UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

FORM 10-K

(Mark One)

x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2016

¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission file number 1-6961

TEGNA INC.

(Exact name of registrant as specified in its charter)

Delaware | 16-0442930 | |

(State or Other Jurisdiction of Incorporation or Organization) | (I.R.S. Employer Identification No.) | |

7950 Jones Branch Drive, McLean, Virginia | 22107-0150 | |

(Address of principal executive offices) | (Zip Code) | |

Registrant’s telephone number, including area code: (703) 873-6600

Securities registered pursuant to Section 12(b) of the Act:

Title of Each Class | Name of Each Exchange on Which Registered | |

Common Stock, par value $1.00 per share | The New York Stock Exchange | |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes x No ¨

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K (Check box if no delinquent filers). x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act:

Large accelerated filer | x | Accelerated filer | ¨ | Non-accelerated filer | ¨ | Smaller reporting company | ¨ |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ¨ No x

The aggregate market value of the voting common equity held by non-affiliates of the registrant based on the closing sales price of the registrant’s Common Stock as reported on The New York Stock Exchange on June 30, 2016, was $4,949,634,035. The registrant has no non-voting common equity.

As of January 31, 2017, 214,716,069 shares of the registrant’s Common Stock were outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

The definitive proxy statement relating to the registrant’s Annual Meeting of Shareholders to be held on May 4, 2017, is incorporated by reference in Part III to the extent described therein.

INDEX TO TEGNA INC.

2016 FORM 10-K

Item No. | Page | |

1. | ||

1A. | ||

1B. | ||

2. | ||

3. | ||

4. | ||

5. | ||

6. | ||

7. | ||

7A. | ||

8. | ||

9. | ||

9A. | ||

10. | ||

11. | ||

12. | ||

13. | ||

14. | ||

15. | ||

16. | ||

2

PART I

ITEM 1.BUSINESS

Overview

Our company is comprised of a dynamic portfolio of media and digital businesses that provide content that matters and brands that deliver. We deliver highly relevant, useful and smart content, when and how people need it, to make the best decisions possible. Our agile and forward-thinking portfolio is comprised of one of the largest, most geographically diverse television broadcasters in the U.S. and two leading digital companies, Cars.com and CareerBuilder. Combined, TEGNA’s brands have tremendous reach.

Our high margin operations generate strong and dependable cash flows and we are very financially disciplined. In addition, our strong balance sheet provides us the flexibility to invest in our businesses and to capitalize on opportunities for organic and acquisition-related growth while returning value to shareholders through dividends and share repurchases.

On September 7, 2016, we announced two strategic actions related to our Digital Segment. These strategic decisions, which are part of our ongoing transformation, are intended to enable us to continue to deliver value to shareholders and position us for future success. First, we announced our intention to spin-off our Cars.com business unit into a separate stand-alone public company. The spin-off will create two independent, publicly traded companies: TEGNA, the largest independent broadcast station group of major network affiliates in the top 25 markets, and Cars.com, a top online destination in the digital automotive marketplace. We expect to complete the spin-off in the first half of 2017. When we announced our intention to spin-off of Cars.com, we also declared our plans to conduct a strategic review of our 53% ownership interest in CareerBuilder, including a possible sale of it in conjunction with the other owners’ interests. We expect to complete our strategic review during the first half of 2017.

The strategic actions are part of our ongoing transformation. We believe the spin-off of Cars.com will provide each company with greater flexibility to invest in organic growth and pursue value enhancing investments and acquisitions. Both companies possess strong balance sheets and generate strong cash flow. When the spin is completed, each company will have tailored capital structures and shareholder return policies aligned with their distinctive businesses.

We believe that CareerBuilder’s breadth, scale, brand recognition, and continued successful transition as well as focus on fast-growing, higher-margin software as a service (SaaS) businesses offers a compelling value proposition. If CareerBuilder is divested, and upon completion of the anticipated spin-off of Cars.com, both TEGNA and Cars.com would become separate standalone businesses, one operating exclusively in broadcasting and the other in the digital automotive space. Should there be a sale of CareerBuilder, any transaction proceeds would provide TEGNA with even further financial flexibility.

We will maintain the current operating and reporting structure for both businesses and will continue to report their financial results in our continuing operations until the anticipated spin-off transaction is complete and during our strategic review of CareerBuilder. As such, we continue to operate the following two reportable segments:

TEGNA Media (Media Segment) - includes 46 television stations (including one station under service agreements) in 38 markets. We are the largest independent station group of major network affiliates in the top 25 markets, covering approximately one-third of all television households nationwide (more than 36 million households per Nielsen). We represent the #1 NBC affiliate group, #2 CBS affiliate group and #5 ABC affiliate group (excluding owner-operators). Each television station also has a robust digital presence across online, mobile and social, reaching consumers whenever, wherever they are across platforms. Throughout 2016, approximately 63 million visitors accessed our Media Segment’s digital properties each month (according to Adobe). Social media is now at the core of all we do and we have over 18 million social subscribers to our station accounts. Our stations keep viewers informed and engaged throughout the day. Along with the advantages associated with our scale, we are ratings leaders well-positioned to continue to take market share. We believe that content comes first, resulting in award-wining local programming and a unique bond with the communities we serve. We continue to make top-notch, innovative programming a priority and invest in local news and other special programming to ensure we stay connected to our audiences and empower them throughout the day.

TEGNA Digital (Digital Segment) - which primarily consists of the Cars.com, CareerBuilder, and G/O Digital businesses. Cars.com is a leading online destination for automotive consumers offering credible, objective information about car shopping, selling and servicing. Cars.com averaged approximately 35 million visits each month during 2016, approximately 52% of which are mobile, and according to comScore, an average of approximately 11.8 million unique monthly visitors over the same time period. Leveraging its market-leading position and large audience, Cars.com also informs digital marketing strategies through consumer insights and innovative products, helping automotive dealers and manufacturers to reach in-market car shoppers more effectively.

In addition, we own a controlling 53% interest in CareerBuilder, a global, end-to-end human capital solutions company focused on helping employers find, hire and manage great talent. Combining advertising, software and services, CareerBuilder is an industry leader in recruiting solutions, employment screening and human capital management. CareerBuilder operates one of the largest job sites in North America, measured both by traffic and revenue, and has a presence in more than 60 markets worldwide. Together, Cars.com and CareerBuilder provide our advertising partners with access to two very important categories - automotive and human capital solutions.

Our Digital Segment also includes G/O Digital, a one-stop shop for digital marketing services for local businesses. As consumers conduct more of their daily lives and day-to-day business online, our digital assets position us well, providing a vast footprint available for our advertisers.

3

In addition to the above reportable segments, our corporate category includes activities that are not directly attributable or allocable to a specific reportable segment. This category primarily consists of broad corporate management functions including legal, human resources, and finance, as well as activities and costs not directly attributable to a particular segment.

General Company Information

TEGNA was founded by Frank E. Gannett and associates in 1906 and was incorporated in 1923. We listed shares publicly for the first time in 1967 and reincorporated in Delaware in 1972. Our approximately 215 million outstanding shares of common stock are held by approximately 6,600 shareholders of record as of December 31, 2016. Our headquarters is located at 7950 Jones Branch Drive, McLean, VA, 22107. Our telephone number is (703) 873-6600 and our website home page is www.tegna.com. We make our website content available for information purposes only. It should not be relied upon for investment purposes, nor is it incorporated by reference into this Annual Report on Form 10-K (Form 10-K).

Our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, proxy statements for our annual stockholders’ meetings and amendments to those reports are available free of charge on our investor website, www.investors.tegna.com as soon as reasonably practical after we electronically file the material with, or furnish it to, the Securities and Exchange Commission (SEC). In addition, copies of our annual reports will be made available, free of charge, upon written request. The SEC also maintains a website at www.sec.gov that contains reports, proxy statements and other information regarding SEC registrants, including TEGNA Inc.

