental agency. As a PRP, we potentially are liable to the government or third parties for the full cost of remediating contamination at a relevant site. In cases where we have been designated a PRP, generally we seek to mitigate these environmental liabilities through available insurance coverage and by pursuing appropriate cost-recovery actions. In the unlikely event we are required to fully fund the remediation of a site, the current statutory framework would allow us to pursue contributions from other PRPs. We regularly assess our compliance status and management of environmental matters.

Operating and maintenance costs associated with environmental compliance and management of contaminated sites are a normal, recurring part of our operations. Historically, these costs have not been material. Environmental costs often are allowable and recoverable under our contracts with the U.S. government. Based on information currently available and current U.S. government policies relating to allowable costs, we do not expect continued compliance with environmental regulations to have a material impact on our results of operations, financial condition or cash flows. For additional information relating to the impact of environmental matters, see Note N to the Consolidated Financial Statements contained in Part II, Item 8, of this Annual Report on Form 10-K.

AVAILABLE INFORMATION

We file several types of reports and other information with the Securities and Exchange Commission (SEC) pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934, as amended. These reports and information include an annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and proxy statements. Free copies of these items are made available on our website (www.generaldynamics.com) as soon as practicable and through the General Dynamics investor relations office at (703) 876-3152.

These items also can be read and copied at the SEC’s Public Reference Room at 100 F Street, N.E., Washington, DC 20549. Information on the operation of the Public Reference Room is available by calling the SEC at (800) SEC-0330. The SEC maintains a website (www.sec.gov) that contains reports, proxy and information statements, and other information regarding issuers that file electronically with the SEC.

General Dynamics Annual Report Ÿ 2010 13

Table of Contents

An investment in our common stock or debt securities is subject to risks and uncertainties. Investors should consider the following factors, in addition to the other information contained in this Annual Report on Form 10-K, before deciding whether to purchase our securities.

Investment risks can be market-wide as well as unique to a specific industry or company. The market risks faced by an investor in our stock are similar to the uncertainties faced by investors in a broad range of industries. There are, however, some risks that apply more specifically to General Dynamics based on our type of business.

Because three of our four business groups serve the defense market, our revenues are concentrated with the U.S. government. This customer relationship involves certain unique risks. In addition, our sales to international customers expose us to different financial and legal risks. In our Aerospace group’s market, we face risks tied to U.S. and global economic conditions. Despite the varying nature of our U.S. and international defense and business-aviation operations and the markets they serve, each group shares some common risks, such as the ongoing development of high-technology products and the price, availability and quality of commodities and subsystems.

We depend on the U.S. government for a significant portion of our revenues. In each of the past three years, more than two-thirds of our revenues were from the U.S. government. U.S. defense spending historically has been driven by perceived threats to national security. While the country has been under an elevated threat level in recent years, there is no assurance that defense budgets will be sustained at current levels. In addition, competing demands for federal funds could pressure all areas of spending, which could further impact the defense budget.

A decrease in U.S. government defense spending or changes in spending allocation could result in one or more of our programs being reduced, delayed or terminated. Reductions in our existing programs could adversely affect our future revenues and earnings.

U.S. government contracts are not always fully funded at inception and are subject to termination. Our U.S. government revenues are funded by agency budgets that operate on an October-to-September fiscal year. In February of each year, the President of the United States presents to the Congress the budget for the upcoming fiscal year. This budget proposes funding levels for every federal agency and is the result of months of policy and program reviews throughout the Executive branch. For the remainder of the year, the appropriations and authorization committees of the Congress review the President’s budget proposals and establish the funding levels for the upcoming fiscal year. Once these levels are enacted into law, the Executive Office of the President administers the funds to the agencies.

There are two primary risks associated with this process. First, the process may be delayed or disrupted. Changes in congressional schedules due to elections or other legislative priorities, negotiations for program funding levels or unforeseen world events can interrupt the funding for a program or contract. Second, future revenues under existing multi-year contracts are conditioned on the continuing availability of congressional appropriations. The Congress typically appropriates funds on a fiscal-year basis, even though contract performance may extend over many years. Changes in appropriations in subsequent years may impact the funding available for these programs. Delays or changes in funding can impact the timing of available funds or lead to changes in program content.

