true2022FY000003989900000398992022-01-012022-12-3100000398992022-06-30iso4217:USD00000398992023-02-17xbrli:shares

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

______________________

FORM 10-K/A

(Amendment No. 1)

______________________

(Mark One)

| | | | | |

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2022

| | | | | |

| o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from _________ to _________

Commission file number 1-6961

______________________

TEGNA INC.

(Exact name of registrant as specified in its charter)

______________________

| | | | | | | | | | | | | | | | | |

| Delaware | | 16-0442930 |

| (State or other jurisdiction of incorporation or organization) | | (I.R.S. Employer identification No.) |

| | | | | |

| 8350 Broad Street, | Suite 2000, | Tysons, | Virginia | | 22102-5151 |

| (Address of principal executive offices) | | (Zip Code) |

| | | | | |

| (703) | 873-6600 | | | | |

Securities registered pursuant to Section 12(b) of the Act: | | | | | | | | | | | | | | |

| Title of each class | | Trading Symbol | | Name of each exchange on which registered |

| Common Stock, par value $1.00 per share | | TGNA | | The New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act: None

______________________

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes x No o

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes x No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer”, “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act:

| | | | | | | | | | | | | | | | | | | | | | | |

| Large Accelerated Filer | x | Accelerated filer | o | Non-accelerated filer | o | Smaller reporting company | o |

| | | | | | | |

| | | | | | Emerging growth company | o |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ¨

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. Yes x No o

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes o No x

The aggregate market value of the voting common equity held by non-affiliates of the registrant based on the closing sales price of the registrant’s Common Stock as reported on The New York Stock Exchange on June 30, 2022, was $4,639,159,645. The registrant has no non-voting common equity. As of February 17, 2023, 223,552,503 shares of the registrant’s Common Stock were outstanding.

| | | | | | | | |

Auditor Firm ID: 238 | Auditor Name: PricewaterhouseCoopers LLP | Auditor Location: Washington, District of Columbia |

EXPLANATORY NOTE

On February 27, 2023, TEGNA Inc. (“TEGNA,” the “Company,” “we,” “us,” or “our”) filed our Annual Report on Form 10-K for the fiscal year ended December 31, 2022 (the “Original Form 10-K”). The Original Form 10-K omitted Part III, Items 10 (Directors, Executive Officers and Corporate Governance), 11 (Executive Compensation), 12 (Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters), 13 (Certain Relationships and Related Transactions, and Director Independence) and 14 (Principal Accountant Fees and Services) in reliance on General Instruction G(3) to Form 10-K, which provides that such information may be either incorporated by reference from the registrant’s definitive proxy statement or included in an amendment to Form 10-K, in either case filed with the Securities and Exchange Commission (the “SEC”) not later than 120 days after the end of the fiscal year.

This Amendment No. 1 to Form 10-K (this “Amendment”) is being filed solely to:

•amend Part III, Items 10, 11, 12, 13 and 14 of the Original Form 10-K to include the information required by such Items; and

•file new certifications of our principal executive officer and principal financial officer as exhibits to this Amendment under Item 15 of Part IV hereof, pursuant to Rule 12b-15 under the Securities Exchange Act of 1934, as amended (the “Exchange Act”).

This Amendment does not otherwise change or update any of the disclosures set forth in the Original Form 10-K and does not otherwise reflect any events occurring after the filing of the Original Form 10-K.

INDEX TO TEGNA INC.

Amendment No. 1 to Form 10-K

For the Year ended December 31, 2022

PART III

10. Directors, Executive Officers and Corporate Governance

Board of Directors

The Board of Directors is currently composed of eleven directors.

Our directors are Gina L. Bianchini, Howard D. Elias, Stuart J. Epstein, Lidia Fonseca, Karen H. Grimes, David T. Lougee, Scott K. McCune, Henry W. McGee, Bruce P. Nolop, Neal Shapiro and Melinda C. Witmer.

The age, principal occupation and business experience of each TEGNA director are described below.

| | | | | | | | | | | | | | |

| | Gina L. Bianchini Founder and CEO, Mighty Networks Age: 50 Director since: 2018 | | TEGNA Committees: • Nominating and Governance • Public Policy and Regulation |

Professional Experience: Ms. Bianchini is Founder and Chief Executive Officer of Mighty Networks (formerly known as Mighty Software, Inc.), a position she has held since September 2010. She served as Chief Executive Officer of Ning, Inc. from 2004 to March 2010. Ms. Bianchini also served as a director of Scripps Networks Interactive, Inc. through 2018, as a director of Empower Ltd until July 2021, and as a director of Empower’s successor, Holley Inc., until May 2022. | | Qualifications and Strategy-Related Experience: •Expertise, vision and creativity in the rapidly evolving world of digital media •Deep knowledge of social media and community building technology platforms •Experience with oversight of acquisitions, equity investments, and investor relations •Significant digital and start-up experience |

| | | | | | | | | | | | | | |

| | Howard D. Elias Chair of TEGNA; Chief Customer Officer and President, Services and Digital, Dell Technologies Age: 65 Director since: 2008 | | TEGNA Committees: • Executive (Chair) • Leadership Development and Compensation |

Professional Experience: Mr. Elias was named the Chair of TEGNA in April 2018 and is President, Services and Digital, of Dell Technologies, a position he has held since September 2016. Prior to that, he served as President and Chief Operating Officer, EMC Global Enterprise Services from January 2013 to September 2016 and was President and Chief Operating Officer, EMC Information Infrastructure and Cloud Services from September 2009 to January 2013. From October 2015 through September 2016, Mr. Elias was also responsible for leading the development of EMC Corporation’s integration plans in connection with its transaction with Dell Inc. Previously, Mr. Elias served as President, EMC Global Services and Resource Management Software Group; Executive Vice President, EMC Corporation from September 2007 to September 2009; and Executive Vice President, Global Marketing and Corporate Development, at EMC Corporation from October 2003 to September 2007. | | Qualifications and Strategy-Related Experience: •Extensive operational, managerial, and leadership experience in cloud computing, supply chain management, marketing, corporate development and global customer support •Experience overseeing M&A, new business development and incubation, and integration of acquisitions •Comprehensive global business and management experience in information technology |

| | | | | | | | | | | | | | |

| | Stuart J. Epstein Former Chief Financial Officer, DAZN Group Age: 60 Director since: 2018 | | TEGNA Committees: • Audit |

Professional Experience: Mr. Epstein is the former Chief Financial Officer of DAZN Group, a position he held from September 2018 to July 2022. Previously, he was Senior Advisor, Evolution Media, from October 2017 to January 2018. He served as Co-Managing Partner of Evolution Media from September 2015 to September 2017 and Executive Vice President and Chief Financial Officer of NBCUniversal from September 2011 to April 2014. Prior to that, Mr. Epstein held various senior positions during his 23 years at Morgan Stanley, including Managing Director and Global Head of the Media & Communications Group within the investment banking division. | | Qualifications and Strategy-Related Experience: •Extensive knowledge of media, technology and capital markets •Deep transactional experience with complex deals involving a range of constituencies •Experience in overseeing local broadcast television stations •Significant expertise in overseeing strategic business initiatives

|

| | | | | | | | | | | | | | |

| | Lidia Fonseca EVP and Chief Digital and Technology Officer, Pfizer Inc. Age: 54 Director since: 2014 | | TEGNA Committees: • Audit • Leadership Development and Compensation Other Public Company Directorships: • Medtronic plc |

Professional Experience: Ms. Fonseca is Executive Vice President and Chief Digital and Technology Officer of Pfizer Inc., a position she has held since January 2019. Prior to that she served as Chief Information Officer and Senior Vice President of Quest Diagnostics from April 2014 to December 2018. Previously, Ms. Fonseca served as Chief Information Officer and Senior Vice President of Laboratory Corporation of America (LabCorp) from 2008 to 2013. She was named a Healthcare Transformer by Medical, Marketing & Media in 2019 and in 2017 she received the Forbes CIO Innovation Award recognizing CIOs who lead revenue enhancing innovation efforts. | | Qualifications and Strategy-Related Experience: •Significant expertise in overseeing strategic transformations •Experience leading information technology operations •Deep knowledge of data analytics, automation, supply chain management and information technology •Experience developing and implementing digital strategies across organizations

|

| | | | | | | | | | | | | | |

| | Karen H. Grimes Retired Partner, Senior Managing Director and Equity Portfolio Manager, Wellington Management Company Age: 67 Director since: 2020 | | TEGNA Committees: • Audit • Nominating and Governance Other Public Company Directorships: • Corteva • Toll Brothers, Inc. |