Business Segments

We operate two business segments: Media and Digital. We organize our business segments based on management and internal reporting structure, the nature of products and services offered by the businesses within the segments, and the financial information that is evaluated regularly by our chief operating decision maker. Financial information for each of our reportable segments can be found under Item 7 “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and Item 8 “Financial Statements and Supplementary Data” of this Form 10-K.

Media Segment

In 2016, our Media Segment generated net revenues of $1.93 billion, which represented 58% of our total consolidated net revenues. We have a presence in almost one-third of U.S. television households with a total market coverage throughout 2016 of more than 36 million households according to Nielsen reports. Our station portfolio includes 46 full-power stations including one station we service through services arrangements. We are diversified by region and network affiliation and are a leading company in the industry. Other than the three major networks (ABC, CBS, and NBC) themselves, we are the largest owner of stations affiliated with each of these three major networks in the top 25 markets.

The primary sources of our Media Segment’s revenues are: 1) core advertising which includes local and national non-political advertising; 2) political advertising revenues which are driven by elections and peak in even years (e.g. 2016, 2014) and particularly in the second half of those years; 3) retransmission revenues representing fees paid by satellite and cable operators and telecommunications companies to carry our television signals on their systems; 4) digital revenues which encompass digital marketing services and advertising on the stations’ websites, tablet and mobile products; and 5) other services, such as production of programming from third parties and production of advertising material.

The advertising revenues generated by a station’s local news programs make up a significant part of its total advertising revenues. Advertising rates are influenced by the demand for advertising time. This demand is influenced by a variety of factors, including the size and demographics of the local populations, the concentration of businesses, local economic conditions in general, and the popularity of the station’s programming. As the market fluctuates with supply and demand, so does the station’s pricing. Almost all national advertising is placed through independent advertising representatives. Local advertising time is sold by each station’s own sales force.

Generally, a network provides programs to its affiliated television stations and the network sells commercial advertising for certain of the available advertising spots within the network programs, while our television stations sell the remaining available commercial advertising spots. Our television stations also produce local programming such as news, sports, and entertainment.

Broadcast affiliates and their network partners continue to have the broadest appeal in terms of household viewership, viewing time and audience reach. The overall reach of events such as the Olympics and NFL Football, along with our extensive local news and non-news programming, continues to surpass the reach in viewership of individual cable channels. Our ratings and reach are driven by the quality of programs we and our network partners produce and by the strong local connections we have to our communities, which gives us a unique position among the numerous program choices viewers have, regardless of platform.

Media’s entire portfolio of NBC, CBS, ABC and FOX stations are under long-term affiliation agreements. Additionally, there are several initiatives underway that we expect to contribute additional revenue and cash flow growth in the coming years to offset the impact of increasing programming fees.

Strategy: Our Media Segment’s quality and scale drives its success. Our television stations empower the people we serve, delivering highly relevant, useful and smart content. From our successful renewals of retransmission agreements and the creation of original, innovative programming to expanded coverage and increased focus on our communities, we had a very strong year in 2016. We initiated significant efforts to transform our content and connect with audiences in new, powerful ways. With increased alignment between our digital and linear television properties as well as increased focus on station-to-station content sharing, we delivered more cross-platform reporting than ever before.

4

Our continued focus and investment in innovation for 2017 and beyond is key to our financial results and growth in the future. Innovations like Hatch, our centralized marketing solutions group, combined with our new Pricing and Business Intelligence team, a comprehensive content innovation plan, and Premion, our newly launched over-the-top (OTT) advertising service, are all positively impacting our business and advancing the way we meet our consumers and our customers’ needs. Key elements of our Media Segment’s strategy are as follows:

Continue to invest in quality content. Our scale has allowed us to invest in comprehensive content and digital innovation initiatives. Our focus on data-driven editorial processes, new storytelling formats, unique visual presentations and more are all helping to deliver content audiences demand. During 2016, we saw audience gains from new talent-driven shows focused on authentic personalities and informal presentations. We saw significant gains in market share from new production styles on digital and social media platforms. We also saw ratings gains from new data-driven processes that brought our storytellers and consumers closer than ever before.

Increase engagement across all platforms. Our Media Segment continues to focus on increasing engagement on all platforms with local customers, including digital marketing services and advertising on the stations’ desktop, tablet and mobile products. In this regard, 2016 was a pivotal year in our Media Segment’s digital development. Several significant product, technology, monetization and staffing building blocks were put in place to position us to capitalize on key trends in the fast-moving and evolving digital landscape.

• | The first trend was a move to embrace a SaaS approach to digital product development. Rather than building all technologies in-house and incurring significant staffing and capital expenses, we began to leverage best-in-class SaaS providers to rapidly enable and iterate on new features and functionalities while augmenting critical components with a small internal team to create unique opportunities and differentiated experiences. This allowed our Media Segment to optimize user experience and create personalized content. |

• | The second key trend is our continued development of products based on the movement of audiences to mobile and off-platform channels such as social and Internet-enabled television services commonly referred to as “over the top” or “OTT”. We have made significant strides engaging consumers based on these new digital content consumption patterns measured by number of Facebook video plays and social interactions according to CrowdTangle and Omniture. |

• | The third trend is around monetization as our Media Segment has effectively optimized its programmatic advertising scale and efficiencies. We believe these key initiatives in 2016 along with the hiring of digital executive leadership have our Media Segment well positioned for an exciting 2017. |

Enhance our digital product offerings to further increase traffic. Our television stations continue to experience strong demand for digital product offerings and product improvements continue to be favorably received by consumers. In 2016, total video plays increased 9% from 2015 on our own platforms while off platform (primarily Facebook and YouTube) surpassed 2 billion video plays (according to Facebook Insights and YouTube Analytics). Usage of our mobile and tablet apps, as well as mobile web, continues to be strong. Product enhancements to both the desktop and mobile digital products occur every year and are part of a continuous cycle of improving the customer experience and increasing consumer engagement.

Capitalize on growth in social media. Our Media Segment is positioned to maximize engagement through social media. There is a strong synergistic relationship between social media and television and we continue to explore ways to socially engage consumers on all screens for all types of programs, from major sporting events such as the Super Bowl, March Madness, and the Olympics to signature television events such as the Grammys and Academy Awards. Our social media reach grew over 40% in 2016 and now totals over 18 million followers on Twitter, Facebook and Instagram (according to CrowdTangle).

Retransmission consent agreements: Pursuant to Federal Communications Commission (FCC) rules, every three years a local television station must elect to either (1) require cable and/or direct broadcast satellite operators to carry the station’s signal or (2) require such cable and satellite operators to negotiate retransmission consent agreements to secure carriage. At present, we have retransmission consent agreements with the majority of cable operators and satellite providers for carriage of our television stations. We also have retransmission agreements with major telecommunications companies. Revenue from television retransmission fees has increased steadily in the last several years, better reflecting the value of the content that our Media Segment provides. While television spot advertising still represents a majority of Media Segment revenues (approximately 62% in 2016), the contribution from retransmission revenues continues to grow. In 2016, our Media Segment renegotiated several new retransmission agreements with major carriers. We believe our content and scale will allow us to grow market share and secure further retransmission fee revenue growth in 2017 and beyond, as we work over the coming years to close the economic gap between the value we provide and the fees that we are currently receiving from many carriers.

Programming and production: The costs of locally produced and purchased syndicated programming is a significant portion of television operating expenses. Syndicated programming costs are determined based on several market factors, including demand from the independent and affiliated stations within the market. In recent years, our television stations have expanded our locally produced news and entertainment programming in an effort to provide programs that distinguish the stations from the competition and to be more cost effective. Due to our scale, we provide stations additional resources from other markets to cover major breaking news stories which gives us a competitive advantage.

5

Competition: Our Media Segment competes for audience share and advertising revenues primarily with other local television broadcasters (including network-affiliated and independent) and with other advertising media, such as radio broadcasters, multichannel video programming distributors (MVPDs), newspapers, magazines, direct mail and Internet media. Other sources of competition for our media stations include home video and audio recorders and players, direct broadcast satellite, low power television, internet radio, video offerings (both wire line and wireless) of telephone companies as well as developing video services. Within their respective Designated Market Area (DMA), our stations compete for audience share and audience composition which is largely driven by program popularity. Our share of the DMA has a direct effect on the rates we are able to charge advertisers. MVPDs can also increase competition by bringing additional cable network channels and content into the DMA.