In addition, U.S. government contracts generally permit the government to terminate a contract, in whole or in part, for convenience. If a contract is terminated for convenience, a contractor usually is entitled to receive payments for its allowable costs and the proportionate share of fees or earnings for the work performed. The government may also terminate a contract for default in the event of a breach by the contractor. If a contract is terminated for default, the government in most cases pays only for the work it has accepted. The loss of anticipated funding or the termination of multiple or large programs could have an adverse effect on our future revenues and earnings.

We are subject to audit by the U.S. government. U.S. government agencies routinely audit and investigate government contractors. These agencies review a contractor’s performance under its contracts, cost structure and compliance with applicable laws, regulations and standards. The U.S. government also reviews the adequacy of, and a contractor’s compliance with, its internal control systems and policies, including the contractor’s purchasing, property, estimating, labor, accounting and information systems. In some cases, audits may result in costs not being reimbursed or subject to repayment. If an audit or investigation were to result in allegations of improper or illegal activities, we could be subject to civil or criminal penalties and administrative sanctions, including termination of contracts, forfeiture of profits, suspension of payments, fines, and suspension or prohibition from doing business with the U.S. government. In addition, we could suffer reputational harm if allegations of impropriety were made against us.

Our Aerospace group is subject to changing customer demand for business aircraft. Our Aerospace group’s business-jet market is driven by the demand for business-aviation products and services by business, individual and government customers in the United States and around the world. The group’s future results also depend on other factors, including general economic conditions, the availability of credit and trends in capital goods markets. If customers default on existing contracts and our Aerospace group is unable to replace those contracts, the group’s anticipated revenues and profitability could be reduced as a result.

14 General Dynamics Annual Report Ÿ 2010

Table of Contents

Our earnings and margins depend on our ability to perform under our contracts. When agreeing to contractual terms, our management makes assumptions and projections about future conditions or events. These projections assess:

| • | the productivity and availability of labor, |

| • | the complexity of the work to be performed, |

| • | the cost and availability of materials, |

| • | the impact of delayed performance and |

| • | the timing of product deliveries. |

If there is a significant change in one or more of these circumstances or estimates, or if we face unexpected contract costs, the profitability of one or more of these contracts may be adversely affected. This could affect our earnings and margins. If we fail to adequately manage the risks under our contracts, particularly fixed-price contracts, our earnings and margins may be adversely affected.

Our earnings and margins depend in part on subcontractor performance, as well as raw material and component availability and pricing. We rely on other companies to provide raw materials, major components and subsystems for our products. Subcontractors perform some of the services that we provide to our customers. We depend on these subcontractors and vendors to meet our contractual obligations in full compliance with customer requirements. Occasionally, we rely on only one or two sources of supply that, if disrupted, could have an adverse effect on our ability to meet our commitments to customers. Our ability to perform our obligations as a prime contractor may be adversely affected if one or more of these suppliers is unable to provide the agreed-upon supplies or perform the agreed-upon services in a timely and cost-effective manner.

International sales and operations are subject to greater risks that sometimes are associated with doing business in foreign countries. Our international business may pose different risks than our business in the United States. In some countries there is increased chance for economic, legal or political changes. Government customers in newly formed free-market economies typically have procurement procedures that are less mature, which can complicate the contracting process. In this context, our international business may be sensitive to changes in a foreign government’s leadership, national priorities and budgets. International transactions can involve increased financial and legal risks arising from foreign exchange-rate variability and differing legal systems. In addition, some international government customers require contractors to agree to specific in-country purchases, manufacturing agreements or financial support arrangements, known as offsets, as a condition for a contract award. The contracts may include penalties if we fail to meet the offset requirements. An unfavorable event or trend in any one or more of these factors could adversely affect our revenues and earnings associated with our international business.