Professional Experience: Ms. Grimes held the position of Senior Managing Director, Partner, and Equity Portfolio Manager at Wellington Management Company LLP, an investment management firm, from January 2008 through December 2018. Prior to joining Wellington Management Company in 1995, she held the position of Director of Research and Equity Analyst at Wilmington Trust Company, a financial investment and banking services firm, from 1988 to 1995. Before that, Ms. Grimes was a Portfolio Manager and Equity Analyst at First Atlanta Corporation from 1983 to 1986 and at Butcher and Singer from 1986 to 1988. Ms. Grimes is a member of the Financial Analysts Society of Philadelphia and holds the Chartered Financial Analyst designation. | | Qualifications and Strategy-Related Experience: •Financial acumen, investment expertise and a returns-focused mindset, including in media and advertising •Extensive executive-level experience and leadership abilities •Deep understanding of financial accounting and internal financial controls •Significant risk management experience •Provides a valuable investor-oriented perspective

|

| | | | | | | | | | | | | | |

| | David T. Lougee President and CEO, TEGNA Inc. Age: 64 Director since: 2017 | | TEGNA Committees: • Executive |

Professional Experience: Mr. Lougee became President and Chief Executive Officer and a director of TEGNA in June 2017. He previously served as the President of TEGNA Media from July 2007 to May 2017. Prior to joining TEGNA, he served as Executive Vice President, Media Operations for Belo Corp. from 2005 to 2007. Mr. Lougee is a past chairman of the National Association of Broadcasters (NAB) as well as the NBC Affiliates Board of Directors and the Television Bureau of Advertising (TVB) Board of Directors. He is currently vice chairman of the Broadcast Music, Inc. Board of Directors and serves on the Board of the Broadcasters Foundation of America. | | Qualifications and Strategy-Related Experience: •Extensive expertise in management and operations •Experience in oversight of strategic acquisitions •Deep and intimate knowledge of the media industry •More than 25 years of experience in a variety of senior leadership roles |

| | | | | | | | | | | | | | |

| | Scott K. McCune Founder, MS&E Ventures; Former VP, Global Media and Integrated Marketing, The Coca Cola Company Age: 66 Director since: 2008 | | TEGNA Committees: • Audit • Executive • Leadership Development and Compensation (Chair) |

Professional Experience: Mr. McCune is the Founder of MS&E Ventures, a firm focused on creating new business value for brands through media, sports and entertainment. Prior to his retirement in March 2014, Mr. McCune spent 20 years at The Coca-Cola Company serving in a variety of roles, including Vice President, Global Partnerships & Experiential Marketing from 2011-2014, Vice President Global Media and Integrated Marketing from 2005-2011, and Vice President, Global Media, Sports & Entertainment Marketing and Licensing from 1994-2004. He also spent 10 years at Anheuser-Busch Inc. where he held a variety of positions in marketing and media. Mr. McCune also serves as a director of First Tee of Atlanta and the College Football Hall of Fame. | | Qualifications and Strategy-Related Experience: •Significant experience as a marketing executive, with an outstanding record of creating value, developing people and building organizational capabilities •Deep knowledge of various aspects of marketing, including integrated marketing media, advertising, digital, licensing, sports & entertainment and experiential •Experience building global brands, leading and inspiring diverse organizations, planning and executing complex operations, innovating new approaches to business, driving productivity and managing P&L |

| | | | | | | | | | | | | | |

| | Henry W. McGee Senior Lecturer, Harvard Business School Age: 70 Director since: 2015 | | TEGNA Committees: • Executive • Nominating and Governance (Chair) • Public Policy and Regulation Other Public Company Directorships: • AmerisourceBergen Corporation |

Professional Experience: Mr. McGee has been a Senior Lecturer at Harvard Business School since July 2013. Previously, he served as a consultant to HBO Home Entertainment from April 2013 to August 2013 after serving as President of HBO Home Entertainment from 1995 until his retirement in March 2013. Mr. McGee held the position of Senior Vice President, Programming, HBO Video, from 1988 to 1995 and prior to that, Mr. McGee served in leadership positions in various divisions of HBO. Mr. McGee also serves as a director of the Pew Research Center and The Black Filmmaker Foundation. He is a former President of the Alvin Ailey Dance Theater Foundation and the Film Society of Lincoln Center. He was recognized by Savoy Magazine in 2016 and 2017 as one of the Most Influential Black Corporate Directors and in 2018 the National Association of Corporate Directors named Mr. McGee to the Directorship 100 as one of the country’s most influential boardroom members. | | Qualifications and Strategy-Related Experience: •Significant business, leadership and management experience in media industry •Expertise in new business planning, operations, marketing and wholesale distribution •Deep understanding of the use of technology in and all aspects of wholesale distribution and international markets •Extensive knowledge of leadership, corporate governance and corporate accountability |

| | | | | | | | | | | | | | |

| | Bruce P. Nolop Retired CFO, E*Trade Financial Corporation Age: 72 Director since: 2015 | | TEGNA Committees: • Audit (Chair) • Executive Other Public Company Directorships: • Marsh & McLennan Companies, Inc. |

Professional Experience: Mr. Nolop retired in 2011 from E*Trade Financial Corporation, where he served as Executive Vice President and Chief Financial Officer from September 2008 through 2010. Mr. Nolop was Executive Vice President and Chief Financial Officer of Pitney Bowes Inc. from 2000 to 2008 and Managing Director of Wasserstein Perella & Co. from 1993 to 2000. Previously, he held positions with Goldman, Sachs & Co., Kimberly-Clark Corporation and Morgan Stanley & Co. Mr. Nolop also served as a director of On Deck Capital, Inc. through October 2020. | | Qualifications and Strategy-Related Experience: •Experience in financial, marketing and shared services operations, expense management, and recapitalizations •Deep understanding of financial accounting, corporate finance, and internal financial controls •Experience in strategic transactions and restructurings |

| | | | | | | | | | | | | | |

| | Neal Shapiro President and CEO, The WNET Group Age: 65 Director since: 2007 | | TEGNA Committees: • Nominating and Governance • Public Policy and Regulation |

Professional Experience: Mr. Shapiro is President and CEO of the public television company WNET, which operates three public television stations in the largest market in the country: Thirteen/WNET, WLIW and NJTV. He is an award-winning producer and media executive with a more than 35-year career spanning print, broadcast, cable and online media. Before joining WNET in February 2007, Mr. Shapiro served in various executive capacities with the National Broadcasting Company beginning in 1993 and was president of NBC News from May 2001 to September 2005. During his career, Mr. Shapiro has won numerous journalism awards, including 32 Emmys, 31 Edward R. Murrow Awards and 3 Columbia DuPont awards. He also serves on the Board of Trustees at Tufts University and as a member of the Board of Trustees of American Public Television. | | Qualifications and Strategy-Related Experience: •Strong broadcast industry experience •Expertise in overseeing operations and strategy of news networks •Expertise in news production and reporting, journalism and First Amendment issues •Deep experience in programming and content sharing |

| | | | | | | | | | | | | | |

| | Melinda C. Witmer Founder and CEO, Foiye Inc.; Former Executive Vice President, Chief Video & Content Officer, Time Warner Cable Age: 61 Director since: 2017 | | TEGNA Committees: • Executive • Leadership Development and Compensation • Public Policy and Regulation (Chair) |