The advertising industry is dynamic and rapidly evolving. Our stations compete in the emerging local electronic media space, which includes the Internet or Internet-enabled devices, handheld wireless devices such as mobile phones and tablets, social media platforms, digital spectrum opportunities and OTT. The technology that enables consumers to receive news and information continues to evolve.

Regulation: Our television stations are operated under the authority of the Federal Communications Commission (FCC or Commission), the Communications Act of 1934, as amended (Communications Act), and the rules and policies of the FCC (FCC regulations). As a result, our television stations are subject to a variety of obligations, such as restrictions on the broadcast of material deemed “indecent” or “profane,” requirements to provide or pass through closed captioning for most programming, rules requiring the public disclosure of certain information about our stations’ operations, and the obligation to offer programming responsive to the needs and interests of our stations’ communities. The FCC may alter or add to these requirements, and any such changes may affect the performance of our business. Certain significant elements of the FCC’s current regulatory framework for broadcast television are described in further detail below.

Television broadcast licenses generally are granted for periods of eight years. They are renewable upon application to the FCC and usually are renewed except in rare cases in which a petition to deny, a complaint or an adverse finding as to the licensee’s qualifications results in loss of the license. We believe we are in substantial compliance with the applicable provisions of the Communications Act and FCC regulations.

FCC regulations limit the concentration of broadcasting control and regulate network and local programming practices. FCC regulations governing media ownership limit, or in some cases prohibit, the common ownership or control of most communications media serving common market areas (for example, television and radio; television and daily newspapers; or radio and daily newspapers). FCC regulations permit common ownership of two television stations in the same market in certain defined circumstances, including situations where at least one of the commonly owned stations is not among the top four rated stations in the market at the time of acquisition and at least eight independently owned television stations would remain after the acquisition. The Communications Act includes a national ownership cap for broadcast television stations that prohibits any one person or entity from having, in the aggregate,

market reach of more than 39% of all U.S. television households. Until recently, FCC regulations permitted stations to discount the market reach of stations that broadcast on UHF channels by 50% (the UHF discount). In September 2016, however, the FCC adopted an order repealing the UHF discount, which has been challenged at the FCC and in court. Our 45 television stations (excluding the station we currently service under a services arrangement) reach approximately 27% of U.S. television households when the UHF discount is applied and approximately 32% without the UHF discount.

The FCC is required under the Communications Act to review its media ownership rules every four years. In an August 2016 order concluding its most recent quadrennial review, the FCC decided to retain in large part its existing limits on television ownership and cross-ownership. In addition, the order readopted rules - previously struck down by the U.S. Court of Appeals for the Third Circuit - that make certain television joint sales agreements (JSAs) attributable in calculating compliance with the local television ownership limits. The order included a grandfathering provision, so that any such JSAs in effect as of March 31, 2014, may remain in place and be assigned or transferred through September 30, 2025. The FCC also will require the disclosure of shared services agreements (SSAs) in stations’ online public inspection files, though these agreements generally are not deemed to be attributable ownership interests. We are party to a transition services agreement (which is similar to, but more limited than, the typical shared services agreement) and a JSA with a third party that owns a television station in Tucson, where we also own a television station. Our JSA is subject to the FCC’s grandfathering provision and, if attributed, would have an insignificant impact on our overall attributable ownership interest. We are not party to any other JSAs or SSAs. The FCC’s recent quadrennial review order is being challenged at the FCC and in court. If upheld, the order could restrict our ability to enter into future transactions and may require us to disclose more information about our station operations.

In 2015, the FCC adopted new rules required by the STELA Reauthorization Act of 2014 that prohibit same-market television broadcast stations from coordinating or jointly negotiating for retransmission consent unless they are under common control. Congress also directed the FCC to commence a rulemaking to “review its totality of the circumstances test for good faith [retransmission consent] negotiations.” The Commission conducted the required proceeding but did not adopt any additional rules concerning these negotiations. Separately, in March 2014, the FCC put forward a proposal to eliminate the Commission’s network non-duplication and syndicated exclusivity rules, which provide television stations with the right to enforce exclusivity rights that prohibit cable operators and direct broadcast satellite systems from importing out-of-market television stations with duplicating programming during a retransmission consent dispute or otherwise. To date, the FCC has taken no action on this proposal. If such changes were adopted, they could give cable and satellite operators leverage against broadcasters in retransmission consent negotiations and, as a result, adversely impact our revenue from retransmission and advertising.

6

Congress authorized the FCC to conduct a voluntary incentive auction to reallocate certain spectrum currently occupied by television broadcast stations to mobile wireless broadband services, along with a related “repacking” of the television spectrum for remaining television stations. The repacking will require that certain television stations move to different channels, and some stations may have smaller service areas and/or experience additional interference. Congress has required that the FCC make “all reasonable efforts” to preserve the coverage area and population served of full-power and Class A television stations. The legislation authorizing the incentive auction and repacking establishes a $1.75 billion fund for reimbursement of costs incurred by stations required to change channels in the repacking. Between January 12, 2016, and February 6, 2017, a “quiet period” under the FCC’s auction rules prohibited broadcast television licensees eligible to participate in the reverse-auction phase of the incentive auction from directly or indirectly communicating with each other or with forward-auction applicants regarding licensees’ bids or bidding strategies in the incentive auction. On January 18, 2017, the FCC announced that the necessary conditions had been met for the auction to close once the current round of bidding for wireless licenses is complete, and on February 6, 2017, the FCC waived the quiet-period rules as they applied to discussions of broadcast television licensees’ reverse-auction bids and bidding strategies. None of our stations will relinquish any spectrum rights as a result of the auction, and accordingly we will not receive any incentive auction proceeds. The FCC has notified us that 13 of our stations will be repacked to new channels; we will be eligible to seek reimbursement for costs associated with implementing these changes. In addition, a station that is not required to move channels may be eligible to apply for an alternate post-auction channel or expanded facilities in the event the station is predicted to experience increased interference resulting in a greater than one percent loss in population served, although costs associated with such changes would not be eligible for reimbursement. We also own various low-power television stations, which are not entitled to repacking protection and may be displaced. Any such displaced low-power stations either would need to cease operations or be relocated to a new channel (if one is available) at our expense. It is still too early to predict the ultimate impact of the incentive auction and repacking upon our business, as this impact will depend upon numerous factors, including the results of the incentive auction and repacking with respect to other television stations in our markets and adjacent markets. The FCC will publicly release the full auction results, including a complete list of all stations repacked to new channels, at a later date.

In December 2014, the FCC proposed to expand the definition of “MVPD” to include certain “over-the-top” distributors of video programming that stream content to consumers over the Internet. If the FCC adopts this proposal, it could result in changes to how our stations’ signals are distributed, as well as how our video programming competitors reach viewers. We are unable to predict at this time whether the FCC will adopt this proposal or what the effect on our retransmission and advertising revenues would be, if any.

Digital Segment

Our Digital Segment is comprised of three business units: Cars.com, CareerBuilder, and G/O Digital. In December 2016 we sold our Cofactor business unit. In 2016, our Digital Segment generated net revenues of $1.41 billion, which represented 42% of our total consolidated net revenues.

Cars.com offers credible and easy-to-understand information from consumers and experts that help car buyers to price and find new and used vehicles and car owners to find qualified service and repair providers. Additionally, Cars.com operates Auto.com, DealerRater.com, NewCars.com and PickupTrucks.com, specialized websites directed towards different consumer segments. Leveraging its market-leading position and growing audience, Cars.com also informs digital marketing strategies through consumer insights and innovative products, helping automotive dealers and manufacturers to reach in-market car shoppers more effectively.