Our future success will depend, in part, on our ability to develop new products and maintain a qualified workforce to meet the needs of our customers. Virtually all of the products that we produce and sell are highly engineered and require sophisticated manufacturing and system-integration techniques and capabilities. The commercial and government markets in which we operate are characterized by rapidly changing technologies. The product and program needs of our government and commercial customers change and evolve regularly. Accordingly, our future performance depends, in part, on our ability to develop and manufacture competitive products, and bring those products to market quickly at cost-effective prices. In addition, because of the highly specialized nature of our business, we must be able to hire and retain the skilled and qualified personnel necessary to perform the services required by our customers. If we are unable to develop new products that meet customers’ changing needs or successfully attract and retain qualified personnel, our future revenues and earnings may be adversely affected.

Developing new technologies entails significant risks and uncertainties that may not be covered by indemnity or insurance. While we maintain insurance for some business risks, it is not practicable to obtain coverage to protect against all operational risks and liabilities. Where permitted by applicable laws, we seek indemnification from the U.S. government. In addition, we may seek limitation of potential liability related to the sale and use of our homeland security products and services through qualification by the Department of Homeland Security under the SAFETY Act provisions of the Homeland Security Act of 2002. We may elect to provide products or services even in instances where we are unable to obtain such indemnification or qualification.

We have made and expect to continue to make investments, including acquisitions and joint ventures, that involve risks and uncertainties. These activities, particularly in the current environment of increased governmental regulation and enforcement both domestically and abroad, may expose us to legal and regulatory risks that are different from the risks we currently experience in our existing businesses. When evaluating potential mergers and acquisitions, we make judgments regarding the value of business opportunities, technologies and other assets, and the risks and costs of potential liabilities based on information available to us at the time of the transaction. Whether we realize the anticipated benefits from these transactions depends on multiple factors, including our integration of the businesses involved, the performance of the underlying products, capabilities or technologies, and market conditions following the acquisition. Although we believe we have established appropriate procedures and processes to mitigate these risks and have a proven track record of successful acquisitions and investments, unanticipated performance issues and acquired liabilities associated with these activities could adversely affect our financial results.

General Dynamics Annual Report Ÿ 2010 15

Table of Contents

FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K contains forward-looking statements that are based on management’s expectations, estimates, projections and assumptions. Words such as “expects,” “anticipates,” “plans,” “believes,” “scheduled,” “estimates,” “should” and variations of these words and similar expressions are intended to identify forward-looking statements. These include but are not limited to projections of revenues, earnings, segment performance, cash flows, contract awards, aircraft production, deliveries and backlog stability. Forward-looking statements are made pursuant to the safe harbor provisions of the Private Securities Litigation Reform Act of 1995, as amended. These statements are not guarantees of future performance and involve certain risks and uncertainties that are difficult to predict. Therefore, actual future results and trends may differ materially from what is forecast in forward-looking statements due to a variety of factors, including, without limitation, the risk factors discussed in this section.

All forward-looking statements speak only as of the date of this report or, in the case of any document incorporated by reference, the date of that document. All subsequent written and oral forward-looking statements attributable to General Dynamics or any person acting on our behalf are qualified by the cautionary statements in this section. We do not undertake any obligation to update or publicly release any revisions to forward-looking statements to reflect events, circumstances or changes in expectations after the date of this report.

ITEM 1B. UNRESOLVED STAFF COMMENTS

None.

We operate in a number of offices, manufacturing plants, laboratories, warehouses and other facilities in the United States and abroad. We believe our main facilities are adequate for our present needs and, given planned improvements and construction, expect them to remain adequate for the foreseeable future.

On December 31, 2010, our business groups had major operations at the following locations:

| • | Aerospace – Lincoln and Long Beach, California; West Palm Beach, Florida; Brunswick and Savannah, Georgia; Cahokia, Illinois; Westfield, Massachusetts; Las Vegas, Nevada; Teterboro, New Jersey; Dallas, Texas; Appleton, Wisconsin; Beijing, China; Dusseldorf and Hannover, Germany; Mexicali, Mexico; Moscow, Russia; Singapore; Basel, Geneva and Zurich, Switzerland; Dubai, United Arab Emirates; Biggin Hill and Luton, United Kingdom. |