Professional Experience: Ms. Witmer is the Founder and CEO of Foiye Inc., a social entertainment platform for real estate and home enthusiasts operating as foiye.com, a position she has held since May 2021. Foiye is the successor to Look Left Media, a startup company Ms. Witmer founded in March 2018 that was focused on the development of new real estate technology and media products. From January 2012 until May 2016, Ms. Witmer served as Executive Vice President, Chief Video & Content Officer of Time Warner Cable and Chief Operating Officer of Time Warner Cable Networks, which followed a five-year period starting in January 2007 as Time Warner Cable’s Executive Vice President and Chief Programming Officer. Prior to joining Time Warner Cable in 2001, Ms. Witmer was Vice President and Senior Counsel at Home Box Office, Inc. | | Qualifications and Strategy-Related Experience: •Significant experience in the industry including media operations, telecommunications programming and content •Expert in the negotiation of content distribution agreements, including retransmission consent agreements with local broadcaster groups •Deep understanding of the changing media landscape •Experience in capitalizing on market opportunities, new technologies and emerging platforms in the media space, including innovative consumer experiences |

Committees of the Board of Directors

The Board of Directors conducts its business through meetings of the Board and its four standing committees: the Audit Committee, Leadership Development and Compensation Committee, Nominating and Governance Committee, and Public Policy and Regulation Committee. The Board also has an Executive Committee (not shown on the chart below) made up of the Board Chair, the CEO and each of the Board committee chairs, that may exercise the authority of the Board between meetings, as required. The chart below shows the current membership and chairperson of each of the standing Board committees and the number of committee meetings held during 2022. Each member of the Audit, Leadership Development and Compensation, Nominating and Governance, and Public Policy and Regulation Committee meets the applicable independence requirements of the SEC and NYSE for service on the Board and each committee on which she or he serves.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| # of

Meetings Held | Bianchini | Elias | Epstein | Fonseca | Grimes | Lougee | McCune | McGee | Nolop | Shapiro | Witmer |

| Audit | 4 | | | l | l | l | | l | | C | | |

| Leadership Development and Compensation | 3 | | l | | l | | | C | | | | l |

| Nominating and Governance | 3 | l | | | | l | | | C | | l | |

| Public Policy and Regulation | 3 | l | | | | | | | l | | | C |

| | | | | | | | | | | | |

| C - Chairperson | | | | | | | | | | | | |

Audit Committee

The Audit Committee assists the Board of Directors in its oversight of financial reporting practices and the quality and integrity of the financial reports of the Company, including compliance with legal and regulatory requirements, the independent registered public accounting firm’s qualifications and independence, and the performance of the Company’s internal audit function. The Audit Committee appoints and is responsible for setting the compensation of the Company’s independent registered public accounting firm. The Audit Committee reviews the Company’s independent registered public accounting firm’s qualification, performance and independence on an annual basis.

The Audit Committee also provides oversight of the Company’s internal audit function and oversees the adequacy and effectiveness of the Company’s accounting and financial controls and the guidelines and policies that govern the process by which the Company undertakes financial, accounting and audit risk assessment and risk management. In connection with the Ethics Policy, the Audit Committee has established procedures for the receipt, retention and treatment of complaints received by the Company regarding accounting controls or auditing matters and the confidential, anonymous submission by employees of the Company of any accounting or auditing concerns. In addition, the Committee monitors the Company’s finance- and investment-related diversity and inclusion efforts, including the Company’s investment, procurement and purchasing involving minority-owned businesses.

The Audit Committee members are not professional accountants or auditors, and their role is not intended to duplicate or certify the activities of management and the independent registered public accounting firm.

The Board has determined that each of Bruce P. Nolop, Stuart J. Epstein and Karen H. Grimes is an audit committee financial expert, as that term is defined under SEC rules, and is independent, as defined in the NYSE listing rules.

Executive Committee

The Executive Committee may exercise the authority of the Board between Board meetings, except as limited by Delaware law. In 2022, the full board was able to review all items requiring Board oversight or approval and did not require the Executive Committee to act in its stead.

Leadership Development and Compensation Committee

The Leadership Development and Compensation Committee discharges the Board’s responsibilities relating to the compensation of the Company’s executives and has overall responsibility for the Company’s compensation plans, principles and programs. The Committee also monitors the Company’s human resources practices, including its performance in diversity, inclusion and equal employment opportunity, and supports the Company’s commitment to

diversity and inclusion and the continuation of the Company’s successful efforts to gain and maintain diversity among its employees and management.

Under its charter, the Committee may, in its sole discretion, engage, retain and compensate any compensation consultant, independent legal counsel or other adviser it deems necessary. In selecting a consultant, counsel or adviser, the Committee evaluates its independence by considering the independence factors set forth in applicable SEC and NYSE rules and any other factors the Committee deems relevant to the adviser’s independence from management.

The Committee retains Meridian Compensation Partners, LLC (Meridian) as its consultant to advise it on executive compensation matters. The Committee has determined that Meridian is an independent compensation consultant based on a review of the independence factors considered by the Committee.

Meridian participates in Committee meetings as requested by the chair of the Committee and communicates directly with the chair and other members of the Committee outside of meetings. Meridian specifically has provided the following services to the Committee:

•Consulted on various compensation plans, policies and practices;

•Participated in Committee executive sessions without management present;

•Assisted in analyzing executive compensation practices and trends and other compensation-related matters;

•Consulted with management and the Committee regarding market data used as a reference for pay decisions;

•Consulted on the structure of the equity award program; and

•Reviewed the CD&A and other compensation related disclosures contained in this report.

Nominating and Governance Committee

The Nominating and Governance Committee regularly monitors the composition of the Board to ensure that it has the necessary mix of skills and experience to support the Company’s strategic focus, including diversity of thought, age, experience and racial, ethnic, and gender diversity. The Committee is charged with identifying individuals qualified to become Board members, recommending to the Board candidates for election or re-election to the Board, and considering from time to time the Board committee structure and makeup. The Committee also monitors and takes a leadership role with respect to the Company’s corporate governance practices.

The Nominating and Governance Committee charter sets forth certain criteria for the Committee to consider in evaluating potential director nominees. In addition to evaluating a potential director’s independence, the Committee considers whether director candidates have relevant experience and skills to assure that the Board has the necessary breadth and depth to perform its oversight function effectively. The charter also encourages the Committee to work to maintain a board that reflects the diversity, in terms of gender, age, race, ethnicity and other self-identified diversity attributes of the communities the Company serves, and to support that goal through appropriate board-level self-assessment, nomination and recruitment processes. The Committee evaluates potential candidates against these requirements and objectives. For those director candidates who appear upon first consideration to meet the Committee’s criteria, the Committee will engage in further research to evaluate their candidacy.

The Nominating and Governance Committee periodically retains search firms to assist in the identification of potential director nominee candidates based on criteria specified by the Committee and in evaluating and pursuing individual candidates at the direction of the Committee. The Committee will also consider timely written suggestions from shareholders. In addition to satisfying the requirements under our By-Laws, to comply with the SEC’s universal proxy rules, stockholders who intend to solicit proxies in support of director nominees other than the Company’s nominees at any annual meeting of stockholders must provide notice that sets forth the information required by Rule 14a-19 under the Exchange Act no later than 60 days prior to the anniversary of the previous year's annual meeting date, except that, if we did not hold an annual meeting during the previous year, or if the date of the meeting has changed by more than 30 calendar days from the previous year, then notice must be provided by the later of 60 calendar days prior to the date of the annual meeting or the 10th calendar day following the day on which we first announce the date of the annual meeting.

The By-laws of the Company establish a mandatory retirement age of 73 for directors who have not been executives of the Company and 65 for directors who have served as executives, except that the Board of Directors may extend the retirement age beyond 65 for directors who are or have been the CEO of the Company. The Company’s Principles of Corporate

Governance also provide that a director who retires from, or has a material change in responsibility or position with, the primary entity by which that director was employed at the time of his or her election to the Board of Directors shall offer to submit a letter of resignation to the Nominating and Governance Committee for its consideration. The Committee will make a recommendation to the Board of Directors on whether to accept or reject the resignation, or whether other action should be taken.

In July 2022, Mr. Epstein resigned from his position with DAZN Group and in February 2022, Mr. Elias informed the Board that he was retiring from Dell Technologies, effective May 5, 2023. In accordance with the procedures outlined in the Company’s Principles of Corporate Governance, Mr. Epstein and Mr. Elias each offered to submit a letter of resignation to the Committee for consideration in connection with their respective changes in employment status. In both cases the Committee recommended that the Board not accept the resignation offers and the Board accepted the Committee’s recommendations. With respect to Mr. Epstein, it was the sense of the Committee, and the Board more generally, that Mr. Epstein’s extensive knowledge of media, technology and capital markets, as well as his deep transactional experience, expertise in overseeing strategic business initiatives and financial acumen would continue to make him a valuable member of the Board. With respect to Mr. Elias, it was the sense of the Committee, and the Board more generally, that Mr. Elias is an exemplary leader of the Board, as most notably illustrated by the valuable strategic guidance he provided in connection with the negotiations relating to the Merger Agreement, and that Mr. Elias’s extensive experience overseeing M&A and new business development and his comprehensive global business and management experience in information technology, would continue to make him an invaluable asset to the Board.