Cars.com generates revenues through the sale of online subscription advertising products targeting car dealerships through its own direct sales force as well as its affiliate sales channels. Cars.com hosts approximately 4.7 million vehicle listings at any given time and serves approximately 20,000 franchise and independent car dealers throughout all 50 states. Cars.com also generates revenue through the sale of display advertising to national advertisers. In January 2015, Cars.com expanded into the area of service, introducing RepairPal Certified, a solution that provides information about reputable certified repair shops and allows consumers to get estimates on potential vehicle repairs. In August 2016, TEGNA acquired DealerRater, the industry’s largest automotive consumer review website, which is consolidated into our Digital Segments results. With nearly 2.8 million consumer reviews of local dealers, DealerRater harnesses the power of social media to help consumers decide which person to ask for advice when they call or arrive at a dealership.

CareerBuilder offers a wide array of solutions that help employers around the world match the right candidate to the right opportunity at the right cost. CareerBuilder has been executing a strategic shift from an advertising-driven business to a business focused on SaaS for human capital. During this transformation, CareerBuilder has built an integrated software platform to handle all aspects of the candidate lifecycle and employee lifecycle, leveraging its existing job advertising and other assets to extend capabilities into a full service software platform.

CareerBuilder has built a pre-hire software platform, providing everything from high-powered candidate sourcing and mass job distribution to talent and labor market analysis, candidate tracking and automatic candidate relationship management - all in one place. Through its technology, constant innovation and customer care delivered at every touch point, CareerBuilder is helping employers hire the best talent, faster.

Revenues are generated by providing recruitment solutions, employment screening and human capital management solutions, and through sales of employment advertising placed with CareerBuilder’s owners’ affiliated media organizations.

7

CareerBuilder made two strategic acquisitions during 2016. First, on March 1, 2016, it acquired Aurico, a provider of background screening and drug testing, which expanded the pre-hire employer service offerings. Second, on September 2, 2016, it acquired a 75% interest in Workterra, a cloud-based human capital management platform that provides onboarding, benefits administration, wellness and compliance solutions to employers, a move that expanded CareerBuilder’s suite of software solutions into the post-hire sector.

CareerBuilder serves both U.S. and international customers. Through its websites and partnerships, CareerBuilder has a presence in more than 60 countries worldwide, including Europe, Canada, Asia, and Australia. In 2016, U.S. customers accounted for 89% and international customers accounted for 11% of CareerBuilder’s net revenue.

In addition, our Digital Segment includes our G/O Digital business which is a one-stop-shop for local businesses looking to connect with media consumers through digital marketing, including via search, social and email advertising.

Strategy: The Digital Segment is driving significant growth as our businesses meet evolving consumer demand.

Cars.com’s strategy is to offer an innovative mix of complementary products and services that create seamless and confident car buying experiences for consumers and efficient marketing solutions for advertisers. Key elements of Cars.com’s strategy to achieve these objectives are as follows:

Leverage competitive strengths to provide targeted, integrated solutions to advertisers. Cars.com intends to leverage its many competitive advantages including its innovative digital advertising services products and brand recognition as a trusted, unbiased third-party research platform to create tailored media and marketing plans that efficiently target in-market consumers, drive dealership car buyer traffic and reinforce advertisers’ message and digital presence. Cars.com is a highly attractive advertising and marketing resource due to its offering of thoughtfully-crafted digital strategies that meet the unique needs of automobile industry marketers and advertisers.

Expand into new markets and continue to offer new complementary products and services. Cars.com believes that there are significant opportunities to expand into adjacent markets in the automotive industry and potentially enter into new industry verticals. As indicated by Cars.com’s successful launches of Sell & Trade and Event Positions, its partnership with RepairPal Certified and the recent acquisition of DealerRater, Cars.com believes its expertise in dealer operations and the retail automotive industry, along with its ability to manage data and develop technological solutions, can be leveraged to provide solutions to the challenges that consumers, retailers, manufacturers and advertisers face in other aspects of the automotive and ancillary industries.

Increase mobile solutions to further drive car buyer traffic. Cars.com believes that on-the-go mobile device car buying research and comparison applications have been playing and will continue to play an increasingly important role in the digital automotive marketplace industry. Cars.com has seized on the opportunities presented by this trend. Visits to Cars.com from smartphones have continued to increase, and at the end of 2016, approximately 52% of total Cars.com shoppers visit the Cars.com sites from mobile devices (according to Adobe Analytics). Cars.com’s user-friendly mobile applications provide in-market car shoppers with real-time, credible research and price comparison tools while they are on the lot and actively engaged in the car buying process.

Supplement organic growth with selective acquisitions. Cars.com believes it will be well-positioned to pursue value-enhancing investments and acquisitions in the increasingly competitive digital automotive marketplace industry. Cars.com will be both opportunistic and disciplined in its acquisition strategy.

CareerBuilder had a very productive year, returning to revenue growth and accelerating sales across all its human capital solutions. CareerBuilder’s pre-hire platform has proven to be one of most innovative offerings on the market, enabling CareerBuilder to offer a mix of recruitment advertising and SaaS solutions, which has resulted in time and cost savings for customers.

CareerBuilder has continued its transformation into a global HR SaaS leader, combining its advertising products with software and services to create a single unified solution for recruiters and employers. The SaaS platform is in addition to CareerBuilder’s existing product line, and not a departure from the core business. CareerBuilder continues to grow its SaaS product offering, achieving SaaS revenues of $162 million in 2016, up 8% from 2015. CareerBuilder is also moving into post-hire solutions with its recent acquisition of Workterra which we anticipate will open up new revenue streams and serve our customers in an even more robust way.

Also, in November 2016, CareerBuilder announced it is collaborating with Google and plans to use the Google Cloud Jobs API to power job search on the site. CareerBuilder has begun leveraging Google’s extensive search and machine-learning capabilities to make job search results faster and more relevant.

Competition: Our Digital Segment faces significant competition from other websites offering integrated Internet products and services, networking websites and e-commerce websites. Several competitors offer online services and/or content in a manner similar to us that competes for the attention of the users of our offerings and advertisers. Specifically, Cars.com competes for a share of total digital advertising spend in the U.S. automotive market. The digital automotive industry is constantly evolving. Low barriers to entry allow new competitors to enter the market with new products, possibly putting pressure on Cars.com’s pricing structure.

In recent years, dealers have shifted an increasing portion of their advertising budgets to new entrants with niche advertising products. Dealers also continue to invest in search engine marketing to drive traffic directly to their own websites, bypassing third-party sites while still investing in traditional media such as television, radio and newspapers. Cars.com has maintained a leadership position through its award-winning site and through innovative new products for its advertisers, and it believes that as the competitive climate evolves, the need to innovate and to connect an advertiser’s investment to eventual sales at a local level will be of increasing importance.

8

For CareerBuilder, the market for online recruitment solutions is highly competitive with a multitude of online and offline competitors. Competitors include other employment related websites, general classified advertising websites, professional networking and social networking websites, traditional media companies, Internet portals, search engines and blogs. The barriers to entry into the online recruitment market are relatively low and new competitors continue to emerge. Recent trends include the rising popularity of professional and social media networking websites and job aggregation sites which have gained traction with employer advertisers. The number of niche job boards targeting specific industry verticals has also continued to increase. CareerBuilder’s ability to maintain its existing customer base while generating new customers depends, to a significant degree, on the quality of its services, pricing, product innovation and reputation among customers and potential customers.

For G/O Digital, the market for digital marketing services is highly competitive and fragmented. On a local level, we face increased competition from a wide range of companies offering similar tools and systems for managing and optimizing advertising campaigns.

Regulation and legislation (impacting Digital Segment businesses and digital operations associated with Media businesses): The U.S. Congress has passed legislation which regulates certain aspects of the Internet, including content, copyright infringement, taxation, access charges, liability for third-party activities and jurisdiction. Federal, state, local and foreign governmental organizations have enacted and also are considering other legislative and regulatory proposals that would regulate the Internet. Areas of potential regulation include, but are not limited to, user privacy, data security, and intellectual property ownership. With respect to user privacy, the legislative and regulatory proposals could regulate behavioral advertising, which specifically refers to the use of user behavioral data for the creation and delivery of more relevant, targeted Internet advertisements. With respect to our international operations, we are also closely monitoring developments regarding regulations relating to the transfer of personal data from Europe to the U.S. Some of our digital properties utilize certain aspects of user behavioral and personal data in their advertising solutions to customers.

Employees

At the end of 2016, TEGNA and its subsidiaries employed approximately 10,100 full-time and part-time people, including approximately 3,300 at CareerBuilder.

2016 | 2015 | ||||

Media | 4,908 | 5,020 | |||

Digital | 5,014 | 4,785 | |||

Corporate | 199 | 215 | |||

Total | 10,121 | 10,020 | |||

Approximately 6% of our employees in the U.S. are represented by labor unions. They are represented by 24 local bargaining units, most of which are affiliated with one of four international unions under collective bargaining agreements. These agreements conform generally with the pattern of labor agreements in the broadcasting industry. We do not engage in industry-wide or company-wide bargaining. All of our union employees are employed by our Media Segment.

Environmental and Sustainability Initiatives

We are committed to managing our environmental impact responsibly and protecting the environment through our media programs and our charitable endeavors.

Our television stations regularly cover environmental and sustainability issues that affect their communities. In 2016, we focused particular attention on water safety. KPNX in Phoenix reported on high uranium levels in the water of a rural, majority Native American community that had not been disclosed to residents. Authorities in Arizona subsequently announced enhanced notification measures in the event of future water quality violations. KBMT in Beaumont also addressed water quality concerns in their region, exposing unsafe contaminant levels in local water as well as the inadequacy of current testing programs. Our station in Spokane, KREM, investigated the testing for water contamination at schools in the Inland Northwest. That report identified a gap in the water testing program that could result in exposure of children to drinking water with elevated levels of lead and copper. In addition, KING in Seattle reported on several ecological issues impacting the Pacific Northwest. KING filmed Washington Department of Fish and Wildlife boat patrols aimed at preventing halibut poaching. In another story, KING covered the release of nine orphaned bears into the wild after lengthy care at a wildlife center. The station also aired reports on the rehabilitation of an endangered sea turtle, which included a hyperbaric treatment used for the first time on an animal as well as a Coast Guard flight from Seattle to San Diego.

We are focused on energy efficiency and reducing our carbon footprint. We sold our corporate headquarters facility in the fourth quarter of 2015, and will be relocating to leased office space of much reduced size in a new, energy-efficient (LEED NC Certified Gold) office building. In connection with this move, we initiated a digitization project to convert paper files to digital files, which will help us reduce our paper storage and usage and further shrink our real estate footprint. We have also installed more energy efficient systems and appliances at some of our facilities. For example, KARE and KREM initiated a LED lighting project and KSDK completed a boiler replacement project resulting in a reduction of electrical and heating costs. WUSA9-TV recently finished the installation of new state-of-the-art solar panels at its Washington, DC studio building, becoming the first local television station to create its own renewable source of electricity to reduce its carbon footprint. Other LED lighting projects are scheduled for 2017.

TEGNA employees and their families took part in nearly 50 Make A Difference Day projects in 2016. Make A Difference Day is one of the largest annual single-days of service nationwide. Since 1992, volunteers and communities have come together on Make A Difference Day with a single purpose: to improve the lives of others. Volunteer efforts often include environmentally beneficial projects such as planting trees or gardens, cleaning up trash and planting sod.

The TEGNA Foundation supports nonprofit activities in communities where we do business and contributes to a variety of charitable causes through its Community Grant Program. One of the TEGNA Foundation’s community action grant priorities is environmental conservation.

9

MARKETS WE SERVE

TELEVISION STATIONS AND AFFILIATED DIGITAL PLATFORMS

State/District of Columbia | City | Station/web site | Channel/Network | Affiliation Agreement Expires in | Market TV Households (5) | Founded | |

Arizona | Flagstaff | KNAZ-TV: 12news.com | Ch. 2/NBC | 2021 | (6 | ) | 1970 |

Phoenix | KPNX-TV: 12news.com | Ch. 12/NBC | 2021 | 1,890,100 | 1953 | ||

Tucson | KMSB-TV: tucsonnewsnow.com | Ch. 11/FOX | 2019 | 425,860 | 1967 | ||

KTTU-TV(1): tucsonnewsnow.com | Ch. 18/MNTV | 2018 | 425,860 | 1984 | |||

Arkansas | Little Rock | KTHV-TV: thv11.com | Ch. 11/CBS | 2019 | 547,950 | 1955 | |

California | Sacramento | KXTV-TV: abc10.com | Ch. 10/ABC | 2018 | 1,379,770 | 1955 | |

Colorado | Denver | KTVD-TV: my20denver.com | Ch. 20/MNTV | 2018 | 1,630,380 | 1988 | |

KUSA-TV: 9news.com | Ch. 9/NBC | 2021 | 1,630,380 | 1952 | |||

District of Columbia | Washington | WUSA-TV: wusa9.com | Ch. 9/CBS | 2019 | 2,476,680 | 1949 | |

Florida | Jacksonville | WJXX-TV: firstcoastnews.com | Ch. 25/ABC | 2018 | 688,500 | 1989 | |

WTLV-TV: firstcoastnews.com | Ch. 12/NBC | 2021 | 688,500 | 1957 | |||

Tampa-St. Petersburg | WTSP-TV: wtsp.com | Ch. 10/CBS | 2019 | 1,908,590 | 1965 | ||

Georgia | Atlanta | WATL-TV: myatltv.com | Ch. 36/MNTV | 2018 | 2,412,730 | 1954 | |

WXIA-TV: 11alive.com | Ch. 11/NBC | 2021 | 2,412,730 | 1948 | |||

Macon | WMAZ-TV: 13wmaz.com | Ch. 13/CBS | 2019 | 232,910 | 1953 | ||

Idaho | Boise | KTVB-TV(3): ktvb.com | Ch. 7/NBC | 2021 | 270,200 | 1953 | |

Kentucky | Louisville | WHAS-TV: whas11.com | Ch. 11/ABC | 2018 | 662,170 | 1950 | |

Louisiana | New Orleans | WWL-TV: wwltv.com | Ch. 4/CBS | 2019 | 641,620 | 1957 | |

WUPL-TV(4): wupltv.com | Ch. 54/MNTV | 2018 | 641,620 | 1955 | |||

Maine | Bangor | WLBZ-TV: wlbz2.com | Ch. 2/NBC | 2021 | 133,310 | 1954 | |

Portland | WCSH-TV: wcsh6.com | Ch. 6/NBC | 2021 | 383,700 | 1953 | ||

Michigan | Grand Rapids | WZZM-TV: wzzm13.com | Ch. 13/ABC | 2018 | 709,670 | 1962 | |

Minnesota | Minneapolis-St. Paul | KARE-TV: kare11.com | Ch. 11/NBC | 2021 | 1,742,530 | 1953 | |

Missouri | St. Louis | KSDK-TV: ksdk.com | Ch. 5/NBC | 2021 | 1,215,570 | 1947 | |

New York | Buffalo | WGRZ-TV: wgrz.com | Ch. 2/NBC | 2021 | 596,710 | 1954 | |

North Carolina | Charlotte | WCNC-TV: wcnc.com | Ch. 36/NBC | 2021 | 1,189,950 | 1967 | |

Greensboro | WFMY-TV: wfmynews2.com | Ch. 2/CBS | 2019 | 690,050 | 1949 | ||

Ohio | Cleveland | WKYC-TV: wkyc.com | Ch. 3/NBC | 2021 | 1,498,960 | 1948 | |

Oregon | Portland | KGW-TV(2): kgw.com | Ch. 8/NBC | 2021 | 1,143,670 | 1956 | |

South Carolina | Columbia | WLTX-TV: wltx.com | Ch. 19/CBS | 2019 | 400,790 | 1953 | |