Public Policy and Regulation Committee

The Public Policy and Regulation Committee assists the Board in its oversight of risks relating to legal, regulatory, compliance, public policy and corporate social responsibility matters that may impact the Company’s operations, performance or reputation. The Committee’s duties and responsibilities include reviewing and providing guidance to the Board about legal, regulatory and compliance matters concerning media, antitrust and data privacy, and monitoring legislative and regulatory trends and public policy developments that may affect the Company’s operations, strategy, performance or reputation. The Public Policy and Regulation Committee also is responsible for reviewing compliance with the Company’s Ethics Policy and assuring appropriate disclosure of any waiver of or change in the Ethics Policy for executive officers, and for reviewing the Ethics Policy on a regular basis and proposing or adopting additions or amendments to the Ethics Policy as appropriate. In addition, the Committee monitors the Company’s policies and programs relating to corporate social responsibility, sustainability, and ESG-related matters within its purview, and periodically discusses with management the Company’s initiatives for promoting racial and ethnic diversity in its news and other content.

Committee Charters

The written charters governing the Audit Committee, the Leadership Development and Compensation Committee, the Nominating and Governance Committee and the Public Policy and Regulation Committee, as well as the Company’s Principles of Corporate Governance, are posted on the Corporate Governance page of the Company’s website at www.tegna.com under the “Investors” menu. You may also obtain a copy of any of these documents without charge by writing to: TEGNA Inc., 8350 Broad Street, Suite 2000, Tysons, Virginia 22102, Attn: Secretary.

Ethics Policy

The Company has long maintained a code of conduct and ethics (the “Ethics Policy”) that sets forth the Company’s policies and expectations. The Ethics Policy, which applies to every Company director, officer and employee, addresses a number of topics, including conflicts of interest, relationships with others, corporate payments, the appearance of impropriety, disclosure policy, compliance with laws, corporate opportunities and the protection and proper use of the Company’s assets. The Ethics Policy meets the NYSE’s requirements for a code of business conduct and ethics as well as the SEC’s definition of a code of ethics applicable to the Company’s senior officers. Neither the Board of Directors nor any Board committee has ever granted a waiver of the Ethics Policy.

The Ethics Policy is available on the Corporate Governance page of the Company’s website at www.tegna.com under the “Investors” menu. You may also obtain a copy of the Ethics Policy without charge by writing to: TEGNA Inc., 8350 Broad Street, Suite 2000, Tysons, Virginia 22102, Attn: Secretary. Any additions or amendments to the Ethics Policy, and any waivers of the Ethics Policy for executive officers or directors, will be posted on the Corporate Governance page under the

“Investors” menu of the Company’s website and similarly provided to you without charge upon written request to this address.

The Company has a telephone hotline staffed by an independent third party for employees and others to submit their concerns regarding violations or suspected violations of the Company’s Ethics Policy or violations of law and for reporting any concerns regarding accounting or auditing matters on a confidential anonymous basis. Employees and others can report concerns by calling 1-800-695-1704 or by emailing or writing to the addresses provided in the Company’s Whistleblower Protection & Ethics Violations Reporting Policy found on the Corporate Governance page of the Company’s website at www.tegna.com under the “Investors” menu. Any concerns regarding accounting or auditing matters so reported will be communicated to the Company’s Audit Committee.

Corporate Governance

The Board and the Company have instituted strong corporate governance practices to ensure that the Company operates in ways that support the long-term interests of our shareholders. Important corporate governance practices of the Company include the following:

| | | | | | | | | | | | | | |

| ü | All of our directors are elected annually. | | ü | Our directors and senior executives are subject to stock ownership guidelines. |

| | | | |

| ü | Ten of the eleven TEGNA directors are independent. | | ü | We do not have a shareholder rights plan (poison pill) in place. |

| | | | |

| ü | We have a robust shareholder engagement program pursuant to which our independent directors and senior management typically engage with investors. | | ü | We have a majority vote standard for uncontested director elections and a director resignation policy. |

| | | | |

| ü | We have an independent Board chair. | | ü | Our Board has adopted a proxy access by-law provision. |

| | | | |

| ü | We maintain an ongoing board refreshment process, which has resulted in our adding four independent directors since 2017 and the transition of the Board chair role during 2018. | | ü | Mergers and other business combinations involving the Company generally may be approved by a simple majority vote. |

Additional information regarding the Company’s corporate governance practices is included in the Company’s Principles of Corporate Governance posted on the Corporate Governance page under the “Investors” menu of the Company’s website at www.tegna.com. See the “Compensation Discussion and Analysis” section of this report for a discussion of the Company’s compensation-related governance practices.

11. Executive Compensation

Compensation Discussion and Analysis

The Leadership Development and Compensation Committee of the Board of Directors (the “Committee”) believes that the 2022 compensation of our Named Executive Officers appropriately reflects and rewards their significant contributions to the Company’s strong performance in a year that included a number of extraordinary events, including the announcement that the Company had entered into a merger agreement with certain affiliates of Standard General L.P. on February 22, 2022 (“Merger Agreement”), and a challenging macroeconomic environment.

The Committee continuously reviews the structure of our executive compensation program and, based on shareholder feedback over recent years, has endeavored to further strengthen the link between pay and performance and enhanced our disclosure of executive compensation structure and practices. Our 2022 compensation program also was impacted by compensation-related provisions contained in the Merger Agreement.

This Compensation Discussion and Analysis (CD&A) explains the guiding principles and practices upon which our executive compensation program is based and the 2022 compensation paid to our Named Executive Officers (also referred to as “NEOs”), who for the 2022 fiscal year were:

•David T. Lougee, President and Chief Executive Officer,

•Victoria D. Harker, Executive Vice President and Chief Financial Officer,

•Lynn Beall (Trelstad)*, Executive Vice President and Chief Operating Officer—Media Operations, and

•Akin S. Harrison, Senior Vice President and General Counsel.

* “Beall” is Ms. Trelstad’s maiden name and the name she uses for business purposes. “Trelstad” is her married and legal name.

Executive Summary

PERFORMANCE HIGHLIGHTS

Highlights of the Company's 2022 performance included:

Record total revenues. Total company revenue was a record $3.3 billion, up ten percent year-over-year and up 12% on a two-year basis.

Record subscription revenue. The company achieved record subscription revenue of $1.5 billion, which was up four percent year-over-year.

Political revenue. The company generated $341 million in political revenue, a record for a non-presidential election year.

GAAP net income. The company’s GAAP net income was a record $631 million.

Record Adjusted EBITDA. Company Adjusted EBITDA was a record $1.1 billion (representing net income attributable to TEGNA before net income attributable to redeemable noncontrolling interest, income taxes, interest expense, equity (loss), other non-operating items, special items, depreciation and amortization), which was an increase of 19% compared to 2021 and was driven by high-margin political and subscription revenues, as well as ongoing cost management to ensure efficient operations. This result was also up 11% on a two-year basis.

PAY FOR PERFORMANCE

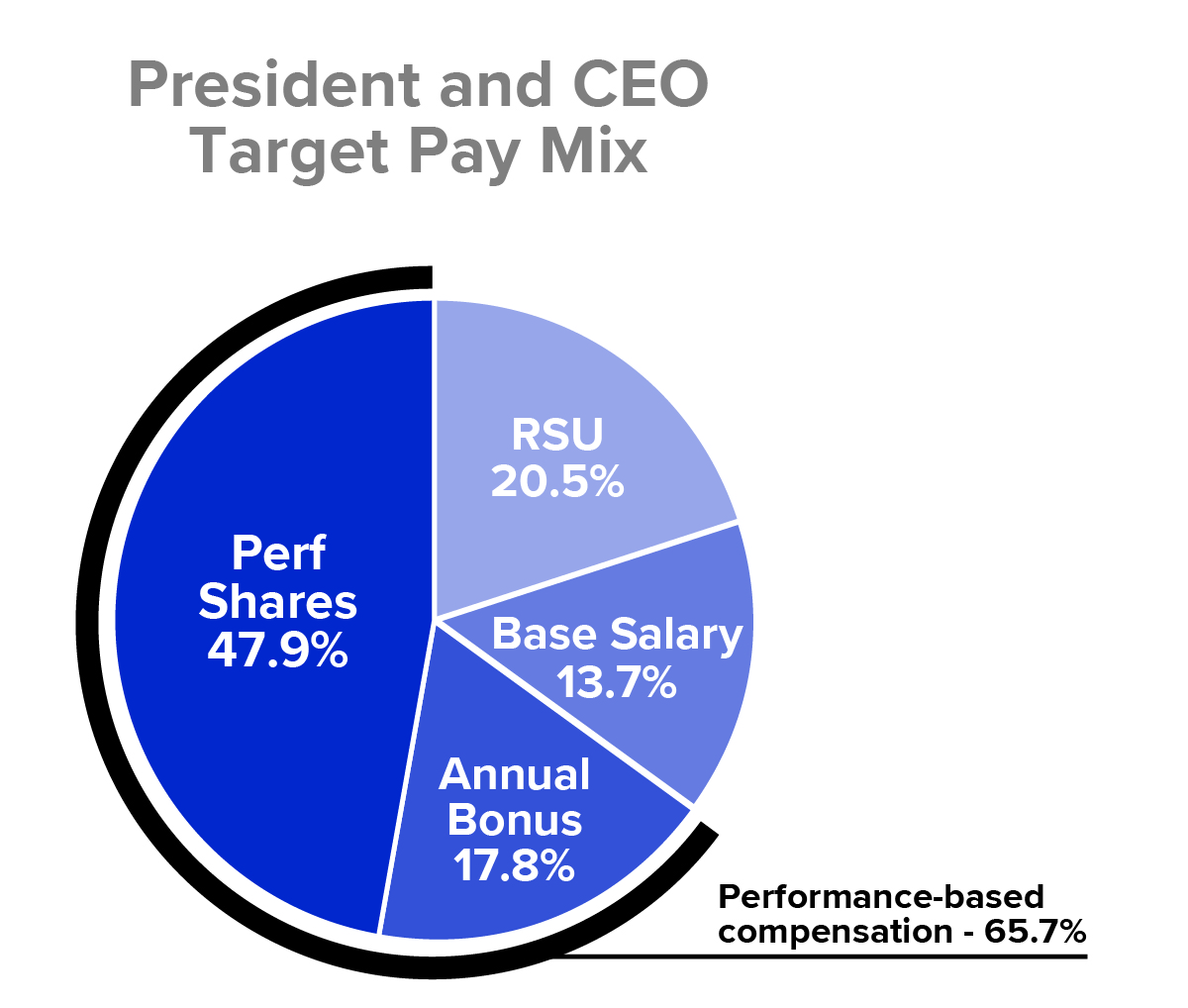

The Committee supports compensation policies that place a heavy emphasis on pay for performance. Our NEOs receive a majority of their long-term equity awards as performance shares that may be earned, if at all, based on the Company’s achievement of performance goals established by the Committee, which we believe strengthens the pay for performance aspect of the Company’s long-term incentive program, and the compensation program overall. The percentage of NEO annual equity awards granted on February 28, 2022 (based on grant date value) that were performance-based were 70% for our CEO (with the remaining 30% being time-based restricted stock units (RSUs)) and 55% for each of the other NEOs (with the remaining 45% being time-based RSUs).

A MAJORITY OF OUR CEO’S 2022 TARGET PAY WAS PERFORMANCE-BASED

LEADERSHIP DEVELOPMENT AND COMPENSATION COMMITTEE RESPONSIBILITIES

The Committee oversees the Company’s executive compensation program and is responsible for:

•Evaluating and approving the Company’s executive compensation plans, principles and programs, as well as overseeing the compensation program for non-employee directors;

•Administering the Company’s equity incentive plans and granting bonuses and equity awards to our senior executives;

•Reviewing and approving on an annual basis corporate goals and objectives relevant to the compensation of the Company’s President and CEO and its other senior executives; and

•Reviewing risks relating to the Company’s executive compensation plans, principles and programs.

The Committee also regularly reviews other components of executive compensation, including benefits, perquisites and post-termination pay. The Board has historically delegated to the Company’s President and CEO the authority for approving equity grants to employees other than our senior executives within the parameters of a pool of shares approved by the Board.

GUIDING PRINCIPLES

In making its NEO compensation decisions, the Committee is guided by the following principles:

•Pay for performance—Compensation should place a heavy emphasis on pay for performance and substantial portions of total compensation should be “at risk.”

•Attract, retain and motivate—Compensation should help us attract and retain superior executive talent and motivate key employees to ensure our overall success and long-term strength.

•Fairness and Shareholder Alignment—Compensation should be fair to both executives and shareholders and should align the interests of our executives with those of our shareholders.

•Pay competitively—Compensation opportunities generally should be in line with those afforded to executives holding similar positions at comparable companies, although we expect variability based on role and incumbent-specific circumstances.

•Promote stock ownership—Compensation in the form of equity grants should allow our executives to acquire and maintain a meaningful level of investment in Company common stock consistent with our stock ownership guidelines. This helps to align the economic interests of our executives with those of our shareholders. The Committee regularly reviews the levels of senior executive stock ownership.

The following table reflects the minimum stock ownership guideline for each NEO. As of the date of this report, all of the NEOs significantly exceed their minimum ownership guideline.

| | | | | | | | |

| NAME | | MINIMUM

GUIDELINE

MULTIPLE

OF BASE

SALARY |

| Mr. Lougee | | 5X |

| Ms. Harker | | 3X |

| Ms. Beall | | 2X |

| Mr. Harrison | | 1X |

The Company’s stock ownership guidelines require that executives hold all after-tax shares they receive from the Company as compensation until they have met the stock ownership guidelines detailed above.

COMPENSATION-RELATED GOVERNANCE PRACTICES

The Board’s commitment to strong corporate governance practices extends to the compensation plans, principles, programs and policies established by the Committee. The Company’s compensation-related governance practices and policies of note include the following:

ü Performance-based pay. We provide compensation to our NEOs that is majority performance-based.

ü Outcome alignment. Each year we review the Company’s compensation and financial performance against internal budgets, financial results from prior years and Comparative Market Data to make sure that executive compensation outcomes are aligned with the absolute and relative performance of the Company.

ü Cap on incentive payouts. We cap the maximum payout under the annual bonus plan and performance share awards at 200% of target.

ü Double-trigger equity vesting upon a change in control. We accelerate the vesting of equity awards in connection with a change in control only upon a double trigger (i.e., upon an executive’s qualifying termination of employment within two years following the date of the change in control) unless the awards are not continued or assumed, in which case the awards immediately vest.

ü Clawback. We have a recoupment policy that provides:

•That fraud or intentional misconduct by any employee that results in an accounting restatement due to material non-compliance with the securities laws would trigger a recoupment of certain incentive compensation from the responsible employee, as determined by the Committee; and

•That the Committee may recoup up to three years of an employee’s incentive compensation if that employee’s gross negligence or intentional misconduct caused the Company material harm (financial, competitive, reputational or otherwise).

ü No unearned dividends. We do not pay dividends or dividend equivalents on unearned performance shares or unpaid restricted stock unit awards granted to employees.

ü All new change-in-control arrangements are double trigger without excise tax gross-ups. Severance for executives who became eligible to participate in a change in control severance plan after April 15, 2010 is double trigger and those executives are not eligible for an excise tax gross-up.

ü Risk evaluation. We regularly evaluate the risks associated with the Company’s compensation plans and programs and consider the potential relationship between compensation and risk taking.

ü Anti-hedging. We maintain a policy that prohibits the Company’s employees and directors from hedging or short-selling the Company’s shares.

ü Anti-pledging. We prohibit the Company’s executive officers and directors from pledging the Company’s shares.