Tennessee | Knoxville | WBIR-TV: wbir.com | Ch. 10/NBC | 2021 | 514,610 | 1956 | |

Texas | Abilene-Sweetwater | KXVA-TV: myfoxzone.com | Ch. 15/FOX | 2017 | 113,080 | 2001 | |

Austin | KVUE-TV: kvue.com | Ch. 24/ABC | 2018 | 771,210 | 1971 | ||

Beaumont-Port Arthur | KBMT-TV: 12newsnow.com | Ch. 12/ABC | 2018 | 165,120 | 1961 | ||

Corpus Christi | KIII-TV: kiiitv.com | Ch. 3/ABC | 2018 | 209,760 | 1964 | ||

Dallas/Ft. Worth | WFAA-TV: wfaa.com | Ch. 8/ABC | 2018 | 2,713,380 | 1949 | ||

Houston | KHOU-TV: khou.com | Ch. 11/CBS | 2019 | 2,450,800 | 1953 | ||

San Angelo | KIDY-TV: myfoxzone.com | Ch. 6/FOX | 2017 | 56,680 | 1984 | ||

San Antonio | KENS-TV: kens5.com | Ch. 5/CBS | 2019 | 938,660 | 1950 | ||

Tyler-Longview | KYTX-TV: cbs19.tv | Ch. 19/CBS | 2019 | 265,690 | 2008 | ||

Waco-Temple-College Station | KCEN-TV: kcentv.com | Ch. 9/NBC | 2021 | 357,720 | 1953 | ||

Virginia | Hampton/Norfolk | WVEC-TV: 13newsnow.com | Ch. 13/ABC | 2018 | 717,170 | 1953 | |

Washington | Seattle/Tacoma | KING-TV: king5.com | Ch. 5/NBC | 2021 | 1,808,530 | 1948 | |

KONG-TV: king5.com | Ch. 16/IND | N/A | 1,808,530 | 1997 | |||

Spokane | KREM-TV: krem.com | Ch. 2/CBS | 2019 | 422,550 | 1954 | ||

KSKN-TV: spokanescw22.com | Ch. 22/CW | 2021 | 422,550 | 1983 | |||

(1) We service this station under service arrangements.

(2) | We also own KGWZ-LD, a low power television station in Portland, OR. |

(3) | We also own KTFT-LD (NBC), a low power television station in Twin Falls, ID. |

(4) | We also own WBXN-CA, a Class A television station in New Orleans, LA. |

(5) | Market TV households is number of television households in each market, according to 2016-2017 Nielsen figures. |

(6) | KNAZ weekly audience is reported as part of KPNX. |

Regional news channel, Northwest Cable News (NWCN) in Seattle/Tacoma, WA, was shut down on January 6, 2017. We operate two local news channels, 24/7 NewsChannel in Boise, ID and NewsWatch on Channel 15 in New Orleans, LA. These operations provide news coverage and certain other programming in a comprehensive 24-hour a day format using the resources of our television stations in several markets.

10

DIGITAL |

Cars.com: www.cars.com Headquarters: Chicago, IL |

CareerBuilder: www.careerbuilder.com Headquarters: Chicago, IL |

G/O Digital: www.godigitalmarketing.com Headquarters: Phoenix, AZ |

INVESTMENTS We have non-controlling ownership interests in the following companies: |

4Info: www.4info.com |

Captivate: www.captivate.com |

Gannett Co., Inc.: www.gannett.com |

Kin Community: www.kincommunity.com |

Livestream: www.livestream.com |

RepairPal: www.repairpal.com |

Topix: www.topix.com |

Video Call Center: www.thevideocallcenter.com |

Whistle Sports: www.whistlesports.com |

WinnersView: www.winnersview.com |

TEGNA ON THE NET: News and information about us is available on our web site, www.TEGNA.com. In addition to news and other information about us, we provide access through this site to our annual report on Form 10-K, our quarterly reports on Form 10-Q, our current reports on Form 8-K and all amendments to those reports as soon as reasonably practicable after we file or furnish them electronically to the Securities and Exchange Commission (SEC). Certifications by our Chief Executive Officer and Chief Financial Officer are included as exhibits to our SEC reports (including to this Form 10-K). We also provide access on this web site to our Principles of Corporate Governance, the charters of our Audit, Executive Compensation and Nominating and Public Responsibility Committees and other important governance documents and policies, including our Ethics and Inside Trading Policies. Copies of all of these corporate governance documents are available to any shareholder upon written request made to our Secretary at the headquarters address. We will disclose on this web site changes to, or waivers of, our corporate Ethics Policy. | |

11

Certain factors affecting forward-looking statements

Certain statements in this Annual Report on Form 10-K contain certain forward-looking statements regarding business strategies, market potential, future financial performance and other matters. The words “believe,” “expect,” “estimate,” “could,” “should,” “intend,” “may,” “plan,” “seek,” “anticipate,” “project” and similar expressions, among others, generally identify “forward-looking statements”. These forward-looking statements are subject to certain risks and uncertainties that could cause actual results and events to differ materially from those anticipated in the forward-looking statements.

Our actual financial results may be different from those projected due to the inherent nature of projections. Given these uncertainties, forward-looking statements should not be relied on in making investment decisions. The forward-looking statements contained in this Form 10-K speak only as of the date of its filing. Except where required by applicable law, we expressly disclaim a duty to provide updates to forward-looking statements after the date of this Form 10-K to reflect subsequent events, changed circumstances, changes in expectations, or the estimates and assumptions associated with them. The forward-looking statements in this Form 10-K are intended to be subject to the safe harbor protection provided by the federal securities laws.

ITEM 1A. RISK FACTORS

An investment in our common stock involves risks and uncertainties and investors should consider carefully the following risk factors before investing in our securities. We seek to identify, manage and mitigate risks to our business, but risk and uncertainty cannot be eliminated or necessarily predicted. The risks described below may not be the only risks we face. Additional risks that we do not yet perceive or that we currently believe are immaterial may adversely affect our business and the trading price of our securities.

Changes in economic conditions in the U.S. markets we serve may depress demand for our products and services

We generate a significant portion of our revenues in our Media Segment from the sale of advertising at our television stations. Expenditures by advertisers tend to be cyclical, reflecting overall economic conditions, as well as budgeting and buying patterns. As a result, our operating results depend on the relative strength of the economy in our principal television and digital markets as well as the strength or weakness of regional and national economic factors. A decline in economic conditions in the U.S. could have a significant adverse impact on our businesses and could significantly impact all key advertising revenue categories. In addition, declining economic conditions could adversely affect employment conditions and consumer sentiment, reducing demand for the product offerings of CareerBuilder and Cars.com, which could impair our ability to maximize the value to our shareholders of these assets or to grow our Digital revenues.

Competition from alternative forms of media may impair our ability to grow or maintain revenue levels in core and new businesses

Advertising produces the majority of our revenues from our Media Segment, with our stations’ affiliated desktop, mobile and tablet advertising revenues being an important component. Technology, particularly new video formats, streaming and downloading capabilities via the Internet, video-on-demand, personal video recorders and other devices and

technologies used in the entertainment industry continues to evolve rapidly, leading to alternative methods for the delivery and storage of digital content. These technological advancements have driven changes in consumer behavior and have empowered consumers to seek more control over when, where and how they consume news and entertainment, including through so-called “cutting the cord” and other consumption strategies. These innovations may affect our ability to generate television audience, which may make our television stations less attractive to both household audiences and advertisers. This competition may make it difficult for us to grow or maintain our Media Segment revenues.

Our Media Segment is dependent on advertising revenues, which, in turn, depend on a number of factors, many of which are beyond our control

In fiscal year 2016, 69% of our Media Segment’s revenues were derived from television spot and digital advertising. Demand for advertising is highly dependent upon the strength of the U.S. economy, both in the markets our stations serve and in the nation as a whole. During an economic downturn, demand for advertising may decrease. Our Media Segment’s advertising revenues can also vary substantially from year to year, driven by the political election cycle (e.g., even years); the ability and willingness of candidates and political action committees to raise and spend funds on television and digital advertising, and the competitive nature of the elections impacting viewers within our stations’ markets.