ü Multi-dimensional performance assessment. Under both the Company’s annual bonus plan and the performance share component of annual equity grants, we assess NEO performance against a number of metrics covering the income and cash-flow statements and quantitative and qualitative KPIs tailored for each executive.

ü No excessive perquisites. We do not provide significant perquisites to our named executive officers.

SAY ON PAY

The Committee reviews and thoughtfully considers the results of Say on Pay votes when evaluating our executive compensation program. Ninety six and one half percent (96.5%) of our shareholders supported our executive compensation program at the Company’s 2022 annual meeting of shareholders, which reflected an overwhelmingly positive level of support for our executive compensation. As a result, we did not make any specific changes to our executive compensation programs as a result of this vote. Additionally, it is typically our practice to actively engage our shareholders throughout the year to garner feedback, including with respect to our executive compensation programs and policies, but in 2022 our engagement with shareholders was limited due to the pendency of the transactions contemplated by the Merger Agreement.

Overview of Executive Compensation Program

Key Components of Annual Compensation Decisions

The table below describes key components of the Company’s 2022 executive compensation program, which generally remained unchanged from 2021. | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | Component | | Description | | Performance

Considerations | | Pay Objective |

Short Term

Cash Compensation | | BASE SALARY | | Pay for service in executive role. | | Based on the nature and responsibility of the position, achievement of key performance indicators, internal pay equity among positions and competitive market data. | | Attraction and retention. Base salary adjustments also allow the Committee to reflect an individual’s performance, scope of the position, and/or changed responsibilities. |

| | | | | | | |

| ANNUAL BONUS | | Short-term program providing NEOs with an annual cash bonus payment. | | Based on the Committee’s assessment of each NEO’s achievement of annual key performance indicators and contributions to Company-wide performance, as well as, for 2022, treatment contemplated by the Merger Agreement. | | Reward performance in attaining Company and individual performance goals based on the Company’s financial and strategic goals on an annual basis. |

| | | | | | | | |

Long-Term

Equity Incentives | | PERFORMANCE

SHARES | | Long-term equity grants that vest based on the Company’s Adjusted EBITDA and Free Cash Flow as a Percentage of Revenue performance over a two-year period compared to preset targets set by the Committee. | | Based on the measurement of the Company’s performance against two important financial metrics on which the Company focuses from a strategic growth perspective. The value of awards is also tied to the Company’s share price performance during the three-year vesting period. | | Reward longer-term performance in attaining Company performance goals, which in turn drives shareholder value creation; align the interests of executives with those of shareholders; and promote retention and foster stock ownership. |

| | | | | | | |

| RESTRICTED

STOCK UNITS

(RSUs) | | Long-term equity grants that generally vest over four years on a pro-rata basis. | | Alignment with shareholders through Company share price performance and the creation of shareholder value. | | Align the interests of executives with those of shareholders, promote retention and foster stock ownership. |

How the Committee Determines NEO Compensation

The Committee determines NEO compensation in its sole discretion based on its business judgment, informed by the experience of the Committee members, input from Meridian (the Committee’s independent compensation consultant),

market data, the Committee’s and the CEO’s assessment of each NEO, achievement of key performance indicators, the Company’s performance and progress towards achievement of its strategic plan and the challenges confronting our business. No NEO participates in the determination of his or her own compensation.

The Committee does not focus on any one particular objective, formula or financial metric, but rather on performance relative to what it considers to be value-added quantitative and qualitative goals in furtherance of our compensation guiding principles described in the Executive Summary of this Compensation Discussion and Analysis.

Key Performance Indicators

The Committee assesses the degree and extent of achievement of key performance indicators (KPIs) as a principal tool for making NEO compensation decisions. KPIs, set annually for each of our executive officers, consist of individually designed qualitative and quantitative goals organized in three areas:

•Profit and Revenue Goals, which include, as appropriate, revenue, adjusted EBITDA, operating income, free cash flow, digital revenue and other financial goals for the Company and the respective businesses and/or functions over which each NEO has operational or overall responsibility;

•Strategic and Business Goals, which include specific areas in which the NEO is asked to innovate and collaborate to adopt and implement new products and programs in support of the Company’s strategic plan; and

•People Goals, which include measures of leadership, achievement of diversity initiatives, First Amendment activities, and other significant qualitative objectives such as promoting an ethical Company work environment and diverse workforce and maintaining our reputation as a good corporate citizen of the communities in which we do business.

Each NEO’s KPIs include multiple goals in each of the three areas. The KPIs are intended to be challenging but realistic, with a high degree of difficulty in achieving all of the goals set for each NEO. Except for the CEO, whose performance scorecard has been enhanced with specific weightings in response to shareholder feedback, the Committee’s assessment of NEO performance versus KPIs is holistic, with no particular weighting ascribed to achievement of any particular item in any area. This allows for the Committee to assess each of our other NEOs’ performance against the goals and metrics that are most pertinent to the area of focus for each NEO and most appropriately measure his or her performance, with the ultimate goal of aligning pay and performance for each NEO. While the Committee takes into consideration the degree of achievement of each NEO’s KPIs and the Company performance goals and financial measures set forth above in making compensation decisions, the Committee exercises its business judgment, in its sole discretion, to set NEO compensation.

Comparative Market Data

•To assist the Committee in making decisions affecting NEO compensation opportunities, the Committee, with support from Meridian, its independent advisor, reviewed a report from Company management providing, among other things, executive compensation market data. The report included data from the Willis Towers Watson Media Compensation Survey, the Willis Towers Watson General Industry Executive Compensation Survey, the Croner Digital Content and Technology Survey, the Equilar Media & Technology Survey, and the Radford Global Compensation Survey, a source of detailed executive compensation information (collectively, “Comparative Market Data”).

•Through use of this data, the Committee compares NEO salaries, bonus opportunities and equity compensation opportunities to those of companies in the media sector and other companies with comparable revenues to confirm that the elements of our compensation program and the compensation opportunities we afford our executives are appropriately competitive. The Committee does not, however, target elements of compensation nor total compensation to a certain range, percentage or percentile within the Comparative Market Data.

BASE SALARY

We pay our NEOs base salaries to compensate them for service in their executive role. Salaries for NEOs take into account:

•the nature and responsibility of the position;

•the achievement of KPIs, both historically and in the immediately prior year;

•internal pay equity among positions; and

•Comparative Market Data, as described above.

The table below shows the 2022 NEO base salaries set by the Committee based on the foregoing factors:

| | | | | | | | |

| EXECUTIVE | | 2022 BASE SALARY |

| Mr. Lougee | | $ | 975,000 | |

| Ms. Harker | | $ | 730,000 | |

| Ms. Beall | | $ | 650,000 | |

| Mr. Harrison | | $ | 500,000 | |

ANNUAL BONUSES

ANNUAL BONUS OPPORTUNITY

Our NEOs participate in an annual bonus program designed to reward each NEO’s contribution to overall Company results and attainment of strategic business objectives during the year. Annual bonuses therefore can vary in amount from year to year.

Beginning in late 2021 and continuing into early 2022, the Committee, in consultation with Meridian, its independent compensation consultant, determined the target bonus opportunities for each NEO. The Committee established these amounts, which are based on a target percentage of each NEO’s base salary, after thorough consideration of:

•the nature and responsibility of the position;

•internal pay equity among positions; and

•Comparative Market Data.

Based on these factors, the Committee approved the following 2022 target bonus opportunities for our NEOs. Only Mr. Lougee’s and Mr. Harrison’s bonus targets were increased from 2021, based on corresponding changes to the target percentage of their respective base salaries:

| | | | | | | | | | | | | | | | | | | | |

| EXECUTIVE | | BASE SALARY | | TARGET

PERCENTAGE

OF BASE

SALARY | | BONUS

GUIDELINE

AMOUNT |

| Mr. Lougee | | $ | 975,000 | | | 130 | % | | $ | 1,267,500 | |

| Ms. Harker | | $ | 730,000 | | | 100 | % | | $ | 730,000 | |

| Ms. Beall | | $ | 650,000 | | | 100 | % | | $ | 650,000 | |

| Mr. Harrison | | $ | 500,000 | | | 85 | % | | $ | 425,000 | |

ANNUAL BONUS PERFORMANCE MEASURES FOR 2022

The Committee determined the extent to which each NEO earned his or her respective 2022 bonus, informed by attainment of the Company’s annual financial and qualitative performance goals, individual contributions made by the NEO during the year and each NEO’s performance against his or her KPIs.

In addition, the Committee considered the performance of the Company across a broad spectrum of financial measures, including total revenues, operating income, net income, earnings per share, Adjusted EBITDA, EBITDA margins, subscription revenue and free cash flow as a percentage of revenue. The Committee selected these financial measures because, individually and collectively, they represent the most significant financial aspects of our Company that we believe drive our financial success as a pure-play media company and enhance shareholder value.

For 2022, the Committee compared the Company’s reported performance with respect to each of these financial performance measures against goals approved by the Board at the beginning of the year, financial results from prior years, and financial performance of peer companies and the industry, and considered the Company’s achievements of budgeted amounts in light of the bonus treatment contemplated by the terms of the Merger Agreement, which provides that employee bonuses for 2022 would be paid at the greater of (i) the employee’s bonus entitlement based on the actual level of

achievement of the applicable performance goals for 2022 and (ii) the employee’s bonus entitlement assuming achievement of target level performance.

In addition, the Committee evaluated the performance of our executives, the roles played by each of them in contributing to the Company’s progress in creating shareholder value, achieving critically important strategic transactions and the performance highlights described in the “Executive Summary” above. Other factors considered by the Committee for the 2022 bonus awarded to each NEO are described below.

David T. Lougee, President and Chief Executive Officer

2022 Goals:

The Committee evaluated Mr. Lougee’s 2022 performance using a scorecard that measures Mr. Lougee’s results against financial and non-financial KPIs, with the financial and non-financial KPIs each assigned an overall 50% weighting by the Committee. Mr. Lougee’s financial KPIs included EBITDA and revenue targets, with the EBITDA target weighted at 35% and the revenue target weighted at 15%.

Mr. Lougee’s non-financial goals included strategic goals relating to driving long-term growth for the Company (taking into account anticipated market forces and dynamics), the Company’s 2022 business priorities (key business initiatives critical to the Company during 2022), and the Company’s 2022 people goals (building the organization with capabilities and a culture for the future, including diversity and inclusion goals). These non-financial goals were weighted as follows: strategic (25%), business priorities (15%) and people (10%). The Committee also assessed Mr. Lougee’s performance in the context of the core CEO responsibility to serve as the Company’s chief spokesperson and effectively communicate with all of the Company’s stakeholders, including its shareholders, employees, customers, Board of Directors and community and industry groups.

2022 Performance Highlights and Accomplishment of 2022 Goals:

During 2022, Mr. Lougee led the Company to record full-year revenue and EBITDA, drove the successful negotiation of the Merger Agreement, successfully negotiated retransmission agreements with certain of the Company’s largest distributors, oversaw record revenue for Premion, and continued to strengthen the Company’s commitment to diversity, equity and inclusion. Mr. Lougee’s annual bonus for 2022 reflected these accomplishments as well as the Committee’s assessment of the performance of his duties and his achievement of the following KPIs:

| | | | | | | | |

| Financial KPIs | | •Achieved full year Company Adjusted EBITDA of $1.1 billion,* which was below his EBITDA KPI, partially driven by weaker political and macroeconomic forces impacting subscribers and advertising revenue. •Achieved record full-year revenue of $3.3 billion, up ten percent year-over-year but short of his revenue KPI due in part to AMS revenue declines as a result of political displacement and macroeconomic headwinds. |

| | |

| Non-financial KPIs: Strategic and Business | | • Successfully led negotiations that culminated in entering into the Merger Agreement, pursuant to which the Company will be acquired by an affiliate of Standard General for $24.00 per share in cash, subject to stockholder and regulatory approvals, and other customary closing conditions. •Successfully led the Company’s negotiations of comprehensive retransmission consent agreements representing approximately 38% of the Company’s subscribers. •Oversaw record revenue for Premion despite macroeconomic challenges. •Continued to execute on the Company’s expense savings plan. |

| | |

| Non-financial KPIs: People | | • Oversaw the Company’s progress on its 2025 diversity, equity and inclusion goals, for which the Company remains on track to achieve on schedule, including increasing the ethnic and gender diversity of the Company’s station general managers. •Enhanced support of Company leaders in the selection of diverse talent and the navigation of complex employee matters regarding race and inclusion. •Expanded the Company’s initiatives to identify and develop its internal talent, including expanding the Producer-in-Residence program and implementing a new Sales-in-Residence program. |

*Reconciliation of the following non-GAAP financial measure to the Company’s results as reported under accounting principles generally accepted in the United States may be found in the Company’s Form 10-K, filed: adjusted EBITDA – page 32.

Victoria D. Harker, Executive Vice President and Chief Financial Officer

2022 Goals:

The Committee evaluated Ms. Harker’s 2022 performance using financial and non-financial KPIs it developed in consultation with Mr. Lougee. Ms. Harker’s financial KPIs included, among other things, Adjusted EBITDA and revenue targets, and expense management.

Ms. Harker’s non-financial goals included, without limitation, acquisition support/transition planning and capital allocation, and people goals relating to hiring and promotion, racial and gender diversity and succession planning.

2022 Performance Highlights and Key Accomplishments:

Ms. Harker delivered a strong performance in 2022 during which she and her finance team supported achievement of the Company’s strong financial performance, provided critical support to prepare for the anticipated closing of the transactions contemplated by the Merger Agreement, continued to actively manage and implement expense reductions, supported the successful negotiation of retransmission agreements and network affiliation agreements, managed the Company’s short term cash investments and provided ongoing oversight over the Company's 401K and pension plans. Her annual bonus for

2022 reflected the Committee’s assessment of her and the Company’s performance, including her achievement of the following KPIs:

| | | | | | | | |

| Financial KPIs | | •Achieved the Company’s full year record Adjusted EBITDA of $1.1 billion,* which fell short of her EBITDA KPI, partially driven by weaker political and macroeconomic forces impacting subscribers and advertising revenue. • Supported achievement of record Company revenue of $3.3 billion, which was below budget, due in part to AMS revenue declines as a result of political displacement and macroeconomic headwinds. |

| | |

| Non-financial KPIs: Strategic and Business Goals | | •Supported the negotiation of the Merger Agreement. •Pivoted from annual budget process to a more refined quarter-ahead forecast process driven by macro-economic volatility. •Successfully completed the relocation of the entire Finance shared service organization, driving space and cost savings and allowing the Company to right-size the shared services functions. •Provided critical financial reporting, analysis and transaction processing operations in a manner that allowed the Company to recognize substantial savings in external audit fees. |

| | |

| Non-financial KPIs: People Goals | | • In collaboration with Mr. Lougee and the Company’s chief human resources officer, continued to develop and execute against a succession and development plan for her successor. |

*Reconciliation of the following non-GAAP financial measure to the Company’s results as reported under accounting principles generally accepted in the United States may be found in the Company’s Form 10-K, filed: adjusted EBITDA – page 32.

Lynn Beall, Executive Vice President and Chief Operating Officer – Media Operations

2022 Goals:

The Committee evaluated Ms. Beall’s 2022 performance using financial and non-financial KPIs it developed in consultation with Mr. Lougee. Ms. Beall’s financial KPIs included, among other things, goals relating to subscription and advertising and marketing services revenue.

Ms. Beall’s non-financial goals included, without limitation, audience growth, content transformation, content leadership development, and retransmission and network affiliation agreement negotiations and people goals relating to talent and culture, racial and gender diversity and succession planning.