In addition, shifting viewer preferences could cause our advertising revenues to decline as a result of changes to the ratings of our programming, which may materially negatively affect our business and results of operations.

The value of our assets or operations may be diminished if our information technology systems fail to perform adequately or if we are the subject of a data breach or cyber attack

Our information technology systems are critically important to operating our business efficiently and effectively. We rely on our information technology systems to manage our business data, communications, news and advertising content, digital products, order entry, fulfillment and other business processes. The failure of our information technology systems to perform as we anticipate could disrupt our business and could result in transaction errors, processing inefficiencies, broadcasting disruptions, and loss of sales and customers, causing our business and results to be impacted.

Furthermore, attempts to compromise information technology systems occur regularly across many industries and sectors, and we may be vulnerable to security breaches beyond our control. We invest in security resources and technology to protect our data and business processes against risk of data security breaches and cyber-attack, but the techniques used to attempt attacks are constantly changing. A breach or successful attack could have a negative impact on our operations or business reputation. We maintain cyber risk insurance, but this insurance may be insufficient to cover all of our losses from any future breaches of our systems.

12

As has historically been the case in the broadcast sector, loss of or changes in affiliation agreements or retransmission consent agreements could adversely affect operating results for our Media Segment’s stations

Most of our stations have network affiliation agreements with the major broadcast television networks (ABC, CBS, NBC, and Fox). These television networks produce and distribute programming in exchange for each of our stations’ commitment to air the programming at specified times and for commercial announcement time during the programming. In most cases, we also make cash payments to the networks.

Each of our affiliation agreements has a stated expiration date. If renewed, our network affiliation agreements may be renewed on terms that are less favorable to us. The non-renewal or termination of any of our network affiliation agreements would prevent us from being able to carry programming of the affiliate network. This loss of programming would require us to obtain replacement programming, which may involve higher costs and/or which may not be as attractive to our audiences, resulting in reduced revenues.

In recent years, the networks have streamed their programming on the Internet and other distribution platforms, in some cases within a short period of the original network programming broadcast on local television stations, including those we own. An increase in the availability of network programming on alternative platforms that either bypass or provide less favorable terms to local stations - such as cable channels, the Internet and other distribution vehicles - may dilute the exclusivity and value of network programming originally broadcast by the local stations and could adversely affect the business, financial condition and results of operations of our stations.

Our retransmission consent agreements with major cable, satellite and telecommunications service providers permit them to retransmit our stations’ signals to their subscribers in exchange for the payment of compensation to us. As is the case in the broadcast television industry generally, if we are unable to renegotiate these agreements on favorable terms, or at all, the failure to do so could have an adverse effect on our business, financial condition, and results of operations.

The proposed separation of our Cars.com business unit from our Digital businesses is subject to various risks and uncertainties, and may not be completed on the terms or timeline currently contemplated, if at all.

On September 7, 2016, we announced our intention to spin-off our Cars.com business unit within our Digital Segment. The separation, which is expected to be completed in the first half of 2017, is subject to final approval of our Board of Directors. In addition, unanticipated developments, regulatory approvals or clearances and uncertainty in the financial markets, could delay or prevent the completion of the proposed separation or cause the proposed separation to occur on terms or conditions that are different from those currently anticipated. As a result, we cannot assure that we will be able to complete the proposed separation on the terms or the timeline that we announced, if at all.

The proposed Cars.com separation may not achieve some or all of the anticipated benefits

Executing the proposed separation of Cars.com will require us to incur costs as well as time and attention from our senior management and key employees, which could distract them from operating our business, disrupt operations, and result in the loss of business opportunities, which could adversely affect our business, financial condition, and results of operations. We may also experience increased difficulties in attracting, retaining and motivating key employees during the pendency of the separation and following its completion, which could harm our business. Even if the proposed separation is completed, we may not realize some or all of the anticipated benefits from the separation and the separation may in fact adversely affect our business. As independent, publicly traded companies, both TEGNA and Cars.com will be smaller, less diversified companies with a narrower business focus and may be more vulnerable to changing market conditions and competitive pressures, which could materially and adversely affect their respective businesses, financial condition and results of operations. There can be no assurance that the combined value of the common stock of the two publicly traded companies following the completion of the proposed separation will be equal to or greater than what the value of our common stock would have been had the proposed separation not occurred.

The strategic review of CareerBuilder business unit is subject to various risks and uncertainties

On September 7, 2016, we also announced that we will conduct a strategic review of our CareerBuilder business unit within our Digital Segment, including a possible sale. There can be no assurance of the terms, timing or structure of any transaction involving such business, or whether any such transaction will take place at all, and any such transaction is subject to risks and uncertainties.

There could be significant liability if the spin-off of the publishing businesses is determined to be a taxable transaction

In June 2015, we spun off our former publishing businesses, Gannett Co. Inc. (Gannett). In connection with the Gannett spin-off, we received an opinion from outside tax counsel to the effect that the requirements for tax-free treatment under Section 355 of the Internal Revenue Code were satisfied. The opinion relies on certain facts, assumptions, representations and undertakings from TEGNA and Gannett regarding the past and future conduct of the companies’ respective businesses and other matters. If any of these facts, assumptions, representations or undertakings is incorrect or not satisfied, TEGNA and its stockholders may not be able to rely on the opinion of tax counsel and could be subject to significant tax liabilities.

Notwithstanding the opinion of tax counsel, the Internal Revenue Service could determine on audit that the Gannett separation is taxable if it determines that any of these facts, assumptions, representations or undertakings were incorrect or have been violated or if it disagrees with the conclusions in the opinion, or for other reasons, including as a result of certain significant changes in the share ownership of TEGNA or Gannett after the separation. If the Gannett separation is determined to be taxable for U.S. federal income tax purposes, TEGNA and its stockholders that are subject to U.S. federal income tax could incur significant U.S. federal income tax liabilities.

13

Volatility in the U.S. credit markets could significantly impact our ability to obtain new financing to fund our operations and strategic initiatives or to refinance our existing debt at reasonable rates and terms as it matures

At December 31, 2016, we had approximately $4.08 billion in debt and approximately $844 million of undrawn additional borrowing capacity under our revolving credit facility that expires in 2020. This debt matures at various times during the years 2017-2027. While our cash flow is expected to be sufficient to pay amounts when due, if operating results deteriorate significantly, a portion of these maturities may need to be refinanced. Access to the capital markets for longer-term financing is unpredictable and volatile credit markets could make it harder for us to obtain debt financings generally.

Changes in the regulatory environment could encumber or impede our efforts to improve operating results or the value of assets

Our media and digital operations are subject to government regulation. Changing regulations, particularly FCC regulations which affect our television stations, may impair or reduce our leverage in negotiating affiliation or retransmission agreements, adversely affecting our revenues, or result in increased costs, reduced valuations for certain broadcasting properties or other impacts, all of which may adversely impact our future profitability. All of our television stations are required to hold television broadcasting licenses from the FCC; when granted, these licenses are generally granted for a period of eight years. Under certain circumstances, the FCC is not required to renew any license and could decline to renew future license applications.

The value of our existing intangible assets may become impaired, depending upon future operating results

Goodwill and other intangible assets were approximately $7.08 billion at December 31, 2016, representing approximately 83% of our total assets. These assets are subject to annual impairment testing and more frequent testing upon the occurrence of certain events or significant changes in circumstance that indicate all or a portion of their carrying values may no longer be recoverable in which case a non-cash charge to earnings may be necessary, as occurred in 2014-2016 (see Notes 4 and 12 to the consolidated financial statements). We may subsequently experience market pressures which could cause future cash flows to decline below our current expectations, or volatile equity markets could negatively impact market factors used in the impairment analysis, including earnings multiples, discount rates, and long-term growth rates. Any future evaluations requiring an asset impairment charge for goodwill or other intangible assets would adversely affect future reported results of operations and shareholders’ equity, although such charges would not affect our cash flow.

Our strategic acquisitions, investments and partnerships could pose various risks, increase our leverage and may significantly impact our ability to expand our overall profitability

Acquisitions involve inherent risks, such as increasing leverage and debt service requirements and combining company cultures and facilities, which could have a material adverse effect on our results of operations or cash flow and could strain our human resources. We may be unable to successfully implement effective cost controls, achieve

expected synergies or increase revenues as a result of an acquisition. Acquisitions may result in us assuming unexpected liabilities and in management diverting its attention from the operation of our business. Acquisitions may result in us having greater exposure to the industry risks of the businesses underlying the acquisition. Strategic investments and partnerships with other companies expose us to the risk that we may be unable to control the operations of our investee or partnership, which could decrease the amount of benefits we realize from a particular relationship. We are exposed to the risk that our partners in strategic investments and infrastructure may encounter financial difficulties which could disrupt investee or partnership activities, or impair assets acquired, which would adversely affect future reported results of operations and shareholders’ equity. The failure to obtain regulatory approvals may prevent us from completing or realizing the anticipated benefits of acquisitions. Furthermore, acquisitions may subject us to new or different regulations which could have an adverse effect on our operations.

ITEM 1B. UNRESOLVED STAFF COMMENTS

None.

ITEM 2. PROPERTIES

Media Segment

Our media facilities are adequately equipped with the necessary television digital broadcasting equipment. We own or lease 49 transmitter facilities. All of our stations have converted to digital television operations in accordance with applicable FCC regulations. Our broadcasting facilities are adequate for present purposes. A listing of television station locations can be found on page 10.

Digital Segment

Generally, our digital businesses lease their facilities. This includes facilities for executive offices, sales offices and data centers. Our facilities are adequate for present operations. We believe that suitable additional or alternative space, including those under lease options, will be available at commercially reasonable terms for future expansion. A listing of our significant Digital facilities can be found on page 11.

Corporate facilities

In October 2015, we sold our corporate headquarters in McLean, VA for a purchase price of $270 million. Since the sale, we have been leasing a portion of the facility pursuant to a lease which runs through January 2019.

ITEM 3. LEGAL PROCEEDINGS

Information regarding legal proceedings may be found in Note 13 of the Notes to consolidated financial statements.

ITEM 4. MINE SAFETY DISCLOSURES

Not applicable.

14

PART II

ITEM 5.MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES

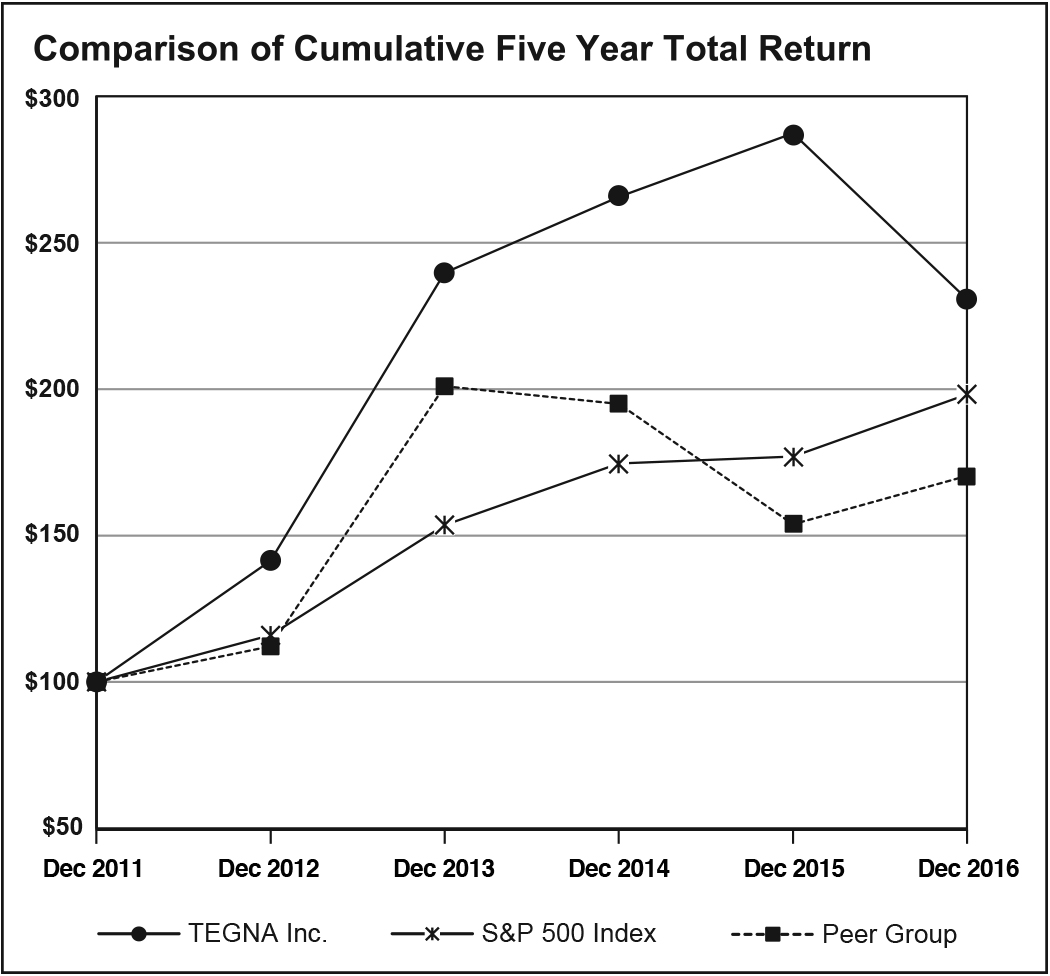

Our shares are traded on the New York Stock Exchange (NYSE) with the symbol TGNA. Information regarding outstanding shares, shareholders and dividends may be found on pages 1, 4 and 15 of this Form 10-K. Information about debt securities sold in private transactions may be found on page 28 of this Form 10-K.

TEGNA Common Stock Prices

High-low range by fiscal quarters based on NYSE-composite prices. On June 29, 2015, the first day of the fiscal third quarter, we completed the separation of our publishing business (Gannett) through a spin-off transaction. TEGNA’s common stock prices in and after the third quarter of 2015 reflect the price impact of the spin-off transaction.

Dividends Paid Per Share | Common Stock Prices | ||||||

Year | Quarter | Low | High | ||||

2016 | First | $0.14 | $21.37 | $25.08 | |||

Second | $0.14 | $21.77 | $24.30 | ||||

Third | $0.14 | $20.16 | $25.00 | ||||

Fourth | $0.14 | $18.02 | $23.25 | ||||

Total 2016 | $0.56 | $18.02 | $25.08 | ||||

2015 | First | $0.20 | $29.62 | $36.56 | |||

Second | $0.20 | $34.27 | $38.01 | ||||

Third | $0.20 | $22.42 | $32.97 | ||||

Fourth | $0.14 | $21.85 | $28.68 | ||||

Total 2015 | $0.74 | $21.85 | $38.01 | ||||

Following the Gannett spin-off on June 29, 2015, we announced that we would begin paying a regular quarterly cash dividend of $0.14 per share. We paid dividends totaling $121.6 million in 2016 and $167.5 million in 2015 (excluding the special spin-off distribution of our publishing businesses). We expect to continue paying comparable regular cash dividends in the future. The rate and frequency of future dividends will depend on future earnings, capital requirements and financial condition and other factors considered relevant by our Board of Directors.

Purchases of Equity Securities

Period | Total Number of Shares Purchased | Average Price Paid per Share | Total Number of Shares Purchased as Part of Publicly Announced Program | Approximate Dollar Value of Shares that May Yet Be Repurchased Under the Program | |||||||

10/1/16 - 10/31/16 | — | — | — | $478,143,186 | |||||||

11/1/16 - 11/30/16 | 143,428 | $21.47 | 143,428 | $475,063,548 | |||||||