2022 Performance Highlights and Key Accomplishments:

In 2022, while overseeing one of the most geographically diverse broadcast groups in the United States, Ms. Beall led the Company’s media operations through another historic news cycle that included unprecedented news events, extreme weather and political activity. Despite these and other challenges, the Company’s media operation realized strong results across the board under her leadership, driven by a strategic plan that focused on people, content and sales. Ms. Beall’s annual bonus for 2022 reflected the Committee’s assessment of her and the Company’s performance, including her achievement of the following KPIs:

| | | | | | | | |

| Financial KPIs | | •Drove the Company’s record Media Operations revenue, subscription revenue, net income and EBITDA, but fell below expectations and internal budget mostly due to economic headwinds beginning in the second quarter of 2022 and continuing through the end of the year. |

| | |

| Non-financial KPIs: Strategic and Business Goals | | •Successfully led the Company’s negotiations of comprehensive retransmission consent agreements representing approximately 38% of the Company’s subscribers. •Led successful renegotiation of a multi-year CBS affiliation agreement. •Oversaw growth of the Company’s original programming and multicast businesses, including signing several foundational distribution deals for the Company's multicast programming networks and improving the year-over-year performance of the Company's Daily Blast Live program. •Achieved strong audience gains for the Company’s VERIFY brand, and launched new digital streaming applications for the Company's stations on the Roku and Fire TV platforms. •Oversaw the Company’s news operations which continued to be awarded and celebrated for quality journalism, receiving six national Edward R. Murrow awards, two Dupont awards, and a prestigious local news Peabody award. |

| | |

| Non-financial KPIs: People Goals | | •Launched the Company’s manager training program, providing leadership training to almost 100 of the Company’s managers in 2022. • Through her succession planning and development efforts, oversaw the hiring of four new station general managers, three of whom were diverse. •Supported newsroom diversity initiatives through continued investment in the Company's inclusive journalism program for all new journalists, and the selection of 25 high-performing managers for participation in a Poynter Institute’s leadership program focused on DE&I. •Remained on track to achieve the 2025 diversity, equity and inclusion goals relating to the Company’s content leadership and content teams, including hiring three diverse station general managers. |

Akin S. Harrison, Senior Vice President and General Counsel

2022 Goals:

The Committee evaluated Mr. Harrison’s 2022 performance using financial and non-financial KPIs it developed in consultation with Mr. Lougee. Mr. Harrison’s financial KPIs included managing the law department’s budget and total Company outside legal fees.

Mr. Harrison’s non-financial goals included providing legal counsel and leadership in support of the Company’s purpose, strategic transactions, negotiations and compliance efforts, ethics standards and initiatives, and people goals relating to diversity and inclusion and leadership development.

2022 Performance Highlights and Key Accomplishments:

In 2022, Mr. Harrison continued to effectively manage the law department and he and his team successfully managed a wide variety of legal matters for the Company, including matters pertaining to the Merger Agreement, FCC compliance, commercial contracts, litigation, and antitrust and First Amendment matters. Mr. Harrison’s annual bonus for 2022

reflected the Committee’s assessment of his and the Company’s performance, including his achievement of the following KPIs:

| | | | | | | | |

| Financial KPIs | | •Continued to successfully manage the legal department’s budget and total Company outside legal fees. |

| | |

Non-financial KPIs:

Strategic and Business Goals | | • Provided legal counsel and coordinated with outside counsel and the Company’s advisor team in connection with the Company's efforts to obtain approval of the Merger Agreement. •Supported the Company’s negotiations of comprehensive retransmission consent agreements representing approximately 38% of the Company’s subscribers. •Advised on the long-term renewal of the Company’s network affiliation agreements with two of its major network partners. •Oversaw the Company’s legal compliance program. |

| | |

| Non-financial KPIs: People Goals | | • Continued to take steps to develop the members of the legal department. •Continued to support company-wide diversity and inclusion initiatives. |

In determining the annual bonus payouts for each NEO, the Committee considered the strong individual and Company performance referenced above. Based on its comprehensive review of these considerations, and consistent with the terms of the Merger Agreement, the Committee determined to pay each NEO’s 2022 annual bonus at target, as follows:

| | | | | | | | |

| EXECUTIVE | | BONUS |

| Mr. Lougee | | $ | 1,267,500 | |

| Ms. Harker | | $ | 730,000 | |

| Ms. Beall | | $ | 650,000 | |

| Mr. Harrison | | $ | 425,000 | |

LONG-TERM INCENTIVES

The Company’s long-term incentive program (the “LTI Program”) consists of awards of Performance Shares and Restricted Stock Units. The Performance Shares are based on the Company’s adjusted EBITDA and Free Cash Flow metrics, which the Committee views as critical to measuring our success in creating value for shareholders.

The Committee uses a two-year performance cycle for the Performance Shares in order to address the significant cyclical revenue increase the Company experiences in even-numbered years due to political spending during mid-term and presidential election years as a result of the Company’s strong political footprint.

| | | | | | | | | | | | | | | | | |

| Cycle | 2020 | 2021 | 2022 | 2023 | 2024 |

| 2020-2021 | Political | Off Year | Political | | |

| 2021-2022 | | Off Year | Political | Off Year | |

| 2022-2023 | | | Political | Off Year | Political |

Under the Performance Share program, grants are made, and a new two-year performance cycle begins, each year. At the end of each two-year performance cycle, the number of shares of Company common stock earned will be determined based upon the Company’s level of achievement versus the aggregate financial performance target or targets set by the Committee for that cycle. Any earned shares of Company common stock will not be distributed to executives until after the completion of the three-year service period. If the Company fails to meet threshold performance against a financial performance metric at the end of any performance cycle, no Performance Shares will be earned and no payout of shares of Company common stock will be made with respect to that financial performance metric.

Determination of Long-term Equity Award Target Value

For the March 1, 2022 grants, the Committee determined total long-term equity award target values for each NEO taking into account the following factors:

•market data;

•recommendation of Mr. Lougee and the Senior Vice President and Chief Human Resources Officer (other than for Mr. Lougee);

•the nature and responsibility of the NEO’s position;

•internal pay equity among positions;

•Comparative Market Data;

•individual performance against KPIs;

•the financial performance of the Company and the operations for which the NEO is responsible; and

•the Company’s progress towards the goals of its strategic plan.

Based on the foregoing factors, the Committee approved 2022 total long-term equity award target values for each of our NEOs, which are shown in the table below. | | | | | | | | | | | | | | | | | | | | |

| EXECUTIVE | | 2022 BASE SALARY | | LONG TERM- AWARD TARGET PERCENTAGE | | TOTAL LONG- TERM AWARD TARGET VALUE |

| Mr. Lougee | | $ | 975,000 | | | 500 | % | | $ | 4,875,000 | |

| Ms. Harker | | $ | 730,000 | | | 250 | % | | $ | 1,825,000 | |

| Ms. Beall | | $ | 650,000 | | | 200 | % | | $ | 1,300,000 | |

| Mr. Harrison | | $ | 500,000 | | | 200 | % | | $ | 1,000,000 | |

On March 1, 2022, the long-term equity award target value for each NEO was translated into a target award of Performance Shares and an award of RSUs based upon the Company’s closing stock price on February 28, 2022 (taking into account that dividends would not be paid on the Performance Shares or RSUs during the respective vesting periods), as follows:

| | | | | | | | | | | | | | |

| EXECUTIVE | | PERFORMANCE SHARES (TARGET #) | | RSUs |

| Mr. Lougee | | 156,465 | | | 66,508 | |

| Ms. Harker | | 46,022 | | | 37,347 | |

| Ms. Beall | | 32,783 | | | 26,603 | |

| Mr. Harrison | | 25,218 | | | 20,464 | |

2022 Performance Share Awards

The 2022 Performance Share grants are subject to achievement against the following Committee-approved performance metrics measured over the applicable performance cycle:

| | | | | | | | | | | | | | |

| Performance Metric | | Weighting(1) | | Description |

| Adjusted EBITDA | | 2/3 | | Compares, in percentage form, (1) the sum of the actual Adjusted EBITDA generated by the Company in each of the two applicable fiscal years, to (2) the sum of the target budgeted amounts of Adjusted EBITDA set by the Committee in connection with its annual budget review process for such fiscal years. |

| | | | |

Free Cash Flow as a Percentage of Revenue | | 1/3 | | Compares, in percentage form, (1) the aggregate amount of Free Cash Flow generated by the Company in the two applicable fiscal years measured as a percentage of the aggregate total Company revenues generated by the Company in such fiscal years, to (2) the weighted average of the targeted level of Free Cash Flow as a percentage of total Company revenues set by the Committee in connection with its annual budget review process for such fiscal years. |

(1)The Performance Shares place a higher weighting on Adjusted EBITDA given the importance of meeting our profitability expectations.

For purposes of the 2022 Performance Share grants: